No. 811-21758

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE

SECURITIES ACT OF 1933

POST-EFFECTIVE AMENDMENT NO. 24

SECURITIES ACT OF 1933

POST-EFFECTIVE AMENDMENT NO. 24

and

REGISTRATION STATEMENT UNDER THE

INVESTMENT COMPANY ACT OF 1940

POST-EFFECTIVE AMENDMENT NO. 24

INVESTMENT COMPANY ACT OF 1940

POST-EFFECTIVE AMENDMENT NO. 24

CLIPPER FUNDS TRUST

2949 East Elvira Road, Suite 101

Tucson, Arizona 85756

(520) 806-7600

Tucson, Arizona 85756

(520) 806-7600

|

Agents For Service:

|

Lisa Cohen

Davis Selected Advisers, L.P.

2949 East Elvira Road, Suite 101

Tucson, AZ 85756

|

|

|

-or-

|

|

|

Richard Cutshall

Greenberg Traurig LLP

1144 15th Street

Suite 3300

Denver, CO 80202

|

|

It is proposed that this filing will become effective:

|

||

|

|

☐

|

Immediately upon filing pursuant to paragraph (b) of Rule 485

|

|

|

☒

|

On May 1, 2026, pursuant to paragraph (b) of Rule 485

|

|

|

☐

|

60 days after filing pursuant to paragraph (a) of Rule 485

|

|

|

☐

|

On [ ] pursuant to paragraph (a) of Rule 485

|

|

|

☐

|

75 days after filing pursuant to paragraph (a)(2) of Rule 485

|

|

|

☐

|

On [ ] pursuant to paragraph (a)(2) of Rule 485

|

|

|

☐

|

This post-effective amendment designates a new effective date for a previously filed

post-effective amendment

|

1

Title of Securities being Registered Common Stock of:

Clipper Fund

EXPLANATORY NOTE

This Post-Effective Amendment contains:

Clipper Fund Prospectus

Clipper Fund Statement of Additional Information

Part C

Signature Pages

Exhibits

Clipper Fund Statement of Additional Information

Part C

Signature Pages

Exhibits

2

Clipper Fund

May 1, 2026

Prospectus

A Portfolio of Clipper Funds Trust

Ticker: CFIMX

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Contents

| 3 | |

| 6 | |

| 9 | |

| 9 | |

| 11 | |

| 11 | |

| 11 | |

| 13 | |

| 13 | |

| 13 | |

| 14 | |

| 15 | |

| 16 | |

| 16 | |

| 16 | |

| 17 | |

| 17 | |

| 18 | |

| 20 | |

| 21 | |

| 21 | |

| 21 | |

| 21 | |

| 22 | |

| | |

This prospectus contains important information. Please read it carefully before investing and keep it for future reference.

No financial adviser, dealer, salesperson, or any other person has been authorized to give any information or to make any representations, other than those contained in this prospectus, in connection with the offer contained in this prospectus and, if given or made, such other information or representations must not be relied on as having been authorized by the Fund, the Fund’s investment adviser or the Fund’s distributor.

This prospectus does not constitute an offer by the Fund or by the Fund’s distributor to sell or a solicitation of an offer to buy any of the securities offered hereby in any jurisdiction to any person to whom it is unlawful for the Fund to make such an offer.

Prospectus | Clipper Fund | 2

Clipper Fund Summary

The Fund seeks long-term capital growth and capital preservation.

This table describes the fees and expenses that you may pay if you buy, hold, and

sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which

are not reflected in the tables and examples below.

|

Shareholder Fees

(fees paid directly from your investment)

|

|

|

Maximum Sales Charge (Load) Imposed on Purchases

(as a percentage of offering price)

|

|

|

Maximum Deferred Sales Charge (Load)

(as a percentage of the lesser of the net asset value of the shares redeemed or the

total cost of such shares)

|

|

|

Redemption Fee

(as a percentage of total redemption proceeds)

|

|

|

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

|

|

|

Management Fees

|

|

|

Distribution and/or Service (12b-1) Fees

|

|

|

Other Expenses

|

|

|

Total Annual Fund Operating Expenses

|

|

|

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

Clipper Fund

|

$ |

$ |

$ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 17 % of the average value of its portfolio.

Davis Selected Advisers, L.P. (“Davis Advisors” or the “Adviser”), the Fund’s investment adviser, uses the Davis Investment Discipline to invest the Fund’s portfolio principally in common stocks (including indirect holdings of common stock through Depositary Receipts (as defined below)) issued by large companies with market capitalizations

of at least $10 billion. The Fund is non-diversified and, therefore, is allowed to focus its investments in fewer

companies than a fund that is required to diversify its portfolio. The Fund’s portfolio generally contains between 15 and 35 companies, although the precise number of its investments will vary over time. Historically, the Fund has invested a significant

portion of its assets in financial services companies and in foreign companies, and may also invest in mid- and small-capitalization

companies.

Davis Investment Discipline. Davis Advisors manages equity funds using the Davis Investment Discipline. Davis

Advisors conducts extensive research to try to identify businesses that possess characteristics

that Davis Advisors believes foster the creation of long-term value, such as proven management, a durable franchise and business

model, and sustainable competitive advantages. Davis Advisors aims to invest in such businesses when they are trading

at discounts to their intrinsic worth. Davis Advisors emphasizes individual stock selection and believes that the ability to evaluate

management is critical. Davis Advisors routinely visits managers at their places of business in order to gain insight into

the relative value of different businesses. Such research, however rigorous, involves predictions and forecasts that are inherently

uncertain. After determining which companies Davis Advisors believes the Fund should own, Davis Advisors then turns its

analysis to determining the intrinsic value of those companies’ equity securities. Davis Advisors seeks companies whose equity securities can be purchased at a discount from Davis Advisors’ estimate of the company’s intrinsic value based upon fundamental analysis of cash flows, assets and liabilities, and other criteria that Davis Advisors deems to be material on a company-by-company basis. Davis Advisors’ goal is to invest in companies for the long term (ideally, five years or longer, although

this goal may not be met). Davis Advisors considers selling a company’s equity securities if the securities’ market price exceeds Davis Advisors’ estimates of intrinsic value, if the ratio of the risks and rewards of continuing to own the company’s equity securities is no longer attractive, to raise cash to purchase a more attractive investment opportunity, to satisfy net

redemptions, or for other purposes.

Prospectus | Clipper Fund | 3

Principal Risks of Investing in the Fund

The principal risks of investing in the Fund are:

Stock Market Risk. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices, including the possibility of sharp declines.

Common Stock Risk. Common stock represents an ownership position in a company. An adverse event may have a negative impact on a company and could result in a decline in the price of its common stock. Common stock is generally subordinate to an issuer’s other securities, including preferred, convertible, and debt securities.

Financial Services Risk. Risks of investing in the financial services sector include: (1) systemic risk: factors outside the control of a particular financial institution may adversely affect the ability of the financial institution to operate normally or may impair its financial condition; (2) regulatory actions: financial services companies may suffer setbacks if regulators change the rules under which they operate; (3) changes in interest rates: unstable and/or rising interest rates may have a disproportionate effect on companies in the financial services sector; (4) non-diversified loan portfolios: financial services companies may have concentrated portfolios that make them vulnerable to economic conditions that affect an industry; (5) credit: financial services companies may have exposure to investments or agreements that may lead to losses; and (6) competition: the financial services sector has become increasingly competitive.

