Apr. 30, 2026

Langar Global HealthTech ETF (the “Fund”) seeks long-term growth of capital.

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund (“Shares”). Investors purchasing or selling Shares in the secondary market may be subject to costs (including customary brokerage commissions) charged by their broker. These costs are not included in the expense example below.

| Annual Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investment) | |

| Management Fees | 0.85% |

| Other Expenses | 0.00% |

| Total Annual Fund Operating Expenses | 0.85% |

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell (or you hold) all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

| $87 |

$271 |

$471 |

$1,049 |

The Fund may pay transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or in the Example, affect the Fund’s performance. For the most recent fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was 51.92% of the average value of its portfolio.

As an actively managed exchange-traded fund (“ETF”), the Fund will not

seek to replicate the performance of an index. The Fund intends to achieve its investment objective by investing a majority of its net assets in U.S. and foreign exchange-listed healthcare technology companies in the U.S and a number of

developed countries around the world. Under normal circumstances, the Fund will invest at least 80% of the Fund’s net assets (plus borrowings for investment purposes) in U.S. and foreign exchange-listed equity

securities of healthcare technology companies and American Depository Receipts (“ADRs”) on those securities. These securities may be of any market capitalization.

Langar Investment Management, LLC (the “Advisor”) uses a combination of a top-down review and a bottom-up research methodology to

select fundamentally strong companies that develop technology to create efficiency in healthcare by addressing key pain points for patients, providers, payors, and/or hospitals. The Advisor defines pain points as consistent

problems that a patient, provider and/or other healthcare stakeholder has when dealing with a product and/or service, which are unmet needs that are not adequately addressed for a company to solve in the market. These companies are generally in

one of the nine subsectors described below and may include robotic surgery companies, virtual and/or telemedicine companies, companies that develop next-generation insurance payment models, drug development companies leveraging artificial

intelligence (AI), digital clinical trial companies, companies that address operational issues within a hospital, and companies that leverage large language model (LLM) AI to develop next best recommendation engines to improve/facilitate the

intake, monitoring, and treatment of a patient. The Advisor’s selection process has four main steps (as further described below): 1) Langar’s HealthTech classification; 2) Langar Rating™; 3) Langar’s HealthTech Industry Risk Score;

and 4) Investment Committee review.

Langar’s HealthTech Classification

The Advisor starts by recategorizing public companies in the healthcare industry as defined by the Standard & Poor’s Global

Industry Classification Standard (“GICS”) to determine the companies that fit into the Advisor’s definition of a HealthTech company. The Advisor defines a “HealthTech Company” as a company that: i) develops technology to create efficiencies in

healthcare by addressing key pain points of patients, providers, payors and/or hospitals; and ii) receives a majority of its revenue from HealthTech products and/or services as reported through filings with the SEC. HealthTech companies can be

grouped into nine subsectors:

Public HealthTech subsector definitions:

|

•

|

Access to Care – Provide care outside of a hospital setting through virtual, in-person, or a hybrid care combination.

|

|

•

|

Biopharma – Pharmaceutical and biotechnology companies that use artificial intelligence/machine learning (“AI/ML”) technologies as an integral

part of their drug design or development process.

|

|

•

|

Clinical Trials – Enables the efficient deployment, tracking and/or completion of trials that support novel medications and/or treatments.

|

|

•

|

Decision Support – Provides clinicians with patient-specific information, which is intelligently filtered or presented at appropriate times to

enhance care.

|

|

•

|

Hospital Operations – Improves the efficiency of hospital workflows that are required to provide care.

|

|

•

|

Insurance – Leverage AI/ML models to save costs and improve services of private and/or government programs.

|

|

•

|

Treatment Device – Devices that leverage an AI/ML algorithm to facilitate treatment of a specific medical problem.

|

Private HealthTech subsector definitions:

|

•

|

Lifestyle Wellness – Assists users in navigating their overall health and wellness journey using monitoring, counseling, education, and

lifestyle changes that help prevent, treat, and provide care.

|

|

•

|

Prescription Management – Ensures a patient is properly educated, has access to and complies with prescribed usage of a

medication.

|

Langar Rating™

Companies that meet the Advisor’s definition of a HealthTech Company are then screened using the Langar Rating™. The Langar

Rating™ is a proprietary metric developed by Langar Holdings, Inc. that helps assess a company’s fundamentals relative to its peers by reviewing press releases, publicly available filings, and third-party data analysis. The metric includes an

active assessment of the qualitative and quantitative strength of the company’s business fundamentals through a review of the company’s financial health, any relevant company controversies, whether the company’s products and/or services are

involved in any vice areas, as defined by the Advisor (adult entertainment, alcoholic beverages, oil and gas exploration, cannabis, weapons/small arms, fur and specialty leathers, gambling, predatory lending, riot control, tobacco products and

whale meat), and the strength of the company’s team (i.e., board of directors and management team) and culture (shared values, attitudes, behaviors, and standards that make up a company’s work environment as it relates to a company’s investment

potential) (derived from a subset of Refinitiv’s Environmental, Social, and Governance database). The purpose of the vice screen is to help identify and remove from the potential universe any companies that have and/or could have performance

challenges as a result of controversies and adverse public sentiment regarding their products and/or services or overall company reputation.

