Investment Strategy

Apr. 30, 2026

purposes) in (1) U.S. and non-U.S. fixed income securities; and (2) exchange-traded funds and derivatives instruments that provide

long and short exposure to U.S. and non-U.S. fixed income securities. The Fund focuses on lower-quality, higher-yielding securities

across a wide range of investable asset classes using both long and short exposures. The Fund will gain exposure to fixed income

securities primarily by investing in one or more of the following investment types:

•Other exchange-traded funds (“ETFs”);

•Individual bonds (or baskets of bonds);

•Bond futures; and

•Credit default swaps, credit default index swaps, and options on such instruments.

The Fund will typically seek exposure among a wide range of fixed income segments, including the following:

Lower Grade Fixed Income

•High-yield corporate bonds

•Leveraged loans, senior loans and bank loans

•Convertible bonds

Higher Grade Fixed Income

•Investment-grade corporate bonds

•Asset-backed securities, including mortgage-related securities and mortgage-backed securities

•U.S. Treasury securities

Peripheral Asset Classes

•Emerging market bonds

•Publicly-traded Business Development Companies (“BDCs”)

•High dividend equity securities

The Fund is designed to provide an actively-managed solution across various sectors of fixed income using Kensington’s investment

process. The Fund will generally feature a blended portfolio that increases or decreases exposure across target asset classes. The Fund

may use both long or short exposures to manage duration and credit risk through a two-step process that involves quantitative analysis

on different aspects of fixed income investing, as well as risk management.

The Fund’s quantitative analysis process incorporates four distinct categories: Trends, Valuation, Macro Environment, and Pricing and

Flow Anomalies, using a quantitative approach with the following rationales:

Trends | The trend-following component of the Fund utilizes numerous inputs, such as par weighted index price, yields, total return index, and credit spreads. For each input, features are generated across long, medium, and short timeframes to obtain a final trend signal. The objective is to capture the essence of trends as they occur. Frequent changes are to be expected but other process components seek to mitigate this volatility. | |

Valuation | This component is an inherently counter-trend or contrarian framework designed to complement trend- following. This aspect of the process is designed to identify areas of relatively “cheap” versus “expensive” valuations, based on historical data. This component is designed to allow the Fund to be more risk-conscious when valuations are overpriced and to identify possible counter-trend buying opportunities when valuations are at extreme historical lows. | |

Macro Environment | This analysis considers factors from different asset classes, such as equities and commodities. The portfolio managers believe that including a “macro-aware” framework can potentially improve allocation guidance and risk-adjusted performance. For example, rising commodity, government bond, and equity prices typically show strong or improving economic growth, whereas falling bond and equity prices but rising commodity prices could be an indicator of a “stagflationary” regime. | |

Pricing and Flow Anomalies | Investor timing and behavior can lead to trading anomalies that produce regular periods of lower or higher- than-average expected returns. Kensington’s quantitative process is designed to identify these periods, and plays a role in determining asset allocation when combined with the other indicator subsets. |

After using these analyses to generate forecasts of expected future performance for asset classes, quantitative portfolio optimization

techniques that weigh forecasts of expected future performance and risk given real life constraints like turnover, transaction costs and

slippage are applied to obtain asset class allocations in the portfolio.

Shorting / Inverse Position: In addition to these four categories, the Fund’s quantitative model contains signals to short exposures

primarily in two asset classes: U.S. Treasuries and U.S. high-yield bonds. Shorting will be typically achieved through the usage of

futures contracts for U.S. Treasuries. For U.S. high-yield bonds, the Fund may short ETFs, purchase credit default swaps or utilize

other derivatives, such as options and futures. The Fund may also gain short exposure through the use of inverse ETFs, which are

ETFs that generally seek to provide investment results that are the inverse of the performance of an underlying index or other asset.

The Fund is flexible and not managed to a benchmark. The Fund may shift its allocations based on changing market conditions, which

may result in investing in a single or multiple markets and sectors. The Fund has broad flexibility to invest in a wide variety of debt

securities and instruments of any maturity. The Fund may invest in fixed and floating rate debt securities issued in both U.S. and

foreign markets, including countries whose economies are less developed (emerging markets). The Fund has discretion to focus its

investments in one or more regions or small groups of countries including both U.S. and foreign markets including emerging markets.

