PUBLIC 17 11 2025 CODE OF ETHICS Version 1.9 Review history: Version Date Edited Signed Comments by off by 1.0 2018 11 WB MT Initial 1.1 2019 01

WB MT Minor clarifications 1.2 2019 04 WB MT Minor clarifications 1.3 2020 03 WB MT Adjustments to gifts and entertainment, personal account dealing 1.4 2021 04 WB MT Annual update 1.5 2022 04 WB MT New OBI

pre-clearance screen; adjustments to Confidentiality, Whistleblowing 1.6 2023 04 WB MT Higher entertainment limit; IAC team 1.7 2023 10 WB MT Adjustments to OBI and Political Contributions; changes to PA

dealing 1.8 2024 10 WB MT Annual update 1.9 2025 11 MC WB Annual update Update frequency: Annual

|

|

|

|

|

| CONTENTS |

|

|

|

|

|

|

| GLOSSARY OF TERMS |

|

|

2 |

|

|

|

| What do we need to know? |

|

|

3 |

|

|

|

| 1. CFM entities |

|

|

3 |

|

|

|

| 2. How does this Code of Ethics fit into CFM’s compliance framework? |

|

|

3 |

|

|

|

| 3. Why do we have a Code of Ethics? |

|

|

4 |

|

|

|

| What do I need to do? |

|

|

5 |

|

|

|

| 1. Acknowledgements |

|

|

5 |

|

|

|

| 2. Personal account dealing |

|

|

5 |

|

|

|

| 3. Gifts and entertainment |

|

|

10 |

|

|

|

| 4. Outside business activities |

|

|

13 |

|

|

|

| 5. U.S Political contributions; Pay-to

Play |

|

|

14 |

|

|

|

| 6. Complaints |

|

|

15 |

|

|

|

| 7. Whistleblowing |

|

|

16 |

|

|

|

| 8. Mandatory holidays |

|

|

18 |

|

|

|

| 9. Bad actor rule |

|

|

18 |

|

|

|

| 10. Other Policies |

|

|

19 |

|

|

|

| 11. Escalation and Breaches |

|

|

21 |

|

GLOSSARY OF TERMS

|

|

|

| CCO |

|

Chief Compliance Officer; the Chief Compliance Officer is identified as the SMF16 Compliance Officer for CFM LLP (as of this document: Wealon

Bouillet), and CFM’s Head of Legal, Compliance and Operations for every other CFM entity (as of this document: Martin Tornqvist) |

| CFM LLP |

|

Capital Fund Management LLP |

| CFM or the Firm |

|

Collectively, the Capital Fund Management group of companies |

| CFM SA |

|

Capital Fund Management S.A. |

| Client |

|

Any fund, mandate or account managed or advised by a CFM entity, including investors in such funds |

| MCO |

|

MyComplianceOffice, a third-party personal account dealing reporting platform operated by TerraNua which CFM has implemented for US and UK staff |

| FCPA |

|

Foreign Corrupt Practices Act |

| SEC |

|

U.S. Securities and Exchange Commission |

2

What do we need to know?

As an employee of a CFM entity, the provisions of this Code of Ethics apply to you regardless of location, team or title. The requirements described in this Code of

Ethics are grouped by theme; CFM asks that you be aware at all times of the existence of obligations related to these themes, and that you refer to this Code of Ethics whenever necessary to fulfil such obligations. Any questions regarding your

obligations should be referred to the applicable CCO.

|

| |

| Who does this document apply to? |

|

| The Code of Ethics applies in its entirety to all employees of CFM, full-time or part-time, regardless of seniority. The Personal Account Dealing section below also applies in full to long-term contractors (defined as those whose

contract duration exceeds 6 months). |

|

| Agreements with contractors and other non-employees (e.g. PhD. students) will also include confidentiality

clauses. |

Introduction

In order

to perform their various activities, most CFM entities are subject to regulatory oversight. Many rules apply not just to regulated entities but also to their staff. This Code of Ethics sets forth the ethical and fiduciary principles and related

compliance requirements under which CFM and its staff must operate and the procedures for implementing those principles. This Code of Ethics is applied on a CFM group basis and thus applies to all CFM staff. Failure to comply with this Code of

Ethics may result in disciplinary action against the employee, including but not limited to a warning, fine, disgorgement, suspension, or termination of employment. In addition to sanctions imposed by CFM, violations may result in referral to civil

or criminal authorities where appropriate.

