485BPOS

2026-04-29

false

0001364924

N-1A

Fidelity Rutland Square Trust II

00013649242026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:MultipleSubAdviserRiskMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:InvestingInOtherFundsMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:StockMarketVolatilityMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:ForeignExposureMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:GeographicExposureMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:GeographicExposureToEuropeMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:IndustryExposureMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:IssuerSpecificChangesMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:InvestingInEtfsMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:QuantitativeInvestingMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberoef:RiskNotInsuredDepositoryInstitutionMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberoef:RiskLoseMoneyMember2026-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2016-01-012016-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2017-01-012017-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2018-01-012018-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2019-01-012019-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2020-01-012020-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2021-01-012021-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2022-01-012022-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2023-01-012023-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2024-01-012024-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2025-01-012025-12-310001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2025-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2021-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Member2016-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsMember2025-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsMember2021-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsMember2016-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsAndSalesMember2025-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsAndSalesMember2021-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:C000089634Memberoef:AfterTaxesOnDistributionsAndSalesMember2016-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:IndexMS001Member2025-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:IndexMS001Member2021-04-292026-04-290001364924fmr:S000029152Memberfmr:StrategicAdvisersInternationalFund-PROMemberfmr:IndexMS001Member2016-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:MultipleSubAdviserRiskMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:InvestingInOtherFundsMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:StockMarketVolatilityMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:InterestRateChangesMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:ForeignExposureMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndustryExposureMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:PrepaymentMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IssuerSpecificChangesMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:LeverageRiskMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:InvestingInEtfsMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberoef:RiskNotInsuredDepositoryInstitutionMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberoef:RiskLoseMoneyMember2026-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2016-01-012016-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2017-01-012017-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2018-01-012018-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2019-01-012019-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2020-01-012020-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2021-01-012021-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2022-01-012022-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2023-01-012023-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2024-01-012024-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2025-01-012025-12-310001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2025-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2021-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Member2016-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsMember2025-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsMember2021-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsMember2016-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsAndSalesMember2025-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsAndSalesMember2021-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:C000089633Memberoef:AfterTaxesOnDistributionsAndSalesMember2016-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexML038Member2025-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexML038Member2021-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexML038Member2016-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexLB091Member2025-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexLB091Member2021-04-292026-04-290001364924fmr:S000029151Memberfmr:StrategicAdvisersIncomeOpportunitiesFund-PROMemberfmr:IndexLB091Member2016-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:MultipleSubAdviserRiskMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:InvestingInOtherFundsMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:StockMarketVolatilityMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:ForeignExposureMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:GeographicExposureMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:GeographicExposureToEuropeMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:GeographicExposureToJapanMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:IndustryExposureMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:IssuerSpecificChangesMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:InvestingInEtfsMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:QuantitativeInvestingMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberoef:RiskNotInsuredDepositoryInstitutionMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberoef:RiskLoseMoneyMember2026-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2016-01-012016-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2017-01-012017-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2018-01-012018-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2019-01-012019-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2020-01-012020-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2021-01-012021-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2022-01-012022-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2023-01-012023-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2024-01-012024-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2025-01-012025-12-310001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2025-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2021-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Member2016-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsMember2025-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsMember2021-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsMember2016-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsAndSalesMember2025-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsAndSalesMember2021-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:C000089635Memberoef:AfterTaxesOnDistributionsAndSalesMember2016-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:IndexMS001Member2025-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:IndexMS001Member2021-04-292026-04-290001364924fmr:S000029153Memberfmr:StrategicAdvisersFidelityInternationalFund-PROMemberfmr:IndexMS001Member2016-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:MultipleSubAdviserRiskMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:InvestingInOtherFundsMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:StockMarketVolatilityMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:ForeignAndEmergingMarketsRiskMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:GeographicExposureMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:GeographicExposureToAsiaMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:GeographicExposureToTheChinaRegionMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:IndustryExposureMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:IssuerSpecificChangesMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:InvestingInEtfsAndClosedEndFundsMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:QuantitativeInvestingMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberoef:RiskNotInsuredDepositoryInstitutionMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberoef:RiskLoseMoneyMember2026-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2016-01-012016-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2017-01-012017-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2018-01-012018-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2019-01-012019-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2020-01-012020-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2021-01-012021-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2022-01-012022-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2023-01-012023-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2024-01-012024-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2025-01-012025-12-310001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2025-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2021-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Member2016-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsMember2025-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsMember2021-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsMember2016-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsAndSalesMember2025-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsAndSalesMember2021-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:C000092425Memberoef:AfterTaxesOnDistributionsAndSalesMember2016-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:IndexMC041Member2025-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:IndexMC041Member2021-04-292026-04-290001364924fmr:S000030092Memberfmr:StrategicAdvisersEmergingMarketsFund-PROMemberfmr:IndexMC041Member2016-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:MultipleSubAdviserRiskMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:InvestingInOtherFundsMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:InterestRateChangesMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:ForeignExposureMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:IndustryExposureMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:PrepaymentMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:IssuerSpecificChangesMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:LeverageRiskMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:InvestingInEtfsMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:QuantitativeInvestingMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:HighPortfolioTurnoverMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberoef:RiskNotInsuredDepositoryInstitutionMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberoef:RiskLoseMoneyMember2026-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2016-01-012016-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2017-01-012017-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2018-01-012018-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2019-01-012019-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2020-01-012020-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2021-01-012021-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2022-01-012022-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2023-01-012023-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2024-01-012024-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2025-01-012025-12-310001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2025-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2021-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Member2016-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsMember2025-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsMember2021-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsMember2016-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsAndSalesMember2025-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsAndSalesMember2021-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:C000089632Memberoef:AfterTaxesOnDistributionsAndSalesMember2016-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:IndexLB001Member2025-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:IndexLB001Member2021-04-292026-04-290001364924fmr:S000029150Memberfmr:StrategicAdvisersCoreIncomeFund-PROMemberfmr:IndexLB001Member2016-04-292026-04-29

iso4217:USD

xbrli:pure

xbrli:shares

Securities Act of 1933 Registration No. 333-139427

Investment Company Act of 1940 Registration No. 811-21991

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

[ ] Pre-Effective Amendment No. ______

[X] Post-Effective Amendment No. __138___

and

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 [X]

[X] Amendment No. _141____

Fidelity Rutland Square Trust II

(Exact Name of Registrant as Specified in Charter)

245 Summer Street, Boston, Massachusetts 02210

(Address of Principal Executive Offices)(Zip Code)

Registrant’s Telephone Number: 617-563-7000

| |

Nicole Macarchuk

Secretary and Chief Legal Officer

245 Summer Street

Boston, Massachusetts 02210

(Name and Address of Agent for Service)

| With copies to:

John V. O’Hanlon, Esq.

