Filed with the U.S. Securities and Exchange Commission on April 30, 2026

Securities Act Registration No. 333-215588

Investment Company Act Reg. No. 811-23226

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [X] | ||||

Pre-Effective Amendment No. | [ ] | ||||

Post-Effective Amendment No. 529 | [X] | ||||

| and | |||||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [X] | ||||

Amendment No. 531 | [X] | ||||

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street, Milwaukee, Wisconsin 53202

(Address of Principal Executive Offices)

(Registrant’s Telephone Number, including Area Code): (608) 716-8890

| Kacie Briody, President | Copy to: | |||||||

| Listed Funds Trust | Laura E. Flores | |||||||

| c/o U.S. Bancorp Fund Services, LLC | Morgan, Lewis & Bockius LLP | |||||||

| 615 East Michigan Street | 1111 Pennsylvania Avenue, NW | |||||||

| Milwaukee, Wisconsin 53202 | Washington, DC 20004-2541 | |||||||

| (Name and Address of Agent for Service) | ||||||||

As soon as practical after the effective date of this Registration Statement

(Approximate Date of Proposed Public Offering)

It is proposed that this filing will become effective

| [X] | immediately upon filing pursuant to paragraph (b) | ||||

| [ ] | on pursuant to paragraph (b) | ||||

| [ ] | 60 days after filing pursuant to paragraph (a)(1) | ||||

| [ ] | on pursuant to paragraph (a)(1) | ||||

| [ ] | 75 days after filing pursuant to paragraph (a)(2) | ||||

| [ ] | on ______________ pursuant to paragraph (a)(2) of Rule 485. | ||||

If appropriate, check the following box

[ ] this post-effective amendment designates a new effective date for a previously filed post-effective amendment.

PROSPECTUS | ||

Principal U.S. Listing Exchange: NYSE Arca, Inc.

Principal U.S. Listing Exchange: Cboe BZX Exchange, Inc.

These securities have not been approved or disapproved by the U.S. Securities and Exchange Commission (the “SEC”) or the U.S. Commodity Futures Trading Commission (the “CFTC”), nor have the SEC or CFTC passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

TABLE OF CONTENTS

2

ROUNDHILL VIDEO GAMES ETF - FUND SUMMARY | ||||||||||||||

| Management Fee | |||||

| Distribution and/or Service (12b-1) Fees | |||||

| Other Expenses | |||||

| Total Annual Fund Operating Expenses | |||||

| 1 Year: | $ | 3 Years: | $ | 5 Years: | $ | 10 Years: | $ | ||||||||||||||||

The Fund is an actively managed exchange-traded fund (“ETF”) that seeks to achieve its investment objective by investing in the equity securities of Video Game Companies.

In seeking to achieve the Fund’s investment objective, the Fund’s adviser, Roundhill Financial, Inc. (the “Adviser”), will construct the portfolio pursuant to its proprietary security selection methodology. Portfolio weights are primarily determined based on each security’s market capitalization, with the Adviser employing an actively managed market capitalization adjustment process designed to limit the overweighting of any single security. Generally, companies in the Fund’s portfolio have a market capitalization of at least $500 million. From this eligible universe, the Adviser applies a proprietary, rules-based security selection methodology that evaluates companies based on factors such as liquidity, relevance to the video game industry, and overall investability characteristics. The Fund is expected to have approximately 25 to 75 issuers comprise its portfolio.

3

The Adviser generally expects to rebalance the weighting of the companies comprising the Fund’s portfolio on at least a quarterly basis. As a result, certain of the companies held by the Fund may have market capitalizations of less than $500 million in between rebalances, but must be at least $250 million at the time of rebalance.

The Fund may invest in non-U.S. securities, including the securities of companies organized in emerging and developing market countries. The Fund generally considers “emerging and developing market” countries to be those countries that have one or more of the following characteristics relative to more developed countries: (i) economies in the process of rapid growth or industrialization, (ii) lower income levels, (iii) underdeveloped but maturing infrastructures, and (iv) functioning but still developing financial systems or markets. Additionally, the Fund may purchase American Depositary Receipts (“ADRs”) or Global Depositary Receipts (“GDRs”). As of March 31, 2026, the Fund had significant exposure to companies in Japan, South Korea, Hong Kong, and China.

Principal Investment Risks

The principal risks of investing in the Fund are summarized below. The principal risks are presented in alphabetical order to facilitate finding particular risks and comparing them with the risks of other funds. Each risk summarized below is considered a “principal risk” of investing in the Fund, regardless of the order in which it appears. As with any investment, there is a risk that you could lose all or a portion of your investment in the Fund. Some or all of these risks may adversely affect the Fund’s net asset value (“NAV”), trading price, yield, total return and/or ability to meet its investment objective. The following risks could affect the value of your investment in the Fund:

•Associated Risks of Video Game Companies. Video game companies face intense competition, both domestically and internationally, may have limited product lines, markets, financial resources, or personnel, may have products that face rapid obsolescence, and are heavily dependent on the protection of patent and intellectual property rights. Such factors may adversely affect the profitability and value of video game companies. These companies also may be subject to increasing regulatory constraints, particularly with respect to cybersecurity and privacy. In addition to the costs of complying with such constraints, the unintended disclosure of confidential information, whether because of an error or a cybersecurity event, could adversely affect the reputation, profitability and value of these companies.

•Cash Transaction Risk. The Fund expects to effect certain of its creations and redemptions for cash, rather than in-kind securities. The Fund may be required to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause the Fund to recognize a capital gain that it might not have recognized if it had made a redemption in kind. As a result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was used. The use of cash creations and redemptions may also cause the Fund’s shares to trade in the market at wider bid-ask spreads or greater premiums or discounts to the Fund’s NAV. Further, effecting purchases and redemptions primarily in cash may cause the Fund to incur certain costs, such as portfolio transaction costs. These costs can decrease the Fund’s NAV if not offset by an authorized participant transaction fee.

•Concentration Risk. The Fund expects to concentrate (i.e., invest more than 25% of its net assets) in the Entertainment Industry. As a result, the Fund is more vulnerable to adverse market, economic, regulatory, political or other developments affecting the industry than a fund that invests its assets in a more diversified manner.

◦Entertainment Industry Risk. The Entertainment Industry is highly competitive and relies on consumer spending and the availability of disposable income for success. The prices of the securities of companies in the Entertainment Industry may fluctuate widely due to competitive pressures, heavy expenses incurred for research and development of products, problems related to bringing products to market, consumer preferences and rapid obsolescence of products. Legislative or regulatory changes and increased government supervision also may affect companies in the Entertainment Industry. The Entertainment Industry is a separate industry within the Communication Services Sector.

•Currency Exchange Rate Risk. The Fund may invest in investments denominated in non-U.S. currencies or in securities that provide exposure to such currencies. Changes in currency exchange rates and the relative value of non-U.S. currencies will affect the value of the Fund’s investment and the value of your Shares. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money.

•Cybersecurity Risk. Cybersecurity incidents may allow an unauthorized party to gain access to Fund assets or proprietary information, or cause the Fund, the Adviser (defined below), the Sub-Adviser and/or other service providers (including custodians and financial intermediaries) to suffer data breaches or data corruption. Additionally, cybersecurity failures or breaches of the electronic systems of the Fund, the Adviser, the Sub-Adviser or the Fund’s other service providers, market makers, Authorized Participants (“APs”), the Fund’s primary listing exchange, or the issuers of securities in which the Fund invests have the ability to disrupt and negatively affect the Fund’s business operations, including the ability to purchase and sell Shares, potentially resulting in financial losses to the Fund and its shareholders.

