UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

For the quarterly period ended March 31, 2026

OR

For the transition period from _____ to _____

Commission File Number: 001-40594

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip code) | |||||||

| (Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ☑ | No ☐ | |||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☑ | No ☐ | |||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Accelerated filer | Non-accelerated filer | Smaller reporting company | Emerging growth company | |||||||||||

| ☑ | ☐ | ☐ | ||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | ||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes | No ☑ | |||||||||

PHILLIPS EDISON & COMPANY, INC. FORM 10-Q

| TABLE OF CONTENTS | |||||||||||

| NOTES TO THE UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS | |||||||||||

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 1 | ||||||||||

w PART I FINANCIAL INFORMATION | ||

ITEM 1. FINANCIAL STATEMENTS

PHILLIPS EDISON & COMPANY, INC.

CONSOLIDATED BALANCE SHEETS

AS OF MARCH 31, 2026 AND DECEMBER 31, 2025

(Condensed and Unaudited)

(In thousands, except per share amounts)

| March 31, 2026 | December 31, 2025 | ||||||||||

| ASSETS | |||||||||||

| Investment in real estate: | |||||||||||

| Land and improvements | $ | $ | |||||||||

| Building and improvements | |||||||||||

| In-place lease assets | |||||||||||

| Above-market lease assets | |||||||||||

| Total investment in real estate assets | |||||||||||

| Accumulated depreciation and amortization | ( | ( | |||||||||

| Net investment in real estate assets | |||||||||||

| Investment in unconsolidated joint ventures | |||||||||||

| Total investment in real estate assets, net | |||||||||||

| Cash and cash equivalents | |||||||||||

| Restricted cash | |||||||||||

| Goodwill | |||||||||||

| Other assets, net | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Liabilities: | |||||||||||

| Debt obligations, net | $ | $ | |||||||||

| Below-market lease liabilities, net | |||||||||||

| Accounts payable and other liabilities | |||||||||||

| Deferred income | |||||||||||

| Total liabilities | |||||||||||

Commitments and contingencies (see Note 8) | |||||||||||

| Equity: | |||||||||||

Preferred stock, $ | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital (“APIC”) | |||||||||||

Accumulated other comprehensive income (“AOCI”) | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Noncontrolling interests | |||||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

See notes to consolidated financial statements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 2 | ||||||||||

PHILLIPS EDISON & COMPANY, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Condensed and Unaudited)

(In thousands, except per share amounts)

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Revenues: | |||||||||||

| Rental income | $ | $ | |||||||||

| Fees and management income | |||||||||||

| Other property income | |||||||||||

| Total revenues | |||||||||||

| Operating Expenses: | |||||||||||

| Property operating | |||||||||||

| Real estate taxes | |||||||||||

| General and administrative | |||||||||||

| Depreciation and amortization | |||||||||||

| Total operating expenses | |||||||||||

| Other: | |||||||||||

| Interest expense, net | ( | ( | |||||||||

| Gain on disposal of property, net | |||||||||||

| Other expense, net | ( | ( | |||||||||

| Net income | |||||||||||

| Net income attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to stockholders | $ | $ | |||||||||

| Earnings per share of common stock: | |||||||||||

Net income per share attributable to stockholders - basic and diluted (see Note 10) | $ | $ | |||||||||

| Comprehensive income: | |||||||||||

| Net income | $ | $ | |||||||||

| Other comprehensive income (loss): | |||||||||||

| Change in unrealized value on interest rate swaps | ( | ||||||||||

| Comprehensive income | |||||||||||

| Net income attributable to noncontrolling interests | ( | ( | |||||||||

| Change in unrealized value on interest rate swaps attributable to noncontrolling interests | ( | ||||||||||

| Reallocation of comprehensive income upon conversion of noncontrolling interests | |||||||||||

| Comprehensive income attributable to stockholders | $ | $ | |||||||||

See notes to consolidated financial statements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 3 | ||||||||||

PHILLIPS EDISON & COMPANY, INC.

CONSOLIDATED STATEMENTS OF EQUITY

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Condensed and Unaudited)

(In thousands, except per share amounts)

| Three Months Ended March 31, 2026 and 2025 | |||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | APIC | AOCI | Accumulated Deficit | Total Stockholders’ Equity | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2025 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Change in unrealized value on interest rate swaps | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

Common distributions declared, $ | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | |||||||||||||||||||||||||||||||||||||||||||||

| Conversion of noncontrolling interests | — | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2025 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2026 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Change in unrealized value on interest rate swaps | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

Common distributions declared, $ | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||

| Conversion of noncontrolling interests | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2026 | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

See notes to consolidated financial statements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 4 | ||||||||||

PHILLIPS EDISON & COMPANY, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Condensed and Unaudited)

(In thousands)

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||||||

Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization of real estate assets | |||||||||||

| Depreciation and amortization of corporate assets | |||||||||||

| Net amortization of above- and below-market leases | ( | ( | |||||||||

| Amortization of deferred financing expenses | |||||||||||

| Amortization of debt and derivative adjustments | |||||||||||

| Loss on extinguishment or modification of debt, net | |||||||||||

| Gain on disposal of property, net | ( | ( | |||||||||

| Straight-line rent, net | ( | ( | |||||||||

| Share-based compensation | |||||||||||

| Return on investment in unconsolidated joint ventures | |||||||||||

| Other | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Other assets, net | ( | ( | |||||||||

| Accounts payable and other liabilities | ( | ( | |||||||||

Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||||||

| Real estate acquisitions, net | ( | ( | |||||||||

| Capital expenditures | ( | ( | |||||||||

| Proceeds from sale of real estate, net | |||||||||||

| Proceeds from secured loan receivable | |||||||||||

| Investment in unconsolidated joint ventures | ( | ( | |||||||||

| Return of investment in unconsolidated joint ventures | |||||||||||

| Investment in marketable securities | ( | ( | |||||||||

| Proceeds from sale of marketable securities | |||||||||||

| Insurance proceeds for property damage claims | |||||||||||

Net cash used in investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||||||

| Proceeds from revolving credit facility | |||||||||||

| Payments on revolving credit facility | ( | ( | |||||||||

| Proceeds from notes and loans payable, net | |||||||||||

| Payments on mortgages and loans payable | ( | ( | |||||||||

| Distributions paid | ( | ( | |||||||||

| Distributions to noncontrolling interests | ( | ( | |||||||||

Net cash provided by financing activities | |||||||||||

NET DECREASE IN CASH, CASH EQUIVALENTS, AND RESTRICTED CASH | ( | ( | |||||||||

| CASH, CASH EQUIVALENTS, AND RESTRICTED CASH: | |||||||||||

| Beginning of period | |||||||||||

| End of period | $ | $ | |||||||||

| RECONCILIATION TO CONSOLIDATED BALANCE SHEETS: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | |||||||||

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 5 | ||||||||||

PHILLIPS EDISON & COMPANY, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Condensed and Unaudited)

(In thousands)

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | |||||||||||

| Cash paid for interest | $ | $ | |||||||||

| SUPPLEMENTAL SCHEDULE OF NON-CASH ACTIVITIES: | |||||||||||

| Secured loan receivable | |||||||||||

| Accrued capital expenditures | |||||||||||

| Change in distributions payable | ( | ( | |||||||||

| Change in distributions payable - noncontrolling interests | ( | ( | |||||||||

See notes to consolidated financial statements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 6 | ||||||||||

Phillips Edison & Company, Inc.

Notes to Consolidated Financial Statements

(Condensed and Unaudited)

| 1. ORGANIZATION | ||

Phillips Edison & Company, Inc. (“we,” the “Company,” “PECO,” “our,” or “us”) was formed as a Maryland corporation in October 2009. Substantially all of our business is conducted through Phillips Edison Grocery Center Operating Partnership I, L.P. (the “Operating Partnership”), a Delaware limited partnership formed in December 2009. We are a limited partner of the Operating Partnership, and our wholly-owned subsidiary, Phillips Edison Grocery Center OP GP I LLC, is the sole general partner of the Operating Partnership.

We are a real estate investment trust (“REIT”) that invests primarily in omni-channel grocery-anchored neighborhood and community shopping centers that have a mix of creditworthy national, regional, and local retailers that sell necessity-based goods and services in strong demographic markets throughout the United States. In addition to managing our own shopping centers, our third-party investment management business provides comprehensive real estate and asset management services to three unconsolidated institutional joint ventures, in which we have partial ownership interests, and one private fund (collectively, the “Managed Funds”).

