| OMB APPROVAL | |

| As filed with the Securities and Exchange Commission on April 29, 2026 Securities Act File No. 333-208542 Investment Company Act File No. 811-23121 |

OMB Number: 3235-0307 Expires: July 31, 2027 Estimated average burden hours per response 297.7 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [X] | |

| Pre-Effective Amendment No. | [ ] | |

| Post-Effective Amendment No. 19 | [X] | |

| and/or | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [X] | |

| Amendment No. 20 | [X] | |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

151 Detroit Street, Denver, Colorado 80206-4805

(Address of Principal Executive Offices) (Zip Code)

Registrant's Telephone Number, including Area Code: 303-333-3863

Cara Owen

151 Detroit Street

Denver, Colorado 80206-4805

(Name and Address of Agent for Service)

With Copies to:

Eric S. Purple

Stradley Ronon Stevens & Young, LLP

2000 K Street, N.W., Suite 700

Washington, District of Columbia 20006

Approximate Date of Proposed Public Offering: As soon as practicable after the effective date of this Registration Statement.

| It is proposed that this filing will become effective: (check appropriate box) | ||

| [ ] | immediately upon filing pursuant to paragraph (b) | |

| [X] | on April 30, 2026 at 12:01am Mountain Time pursuant to paragraph (b) | |

| [ ] | 60 days after filing pursuant to paragraph (a)(1) | |

| [ ] | on (date) pursuant to paragraph (a)(1) | |

| [ ] | 75 days after filing pursuant to paragraph (a)(2) | |

| [ ] | on (date) pursuant to paragraph (a)(2) of rule 485. | |

| If appropriate, check the following box: | ||

| [ ] | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. | |

|

|

Protective Life Dynamic Allocation Series – Conservative Portfolio |

|

Protective Life Dynamic Allocation Series – Moderate Portfolio |

|

Protective Life Dynamic Allocation Series – Growth Portfolio |

Clayton Street Trust

Prospectus

The Securities and Exchange Commission has not approved or disapproved of these securities or passed on the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

This Prospectus describes three portfolios (each, a “Portfolio” and collectively, the “Portfolios”), each a separate series of Clayton Street Trust (the “Trust”). Janus Henderson Investors US LLC (the “Adviser”) serves as investment adviser to each Portfolio.

Each Portfolio currently offers one class of shares (the “Shares”). The Shares are offered by this Prospectus in connection with investment in and payments under variable annuity contracts issued exclusively by Protective Life Insurance Company and its affiliates (“Protective Life”).

This Prospectus contains information that variable annuity contract holders and prospective purchasers should consider in conjunction with the accompanying Protective Life separate account prospectus before allocating purchase payments or premiums to the Portfolios. Each variable annuity contract involves fees and expenses that are not described in this Prospectus. Refer to the accompanying contract prospectus for information regarding contract fees and expenses and any restrictions on purchases or allocations.

Table of Contents

Portfolio Summary |

|

Protective Life Dynamic Allocation Series – Conservative Portfolio |

2 |

Protective Life Dynamic Allocation Series – Moderate Portfolio |

13 |

Protective Life Dynamic Allocation Series – Growth Portfolio |

23 |

Additional Information about the Portfolios |

|

Additional Investment Strategies and General Portfolio Policies |

33 |

Risks of the Portfolios |

40 |

Management of the Portfolios |

|

Investment Adviser |

53 |

Management Expenses |

54 |

Portfolio Management |

55 |

Other Information |

56 |

Distributions and Taxes |

57 |

Shareholder’s Guide |

|

Pricing of Portfolio Shares |

59 |

Distribution, Servicing, and Administrative Fees |

60 |

Payments to Protective Life by the Adviser or its Affiliates |

60 |

Purchases |

61 |

Redemptions |

61 |

Excessive Trading |

62 |

Shareholder Communications |

64 |

Financial Highlights |

65 |

Appendix A |

68 |

1 | Clayton Street Trust

Portfolio Summary

Protective Life Dynamic Allocation Series – Conservative Portfolio

Protective Life Dynamic Allocation Series – Conservative Portfolio (“Conservative Portfolio”) seeks total return through income and growth of capital, balanced by capital preservation.

This table describes the fees and expenses that you may pay if you buy, hold, and sell Shares of the Portfolio. Owners of variable annuity contracts that invest in Shares of the Portfolio should refer to the variable annuity contract prospectus for a description of fees and expenses, as the following table and examples do not reflect deductions at the separate account level or contract level for any charges that may be incurred under a contract. Inclusion of these charges would increase the fees and expenses described below.

|

|

Management Fees |

|

Distribution/Service (12b-1) Fees |

|

Other Expenses |

|

Acquired Fund(1) Fees and Expenses |

|

Total Annual Fund Operating Expenses |

|

Fee Waiver and/or Expense Reimbursement(2)(3) |

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement(2)(3) |

|

(1) |

|

|

(2) |

|

(3) |

|

The Example is intended to help you compare the cost of investing in the Portfolio with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Portfolio for the time periods indicated, reinvest all dividends and distributions, and then redeem all of your Shares at the end of each period. The Example also assumes that your investment has a 5% return each year and that the Portfolio’s operating expenses are equal to the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement for the first year and the Total Annual Fund Operating Expenses thereafter. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

|

$ | $ | $ | $ | ||||||||||||

Portfolio Turnover: The Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Portfolio’s performance. During the most recent fiscal year, the Portfolio’s turnover rate was

2 | Protective Life Dynamic Allocation Series – Conservative Portfolio

The Portfolio seeks to achieve its investment objective by investing in a dynamic portfolio of ETFs (also referred to in this Prospectus as “underlying ETFs”) across seven different equity asset classes, as well as intermediate- and long-duration fixed- income investments (the “Static Fixed-Income Allocation”), and an allocation to short-duration investments (the “Variable Short- Duration Allocation”), which can include cash, money market instruments and short-duration affiliated and unaffiliated underlying ETFs (“short-duration investments”). The equity asset classes and the Variable Short-Duration Allocation are adjusted weekly based on market conditions pursuant to a proprietary, quantitative-based allocation program (the “Allocation Adjustment Program”). Over the long term, and when fully invested, the Portfolio seeks to maintain an asset allocation of approximately 50% global equity investments and 50% intermediate- and long-duration fixed-income investments.

The Allocation Adjustment Program

The Allocation Adjustment Program, a proprietary methodology co-developed by the Adviser and Protective Life, allocates the Portfolio’s assets on a weekly basis among seven different equity asset classes, as well as the Variable Short-Duration Allocation, based on historical market indicators.

The Portfolio’s asset allocation is intended to diversify investments throughout the world among equity investments and intermediate- and long-duration fixed-income investments, and mitigate market risk by adjusting equity investments between market exposure and short-duration investments. Portfolio management oversees the Allocation Adjustment Program and are responsible for the day-to-day management of the Portfolio. Within the parameters of each asset class’ allocation relative to the Portfolio’s total assets, and the target allocation ranges within each asset class, portfolio management reviews the allocation of Portfolio assets in the underlying ETFs and may, without shareholder notice, cease investing in one or more underlying ETFs, modify the underlying ETFs’ weightings or add or substitute other underlying ETFs that provide similar investment exposure, to emphasize and mitigate risk exposures that may arise as a result of the implementation of the allocations.

At no time will an individual asset class exposure be less than zero for investment purposes (i.e., no short exposure), and generally an asset class exposure will not be greater than its maximum target allocation, except due to market movements between periodic rebalancing of the Portfolio. To the extent market movements between periodic rebalancing of the Portfolio results in an asset class exposure in excess of its maximum target allocation, the Portfolio will continue to buy and sell assets reflecting the Portfolio’s current composition as it manages purchase and redemption orders for the Portfolio, and when it implements trades directed by the weekly Allocation Adjustment Program.

Portfolio management may change the Portfolio’s allocations among the asset classes without shareholder notice, unless the Adviser determines it would be a material change to the Portfolio’s investment strategy, in which case shareholders would receive advance notice.

