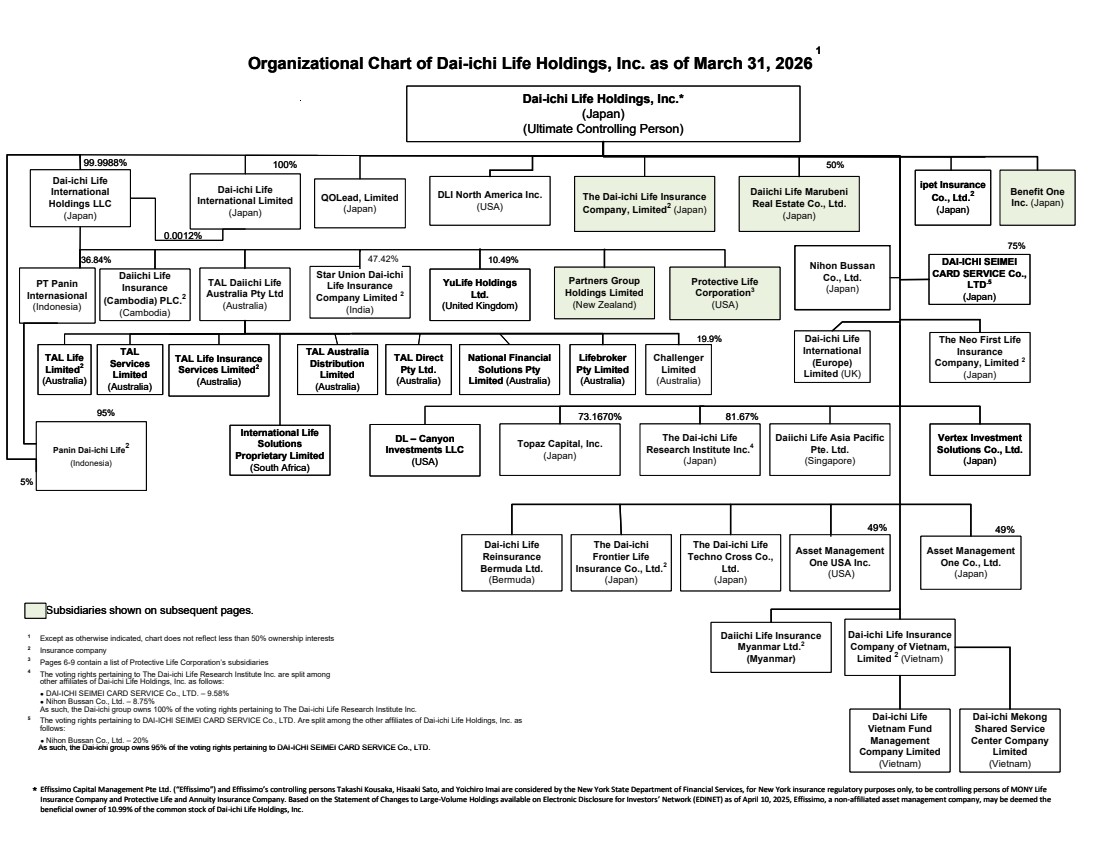

| 1 Except as otherwise indicated, chart does not reflect less than 50% ownership interests 2 Insurance company 3 Pages 6-9 contain a list of Protective Life Corporation’s subsidiaries 4 The voting rights pertaining to The Dai-ichi Life Research Institute Inc. are split among other affiliates of Dai-ichi Life Holdings, Inc. as follows: ● DAI-ICHI SEIMEI CARD SERVICE Co., LTD. – 9.58% ● Nihon Bussan Co., Ltd. – 8.75% As such, the Dai-ichi group owns 100% of the voting rights pertaining to The Dai-ichi Life Research Institute Inc. 5 The voting rights pertaining to DAI-ICHI SEIMEI CARD SERVICE Co., LTD. Are split among the other affiliates of Dai-ichi Life Holdings, Inc. as follows: ● Nihon Bussan Co., Ltd. – 20% As such, the Dai-ichi group owns 95% of the voting rights pertaining to DAI-ICHI SEIMEI CARD SERVICE Co., LTD. Dai-ichi Life Holdings, Inc.* (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Life International Holdings LLC (Japan) TAL Life Limited2 (Australia) Asset Management One Co., Ltd. (Japan) TAL Direct Pty Ltd. (Australia) TAL Services Limited (Australia) Asset Management One USA Inc. (USA) Dai-ichi Life Vietnam Fund Management Company Limited (Vietnam) The Dai-ichi Life Insurance Company, Limited2 (Japan) 1 49% Dai-ichi Life Insurance Company of Vietnam, Limited 2 (Vietnam) 81.67% International Life Solutions Proprietary Limited (South Africa) The Neo First Life Insurance Company, Limited 2 (Japan) Dai-ichi Life International (Europe) Limited (UK) Daiichi Life Asia Pacific Pte. Ltd. (Singapore) The Dai-ichi Life Research Institute Inc.4 (Japan) Star Union Dai-ichi Life Insurance Company Limited 2 (India) 36.84% 47.42% Lifebroker Pty Limited (Australia) DLI North America Inc. (USA) QOLead, Limited (Japan) Dai-ichi Life International Limited (Japan) Effissimo Capital Management Pte Ltd. (“Effissimo”) and Effissimo’s controlling persons Takashi Kousaka, Hisaaki Sato, and Yoichiro Imai are considered by the New York State Department of Financial Services, for New York insurance regulatory purposes only, to be controlling persons of MONY Life Insurance Company and Protective Life and Annuity Insurance Company. Based on the Statement of Changes to Large-Volume Holdings available on Electronic Disclosure for Investors’ Network (EDINET) as of April 10, 2025, Effissimo, a non-affiliated asset management company, may be deemed the beneficial owner of 10.99% of the common stock of Dai-ichi Life Holdings, Inc. * 99.9988% Daiichi Life Insurance (Cambodia) PLC.2 (Cambodia) The Dai-ichi Life Techno Cross Co., Ltd. (Japan) TAL Daiichi Life Australia Pty Ltd (Australia) National Financial Solutions Pty Limited (Australia) TAL Australia Distribution Limited (Australia) Vertex Investment Solutions Co., Ltd. (Japan) TAL Life Insurance Services Limited2 (Australia) YuLife Holdings Ltd. (United Kingdom) 10.49% Partners Group Holdings Limited (New Zealand) Protective Life Corporation3 (USA) PT Panin Internasional (Indonesia) ipet Insurance Co., Ltd.2 (Japan) Topaz Capital, Inc. (Japan) 73.1670% Panin Dai-ichi Life2 (Indonesia) 95% Dai-ichi Life Reinsurance Bermuda Ltd. (Bermuda) The Dai-ichi Frontier Life Insurance Co., Ltd.2 (Japan) 49% 5% Benefit One Inc. (Japan) DL – Canyon Investments LLC (USA) 100% 0.0012% DAI-ICHI SEIMEI CARD SERVICE Co., LTD.5 (Japan) 75% Daiichi Life Insurance Myanmar Ltd.2 (Myanmar) Daiichi Life Marubeni Real Estate Co., Ltd. (Japan) 50% Subsidiaries shown on subsequent pages. Challenger Limited (Australia) 19.9% Dai-ichi Mekong Shared Service Center Company Limited (Vietnam) Nihon Bussan Co., Ltd. (Japan) 1 Except as otherwise indicated, chart does not reflect less than 50% ownership interests 2 Insurance company 3 Pages 6-9 contain a list of Protective Life Corporation’s subsidiaries 4 The voting rights