As

filed with the U.S. Securities and Exchange Commission on April 29, 2026

1933 Act Registration No. 333-103454

1940 Act Registration No. 811-08289

1940 Act Registration No. 811-08289

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-6

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

☒ |

| Pre-Effective Amendment No. |

☐ |

| Post-Effective Amendment No. 23 |

☒ |

| and/or |

|

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

☒ |

| Amendment No. 70 |

☒ |

THRIVENT VARIABLE LIFE ACCOUNT I

(Exact Name of Registrant)

Thrivent Financial for Lutherans

(Name of Depositor)

600 Portland Avenue South, Suite 100

Minneapolis, Minnesota 55415

Minneapolis, Minnesota 55415

(Address of Principal Executive Offices)

Depositor’s Telephone Number, including Area Code:

612-844-5499

Thomas P. Trier, JD

Director, Senior Counsel

Thrivent Financial for Lutherans

600 Portland Avenue South, Suite 100

Minneapolis, Minnesota 55415

(Name and Address of Agent for Service)

Director, Senior Counsel

Thrivent Financial for Lutherans

600 Portland Avenue South, Suite 100

Minneapolis, Minnesota 55415

(Name and Address of Agent for Service)

It is proposed that this filing will become

effective (check appropriate box):

| ☐ |

immediately upon filing pursuant to paragraph (b) of Rule 485 |

| ☒ |

on April 30, 2026, pursuant to paragraph (b) (1) of Rule 485 |

| ☐ |

60 days after filing pursuant to paragraph (a)(1) of Rule 485 |

| ☐ |

on (date) pursuant to paragraph (a)(1) of Rule 485 |

If appropriate, check the following

box:

| ☐ |

this post-effective amendment designates a new effective date for a previously filed post-effective amendment |

|

Thrivent Variable Universal Life Insurance |

| | |

| | |

| Thrivent Variable Life Account I | |

| Statutory Prospectus April 30, 2026 |

This prospectus describes key features of a flexible premium individual variable adjustable life insurance contract (the “Contract”) previously offered by Thrivent Financial for Lutherans (“Thrivent”) between 2004 and 2008. The Contract is a long-term investment designed to provide significant life insurance benefits. Even though we no longer issue new

Contracts on this form as described in this prospectus, the Contract Owner (“you”) may continue to allocate Net Premiums among investment alternatives with different investment objectives and make changes including increases in coverage pursuant

to the terms of the Contract.

Additional general information about certain investment products, including variable life insurance contracts, has been

prepared by the Securities and Exchange Commission’s staff and is available at Investor.gov.

The Securities and Exchange Commission has not approved or disapproved this Contract or passed upon the adequacy of this statutory prospectus. Any representation to the contrary is a criminal offense.

Table of

Contents

| 1 | |

| 4 | |

| 4 | |

| 4 | |

| 4 | |

| 4 | |

| 4 | |

| 5 | |

| 8 | |

| 12 | |

| 12 | |

| 12 | |

| 12 | |

| 13 | |

| 13 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 14 | |

| 15 | |

| 15 | |

| 15 | |

| 15 | |

| 15 | |

| 16 | |

| 16 | |

| 16 | |

| 16 | |

| 16 | |

| 16 | |

| 17 | |

| 17 | |

| 18 | |

| 18 | |

| 19 | |

| 19 | |

| 20 | |

| 20 | |

| 20 | |

| 20 | |

| 20 | |

| 20 | |

| 21 | |

| 21 | |

| 21 | |

| 21 |

| 22 | |

| 22 | |

| 23 | |

| 23 | |

| 24 | |

| 25 | |

| 25 | |

| 25 | |

| 25 | |

| 26 | |

| 26 | |

| 26 | |

| 26 | |

| 26 | |

| 27 | |

| 27 | |

| 27 | |

| 28 | |

| 29 | |

| 30 | |

| 30 | |

| 30 | |

| 31 | |

| 31 | |

| 31 | |

| 32 | |

| 32 | |

| 32 | |

| 32 | |

| 33 | |

| 33 | |

| 33 | |

| 33 | |

| 34 | |

| 34 | |

| 34 | |

| 34 | |

| 34 | |

| 35 | |

| 35 | |

| 36 | |

| 39 | |

| 39 | |

| 39 | |

| 40 | |

| 40 | |

| 41 | |

| 42 | |

| 42 | |

| 42 | |

| 42 | |

| 42 | |

| 43 | |

| 43 |

Key Information

Important Information You Should

Consider About the

Contract.

| FEES AND EXPENSES |

Location in

Statutory

Prospectus | |||

| Charges for Early

Withdrawals |

A Decrease Charge (early withdrawal charge) may be assessed upon

surrender, lapse or any decrease in the

Face Amount. A

Decrease Charge will

be assessed for 10 years after each increase in

Face Amount. The

Decrease Charge will vary depending on the number of years since the last increase in

Face Amount

. The maximum amount that may be charged is $49.25 per $1,000 of decrease in Face Amount

. For example, if you make an early withdrawal, you could pay a Decrease

Charge of up to $4,925 on a $100,000 decrease. |

Charges

Fee Table | ||

| Transaction

Charges |

In addition to

Decrease Charges (early withdrawal charges), you also may be

charged for other transactions such as when you pay a premium, transfer

accumulated value between investment options, make more than one

partial surrender in a

Contract Year or exercise your Accelerated Death Benefit Rider.

A premium charge of 5% is deducted upon receipt of most premiums.

A transfer charge applies to each transfer in excess of the first twelve

transfers made in a

Contract Year. The maximum amount deducted is $25 per transfer.

You may add an Accelerated Death Benefit Rider to your

Contract at any time

without cost. The rider allows you to receive the present value of the death

benefit tax free if eligibility requirements are met, including

doctor certification that the

Insured is terminally ill. A one-time charge of up to $150 will apply if

you exercise the benefit. The charge may be lower in some states.

State variations may apply.

An illustration charge of $25 applies upon each request in excess of one per

|

Charges

Fee Table

| ||

| Ongoing Fees and

Expenses (annual

charges) |

In addition to

Decrease Charges (early withdrawal charges) and transaction

charges, investment in the

Contract is subject to certain ongoing fees and

expenses (typically assessed monthly), including fees and expenses covering

the cost of insurance under the

Contract, mortality and expense risk charges,

basic monthly charges, interest on any

Debt, and the cost of optional benefits

available under the

Contract. Some of these fees and expenses are set based

on characteristics of the

Insured (e.g. age, sex (in most states), and rating

classification). See the specifications page of your

Contract for rates

applicable to your

Contract.

Investors will also bear expenses associated with

Portfolios that correspond to

Subaccounts available under the Contract

, as shown in the following table: |

|||

| Annual Fee |

Minimum |

Maximum | ||

| Annual Portfolio Expenses (deducted

from Portfolio assets) |

0.22%

|

1.52%

| ||

1

| RISKS |

Location in

Statutory

Prospectus | |||

| Risk of Loss |

You can lose money by investing in this

Contract, including loss of your

premiums (principal), and your

Contract can lapse without value.

the amount of premiums considered to meet the

Death Benefit Guarantee Premium requirement. If you surrender the

Contract or allow it to lapse while a

contract loan is outstanding, the amount of

Debt, to the extent it has not

previously been taxed, will be considered part of the amount you receive and

taxed accordingly. Loans may have tax consequences.

|

|||

| Not a Short-Term

Investment |

||||

| Risk Associated

with Investment

Options |

An investment in this

Contract is subject to the risk of poor investment

performance of the investment options you choose.

Each investment option has its own unique risks.

We do not guarantee any money you place in the

Subaccounts. The value of

each Subaccount will increase or decrease, depending on the investment

performance of the corresponding

Portfolio and fees and charges under the

Contract. You could lose some or all of your money. You should review the available Portfolio

s’ prospectuses before making an investment decision. |

|||

| Insurance

Company Risks |

||||

| Contract Lapse |

If your monthly deductions exceed your

Cash Surrender Value, then unless

will enter a 61-day grace period. We will notify you that your

Contract will lapse

(that is, terminate without value) if you do not send us a sufficient payment by

a specified date. No

Death Benefit will be paid if the

Contract is lapsed. We will

reinstate a Contract only if our requirements for reinstatement are satisfied,

which may include requiring new proof of insurability of the

Insured person. |

Lapse and

Reinstatement | ||

2

| RESTRICTIONS |

Location in

Statutory

Prospectus | |||

| Investments |

We place limits on frequent trading.