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, Massachusetts 02110

|

It is proposed that this filing will become effective on April 29, 2026 pursuant to paragraph (b) of Rule 485 at 12:01 a.m. Eastern Time.

Fund /Ticker

Strategic Advisers® International Fund /FILFX

Offered exclusively to certain managed account clients of Strategic Advisers LLC or its affiliates - not available for sale to the general public

Prospectus

April 29,

2026

Like securities of all mutual funds, these securities have not been approved or disapproved by the Securities and Exchange Commission, and the Securities and Exchange Commission has not determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense. |

245 Summer Street, Boston, MA 02210 |

Contents

Fund Summary

Fund:

Strategic Advisers® International Fund

Investment Objective

Strategic Advisers® International Fund seeks capital appreciation.

Fee Table

The following table describes the fees and expenses that may be incurred when you buy, hold, and sell shares of the fund.

Shareholder fees

|

(fees paid directly from your investment)

|

None

|

Annual Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

|

Management fee (fluctuates based on the fund's allocation among underlying funds and sub-advisers)

|

%

A

|

|

Distribution and/or Service (12b-1) fees

|

None

|

|

Other expenses

|

0.01

%

|

|

Acquired fund fees and expenses

|

0.22

%

|

|

Total annual operating expenses

|

%

B

|

|

Fee waiver and/or expense reimbursement

|

%

A

|

|

Total annual operating expenses after fee waiver and/or expense reimbursement

|

%

B

|

This

example

helps compare the cost of investing in the fund with the cost of investing in other funds.

Let's say, hypothetically, that the annual return for shares of the fund is 5% and that the fees and the annual operating expenses for shares of the fund are exactly as described in the fee table. This example illustrates the effect of fees and expenses, but is not meant to suggest actual or expected fees and expenses or returns, all of which may vary. For every $10,000 you invested, here's how much you would pay in total expenses if you sell all of your shares at the end of each time period indicated:

|

1 year

|

$

|

42

|

|

3 years

|

$

|

143

|

|

5 years

|

$

|

301

|

|

10 years

|

$

|

758

|

Portfolio Turnover

The fund will not incur transaction costs, such as commissions, when it buys and sells shares of affiliated mutual funds but may incur transaction costs when buying or selling non-affiliated funds and other types of securities (including Exchange Traded Funds (ETFs)) directly (or "turns over" its portfolio).

A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual operating expenses or in the example, affect the fund's performance. During the most recent fiscal year, the fund's portfolio turnover rate was

45

% of the average value of its portfolio.

Principal Investment Strategies

-

Normally investing primarily in non-U.S. securities, including securities of issuers located in emerging markets. Emerging markets include countries that have an emerging stock market as defined by MSCI, countries or markets with low- to middle-income economies as classified by the World Bank, and other countries or markets that the Adviser identifies as having similar emerging markets characteristics.

The Adviser considers non-U.S. securities to include investments that are tied economically to a particular country or region outside the U.S.

The Adviser considers a number of factors to determine whether an issuer is located in or tied economically to a particular country or region including: whether a third-party vendor has assigned a particular country or region classification to the issuer or included the issuer in an index representative of a particular country or region; the issuer's domicile, incorporation, and location of assets; whether the issuer derives at least 50% of its revenues from, or has at least 50% of its assets in, a particular country or region; the source of government guarantees (if any); and the primary trading market or listing exchange. Whether an issuer is located in or tied economically to a particular country can be determined under any of these factors.

- Normally investing primarily in common stocks.

- Allocating investments across different countries and regions.

- Implementing investment strategies by investing directly in securities through one or more managers (sub-advisers) or indirectly in securities through one or more other funds, referred to as underlying funds, which in turn invest directly in securities (as described below).

- Allocating assets among affiliated

funds (i.e., Fidelity® funds, including mutual funds and ETFs), non-affiliated

funds

and non-affiliated ETFs

.

- Allocating assets among underlying funds and sub-advisers to attempt to diversify its portfolio in terms of market capitalization, investment style, and geographic region.

- Allocating assets among sub-advisers and underlying funds using proprietary fundamental and quantitative research, considering factors including, but not limited to, performance in different market environments, manager experience and investment style, management company infrastructure, costs, asset size, and portfolio turnover.

Pursuant to an exemptive order granted by the Securities and Exchange Commission (SEC), Strategic Advisers LLC (Strategic Advisers) is permitted, subject to the approval of the Board of Trustees, to enter into new or amended sub-advisory agreements with one or more unaffiliated sub-advisers without obtaining shareholder approval of such agreements. Subject to oversight by the Board of Trustees, Strategic Advisers has the ultimate responsibility to oversee the fund's sub-advisers and recommend their hiring, termination, and replacement. In the event the Board of Trustees approves a sub-advisory agreement with a new unaffiliated sub-adviser, shareholders will be provided with information about the new sub-adviser and sub-advisory agreement .

Principal Investment Risks

- Multiple Sub-Adviser Risk.

Separate investment decisions and the resulting purchase and sale activities of the fund's sub-advisers might adversely affect the fund's performance or lead to disadvantageous tax consequences.

