UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended March 31, 2026

For the transition period from ______________ to ______________

Commission File Number 001-41705

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||

(Address of principal executive offices and zip code)

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,”

“accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

☒ | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares of the registrant's common stock outstanding as of May 12, 2026 was 16,192,438 .

Part 1 FINANCIAL INFORMATION

ITEM 1. Financial Statements.

AZITRA, INC.

CONDENSED BALANCE SHEETS

March 31, 2026 | December 31, 2025 | ||||||||||

ASSETS | (Unaudited) | ||||||||||

Current assets: | |||||||||||

Cash and cash equivalents | $ | $ | |||||||||

Accounts receivable | |||||||||||

Tax credits receivable | |||||||||||

Prepaid expenses | |||||||||||

Total current assets | |||||||||||

Property and equipment, net | |||||||||||

Financing lease right-of-use asset, net | |||||||||||

Operating lease right-of-use asset, net | |||||||||||

Intangible assets, net | |||||||||||

Deferred patent costs | |||||||||||

Other assets | |||||||||||

Total assets | $ | $ | |||||||||

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||||||

Current liabilities: | |||||||||||

Accounts payable | |||||||||||

Income tax payable | |||||||||||

Current financing lease liability | |||||||||||

Current operating lease liability | |||||||||||

Insurance premium financing liability | |||||||||||

Accrued expenses | |||||||||||

Total current liabilities | |||||||||||

Long-term operating lease liability | |||||||||||

Total liabilities | |||||||||||

Commitments and contingencies (Note 10) | |||||||||||

Stockholders' equity | |||||||||||

Preferred stock; $ | |||||||||||

Common stock; $ | |||||||||||

Additional paid-in capital | |||||||||||

Accumulated deficit | ( | ( | |||||||||

Total stockholders' equity | |||||||||||

Total liabilities and stockholders' equity | $ | $ | |||||||||

F-1

The accompanying notes are an integral part of these financial statements.

AZITRA, INC.

UNAUDITED CONDENSED STATEMENTS OF OPERATIONS

For the Three Months Ended March 31, | |||||||||||||||||

2026 | 2025 | ||||||||||||||||

Operating expenses: | |||||||||||||||||

General and administrative | $ | $ | |||||||||||||||

Research and development | |||||||||||||||||

Total operating expenses | |||||||||||||||||

Loss from operations | ( | ( | |||||||||||||||

Other income (expense): | |||||||||||||||||

Interest income | |||||||||||||||||

Interest expense | ( | ( | |||||||||||||||

Change in fair value of warrants | |||||||||||||||||

Other expense | ( | ( | |||||||||||||||

Total other income | |||||||||||||||||

Loss before income taxes | ( | ( | |||||||||||||||

Income tax expense | |||||||||||||||||

Net loss attributable to common shareholders | $ | ( | $ | ( | |||||||||||||

Net loss per share, basic and diluted | $ | ( | $ | ( | |||||||||||||

Weighted average common stock outstanding, basic and diluted | |||||||||||||||||

F-2

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (UNAUDITED)

Preferred Stock | Common Stock | Additional Paid-in-Capital | Accumulated Deficit | Total Stockholders' Equity | |||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||

Balance - December 31, 2024 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||

Follow-on public offering, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

Follow-on public offering, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

Net loss | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

Balance, March 31, 2025 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||

Preferred Stock | Common Stock | Additional Paid-in-Capital | Accumulated Deficit | Total Stockholders' Equity | |||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||

Balance - December 31, 2025 | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

Private Placement, net of issuance costs of $ | — | — | — | — | |||||||||||||||||||||||||||||||||||||

Draws on equity line of credit, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

Exercise of Prefunded Warrants | — | — | ( | — | |||||||||||||||||||||||||||||||||||||

Stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

Net loss | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

Balance - March 31, 2026 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||

Amounts in the Condensed Statements of Changes in Stockholders' may not foot or tie to preceding financial statements due to rounding | |||||||||||||||||||||||||||||||||||||||||

F-3

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

CONDENSED STATEMENTS OF CASH FLOWS (UNAUDITED)

For the Three Months Ended March 31, | |||||||||||

2026 | 2025 | ||||||||||

Cash flows from operating activities: | |||||||||||

Net loss | $ | ( | $ | ( | |||||||

Adjustments to reconcile net loss to net cash used in operating activities: | |||||||||||