Focused Portfolio Risk. Funds that invest in a limited number of companies may have more risk because changes in the value of a single security may have a more significant effect, either negative or positive, on the value of the Fund’s total portfolio.

Foreign Country Risk. Securities of foreign companies (including Depositary Receipts) may be subject to greater risk, as foreign economies may not be as strong or diversified, foreign political systems may not be as stable and foreign financial reporting standards may not be as rigorous as they are in the United States. There may also be less information publicly available regarding the non-U.S. issuers and their securities. These securities may be less liquid (and, in some cases, may be illiquid) and could be harder to value than more liquid securities.

Headline Risk. The Fund may invest in a company when the company becomes the center of controversy after receiving adverse media attention concerning its operations, long-term prospects, management, or for other reasons. While Davis Advisors researches companies subject to such contingencies, it cannot be correct every time, and the company’s stock may never recover or may become worthless.

Large-Capitalization Companies Risk. Companies with $10 billion or more in market capitalization are considered by the Adviser to be large-capitalization companies. Large-capitalization companies generally experience slower rates of growth in earnings per share than do mid- and small-capitalization companies.

Manager Risk. Poor security selection or focus on securities in a particular sector, category, or group of companies may cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective. Even if the Adviser implements the intended investment strategies, the implementation of the strategies may be unsuccessful in achieving the Fund’s investment objective.

Depositary Receipts Risk. Depositary Receipts, consisting of American Depositary Receipts, European Depositary Receipts, and Global Depositary Receipts, are certificates evidencing ownership of shares of a foreign issuer. Depositary Receipts are subject to many of the risks associated with investing directly in foreign securities. Depositary Receipts may trade at a discount, or a premium, to the underlying security and may be less liquid than the underlying securities listed on an exchange.

Fees and Expenses Risk. The Fund may not earn enough through income and capital appreciation to offset the operating expenses of the Fund. All mutual funds incur operating fees and expenses. Fees and expenses reduce the return that a shareholder may earn by investing in a fund, even when a fund has favorable performance. A low-return environment, or a bear market, increases the risk that a shareholder may lose money.

Foreign Currency Risk. The change in value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency. For example, when the Fund holds a security that is denominated in a foreign currency, a decline of that foreign currency against the U.S. dollar would generally cause the value of the Fund’s shares to decline.

Mid- and Small-Capitalization Companies Risk. Companies with less than $10 billion in market capitalization are considered by the Adviser to be mid- or small-capitalization companies. Mid- and small-capitalization companies typically have more limited product lines, markets, and financial resources than larger companies and their securities may trade less frequently and in more limited volume than those of larger, more mature companies.

An investment in the Fund is not a deposit of the bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Prospectus | Clipper Fund | 4

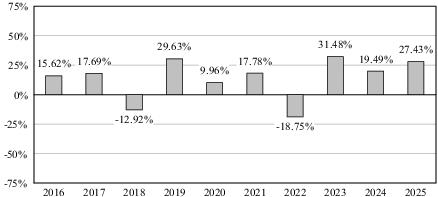

| | Returns | Period Ending |

| Quarter | | |

| Quarter | - | |

| | - | |

| Average Annual Total Returns (For the periods ended December 31, 2025) | Past 1 Year | Past 5 Years | Past 10 Years |

| Return before taxes | | | |

| Return after taxes on distributions | | | |

| Return after taxes on distributions and sale of Fund shares | | | |

| S&P 500 Index reflects no deduction for fees, expenses or taxes | | | |

Management

Investment Adviser. Davis Selected Advisers, L.P. serves as the Fund’s investment adviser.

Sub-Adviser. Davis Selected Advisers–NY, Inc., a wholly owned subsidiary of the Adviser, serves as the Fund’s sub-adviser.

Portfolio Managers. As of the date of this prospectus, the Portfolio Managers listed below are jointly

and primarily responsible for the day-to-day management of the Fund’s portfolio.

|

Portfolio Managers

|

Experience with this Fund

|

Primary Title with Investment Adviser or Sub-Adviser

|

|

Christopher Davis

|

Since January 2006

|

Chairman, Davis Selected Advisers, L.P.

|

|

Danton Goei

|

Since January 2014

|

Vice President, Davis Selected Advisers–NY, Inc.

|

Purchase and Sale of Fund Shares

|

Minimum Initial Investment

|

$2,500

|

|

Minimum Additional Investment

|

$25

|

You may sell (redeem) shares each day the New York Stock Exchange is open. Your transaction

may be placed through your dealer or financial adviser, by writing to Clipper Fund, P.O. Box 219167, Kansas City,

MO 64121-9167, telephoning 1-800-432-2504 or accessing the Fund’s website, www.clipperfund.com. Certain financial intermediaries may impose different restrictions than those shown above.

Tax Information

If the Fund earns income or realizes capital gains, it intends to make distributions

that may be taxed as ordinary income, qualified dividend income or capital gains by federal, state and local authorities.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the Fund through a broker-dealer or other financial intermediary (such

as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services.

These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson

to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Prospectus | Clipper Fund | 5

Additional Information About Investment Objective, Principal Strategies, and Principal Risks

This prospectus contains important information about investing in the Fund. Please

read this prospectus carefully before you make any investment decisions. Additional information regarding the Fund is available

at clipperfund.com/resources/regulatory-documents.

Investment Objective

Clipper Fund’s investment objective is long-term capital growth and capital preservation. The Fund’s investment objective is a fundamental policy, which means that it may not be changed by the Fund’s Board of Trustees without shareholder approval.

Principal Investment Strategies

The principal investment strategies and risks for the Fund are described in more detail

above and below. The prospectus and statement of additional information (“SAI”) contain a number of investment strategies and risks that may be important to consider even though they are not principal investment strategies or principal risks

for the Fund. The prospectus also contains disclosure that describes Davis Advisors’ process for determining when the Fund may pursue a non-principal investment strategy.

Davis Advisors uses the Davis Investment Discipline to invest Clipper Fund’s portfolio principally in common stocks (including indirect holdings of common stock through Depositary Receipts) issued by

large companies with market capitalizations of at least $10 billion. The Fund is non-diversified and, therefore,

is allowed to focus its investments in fewer companies than a fund that is required to diversify its portfolio. The Fund’s portfolio generally contains between 15 and 35 companies, although the precise number of its investments will vary over time. Historically,

the Fund has invested a significant portion of its assets in financial services companies and in foreign companies, and

may also invest in mid- and small-capitalization companies.

Principal Risks of Investing in the Fund

If you buy shares of the Fund, you may lose some or all of the money that you invest.

The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The likelihood of loss may be greater if you invest for a shorter period

of time. This section describes the principal risks (but not the only risks) that could cause the value of your investment

in the Fund to decline and which could prevent it from achieving its stated investment objective.

The principal risks of investing in the Fund, listed alphabetically, include:

Common Stock Risk. Common stock represents ownership positions in companies. The prices of common stock

fluctuate based on changes in the financial condition of their issuers and on market and economic

conditions. Events that have a negative impact on a business probably will be reflected in a decline in the price

of its common stock. Furthermore, when the total value of the stock market declines, most common stocks, even those issued by

strong companies, likely will decline in value. Common stock is generally subordinate to an issuer’s other securities, including preferred, convertible, and debt securities.

