| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| - |

- |

- |

As

filed with the Securities and Exchange Commission on

Securities Act Registration No. 333-174926

Investment Company Act Registration No. 811-22549

FORM

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | x |

| Pre-Effective Amendment No. ___ | o |

| Post-Effective Amendment No. 616 | x |

and/or

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | x | |

| Amendment No. 618 | (Check Appropriate Box or Boxes) | |

(Exact Name of Registrant as Specified in Charter)

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Address of Principal Executive Offices) (Zip Code)

(631) 490-4300

(Registrant’s Telephone Number, Including Area Code)

The Corporation Trust Company

Corporate Trust Center

251 Little Falls Drive

Wilmington, DE 19808

(Name and Address of Agent for Service)

With a copy to:

| David

J. Baum, Esq. Vedder Price P.C. 1401 New York Avenue NW Washington, DC 20005 (202) 312-3375 |

Kevin

Wolf Ultimus Fund Solutions, LLC 80 Arkay Drive, Suite 110 Hauppauge, New York 11788 (631) 470-2635 |

Approximate Date of Proposed Public Offering:

It is proposed that this filing will become effective (check appropriate box):

| o | immediately upon filing pursuant to paragraph (b). | |

| x | On

|

|

| o | 60 days after filing pursuant to paragraph (a)(1). | |

| o | On pursuant to paragraph (a)(1) | |

| o | 75 days after filing pursuant to paragraph (a)(2). | |

| o | on (date) pursuant to paragraph (a)(2) of Rule 485. |

If appropriate, check the following box:

| o | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Pursuant to Rule 24f-2 under the Investment Company Act of 1940, as amended, Registrant hereby elects to register an indefinite number of shares of Registrant and any series thereof hereinafter created.

EXPLANATORY NOTE

This Post-Effective Amendment No. 616 to the Registration Statement contains the Prospectus and Statement of Additional Information describing the M International Equity Fund, M Large Cap Growth Fund, M Capital Appreciation Fund and M Large Cap Value Fund, (the “Funds”), each a series of the Registrant. This Post-Effective Amendment to the Registration Statement is organized as follows: (a) Prospectus relating to the Funds; (b) Statement of Additional Information relating to the Funds; and (c) Part C Information relating to all series of the Registrant. The Prospectuses and Statements of Additional Information for the other series of the Registrant are not affected hereby.

| M International Equity Fund |

| (Symbol: MBEQX) |

| M Large Cap Growth Fund |

| (Symbol: MTCGX) |

| M Capital Appreciation Fund |

| (Symbol: MFCPX) |

| M Large Cap Value Fund |

| (Symbol: MBOVX) |

| PROSPECTUS |

| Advised

by: M Financial Investment Advisers, Inc. 1125 NW Couch Street, Suite 900 Portland, Oregon 97209 |

||

www.mfin.com/m-funds

(866) 439-9093

The M International Equity Fund, M Large Cap Growth Fund, M Capital Appreciation Fund and M Large Cap Value Fund (each a “Fund” and collectively, the Funds”) are each a separate series of Northern Lights Fund Trust II (the “Trust”), a registered management investment company.

This prospectus provides important information about the Fund that you should know before investing. Please read it carefully and keep it for future reference.

The U.S. Securities and Exchange Commission (“SEC”) has not approved or disapproved of these securities or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

M

International Equity Fund

M Large Cap Growth Fund

M Capital Appreciation Fund

M Large Cap Value Fund

(each a series of the Northern Lights Fund Trust II (the “Trust”)

CONTENTS

| Summary Section – M INTERNATIONAL EQUITY FUND | 2 |

| Summary Section – M LARGE CAP GROWTH FUND | 10 |

| Summary Section – M CAPITAL APPRECIATION FUND | 16 |

| Summary Section – M LARGE CAP VALUE FUND | 22 |

| Additional Information About Principal Investment Strategies and Related Risks | 29 |

| M INTERNATIONAL EQUITY FUND | 29 |

| Investment Objective | 29 |

| Principal Investment Strategies | 29 |

| Other Investment Strategies | 30 |

| Investments in the Underlying Fund: Investment Objective, Strategies, and Policies of the Underlying Fund | 30 |

| M LARGE CAP GROWTH FUND | 31 |

| Investment Objective | 31 |

| Principal Investment Strategies | 31 |

| Additional Information Regarding the Security Selection Process | 31 |

| Other Investment Strategies | 32 |

| M CAPITAL APPRECIATION FUND | 32 |

| Investment Objective | 32 |

| Principal Investment Strategies | 32 |

| Other Investment Strategies | 33 |

| M LARGE CAP VALUE FUND | 33 |

| Investment Objective | 33 |

| Principal Investment Strategies | 33 |

| Other Investment Strategies | 34 |

| Security Types | 34 |

| RISKS OF INVESTING IN THE FUNDS | 35 |

| Principal Risks | 36 |

| Non-Principal Risks | 42 |

| Management of the Fund | 42 |

| The Adviser | 42 |

| Shareholder Information | 46 |

| Choosing the Appropriate Funds to Match Your Goals | 46 |

| Purchasing Shares | 46 |

| Market Timing | 46 |

| Redeeming Shares | 47 |

| Pricing of Fund Shares | 47 |

| Distributions and Taxes | 48 |

| Financial Highlights | 49 |

| Privacy Policy | 54 |

1

The Fund seeks long-term capital appreciation.

The fees and expenses reflected in the table below do not include the fees and charges associated with variable annuities or variable life insurance plans. Fees and charges for life insurance and annuity products typically include a sales load and/or a surrender charge and other charges for insurance benefits. If those fees and charges were included, the costs shown below would be higher.

The following table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investments)

| Management Fees | |

| Distribution (12b-1) Fee | |

| Other Expenses1 | |

| Acquired Fund Fees and Expenses2 | |

| Total Annual Fund Operating Expenses |

| 1 |

| 2 |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

| 1 year | 3 years | 5 years | 10 years |

| $ |

$ |

$ |

$ |

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher

portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses

or in the example, affect the Fund’s performance. During the most recent fiscal year, the Predecessor International Equity Fund’s

portfolio turnover rate was

2

To achieve the Fund’s investment objective, Dimensional Fund Advisors LP (“Dimensional”) implements an integrated investment approach that combines research, portfolio design, portfolio management, and trading functions. As further described below, the Fund’s design emphasizes long-term drivers of expected returns identified by Dimensional’s research, while balancing risk through broad diversification across companies and sectors. Dimensional’s portfolio management and trading processes further balance those long-term drivers of expected returns with shorter-term drivers of expected returns and trading costs.