Depreciation and amortization | |||||||||||

Loss on lease modification | |||||||||||

Amortization of right-of-use assets | |||||||||||

Stock based compensation | |||||||||||

Change in fair value of warrant liability | ( | ||||||||||

Gain on disposal of property and equipment | ( | ||||||||||

Impairment of intangible assets and deferred patent costs | |||||||||||

Changes in operating assets and liabilities: | |||||||||||

Accounts receivable | ( | ||||||||||

Prepaid expenses | |||||||||||

Other assets | |||||||||||

Tax credits receivable | ( | ( | |||||||||

Income tax payable | ( | ( | |||||||||

Accounts payable and accrued expenses | ( | ||||||||||

Operating lease liability | ( | ( | |||||||||

Net cash used in operating activities | ( | ( | |||||||||

Cash flows from investing activities: | |||||||||||

Purchases of property and equipment | ( | ||||||||||

Proceeds from sale of property and equipment | |||||||||||

Deferred patent costs | ( | ( | |||||||||

Net cash used in investing activities | ( | ( | |||||||||

Cash flows from financing activities | |||||||||||

Principal payments on finance leases | ( | ( | |||||||||

Proceeds from public offerings, net | |||||||||||

Proceeds from private placement, net | |||||||||||

Proceeds from equity line of credit | |||||||||||

Repayment of insurance premium financing liability | ( | ||||||||||

Net cash provided by financing activities | |||||||||||

Net change in cash and cash equivalents | ( | ||||||||||

Cash and cash equivalents at beginning of period | |||||||||||

Cash and cash equivalents at end of period | $ | $ | |||||||||

F-4

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

1. Organization and Nature of Operations

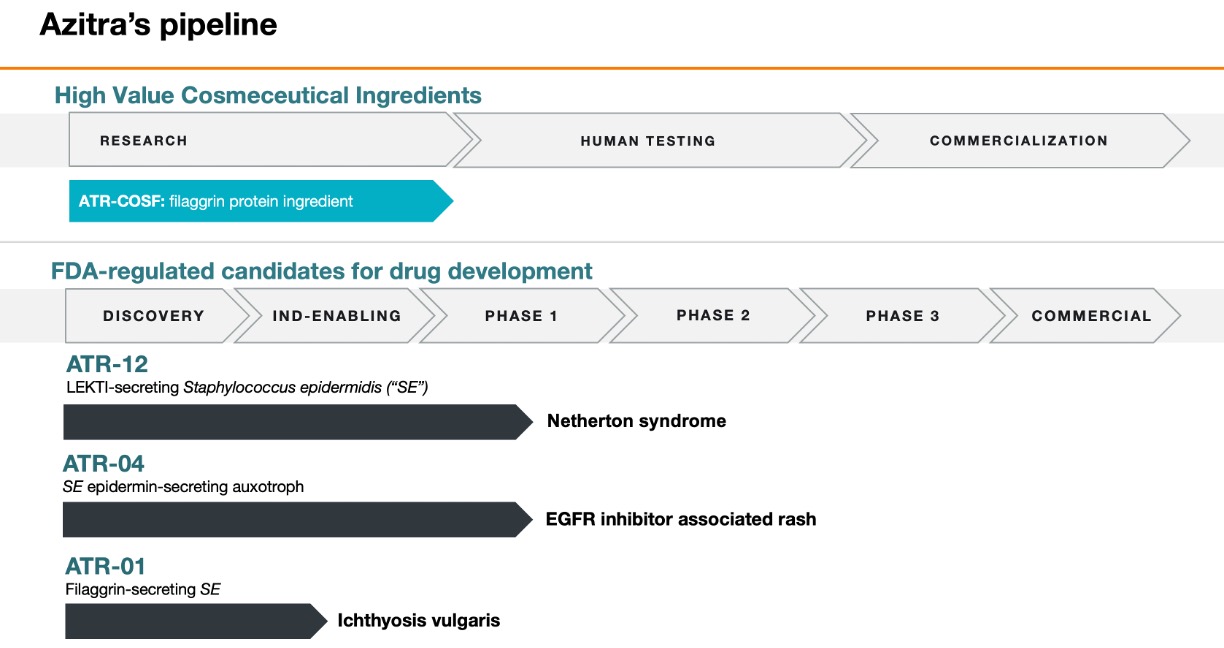

Azitra, Inc. (the "Company," "Azitra," "We," "us," and "our".) was founded on January 2, 2014. We are a synthetic biology company focused on screening and genetically engineering microbes of the skin. The mission is to discover and develop novel therapeutics to create a new paradigm for treating skin disease. The Company’s discovery platform is screened for naturally occurring bacterial cells with beneficial effects. These microbes are then genomically sequenced and engineered to make cellular therapies, recombinant therapeutic proteins, peptides and small molecules for precision treatment of dermatology diseases. The Company also leverages these technologies to develop cosmetic ingredients for consumer-oriented products. On May 17, 2023, the Company changed its name to from “Azitra Inc” to “Azitra, Inc.”

In addition to our corporate headquarters located in Branford, Connecticut, the Company maintains a location in Montreal, Canada for certain research activities. The Company also opened a manufacturing and laboratory space in Groton, Connecticut during 2021.

Stock Splits, Change in Par Value, Increase in Shares Authorized, Initial and Follow-on Public Offerings, and Equity Line of Credit Issuances

In June 2023, the Company completed its initial public offering (IPO) in which it issued and sold 7,508 shares of its common stock at a price to the public of $999.00 per share. The shares began trading on the NYSE American on June 16, 2023 under the symbol “AZTR”. The net proceeds received by the Company from the IPO were $6.0 million, after deducting underwriting discounts, commissions and other offering expenses.

Immediately prior to the effectiveness of the Company’s registration statement, the Company effected a 7.1 -for-1 forward stock split (the "Forward Stock Split") of its issued and outstanding shares of common stock. On May 17, 2023, the Company changed the par value of its capital stock from $0.01 to $0.0001 . Accordingly, all share and per share amounts for all periods presented in the accompanying unaudited condensed financial statements and notes thereto have been adjusted retroactively, unless otherwise noted, to reflect the effect of the Forward Stock Split. Refer to Note 6 for additional details relating to the Forward Stock Split.

In February 2024, the Company completed a follow-on public offering (the "February 2024 Offering") in which it issued and sold 83,404 shares of its common stock at a price to the public of $59.94 per share. The net proceeds received by the Company from the follow-on public offering were $4.3 million, after deducting underwriting discounts, commissions and other offering expenses. For further information regarding the February 2024 Offering and related warrant issuance, refer to Notes 6 and 7 respectively.

On July 1, 2024, the Company effected a 30-for-1 reverse stock split of its issued and outstanding shares of common stock (the "2024 Reverse Stock Split") and began trading on a split-adjusted basis the same day. There was no change in par value. Accordingly, all share and per share amounts for all periods presented in the accompanying unaudited condensed financial statements and notes thereto have been adjusted retroactively, where applicable, to reflect the effect of the 2024 Reverse Stock Split. Refer to Note 6 for additional details relating to the Reverse Stock Split.

In July 2024, the Company completed a follow-on public offering (the "July 2024 Offering") in which it issued and sold 1,000,750 shares of its common stock at a price of $9.99 per share and Class A Warrants exercisable for an aggregate 2,001,502 shares of common stock. The net proceeds received by the Company from the follow-on public offering were $9.1 million, after deducting placement agent's fees and other offering expenses. For further information regarding the July 2024 Offering and related warrant issuance, refer to Notes 6 and 7 respectively.

In January 2025, the Company completed a follow-on offering (the "January 2025 Offering") in which it issued and sold 729,381 shares of its common stock at a price of $2.00 per share. The net proceeds received by the Company from the follow-on offering were $1.2 million, after deducting placement agent's fees and other offering expenses. The shares were offered by the Company pursuant to a shelf registration statement on Form S-3 filed with the SEC on July 1, 2024, and a final prospectus supplement dated January 15, 2025. For further information regarding the January 2025 Offering, refer to Notes 6 and 7 respectively.

In February 2025, the Company completed a follow-on offering (the "February 2025 Offering") in which it issued 374,696 shares of its common stock at a public offering price of $1.85 per share and warrants to purchase up to 337,232 shares of common stock at an exercise price of $3.60 . The net proceeds received by the Company from the follow-on offering were $560,976 after deducting placement agent's fees and other offering expenses. The shares were offered by the Company pursuant to a shelf registration statement on Form S-3 filed with the SEC on July 1, 2024, and a final prospectus supplement dated February 6, 2025. For further information regarding the February 2025 Offering and related warrant issuance, refer to Notes 6 and 7, respectively.

F-5

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

On April 24, 2025, the Company entered into an Equity Line of Credit ("ELOC"), as amended, with Alumni Capital LP ("Alumni Capital"), whereby the Company has the right, but not the obligation, to sell to Alumni Capital, and Alumni Capital is obligated to purchase, up to an aggregate of $20 million of shares of the Company's common stock in a series of purchases. Upon each purchase, Alumni Capital will receive warrants to purchase shares of the Company's common stock equal to 10 % of the number of shares purchased in the related purchase.

Under the terms of the ELOC, the Company has issued an aggregate of 9,255,823 shares of common stock and issued 925,579 warrants. The aggregate gross proceeds received by the Company under the ELOC are $6.2 million. As of May 12, 2026, approximately $13.8 million is available under the ELOC for future share issuances. For further information regarding the ELOC, refer to Notes 6 and 7 respectively.

In July 2025, the Company amended and restated its Certificate of Incorporation (the "Amended and Restated Certificate of Incorporation") increasing the number of authorized shares of common stock from 100,000,000 to 200,000,000 .

On August 21, 2025, the Company effected a 6.66-for-1 reverse stock split of its issued and outstanding shares of common stock (the "2025 Reverse Stock Split") and began trading on a split-adjusted basis the same day. There was no change in par value. Accordingly, all share and per share amounts for all periods presented in the accompanying unaudited condensed financial statements and notes thereto have been adjusted retroactively, where applicable, to reflect the effect of the 2025 Reverse Stock Split. Refer to Note 6 for additional details relating to the 2024 Reverse Stock Split, and the 2025 Reverse Stock Split (together, the "Reverse Stock Splits").