4

•Depositary Receipt Risk. Depositary receipts, including ADRs, EDRs and GDRs, involve risks similar to those associated with investments in foreign securities, such as changes in political or economic conditions of other countries and changes in the exchange rates of foreign currencies. Depositary receipts listed on U.S. exchanges are issued by banks or trust companies, and entitle the holder to all dividends and capital gains that are paid out on the underlying foreign shares (“Underlying Shares”). GDRs and EDRs are similar to ADRs in that they are certificates evidencing ownership of shares of a foreign issuer; however, GDRs and EDRs may be issued in bearer form and denominated in other currencies and are generally designed for use in specific or multiple securities markets outside the U.S. When the Fund invests in depositary receipts as a substitute for an investment directly in the Underlying Shares, the Fund is exposed to the risk that the depositary receipts may not provide a return that corresponds precisely with that of the Underlying Shares. Because the Underlying Shares trade on foreign exchanges that may be closed when the Fund’s primary listing exchange is open, the Fund may experience premiums and discounts greater than those of funds without exposure to such Underlying Shares.

•Emerging and Developing Markets Risk. The Fund may invest in companies organized in emerging and developing market nations. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic, or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets. Such conditions may impact the ability of the Fund to buy, sell or otherwise transfer securities, adversely affect the trading market and price for Fund shares and cause the Fund to decline in value.

•Equity Securities Risk. The equity securities held in the Fund’s portfolio may experience sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect securities markets generally or factors affecting specific issuers, industries, sectors or companies in which the Fund invests. Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value as market confidence in and perceptions of their issuers change. Preferred stocks are subject to the risk that the dividend on the stock may be changed or omitted by the issuer, and that participation in the growth of an issuer may be limited.

•ETF Risks. The Fund is an exchange-traded fund (“ETF”) and, as a result of its structure, it is exposed to the following risks:

◦Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited number of financial institutions that may act as APs. In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. Shares may trade at a material discount to NAV and possibly face delisting if either: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

◦Costs of Buying or Selling Shares Risk. Due to the costs of buying or selling Shares, including brokerage commissions imposed by brokers and bid/ask spreads, frequent trading of Shares may significantly reduce investment results and an investment in Shares may not be advisable for investors who anticipate regularly making small investments.

◦Shares May Trade at Prices Other Than NAV Risk. As with all ETFs, Shares may be bought and sold in the secondary market at market prices. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price of Shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount) due to supply and demand of Shares or during periods of market volatility. This risk is heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading activity for Shares in the secondary market, in which case such premiums or discounts may be significant. Because securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing exchange is open, the Fund is likely to experience premiums or discounts greater than those of ETFs that invest in and hold only securities and other investments that are listed and trade in the U.S.

•Foreign Securities Risk. Investments in non-U.S. securities involve certain risks that may not be present with investments in U.S. securities. These include risks of adverse changes in foreign economic, political, regulatory and other conditions, or changes in currency exchange rates or exchange control regulations (including limitations on currency movements and exchanges). The securities of some foreign companies may be less liquid and, at times, more volatile than securities of comparable U.S. companies. There may be less information publicly available about a non-U.S. issuer than a U.S. issuer. Non-U.S. issuers may be subject to different accounting, auditing, financial reporting and investor protection standards than U.S. issuers. Investments in non-U.S. securities also may be subject to withholding or other taxes and may be subject to additional trading, settlement, custodial, and operational risks. With respect to certain countries, there is the possibility of government intervention and expropriation or nationalization of assets. Because legal systems differ, there also is the possibility that it will be difficult to obtain

5

•Geographic Investment Risk. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region.

◦Risks Relating to Investing in Asia. Although many Asian economies have experienced growth and development in recent years, there is no assurance that this growth will continue. Other Asian economies, however, have been and continue to be subject, to some extent, to over-extension of credit, currency devaluations and restrictions, high unemployment, high inflation, decreased exports and economic recessions. Economic events in any one country can have a significant economic effect on the entire Asian region as well as on major trading partners outside Asia. Many Asian countries are subject to political risk, including corruption and conflict with neighboring Asian and non-Asian countries. For instance, the historical tensions between North Korea and South Korea, each of which has substantial military capabilities, present the risk of war and any outbreak of hostility between the two countries could adversely affect Asia as a whole. In addition, in recent years, certain Asian nations have developed strained relations with the United States and, if these relations worsen, they could affect international trade. In addition, many Asian countries are prone to natural disasters such as earthquakes and tsunamis, and the Fund’s investments in Asian issuers may be more likely to be affected by such events than its investments in other geographic regions. Any changes or trends in these economic, political and social factors could have a significant impact on Asian economies overall and may negatively affect the Fund’s investments. Moreover, the Fund may be more volatile than a geographically diversified equity fund.

◦Risks Related to Investing in China. The Chinese economy is generally considered an emerging market and can be significantly affected by economic and political conditions and policy in China and surrounding Asian countries. A relatively small number of Chinese companies represent a large portion of China’s total market and thus may be more sensitive to adverse political or economic circumstances and market movements. The economy of China differs, often unfavorably, from the U.S. economy in such respects as structure, general development, government involvement, wealth distribution, rate of inflation, growth rate, allocation of resources and capital reinvestment, among others. Under China’s political and economic system, the central government has historically exercised substantial control over virtually every sector of the Chinese economy through administrative regulation and/or state ownership. In addition, expropriation, including nationalization, confiscatory taxation, political, economic or social instability or other developments could adversely affect and significantly diminish the values of the Chinese companies in which the Fund invests. Additionally, from time to time, China has experienced outbreaks of infectious illnesses, including the COVID-19 pandemic, and the country may be subject to other public health threats, diseases or similar issues in the future. The Fund may invest in shares of Chinese companies traded on stock markets in Mainland China or Hong Kong. These stock markets have experienced high levels of volatility, which may continue in the future. The Hong Kong stock market may behave differently from the Mainland China stock market and there may be little to no correlation between the performance of the Hong Kong stock market and the Mainland China stock market.

◦Risks Related to Investing in Hong Kong. Investments in Hong Kong issuers will subject the Fund to legal, regulatory, political, currency, security, and economic risk specific to Hong Kong. China is Hong Kong’s largest trading partner, both in terms of exports and imports. Any changes in the Chinese economy, trade regulations or currency exchange rates, or a tightening of China’s control over Hong Kong, may have an adverse impact on Hong Kong’s economy. Additionally, Hong Kong is a small island state with few raw material resources and limited land area and is reliant on imports for its commodity needs. Any fluctuations or shortages in the commodity markets could have a negative impact on the Hong Kong economy.

◦Risks Related to Investing in Japan. The Japanese economy may be subject to considerable degrees of economic, political and social instability, which could have a negative impact on Japanese securities. Japan’s economic growth rate has remained relatively low for an extended period of time and it may remain low in the future. In addition, Japan is subject to the risk of natural disasters, such as earthquakes, volcanoes, typhoons and tsunamis. Additionally, decreasing U.S. imports, new trade regulations, changes in the U.S. dollar exchange rates, a recession in the United States or continued increases in foreclosure rates may have an adverse impact on the economy of Japan. Japan also has few natural resources, and any fluctuation or shortage in the commodity markets could have a negative impact on Japanese securities.