There is a $25 charge for each transfer when you transfer money between

investment options in excess of 12 times a year.

Thrivent reserves the right to remove or substitute

Portfolio companies as

investment options that are available under the

Contract.

We reserve the right to not accept any premiums when the

Death Benefit is

based on the

Table of Factors in your

Contract.

We will also have the right to limit or refund a premium payment or make

as life insurance under federal tax law or to avoid the classification of your

Contract

as a “modified endowment contract” (MEC). |

Frequent Trading

Among

Subaccounts and Other

Transactions Addition, Deletion,

Combination or

Substitution of

Investments

Premium Limits

Taxes | ||

| Optional Benefits |

Optional benefits may be subject to age and underwriting requirements. We

generally deduct any monthly costs for these Additional Benefits

from the Accumulated Value as part of the monthly deduction. Optional benefits may

not be available for all ages or underwriting classes, may not be

available after original issue of the

Contract and may terminate at certain ages. We may stop

offering an optional benefit at any time prior to the time you elect to add it to

your Contract. |

|||

| TAXES |

| |||

| Tax Implications |

You should consult with a tax professional to determine the tax implications of

an investment in and payments received under this

Contract.

Distributions from your

Contract, if taxable, will be taxed at ordinary income tax

rates.

Depending on the total amount of premiums you pay and the frequency of

such payments, the

Contract may be treated as a MEC.

Distributions including loans and loan interest will be taxed on an “income

first” basis and may be subject to a penalty tax if taken

before you are age 59 1∕2 if

your Contract is a MEC.

The transfer of the

Contract or designation of a

Beneficiary may have federal,

state, and/or local transfer and inheritance tax consequences, including the

impositions of gift, estate, and generation skipping transfer

taxes. |

Taxes | ||

| CONFLICTS OF INTEREST |

Location in

Statutory

Prospectus | |||

| Investment

Professional

Compensation |

We no longer issue this

Contract to new owners. Your financial advisor or

professional may receive compensation which may consist of commissions,

bonuses, asset-based compensation, and promotional incentives. This

conflict of interest may influence your financial advisor or

professional to recommend continued or larger future investments

into this Contract, or another contract issued by Thrivent, over another investment. |

|||

| Exchanges |

Some investment professionals may have a financial incentive to offer you a

new contract in place of the one you own. You should only exchange

your contract if you determine, after comparing the features, fees,

and risks of both contracts, that it is better for you to purchase

the new contract rather than continue to own your existing

contract. |

Distribution of the | ||

3

Overview of the Contract

This summary describes the Contract’s important benefits and risks. The sections in the prospectus following this summary discuss the Contract’s benefits and other provisions in more detail. For your convenience, we have provided Special Terms at the end of this prospectus that define certain words and phrases used in this prospectus.

Purpose

The Contract is a flexible

premium variable adjustable life insurance contract and is a long-term investment, not appropriate for a customer with near term liquidity needs. The primary purpose of the

Contract is to provide a death benefit to beneficiaries upon the death of the Insured. Secondarily, the Accumulated Value in the Contract may provide a source of supplemental funds in the future.

Premiums

You may pay premiums at any time and in any amount, subject to some restrictions. Insufficient premiums may result in a lapse of the Contract. Therefore, we recommend that you pay at least a Death Benefit Guarantee Premium to protect your

Contract from lapsing. While there are no scheduled premium due dates, you may schedule planned periodic premiums

and then you will receive billing statements for the amount you select. You may elect to receive billing statements quarterly, semi-annually or annually. In most cases, you may make changes in the frequency and payment amounts at any time

by giving adequate Notice to our Service Center. Premiums may be allocated to the Subaccounts of the Variable Account and/or to the Fixed Account. Additional information about the

Portfolios corresponding to the Subaccounts is provided in the Appendix to this prospectus.

Death Benefit

Option 1 (Level Death Benefit Option). Under this option and before age 100, the Death

Benefit is the greater of the Face Amount or the death benefit factor multiplied by Accumulated Value. The death benefit factor depends on the Insured’s Attained Age. The Death Benefit for this option generally remains level. The Death Benefit on any day on or after the Insured’s Attained Age 100 is equal to the Accumulated Value on that day.

Option 2 (Variable Death Benefit Option).Under this option and before age 100, the Death Benefit is the greater of the Face Amount plus Accumulated Value, or the

death benefit factor multiplied by Accumulated Value. The death benefit factor depends on the Insured’s Attained Age. The Death Benefit for this option will vary over time,

meaning it may increase or decrease. The Death Benefit on any day on or after the Insured’s Attained Age 100 is equal to the Accumulated Value on that day.

Death Proceeds

We pay Death Proceeds to the

Beneficiary upon receipt at our Service Center of due proof of death of the Insured. The Death Proceeds will equal the Death Benefit and any insurance on the life of the Insured

provided by Additional Benefits less any Debt and the amount, if any, needed to cover monthly deductions through the month of death.

Death Benefit Guarantee

Two Death Benefit Guarantees were generally available at issue: a basic and an enhanced Death Benefit Guarantee. The Death Benefit Guarantee ensures that your Contract will remain in effect, even if the Cash Surrender Value is insufficient

to pay the current monthly deductions, if the Death Benefit Guarantee requirements are met. (In some states, this feature is referred to as a “no-lapse guarantee.”) The enhanced Death Benefit Guarantee was available for Contracts issued

before age 70 and is in effect until the Insured reaches age 75 if the requirements are met. The Basic Death Benefit Guarantee is no longer active on any Contracts.

4

Access to Accumulated

Value

Transfers. You may transfer accumulated value among the Subaccounts and the Fixed Account. You will not be charged

for the first 12 transfers in a Contract Year. We will charge $25 for each additional transfer during a Contract Year. The minimum amount that may be transferred from a Subaccount or Fixed Account is $50, or if less, the total value in the

Subaccount or the Fixed Account. There is no minimum amount that can be received by a Subaccount or Fixed Account.

Automatic Asset Rebalancing Program. The Automatic Asset Rebalancing program transfers your Contract’s Accumulated Value among Subaccounts (this excludes the Fixed Account) on a regular basis according to your

instructions.

Dollar Cost Averaging Program. Dollar Cost Averaging allows you to make regular transfers of predetermined amounts from your Money Market Subaccount to any

or all of the other Subaccounts. The Dollar Cost Averaging amount from the Money Market Subaccount must be at least $50. You may choose to use the Money Market Subaccount as the

source account at any time and for any length of time.

Loans. You may borrow an amount equal to up to 90% (in most states) of the Accumulated Value of your Contract less any applicable

Decrease Charge and existing Debt. The maximum annual interest rate is 5%. After the 10th Contract Year, you may borrow a portion of your Accumulated Value at an annual rate of 3%

(preferred loan). For amounts that are left as collateral in the Loan Account, we pay an annual rate of 3%. Debt on non-preferred loan amounts will continue to increase unless it is repaid. Loans will impact your Contract’s performance, must be repaid, could cause the Contract to lapse and may result in tax consequences. In your Contract, the discussion of the operation of the loan feature is described as a Loan

Account. For additional information see Loans in this prospectus and in your

Contract.

Partial Surrenders. You may make a request to withdraw part of your Accumulated Value by giving us Notice. Decrease Charges may apply if the partial surrender results in a decrease in Face Amount and it has been less than 10 years since you

increased the Face Amount. Partial surrenders may have tax consequences. Partial surrenders may decrease your Death Benefit and may impact the performance of the Contract including

the number of years your Contract is expected to provide coverage. See Charges for more information on Decrease Charges.

Surrenders. At any time while the Contract is in force and the Insured is living, you may

surrender this Contract by giving us Notice. A surrender may result in a Decrease Charge depending on how long it has been since you last increased the Face Amount. For more information on Decrease Charges, see Charges. Surrenders may have tax consequences.

Additional Benefits and Riders

We offer several optional insurance benefits and riders that provide additional benefits under the Contract. There is a

charge associated with most of these insurance benefits and riders. Your financial advisor or professional can help you determine whether any of these benefits and riders are suitable for you.

Accidental Death Benefit (Optional Benefit)

This benefit generally provides an additional death benefit when the Insured dies from accidental bodily injury. Subject to our overall limit on accidental death benefits, you may select the amount of coverage up to the same amount as the Face Amount of your Contract. Any accidental death benefit payable would be in addition to your basic death benefit. The charge for this rider, based on Issue Age, is a per-thousand rate multiplied by the accidental death amount.