- Investing in Other Funds.

Regulatory restrictions may limit the amount that one fund can invest in another, which means that the fund's manager may not be able to invest as much as it wants to in some other funds. The fund bears all risks of investment strategies employed by the underlying funds, including the risk that the underlying funds will not meet their investment objectives. Underlying funds that are passively managed attempt to track the performance of an unmanaged index of securities and as such their performance could be lower than actively managed funds, which may shift their portfolio assets to take advantage of market opportunities or lessen the impact of a market decline. In addition, errors in the construction of the index tracked by an underlying passively managed fund may have an adverse impact on the performance of such underlying fund.

Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Different parts of the market, including different market sectors, and different types of securities can react differently to these developments.

Foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market.

The extent of economic development; political stability; market depth, infrastructure, and capitalization; and regulatory oversight can be less than in more developed markets. Emerging markets typically have less established legal, accounting and financial reporting systems than those in more developed markets, which may reduce the scope or quality of financial information available to investors.

Emerging markets can be subject to greater social, economic, regulatory, and political uncertainties and can be extremely volatile.

Foreign exchange rates also can be extremely volatile.

Social, political, and economic conditions and changes in regulatory, tax, or economic policy in a country or region could significantly affect the market in that country or region.

- Geographic Exposure to Europe.

Because the fund invests a meaningful portion of its assets in Europe, the fund's performance is expected to be closely tied to social, political, and economic conditions within Europe and to be more volatile than the performance of more geographically diversified funds.

Market conditions, interest rates, and economic, regulatory, or financial developments could significantly affect a single industry or group of related industries.

The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole.

The value of securities of smaller issuers can be more volatile than that of larger issuers.

ETFs may trade in the secondary market at prices below the value of their underlying portfolios and may not be liquid. ETFs that track an index are subject to tracking error and may be unable to sell poorly performing assets that are included in their index or other benchmark.

Securities selected using quantitative analysis can perform differently from the market as a whole as a result of the factors used in the analysis, the weight placed on each factor, and changes in the factors' historical trends.

An investment in the fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency

.

You could lose money by investing in the fund.

Performance

The following information is intended to help you understand the risks of investing in the fund.

The information illustrates the changes in the performance of the fund's shares from year to year and compares the performance of the fund's shares to the performance of a securities market index over various periods of time.

The index description appears in the "Additional Index Information" section of the prospectus.

Past performance (before and after taxes) is not an indication of future performance.

Visit

www.fidelity.com

for more recent performance information.

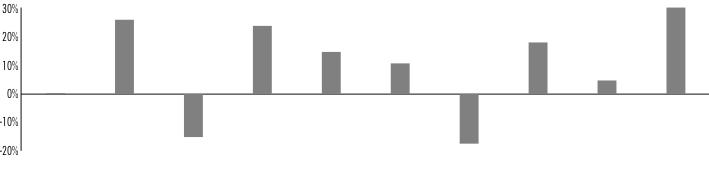

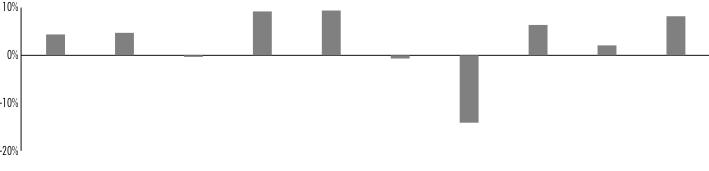

Year-by-Year Returns

|

|

2016

|

2017

|

2018

|

2019

|

2020

|

2021

|

2022

|

2023

|

2024

|

2025

|

|

|

0.36

%

|

26.22

%

|

-

15.14

%

|

24.06

%

|

14.88

%

|

10.84

%

|

-

17.47

%

|

18.22

%

|

4.81

%

|

30.52

%

|

|

During the periods shown in the chart:

|

Returns

|

Quarter ended

|

|

Highest Quarter Return

|

18.79

%

|

June 30, 2020

|

|

Lowest Quarter Return

|

-

22.31

%

|

March 31, 2020

|

|

Year-to-Date Return

|

0.64

%

|

March 31, 2026

|

Average Annual Returns

After-tax returns are calculated using the historical highest individual federal marginal income tax rates, but do not reflect the impact of state or local taxes.

Actual after-tax returns may differ depending on your individual circumstances.

The after-tax returns shown are not relevant if you hold your shares in a retirement account or in another tax-deferred arrangement, such as an employee benefit plan (profit sharing, 401(k), or 403(b) plan).

Return After Taxes on Distributions and Sale of Fund Shares may be higher than other returns for the same period due to a tax benefit of realizing a capital loss upon the sale of fund shares.

|

For the periods ended December 31, 2025

|

Past 1

year

|

Past 5

years

|

Past 10

years

|

|

Strategic Advisers® International Fund

|

|

|

|

|

Return Before Taxes

|

30.52

%

|

8.15

%

|

8.53

%

|

|

Return After Taxes on Distributions

|

28.33

%

|

6.80

%

|

7.48

%

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

19.54

%

|

6.18

%

|

6.75

%

|

|

MSCI EAFE Index

(reflects no deduction for fees or expenses)

|

31.59

%

|

9.17

%

|

8.42

%

|

|

|

|

|

|

Investment Adviser

Strategic Advisers (the Adviser) is the fund's manager. Arrowstreet Capital, Limited Partnership, Causeway Capital Management LLC, FIAM LLC, FIL Investment Advisors, Fidelity Diversifying Solutions LLC, Geode Capital Management, LLC, J.P. Morgan Investment Management Inc., Massachusetts Financial Services Company, T. Rowe Price Associates, Inc., Thompson, Siegel & Walmsley LLC, Wellington Management Company LLP, and William Blair Investment Management, LLC have been retained to serve as sub-advisers for the fund.

