485BPOS0001511699false11.30xbrli:pureiso4217:USD00015116992026-04-302026-04-300001511699ck0001511699:S000097905Member2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:C000267415Member2026-04-302026-04-300001511699ck0001511699:S000097905Memberoef:RiskLoseMoneyMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ManagementRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ModelsAndDataRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:HighYieldBondRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksCallRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksCreditRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksInterestRateRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksPrepaymentAndExtensionRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksLiquidityRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:FixedIncomeSecuritiesRisksDurationRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksAuthorizedParticipantsMarketMakersAndLiquidityProvidersConcentrationRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksCashRedemptionRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksCostsOfBuyingOrSellingShareMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksSharesMayTradeAtPricesOtherThanNAVRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ETFRisksTradingRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:BusinessDevelopmentCompanyRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ForeignInvestmentRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:EmergingMarketRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:CurrencyRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:GeographicFocusRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:LoansRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DistributionRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:MarketRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:UnderlyingFundsRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:UnderlyingFundsRiskNetAssetValueAndMarketPriceRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:UnderlyingFundsRiskTrackingRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DerivativesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DerivativesRiskFuturesContractRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DerivativesRiskSwapAgreementsRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DerivativesRiskOptionsRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ValuationRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ShortSaleRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:ConvertibleSecuritiesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:MortgageBackedAndAssetBackedSecuritiesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:LeverageRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberoef:RiskNondiversifiedStatusMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:TurnoverRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:SecuritiesLendingRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:U.S.GovernmentSecuritiesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:EquitySecuritiesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:DividendOrientedCompaniesRiskMember2026-04-302026-04-300001511699ck0001511699:S000097905Memberck0001511699:LimitedHistoryOfOperationsRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Member2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:C000253083Member2026-04-302026-04-300001511699ck0001511699:S000087366Memberoef:RiskLoseMoneyMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ManagementRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:EquitySecuritiesRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksAuthorizedParticipantsMarketMakersAndLiquidityProvidersConcentrationRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksCashRedemptionRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksCostsOfBuyingOrSellingShareMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksSharesMayTradeAtPricesOtherThanNAVRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:ETFRisksTradingRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:MarketRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:UnderlyingFundsRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:UnderlyingFundsRiskNetAssetValueAndMarketPriceRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:UnderlyingFundsRiskTrackingRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:DerivativesRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:DerivativesRiskOptionsRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:LeverageRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberck0001511699:LimitedHistoryOfOperationsRiskMember2026-04-302026-04-300001511699ck0001511699:S000087366Memberoef:RiskNondiversifiedStatusMember2026-04-302026-04-300001511699ck0001511699:C000253083Member2026-04-302026-04-300001511699ck0001511699:C000253083Member2025-01-012025-12-310001511699ck0001511699:C000253083Member2024-09-042025-12-310001511699oef:AfterTaxesOnDistributionsMemberck0001511699:C000253083Member2026-04-302026-04-300001511699oef:AfterTaxesOnDistributionsMemberck0001511699:C000253083Member2025-01-012025-12-310001511699oef:AfterTaxesOnDistributionsMemberck0001511699:C000253083Member2024-09-042025-12-310001511699oef:AfterTaxesOnDistributionsAndSalesMemberck0001511699:C000253083Member2026-04-302026-04-300001511699oef:AfterTaxesOnDistributionsAndSalesMemberck0001511699:C000253083Member2025-01-012025-12-310001511699oef:AfterTaxesOnDistributionsAndSalesMemberck0001511699:C000253083Member2024-09-042025-12-310001511699ck0001511699:MerQubeHedgedPremiumIncomeIndexReflectsNoDeductionForFeesExpensesOrTaxesIndexMember2026-04-302026-04-300001511699ck0001511699:MerQubeHedgedPremiumIncomeIndexReflectsNoDeductionForFeesExpensesOrTaxesIndexMember2025-01-012025-12-310001511699ck0001511699:MerQubeHedgedPremiumIncomeIndexReflectsNoDeductionForFeesExpensesOrTaxesIndexMember2024-09-042025-12-310001511699ck0001511699:SP500TotalReturnIndexreflectsnodeductionforfeesexpensesortaxesIndexMember2026-04-302026-04-300001511699ck0001511699:SP500TotalReturnIndexreflectsnodeductionforfeesexpensesortaxesIndexMember2025-01-012025-12-310001511699ck0001511699:SP500TotalReturnIndexreflectsnodeductionforfeesexpensesortaxesIndexMember2024-09-042025-12-310001511699ck0001511699:S000087366Memberck0001511699:C000253083Member2025-01-012025-12-31

Filed with the Securities and Exchange Commission on April 29, 2026

1933 Act Registration File No. 333-172080

1940 Act File No. 811-22525

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

| | | | | | | | | | | | | | | | | |

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [ | X | ] |

| Pre-Effective Amendment No. | | | [ | | ] |

| Post-Effective Amendment No. | 644 | | [ | X | ] |

and/or

| | | | | | | | | | | | | | | | | |

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [ | X | ] |

| Amendment No. | 645 | | [ | X | ] |

(Check appropriate box or boxes.)

MANAGED PORTFOLIO SERIES

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of Principal Executive Offices, including Zip Code)

Registrant’s Telephone Number, including Area Code: (414) 765-6844

| | |

Brian R. Wiedmeyer, President and Principal Executive Officer

Managed Portfolio Series

615 East Michigan Street

Milwaukee, WI 53202 |

(Name and Address of Agent for Service)

Copy to:

| | |

Christopher D. Menconi

Morgan, Lewis & Bockius LLP

1111 Pennsylvania Ave, NW

Washington, DC 20004 |

It is proposed that this filing will become effective (check appropriate box)

| | | | | | | | | | | |

| [ | | ] | immediately upon filing pursuant to Rule 485(b) |

| [ | X | ] | On April 30, 2026 pursuant to Rule 485(b) |

| [ | | ] | 60 days after filing pursuant to Rule(a)(1) |

| [ | | ] | on (date) pursuant to Rule(a)(1) |

| [ | | ] | 75 days after filing pursuant to Rule(a)(2) |

| [ | | ] | on (date) pursuant to Rule 485(a)(2). |

If appropriate, check the following box:

| | | | | | | | | | | |

| [ | | ] | This post-effective amendment designates a new effective date for a previously filed post- effective amendment. |

Explanatory Note: This Post-Effective Amendment No. 644 to the Registration Statement of Managed Portfolio Series (the “Trust”) is being filed for the purpose of updating the financial information and to make other permissible changes under Rule 485(b).

| |

| |

| |

Kensington Credit Opportunities ETF | |

Listed on Cboe BZX Exchange, Inc. |

Kensington Hedged Premium Income ETF | |

Listed on Cboe BZX Exchange, Inc. |

PROSPECTUS

These securities have not been approved or disapproved by the Securities and Exchange Commission, nor has the Securities and

Exchange Commission passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal

offense.

Table of Contents

| |

FUND SUMMARY ......................................................................................................................................................................... | |

| |

| |

| |

Investment Objective .................................................................................................................................................................. | |

Principal Investment Risks .......................................................................................................................................................... | |

Fund Holdings Disclosure ........................................................................................................................................................... | |

Cybersecurity .............................................................................................................................................................................. | |

MANAGEMENT............................................................................................................................................................................. | |

Investment Adviser and Sub-Adviser ......................................................................................................................................... | |

Portfolio Managers ...................................................................................................................................................................... | |

BUYING AND SELLING FUND SHARES ................................................................................................................................. | |

OTHER CONSIDERATIONS ....................................................................................................................................................... | |

| |

ADDITIONAL INFORMATION .................................................................................................................................................. | |

FINANCIAL HIGHLIGHTS ......................................................................................................................................................... | |

KENSINGTON CREDIT OPPORTUNITIES ETF

Investment Objective: The Kensington Credit Opportunities ETF (KAMO) (the “Fund”) seeks income and capital appreciation.