pertaining to The Dai-ichi Life Research Institute Inc. are split among other affiliates of Dai-ichi Life Holdings, Inc. as follows: ● DAI-ICHI SEIMEI CARD SERVICE Co., LTD. – 9.58% ● Nihon Bussan Co., Ltd. – 8.75% As such, the Dai-ichi group owns 100% of the voting rights pertaining to The Dai-ichi Life Research Institute Inc. 5 The voting rights pertaining to DAI-ICHI SEIMEI CARD SERVICE Co., LTD. Are split among the other affiliates of Dai-ichi Life Holdings, Inc. as follows: ● Nihon Bussan Co., Ltd. – 20% As such, the Dai-ichi group owns 95% of the voting rights pertaining to DAI-ICHI SEIMEI CARD SERVICE Co., LTD. Dai-ichi Life Holdings, Inc.* (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Life International Holdings LLC (Japan) TAL Life Limited2 (Australia) Asset Management One Co., Ltd. (Japan) TAL Direct Pty Ltd. (Australia) TAL Services Limited (Australia) Asset Management One USA Inc. (USA) Dai-ichi Life Vietnam Fund Management Company Limited (Vietnam) The Dai-ichi Life Insurance Company, Limited2 (Japan) 1 49% Dai-ichi Life Insurance Company of Vietnam, Limited 2 (Vietnam) 81.67% International Life Solutions Proprietary Limited (South Africa) The Neo First Life Insurance Company, Limited 2 (Japan) Dai-ichi Life International (Europe) Limited (UK) Daiichi Life Asia Pacific Pte. Ltd. (Singapore) The Dai-ichi Life Research Institute Inc.4 (Japan) Star Union Dai-ichi Life Insurance Company Limited 2 (India) 36.84% 47.42% Lifebroker Pty Limited (Australia) DLI North America Inc. (USA) QOLead, Limited (Japan) Dai-ichi Life International Limited (Japan) Effissimo Capital Management Pte Ltd. (“Effissimo”) and Effissimo’s controlling persons Takashi Kousaka, Hisaaki Sato, and Yoichiro Imai are considered by the New York State Department of Financial Services, for New York insurance regulatory purposes only, to be controlling persons of MONY Life Insurance Company and Protective Life and Annuity Insurance Company. Based on the Statement of Changes to Large-Volume Holdings available on Electronic Disclosure for Investors’ Network (EDINET) as of April 10, 2025, Effissimo, a non-affiliated asset management company, may be deemed the beneficial owner of 10.99% of the common stock of Dai-ichi Life Holdings, Inc. * 99.9988% Daiichi Life Insurance (Cambodia) PLC.2 (Cambodia) The Dai-ichi Life Techno Cross Co., Ltd. (Japan) TAL Daiichi Life Australia Pty Ltd (Australia) National Financial Solutions Pty Limited (Australia) TAL Australia Distribution Limited (Australia) Vertex Investment Solutions Co., Ltd. (Japan) TAL Life Insurance Services Limited2 (Australia) YuLife Holdings Ltd. (United Kingdom) 10.49% Partners Group Holdings Limited (New Zealand) Protective Life Corporation3 (USA) PT Panin Internasional (Indonesia) ipet Insurance Co., Ltd.2 (Japan) Topaz Capital, Inc. (Japan) 73.1670% Panin Dai-ichi Life2 (Indonesia) 95% Dai-ichi Life Reinsurance Bermuda Ltd. (Bermuda) The Dai-ichi Frontier Life Insurance Co., Ltd.2 (Japan) 49% 5% Benefit One Inc. (Japan) DL – Canyon Investments LLC (USA) 100% 0.0012% DAI-ICHI SEIMEI CARD SERVICE Co., LTD.5 (Japan) 75% Daiichi Life Insurance Myanmar Ltd.2 (Myanmar) Daiichi Life Marubeni Real Estate Co., Ltd. (Japan) 50% Subsidiaries shown on subsequent pages. Challenger Limited (Australia) 19.9% Dai-ichi Mekong Shared Service Center Company Limited (Vietnam) Nihon Bussan Co., Ltd. (Japan) |

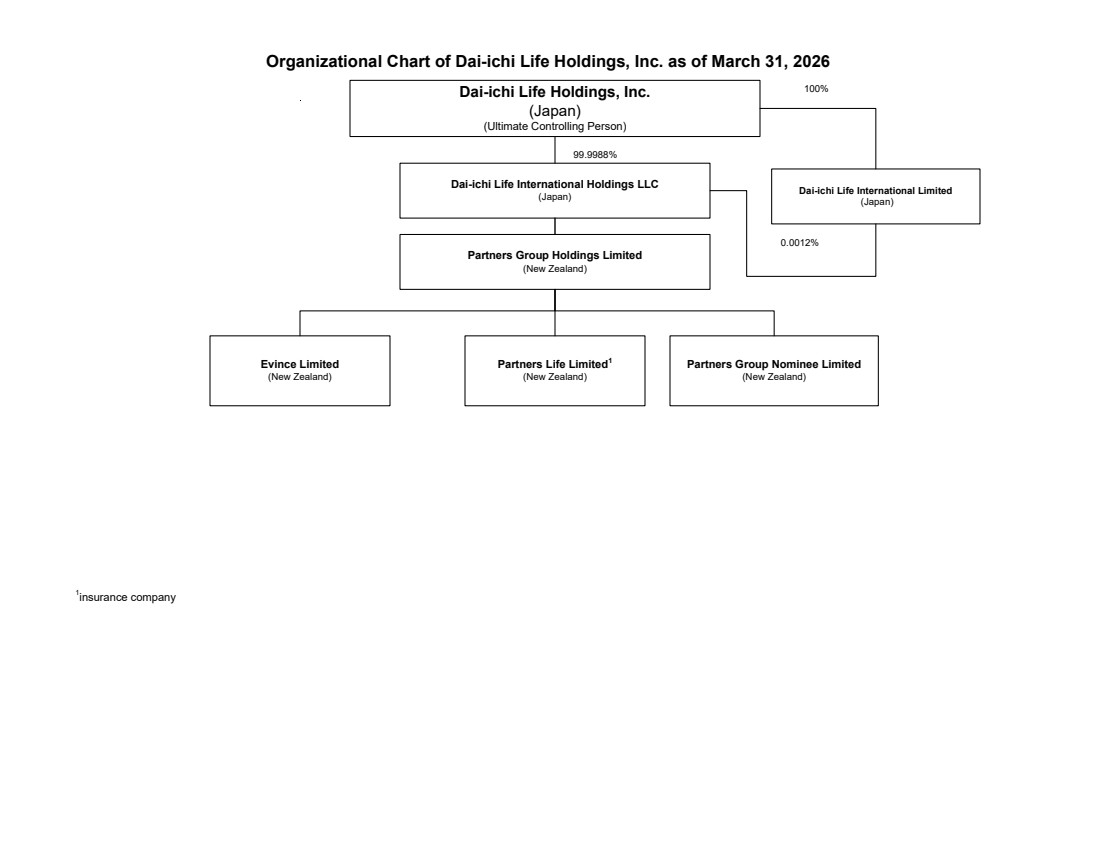

| Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Partners Life Limited1 (New Zealand) Dai-ichi Life International Holdings LLC (Japan) Evince Limited (New Zealand) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Partners Group Nominee Limited (New Zealand) Partners Group Holdings Limited (New Zealand) 1 insurance company Dai-ichi Life International Limited (Japan) 99.9988% 0.0012% 100% |