1. CFM entities

Capital

Fund Management S.A. (“CFM SA”) serves as discretionary investment manager for its clients, which include private funds and managed accounts. CFM SA is a French limited liability company registered as a UCITS portfolio management company

with the French AMF.

CFM SA has five wholly owned subsidiaries: Capital Fund Management International, Inc. (“CFMI”), CFM North America, Inc (“CFM

NA”), both incorporated in Delaware (U.S.A.), CFM Canada Ltd incorporated in Canada, CFM Corporate Member Ltd incorporated in the UK and CSysNet in France.

CFM NA serves as the general partner of the Cayman limited partnerships and managing member of the Delaware limited liability companies (as described below); CFMI

carries out the investor relations activities of CFM in the US; CFM Canada Ltd carries out the investor relations activities of CFM in Canada. CFM Corporate Member Ltd is the managing member of Capital Fund Management LLP (“CFM LLP”)

which is authorised as an AIFM with the UK Financial Conduct Authority (“FCA”) and has filed as an exempt reporting adviser with the SEC. CSysNet is a French company dedicated to the procurement of IT hardware and software to the CFM

group of companies.

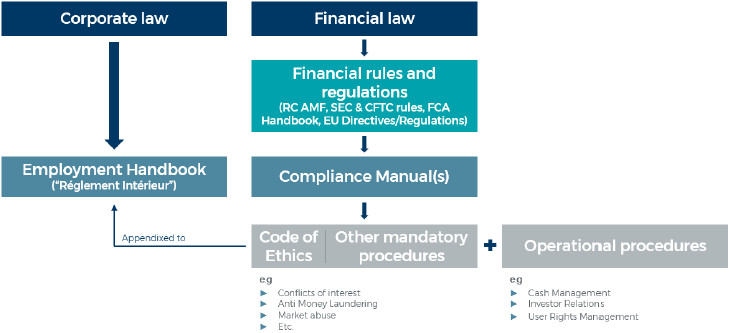

2. How does this Code of Ethics fit into CFM’s compliance framework?

The Code of Ethics is part of CFM’s procedures, which derive from various applicable financial rules and regulations. It is appendixed to CFM SA’s employment

handbook.

3

3. Why do we have a Code of Ethics?

Most of the rules mentioned above relate in some way or another to the notion of conflict of interest. Principles of fiduciary duty which apply to CFM dictate that CFM

conduct its business in a manner that places the interests of Clients above the interests of the Firm.

CFM is a fiduciary of the funds and accounts it manages and

owes each of them an affirmative duty of good faith and full and fair disclosure of all material facts. Mere negligence on the part of the Firm in breaching its fiduciary duty to a fund, its investors or prospective investors, may be sufficient to

establish a violation under the applicable rules. For example, CFM must take care not to include false or misleading statements in fund documents, regulatory disclosures, investor reports, responses to “requests for proposals,” or other

disclosures to Clients or prospective Clients. CFM and all employees must affirmatively exercise authority and responsibility for the benefit of Clients, and may not participate in any activities that may conflict with the interests of Clients

except in accordance with this Code of Ethics. In addition, employees must avoid activities, interests and relationships that might interfere or appear to interfere with making decisions in the best interests of CFM’s Clients. Accordingly, at

all times, CFM must conduct its business with the following precepts in mind:

| u |

Place the interests of Clients first. CFM employees may not cause a Client to take action, or not to take action,

for their personal or the Firm’s benefit rather than the benefit of the Client. For example, causing a Client to purchase a security owned by an employee for the purpose of increasing the price of that security would be a violation of this