On November 24, 2025, the Company entered into a securities purchase agreement (the “Purchase Agreement”) with Alumni Capital pursuant to which the Company agreed to issue and sell to Alumni Capital in a private placement offering (the "PIPE Offering") priced at a premium to market in accordance with NYSE rules (the “Offering”) an aggregate of 535,759 shares of common stock of the Company, (ii) pre-funded warrants (the “Pre-Funded Warrants”) to purchase up to an aggregate of 4,151,741 shares of Common Stock (the “Pre-Funded Warrants Shares”) at an exercise price of $0.0001 per Pre-Funded Warrant, and (iii) common stock purchase warrants (the “Common Warrants” together with the Pre-Funded Warrants, the “Warrants”) to purchase up to an aggregate of 4,687,500 shares of Common Stock (the “Common Warrant Shares” together with the Pre-Funded Warrant Shares, the “Warrant Shares”) at an exercise price of $0.32 per Common Warrant. The offering price was $0.32 per share of Common Stock or Pre-Funded Warrant and accompanying Common Warrant (the “Offering Price”). The Pre-Funded Warrants are immediately exercisable and do not expire until exercised in full. The Common Warrants are exercisable upon shareholder approval and will expire on the five-year anniversary of shareholder approval. For further information regarding the PIPE Offering, refer to Notes 6 and 7 respectively.

During the three months ended March 31, 2026, all Pre-Funded Warrants have been exercised by Alumni Capital.

On March 18, 2026, the Company entered into a securities purchase agreement (the "Series A Purchase Agreement") in which it issued and sold 10,485 shares of its Series A Preferred Stock (the "Series A Offering") at a price of $1,000 per share, which are convertible into 85,223,129 shares of common stock, Series B Warrants exercisable for an aggregate 85,223,126 shares of common stock, and Series C Warrants exercisable for an aggregate 85,223,126 shares of common stock. The net proceeds received by the Company from the Series A Offering were $10.4 million, after deducting offering expenses. For further information related to the Series A Offering and related warrant issuances, refer to Notes 6 and 7 respectively.

Other Events

On October 1, 2025, the Company received a deficiency letter (the “Deficiency Letter”) from the NYSE American LLC ("NYSE American") indicating that the Company is not in compliance with the NYSE American continued listing standards set forth in Section 1003(a)(ii) of the NYSE American Company Guide. Section 1003(a)(ii) of the NYSE American Company Guide requires a listed company’s stockholders’ equity be at least $4.0 million if it has reported losses from continuing operations and/or net losses in three of its four most recent fiscal years. The Deficiency Letter noted that the Company reported stockholders’ equity of $2.2 million as of June 30, 2025, and losses from continuing operations and/or net losses in three of its four most recent fiscal years ended December 31, 2024.

In order to maintain the Company’s listing on the NYSE American, the NYSE American requested that the Company submit a plan of compliance (the “Plan”) by October 31, 2025 addressing how the Company intends to regain compliance with Section 1003(a)(ii) of the NYSE American Company Guide by April 1, 2027.

The Company’s management submitted the Plan to the NYSE American by the October 31, 2025 deadline which was accepted by the NYSE American on December 16, 2025. If the Company does not make progress consistent with the Plan during the plan period or if

F-6

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

the Company is not in compliance with the listing standards by April 1, 2027, then the Company will be subject to delisting procedures as set forth in the NYSE American Company Guide.

The Company is committed to undertaking a transaction or transactions in the future to achieve compliance with the NYSE American’s requirements. There can be no assurance that the Company will be able to achieve compliance with the NYSE American’s continued listing standards within the required time frame.

Going Concern Matters

The unaudited condensed financial statements have been prepared on the going concern basis, which assumes that the Company will continue in operation for the foreseeable future, and which contemplates the realization of assets and liquidation of liabilities in the normal course of business. However, management has identified the following conditions and events that created an uncertainty about the ability of the Company to continue as a going concern. As of and for the three months ended March 31, 2026, the Company has an accumulated deficit of approximately $72.4 million, a loss from operations of approximately $3.9 million, used approximately $2.5 million to fund operations and had approximately $9.2 million of working capital.

The Company will require a significant amount of additional funds to complete the development of its product and to fund additional losses which the Company expects to incur over the next few years. The Company is still in its pre-commercialization phase and therefore does not yet have product revenue. Management plans to continue to raise funds through equity and/or debt financing to fund operating and working capital needs; however, there can be no assurance that the Company will be successful in securing additional financing, if needed, to meet its operating needs.

These conditions and events create substantial doubt about the ability of the Company to continue as a going concern for twelve months from the date that the financial statements are available to be issued. The financial statements do not include any adjustments that might be necessary should the Company be unable to continue as a going concern.

2. Summary of Significant Accounting Policies

Basis of Accounting

The financial statements of the Company are prepared in accordance with United States generally accepted accounting principles (“U.S. GAAP”). Certain amounts in the condensed financial statements and associated notes may not add up due to rounding.

Unaudited Interim Financial Information

The unaudited interim financial statements and related notes have been prepared in accordance with U.S. GAAP for interim financial information, within the rules and regulations of the United States Securities and Exchange Commission (the “SEC”). Certain information and disclosures normally included in the annual financial statements prepared in accordance with U.S. GAAP have been condensed or omitted pursuant to such rules and regulations. The unaudited interim financial statements have been prepared on a basis consistent with the audited financial statements and in the opinion of management, reflect all adjustments, consisting of only normal recurring adjustments, necessary for the fair presentation of the results for the interim periods presented and of the financial condition as of the date of the interim balance sheet. The financial data and the other information disclosed in these notes to the interim financial statements related to the three months are unaudited. Unaudited interim results are not necessarily indicative of the results for the full fiscal year. These unaudited interim financial statements should be read in conjunction with the financial statements of the Company for the year ended December 31, 2025, and notes thereto that are included in the Company’s Annual Report on Form 10-K as filed with the SEC on February 27, 2026.

Use of Estimates

The preparation of the financial statement in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the balance sheet. While management believes the estimates and assumptions used in the preparation of the financial statements are appropriate, actual results could differ from those estimates. The most significant estimates in the Company's financial statements relate to accruals for research and development expenses, valuation of warrants and valuation of equity awards, and the recoverability of our deferred patent costs. These estimates and assumptions are based on current facts, historical experience and various other factors believed to be reasonable under the circumstances, the results of which form the basis for making judgements about the carrying values of assets and liabilities and the recording of expenses that are not readily apparent from other sources.

F-7

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

Concentration of Credit Risks and other Risks and Uncertainties

Financial instruments, which potentially subject the Company to significant concentrations of risk, consist principally of cash and cash equivalents. The Company’s cash is deposited with a federally insured U.S. financial institution. The Company has no off-balance sheet concentrations of credit risk, such as foreign currency exchange contracts, option contracts or other hedging arrangements.

The Company is dependent on contract research organizations ("CRO") to conduct, and manage our on-going clinical trials, and contract manufacturing organizations (“CMO”) to supply products for research and development of its product candidates, including preclinical and clinical studies, and for commercialization of its product candidates, if approved. The Company’s development programs could be adversely affected by any significant interruption in either the CRO's or the CMO’s operations or by a significant interruption in the supply of active pharmaceutical ingredients and other components.

Products developed by the Company require approval from the U.S. Food and Drug Administration (“FDA”) or other international regulatory agencies prior to commercial sales. There can be no assurance the Company’s product candidates will receive the necessary approvals. If the Company is denied approvals, approvals are delayed, or the Company is unable to maintain approvals received, such events could have a materially adverse impact on the Company.

The Company’s activities are subject to significant risks and uncertainties including the risk of failure to secure additional funding to properly execute the Company’s business plan. The Company is subject to risks that are common to companies in the pharmaceutical industry, including, but not limited to, development by the Company or its competitors of new technological innovations, dependence on key personnel, reliance on third party manufacturers, protection of proprietary technology, and compliance with regulatory requirements.

Segment Information

Cash and Cash Equivalents

For purposes of the balance sheets and statements of cash flows, the Company considers all cash on hand, demand deposits and all highly liquid investments with original maturities of three months or less to be cash equivalents.