Fees and Expenses of the Fund: This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the

Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not

reflected in the table and Examples below.

| |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) | |

| |

Distribution and/or Service (12b-1) Fees | |

| |

Acquired Fund Fees and Expenses(2) | |

Total Annual Fund Operating Expenses | |

(1)Kensington Asset Management, LLC (the “Adviser”) has agreed to pay all expenses of the Fund, except for: (i) brokerage expenses and other fees, charges, taxes,

levies or expenses incurred in connection with the execution of portfolio transactions or in connection with creation and redemption transactions; (ii) fees or

expenses in connection with any arbitration, litigation or pending or threatened arbitration or litigation, including any settlements in connection therewith; (iii)

extraordinary expenses; (iv) distribution fees and expenses paid by the Fund under any distribution plan adopted pursuant to Rule 12b-1 under the Investment

Company Act of 1940, as amended (“1940 Act”); (v) interest and taxes of any kind or nature; (vi) any fees and expenses related to the provision of securities

lending services; (vii) the advisory fee payable to the Adviser; (viii) Acquired Fund Fees and Expenses; and (ix) all costs incurred in connection with shareholder

meetings and all proxy solicitations (except for such shareholder meetings and proxy solicitations related to: (a) changes to the Adviser’s investment advisory

agreement, (b) changes in control at the Adviser, (c) the election of any Board member who is an “interested person” of the Adviser (as that term is defined under

Section 2(a)(19) of the 1940 Act), (d) matters initiated by the Adviser, or (e) any other matters that directly benefit the Adviser).

(2)Other Expenses and Acquired Fund Fees and Expenses (“AFFE”) are estimated for the current fiscal year. AFFE are indirect costs of investing in other investment

companies. The operating expenses in this fee table do not correlate to the expense ratio in the Fund’s financial highlights because the financial statements include

only the direct operating expenses incurred by the Fund and not the indirect costs of investing in other investment companies.

Example: This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all your shares at the end of

those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses

remain the same. Although your actual costs may be higher or lower, based upon these assumptions your costs would be:

Portfolio Turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its

portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are

held in a taxable account at the shareholder level. These costs, which are not reflected in annual fund operating expenses or in the

example above, affect the Fund’s performance. During the most recent fiscal period from the Fund’s inception on December 16, 2025,

through December 31, 2025, the Fund’s portfolio turnover rate was 1% of its average portfolio value. The portfolio turnover rate is

calculated without regard to short positions intended to be held for less than a year and most derivatives. If such instruments were

included, the Fund’s portfolio turnover rate might be significantly higher.

Principal Investment Strategies

The Fund invests, under normal circumstances, at least 80% of its assets (including the amount of borrowings for investment

purposes) in (1) U.S. and non-U.S. fixed income securities; and (2) exchange-traded funds and derivatives instruments that provide

long and short exposure to U.S. and non-U.S. fixed income securities. The Fund focuses on lower-quality, higher-yielding securities

across a wide range of investable asset classes using both long and short exposures. The Fund will gain exposure to fixed income

securities primarily by investing in one or more of the following investment types:

•Other exchange-traded funds (“ETFs”);

•Individual bonds (or baskets of bonds);

•Bond futures; and

•Credit default swaps, credit default index swaps, and options on such instruments.

The Fund will typically seek exposure among a wide range of fixed income segments, including the following:

Lower Grade Fixed Income

•High-yield corporate bonds

•Leveraged loans, senior loans and bank loans

•Convertible bonds

Higher Grade Fixed Income

•Investment-grade corporate bonds

•Asset-backed securities, including mortgage-related securities and mortgage-backed securities

•U.S. Treasury securities

Peripheral Asset Classes

•Emerging market bonds

•Publicly-traded Business Development Companies (“BDCs”)

•High dividend equity securities

The Fund is designed to provide an actively-managed solution across various sectors of fixed income using Kensington’s investment

process. The Fund will generally feature a blended portfolio that increases or decreases exposure across target asset classes. The Fund

may use both long or short exposures to manage duration and credit risk through a two-step process that involves quantitative analysis

on different aspects of fixed income investing, as well as risk management.

The Fund’s quantitative analysis process incorporates four distinct categories: Trends, Valuation, Macro Environment, and Pricing and

Flow Anomalies, using a quantitative approach with the following rationales:

| | |

| | |

| | The trend-following component of the Fund utilizes numerous inputs, such as par weighted index price, yields, total return index, and credit spreads. For each input, features are generated across long, medium, and short timeframes to obtain a final trend signal. The objective is to capture the essence of trends as they occur. Frequent changes are to be expected but other process components seek to mitigate this volatility. |

| | |

| | |

| | This component is an inherently counter-trend or contrarian framework designed to complement trend- following. This aspect of the process is designed to identify areas of relatively “cheap” versus “expensive” valuations, based on historical data. This component is designed to allow the Fund to be more risk-conscious when valuations are overpriced and to identify possible counter-trend buying opportunities when valuations are at extreme historical lows. |

| | |

| | |

| | This analysis considers factors from different asset classes, such as equities and commodities. The portfolio managers believe that including a “macro-aware” framework can potentially improve allocation guidance and risk-adjusted performance. For example, rising commodity, government bond, and equity prices typically show strong or improving economic growth, whereas falling bond and equity prices but rising commodity prices could be an indicator of a “stagflationary” regime. |

| | |

| | |

Pricing and Flow Anomalies | | Investor timing and behavior can lead to trading anomalies that produce regular periods of lower or higher- than-average expected returns. Kensington’s quantitative process is designed to identify these periods, and plays a role in determining asset allocation when combined with the other indicator subsets. |

After using these analyses to generate forecasts of expected future performance for asset classes, quantitative portfolio optimization

techniques that weigh forecasts of expected future performance and risk given real life constraints like turnover, transaction costs and

slippage are applied to obtain asset class allocations in the portfolio.

Shorting / Inverse Position: In addition to these four categories, the Fund’s quantitative model contains signals to short exposures

primarily in two asset classes: U.S. Treasuries and U.S. high-yield bonds. Shorting will be typically achieved through the usage of

futures contracts for U.S. Treasuries. For U.S. high-yield bonds, the Fund may short ETFs, purchase credit default swaps or utilize

other derivatives, such as options and futures. The Fund may also gain short exposure through the use of inverse ETFs, which are

ETFs that generally seek to provide investment results that are the inverse of the performance of an underlying index or other asset.

The Fund is flexible and not managed to a benchmark. The Fund may shift its allocations based on changing market conditions, which

may result in investing in a single or multiple markets and sectors. The Fund has broad flexibility to invest in a wide variety of debt

securities and instruments of any maturity. The Fund may invest in fixed and floating rate debt securities issued in both U.S. and

foreign markets, including countries whose economies are less developed (emerging markets). The Fund has discretion to focus its

investments in one or more regions or small groups of countries including both U.S. and foreign markets including emerging markets.

The Fund invests primarily in U.S. dollar denominated securities, although the Fund may also invest in non-dollar denominated

securities. The fixed-income securities to which the Fund may have exposure are not restricted as to issuer credit quality, country,

capitalization, security maturity, currency, or leverage.

The Fund will typically have significant exposure to high-yield securities, which are debt instruments rated lower than Baa3 by

Moody’s Ratings (“Moody’s”) or lower than BBB- by Standard and Poor’s Rating Group (“S&P”), or, if unrated, determined by the

Adviser, or the underlying fund’s adviser where applicable, to be of similar credit quality. High-yield securities are also known as

“junk bonds.” The Fund may have exposure to junk bonds that are in default, subject to bankruptcy or reorganization. The Fund may

also take short positions from time to time to hedge or offset existing long positions.

The Fund may hold cash or cash equivalents or invest directly or indirectly in underlying funds that invest in U.S. Treasury securities

of various maturities.

A portion of the Fund’s assets may be invested in asset-backed securities, mortgage-related securities and mortgage-backed securities.

Such securities may be structured as collateralized mortgage obligations (CMOs) and stripped mortgage-backed securities, including

those structured such that payments consist of interest-only (IO), principal-only (PO) or principal and interest. The Fund also may

invest in inverse floaters and inverse IOs, which are debt securities with interest rates that reset in the opposite direction from the

market rate to which the security is indexed. The Fund may also invest in structured investments and adjustable rate mortgage loans

(ARMs). The Fund may invest a portion of its assets in sub-prime mortgage-related securities.

In selecting underlying funds, the Adviser considers the performance, relative fees, management experience, and underlying portfolio

composition and strategy of such underlying funds.

While the Fund has no present intention to do so, the Fund may be invested in securities that become illiquid investments, which may

include securities that are not readily marketable and securities that are not registered under the Securities Act. The Fund may not

acquire any illiquid investments if, immediately after the acquisition, the Fund would have invested more than 15% of its net assets in

illiquid investments that are assets.