This benefit generally provides an additional death benefit when the Insured dies from accidental bodily injury. Subject to our overall limit on accidental death benefits, you may select the amount of coverage up to the same amount as the Face Amount of your Contract. Any accidental death benefit payable would be in addition to your basic death benefit. The charge for this rider, based on Issue Age, is a per-thousand rate multiplied by the accidental death amount.

Disability Waivers (Optional Benefit)

You may choose one of two different disability waivers. Waiver of monthly deductions provides that, in the event of your qualifying disability, we will waive your cost of insurance and expense deductions until the earlier of your age 100 or your recovery from disability. The charge for this rider is a percentage based on Attained Age multiplied by the amount of each monthly deduction. Waiver of selected amount credits the amount selected at issue. The charge for this rider is a percentage based on Attained Age multiplied by the selected amount.

You may choose one of two different disability waivers. Waiver of monthly deductions provides that, in the event of your qualifying disability, we will waive your cost of insurance and expense deductions until the earlier of your age 100 or your recovery from disability. The charge for this rider is a percentage based on Attained Age multiplied by the amount of each monthly deduction. Waiver of selected amount credits the amount selected at issue. The charge for this rider is a percentage based on Attained Age multiplied by the selected amount.

5

Applicant Waiver of Selected

Amount (Optional Benefit)

This benefit enables the applicant on a Contract on the life of a minor to have selected amounts credited to the Contract if the applicant becomes disabled (as described above) or dies. Amounts will be credited until the end of the benefit period as defined in the rider. The charge for this benefit is a percentage based on Attained Age of the applicant and Issue Age of the Insured multiplied by the selected amount. The charge will apply until the rider terminates. The rider will terminate on the earliest of the following dates:

This benefit enables the applicant on a Contract on the life of a minor to have selected amounts credited to the Contract if the applicant becomes disabled (as described above) or dies. Amounts will be credited until the end of the benefit period as defined in the rider. The charge for this benefit is a percentage based on Attained Age of the applicant and Issue Age of the Insured multiplied by the selected amount. The charge will apply until the rider terminates. The rider will terminate on the earliest of the following dates:

1.The date the applicant reaches age 65 or the end of a benefit period, if later.

2.The date control of the Contract is transferred to the Insured.

3.The date the Contract terminates.

4.The first monthly anniversary on or after the date we receive Notice to cancel the rider.

Guaranteed Increase Option (Optional Benefit)

Purchasing this option allows you to increase the amount of coverage without having to show evidence of insurability at certain pre-defined opportunities. The charge is a per-thousand rate multiplied by the size of the guaranteed increase amount. A new No-Lapse Guarantee Premium will be determined for any No Lapse Guarantee in effect on the date of increase.

Purchasing this option allows you to increase the amount of coverage without having to show evidence of insurability at certain pre-defined opportunities. The charge is a per-thousand rate multiplied by the size of the guaranteed increase amount. A new No-Lapse Guarantee Premium will be determined for any No Lapse Guarantee in effect on the date of increase.

Child Term Life Insurance (Optional Benefit)

This rider generally pays a benefit to the Beneficiary in the event of the death of a covered child of the Insured prior to the rider anniversary following the child’s 25th birthday. Conversely, in the event of the death of the Insured, the rider for any covered child will become child paid-up term insurance in force to the child’s 25th birthday. Beginning on the rider anniversary on or after the covered child’s 21st birthday until the rider anniversary on or after that child’s 25th birthday, the child will have the option to purchase his or her own life Contract without having to provide evidence of insurability. The charge for this benefit is a per-thousand rate multiplied by the amount of rider coverage. The charge does not depend upon the number of children insured.

This rider generally pays a benefit to the Beneficiary in the event of the death of a covered child of the Insured prior to the rider anniversary following the child’s 25th birthday. Conversely, in the event of the death of the Insured, the rider for any covered child will become child paid-up term insurance in force to the child’s 25th birthday. Beginning on the rider anniversary on or after the covered child’s 21st birthday until the rider anniversary on or after that child’s 25th birthday, the child will have the option to purchase his or her own life Contract without having to provide evidence of insurability. The charge for this benefit is a per-thousand rate multiplied by the amount of rider coverage. The charge does not depend upon the number of children insured.

This rider may be issued even if there are no eligible children at the time the Contract is issued. In this case, there is no

charge for this rider while there are no covered children. If you notify us within six months of the first birth or adoption, your child, and any subsequent children, will be covered without evidence of insurability. Charges will begin six months after

the date of birth or adoption.

Term Life Insurance and Spouse Term Life Insurance (Optional Benefit)

These riders provide additional term life insurance. The riders are available on the life of the Insured and/or on the life of the spouse of the Insured for up to 30 years. The charge for this benefit is a per-thousand cost of insurance rate multiplied by the amount of rider coverage.

These riders provide additional term life insurance. The riders are available on the life of the Insured and/or on the life of the spouse of the Insured for up to 30 years. The charge for this benefit is a per-thousand cost of insurance rate multiplied by the amount of rider coverage.

Cost of Living Adjustment Benefit (Optional Benefit)

This benefit annually adjusts the Face Amount of the Contract and, if elected, your premium payments to keep pace with the Consumers’ Price Index (CPI). The maximum increase is the smallest of 1) the CPI increase on a Contract Anniversary multiplied by the Face Amount rounded up to the next $100; 2) 10% of the Face Amount; and 3) $50,000. As a result of increasing the Face Amount, monthly deductions will increase. Furthermore, a new schedule of decrease charges will apply to any resulting increase in Face Amount. Any resulting increase to the Face Amount will also require a new Death Benefit Guarantee Premium amount to be determined. There is no separate charge to implement this benefit, however, by electing the benefit you should anticipate increasing costs associated with increasing your Face Amount. This benefit terminates at the earliest of the:

This benefit annually adjusts the Face Amount of the Contract and, if elected, your premium payments to keep pace with the Consumers’ Price Index (CPI). The maximum increase is the smallest of 1) the CPI increase on a Contract Anniversary multiplied by the Face Amount rounded up to the next $100; 2) 10% of the Face Amount; and 3) $50,000. As a result of increasing the Face Amount, monthly deductions will increase. Furthermore, a new schedule of decrease charges will apply to any resulting increase in Face Amount. Any resulting increase to the Face Amount will also require a new Death Benefit Guarantee Premium amount to be determined. There is no separate charge to implement this benefit, however, by electing the benefit you should anticipate increasing costs associated with increasing your Face Amount. This benefit terminates at the earliest of the:

1)expiration date for the rider shown on page 5-COL of the Contract;

2)date the Contract terminates;

3)date the Contract owner rejects an increase in Face Amount under the rider;

4)effective date of any decrease in Face Amount;

6

5)date the sum of the increases in Face Amount due to this rider equals or exceeds two times the Face Amount on

the date of issue of the rider;

6)the effective date of any increase in Face Amount that has a rated Risk Class; and

7)the date the Contract owner gives Notice to cancel the rider.

Accelerated Benefits Rider-Generally Available on Contracts Applied for Prior to January 15, 2008 (Optional Benefit)

This rider pays a portion of the death benefit when requested if the Insured has a life expectancy of 12 months or less or has been in a nursing home for at least six consecutive months and is expected to remain there for the rest of his or her life. Tax consequences may result. See Taxes.

This rider pays a portion of the death benefit when requested if the Insured has a life expectancy of 12 months or less or has been in a nursing home for at least six consecutive months and is expected to remain there for the rest of his or her life. Tax consequences may result. See Taxes.

Accelerated Death Benefit for Terminal Illness (Optional Benefit)

You may add this rider at any time without cost. The rider allows you to receive the present value of the death benefit tax free if eligibility requirements are met. Eligibility requirements include doctor certification that the Insured is terminally ill. State variations apply.

You may add this rider at any time without cost. The rider allows you to receive the present value of the death benefit tax free if eligibility requirements are met. Eligibility requirements include doctor certification that the Insured is terminally ill. State variations apply.

7

The following tables describe the fees and expenses that you will pay when buying, owning, and surrendering or making withdrawals from the Contract

. Please refer to your Contract specifications page for information about the specific fees you will pay each year based on the options you have selected.

The first table describes the fees and expenses that you will pay at the time that

you buy the Contract, surrender or make withdrawals from the

Contract, or transfer accumulated value between investment options.