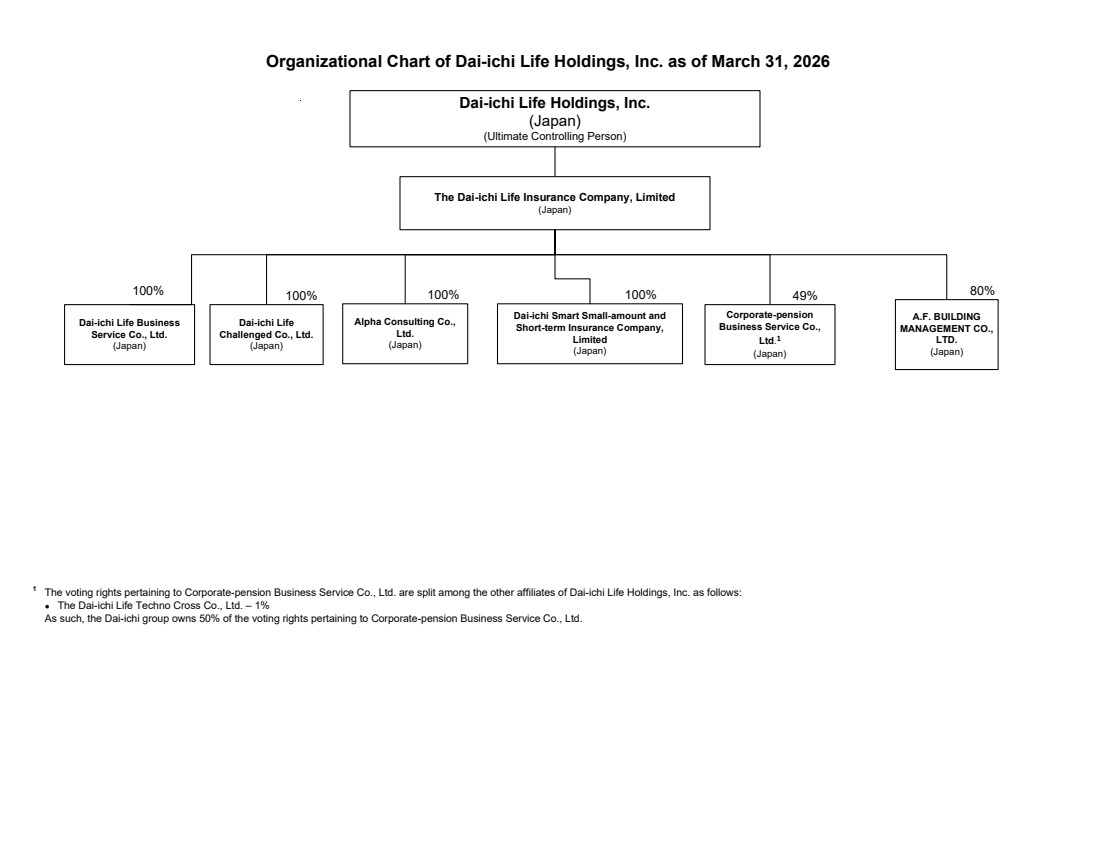

| Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life Challenged Co., Ltd. (Japan) 49% 80% 1 The voting rights pertaining to Corporate-pension Business Service Co., Ltd. are split among the other affiliates of Dai-ichi Life Holdings, Inc. as follows: ● The Dai-ichi Life Techno Cross Co., Ltd. – 1% As such, the Dai-ichi group owns 50% of the voting rights pertaining to Corporate-pension Business Service Co., Ltd. The Dai-ichi Life Insurance Company, Limited (Japan) A.F. BUILDING MANAGEMENT CO., LTD. (Japan) Dai-ichi Life Business Service Co., Ltd. (Japan) 100% Alpha Consulting Co., Ltd. (Japan) 100% Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Smart Small-amount and Short-term Insurance Company, Limited (Japan) 100% 100% Corporate-pension Business Service Co., Ltd. 1 (Japan) |

