As

filed with the Securities and Exchange Commission on

Securities Act Registration No. 333-206491

Investment Company Act Reg. No. 811-23089

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | ☒ | |

| Pre-Effective Amendment No. | ☐ | |

| Post-Effective Amendment No. 56 | ☒ | |

| and/or | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | ☒ | |

| Amendment No. 61 | ☒ | |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

3000 Auburn Drive, Suite 410

Beachwood, OH 44122

(Address of Principal Executive Offices) (Zip Code)

Registrant's Telephone Number, including Area Code: (216) 329-4271

| Andrew Davalla |

| Thompson Hine, LLP |

| 3900 Key Center, 127 Public Square |

| Cleveland, OH 44114 |

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

It is proposed that this filing will become effective (check appropriate box)

| ☐ | immediately upon filing pursuant to paragraph (b) |

| ☒ | on April 30, 2026 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of rule 485 |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously filed post-effective amendment.

|

IDX Adaptive Opportunities Fund Institutional Class Shares (Ticker Symbol: COIDX)

series of Trailmark Series Trust

9311 E Via De Ventura, Suite 105 Scottsdale, AZ 85258

|

PROSPECTUS

|

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission, nor has the Securities and Exchange Commission or any state securities commission passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

The IDX Adaptive Opportunities Fund (the “Fund”) seeks total return, which includes long-term capital appreciation. There can be no assurance that the Fund will achieve its investment objective.

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

Institutional Class shares | |

| Management Fees | |

| Distribution and Service (12b-1) Fees | |

| Shareholder Services Fees | |

| Other Expenses | |

| Acquired Fund Fees and Expenses(1) | |

| Total Annual Fund Operating Expenses | |

| Fee Waivers and Expense Reimbursement(2) | |

| Total Annual Fund Operating Expenses After Waivers and/or Expense Reimbursements |

| (1) |

| (2) |

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the periods indicated and then redeem all your shares at the end of those periods. The expense example also assumes that your investment has a 5% return each year and the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your cost would be:

| Period Invested | 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Institutional Class | $ |

$ |

$ |

$ |

1

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over”

its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund

shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example,

affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was

The Fund is actively managed and has flexibility to over- or underweight sectors, at the Adviser’s discretion. There is no stated limit on the percentage of assets the Fund can invest in any one sector, and at times the Fund may focus on a small number of sectors.

The Fund invests in commodities (through futures contracts) as well as in the equity and fixed-income securities of commodity-related companies whose operations relate to commodities, natural resources, energy, real estate, or other “hard assets,” and companies that provide services or have exposure to such businesses, and commodity-related derivatives and Instruments. The Fund can shift its allocation across asset classes and markets worldwide by assessing their relative attractiveness, as determined by the Adviser. This means the Fund may concentrate its investments in any one asset class or geographic region, subject to any limitations imposed by the federal securities and tax laws, including the Investment Company Act of 1940 (the “1940 Act”).

Digital assets include indirect (e.g., futures or operating companies) exposure to bitcoin, ether, or other digital assets (collectively, “Digital Assets”). The Fund defines “other digital assets” as cryptocurrencies and blockchain-based or decentralized assets that are traded on a digital exchange. These assets include, but are not limited to, digital currencies such as bitcoin and ethereum, as well as other tokens and digital representations of value created, stored, and exchanged on blockchain networks. These assets are characterized by their decentralized nature, meaning any single entity does not control them, and their transactions are recorded on a distributed ledger technology known as blockchain. The Fund does not directly invest in bitcoin, ether, or other digital assets or in any digital assets traded OTC, such as pooled investment vehicles or other OTC trusts.

Portfolio Construction

The Adviser uses a bottom-up analysis process that considers quantitative and qualitative investment factors, including price and volume data (e.g., momentum and/or mean-reversion), macroeconomic data, fundamental valuation, term structure (e.g., carry), and other factors. The statutory prospectus describes each of these factors in more detail.

The Adviser uses a proprietary, systematic, and quantitative investment process that seeks to benefit from price trends in commodity, currency, equity, volatility, and fixed-income Instruments. As part of this process, the Fund will take either a long or short position in each Instrument. The owner of a long position in an Instrument will benefit from an increase in the underlying instrument’s price. The owner of a short position in an Instrument will benefit from a decrease in the underlying instrument’s price. The Adviser will generally seek to allocate among instruments and asset classes to enhance the risk-adjusted return relative to a long-only allocation. The Adviser expects this approach will reduce volatility and drawdowns while capturing the majority of the upside of the underlying markets.

2

The Fund will invest across sectors. In allocating assets among sectors, the Adviser will largely employ a trend-following approach that seeks to balance the allocation of risk (as measured by proprietary and established risk measures such as annualized standard deviation) over time. The Adviser uses its proprietary quantitative model to statistically gauge the strength of price trends. The model uses publicly available daily price information to evaluate momentum measures and determine appropriate allocations. The Adviser will also use its models to manage the allocation of investments across sectors based on the Adviser’s assessment of a sector’s risk and prevailing market conditions. Shifts in allocations among sectors will be determined following various quantitative signals based upon the Adviser’s research, that rely on the evaluation of technical and fundamental indicators, such as trends in historical prices, spreads between futures’ prices of differing expiration dates, supply/demand data, momentum, and macroeconomic data of commodity consuming countries.

During stressed or abnormal market conditions, including periods when the Adviser believes it is prudent to take a temporary defensive position, the Fund will reduce its exposure to certain asset classes significantly, including eliminating the asset class from the portfolio. The Fund defines stressed or abnormal market conditions as a significant drop in the price of the underlying assets over a short trading period. The targeted risk at any given time can vary based on several factors, including the Adviser’s systematic tactical views. The desired overall risk level of the Fund may be increased or decreased by the Adviser, subject to the Adviser’s risk controls which may result in the Adviser’s targeted risk level not being achieved in certain circumstances.

Derivatives and Instruments

In seeking to achieve its investment objective, the Fund will enter into both long and short positions using derivative instruments such as futures, forwards, options, and swaps, including equity index futures, swaps on equity index futures, equity swaps, and options on equity indices, fixed income futures, bond and interest rate futures, and credit default index swaps (collectively, “Derivatives”).

The Fund may also invest in fixed-income securities, including U.S. Government securities, U.S. Government agency securities (including inflation-linked bonds, such as Treasury Inflation-Protected Securities (“TIPS”)), short-term fixed-income securities, overnight or fixed-term repurchase agreements, money market fund shares corporate bonds, exchange-traded funds (“ETFs”) and exchange-traded notes (“ETNs”), foreign government bonds, and repurchase (“repo”) and reverse repo agreements. (collectively with Derivatives, the “Instruments”). Leverage may be created when the Fund enters into reverse repo agreements, as noted in the Principal Risks below. The Fund will primarily invest in Derivatives for investment purposes, although it may do so for tax purposes.

The Fund may invest in Instruments listed on U.S. or non-U.S. exchanges, some of which could be denominated in currencies other than the U.S. dollar. Although the Fund is not required to hedge against currency value changes, it expects to hedge its non-U.S. currency exposure. The Fund may invest in or have exposure to issuers of any size. The Fund may invest in or have exposure to U.S. or non-U.S. issuers. The Fund will either invest directly in the Instruments or indirectly by investing in the Subsidiary (as described below) that invests in the Instruments.