◦Risks of Investing in South Korea. Investments in South Korean issuers may subject the Fund to legal, regulatory, political, currency, security, and economic risks that are specific to South Korea. In addition, economic and political developments of South Korea’s neighbors may have an adverse effect on the South Korean economy.

•Illiquidity Risk. Illiquidity risk exists when particular investments are difficult to purchase or sell, possibly preventing the Fund from selling these illiquid investments at an advantageous price or at the time desired. A lack of liquidity may also cause the value of investments to decline. Illiquid investments may also be difficult to value.

6

•Management Risk. The Fund is actively managed and may not meet its investment objective based on the Adviser’s and Sub-Adviser’s success or failure to implement investment strategies for the Fund. The Sub-Adviser’s evaluations and assumptions regarding issuers, securities, and other factors may not successfully achieve the Fund’s investment objective given actual market conditions.

•Market Capitalization Risk.

◦Large-Capitalization Investing Risk. The securities of large-capitalization companies may be relatively mature compared to smaller companies and, therefore, subject to slower growth during times of economic expansion. Large-capitalization companies also may be unable to respond quickly to new competitive challenges, such as changes in technology and consumer tastes.

◦Mid-Capitalization Investing Risk. The securities of mid-capitalization companies may be more vulnerable to adverse issuer, market, political, or economic developments than securities of large-capitalization companies. The securities of mid-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than large-capitalization stocks or the stock market as a whole.

•Market Risk. The trading prices of securities and other instruments fluctuate in response to a variety of factors. These factors include events impacting the entire market or specific market segments, such as political, market and economic developments, as well as events that impact specific issuers. The Fund’s NAV and market price, like security and commodity prices generally, may fluctuate significantly in response to these and other factors. As a result, an investor could lose money over short or long periods of time. In addition, government actions or interventions (including, but not limited, to the threat or imposition of tariffs, trade restrictions, currency restrictions or similar actions) as well as developments related to economic, political (including geopolitical), social, public health, market, extreme weather, natural or man-made disasters, or other conditions or events have in the past and may in the future result in volatility in financial markets and reduced liquidity in equity, credit, and/or debt markets, which could adversely impact the Fund and its investments and their value and performance. These developments as well as other events could result in further market volatility and negatively affect financial asset prices, the liquidity of certain securities and the normal operations of securities exchanges and other markets.

•Non-Diversification Risk. Because the Fund is “non-diversified,” it may invest a greater percentage of its assets in the securities of a single issuer or a lesser number of issuers than if it was a diversified fund. As a result, a decline in the value of an investment in a single issuer or a lesser number of issuers could cause the Fund’s overall value to decline to a greater degree than if the Fund held a more diversified portfolio. This may increase the Fund’s volatility and have a greater impact on the Fund’s performance.

•Sector Risk. To the extent the Fund invests more heavily in particular sectors of the economy, its performance will be especially sensitive to developments that significantly affect those sectors. The Fund may invest a significant portion of its assets in the following sector and, therefore, the performance of the Fund could be negatively impacted by events affecting this sector.

•Securities Lending Risk. To the extent the Fund engages in securities lending, there are certain risks associated with securities lending, including the risk that the borrower may fail to return the securities on a timely basis or even the loss of rights in the collateral deposited by the borrower, if the borrower should fail financially. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. As a result, the Fund may lose money.

7

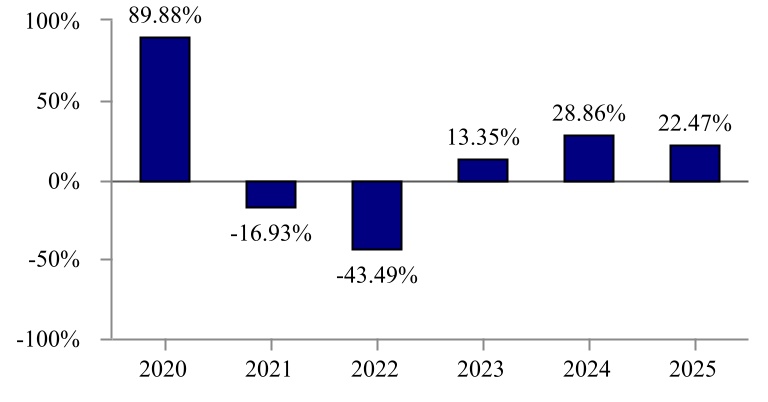

Average Annual Total Returns

(for periods ended December 31, 2025)

Roundhill Video Games ETF | 1 Year | 5 Years | Since Inception ( | ||||||||

| - | |||||||||||

| - | |||||||||||

| - | |||||||||||

Solactive GBS Global Markets All Cap USD Index TR (reflects no deduction for fees, expenses, or taxes) | |||||||||||

Roundhill Video Games Blended Index* | - | ||||||||||

*The Roundhill Video Games Blended Index represents the linked performance of two different performance benchmarks – for periods prior to September 26, 2022, the Roundhill BITKRAFT Esports Index and for periods thereafter, the Nasdaq CTA Global Video Games Software IndexTM, the Fund’s index until September 30, 2025.

8

Portfolio Management

| Adviser | Roundhill Financial Inc. (the “Adviser”) | ||||

| Sub-Adviser | Exchange Traded Concepts, LLC | ||||

| Portfolio Managers | William Hershey, Timothy Maloney and David Mazza, each a portfolio manager for the Adviser, have been portfolio managers of the Fund since March 2025. Andrew Serowik, Todd Alberico, Gabriel Tan, and Brian Cooper are each portfolio managers for the Sub-Adviser. Mr. Serowik has been a portfolio manager of the Fund since its inception in June 2019, Mr. Alberico and Mr. Tan have been portfolio managers of the Fund since July 2021, and Mr. Cooper has been a portfolio manager for the Fund since November 2021. | ||||

Purchase and Sale of Shares

The Fund issues and redeems Shares at NAV only in large blocks known as “Creation Units,” which only APs (typically, broker-dealers) may purchase or redeem. The Fund generally issues and redeems Creation Units in exchange for a portfolio of securities and/or a designated amount of U.S. cash.

Shares are listed on the Exchange, and individual Shares may only be bought and sold in the secondary market through a broker or dealer at market prices, rather than NAV. Because Shares trade at market prices rather than NAV, Shares may trade at a price greater than NAV (premium) or less than NAV (discount).

An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares (the “bid” price) and the lowest price a seller is willing to accept for Shares (the “ask” price) when buying or selling Shares in the secondary market. The difference in the bid and ask prices is referred to as the “bid-ask spread.”

Recent information regarding the Fund’s NAV, market price, how often Shares traded on the Exchange at a premium or discount, and bid-ask spreads can be found on the Fund’s website at www.roundhillinvestments.com/etf/NERD.

Tax Information

The Fund’s distributions are generally taxable as ordinary income, qualified dividend income, or capital gains (or a combination), unless your investment is held in an IRA or other tax-advantaged account. Distributions on investments made through tax-deferred arrangements may be taxed later upon withdrawal of assets from those accounts.

Financial Intermediary Compensation

If you purchase Shares through a broker-dealer or other financial intermediary (such as a bank) (an “Intermediary”), the Adviser or its affiliates may pay Intermediaries for certain activities related to the Fund, including participation in activities that are designed to make Intermediaries more knowledgeable about exchange-traded products, including the Fund, or for other activities, such as marketing, educational training or other initiatives related to the sale or promotion of Shares. These payments may create a conflict of interest by influencing the Intermediary and your salesperson to recommend the Fund over another investment. Any such arrangements do not result in increased Fund expenses. Ask your salesperson or visit the Intermediary’s website for more information.