Depositary Receipts Risk. Securities of a foreign company may involve investing in Depositary Receipts, which

include American Depositary Receipts, European Depositary Receipts, and Global Depositary

Receipts, which are certificates evidencing ownership of shares of a foreign issuer. These certificates, which may

be sponsored or unsponsored, are issued by depositary banks and, generally, trade on an established market in the United States

or elsewhere. The underlying shares are held in trust by a custodian bank or similar financial institution in the issuer’s home country. The depositary bank may not have physical custody of the underlying securities at all times and may charge fees for

various services, including forwarding dividends, interest, and corporate actions. Depositary Receipts are alternatives to

directly purchasing the underlying foreign securities in their national markets and currencies. However, Depositary Receipts

continue to be subject to many of the risks associated with investing directly in foreign securities. These risks include foreign

exchange risk as well as the political and economic risks of the underlying issuer’s country. Depositary Receipts may trade at a discount or a premium to the underlying security and may be less liquid than the underlying securities listed on an exchange.

Fees and Expenses Risk. The Fund may not earn enough through income and capital appreciation to offset its

operating expenses. All mutual funds incur operating fees and expenses. Fees and expenses reduce

the return that a shareholder may earn by investing in a fund even when that fund has favorable performance. A low-return

environment, or a bear market, increases the risk that a shareholder may lose money.

Financial Services Risk. A company is “principally engaged” in financial services if it owns financial services related assets constituting at least 50% of the total value of its assets, or if at least 50% of

its revenues are derived from its provision of financial services. The financial services sector consists of several different industries

that behave differently in different economic and market environments, including banking, insurance, and securities brokerage

houses. Companies in the financial services sector include commercial banks, industrial banks, savings institutions,

finance companies, diversified financial services companies, investment banking firms, securities brokerage houses,

investment advisory companies, leasing

Prospectus | Clipper Fund | 6

companies, insurance companies, and companies providing similar services. Due to the

wide variety of companies in the financial services sector, they may react in different ways to changes in economic

and market conditions.

Risks of investing in the financial services sector include: (1) systemic risk: factors

outside the control of a particular financial institution — like the failure of another, significant financial institution or material disruptions to the credit markets — may adversely affect the ability of the financial institution to operate normally or may

impair its financial condition; (2) regulatory actions: financial services companies may suffer setbacks if regulators change the

rules under which they operate; (3) changes in interest rates: unstable and/or rising interest rates may have a disproportionate

effect on companies in the financial services sector; (4) non-diversified loan portfolios: financial services companies, whose securities

a fund purchases, may themselves have concentrated portfolios, such as a high level of loans to real estate developers,

which makes them vulnerable to economic conditions that affect that industry; (5) credit: financial services companies may

have exposure to investments or agreements, which, under certain circumstances, may lead to losses, e.g., sub-prime loans; and

(6) competition: the financial services sector has become increasingly competitive.

Banking. Commercial banks (including “money center” regional and community banks), savings and loan associations, and holding companies of the foregoing are especially subject to adverse effects of volatile

interest rates, concentrations of loans in particular industries or classifications (such as real estate, energy, or sub-prime

mortgages), and significant competition. The profitability of these businesses is to a significant degree dependent on the

availability and cost of capital funds. Economic conditions in the real estate market may have a particularly strong effect

on certain banks and savings associations. Commercial banks and savings associations are subject to extensive federal and, in

many instances, state regulation. Neither such extensive regulation nor the federal insurance of deposits ensures the solvency

or profitability of companies in this industry and there is no assurance against losses in securities issued by such companies.

Insurance. Insurance companies are particularly subject to government regulation and rate setting,

potential anti-trust and tax law changes, and industry-wide pricing and competition cycles. Property and casualty

insurance companies also may be affected by weather, terrorism, long-term climate changes, and other catastrophes.

Life and health insurance companies may be affected by mortality and morbidity rates, including the effects of epidemics.

Individual insurance companies may be exposed to reserve inadequacies, problems in investment portfolios (e.g., real estate or “junk” bond holdings), and failures of reinsurance carriers.

Other Financial Services Companies. Many of the investment considerations discussed in connection with banks and insurance companies also apply to other financial services companies. These companies

are subject to extensive regulation, rapid business changes and volatile performance dependent on the availability and

cost of capital, and prevailing interest rates and significant competition. General economic conditions significantly affect these

companies. Credit and other losses resulting from the financial difficulty of borrowers or other third parties have a

potentially adverse effect on companies in this industry. Investment banking, securities brokerage, and investment advisory companies

are particularly subject to government regulation and the risks inherent in securities trading and underwriting activities.

Other Regulatory Limitations. Regulations of the Securities and Exchange Commission (“SEC”) impose limits on: (1) investments in the securities of companies that derive more than 15% of their gross

revenues from the securities or investment management business (although there are exceptions, the Fund is prohibited from investing

more than 5% of its total assets in a single company that derives more than 15% of its gross revenues from the securities

or investment management business); and (2) investments in insurance companies. The Fund, generally, is prohibited from

owning more than 10% of the outstanding voting securities of an insurance company.

Focused Portfolio Risk. The Fund is non-diversified and, therefore, is allowed to focus its investments in

fewer companies than a fund that is required to diversify its portfolio. Davis Advisors believes that concentrating the Fund’s portfolio in a select, limited number of companies allows its best ideas to have a meaningful impact on the Fund’s performance. The Fund’s portfolio generally contains between 15 and 35 companies rather than hundreds of companies;

however, it may contain fewer than 15 companies or more than 35 companies if considered prudent and desirable by

Davis Advisors. Investors should be aware that a non-diversified portfolio may experience greater price volatility than

would a diversified portfolio.

Foreign Country Risk. Foreign companies may issue both equity and fixed income securities. A company may

be classified as either “domestic” or “foreign” depending upon which factors the Adviser considers most important for a given company. Factors that the Adviser considers in classifying a company as domestic or foreign

include: (1) whether the company is organized under the laws of the United States or a foreign country; (2) whether the company’s securities principally trade in securities markets outside of the United States; (3) the source of the majority of the company’s revenues or profits; and (4) the location of the majority of the company’s assets. The Adviser generally follows the country classification indicated by a third-party service provider but may use a different country classification if the Adviser’s analysis of the four factors provided above, or other factors that the Adviser deems relevant, indicate that a different

country classification is more appropriate. Foreign country risk can be more focused on factors concerning specific countries or geographic areas when the Fund’s holdings are more focused in these countries or geographic areas.

The Fund may invest a significant portion of its assets in securities issued by companies

operating, incorporated, or principally traded in foreign countries. Investing in foreign countries involves risks that may cause the Fund’s performance to be more volatile than it would be if the Fund invested solely in the United States. Foreign

economies may not be as strong or as diversified, foreign political systems may not be as stable and foreign financial

reporting standards may not be as rigorous as

Prospectus | Clipper Fund | 7

they are in the United States. In addition, foreign capital markets may not be as

well developed, so securities may be less liquid, transaction costs may be higher, and investments may be subject to more government

regulation. When the Fund invests in foreign securities, its operating expenses are likely to be higher than those of

an investment company investing exclusively in U.S. securities, since the custodial and certain other expenses associated with

foreign investments are expected to be higher.

Foreign Currency Risk. Securities issued by foreign companies in foreign markets are frequently denominated

in foreign currencies. The change in value of a foreign currency against the U.S. dollar will

result in a change in the U.S. dollar value of securities denominated in that foreign currency. For example, when the Fund holds

a security that is denominated in a foreign currency, a decline of that foreign currency against the U.S. dollar would generally cause the value of the Fund’s shares to decline. The Fund may, but generally does not, hedge its currency risk.