The Fund’s use of Derivatives will have the economic effect of financial leverage. Leverage will magnify exposure to the price movements of an asset class underlying a Derivative, which will result in increased volatility. This means the Fund will have the potential for greater gains, as well as the potential for greater losses, than if the Fund did not use Derivatives that have a leveraging effect. While the Fund normally does not engage in any direct borrowing, leverage is implicit in the futures and other derivatives it trades. There is no assurance that the Fund’s use of Derivatives providing enhanced exposure will enable it to achieve its investment objective.

3

The Fund intends to make investments through a wholly-owned and controlled subsidiary of the Fund (the “Subsidiary”), and may invest up to 25% of its total assets in the Subsidiary, which is organized under the laws of the Cayman Islands as an exempted company. Generally, the Subsidiary will invest primarily in Derivatives and other investments intended to serve as margin or collateral for the Subsidiary’s Derivative positions. The Fund will invest in the Subsidiary to gain exposure to the commodities, digital assets, and derivatives markets within the limitations of the federal tax laws, rules, and regulations that apply to registered investment companies. Unlike the Fund, the Subsidiary may invest without limitation in derivatives; however, the Subsidiary will comply with the same 1940 Act asset coverage requirements for its investments in derivatives that apply to the Fund’s transactions in derivatives. In addition, the Fund and the Subsidiary will be subject to the same fundamental investment restrictions on a consolidated basis, and to the extent applicable to the investment activities of the Subsidiary, it will follow the same compliance policies and procedures as the Fund. Unlike the Fund, the Subsidiary will not seek to qualify as a RIC under Subchapter M of the Internal Revenue Code (the “Code”). The Fund is the sole shareholder of the Subsidiary and does not expect shares of it to be offered or sold to other investors.

Commodity Investments

The Fund (including its Subsidiary) pursues its investment objective by allocating assets among various commodity sectors (including agricultural, energy, livestock, softs (e.g., non-grain agricultural products such as coffee, sugar, cocoa, etc.), and precious and base metals). The Fund will obtain exposure to commodity sectors by investing in commodity-linked Derivatives, directly or through the Subsidiary, not through direct investments in physical commodities. The Fund may also invest in ETFs, ETPs, ETNs, and commodity pools that provide exposure to commodities or affiliated sectors. The Fund will limit its investments in other pooled investment vehicles so that no single pool represents more than 25% of the Fund’s total assets to satisfy asset diversification requirements under the Code.

Equity Investments

The Fund may invest directly or indirectly in equity securities of issuers in any sector, including the commodity, financial, and technology sectors. While the Fund can hold equity securities such as common stocks, preferred stocks, convertible securities, warrants, depositary receipts, and other instruments whose price is linked to the value of common stock, the Fund will gain most of its equity exposure through ETFs.

For commodities, the Fund will invest in commodity-related companies whose operations relate to commodities, natural resources, energy, real estate, or other “hard assets,” and companies that provide services or have exposure to such businesses. These companies include companies engaged in the exploration, ownership, production, refinement, processing, transportation, distribution, or marketing of commodities and use them extensively in their products and companies that provide technology and services to commodity-related companies. This includes companies that are engaged in businesses such as integrated oil, oil, and gas exploration and production, energy services and technology, chemicals and oil products, coal, and other consumable fuels, gold and precious metals, metals and minerals, forest products, agricultural chemicals and services, farmland, alternative energy sources, environmental services, and agricultural products (including crop growers, owners of plantations, and companies that produce and process foods), as well as related transportation companies, equipment manufacturers, service providers and engineering, procurement and construction. companies. This may also include companies engaged in photonics and optical technologies, which the Adviser believes are integral to the infrastructure buildout required to support increasing demand for commodities and natural resources driven by artificial intelligence and data center expansion.

4

Fixed Income Investments

A significant portion of the assets of the Fund may be invested directly or indirectly in investment-grade fixed-income securities, cash, and cash equivalents with one year or less term to maturity and an average portfolio duration of one year or less. The Fund defines “investment grade” as fixed-income securities being rated no lower than the A category by Standard & Poor’s Ratings Group, Moody’s Investors Service, or Fitch Ratings, Inc. The fixed income portion of the Fund is intended to provide liquidity, preserve capital, and serve as margin or collateral for the Fund’s or Subsidiary’s derivative positions. These cash or cash equivalent holdings also serve as collateral for the positions the Fund takes and earn income for the Fund. The Adviser seeks to develop an appropriate fixed-income portfolio by considering the differences in yields among securities of different maturities, market sectors, and issuers.

Additional Portfolio Information

The Fund generally does not intend to close out, sell, or redeem its Instruments except (i) to meet redemptions or (ii) when an Instrument is nearing expiration, at which point the Fund will generally sell it and use the proceeds to buy another Instrument with a later expiration date to maintain its commodities exposure. This is commonly referred to as “rolling.”

The Fund’s strategy involves frequent portfolio trading, which may result in a higher portfolio turnover rate than a fund with less frequent trading and correspondingly greater transactional expenses. These expenses are borne by the Fund and its shareholders and may have adverse tax consequences on them. The Adviser considers the transaction costs associated with trading each Instrument and takes this into consideration when determining the appropriate frequency for trading. The Fund also employs sophisticated proprietary trading techniques to mitigate trading costs and the execution impact on the Fund.

Principal

Risks of Investing in the Fund.

Generally, the Fund will be subject to the following additional risks:

Commodities Risk – Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, embargoes, tariffs, and international economic, political, and regulatory developments. Additionally, the Fund may gain exposure to the commodities markets through investments in ETPs, the value of which may be influenced by, among other things, time to maturity, level of supply and demand for the product, volatility, and lack of liquidity in underlying markets, the performance of the reference instrument, changes in the issuer’s credit rating and economic, legal, political or geographic events that affect the reference instrument.

5

Derivatives Risk – In general, a derivative instrument typically involves leverage (i.e., it provides exposure to potential gain or loss from a change in the level of the market price of the underlying commodity, security, currency, or a basket or index of such investments) in a notional amount that exceeds the amount of cash or assets required to establish or maintain the derivative instrument. Adverse changes in the value or level of the underlying asset or index, which the Fund may not directly own, can result in a loss to the Fund substantially greater than the amount invested in the derivative itself. The use of derivative instruments also exposes the Fund to additional risks and transaction costs. These instruments come in many varieties and have a wide range of potential risks and rewards, and may include futures contracts, forward contracts, options, and swaps. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate perfectly with the overall commodities markets. Additionally, to the extent the Fund is required to segregate or “set aside” liquid assets or otherwise cover open positions with respect to certain derivative instruments, the Fund may be required to sell portfolio instruments to meet these asset segregation requirements. There is a possibility that segregation involving a large percentage of the Fund’s assets could impede portfolio management or the Fund’s ability to meet redemption requests or other current obligations.