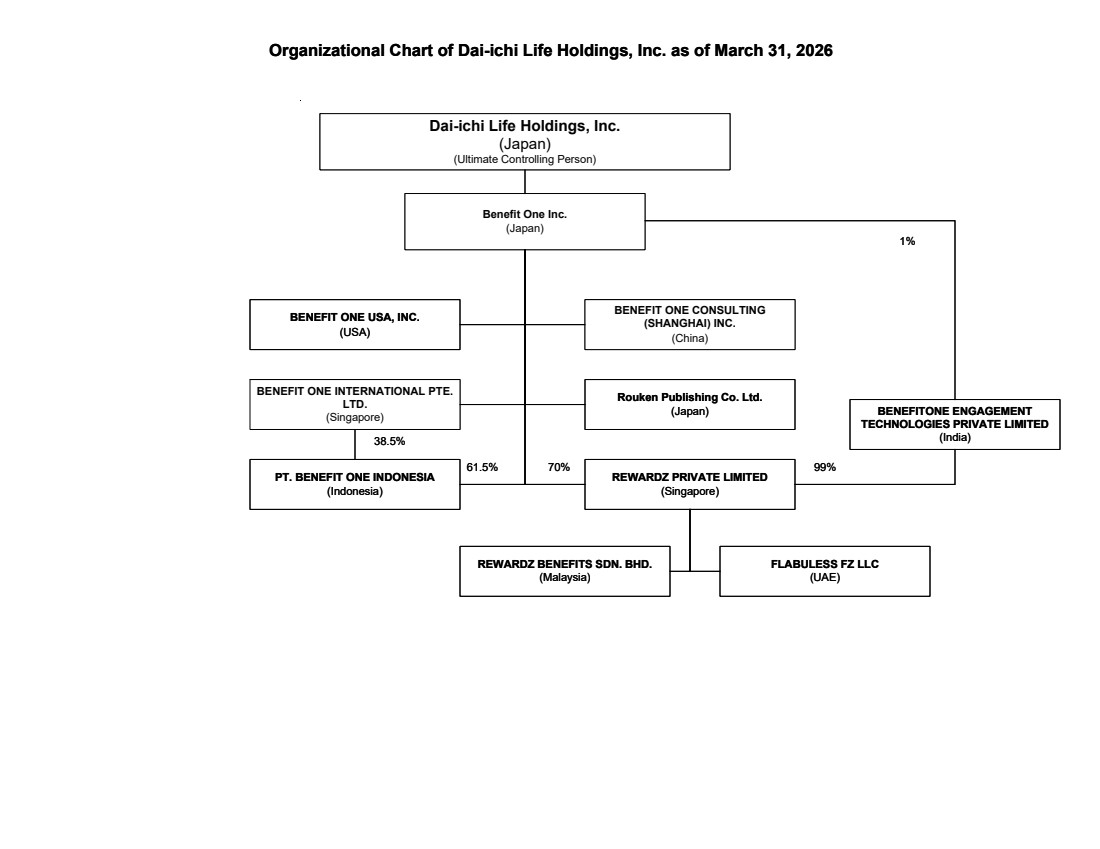

| Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Benefit One Inc. (Japan) BENEFIT ONE USA, INC. (USA) BENEFIT ONE INTERNATIONAL PTE. LTD. (Singapore) PT. BENEFIT ONE INDONESIA (Indonesia) REWARDZ BENEFITS SDN. BHD. (Malaysia) FLABULESS FZ LLC (UAE) REWARDZ PRIVATE LIMITED (Singapore) BENEFITONE ENGAGEMENT TECHNOLOGIES PRIVATE LIMITED (India) Rouken Publishing Co. Ltd. (Japan) BENEFIT ONE CONSULTING (SHANGHAI) INC. (China) 1% 61.5% 70% 99% 38.5% Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Benefit One Inc. (Japan) BENEFIT ONE USA, INC. (USA) BENEFIT ONE INTERNATIONAL PTE. LTD. (Singapore) PT. BENEFIT ONE INDONESIA (Indonesia) REWARDZ BENEFITS SDN. BHD. (Malaysia) FLABULESS FZ LLC (UAE) REWARDZ PRIVATE LIMITED (Singapore) BENEFITONE ENGAGEMENT TECHNOLOGIES PRIVATE LIMITED (India) Rouken Publishing Co. Ltd. (Japan) BENEFIT ONE CONSULTING (SHANGHAI) INC. (China) 1% 61.5% 70% 99% 38.5% |