The Fund invests primarily in U.S. dollar denominated securities, although the Fund may also invest in non-dollar denominated

securities. The fixed-income securities to which the Fund may have exposure are not restricted as to issuer credit quality, country,

capitalization, security maturity, currency, or leverage.

The Fund will typically have significant exposure to high-yield securities, which are debt instruments rated lower than Baa3 by

Moody’s Ratings (“Moody’s”) or lower than BBB- by Standard and Poor’s Rating Group (“S&P”), or, if unrated, determined by the

Adviser, or the underlying fund’s adviser where applicable, to be of similar credit quality. High-yield securities are also known as

“junk bonds.” The Fund may have exposure to junk bonds that are in default, subject to bankruptcy or reorganization. The Fund may

also take short positions from time to time to hedge or offset existing long positions.

The Fund may hold cash or cash equivalents or invest directly or indirectly in underlying funds that invest in U.S. Treasury securities

of various maturities.

A portion of the Fund’s assets may be invested in asset-backed securities, mortgage-related securities and mortgage-backed securities.

Such securities may be structured as collateralized mortgage obligations (CMOs) and stripped mortgage-backed securities, including

those structured such that payments consist of interest-only (IO), principal-only (PO) or principal and interest. The Fund also may

invest in inverse floaters and inverse IOs, which are debt securities with interest rates that reset in the opposite direction from the

market rate to which the security is indexed. The Fund may also invest in structured investments and adjustable rate mortgage loans

(ARMs). The Fund may invest a portion of its assets in sub-prime mortgage-related securities.

In selecting underlying funds, the Adviser considers the performance, relative fees, management experience, and underlying portfolio

composition and strategy of such underlying funds.

While the Fund has no present intention to do so, the Fund may be invested in securities that become illiquid investments, which may

include securities that are not readily marketable and securities that are not registered under the Securities Act. The Fund may not

acquire any illiquid investments if, immediately after the acquisition, the Fund would have invested more than 15% of its net assets in

illiquid investments that are assets.

The Fund is non-diversified, which means it may invest a high percentage of its assets in a limited number of securities. The Fund will

typically limit its investment in a single underlying fund to three percent of such underlying fund’s net assets, although the percentage

of such underlying fund owned by the Fund may change over time as the value of such investment changes and the Fund’s overall

portfolio changes.

The Fund may lend its portfolio securities to brokers, dealers, and other financial organizations. These loans, if and when made, may

not exceed 33 1/3% of the total asset value of the Fund (including the loan collateral). By lending its securities, the Fund may increase

its income by receiving payments from the borrower.

the S&P 500® Index (the “S&P 500”). The foundation of the Fund’s strategy involves buying shares of one or more cost-effective

ETFs that track the S&P 500, providing direct exposure to the broad market's performance. The Fund simultaneously implements a

monthly call option strategy to generate income and a quarterly put option strategy to protect against large declines in the S&P 500. In

strategically buying and selling put and call options on the S&P 500, the Fund seeks to provide a partial buffer against market

downturns, as well as provide additional income in flat to down markets, but resulting in lower upside potential during strong market

rallies.

In implementing its strategy, the Fund employs a methodology similar the MerQube Hedged Premium Income Index (the

“MQKHPI”). The MQKHPI is designed to be 100% invested in the Vanguard S&P 500 ETF (VOO) while selling 1-Month call

options and purchasing 3-Month put options on the SPDR S&P 500 ETF (SPY). The MQKHPI aims to generate income from selling

call spreads while providing downside protection through the purchase of put spreads, maintaining exposure to the U.S. large-cap

equity market.