FIL Investment Advisors (UK) Limited (FIA(UK)), FMR Investment Management (UK) Limited (FMR UK), Fidelity Management & Research (Hong Kong) Limited (FMR H.K.), Fidelity Management & Research (Japan) Limited (FMR Japan), and T. Rowe Price International Ltd (TRPIL) have been retained to serve as sub-subadvisers for the fund.

The Adviser may change a sub-adviser's asset allocation at any time, including allocating no assets to, or terminating the sub-advisory contract with, a sub-adviser.

Portfolio Manager(s)

Wilfred Chilangwa (Lead Portfolio Manager) has managed the fund since 2006.

Purchase and Sale of Shares

The fund is not available for sale to the general public.

The price to buy one share is its net asset value per share (NAV). Shares will be bought at the NAV next calculated after an order is received in proper form.

The price to sell one share is its NAV. Shares will be sold at the NAV next calculated after an order is received in proper form.

The fund is open for business each day the New York Stock Exchange (NYSE) is open.

There is no purchase minimum for fund shares.

Tax Information

Distributions you receive from the fund are subject to federal income tax and generally will be taxed as ordinary income or capital gains, and may also be subject to state or local taxes, unless you are investing through a tax-advantaged retirement account (in which case you may be taxed later, upon withdrawal of your investment from such account).

Payments to Broker-Dealers and Other Financial Intermediaries

The fund, the Adviser, Fidelity Distributors Company LLC (FDC), and/or their affiliates may pay intermediaries, which may include banks, broker-dealers, retirement plan sponsors, administrators, or service-providers (who may be affiliated with the Adviser or FDC), for the sale of fund shares and related services. These payments may create a conflict of interest by influencing your intermediary and your investment professional to recommend the fund over another investment. Ask your investment professional or visit your intermediary's web site for more information.

Fund Basics

Investment Details

Investment Objective

Strategic Advisers® International Fund seeks capital appreciation.

Principal Investment Strategies

The fund normally invests primarily in non-U.S. securities, including securities of issuers located in emerging markets. Emerging markets include countries that have an emerging stock market as defined by MSCI, countries or markets with low- to middle-income economies as classified by the World Bank, and other countries or markets that the Adviser identifies as having similar emerging markets characteristics. Emerging markets tend to have relatively low gross national product per capita compared to the world's major economies and may have the potential for rapid economic growth.

The Adviser considers non-U.S. securities to include investments that are tied economically to a particular country or region outside the U.S.

The Adviser considers a number of factors to determine whether an issuer is located in or tied economically to a particular country or region including: whether a third-party vendor has assigned a particular country or region classification to the issuer or included the issuer in an index representative of a particular country or region; the issuer's domicile, incorporation, and location of assets; whether the issuer derives at least 50% of its revenues from, or has at least 50% of its assets in, a particular country or region; the source of government guarantees (if any); and the primary trading market or listing exchange. Whether an issuer is located in or tied economically to a particular country can be determined under any of these factors.

The fund normally invests primarily in common stocks.

The fund allocates investments across different countries and regions.

The fund implements its investment strategies by investing directly in securities through one or more sub-advisers or indirectly in securities through one or more underlying funds, which in turn invest directly in securities.

The Adviser may allocate the fund's assets among any number of underlying funds or sub-advisers

. The Adviser may actively adjust allocations among underlying funds or sub-advisers

at any time, including making no allocation at all to one or more sub-advisers.

The Adviser allocates the fund's assets among underlying funds and sub-advisers to attempt to diversify the fund's portfolio in terms of market capitalization, investment style, and geographic region.

The Adviser pursues a disciplined, benchmark-driven approach to portfolio construction, and monitors and adjusts allocations to underlying funds and sub-advisers as necessary to favor those underlying funds and sub-advisers that the Adviser believes will provide the most favorable outlook for achieving the fund's investment objective.

When determining how to allocate the fund's assets among sub-advisers and underlying funds, the Adviser uses proprietary fundamental and quantitative research, considering factors including, but not limited to, performance in different market environments, manager experience and investment style, management company infrastructure, costs, asset size, and portfolio turnover.

The fund may invest in affiliated

funds ( i.e., Fidelity ® funds, including mutual funds and ETFs), non-affiliated

funds and non-affiliated ETFs. Underlying funds include

funds managed by Fidelity Management & Research Company LLC (FMR) (an affiliated company that, together with the Adviser, is part of Fidelity Investments) or an affiliate and funds managed by investment advisers other than Fidelity. Fidelity may receive service fees that typically are at an annual rate of up to 0.40% of a non-affiliated underlying fund's average daily net assets attributable to purchases of underlying funds through Fidelity's FundsNetwork ® , though such fees may be higher or lower, or may be charged as transaction and/or account fees. In addition, the fund may invest in mutual funds and ETFs in transactions not occurring through Fidelity's FundsNetwork ® .

The Adviser generally classifies underlying funds by reference to a fund's name, policies, or investments.

For information on the underlying funds, see the underlying funds' prospectuses. A copy of any underlying Fidelity ® fund's prospectus is available at www.fidelity.com or institutional.fidelity.com. For a copy of any other underlying fund's prospectus, visit the web site of the company that manages or sponsors that underlying fund.

Common types of investment approaches that a sub-adviser may use in selecting investments for a fund include, but are not limited to, quantitative analysis, fundamental analysis, or a combination of both approaches. Quantitative analysis refers to programmatic models that analyze such factors as growth potential, valuation, liquidity, and investment risk based on data inputs. Fundamental analysis involves a bottom-up assessment of a company's potential for success in light of factors including its financial condition, earnings outlook, strategy, management, industry position, and economic and market conditions.

It is not possible to accurately predict the extent to which the fund's assets will be invested by a particular sub-adviser at any given time

.