Code of Ethics. Similarly, an employee investing for him- or herself in a security of limited availability that was appropriate for a Client without first considering offering that investment for such Client

may violate this Code. |

| u |

Conduct all personal securities transactions in compliance with this Code of Ethics. This includes all pre-clearance and reporting requirements and procedures regarding inside information and personal and proprietary trades. While CFM does not discourage employees and their families to develop personal investment

programs, employees must not take any action that could result in even the appearance of impropriety. |

| u |

Moderate gifts and entertainment. The receipt of investment opportunities, entertainment, or gifts from persons

doing or seeking to do business with CFM could call into question the exercise of CFM’s independent judgment. The giving of gifts or entertainment to Clients or prospective Clients could raise similar concerns. Accordingly, employees may

accept or give such items only in accordance with the limitations in this Code of Ethics. |

4

| u |

Keep information confidential. Information concerning Client investment recommendations, investment decisions,

transactions or holdings may be material non-public information and employees may not use knowledge of any such information to profit from the market effect of those transactions. |

| u |

Comply with all laws and regulations applicable to CFM’s business. It is the responsibility of every employee

to know what is required of CFM as an investment manager, adviser or other financial services provider, and of him or her as an employee of the Firm, and integrate compliance into the performance of all duties. |

| u |

Seek advice when in doubt about the propriety of any action or situation. Any questions concerning this Code of

Ethics should be addressed to the CCO, who is encouraged to consult with outside counsel, outside auditors or other professionals, as necessary. |

This Code of Ethics implements these general fiduciary principles in the context of specific situations. Additional matters relating to fiduciary duties under ERISA are

addressed more in detail in the ERISA Policy. This Code of Ethics should also be read in conjunction with CFM’s Conflicts of Interests Policy and the relevant employee handbook (Réglement Intérieur or Employment Manual as the

case may be).

What do I need to do?

1. Acknowledgements

Upon

joining CFM, and on a periodic basis thereafter, all staff is required to complete the following acknowledgements:

|

|

|

|

|

|

|

| Concerned staff |

|

Acknowledgement |

|

Frequency |

|

Location |

|

|

|

|

| All |

|

Compliance Certifications |

|

Upon joining and annually |

|

CFM Intranet |

|

|

|

|

| All |

|

SEC questionnaire |

|

Upon joining and annually |

|

CFM Intranet |

|

|

|

|

| All |

|

Personal Account Declaration |

|

Upon joining and ad hoc |

|

CFM Intranet / MCO |

|

|

|

|

| All |

|

Quarterly trading report |

|

Quarterly |

|

CFM Intranet / MCO |

|

|

|

|

| All |

|

Holdings report |

|

Upon joining and annually |

|

CFM Intranet / MCO |

|

|

|

|

| All |

|

Ancillary activities pre-clearance |

|

Upon joining and ad hoc |

|

CFM Intranet |

|

|

|

|

| All |

|

Ancillary activities form |

|

Annually |

|

CFM Intranet |

|

|

|

|

| CFM LLP |

|

Compliance Declaration Memo |

|

Upon joining and annually |

|

Sent by email |

|

|

|

|

| Semi-Systematic team |

|

Semi-Systematic Questionnaire |

|

Quarterly |

|

CFM Intranet |

|

|

|

|

| Equity Capital Market team |

|

Equity Capital Market Questionnaire |

|

Quarterly |

|

CFM Intranet |

2. Personal account dealing

Personal investments must be consistent with CFM’s mission to always put Client interests first and with the requirements that CFM and its employees do not trade

on the basis of material non-public information, including information concerning CFM’s investment decisions for Clients or Client transactions or holdings.

a. Declaring your accounts

Access Persons, i.e. persons subject to the Personal Account Dealing provisions of this Code of Ethics