The Fund will operate similarly to the MQKHPI, but with several differences. For one, while the Fund may elect to purchase VOO

and put and call options on SPY, the Fund will be more flexible in determining which cost-effective S&P 500 ETFs to purchase and

what S&P 500 call and put options to buy and sell. Additionally, unlike the MQKHPI that holds options to expiration, the Fund will

actively manage the risk-to-reward ratio of the Fund’s option strategies. If the perceived reward (premium or cost to close out a

position) is not proportional to the risk (maximum potential loss), the Fund’s Sub-advisor will use its discretion to adjust or close the

position if determined to be advantageous to the portfolio. The Fund’s Sub-adviser will also use independent judgement in

determining what particular option spreads to buy and sell under various market conditions, unlike the fixed spreads used by the

MQKHPI.

Although the Fund’s strategy is not expected to materially change in different interest rate environments, varying levels of market

volatility will impact the relative costs of downside protection and relative option spreads. Additionally, the sequence of investment

returns will affect the various strikes prices, expiration dates, and intended purposes of the options used by the Fund, and could

significantly impact Fund’s overall performance. The Fund, based on current market conditions, seeks to achieve the best balance of

premium income/costs, downside protection, and upside potential to meet its investment objective of current income with the potential

for capital appreciation.

Monthly Call Options Strategy

Call options are derivative instruments that allow the option purchaser to contractually purchase a particular security (or the security

index) from the option issuer at a set price (the “strike price”) up to the expiration date of the options. When the issuer sells the call

option, it receives a premium from the buyer in hopes that the option will not be exercised by the buyer.

The monthly call options strategy consists of a mix of selling and purchasing call options on the S&P 500 (“S&P 500 call options”).

The Fund seeks to generate income from the premiums earned from the sold S&P 500 call options. At the same time, the Fund seeks

to realize capital appreciation from its S&P 500 ETF holdings as the S&P 500 increases in value, but with potentially reduced upside

because of the sold S&P 500 call options it uses to generate premium income. The Fund’s purchased S&P 500 call options, however,

are intended to offset this reduced upside potential and limit the risk of missing out on strong market rallies of the S&P 500.

On a regular basis, typically monthly, the Fund sells S&P 500 call options to generate premium income while simultaneously buying

“out of the money” long S&P 500 call options (i.e., options to purchase at a strike price that is higher than the current price of the

reference security or index) to hedge against the possibility that the sold S&P 500 call options are exercised because the S&P 500

increases above the strike price of the sold S&P 500 call options. For example, as the S&P 500 increases in value during the month,

the holders of the sold S&P 500 call options may be more incentivized to exercise their options which will create some losses for the

Fund. However, if the price of the S&P 500 increases above the strike price of the purchased S&P 500 call options, the Fund will be

protected from larger losses because the Fund will exercise its purchased S&P 500 call options, offsetting a portion of its losses on the

sold S&P 500 call options.