Headline Risk. Davis Advisors seeks to acquire companies with durable business models that can be

purchased at attractive valuations relative to what Davis Advisors believes to be the companies’ intrinsic values. Davis Advisors may make such investments when a company becomes the center of controversy after receiving adverse

media attention. The company may be involved in litigation, the company’s financial reports or corporate governance may be challenged, the company’s public filings may disclose a weakness in internal controls, greater government regulation

may be contemplated, or other adverse events may threaten the company’s future. While Davis Advisors researches companies subject to such contingencies, it cannot be correct every time and the company’s stock may never recover or may become worthless.

Large-Capitalization Companies Risk. Companies with $10 billion or more in market capitalization are considered by the

Adviser to be large-capitalization companies. Large-capitalization companies generally

experience slower rates of growth in earnings per share than do mid- and small-capitalization companies.

Manager Risk. Poor security selection or focus on securities in a particular sector, category,

or group of companies may cause the Fund to underperform relevant benchmarks or other funds with a similar investment

objective. Even if the Adviser implements the intended investment strategies, the implementation of the strategies

may be unsuccessful in achieving the Fund’s investment objective.

Mid- and Small-Capitalization Companies Risk. Companies with less than $10 billion in market capitalization are considered by the Adviser to be mid- or small-capitalization companies. Investing in mid- and

small-capitalization companies may be more risky than investing in large-capitalization companies. Smaller companies typically

have more limited product lines, markets, and financial resources than larger companies and their securities may trade

less frequently and in more limited volume than those of larger, more mature companies. Securities of these companies

may be subject to volatility in their prices. They may have a limited trading market, which may adversely affect the Fund’s ability to dispose of them and can reduce the price the Fund might be able to obtain for them. Other investors that own a security

issued by a mid- or small-capitalization company for whom there is limited liquidity might trade the security when the Fund

is attempting to dispose of its holdings in that security. In that case, the Fund might receive a lower price for its holdings

than otherwise might be obtained. Mid- and small-capitalization companies also may be unseasoned. These include companies that

have been in operation for less than three years, including the operations of any predecessors.

Stock Market Risk. Stock markets tend to move in cycles, with periods of rising prices and periods of

falling prices, including the possibility of sharp declines. As an example, U.S. and international markets have

experienced volatility in recent months and years due to a number of economic, political, and global macro factors including

the impact of the coronavirus (COVID-19) as a global pandemic, uncertainties regarding interest rates, rising inflation, trade

tensions, and the threat of tariffs and/or retaliatory tariffs imposed by the U.S. and other countries. While COVID-19 is no

longer a global pandemic as of 2023, the recovery from COVID-19 may last for a prolonged period of time. In addition, as a

result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European

Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions,

and have limited certain exports and imports to and from Russia. The war may continue to contribute to market volatility.

Further, the conflicts in the Middle East may lead to overall economic uncertainty and negative impacts on the global economy

and major financial markets. These developments as well as other events could result in further market volatility and

negatively affect financial asset prices, the liquidity of certain securities, and the normal operations of securities exchanges

and other markets. Continuing market volatility as a result of recent market conditions, U.S. political developments, or

other events may have an adverse effect on the performance of the Fund.

An investment in the Fund is not a deposit of the bank and is not insured or guaranteed

by the Federal Deposit Insurance Corporation or any other government agency.

Prospectus | Clipper Fund | 8

Additional Information About Expenses, Fees, and Performance

All Fund results in this prospectus reflect the reinvestment of dividends and capital

gain distributions, if any. Unless otherwise noted, Fund results reflect any fee waivers and/or expense reimbursements in effect

during the periods presented.

Information Concerning After-Tax Returns

As of the date of this prospectus, the tax rates are 37% for ordinary income, 20%

for qualified income, and 20% for long-term capital gains. An additional 3.8% tax imposed by the Affordable Care Act is included

on all investment income as part of the highest marginal rate used in all after-tax performance calculations.

Non-Principal Investment Strategies and Risks

Clipper Fund may implement investment strategies that are not principal investment strategies if, in the Adviser’s professional judgment, the strategies are appropriate. A strategy includes any policy, practice,

or technique used by the Fund to achieve its investment objective. Whether a particular strategy, including a strategy to invest

in a particular type of security, is a principal investment strategy depends on the strategy’s anticipated importance in achieving the Fund’s investment objective and how the strategy affects the Fund’s potential risks and returns. In determining what is a principal investment strategy, the Adviser considers, among other things, the amount of the Fund’s assets expected to be committed to the strategy, the amount of the Fund’s assets expected to be placed at risk by the strategy, and the likelihood of the Fund losing some or all of those assets from implementing the strategy. Non-principal investment strategies are generally

those investments that constitute less than 5% to 10% of the Fund’s assets, depending upon their potential impact on the investment performance of the Fund.

While the Adviser expects to pursue the Fund’s investment objective by implementing the principal investment strategies described in this prospectus, the Adviser may employ non-principal investment strategies or securities if, in Davis Advisors’ professional judgment, the securities, trading, or investment strategies are appropriate.

Factors that Davis Advisors considers in pursuing these other strategies include whether the strategy: (1) is likely to be consistent with shareholders’ reasonable expectations; (2) is likely to assist the Adviser in pursuing the Fund’s investment objective; (3) is consistent with the Fund’s investment objective; (4) will not cause the Fund to violate any of its fundamental

or non-fundamental investment restrictions; and (5) will not materially change the Fund’s risk profile from the risk profile that results from following the principal investment strategies as described in this prospectus and further explained in the

SAI, as amended from time to time.

Liquidity Risk Management. While it is not anticipated to be an issue, the Fund’s Portfolio is managed with the restrictions and requirements of the Liquidity Rule’s limitations in mind, by the implementation of a Liquidity Risk Management Program (the “LRMP”). The Adviser monitors the adequacy and effectiveness of the implementation of the LRMP on an ongoing basis. This monitoring includes a review of the Fund’s liquidity risk based on a variety of factors including the Fund’s: (1) investment strategy, (2) portfolio liquidity and cash flow projections during normal and reasonably

foreseeable stressed conditions, (3) shareholder redemptions, and (4) borrowing arrangements and other funding sources.

The Liquidity Rule places a 15% limit on the Fund’s illiquid investments and requires a fund that does not primarily hold assets that are highly liquid investments to determine and maintain a minimum percentage of that fund’s net assets in highly liquid investments (highly liquid investment minimum or HLIM). The LRMP includes provisions and safeguards that are reasonably

designed to comply with the 15% limit on illiquid investments and the Fund is currently classified as a fund that

primarily holds highly liquid investments. The LRMP includes the classification, no less than monthly, of the Clipper Fund’s investments into one of four liquidity classifications as provided for in the Liquidity Rule.

At a recent meeting of the Fund’s Board of Trustees, the Adviser provided a written report to the Board pertaining to the operation, adequacy, and effectiveness of implementation of the LRMP from April 1,

2024, through March 31, 2025. The report concluded that the LRMP is operating effectively and is reasonably designed to assess and manage the Fund’s liquidity risk. There can be no guarantee that the LRMP will achieve its objectives in the future.