Static Fixed-Income Allocation

The Static Fixed-Income Allocation is expected to remain constant over time, subject to market movement, and will be rebalanced to its target allocation on a quarterly basis. The Portfolio will generally obtain intermediate- and long-duration fixed- income exposure by investing in unaffiliated ETFs that provide broad exposure to the total U.S. investment-grade bond market.

The Underlying ETFs

The Portfolio will obtain the desired market exposure by investing primarily in unaffiliated ETFs that seek to track the performance of one or more broad-based indices, using a passive investment strategy. Because it invests primarily in ETFs, the Portfolio is considered a “fund of funds.” The Portfolio will normally allocate its investments to underlying ETFs to diversify investments throughout the world and provide varying exposure to large-, mid-, or small-capitalization companies, U.S. based and non-U.S. based companies (including those with exposure to emerging markets), and fixed-income securities (including U.S. Treasury, government-related, and corporate, mortgage-backed pass-through securities, commercial mortgage-backed securities, and asset-backed securities). As noted above, the Portfolio may invest in short-duration affiliated and unaffiliated underlying ETFs within its Variable Short-Duration Allocation to seek to mitigate market risk associated with its equity allocation.

3 | Protective Life Dynamic Allocation Series – Conservative Portfolio

The table below shows, for each asset class, the ETFs in which the Portfolio, as of the date of this Prospectus, expects to invest. Portfolio management may choose in their sole discretion, without shareholder notice, to remove, add or substitute other ETFs that provide similar investment exposure in order to obtain the desired market exposure, to further diversify and/or mitigate risk for the Portfolio, or for other reasons, including the liquidity of one or more of the ETFs.

Asset Class |

Potential Underlying ETFs+ |

||

Global Equity Investments (Stocks) |

Asset Class |

Exchange-Traded Funds |

Ticker |

U.S. Large Cap Equity |

20.00% |

SPDR® S&P 500® ETF# iShares® Core S&P 500 ETF* Vanguard S&P 500 ETF |

SPY IVV VOO |

U.S. Small Cap Equity |

7.50% |

iShares® Russell 2000 ETF* iShares® Core S&P Small-Cap ETF* Vanguard Small-Cap ETF |

IWM IJR VB |

U.S. High Growth Equity |

7.50% |

Invesco QQQ TrustSM, Series 1 Invesco NASDAQ 100 ETF |

QQQ QQQM |

U.K. Equity |

5.00% |

iShares® MSCI United Kingdom ETF* Franklin FTSE United Kingdom ETF |

EWU FLGB |

European Equity |

5.00% |

SPDR® Euro Stoxx 50® ETF# Vanguard FTSE Europe ETF JPMorgan BetaBuilders Europe ETF Franklin FTSE Europe ETF |

FEZ VGK BBEU FLEE |

Japan Equity |

2.50% |

iShares® MSCI Japan ETF* Franklin FTSE Japan ETF JPMorgan BetaBuilders Japan ETF |

EWJ FLJP BBJP |

Asia Equity, ex-Japan |

2.50% |

iShares® MSCI All Country Asia ex-Japan ETF* Franklin FTSE Asia ex Japan ETF JPMorgan BetaBuilders Developed Asia Pacific ex-Japan ETF |

AAXJ FLAX BBAX |

Intermediate- and Long-Duration Fixed-Income Investments (Bonds) |

50.00% |

iShares® Core U.S. Aggregate Bond ETF* Vanguard Total Bond Market ETF |

AGG BND |

Short-Duration Fixed-Income Investments |

N/A |

Janus Henderson Short Duration Income ETF JPMorgan Ultra-Short Income ETF PIMCO Enhanced Short Maturity Active ETF Invesco Ultra Short-Duration ETF |

VNLA JPST MINT GSY |

|

(1) |

Represents the target allocation to the respective asset class as a percentage of the Portfolio’s total assets plus, with respect to the equity classes, the remainder, if any, held in short-duration investments. |

|

* |

iShares® is a registered trademark of BlackRock (BlackRock, Inc. and its subsidiaries). |

|

# |

SPDR® is a registered trademark of Standard & Poor’s Financial Services LLC. |

|

+ |

The investment advisers, sponsors and distributors of the underlying ETFs, and the underlying ETFs themselves, do not make any representations regarding the advisability of investing in any of the underlying ETFs. |

Refer to Appendix A in this Prospectus for a brief description of the investment objective and strategies of each of the potential underlying ETFs in which the Portfolio, as of the date of this Prospectus, expects to invest.

As a result of its investments in the underlying ETFs, the Portfolio will have exposure to foreign markets, including emerging markets (which include, but are not limited to, Asia, China, Europe, India, Japan, North America, and South Korea) and various economic sectors (which include, but are not limited to, consumer discretionary, consumer staples, energy, financials, healthcare, industrials, and information technology). Please refer to “Principal Investment Risks” and “Additional Information About the Portfolios” in this Prospectus for more detail.

4 | Protective Life Dynamic Allocation Series – Conservative Portfolio

Variable Short-Duration Allocation

The Portfolio’s Variable Short-Duration Allocation may be as low as 0% or as high as 50% of its assets, depending on prevailing market conditions and the weekly results of the Allocation Adjustment Program. Under normal circumstances, the Portfolio expects the Variable Short-Duration Allocation to be comprised of or provide exposure to securities with varying maturities and an average duration of 2 years or less. Permissible short-duration investments include cash, money market instruments (eligible securities, as defined by Rule 2a-7 under the Investment Company Act of 1940, as amended (the “1940 Act”)) determined by the Adviser to present minimal credit risk, affiliated or unaffiliated money market funds and/or investments in affiliated and unaffiliated underlying ETFs that invest in a portfolio of fixed-income instruments across a broad range of sectors and geographies while maintaining a short-duration portfolio. These underlying ETFs primarily invest in investment grade debt securities including, among others, short-term instruments, such as commercial paper and repurchase agreements, mortgage- backed securities, asset-backed securities, including collateralized debt obligations, and derivatives. The underlying ETFs may also invest in high-yield (or “junk”) bonds. The Portfolio’s short-duration investments may include securities of U.S. and foreign public- and private-sector issuers.

Portfolio management’s selection of investments for the Variable Short-Duration Allocation among short-duration affiliated ETFs, short-duration unaffiliated ETFs, money market instruments and cash may be based on a variety of factors, including prevailing market conditions, to seek to enhance total return and managing risk.

The Portfolio may also invest its cash in a cash sweep program, an arrangement in which the Portfolio’s uninvested cash balance at the end of each day is pooled with uninvested cash of other funds and invested in certain securities such as repurchase agreements or is used to purchase shares of affiliated or non-affiliated money market funds or cash management pooled investment vehicles.

The Portfolio may seek to earn additional income through lending its securities to certain qualified broker-dealers and institutions on a short-term or long-term basis, in an amount equal to up to one-third of its total assets as determined at the time of the loan origination.

Due to the nature of the Allocation Adjustment Program, the Portfolio may have relatively high portfolio turnover compared to other funds.

PRINCIPAL INVESTMENT RISKS |

Main Risks Associated with the Portfolio

Allocation Risk. The Portfolio’s ability to achieve its investment objective depends largely upon the Portfolio’s allocation of assets among the underlying ETFs and short-duration investments, using the Allocation Adjustment Program (a quantitative- based process that allocates equity investments between market exposure and short-duration investments, based on historical market indicators). You could lose money on your investment in the Portfolio as a result of these allocations. The Portfolio will typically invest in a range of different underlying ETFs and short-duration investments; however, to the extent that the Portfolio invests a significant portion of its assets in a single underlying ETF, it will be more sensitive to the risks associated with that underlying ETF and any investments in which that underlying ETF focuses. To the extent the Portfolio’s assets are allocated to short-duration investments, the Portfolio will be subject to risks associated with those investments, may generate returns that are lower than inflation and, in periods of rising market prices, the Portfolio may be unable to participate in such price increases as fully as it may have if its assets were allocated to the equity asset classes.