The Fund is non-diversified, which means it may invest a high percentage of its assets in a limited number of securities. The Fund will

typically limit its investment in a single underlying fund to three percent of such underlying fund’s net assets, although the percentage

of such underlying fund owned by the Fund may change over time as the value of such investment changes and the Fund’s overall

portfolio changes.

The Fund may lend its portfolio securities to brokers, dealers, and other financial organizations. These loans, if and when made, may

not exceed 33 1/3% of the total asset value of the Fund (including the loan collateral). By lending its securities, the Fund may increase

its income by receiving payments from the borrower.

Principal Investment Risks

As with all funds, there is the risk that you could lose money through your investment in the Fund. The Fund is not intended to be a

complete investment program. Many factors affect the Fund’s net asset value and performance. The following risks apply to the Fund

directly and indirectly through the Fund’s investment in underlying funds.

•Management Risk. The Adviser’s reliance on its proprietary investment process and the Adviser’s judgments about the

attractiveness, value, and potential appreciation of particular assets and asset classes may prove to be incorrect and may not

produce the desired results.

•Models and Data Risk. The Fund’s investment exposure is heavily dependent on proprietary quantitative models as well as

information and data supplied by third parties (“Models and Data”). When Models and Data prove to be incorrect or

incomplete, any decisions made in reliance thereon may lead to securities being included in or excluded from the Fund’s

portfolio that would have been excluded or included had the Models and Data been correct and complete. Some of the models

used by the Fund are predictive in nature. The use of predictive models has inherent risks. For example, such models may

incorrectly forecast future behavior, leading to potential losses. In addition, in unforeseen or certain low-probability scenarios

(often involving a market disruption of some kind), such models may produce unexpected results, which can result in losses

for the Fund.

•High-Yield Bond Risk. Lower-quality fixed income securities, known as “high-yield” or “junk” bonds, present greater risk

than bonds of higher quality, including an increased risk of default. These securities are considered speculative. Defaulted

securities or those subject to a reorganization proceeding may become worthless and are illiquid.

•Fixed-Income Securities Risks. The Fund may invest in or have exposure to fixed-income securities. Fixed-income securities

are or may be subject to interest rate, credit, liquidity, prepayment and extension risks. Interest rates may go up resulting in a

decrease in the value of fixed-income securities. Credit risk is the risk that an issuer will not make timely payments of

principal and interest. There is also the risk that an issuer may “call,” or repay, its high-yielding bonds before their maturity

dates. Fixed-income securities subject to prepayment can offer less potential for gains during a declining interest rate

environment and similar or greater potential for loss in a rising interest rate environment. Limited trading opportunities for

certain fixed-income securities may make it more difficult to sell or buy a security at a favorable price or time. Changes in

market conditions and government policies may lead to periods of heightened volatility and reduced liquidity in the fixed-

income securities market, and could result in an increase in redemptions. Interest rate changes and their impact on the Fund

and its share price can be sudden and unpredictable.

◦Call Risk. During periods of declining interest rates, a bond issuer may “call,” or repay, its high-yielding bonds

before their maturity dates. In this event the Fund would then be forced to invest the unanticipated proceeds at lower

interest rates, resulting in a decline in its income.

◦Credit Risk . Fixed-income securities are generally subject to the risk that the issuer may be unable or unwilling to

make principal and interest payments when they are due. There is also the risk that the securities could lose value

because of a loss of confidence in the ability of the borrower to pay back debt. Lower rated fixed-income securities

involve greater credit risk, including the possibility of default or bankruptcy.

◦Interest Rate Risk. Generally, the value of fixed income securities will change inversely with changes in interest

rates. As interest rates rise, the market value of fixed income securities tends to decrease. Conversely, as interest

rates fall, the market value of fixed income securities tends to increase. This risk will be greater for long-term

securities than for short-term securities.

◦Prepayment and Extension Risk. In times of declining interest rates, the Fund’s higher yielding securities may be

prepaid and such fund may have to replace them with securities having a lower yield. In times of rising interest rates,

prepayments will slow causing portfolio securities considered short or intermediate term to be long-term securities,

which fluctuate more widely in response to changes in interest rates than shorter term securities.

◦Liquidity Risk. There may be no willing buyer of the Fund’s portfolio securities and such fund may have to sell those

securities at a lower price or may not be able to sell the securities at all, each of which would have a negative effect

on performance.

◦Duration Risk. The Fund can invest in securities of any maturity or duration. Duration is a measure of sensitivity of

a security’s price to changes in interest rates. For example, a security with a duration of 2.0 would be expected to

decrease in price 2% for every 1% rise in interest rates (the inverse is true as well). Holding long duration and long

maturity investments will magnify certain risks, including interest rate risk and credit risk.

•ETF Risks. The Fund is an ETF, and, as a result of an ETF’s structure, it is exposed to the following risks:

◦Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited

number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited

number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events

occur, shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or

otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform

these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their functions.

◦Cash Redemption Risk. While not expected to be a regular occurrence, the Fund’s investment strategy may require it

to redeem shares for cash or to otherwise include cash as part of its redemption proceeds. The Fund may be required

to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause

the Fund to recognize a capital gain that it might not have recognized if it had made a redemption in-kind. As a

result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was

used.

◦Costs of Buying or Selling Shares. Due to the costs of buying or selling shares, including brokerage commissions

imposed by brokers and bid-ask spreads, frequent trading of shares may significantly reduce investment results and

an investment in shares may not be advisable for investors who anticipate regularly making small investments.

◦Shares May Trade at Prices Other Than NAV. As with all ETFs, shares may be bought and sold in the secondary

market at market prices. Although it is expected that the market price of shares will approximate the Fund’s NAV,

there may be times when the market price of shares is more than the NAV intra-day (premium) or less than the NAV

intra-day (discount) due to supply and demand of shares or during periods of market volatility. This risk is

heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading

activity for shares in the secondary market, in which case such premiums or discounts may be significant. Because

securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing

exchange is open, there are likely to be deviations between the current price of a security and the security’s last

quoted price from the closed foreign market. This may result in premiums and discounts that are greater than those

experienced by domestic ETFs.

◦Trading. Although shares are listed for trading on the Cboe BZX Exchange, Inc. (the “Exchange”) and may be

traded on U.S. exchanges other than the Exchange, there can be no assurance that shares will trade with any volume,

or at all, on any stock exchange. In stressed market conditions, the liquidity of shares may begin to mirror the

liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than shares, and this

could lead to differences between the market price of the shares and the underlying value of those shares.

•Business Development Company (“BDC”) Risk. There are certain risks inherent in investing in BDCs, whose principal

business is to invest in, and lend capital or provide services to privately held companies. BDCs are regulated under the 1940

Act and are subject to certain restraints. For example, BDCs are required to invest at least 70% of their total assets primarily

in securities of private companies or thinly traded U.S. public companies, cash, cash equivalents, U.S. government securities

and high quality debt investments that mature in one year or less. Because little public information exists for private and

thinly traded companies in which a BDC may invest, there is a risk that investors may not be able to make a fully informed

investment decision. In addition, investments made by BDCs are typically illiquid and may be difficult to value. A BDC may

only incur indebtedness in amounts such that the BDC's asset coverage, subject to certain conditions, equals at least 150%

after such incurrence. These limitations on asset mix and leverage may prohibit the way that the BDC raises capital.

•Foreign Investment Risk. Foreign investments may be riskier than U.S. investments for many reasons, such as changes in

currency exchange rates and unstable political, social, and economic conditions.

•Emerging Market Risk. The Fund intends to have exposure to emerging markets. Emerging markets are riskier than more

developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets

may be considered speculative.

•Currency Risk. Changes in currency exchange rates may negatively affect the value of the Fund’s investments. Fluctuations

in currency exchange rates (relative to the U.S. dollar) may erode or reverse any potential gains from the Fund’s investments

in securities denominated in a foreign currency or may widen existing losses.

•Geographic Focus Risk. The Fund may focus its investments in one or more regions or a limited number of countries. As a

result, the Fund’s performance may be subject to greater volatility than a more geographically diversified fund.