The Fund is designed to purchase a broad and diverse group of equity securities of non-U.S. companies in countries with developed and emerging markets. The Fund invests in companies of all sizes, with increased exposure to smaller capitalization, lower relative price, and higher profitability companies as compared to their representation in the International Universe. For purposes of the Fund, Dimensional defines the International Universe as a market capitalization weighted set (e.g., the larger the company, the greater the proportion of the International Universe it represents) of non-U.S. companies in developed and emerging markets that have been authorized for investment as approved markets by Dimensional’s Investment Committee. The Fund may pursue its investment objective by investing its assets directly and/or indirectly in the Emerging Markets Core Equity Portfolio of DFA Investment Dimensions Group Inc. (the “Underlying Fund”). The Underlying Fund is designed to purchase a broad and diverse group of equity securities associated with emerging markets, which may include frontier markets (emerging market countries in an earlier stage of development). The Underlying Fund invests in companies of all sizes, with increased exposure to smaller capitalization, lower relative price, and higher profitability companies. As of the date of this prospectus, it is anticipated that a significant portion of the Fund’s assets will be invested indirectly through the Underlying Fund.

The Fund’s increased exposure to smaller capitalization, lower relative price, and higher profitability companies may be achieved by decreasing the allocation of the Fund’s assets to larger capitalization, higher relative price, or lower profitability companies relative to their weight in the International Universe. An equity issuer is considered to have a high relative price (i.e., a growth stock) primarily because it has a high price in relation to its book value. An equity issuer is considered to have a low relative price (i.e., a value stock) primarily because it has a low price in relation to its book value. In assessing relative price, Dimensional may consider additional factors such as price-to-cash flow or price-to-earnings ratios. An equity issuer is considered to have high profitability because it has high earnings or profits from operations in relation to its book value or assets. The criteria Dimensional uses for assessing relative price and profitability are subject to change from time to time.

Dimensional may also increase or reduce the Fund’s exposure to an eligible company, or exclude a company, based on shorter-term considerations, such as a company’s price momentum, short-run reversals, and investment characteristics. In assessing a company’s investment characteristics, Dimensional considers ratios such as recent changes in assets divided by total assets. The criteria Dimensional uses for assessing a company’s investment characteristics are subject to change from time to time. In addition, Dimensional seeks to reduce trading costs using a flexible trading approach that looks for opportunities to participate in the available market liquidity, while managing turnover and explicit transaction costs.

The Fund will normally invest at least 80% of its total assets in equity securities of issuers located in at least three countries other than the United States. These countries may include, but are not limited to, the nations of Western Europe, North and South America, Australia, Africa and Asia. This strategy is not fundamental (it may be changed without shareholder approval), but should the Fund decide to change this strategy, it will provide shareholders with at least 60 days’ notice. The Fund may invest up to 40% of its total assets in emerging markets.

The Fund may gain exposure to companies associated with approved markets by purchasing equity securities in the form of depositary receipts, which may be listed or traded outside the issuer’s domicile country. The Fund may also purchase or sell futures contracts and options on futures contracts for foreign or U.S. equity securities and indices to increase or decrease equity market exposure based on actual or expected cash inflows to or outflows from the Fund. Because many of the Fund’s investments may be denominated in foreign currencies, the Fund may enter into foreign currency exchange transactions, including foreign currency forward contracts, in connection with the settlement of foreign securities or to transfer cash balances from one currency to another currency.

3

Principal Investment Risks

As with any mutual fund, there is no guarantee that the Fund will achieve its goal. The Fund’s share price will fluctuate, which means you could lose money on your investment in the Fund. The principal risks of investing in the Fund are summarized below.

| ● | Market Risk. Investments in common stocks are subject to stock market risk. Stock prices in general may decline over short or even extended periods, regardless of the success or failure of a particular company’s operations. Stock markets tend to run in cycles, with periods when stock prices generally go up and periods when they generally go down. Common stock prices tend to go up and down more than those of bonds. |

| ● | Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates fluctuate or economic conditions deteriorate. Similarly, political events within the United States at times have resulted, and may in the future result, in a shutdown of government services, which could negatively affect the U.S. economy, decrease the value of a Fund’s investments, and increase uncertainty in or impair the operation of the U.S. or other securities markets. In recent years, the U.S. renegotiated many of its global trade relationships and also has recently imposed or threatened to impose significant import tariffs. Such actions could lead to price volatility and overall declines in U.S. and global investment markets. |

| ● | Additional Market Disruption Risk. Financial and securities markets are volatile and may be affected by political, regulatory, social, economic, and other global developments and disruptions, including those arising out of geopolitical events, armed conflict, public health emergencies (such as the spread of infectious diseases, pandemics, and epidemics), natural disasters, terrorism and governmental or quasi-governmental actions. Such changes may be rapid and unpredictable. These events may negatively affect issuers, industries and markets worldwide and adversely affect the value and liquidity of the Fund and its investments. |

In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, and these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; the potential for wider conflict; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly. In addition, rising tensions between China and Taiwan over a forced reunification have caused concerns in the region and globally. China sees self-ruled Taiwan as a breakaway province that will eventually be part of China again. Previous efforts by China’s leadership sought to bring about reunification by non-military means. Beginning in 2021, concerns escalated when China began sending military aircraft into Taiwan’s air defense zone, a self-declared area where foreign aircraft are identified, monitored and controlled in the interests of Taiwan’s national security. These actions have caused Taiwan and other countries to fear further escalation in the region. Any escalation of hostility between China and/or Taiwan would likely have a significant adverse impact on the value of investments in both countries and on economies, markets and individual securities globally, which could negatively affect the value and liquidity of the Fund’s investments. Beginning in October 2023, the Israel-Hamas war has resulted in significant loss of life and increased volatility in the Middle East. The conflict between Israel and Hamas and the involvement of the U.S. and other countries could present material uncertainty and risk with respect to a Fund’s performance and ability to achieve its investment objective. The extent of any market disruptions are impossible to predict, but could be substantial.