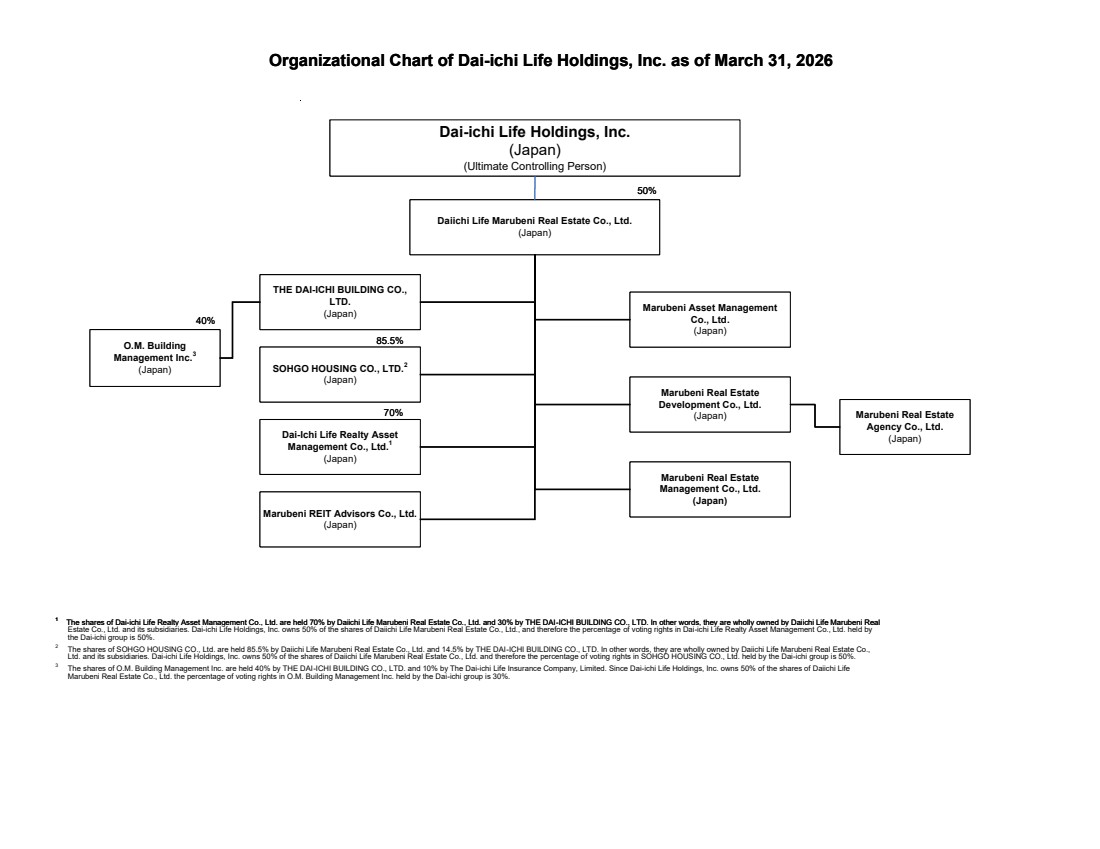

| Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Daiichi Life Marubeni Real Estate Co., Ltd. (Japan) THE DAI-ICHI BUILDING CO., LTD. (Japan) Marubeni Asset Management Co., Ltd. (Japan) O.M. Building Management Inc.3 (Japan) 50% SOHGO HOUSING CO., LTD.2 (Japan) Dai-Ichi Life Realty Asset Management Co., Ltd.1 (Japan) Marubeni REIT Advisors Co., Ltd. (Japan) Marubeni Real Estate Development Co., Ltd. (Japan) Marubeni Real Estate Management Co., Ltd. (Japan) 85.5% 40% 70% 1 The shares of Dai-ichi Life Realty Asset Management Co., Ltd. are held 70% by Daiichi Life Marubeni Real Estate Co., Ltd. and 30% by THE DAI-ICHI BUILDING CO., LTD. In other words, they are wholly owned by Daiichi Life Marubeni Real Estate Co., Ltd. and its subsidiaries. Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd., and therefore the percentage of voting rights in Dai-ichi Life Realty Asset Management Co., Ltd. held by the Dai-ichi group is 50%. 2 The shares of SOHGO HOUSING CO., Ltd. are held 85.5% by Daiichi Life Marubeni Real Estate Co., Ltd. and 14.5% by THE DAI-ICHI BUILDING CO., LTD. In other words, they are wholly owned by Daiichi Life Marubeni Real Estate Co., Ltd. and its subsidiaries. Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd. and therefore the percentage of voting rights in SOHGO HOUSING CO., Ltd. held by the Dai-ichi group is 50%. 3 The shares of O.M. Building Management Inc. are held 40% by THE DAI-ICHI BUILDING CO., LTD. and 10% by The Dai-ichi Life Insurance Company, Limited. Since Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd. the percentage of voting rights in O.M. Building Management Inc. held by the Dai-ichi group is 30%. Marubeni Real Estate Agency Co., Ltd. (Japan) Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Daiichi Life Marubeni Real Estate Co., Ltd. (Japan) THE DAI-ICHI BUILDING CO., LTD. (Japan) Marubeni Asset Management Co., Ltd. (Japan) O.M. Building Management Inc.3 (Japan) 50% SOHGO HOUSING CO., LTD.2 (Japan) Dai-Ichi Life Realty Asset Management Co., Ltd.1 (Japan) Marubeni REIT Advisors Co., Ltd. (Japan) Marubeni Real Estate Development Co., Ltd. (Japan) Marubeni Real Estate Management Co., Ltd. (Japan) 85.5% 40% 70% 1 The shares of Dai-ichi Life Realty Asset Management Co., Ltd. are held 70% by Daiichi Life Marubeni Real Estate Co., Ltd. and 30% by THE DAI-ICHI BUILDING CO., LTD. In other words, they are wholly owned by Daiichi Life Marubeni Real Estate Co., Ltd. and its subsidiaries. Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd., and therefore the percentage of voting rights in Dai-ichi Life Realty Asset Management Co., Ltd. held by the Dai-ichi group is 50%. 2 The shares of SOHGO HOUSING CO., Ltd. are held 85.5% by Daiichi Life Marubeni Real Estate Co., Ltd. and 14.5% by THE DAI-ICHI BUILDING CO., LTD. In other words, they are wholly owned by Daiichi Life Marubeni Real Estate Co., Ltd. and its subsidiaries. Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd. and therefore the percentage of voting rights in SOHGO HOUSING CO., Ltd. held by the Dai-ichi group is 50%. 3 The shares of O.M. Building Management Inc. are held 40% by THE DAI-ICHI BUILDING CO., LTD. and 10% by The Dai-ichi Life Insurance Company, Limited. Since Dai-ichi Life Holdings, Inc. owns 50% of the shares of Daiichi Life Marubeni Real Estate Co., Ltd. the percentage of voting rights in O.M. Building Management Inc. held by the Dai-ichi group is 30%. Marubeni Real Estate Agency Co., Ltd. (Japan) |

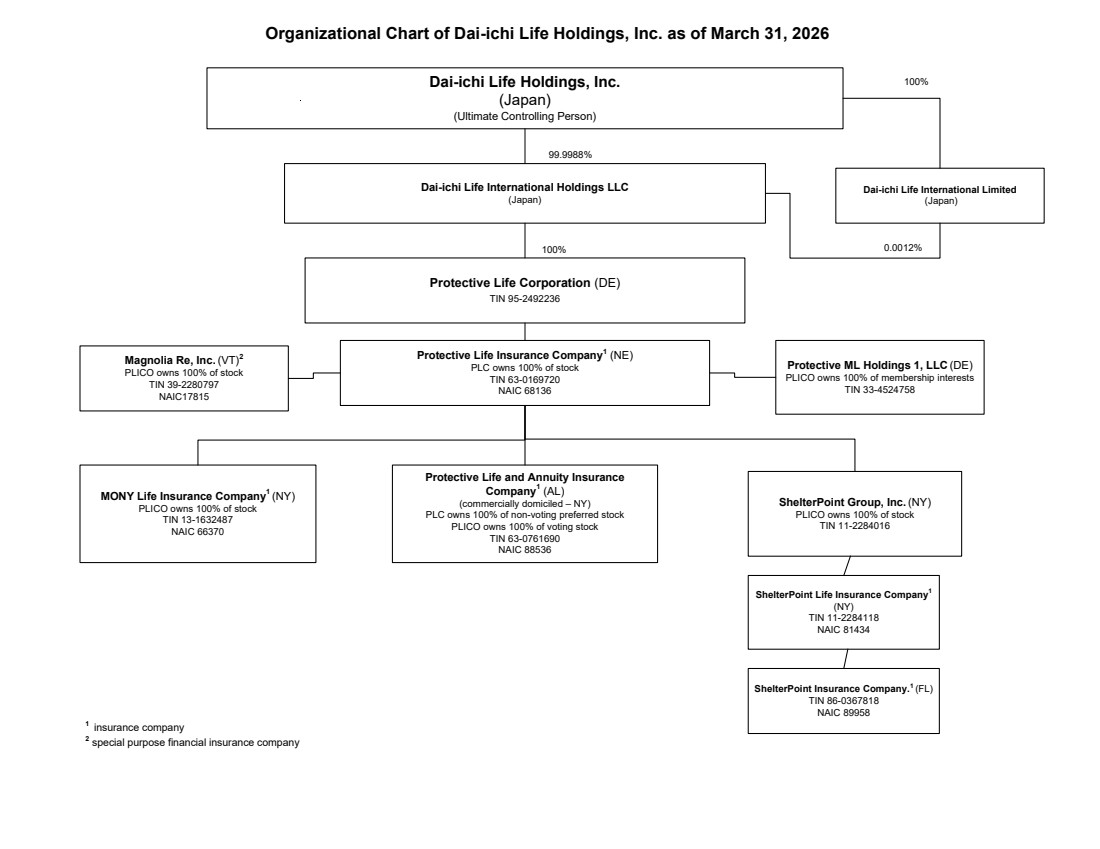

| Protective Life Corporation (DE) TIN 95-2492236 Protective Life Insurance Company1 (NE) PLC owns 100% of stock TIN 63-0169720 NAIC 68136 1 insurance company 2 special purpose financial insurance company Protective Life and Annuity Insurance Company1 (AL) (commercially domiciled – NY) PLC owns 100% of non-voting preferred stock PLICO owns 100% of voting stock TIN 63-0761690 NAIC 88536 MONY Life Insurance Company1 (NY) PLICO owns 100% of stock TIN 13-1632487 NAIC 66370 Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) ShelterPoint Group, Inc. (NY) PLICO owns 100% of stock TIN 11-2284016 ShelterPoint Life Insurance Company1 (NY) TIN 11-2284118 NAIC 81434 ShelterPoint Insurance Company.1 (FL) TIN 86-0367818 NAIC 89958 Dai-ichi Life International Limited (Japan) 99.9988% 0.0012% 100% 100% Protective ML Holdings 1, LLC (DE) PLICO owns 100% of membership interests TIN 33-4524758 Magnolia Re, Inc. (VT)2 PLICO owns 100% of stock TIN 39-2280797 NAIC17815 |