Transaction Fees

| Percent of Premium Charge |

Upon receipt of each premium

payment |

5% of each premium payment |

| Premium Tax Charge |

Not currently applicable1 |

Not currently applicable1 |

| Decrease Charge2 |

Upon surrender, lapse, or decrease

in the Face Amount |

|

| Maximum |

|

$49.25 per $1,000 of decrease in Face Amount |

| Minimum |

|

$1.66 per $1,000 of decrease in Face Amount |

| Charge for a male Insured,

Issue Age 40, in the standard

non-tobacco risk class with a

Face Amount of $225,000, in

the first Contract Year. |

|

$15.57 per $1,000 of decrease in

Face Amount |

| Transfer Charge |

Upon each transfer after the twelfth

in a Contract Year.3 |

$25 per transfer |

| Accelerated Death Benefit |

On exercise of benefit4 |

$150 |

| Illustration of Hypothetical

Values |

Upon each request5 |

$25 per illustration |

1 We are not currently subject to premium taxes. However, we reserve the right to impose a

charge for these taxes in the future if we have to pay them. If imposed, the premium tax charge would be between 0% and 5% of premium payments. 2 The Decrease Charge remains level for the first five years following an increase in Face

Amount, and then decreases each Contract Year to zero after the 10th year following an increase in Face Amount. Decrease charges depend on the Insured’s Issue Age, sex (in

most states), amount of decrease in Face Amount, risk class and the amount of time since the last increase in Face Amount. The decrease charges shown in the table may not be representative of the charges you will pay. For decreases in Face Amount during the first 10 Contract Years following an increase in Face Amount, we calculate the amount of the Decrease Charge at the time of the decrease or surrender.

3 We do not assess a transfer charge for the first twelve Subaccount transfers made

each Contract Year. 4 The charge may vary by state and may be lower in

some states. 5 The charge applies upon each request in excess of one

per Contract Year. There is no charge for illustrations provided prior to Contract purchase.

Periodic Charges Other Than Fund Operating Expenses

The next table describes the fees and expenses that you will pay

periodically during the time that you own the Contract, not including Fund fees and expenses.

8

Periodic Charges

Other Than Fund Operating Expenses, cont.

| Cost of Insurance Charge6 |

On Date of Issue and monthly

thereafter |

|

| Maximum |

|

$83.3333 per $1,000 of amount at risk7 |

| Minimum |

|

$0.0106 per $1,000 of amount at risk7 |

| Charge for a male Insured,

Issue Age 40, in the standard

non-tobacco risk class with a

Face Amount of $225,000, in

the first Contract Year |

|

$0.19 per $1,000 of amount at

risk7 |

| Mortality and Expense Risk

Charge A tiered charge based on

Subaccount Accumulated Value

up to $25,000 |

On Date of Issue and monthly

thereafter |

0.07469% of the Subaccount

Accumulated Value within this

range8 |

| Administrative Charge (Basic

Monthly Charge) |

On Date of Issue and monthly

thereafter |

$9.00 for adults9 |

| Loan Interest |

On the monthly anniversary after a

loan is taken and monthly thereafter |

2% net interest rate on loan

balance.10 |

| Preferred Loan Interest |

On the monthly anniversary after a

loan is taken and monthly thereafter |

0% net interest rate on preferred

loan balance after the 10th

Contract Anniversary11 |

| Additional Benefit Charges:12 |

|

|

| Accidental Death Benefit |

On the rider date of issue and

monthly thereafter13 |

|

6 Cost of insurance charges depend on the Insured’s Issue Age, sex (in most states),

amount at risk, Face Amount, risk class and duration of the Contract. The cost of insurance charges shown in the table are extremes and may not be representative of the charges you

will pay. For more information on the calculation of this charge see Charges. 7 The amount

at risk is equal to the death benefit divided by 1.0024663, then less the Accumulated Value on the date the charge is deducted. 8 After the 10th Contract Year the maximum annual rate dropped. For the first $25,000 the maximum annual rate is 0.90% of the Subaccount Accumulated Value. For Subaccount Accumulated Values in excess of $25,000 up to $100,000, the maximum annual rate is 0.80%. For Subaccount Accumulated Values in excess of $100,000, the maximum annual rate is 0.70%. This is a tiered charge. Actual current charges may be less. For additional information regarding this charge please see Charges and Deductions in this prospectus. 9 Charge shown is for adults (Issue Age 18+ years) and is $9.00 per month. For juvenile (Issue Age 0-17) Contracts, the charge is $7.50 per month. 10 You may borrow up to an amount such that the total loan amount does not exceed 90% of the

Accumulated Value less decrease charges at the time of the loan request. We pay an annual rate of 3% on amounts that are left as collateral in the Loan Account, resulting in a

maximum net interest rate of 2%. 11 See the Loans section later in this

prospectus for more information on preferred loans. We pay an annual rate of 3% on amounts that are left as collateral in the Loan Account, resulting in a maximum net interest rate

of 0%. 12 Charges for Additional Benefits may vary based on the

Insured’s Attained Age or Issue Age, sex (in most states), risk class, Face Amount, amount at risk, or rider coverage amount. Charges based on age may increase as the Insured

ages. The charges noted apply if the rider is included in your Contract and the Contract and/or rider has not otherwise terminated. The rider charges shown in the table may not be

representative of the charges you will pay. Before you purchase a Contract, we will provide you personalized illustrations of your future benefits under the Contract, based upon the

Insured’s age, sex, risk class, death benefit option chosen, Face Amount and riders requested. 13 This charge applies until the Insured’s Attained Age 70.

9

Periodic Charges

Other Than Fund Operating Expenses, cont.

| Maximum |

|

$1.0934 per $1,000 of rider coverage amount |

| Minimum |

|

$0.0058 per $1,000 of rider coverage amount |

| Charge for a male Insured,

Issue Age 40, in the standard

risk class in the first Contract

Year |

|

$0.035 per $1,000 of rider

coverage amount |

| Term Life Insurance Benefit |

On the rider date of issue and

monthly thereafter14 |

|

| Maximum |

|

$83.3333 per $1,000 of rider coverage amount |

| Minimum |

|

$0.02 per $1,000 of rider coverage amount |

| Charge for a male Insured,

Issue Age 40, in the standard

nontobacco risk class with a

Face Amount/rider coverage

amount of $225,00015, in the

first Contract Year |

|

$0.13 per $1,000 of rider

coverage amount |

| Child Term Life Insurance

Benefit |

On the rider date of issue and

monthly thereafter16 |

$0.45 per $1,000 of rider

coverage amount |

| Cost of Living Adjustment

Benefit |

|

No charge for this benefit17 |

| Disability Waiver of Monthly

Deduction Benefit |

On the rider date of issue and

monthly thereafter18 |

|

| Maximum |

|

195.5% of the selected monthly premium amount19 |

| Minimum |

|

4.8% of the selected monthly premium amount19 |

| Charge for an Insured, Issue

Age 40, in the standard risk

class, in the first Contract Year. |

|

7.7% of all monthly deductions19 |

| Disability Waiver of Selected

Amount Benefit |

On the rider date of issue and

monthly thereafter |

|

14 The charge applies until the 30th rider anniversary. 15 Any amount of coverage includes $90,000 of base coverage and $135,000 of term rider coverage

with a total of $225,000. 16 The charge applies until the child’s

Attained Age 25. 17 This benefit will result in annual increases in

Face Amount, which will result in increases in your overall cost of insurance deductions. 18 The charge applies until the Insured’s Attained Age 65. 19 Monthly deductions include cost of insurance, benefit rider, administrative, and mortality and expense risk charges.

10

Periodic Charges

Other Than Fund Operating Expenses, cont.

| Maximum |

|

98% of the selected monthly premium amount20 |

| Minimum |

|

1.9% of the selected monthly premium amount20 |

| Charge for a male Insured,

Issue Age 40, in the standard

risk class in the first Contract

Year |

|

3.7% of the selected monthly

premium amount20 |

| Applicant Waiver of Selected

Amount Benefit |

On the rider date of issue and

monthly thereafter21 |

|

| Maximum |

|

195% of the selected monthly premium amount20 |

| Minimum |

|

5% of the selected monthly premium amount20 |

| Charge for an Insured, Issue

Age 0 and applicant age 30, in

the standard risk class, in the

first Contract Year |

|

6% of the selected monthly

premium amount20 |

| Guaranteed Increase Option

Benefit |

On the rider date of issue and

monthly thereafter22 |

|

| Maximum |

|

$0.21 per $1,000 of rider coverage amount |

| Minimum |

|

$0.03 per $1,000 of rider coverage amount |

| Charge for an Insured, Issue

Age 0 |

|

$0.03 per $1,000 of rider

coverage amount |

| Spouse Term Life Insurance

Benefit |

On the rider date of issue and

monthly thereafter23 |

|

| Maximum |

|

$83.3333 per $1,000 of rider coverage amount |

| Minimum |

|

$0.02 per $1,000 of rider coverage amount |

| Charge for a female Insured,

Issue Age 40, in the standard

nontobacco risk class with a

rider coverage amount of

$250,000, in the first Contract

Year |

|

$0.10 per $1,000 of rider coverage amount |

20 Any amount selected by the Contract Owner at issue between a pre-defined range. The minimum

amount is the basic Death Benefit Guarantee Premium amount and the maximum amount is the guideline level premium as described under the Internal Revenue Code. 21 The charge stops when the rider terminates. 22 This charge applies until the Insured’s Attained Age 43. 23 This charge applies until the rider coverage ends.