Investment Process Risk. No assurance can be given that the Portfolio’s investment strategy will be successful under all or any market conditions. Although the Allocation Adjustment Program is designed to achieve the Portfolio’s investment objective, there is no guarantee that it will achieve the desired results, and there is a risk that it may not be successful in identifying how the Portfolio’s assets should be adjusted to reduce the risk of loss in down markets while participating in the upside growth of markets. The Allocation Adjustment Program is a quantitative, model-driven (i.e., rules-based) investment strategy that may perform differently from the market as a whole based on the factors used in the model, the weight placed on each factor, as well as changes in historical trends and market conditions. Historical performance does not indicate future performance, and the assumption that markets will continue to rise or fall based on historical market indicators may prove to be incorrect under certain market conditions. In such cases, implementing a signal from the Allocation Adjustment Program may result

5 | Protective Life Dynamic Allocation Series – Conservative Portfolio

in maintaining or increasing market exposure (or a reduction in exposure), might not provide the intended results, and may adversely impact the Portfolio’s performance. The risk of loss may be heightened during periods of significant market volatility if the Allocation Adjustment Program is not designed to address the specific market conditions present at that time.

Fund of Funds Structure Risk. The Portfolio pursues its investment objective by investing its assets in the underlying ETFs or short-duration investments. The allocation of the Portfolio’s assets to underlying ETFs may not be successful in achieving the Portfolio’s investment objective. There is a risk that you may experience lower returns by investing in the Portfolio instead of investing directly in an underlying ETF. The Portfolio’s returns are directly related to the aggregate performance and expenses of the underlying ETFs in which it invests. The Portfolio, as a shareholder in an underlying ETF, will indirectly bear its pro rata share of the expenses incurred by the underlying ETF. The Portfolio’s return will be net of these expenses, and these expenses may be higher or lower depending upon the allocation of the Portfolio’s assets among the underlying ETFs and the actual expenses of the underlying ETFs. There is additional risk for the Portfolio with respect to aggregation of holdings of underlying ETFs. The aggregation of holdings of underlying ETFs may result in the Portfolio indirectly having increased exposure to a particular industry, geographical sector, or single company. Such indirect exposure may have the effect of increasing the volatility of the Portfolio’s returns. The Portfolio does not control the investments of the underlying ETFs, or any indirect exposure that occurs as a result of the underlying ETFs following their investment objectives. Additionally, to the extent the Portfolio purchases shares of affiliated or non-affiliated money market funds, or cash management pooled investment vehicles, it would bear its pro rata portion of such fund’s expenses, in addition to the expenses the Portfolio bears directly in connection with its own operation.

Exchange-Traded Funds Risk. ETFs are typically open-end investment companies, which may seek to track the performance of a specific index or be actively managed. ETFs are traded on a national securities exchange at market prices that may vary from the net asset value (“NAV”) of their underlying investments. Accordingly, there may be times when an ETF trades at a premium or discount to NAV. As a result, the Portfolio may pay more or less than NAV when it buys ETF shares, and may receive more or less than NAV when it sells those shares. ETFs also involve the risk that an active trading market for an ETF’s shares may not develop or be maintained. Similarly, because the value of ETF shares depends on the demand in the market, the Portfolio may not be able to purchase or sell an ETF at the most optimal time, which could adversely affect the Portfolio’s performance. In addition, ETFs that track particular indices may be unable to match the performance of such underlying indices due to the temporary unavailability of certain index securities in the secondary market or other factors, such as discrepancies with respect to the weighting of securities. Trading of an underlying ETF’s shares may be halted by the activation of individual or market- wide “circuit breakers” (which halt trading for a specific period of time when the price of a particular security or overall market prices decline by a specified percentage). Trading of an ETF’s shares may also be halted if (1) the shares are delisted from an exchange without first being listed on another exchange or (2) exchange officials determine that such action is appropriate in the interest of a fair and orderly market or for the protection of investors.

Affiliated Underlying Fund Risk. The Adviser may invest in certain underlying affiliated ETFs and money market funds (or unregistered cash management pooled investment vehicles that operate as money market funds) as investments for the Portfolio. The Adviser will generally receive fees for managing such funds, in addition to the fees paid to the Adviser by the Portfolio. The payment of such fees by underlying affiliated funds creates a conflict of interest when selecting underlying affiliated funds for investment in the Portfolio. The Adviser, however, is a fiduciary to the Portfolio and its shareholders and is legally obligated to act in their best interest when selecting underlying affiliated funds. In addition, the Adviser has contractually agreed to waive and/or reimburse a portion of the Portfolio’s management fee in an amount equal to the management fee it earns as an investment adviser to any of the underlying affiliated ETFs with respect to the Portfolio’s investment in such ETF, less certain asset-based operating fees and expenses.

Risks of Holding Short-Duration Investments. To the extent the Portfolio’s assets are allocated to short-duration investments, the Portfolio may be subject to the following risks:

|

● |

Credit Quality Risk. The value of the securities which the Portfolio may hold may fall based on an issuer’s actual or perceived creditworthiness, or an issuer’s ability to meet its obligations. The credit quality of the Portfolio’s holdings can change rapidly in certain market environments and any downgrade or default of a portfolio security could result in a decline in the Portfolio’s income and potentially in the value of the Portfolio’s investments. |

|

● |

Counterparty Risk. Portfolio transactions involving a counterparty are subject to the risk that the counterparty or a third party will not fulfill its obligation to the Portfolio (“counterparty risk”). Counterparty risk may arise because of the counterparty’s financial condition (i.e., financial difficulties, bankruptcy, or insolvency), market activities and developments, or other reasons, whether foreseen or not. A counterparty’s inability to fulfill its obligation may result in |

6 | Protective Life Dynamic Allocation Series – Conservative Portfolio

significant financial loss to the Portfolio. The Portfolio may be unable to recover its investment from the counterparty or may obtain a limited recovery, and/or recovery may be delayed. The Portfolio may be exposed to counterparty risk through its investments in certain securities, including, but not limited to, repurchase agreements and debt securities. The Portfolio intends to enter into financial transactions with counterparties that the Adviser believes to be creditworthy at the time of the transaction. There is always the risk that the Adviser’s analysis of a counterparty’s creditworthiness is incorrect or may change due to market conditions. To the extent that the Portfolio focuses its transactions with a limited number of counterparties, it will have greater exposure to the risks associated with one or more counterparties.

|

● |

Interest Rate Risk. An increase in interest rates may cause the value of fixed-income securities held by the Portfolio to decline. In inflationary conditions, the Portfolio may be subject to a greater risk of rising interest rates as a result of government fiscal policy initiatives and resulting market reaction to those initiatives. Variable and floating rate securities may increase or decrease in value in response to changes in interest rates, although generally to a lesser degree than fixed-income securities. |

Securities Lending Risk. There is the risk that when portfolio securities are lent, the securities may not be returned on a timely basis, and the Portfolio may experience delays and costs in recovering the security or gaining access to the collateral provided to the Portfolio to collateralize the loan. If the Portfolio is unable to recover a security on loan, the Portfolio may use the collateral to purchase replacement securities in the market. There is a risk that the value of the collateral could decrease below the cost of the replacement security by the time the replacement investment is made, resulting in a loss to the Portfolio.

Portfolio Turnover Risk. Increased portfolio turnover may result in higher costs, which may have a negative effect on the Portfolio’s performance. Due to operation of the Allocation Adjustment Program, the Portfolio may experience higher portfolio turnover as the result of equity market volatility.