The fund's initial shareholder approved a proposal permitting the Adviser to enter into new or amended sub-advisory agreements with one or more unaffiliated sub-advisers without obtaining shareholder approval of such agreements, subject to conditions of an exemptive order that has been granted by the SEC (Exemptive Order). One of the conditions of the Exemptive Order requires the Board of Trustees to approve any such agreement. Subject to oversight by the Board of Trustees, the Adviser has the ultimate responsibility to oversee the fund's sub-advisers and recommend their hiring, termination, and replacement. In the event the Board of Trustees approves a sub-advisory agreement with a new unaffiliated sub-adviser, shareholders will be provided with information about the new sub-adviser and sub-advisory agreement within ninety days of appointment.

Description of Principal Security Types

In addition to investing in underlying funds and the security types discussed above, the fund may invest directly in the following principal security types:

Equity securities represent an ownership interest, or the right to acquire an ownership interest, in an issuer. Equity securities include common stocks (including depositary receipts evidencing ownership of common stock), preferred stocks and other preferred securities, convertible securities, rights and warrants, and other securities, such as hybrid securities and trust preferred securities, believed to have equity-like characteristics.

Principal Investment Risks

Many factors affect the fund's performance. Developments that disrupt global economies and financial markets, such as

public health emergencies, military conflicts, terrorism, government restrictions, political changes, and environmental disasters, may significantly affect a fund's investment performance.

The fund's NAV changes daily based on the performance of the

fund's investments and on changes in market conditions and interest rates and in response to other economic, political, or financial developments. The fund's reaction to these developments will be affected by the types of

investments, the financial condition, industry and economic sector, and geographic location of an issuer, and the fund's level of investment in the securities of that underlying fund or issuer.

When your shares are sold they may be worth more or less than what you paid for them, which means that you could lose money by investing in the fund.

The following factors can significantly affect the fund's performance:

Asset Allocation Risk. The fund is subject to risks resulting from the Adviser's or a sub-adviser's asset allocation decisions. The selection of underlying funds or individual securities and the allocation of the fund's assets among various asset classes could cause the fund to lose value or its results to lag relevant benchmarks or other funds with similar objectives.

Multiple Sub-Adviser Risk . Because each sub-adviser manages its allocated portion, if any, independently from another sub-adviser, it is possible that the sub-advisers' security selection processes may not complement one another. As a result, the fund's aggregate exposure to a particular industry or group of industries, or to a single issuer, could unintentionally be larger or smaller than intended. Because each sub-adviser directs the trading for its own portion, if any, of the fund, and does not aggregate its transactions with those of the other sub-advisers, the fund may incur higher brokerage costs than would be the case if a single sub-adviser were managing the entire fund.

Investing in Other Funds. Regulatory restrictions may limit the amount that one fund can invest in another, and in certain cases further limit investments to the extent a fund's shares are already held by the Adviser or its affiliates. The fund bears all risks of investment strategies employed by the underlying funds. The fund does not control the investments of the underlying funds, which may have different investment objectives and may engage in investment strategies that the fund would not engage in directly. Aggregation of underlying fund holdings may result in indirect concentration of assets in a particular industry or group of industries, or in a single issuer, which may increase volatility. Some of the underlying funds in which the fund invests are managed with a passive investment strategy, attempting to track the performance of an unmanaged index of securities, regardless of the current or projected performance of an underlying fund's index or of the actual securities included in the index. This differs from an actively managed fund, which typically seeks to outperform a benchmark index. As a result, the performance of these underlying passively managed funds could be lower than actively managed funds that may shift their portfolio assets to take advantage of market opportunities or lessen the impact of a market decline or a decline in the value of one or more issuers. In addition, errors in the construction or calculation of the index tracked by an underlying passively managed fund may occur from time to time and may not be identified and corrected for some period of time, which may have an adverse impact on the performance of the underlying fund and its shareholders.

Stock Market Volatility . The value of equity securities fluctuates in response to issuer, political, market, and economic developments. Fluctuations, especially in foreign markets, can be dramatic over the short as well as long term, and different parts of the market, including different market sectors, and different types of equity securities can react differently to these developments. For example, stocks of companies in one sector can react differently from those in another, large cap stocks can react differently from small cap stocks, "growth" stocks can react differently from "value" stocks, and stocks selected using quantitative or technical analysis can react differently than stocks selected using fundamental analysis. Issuer, political, or economic developments can affect a single issuer, issuers within an industry or economic sector or geographic region, or the market as a whole. Changes in the financial condition of a single issuer can impact the market as a whole. Terrorism and related geo-political risks have led, and may in the future lead, to increased short-term market volatility and may have adverse long-term effects on world economies and markets generally.

Foreign Exposure. Foreign securities, foreign currencies, and securities issued by U.S. entities with substantial foreign operations can involve additional risks relating to political, economic, or regulatory conditions in foreign countries. These risks include fluctuations in foreign exchange rates; withholding or other taxes; trading, settlement, custodial, and other operational risks; and the less stringent investor protection and disclosure standards of some foreign markets. All of these factors can make foreign investments, especially those in emerging markets, more volatile and potentially less liquid than U.S. investments. In addition, foreign markets can perform differently from the U.S. market.

Investing in emerging markets can involve risks in addition to and greater than those generally associated with investing in more developed foreign markets. The extent of economic development; political stability; market depth, infrastructure, and capitalization; and regulatory oversight can be less than in more developed markets. Emerging markets typically have less established legal, accounting and financial reporting systems than those in more developed markets, which may reduce the scope or quality of financial information available to investors. Emerging markets economies can be subject to greater social, economic, regulatory, and political uncertainties and can be extremely volatile. All of these factors can make emerging markets securities more volatile and potentially less liquid than securities issued in more developed markets.

Global economies and financial markets are becoming increasingly interconnected, which increases the possibilities that conditions in one country or region might adversely impact issuers or providers in, or foreign exchange rates with, a different country or region.