•Loans Risk. The market for loans, including bank loans, loan participations, and syndicated loan assignments may not be

highly liquid, and the holder may have difficulty selling them. These investments expose the Fund to the credit risk of both

the financial institution and the underlying borrower. Bank loans settle on a delayed basis, which can be greater than seven

days, potentially leading to the sale proceeds of such loans not being available for a substantial period of time after the sale of

the bank loans.

•Distribution Risk. The Fund is not designed to provide a predictable level of dividend income. The income payable on debt

securities in general and the availability of investment opportunities varies based on market conditions. In addition, the Fund

may not be effective in identifying income producing securities and managing distributions; as a result, the level of dividend

income will fluctuate. The Fund’s investments are subject to various risks including the risk that the counterparty will not pay

income when due which may adversely impact the level and volatility of dividend income paid by the Fund. The Fund does

not guarantee that distributions will always be paid or that such dividends will not fluctuate.

•Market Risk. Overall investment market risks affect the value of the Fund. Factors such as economic growth and market

conditions, interest rate levels, and political events affect U.S. and international investment markets. Additionally, unexpected

local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental

or man-made disasters; the spread of infectious illnesses or other public health issues (such as the COVID-19 global

pandemic); and recessions and depressions could have a significant impact on the Fund and its investments and may impair

market liquidity. Such events can cause investor fear, which can adversely affect the economies of nations, regions and the

market in general, in ways that cannot necessarily be foreseen.

•Underlying Funds Risk. Investments in underlying funds involve duplication of investment advisory fees and certain other

expenses. Each underlying fund is subject to specific risks, depending on the nature of its investment strategy. The manager

of an underlying fund may not be successful in implementing its strategy. ETF shares may trade at a market price that may be

lower (a discount) or higher (a premium) than the ETF’s net asset value. ETFs are also subject to brokerage and/or other

trading costs, which could result in greater expenses to the Fund. Because the value of ETF shares depends on the demand in

the market, the Adviser may not be able to liquidate the Fund’s holdings at the most optimal time, adversely affecting

performance.

◦Net Asset Value and Market Price Risk. The market value of ETF shares may differ from their NAV. This difference

in price may be due to the fact that the supply and demand in the market for ETF shares at any point in time is not

always identical to the supply and demand in the market for the underlying holdings. Accordingly, there may be

times when an ETF share trades at a premium or discount to its NAV.

◦Tracking Risk. ETFs in which the Fund invests will not be able to replicate exactly the performance of any indices or

prices they track because the total return generated by the securities will be reduced by transaction costs incurred in

adjusting the actual balance of the securities or derivatives. Certain securities comprising an index may, from time to

time, temporarily be unavailable, which may further impede the security’s ability to track an index.

•Derivatives Risk. In general, a derivative instrument typically involves leverage, i.e., it provides exposure to potential gain or

loss from a change in the level of the market price of the underlying security (or a basket or index) in a notional amount that

exceeds the amount of cash or assets required to establish or maintain the derivative instrument. Adverse changes in the value

or level of the underlying asset or index, which the Fund may not directly own, can result in a loss to the Fund substantially

greater than the amount invested in the derivative itself. The use of derivative instruments also exposes the Fund to additional

risks and transaction costs. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate

perfectly with the overall securities markets.

◦Futures Contract Risk. The successful use of futures contracts draws upon the Adviser’s skill and experience with

respect to such instruments and is subject to special risk considerations. The primary risks associated with the use of

futures contracts, which may adversely affect the Fund’s NAV and total return, are (a) the imperfect correlation between

the change in market value of the instruments held by the Fund and the price of the futures contract; (b) possible lack of a

liquid secondary market for a futures contract and the resulting inability to close a futures contract when desired; (c)

losses caused by unanticipated market movements, which are potentially unlimited; (d) the Adviser’s inability to predict

correctly the direction of securities prices, interest rates, currency exchange rates and other economic factors; (e) the

possibility that the counterparty will default in the performance of its obligations; and (f) if the Fund has insufficient

cash, it may have to sell securities from its portfolio to meet daily variation margin requirements, and the Fund may have

to sell securities at a time when it may be disadvantageous to do so.

◦Credit Default Swap Agreements Risk. The Fund may enter into credit default index swap agreements or credit default

swap agreements as a “buyer” or “seller” of credit protection. Credit default index swap agreements and credit default

swap agreements involve special risks because they may be difficult to value, are highly susceptible to liquidity and

credit risk, and generally pay a return to the party that has paid the premium only in the event of an actual default by the

issuer of the underlying obligation (as opposed to a credit downgrade or other indication of financial difficulty).

◦Options Risk. An option is an agreement that, for a premium payment or fee, gives the option holder (the purchaser) the

right but not the obligation to buy (a “call option”) or sell (a “put option”) the underlying asset (or settle for cash an

amount based on an underlying asset, rate, or index) at a specified price (the “exercise price”) during a period of time or

on a specified date. Investments in options are considered speculative. When the Fund purchases an option, it may lose

the premium paid for it if the price of the underlying security or other assets decreased or remained the same (in the case

of a call option) or increased or remained the same (in the case of a put option). If a put or call option purchased by the

Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund.

•Valuation Risk. Valuation risk is the risk that the Fund has valued certain securities or positions at a higher price than the

price at which they can be sold. There is no assurance that the Fund could sell a portfolio investment for the value established

for it at any time, and the Fund may incur a loss because a portfolio investment is sold at a discount to its established value.

•Short Sale Risk. The Fund will suffer a loss if it sells a security short and the value of the security rises rather than falls. It is

possible that the Fund’s long positions will decline in value at the same time that the value of its securities sold short

increase, thereby increasing potential losses to the Fund. A short position involves the risk of a theoretically unlimited

increase in the value of the underlying instrument which could cause the Fund to suffer a (potentially unlimited) loss. Short

sales also involve transaction and financing costs that will reduce potential Fund gains and increase potential Fund losses.

When the Fund invests in inverse ETFs to achieve short exposure, the Fund will indirectly be subject to the risk that the

performance of such inverse ETFs will fall as the performance of the inverse ETF’s benchmark or other reference asset rises -

a result that is the opposite from traditional ETFs. In addition, the inverse ETFs held by the Fund may utilize leverage to

acquire their underlying portfolio investments. The use of leverage may exaggerate changes in an inverse ETF’s share price

and the return on its investments.

•Convertible Securities Risk. Convertible securities are subject to the risks of stocks when the underlying stock price is high

relative to the conversion price (because more of the security's value resides in the conversion feature) and debt securities

when the underlying stock price is low relative to the conversion price (because the conversion feature is less valuable). The

value of convertible securities may rise and fall with the market value of the underlying stock or, like a debt security, vary

with changes in interest rates and the credit quality of the issuer. A convertible security is not as sensitive to interest rate

changes as a similar non-convertible debt security, and generally has less potential for gain or loss than the underlying stock.

•Mortgage Securities and Asset-Backed Securities Risk. Mortgage securities differ from conventional debt securities because

principal is paid back periodically over the life of the security rather than at maturity. The Fund may receive unscheduled

payments of principal due to voluntary prepayments, refinancings or foreclosures on the underlying mortgage loans. Because

of prepayments, mortgage securities may be less effective than some other types of debt securities as a means of "locking in"

long-term interest rates and may have less potential for capital appreciation during periods of falling interest rates. A

reduction in the anticipated rate of principal prepayments, especially during periods of rising interest rates, may increase or

extend the effective maturity and duration of mortgage securities, making them more sensitive to interest rate changes,

subject to greater price volatility, and more susceptible than some other debt securities to a decline in market value when

interest rates rise. Issuers of asset-backed securities may have limited ability to enforce the security interest in the underlying

assets, and credit enhancements provided to support the securities, if any, may be inadequate to protect investors in the event

of default. Like mortgage securities, asset-backed securities are subject to prepayment and extension risks.

•Leverage Risk. As part of the Fund’s principal investment strategy, the Fund may make investments in derivative instruments.

These derivative instruments provide the economic effect of financial leverage by creating additional investment exposure to

the underlying asset, as well as the potential for greater loss. If the Fund uses leverage through activities such as entering into

derivative instruments, the Fund has the risk that losses may exceed the net assets of the Fund. The net asset value of the

Fund while employing leverage will be more volatile and sensitive to market movements.