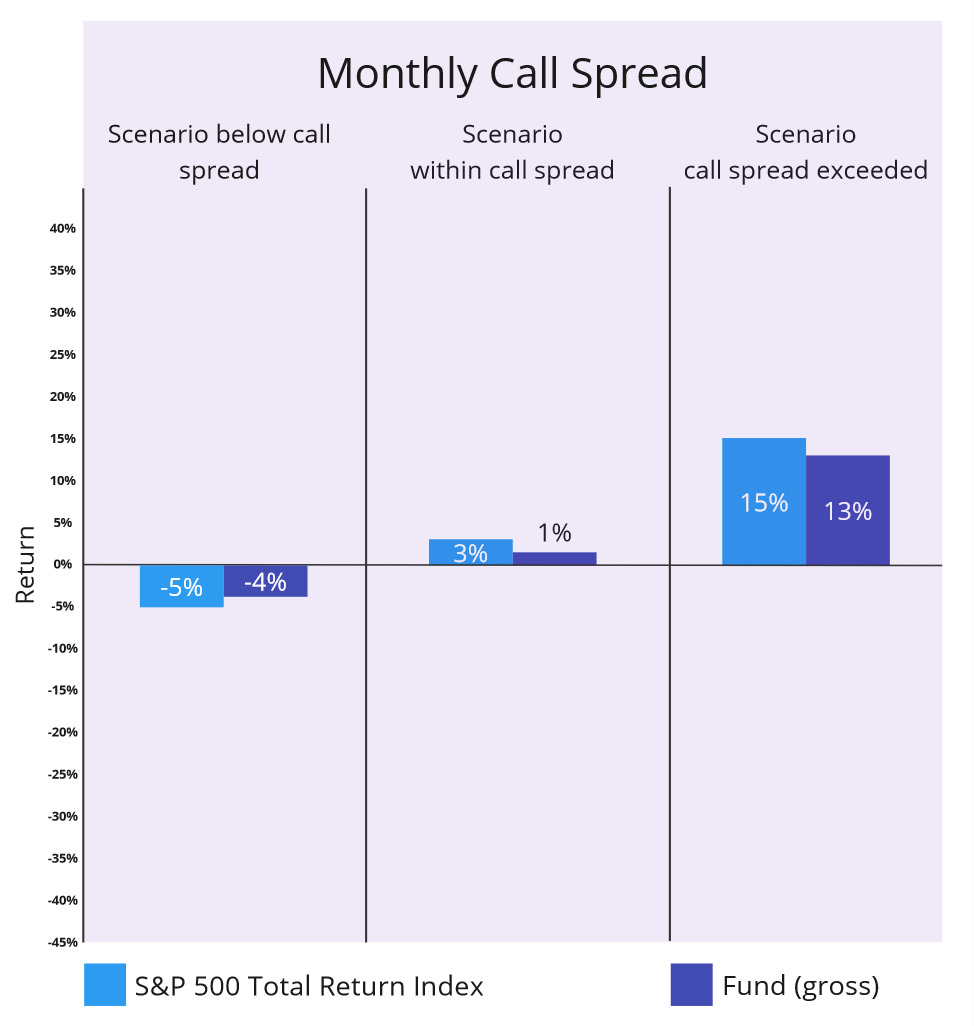

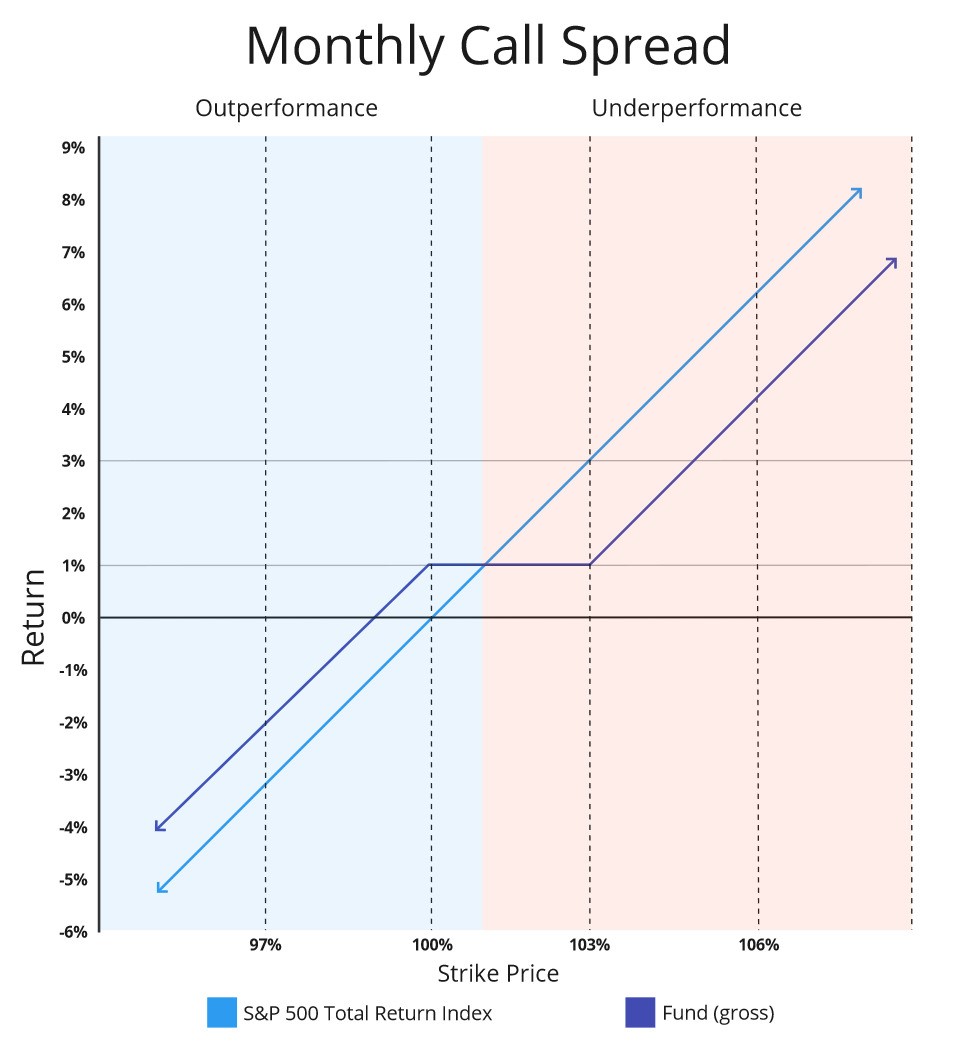

The call option strategy aims to profit from stable or declining S&P 500 prices, with the ideal scenario being the S&P 500 staying

below the strike price of the sold S&P 500 call options. At the same time, the strategy seeks to control and cap the risk of loss from

rapid gains of the S&P 500 with the purchased S&P 500 call options. While the strike prices of the S&P 500 call options may vary, the

Fund will typically sell call options with a strike price between approximately 98-105% of the current value of the S&P 500, and

purchase call options with a strike price between approximately 101-110% of the current value of the S&P 500. Once the S&P 500

appreciates by approximately 5% from its current level (the strike price of the sold call), such call spreads will begin to create a loss.

This loss will, however, will typically be capped at approximately 3% (the difference in strike prices) after the net income from the

call spreads.

Because the call option strategy is typically executed every month, it may have a larger impact on the Fund’s returns than the put

option strategy discussed below that is typically executed on a quarterly basis.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Quarterly Put Options Strategy

Put options are derivative instruments that allow the option purchaser to contractually sell a particular security (or the value of a

security index) to the option issuer at a strike price up to the expiration date of the options. When the issuer sells the put option, it

receives a premium from the buyer in hopes that the buyer will not exercise the option.