Under applicable

regulation, certain persons must report their accounts, transactions and holdings periodically to the CCO. The concerned persons are generally officers, directors and employees of CFM who:

5

| |

1. |

Have access to non-public information regarding any Client’s purchase or sale of

securities, or non-public information regarding the holdings of any Client; or |

| |

2. |

Are involved in making securities recommendations to Clients or have access to such recommendations that are non-public. |

CFM considers CFM SA Board members, every employee of the CFM group, as well as long-term

contractors to be Access Persons. Certain other individuals may from time to time be Access Persons. As they have no day-to-day access to CFM systems and data,

independent Board members of CFM entities or funds as well as independent members of the Remuneration Committee are not considered Access Persons. Finally, prior to the start of their internship, interns declare in writing that they will refrain

from carrying out any personal trading during their stay at CFM.

Disclosable and Trade Reporting Accounts

Disclosable Accounts are, generally speaking, accounts which the Access Person has the opportunity to personally profit (or share in the profits) from, directly or

indirectly, and through any contract or relationship or other means.

In accordance with regulation, CFM considers Disclosable Accounts to include, among other

accounts meeting the conditions above:

| u |

Accounts of the Access Person, his or her spouse, and their un-emancipated minor

children; |

| u |

Accounts of any family member who shares the Access Person’s household; |

| u |

Accounts of anyone to whose support the Access Person materially contributes (e.g. adult child whose sole income derives

from such Access Person); |

| u |

Accounts over which the Access Person exercises discretion or a controlling influence (e.g. parent’s investment

account for which the Access Person holds a procuration). |

Access Persons with accounts that they do not view to be Disclosable Accounts should

consult with the Regulatory team to verify and document their conclusion. The Regulatory team may require the Access Person to provide additional or renewed certifications or information about these accounts.

The following are considered Non-Disclosable Accounts by CFM:

| u |

Cash accounts such as checking accounts, fixed term accounts, and cash-only savings accounts (e.g. French Livret A, LDD);

|

| u |

Any retirement or savings schemes which are offered in connection with your employment at CFM; and1 |

| u |

Any accounts that have only held funds managed by CFM or CFM stock since they were opened.2 |

Trade Reporting Accounts are a subset of Disclosable Accounts. Every Disclosable Account

is a Trade Reporting Account with the below exceptions:

| u |

Accounts for which you don’t have investment discretion at the instrument level (for instance, because a

third party has a discretionary mandate to invest on your behalf; or an account where you only select broad categories of investments on a forward-looking basis); and |

| u |

Accounts which regulation otherwise excludes from the scope of most Personal Account Dealing provisions.

|

The Compliance team will require documentation of any of the above conditions.

Declaring accounts

All Disclosable Accounts must

be declared in MCO for US and UK staff, or using the declaration form on CFM’s intranet for others (LINK),

| 1 |

In the general sense these would normally be reportable accounts. However, we are comfortable

treating them as Non-Disclosable because (i) we know every employee has such an account; and (ii) we know that the retirement schemes that CFM offers only allow UCITS funds for EU residents; or

allocations based on broad instrument types, for US residents. |

| 2 |

CFM”s Regulatory team has visibility, both pre-trade

and post-trade, on any employee investment in CFM funds or stock, so pre-clearance and reporting would be redundant. |

6

Summary table

The below table presents a summarized view of typical investment accounts, and which category they fall into.