•Non-Diversification Risk. As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of

one or more issuers. The Fund also invests in underlying funds that are non-diversified. The Fund’s performance may be

more sensitive to any single economic, business, political or regulatory occurrence than the value of shares of a diversified

investment company.

•Turnover Risk. A higher portfolio turnover may result in higher transactional and brokerage costs. The Fund’s portfolio

turnover rate may be significantly above 100% annually.

•Securities Lending Risk. There are certain risks associated with securities lending, including the risk that the borrower may

fail to return the securities on a timely basis or even the loss of rights in the collateral deposited by the borrower, if the

borrower should fail financially. As a result, the Fund may lose money. The Fund could also lose money in the event of a

decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash

collateral. These events could also trigger adverse tax consequences for the Fund.

•U.S. Government Securities Risk. The Fund may invest directly or indirectly in obligations issued by agencies and

instrumentalities of the U.S. government. The U.S. government may choose not to provide financial support to U.S.

government sponsored agencies or instrumentalities if it is not legally obligated to do so, in which case, if the issuer

defaulted, the Fund might not be able to recover its investment.

•Equity Securities Risk. The Fund may invest in or have exposure to equity securities. Equity securities may experience

sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect

securities markets generally or factors affecting specific industries, sectors, geographic markets, or companies in which the

Fund invests.

•Dividend-Oriented Companies Risk. Companies that have historically paid regular dividends to shareholders may decrease or

eliminate dividend payments in the future. A decrease in dividend payments by an issuer may result in a decrease in the value

of the issuer's stock and less available income for the Fund.

•Limited History of Operations Risk. The Fund has a limited history of operations for investors to evaluate. The Fund may fail

to attract sufficient assets to operate efficiently.

Performance: As of the date of this Prospectus, the Fund does not have a full calendar year of performance as an ETF. When the Fund

has been in operation for a full calendar year, performance information will be shown here. You should be aware that the Fund’s past

performance (before and after taxes) may not be an indication of how the Fund will perform in the future. Updated performance

information and daily NAV per share is available at no cost by calling toll-free 866-303-8623 and on the Fund’s website at https://

www.kensingtonassetmanagement.com/solutions/etfs-kamo/.

Investment Adviser: Kensington Asset Management, LLC

Portfolio Managers:

Patrick Sommerstad

Patrick Sommerstad serves as Portfolio Manager and Investment Committee Member for Kensington Asset Management. He has

served the Fund since its inception in 2025.

Jason Sim

Jason Sim serves as Portfolio Manager and Investment Committee Member for Kensington Asset Management. He has served the

Fund since its inception in 2025.

Jordan Flebotte

Jordan Flebotte serves as Portfolio Manager and Investment Committee Member for Kensington Asset Management. He has served

the Fund since its inception in 2025.

Purchase and Sale of Fund Shares: The Fund will issue (or redeem) shares to certain institutional investors (typically market makers

or other broker-dealers) only in blocks of shares known as “Creation Units.” Creation Unit transactions are typically conducted in

exchange for the deposit or delivery of in-kind securities and/or cash constituting a substantial replication, or a representation, of the

securities included in the Fund’s portfolio. Individual shares may only be purchased and sold on a national securities exchange

through a broker-dealer. You can purchase and sell individual shares of the Fund throughout the trading day like any publicly traded

security. The Fund’s shares are listed on the Cboe BZX Exchange, Inc. (the “Exchange”). The price of the Fund’s shares is based on

market price, and because exchange-traded fund shares trade at market prices rather than net asset value (“NAV”), the Fund’s shares

may trade at a price greater than NAV (premium) or less than NAV (discount). Except when aggregated in Creation Units, the Fund’s

shares are not redeemable securities.

Investors may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase shares of the

Fund (bid) and the lowest price a seller is willing to accept for shares of the Fund (ask) when buying or selling shares of the Fund in

the secondary market (the “bid-ask spread”). Recent information about the Fund, including its NAV, market price, premiums and

discounts, and bid-ask spreads is available on the Fund’s website at https://www.kensingtonassetmanagement.com/solutions/etfs-

kamo/.

Tax Information: Distributions made by the Fund may be taxable to you as ordinary income or capital gains, unless you are a tax-

exempt organization or are investing through a tax advantaged arrangement, such as a 401(k) plan or individual retirement account.

Any withdrawals made from such tax advantaged arrangement generally will be taxable to you as ordinary income.

Payments to Broker-Dealers and Other Financial Intermediaries: If you purchase the Fund through a broker-dealer or other

financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and

related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your

salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for

more information.

KENSINGTON HEDGED PREMIUM INCOME ETF

Investment Objective: The Kensington Hedged Premium Income ETF (the “Fund”) seeks current income with the potential for capital

appreciation.

Fees and Expenses of the Fund: This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the

Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not

reflected in the table and Examples below.

| |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) | |

| |

Distribution and/or Service (12b-1) Fees | |

| |

Acquired Fund Fees and Expenses(2) | |

Total Annual Fund Operating Expenses | |

(1)Kensington Asset Management, LLC (the “Adviser”) has agreed to pay all expenses of the Fund, except for: (i) brokerage expenses and other fees, charges, taxes,

levies or expenses incurred in connection with the execution of portfolio transactions or in connection with creation and redemption transactions; (ii) fees or

expenses in connection with any arbitration, litigation or pending or threatened arbitration or litigation, including any settlements in connection therewith; (iii)

extraordinary expenses; (iv) distribution fees and expenses paid by the Fund under any distribution plan adopted pursuant to Rule 12b-1 under the Investment

Company Act of 1940, as amended (“1940 Act”); (v) interest and taxes of any kind or nature; (vi) any fees and expenses related to the provision of securities

lending services; (vii) the advisory fee payable to the Adviser; (viii) Acquired Fund Fees and Expenses; and (ix) all costs incurred in connection with shareholder

meetings and all proxy solicitations (except for such shareholder meetings and proxy solicitations related to: (a) changes to the Adviser’s investment advisory

agreement, (b) changes in control at the Adviser or a sub-adviser, (c) the election of any Board member who is an “interested person” of the Adviser (as that term

is defined under Section 2(a)(19) of the 1940 Act), (d) matters initiated by the Adviser, or (e) any other matters that directly benefit the Adviser).

(2)Acquired Fund Fees and Expenses (“AFFE”) are indirect costs of investing in other investment companies. The operating expenses in this fee table do not

correlate to the expense ratio in the Fund’s financial highlights because the financial statements include only the direct operating expenses incurred by the Fund

and not the indirect costs of investing in other investment companies.

Example: This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all your shares at the end of

those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses

remain the same. Although your actual costs may be higher or lower, based upon these assumptions your costs would be:

Portfolio Turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its

portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are

held in a taxable account at the shareholder level. These costs, which are not reflected in annual fund operating expenses or in the

example above, affect the Fund’s performance. During the most recent fiscal year ended December 31, 2025, the Fund’s portfolio

turnover rate was 9% of its average portfolio value.

Principal Investment Strategies

The Fund is an actively managed exchange-traded fund (“ETF”) that seeks to achieve its investment objective by gaining exposure to

the S&P 500® Index (the “S&P 500”). The foundation of the Fund’s strategy involves buying shares of one or more cost-effective

ETFs that track the S&P 500, providing direct exposure to the broad market's performance. The Fund simultaneously implements a

monthly call option strategy to generate income and a quarterly put option strategy to protect against large declines in the S&P 500. In

strategically buying and selling put and call options on the S&P 500, the Fund seeks to provide a partial buffer against market

downturns, as well as provide additional income in flat to down markets, but resulting in lower upside potential during strong market

rallies.

In implementing its strategy, the Fund employs a methodology similar the MerQube Hedged Premium Income Index (the

“MQKHPI”). The MQKHPI is designed to be 100% invested in the Vanguard S&P 500 ETF (VOO) while selling 1-Month call

options and purchasing 3-Month put options on the SPDR S&P 500 ETF (SPY). The MQKHPI aims to generate income from selling

call spreads while providing downside protection through the purchase of put spreads, maintaining exposure to the U.S. large-cap

equity market.