| ● | Forward and Futures Contract Risk. The successful use of forward and futures contracts draws upon the Adviser’s skill and experience with respect to such instruments and is subject to special risk considerations. The primary risks associated with the use of forward and futures contracts, which may adversely affect the Fund’s NAV and total return, are (a) the imperfect correlation between the change in market value of the instruments held by the Fund and the price of the forward or futures contract; (b) possible lack of a liquid secondary market for a forward or futures contract and the resulting inability to close a forward or futures contract when desired; (c) losses caused by unanticipated market movements, which are potentially unlimited; (d) the Adviser’s inability to predict correctly the direction of securities prices, interest rates, currency exchange rates and other economic factors; (e) the possibility that the counterparty will default in the performance of its obligations; and (f) if the Fund has insufficient cash, it may have to sell securities from its portfolio to meet daily variation margin requirements, and the Fund may have to sell securities at a time when it may be disadvantageous to do so. |

| ● | Options Risk. An option is an agreement that, for a premium payment or fee, gives the option holder (the purchaser) the right but not the obligation to buy (a “call option”) or sell (a “put option”) the underlying asset (or settle for cash an amount based on an underlying asset, rate, or index) at a specified price (the “Exercise Price”) during a period of time or on a specified date. Investments in options are considered speculative. When the Fund purchases an option, it may lose the premium paid for it if the price of the underlying security or other assets decreases or remains the same (in the case of a call option) or increases or remains the same (in the case of a put option). If a put or call option purchased by the Fund were permitted to expire without being sold or exercised, its premium would represent a loss to the Fund. |

| ● | Repurchase Agreements Risk. The Fund may invest in repurchase agreements. When entering into a repurchase agreement, the Fund essentially makes a short-term loan to a qualified bank or broker-dealer. The Fund buys securities that the seller has agreed to buy back at a specified time and at a set price that includes interest. There is a risk that the seller will be unable to buy back the securities at the time required, and the Fund could experience delays in recovering amounts owed to it. |

| ● | Reverse Repurchase Agreements Risk. Reverse repurchase agreements involve the sale of securities held by the Fund with an agreement to repurchase the securities at an agreed-upon price, date, and interest payment. Reverse repurchase agreements involve the risk that the other party may fail to return the securities on time or at all. The Fund could lose money if it cannot recover the securities, and the value of the collateral held by the Fund, including the value of the investments made with cash collateral, is less than the value of the securities. These events could also trigger adverse tax consequences to the Fund. Furthermore, reverse repurchase agreements involve the risks that (i) the interest income earned in the investment of the proceeds will be less than the interest expense, (ii) the market value of the securities retained in lieu of sale by the Fund may decline below the price of the securities the Fund has sold but is obligated to repurchase, and (iii) the market value of the securities sold will decline below the price at which the Fund is required to repurchase them. In addition, the use of reverse repurchase agreements may be regarded as leveraging. |

6

| ● | Short Selling Risk. If a security sold short or other instrument increases in price, the Fund may have to cover its short position at a higher price than the short sale price, resulting in a loss. Because losses on short sales arise from increases in the value of the security sold short, such losses are theoretically unlimited. The Fund may not be able to successfully implement its short sale strategy due to the limited availability of desired securities or for other reasons. |

| ● | Swap Risk. Swaps are subject to tracking risk because they may not be perfect substitutes for the instruments they are intended to hedge or replace. OTC swaps are subject to counterparty default. Leverage inherent in derivatives will tend to magnify the Fund’s losses. |

Leverage Risk - As part of the Fund’s principal investment strategy, the Fund will invest in Derivatives and other Instruments that provide the economic effect of financial leverage by creating additional investment exposure to the underlying instrument and the potential for greater loss. If the Fund uses leverage through activities such as purchasing Derivatives and other Instruments, the Fund has the risk that losses may exceed the net assets of the Fund. For example, reverse repos create leverage because the value of the securities sold may decline below the price at which the Fund is obligated to repurchase them, resulting in a loss. The Fund’s NAV while employing leverage will be more volatile and sensitive to market movements.

Liquidity Risk - Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices to satisfy its obligations.

Portfolio Turnover Risk — The Fund may incur high portfolio turnover to manage the Fund’s investment exposure. Additionally, active trading of the Fund’s shares may cause more frequent purchase and sales activities that could, in certain circumstances, increase the number of portfolio transactions. High levels of portfolio transactions increase brokerage and other transaction costs and may result in increased taxable capital gains. Each of these factors could have a negative impact on the performance of the Fund.

Investment Strategy Risk – The Fund actively invests in Derivatives and other Instruments that provide exposure to various asset classes, including commodities. The Fund does not invest directly in or hold commodities. The price of Derivatives should be expected to differ from the current cash price of the underlying commodity, which is sometimes referred to as the “spot” price. Consequently, the performance of the Fund should be expected to perform differently from the spot price of commodities. These differences could be significant.

| ● | Active Management Risk. The Fund is actively managed, and its performance reflects the investment decisions that the Adviser makes for the Fund. The Adviser’s judgments about the Fund’s investments may prove to be incorrect. If the investments selected and strategies employed by the Fund fail to produce the intended results, the Fund could underperform or have negative returns as compared to other funds with a similar investment objective and/ or strategies. |

| ● | Model and Data Risk. Given the complexity of the strategies of the Fund, the Adviser relies heavily on quantitative models and information and data both proprietary and supplied by third parties (“Models and Data”). Models and Data are used to rank investments and provide risk management insights. The use of predictive models has inherent risks. Because predictive models are constructed based on historical data supplied by third parties, the success of relying on such models may depend heavily on the accuracy and reliability of the supplied historical data. In addition, there is an inherent risk that the quantitative models used by the adviser will not be successful in forecasting movements in industries, sectors, or companies or in determining the weighting of investment positions that will enable the Fund to achieve its investment objective. |

7

| ● | Subsidiary Risk. By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. Although the Subsidiary is not registered under the 1940 Act, it will provide investors with the same 1940 Act protections the Fund provides. |

Market and Volatility Risk – The prices of Derivatives and commodities have historically been highly volatile. The value of the Fund’s investments in Derivatives and other Instruments that provide exposure to commodities and other asset classes could decline significantly and without warning, including to zero. If you are not prepared to accept significant and unexpected changes in the value of the Fund and the possibility that you could lose your entire investment in the Fund you should not invest in the Fund.

Tax Risk — In order to qualify for the special tax treatment accorded a RIC and its shareholders, the Fund must derive at least 90% of its gross income for each taxable year from “qualifying income,” meet certain asset diversification tests at the end of each taxable quarter and meet annual distribution requirements. If, in any year, the Fund were to fail to qualify for the special tax treatment accorded a RIC and its shareholders were ineligible to or were not to cure such failure, the Fund would be taxed in the same manner as an ordinary corporation subject to U.S. federal income tax on all its income at the fund level. The resulting taxes could substantially reduce the Fund’s net assets and the amount of income available for distribution. The Fund uses a Subsidiary to manage non-qualifying income for purposes of Internal Revenue Code Section 851(b)(2). The Subsidiary converts the income to qualifying income to the extent that earnings and profits exist at the subsidiary level. According to Treasury Regulation Sec 1.851-2(b)(2)(iii), income generated from a Subsidiary is considered other income derived from the corporation’s business of investing in commodity interests, securities, or currencies; it therefore is qualifying income under the tax code.