Geographic Exposure. Social, political, and economic conditions and changes in regulatory, tax, or economic policy in a country or region could significantly affect the market in that country or region. From time to time, a small number of companies and industries may represent a large portion of the market in a particular country or region, and these companies and industries can be sensitive to adverse social, political, economic, currency, or regulatory developments. Similarly, from time to time, the fund or an underlying fund may invest a meaningful portion of its assets in the securities of issuers located in a single country or a limited number of countries. If the fund or an underlying fund invests in this manner, there is a higher risk that social, political, economic, tax (such as a tax on foreign investments or financial transactions), currency, or regulatory developments in those countries may have a significant impact on the fund's or the underlying fund's investment performance.

Special Considerations regarding Europe . Europe includes both developed and emerging markets. Most developed countries in Western Europe are members of the European Union (EU), and many are also members of the European Economic and Monetary Union (EMU). European countries can be significantly affected by the tight fiscal and monetary controls with which EU members and candidates for EMU membership are required to comply.

The financial instability of some countries in the EU, together with the risk of such instability impacting other more stable countries may increase the economic risk of investing in companies in Europe. Eastern European countries generally continue to move toward market economies. However, their markets remain relatively undeveloped and can be particularly sensitive to social, political, and economic developments. The EU faces challenges related to member states seeking to change their relationship with the EU, exemplified by the United Kingdom's withdrawal. There can be significant uncertainty as to the terms and consequences of EU member states seeking to change their relationship with the EU. Among other things, a member state's decision to leave the EU could result in increased volatility and illiquidity in the European and such member state's economies, as well as the broader global economy. Companies with a significant amount of business in the member state or Europe may experience lower revenue and/or profit growth, which may adversely affect the value of a fund's investments. In addition, uncertainty regarding any member state's exit from the EU may lead to instability in the foreign exchange markets, including volatility in the value of the euro.

Industry Exposure. Market conditions, interest rates, and economic, regulatory, or financial developments could significantly affect a single industry or a group of related industries, and the securities of companies in that industry or group of industries could react similarly to these or other developments. In addition, from time to time, a small number of companies may represent a large portion of a single industry or a group of related industries as a whole, and these companies can be sensitive to adverse economic, regulatory, or financial developments.

Issuer-Specific Changes. Changes in the financial condition of an issuer or counterparty, changes in specific economic or political conditions that affect a particular type of security or issuer, and changes in general economic or political conditions can increase the risk of default by an issuer or counterparty, which can affect a security's or instrument's value. The value of securities of smaller, less well-known issuers can be more volatile than that of larger issuers. Smaller issuers can have more limited product lines, markets, or financial resources.

Investing in ETFs. ETFs may trade in the secondary market ( e.g. , on a stock exchange) at prices below the value of their underlying portfolios and may not be liquid. An ETF that is not actively managed cannot sell poorly performing stocks or other assets as long as they are represented in its index or other benchmark. ETFs that track an index are subject to tracking error risk (the risk of errors in matching the ETF's underlying assets to its index or other benchmark).

Quantitative Investing. The value of securities selected using quantitative analysis can react differently to issuer, political, market, and economic developments than the market as a whole or securities selected using only fundamental analysis. The factors used in quantitative analysis and the weight placed on those factors may not be predictive of a security's value. In addition, factors that affect a security's value can change over time and these changes may not be reflected in the quantitative model.

In response to market, economic, political, or other conditions, a fund may temporarily use a different investment strategy for defensive purposes. If the fund does so, different factors could affect its performance and the fund may not achieve its investment objective.

Other Investment Strategies

In addition to the principal investment strategies discussed above, the Adviser may lend the fund's securities to broker-dealers or other institutions to earn income for the fund.

The fund may also use various techniques, such as buying and selling futures contracts, to increase or decrease its exposure to changing security prices or other factors that affect security values. The fund may also enter into foreign currency forward and options contracts for hedging purposes. In addition, the fund may have indirect exposure to derivatives through its investments in underlying funds.

Non-Fundamental Investment Policies

The fund's investment objective is non-fundamental and may be changed without shareholder approval.

Valuing Shares

The fund is open for business each day the NYSE is open.

The NAV is the value of a single share. Fidelity normally calculates NAV as of the close of business of the NYSE, normally 4:00 p.m. Eastern time. The fund's assets normally are valued as of this time for the purpose of computing NAV.

NAV is not calculated and the fund will not process purchase and redemption requests submitted on days when the fund is not open for business. The time at which shares are priced and until which purchase and redemption orders are accepted may be changed as permitted by the SEC.

To the extent that the fund's assets are traded in other markets on days when the fund is not open for business, the value of the fund's assets may be affected on those days. In addition, trading in some of the fund's assets may not occur on days when the fund is open for business.

Shares of underlying funds (other than ETFs) are valued at their respective NAVs. NAV is calculated using the values of the underlying funds in which the fund invests. For an explanation of the circumstances under which the underlying funds will use fair value pricing and the effects of using fair value pricing, see the underlying funds' prospectuses and Statements of Additional Information (SAIs). Other assets (including securities issued by ETFs) are valued primarily on the basis of market quotations, official closing prices, or information furnished by a pricing service. Certain short-term securities are valued on the basis of amortized cost. If market quotations, official closing prices, or information furnished by a pricing service are not readily available or, in the Adviser's opinion, are deemed unreliable for a security, then that security will be fair valued in good faith by the Adviser in accordance with applicable fair value pricing policies. For example, if, in the Adviser's opinion, a security's value has been materially affected by events occurring before a fund's pricing time but after the close of the exchange or market on which the security is principally traded, then that security will be fair valued in good faith by the Adviser in accordance with applicable fair value pricing policies.

Arbitrage opportunities may exist when trading in a portfolio security or securities is halted and does not resume before a fund calculates its NAV. These arbitrage opportunities may enable short-term traders to dilute the NAV of long-term investors. Securities trading in overseas markets, if applicable, present time zone arbitrage opportunities when events affecting portfolio security values occur after the close of the overseas markets but prior to the close of the U.S. market. Fair valuation of a fund's portfolio securities can serve to reduce arbitrage opportunities available to short-term traders, but there is no assurance that fair value pricing policies will prevent dilution of NAV by short-term traders.