11

The next item shows the minimum

and maximum total annual operating expenses charged by the Portfolios that investors will bear during the time that they own the

Contract. This table shows the range (maximum and minimum) of fees and expenses (including management fees and other expenses) charged by the Portfolios, expressed as an annual percentage of average daily net assets. A complete list of the Portfolios corresponding to

Subaccounts available under the

Contract, including their annual expenses, may be found at the back of this

document in the Appendix

.

| Annual Portfolio Expenses |

MINIMUM |

MAXIMUM |

| Expenses that are deducted from

Portfolio assets, including management fees, distribution

fees and other expenses. |

0.22% |

1.52% |

| Expenses that are deducted from

Portfolio assets, after reimbursements and/or fee

waivers.* |

0.22% |

1.15%* |

* The reimbursements and/or fee waivers will last until April 30, 2026, but may be terminated at any time in the future.

As a fraternal benefit society, Thrivent is also required to have a Maintenance of Solvency provision that could require you

to pay us an amount to maintain our financial strength. For a complete discussion of the Maintenance of Solvency

provision, see Maintenance of Solvency in the statutory prospectus.

Investment Risk

The Contract is not suitable as a short-term investment vehicle. If you invest your accumulated value in one or more Subaccounts, then you will be subject to the risk that investment performance of the Subaccounts will be unfavorable and

that the accumulated value will decrease. The assets in each Subaccount are invested in a corresponding Portfolio of the Fund. A comprehensive discussion of the risks of each Portfolio may be found in the Fund’s prospectus. You could lose

everything you invest and your Contract could lapse without value, unless you pay additional premium. If you allocate premiums to the Fixed Account, then we credit your accumulated value in the Fixed Account with a declared rate of interest.

You assume the risk that the rate may decrease, although the Fixed Account rate will never be lower than a guaranteed minimum annual effective rate of 3%.

Risk of Lapse

If your monthly deductions

exceed your Cash Surrender Value and a Death Benefit Guarantee is not in effect, your Contract will enter a 61-day (in most states) grace period. We will notify you that

your Contract will lapse (that is, terminate without value) if you do not send us a sufficient payment by a specified date. Your Contract generally will not lapse:

♦

if you make timely payment of the minimum premium amount required to keep your Death Benefit

Guarantee in effect; or

♦

if during the grace period you make a payment sufficient to cover the next two monthly

deductions plus any additional amount necessary to bring your Cash Surrender Value to a positive balance before the end of the grace period. Subject to certain conditions, you may reinstate a lapsed Contract.

Tax Risks

We anticipate that the Contract should be deemed a life insurance contract under federal tax law. However, the federal income tax requirements applicable to the Contract are complex and there is limited guidance and some uncertainty about the

application of the federal tax law to the Contract. Assuming that the Contract qualifies as a life insurance contract for federal income tax purposes, you should not be deemed to

be in constructive receipt of Accumulated Value. However, the IRS could determine that a Contract Owner is in constructive receipt of the Accumulated Value if the Accumulated Value

becomes equal to the Death Benefit, which can occur in some instances where the Insured is Attained Age 95 or older. In a case where there may be constructive receipt, an amount equal to the excess of the Accumulated Value over the investment

in the contract could be includible in the Contract Owner’s income at that time. Under current tax law, Death

12

Proceeds payable under the Contract generally

would be excludable from the gross income of the Beneficiary. As a result, the Beneficiary generally should not have to pay U.S. federal income tax on the Death Proceeds. However,

the Death Proceeds may be subject to state and/or federal estate and/or inheritance tax.

Depending on the total amount of premiums you pay, the Contract may be treated as a MEC under federal tax laws. If a contract is treated as a MEC, then surrenders, partial surrenders, and loans under the Contract will be taxable as ordinary

income to the extent there are earnings in the Contract. In addition, a 10% penalty tax may be imposed on surrenders, partial surrenders, and loans taken before you reach age 59 1∕2. If the Contract is not a MEC, distributions

generally will be treated first as a return of your investment in the Contract and then as taxable income. Moreover, loans generally will not be treated as distributions. Finally, neither distributions nor loans from a Contract that is not a MEC are subject to the 10%

penalty tax. See

Taxes.

If the Contract lapses, a tax may result. Additionally, if the

Contract lapses and is later reinstated, the Contract may be treated as a MEC.

We make no guarantees regarding any tax treatment—federal, state or

local—of any Contract or of any transaction involving a Contract.

You should consult a qualified tax advisor for assistance in all Contract-related tax

matters.

Surrender and Partial Surrender

Risks

A Decrease Charge applies during the first 10 Contract Years after the Date of Issue and for 10 years after each

increase in Face Amount. Depending on the amount of premium paid, or any decreases in Face Amount, there may be little or no Cash Surrender Value available to you at the time you surrender your Contract. You should purchase the Contract only if you

have the financial ability to keep it in force for a substantial period of time. You should not purchase the Contract if you intend to surrender all or part of the Accumulated

Value in the near future. We designed the Contract to meet long-term financial goals. The Contract is not suitable as a short-term investment.

Even if you do not ask to surrender your Contract, Decrease Charges may play a role in determining whether your Contract will lapse (terminate without value). This is because Decrease Charges affect the Cash Surrender Value, a measure

we use to determine whether your Contract will enter a grace period (and possibly lapse). See Risk of Lapse in this section.

A partial surrender will reduce Accumulated Value, death benefit and the amount of premiums

considered paid to meet the Death Benefit Guarantee Premium requirement. If you select a Level Death Benefit Option, a partial surrender also will generally reduce the Face Amount of the Contract.

A surrender or partial surrender may have tax consequences. See Taxes.

Loan Risks

A Contract loan will affect Accumulated Value over time because we transfer the amount of the loan from the Subaccounts and/or Fixed Account to the Loan Account where the value serves as collateral to assure repayment of the Loan. This loan

collateral does not participate in the investment performance of the Subaccounts.

The non-preferred loan amounts will grow and must be repaid. If the

loan is not repaid during the Insured’s life, we reduce the amount we pay on the Insured’s death by the amount of any outstanding Debt to repay the loan. A loan will reduce your Cash Surrender Value, Death Proceeds and the amount of premiums considered to meet the Death

Benefit Guarantee Premium requirement. If you surrender the Contract or allow it to lapse while a Contract loan is outstanding, the Loan Account collateral will be used to repay the Debt and the amount of Debt, to the extent it has not previously been

taxed, will be considered part of the amount you have received and taxed accordingly. A loan may have immediate tax consequences if your Contract is a MEC, even if you do not surrender the Contract or allow it to lapse. See

Taxes.

13

Portfolio Risks

A comprehensive discussion of the risks of each Portfolio in which the Subaccounts invest may be found in the summary prospectus for each Fund. Please refer to the summary prospectus for the Fund for more information. There is no assurance

that any Portfolio will achieve its stated investment objective.

Short-Term Investment Risk

The Contract is not designed for short-term investing and is not appropriate for an investor who needs ready access to cash. The Contract is more beneficial to investors with a long time horizon. Surrender charges, expenses, and tax

consequences make the Contract unsuitable as a short-term investment.

Insurance Company Risk

An investment in the

Contract is subject to the risks related to Thrivent. Any obligations, guarantees, and benefits of the Contract are subject to the claims-paying ability and financial strength of

Thrivent. If Thrivent experiences financial distress, it may not be able to meet its obligations to you. More information about Thrivent, including its financial strength

ratings, is available upon request by calling 1-800-847-4836.

Fixed Account Risk

Interest guarantees are

subject to Thrivent's claims paying ability.