4

| ● | Profitability Investment Risk. High relative profitability stocks may perform differently from the market as a whole and an investment strategy purchasing these securities may cause the Fund to at times underperform equity funds that use other investment strategies. |

| ● | Value Investment Risk. Value stocks may perform differently from the market as a whole and an investment strategy purchasing these securities may cause the Fund to at times underperform equity funds that use other investment strategies. Value stocks can react differently to political, economic, and industry developments than the market as a whole and other types of stocks. Value stocks also may underperform the market for long periods of time. |

| ● | Small and Medium Capitalization Companies Risk. The Fund may invest in small and medium capitalization companies, which tend to be more vulnerable to adverse developments than larger companies. These companies may have limited product lines, markets, or financial resources, or may depend on a limited management group. They may be recently organized, without proven records of success. Their securities may trade infrequently and in limited volumes. As a result, the prices of these securities may fluctuate more than prices of securities of larger, more widely traded companies and the Fund may experience difficulty in establishing or closing out positions in these securities at prevailing market prices. Also, there may be less publicly available information about small and medium capitalization companies or less market interest in their securities as compared to larger companies, and it may take longer for the prices of the securities to reflect the full value of their issuers’ earnings potential or assets. |

| ● | Foreign Securities and Currencies Risk. Foreign securities prices may decline or fluctuate because of: (a) economic or political actions of foreign governments, and/or (b) less regulated or liquid securities markets. Investors holding these securities may also be exposed to foreign currency risk (the possibility that foreign currency will fluctuate in value against the U.S. dollar or that a foreign government will convert, or be forced to convert, its currency to another currency, changing its value against the U.S. dollar), which may make the return on an investment increase or decrease unrelated to the quality or performance of the investment itself. The Fund does not hedge foreign security risk or foreign currency risk. |

Foreign issuers may not be subject to uniform accounting, auditing and financial reporting standards and there may be less publicly available financial and other information about such issuers, as compared to U.S. issuers. A fund may have greater difficulty voting proxies, exercising shareholder rights, securing dividends and/or interest and obtaining information regarding corporate actions on a timely basis, pursuing legal remedies, and obtaining judgments with respect to foreign investments in foreign courts than with respect to domestic issuers in U.S. courts.

Depositary receipts are generally subject to the same risks as the foreign securities that they evidence or into which they may be converted. In addition, the underlying issuers of certain depositary receipts, particularly unsponsored or unregistered depositary receipts, are under no obligation to distribute shareholder communications to the holders of such receipts, or to pass through to them any voting rights with respect to the deposited securities. Depositary receipts that are not sponsored by the issuer may be less liquid and there may be less readily available public information about the issuer.

5

| ● | Emerging Markets Risk. Securities of issuers associated with emerging market countries may be subject to higher and additional risks than securities of issuers in developed foreign markets. Numerous emerging market countries have a history of, and continue to experience serious, and potentially continuing, economic and political problems. Stock markets in many emerging market countries are relatively small, expensive to trade in and generally have higher risks than those in developed markets. Securities in emerging markets also may be less liquid than those in developed markets and there are frequently government controls on foreign investments and limitations on repatriation of invested capital. Additional restrictions may be imposed under other conditions. Emerging market companies may also be held to lower disclosures, corporate governance, auditing and financial reporting standards than companies in more developed markets. Frontier market countries (emerging market countries in an earlier stage of development) generally have smaller economies or less developed capital markets and, as a result, the risks of investing in emerging market countries are magnified in frontier market countries. |

| ● | China Investments Risk. There are special risks associated with investments in China and Taiwan, which are considered emerging market countries by the Fund. The Chinese government has implemented significant economic reforms in order to liberalize trade policy, promote foreign investment in the economy, reduce government control of the economy and develop market mechanisms. But there can be no assurance that these reforms will continue or that they will be effective. Despite reforms and privatizations of companies in certain sectors, the Chinese government still exercises substantial influence over many aspects of the private sector and may own or control many companies. The Chinese government continues to maintain a major role in economic policy making and investing in China involves risks of losses due to expropriation, nationalization, confiscation of assets and property, and the imposition of restrictions on foreign investments and on repatriation of capital invested. Further, investors in Chinese issuers may have difficulty obtaining information regarding the issuer, particularly high-quality and reliable financial reporting. |

A reduction in spending on Chinese products and services or the institution of additional tariffs or other trade barriers, including as a result of heightened trade tensions between China and the United States may also have an adverse impact on the Chinese economy. In addition, investments in Taiwan could be adversely affected by its political and economic relationship with China. Certain securities issued by companies located or operating in China, such as China A-shares, are also subject to trading restrictions, quota limitations and less market liquidity, which could pose risks to the Fund. The Fund may also invest in special structures that utilize contractual arrangements to provide exposure to certain Chinese companies, known as variable interest entities (“VIEs”) that operate in sectors in which China restricts and/or prohibits foreign investments. Investments involving a VIE structure may pose additional risks because such investments are made through a company whose interests in the underlying operating company are established through contract rather than through direct equity ownership. The Chinese government’s acceptance of the VIE structure is evolving. Investing through a VIE does not offer the same level of investor protection as direct ownership, and is subject to additional risks as it is uncertain whether Chinese officials and regulators will withdraw their acceptance of the structure or whether Chinese courts or arbitration bodies would decline to enforce the contractual rights of foreign investors, each of which would likely have significant, detrimental, and possibly permanent losses on the value of such investments.

| ● | Fund of Funds Risk. The investment performance of the Fund is affected by the investment performance of the Underlying Fund in which the Fund invests. The ability of the Fund to achieve its investment objective depends on the ability of the Underlying Fund to meet its investment objective and on Dimensional’s decisions regarding the allocation of the Fund’s assets to the Underlying Fund. The Fund may allocate assets to the Underlying Fund or asset class that underperforms other funds or asset classes. There can be no assurance that the investment objective of the Fund or the Underlying Fund will be achieved. When the Fund invests in the Underlying Fund, investors are exposed to a proportionate share of the expenses of the Underlying Fund in addition to the expenses of the Fund. Through its investments in the Underlying Fund, the Fund is subject to the risks of the Underlying Fund’s investments. |

6

| ● | Management Risk. The Fund is subject to management risk because it is actively managed. Management risk is the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause the Fund to incur losses or underperform relative to its benchmarks or other investments with similar investment objectives. The sub-adviser will apply its investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these will produce the desired results. |

| ● | Liquidity Risk. Liquidity risk exists when investments are difficult to sell as the result of low trading volume, lack of market makers, and/or legal restrictions. Illiquid securities may prevent the Fund from entering into security transactions at advantageous times or prices, potentially reducing the return of the Fund’s portfolio. Investments in smaller market capitalizations and over-the-counter markets have greater exposure to liquidity risk. |

| ● | Derivatives Risk. Derivatives are instruments, such as futures, and options thereon, and foreign currency forward contracts, whose value is derived from that of other assets, rates or indices. The use of derivatives for non-hedging purposes may be considered to carry more risk than other types of investments. When the Fund uses derivatives, the Fund will be directly exposed to the risks of those derivatives. Derivative instruments are subject to a number of risks including counterparty and credit risk (the risk that the derivative counterparty will not fulfill its contractual obligations, whether because of bankruptcy or other default), settlement risk (the risk faced when one party to a transaction has performed its obligations under a contract but has not yet received value from its counterparty), interest rate risk (the risk that certain derivatives are more sensitive to interest rate changes and market price fluctuations than other securities), liquidity risk, market risk, and management risk, as well as the risk of improper valuation. Changes in the value of a derivative may not correlate perfectly with the underlying asset, rate or index, and the Fund could lose more than the principal amount invested. |

| ● | Operational Risk. Operational risks include human error, changes in personnel, system changes, faults in communication, and failures in systems, technology, or processes. Various operational events or circumstances are outside the sub-adviser’s control, including instances at third parties. The Fund and the sub-adviser seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address these risks. |

| ● | Cyber Security Risk. The Fund’s and its service providers’ use of internet, technology and information systems may expose the Fund to potential risks linked to cyber security breaches of those technological or information systems. Cyber security breaches, amongst other things, could allow an unauthorized party to gain access to proprietary information, customer data, or fund assets, or cause the Fund and/or its service providers to suffer data corruption or lose operational functionality. |