As of March 31, 2026, we wholly-owned 299 real estate properties. Additionally, we owned a 14 % interest in Grocery Retail Partners I LLC (“GRP I”), which owned 20 properties, a 20 % interest in Necessity Retail Venture LLC (“NRV”), which owned four properties, and a 31 % interest in Neighborhood Grocery Catalyst Fund LLC (“NGCF”), which owned three properties.

| 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES | ||

Set forth below is a summary of the significant accounting estimates and policies that management believes are important to the preparation of our consolidated interim financial statements. Certain of our accounting estimates are particularly important for an understanding of our financial position and results of operations and require the application of significant judgment by management. For example, significant estimates and assumptions have been made with respect to the useful lives of assets; remaining hold periods of assets; recoverable amounts of receivables; initial valuations of tangible and intangible assets and liabilities, including goodwill, and related amortization periods of deferred costs and intangibles, particularly with respect to property acquisitions; and other fair value measurement assessments required for the preparation of the consolidated interim financial statements. As a result, these estimates are subject to a degree of uncertainty.

There were no changes to our significant accounting policies during the three months ended March 31, 2026. For a full summary of our significant accounting policies, refer to our 2025 Annual Report on Form 10-K, filed with the U.S. Securities and Exchange Commission (“SEC”) on February 10, 2026.

Basis of Presentation and Principles of Consolidation—The accompanying consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information and with instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. Readers of this Quarterly Report on Form 10-Q should refer to our audited consolidated financial statements for the year ended December 31, 2025, which are included in our 2025 Annual Report on Form 10-K. In the opinion of management, all normal and recurring adjustments necessary for the fair presentation of the unaudited consolidated financial statements for the periods presented have been included in this Quarterly Report. Our results of operations for the three months ended March 31, 2026 are not necessarily indicative of the operating results expected for the full year.

The accompanying consolidated financial statements include our accounts and the accounts of the Operating Partnership and its wholly-owned subsidiaries (over which we exercise financial and operating control). The financial statements of the Operating Partnership are prepared using accounting policies consistent with our accounting policies. All intercompany balances and transactions are eliminated upon consolidation.

Income Taxes—Our consolidated financial statements include the operations of wholly-owned subsidiaries that have jointly elected to be treated as taxable REIT subsidiary entities and are subject to U.S. federal, state, and local income taxes at regular corporate tax rates. We recognized federal, state, and local income tax expense of $0.2 million and $0.1 million for the three months ended March 31, 2026 and 2025, respectively. All income tax amounts are included in Other Expense, Net on our consolidated statements of operations and comprehensive income (“consolidated statements of operations”).

Recently Issued or Adopted Accounting Pronouncements—There were no recently issued or adopted accounting pronouncements during the three months ended March 31, 2026 that impacted the Company.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 7 | ||||||||||

| 3. LEASES | ||

Lessor—The majority of our leases are largely similar in that the leased asset is retail space within our properties, and the lease agreements generally contain similar provisions and features, without substantial variations. All of our leases are currently classified as operating leases. Lease income related to our operating leases was as follows (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

Rental income related to fixed lease payments(1) | $ | $ | |||||||||

Rental income related to variable lease payments(1)(2) | |||||||||||

Straight-line rent amortization(3) | |||||||||||

| Amortization of lease assets | |||||||||||

| Lease buyout income | |||||||||||

Adjustments for collectibility(4) | ( | ( | |||||||||

| Total rental income | $ | $ | |||||||||

(1)Includes rental income related to lease payments before assessing for collectibility.

(2)Variable payments are primarily related to tenant recovery income.

(3)Includes revenue adjustments to straight-line rent for tenants considered non-creditworthy.

(4)Includes general reserves as well as adjustments for tenants considered non-creditworthy for which we are recording revenue on a cash basis, per Accounting Standards Codification (“ASC”) Topic 842, Leases.

Approximate future fixed contractual lease payments to be received under non-cancelable operating leases in effect as of March 31, 2026, assuming no new or renegotiated leases or option extensions on lease agreements, and including the impact of rent abatements and tenants who have been moved to the cash basis of accounting for revenue recognition purposes, were as follows (in thousands):

| Year | Amount | ||||

| Remaining 2026 | $ | ||||

| 2027 | |||||

| 2028 | |||||

| 2029 | |||||

| 2030 | |||||

| Thereafter | |||||

| Total | $ | ||||

No single tenant comprised 10% or more of our aggregate annualized base rent (“ABR”) as of March 31, 2026. As of March 31, 2026, our wholly-owned real estate investments in Florida, California, and Texas represented 11.9 %, 11.3 %, and 10.0 % of our ABR, respectively. As a result, the geographic concentration of our portfolio makes it particularly susceptible to adverse natural or economic events in the Florida, California, and Texas real estate markets.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 8 | ||||||||||

| 4. REAL ESTATE ACTIVITY | ||

Acquisitions—The following table summarizes our real estate acquisition activity (dollars in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

Number of properties acquired(1) | |||||||||||

Number of outparcels and land for future development acquired(2) | |||||||||||

| Contract price | $ | $ | |||||||||

Total price of acquisitions(3) | |||||||||||

(1)During the three months ended March 31, 2026, we acquired a property adjacent to one that was already wholly-owned. Therefore, the property was not an addition to our total property count.

(2)Outparcels acquired are adjacent to shopping centers that we own.

Subsequent to March 31, 2026, we acquired three properties for $58.9 million.

The aggregate purchase price of the assets acquired during the three months ended March 31, 2026 and 2025 was allocated as follows (in thousands):

| March 31, 2026 | March 31, 2025 | ||||||||||

| ASSETS | |||||||||||

| Land and improvements | $ | $ | |||||||||

| Building and improvements | |||||||||||

| In-place lease assets | |||||||||||

| Above-market lease assets | |||||||||||

| Total assets | |||||||||||

| LIABILITIES | |||||||||||

| Below-market lease liabilities | |||||||||||

| Total liabilities | |||||||||||

| Net assets acquired | $ | $ | |||||||||

The weighted-average amortization periods for in-place, above-market, and below-market lease intangibles acquired during the three months ended March 31, 2026 and 2025 were as follows (in years):

| March 31, 2026 | March 31, 2025 | ||||||||||

| Acquired in-place leases | |||||||||||

| Acquired above-market leases | |||||||||||

| Acquired below-market leases | |||||||||||

Property Dispositions—The following table summarizes our real estate disposition activity for the three months ended March 31, 2026 and 2025 (dollars in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Number of properties sold | |||||||||||

| Contract price | $ | $ | |||||||||

Proceeds from sale of real estate, net(1)(2) | |||||||||||

Gain on disposal of property, net | |||||||||||

(1)Total proceeds from sale of real estate, net includes closing costs less credits and secured loans received.

Subsequent to March 31, 2026, we sold one parcel of land for $6.7 million.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 9 | ||||||||||

| 5. OTHER ASSETS, NET | ||

The following is a summary of Other Assets, Net outstanding as of March 31, 2026 and December 31, 2025 (in thousands):

| March 31, 2026 | December 31, 2025 | ||||||||||

| Other assets, net: | |||||||||||

| Deferred leasing commissions and costs | $ | $ | |||||||||

Deferred financing expenses(1) | |||||||||||

| Office equipment, including capital lease assets, and other | |||||||||||

| Corporate intangible assets | |||||||||||

| Total depreciable and amortizable assets | |||||||||||

| Accumulated depreciation and amortization | ( | ( | |||||||||

| Net depreciable and amortizable assets | |||||||||||

Accounts receivable, net(2) | |||||||||||

| Accounts receivable - affiliates | |||||||||||

Secured loan receivable(3) | |||||||||||

Deferred rent receivable, net(4) | |||||||||||

| Prepaid expenses and other | |||||||||||

| Investment in third parties | |||||||||||

| Investment in marketable securities | |||||||||||

| Total other assets, net | $ | $ | |||||||||

(1)Deferred financing expenses per the above table are related to our revolving credit facility, and as such we have elected to classify them as an asset rather than as a contra-liability.

(2)Net of $2.4 million and $2.6 million of general reserves for uncollectible amounts as of March 31, 2026 and December 31, 2025, respectively. Receivables that were removed for tenants considered to be non-creditworthy were $6.2 million and $6.5 million as of March 31, 2026 and December 31, 2025, respectively.

(3)Secured loan receivable relates to the financing provided for the sale of one of our properties during the three months ended March 31, 2025. See Note 4.