Fair value pricing is based on subjective judgments and it is possible that the fair value of a security may differ materially from the value that would be realized if the security were sold.

Shareholder Information

Additional Information about the Purchase and Sale of Shares

NOT AVAILABLE FOR SALE TO THE GENERAL PUBLIC.

As used in this prospectus, the term "shares" generally refers to the shares offered through this prospectus.

General Information

Shares can be purchased only through certain discretionary investment programs offered by the Adviser or its affiliates. If you are not currently a client of a Fidelity discretionary investment program, please call 1-800-544-3455 (9:00 a.m. - 6:00 p.m. Eastern time, Monday through Friday) for more information. Additional fees apply for discretionary investment programs. For more information on these fees, please refer to the "Buying and Selling Information" section of the SAI.

The fund may reject for any reason, or cancel as permitted or required by law, any purchase orders.

Excessive trading of fund shares can harm shareholders in various ways, including reducing the returns to long-term shareholders by increasing costs to the fund (such as brokerage commissions or spreads paid to dealers who sell money market instruments), disrupting portfolio management strategies, and diluting the value of the shares in cases in which fluctuations in markets are not fully priced into the fund's NAV.

Because investments in the fund can only be made by the Adviser or an affiliate on behalf of its clients, the potential for excessive or short-term disruptive purchases and sales is reduced. Accordingly, the Board of Trustees has not adopted policies and procedures designed to discourage excessive trading of fund shares and the fund accommodates frequent trading.

The fund does not place a limit on purchases or sales of fund shares by the Adviser or its affiliates. The fund reserves the right, but does not have the obligation, to reject any purchase transaction at any time. In addition, the fund reserves the right to impose restrictions on disruptive, excessive, or short-term trading.

Buying Shares

Eligibility

Shares are generally available only to investors residing in the United States.

Shares are available only to certain discretionary investment programs offered by the Adviser or its affiliates.

There is no minimum balance or purchase minimum for fund shares.

Price to Buy

The price to buy one share is its NAV. Shares are sold without a sales charge.

Shares will be bought at the NAV next calculated after an order is received in proper form.

Provided the fund receives an order to buy shares in proper form before the close of business, the fund may place an order to buy shares of an underlying Fidelity ® fund after the close of business, pursuant to a pre-determined allocation, and receive that day's NAV.

The fund may stop offering shares completely or may offer shares only on a limited basis, for a period of time or permanently.

Under applicable anti-money laundering rules and other regulations, purchase orders may be suspended, restricted, or canceled and the monies may be withheld.

Selling Shares

The price to sell one share is its NAV.

Shares will be sold at the NAV next calculated after an order is received in proper form.

Normally, redemptions will be processed by the next business day, but it may take up to seven days to pay the redemption proceeds if making immediate payment would adversely affect the fund.

Provided the fund receives an order to sell shares in proper form before the close of business, the fund may place an order to sell shares of an underlying Fidelity ® fund after the close of business, pursuant to a pre-determined allocation, and receive that day's NAV.

See "Policies Concerning the Redemption of Fund Shares" below for additional redemption information.

Redemptions may be suspended or payment dates postponed when the NYSE is closed (other than weekends or holidays), when trading on the NYSE is restricted, or as permitted by the SEC.

Redemption proceeds may be paid in underlying fund shares, securities, or other property rather than in cash if the Adviser determines it is in the best interests of the fund.

Under applicable anti-money laundering rules and other regulations, redemption requests may be suspended, restricted, canceled, or processed and the proceeds may be withheld.

Policies Concerning the Redemption of Fund Shares

Shares of the fund are only available to certain discretionary investment programs offered by the Adviser or its affiliates.

If your account is held directly with a fund , the length of time that a fund typically expects to pay redemption proceeds depends on the method you have elected to receive such proceeds. A fund typically expects to make payment of redemption proceeds by wire, automated clearing house (ACH) or by issuing a check by the next business day following receipt of a redemption order in proper form. Proceeds from the periodic and automatic sale of shares of a Fidelity ® money market fund that are used to buy shares of another Fidelity ® fund are settled simultaneously.

If your account is held through an intermediary , the length of time that a fund typically expects to pay redemption proceeds depends, in part, on the terms of the agreement in place between the intermediary and a fund. For redemption proceeds that are paid either directly to you from a fund or to your intermediary for transmittal to you, a fund typically expects to make payments by wire, by ACH or by issuing a check on the next business day following receipt of a redemption order in proper form from the intermediary by a fund. Redemption orders that are processed through investment professionals that utilize the National Securities Clearing Corporation will generally settle one to three business days following receipt of a redemption order in proper form.

As noted elsewhere, payment of redemption proceeds may take longer than the time a fund typically expects and may take up to seven days from the date of receipt of the redemption order as permitted by applicable law.

Redemption Methods Available. Generally a fund expects to pay redemption proceeds in cash. To do so, a fund typically expects to satisfy redemption requests either by using available cash (or cash equivalents) or by selling portfolio securities. On a less regular basis, a fund may also satisfy redemption requests by utilizing one or more of the following sources, if permitted: borrowing from another Fidelity ® fund; drawing on an available line or lines of credit from a bank or banks; or using reverse repurchase agreements. These methods may be used during both normal and stressed market conditions.

In addition to paying redemption proceeds in cash, a fund reserves the right to pay part or all of your redemption proceeds in readily marketable securities instead of cash (redemption in-kind). Redemption in-kind proceeds will typically be made by delivering the selected securities to the redeeming shareholder within seven days after the receipt of the redemption order in proper form by a fund.

When your relationship with your managed account provider is terminated, your shares may be sold at the discretion of the managed account provider at the NAV next calculated after the sell order is placed, in which case the redemption proceeds will remain in your account pending your instruction.

Dividends and Capital Gain Distributions

The fund earns interest, dividends, and other income from its investments, and distributes this income (less expenses) to shareholders as dividends. The fund also realizes capital gains from its investments, and distributes these gains (less any losses) to shareholders as capital gain distributions.