7

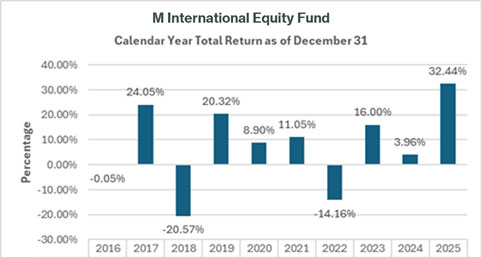

The

following information may give some indication of the risks of investing in the Fund. The Fund is the successor to the Predecessor International

Equity Fund, a mutual fund with identical investment objectives, policies, and restrictions, as a result of the reorganization of the

Predecessor International Equity Fund into the Fund on April 24, 2026. The performance provided in the bar chart and table is that of

the Predecessor International Equity Fund.

The

table below shows the Predecessor International Equity Fund’s average annual total returns for the periods indicated and how those returns

compare to those of the MSCI ACWI (All Country World Index) ex USA IMI Index and the MSCI All Country World ex USA Index. You cannot

invest directly in an index.

Average Annual Total Returns

(for the periods ended December 31, 2025)

| One Year | Five Years | Ten Years | ||||

| Predecessor International Equity Fund | ||||||

| MSCI ACWI (All Country World Index) ex USA IMI Index1 |

| 1 |

8

Fund Management

M Financial Investment Advisers, Inc. is the investment adviser for the Fund and Dimensional is the sub-adviser for the Fund.

The Fund is managed by a team of investment professionals from Dimensional. The following persons are responsible for coordinating the day-to-day management of the Fund’s portfolio:

| Portfolio Manager | Since | Title | ||

| Jed S. Fogdall | December 2018 for the Predecessor International Equity Fund | Global Head of Portfolio Management, Chairman of the Investment Committee, Vice President and Senior Portfolio Manager of Dimensional | ||

| Mary T. Phillips, CFA | December 2018 for the Predecessor International Equity Fund | Deputy Head of Portfolio Management, North America, Member of the Investment Committee, Vice President and Senior Portfolio Manager of Dimensional | ||

| William B. Collins-Dean, CFA | December 2018 for the Predecessor International Equity Fund | Vice President and Senior Portfolio Manager of Dimensional | ||

Other Important Information

For important information about Purchase and Redemption of Fund Shares, Tax Information and Payments to Insurance Companies and their Affiliates, please turn to page 28 of this prospectus.

9

The Fund seeks long-term capital appreciation.

The fees and expenses reflected in the table below do not include the fees and charges associated with variable annuities or variable life insurance plans. Fees and charges for life insurance and annuity products typically include a sales load and/or a surrender charge and other charges for insurance benefits. If those fees and charges were included, the costs shown below would be higher.

The following table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investments)

| Management Fees | |||

| Distribution (12b-1) Fee | |||

| Other Expenses1 | |||

| Total Annual Fund Operating Expenses |

| 1 |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

| 1 year | 3 years | 5 years | 10 years |

| $ |

$ |

$ |

$ |

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher

portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses

or in the example, affect the Fund’s performance. During the most recent fiscal year, the Predecessor Large Cap Growth Fund’s

portfolio turnover rate was

The Fund will normally invest at least 80% of its total assets in domestic equity securities of U.S. large capitalization (“large-cap”) securities. The Fund seeks to achieve its objective by investing primarily in the common stock of large-sized U.S. companies. The investment strategy of Federated MDTA LLC (“Federated”), the Fund’s sub-adviser, utilizes a large-cap growth approach by selecting most of its investments from companies listed in the Russell 1000® Growth Index, an index that measures the performance of those companies with higher price-to-book ratios and higher forecasted growth values within the large-cap segment of the U.S. equity universe, which includes the 1,000 largest U.S. companies by market capitalization. Federated considers a company to be large-cap if it falls within the market capitalization range of the Russell 1000® Growth Index. As the Fund’s sector exposure approximates the Russell 1000® Growth Index, the Fund may, from time to time, have large allocations to certain broad market sectors, such as technology, consumer discretionary and healthcare. As of March 31, 2025, companies in the Russell 1000® Growth Index ranged in market capitalization from $681 million to $3.3 trillion.

10

The Fund is classified as a non-diversified mutual fund, which means that the Fund may invest a larger percentage of its assets in the securities of a small number of issuers than a diversified fund.

Federated implements its strategy using a quantitative model driven by fundamental and technical stock selection variables. This process seeks to impose strict discipline over stock selection, unimpeded by market or manager psychology. It seeks to maximize compound annual return while controlling risk. The process also takes into account trading costs in an effort to ensure that trades are generated only to the extent they are expected to be profitable on an after-trading-cost basis. Additionally, risk is controlled through diversification constraints which limit exposure to individual companies as well as groups of correlated companies.

This strategy to invest at least 80% of its total assets in domestic equity securities of U.S. large-cap securities is not fundamental (it may be changed without shareholder approval), but should the Fund decide to change this strategy, it will provide shareholders with at least 60 days’ notice.

The Fund actively trades its portfolio securities in an attempt to achieve its investment objective.