Valuation Risk — In certain circumstances (e.g., if the Adviser believes market quotations do not accurately reflect the fair value of an investment, or a trading halt closes an exchange or market early), the Adviser may, subject to the policies and procedures established by the Fund’s Board, choose to determine a fair value price as the basis for determining the market value of such investment for such day. The fair value of an investment determined by the Adviser may be different from other value determinations of the same investment. Portfolio investments that are valued using techniques other than market quotations, including “fair valued” investments, may be subject to greater fluctuation in their value from one day to the next than would be the case if market quotations were used. In addition, there is no assurance that the Fund could sell a portfolio investment for the value established for it at any time, and it is possible that the Fund would incur a loss because a portfolio investment is sold at a discount to its established value. The fair value of the Fund’s futures contracts may be determined by reference, in whole or in part, to the cash market in the underlying asset.

Sector Focus Risk – The Fund may invest a significant portion of its assets in a particular sector of the market, the Fund may be especially sensitive to factors and economic risks that specifically affect that sector. As a result, the Fund’s share price may fluctuate more widely than the share price of a fund that is more broadly invested across numerous sectors.

Non-Diversification Risk – The Fund is classified as “non-diversified” under the 1940 Act. This means it can invest a relatively high percentage of its assets in the assets of a small number of issuers or financial instruments with a single counterparty or a few counterparties. This may increase the Fund’s volatility and increase the risk that the Fund’s performance will decline based on the performance of a single issuer or the credit of a single counterparty. A non-diversified fund’s greater investment in a single issuer or asset type makes the Fund more susceptible to financial, economic, and market events impacting such issuer or asset type. For the Fund’s portfolio, a decline in the value of futures contracts will have a greater negative effect than a similar decline or default by a single security in a diversified portfolio.

8

Equity Securities Risk - Equity markets are volatile. The price of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions.

| ● | Small Cap Securities Risk. Small cap companies may have limited product lines or markets. They may be less financially secure than larger, more established companies. They may depend on a more limited management group than larger capitalized companies. |

| ● | Mid Cap Securities Risk. The securities of mid cap companies generally trade in lower volumes and are generally subject to greater and less predictable price changes than the securities of larger capitalization companies. |

| ● | Large Cap Securities Risk. While large cap companies tend to be more stable than small or mid cap companies, they can still experience significant volatility. These companies may face challenges such as slower growth rates, market saturation, and operational risks that could negatively impact their stock prices. |

| ● | ETP Risk. Investing in ETPs carries several risks, including market risk, where the value of ETPs may fluctuate; tracking error, which can lead to returns differing from the underlying asset; and liquidity risk, making it difficult to buy or sell shares at desired prices. ETPs linked to Digital Assets like bitcoin and ether are subject to high price volatility and regulatory risk, with potential impacts from regulation changes. Additionally, ETPs may involve counterparty, issuer, and leverage risks, which can amplify gains and losses, increasing overall risk for the Fund. |

ETF Risk - The Fund may invest in ETFs as part of its principal investment strategies. ETFs are subject to investment advisory and other expenses, which the Fund will indirectly pay. As a result, your cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that do not invest in such investments. ETFs are listed on national stock exchanges and are traded like stocks listed on an exchange. The market price for the Fund’s shares may deviate from the Fund’s NAV, particularly during times of market stress, with the result that investors may pay significantly more or receive significantly less for Fund shares than the Fund’s NAV, which is reflected in the bid and ask price for Fund shares or in the closing price. For example, shares of ETFs may trade at a discount or a premium to an ETF’s NAV, which may result in an ETF’s market price being more or less than the value of the index that the ETF tracks, especially during periods of market volatility or disruption. There may also be additional trading costs due to an ETF’s bid-ask spread, or the underlying fund may suspend sales of its shares due to market conditions that make it impracticable to conduct such transactions, any of which may adversely affect the Fund’s performance.

| ● | Tracking Risk. ETFs in which the Fund invests will not be able to replicate exactly the performance of any indices or prices they track because the total return generated by the securities will be reduced by transaction costs incurred in adjusting the actual balance of the securities or derivatives. In addition, the index-tracking ETFs will incur expenses not incurred by their applicable indices. Certain securities comprising an index may temporarily be unavailable occasionally, further impeding the security’s ability to track an index. |

| ● | Authorized Participants Concentration Risk. The Fund may have limited financial institutions that may act as authorized participants (“Authorized Participants”). If those Authorized Participants exit the business or cannot process creation or redemption orders, Shares may trade at larger bid-ask spreads and/or premiums or discounts to NAV. Authorized Participant concentration risk may be heightened for a fund that invests in non-U.S. or other securities or instruments with lower trading volumes. |

9

| ● | Absence of Active Market Risk. Although Shares are listed for trading on a stock exchange, there is no assurance that an active trading market for them will develop or be maintained. Without an active trading market for Shares, they will likely trade with a wider bid/ask spread and at a greater premium or discount to NAV. |

| ● | Market Price Variance Risk. Fund Shares can be bought and sold in the secondary market at market prices, which may be higher or lower than the Fund’s NAV. The market price of Shares fluctuates based on changes in the value of the Fund’s holdings and on the supply and demand for Shares. The market price of Shares may vary significantly from the Fund’s NAV, especially during market volatility. Further, to the extent that exchange specialists, market makers, Authorized Participants, or other market participants are unavailable or unable to trade the Fund’s Shares and/or create or redeem creation units premiums or discounts may increase. |

| ● | Trading Cost Risk. When buying or selling shares of the Fund in the secondary market, you will likely incur brokerage commission or other charges. In addition, you may incur the cost of the “spread,” also known as the bid-ask spread, which is the difference between what investors are willing to pay for Fund shares (the “bid” price) and the price at which they are willing to sell Fund shares (the “ask” price). The bid-ask spread varies over time based on, among other things, trading volume, market liquidity and market volatility. Because of the costs inherent in buying or selling Fund shares, frequent trading may detract significantly from investment results, and investment in Fund shares may not be advisable for investors who anticipate regularly making small investments due to the associated trading costs. |

| ● | Exchange Trading Risk. Trading in Shares on their listing exchange may be halted due to market conditions or for reasons that, in the view of the exchange, make trading in Shares inadvisable, such as extraordinary market volatility. Also, there is no assurance that Shares will continue to meet the exchange’s listing requirements, and Shares may be delisted. Like other listed securities, Shares of the Fund may be sold short, and short positions in Shares may place downward pressure on their market price. |

Fixed Income Securities Risk

| ● | Interest Rate Risk. Interest rate risk is the risk that prices of fixed-income securities generally increase when interest rates decline and decrease when interest rates increase. The Fund may lose money if short-term or long-term interest rates rise sharply or otherwise change in a manner not anticipated by the Adviser. |

| ● | Credit Risk. Credit risk refers to the possibility that the issuer of a security or the issuer of the reference asset of a derivative instrument will not be able to make principal and interest payments when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. Securities rated in the four highest categories by the rating agencies are considered investment grade but they may also have some speculative characteristics. Investment grade ratings do not guarantee that the issuer will not default on its payment obligations or that bonds will not otherwise lose value. |

10

| ● | U.S. Government Securities Risk. Treasury obligations may differ in their interest rates, maturities, times of issuance, and other characteristics. Obligations of U.S. Government agencies and authorities are supported by varying degrees of credit but generally are not backed by the full faith and credit of the U.S. Government. No assurance can be given that the U.S. Government will provide financial support to its agencies and authorities if it is not obligated by law to do so. Some of the government agency securities the Fund may purchase are backed only by the credit of the government agency and not by full faith and credit of the United States. |

| ● | ETN Risk. Because ETNs are unsecured, unsubordinated debt securities, an investment in an ETN exposes the Fund to the risk that an ETN’s issuer may be unable to pay. In addition, the Fund will bear its proportionate share of the fees and expenses of the ETN, which may cause the Fund’s operating expenses to be higher and its performance to be lower. |