Deferred Offering and Deferred Issuance Costs

The Company capitalizes deferred offering costs, which primarily consists of direct, incremental legal, professional, accounting, and other third-party fees relating to the Company’s public offering initiatives associated with the filing of an S-1 Registration Statement. Once the Company completes the public offering, the Company records these amounts against the gross proceeds of these public offerings within the statements of stockholders’ equity.

In July 2024, the Company also filed a Form S-3 Registration Statement and recorded deferred issuance costs as a long-term asset. In September 2025, the Company wrote off the remaining deferred issuance costs of $35,435 as it was uncertain the Company would be able to issue additional shares against the Form S-3 Registration Statement. The write-off resulted in a reduction to additional paid-in capital.

Leases

The Company has 3 operating leases for buildings and record an initial ROU assets and lease liabilities totaling $1,418,502 . The basis, terms and conditions of the leases are determined by the individual agreements. The Company’s option to extend certain leases ranges from 36 – 52 months. All options to extend have been included in the calculation of the ROU asset and lease liability. The leases do not contain residual value guarantees, restrictions, or covenants that could incur additional financial obligations to the Company. There are no subleases, sale-leaseback, or related party transactions.

F-8

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

At March 31, 2026, the Company had operating right-of-use assets with a net value of $329,353 and current and long-term operating lease liabilities of $240,740 and $96,740 , respectively.

In 2023, the Company entered into a lease for the use of certain equipment that is classified as a finance lease. The finance lease has a term of 36 months. At March 31, 2026, the Company had financing right-of-use assets with a net value of $5,171 and current and long-term operating lease liabilities of $5,850 and $— , respectively.

Deferred Patent Costs

Research and Development

At March 31, 2026 and December 31, 2025, the Company had state tax credit receivables of $103,601 26,799 and $27,269 , respectively, for pending refunds related to Canadian Scientific Research and Experimental Development (SRED) credits. At March 31, 2026 and December 31, 2025, the Company had recorded $18,984 and $9,513 , respectively, related to refunds of Canadian Goods and Services Tax (GST) and Quebec Sales Tax (QST). Receipts of refunds are recorded in research and development on the statements of operations.

Recent and Adopted Accounting Pronouncements

In November 2024, the FASB issued ASU 2024-03, "Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40)." Additionally, in January 2025, the FASB issued ASU 2025-01 to clarify the effective date of ASU 2024-03. The standard provides guidance to expand disclosures related to the disaggregation of income statement expenses. The standard requires, in the notes to the financial statements, disclosure of specified information about certain costs and expenses which includes purchases of inventory, employee compensation, depreciation, and intangible asset amortization included in each relevant expense caption. This guidance is effective for fiscal years beginning after December 15, 2026, and interim periods within annual reporting periods beginning after December 15, 2027, on a retrospective or prospective basis, with early adoption permitted. We are currently evaluating this ASU to determine its impact on our disclosures.

In July 2025, the FASB issued ASU 2025-05, “Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses for Accounts Receivable and Contract Assets”, which introduces a practical expedient that allows entities to assume that current conditions at the balance sheet date remain unchanged for the remaining life of the asset when developing reasonable and supportable forecasts. This eliminates the need to incorporate macroeconomic forecasts for short term receivables. The ASU is effective for fiscal years beginning after December 15, 2025. The Company adopted ASU 2025-05 on January 1, 2026, on a prospective basis, which did not have a significant impact on the financial statements and related disclosures.

F-9

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

3. Property and Equipment

Property and equipment consisted of the following at:

March 31, 2026 | December 31, 2025 | |||||||||||||

Laboratory equipment | $ | $ | ||||||||||||

Computers and office equipment | ||||||||||||||

Furniture and fixtures | ||||||||||||||

Leasehold improvements | ||||||||||||||

Building equipment | ||||||||||||||

Total property and equipment | ||||||||||||||

Less accumulated depreciation & amortization | ( | ( | ||||||||||||

Total property and equipment, net | $ | $ | ||||||||||||

Depreciation and amortization expense was $33,081 and $30,967 for the periods ended March 31, 2026 and 2025, respectively.

Fixed assets are reviewed for impairment each reporting period. For the periods ended March 31, 2026 and 2025 there was $— and $1,175 of gains on disposal of property and equipment recorded, respectively.

4. Intangible Assets

Intangible assets consisted of the following at:

March 31, 2026:

Estimated Useful Life | Gross Amount | Accumulated Amortization | Impairment | Net Amount | |||||||||||||||||||||||||

Trademarks | Indefinite | $ | $ | — | $ | $ | |||||||||||||||||||||||

Patents | |||||||||||||||||||||||||||||

Intangible assets | $ | $ | $ | $ | |||||||||||||||||||||||||

December 31, 2025:

Estimated Useful Life | Gross Amount | Accumulated Amortization | Impairment | Net Amount | |||||||||||||||||||||||||

Trademarks | Indefinite | $ | $ | — | $ | $ | |||||||||||||||||||||||

Patents | |||||||||||||||||||||||||||||

Intangible assets | $ | $ | $ | $ | |||||||||||||||||||||||||

F-10

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

5. Accrued Expenses

Accrued expenses consisted of the following at:

March 31, 2026 | December 31, 2025 | ||||||||||

Employee payroll and bonuses | $ | $ | |||||||||

Vacation | |||||||||||

Research and development projects | |||||||||||

Professional fees | |||||||||||

Other | |||||||||||

Total accrued expenses | $ | $ | |||||||||

6. Stockholders’ Equity

On May 17, 2023, the Company effected a 7.1 -for-1 Forward Stock Split of its issued and outstanding shares of common stock and a proportional adjustment to the existing conversion ratios for each series of the Company’s preferred stock. The par value of the common stock was adjusted as a result of the Forward Stock Split from $0.01 to $0.0001 and the authorized shares were increased to 100,000,000 shares of common stock in connection with the Forward Stock Split. In lieu of any fractional shares issued as a result of the split the Company paid a cash amount to the holder of such fractional share. The accompanying financial statements and notes to the financial statements give retroactive effect to the Forward Stock Split for all periods presented. Shares of common stock underlying outstanding stock-based awards and other equity instruments were proportionately increased and the respective per share value and exercise prices, if applicable, were proportionately decreased in accordance with the terms of the agreements governing such securities.

On February 16, 2024, the Company completed the February 2024 Offering, consisting of an aggregate of 83,404 shares of its common stock at a public offering price of $59.94 per share. The gross proceeds from the February 2024 Offering, before deducting the placement agent's fees and other offering expenses, were approximately $5 million.

As consideration for ThinkEquity LLC serving as the Placement Agent for the February 2024 Offering (the "February 2024 Placement Agent"), the Company paid the February 2024 Placement Agent a cash fee of 7.5 % of the aggregate gross proceeds of the February 2024 Offering and reimbursed the February 2024 Placement Agent for certain expenses, legal fees for a total of $537,559 , and issued February 2024 Placement Agent Warrants to designees to the February 2024 Placement Agent.

On July 1, 2024, the Company effected a 30-for-1 Reverse Stock Split of its issued and outstanding shares of common stock and began trading on a split-adjusted basis the same day. There was no change to the par value of the common stock. In lieu of any fractional shares issued as a result of the split the Company paid a cash amount to the holder of such fractional share. The accompanying financial statements and notes to the financial statements give retroactive effect to the Reverse Stock Split for all periods presented unless otherwise noted. Shares of common stock underlying outstanding stock-based awards and other equity instruments were proportionately decreased and the respective per share value and exercise prices, if applicable, were proportionately increased in accordance with the terms of the agreements governing such securities.