(4)Net of $4.0 million and $4.3 million of receivables removed as of March 31, 2026 and December 31, 2025, respectively, related to straight-line rent for tenants previously or currently considered to be non-creditworthy.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 10 | ||||||||||

| 6. DEBT OBLIGATIONS | ||

The following is a summary of the outstanding principal balances and interest rates, which includes the effect of derivative financial instruments, for our debt obligations as of March 31, 2026 and December 31, 2025 (dollars in thousands):

Interest Rate(1) | March 31, 2026 | December 31, 2025 | |||||||||||||||

Revolving credit facility(2) | SOFR + | $ | $ | ||||||||||||||

Term loans(2) | |||||||||||||||||

| Senior unsecured notes due 2031 | |||||||||||||||||

| Senior unsecured notes due 2032 | |||||||||||||||||

| Senior unsecured notes due 2033 | |||||||||||||||||

| Senior unsecured notes due 2034 | |||||||||||||||||

| Senior unsecured notes due 2035 | |||||||||||||||||

| Secured loan facilities | |||||||||||||||||

| Mortgages | |||||||||||||||||

| Finance lease liability | |||||||||||||||||

| Discount on notes payable | ( | ( | |||||||||||||||

| Assumed market debt adjustments, net | |||||||||||||||||

| Deferred financing expenses, net | ( | ( | |||||||||||||||

| Total | $ | $ | |||||||||||||||

Weighted-average interest rate(3) | % | % | |||||||||||||||

(1)Interest rates are as of March 31, 2026.

(2)Our revolving credit facility and term loans carry an interest rate of the Secured Overnight Financing Rate (“SOFR”) plus a spread. While some of the rates are fixed through the use of swaps, a portion of this debt is not subject to a swap, and thus is still indexed to SOFR.

(3)Includes the effects of derivative financial instruments as of March 31, 2026 and December 31, 2025 (see Notes 7 and 12).

2026 Debt Activity—In January 2026, we extended the maturity of our $161.8 million term loan from January 2026 to January 2027.

In February 2026, we issued $350 million of 4.750 % senior notes due 2033 at an issue price of 99.920 % in an underwritten offering. The offering resulted in gross proceeds of $346.5 million, which were used to fully repay two term loans that were set to mature in January 2027 for $158 million and $165 million, respectively, with the remaining balance of $23.5 million used to pay down our revolving credit facility.

The 2026 senior notes are fully and unconditionally guaranteed by us.

Debt Allocation—The allocation of total debt between fixed-rate and variable-rate as well as between secured and unsecured, excluding market debt adjustments, discount on senior notes, and deferred financing expenses, net, and including the effects of derivative financial instruments as of March 31, 2026 and December 31, 2025 is summarized below (in thousands):

| March 31, 2026 | December 31, 2025 | ||||||||||

As to interest rate(1): | |||||||||||

| Fixed-rate debt | $ | $ | |||||||||

| Variable-rate debt | |||||||||||

| Total | $ | $ | |||||||||

| As to collateralization: | |||||||||||

| Unsecured debt | $ | $ | |||||||||

| Secured debt | |||||||||||

| Total | $ | $ | |||||||||

Pursuant to the terms of our credit agreements, we are subject to, among other things, the maintenance of various financial covenants. We were in compliance with these covenants as of March 31, 2026.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 11 | ||||||||||

| 7. DERIVATIVES AND HEDGING ACTIVITIES | ||

Risk Management Objective of Using Derivatives—We are exposed to certain risks arising from both our business operations and economic conditions. We principally manage our exposure to a wide variety of business and operational risks through management of our core business activities. We manage economic risks, including interest rate, liquidity, and credit risk, primarily by managing the amount, sources, and duration of our debt funding, and through the use of derivative financial instruments. Specifically, we enter into interest rate swaps to manage exposures that arise from business activities that result in the receipt or payment of future known and uncertain cash amounts, the value of which are determined by interest rates. Our derivative financial instruments are used to manage differences in the amount, timing, and duration of our known or expected cash receipts and our known or expected cash payments principally related to our investments and borrowings.

Cash Flow Hedges of Interest Rate Risk—Interest rate swaps designated as cash flow hedges involve the receipt of variable amounts from a counterparty in exchange for our making fixed-rate payments over the life of the agreements without exchange of the underlying notional amount.

The changes in the fair value of derivatives designated, and that qualify, as cash flow hedges are recorded in AOCI and are subsequently reclassified into earnings in the period that the hedged forecasted transaction affects earnings. During the three months ended March 31, 2026 and 2025, such derivatives were used to hedge the variable cash flows associated with certain variable-rate debt. Amounts reported in AOCI related to these derivatives will be reclassified to Interest Expense, Net as interest payments are made on the variable-rate debt. During the next twelve months, we estimate that an additional $0.2 million will be reclassified from AOCI as a decrease to Interest Expense, Net.

The following is a summary of our interest rate swaps that were designated as cash flow hedges of interest rate risk as of March 31, 2026 and December 31, 2025 (dollars in thousands):

| March 31, 2026 | December 31, 2025 | ||||||||||

| Count | |||||||||||

| Notional amount | $ | $ | |||||||||

| Fixed SOFR | |||||||||||

| Maturity date | 2026 | 2026 | |||||||||

| Weighted-average term (in years) | |||||||||||

The table below details the nature of the gain and loss recognized on interest rate derivatives designated as cash flow hedges in the consolidated statements of operations (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Amount of gain (loss) recognized in Other Comprehensive Income | $ | $ | ( | ||||||||

| Amount of gain reclassified from AOCI into Interest Expense, Net | ( | ( | |||||||||

Credit-risk-related Contingent Features—We have agreements with our derivative counterparties that contain provisions where, if we default, or are capable of being declared in default, on any of our indebtedness, we could also be declared to be in default on our derivative obligations. As of March 31, 2026, there were no derivatives with a fair value in a net liability position, which would include accrued interest but exclude any adjustment for nonperformance risk related to these agreements.

| 8. COMMITMENTS AND CONTINGENCIES | ||

Litigation—We are involved in various claims and litigation matters arising in the ordinary course of business, some of which involve claims for damages. Many of these matters are covered by insurance, although they may nevertheless be subject to deductibles or retentions. Although the ultimate liability for these matters cannot be determined, based upon information currently available, we believe the resolution of such claims and litigation will not have a material adverse effect on our consolidated financial statements.

Environmental Matters—In connection with the ownership and operation of real estate, we may potentially be liable for costs and damages related to environmental matters. In addition, we may own or acquire certain properties that are subject to environmental remediation. Depending on the nature of the environmental matter, the seller of the property, a tenant of the property, and/or another third party may be responsible for environmental remediation costs related to a property. Additionally, in connection with the purchase of certain properties, the respective sellers and/or tenants may agree to indemnify us against future remediation costs. We also carry environmental liability insurance on our properties that provides limited coverage for any remediation liability and/or pollution liability for third-party bodily injury and/or property damage

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 12 | ||||||||||

claims for which we may be liable. We are not currently aware of any environmental matters that we believe are reasonably likely to have a material adverse effect on our consolidated financial statements.

Captive Insurance—Our captive insurance company, Silver Rock Insurance, Inc. (“Silver Rock”), provides general liability insurance, wind, reinsurance, and other coverage to us and our GRP I, NRV, and NGCF joint ventures. We capitalize Silver Rock in accordance with applicable regulatory requirements.

Silver Rock establishes annual premiums based on the past loss experience of the insured properties. An independent third party was engaged to perform an actuarial estimate of projected future claims, related deductibles, and projected future expenses necessary to fund associated risk management programs. Premiums paid to Silver Rock may be adjusted based on this estimate, and such premiums may be reimbursed by tenants pursuant to specific lease terms.

As of March 31, 2026, we had three letters of credit outstanding totaling approximately $31.1 million to provide security for our obligations under Silver Rock’s insurance and reinsurance contracts.

| 9. EQUITY | ||

General—The holders of common stock are entitled to one vote per share on all matters voted on by stockholders, including one vote per nominee in the election of our Board of Directors (the “Board”). Our charter does not provide for cumulative voting in the election of directors.

At-the-Market Offering (“ATM”)—In February 2024, we entered into a sales agreement relating to the potential sale of shares of common stock pursuant to a continuous offering program. In accordance with the terms of the sales agreement, we may offer and sell shares of our common stock having an aggregate offering price of up to $250 million from time to time through our sales agents, or, if applicable, as forward sellers. We issued no 177 million of common stock remained available for issuance under the ATM program.

Distributions—For each month beginning January 2026 through March 2026, we declared and paid monthly distributions of $0.1083

| Month | Date of Record | Date Distribution Paid | Monthly Distribution Rate | Cash Distribution | |||||||||||||

| March | 3/16/2026 | 4/1/2026 | $ | $ | |||||||||||||

Convertible Noncontrolling Interests—As of March 31, 2026 and December 31, 2025, we had approximately 12.7

Under the terms of the Fourth Amended and Restated Agreement of Limited Partnership, OP unit holders may elect to cause the Operating Partnership to redeem their OP units. The Operating Partnership controls the form of the redemption, and may elect to redeem OP units for shares of our common stock, provided that the OP units have been outstanding for at least one year , or for cash. As the form of redemption for OP units is within our control, the OP units outstanding as of March 31, 2026 and December 31, 2025 are classified as Noncontrolling Interests within permanent equity on our consolidated balance sheets.