Foreign Investments Risk - Foreign investments often involve special risks that are not present in U.S. investments, which can increase the chances that the Fund will lose money. For example, the Fund may invest in foreign Instruments or hold cash in foreign banks and securities depositories, which may be recently organized or new to the foreign custody business and may be subject to only limited or no regulatory oversight. The economies of certain foreign markets may not compare favorably with the economy of the United States with respect to such issues as growth of gross national product, reinvestment of capital, resources, and balance of payments position. The governments of certain countries may prohibit or impose substantial restrictions on foreign investments in their capital markets or in certain industries. Many foreign governments do not supervise and regulate stock exchanges, brokers, and the sale of securities to the same extent as the United States and may not have laws to protect investors that are comparable to U.S. securities laws. Settlement and clearance procedures in certain foreign markets may result in delays in payment for or delivery of securities not typically associated with settlement and clearance of U.S. investments. The regulatory, financial reporting, accounting, recordkeeping, and auditing standards of foreign countries may differ, in some cases significantly, from U.S. standards.

| ● | Currency Risk. Currency risk is the risk that changes in currency exchange rates will negatively affect securities denominated in, and/or receiving revenues in, foreign currencies. The liquidity and trading value of foreign currencies could be affected by global economic factors, such as inflation, interest rate levels, and trade balances among countries, as well as the actions of sovereign governments and central banks. Adverse changes in currency exchange rates (relative to the U.S. dollar) may erode or reverse any potential gains from the Fund’s investments in securities denominated in a foreign currency or may widen existing losses. |

| ● | Sovereign Debt Risk. The Fund may invest in, or have exposure to, sovereign debt instruments. These investments are subject to the risk that a governmental entity may delay or refuse to pay interest or repay principal on its sovereign debt, due, for example, to cash flow problems, insufficient foreign currency reserves, political considerations, the relative size of the governmental entity’s debt position in relation to the economy or the failure to put in place economic reforms required by the International Monetary Fund or other multilateral agencies. If a governmental entity defaults, it may ask for more time in which to pay or for further loans. There is no legal process for collecting sovereign debt that a government does not pay nor are there bankruptcy proceedings through which all or part of the sovereign debt that a governmental entity has not repaid may be collected. |

| ● | Emerging Markets Risk. Emerging markets are riskier than more developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets may be considered speculative. Emerging markets are more likely to experience hyperinflation and currency devaluations, which adversely affect returns to U.S. investors. In addition, many emerging securities markets have far lower trading volumes and less liquidity than developed markets. |

11

Bitcoin Risk – Bitcoin is a relatively new financial innovation, and the market for bitcoin is subject to rapid price swings, changes, and uncertainty. The value of bitcoin has been and may continue to be, substantially dependent on speculation, such that trading and investing bitcoin generally may not be based on fundamental analysis. The further development of the Bitcoin Network and the acceptance and use of bitcoin are subject to various factors that are difficult to evaluate. The slowing, stopping, or reversing of the development of the Bitcoin Network or the acceptance of bitcoin may adversely affect the price of bitcoin. Bitcoin is subject to the risk of fraud, theft, manipulation, security failures, operational, or other problems that impact bitcoin trading venues. Unlike the exchanges for more traditional assets, such as equity securities and futures contracts, bitcoin and bitcoin trading platforms are largely unregulated. As a result of the lack of regulation, individuals or groups may engage in fraud or market manipulation, and investors may be more exposed to the risk of theft, fraud, and market manipulation than when investing in more traditional asset classes. Legal or regulatory changes may negatively impact the operation of the Bitcoin Network or restrict the use of bitcoin. Realizing any of these risks could result in a decline in the acceptance of bitcoin and, consequently, a reduction in the value of bitcoin, bitcoin futures, and the Fund.

The Bitcoin blockchain faces significant challenges from competing public blockchains designed as alternative payment systems, many of which offer greater privacy, faster transaction processing, and lower fees. Additionally, the Bitcoin network has inherent drawbacks, such as slow transaction processing, variable transaction fees, and high price volatility, which may hinder its adoption as a payment method. These factors could reduce the demand for Bitcoin, negatively affecting its value and the performance of the Fund’s investments in bitcoin and related assets.

The continued development and widespread use of the Bitcoin blockchain as a payment network increasingly relies on “Layer 2” solutions like the Lightning Network, which are designed to improve scalability, speed, and efficiency. However, these solutions pose risks, including challenges in widespread adoption, potential security vulnerabilities, increased complexity, and the possibility of centralization. Any issues with these Layer 2 networks could negatively impact the Bitcoin blockchain’s scalability and effectiveness, potentially affecting its value and the performance of the Fund’s investments in bitcoin and related assets.

Additionally, the Bitcoin protocol, maintained by a decentralized group of developers, is open-source, which allows for continuous review but also means it may contain undiscovered vulnerabilities. If attackers exploit these flaws, it could disrupt the Bitcoin network, compromise transaction security, and create instability, potentially undermining trust in the network and negatively impacting the value of bitcoin and the Fund’s investments in bitcoin. Similarly, if one or a coordinated group of miners were to gain control of 51% of the Bitcoin Network or the concentration of a majority of bitcoin in one ore a few holders (i.e., “whales”) could manipulate transactions, halt payments and fraudulently obtain bitcoin.

Finally, bitcoin and bitcoin Futures are also exposed to the instability of other speculative parts of the crypto assets industry. Events such as the collapse of TerraUSD in May 2022 and FTX Trading Ltd. in November 2022, while not directly related to the security or utility of the Bitcoin blockchain, can nonetheless trigger significant declines in the price of bitcoin or bitcoin Futures.

Ether Risk – Ether is a relatively new innovation, and the ether market is subject to rapid price swings, changes and uncertainty and is a largely unregulated marketplace, which may be attributable to a possible lack of regulatory compliance. The value of ether has been and may continue to be, substantially dependent on speculation, such that trading and investing ether generally may not be based on fundamental analysis. The further development of the Ethereum Network and the acceptance and use of ether are subject to various factors that are difficult to evaluate. The slowing, stopping, or reversing of the development of the Ethereum Network or the acceptance of ether may adversely affect the price of ether. Ether is subject to the risk of fraud, theft, manipulation or security failures, operational, or other problems that impact ether trading venues. Unlike the exchanges for more traditional assets, such as equity securities and futures contracts, ether and ether trading platforms are largely unregulated. As a result of the lack of regulation, individuals or groups may engage in fraud or market manipulation, and investors may be more exposed to the risk of theft, fraud, and market manipulation than when investing in more traditional asset classes. Legal or regulatory changes may negatively impact the operation of the Ethereum Network or restrict the use of ether. Realizing any of these risks could result in a decline in the acceptance of ether and, consequently, a reduction in the value of ether, ether futures, and the Fund.