The fund normally pays dividends and capital gain distributions per the tables below:

|

Fund Name

|

|

Dividends Paid

|

|

Strategic Advisers® International Fund

|

|

April, December

|

|

Fund Name

|

|

Capital Gains Paid

|

|

Strategic Advisers® International Fund

|

|

April, December

|

Distribution Options

Any dividends and capital gain distributions may be reinvested in additional shares or paid in cash.

Tax Consequences

As with any investment, your investment in the fund could have tax consequences for you (for non-retirement accounts).

Taxes on Distributions

Distributions you receive from the fund are subject to federal income tax, and may also be subject to state or local taxes.

For federal tax purposes, certain distributions, including dividends and distributions of short-term capital gains, are taxable to you as ordinary income, while certain distributions, including distributions of long-term capital gains, are taxable to you generally as capital gains. A percentage of certain distributions of dividends may qualify for taxation at long-term capital gains rates (provided certain holding period requirements are met).

If the Adviser buys shares on your behalf when a fund has realized but not yet distributed income or capital gains, you will be "buying a dividend" by paying the full price for the shares and then receiving a portion of the price back in the form of a taxable distribution.

Any taxable distributions you receive from the fund will normally be taxable to you when you receive them, regardless of your distribution option.

Taxes on Transactions

Your redemptions may result in a capital gain or loss for federal tax purposes. A capital gain or loss on your investment in the fund generally is the difference between the cost of your shares and the price you receive when you sell them.

Fund Services

Fund Management

The fund is a mutual fund, an investment that pools shareholders' money and invests it toward a specified goal.

The fund employs a multi-manager and a fund of funds investment structure. The Adviser may allocate the fund's assets among any number of sub-advisers or underlying funds. The Adviser may adjust allocations among underlying funds or sub-advisers from time to time, including making no allocation to, or terminating the sub-advisory contract with, a sub-adviser.

Adviser

Strategic Advisers LLC. The Adviser is the fund's manager. The address of the Adviser is 155 Seaport Boulevard, Boston, Massachusetts 02210.

As of December 31,

2025, the Adviser had approximately $1.

3 trillion in discretionary assets under management, and approximately

$7.

1 trillion when combined with all of its affiliates' assets under management.

As the manager, the Adviser has overall responsibility for directing the fund's investments and handling its business affairs.

Sub-Adviser(s)

Arrowstreet Capital, Limited Partnership (Arrowstreet) , at 200 Clarendon Street, 30th Floor, Boston, Massachusetts, 02116, has been retained to serve as a sub-adviser for the fund. As of February 28,

2026, Arrowstreet had approximately

$321.6 billion in assets under management.

Causeway Capital Management LLC (Causeway) , at 11111 Santa Monica Boulevard, 15th Floor, Los Angeles, California 90025, has been retained to serve as a sub-adviser for the fund. As of February 28,

2026, Causeway had approximately

$78.7 billion in assets under management.

Fidelity Diversifying Solutions LLC (FDS) , at 245 Summer Street, Boston, Massachusetts 02210, has been retained to serve as a sub-adviser for the fund. FDS is an affiliate of Strategic Advisers. As of December 31,

2025, FDS had approximately

$18.

8 billion in discretionary assets under management.

Other investment advisers have been retained to assist FDS with foreign investments:

- FMR UK, at

25 Cannon Street, London,

EC4M 5SB, United Kingdom, has been retained to serve as a sub-subadviser for the fund. As of December 31,

2025, FMR UK had approximately

$25.8 billion in discretionary assets under management. FMR UK may provide investment research and advice on issuers based outside the United States and may also provide investment advisory services for the fund. FMR UK is an affiliate of both FDS and the Adviser.

- FMR H.K., at Floor 19, 41 Connaught Road Central, Hong Kong, has been retained to serve as a sub-subadviser for the fund. As of December 31,

2025, FMR H.K. had approximately

$32.5 billion in discretionary assets under management. FMR H.K. may provide investment research and advice on issuers based outside the United States and may also provide investment advisory services for the fund. FMR H.K. is an affiliate of both FDS and the Adviser.

- FMR Japan, at Kamiyacho Prime Place, 1-17, Toranomon-4-Chome, Minato-ku, Tokyo, Japan, has been retained to serve as a sub-subadviser for the fund. As of March 31,

2025, FMR Japan had approximately $2.8 billion in discretionary assets under management. FMR Japan may provide investment research and advice on issuers based outside the United States and may also provide investment advisory services for the fund. FMR Japan is an affiliate of both FDS and the Adviser.

FIAM LLC (FIAM) , at 900 Salem Street, Smithfield, Rhode Island 02917, has been retained to serve as a sub-adviser for the fund. FIAM is an affiliate of Strategic Advisers. As of December 31,

2025, FIAM had approximately

$347.7 billion in discretionary assets under management.

Other investment advisers have been retained to assist FIAM with foreign investments:

- FMR UK, at

25 Cannon Street, London,

EC4M 5SB, United Kingdom, has been retained to serve as a sub-subadviser for the fund. As of December 31,

2025, FMR UK had approximately

$25.8 billion in discretionary assets under management. FMR UK may provide investment research and advice on issuers based outside the United States and may also provide investment advisory services for the fund. FMR UK is an affiliate of both FIAM and the Adviser.

- FMR H.K., at Floor 19, 41 Connaught Road Central, Hong Kong, has been retained to serve as a sub-subadviser for the fund. As of December 31,

2025, FMR H.K. had approximately

$32.5 billion in discretionary assets under management. FMR H.K. may provide investment research and advice on issuers based outside the United States and may also provide investment advisory services for the fund. FMR H.K. is an affiliate of both FIAM and the Adviser.

- FMR Japan, at Kamiyacho Prime Place, 1-17, Toranomon-4-Chome, Minato-ku, Tokyo, Japan, has been retained to serve as a sub-subadviser for the fund. As of March 31,