On July 25, 2024, the Company completed the July 2024 Offering, consisting of an aggregate of 1,000,750 shares of its common stock and Class A warrants to purchase 2,001,502 shares of common stock, at a combined public offering price of $9.99 . The Class A warrant had an initial exercise price of $9.99 per share, was exercisable immediately upon issuance, and will expire on the fifth anniversary of the original issuance date. However, if on the date that was 30 calendar days immediately following the date of issuance of the Class A Warrants, or August 24, 2024 (the “Reset Date”), the Reset Price, as defined below, was less than the exercise price at such time, the exercise price would be decreased to the Reset Price. “Reset Price” is defined as 100 % of the trailing five-day VWAP immediately preceding the Reset Date, provided, that in no event would the Reset Price be less than $2.13 (subject to adjustment for reverse and forward stock splits, recapitalizations and similar transactions), which represented 20 % of the most recent closing price for the Common Stock at the time of execution of the placement agent agreement with respect to the offering. The Reset Price of the Class A Warrants as calculated on the Reset Date was $4.69 . The number of shares of Common Stock issuable upon exercise of the Class A Warrants has not been proportionately adjusted due to the reset of the exercise price.

In consideration for Maxim Group LLC serving as the placement agent of the July 2024 Offering (the “July 2024 Placement Agent”), the Company paid the July 2024 Placement Agent a cash fee equal to 7.0 % of the aggregate gross proceeds of the July 2024 Offering,

F-11

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

reimbursed the July 2024 Placement Agent for certain expenses and legal fees for a total of $809,825 , and issued Placement Agent Warrants.

The gross proceeds from the July 2024 Offering, before deducting the July 2024 Placement Agent’s fees and other offering expenses, were approximately $10.0 million.

On January 14, 2025, the Company completed the January 2025 Offering in which it issued and sold 729,381 shares of its common stock at a price of $2.00 per share. The net proceeds received by the Company from the January 2025 Offering were approximately $1.2 million, after deducting underwriting discounts, commissions and other offering expenses. The shares were offered by the Company pursuant to a shelf registration statement on Form S-3 filed with the SEC on July 1, 2024, and a final prospectus supplement dated January 15, 2025.

In consideration for Maxim Group LLC serving as the placement agent of the January 2025 Offering (the "January 2025 Placement Agent"), the Company paid the January 2025 Placement Agent a cash fee equal to 7.0 % of the aggregate gross proceeds raised in the January 2025 Offering and the reimbursed the January 2025 Placement Agent for certain expenses and legal fees of $60,000 . The Company also issued warrants to designees of the January 2025 Placement Agent (the "Placement Agent Warrants").

On February 5, 2025, the Company completed the February 2025 Offering in which it issued 374,696 shares of its common stock at a public offering price of $1.85 per share and warrants to purchase up to 337,232 shares of common stock. The net proceeds received by the Company from the February 2025 Offering were $561,000 after deducting placement agent's fees and other offering expenses. The shares were offered by the Company pursuant to a shelf registration statement on Form S-3 filed with the SEC on July 1, 2024, and a final prospectus supplement dated February 6, 2025.

In consideration for Maxim Group LLC serving as the placement agent of the February 2025 Offering (the "February 2025 Placement Agent"), the Company paid the February 2025 Placement Agent a cash fee equal to 4.0 % of the aggregate gross proceeds raised in the February 2025 Offering, reimbursed the February 2025 Placement Agent for certain expenses and legal fees of $35,000 , and issued Placement Agent Warrants.

On April 24, 2025, the Company entered into an ELOC, as amended, with Alumni Capital, whereby the Company has the right, but not the obligation, to sell to Alumni Capital, and Alumni Capital is obligated to purchase, up to an aggregate of $20 million of shares of the Company’s common stock in a series of purchases. The term of the ELOC is through December 31, 2026, or the date on which Alumni Capital shall have purchased the shares pursuant to the ELOC for an aggregate purchase price of $20 million. During the term, the Company may at its election cause Alumni Capital to make a series of purchases of shares, each up to $750,000 , or up to $4 million dollars upon consent of Alumni Capital. The closing of each purchase pursuant to the ELOC will be no later than business days after the Company provides a notice to Alumni Capital. The purchase price of the shares that the Company elects to sell to Alumni Capital pursuant to the ELOC will be equal to the lowest daily volume weighted average price of the Common Stock during the period commencing on the date that the Company delivers a notice requiring the purchase of shares by Alumni Capital and ending on the earlier to occur of (i) (5) business days immediately following such date and (ii) the date on which Alumni Capital notifies the Company that it is prepared to proceed with the relevant closing, multiplied by 90 %.

On August 26, 2025, the Company entered into a Modification Agreement (the “Modification Agreement”) with Alumni Capital to amend certain terms of the Purchase Agreement, dated April 24, 2025, between the Company and Alumni Capital (the “Purchase Agreement”). Pursuant to the Modification Agreement, the Company may at its election, cause Alumni Capital to make a series of purchases of ELOC Shares either at (i) the lowest daily volume weighted average price of the Common Stock during the period commencing on the date that the Company delivers written notice (the “Purchase Notice”) and ending on the earlier of (a) (5) business days immediately following the date of a Purchase Notice, and (b) the date on which Alumni Capital notifies the Company that it is prepared to proceed with the closing of the purchase, multiplied by 90 % (“Purchase Notice Option 1”) or (ii) the lowest traded price of Common Stock during the period commencing on the date the Company delivers a Purchase Notice and ending on the earlier of (x) the same business day a Purchase Notice is delivered, and (y) the date on which Alumni Capital notifies the Company that it is prepared to proceed with the closing of the purchase, multiplied by 97 % (“Purchase Notice Option 2”). Each Purchase Notice delivered by the Company must specify whether Purchase Notice Option 1 or Purchase Notice Option 2 is selected and the number of ELOC Shares to be purchased. All other terms and conditions of the Purchase Agreement remain in full force and effect. Refer to Note 7 regarding the terms of the warrants issued in conjunction with the shares.

Through March 31, 2026 the Company has issued an aggregate 9,255,823 shares of common stock and issued an aggregate 925,579 warrants. During the three months ended March 31, 2026, the Company issued 1,300,000 shares of common stock and 130,000

F-12

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

warrants under the ELOC resulting in net proceeds of approximately $215,000 . As of the date of this filing, the aggregate gross proceeds received by the Company under the ELOC were approximately $6.2 million.

On November 24, 2025, the Company completed the PIPE Offering of 535,759 shares of common stock of the Company, Pre-Funded Warrants to purchase up to an aggregate of 4,151,741 shares of common at an exercise price of $0.0001 per Pre-Funded Warrant, and Common Warrants to purchase up to an aggregate of 4,687,500 shares of common stock at an exercise price of $0.32 per Common Warrant. The offering price was $0.32 per share of common stock or Pre-Funded Warrant and accompanying Common Warrant Price. The Pre-Funded Warrants are immediately exercisable and do not expire until exercised in full. The Common Warrants are exercisable upon shareholder approval and will expire on the five-year anniversary of shareholder approval.

For the three months ended March 31, 2026, all Pre-Funded Warrants have been exercised by Alumni Capital.

In consideration for Maxim Group LLC serving as the placement agent for the PIPE Offering (the "PIPE Placement Agent"), the Company paid a cash fee equal to 7.0 % of the aggregate gross proceeds raised in the PIPE Offering, reimbursed the PIPE Placement Agent for certain expenses and legal fees of $50,000 , and issued Placement Agent Warrants.