The Fund will operate similarly to the MQKHPI, but with several differences. For one, while the Fund may elect to purchase VOO

and put and call options on SPY, the Fund will be more flexible in determining which cost-effective S&P 500 ETFs to purchase and

what S&P 500 call and put options to buy and sell. Additionally, unlike the MQKHPI that holds options to expiration, the Fund will

actively manage the risk-to-reward ratio of the Fund’s option strategies. If the perceived reward (premium or cost to close out a

position) is not proportional to the risk (maximum potential loss), the Fund’s Sub-advisor will use its discretion to adjust or close the

position if determined to be advantageous to the portfolio. The Fund’s Sub-adviser will also use independent judgement in

determining what particular option spreads to buy and sell under various market conditions, unlike the fixed spreads used by the

MQKHPI.

Although the Fund’s strategy is not expected to materially change in different interest rate environments, varying levels of market

volatility will impact the relative costs of downside protection and relative option spreads. Additionally, the sequence of investment

returns will affect the various strikes prices, expiration dates, and intended purposes of the options used by the Fund, and could

significantly impact Fund’s overall performance. The Fund, based on current market conditions, seeks to achieve the best balance of

premium income/costs, downside protection, and upside potential to meet its investment objective of current income with the potential

for capital appreciation.

Monthly Call Options Strategy

Call options are derivative instruments that allow the option purchaser to contractually purchase a particular security (or the security

index) from the option issuer at a set price (the “strike price”) up to the expiration date of the options. When the issuer sells the call

option, it receives a premium from the buyer in hopes that the option will not be exercised by the buyer.

The monthly call options strategy consists of a mix of selling and purchasing call options on the S&P 500 (“S&P 500 call options”).

The Fund seeks to generate income from the premiums earned from the sold S&P 500 call options. At the same time, the Fund seeks

to realize capital appreciation from its S&P 500 ETF holdings as the S&P 500 increases in value, but with potentially reduced upside

because of the sold S&P 500 call options it uses to generate premium income. The Fund’s purchased S&P 500 call options, however,

are intended to offset this reduced upside potential and limit the risk of missing out on strong market rallies of the S&P 500.

On a regular basis, typically monthly, the Fund sells S&P 500 call options to generate premium income while simultaneously buying

“out of the money” long S&P 500 call options (i.e., options to purchase at a strike price that is higher than the current price of the

reference security or index) to hedge against the possibility that the sold S&P 500 call options are exercised because the S&P 500

increases above the strike price of the sold S&P 500 call options. For example, as the S&P 500 increases in value during the month,

the holders of the sold S&P 500 call options may be more incentivized to exercise their options which will create some losses for the

Fund. However, if the price of the S&P 500 increases above the strike price of the purchased S&P 500 call options, the Fund will be

protected from larger losses because the Fund will exercise its purchased S&P 500 call options, offsetting a portion of its losses on the

sold S&P 500 call options.

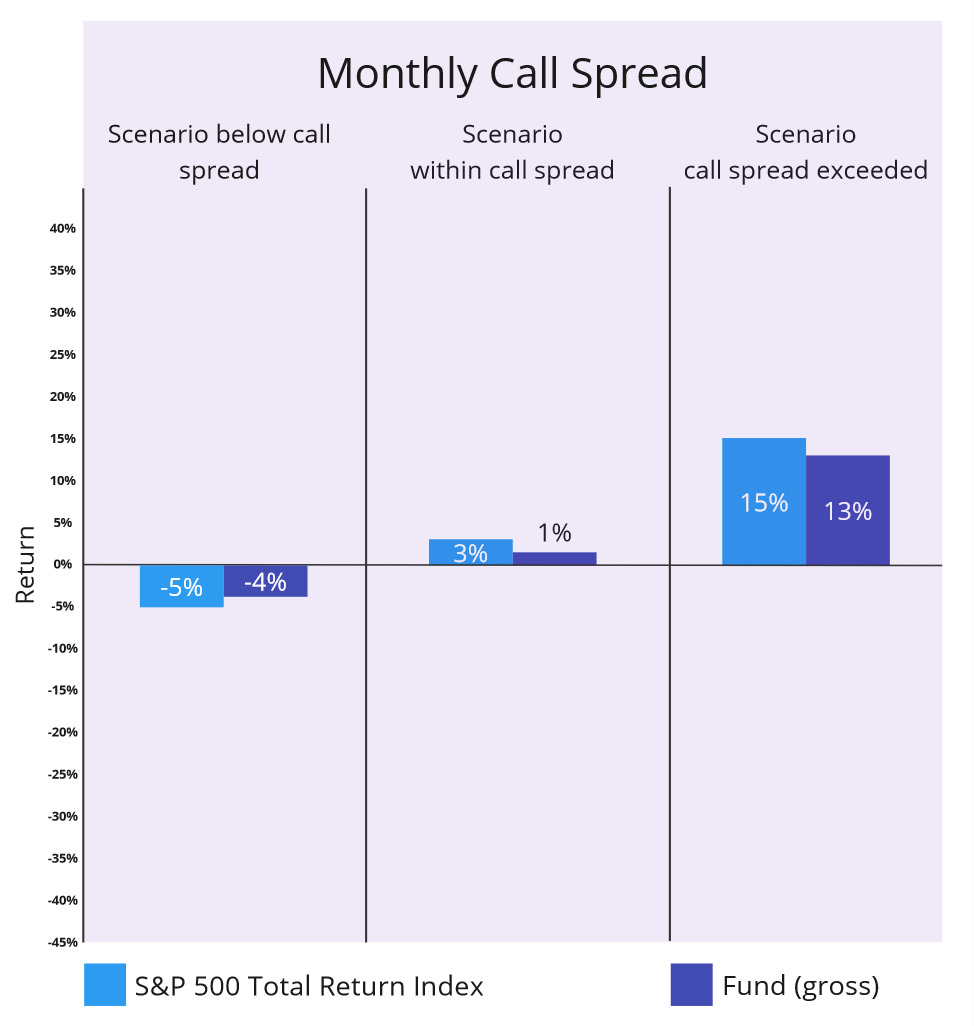

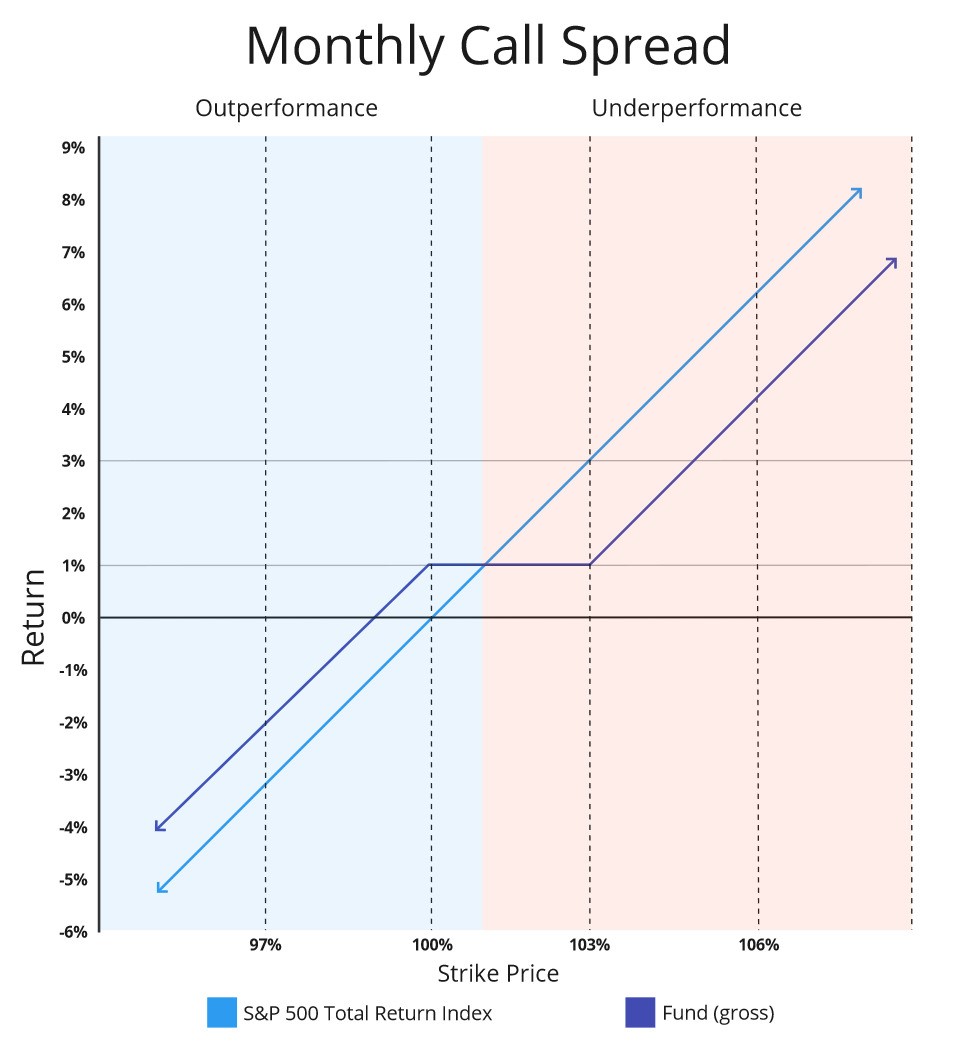

The call option strategy aims to profit from stable or declining S&P 500 prices, with the ideal scenario being the S&P 500 staying

below the strike price of the sold S&P 500 call options. At the same time, the strategy seeks to control and cap the risk of loss from

rapid gains of the S&P 500 with the purchased S&P 500 call options. While the strike prices of the S&P 500 call options may vary, the