Premium Payment Risk

We reserve the right to not accept premiums when the Death Benefit is based on the Table of Factors in your Contract. We will also have the right to limit or refund a premium payment or make distributions from the Contract as necessary to

continue to qualify the Contract as life insurance under federal tax law or to avoid the classification of your Contract as a MEC.

Fees and Charges

Deduction of Contract fees and charges, and optional benefit charges, may result in loss of principal. We reserve the right to increase the fees and charges under the Contract and optional benefits up to the maximum guaranteed fees and charges

stated in your Contract or optional benefit rider.

Risks Affecting our Administration of Your Contract

We and our service providers and business partners are subject to certain risks, including those resulting from system failures, cybersecurity events, pandemics and epidemics and other disasters. Such events can adversely impact us and our

operations. These risks are common to all insurers and financial service providers and may materially impact our ability to administer the Contract (and to keep Contract owner

information confidential).

Alternatives to the Contract

Other contracts or investments may provide more favorable returns or benefits than the Contract.

Potentially Harmful Transfer Activity

The Contract is not designed for frequent transfers by anyone. Frequent transfers between subaccounts may disrupt the underlying Portfolios and could negatively impact performance, by interfering with efficient management and reducing

long-term returns, and increasing administrative costs. Frequent transfers may also dilute the value of shares of an underlying Portfolio. Neither the Contracts nor the underlying Portfolios are meant to promote any active trading strategy,

like market timing. Allowing frequent transfers by one or some Contract Owners could be at the expense of other Contract Owners. To protect Contract Owners and the underlying Portfolios, we have policies and procedures to deter frequent

transfers between and among the Subaccounts. We cannot guarantee that these policies and procedures will be effective in detecting and preventing all transfer activity that could potentially disadvantage or hurt the rights or interests of other

Contract Owners.

14

Risk of Increase in Current Fees

and Expenses

Certain

insurance charges are currently assessed at less than their maximum levels. We may increase these current charges in the future up to the guaranteed maximum levels, based on

changes in the Company’s future expectations of relevant factors, as determined in its sole discretion. Although some Portfolios may have expense limitation

agreements, the operating expenses of the Portfolios are not guaranteed and may increase or decrease over time. If fees and expenses are increased, you may need to increase the amount and/or frequency of Premium Payments to keep

the Contract in force.

Cybersecurity Risk

We and our service providers may be susceptible to operational, cybersecurity, and related risks. In general, cybersecurity events can result from deliberate or unintentional events. Cybersecurity events include, but are not limited to, acts or

attempts to gain unauthorized access to information and/or information systems, or to otherwise disrupt operations. Cybersecurity events affecting us, a Subaccount, or our service providers have the ability to disrupt and impact your

Contract and our operations, including but not limited to, financial losses, ability to calculate Contract values and benefits, corrupting data or preventing parties from sharing information necessary for our operations, preventing and/or slowing

transactions, potentially subjecting us to regulatory fines and penalties, and creating additional compliance costs. Similar types of cybersecurity risks are also present for issuers or securities in which the Subaccounts may invest, which could

result in material adverse consequences for such issuers and may cause the Subaccounts’ investments in such

companies to lose value. While we and our service providers have established reasonable controls to mitigate the risk of a cybersecurity event, there are inherent limitations in such controls, plans and systems. Additionally, while we do have

control frameworks and we do perform due diligence on our service providers, we cannot fully control the cybersecurity plans and systems put in place by our service providers or any other third parties whose operations may affect the

Subaccounts or your Contract. Although we attempt to minimize such failures through controls and oversight, it is not possible to identify all operation risks that may affect the Subaccounts or your Contract, or to develop processes and

controls that completely eliminate or mitigate the occurrence of such failures or other disruptions in service. The value of an investment in a Subaccount may be adversely affected by the occurrence of the operational errors, failures, technological

issues, or other similar events, and you may bear costs tied to these risks.

Description of the Insurance Company, Registered Separate Account, and

Portfolios

Insurance Company

Thrivent Financial for

Lutherans is the insurance company that issues the Contract with principal executive offices located at 600 Portland Ave S., Suite 100 Minneapolis, MN 55415. Thrivent is a

not-for-profit financial services membership organization of Christians helping our members achieve financial security and give back to their communities. We were organized in 1902 as a fraternal benefit society under Wisconsin law, and comply with Internal Revenue Code Section

501(c)(8). We are licensed to sell insurance in all states and the District of Columbia. For more information, visit Thrivent.com.

Registered Separate Account

Thrivent Variable Life Account I is the Registered Separate Account for the Contract. Thrivent Variable Life Account

I is a segregated asset account established by the Board of Directors of Thrivent (then, Aid Association for Lutherans) on May 8, 1997, pursuant to the laws of the State of Wisconsin, and the first investment was made on March 31, 1998. The

account meets the definition of “separate account” under the federal securities laws. The Variable Account is a unit investment trust, which is a type of investment company. It is registered with the Securities and Exchange Commission (SEC)

under the 1940 Act. Such registration does not involve supervision by the SEC of the management or investment policies or practices of the Variable Account.

15

Income, gains and losses credited to, or charged

against, the separate account reflect the separate account’s own investment experience and not the investment experience for the Insurance Company’s other assets. The

assets of the separate account may not be used to pay any liabilities of the Insurance Company other than those arising from the Contracts. The Insurance Company is obligated to pay all amounts promised to investors under the Contracts. Thrivent is

relying on the exemption provided by rule 12h-7 under the Securities Exchange Act (17 CFR 240.12h-7).

Portfolios

Information regarding each Portfolio, including its name, investment type, investment advisor and sub-advisor (if applicable), current expenses and performance is available in the Appendix to this prospectus. Each Portfolio has issued a

prospectus containing more detailed information about the Portfolio. You can view these online at dfinview.com/Thrivent/VariableLife03. You can also request paper copy by calling our Service Center at 1-800-847-4836, or by sending an email request to

mail@thrivent.com.

Voting

To the extent required by

law, we will vote the Portfolio’s shares held in the Variable Account at regular and special shareholder meetings of the Portfolio in accordance with instructions received

from persons having voting interests in the corresponding Subaccounts (investment options) of the Variable Account. If, however, the 1940 Act or any regulation thereunder should be amended or if the present interpretation thereof should change, and as a result we determine that we

are permitted to vote the Fund’s shares in our own right, we may elect to do so.

Any Portfolio shares held in the Variable Account for which we do not receive timely voting

instructions, or which are not attributable to Contract Owners, will be voted by us in proportion to the instructions received from all Contract Owners. Any Portfolio shares held by us or our affiliates in General Accounts will, for voting purposes, be allocated to all separate

accounts of ours and our affiliates having a voting interest in that Portfolio in proportion to each such separate account’s votes. Voting instructions to abstain on any item to be voted upon will be applied on a pro rata basis to reduce the votes

eligible to be cast.

Each person having a voting interest in a Subaccount will receive proxy materials, reports

and other materials relating to the appropriate Portfolio.

Important Notice Regarding Delivery of Documents

In response to concerns

regarding multiple mailings, we send one copy of a prospectus to each household. This process is known as householding. This consolidation helps reduce printing and postage costs,

thereby saving money. If you wish to receive additional copies, call us toll-free at 800-847-4836. If you wish to revoke householding in the future, you may write to us at P.O. Box 8075, Appleton, WI 54912-8075, or call us at 800-847-4836. We will begin to mail separate regulatory

mailings within 30 days of receiving your request.

Charges are necessary to pay Death Benefits and to cover the expenses generated by issuing, distributing and administering the Contract. We expect to profit from one or more of the charges under the Contract. We can use these profits

from any of these charges for any corporate purpose including our fraternal activities.

Percent of Premium Charge

We charge a Percent

of Premium Charge of 5% on premiums. We use this charge to cover the costs of sales and other expenses.

Decrease Charge

If you elect to surrender your Contract, reduce the Face Amount, or if the Face Amount is decreased as a result of a partial surrender or Death Benefit Option change, we will reduce your Accumulated Value by the applicable Decrease Charge.

Decrease Charges compensate us for expenses associated with underwriting, issuing and distributing the

16

Contract. For decreases in the Face Amount or

partial surrenders that result in a decrease in Face Amount during the first 10 Contract Years (or first 10 years following an increase in Face Amount), we calculate the amount of

the Decrease Charge at the time of the reduction in Face Amount or surrender. We do not deduct this amount until the next Monthly Anniversary or upon surrender or lapse, if earlier. We do not impose any other charges (such as mortality and expense risk

charges) on the Decrease Charge amount during this time. Because the Decrease Charge is not immediately deducted, you retain the investment risk on such amount prior to deduction

and will bear any investment loss and benefit from any investment gain on such amounts. If the Decrease Charge applies to a partial surrender, the Decrease Charge will be deducted from the Subaccounts and Fixed Account in the same ratios as used for the partial surrender. If the

Decrease Charge applies to other Face Amount decreases, the Decrease Charge will be deducted from the Subaccounts

and Fixed Account in the same ratios as the monthly deduction is taken. New Decrease Charges apply to each Face

Amount increase.