On March 20, 2026, the Company completed the Series A Offering, for the sale of a unit, each unit consisting of one Series A Preferred Share ("Series A PS"), which is convertible into 8,128.1 shares of common stock, one Series B Warrant ("B Warrant") exercisable for 8,128.1 shares of common stock and one Series C Warrant ("C Warrant") exercisable for 8,128.1 shares of common stock (the "B Warrant and C Warant" collectively the "Series A Preferred Warrants") and (the "Series A PS, B Warrant and C Warrant", collectively, the Series A Unit") The Series A Preferred warrants are exercisable at $0.123 1,000 per Unit and a total of 10,485 Units were sold in the Series A Offering resulting in net proceeds of approximately $10.4 million after deducting offering costs of approximately $101,000 .

The Series A PS is convertible into 85,223,126 shares of common stock and each of the B Warrants and C Warrants are exercisable for 85,223,126 shares of Common Stock. The Series B Warrants will be exercisable following the receipt of the requisite stockholder approval and will terminate 18 months following such approval. The Series C Warrants will become exercisable upon the requisite shareholder approval and the certificate of amendment filing as defined in the Series A Purchase Agreement and will terminate 30 calendar days after the date the Company publicly announces data from its cosmetic filaggrin study in humans.

Common Stock

At March 31, 2026 and December 31, 2025, per the Company’s amended and restated Certificate of Incorporation, the Company was authorized to issue 200,000,000 0.0001

Each share of common stock entitles the holder to one vote on all matters submitted to a vote of the Company’s stockholders.

Pending stockholder approval of the Certificate of Amendment to the Amended and Restated Certificate of Incorporation, increasing the authorized number of shares of common stock from 200,000,000 to 750,000,000 shares at the 2026 Annual Meeting of Stockholders, the Company will reserve 264,019,900 shares of common stock reserved for future issuance for the potential conversion of the Company's Series A Preferred, and the potential exercise of stock options and warrants outstanding at March 31, 2026.

Except as otherwise indicated, all share and share price amounts in this report gives effect to a forward stock split effected on May 17, 2023 at a ratio of 7.1 -for-1, a reverse stock split effected on July 1, 2024 at a ratio of 1-for-30, and a reverse stock split effected on August 21, 2025 at a ratio of 1-for-6.66.

Preferred Stock

At March 31, 2026 and December 31, 2025, per the Company’s Amended and Restated Certificate of Incorporation, the Company has authorized 10,000,000 0.0001

Upon the close of the Company’s IPO in June 2023, all of the then outstanding preferred stock converted to common stock, resulting in the issuance of shares of common stock in exchange for outstanding Series A (7,298 shares), Series A-1 (14,839 shares), and Series B Preferred Stock (16,439 shares), respectively. There was no gain or loss upon conversion.

The Company currently has 10,485 shares of Series A Preferred stock outstanding that automatically convert to 85,223,126 shares of common stock upon the requisite shareholder approval and increase in authorized shares of common stock from 200,000,000 750,000,000 shares.

The holders of our Series A Preferred Stock have the following rights and privileges:

F-13

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

Redemption Rights

Non-redeemable at any time.

Rank

The Series A Preferred Stock shall rank (i) senior to any class or series of capital stock of the Corporation hereafter created specifically ranking by its terms junior to any Series A Preferred Stock; (ii) on parity with the Common Stock and any other class or series of capital stock of the Corporation hereafter created specifically ranking by its terms on parity with the Series A Preferred Stock; and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking by its terms senior to any Series A Preferred Stock .

Dividend Rights

If the Board of Directors shall declare a dividend or other distribution payable upon the then outstanding shares of Common Stock, whether in cash, in kind or in other securities or property (other than dividends payable in shares of Common Stock), the holders of the outstanding shares of Series A Preferred shall be entitled to the amount of dividends as would be payable in respect of the number of shares of Common Stock into which the shares of Series A Preferred held by each holder thereof could be converted, without regard to any restrictions on conversion (including the Beneficial Ownership Limitation).

Conversion Rights

The Series A Preferred are not convertible into common stock until the requisite shareholder approval at which time the Series A Preferred shall automatically convert into the Company's common stock subject to the holder's ownership limitations.

Voting Rights

Except as otherwise provided by the Delaware General Corporate Law ("DGCL"), other applicable law or as provided in this Certificate of Designations, the holders of Series A Preferred Stock shall not be entitled to vote (or render written consents) on any matter submitted for a vote of (or written consents in lieu of a vote as permitted by the DGCL, the Certificate of Incorporation and the Bylaws) holders of Common Stock.

Liquidation Rights

The Series A Preferred shall rank (i) senior to any class or series of capital stock of the Corporation hereafter created specifically ranking by its terms junior to any Series A Preferred (“Junior Securities”); (ii) on parity with the Common Stock and any other class or series of capital stock of the Corporation hereafter created specifically ranking by its terms on parity with the Series A Preferred (“Parity Securities”); and (iii) junior to any class or series of capital stock of the Corporation hereafter created specifically ranking by its terms senior to any Series A Preferred (“Senior Securities”), in each case, as to distributions of assets upon liquidation, dissolution or winding up of the Corporation, whether voluntarily or involuntarily (each, a “Dissolution”).

The Series A Preferred were evaluated pursuant to ASC 480 - Distinguishing Liabilities from Equity and determined to be equity instruments.

7. Warrants

The Company issued warrants to purchase 238 shares of common stock in 2018 in conjunction with convertible debt financing that have a redemption provision providing the holder the right to have the Company redeem all or any portion of the warrant (or shares it has converted into) at a purchase price equal to the fair market value of the shares as determined by the board of directors or an independent appraiser. As a result of this redemption provision, the warrants have been classified as a liability in the financial statements based on ASC 480. These warrants have an exercise price of $95.90 per share and a term of 10 years. The warrants are adjusted to their current fair value each reporting period. The fair value was $— and $— at March 31, 2026 and December 31, 2025, respectively.

The Company issued 300 warrants to its underwriters as part of our initial public offering in fiscal 2023. In fiscal 2024, the Company issued an additional 3,336 warrants in February, and 40,030 warrants in July to its underwriters as part of our February, and July Offerings. The underwriter warrants have a term of 5 years.

In connection with the February 2024 Offering, the Company also issued warrants to designees to the February 2024 Placement Agent exercisable for an aggregate of 3,336 shares of Common Stock at an exercise price of $75.92 per share (125% of the $60.74 public

F-14

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

offering price) and which expire on February 16, 2029. The warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

The Company issued 2,001,502 Class A Warrants to investors who participated in the Company's July 2024 Offering. The Class A Warrants had an initial exercise price of $9.99 per share of Common Stock; however, on August 24, 2024 the exercise price was reset to $4.69 . See Note 6. The number of shares of Common Stock issuable upon exercise of the Class A Warrants were not proportionately adjusted in connection with the reset of the exercise price.

The Class A Warrants are exercisable upon issuance and expire five years from the date of issuance. The Class A Warrants contain ownership limitations pursuant to which a holder does not have the right to exercise any portion of their warrants if it would result in the holder (together with its affiliates) beneficially owning more than 4.99 % (or, at the election of the holder, 9.99 %) of the Company’s outstanding Common Stock. The Class A Warrants are issued pursuant to a Warrant Agent Agreement dated July 25, 2024 (“Warrant Agent Agreement”) between the Company and VStock Transfer LLC, as warrant agent. In August 2024, 150 warrants were exercised for proceeds of $704 .