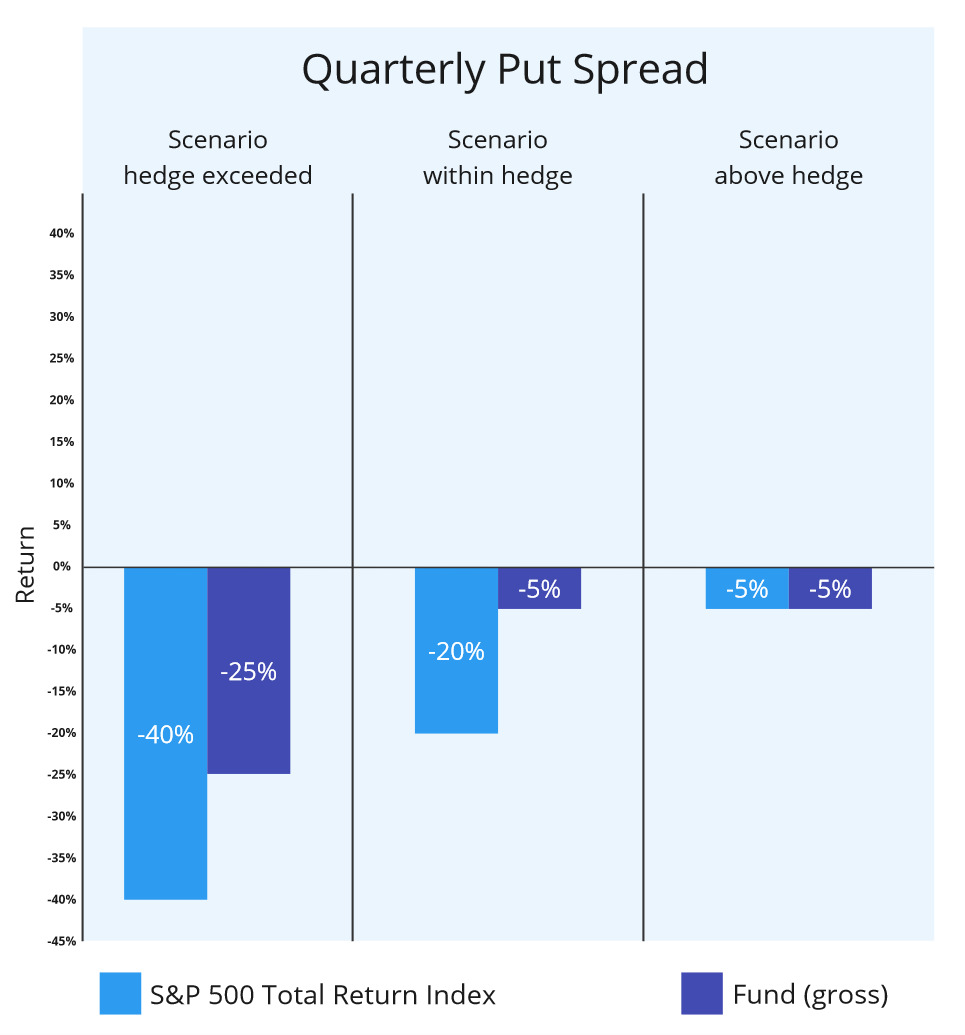

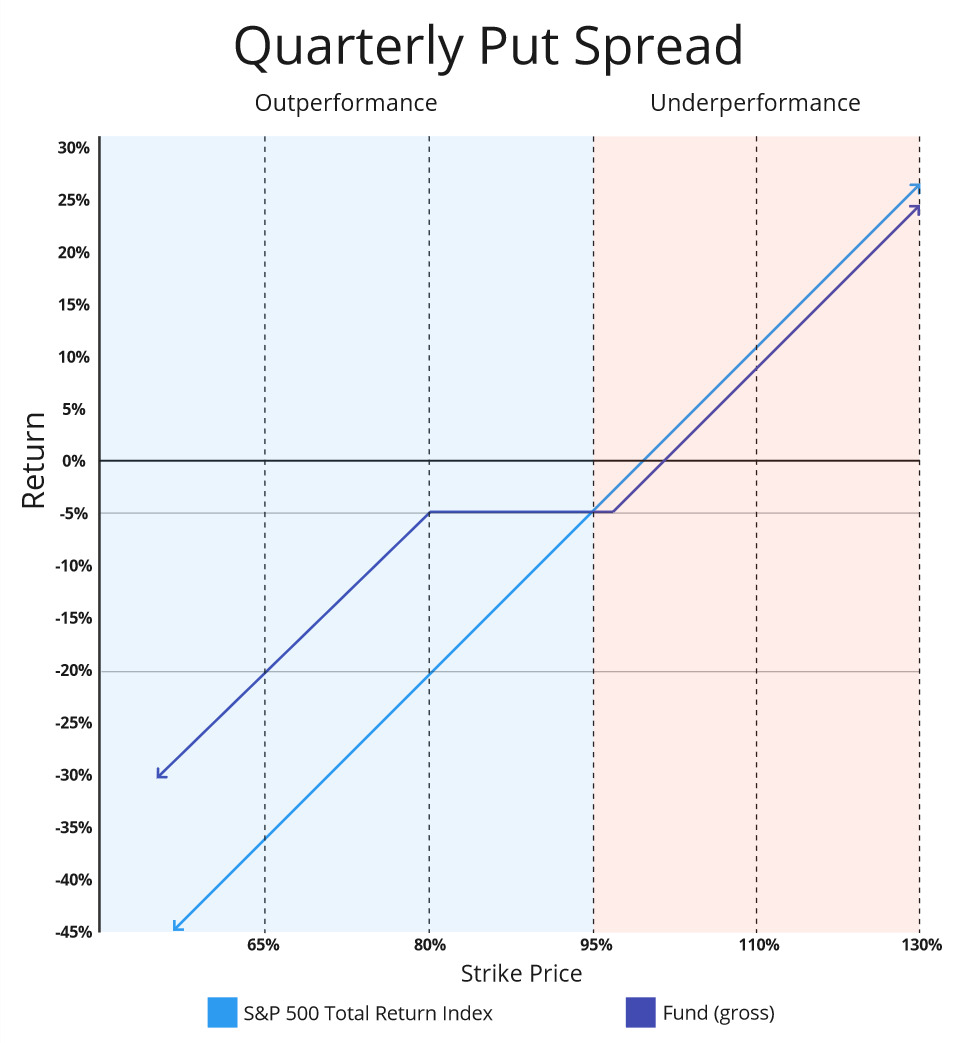

The Fund’s put options strategy, typically executed on a quarterly basis, is designed to protect against large declines in the S&P 500.

The quarterly put options strategy consists of a mix of purchased (or “long”) put options and sold (or “written”) put options on the

S&P 500 Index (“S&P 500 put options”). While the strike prices of the put options may vary, each quarter the Fund typically

purchases S&P 500 put options that are approximately 94-96% of the current S&P 500 level, paying a premium for downside

protection from a large decline in the S&P 500. The Fund simultaneously sells S&P 500 put options with a strike price that is

approximately 75-85% of the current price of the S&P 500 to generate some premium income to offset a portion of the cost of the

purchased put options. The quarterly options strategy of buying a put slightly below the current market price and selling another put

farther below the current market price is designed to protect against significant market downturns at a reduced cost. While the strike

prices of the put options will vary, the put spreads will typically provide a payment to offset losses once the S&P 500 declines by

approximately 5% (the strike price of the purchase put) but will no longer offset losses once the S&P 500 declines by more than an

approximately 20% (the difference in strike prices) after the net costs of the put spreads.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Expected Relative Performance of the Strategy

The Fund’s performance will vary, at times substantially, from the performance of the MQKHPI and the S&P 500. In general,

however, the Fund expects to perform somewhat in line with the MQKHPI, with the Fund’s active decisions around the

implementation of its options strategies intended to improve the Fund’s performance relative to the MQKHPI.

The Fund’s expected performance relative to the S&P 500 under various market conditions can be summarized as follows:

When the S&P 500 is Flat or Declines: Expected Outperformance. In months and quarters where the S&P 500 shows minimal

movement or decreases, the Fund’s overall performance is generally expected to also be flat to negative. However, the Fund would be