Principal Investment Risks

As with any mutual fund, there is no guarantee that the Fund will achieve its goals. The Fund’s share price will fluctuate, which means you could lose money on your investment in the Fund. The principal risks of investing in the Fund are summarized below.

| ● | Market Risk. Investments in common stocks are subject to stock market risk. Stock prices in general may decline over short or even extended periods, regardless of the success or failure of a particular company’s operations. Stock markets tend to run in cycles, with periods when stock prices generally go up and periods when they generally go down. Common stock prices tend to go up and down more than those of bonds. |

| ● | Active Trading Risk. Active trading will cause the Fund to have an increased portfolio turnover rate and increase the Fund’s trading costs, which may have an adverse impact on the Fund’s performance. |

| ● | Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates fluctuate or economic conditions deteriorate. Similarly, political events within the United States at times have resulted, and may in the future result, in a shutdown of government services, which could negatively affect the U.S. economy, decrease the value of a Fund’s investments, and increase uncertainty in or impair the operation of the U.S. or other securities markets. In recent years, the U.S. renegotiated many of its global trade relationships and also has recently imposed or threatened to impose significant import tariffs. Such actions could lead to price volatility and overall declines in U.S. and global investment markets. |

| ● | Additional Market Disruption Risk. Financial and securities markets are volatile and may be affected by political, regulatory, social, economic, and other global developments and disruptions, including those arising out of geopolitical events, armed conflict, public health emergencies (such as the spread of infectious diseases, pandemics, and epidemics), natural disasters, terrorism and governmental or quasi-governmental actions. Such changes may be rapid and unpredictable. These events may negatively affect issuers, industries and markets worldwide and adversely affect the value and liquidity of the Fund and its investments. |

11

In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, and these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; the potential for wider conflict; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly. In addition, rising tensions between China and Taiwan over a forced reunification have caused concerns in the region and globally. China sees self-ruled Taiwan as a breakaway province that will eventually be part of China again. Previous efforts by China’s leadership sought to bring about reunification by non-military means. Beginning in 2021, concerns escalated when China began sending military aircraft into Taiwan’s air defense zone, a self-declared area where foreign aircraft are identified, monitored and controlled in the interests of Taiwan’s national security. These actions have caused Taiwan and other countries to fear further escalation in the region. Any escalation of hostility between China and/or Taiwan would likely have a significant adverse impact on the value of investments in both countries and on economies, markets and individual securities globally, which could negatively affect the value and liquidity of the Fund’s investments. Beginning in October 2023, the Israel-Hamas war has resulted in significant loss of life and increased volatility in the Middle East. The conflict between Israel and Hamas and the involvement of the U.S. and other countries could present material uncertainty and risk with respect to a Fund’s performance and ability to achieve its investment objective. The extent of any market disruptions are impossible to predict, but could be substantial.

| ● | Growth Securities Risk. The Fund invests in growth securities, which may be more volatile than other types of investments, may perform differently than the market as a whole and may underperform when compared to securities with different investment parameters. Under certain market conditions, growth securities have performed better during the later stages of economic recovery. Therefore, growth securities may go in and out of favor over time. |

| ● | Large-Capitalization Investing Risk. Large-capitalization stocks as a group could fall out of favor with the market, causing the Fund to underperform investments that focus on small- or medium-capitalization stocks. Larger, more established companies may be slow to respond to challenges and may grow more slowly than smaller companies. |

| ● | Sector Risk. Because the Fund may allocate relatively more assets to certain industry sectors than others, the Fund’s performance may be more susceptible to any developments which affect those sectors emphasized by the Fund. |

| ● | Quantitative Modeling Risk. The Fund employs quantitative models as a management technique. These models examine multiple economic factors using various proprietary and third-party data. The results generated by quantitative analysis may perform differently than expected and may negatively affect Fund performance for various reasons (for example, human judgment, data imprecision, software or other technology malfunctions, or programming inaccuracies). |

12

| ● | Management Risk. The Fund is subject to management risk because it is actively managed. Management risk is the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause the Fund to incur losses or underperform relative to its benchmarks or other investments with similar investment objectives. The sub-adviser will apply its investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these will produce the desired results. |

| ● | Operational Risk. Operational risks include human error, changes in personnel, system changes, faults in communication, and failures in systems, technology, or processes. Various operational events or circumstances are outside the sub-adviser’s control, including instances at third parties. The Fund and the sub-adviser seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address these risks. |

| ● | Non-Diversification Risk. The Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund, which means it may have more exposure to the price movements of a single security or small group of securities than funds that diversify their investments among many companies. |

| ● | Cyber Security Risk. The Fund’s and its service providers’ use of internet, technology and information systems may expose the Fund to potential risks linked to cyber security breaches of those technological or information systems. Cyber security breaches, amongst other things, could allow an unauthorized party to gain access to proprietary information, customer data, or fund assets, or cause the Fund and/or its service providers to suffer data corruption or lose operational functionality. |

| ● | Liquidity Risk. Liquidity risk exists when investments are difficult to sell as the result of low trading volume, lack of market makers, and/or legal restrictions. Illiquid securities may prevent the Fund from entering into security transactions at advantageous times or prices, potentially reducing the return of the Fund’s portfolio. Investments in smaller market capitalizations and over-the-counter markets have greater exposure to liquidity risk. |

13

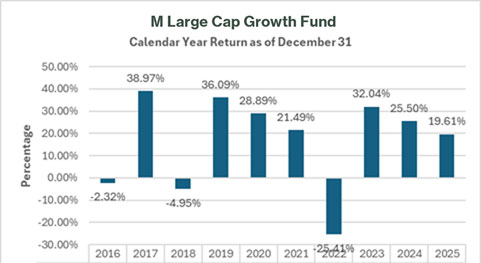

The

following information may give some indication of the risks of investing in the Fund. The Fund is the successor to the Predecessor Large

Cap Growth Fund, a mutual fund with identical investment objectives, policies, and restrictions, as a result of the reorganization of

the Predecessor Large Cap Growth Fund into the Fund on April 24, 2026. The performance provided in the bar chart and table is that of

the Predecessor Large Cap Growth Fund.

The

table below shows the Predecessor Large Cap Growth Fund’s average annual total returns for the periods indicated and how those returns

compare to those of the S&P 500® Index and the Russell 1000® Growth

Index. You cannot invest directly in an index.

Average Annual Total Returns

(for the periods ended December 31, 2025)

| One Year | Five Years | Ten Years | ||||

| Predecessor Large Cap Growth Fund | ||||||

| S&P 500® Index1 | ||||||

| Russell 1000® Growth Index2 ( |

| 1 |

| 2 |

14

Fund Management

M Financial Investment Advisers, Inc. is the investment adviser for the Fund and Federated is the sub-adviser for the Fund.

The Fund is managed by a team of investment professionals from Federated. The following persons are primarily responsible for the day-to-day management of the Fund’s portfolio:

| Portfolio Manager | Since | Title | ||

| Daniel J. Mahr, CFA | May

2025 for the Predecessor Large Cap Growth Fund |

Portfolio Manager | ||

| Damien Zhang, CFA | May

2025 for the Predecessor Large Cap Growth Fund |

Portfolio Manager | ||

| Frederick L. Konopka, CFA | May

2025 for the Predecessor Large Cap Growth Fund |

Portfolio Manager | ||

| John Paul Lewicke | May

2025 for the Predecessor Large Cap Growth Fund |

Portfolio Manager | ||

Each portfolio manager is primarily and jointly responsible for the day-to-day management of the Fund.