Risks Through Investing in the Underlying ETFs

The ability of the Portfolio to realize its investment objective will depend, in large part, on the extent to which the underlying ETFs realize their respective investment objectives. Similarly, the Portfolio’s investment performance is directly related to the investment performance of the underlying ETFs it holds. The Portfolio is subject to the risk factors associated with the investments of the underlying ETFs, and will be affected by such risks in direct proportion to the allocation of its assets among the underlying ETFs. Therefore, to the extent that the Portfolio invests significantly in a particular underlying ETF, the Portfolio’s performance would be significantly impacted by the performance of such underlying ETF. What follows are the main risks associated with the underlying ETFs, which, in turn, may be considered to be principal risks of the Portfolio. These risks are subject to change based on the allocation of the Portfolio’s assets among the underlying ETFs.

Market Risk. The market price of investments owned by the Portfolio or an underlying ETF may go up or down. Market risk may affect a single issuer, industry, economic sector, or the market as a whole. Market risk may be magnified if certain social, political, economic and other conditions and events (such as financial institution failures, economic recessions, tariffs, trade disputes, terrorism, war, armed conflicts, including related sanctions, social unrest, natural disasters, and epidemics and pandemics) adversely interrupt the global economy and financial markets. It is important to understand that the value of your investment may fall, sometimes sharply, in response to changes in the market, and you could lose money.

Equity Securities Risk. Equity securities are subject to changes in value, and their values may be more volatile than those of other asset classes. The value of an underlying ETF’s portfolio may decrease if the value of an individual company or security, or multiple companies or securities, in the portfolio decreases. Further, regardless of how well individual companies or securities perform, the value of an underlying ETF’s portfolio could also decrease if there are deteriorating economic or market conditions or perceptions regarding the industries in which the issuers of securities the underlying ETF holds participate.

Passive Investment Risk. Certain of the underlying ETFs are not actively managed and therefore an underlying ETF might not sell shares of a security due to current or projected underperformance of a security, industry, or sector, unless that security is removed from the index or the selling of shares is otherwise required upon a rebalancing of the index the underlying ETF seeks to track. Maintaining investments in securities without attempting to take defensive positions, regardless of market conditions or the performance of individual securities, could cause an underlying ETF’s return to be lower than if it had employed an active strategy.

Fixed-Income Securities Risk. Certain of the underlying ETFs invest in a variety of fixed-income securities that are generally subject to the following risks:

7 | Protective Life Dynamic Allocation Series – Conservative Portfolio

|

● |

Interest rate risk, which is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. Changes in interest rates have unpredictable effects on the markets and may expose fixed-income and related markets to heightened volatility. |

|

● |

Credit risk, which is the risk that the credit strength of an issuer of a fixed-income security will weaken and/or that the issuer will be unable to make timely principal and interest payments and that the security may go into default. |

|

● |

Prepayment risk, which is the risk that, during periods of falling interest rates, certain fixed-income securities may be paid off quicker than originally anticipated, which may cause an underlying ETF to reinvest its assets in securities with lower yields, resulting in a decline in an underlying ETF’s income or return potential. |

|

● |

Income risk, which is the risk that an underlying ETF’s income may decline when interest rates fall, or when there is a change in an underlying ETF’s investments because (i) the fixed-income securities in the underlying ETF’s portfolio mature and it subsequently invests in lower-yielding fixed-income securities, (ii) the fixed-income securities in the ETF’s underlying index are substituted, or (iii) the underlying ETF otherwise needs to purchase additional fixed-income securities. |

|

● |

Extension risk, which is the risk that, during periods of rising interest rates, certain fixed-income securities may be paid off substantially slower than originally anticipated, and as a result, the value of those fixed-income securities may fall. |

|

● |

Valuation risk, which is the risk that one or more of the fixed-income securities in which an underlying ETF invests are priced differently than the value realized upon such security’s sale. In times of market instability, valuation may be more difficult. Valuation may also be affected by changes in the issuer’s financial strength, the market’s perception of such strength, or in the credit rating of the issuer or the security. |

|

● |

Liquidity risk, which is the risk that fixed-income securities may be difficult or impossible to sell at the time that an underlying ETF seeks to sell. In unusual market conditions, even normally liquid securities may be affected by a degree of liquidity risk (i.e., if the number and capacity of traditional market participants is reduced). |

|

● |

Call risk, which is the risk that during periods of falling interest rates, an issuer of a callable fixed-income security held by an underlying ETF may “call” or repay the security before its stated maturity, and the underlying ETF may have to reinvest the proceeds at lower interest rates, resulting in a decline in the underlying ETF’s income. |

High-Yield Bonds Risk. High-yield bonds (also known as “junk” bonds) are considered speculative and may be more sensitive than other types of bonds to economic changes, political changes, or adverse developments specific to the entity that issued the bond, which may adversely affect their value.

Derivatives Risk. Derivatives used by an underlying ETF, such as swaps, forwards, futures, and options, involve risks in addition to the risks of the underlying referenced securities or asset. Gains or losses from a derivative investment can be substantially greater than the derivative’s original cost and can therefore involve leverage. Leverage may cause an underlying ETF to be more volatile than if it had not used leverage. Because most derivatives are not currently eligible to be transferred in-kind, an underlying ETF may be subject to increased liquidity risk to the extent its derivative positions become less liquid. Derivatives entail the risk that the counterparty will default on its payment obligations. Derivatives used for hedging purposes may reduce or eliminate losses if the market moves in a manner different from that anticipated by portfolio management or if the cost of the derivative outweighs the benefit of the hedge. The risks associated with derivatives may be heightened when they are used to enhance an underlying ETF’s return rather than solely for hedging purposes. Changes in laws or regulations may make the use of derivatives more costly, may limit the availability of derivatives, or may otherwise adversely affect the use, value or performance of derivatives.

Sovereign Debt Risk. An underlying ETF may invest in U.S. and non-U.S. government debt securities (“sovereign debt”). Investments in sovereign debt can involve a high degree of risk, including the risk that the governmental entity that controls the repayment of sovereign debt may not be willing or able to repay the principal and/or to pay the interest on its sovereign debt in a timely manner. A sovereign debtor’s willingness or ability to satisfy its debt obligation may be affected by various factors including, but not limited to, its cash flow situation, the extent of its foreign currency reserves, the availability of foreign exchange when a payment is due, and the relative size of its debt position in relation to its economy as a whole. In the event of default, there may be limited or no legal remedies for collecting sovereign debt and there may be no bankruptcy proceedings through which the underlying ETF may collect all or part of the sovereign debt that a governmental entity has not repaid. In addition, to the extent the underlying ETF invests in non-U.S. sovereign debt, it may be subject to currency risk.

8 | Protective Life Dynamic Allocation Series – Conservative Portfolio

Foreign Exposure Risk. Foreign markets, including emerging markets, can be more volatile than the U.S. market. As a result, an underlying ETF’s returns and net asset value may be affected by fluctuations in currency exchange rates or political or economic conditions in a particular country. Investments in foreign securities, particularly those of issuers located in emerging market countries, tend to have greater exposure to liquidity risk than domestic securities. In some foreign markets, there may not be protection against failure by other parties to complete transactions. It may not be possible for an underlying ETF to repatriate capital, dividends, interest, and other income from a particular country or governmental entity. In addition, a market swing in one or more countries or regions where an underlying ETF has invested a significant amount of its assets may have a greater effect on an underlying ETF’s performance than it would in a more geographically diversified portfolio. To the extent that an underlying ETF invests in foreign debt securities, such investments are sensitive to changes in interest rates. Additionally, investments in securities of foreign governments involve the risk that a foreign government may not be willing or able to pay interest or repay principal when due. An underlying ETF’s investments in emerging market countries may involve risks greater than, or in addition to, the risks of investing in more developed countries.