Langar’s HealthTech Industry Risk Score

The Advisor then applies the Langar Industry Risk Score™ to assign an industry risk score to each company. The proprietary

algorithm evaluates the healthcare industry risk of the company by defining a quantitative risk and qualitative risk category for each company and weights the company accordingly. The quantitative risk category includes revenue risk (which is

defined as which customer segment contributes to a majority of the company’s revenue) and innovation risk (which evaluates how well a company has protected its intellectual property and whether they are able to generate a gross profit). The

qualitative risk category includes standard of care risk (which analyzes whether a company’s product and/or service has aligned with current clinical practices), and policy risk (which determines if the company’s product and/or service is subject

to state and/or federal policy shifts). The Advisor applies weighting to the portfolio based on the market cap and revenue growth to place more weight on high growth potential companies.

Investment Committee Review

Finally, each company is then reviewed by the Advisor’s Investment Committee, which includes a seasoned team of healthcare and

financial subject matter experts and provides input on the companies presented before the portfolio manager selects the companies to be included in the Fund’s portfolio. However, the Fund’s portfolio manager has complete discretion

over the companies ultimately selected for inclusion in the Fund’s portfolio.

On at least a quarterly basis, the Advisor may rebalance the portfolio to add new securities that meet the criteria discussed

above, change the weighting of securities or remove securities that no longer meet the criteria discussed above. The Advisor may sell securities at any time if the Advisor believes that the company has made a business decision that will negatively

impact its long-term growth.

The Fund is classified as “non-diversified” for purposes of the Investment Company Act of 1940, as amended (the “1940 Act”),

which means a relatively high percentage of the Fund’s assets may be invested in the securities of a limited number of issuers. The Fund will also be concentrated (invest at least 25% of the Fund’s assets) in companies in healthcare industry as

defined by GICS.

As an actively managed ETF that does not seek to replicate the performance of a specified index, the Fund may have a higher

degree of portfolio turnover than funds that seek to replicate the performance of an index.

From time to time the Fund may focus its investments in one or more particular sectors. As of December 31, 2025, the Fund

focused its investments in the medical equipment sector.

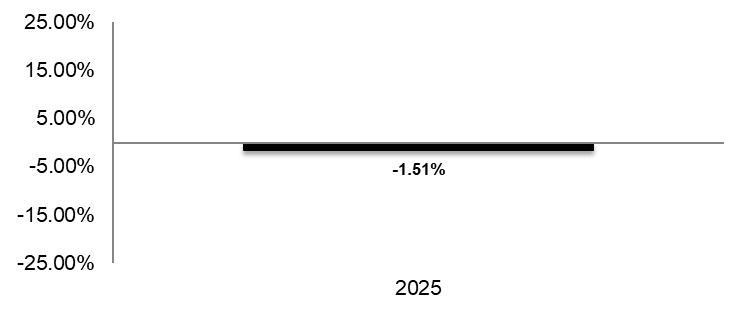

The following bar chart and table provide an indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year and by showing how the average annual total returns compared to that of a broad-based securities market index and a style-specific index (one reflecting the market segments in which the Fund invests). The Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Updated performance information on the Fund’s results can be obtained by visiting www.langarfunds.com.

During the periods shown in the bar chart above, the Fund’s highest quarterly return was 6.97% (quarter ended June 30,2025) and the Fund’s lowest quarterly return was -3.82% (quarter ended September 30, 2025).

| Average Annual Total Returns Period Ended December 31, 2025 | Past 1 Year | Since Inception1 |

| Before taxes | -1.51% | -0.07% |

| After taxes on distributions | -1.51% | -0.07% |

| After taxes on distributions and sale of shares | -0.90% | -0.05% |

| S&P 500 Index (reflects no deductions for fees and expenses) | 17.88% | 21.81% |

| S&P 500 Health Care Index (reflects no deductions for fees and expenses) | 14.60% | 6.91% |

1 The Fund commenced operations on January 9, 2024.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown and are not applicable to investors who hold Shares through tax-deferred arrangements such as a 401(k) plan or an individual retirement account (IRA).