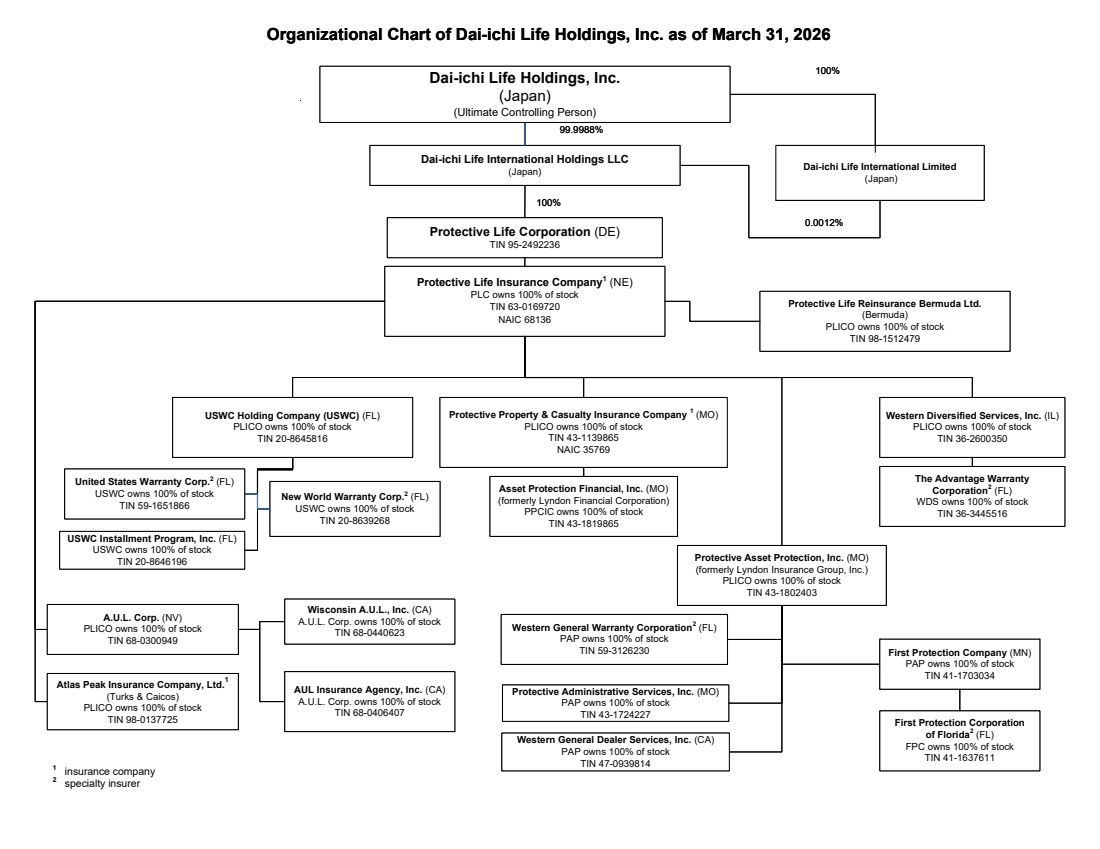

| Protective Life Corporation (DE) TIN 95-2492236 Protective Life Insurance Company1 (NE) PLC owns 100% of stock TIN 63-0169720 NAIC 68136 Protective Property & Casualty Insurance Company 1 (MO) PLICO owns 100% of stock TIN 43-1139865 NAIC 35769 Protective Asset Protection, Inc. (MO) (formerly Lyndon Insurance Group, Inc.) PLICO owns 100% of stock TIN 43-1802403 Asset Protection Financial, Inc. (MO) (formerly Lyndon Financial Corporation) PPCIC owns 100% of stock TIN 43-1819865 Western General Dealer Services, Inc. (CA) PAP owns 100% of stock TIN 47-0939814 Western General Warranty Corporation2 (FL) PAP owns 100% of stock TIN 59-3126230 First Protection Company (MN) PAP owns 100% of stock TIN 41-1703034 First Protection Corporation of Florida2 (FL) FPC owns 100% of stock TIN 41-1637611 Protective Administrative Services, Inc. (MO) PAP owns 100% of stock TIN 43-1724227 1 insurance company 2 specialty insurer USWC Holding Company (USWC) (FL) PLICO owns 100% of stock TIN 20-8645816 New World Warranty Corp.2 (FL) USWC owns 100% of stock TIN 20-8639268 USWC Installment Program, Inc. (FL) USWC owns 100% of stock TIN 20-8646196 United States Warranty Corp.2 (FL) USWC owns 100% of stock TIN 59-1651866 Western Diversified Services, Inc. (IL) PLICO owns 100% of stock TIN 36-2600350 The Advantage Warranty Corporation2 (FL) WDS owns 100% of stock TIN 36-3445516 Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Atlas Peak Insurance Company, Ltd.1 (Turks & Caicos) PLICO owns 100% of stock TIN 98-0137725 A.U.L. Corp. (NV) PLICO owns 100% of stock TIN 68-0300949 Wisconsin A.U.L., Inc. (CA) A.U.L. Corp. owns 100% of stock TIN 68-0440623 AUL Insurance Agency, Inc. (CA) A.U.L. Corp. owns 100% of stock TIN 68-0406407 Dai-ichi Life International Limited (Japan) 100% 99.9988% 0.0012% 100% Protective Life Reinsurance Bermuda Ltd. (Bermuda) PLICO owns 100% of stock TIN 98-1512479 Protective Life Corporation (DE) TIN 95-2492236 Protective Life Insurance Company1 (NE) PLC owns 100% of stock TIN 63-0169720 NAIC 68136 Protective Property & Casualty Insurance Company 1 (MO) PLICO owns 100% of stock TIN 43-1139865 NAIC 35769 Protective Asset Protection, Inc. (MO) (formerly Lyndon Insurance Group, Inc.) PLICO owns 100% of stock TIN 43-1802403 Asset Protection Financial, Inc. (MO) (formerly Lyndon Financial Corporation) PPCIC owns 100% of stock TIN 43-1819865 Western General Dealer Services, Inc. (CA) PAP owns 100% of stock TIN 47-0939814 Western General Warranty Corporation2 (FL) PAP owns 100% of stock TIN 59-3126230 First Protection Company (MN) PAP owns 100% of stock TIN 41-1703034 First Protection Corporation of Florida2 (FL) FPC owns 100% of stock TIN 41-1637611 Protective Administrative Services, Inc. (MO) PAP owns 100% of stock TIN 43-1724227 1 insurance company 2 specialty insurer USWC Holding Company (USWC) (FL) PLICO owns 100% of stock TIN 20-8645816 New World Warranty Corp.2 (FL) USWC owns 100% of stock TIN 20-8639268 USWC Installment Program, Inc. (FL) USWC owns 100% of stock TIN 20-8646196 United States Warranty Corp.2 (FL) USWC owns 100% of stock TIN 59-1651866 Western Diversified Services, Inc. (IL) PLICO owns 100% of stock TIN 36-2600350 The Advantage Warranty Corporation2 (FL) WDS owns 100% of stock TIN 36-3445516 Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Atlas Peak Insurance Company, Ltd.1 (Turks & Caicos) PLICO owns 100% of stock TIN 98-0137725 A.U.L. Corp. (NV) PLICO owns 100% of stock TIN 68-0300949 Wisconsin A.U.L., Inc. (CA) A.U.L. Corp. owns 100% of stock TIN 68-0440623 AUL Insurance Agency, Inc. (CA) A.U.L. Corp. owns 100% of stock TIN 68-0406407 Dai-ichi Life International Limited (Japan) 100% 99.9988% 0.0012% 100% Protective Life Reinsurance Bermuda Ltd. (Bermuda) PLICO owns 100% of stock TIN 98-1512479 |