Risk of Investing in Europe. Certain underlying ETFs may have significant exposure to European markets. Developed and emerging market countries in Europe will be significantly affected by the fiscal and monetary controls of the European Monetary Union. Changes in regulations on trade, decreasing imports or exports, changes in the exchange rate of the euro, and recessions among European countries may have a significant adverse effect on the economies of other European countries including those of Eastern Europe. The markets in Eastern Europe remain relatively undeveloped and can be particularly sensitive to political and economic developments.

|

● |

Risk of Investing in the United Kingdom. Certain underlying ETFs may have significant exposure to the United Kingdom. Investments in British issuers may subject an underlying ETF to regulatory, political, currency, security, and economic risk specific to the United Kingdom. The United Kingdom has one of the largest economies in Europe, and the United States and other European countries are substantial trading partners of the United Kingdom. As a result, the British economy may be impacted by changes to the economic health of the United States and other European countries. |

Risk of Investing in Japan. The Japanese economy may be subject to considerable degrees of economic, political, and social instability, which could have a negative impact on Japanese securities. Since the year 2000, Japan’s economic growth rate has remained relatively low, and it may remain low in the future. In addition, Japan is subject to the risk of natural disasters, such as earthquakes, volcanic eruptions, typhoons, and tsunamis, which could negatively affect an underlying ETF’s investment.

Risk of Investing in Asia. Investments in securities of issuers in certain Asian countries involve risks that are specific to Asia, including certain legal, regulatory, political, and economic risks. Certain Asian countries have experienced expropriation and/or nationalization of assets, confiscatory taxation, political instability, armed conflict and social instability as a result of religious, ethnic, socio-economic and/or political unrest. Some economies in this region are dependent on a range of commodities, and are strongly affected by international commodity prices and particularly vulnerable to price changes for these products. The market for securities in this region may also be directly influenced by the flow of international capital, and by the economic and market conditions of neighboring countries. Many Asian economies have experienced rapid growth and industrialization, and there is no assurance that this growth rate will be maintained. Some Asian economies are highly dependent on trade and economic conditions in other countries can impact these economies.

Industry and Sector Risk. To the extent that an underlying ETF’s investments are focused in the securities of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class, the underlying ETF may be susceptible to an increased risk of loss, including losses due to adverse events that affect the underlying ETF’s investments more than the market as a whole.

Large-Capitalization Companies Risk. Certain underlying ETFs’ investments in securities issued by large-capitalization companies will be subject to the risk that returns on stocks of large companies could trail the returns on investments in stocks of small- and mid-sized companies. Large-cap stocks tend to go through cycles of doing better – or worse – than other segments of the stock market or the stock market in general. These periods have, in the past, lasted for as long as several years.

Small- and Mid-Sized Companies Risk. Certain underlying ETFs’ investments in securities issued by small- and mid-sized companies, which can include smaller, start-up companies offering emerging products or services, may involve greater risks than are customarily associated with larger, more established companies. For example, small- and mid-sized companies may suffer more significant losses as a result of their narrow product lines, limited operating history, greater exposure to competitive threats, limited financial resources, limited trading markets, and the potential lack of management depth.

9 | Protective Life Dynamic Allocation Series – Conservative Portfolio

Securities issued by small- and mid-sized companies tend to be more volatile and somewhat more speculative than securities issued by larger or more established companies and may underperform as compared to the securities of larger or more established companies. These holdings are also subject to wider price fluctuations and tend to be less liquid than stocks of larger or more established companies, which could have a significant adverse effect on an underlying ETF’s returns, especially as market conditions change.

Mortgage- and Asset-Backed Securities Risk. Mortgage- and asset-backed securities represent interests in “pools” of commercial or residential mortgages or other assets, including consumer loans or receivables. The value of mortgage- and asset- backed securities will be influenced by factors affecting the real estate market and the assets underlying these securities. Investments in mortgage- and asset-backed securities may be subject to credit risk, valuation risk, liquidity risk, extension risk, and prepayment risk. These securities also are subject to risk of default on the underlying mortgage or asset, particularly during periods of economic downturn.

Illiquid Investments Risk. To the extent the Portfolio or underlying ETF invests in illiquid investments or investments that become less liquid, such investments may have a negative effect on the returns of the Portfolio or underlying ETF because the Portfolio or underlying ETF may be unable to sell the illiquid investments at an advantageous time or price.

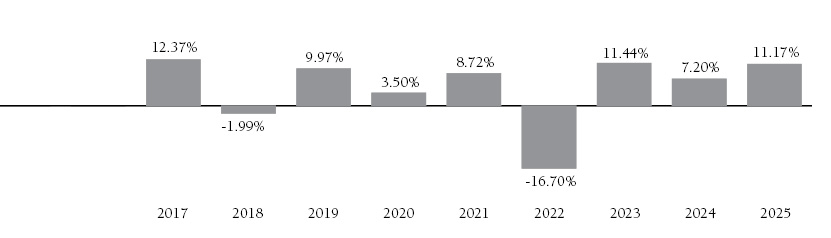

Annual Total Returns (calendar year-end) |

4th Quarter 2023 |

1st Quarter 2020 |

– |

10 | Protective Life Dynamic Allocation Series – Conservative Portfolio

|

1 Year |

5 Years |

Since |

Protective Life Dynamic Allocation Series – Conservative Portfolio |

|||

Protective Life Dynamic Allocation Series – Conservative Portfolio |

|||

MSCI All Country World IndexSM (reflects no deduction for expenses, fees or taxes, except foreign withholding taxes) |

|||

Protective Life Conservative Allocation Index (reflects no deduction for expenses, fees or taxes) |

The Portfolio’s broad-based benchmark index is the MSCI All Country World Index. The Portfolio’s additional benchmark index is the Protective Life Conservative Allocation Index. The indices are described below.

|

● |

The MSCI All Country World Index is designed to measure equity market performance in global developed and emerging markets. |

|

● |

The Protective Life Conservative Allocation Index is an internally-calculated, hypothetical combination of total returns from the MSCI All Country World Index (50%) and the Bloomberg U.S. Aggregate Bond Index (50%). The Bloomberg U.S. Aggregate Bond Index is a broad-based measure of the U.S. investment grade fixed-rate debt market. |

MANAGEMENT |

Investment Adviser: Janus Henderson Investors US LLC

Portfolio Management: Benjamin Wang, CFA, is Co-Portfolio Manager of the Portfolio, which he has co-managed since inception in April 2016. Zoey Zhu, CFA, is Co-Portfolio Manager of the Portfolio, which she has co-managed since May 2020.

PURCHASE AND SALE OF PORTFOLIO SHARES |

Purchases of Shares of the Portfolio may be made only by the separate accounts of Protective Life for the purpose of funding variable annuity contracts. Redemptions, like purchases, may be effected only through the separate accounts of Protective Life. Requests are duly processed at the NAV next calculated after your order is received in good order by the Portfolio or its agents. Refer to Protective Life’s separate account prospectus for details.

TAX INFORMATION |

Because Shares of the Portfolio may be purchased only through variable annuity contracts, it is anticipated that any income dividends or net capital gains distributions made by the Portfolio will be exempt from current federal income taxation if left to accumulate within the variable annuity contract. Generally, withdrawals from such contracts may be subject to federal income tax at ordinary income rates and, if made before age 59 ½, a 10% penalty. The federal income tax status of your investment depends on the features of your variable annuity contract. Further information may be found in Protective Life’s separate account prospectus.

PAYMENTS TO INSURERS, BROKER-DEALERS, AND OTHER FINANCIAL INTERMEDIARIES |

Shares of the Portfolio are only available through Protective Life’s variable annuity contracts. The Portfolio or its distributor (and/or their related companies) make payments to Protective Life and/or its related companies for distribution and/or other services; some of the payments may go to broker-dealers and other financial intermediaries. These payments may create a

11 | Protective Life Dynamic Allocation Series – Conservative Portfolio

conflict of interest for an intermediary, or be a factor in Protective Life’s decision to include the Portfolio as an underlying investment option in a variable annuity contract. Ask your financial advisor, visit Protective Life’s website, or consult your variable annuity contract prospectus for more information.