Other Important Information

For important information about Purchase and Redemption of Fund Shares, Tax Information and Payments to Insurance Companies and their Affiliates, please turn to page 28 of this prospectus.

15

The Fund seeks long-term capital appreciation.

The fees and expenses reflected in the table below do not include the fees and charges associated with variable annuities or variable life insurance plans. Fees and charges for life insurance and annuity products typically include a sales load and/or a surrender charge and other charges for insurance benefits. If those fees and charges were included, the costs shown below would be higher.

The following table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investments)

| Management Fees | ||

| Distribution (12b-1) Fee | ||

| Other Expenses1 | ||

| Total Annual Fund Operating Expenses | ||

| 1 |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

| 1 year | 3 years | 5 years | 10 years |

| $ |

$ |

$ |

$ |

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher

portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses

or in the example, affect the Predecessor Capital Appreciation Fund’s performance. During the most recent fiscal year, the Fund’s

portfolio turnover rate was

The Fund principally invests in common stock of U.S. companies of all sizes, with emphasis on stocks of companies with capitalizations that are consistent with the capitalizations of those companies found in the Russell 2500® Index. As of March 31, 2025, the market capitalization range of companies in the Russell 2500® Index was between approximately $567.8 million and $31.4 billion. The Fund may invest up to 15% of the value of its total assets in equity securities of foreign issuers. The Fund’s sub-adviser, Frontier Capital Management Company, LLC (“Frontier”) seeks long-term capital appreciation by employing a Growth-At-A-Reasonable-Price approach to identify, in its view, the best risk/reward investment ideas in the U.S. small- and mid-capitalization equity universe. Frontier purchases companies that, in its view, have above-average earnings growth potential and are available at reasonable valuations. Frontier’s philosophy combines rigorous bottom-up fundamental analysis with a proven investment process.

16

Frontier may sell stocks for a number of reasons, including when price objectives are reached, fundamental conditions have changed so that future earnings progress is likely to be adversely affected, or a stock is fully invested and an attractive, new opportunity causes the sale of a current holding with less appreciation potential. Frontier does not sell stocks solely on changes to a company’s market capitalization.

Principal Investment Risks

As with any mutual fund, there is no guarantee that the Fund will achieve its goals. The Fund’s share price will fluctuate which, means you could lose money on your investment in the Fund. The principal risks of investing in the Fund are summarized below.

| ● | Small and Medium Capitalization Companies Risk. The Fund may invest in small and medium capitalization companies, which tend to be more vulnerable to adverse developments than larger companies. These companies may have limited product lines, markets, or financial resources, or may depend on a limited management group. They may be recently organized, without proven records of success. Their securities may trade infrequently and in limited volumes. As a result, the prices of these securities may fluctuate more than prices of securities of larger, more widely traded companies and the Fund may experience difficulty in establishing or closing out positions in these securities at prevailing market prices. Also, there may be less publicly available information about small and medium capitalization companies or less market interest in their securities as compared to larger companies, and it may take longer for the prices of the securities to reflect the full value of their issuers’ earnings potential or assets. |

| ● | Market Risk. Investments in common stocks are subject to stock market risk. Stock prices in general may decline over short or even extended periods, regardless of the success or failure of a particular company’s operations. Stock markets tend to run in cycles, with periods when stock prices generally go up and periods when they generally go down. Common stock prices tend to go up and down more than those of bonds. |

| ● | Growth Securities Risk. The Fund invests in growth securities, which may be more volatile than other types of investments, may perform differently than the market as a whole and may underperform when compared to securities with different investment parameters. Under certain market conditions, growth securities have performed better during the later stages of economic recovery. Therefore, growth securities may go in and out of favor over time. |

| ● | Management Risk. The Fund is subject to management risk because it is actively managed. Management risk is the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause the Fund to incur losses or underperform relative to its benchmarks or other investments with similar investment objectives. The sub-adviser will apply its investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these will produce the desired results. |

| ● | Foreign Securities and Currencies Risk. Foreign securities prices may decline or fluctuate because of: (a) economic or political actions of foreign governments, and/or (b) less regulated or liquid securities markets. Investors holding these securities may also be exposed to foreign currency risk (the possibility that foreign currency will fluctuate in value against the U.S. dollar or that a foreign government will convert, or be forced to convert, its currency to another currency, changing its value against the U.S. dollar), which may make the return on an investment increase or decrease unrelated to the quality or performance of the investment itself. The Fund does not hedge foreign security risk or foreign currency risk. |

17

Foreign issuers may not be subject to uniform accounting, auditing and financial reporting standards and there may be less publicly available financial and other information about such issuers, as compared to U.S. issuers. A fund may have greater difficulty voting proxies, exercising shareholder rights, securing dividends and/or interest and obtaining information regarding corporate actions on a timely basis, pursuing legal remedies, and obtaining judgments with respect to foreign investments in foreign courts than with respect to domestic issuers in U.S. courts.

Depositary receipts are generally subject to the same risks as the foreign securities that they evidence or into which they may be converted. In addition, the underlying issuers of certain depositary receipts, particularly unsponsored or unregistered depositary receipts, are under no obligation to distribute shareholder communications to the holders of such receipts, or to pass through to them any voting rights with respect to the deposited securities. Depositary receipts that are not sponsored by the issuer may be less liquid and there may be less readily available public information about the issuer.

| ● | Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates fluctuate or economic conditions deteriorate. Similarly, political events within the United States at times have resulted, and may in the future result, in a shutdown of government services, which could negatively affect the U.S. economy, decrease the value of a Fund’s investments, and increase uncertainty in or impair the operation of the U.S. or other securities markets. In recent years, the U.S. renegotiated many of its global trade relationships and also has recently imposed or threatened to impose significant import tariffs. Such actions could lead to price volatility and overall declines in U.S. and global investment markets. |

| ● | Additional Market Disruption Risk. Financial and securities markets are volatile and may be affected by political, regulatory, social, economic, and other global developments and disruptions, including those arising out of geopolitical events, armed conflict, public health emergencies (such as the spread of infectious diseases, pandemics, and epidemics), natural disasters, terrorism and governmental or quasi-governmental actions. Such changes may be rapid and unpredictable. These events may negatively affect issuers, industries and markets worldwide and adversely affect the value and liquidity of the Fund and its investments. |