ReFlow Liquidity Program. Clipper Fund may participate in the ReFlow Fund, LLC (“ReFlow”) liquidity program, which is designed to provide an alternative liquidity source for mutual funds experiencing

net redemptions of their shares. Pursuant to the program, ReFlow provides participating mutual funds with a source of cash to meet

net shareholder redemptions by standing ready each business day to purchase Fund shares up to the value of the net

shares redeemed by other shareholders that are expected to settle that business day. Following purchases of Fund shares, ReFlow

then generally redeems those shares when the Fund experiences net sales, at the end of a maximum holding period determined

by ReFlow (currently 8 days), or at other times at ReFlow’s or the Adviser’s discretion. While ReFlow holds Fund shares, it will have the same rights and privileges with respect to those shares as any other shareholder. In the event the

Fund uses the ReFlow service, the Fund will pay a fee to ReFlow each time ReFlow purchases Fund shares, calculated by applying

to the purchase amount a fee rate determined through an automated daily auction among participating mutual funds. The

current minimum fee rate is 0.14%, although the Fund may submit a bid at a higher rate if it determines that doing so

is in the best interest of Fund shareholders. ReFlow’s purchases of Fund shares through the liquidity program are made on an investment-blind basis without regard to the Fund’s objective, policies, or anticipated performance. In accordance with federal securities laws, ReFlow is prohibited from acquiring more than 3% of the outstanding voting securities of the Fund. ReFlow will

periodically redeem its entire share position in the Fund and may request that such redemption be met in-kind in accordance with the Fund’s policy on purchases and redemptions in-kind. The Board of Trustees has approved the Fund’s participation in the ReFlow program.

Prospectus | Clipper Fund | 9

The Adviser believes that participation in the ReFlow liquidity program may assist in stabilizing the Fund’s net assets, to the benefit of the Fund and its shareholders, although there is no guarantee that the program will do so. To the extent the Fund’s net assets do not decline, the Adviser typically will also benefit.

Repurchase Agreements. The Fund may enter into repurchase agreements. Repurchase agreements are transactions

in which the Fund purchases government securities and simultaneously commits to resell them

to the same counterparty at a future time and at a price reflecting a market rate of interest. Income from repurchase agreements

may not be exempt from state and local taxation. Repurchase agreements often offer a higher yield than investments directly

in government securities. The resale price reflects the purchase price plus an agreed-on incremental amount, which is unrelated

to the coupon rate or maturity of the purchased security. The repurchase obligation of the seller is, in effect, secured

by the underlying securities. In the event of a bankruptcy or other default of a seller of a repurchase agreement, the Fund could

experience both delays in liquidating the underlying securities and losses, including (1) possible decline in the value of the

collateral during the period, while the Fund seeks to enforce its rights thereto; (2) possible loss of all or a part of the income

during this period; and (3) expenses of enforcing its rights.

The Fund will enter into repurchase agreements only when the seller agrees that the

value of the underlying securities, including accrued interest (if any), will at all times be equal to or exceed the value

of the repurchase agreement. The Fund may enter into tri-party repurchase agreements in which a third-party custodian bank ensures

the timely and accurate exchange of cash and collateral. The majority of these transactions run from day-to-day and delivery

pursuant to the resale typically occurs within one to seven days of the purchase. The Fund normally will not enter into repurchase

agreements maturing in more than seven days.

Restricted and Illiquid Securities. The Fund may invest in restricted securities that are subject to contractual restrictions

on resale. The Fund is prohibited from purchasing or holding illiquid securities (which

may include restricted securities) if more than 15% of the Fund’s net assets would then be illiquid. If illiquid securities were to exceed 15% of the value of the Fund’s net assets, the Adviser would attempt to reduce the Fund’s investment in illiquid securities in an orderly fashion. Companies whose securities are not publicly traded may not be subject to the disclosure or other

investor protection requirements that would be applicable if their securities were publicly traded.

The restricted securities that the Fund may purchase include securities that have

not been registered under the Securities Act of 1933, as amended (the “1933 Act”), but are eligible for purchase and sale pursuant to Rule 144A (“Rule 144A Securities”). This Rule permits certain qualified institutional buyers, such as the Fund, to trade

in privately placed securities even though such securities are not registered under the 1933 Act. The Adviser, under criteria established by the Fund’s Board of Trustees, will consider whether Rule 144A Securities being purchased or held by the Fund are illiquid and thus subject to the Fund’s policy limiting investments in illiquid securities. In making this determination,

the Adviser will consider the frequency of trades and quotations, the number of dealers and potential purchasers, dealer undertakings

to make a market, and the nature of the security and the marketplace trades (for example, the time needed to dispose of

the security, the method of soliciting offers, and the mechanics of transfer). The liquidity of Rule 144A Securities also will be

monitored by the Adviser and if, as a result of changed conditions, it is determined that a Rule 144A Security is no longer liquid, the Fund’s holding of illiquid securities will be reviewed to determine what, if any, action is required in light of the policy

limiting investments in such securities. Investing in Rule 144A Securities could have the effect of increasing the amount of

investments in illiquid securities if qualified institutional buyers are unwilling to purchase such securities.

The Fund may also invest in securities of U.S. and non-U.S. issuers that are issued

through private offerings pursuant to Regulation S of the 1933 Act, as amended. Regulation S securities are subject to legal

or contractual restrictions on resale. These securities may be considered illiquid, as described above. Although Regulation

S securities may be resold in privately negotiated transactions, the price realized from these sales could be less than the

price paid by the Fund. Companies whose securities are not publicly traded may not be subject to the disclosure and other

investor protection requirements that would be applicable if their securities were publicly traded.

See the Fund’s SAI for additional information regarding restricted and illiquid securities.

Short-Term Investments. The Fund may use short-term investments, such as treasury bills and repurchase agreements,

to maintain flexibility while evaluating long-term opportunities.

Temporary Defensive Investments. The Fund may, but is not required to, use short-term investments for temporary defensive

purposes. In the event that Davis Advisors’ Portfolio Managers anticipate a decline in the values of the companies in which the Fund invests (due to economic, political, or other factors), the Fund may reduce

its risk by investing in short-term securities until market conditions improve. While the Fund is invested in short-term

investments, it will not be pursuing its stated investment objective. Unlike equity securities, these investments will not

appreciate in value when the market advances and will not contribute to long-term growth of capital.

For more details concerning current investments and market outlook, please see the Fund’s most recent shareholder report.

Prospectus | Clipper Fund | 10

Management and Organization

Davis Selected Advisers, L.P. (“Davis Advisors”) serves as the investment adviser for the Clipper Fund. Davis Advisors’ offices are located at 2949 East Elvira Road, Suite 101, Tucson, Arizona 85756. Davis

Advisors provides investment advice for Clipper Fund, manages its business affairs and provides day-to-day administrative

services. Davis Advisors also serves as investment adviser for other mutual funds, exchange-traded funds and institutional

and individual clients. For the fiscal year-ended December 31, 2025, Davis Advisors’ net management fee paid by the Fund for its services (based on average net assets) was 0.55%. A discussion regarding the basis for the approval of the Fund’s investment advisory and service agreement by the Fund’s Board of Trustees is contained in the Fund’s most recent semi-annual Form N-CSR financial statements.

Davis Selected Advisers–NY, Inc. serves as the sub-adviser for the Clipper Fund. Davis Selected Advisers–NY, Inc.’s offices are located at 620 Fifth Avenue, 3rd Floor, New York, New York 10020. Davis Selected Advisers–NY, Inc. provides investment management and research services for the Clipper Fund and other institutional clients,

and is a wholly owned subsidiary of Davis Advisors. Davis Selected Advisers–NY, Inc.’s fee is paid by Davis Advisors, not Clipper Fund.