12 | Protective Life Dynamic Allocation Series – Conservative Portfolio

Portfolio summary

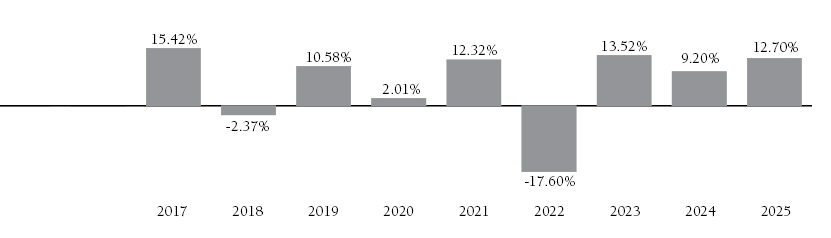

Protective Life Dynamic Allocation Series – Moderate Portfolio

Protective Life Dynamic Allocation Series – Moderate Portfolio (“Moderate Portfolio”) seeks total return through growth of capital and income, balanced by capital preservation.

This table describes the fees and expenses that you may pay if you buy, hold, and sell Shares of the Portfolio. Owners of variable annuity contracts that invest in Shares of the Portfolio should refer to the variable annuity contract prospectus for a description of fees and expenses, as the following table and examples do not reflect deductions at the separate account level or contract level for any charges that may be incurred under a contract. Inclusion of these charges would increase the fees and expenses described below.

|

|

Management Fees |

|

Distribution/Service (12b-1) Fees |

|

Other Expenses |

|

Acquired Fund(1) Fees and Expenses |

|

Total Annual Fund Operating Expenses |

|

Fee Waiver and/or Expense Reimbursement(2)(3) |

|

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement(2)(3) |

|

(1) |

|

|

(2) |

|

|

(3) |

|

The Example is intended to help you compare the cost of investing in the Portfolio with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Portfolio for the time periods indicated, reinvest all dividends and distributions, and then redeem all of your Shares at the end of each period. The Example also assumes that your investment has a 5% return each year and that the Portfolio’s operating expenses are equal to the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement for the first year and the Total Annual Fund Operating Expenses thereafter. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

1 Year |

3 Years |

5 Years |

10 Years |

||||||||||||

|

$ | $ | $ | $ | ||||||||||||

Portfolio Turnover: The Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Portfolio’s performance. During the most recent fiscal year, the Portfolio’s turnover rate was

13 | Protective Life Dynamic Allocation Series – Moderate Portfolio

The Portfolio seeks to achieve its investment objective by investing in a dynamic portfolio of ETFs (also referred to in this Prospectus as “underlying ETFs”) across seven different equity asset classes, as well as intermediate- and long-duration fixed- income investments (the “Static Fixed-Income Allocation”), and an allocation to short-duration investments (the “Variable Short- Duration Allocation”), which can include cash, money market instruments and short-duration affiliated and unaffiliated underlying ETFs (“short-duration investments”). The equity asset classes and the Variable Short-Duration Allocation are adjusted weekly based on market conditions pursuant to a proprietary, quantitative-based allocation program (the “Allocation Adjustment Program”). Over the long term, and when fully invested, the Portfolio seeks to maintain an asset allocation of approximately 65% global equity investments and 35% intermediate- and long-duration fixed-income investments.

The Allocation Adjustment Program

The Allocation Adjustment Program, a proprietary methodology co-developed by the Adviser and Protective Life, allocates the Portfolio’s assets on a weekly basis among seven different equity asset classes, as well as the Variable Short-Duration Allocation, based on historical market indicators.

The Portfolio’s asset allocation is intended to diversify investments throughout the world among equity investments and intermediate- and long-duration fixed-income investments, and mitigate market risk by adjusting equity investments between market exposure and short-duration investments. Portfolio management oversees the Allocation Adjustment Program and are responsible for the day-to-day management of the Portfolio. Within the parameters of each asset class’ allocation relative to the Portfolio’s total assets, and the target allocation ranges within each asset class, portfolio management reviews the allocation of Portfolio assets in the underlying ETFs and may, without shareholder notice, cease investing in one or more underlying ETFs, modify the underlying ETFs’ weightings or add or substitute other underlying ETFs that provide similar investment exposure, to emphasize and mitigate risk exposures that may arise as a result of the implementation of the allocations.

At no time will an individual asset class exposure be less than zero for investment purposes (i.e., no short exposure), and generally an asset class exposure will not be greater than its maximum target allocation, except due to market movements between periodic rebalancing of the Portfolio. To the extent market movements between periodic rebalancing of the Portfolio results in an asset class exposure in excess of its maximum target allocation, the Portfolio will continue to buy and sell assets reflecting the Portfolio’s current composition as it manages purchase and redemption orders for the Portfolio, and when it implements trades directed by the weekly Allocation Adjustment Program.

Portfolio management may change the Portfolio’s allocations among the asset classes without shareholder notice, unless the Adviser determines it would be a material change to the Portfolio’s investment strategy, in which case shareholders would receive advance notice.

Static Fixed-Income Allocation

The Static Fixed-Income Allocation is expected to remain constant over time, subject to market movement, and will be rebalanced to its target allocation on a quarterly basis. The Portfolio will generally obtain intermediate- and long-duration fixed- income exposure by investing in unaffiliated ETFs that provide broad exposure to the total U.S. investment-grade bond market.

The Underlying ETFs

The Portfolio will obtain the desired market exposure by investing primarily in unaffiliated ETFs that seek to track the performance of one or more broad-based indices, using a passive investment strategy. Because it invests primarily in ETFs, the Portfolio is considered a “fund of funds.” The Portfolio will normally allocate its investments to underlying ETFs to diversify investments throughout the world and provide varying exposure to large-, mid-, or small-capitalization companies, U.S. based and non-U.S. based companies (including those with exposure to emerging markets), and fixed-income securities (including U.S. Treasury, government-related, and corporate, mortgage-backed pass-through securities, commercial mortgage-backed securities, and asset-backed securities). As noted above, the Portfolio may invest in short-duration affiliated and unaffiliated underlying ETFs within its Variable Short-Duration Allocation to seek to mitigate market risk associated with its equity allocation.

14 | Protective Life Dynamic Allocation Series – Moderate Portfolio

The table below shows, for each asset class, the ETFs in which the Portfolio, as of the date of this Prospectus, expects to invest. Portfolio management may choose in their sole discretion, without shareholder notice, to remove, add or substitute other ETFs that provide similar investment exposure in order to obtain the desired market exposure, to further diversify and/or mitigate risk for the Portfolio, or for other reasons, including the liquidity of one or more of the ETFs.

Asset Class |

Potential Underlying ETFs+ |

||

Global Equity Investments (Stocks) |

Asset Class |

Exchange-Traded Funds |

Ticker |

U.S. Large Cap Equity |

26.00% |

SPDR® S&P 500® ETF# iShares® Core S&P 500 ETF* Vanguard S&P 500 ETF |

SPY IVV VOO |

U.S. Small Cap Equity |

9.75% |

iShares® Russell 2000 ETF* iShares® Core S&P Small-Cap ETF* Vanguard Small-Cap ETF |

IWM IJR VB |

U.S. High Growth Equity |

9.75% |

Invesco QQQ TrustSM, Series 1 Invesco NASDAQ 100 ETF |

QQQ QQQM |

U.K. Equity |

6.50% |

iShares® MSCI United Kingdom ETF* Franklin FTSE United Kingdom ETF |

EWU FLGB |

European Equity |

6.50% |

SPDR® Euro Stoxx 50® ETF# Vanguard FTSE Europe ETF JPMorgan BetaBuilders Europe ETF Franklin FTSE Europe ETF |

FEZ VGK BBEU FLEE |

Japan Equity |

3.25% |

iShares® MSCI Japan ETF* Franklin FTSE Japan ETF JPMorgan BetaBuilders Japan ETF |

EWJ FLJP BBJP |

Asia Equity, ex-Japan |

3.25% |

iShares® MSCI All Country Asia ex-Japan ETF* Franklin FTSE Asia ex Japan ETF JPMorgan BetaBuilders Developed Asia Pacific ex-Japan ETF |