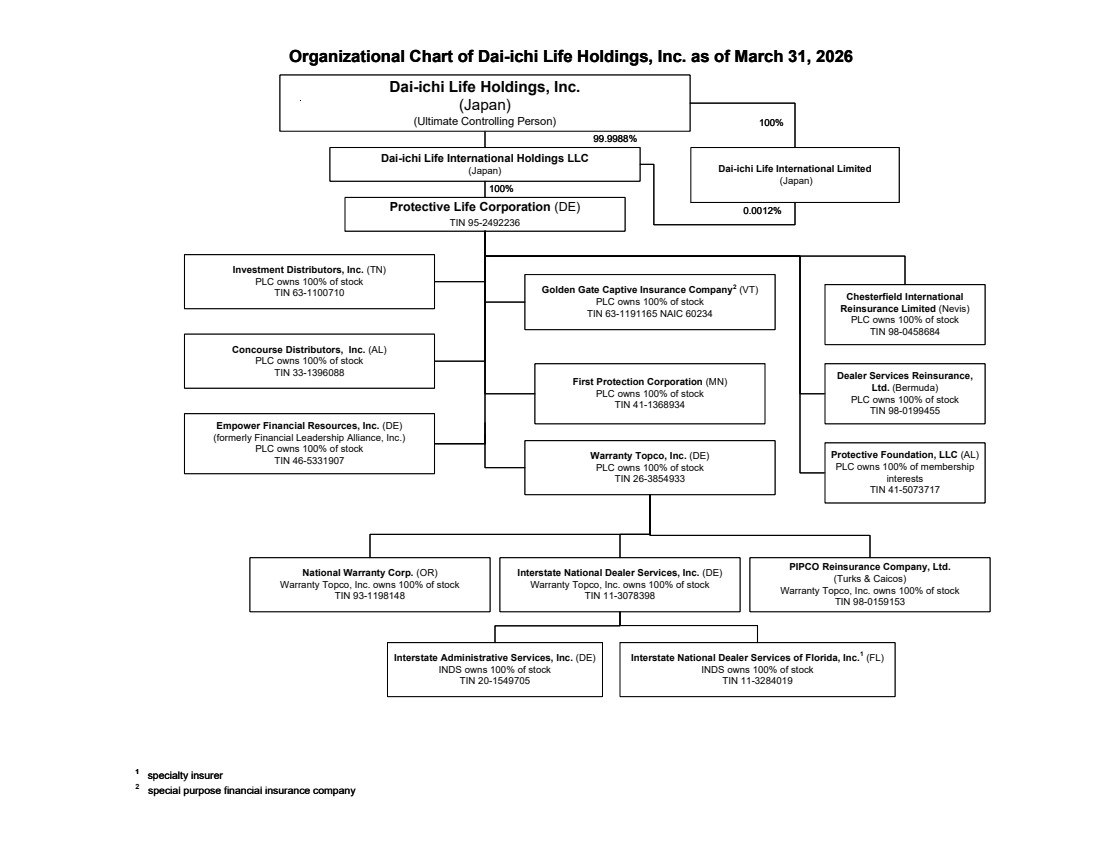

| Protective Life Corporation (DE) TIN 95-2492236 1 specialty insurer 2 special purpose financial insurance company Investment Distributors, Inc. (TN) PLC owns 100% of stock TIN 63-1100710 Warranty Topco, Inc. (DE) PLC owns 100% of stock TIN 26-3854933 Empower Financial Resources, Inc. (DE) (formerly Financial Leadership Alliance, Inc.) PLC owns 100% of stock TIN 46-5331907 Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 National Warranty Corp. (OR) Warranty Topco, Inc. owns 100% of stock TIN 93-1198148 Interstate National Dealer Services, Inc. (DE) Warranty Topco, Inc. owns 100% of stock TIN 11-3078398 PIPCO Reinsurance Company, Ltd. (Turks & Caicos) Warranty Topco, Inc. owns 100% of stock TIN 98-0159153 Interstate National Dealer Services of Florida, Inc.1 (FL) INDS owns 100% of stock TIN 11-3284019 Interstate Administrative Services, Inc. (DE) INDS owns 100% of stock TIN 20-1549705 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Golden Gate Captive Insurance Company2 (VT) PLC owns 100% of stock TIN 63-1191165 NAIC 60234 Concourse Distributors, Inc. (AL) PLC owns 100% of stock TIN 33-1396088 Chesterfield International Reinsurance Limited (Nevis) PLC owns 100% of stock TIN 98-0458684 Dealer Services Reinsurance, Ltd. (Bermuda) PLC owns 100% of stock TIN 98-0199455 First Protection Corporation (MN) PLC owns 100% of stock TIN 41-1368934 Dai-ichi Life International Limited (Japan) 100% 99.9988% 0.0012% 100% Protective Foundation, LLC (AL) PLC owns 100% of membership interests TIN 41-5073717 Protective Life Corporation (DE) TIN 95-2492236 1 specialty insurer 2 special purpose financial insurance company Investment Distributors, Inc. (TN) PLC owns 100% of stock TIN 63-1100710 Warranty Topco, Inc. (DE) PLC owns 100% of stock TIN 26-3854933 Empower Financial Resources, Inc. (DE) (formerly Financial Leadership Alliance, Inc.) PLC owns 100% of stock TIN 46-5331907 Organizational Chart of Dai-ichi Life Holdings, Inc. as of March 31, 2026 National Warranty Corp. (OR) Warranty Topco, Inc. owns 100% of stock TIN 93-1198148 Interstate National Dealer Services, Inc. (DE) Warranty Topco, Inc. owns 100% of stock TIN 11-3078398 PIPCO Reinsurance Company, Ltd. (Turks & Caicos) Warranty Topco, Inc. owns 100% of stock TIN 98-0159153 Interstate National Dealer Services of Florida, Inc.1 (FL) INDS owns 100% of stock TIN 11-3284019 Interstate Administrative Services, Inc. (DE) INDS owns 100% of stock TIN 20-1549705 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Golden Gate Captive Insurance Company2 (VT) PLC owns 100% of stock TIN 63-1191165 NAIC 60234 Concourse Distributors, Inc. (AL) PLC owns 100% of stock TIN 33-1396088 Chesterfield International Reinsurance Limited (Nevis) PLC owns 100% of stock TIN 98-0458684 Dealer Services Reinsurance, Ltd. (Bermuda) PLC owns 100% of stock TIN 98-0199455 First Protection Corporation (MN) PLC owns 100% of stock TIN 41-1368934 Dai-ichi Life International Limited (Japan) 100% 99.9988% 0.0012% 100% Protective Foundation, LLC (AL) PLC owns 100% of membership interests TIN 41-5073717 |