The table below is a summary of our OP unit activity for the three months ended March 31, 2026 and 2025 (dollars and shares in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

OP units converted into shares of common stock(1) | |||||||||||

Distributions declared on OP units(2) | $ | $ | |||||||||

(1)OP units convert into shares of our common stock at a 1 :1 ratio.

(2)Distributions declared on OP units are included in Distributions to Noncontrolling Interests on the consolidated statements of equity.

Share Repurchase Program—We have a Board approved share repurchase program of up to $250 million of common stock. The program may be suspended or discontinued at any time, and does not obligate us to repurchase any dollar amount or particular number of shares. No share repurchases have been made to date under this program.

| 10. EARNINGS PER SHARE | ||

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 13 | ||||||||||

The following table provides a reconciliation of the numerator and denominator of the earnings per share calculations (in thousands, except per share amounts):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Numerator: | |||||||||||

Net income attributable to stockholders - basic | $ | $ | |||||||||

Net income attributable to convertible OP units(1) | |||||||||||

Net income - diluted | $ | $ | |||||||||

| Denominator: | |||||||||||

| Weighted-average shares - basic | |||||||||||

OP units(1) | |||||||||||

Dilutive restricted stock awards(2) | |||||||||||

| Adjusted weighted-average shares - diluted | |||||||||||

| Earnings per common share: | |||||||||||

Basic and diluted income per share | $ | $ | |||||||||

(1)OP units include units that are convertible into common stock or cash, at the Operating Partnership’s option. The Operating Partnership income or loss attributable to these OP units, which is included as a component of Net Income Attributable to Noncontrolling Interests on the consolidated statements of operations, has been added back in the numerator as these OP units were included in the denominator for all periods presented. OP units are allocated income on a consistent basis with the common stockholder and therefore have no dilutive impact to earnings per share of common stock.

(2)For the three months ended March 31, 2026, our diluted adjusted weighted-average share count excluded the impact of approximately 78 ,000 shares related to certain performance-based awards that are earned based on the achievement of specified performance metrics, which were anti-dilutive to the weighted-average share count based on the performance measurement at March 31, 2026.

| 11. RELATED PARTY TRANSACTIONS | ||

Revenue—We have entered into agreements with the Managed Funds related to certain advisory, management, and administrative services we provide to their real estate assets in exchange for fees and reimbursement of certain expenses. Summarized below are amounts included in Fees and Management Income. The revenue includes the fees and reimbursements earned by us from the Managed Funds and other revenues that are not in the scope of ASC Topic 606, Revenue from Contracts with Customers, but that are included in this table for the purpose of disclosing all related party revenues (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

Recurring fees(1) | $ | $ | |||||||||

Transactional revenue and reimbursements(2) | |||||||||||

Insurance premiums(3) | |||||||||||

| Total fees and management income | $ | $ | |||||||||

(1)Recurring fees include asset management fees and property management fees.

(2)Transactional revenue includes items such as leasing commissions and construction management fees.

(3)Insurance premium income includes amounts for reinsurance from third parties not affiliated with us.

Tax Protection Agreement—Through our Operating Partnership, we are currently party to a tax protection agreement (the “2017 TPA”) with certain partners that contributed property to our Operating Partnership on October 4, 2017, among them certain of our executive officers, including Jeffrey S. Edison, our Chairman and Chief Executive Officer, under which the Operating Partnership agreed to indemnify such partners for tax liabilities that could accrue to them personally related to our potential disposition of certain properties within our portfolio. The 2017 TPA will expire on October 4, 2027. On July 19, 2021, we entered into an additional tax protection agreement (the “2021 TPA”) with certain of our executive officers and board members, including Mr. Edison. The 2021 TPA carries a term of four years and will become effective upon the expiration of the 2017 TPA. As of March 31, 2026, the potential “make-whole amount” on the estimated aggregate amount of built-in gain subject to protection under the agreements is approximately $113.3 million. The protection provided under the terms of the 2021 TPA will expire in 2031. We have not recorded any liability related to the 2017 TPA or the 2021 TPA on our consolidated balance sheets for any periods presented, nor recognized any expense since the inception of the 2017 TPA, owing to the fact that any potential liability under the agreements is controlled by us and we believe we will either (i) continue to own and operate the protected properties or (ii) be able to successfully complete tax-deferred exchanges under Section 1031 of the Internal Revenue Code of 1986, as amended (unless there is a change in applicable law) or complete other tax-efficient transactions to avoid any liability under the agreements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 14 | ||||||||||

Other Related Party Matters— As of March 31, 2026, we were the limited guarantor of $173.8 million, $102.7 million, and $31.7 million in mortgage loans secured by properties owned by GRP I, NRV, and NGCF, respectively. Our guaranties for the GRP I, NRV, and NGCF debt are limited to being the non-recourse carveout guarantor and the environmental indemnitor. Further, we are also party to agreements with each of GRP I, NRV, and NGCF, as applicable, in which any potential liability under such guaranties will be apportioned between us and GRP I, NRV, and NGCF based on our respective ownership percentages in the joint ventures. We had no liability recorded on our consolidated balance sheets for the guaranties as of March 31, 2026 and December 31, 2025.

| 12. FAIR VALUE MEASUREMENTS | ||

The following describes the methods we use to estimate the fair value of our financial and nonfinancial assets and liabilities:

Cash and Cash Equivalents, Restricted Cash, Accounts Receivable, and Accounts Payable—We consider the carrying values of these financial instruments to approximate fair value because of the short period of time between origination of the instruments and their expected realization.

Real Estate Investments—The purchase prices of the investment properties, including related lease intangible assets and liabilities, are allocated at estimated fair value based on Level 3 inputs, such as discount rates, capitalization rates, comparable sales, replacement costs, income and expense growth rates, and current market rents and allowances as determined by management.

Debt Obligations—We estimate the fair value of our revolving credit facility, term loans, secured portfolio of loans, and mortgages by discounting the future cash flows of each instrument at rates currently offered for similar debt instruments of comparable maturities by our lenders using Level 3 inputs. The discount rates used approximate current lending rates for loans or groups of loans with similar maturities and credit quality, assuming the debt is outstanding through maturity and considering the debt’s collateral (if applicable). We have utilized market information, as available, or present value techniques to estimate the amounts required to be disclosed. We estimate the fair value of our senior unsecured notes by using quoted prices in active markets, which are considered Level 1 inputs.

The following is a summary of borrowings as of March 31, 2026 and December 31, 2025 (in thousands):

| March 31, 2026 | December 31, 2025 | ||||||||||||||||||||||

Recorded Principal Balance(1) | Fair Value | Recorded Principal Balance(1) | Fair Value | ||||||||||||||||||||

| Revolving credit facility | $ | $ | $ | $ | |||||||||||||||||||

| Term loans | |||||||||||||||||||||||

| Senior unsecured notes due 2031 | |||||||||||||||||||||||

| Senior unsecured notes due 2032 | |||||||||||||||||||||||

| Senior unsecured notes due 2033 | |||||||||||||||||||||||

| Senior unsecured notes due 2034 | |||||||||||||||||||||||

| Senior unsecured notes due 2035 | |||||||||||||||||||||||

| Secured portfolio loan facilities | |||||||||||||||||||||||

Mortgages(2) | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(1)As of March 31, 2026 and December 31, 2025, respectively, recorded principal balances include: (i) net deferred financing fees of $2.0 million and $3.4 million; (ii) assumed market debt adjustments of $0.2 million and $0.3 million; and (iii) notes payable discounts of $26.5 million and $23.6 million.

Recurring and Nonrecurring Fair Value Measurements—Our marketable securities and interest rate swaps are measured and recognized at fair value on a recurring basis, while certain real estate assets and liabilities are measured and recognized at fair value as needed. Fair value measurements that occurred as of and during the three months ended March 31, 2026 and the year ended December 31, 2025 were as follows (in thousands):

| March 31, 2026 | December 31, 2025 | ||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Level 1 | Level 2 | Level 3 | ||||||||||||||||||

| Recurring | |||||||||||||||||||||||

Marketable securities(1) | $ | $ | $ | $ | $ | $ | |||||||||||||||||

Derivative assets(1)(2) | |||||||||||||||||||||||

(1)We record marketable securities and derivative assets in Other Assets, Net on our consolidated balance sheets.