AAXJ FLAX BBAX |

Intermediate-and Long-Duration Fixed-Income Investments (Bonds) |

35.00% |

iShares® Core U.S. Aggregate Bond ETF* Vanguard Total Bond Market ETF |

AGG BND |

Short-Duration Fixed-Income Investments |

N/A |

Janus Henderson Short Duration Income ETF JPMorgan Ultra-Short Income ETF PIMCO Enhanced Short Maturity Active ETF Invesco Ultra Short-Duration ETF |

VNLA JPST MINT GSY |

|

(1) |

Represents the target allocation to the respective asset class as a percentage of the Portfolio’s total assets plus, with respect to the equity classes, the remainder, if any, held in short-duration investments. |

|

* |

iShares® is a registered trademark of BlackRock (BlackRock, Inc. and its subsidiaries). |

|

# |

SPDR® is a registered trademark of Standard & Poor’s Financial Services LLC. |

|

+ |

The investment advisers, sponsors and distributors of the underlying ETFs, and the underlying ETFs themselves, do not make any representations regarding the advisability of investing in any of the underlying ETFs. |

Refer to Appendix A in this Prospectus for a brief description of the investment objective and strategies of each of the potential underlying ETFs in which the Portfolio, as of the date of this Prospectus, expects to invest.

As a result of its investments in the underlying ETFs, the Portfolio will have exposure to foreign markets, including emerging markets (which include, but are not limited to, Asia, China, Europe, India, Japan, North America, and South Korea) and various economic sectors (which include, but are not limited to, consumer discretionary, consumer staples, energy, financials, healthcare, industrials, and information technology). Please refer to “Principal Investment Risks” and “Additional Information About the Portfolios” in this Prospectus for more detail.

15 | Protective Life Dynamic Allocation Series – Moderate Portfolio

Variable Short-Duration Allocation

The Portfolio’s Variable Short-Duration Allocation may be as low as 0% or as high as 65% of its assets, depending on prevailing market conditions and the weekly results of the Allocation Adjustment Program. Under normal circumstances, the Portfolio expects the Variable Short-Duration Allocation to be comprised of or provide exposure to securities with varying maturities and an average duration of 2 years or less. Permissible short-duration investments include cash, money market instruments (eligible securities, as defined by Rule 2a-7 under the Investment Company Act of 1940, as amended (the “1940 Act”)) determined by the Adviser to present minimal credit risk, affiliated or unaffiliated money market funds and/or investments in affiliated and unaffiliated underlying ETFs that invest in a portfolio of fixed-income instruments across a broad range of sectors and geographies while maintaining a short-duration portfolio. These underlying ETFs primarily invest in investment grade debt securities including, among others, short-term instruments, such as commercial paper and repurchase agreements, mortgage- backed securities, asset-backed securities, including collateralized debt obligations, and derivatives. The underlying ETFs may also invest in high-yield (or “junk”) bonds. The Portfolio’s short-duration investments may include securities of U.S. and foreign public- and private-sector issuers.

Portfolio management’s selection of investments for the Variable Short-Duration Allocation among short-duration affiliated ETFs, short-duration unaffiliated ETFs, money market instruments and cash may be based on a variety of factors, including prevailing market conditions, to seek to enhance total return and managing risk.

The Portfolio may also invest its cash in a cash sweep program, an arrangement in which the Portfolio’s uninvested cash balance at the end of each day is pooled with uninvested cash of other funds and invested in certain securities such as repurchase agreements or is used to purchase shares of affiliated or non-affiliated money market funds or cash management pooled investment vehicles.

The Portfolio may seek to earn additional income through lending its securities to certain qualified broker-dealers and institutions on a short-term or long-term basis, in an amount equal to up to one-third of its total assets as determined at the time of the loan origination.

Due to the nature of the Allocation Adjustment Program, the Portfolio may have relatively high portfolio turnover compared to other funds.

PRINCIPAL INVESTMENT RISKS |

Main Risks Associated with the Portfolio

Allocation Risk. The Portfolio’s ability to achieve its investment objective depends largely upon the Portfolio’s allocation of assets among the underlying ETFs and short-duration investments, using the Allocation Adjustment Program (a quantitative- based process that allocates equity investments between market exposure and short-duration investments, based on historical market indicators). You could lose money on your investment in the Portfolio as a result of these allocations. The Portfolio will typically invest in a range of different underlying ETFs and short-duration investments; however, to the extent that the Portfolio invests a significant portion of its assets in a single underlying ETF, it will be more sensitive to the risks associated with that underlying ETF and any investments in which that underlying ETF focuses. To the extent the Portfolio’s assets are allocated to short-duration investments, the Portfolio will be subject to risks associated with those investments, may generate returns that are lower than inflation and, in periods of rising market prices, the Portfolio may be unable to participate in such price increases as fully as it may have if its assets were allocated to the equity asset classes.

Investment Process Risk. No assurance can be given that the Portfolio’s investment strategy will be successful under all or any market conditions. Although the Allocation Adjustment Program is designed to achieve the Portfolio’s investment objective, there is no guarantee that it will achieve the desired results, and there is a risk that it may not be successful in identifying how the Portfolio’s assets should be adjusted to reduce the risk of loss in down markets while participating in the upside growth of markets. The Allocation Adjustment Program is a quantitative, model-driven (i.e., rules-based) investment strategy that may perform differently from the market as a whole based on the factors used in the model, the weight placed on each factor, as well as changes in historical trends and market conditions. Historical performance does not indicate future performance, and the assumption that markets will continue to rise or fall based on historical market indicators may prove to be incorrect under certain market conditions. In such cases, implementing a signal from the Allocation Adjustment Program may result

16 | Protective Life Dynamic Allocation Series – Moderate Portfolio

in maintaining or increasing market exposure (or a reduction in exposure), might not provide the intended results, and may adversely impact the Portfolio’s performance. The risk of loss may be heightened during periods of significant market volatility if the Allocation Adjustment Program is not designed to address the specific market conditions present at that time.

Fund of Funds Structure Risk. The Portfolio pursues its investment objective by investing its assets in the underlying ETFs or short-duration investments. The allocation of the Portfolio’s assets to underlying ETFs may not be successful in achieving the Portfolio’s investment objective. There is a risk that you may experience lower returns by investing in the Portfolio instead of investing directly in an underlying ETF. The Portfolio’s returns are directly related to the aggregate performance and expenses of the underlying ETFs in which it invests. The Portfolio, as a shareholder in an underlying ETF, will indirectly bear its pro rata share of the expenses incurred by the underlying ETF. The Portfolio’s return will be net of these expenses, and these expenses may be higher or lower depending upon the allocation of the Portfolio’s assets among the underlying ETFs and the actual expenses of the underlying ETFs. There is additional risk for the Portfolio with respect to aggregation of holdings of underlying ETFs. The aggregation of holdings of underlying ETFs may result in the Portfolio indirectly having increased exposure to a particular industry, geographical sector, or single company. Such indirect exposure may have the effect of increasing the volatility of the Portfolio’s returns. The Portfolio does not control the investments of the underlying ETFs, or any indirect exposure that occurs as a result of the underlying ETFs following their investment objectives. Additionally, to the extent the Portfolio purchases shares of affiliated or non-affiliated money market funds, or cash management pooled investment vehicles, it would bear its pro rata portion of such fund’s expenses, in addition to the expenses the Portfolio bears directly in connection with its own operation.