Fund will typically sell call options with a strike price between approximately 98-105% of the current value of the S&P 500, and

purchase call options with a strike price between approximately 101-110% of the current value of the S&P 500. Once the S&P 500

appreciates by approximately 5% from its current level (the strike price of the sold call), such call spreads will begin to create a loss.

This loss will, however, will typically be capped at approximately 3% (the difference in strike prices) after the net income from the

call spreads.

Because the call option strategy is typically executed every month, it may have a larger impact on the Fund’s returns than the put

option strategy discussed below that is typically executed on a quarterly basis.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Quarterly Put Options Strategy

Put options are derivative instruments that allow the option purchaser to contractually sell a particular security (or the value of a

security index) to the option issuer at a strike price up to the expiration date of the options. When the issuer sells the put option, it

receives a premium from the buyer in hopes that the buyer will not exercise the option.

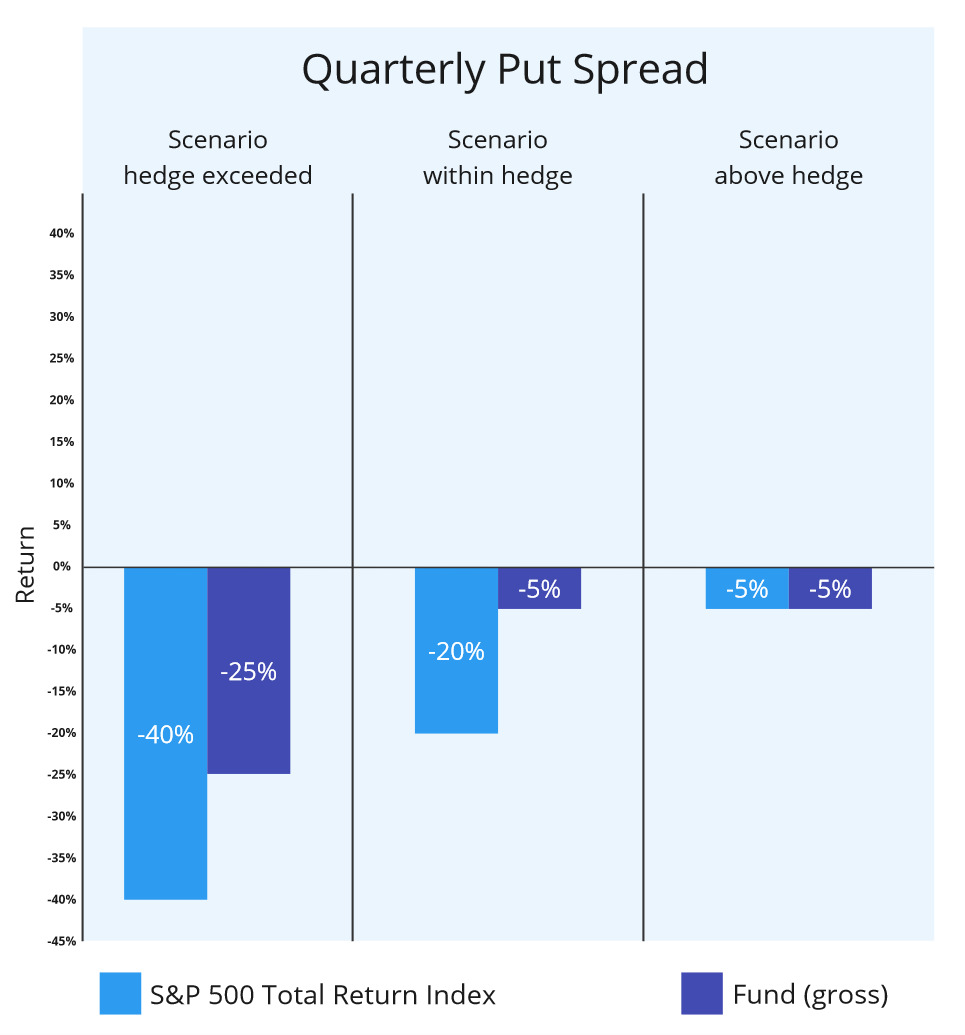

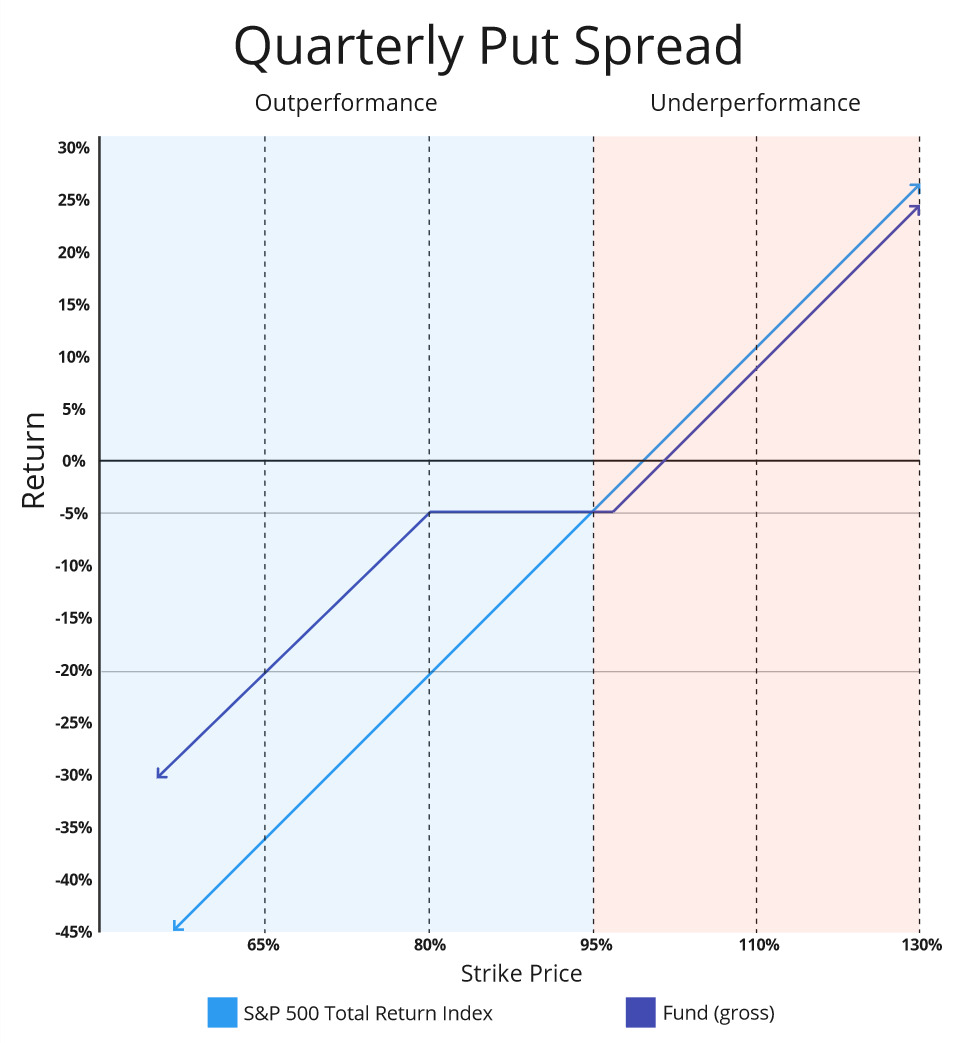

The Fund’s put options strategy, typically executed on a quarterly basis, is designed to protect against large declines in the S&P 500.