12

Investors should also know that the Ethereum blockchain faces increased vulnerability to attacks if ownership or staking of ether becomes concentrated in one participant. Like the Bitcoin blockchain, the Ethereum blockchain may be at risk of attacks if there is a high concentration of ether ownership or staking. If an entity controls 33% or more of staked ether, it could execute attacks, with greater risks, including transaction censorship and block reordering, occurring if more than 50% is controlled. Such attacks could negatively impact ether futures and, in turn, the value of the Fund’s investments. The risk of such attacks increases as the concentration of staked ether grows. Whales could manipulate transactions, halt payments, and fraudulently obtain ether.

Although the price movements of ether and bitcoin have generally been correlated, with both assets experiencing similar trends, ether has historically been more volatile. This means that it tends to rise more than bitcoin during market upswings and fall more sharply during downturns. The differences in the design and use cases of the bitcoin and Ethereum blockchains contribute to these distinct risk profiles. Bitcoin is more established as a store of value and crypto assets, while ether’s value is closely tied to its broader use in powering decentralized applications and smart contracts.

Investors should be aware that these differences in the characteristics and design of bitcoin and ether present different risks. While both are subject to the volatility and uncertainty of the crypto assets markets, the factors driving the performance of each asset may differ significantly, leading to varied investment outcomes.

Legal or regulatory changes could negatively impact the Ethereum Network or restrict the use of ether. Although the Commodity Futures Trading Commission (“CFTC”) currently classifies ether as a commodity, a future determination by a court or regulator that ether is a security could lead to the halting of ether trading on certain platforms, increased volatility in ether futures, and a significant decline in the Fund’s value, potentially to zero. Such a determination could also affect the Fund’s investment strategy, including its use of the Subsidiary.

Finally, ether and ether Futures are also exposed to the instability of other speculative parts of the crypto industry, such as the collapse of TerraUSD in May 2022 and FTX Trading Ltd. In November 2022, which may not be necessarily related to the security or utility of the Ethereum blockchain but can nonetheless precipitate a significant decline in the price of ether or ether Futures.

Blockchain Forks Risk – A blockchain fork occurs when protocol changes create two separate, incompatible versions, each with its own digital assets. This can lead to market disruption, price volatility, and competition between the resulting blockchains. Forks have occurred in both the Bitcoin and Ethereum Networks, creating new assets like Bitcoin Cash and Ethereum Classic. These events can negatively impact the value and liquidity of the original assets and their related futures, posing significant risks to investors.

13

Digital Asset Trading Platform Risk – Bitcoin, the Bitcoin Network, ether, the Ethereum Network, and Digital Asset trading venues are relatively new and, in most cases, largely unregulated. As a result of this lack of regulation, individuals, or groups may engage in insider trading, fraud, or market manipulation with respect to Digital Assets. Such manipulation could cause investors in Digital Assets to lose money, possibly the entire value of their investments. Additionally, some Digital Asset trading platforms may not comply with applicable law, and such non-compliance may cause such platforms to close operations in certain jurisdictions or be subject to regulatory investigations.

Digital Asset trading platforms, where bitcoin and ether are traded, are not regulated as exchanges under federal securities laws and may lack consistent regulatory oversight. As a result, these platforms are more susceptible to fraud, manipulation, and operational issues. Additionally, these crypto trading platforms are or may become subject to enforcement actions by regulatory authorities, which could impact their operations, liquidity, and the overall stability of the markets for these digital assets. Such enforcement actions may result in restrictions, fines, or other penalties that could adversely affect the trading of crypto assets, leading to increased volatility and potential losses for investors.

Over the past several years, some digital asset trading venues have been closed due to fraud, failure, or security breaches. The nature of the assets held at digital asset trading venues makes them appealing targets for hackers, and several digital asset trading venues have been victims of cybercrimes and other fraudulent activities. These activities have caused significant, in some cases total, losses for Digital Asset investors. Investors in Digital Assets may have little or no recourse should such theft, fraud, or manipulation occur. No central registry shows which individuals or entities own Digital Assets or the quantity of Digital Assets owned by any particular person or entity. No regulations in place would prevent a large holder of Digital Assets or a group of holders from selling their Digital Assets, which could depress the price of Digital Assets, or otherwise attempt to manipulate the price of Digital Assets. Events that reduce user confidence in Digital Assets and the fairness of digital asset trading venues could harm the price of Digital Assets and the value of an investment in the Fund.

If the crypto asset trading venues, which may serve as a pricing source for the calculation of the BBR or ETHUSD_RR that is used to value the Fund’s investments, become subject to onerous regulations or are subject to enforcement actions by regulatory authorities (including the Financial Crimes Enforcement Network (“FinCEN”), the U.S. Securities and Exchange Commission (“SEC”), CFTC, Financial Industry Regulatory Authority, Inc. (“FINRA”), the Consumer Financial Protection Bureau, the Department of Justice, the Department of Homeland Security, the Federal Bureau of Investigation, the Internal Revenue Service (“IRS”), the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the Federal Reserve and state financial institution regulators), among other things, trading in bitcoin and ether may be concentrated in a smaller number of trading venues, which may materially impact the price, volatility, and trading volumes of bitcoin and ether. Additionally, the trading venues may be required to comply with tax, anti-money laundering, know-your-customer, and other regulatory requirements, compliance, and reporting obligations that may make it more costly to transact in or trade bitcoin and ether (which may materially impact price, volatility, or trading of bitcoin and ether more generally). Each of these events could harm bitcoin and ether Futures and the value of an investment in the Fund.

Digital Asset trading is fragmented across numerous crypto trading platforms, many of which are not regulated as exchanges under federal securities laws. This fragmentation can lead to higher volatility and price discrepancies across different platforms, increasing the likelihood of price differences and market manipulation. The lack of centralized oversight and regulation also heightens the risk of fraud and manipulation, as these platforms may not adhere to consistent standards for security, transparency, or market integrity. Market participants trading digital assets may seek to hedge or manage their exposure by taking offsetting positions in Digital Assets on these platforms. However, the fragmented nature of the market may require participants to analyze multiple prices, which may be inconsistent, quickly changing, and potentially subject to manipulation. This fragmentation also may require participants to fill their positions through multiple transactions on different platforms, increasing the cost, uncertainty, and risk of trading. These factors may reduce the effectiveness of using Digital Asset transactions to manage or offset positions in Digital Assets. Market participants who cannot fully or effectively hedge their positions in Digital Asset may widen bid-ask spreads on such contracts, potentially decreasing the trading volume and liquidity of these contracts and negatively impacting their price.

14

Digital Asset-Related Operating Company Risk – The Fund may invest in Digital Asset-related companies, which are companies that derive a significant portion of their revenue or hold substantial assets related to Digital Assets such as bitcoin, ether, or blockchain technology. However, the extent to which these companies have economic exposure to bitcoin, ether, or other Digital Assets may vary significantly. Some companies may derive a substantial portion of their revenue or assets from Digital Asset-related activities, while others may have limited exposure to these markets. This variability can affect the Fund’s exposure to Digital Assets and may influence its performance based on these companies’ underlying activities.