9

ROUNDHILL SPORTS BETTING & IGAMING ETF – FUND SUMMARY | ||

| Management Fee | |||||

| Distribution and/or Service (12b-1) Fees | |||||

| Other Expenses | |||||

| Total Annual Fund Operating Expenses | |||||

| 1 Year: | $ | 3 Years: | $ | 5 Years: | $ | 10 Years: | $ | ||||||||||||||||

The Fund seeks to track the total return performance, before fees and expenses, of the Index.

Morningstar® Sports Betting & iGaming Select Index

The Index was developed by Morningstar, Inc. (the “Index Provider”) and is designed to provide pure exposure to sports and online betting themes. In order to achieve such exposure, the Index is comprised of common stock (or corresponding American Depositary Receipts (“ADRs”) or Global Depositary Receipts (“GDRs”)) of domestic and foreign sports and online betting (a/k/a iGaming) companies. The Index Provider defines sports betting and iGaming companies as follows (although the definitions may change over time):

◦Sports Betting Companies – companies engaged, directly or indirectly, in analyzing sports events and wagering on the outcome, such as online bookmaking.

◦iGaming Companies – companies engaged, directly or indirectly, in betting online in games of chance, such as poker, slots, blackjack, or the lottery.

The composition of the Index is based on the following rules:

Stocks included in the Index must (i) receive a score 1 or higher from the Index Provider on either a Sports Betting or iGaming theme, (ii) have a free-float market capitalization of at least $100 million (USD), and (iii) have a minimum three-month average daily traded value of $250,000 (USD). The Index Provider will assign a score of 1 or higher to a company that the Index Provider has determined (a) is a producer of related goods or services or a supplier of those producers, and (b) is highly likely to enjoy a material net profit increase from its exposure to such Sports Betting or iGaming theme over the next five years. The Index Provider estimates the percent revenue a company will derive from its exposure to each theme at a point in time five years forward, which translates to the following scores: 0 = less than 10% revenue; 1 = 10% - 25% of revenue for a producer or supplier; 2 = 25% - 50% of revenue for a producer or

10

supplier; 3 = greater than 50% of revenue for a supplier; 4 = greater than 50% revenue for a producer. Scores are reviewed by the Index Provider’s steering committee for quality control and to ensure consistency.

Index components are weighted in proportion to both their combined theme score and their free-float market capitalization, subject to capping constraints. Companies with higher combined theme scores are allocated a greater weight in the Index. Index components are capped to ensure that no Index component has a weight greater than 10% and the sum of components with weights greater than or equal to 5% cannot exceed 40%.

The Index is reconstituted and rebalanced annually on the Monday following the third Friday in December. The number of stocks included in the Index may vary and is subject to the selection and eligibility criteria at the time of reconstitution. As of March 31, 2026, the Index had 28 components.

The Fund’s Investment Strategy

The Fund will generally invest all, or substantially all, of its assets in the component securities of the Index, but also may invest in investments that provide comparable exposure, including but not limited to depositary receipts representing Index components and investments in other exchange-traded funds (“ETFs”). Under normal circumstances, at least 80% of the Fund’s net assets (plus borrowings for investment purposes) will be invested in securities issued by Sports Betting and iGaming Companies. Sports Betting and iGaming Companies are companies that the Index Provider determines provide exposure to the sports and online betting and iGaming themes and which satisfy the Index Provider’s Index security selection criteria, as such criteria may be modified from time to time. Sports Betting Companies generally are engaged, directly or indirectly, in analyzing sports events and wagering on the outcome. Sports Betting Companies may include companies engaged in: online bookmaking; media production connected to sports betting activities, such as the producers of podcasts, videos and blogs; developing and/or providing technology solutions and services for other Sports Betting Companies; providing marketing solutions and services for other Sports Betting Companies; and investing in Sports Betting Companies, such as owners of investment portfolios comprising companies exposed to sports betting activities or the underlying assets of such companies. Generally, iGaming Companies are engaged, directly or indirectly, in betting online in games of chance, such as poker, slots, blackjack, or the lottery. iGaming Companies may include companies engaged in: online bookmaking; media production connected to sports betting activities, such as the producers of podcasts, videos and blogs; developing and/or providing technology solutions and services for other iGaming Companies; providing marketing solutions and services for other iGaming Companies; investing in iGaming Companies, such as owners of investment portfolios comprising companies exposed to iGaming activities or the underlying assets of such companies; and developing and/or providing games, such as casino developers and bingo and lottery game developers.

The Fund will generally use a “replication” strategy to achieve its investment objective, meaning the Fund generally will invest in all of the component securities of the Index in approximately the same proportions as in the Index. However, the Fund may use a “representative sampling” strategy, meaning it may invest in a sample of the securities in the Index whose risk, return, and other characteristics closely resemble the risk, return, and other characteristics of the Index as a whole, when Exchange Traded Concepts, LLC (the “Sub-Adviser”), the Fund’s sub-adviser, believes it is in the best interests of the Fund (e.g., when replicating the Index involves practical difficulties or substantial costs, an Index component becomes temporarily illiquid, unavailable, or less liquid, or as a result of legal restrictions or limitations that apply to the Fund but not to the Index).

The Fund also may invest in securities or other investments not included in the Index, but which the Sub-Adviser believes will help the Fund track the Index. For example, the Fund may invest in securities that are not components of the Index to reflect various corporate actions and other changes to the Index (such as reconstitutions, additions, and deletions).

Principal Investment Risks

The principal risks of investing in the Fund are summarized below. The principal risks are presented in alphabetical order to facilitate finding particular risks and comparing them with the risks of other funds. Each risk summarized below is considered a “principal risk” of investing in the Fund, regardless of the order in which it appears. As with any investment, there is a risk that you could lose all or a portion of your investment in the Fund. Some or all of these risks may adversely affect the Fund’s net asset value (“NAV”), trading price, yield, total return and/or ability to meet its investment objective. The following risks could affect the value of your investment in the Fund:

•Associated Risks of iGaming and Sports Betting Companies. The iGaming and sports betting industry is characterized by an increasingly high degree of competition among a large number of participants including from participants performing illegal activities or unregulated companies. Expansion of iGaming and sports betting in other jurisdictions (both regulated and unregulated) could increase competition with traditional betting companies, which could have an adverse impact on their financial

11

•Concentration Risk. Because the Fund’s assets will be concentrated in an industry or group of industries to the extent the Index concentrates in a particular industry or group of industries, the Fund is subject to loss due to adverse occurrences that may affect that industry or group of industries.

•Currency Exchange Rate Risk. The Fund may invest in investments denominated in non-U.S. currencies or in securities that provide exposure to such currencies. Changes in currency exchange rates and the relative value of non-U.S. currencies will affect the value of the Fund’s investment and the value of your Shares. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money.

•Cybersecurity Risk. Cybersecurity incidents may allow an unauthorized party to gain access to Fund assets or proprietary information, or cause the Fund, the Adviser (defined below), the Sub-Adviser and/or other service providers (including custodians and financial intermediaries) to suffer data breaches or data corruption. Additionally, cybersecurity failures or breaches of the electronic systems of the Fund, the Adviser, the Sub-Adviser or the Fund’s other service providers, market makers, Authorized Participants (“APs”), the Fund’s primary listing exchange, or the issuers of securities in which the Fund invests have the ability to disrupt and negatively affect the Fund’s business operations, including the ability to purchase and sell Shares, potentially resulting in financial losses to the Fund and its shareholders.