In connection with the July 2024 Offering, the Company evaluated the Class A Warrants and determined they met the criteria for liability classification as they met the criteria in ASC 815 - Derivatives and Hedging due to the reset provision. The Class A Warrants had an initial fair value of $12.1 million. The gross proceeds of approximately $10.0 million from the July 2024 follow-on public offering was allocated to the Class A Warrants resulting in a loss on issuance of common stock of approximately $2.1 million recorded in Other income (expenses). Upon the reset of the Class A Warrant exercise price, the Class A Warrants no longer met the criteria for liability classification pursuant to ASC 815; at which time the Company recorded a gain in Other income (expenses) - Change in fair value of Class A warrants of $4.0 million, and reclassified $1.9 million to equity representing the difference between the change in the fair value, and the loss upon issuance of our common stock.

The Class A Warrants were valued utilizing a probability weighted scenario method with a Monte Carlo simulation model and Black-Scholes Model. The significant assumptions in the Monte Carlo simulation model include a stay public assumption of 90 %, and a fundamental transaction assumption of 10 %. The significant assumptions utilized in estimating the fair value of the Class A Warrants at issuance include (i) a per share price of common stock range of $1.14 - $1.40 ; (ii) a dividend yield of 0 %; (iii) a risk-free rate range of 4.13 % - 4.14 %; (iv) expected volatility of 119 %; (v) projected stock price and volume weighted average price as of the Reset Date of $1.14 ; (vi) a strike price range of $1.40 - $1.50 ; and (vii) expected term of 4.92 years.

In connection with the July 2024 Offering, the Company also issued warrants to designees of the July 2024 Placement Agent exercisable for an aggregate of 40,030 shares of common stock. The warrants have substantially the same terms as the Class A Warrants, except that the July 2024 Placement Agent warrants have an exercise price equal to $12.49 per share (125% of the $9.99 public offering price), have an initial exercise date of January 23, 2025 and expire on July 23, 2029. The 2024 Placement Agent warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

In connection with the January 2025 Offering, as consideration for Maxim Group LLC serving as the Placement Agent of the January 2025 Offering, the Company also issued warrants to designees of the Placement Agent exercisable for an aggregate of 29,175 shares of common stock, which represent 4.0 % of the aggregate number of shares of common stock sold in the offering, at an exercise price per share equal to 125 % of the public offering price of $2.50 . The warrants are exercisable six months from the date of issuance and expire five years from the commencement of the sales in this offering. The warrants may be exercisable via cashless exercise in certain circumstances. The warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

In connection with the February 2025 Offering, the Company issued warrants to purchase up to 337,232 shares of common stock at an exercise price of $3.60 . The warrants are exercisable on the six-month and one day anniversary of their issuance, and their exercise price was calculated as the greater of the (1) book value of the common stock or (ii) market value of the common stock as determined by the NYSE American Rules. The warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

In connection with shares issued to Alumni Capital under the terms of the ELOC, as amended, Alumni Capital will receive warrants to purchase such number of shares of the Company’s common stock equal to 10 % of the number of shares purchased in the related purchase. The Exercise Price shall equal 130 % of the price per share paid upon closing. The exercise of the warrant will be subject to stockholder approval and expire five years after issuance. The warrants may be exercised via cashless exercise if there is no effective registration statement, or current prospectus available for, the resale of the warrant shares. The Company has issued an aggregate 925,579 warrants as of March 31, 2026 and 130,000 warrants for the three months ended March 31, 2026.

In connection with the PIPE Offering, the Company issued Pre-Funded Warrants to purchase up to 4,151,741 shares of common stock at an exercise price of $0.0001 , and Common Warrants to purchase up to an aggregate of 4,687,500 shares of common stock at an exercise price of $0.32 per Common Warrant. The Pre-Funded Warrants are immediately exercisable and do not expire until exercised

F-15

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

in full. The Common Warrants are exercisable upon shareholder approval and will expire on the five-year anniversary of shareholder approval. For the three months ended March 31, 2026, all Pre-Funded Warrants have been exercised by Alumni Capital.

In connection with the PIPE Offering, as consideration for Maxim Group LLC serving as the PIPE Placement Agent, the Company also issued warrants to designees of the PIPE Placement Agent exercisable for an aggregate of 187,500 shares of common stock, which represent 4.0 % of the aggregate number of shares of common stock sold in the offering, at an exercise price per share equal to 125 % of the public offering price of $0.32 . The warrants are exercisable six months from the date of issuance and expire five years from the commencement of the sales in this offering. The warrants may be exercisable via cashless exercise in certain circumstances. The warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

In connection with the Series A Preferred Offering, the Company issued Series B and Series C Warrants to purchase up to 85,223,126 and 85,223,126 shares of common stock with an exercise price of $0.123 18 months following such approval. The Series C Warrants will become exercisable upon the requisite shareholder approval and the certificate of amendment filing as defined in the Series A Purchase Agreement and will terminate 30 calendar days after the date the Company publicly announces data from its cosmetic filaggrin study in humans. The warrants were evaluated in accordance with ASC 718 and recorded within stockholders' equity.

The following table summarizes information about warrants outstanding at March 31, 2026:

Warrants Outstanding | Warrants Exercisable | |||||||||||||||||||||||||||||||||||||||||||

Year Granted | Exercise Price | Number of Warrants at 03/31/2026 | Weighted Average Remaining Contractual Life | Weighted Average Exercise Price | Number of Warrants at 03/31/2026 | Weighted Average Remaining Contractual Life | Weighted Average Exercise Price | |||||||||||||||||||||||||||||||||||||

2018 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2023 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2024 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2024 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2024 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

F-16

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | — | 0 | $ | — | ||||||||||||||||||||||||||||||||||||||

2025 | $ | $ | — | 0 | $ | — | ||||||||||||||||||||||||||||||||||||||

2026 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2026 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2026 | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||

2026 | $ | $ | — | 0 | $ | — | ||||||||||||||||||||||||||||||||||||||

$ | $ | |||||||||||||||||||||||||||||||||||||||||||

8. Stock Options

In March 2023, the Company’s Board of Directors and stockholders approved the 2023 Stock Incentive Plan (“2023 Plan”). The 2023 Plan allows the Compensation Committee to grant up to 181,842 shares of Common Stock in the form of incentive and non-statutory stock options, restricted stock awards, restricted stock units, and other stock-based awards to employees, directors, and non-employees. As of March 31, 2026, options to purchase 134,284 shares of common stock had been granted and were outstanding under the 2023 Plan and 584,592 shares of common stock were available for grant under the plan. On October 3, 2024, the Company’s Board of Directors approved amendments to the 2023 Plan to (i) increase the number of shares of Common Stock that may be issued under the 2023 Plan by 171,832 shares and (ii) adopt an evergreen provision to the 2023 Plan providing for an automatic 5 % annual increase in the shares of Common Stock available for issuance under the 2023 Plan over the next 10 years. Both amendments were approved by the Company’s stockholders at the Company’s annual stockholder meeting held on November 20, 2024. On January 1, 2026, the shares of Common Stock that may be issued under the 2023 Plan increased by 537,034 shares in accordance with the evergreen provision.

During 2016, the Company established the Azitra Inc. 2016 Stock Incentive Plan ("2016 Plan") which provides for the grant up to 7,460 shares of Common Stock in the form of stock options and restricted shares to the Company’s employees, officers, directors, advisors and consultants. As of March 31, 2026, options to purchase 4,091 shares of common stock had been granted and 3,075 shares of common stock were available for grant under the 2016 Plan.

At March 31, 2026, there was $43,355 of unamortized compensation expense that will be amortized over the remaining vesting period. The Company determined the options qualified as plain vanilla under the provisions of SAB 107 and the simplified method was used to estimate the expected option life.