Investing in Digital Asset-related companies involves several risks, including variability in the economic exposure to bitcoin, ether, or other Digital Assets, non-blockchain or crypto-related activities, and operational and regulatory risks.

| ● | Companies with greater exposure to Digital Assets will be more directly affected by the volatility and regulatory risks associated with the Digital Asset markets. Conversely, companies with limited exposure may not benefit as much from positive developments in the Digital Asset space, potentially reducing the Fund’s overall exposure to the growth of these assets. |

| ● | Many Digital Asset-related companies may also engage in non-blockchain or non-crypto-related activities, which could introduce additional risks and uncertainties that are not directly related to Digital Assets. For example, a company that operates a crypto trading platform may also be involved in unrelated business ventures, such as traditional financial services or technology development. These non-crypto activities could negatively impact the company’s overall performance and, by extension, the performance of the Fund. Moreover, adverse developments in these other business areas could detract from the company’s focus on its Digital Asset-related operations, further affecting its financial results. |

| ● | Companies involved in the Digital Asset ecosystem may face operational challenges like technological issues, cybersecurity threats, and regulatory scrutiny. These risks can be amplified by the company’s involvement in Digital Assets, where the regulatory environment is still evolving, and the technology is complex and rapidly changing. Additionally, companies that diversify their operations across blockchain-related and traditional sectors may face difficulties managing these diverse business activities, adversely affecting their overall operational effectiveness. |

| ● | Many Digital Asset-related companies may operate in a rapidly evolving and uncertain regulatory environment, which could result in non-compliance with existing regulations and potential enforcement actions by regulatory authorities. Such actions, including fines, penalties, or business restrictions, could significantly impact these companies’ operations and, in turn, negatively affect the Fund’s performance. |

Counterparty Risk — Investing in derivatives and repurchase agreements involves entering into contracts with third parties (i.e., counterparties). The use of derivatives and repurchase agreements involves risks that are different from those associated with ordinary portfolio securities transactions. The Fund will be subject to credit risk (i.e., the risk that a counterparty is or is perceived to be unwilling or unable to make timely payments or otherwise meet its contractual obligations) with respect to the amount it expects to receive from counterparties to derivatives and repurchase agreements entered into by the Fund. If a counterparty becomes bankrupt or fails to perform its obligations, or if any collateral posted by the counterparty for the benefit of the Fund is insufficient, or if there are delays in the Fund’s ability to access such collateral, the value of an investment in the Fund may decline. The counterparty to a listed futures contract is the derivatives clearing organization for the listed future. The listed future is held through a FCM acting on behalf of the Fund. Consequently, the counterparty risk on a listed futures contract is the creditworthiness of the FCM and the exchange’s clearing corporation.

15

Hedging Transactions Risk - The Adviser, from time to time, employs various hedging techniques. The success of the Fund’s hedging strategy will be subject to the Adviser’s ability to correctly assess the degree of correlation between the performance of the instruments used in the hedging strategy and the performance of the investments in the portfolio being hedged. Since the characteristics of many securities change as markets change or time passes, the success of the Fund’s hedging strategy will also be subject to the Adviser’s ability to continually recalculate, readjust, and execute hedges in an efficient and timely manner. For a variety of reasons, the Adviser may not seek to establish a perfect correlation between such hedging instruments and the portfolio holdings being hedged. Such imperfect correlation may prevent the Fund from achieving the intended hedge or expose the Fund to risk of loss. In addition, it is not possible to hedge fully or perfectly against any risk, and hedging entails its own costs (such as trading commissions and fees).

Other Investment Companies Risk - As with other investments, investments in other investment companies are subject to market and manager risk. In addition, if the Fund acquires shares of investment companies, shareholders bear both their proportionate share of expenses in the Fund (including management and advisory fees) and, indirectly, the investment companies’ expenses. The Fund may invest in money market mutual funds. An investment in a money market mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although money market mutual funds that invest in U.S. government securities seek to preserve the value of the Fund’s investment at $1.00 per share, it is possible to lose money by investing in a stable NAV money market mutual fund. Moreover, prime money market mutual funds must use floating NAVs that do not preserve the value of the Fund’s investment at $1.00 per share.

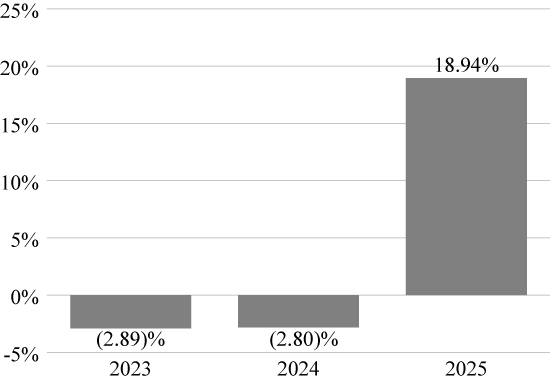

| th Quarter 2025 | ||

| - |

nd Quarter 2024 |

16

Average Annual Total Returns

(For the periods ended December 31, 2025)

| One Year | Since Inception | |

| Return Before Taxes | ||

| Return After Taxes on Distributions | ||

| Return

After Taxes on Distributions and Sale of Fund Shares |

||

| Bloomberg Global-Aggregate Total Return Index | ||

| ICE BofA SOFR Overnight Rate Index | ||

| SGA CTA Index | - |

- |

Management. IDX Advisors, LLC is the investment adviser to the Fund.

Portfolio Manager. Ben McMillan and Joshua Myers have managed the Fund since its inception.

Purchase and Sale of Fund Shares. The Fund offers Institutional Class shares only, which is offered by this Prospectus. The minimum investment for Institutional Class is $10,000. The Fund may waive these minimums at its discretion. Investors generally may meet the minimum investment amount for the Institutional Class by aggregating multiple accounts within the Fund if desired. There is no subsequent investment minimum. The Fund may, in the Adviser’s sole discretion, accept accounts with less than the minimum investment.

You can purchase or redeem shares directly from the Fund on any business day the NYSE is open by calling the Fund at 216-329-4271, where you may also obtain more information about purchasing or redeeming shares by mail, facsimile, or bank wire. The Fund has also authorized certain broker-dealers to accept purchase and redemption orders on its behalf. Investors who wish to purchase or redeem Fund shares through a broker-dealer should contact their broker-dealer directly.

Tax Information. For U.S. federal income tax purposes, the Fund’s distributions are taxable and will be taxed as ordinary income, capital gains, or, in some cases, qualified dividend income of individual shareholders subject to tax at maximum federal rates applicable to long-term capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an IRA. Such tax-deferred arrangements may be subject to U.S. federal income tax at rates applicable to ordinary income upon withdrawal of monies from those arrangements.

Payments to Broker-Dealers and Other Financial Intermediaries. If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

17

Purchases through Broker-Dealers and Other Financial Intermediaries. You may be charged a fee if you effect transactions through a broker or agent. The Fund has authorized one or more brokers to receive on its behalf purchase and redemption orders. Such brokers are authorized to designate other intermediaries to receive purchase and redemption orders on the Fund’s behalf. The Fund will be deemed to have received a purchase or redemption order when an authorized broker or, if applicable, a broker’s authorized designee, receives the order. Customer orders will be priced at the Fund’s NAV next computed after they are received by an authorized broker or the broker’s authorized designee.

18

INVESTMENT OBJECTIVES, STRATEGIES, RISKS AND PORTFOLIO HOLDINGS

The Fund’s Investment Objectives and Principal Investment Strategies. This section of the Prospectus provides additional information about the investment practices and related risks of the Fund. The Fund’s investment objective may be changed without shareholder approval; however, the Fund will provide 60 days’ advance notice to shareholders before implementing a change in the Fund’s investment objective.