The quarterly put options strategy consists of a mix of purchased (or “long”) put options and sold (or “written”) put options on the

S&P 500 Index (“S&P 500 put options”). While the strike prices of the put options may vary, each quarter the Fund typically

purchases S&P 500 put options that are approximately 94-96% of the current S&P 500 level, paying a premium for downside

protection from a large decline in the S&P 500. The Fund simultaneously sells S&P 500 put options with a strike price that is

approximately 75-85% of the current price of the S&P 500 to generate some premium income to offset a portion of the cost of the

purchased put options. The quarterly options strategy of buying a put slightly below the current market price and selling another put

farther below the current market price is designed to protect against significant market downturns at a reduced cost. While the strike

prices of the put options will vary, the put spreads will typically provide a payment to offset losses once the S&P 500 declines by

approximately 5% (the strike price of the purchase put) but will no longer offset losses once the S&P 500 declines by more than an

approximately 20% (the difference in strike prices) after the net costs of the put spreads.

For illustrative purposes only. Figures are approximate and subject to change. Charts assume a quarterly net premium gain of 3%, which results from three

monthly call spreads and one quarterly put spread.

Expected Relative Performance of the Strategy

The Fund’s performance will vary, at times substantially, from the performance of the MQKHPI and the S&P 500. In general,

however, the Fund expects to perform somewhat in line with the MQKHPI, with the Fund’s active decisions around the

implementation of its options strategies intended to improve the Fund’s performance relative to the MQKHPI.

The Fund’s expected performance relative to the S&P 500 under various market conditions can be summarized as follows:

When the S&P 500 is Flat or Declines: Expected Outperformance. In months and quarters where the S&P 500 shows minimal

movement or decreases, the Fund’s overall performance is generally expected to also be flat to negative. However, the Fund would be

positioned to outperform the S&P 500 primarily due to the monthly premium income generated from the monthly call options.

•This anticipated relative outperformance is expected to increase during quarters where the S&P 500 declines by more than

approximately 4-6%, due to the additional downside protection from the quarterly put options.

•If the S&P 500 declines by more than approximately 20% from the purchase price of the put options, the Fund would have no

further downside protection other than the call option premiums. The Fund would participate fully in the decline of the S&P

500 until new put options are purchased.

When the S&P 500 is Up: Expected Underperformance. In months and quarters where the S&P 500 experiences an increase greater

than approximately 1% (the estimated long-term average of option premiums collected), the Fund’s overall performance is generally

expected to be positive. However, the Fund is likely to underperform the S&P 500 primarily be due to the Fund's option strategy that

is intended to sacrifice a portion of the Fund’s upside potential in return for reduced volatility and additional income.

•The underperformance for each monthly call option expiration cycle would be limited to the difference in call option strike

prices (expected to be approximately 3%) and the approximate 1% premium collected.

•If the S&P 500 rises above the strike prices of both call options, the Fund will no longer have capped appreciation until it

sells new call options.”

The Fund is considered to be non-diversified, which means it may invest a high percentage of its assets in a limited number of

investments. Additionally, the Fund’s investment strategies will involve active and frequent purchases and sales of call and put

options, but are not expected to result in high portfolio turnover.

Option Premiums – Income/Return of Capital

As part of the Fund’s options strategies, it sells (or writes) options in return for options premiums, which are expected to contribute to

the overall performance of the Fund. Distributions related to these options premiums may include a significant portion classified as

return of capital. Distributions characterized as a return of capital may reduce the Fund’s net asset value and should not be confused

with yield or income.

Principal Investment Risks

As with all funds, there is the risk that you could lose money through your investment in the Fund. The Fund is not intended to be a

complete investment program. Many factors affect the Fund’s Net Asset Value and performance. The following risks apply to the

Fund directly and indirectly through the Fund’s investment in underlying funds.

•Management Risk. The Adviser’s reliance on its proprietary investment process and the Adviser’s judgments about the

attractiveness, value, and potential appreciation of particular assets and asset classes may prove to be incorrect and may not

produce the desired results.

•Equity Securities Risk. The Fund may invest in or have exposure to equity securities. Equity securities may experience

sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect

securities markets generally or factors affecting specific industries, sectors, geographic markets, or companies in which the

Fund invests.

•ETF Risks. The Fund is an ETF, and, as a result of an ETF’s structure, it is exposed to the following risks:

◦Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited

number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited

number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events

occur, shares may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or

otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform

these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business

activities and no other entities step forward to perform their functions.

◦Cash Redemption Risk. While not expected to be a regular occurrence, the Fund’s investment strategy may require it

to redeem shares for cash or to otherwise include cash as part of its redemption proceeds. The Fund may be required

to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause

the Fund to recognize a capital gain that it might not have recognized if it had made a redemption in-kind. As a

result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was

used.

◦Costs of Buying or Selling Shares. Due to the costs of buying or selling shares, including brokerage commissions

imposed by brokers and bid-ask spreads, frequent trading of shares may significantly reduce investment results and

an investment in shares may not be advisable for investors who anticipate regularly making small investments.

◦Shares May Trade at Prices Other Than NAV. As with all ETFs, shares may be bought and sold in the secondary

market at market prices. Although it is expected that the market price of shares will approximate the Fund’s NAV,

there may be times when the market price of shares is more than the NAV intra-day (premium) or less than the NAV

intra-day (discount) due to supply and demand of shares or during periods of market volatility. This risk is

heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading

activity for shares in the secondary market, in which case such premiums or discounts may be significant. Because

securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing

exchange is open, there are likely to be deviations between the current price of a security and the security’s last

quoted price from the closed foreign market. This may result in premiums and discounts that are greater than those

experienced by domestic ETFs.

◦Trading. Although shares are listed for trading on the Cboe BZX Exchange, Inc. (the “Exchange”) and may be

traded on U.S. exchanges other than the Exchange, there can be no assurance that shares will trade with any volume,

or at all, on any stock exchange. In stressed market conditions, the liquidity of shares may begin to mirror the

liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than shares, and this

could lead to differences between the market price of the shares and the underlying value of those shares.

•Market Risk. Overall investment market risks affect the value of the Fund. Factors such as economic growth and market

conditions, interest rate levels, and political events affect U.S. and international investment markets. Additionally, unexpected

local, regional or global events, such as war; acts of terrorism; financial, political or social disruptions; natural, environmental

or man-made disasters; the spread of infectious illnesses or other public health issues (such as the COVID-19 global

pandemic); and recessions and depressions could have a significant impact on the Fund and its investments and may impair

market liquidity. Such events can cause investor fear, which can adversely affect the economies of nations, regions and the

market in general, in ways that cannot necessarily be foreseen.

•Underlying Funds Risk. Investments in underlying funds involve duplication of investment advisory fees and certain other

expenses. Each underlying fund is subject to specific risks, depending on the nature of its investment strategy. The manager

of an underlying fund may not be successful in implementing its strategy. ETF shares may trade at a market price that may be

lower (a discount) or higher (a premium) than the ETF’s net asset value. ETFs are also subject to brokerage and/or other

trading costs, which could result in greater expenses to the Fund. Because the value of ETF shares depends on the demand in

the market, the Adviser may not be able to liquidate the Fund’s holdings at the most optimal time, adversely affecting

performance.

◦Net Asset Value and Market Price Risk. The market value of ETF shares may differ from their NAV. This difference

in price may be due to the fact that the supply and demand in the market for ETF shares at any point in time is not

always identical to the supply and demand in the market for the underlying holdings. Accordingly, there may be

times when an ETF share trades at a premium or discount to its NAV.

◦Tracking Risk. ETFs in which the Fund invests will not be able to replicate exactly the performance of any indices or

prices they track because the total return generated by the securities will be reduced by transaction costs incurred in

adjusting the actual balance of the securities or derivatives. Certain securities comprising an index may, from time to

time, temporarily be unavailable, which may further impede the security’s ability to track an index.

•Derivatives Risk. In general, a derivative instrument typically involves leverage, i.e., it provides exposure to potential gain or

loss from a change in the level of the market price of the underlying security (or a basket or index) in a notional amount that