The Decrease Charge is assessed on a per thousand basis. The amount per thousand of Face

Amount varies by sex (in most states), Face Amount, risk class and Issue Age. For the first five Contract Years, the Decrease Charge remains level then grades to zero after the 10th Contract Year. Beginning in the 11th year after the Date of Issue (assuming no increases

in Face Amount), the Decrease Charge will be zero. We list your Decrease Charges in your Contract.

If you increase your Contract’s Face Amount, a new Decrease Charge is applicable to

the increase, in addition to any existing Decrease Charge. We list your actual Decrease Charges for the increased Face Amount separately on a supplementary Contract schedule. We mail the supplementary Contract schedule to you after we process the request for

increase in Face Amount.

Range of Decrease Charges as a Percentage of Face Amount

Reduction

| Duration in Years Since Face

Amount Increase |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

| Lowest Possible Charge at

Any Age |

0.17% |

0.17% |

0.17% |

0.17% |

0.17% |

0.14% |

0.11% |

0.08% |

0.06% |

0.03% |

0.00% |

| Highest Possible Charge at

Any Age |

4.93% |

4.93% |

4.93% |

4.93% |

4.93% |

4.10% |

3.28% |

2.46% |

1.64% |

0.82% |

0.00% |

If you decrease the Face Amount while the Decrease Charge applies, we assess a Decrease Charge on a per $1,000 basis. We

subtract the amount of decrease first from any previous increases in the Face Amount, starting with the most recent and then as needed from the original Face Amount.

Transfer Charge

You may make up to twelve transfers per Contract Year from the Subaccounts without charge. We charge $25 for each transfer in excess of twelve per Contract Year. This charge is deducted from the Subaccounts and the Fixed Account in

proportion to the amount transferred from each. Transfers resulting from Dollar Cost Averaging, asset rebalancing and loans do not count as transfers for the purpose of assessing this charge.

Monthly Deductions from Accumulated Value

We

deduct certain charges from Accumulated Value on a monthly basis. We refer to these charges as monthly deductions. Monthly deductions are deducted from each Subaccount or Fixed

Account on a basis proportional to the Accumulated Value less any loan interest in the Contract. With our approval, you may choose other allocations of the monthly deductions. We deduct charges each month, beginning with the Contract Date (effective retroactive to the Date of

Issue, if different) then monthly thereafter on each Monthly Deduction Date, provided that day of the month is a Valuation Date. If that day of the month does not fall on a Valuation Date, we use the next Valuation Date. Because portions of the

deductions (e.g., the cost of insurance) can vary from month to month, the aggregate monthly deductions also will vary.

17

The monthly deductions consist of:

♦

the cost of insurance charge;

♦

the monthly mortality and expense risk charge;

♦

the monthly administrative charge; and

♦

charges for additional insurance benefits (riders), if any.

Cost of

Insurance Charge

We assess a monthly cost of insurance charge to compensate us for underwriting the death benefit. The

charge depends on a number of variables (including Issue Age, sex (in most states), risk class, rating class, duration, and Face Amount) that would cause it to vary from Contract to Contract.

The primary factors in the determination of the cost of insurance are the cost of insurance rate (or rates) and the net

amount at risk. The cost of insurance charge for the initial Face Amount equals: the cost of insurance rate for the Insured’s age shown in your Contract, multiplied by the initial net amount at risk of your Contract divided by 1,000. Factors that

affect the amount at risk include investment performance, payment of premiums, charges, partial surrenders and

surrenders. We deduct the cost of insurance charge on each date we assess monthly deductions, starting with your

Contract Date (effective retroactive to the Date of Issue, if different).

We underwrite the applicant to determine the risk class using information provided in the

application and in other sources permitted by law. The factors that we consider for underwriting include, but are not limited to:

♦

the amount of insurance applied for,

♦

the proposed Insured’s age,

♦

outcome of medical testing,

♦

reports from physicians (attending physicians’ statements); and/or

♦

other information such as financial information that may be required.

Based on this information, standard or preferred coverage may be offered, or if it is determined that risks for a proposed

Insured are higher than would be the case for a healthy individual, the proposed Insured may receive a rating which increases cost of insurance rates or, in some cases, the proposed Insured may be declined.

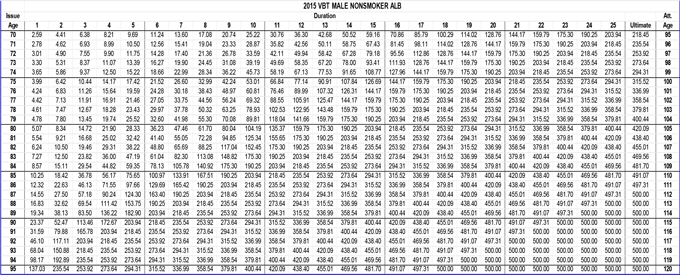

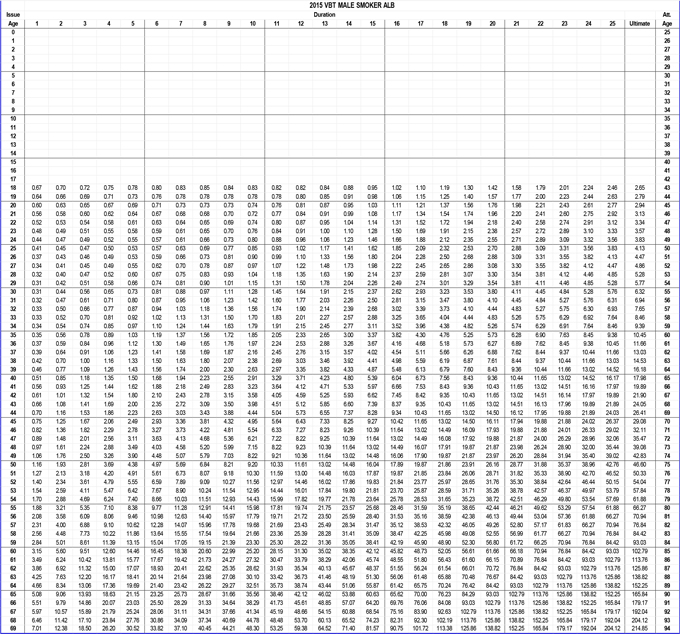

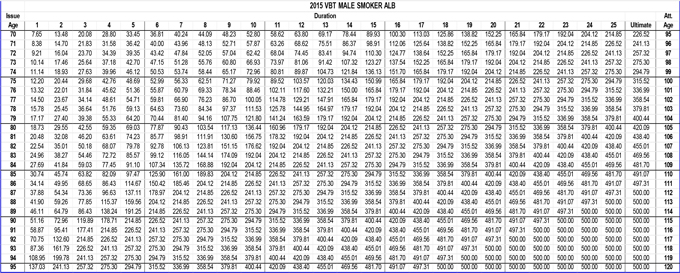

Cost of Insurance Rates

Cost of insurance rates are determined for the initial Face Amount and each increase in Face Amount. Actual cost of

insurance rates may change, and we will determine the actual monthly cost of insurance rates based on allowable factors.