Execution of Portfolio Transactions. Davis Advisors places orders with broker-dealers for the portfolio transactions of

Clipper Fund. Davis Advisors seeks to place portfolio transactions with brokers or

dealers who will execute transactions as efficiently as possible and at the most favorable net price. In placing executions

and paying brokerage commissions or dealer markups, Davis Advisors considers price, commission, timing, competent block trading

coverage, capital strength and stability, research resources, and other factors. Subject to best price and execution,

Davis Advisors may place orders for Clipper Fund’s portfolio transactions with broker-dealers who have sold shares of the Fund. However, when Davis Advisors places orders for the Fund’s portfolio transactions, it does not give any consideration to whether a broker-dealer has sold shares of the Fund. In placing orders for Clipper Fund’s portfolio transactions, the Adviser does not commit to any specific amount of business with any particular broker-dealer.

Over the last three fiscal years, the Fund paid the following brokerage commissions:

|

Fiscal Year-Ended December 31,

|

2025

|

2024

|

2023

|

|

Brokerage commissions paid

|

$133,732

|

$188,439

|

$82,564

|

|

Brokerage as a percentage of average net assets

|

0.01%

|

0.02%

|

0.01%

|

Portfolio Managers

◼

Christopher Davis has served as a Portfolio Manager of Clipper Fund since January 2006 and also manages

other equity funds advised by Davis Advisors. Mr. Davis has served as an analyst and Portfolio

Manager for Davis Advisors since September 1989.

◼

Danton Goei has served as a Portfolio Manager of Clipper Fund since January 2014 and also manages

other equity funds advised by Davis Advisors. Mr. Goei started with Davis Advisors as a research analyst

in November 1998.

The Portfolio Managers listed above are jointly and primarily responsible for the day-to-day management of the Fund’s portfolio. A limited portion of the Fund’s assets may be managed by Davis Advisors’ research analysts, subject to review by the Fund’s Portfolio Managers.

The SAI provides additional information about the Portfolio Managers’ compensation, other accounts managed by the Portfolio Managers and the Portfolio Managers’ investments in the Fund.

Certain Portfolio Managers may serve on the board(s) of public companies where they,

from time to time, may have access to material, non-public information (“MNPI”). Davis Advisors has instituted policies and procedures to ensure that these Portfolio Managers will not be able to utilize MNPI for their own benefit or for any

of the accounts they manage.

Shareholder Information

Procedures and Shareholder Rights Are Described by Current Prospectus and Other Disclosure

Documents

Investors should look to the most recent prospectus and SAI, as amended or supplemented

from time to time, for information concerning the Fund, including information on how to purchase and redeem Fund shares

and how to contact the Fund. The most recent prospectus and SAI (including any supplements or amendments thereto) will

be on file with the Securities and Exchange Commission as part of the Fund’s registration statement. Please also see the back cover of this prospectus for information on other ways to obtain information about the Fund.

How Your Shares Are Valued

Once you open your Clipper Fund account, you may purchase or sell shares at the net asset value (“NAV”) next determined after Clipper Fund’s transfer agent or other “qualified financial intermediary” (a financial institution that has entered into a contract with Davis Advisors or its affiliates to offer, sell and redeem shares of

the Fund) receives your request to purchase or sell shares in “good order.” A request is in good order when all documents which are required to constitute a legal purchase or sale of shares have been received by Clipper Fund’s transfer agent or other qualified financial intermediary (as defined above).

Prospectus | Clipper Fund | 11

The documents required to achieve good order vary depending upon a number of factors

(are shares held in a joint account or a corporate account, has the account had a recent address change, etc.). Contact your

financial adviser or Clipper Fund if you have questions about what documents will be required.

If your purchase or sale order is received in good order prior to the close of trading

on the New York Stock Exchange (“NYSE”), your transaction will be executed that day at that day’s NAV. If your purchase or sale order is received in good order after the close of the NYSE, your transaction will be processed the next business day at that next day’s NAV. Clipper Fund calculates the NAV of the shares issued by the Fund as of the close of trading on

the NYSE, normally 4:00 p.m., Eastern time, on each day when the NYSE is open. NYSE holidays currently include New Year’s Day, Martin Luther King, Jr. Day, Washington’s Birthday, Good Friday, Memorial Day, Juneteenth National Independence Day, Independence Day, Labor Day, Thanksgiving Day, and Christmas Day.

The NAV of the shares is determined by taking the value of the class of shares’ total assets, subtracting the class of shares’ liabilities and then dividing the result (net assets) by the number of outstanding

shares. Since the Fund invests in securities that may trade in foreign markets on days other than when Clipper Fund calculates its NAV, the value of the Fund’s portfolio may change on days that shareholders will not be able to purchase or redeem shares in

the Fund.

If you have access to the Internet, you can also check the NAV on the Fund’s website, www.clipperfund.com.

Valuation of Portfolio Securities

The Board of Trustees of the Clipper Fund has delegated the determination of fair

value of securities to Davis Selected Advisers, L.P. The Adviser has implemented policies and procedures that govern the

pricing of securities for the Clipper Fund, as discussed below.

The Adviser values securities for which market quotations are readily available at

current value. Short-term investments purchased within 60 days to maturity and of sufficient credit quality are valued at

amortized cost, which approximates fair value. Securities listed on the NYSE, NASDAQ, and other national exchanges are valued

at the last reported sales price on the day of valuation. Listed securities for which no sale was reported on that date are

valued at the last quoted bid price. Securities traded on foreign exchanges are valued based upon the last sales price on the principal

exchange on which the security is traded prior to the time when the Fund’s assets are valued.

Securities, including illiquid or restricted securities, for which market quotations

are not readily available are valued at their fair value. Securities whose values have been materially affected by a significant event occurring before the Fund’s assets are valued but after the close of their respective exchanges will be fair valued. Fair

value is determined in good faith using consistently applied procedures. Fair valuation is based on subjective factors and,

as a result, the fair value price of a security may differ from the security’s market price and may not be the price at which the security may be sold. Fair valuation could result in a different NAV than an NAV determined by using market quotations. The Board

of Trustees reviews and discusses with management a summary of fair valued securities in quarterly board meetings.

In general, foreign securities are more likely to require a fair value determination

than domestic securities because circumstances may arise between the close of the market on which the securities trade

and the time when the Fund values its portfolio securities, which may affect the value of such securities. Securities denominated

in foreign currencies and traded in foreign markets will have their values converted into U.S. dollar equivalents at the

prevailing exchange rates as computed by State Street Bank and Trust Company. Fluctuation in the values of foreign currencies

in relation to the U.S. dollar may affect the net asset value of the Fund’s shares even if there has not been any change in the foreign currency prices of the Fund’s investments.

Securities of smaller companies are also generally more likely to require a fair value

determination because they may be thinly traded and less liquid than traditional securities of larger companies.

The Fund may occasionally be entitled to receive award proceeds from litigation relating

to an investment security. The Fund generally does not recognize a gain on contingencies until such payment is certain,

which in most cases is when it receives payment.

To the extent that the Fund’s portfolio investments trade in markets on days when the Fund is not open for business, the Fund’s NAV may vary on those days. In addition, trading in certain portfolio investments

may not occur on days the Fund is open for business because markets or exchanges other than the NYSE may be closed. If the exchange or market on which the Fund’s underlying investments are primarily traded closes early, the NAV may be calculated

prior to its normal market calculation time. For example, the primary trading markets for the Fund may close early on the

day before certain holidays and the day after Thanksgiving.