•Depositary Receipt Risk. Depositary receipts, including ADRs and GDRs, involve risks similar to those associated with investments in foreign securities, such as changes in political or economic conditions of other countries and changes in the exchange rates of foreign currencies. Depositary receipts listed on U.S. exchanges are issued by banks or trust companies, and entitle the holder to all dividends and capital gains that are paid out on the underlying foreign shares (“Underlying Shares”). GDRs are similar to ADRs in that they are certificates evidencing ownership of shares of a foreign issuer; however, GDRs may be issued in bearer form and denominated in other currencies and are generally designed for use in specific or multiple securities markets outside the U.S. When the Fund invests in depositary receipts as a substitute for an investment directly in the Underlying Shares, the Fund is exposed to the risk that the depositary receipts may not provide a return that corresponds precisely with that of the Underlying Shares.

•Equity Securities Risk. The equity securities held in the Fund’s portfolio may experience sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect securities markets generally or factors affecting specific issuers, industries, sectors or companies in which the Fund invests. Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value as market confidence in and perceptions of their issuers change. Preferred stocks are subject to the risk that the dividend on the stock may be changed or omitted by the issuer, and that participation in the growth of an issuer may be limited.

•ETF Risks. The Fund is an ETF and, as a result of its structure, it is exposed to the following risks:

◦Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited number of financial institutions that may act as APs. In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. Shares may trade at a material discount to NAV and possibly face delisting if either: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

12

◦Costs of Buying or Selling Shares Risk. Due to the costs of buying or selling Shares, including brokerage commissions imposed by brokers and bid/ask spreads, frequent trading of Shares may significantly reduce investment results and an investment in Shares may not be advisable for investors who anticipate regularly making small investments.

◦Shares May Trade at Prices Other Than NAV Risk. As with all ETFs, Shares may be bought and sold in the secondary market at market prices. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price of Shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount) due to supply and demand of Shares or during periods of market volatility. This risk is heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading activity for Shares in the secondary market, in which case such premiums or discounts may be significant. Because securities held by the Fund may trade on foreign exchanges that are closed when the Fund’s primary listing exchange is open, the Fund is likely to experience premiums or discounts greater than those of ETFs that invest in and hold only securities and other investments that are listed and trade in the U.S.

•Foreign Securities Risk. Investments in non-U.S. securities involve certain risks that may not be present with investments in U.S. securities. These include risks of adverse changes in foreign economic, political, regulatory and other conditions, or changes in currency exchange rates or exchange control regulations (including limitations on currency movements and exchanges). The securities of some foreign companies may be less liquid and, at times, more volatile than securities of comparable U.S. companies. There may be less information publicly available about a non-U.S. issuer than a U.S. issuer. Non-U.S. issuers may be subject to different accounting, auditing, financial reporting and investor protection standards than U.S. issuers. Investments in non-U.S. securities also may be subject to withholding or other taxes and may be subject to additional trading, settlement, custodial, and operational risks. With respect to certain countries, there is the possibility of government intervention and expropriation or nationalization of assets. Because legal systems differ, there also is the possibility that it will be difficult to obtain or enforce legal judgments in certain countries. Since foreign exchanges may be open on days when the Fund does not price its shares, the value of the securities in the Fund’s portfolio may change on days when shareholders will not be able to purchase or sell the Fund’s shares. Conversely, Shares may trade on days when foreign exchanges are closed. Each of these factors can make investments in the Fund more volatile and potentially less liquid than other types of investments.

•Geographic Investment Risk. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region.

•Illiquidity Risk. Illiquidity risk exists when particular investments are difficult to purchase or sell, possibly preventing the Fund from selling these illiquid investments at an advantageous price or at the time desired. A lack of liquidity may also cause the value of investments to decline. Illiquid investments may also be difficult to value.

•Index Provider Risk. There is no assurance that the Index Provider, or any agents that act on its behalf, will compile the Index accurately, or that the Index will be determined, constructed, reconstituted, rebalanced, composed, calculated or disseminated accurately. The Adviser relies upon the Index Provider and its agents to compile, determine, construct, reconstitute, rebalance, compose, calculate (or arrange for an agent to calculate), and disseminate the Index accurately. Any losses or costs associated with errors made by the Index Provider or its agents generally will be borne by the Fund and its shareholders.

•Market Capitalization Risk.

◦Large-Capitalization Investing Risk. The securities of large-capitalization companies may be relatively mature compared to smaller companies and, therefore, subject to slower growth during times of economic expansion. Large-capitalization companies also may be unable to respond quickly to new competitive challenges, such as changes in technology and consumer tastes.

◦Mid-Capitalization Investing Risk. The securities of mid-capitalization companies may be more vulnerable to adverse issuer, market, political, or economic developments than securities of large-capitalization companies. The securities of mid-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than large-capitalization stocks or the stock market as a whole.

13

•Market Risk. The trading prices of securities and other instruments fluctuate in response to a variety of factors. These factors include events impacting the entire market or specific market segments, such as political, market and economic developments, as well as events that impact specific issuers. The Fund’s NAV and market price, like security and commodity prices generally, may fluctuate significantly in response to these and other factors. As a result, an investor could lose money over short or long periods of time. In addition, government actions or interventions (including, but not limited, to the threat or imposition of tariffs, trade restrictions, currency restrictions or similar actions) as well as developments related to economic, political (including geopolitical), social, public health, market, extreme weather, natural or man-made disasters, or other conditions or events have in the past and may in the future result in volatility in financial markets and reduced liquidity in equity, credit, and/or debt markets, which could adversely impact the Fund and its investments and their value and performance. These developments as well as other events could result in further market volatility and negatively affect financial asset prices, the liquidity of certain securities and the normal operations of securities exchanges and other markets.

•Non-Diversification Risk. Because the Fund is “non-diversified,” it may invest a greater percentage of its assets in the securities of a single issuer or a lesser number of issuers than if it was a diversified fund. As a result, the Fund may be more exposed to the risks associated with and developments affecting an individual issuer or a lesser number of issuers than a fund that invests more widely. This may increase the Fund’s volatility and cause the performance of a relatively small number of issuers to have a greater impact on the Fund’s performance.

•Passive Investment Risk. The Fund is not actively managed and its Sub-Adviser would not sell an investment designed to provide exposure to the Index or a constituent holding of the Index due to current or projected underperformance of a security industry or sector unless that security is removed from the Index or the selling of shares of that security is otherwise required upon a rebalancing of the Index as addressed in the Index methodology.

•Sector Risk. To the extent the Fund invests more heavily in particular sectors of the economy, its performance will be especially sensitive to developments that significantly affect those sectors. The Fund may invest a significant portion of its assets in the following sectors and, therefore, the performance of the Fund could be negatively impacted by events affecting each of these sectors.

•Securities Lending Risk. To the extent the Fund engages in securities lending, there are certain risks associated with securities lending, including the risk that the borrower may fail to return the securities on a timely basis or even the loss of rights in the collateral deposited by the borrower, if the borrower should fail financially. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. As a result, the Fund may lose money.

•Tracking Error Risk. As with all index funds, the performance of the Fund and its Index may differ from each other for a variety of reasons. For example, the Fund incurs operating expenses and portfolio transaction costs not incurred by the Index. In addition, the Fund may not be fully invested in the securities of the Index at all times or may hold securities not included in the Index.