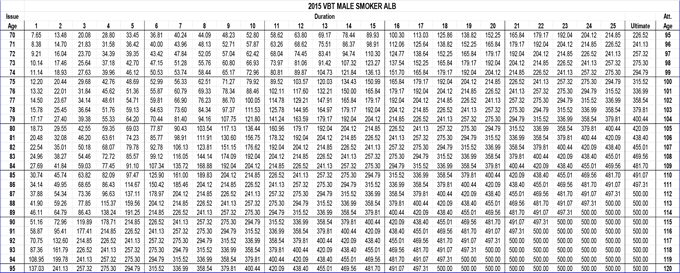

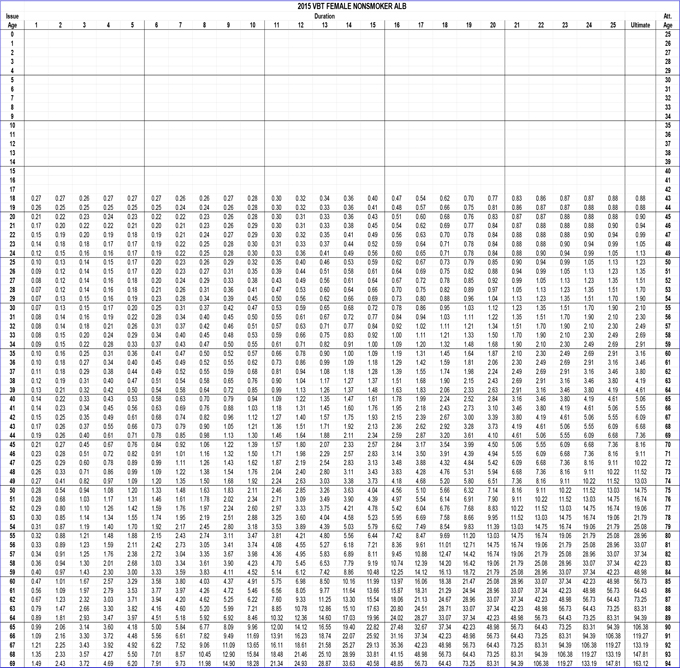

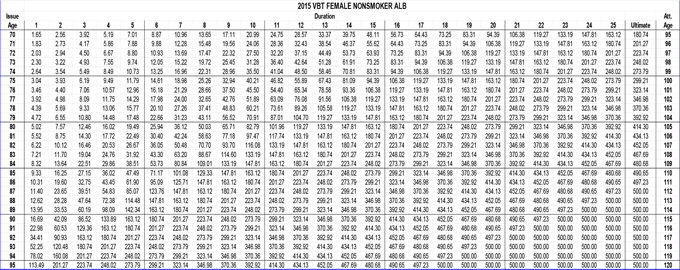

Actual cost of insurance rates will never be greater than the guaranteed maximum cost of insurance rates in the Contract. These guaranteed rates are determined based upon the Insured’s Attained Age and the applicable rate in the 1980 CSO

Mortality Tables for Non-smokers and Smokers. We currently use cost of insurance rates that are generally lower than the guaranteed cost of insurance rates, and we reserve the right to raise those current rates.

Our current cost of insurance rates apply uniformly to all Insureds of the same

Issue Age, Attained Age, sex, risk class and rating within the same band. Banding refers to the Face Amount. For purposes of this charge, the Insurance Coverage Amount includes any increases to the Face Amount made subsequent to the initial Face Amount and also includes the

amount of any term rider coverage on the Insured under this Contract. Face Amounts within increasingly higher bands will generally result in a reduced cost of insurance on a per

thousand basis. Any changes in the cost of insurance rates will apply uniformly to all Insureds of the same risk class within the same band. The bands for this charge are as follows:

18

| Banded Levels |

| $25,000 to $99,999 |

| $100,000 to $249,999 |

| $250,000 to $499,999 |

| $500,000 to $999,999 |

| $1,000,000 and above |

The cost of insurance rates generally increase as the Insured’s Attained Age increases, and they vary with the number of

years the Face Amount or any increase in Face Amount has been in force. The risk class of an Insured also will affect the cost of insurance rate. Insureds in the preferred risk class generally will have a lower cost of insurance rate than those in

risk classes involving higher mortality risk.

Insureds in non-tobacco risk classes will generally have a lower cost of insurance rate

than similarly situated Insureds in tobacco risk classes. We use the same guidelines in determining premiums for the cost of insurance for the Contract as we would for any other life insurance Contract of similar risk class we offer.

Mortality and Expense Risk Charges

The mortality and expense risk charge is a monthly charge for risks that we assume in the Contracts. The mortality risk

assumed is that Insureds, as a group, may live for a shorter period of time than we estimate and, therefore, the cost of insurance charges specified in the Contract would be insufficient to meet actual claims. The expense risk is that expenses

incurred in issuing and administering the Contracts and operating the Variable Account may be greater than the charges we assess for such expenses. We may use any profit to pay distribution, sales and other expenses.

The following table outlines our current annual mortality and expense risk

charge that will be assessed from and based on the Accumulated Value of all of your Subaccounts. These charges are different in Maryland. No mortality and expense risk charges are deducted from the Fixed Account. This is a tiered charge based on your Accumulated Value at the time the charge

is deducted.

| |

Maximum M&E Charge | |

| For Contract Years: | ||

| Subaccount Accumulated Value |

More than 10 years |

|

| 0 up to $25,000 |

0.90% |

|

| (monthly) |

(0.07469) |

|

| Next $75,000 |

0.80% |

|

| (monthly) |

(0.06642) |

|

| $100,000 and above |

0.70% |

|

| (monthly) |

(0.05815) |

|

Administrative Charge (Basic Monthly Charge)

We deduct a charge to cover administrative costs. This charge covers such expenses as premium billing and collection,

Accumulated Value calculation, transaction confirmations and periodic reports. This charge is dependent upon the Issue Age of the Insured. For Contracts we issue to Insureds whose Issue Age is from 0 to 17, we charge a monthly charge of $7.50.

We charge all others $9 per month.

19

Rider or Additional Benefit

Charge

If your Contract includes riders or additional benefits, we will deduct a monthly cost for those benefits from the

Accumulated Value. Benefits include guaranteed increase option, disability waivers, applicant waiver and accidental death, term insurance rider, child term rider and spouse term insurance rider.

Fund Charges

The value of the net assets of

each Subaccount reflects the investment advisory fee and other expenses incurred by the underlying Portfolios in which the Subaccount invests. For more information on these fees

and expenses, refer to the Fund’s summary prospectuses and Fee Tables above.

Variation or Reduction of Charges

We may vary the charges and other terms of the Contracts if special circumstances result in reduced sales expenses,

administrative expenses, or various risks. These variations will not be unfairly discriminatory to the interests of other Contract Owners. Variations may occur in Contracts sold to members of a class of associated individuals, an employer or

other entities representing an associated class.

Compensation Paid to Financial Advisors and Professionals

Compensation consists of commissions, bonuses and promotional incentives. Increases in coverage pay at a first-year commission rate of 20% to 92% of commissionable

premiums paid into the Contract. Your financial advisor or professional also receives a premium based trail compensation ranging from 0% to 7.448% annually.

Your financial advisor or professional may receive asset-based compensation in the amount of 0% to 0.312% of the Accumulated Value, if eligible. If you elect a settlement option, we pay commissions to the financial advisor or professional

ranging from 0% to 0.980% of the premium

applied to the settlement option, if eligible.

See Distribution of the Contracts for more information.

The Maintenance of Solvency provision is a legal requirement of a fraternal benefit society. The provision can come into play only when the reserves of a fraternal benefit society become impaired. That means there would be a serious concern with

the financial position of the society. It is extremely unlikely that Thrivent would be in an impaired condition considering its financial position. In the extraordinary event that

our reserves become impaired, you may be required to make an extra payment. This can happen only in the rare event that the insurance commissioner issued an order declaring us to

be in a hazardous condition. If that happened, our Board of Directors would work with the commissioner to determine each member’s portion of the deficiency. You could submit additional funds, have the amount treated as a debt against the

Contract, or take a reduction in benefits. Please be advised that a Maintenance of Solvency provision is applicable to all fraternal benefit societies, regardless of the financial position and ratings of the society. You may review our financial

statements and reports from our independent public accounting firm in the Statement of Additional Information (SAI) found online at dfinview.com/Thrivent/VariableLife03

General Description of the Contract

While the Insured is alive, the Owner of the Contract may exercise every right and enjoy

every benefit provided in the Contract.

For a Contract where the Insured and Owner of the Contract is younger than age 16

(juvenile), an adult must apply on behalf of the Insured in this case and retain control over the Contract. The adult is referred to as the applicant controller in the Contract. The applicant controller exercises certain rights of ownership on behalf of the juvenile. These rights are

described in the Contract. The applicant controller may transfer control to another eligible person but cannot transfer ownership of the Contract.

20

After the juvenile Insured/Owner attains age 16,

control will transfer to the Insured/Owner on the earlier of:

♦

the Contract Anniversary after the Insured’s 21st birthday;

♦

the date on which the applicant controller transfers control to the Insured/Owner by giving us

Notice; or

♦

the date of death of the applicant controller.

If the person who has control of the Contract dies before the juvenile Insured attains age 16, control will be vested in an

eligible person according to our bylaws. If we determine that it is best for the Insured, we may transfer control of the Contract to some other eligible person according to our bylaws.

Illustrations