The Fund pursues its investment objective by investing globally across a wide range of asset classes, including commodities, equities, fixed income, digital assets, and currencies, and may take both long and short positions in each of the asset classes or Instruments (as defined below). While the Fund expects to invest about 30% to 50% in long and short positions of commodity-related companies, as defined below, its tactical allocation will include investments in other sectors. The Fund can invest in U.S. and foreign companies of any size, including issuers from emerging markets.

The Fund is actively managed and has flexibility to over-or underweight sectors, at the Adviser’s discretion. There is no stated limit on the percentage of assets the Fund can invest in any one sector, and at times the Fund may focus on a small number of sectors.

The Fund does not invest in commodities directly, rather, it invests in the equity and fixed-income securities of commodity-related companies whose operations relate to commodities, natural resources, energy, real estate, or other “hard assets,” and companies that provide services or have exposure to such businesses, and commodity-related derivatives and Instruments. The Fund can shift its allocation across asset classes and markets around the world by assessing their relative attractiveness, as determined the Adviser. This means the Fund may concentrate its investments in any one asset class or geographic region, subject to any limitations imposed by the federal securities and tax laws, including the Investment Company Act of 1940, as amended (the “1940 Act”).

Digital assets include direct (e.g., spot) or indirect (e.g., futures or operating companies) exposure to bitcoin, ether, or other digital assets (collectively, “Digital Assets”). The Fund defines “other digital assets” as cryptocurrencies and blockchain-based or decentralized assets that are traded on a digital exchange. These assets include, but are not limited to, digital currencies such as bitcoin and ethereum, as well as other tokens and digital representations of value created, stored, and exchanged on blockchain networks. These assets are characterized by their decentralized nature, meaning any single entity does not control them, and their transactions are recorded on a distributed ledger technology known as blockchain. The Fund does not directly invest in bitcoin, ether, or other digital assets or in any digital assets traded OTC, such as pooled investment vehicles or the OTC trusts.

Portfolio Construction.

IDX Advisors, LLC, (the “Adviser”) uses a bottom-up analysis process that considers quantitative and qualitative investment factors, including price and volume data (e.g., momentum and/or mean-reversion), macroeconomic data, fundamental valuation, term structure (e.g., carry), and other factors. Each of these factors is described in more detail in the statutory prospectus.

| ● | Momentum: Momentum strategies favor investments that have performed well over the past few months, seeking to capture the tendency that an asset’s recent performance will continue. The Fund will generally seek to buy assets that recently outperformed and sell those that recently underperformed relative to their historical averages and other asset classes. Examples of momentum measures include simple price momentum for selecting equities and price- and yield-based momentum for selecting fixed-income securities. |

19

| ● | Mean-Reversion: At some point in time, momentum may carry an asset far beyond its historic averages. In such cases, the Fund will shift from a momentum strategy to a mean-reversion strategies, which recognize that over certain time frames, investments that have performed very well or poorly exhibit a tendency to revert to their historic averages over time. The Fund may seek to sell investments (or reduce existing exposures) in assets that have demonstrated extreme recent outperformance relative to their historic averages and buy (or reduce short exposures) in assets that have extreme recent underperformance (e.g., “oversold” conditions). |

| ● | Macroeconomic Data: The Adviser seeks to evaluate the impact of macroeconomic news and macroeconomic momentum on the attractiveness of Instruments and asset classes around the world. Macroeconomic themes considered include but are not limited to, business cycles, international trade, monetary policy, investor sentiment, political developments, environmental trends, and asset-specific fundamentals. |

| ● | Fundamental valuation: The Adviser seeks to evaluate investments and favor those that appear comparatively cheap relative to those that appear expensive based on fundamental measures related to price. Over time, the Adviser believes that relatively cheap assets will outperform relatively expensive assets. |

| ● | Term-Structure: Carry strategies favor investments with higher yields over those with lower yields, seeking to capture the tendency for higher-yielding assets to provide higher returns than lower-yielding assets. The Fund will seek to buy high-yielding assets and sell low-yielding assets relative to similar investments globally and relative to their historical averages. An example of carry measures includes using interest rates to select currencies and fixed-income securities. |

The Adviser considers each of the primary investment factors (momentum, macroeconomic data, fundamental value, and term structure) when constructing the Fund’s portfolio. Over time, the Fund seeks to capture most of the upside participation in the asset classes through long positions, while limiting the downside exposure through short positions. The owner of a long position in an Instrument will benefit from an increase in the price of the underlying instrument. The owner of a short position in an Instrument will benefit from a decrease in the price of the underlying instrument. The Adviser will generally seek to allocate among instruments and asset classes in such a way that it enhances the risk-adjusted return relative to a long-only allocation. The Adviser expects this approach will reduce volatility and drawdowns while capturing the majority of the upside of the underlying markets.

Volatility is a statistical measurement of the dispersion of returns of an asset, as measured by the annualized standard deviation of its returns. The Adviser expects that the Fund’s annualized volatility will typically be lower than a long-only allocation, but the Fund’s actual volatility level in certain periods may be materially higher or lower depending on market conditions. Higher volatility generally indicates higher risk. The Adviser generally expects that the Fund’s performance will have a low correlation to the performance of global equity, fixed income, currency, and commodity markets over any given market cycle, but the Fund’s performance may correlate to the performance of any one or more of those markets over short-term periods.

The Fund will invest across sectors. In allocating assets among sectors, the Adviser will largely employ a trend-following approach that seeks to balance the allocation of risk (as measured by proprietary and established risk measures such as annualized standard deviation) over time. The Adviser uses its proprietary quantitative model to statistically gauge the strength of price trends. The model uses publicly available daily price information to evaluate momentum measures and determine appropriate allocations. The Adviser will also use its models to manage the allocation of investments across sectors based on the Adviser’s assessment of a sector’s risk and prevailing market conditions. Shifts in allocations among sectors will be determined following various quantitative signals based upon the Adviser’s research, that rely on the evaluation of technical and fundamental indicators, such as trends in historical prices, spreads between futures’ prices of differing expiration dates, supply/demand data, momentum, and macroeconomic data of commodity consuming countries.

20

During stressed or abnormal market conditions, including periods when the Adviser believes it is prudent to take a temporary defensive position, the Fund will reduce its exposure to certain asset classes significantly, including eliminating the asset class from the portfolio. The Fund defines stressed or abnormal market conditions as a significant drop in the price of the underlying assets over a short trading period. The targeted risk at any given point in time can vary based on a number of factors, including the Adviser’s systematic tactical views. The desired overall risk level of the Fund may be increased or decreased by the Adviser, subject to the Adviser’s risk controls which may result in the Adviser’s targeted risk level not being achieved in certain circumstances.

Derivatives and Instruments.

In seeking to achieve its investment objective, the Fund will enter into both long and short positions using derivative instruments such as futures, forwards, options, and swaps, including equity index futures, swaps on equity index futures, equity swaps, and options on equity indices, fixed income futures, bond and interest rate futures, and credit default index swaps (collectively, “Derivatives”). Futures and forward contracts are contractual agreements to buy or sell a particular currency, commodity, or financial instrument at a pre-determined price in the future.