(2)The fair values of the derivative assets exclude associated accrued interest receivable of $0.1

Marketable Securities—We estimate the fair value of marketable securities using Level 1 inputs. We utilize unadjusted quoted prices for identical assets in active markets that we have the ability to access.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 15 | ||||||||||

Derivative Instruments—As of March 31, 2026 and December 31, 2025, we had an interest rate swap that fixed SOFR on portions of our unsecured term loan and revolving credit facilities.

All interest rate swap agreements are measured at fair value on a recurring basis. The valuation of these instruments is determined using widely accepted valuation techniques, including discounted cash flow analysis on the expected cash flows of each derivative. This analysis reflects the contractual terms of the derivatives, including the period to maturity, and uses observable market-based inputs, including interest rate curves and implied volatilities. The fair values of interest rate swaps are determined using the market standard methodology of netting the discounted future fixed cash receipts (or payments) and the discounted expected variable cash payments (or receipts). The variable cash payments (or receipts) are based on an expectation of future interest rates (forward curves) derived from observable market interest rate curves.

To comply with the provisions of ASC Topic 820, Fair Value Measurement, we incorporate credit valuation adjustments to appropriately reflect both our own nonperformance risk and the respective counterparty’s nonperformance risk in the fair value measurements. In adjusting the fair value of our derivative contracts for the effect of nonperformance risk, we have considered the impact of netting and any applicable credit enhancements, such as collateral postings, thresholds, mutual puts, and guarantees.

Although we determined that the significant inputs used to value our derivatives fell within Level 2 of the fair value hierarchy, the credit valuation adjustments associated with our counterparties and our own credit risk utilize Level 3 inputs, such as estimates of current credit spreads, to evaluate the likelihood of default by us and our counterparties. However, as of March 31, 2026 and December 31, 2025, we have assessed the significance of the impact of the credit valuation adjustments on the overall valuation of our derivative positions and have determined that the credit valuation adjustments are not significant to the overall valuation of our derivatives. As a result, we have determined that our derivative valuations in their entirety are classified in Level 2 of the fair value hierarchy.

Real Estate Asset Impairment—Our real estate assets are measured and recognized at fair value, less costs to sell for held-for-sale properties, on a nonrecurring basis dependent upon when we determine an impairment has occurred. There were no

On a quarterly basis, we employ a multi-step approach to assess our real estate assets for possible impairment and record any impairment charges identified. The first step is the identification of potential triggering events, such as significant decreases in occupancy or the presence of large dark or vacant spaces. If we observe any of these indicators for a shopping center, we then perform an additional screen test consisting of a years-to-recover analysis to determine if we will recover the net book value of the property over its remaining economic life based upon net operating income (“NOI”) as forecasted for the current year. In the event that the results of this first step indicate a triggering event for a center, we proceed to the second step, utilizing an undiscounted cash flow model for the center to identify potential impairment. If the undiscounted cash flows are less than the net book value of the center as of the balance sheet date, we record an impairment charge based on the fair value determined in the third step. In performing the third step, we utilize market data such as capitalization rates and sales price per square foot on comparable recent real estate transactions to estimate the fair value of the real estate assets. We also utilize expected net sales proceeds to estimate the fair value of any centers that are actively being marketed for sale.

In addition to these procedures, we also review undeveloped or unimproved land parcels that we own for evidence of impairment and record any impairment charges as necessary. Primary impairment triggers for these land parcels are changes to our plans or intentions with regards to such properties, or planned dispositions at prices that are less than the current carrying values.

| 13. REPORTABLE SEGMENTS | ||

Our principal business is the ownership and operation of community and neighborhood shopping centers. We conduct our operations solely in the United States, and we do not distinguish our principal business, or group our operations, by geography or size for the purpose of measuring performance. We concluded that we have only one

Our Real Estate Properties segment derives a majority of its revenue from the lease contracts it enters into as a lessor, which are all in the form of operating leases. Further, our lease contracts typically provide for reimbursements from tenants for common area maintenance, insurance, and real estate tax expense. No single tenant comprised 10% or more of our aggregate ABR for the three months ended March 31, 2026 and 2025.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 16 | ||||||||||

Our CODM is Mr. Edison, our Chairman and Chief Executive Officer. Our CODM assesses performance, makes decisions, and allocates operating and capital resources of the Real Estate Properties segment by utilizing net income (loss) on a consolidated basis. Our CODM evaluates net income (loss) by monitoring budget versus actual as well as variance analysis to prior periods to analyze the performance of the segment. Information about the net income (loss) of the Real Estate Properties segment that is regularly reviewed by our CODM, including revenue and significant expenses, was as follows for the three months ended March 31, 2026 and 2025 (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| Revenues: | |||||||||||

| Rental income | $ | $ | |||||||||

| Fees and management income | |||||||||||

| Other property income | |||||||||||

| Total revenues | |||||||||||

| Operating Expenses: | |||||||||||

Property operating(1) | |||||||||||

| Real estate taxes | |||||||||||

| Employee-related expenses | |||||||||||

Other general and administrative expenses(2) | |||||||||||

| Depreciation and amortization | |||||||||||

| Total operating expenses | |||||||||||

| Other: | |||||||||||

Interest expense, net(3) | ( | ( | |||||||||

| Gain on disposal of property, net | |||||||||||

| Other expense, net | ( | ( | |||||||||

| Net income | |||||||||||

| Net income attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to stockholders | $ | $ | |||||||||

(1)Property operating is primarily made up of common area maintenance, compensation, insurance, and other costs related to the leasing of our real estate properties. Our CODM is not provided with further disaggregation and uses total property operating expenses to manage the business.

(2)Other general and administrative expenses is primarily made up of professional fees, technology and communication expense, and insurance, taxes, and board costs.

(3)Interest income is not a significant component of Interest Expense, Net.

The measure of segment assets regularly reviewed by our CODM is reported on the consolidated balance sheets as Total Assets.

| 14. SUBSEQUENT EVENTS | ||

In preparing the condensed and unaudited consolidated financial statements, we have evaluated subsequent events through the date of filing of this report on Form 10-Q for recognition and/or disclosure purposes. Based on this evaluation, we have determined that there were no events that have occurred that require recognition or disclosure, other than certain events and transactions that have been disclosed elsewhere in these consolidated financial statements.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 17 | ||||||||||

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis should be read in conjunction with our accompanying consolidated financial statements and notes thereto and the more detailed information contained in our 2025 Annual Report on Form 10-K, filed with the SEC on February 10, 2026. All references to “Notes” throughout this document refer to the footnotes to the consolidated financial statements in “Item 1. Financial Statements”. See also “Cautionary Note Regarding Forward-Looking Statements” below.

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | ||

Certain statements contained in this Quarterly Report on Form 10-Q of Phillips Edison & Company, Inc. (“we,” the “Company,” “our,” or “us”) other than historical facts may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995 (collectively with the Securities Act and the Exchange Act, the “Acts”). These forward-looking statements are based on current expectations, estimates, and projections about the industry and markets in which we operate, and beliefs of, and assumptions made by, management of our company and involve uncertainties that could significantly affect our financial results. We intend for all such forward-looking statements to be covered by the applicable safe harbor provisions for forward-looking statements contained in the Acts. Such forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” “seek,” “objective,” “goal,” “strategy,” “plan,” “focus,” “priority,” “should,” “could,” “potential,” “possible,” “look forward,” “optimistic”, “commit,” or other similar words. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date this report is filed with the SEC. Such statements include, but are not limited to: (a) statements about our plans, strategies, initiatives, and prospects; (b) statements about our underwritten incremental yields; and (c) statements about our future results of operations, capital expenditures, and liquidity. Such statements are subject to known and unknown risks and uncertainties, which could cause actual results to differ materially from those projected or anticipated, including, without limitation: (i) changes in national, regional, or local economic climates; (ii) local market conditions, including an oversupply of space in, or a reduction in demand for, properties similar to those in our portfolio; (iii) vacancies, changes in market rental rates, and the need to periodically repair, renovate, and re-let space; (iv) competition from other available shopping centers and the attractiveness of properties in our portfolio to our tenants; (v) the financial stability of our tenants, including, without limitation, their ability to pay rent; (vi) our ability to pay down, refinance, restructure, or extend our indebtedness as it becomes due; (vii) increases in our borrowing costs as a result of changes in interest rates and other factors; (viii) potential liability for environmental matters; (ix) damage to our properties from catastrophic weather and other natural events, and the physical effects of climate change; (x) our ability and willingness to maintain our qualification as a REIT in light of economic, market, legal, tax, and other considerations; (xi) changes in tax, real estate, environmental, and zoning laws; (xii) information technology security breaches; (xiii) our corporate responsibility initiatives; (xiv) loss of key executives; (xv) the concentration of our portfolio in a limited number of industries, geographies, or investments; (xvi) the economic, political, and social impact of, and uncertainty relating to, pandemics or other health crises; (xvii) our ability to re-lease our properties on the same or better terms, or at all, in the event of non-renewal or in the event we exercise our right to replace an existing tenant; (xviii) the loss or bankruptcy of our tenants; (xix) to the extent we are seeking to dispose of properties, our ability to do so at attractive prices or at all; and (xx) the impact of heightened geopolitical instability, international conflicts, tariffs, and global trade disruptions on us, our tenants, and consumers, including the impact on inflation, supply chains, and consumer sentiment. Additional important factors that could cause actual results to differ are described in the filings made from time to time by the Company with the SEC and include the risk factors and other risks and uncertainties described in our 2025 Annual Report on Form 10-K, filed with the SEC on February 10, 2026, as updated from time to time in our periodic and/or current reports filed with the SEC, which are accessible on the SEC’s website at www.sec.gov. Therefore, such statements are not intended to be a guarantee of our performance in future periods.