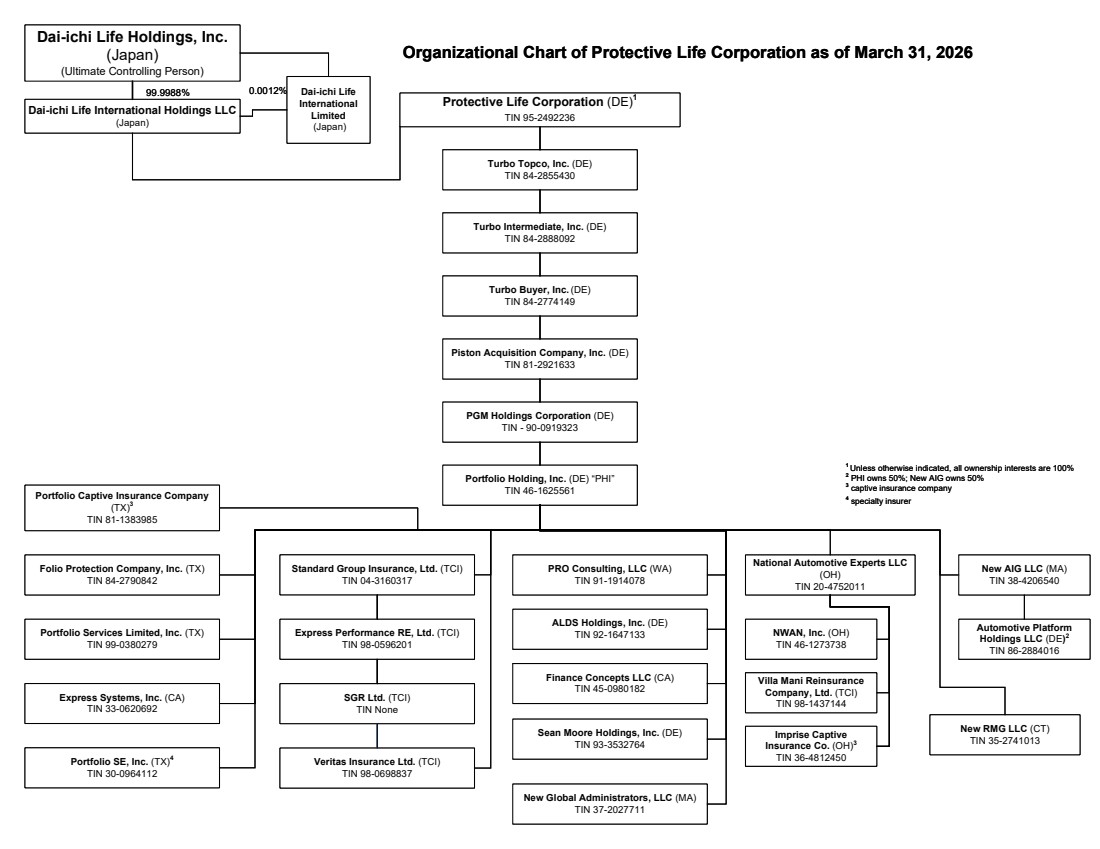

| Organizational Chart of Protective Life Corporation as of March 31, 2026 Protective Life Corporation (DE)1 TIN 95-2492236 Turbo Topco, Inc. (DE) TIN 84-2855430 Turbo Buyer, Inc. (DE) TIN 84-2774149 PGM Holdings Corporation (DE) TIN - 90-0919323 Piston Acquisition Company, Inc. (DE) TIN 81-2921633 Portfolio Holding, Inc. (DE) “PHI” TIN 46-1625561 Turbo Intermediate, Inc. (DE) TIN 84-2888092 Folio Protection Company, Inc. (TX) TIN 84-2790842 Portfolio Services Limited, Inc. (TX) TIN 99-0380279 Express Systems, Inc. (CA) TIN 33-0620692 Portfolio SE, Inc. (TX)4 TIN 30-0964112 Standard Group Insurance, Ltd. (TCI) TIN 04-3160317 Express Performance RE, Ltd. (TCI) TIN 98-0596201 SGR Ltd. (TCI) TIN None Portfolio Captive Insurance Company (TX)3 TIN 81-1383985 PRO Consulting, LLC (WA) TIN 91-1914078 National Automotive Experts LLC (OH) TIN 20-4752011 Veritas Insurance Ltd. (TCI) TIN 98-0698837 ALDS Holdings, Inc. (DE) TIN 92-1647133 Finance Concepts LLC (CA) TIN 45-0980182 Sean Moore Holdings, Inc. (DE) TIN 93-3532764 New Global Administrators, LLC (MA) TIN 37-2027711 New RMG LLC (CT) TIN 35-2741013 New AIG LLC (MA) TIN 38-4206540 NWAN, Inc. (OH) TIN 46-1273738 Villa Mani Reinsurance Company, Ltd. (TCI) TIN 98-1437144 Imprise Captive Insurance Co. (OH)3 TIN 36-4812450 Automotive Platform Holdings LLC (DE) 2 TIN 86-2884016 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Dai-ichi Life International Limited (Japan) 99.9988% 0.0012% 1 Unless otherwise indicated, all ownership interests are 100% 2 PHI owns 50%; New AIG owns 50% 3 captive insurance company 4 specialty insurer Organizational Chart of Protective Life Corporation as of March 31, 2026 Protective Life Corporation (DE)1 TIN 95-2492236 Turbo Topco, Inc. (DE) TIN 84-2855430 Turbo Buyer, Inc. (DE) TIN 84-2774149 PGM Holdings Corporation (DE) TIN - 90-0919323 Piston Acquisition Company, Inc. (DE) TIN 81-2921633 Portfolio Holding, Inc. (DE) “PHI” TIN 46-1625561 Turbo Intermediate, Inc. (DE) TIN 84-2888092 Folio Protection Company, Inc. (TX) TIN 84-2790842 Portfolio Services Limited, Inc. (TX) TIN 99-0380279 Express Systems, Inc. (CA) TIN 33-0620692 Portfolio SE, Inc. (TX)4 TIN 30-0964112 Standard Group Insurance, Ltd. (TCI) TIN 04-3160317 Express Performance RE, Ltd. (TCI) TIN 98-0596201 SGR Ltd. (TCI) TIN None Portfolio Captive Insurance Company (TX)3 TIN 81-1383985 PRO Consulting, LLC (WA) TIN 91-1914078 National Automotive Experts LLC (OH) TIN 20-4752011 Veritas Insurance Ltd. (TCI) TIN 98-0698837 ALDS Holdings, Inc. (DE) TIN 92-1647133 Finance Concepts LLC (CA) TIN 45-0980182 Sean Moore Holdings, Inc. (DE) TIN 93-3532764 New Global Administrators, LLC (MA) TIN 37-2027711 New RMG LLC (CT) TIN 35-2741013 New AIG LLC (MA) TIN 38-4206540 NWAN, Inc. (OH) TIN 46-1273738 Villa Mani Reinsurance Company, Ltd. (TCI) TIN 98-1437144 Imprise Captive Insurance Co. (OH)3 TIN 36-4812450 Automotive Platform Holdings LLC (DE) 2 TIN 86-2884016 Dai-ichi Life Holdings, Inc. (Japan) (Ultimate Controlling Person) Dai-ichi Life International Holdings LLC (Japan) Dai-ichi Life International Limited (Japan) 99.9988% 0.0012% 1 Unless otherwise indicated, all ownership interests are 100% 2 PHI owns 50%; New AIG owns 50% 3 captive insurance company 4 specialty insurer |