In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, and these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; the potential for wider conflict; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly. In addition, rising tensions between China and Taiwan over a forced reunification have caused concerns in the region and globally. China sees self-ruled Taiwan as a breakaway province that will eventually be part of China again. Previous efforts by China’s leadership sought to bring about reunification by non-military means. Beginning in 2021, concerns escalated when China began sending military aircraft into Taiwan’s air defense zone, a self-declared area where foreign aircraft are identified, monitored and controlled in the interests of Taiwan’s national security. These actions have caused Taiwan and other countries to fear further escalation in the region. Any escalation of hostility between China and/or Taiwan would likely have a significant adverse impact on the value of investments in both countries and on economies, markets and individual securities globally, which could negatively affect the value and liquidity of the Fund’s investments. Beginning in October 2023, the Israel-Hamas war has resulted in significant loss of life and increased volatility in the Middle East. The conflict between Israel and Hamas and the involvement of the U.S. and other countries could present material uncertainty and risk with respect to a Fund’s performance and ability to achieve its investment objective. The extent of any market disruptions are impossible to predict, but could be substantial.

18

| ● | Liquidity Risk. Liquidity risk exists when investments are difficult to sell as the result of low trading volume, lack of market makers, and/or legal restrictions. Illiquid securities may prevent the Fund from entering into security transactions at advantageous times or prices, potentially reducing the return of the Fund’s portfolio. Investments in smaller market capitalizations and over-the-counter markets have greater exposure to liquidity risk. |

| ● | Operational Risk. Operational risks include human error, changes in personnel, system changes, faults in communication, and failures in systems, technology, or processes. Various operational events or circumstances are outside the sub-adviser’s control, including instances at third parties. The Fund and the sub-adviser seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address these risks. |

| ● | Cyber Security Risk. The Fund’s and its service providers’ use of internet, technology and information systems may expose the Fund to potential risks linked to cyber security breaches of those technological or information systems. Cyber security breaches, amongst other things, could allow an unauthorized party to gain access to proprietary information, customer data, or fund assets, or cause the Fund and/or its service providers to suffer data corruption or lose operational functionality. |

19

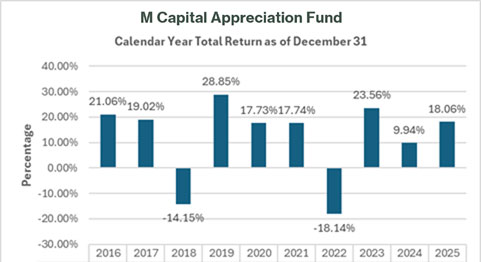

The

following information may give some indication of the risks of investing in the Fund. The Fund is the successor to the Predecessor Capital

Appreciation Fund, a mutual fund with identical investment objectives, policies, and restrictions, as a result of the reorganization

of the Predecessor Capital Appreciation Fund into the Fund on April 24, 2026. The performance provided in the bar chart and table is

that of the Predecessor Capital Appreciation Fund.

The table below shows the Predecessor Capital Appreciation Fund’s average annual total returns for the periods indicated and how those returns compare to those of the S&P 500® Index and the Russell 2500® Index. You cannot invest directly in an index. The Index returns are calculated on a total return basis and reflects no deduction for fees, expenses or taxes.

Average Annual Total Returns

(for the periods ended December 31, 2025)

| One Year | Five Years | Ten Years | ||||

| Predecessor Capital Appreciation Fund | ||||||

| S&P 500® Index1 | ||||||

| Russell 2500® Index2 ( |

| 1 | |

| 2 |

20

Fund Management

M Financial Investment Advisers, Inc. is the investment adviser for the Fund and Frontier is the sub-adviser for the Fund.’

The following people are primarily responsible for the day-to-day management of the Fund’s portfolio:

| Portfolio Manager | Since | Title | ||

| Andrew B. Bennett, CFA | December 2013 for the Predecessor Capital Appreciation Fund | Portfolio Manager | ||

| Peter G. Kuechle | April 2018 for the Predecessor Capital Appreciation Fund | Portfolio Manager |

Other Important Information

For

important information about Purchase and Redemption of Fund Shares, Tax Information and Payments to Insurance Companies and their Affiliates,

please turn to page 28 of this prospectus.

21

The Fund seeks long-term capital appreciation.

The fees and expenses reflected in the table below do not include the fees and charges associated with variable annuities or variable life insurance plans. Fees and charges for life insurance and annuity products typically include a sales load and/or a surrender charge and other charges for insurance benefits. If those fees and charges were included, the costs shown below would be higher.

The following table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investments)

| Management Fees | ||

| Distribution (12b-1) Fee | ||

| Other Expenses1 | ||

| Total Annual Fund Operating Expenses |

| 1 |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

| 1 year | 3 years | 5 years | 10 years |

| $ |

$ |

$ |

$ |

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher

portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses

or in the example, affect the Fund’s performance. During the most recent fiscal year, the Predecessor Large Cap Value Fund’s

portfolio turnover rate was

The Fund normally invests at least 80% of its net assets, plus the amount of borrowings for investment purposes, if any, in issuers domiciled, or having their principal activities, in the United States, at the time of investment or other instruments with similar economic characteristics. In addition, the Fund normally invests at least 80% of its net assets in equity securities of large capitalization companies. Brandywine Global Investment Management, LLC (“Brandywine”), the Fund’s sub-adviser, defines “large capitalization” companies as those companies with market capitalizations similar to companies in the Russell 1000® Index. As of March 31, 2025, the market capitalization range of companies in the Russell 1000® Index was between approximately $273 million and $3.3 trillion. This strategy is not fundamental (it may be changed without shareholder approval), but should the Fund decide to change this strategy, it will provide shareholders with at least 60 days’ notice.

22

The Fund invests primarily in equity securities that, in Brandywine’s opinion, are undervalued or out of favor. Brandywine invests in securities that meet its value criteria, primarily price-to-earnings, price-to-book, price momentum and share change and quality, based on both quantitative and fundamental analysis. The Fund expects to hold approximately 175-250 stocks under normal market conditions.

Brandywine bases portfolio price targets on quantitative criteria determined in its sell process. Brandywine’s systems update these quantitatively determined buy and sell limits on a daily basis. Buy candidates must have a price that qualifies the stock as a value such that the price-to-earnings ratio is in the lower 40% of its universe or the price-to-book is in the lower 25% of its universe at time of purchase. Additionally, the current price compared to the price nine months ago must place it above the lower quartile of other universe stocks when ranked by nine-month price momentum and the change in shares outstanding over the past year must place it below the upper quartile.