14

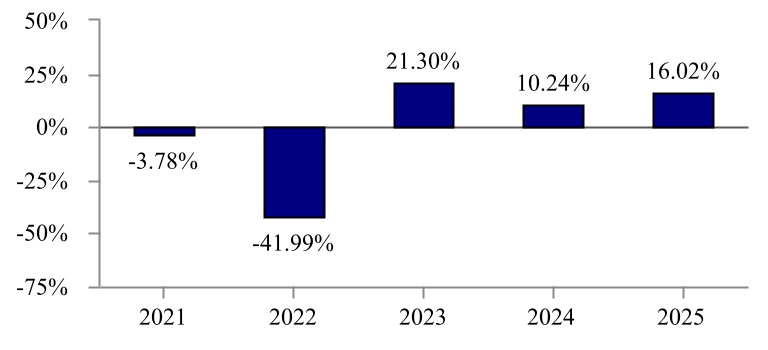

Average Annual Total Returns

(for periods ended December 31, 2025)

Roundhill Sports Betting & iGaming ETF | 1 Year | 5 Years | Since Inception ( | ||||||||

| - | |||||||||||

| - | |||||||||||

| - | |||||||||||

Solactive GBS Global Markets All Cap USD Index TR (reflects no deduction for fees, expenses, or taxes) | |||||||||||

Roundhill Sports Betting & iGaming Blended Index* | - | ||||||||||

*The Roundhill Sports Betting & iGaming Blended Index represents the linked performance of two different performance benchmarks – for periods prior to October 2, 2023, the Roundhill Sports Betting & iGaming Index, the Fund’s prior index, and for periods thereafter, the Morningstar® Sports Betting & iGaming Select Index, the Fund’s current index.

Portfolio Management

| Adviser | Roundhill Financial Inc. (the “Adviser”) | ||||

| Sub-Adviser | Exchange Traded Concepts, LLC | ||||

| Portfolio Managers | William Hershey, Timothy Maloney and David Mazza, each a portfolio manager for the Adviser, have been portfolio managers of the Fund since March 2025. Andrew Serowik, Todd Alberico, Gabriel Tan, and Brian Cooper are each portfolio managers for the Sub-Adviser. Mr. Serowik has been a portfolio manager of the Fund since its inception in June 2020, Mr. Alberico and Mr. Tan have been portfolio managers of the Fund since July 2021, and Mr. Cooper has been a portfolio manager for the Fund since November 2021. | ||||

Purchase and Sale of Shares

The Fund issues and redeems Shares at NAV only in large blocks known as “Creation Units,” which only APs (typically, broker-dealers) may purchase or redeem. The Fund generally issues and redeems Creation Units in exchange for a portfolio of securities and/or a designated amount of U.S. cash.

Shares are listed on the Exchange, and individual Shares may only be bought and sold in the secondary market through a broker or dealer at market prices, rather than NAV. Because Shares trade at market prices rather than NAV, Shares may trade at a price greater than NAV (premium) or less than NAV (discount).

15

An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares (the “bid” price) and the lowest price a seller is willing to accept for Shares (the “ask” price) when buying or selling Shares in the secondary market. The difference in the bid and ask prices is referred to as the “bid-ask spread.”

Recent information regarding the Fund’s NAV, market price, how often Shares traded on the Exchange at a premium or discount, and bid-ask spreads can be found on the Fund’s website at www.roundhillinvestments.com/etf/BETZ.

Tax Information

The Fund’s distributions are generally taxable as ordinary income, qualified dividend income, or capital gains (or a combination), unless your investment is held in an IRA or other tax-advantaged account. Distributions on investments made through tax-deferred arrangements may be taxed later upon withdrawal of assets from those accounts.

Financial Intermediary Compensation

If you purchase Shares through a broker-dealer or other financial intermediary (such as a bank) (an “Intermediary”), the Adviser or its affiliates may pay Intermediaries for certain activities related to the Fund, including participation in activities that are designed to make Intermediaries more knowledgeable about exchange-traded products, including the Fund, or for other activities, such as marketing, educational training or other initiatives related to the sale or promotion of Shares. These payments may create a conflict of interest by influencing the Intermediary and your salesperson to recommend the Fund over another investment. Any such arrangements do not result in increased Fund expenses. Ask your salesperson or visit the Intermediary’s website for more information.

16

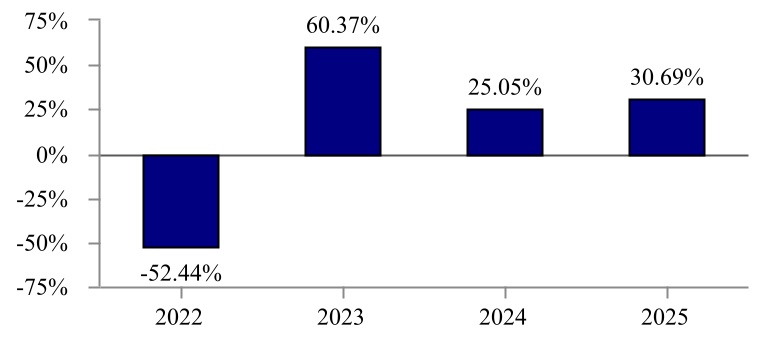

ROUNDHILL BALL METAVERSE ETF – FUND SUMMARY | ||

| Management Fee | |||||

| Distribution and/or Service (12b-1) Fees | |||||

| Other Expenses | |||||

Total Annual Fund Operating Expenses(1) | |||||

(1)The Total Annual Fund Operating Expenses do not correlate to the expense ratio in the Fund’s Financial Highlights and financial statements because the Financial Highlights and financial statements reflect the Fund’s receipt of a rebate on certain of its investments that had the effect of reducing the Fund’s Total Annual Fund Operating Expenses to 0.58%. There is no guarantee that such rebate will be paid to the Fund in the future. The Adviser and the sponsor of certain of the funds in which the Fund invests have established an arrangement whereby the Fund is eligible to receive fee rebates equivalent to a portion of the fees paid on its investments in those funds. In accordance with this arrangement, for the fiscal year ended December 31, 2025, the Fund received a rebate amounting to 0.01% of the Fund’s net assets.

| 1 Year: | $ | 3 Years: | $ | 5 Years: | $ | 10 Years: | $ | ||||||||||||||||

The Fund seeks to track the performance, before fees and expenses, of the Index. The Index seeks to track the performance of equity securities of foreign and domestic issuers that engage in activities or provide products, services, technologies, or technological capabilities to enable the Metaverse, and benefit from its generated revenues (“Metaverse Companies”). “Metaverse” is a term used to refer to a future iteration of the Internet. Users will primarily engage with the Metaverse through persistent, simultaneous, and shared three-dimensional virtual simulations and spaces. The Metaverse will also connect to physical spaces, two-dimensional Internet experiences (e.g., standard apps, webpages), and finite simulations (e.g., a game). The Metaverse will be supported by a wide range of technologies, tools, and standards that enable high volumes of concurrent users, a rich virtual-only economy of labor, goods, and services, and wide ranging interoperability of data, digital assets, and content. The Index was developed and is owned by Ball Metaverse Research Partners LLC (the “Index Provider”).