Except as required by law, we do not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events, or otherwise.

KEY PERFORMANCE INDICATORS AND DEFINED TERMS | ||

We use certain key performance indicators (“KPIs”), which include both financial and nonfinancial metrics, to measure the performance of our operations. We believe these KPIs, as well as the core concepts and terms defined below, allow our Board, management, and investors to analyze trends around our business strategy, financial condition, and results of operations in a manner that is focused on items unique to the retail real estate industry.

We do not consider our non-GAAP measures to be alternatives to measures required in accordance with GAAP. Certain non-GAAP measures should not be viewed as an alternative measure of our financial performance as they may not reflect the operations of our entire portfolio, and they may not reflect the impact of general and administrative expenses, depreciation and amortization, interest expense, other income (expense), or the level of capital expenditures and leasing costs necessary to maintain the operating performance of our shopping centers that could materially impact our results from operations. Additionally, certain non-GAAP measures should not be considered as an indication of our liquidity, nor as an indication of funds available to cover our cash needs, including our ability to fund distributions, and may not be a useful measure of the impact of long-term operating performance on value if we do not continue to operate our business in the manner currently contemplated. Accordingly, non-GAAP measures should be reviewed in connection with other GAAP measurements and should not be viewed as more prominent measures of performance than net income (loss) or cash flows from operations prepared in accordance with GAAP. Other REITs may use different methodologies for calculating similar non-GAAP measures, and accordingly, our non-GAAP measures may not be comparable to other REITs.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 18 | ||||||||||

Our KPIs and terminology can be grouped into three key areas:

PORTFOLIO—Portfolio metrics help management to gauge the health of our centers overall and individually.

•Anchor space—We define an anchor space as a space greater than or equal to 10,000 square feet of gross leasable area (“GLA”).

•ABR—We use ABR to refer to the monthly contractual base rent at the end of the period multiplied by twelve months.

•ABR Per Square Foot (“PSF”)—This metric is calculated by dividing ABR by leased GLA. Increases in ABR PSF can be an indication of our ability to create rental rate growth in our centers, as well as an indication of demand for our spaces, which generally provides us with greater leverage during lease negotiations.

•GLA—We use GLA to refer to the total occupied and unoccupied square footage of a building that is available for tenants (whom we refer to as a “Neighbor” or our “Neighbors”) or other retailers to lease.

•Inline space—We define an inline space as a space containing less than 10,000 square feet of GLA.

•Leased Occupancy—This metric is calculated as the percentage of total GLA for which a lease has been signed regardless of whether the lease has commenced or the Neighbor has taken possession. High occupancy is an indicator of demand for our spaces, which generally provides us with greater leverage during lease negotiations.

•Underwritten incremental unlevered yield—This reflects the yield we target to generate from a project upon expected stabilization and is calculated as the estimated incremental NOI for a project at stabilization divided by its estimated net project investment. The estimated incremental NOI is the difference between the estimated annualized NOI we target to generate by a project upon stabilization and the estimated annualized NOI without the planned improvements. Underwritten incremental unlevered yield does not include peripheral impacts, such as lease rollover risk or the impact on the long-term value of the property upon sale or disposition. Actual incremental unlevered yields may vary from our underwritten incremental unlevered yield range based on the actual total cost to complete a project and its actual incremental NOI at stabilization.

LEASING—Leasing is a key driver of growth for our company.

•Comparable lease—We use this term to refer to a lease with consistent terms that is executed for substantially the same space that has been vacant less than twelve months.

•Comparable rent spread—This metric is calculated as the percentage increase or decrease in first-year ABR (excluding any free rent or escalations) on new or renewal leases (excluding options) where the lease was considered a comparable lease. This metric provides an indication of our ability to generate revenue growth through leasing activity.

•Cost of executing new leases—We use this term to refer to certain costs associated with new leasing, namely, leasing commissions, tenant improvement costs, and tenant concessions.

•Portfolio retention rate—This metric is calculated by dividing (i) the total square feet of retained Neighbors with current period lease expirations by (ii) the total square feet of leases expiring during the period. The portfolio retention rate provides insight into our ability to retain Neighbors at our shopping centers as their leases approach expiration. Generally, the costs to retain an existing Neighbor are lower than costs to replace with a new Neighbor.

•Recovery rate—This metric is calculated by dividing (i) total recovery income by (ii) total recoverable expenses during the period. A high recovery rate is an indicator of our ability to recover certain property operating expenses and capital costs from our Neighbors.

FINANCIAL PERFORMANCE—In addition to financial metrics calculated in accordance with GAAP, such as net income or cash flows from operations, we utilize non-GAAP metrics to measure our operational and financial performance. See “Non-GAAP Measures” below for further discussion on the following metrics.

•Adjusted Earnings Before Interest, Taxes, Depreciation, and Amortization for Real Estate (“Adjusted EBITDAre”)—To arrive at Adjusted EBITDAre, we adjust EBITDAre, as defined below, to exclude certain recurring and non-recurring items including, but not limited to: (i) changes in the fair value of the earn-out liability; (ii) other impairment charges; (iii) adjustments related to our investments in unconsolidated joint ventures; (iv) transaction and acquisition expenses; and (v) realized performance income. We use EBITDAre and Adjusted EBITDAre as additional measures of operating performance which allow us to compare earnings independent of capital structure and evaluate debt leverage and fixed cost coverage.

•Core Funds From Operations Attributable to Stockholders and OP Unit Holders (“Core FFO”)—To arrive at Core FFO, we adjust Nareit FFO, as defined below, to exclude certain recurring and non-recurring items including, but not limited to: (i) depreciation and amortization of corporate assets; (ii) changes in the fair value of the earn-out liability; (iii) adjustments related to our investments in unconsolidated joint ventures; (iv) gains or losses on the extinguishment or modification of debt and other; (v) other impairment charges; (vi) transaction and acquisition expenses; and (vii) realized performance income. We believe Nareit FFO provides insight into our operating performance as it excludes certain items that are not indicative of such performance. Core FFO provides further insight into the sustainability of our operating performance and provides an additional measure to compare our performance across reporting periods on a consistent basis by excluding items that may cause short-term fluctuations in net income (loss).

•EBITDAre—The National Association of Real Estate Investment Trusts (“Nareit”) defines EBITDAre as net income (loss) computed in accordance with GAAP before: (i) interest expense; (ii) income tax expense; (iii) depreciation and amortization; (iv) gains or losses from disposition of depreciable property; and (v) impairment write-downs of

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 19 | ||||||||||

depreciable property. Adjustments for unconsolidated partnerships and joint ventures are calculated to reflect EBITDAre on the same basis.

•Equity Market Capitalization—We calculate equity market capitalization as the total dollar value of all outstanding shares and OP Units using the closing price for the applicable date.

•Nareit FFO Attributable to Stockholders and OP Unit Holders (“Nareit FFO”)—Nareit defines Funds From Operations (“FFO”) as net income (loss) computed in accordance with GAAP, excluding: (i) gains (or losses) from sales of property and gains (or losses) from change in control; (ii) depreciation and amortization related to real estate; (iii) impairment losses on real estate and impairments of in-substance real estate investments in investees that are driven by measurable decreases in the fair value of the depreciable real estate held by the unconsolidated partnerships and joint ventures; and (iv) adjustments for unconsolidated partnerships and joint ventures, calculated to reflect FFO on the same basis. We calculate Nareit FFO in a manner consistent with the Nareit definition.