Sell candidates will have a price that when compared to earnings and book place the stock above the median on a price-to-earnings basis and above the 40th percentile on a price-to-book basis. If a stock’s price declines relative to the universe such that it falls to the lower 10% of stocks as ranked on nine-month price momentum or the company issues sufficient shares to rank among the top 10% largest issuers (as a percentage of shares outstanding) in the year, the holding will be a sell candidate. Additionally, a stock will be sold if the capitalization falls 20% below the minimum purchase capitalization criteria.

Brandywine may modify buy and sell trigger points and decisions only due to tracking error considerations, trading opportunities or limitations such as position, industry or sector size. Brandywine does not violate its buy and sell rules based on analyst affinity for the stock. Its investment process requires disciplined buy and sell decisions rules with carefully outlined exceptions.

If a security experiences a severe fundamental deterioration event that is not captured in the price change, share change or valuation rules, Brandywine will initiate a sell. The rank order of the most common occurrences are price momentum, valuation expansion into the sell range, share issuance or fundamental deterioration.

Principal Investment Risks

As with any mutual fund, there is no guarantee that the Fund will achieve its goals. The Fund’s share price will fluctuate, which means you could lose money on your investment in the Fund. The principal risks of investing in the Fund are summarized below.

| ● | Large-Capitalization Investing Risk. Large-capitalization stocks as a group could fall out of favor with the market, causing the Fund to underperform investments that focus on small- or medium-capitalization stocks. Larger, more established companies may be slow to respond to challenges and may grow more slowly than smaller companies. |

| ● | Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates fluctuate or economic conditions deteriorate. Similarly, political events within the United States at times have resulted, and may in the future result, in a shutdown of government services, which could negatively affect the U.S. economy, decrease the value of a Fund’s investments, and increase uncertainty in or impair the operation of the U.S. or other securities markets. In recent years, the U.S. renegotiated many of its global trade relationships and also has recently imposed or threatened to impose significant import tariffs. Such actions could lead to price volatility and overall declines in U.S. and global investment markets. |

23

| ● | Additional Market Disruption Risk. Financial and securities markets are volatile and may be affected by political, regulatory, social, economic, and other global developments and disruptions, including those arising out of geopolitical events, armed conflict, public health emergencies (such as the spread of infectious diseases, pandemics, and epidemics), natural disasters, terrorism and governmental or quasi-governmental actions. Such changes may be rapid and unpredictable. These events may negatively affect issuers, industries and markets worldwide and adversely affect the value and liquidity of the Fund and its investments. |

In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, and these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; the potential for wider conflict; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly. In addition, rising tensions between China and Taiwan over a forced reunification have caused concerns in the region and globally. China sees self-ruled Taiwan as a breakaway province that will eventually be part of China again. Previous efforts by China’s leadership sought to bring about reunification by non-military means. Beginning in 2021, concerns escalated when China began sending military aircraft into Taiwan’s air defense zone, a self-declared area where foreign aircraft are identified, monitored and controlled in the interests of Taiwan’s national security. These actions have caused Taiwan and other countries to fear further escalation in the region. Any escalation of hostility between China and/or Taiwan would likely have a significant adverse impact on the value of investments in both countries and on economies, markets and individual securities globally, which could negatively affect the value and liquidity of the Fund’s investments. Beginning in October 2023, the Israel-Hamas war has resulted in significant loss of life and increased volatility in the Middle East. The conflict between Israel and Hamas and the involvement of the U.S. and other countries could present material uncertainty and risk with respect to a Fund’s performance and ability to achieve its investment objective. The extent of any market disruptions are impossible to predict, but could be substantial.

| ● | Market Risk. Investments in common stocks are subject to stock market risk. Stock prices in general may decline over short or even extended periods, regardless of the success or failure of a particular company’s operations. Stock markets tend to run in cycles, with periods when stock prices generally go up and periods when they generally go down. Common stock prices tend to go up and down more than those of bonds. |

| ● | Value Investment Risk. Value stocks may perform differently from the market as a whole and an investment strategy purchasing these securities may cause the Fund to at times underperform equity funds that use other investment strategies. Value stocks can react differently to political, economic, and industry developments than the market as a whole and other types of stocks. Value stocks also may underperform the market for long periods of time. |

24

| ● | Management Risk. The Fund is subject to management risk because it is actively managed. Management risk is the chance that security selection or focus on securities in a particular style, market sector or group of companies will cause the Fund to incur losses or underperform relative to its benchmarks or other investments with similar investment objectives. The sub-adviser will apply its investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these will produce the desired results. |

| ● | Operational Risk. Operational risks include human error, changes in personnel, system changes, faults in communication, and failures in systems, technology, or processes. Various operational events or circumstances are outside the sub-adviser’s control, including instances at third parties. The Fund and the sub-adviser seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address these risks. |

| ● | Cyber Security Risk. The Fund’s and its service providers’ use of internet, technology and information systems may expose the Fund to potential risks linked to cyber security breaches of those technological or information systems. Cyber security breaches, amongst other things, could allow an unauthorized party to gain access to proprietary information, customer data, or fund assets, or cause the Fund and/or its service providers to suffer data corruption or lose operational functionality. |

| ● | Liquidity Risk. Liquidity risk exists when investments are difficult to sell as the result of low trading volume, lack of market makers, and/or legal restrictions. Illiquid securities may prevent the Fund from entering into security transactions at advantageous times or prices, potentially reducing the return of the Fund’s portfolio. Investments in smaller market capitalizations and over-the-counter markets have greater exposure to liquidity risk. |

25

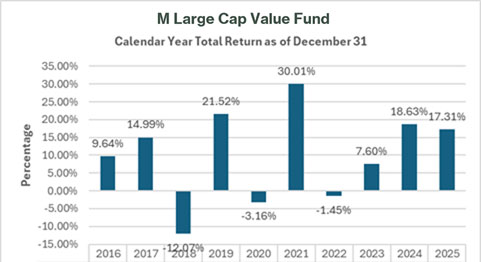

The

following information may give some indication of the risks of investing in the Fund. The Fund is the successor to the Predecessor Large

Cap Value Fund, a mutual fund with identical investment objectives, policies, and restrictions, as a result of the reorganization of

the Predecessor Large Cap Value Fund into the Fund on April 24 , 2026. The performance provided in the bar chart and table is that of

the Predecessor Large Cap Value Fund.

The table below shows the Predecessor Large Cap Value Fund’s average annual total returns for the periods indicated and how those returns compare to those of the Russell 1000® Index and the Russell 1000® Value Index. You cannot invest directly in an index. The Index returns are calculated on a total return basis and reflects no deduction for fees, expenses or taxes.

Average Annual Total Returns

(for the periods ended December 31, 2025)

| One Year | Five Years | Ten Years | ||||