Ball Metaverse Index

To be eligible for inclusion in the Index, issuers generally must have a market capitalization or assets under management (“AUM”), as appropriate, of at least $250 million USD (and thereafter maintain a market capitalization or AUM of $200 million USD) and average daily trading volume (“ADV”) of at least $2 million over a trailing 6-month period (or if unavailable, since the issuer’s listing date). Such issuers include foreign exchange-traded funds, and, in the future, may include domestic exchange-traded products, that primarily hold cryptocurrencies (each, a “Cryptocurrency ETF”) to the extent consistent with U.S. federal securities laws and related guidance

17

applicable to the Fund. In addition, Cryptocurrency ETFs may invest in bitcoin, ether, tokens related to the Solana Network (“SOL”), XRP, and any other cryptocurrency eligible to be held by U.S. registered investment companies, and seek to generate income and capital appreciation through staking the underlying cryptocurrency. Cryptocurrency ETFs eligible for inclusion in the Index include both investment companies registered under the Investment Company Act of 1940 (“1940 Act”) and exchange-traded products that are not registered under the 1940 Act. Exchange-traded products that are not registered under the 1940 Act do not afford investors, including the Fund, the investor protections available under the 1940 Act. The Index Provider may determine, in its discretion, to retain a Cryptocurrency ETF in the Index should its AUM and/or ADV decline below the referenced thresholds. A committee comprised of representatives from Ball Metaverse Research Partners LLC and external subject matter experts (the “Index Committee”) analyzes issuers for their current and future potential to experience profits or earn revenue from their activities or provision of products, services, technologies, or technological capabilities to enable the Metaverse, and benefit from its generated revenues. The Metaverse Companies selected for inclusion in the Index are engaged in activities that fall into one or more of the categories described below. The categories, which may change over time as technology and consumer behavior evolve, are determined by the Index Committee through its analyses of a variety of information, including information derived from corporate announcements and filings, patent filings, third-party industry assessments, third-party usage data and metrics, scientific and technology updates, executive presentations, and consumer interviews. Currently, the seven categories and their descriptions are as follows:

•Hardware – The sale and support of physical technologies and devices used to access, interact with or develop the Metaverse. This includes, but is not limited to, consumer-facing hardware, such as virtual reality headsets, mobile phones, and haptic gloves, as well as enterprise hardware such as those used to operate or create virtual or augmented reality-based environments, such as industrial cameras, projection and tracking systems, and scanning sensors. This category does not include compute-specific hardware, such as graphic processing unit chips and servers, or networking-specific hardware, such as fiber optic cabling or wireless chipsets.

•Compute – The enablement and supply of computing power to support the Metaverse, supporting such diverse and demanding functions as physics calculation, rendering, data reconciliation and synchronization, artificial intelligence, projection, motion capture and translation. This category may include blockchain-based technologies for the management of marketplaces and networks for decentralized computing capacity.

•Networking – The provision of persistent, real-time connections, high bandwidth, and decentralized data transmission by backbone providers (i.e., companies that provide access to high-speed data transmission networks), the networks, exchange centers, and services that route amongst them, as well as those managing “last mile” (i.e., the function of connecting telecommunication services directly to end-users, both businesses and residential customers, usually in a dense area) data to consumers.

•Virtual Platforms – The development and operation of immersive digital and often three-dimensional simulations, environments and worlds wherein users and businesses can explore, create, socialize and participate in a wide variety of experiences (e.g., race a car, paint a painting, attend a class, listen to music), and engage in economic activity. These businesses are differentiated from traditional online experiences and multiplayer video games by the existence of a large ecosystem of developers and content creators which generate the majority of content on and/or collect the majority of revenues built on top of the underlying platform.

•Interchange Standards – The tools, protocols, formats, services, and engines which serve as actual or de facto standards for interoperability, and enable the creation, operation and ongoing improvements to the Metaverse. These standards support activities such as rendering, physics and artificial intelligence, as well as asset formats and their import/export from experience to experience, forward compatibility management and updating, tooling and authoring activities, and information management.

•Payments – The support of digital payment processes, platforms, and operations, which includes cryptocurrencies, the companies that are fiat on-ramps to those cryptocurrencies, companies that provide or service the infrastructure and technologies to “mint” cryptocurrencies, and companies that provide the financial services necessary to trade and manage cryptocurrencies, as well as issuers of financial products that provide a means of obtaining exposure to cryptocurrencies.

•Content, Assets and Identity Services – The design/creation, sale, re-sale, storage, secure protection and financial management of digital assets, such as virtual goods, as connected to user data and identity. This contains all business and services “built on top of” and/or which “service” the Metaverse, but which are not vertically integrated into a virtual platform by the platform owner, including content which is built specifically for the Metaverse. This category may include blockchain-based technologies for the decentralized creation and trading of digital assets.

Once identified and allocated to one or more categories, Metaverse Companies are further ranked within the categories as follows:

•“Pure-Play” Companies – Issuers whose primary business models and/or growth prospects are directly linked to the Metaverse. For these issuers, continued growth in the Metaverse is expected to be critical to their economic success going forward.

18

•“Core” Companies – Issuers with substantial operations and/or growth prospects linked to the Metaverse. These issuers have other business units driving their economics, and thus are less affected by the growth of Metaverse than “pure-play” companies. In time, growth in the industry and/or investments in their Metaverse-specific units may lead these issuers to become “pure-play” companies if their Metaverse operations become a primary driver of economic performance. In most cases, the Metaverse-specific offerings of these issuers are core components of the Metaverse.

•“Non-Core” Companies – Issuers with operations and/or growth prospects linked to the Metaverse. These issuers derive the majority of their revenue from business lines not directly related to the Metaverse. In time, growth in the industry and/or investments in their Metaverse-specific units may lead these issuers to become “core” companies if their Metaverse operations become a relevant driver of economic performance. It is unlikely, based on current information, that the Metaverse-specific offerings of “non-core” companies would become the primary driver of such economic performance going forward.

Metaverse Companies are weighted on a tiered basis whereby “pure-play” companies receive two and a half times the initial weighting of “core” companies and five times the initial weighting of “non-core” companies, while “core” companies” receive two times the initial weighting of “non-core” companies. These initial weights are calculated based on the number of issuers in each category in the Index upon rebalancing to ensure the aggregate combined weight of each category equals 100%.

A category may have any number of “pure-play,” “core” or “non-core” companies, or none. In the event no issuers are identified for a particular category, the weight for that category will be allocated across the other categories on a pro rata basis. The weight of any category is capped at 25% of the total Index weight upon rebalance.

The weight of any issuer in the Index is capped at 8%. Any issuer weight in excess of 8% will be pro-rated across the remaining Index components, subject to the 25% category cap.

Index component changes resulting from reconstitutions are made after the market close on the third Friday in March, June, September and December and become effective at the market opening on the next trading day. Depending on the number of issuers that qualify as Metaverse Companies, the number of Index components, and therefore the anticipated number of Fund holdings, may range from 25 to 100.

The Fund’s Investment Strategy

Under normal circumstances, at least 80% of the Fund’s net assets (plus any borrowings for investment purposes) will be invested in Metaverse Companies, which may include investments in American Depository Receipts (“ADRs”). For purposes of this policy, the Fund defines Metaverse Companies as foreign and domestic issuers that engage in activities or provide products, services, technologies, or technological capabilities to enable the Metaverse, and benefit from its generated revenues. Like the Index, the Fund may have indirect exposure to cryptocurrencies, such as bitcoin and ether, through investments in one or more Cryptocurrency ETFs, as well as through publicly traded securities of companies engaged in cryptocurrency-related businesses and activities. The Fund will not invest directly in cryptocurrencies.