•Net Debt—We calculate net debt as total debt, excluding discounts, market adjustments, and deferred financing expenses, less cash and cash equivalents.

•Net Debt to Adjusted EBITDAre—This ratio is calculated by dividing net debt by Adjusted EBITDAre (included on an annualized basis within the calculation). It provides insight into our leverage rate based on earnings and is not impacted by fluctuations in our equity price.

•Net Debt to Total Enterprise Value—This ratio is calculated by dividing net debt by total enterprise value, as defined below. It provides insight into our capital structure and usage of debt.

•NOI—We calculate NOI as total operating revenues, adjusted to exclude non-cash revenue items and lease buyout income, less property operating expenses and real estate taxes. NOI provides insight about our financial and operating performance because it provides a performance measure of the revenues and expenses directly involved in owning and operating real estate assets and provides a perspective not immediately apparent from net income (loss).

•Same-Center—We use this term to refer to a property, or portfolio of properties, owned for the entirety of both calendar year periods being compared.

•Total Enterprise Value—We calculate total enterprise value as our net debt plus our equity market capitalization on a fully diluted basis.

| OVERVIEW | ||

We are a REIT and one of the nation’s largest owners and operators of omni-channel grocery-anchored shopping centers. Our portfolio primarily consists of neighborhood centers anchored by the #1 or #2 grocer tenants by sales within their respective formats by trade area. Our Neighbors are a mix of national, regional, and local retailers that primarily provide necessity-based goods and services.

As of March 31, 2026, we owned equity interests in 326 shopping centers, including 299 wholly-owned shopping centers and 27 shopping centers owned through three unconsolidated joint ventures, which comprised approximately 36.9 million square feet in 31 states. In addition to managing our shopping centers, our third-party investment management business provides comprehensive real estate management services to the Managed Funds.

PORTFOLIO AND LEASING STATISTICS—Below are statistical highlights of our wholly-owned portfolio as of March 31, 2026 and 2025 (dollars and square feet in thousands):

| March 31, 2026 | March 31, 2025 | ||||||||||

| Number of properties | 299 | 298 | |||||||||

| Number of states | 31 | 31 | |||||||||

| Total square feet | 33,669 | 33,512 | |||||||||

| ABR | $ | 548,490 | $ | 518,115 | |||||||

| % ABR from omni-channel grocery-anchored shopping centers | 94.3 | % | 95.3 | % | |||||||

| % ABR from necessity-based goods and services | 74.3 | % | 70.6 | % | |||||||

| Leased occupancy %: | |||||||||||

| Total portfolio spaces | 97.1 | % | 97.1 | % | |||||||

| Anchor spaces | 98.4 | % | 98.4 | % | |||||||

| Inline spaces | 95.0 | % | 94.6 | % | |||||||

Average remaining lease term (in years)(1) | 4.6 | 4.5 | |||||||||

(1)The average remaining lease term in years excludes future options to extend the term of the lease.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 20 | ||||||||||

The following table details information for our unconsolidated joint ventures as of March 31, 2026, which is the basis for determining the prorated information included in the subsequent tables (dollars and square feet in thousands):

| March 31, 2026 | |||||||||||||||||||||||

| Joint Venture | Ownership Percentage | Number of Properties | ABR | GLA | |||||||||||||||||||

| GRP I | 14% | 20 | $ | 33,917 | 2,221 | ||||||||||||||||||

| NRV | 20% | 4 | 12,845 | 744 | |||||||||||||||||||

| NGCF | 31% | 3 | 4,315 | 225 | |||||||||||||||||||

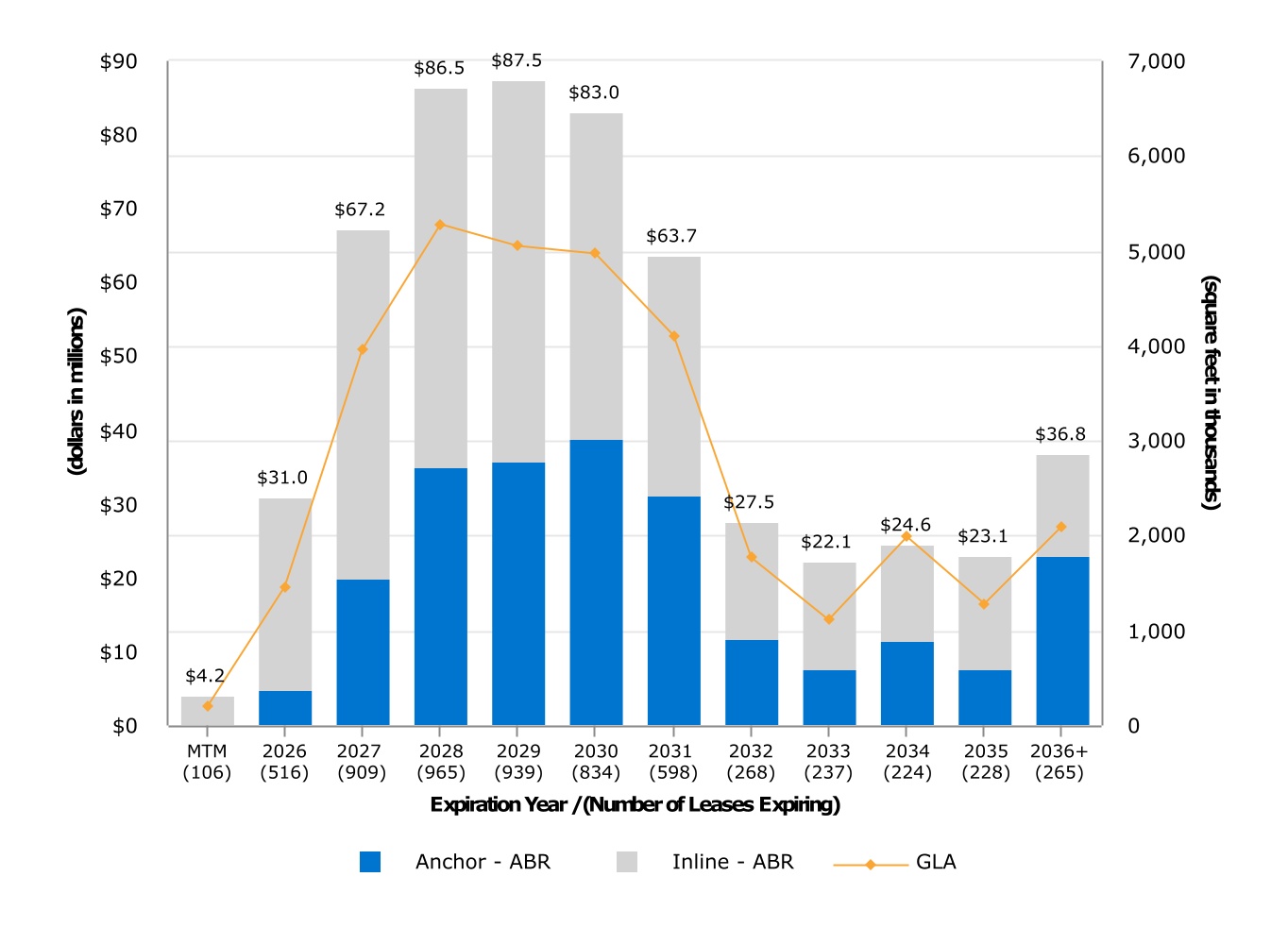

LEASE EXPIRATIONS—The following chart shows the aggregate scheduled lease expirations for our over 3,500 unique Neighbors, excluding our Neighbors who are occupying space on a temporary basis, after March 31, 2026 for each of the next ten years and thereafter for our wholly-owned properties and the prorated portion of those owned through our unconsolidated joint ventures:

Our ability to create rental rate growth generally depends on our leverage during new and renewal lease negotiations with prospective and existing Neighbors, which typically occurs when occupancy at our centers is high or during periods of economic growth and recovery. Conversely, we may experience rental rate decline when occupancy at our centers is low or during periods of economic recession, as the leverage during new and renewal lease negotiations may shift to prospective and existing Neighbors.

See “Results of Operations - Leasing Activity” below for further discussion of leasing activity.