positioned to outperform the S&P 500 primarily due to the monthly premium income generated from the monthly call options.

•This anticipated relative outperformance is expected to increase during quarters where the S&P 500 declines by more than

approximately 4-6%, due to the additional downside protection from the quarterly put options.

•If the S&P 500 declines by more than approximately 20% from the purchase price of the put options, the Fund would have no

further downside protection other than the call option premiums. The Fund would participate fully in the decline of the S&P

500 until new put options are purchased.

When the S&P 500 is Up: Expected Underperformance. In months and quarters where the S&P 500 experiences an increase greater

than approximately 1% (the estimated long-term average of option premiums collected), the Fund’s overall performance is generally

expected to be positive. However, the Fund is likely to underperform the S&P 500 primarily be due to the Fund's option strategy that

is intended to sacrifice a portion of the Fund’s upside potential in return for reduced volatility and additional income.

•The underperformance for each monthly call option expiration cycle would be limited to the difference in call option strike

prices (expected to be approximately 3%) and the approximate 1% premium collected.

•If the S&P 500 rises above the strike prices of both call options, the Fund will no longer have capped appreciation until it

sells new call options.”

The Fund is considered to be non-diversified, which means it may invest a high percentage of its assets in a limited number of

investments. Additionally, the Fund’s investment strategies will involve active and frequent purchases and sales of call and put

options, but are not expected to result in high portfolio turnover.

Option Premiums – Income/Return of Capital

As part of the Fund’s options strategies, it sells (or writes) options in return for options premiums, which are expected to contribute to

the overall performance of the Fund. Distributions related to these options premiums may include a significant portion classified as

return of capital. Distributions characterized as a return of capital may reduce the Fund’s net asset value and should not be confused

with yield or income.