The Fund will generally use a “replication” strategy to achieve its investment objective, meaning it generally will invest in all of the component securities of the Index in approximately the same proportions as in the Index. However, the Fund may use a “representative sampling” strategy, meaning it may invest in a sample of the securities in the Index whose risk, return and other characteristics closely resemble the risk, return and other characteristics of the Index as a whole, when Exchange Traded Concepts, LLC (the “Sub-Adviser”), the Fund’s sub-adviser, believes it is in the best interests of the Fund (e.g., when replicating the Index involves practical difficulties or substantial costs, an Index constituent becomes temporarily illiquid, unavailable, or less liquid, or as a result of legal restrictions or limitations that apply to the Fund but not to the Index).

The Fund also may invest in securities or other investments not included in the Index, but which the Sub-Adviser believes will help the Fund track the Index. For example, the Fund may invest in securities that are not components of the Index to reflect various corporate actions and other changes to the Index (such as reconstitutions, additions, and deletions).

Principal Investment Risks

The principal risks of investing in the Fund are summarized below. The principal risks are presented in alphabetical order to facilitate finding particular risks and comparing them with the risks of other funds. Each risk summarized below is considered a “principal risk” of investing in the Fund, regardless of the order in which it appears. As with any investment, there is a risk that you could lose all or a portion of your investment in the Fund. Some or all of these risks may adversely affect the Fund’s net asset value (“NAV”), trading

19

price, yield, total return and/or ability to meet its investment objective. The following risks could affect the value of your investment in the Fund:

•Bitcoin Risk. Bitcoin is a relatively new innovation and the market for bitcoin is subject to rapid price swings, changes and uncertainty. The value of bitcoin has been and may continue to be substantially dependent on speculation. The further development of the Bitcoin Network and the acceptance and use of bitcoin are subject to a variety of factors that are difficult to evaluate. The slowing, stopping or reversing of the development of the Bitcoin Network or the acceptance of bitcoin may adversely affect the price of bitcoin. Bitcoin is subject to the risk of fraud, theft, manipulation or security failures, operational or other problems that impact bitcoin trading venues. Additionally, if one or a coordinated group of miners were to gain control of 51% of the Bitcoin Network, they would have the ability to manipulate transactions, halt payments and fraudulently obtain bitcoin. A significant portion of bitcoin is held by a small number of holders sometimes referred to as “whales.” These holders have the ability to manipulate the price of bitcoin. Unlike the exchanges for more traditional assets, such as equity securities and futures contracts, bitcoin and bitcoin trading venues are largely unregulated. As a result of the lack of regulation, individuals or groups may engage in fraud or market manipulation (including using social media to promote bitcoin in a way that artificially increases the price of bitcoin). Investors may be more exposed to the risk of theft, fraud and market manipulation than when investing in more traditional asset classes. Over the past several years, a number of bitcoin trading venues have been closed due to fraud, failure or security breaches. Investors in bitcoin may have little or no recourse should such theft, fraud or manipulation occur and could suffer significant losses. Legal or regulatory changes may negatively impact the operation of the Bitcoin Network. The realization of any of these risks could result in a decline in the acceptance of bitcoin and consequently a reduction in the value of bitcoin, bitcoin futures, and the Fund. In addition, bitcoin is a bearer asset that can be irrevocably lost or stolen to the extent that private keys are lost or stolen.

The slowness of transaction processing and finality, the variability of transaction fees, and volatility of bitcoin’s price could disadvantage or impede the adoption of the Bitcoin Blockchain as a payment network. The further development and use of the Bitcoin Blockchain for its intended purpose and other allowable applications are, and may continue to be, substantially dependent upon “Layer-2” solutions operating on top of the Bitcoin Blockchain, such as the Lightning Network, which is intended to expand the scale and speed of payments across the underlying Bitcoin Blockchain through the use of channels and payment networks outside of the Bitcoin Blockchain. To the extent these Layer-2 solutions have not been developed or have not been fully developed in a way that is adequate to improve scalability, transactions speed or efficiency, the use and/or value of the Bitcoin Blockchain may be limited, which could adversely affect the Fund. Further, the industry is actively researching, investing in and in some cases creating alternative blockchains that are able to support more advanced applications, such as the Ethereum Blockchain. The emergence of other public blockchains and related technologies may compete with bitcoin and result in a reduction in the use of bitcoin, which could reduce its value or increase the volatility of the price of bitcoin due to changes in the supply and demand of bitcoin relative to alternatives, thus negatively impacting investment in the Fund. The Bitcoin Blockchain may also be vulnerable to attacks to the extent a miner or group of miners possess more than 50% of its hashing power and the Bitcoin Blockchain’s protocol may contain flaws that can be exploited by attackers.

•Concentration Risk. Because the Fund’s assets will be concentrated in an industry or group of industries to the extent the Index concentrates in a particular industry or group of industries, the Fund is subject to loss due to adverse occurrences that may affect that industry or group of industries.

•Cryptocurrency Risk. While the Fund will not invest directly in cryptocurrencies, certain of the Fund’s investments in Cryptocurrency ETFs and in publicly traded securities of companies engaged in cryptocurrency-related businesses and activities

20

are subject to fluctuations in the value of the cryptocurrencies in which they invest or to which they have exposure, and the value of such cryptocurrencies may be highly volatile. Cryptocurrencies (also referred to as “virtual currencies” and “digital currencies”) are digital assets designed to act as a medium of exchange. The value of cryptocurrencies is determined by supply and demand in the global cryptocurrency markets, which consist primarily of transactions of the respective cryptocurrencies on electronic exchanges or trading venues. Cryptocurrencies are relatively new, and their value is influenced by a wide variety of factors that are uncertain and difficult to evaluate, such as the infancy of their development, regulatory changes, a crisis of confidence, their dependence on technologies such as cryptographic protocols, their dependence on the role played by miners and developers and the potential for malicious activity (e.g., theft). Cryptocurrency generally operates without central authority (such as a bank) and is not backed by any government. Cryptocurrency is not legal tender. Currently, there is relatively limited use of cryptocurrency in the retail and commercial marketplaces, which contributes to price volatility. Federal, state and/or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in the U.S. is still developing. The market price of cryptocurrencies has been subject to extreme fluctuations. If cryptocurrency markets continue to be subject to sharp fluctuations, investors may experience losses. Similar to fiat currencies (i.e., a currency that is backed by a central bank or a national, supranational or quasi-national organization), cryptocurrencies are susceptible to theft, loss, and destruction. Cryptocurrency exchanges and other trading venues on which cryptocurrencies trade are relatively new and, in most cases, largely unregulated and may therefore be more exposed to market manipulation, fraud and failure than established, regulated exchanges for securities, derivatives and other currencies. Investors in cryptocurrency may have little or no recourse should such theft, fraud or manipulation occur and could suffer significant losses. Additionally, holders of cryptocurrency may not be able to access their wallets due to the loss, theft, compromise or destruction of the private keys associated with the public addresses that hold the cryptocurrency. The Fund’s indirect investment in cryptocurrency subjects it to volatility experienced by the cryptocurrency exchanges and other cryptocurrency trading venues, which may adversely affect the value of the Fund. Cryptocurrency exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers or malware, which may also affect the price of cryptocurrencies and thus the Fund’s investments in cryptocurrency-related instruments or in publicly traded securities of companies engaged in cryptocurrency-related businesses and activities.

The value of one or more cryptocurrencies may be adversely impacted if their respective networks do not develop at the pace of demand; if network participants acquire a significant share that would allow them to have unintended capabilities; and if “forks,” as discussed later in this prospectus, or similar events occur.