Fixed income securities may be valued at prices supplied by the Clipper Fund’s pricing agent based on broker or dealer supplied valuations or matrix pricing, a method of valuing securities by reference

to the value of other securities with similar characteristics, such as rating, interest rate and maturity. Government bonds, corporate

bonds, asset-backed bonds, convertible securities, and high-yield or junk bonds are normally valued on the basis of prices

provided by independent pricing services. Prices provided by the pricing services may be determined without exclusive reliance

on quoted prices and may reflect appropriate factors such as institutional trading in similar groups of securities,

developments related to special securities, dividend rate, maturity, and other market data. Prices for fixed income securities

received from pricing services sometimes

Prospectus | Clipper Fund | 12

represent best estimates. In addition, if the prices provided by the pricing service

and independent quoted prices are unreliable, the Adviser will arrive at its own fair valuation using its fair value procedures.

Portfolio Holdings

A description of Clipper Fund’s policies and procedures with respect to the disclosure of the Fund’s portfolio holdings is available in the SAI.

The Fund’s complete schedules of investments are filed with the SEC on Form N-CSR (as of the end of the second and fourth quarters) and on Form N-PORT Part F (as of the end of the first and third quarters). The Fund’s Forms N-CSR (Annual and Semi-Annual Reports) and N-PORT Part F are available, without charge, upon request,

by calling 1-800-432-2504, on the Clipper Fund’s website at clipperfund.com/resources/regulatory-documents, and on the SEC’s website at www.sec.gov. Lists of the Fund’s month-end and quarter-end holdings are also available at www.clipperfund.com. They become available on or about the 10th day following each respective time period and remain available on the website until

the list is updated for the subsequent period.

How Clipper Fund Pays Earnings

There are two ways you can receive payments from Clipper Fund:

◼

Dividends. Dividends are distributions to shareholders of net investment income and short-term

capital gains on investments.

◼

Capital Gains. Capital gains are profits received by the Fund from the sale of securities held for

the long term, which are then distributed to shareholders.

If you would like information about when Clipper Fund pays dividends and distributes

capital gains, please call 1-800-432-2504. Unless you choose otherwise, the Clipper Fund will automatically reinvest your dividends

and capital gains in additional Fund shares.

You can request to have your dividends and capital gains paid to you by check or deposited

directly into your bank account. Dividends and capital gains of $50 or less will not be sent by check but will be reinvested

in additional Fund shares.

You will receive a statement each year detailing the amount of all dividends and capital

gains paid to you during the previous year. To ensure that these distributions are reported properly to the U.S. Treasury,

you must certify on your Clipper Fund Application Form, or on IRS Form W-9, that your Taxpayer Identification Number is

correct and you are not subject to backup withholding. If you are subject to backup withholding, or if you did not certify your

Taxpayer Identification Number, the IRS requires Clipper Fund to withhold a percentage of any dividends paid and redemption

proceeds received.

Dividends and Distributions

◼

Clipper Fund ordinarily distributes its dividends and capital gains, if any, in June

and December.

◼

When a dividend or capital gain is distributed, the net asset value per share is reduced

by the amount of the payment.

◼

You may elect to reinvest dividend and/or capital gain distributions to purchase additional

shares of Clipper Fund or you may elect to receive them in cash. Many shareholders do not elect to take capital

gain distributions in cash because these distributions reduce principal value.

◼

If a dividend or capital gain distribution is for an amount less than $50, the Fund

will not issue a check. Instead, the dividend or capital gain distribution will be automatically reinvested in additional

shares of the Fund.

◼

If a dividend or capital gain distribution check remains uncashed for four months

or is undeliverable by the United States Postal Service, the Fund may reinvest the dividend or capital gain distribution in

additional shares of the Fund, promptly after making this determination, and future dividends and capital gains distributions

will be automatically reinvested in additional shares of the Fund.

Federal Income Taxes

The following discussion is very general. Because each shareholder’s circumstances are different and special tax rules may apply, you should consult your tax adviser about your investment in the Fund.

Prospectus | Clipper Fund | 13

You will generally have to pay federal income taxes, as well as any other state and

local taxes, on any distributions which may be received from the Fund. If you sell Fund shares it is generally considered a taxable

event. The following table summarizes the tax status to you of certain transactions related to the Fund:

|

Transaction

|

Federal Tax Status

|

|

Redemption of shares

|

Usually capital gain or loss; long-term, only if shares owned more than

one year

|

|

Distributions of net capital gain

(excess of net long-term capital gain over net short-term

capital loss)

|

Long-term capital gain

|

|

Ordinary dividends

(including distributions of net short-term capital gain)

|

Ordinary income; certain dividends potentially taxable at long-term

capital gain rates

|

Distributions of net capital gain are taxable to you as long-term capital gains regardless

of how long you have owned your shares. Certain dividends may be treated as “qualified dividend income,” which for noncorporate shareholders is taxed at reduced rates. “Qualified dividend income” generally is income derived from dividends paid by U.S. corporations or certain foreign corporations that are either incorporated in a U.S. possession or eligible

for tax benefits under certain U.S. income tax treaties. In addition, dividends received from foreign corporations may be treated

as qualified dividend income if the stock with respect to which the dividends are paid is readily tradable on an established

U.S. securities market. A portion of the dividends received from the Fund (but none of the Fund’s capital gain distributions) may qualify for the dividends-received deduction for corporate shareholders.

You may want to avoid buying shares when the Fund is about to declare a dividend or

distribution, because it will be taxable to you even though it may effectively be a return of a portion of your investment. Similarly,

shareholders that are investing through a taxable account should consider the embedded gains or losses of the Fund.

For example, a new shareholder could be subject to taxes on a distribution it receives from the Fund that was earned when

it was not a shareholder. It is important to note that investors are only taxed on their own economic income over the life of the

investment. The embedded gains or losses for the Fund are disclosed in the most recent Annual and Semi-Annual Financial Statements

and Other Information.

The Fund’s dividends and other distributions are generally treated as received by shareholders when they are paid. However, if any dividend or distribution is declared by the Fund in October, November or December

of any calendar year and payable to shareholders of record on a specified date in such a month but is actually paid during

the following January, such dividend or distribution will be treated as received by each shareholder on December 31 of the

year in which it was declared.

After the end of the year, the Fund will provide you with information about the distributions

and dividends you received and any redemption of shares during the previous year. If you are neither a citizen nor

a resident of the United States, certain dividends that you receive from the Fund may be subject to federal withholding tax. To the extent that the Fund’s distributions consist of ordinary dividends or other payments that are subject to withholding, the

Fund will withhold federal income tax at the rate of 30% (or such lower rate as may be determined in accordance with any applicable

treaty). Dividends that are reported by the Fund as “interest-related dividends” or “short-term capital gain dividends” are generally exempt from such withholding for taxable years of the Fund beginning before January 1, 2014.

If you do not provide the Fund with your correct taxpayer identification number and

any required certifications, you will be subject to backup withholding on your redemption proceeds, dividends, and other distributions.

The backup withholding rate is currently 28%. Backup withholding will not, however, be applied to payments that

have been subject to the 30% withholding tax on shareholders who are neither citizens nor residents of the United

States.

Fees and Expenses of the Fund

The Fund must pay operating fees and expenses.