To determine the estimated fair value of the options granted during 2025, the Company used the Black-Scholes option pricing model with the following assumptions: Underlying common stock value of $0.30 ; Expected term of 6.5 to 10 years; Expected Volatility of 86.7 %; to 89.1 % Risk Free Interest Rate of 3.86 % - 4.12 %; and Dividend Yield of 0 %.

F-17

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

Stock-based compensation expense recognized for options was as follows:

For the Three Months Ended March 31, | ||||||||||||||

2026 | 2025 | |||||||||||||

Research and development | $ | $ | ||||||||||||

General and administrative | ||||||||||||||

Total | $ | $ | ||||||||||||

The following table summarizes information about options outstanding and exercisable at March 31, 2026:

Options Outstanding | Options Exercisable | |||||||||||||||||||||||||||||||||||||

Exercise Price | Number of Options at March 31, 2026 | Weighted Average Remaining Contractual Life | Weighted Average Exercise Price | Number of Options Exercisable at March 31, 2026 | Weighted Average Remaining Contractual Life | Weighted Average Exercise Price | ||||||||||||||||||||||||||||||||

$ | $ | $ | ||||||||||||||||||||||||||||||||||||

$ | $ | $ | ||||||||||||||||||||||||||||||||||||

$ | $ | $ | ||||||||||||||||||||||||||||||||||||

Total stock option activity for the three months ended March 31, 2026, is summarized as follows:

Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term (years) | Aggregate Intrinsic Value (in thousands) | |||||||||||||||||||||||

Outstanding at December 31, 2025 | $ | |||||||||||||||||||||||||

Granted | — | — | ||||||||||||||||||||||||

Exercised | — | — | ||||||||||||||||||||||||

Forfeited | ( | — | — | |||||||||||||||||||||||

Outstanding at March 31, 2026 | $ | |||||||||||||||||||||||||

Vested and Exercisable at March 31, 2026 | ||||||||||||||||||||||||||

9. Net Loss Per Share

The following potential common stock equivalents, presented based on amounts outstanding at each period end, were excluded from the calculation of diluted net loss per share for the periods indicated because including them would have had an anti-dilutive effect.

March 31, | |||||||||||

2026 | 2025 | ||||||||||

Options to purchase shares of common stock | |||||||||||

Warrants outstanding | |||||||||||

Conversion of preferred stock to common stock | |||||||||||

Total | |||||||||||

F-18

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

10. Commitments and Contingencies

Legal

The Company is subject to legal proceedings or claims which arise in the ordinary course of its business. Although occasional adverse decisions or settlements may occur, the Company believes that the final disposition of such matters should not have a material adverse effect on its financial position, results of operations or liquidity.

License Agreement

Effective January 26, 2022, the Company entered into an Exclusive License Agreement (the License Agreement) with an unrelated third party. Under the License Agreement, the Company is granted an exclusive license for certain patents and a non-exclusive license for certain know-how. The License Agreement continues until the later of the expiration of the last to expire licensed patent or ten years after the first commercial sale of the first licensed therapeutic or non-therapeutic product. The Company may terminate the License Agreement at any time by providing at least 30 days written notice to the third party. The License Agreement is also terminated upon breach of a material obligation under the agreement or bankruptcy. Upon any termination of the License Agreement, neither party is relieved of obligations incurred prior to the termination.

During the periods ended March 31, 2026 and 2025, the Company did not capitalize any payments made under this license.

Operating Leases

The Company leases office and lab space in Branford, CT, Groton, CT, and Montreal, Quebec. The Company’s leases expire at various dates through May 31, 2027. Most leases are for a fixed term and for a fixed amount.

During 2019, the Company entered into a new lease agreement for office and laboratory space in Montreal, Quebec. The Montreal lease required monthly payments of $6,906 , CAD which increases approximately 4 % in each of the following years. The Montreal lease was increased to $8,130 CAD in 2021 upon leasing additional space. The Montreal lease was initially for a one-year term, renewable annually. The Montreal lease also requires the Company to pay additional common area maintenance.

During 2020, the Company entered into a new lease agreement for the Company’s primary office and laboratory space in Branford, CT. The Branford lease requires monthly payments of $13,033 for the first year of the lease, which increases approximately 2 % in each of the following years. The Branford lease also requires the Company to pay a pro-rata share of common area maintenance.

During May 2021, the Company entered into a new lease for office and laboratory space in Groton, CT. The Groton lease required monthly payments of $4,234 , which was increased to $6,824 in September 2021 upon leasing additional space. In August 2024, the Company reassessed its needs and released certain lab space resulting in a decrease to the monthly payment to $5,216 . The Groton lease is initially for a one-year term, renewable annually for up to additional years.

Future minimum payments under non-cancelable operating leases with initial or remaining terms in excess of one year during each of the next five years follow:

2026 | $ | ||||

2027 | |||||

2028 | |||||

Thereafter | |||||

Total future undiscounted lease payments | |||||

Less interest | ( | ||||

Present value of minimum lease payments | $ | ||||

Rent expense for all operating leases was $79,488 and $84,717 for the for the periods ended March 31, 2026 and 2025, respectively. The weighted average lease term for all operating leases is 1.4 years. The weighted average discount rate for all operating leases is 4.90 %.

F-19

The accompanying notes are an integral part of these unaudited condensed financial statements.

AZITRA, INC.

NOTES TO UNAUDITED CONDENSED FINANCIAL STATEMENTS

Finance Leases

During 2023, the Company entered into an agreement with Hewlett Packard to lease equipment. The lease requires monthly payments of $1,478 , including tax. The lease is for a 3 year term with option of purchase or extension at term end. The remaining lease term is 0.3 years and the discount rate is 9.60 %.

The following is a schedule showing the future minimum lease payments under finance leases by years and the present value of the minimum payments as of March 31, 2026.

2026 | $ | ||||

Total future undiscounted lease payments | |||||

Less interest | ( | ||||

Present value of minimum lease payments | $ | ||||

11. Retirement Plan

12. Concentration of Credit Risk

Financial instruments that potentially subject the Company to credit risk consist principally of cash.

The cash balance identified in the balance sheet is held in an account with a financial institution and insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000. At times, cash maintained on deposit may be in excess of FDIC limits.

13. Segment Information

The Company operates and manages its business as a single reportable segment, which is to discover and develop novel therapeutics to create a new paradigm for treating skin diseases. The Chief Executive Officer, who is the Chief Operating Decision Maker ("CODM"), manages and evaluates the Company's performance on a total Company basis of net loss and assessing how to allocate resources based on the Company cash position as reported in the Company's balance sheet and statement of operations. The Company's significant expenses are consistent with the expense categories presented in the statement of operations.

As of March 31, 2026, all of the Company's fixed assets were maintained in the United States and Canada on an original costs basis of $908,166 and $288,397 , respectively.

F-20

The accompanying notes are an integral part of these unaudited condensed financial statements.

14. Subsequent Events

The Company has evaluated events subsequent to the balance sheet date through May 13, 2026, the date these financial statements are issued.

On April 17, 2026 the compensation committee approved the payment of retention bonuses to employees in the amount of $329,000 and the grant of 514,684 options.

F-21

The accompanying notes are an integral part of these unaudited condensed financial statements.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Cautionary Statement Regarding Forward-looking Statements

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed financial statements and the related notes thereto contained elsewhere in this report. The information contained in this quarterly report on Form 10-Q is not a complete description of our business or the risks associated with an investment in our common stock. We urge you to carefully review and consider the various disclosures made by us in this report and in our other filings with the Securities and Exchange Commission, or SEC, including our Form 10-K for the year ended December 31, 2025, filed with the SEC on February 27, 2026.