Exchange-Traded Funds Risk. ETFs are typically open-end investment companies, which may seek to track the performance of a specific index or be actively managed. ETFs are traded on a national securities exchange at market prices that may vary from the net asset value (“NAV”) of their underlying investments. Accordingly, there may be times when an ETF trades at a premium or discount to NAV. As a result, the Portfolio may pay more or less than NAV when it buys ETF shares, and may receive more or less than NAV when it sells those shares. ETFs also involve the risk that an active trading market for an ETF’s shares may not develop or be maintained. Similarly, because the value of ETF shares depends on the demand in the market, the Portfolio may not be able to purchase or sell an ETF at the most optimal time, which could adversely affect the Portfolio’s performance. In addition, ETFs that track particular indices may be unable to match the performance of such underlying indices due to the temporary unavailability of certain index securities in the secondary market or other factors, such as discrepancies with respect to the weighting of securities. Trading of an underlying ETF’s shares may be halted by the activation of individual or market- wide “circuit breakers” (which halt trading for a specific period of time when the price of a particular security or overall market prices decline by a specified percentage). Trading of an ETF’s shares may also be halted if (1) the shares are delisted from an exchange without first being listed on another exchange or (2) exchange officials determine that such action is appropriate in the interest of a fair and orderly market or for the protection of investors.

Affiliated Underlying Fund Risk. The Adviser may invest in certain underlying affiliated ETFs and money market funds (or unregistered cash management pooled investment vehicles that operate as money market funds) as investments for the Portfolio. The Adviser will generally receive fees for managing such funds, in addition to the fees paid to the Adviser by the Portfolio. The payment of such fees by underlying affiliated funds creates a conflict of interest when selecting underlying affiliated funds for investment in the Portfolio. The Adviser, however, is a fiduciary to the Portfolio and its shareholders and is legally obligated to act in their best interest when selecting underlying affiliated funds. In addition, the Adviser has contractually agreed to waive and/or reimburse a portion of the Portfolio’s management fee in an amount equal to the management fee it earns as an investment adviser to any of the underlying affiliated ETFs with respect to the Portfolio’s investment in such ETF, less certain asset-based operating fees and expenses.

Risks of Holding Short-Duration Investments. To the extent the Portfolio’s assets are allocated to short-duration investments, the Portfolio may be subject to the following risks:

|

● |

Credit Quality Risk. The value of the securities which the Portfolio may hold may fall based on an issuer’s actual or perceived creditworthiness, or an issuer’s ability to meet its obligations. The credit quality of the Portfolio’s holdings can change rapidly in certain market environments and any downgrade or default of a portfolio security could result in a decline in the Portfolio’s income and potentially in the value of the Portfolio’s investments. |

|

● |

Counterparty Risk. Portfolio transactions involving a counterparty are subject to the risk that the counterparty or a third party will not fulfill its obligation to the Portfolio (“counterparty risk”). Counterparty risk may arise because of the counterparty’s financial condition (i.e., financial difficulties, bankruptcy, or insolvency), market activities and developments, or other reasons, whether foreseen or not. A counterparty’s inability to fulfill its obligation may result in |

17 | Protective Life Dynamic Allocation Series – Moderate Portfolio

significant financial loss to the Portfolio. The Portfolio may be unable to recover its investment from the counterparty or may obtain a limited recovery, and/or recovery may be delayed. The Portfolio may be exposed to counterparty risk through its investments in certain securities, including, but not limited to, repurchase agreements and debt securities. The Portfolio intends to enter into financial transactions with counterparties that the Adviser believes to be creditworthy at the time of the transaction. There is always the risk that the Adviser’s analysis of a counterparty’s creditworthiness is incorrect or may change due to market conditions. To the extent that the Portfolio focuses its transactions with a limited number of counterparties, it will have greater exposure to the risks associated with one or more counterparties.

|

● |

Interest Rate Risk. An increase in interest rates may cause the value of fixed-income securities held by the Portfolio to decline. In inflationary conditions, the Portfolio may be subject to a greater risk of rising interest rates as a result of government fiscal policy initiatives and resulting market reaction to those initiatives. Variable and floating rate securities may increase or decrease in value in response to changes in interest rates, although generally to a lesser degree than fixed-income securities. |

Securities Lending Risk. There is the risk that when portfolio securities are lent, the securities may not be returned on a timely basis, and the Portfolio may experience delays and costs in recovering the security or gaining access to the collateral provided to the Portfolio to collateralize the loan. If the Portfolio is unable to recover a security on loan, the Portfolio may use the collateral to purchase replacement securities in the market. There is a risk that the value of the collateral could decrease below the cost of the replacement security by the time the replacement investment is made, resulting in a loss to the Portfolio.

Portfolio Turnover Risk. Increased portfolio turnover may result in higher costs, which may have a negative effect on the Portfolio’s performance. Due to operation of the Allocation Adjustment Program, the Portfolio may experience higher portfolio turnover as the result of equity market volatility.

Risks Through Investing in the Underlying ETFs

The ability of the Portfolio to realize its investment objective will depend, in large part, on the extent to which the underlying ETFs realize their respective investment objectives. Similarly, the Portfolio’s investment performance is directly related to the investment performance of the underlying ETFs it holds. The Portfolio is subject to the risk factors associated with the investments of the underlying ETFs, and will be affected by such risks in direct proportion to the allocation of its assets among the underlying ETFs. Therefore, to the extent that the Portfolio invests significantly in a particular underlying ETF, the Portfolio’s performance would be significantly impacted by the performance of such underlying ETF. What follows are the main risks associated with the underlying ETFs, which, in turn, may be considered to be principal risks of the Portfolio. These risks are subject to change based on the allocation of the Portfolio’s assets among the underlying ETFs.

Market Risk. The market price of investments owned by the Portfolio or an underlying ETF may go up or down. Market risk may affect a single issuer, industry, economic sector, or the market as a whole. Market risk may be magnified if certain social, political, economic and other conditions and events (such as financial institution failures, economic recessions, tariffs, trade disputes, terrorism, war, armed conflicts, including related sanctions, social unrest, natural disasters, and epidemics and pandemics) adversely interrupt the global economy and financial markets. It is important to understand that the value of your investment may fall, sometimes sharply, in response to changes in the market, and you could lose money.

Equity Securities Risk. Equity securities are subject to changes in value, and their values may be more volatile than those of other asset classes. The value of an underlying ETF’s portfolio may decrease if the value of an individual company or security, or multiple companies or securities, in the portfolio decreases. Further, regardless of how well individual companies or securities perform, the value of an underlying ETF’s portfolio could also decrease if there are deteriorating economic or market conditions or perceptions regarding the industries in which the issuers of securities the underlying ETF holds participate.

Passive Investment Risk. Certain of the underlying ETFs are not actively managed and therefore an underlying ETF might not sell shares of a security due to current or projected underperformance of a security, industry, or sector, unless that security is removed from the index or the selling of shares is otherwise required upon a rebalancing of the index the underlying ETF seeks to track. Maintaining investments in securities without attempting to take defensive positions, regardless of market conditions or the performance of individual securities, could cause an underlying ETF’s return to be lower than if it had employed an active strategy.

Fixed-Income Securities Risk. Certain of the underlying ETFs invest in a variety of fixed-income securities that are generally subject to the following risks:

18 | Protective Life Dynamic Allocation Series – Moderate Portfolio

|

● |

Interest rate risk, which is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. Changes in interest rates have unpredictable effects on the markets and may expose fixed-income and related markets to heightened volatility. |

|

● |

Credit risk, which is the risk that the credit strength of an issuer of a fixed-income security will weaken and/or that the issuer will be unable to make timely principal and interest payments and that the security may go into default. |

|

● |

Prepayment risk, which is the risk that, during periods of falling interest rates, certain fixed-income securities may be paid off quicker than originally anticipated, which may cause an underlying ETF to reinvest its assets in securities with lower yields, resulting in a decline in an underlying ETF’s income or return potential. |

|

● |

Income risk, which is the risk that an underlying ETF’s income may decline when interest rates fall, or when there is a change in an underlying ETF’s investments because (i) the fixed-income securities in the underlying ETF’s portfolio mature and it subsequently invests in lower-yielding fixed-income securities, (ii) the fixed-income securities in the ETF’s underlying index are substituted, or (iii) the underlying ETF otherwise needs to purchase additional fixed-income securities. |

|

● |