Management Fee

The management fee covers the normal expenses of managing the Fund, including compensation,

research costs, corporate overhead and related expenses.

12b-1 Fees

Clipper Fund does not charge any Rule 12b-1 distribution fees.

Other Expenses

Other expenses include miscellaneous fees from affiliated and outside service providers.

These fees may include legal, audit, custodial fees, the costs of printing and mailing of reports and statements, automatic

reinvestment of distributions and other conveniences, and payments to third parties that provide recordkeeping services or

administrative services for investors in the Fund.

Prospectus | Clipper Fund | 14

Total Fund Operating Expenses

The total cost of operating a mutual fund is reflected in its expense ratio. A shareholder

does not pay operating costs directly. Instead, operating costs are deducted before the Fund’s NAV is calculated and are expressed as a percentage of the Fund’s average daily net assets. The effect of these expenses is reflected in the performance

results for the Fund. Investors should examine total operating expenses closely in the prospectus, especially when comparing

one fund with another fund in the same investment category.

Fees Paid to Dealers and Other Financial Intermediaries

Broker-dealers and other financial intermediaries (“Qualifying Dealers”) may charge Davis Distributors, LLC (the “Distributor”) or the Adviser substantial fees for selling Clipper Fund’s shares and providing continuing support to shareholders. The fees charged by Qualifying Dealers may include, but are not limited

to: (1) recordkeeping fees from the Fund for providing recordkeeping services to investors who hold Clipper Fund shares

through dealer-controlled omnibus accounts; and (2) other fees, described below, paid by Davis Advisors or the Distributor

from their own resources.

Qualifying Dealers may, as a condition to distributing shares of Clipper Fund, request

that the Distributor, or the Adviser, pay or reimburse the Qualifying dealer for: (1) marketing support payments, including

business planning assistance, client servicing and data analytics, educating personnel about Clipper Fund and shareholder

financial planning needs, placement on the Qualifying dealer’s list of offered funds, and access to sales meetings, sales representatives and management representatives of the Qualifying dealer; and (2) financial assistance charged to

allow the Distributor to participate in and/or present at conferences or seminars, sales or training programs for invited registered

representatives and other employees, client and investor events, and other dealer-sponsored events. These additional fees are sometimes referred to as “revenue sharing” payments. A number of factors are considered in determining fees paid to Qualifying Dealers, including the dealer’s sales and assets and the quality of the dealer’s relationship with the Distributor. Fees are generally based on the value of shares of the Fund held by the Qualifying dealer or financial institution for its customers or based

on sales of Fund shares by the dealer or financial institution, or a combination thereof. In some cases, the charges or fees

may be a negotiated lump sum payment. Davis Advisors may use its profits from the advisory fee it receives from the Fund

to pay some or all of these fees. Some Qualifying Dealers may also choose to pay additional compensation to their registered

representatives who sell the Fund. Such payments may be associated with the status of the Fund on a Qualifying dealer’s preferred list of funds or otherwise associated with the Qualifying dealer’s marketing and other support activities. The foregoing arrangements may create an incentive for the Qualifying Dealers, brokers, or other financial institutions, as well as their

registered representatives, to sell Clipper Fund rather than other funds.

In 2025, the Distributor, or the Adviser, was charged additional fees by the Qualifying

Dealers listed below. The Distributor or the Adviser paid these fees from its own resources. These Qualifying Dealers may provide

Clipper Fund enhanced sales and marketing support and financial advisers employed by the Qualifying Dealers may recommend

Clipper Fund rather than other funds. Qualifying Dealers may be added or deleted at any time.

BMO Harris (fka Marshall & Ilsley Trust Company); Charles Schwab & Co., Inc.; Edward

D Jones; Fidelity Brokerage Services, LLC; LPL Financial; Matrix Settlement; Merrill Lynch; Mid-Atlantic Capital;

Morgan Stanley Smith Barney; Pershing, LLC; Raymond James & Associates, Inc.; RBC Capital Markets Corp.; Vanguard

Marketing Corporation; and Wells Fargo Advisors, LLC.

In addition, the Distributor may, from time-to-time, pay additional cash compensation

or other promotional incentives to authorized dealers or agents who sell shares of Clipper Fund. In some instances, such

cash compensation or other incentives may be offered only to certain dealers or agents who employ registered representatives

who have sold or may sell significant amounts of shares of Clipper Fund during specified periods of time.

Although Clipper Fund may use brokers who sell shares of the Fund to execute portfolio

transactions, the Fund does not consider the sale of Fund shares as a factor when selecting brokers to execute portfolio

transactions.

Investors should consult their financial intermediaries regarding the details of payments

they may receive in connection with the sale of Fund shares.

Due Diligence Meetings. The Distributor routinely sponsors due diligence meetings for registered representatives,

during which they receive updates on Clipper Fund and are afforded the opportunity to speak with the Fund’s Portfolio Managers. Invitation to these meetings is not conditioned on selling a specific number of shares.

Those who have shown an interest in Clipper Fund, however, are more likely to be considered. To the extent permitted by their firm’s policies and procedures, registered representatives’ expenses in attending these meetings may be covered by the Distributor.

Seminars and Educational Meetings. The Distributor may defray certain expenses of Qualifying Dealers incurred in connection with seminars and other educational efforts subject to the Distributor’s policies and procedures governing payments for such seminars. The Distributor may share expenses with Qualifying Dealers

for costs incurred in conducting training and educational meetings about various aspects of the Clipper Fund for the

employees of Qualifying Dealers. In addition, the Distributor may share expenses with Qualifying Dealers for costs incurred

in hosting client seminars at which the Fund is discussed.

Prospectus | Clipper Fund | 15

Recordkeeping Fees. Certain Qualifying Dealers have chosen to maintain “omnibus accounts” with Clipper Fund. In an omnibus account, the Fund maintains a single account in the name of the Qualifying

dealer and the dealer maintains all of its clients’ individual shareholder accounts. Likewise, for many retirement plans, a third-party administrator may open an omnibus account with Clipper Fund and the administrator will then maintain all of

the participant accounts. Davis Advisors, on behalf of the Fund, enters into agreements whereby the Fund is charged by the Qualifying

dealer or administrator for such recordkeeping services.

Recordkeeping services typically include: (1) establishing and maintaining shareholder

accounts and records; (2) recording shareholder account balances and changes thereto; (3) arranging for the wiring of

funds; (4) providing statements to shareholders; (5) furnishing proxy materials, periodic Clipper Fund reports, prospectuses,

and other communications to shareholders as required; (6) transmitting shareholder transaction information; and

(7) providing information in order to assist the Clipper Fund in its compliance with state securities laws. Clipper Fund, typically,

would be paying these shareholder servicing fees directly if a Qualifying dealer did not hold all customer accounts

in a single omnibus account with Clipper Fund.

Other Compensation. The Distributor may, from its own resources and not from the Fund’s, pay additional fees to the extent not prohibited by state or federal laws, the Securities and Exchange Commission (SEC),

or any self-regulatory agency such as the Financial Industry Regulatory Authority (FINRA).

How to Open an Account

To open an account with Clipper Fund you must initially invest at least $2,500 in

a regular or IRA account.

At the Distributor’s discretion, the minimum may be waived for an account established under a “wrap account” or other fee-based program that is sponsored and maintained by a registered broker-dealer approved by

the Distributor. The Distributor reserves the right, at its discretion and without notice, to modify, waive, or increase