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 21 | ||||||||||

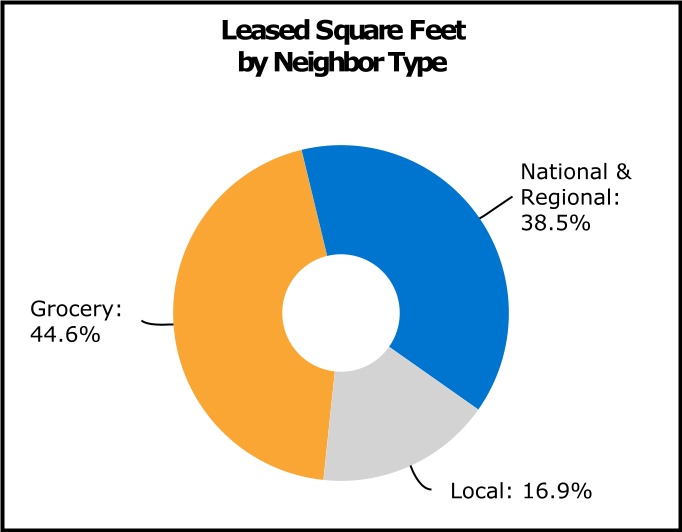

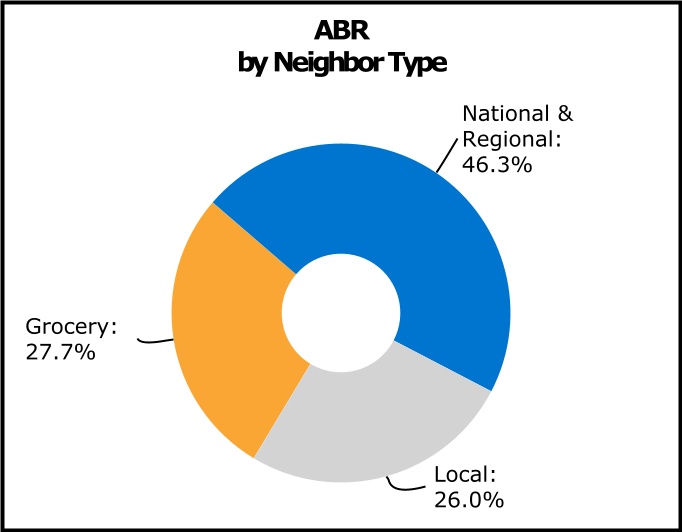

PORTFOLIO TENANCY—We define national Neighbors as those Neighbors that operate in at least three states. Regional Neighbors are defined as those Neighbors that have at least three locations in fewer than three states. The following charts present the composition of our portfolio, including our wholly-owned properties and the prorated portion of those owned through our unconsolidated joint ventures, by Neighbor type as of March 31, 2026:

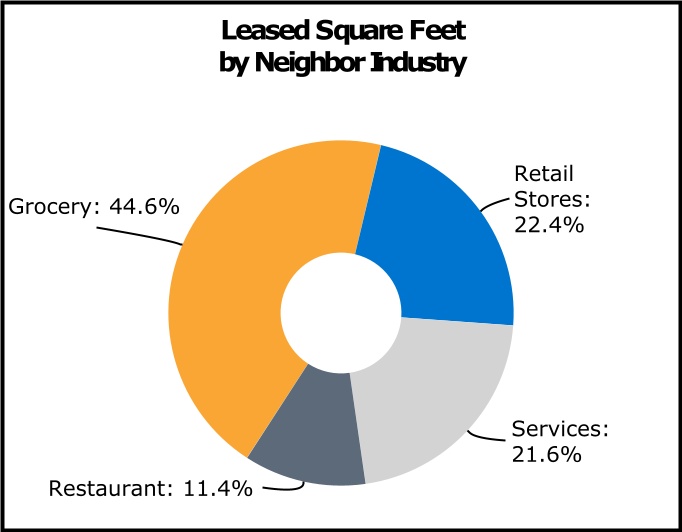

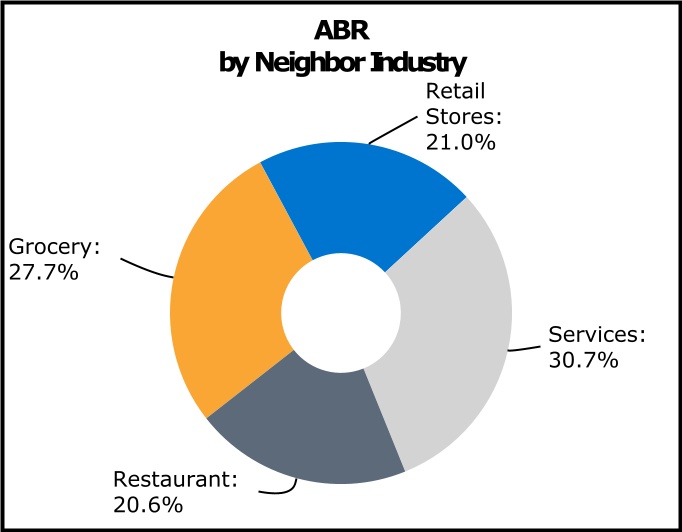

The following charts present the composition of our portfolio by Neighbor industry as of March 31, 2026:

PHILLIPS EDISON & COMPANY MARCH 31, 2026 FORM 10-Q | 22 | ||||||||||

NECESSITY-BASED GOODS AND SERVICES—We define “necessity-based goods and services” as goods and services that are indispensable, necessary, or common for day-to-day living, or that tend to be inelastic (i.e., those for which the demand does not change based on a consumer’s income level). We estimate that approximately 74% of our ABR, including the pro rata portion attributable to properties owned through our unconsolidated joint ventures, is generated from Neighbors providing necessity-based goods and services.

TOP 20 NEIGHBORS—The following table presents our top 20 Neighbors by ABR, including our wholly-owned properties and the prorated portion of those owned through our unconsolidated joint ventures, as of March 31, 2026 (dollars and square feet in thousands):

Neighbor(1) | ABR | % of ABR | Leased Square Feet | % of Leased Square Feet | Number of Locations(2) | ||||||||||||||||||||||||

| Kroger | $ | 28,409 | 5.1 | % | 3,475 | 10.5 | % | 63 | |||||||||||||||||||||

| Publix | 27,838 | 5.0 | % | 2,530 | 7.6 | % | 62 | ||||||||||||||||||||||

| Albertsons | 19,088 | 3.4 | % | 1,683 | 5.1 | % | 30 | ||||||||||||||||||||||

| Ahold Delhaize | 17,215 | 3.1 | % | 1,184 | 3.6 | % | 22 | ||||||||||||||||||||||

| Walmart | 8,483 | 1.5 | % | 1,733 | 5.2 | % | 12 | ||||||||||||||||||||||

| TJX Companies | 7,517 | 1.3 | % | 605 | 1.8 | % | 21 | ||||||||||||||||||||||

| Giant Eagle | 7,437 | 1.3 | % | 759 | 2.3 | % | 10 | ||||||||||||||||||||||

| Sprouts Farmers Market | 6,725 | 1.2 | % | 411 | 1.2 | % | 14 | ||||||||||||||||||||||

| Raley's | 4,708 | 0.8 | % | 288 | 0.9 | % | 5 | ||||||||||||||||||||||

| Dollar Tree | 4,521 | 0.8 | % | 399 | 1.2 | % | 39 | ||||||||||||||||||||||

| Planet Fitness | 3,951 | 0.7 | % | 315 | 0.9 | % | 16 | ||||||||||||||||||||||

| Starbucks Corporation | 3,912 | 0.7 | % | 82 | 0.2 | % | 42 | ||||||||||||||||||||||

| Big Y | 3,540 | 0.6 | % | 167 | 0.5 | % | 3 | ||||||||||||||||||||||

| UNFI (SuperValu) | 3,500 | 0.6 | % | 336 | 1.0 | % | 5 | ||||||||||||||||||||||

| United Parcel Service | 3,204 | 0.6 | % | 105 | 0.3 | % | 84 | ||||||||||||||||||||||

| Subway Group | 3,015 | 0.6 | % | 96 | 0.3 | % | 66 | ||||||||||||||||||||||

| Pet Supplies Plus | 3,014 | 0.5 | % | 185 | 0.6 | % | 24 | ||||||||||||||||||||||

| Great Clips | 2,863 | 0.5 | % | 94 | 0.3 | % | 83 | ||||||||||||||||||||||

| Trader Joe's | 2,860 | 0.5 | % | 122 | 0.4 | % | 9 | ||||||||||||||||||||||

| H&R Block | 2,773 | 0.5 | % | 99 | 0.3 | % | 59 | ||||||||||||||||||||||

| Total | $ | 164,573 | 29.3 | % | 14,668 | 44.2 | % | 669 | |||||||||||||||||||||

(1)Neighbors are grouped by parent company and may represent multiple subsidiaries and banners.

(2)Number of locations excludes auxiliary leases with grocery anchors such as fuel stations, pharmacies, and liquor stores. Additionally, if a parent company has multiple subsidiaries or banners in a single shopping center, those subsidiaries are included as one location.

| RESULTS OF OPERATIONS | ||