|

|

|

|

|

|

|

| |

|

|

|

Disclosable Accounts |

| Type of account |

|

Non-Disclosable

Accounts |

|

Non-Trade Reporting Accounts |

|

Trade Reporting Accounts |

|

|

|

|

| Your obligations |

|

u None |

|

u Declare the account |

|

u Declare the account |

|

|

|

|

|

|

u Pre-clear transactions (see below) |

|

|

|

|

|

|

u Report trades quarterly (see below) |

| |

|

|

|

|

|

u Provide year-end statements (see below) |

|

|

|

|

| Examples |

|

u Checking account

u Fixed

term account

u Livret

A

u LDD

u French

PEL

u CFM

PEE

u CFM

PERCO

u CFM

401k

u CFM

SIPP

u Cryptocurrency

wallets

u Accounts

which have only ever held CFM funds or stock |

|

u Any account for which you don’t have investment discretion at the instrument level, such as when a

third party manages it on your behalf. This includes accounts where you only determine an allocation (e.g. 30% stocks, 50% bonds, 20% cash) but not individual positions. |

|

Any other securities or trading account for which you have investment discretion, including

(but not limited to): u French PEA or Assurance-vie

u UK

ISA

u US

IRA (unless you are able to confirm that you do not have discretion at the instrument level) u Non-CFM PEE, PERCO, 401k or other retirement or pension account

(including SIPPs, Superannuations and Group Personal Pensions) |

|

| |

| What about private placements? |

|

| Some investments do not always sit in accounts such as those listed above - for example some hedge funds, private equity or unlisted stocks. Such investments, unless

they are Exempted Trades, are subject to pre-clearance and reporting (see below), but no account needs to be declared. |

b. Pre-clearance; exempted trades; prohibited

transactions

Access Persons must obtain the written approval of the Regulatory team prior to carrying out transactions (both long and short) in listed or

unlisted equity or debt securities, listed or unlisted derivatives, or before participating in initial public offerings or private placements (e.g., hedge funds, private equity funds, initial coin offerings, limited offerings). Exempted Trades as

defined below are excluded from this obligation.

The Regulatory team’s approval must be requested in MCO for US and UK staff, or using the dedicated intranet

screen for others (LINK). In matters pertaining to Initial Public Offerings (IPOs) and private placements, the employee should first seek pre-clearance and consult with the Regulatory team. They must provide all relevant information, including details on how the investment opportunity came to their attention and information about the company involved.

The employee must also submit any relevant documents, such as the prospectus, private placement memoranda, subscription documents or other materials about the investment.

7

A decision on permissibility of the trade generally will be rendered by the end of the trading day on which the request

is received. In approving any such transaction, the Regulatory team must cite the reasons for such approval. Pre-clearance will be effective for a 24-hour period,

with the exception of private placements. Approval for private placements will remain in effect for 30 days, unless terminated earlier by the Regulatory team on a

case-by-case basis. Should the effectiveness period lapse, a new pre-approval must be requested. The confirmation of such pre-clearance requests shall include a declaration that such reports also include transactions of any other related Access Persons.

Exempted Trades

The following are

excluded from the pre-clearance obligation (“Exempted Trades”):

| u |

Trades in the following instruments (“Exempted Instruments”): |

| |

> |

Government bonds of G20 countries; |

| |

> |

money market instruments — bankers’ acceptances, bank certificates of deposit, commercial paper, repurchase

agreements and other high quality short-term debt instruments; |

| |

> |

money market fund shares, where the Access Person, CFM or its affiliates are not involved in the management of such fund;

|

| |

> |

shares or interests in CFM funds; |

| |

> |

shares or interests in CFM corporate entities; |

| |

> |

shares or interests in other types of diversified regulated funds, where the Access Person, CFM or its affiliates are not

involved in the management of such fund (this would include, for instance, US mutual funds and ETFs3, EU UCITS funds and ETFs, French FIPs and FCPRs – but not unregulated EU Alternative

Investment Funds, highly concentrated ETFs or certain French FCPEs providing exposure to a single stock). |

| u |

Trades initiated by a third party with investment discretion over the Trade Reporting Account, where there was no prior

instruction or suggestions from the Access Person (e.g.: wealth management services, blind trusts, dividends paid in stock, transactions effected pursuant to an automatic investment plan). |

| u |

Instruments (stock or stock options usually) obtained as part of a person’s compensation package. For the sake of

clarity, only the acquisition of these instruments is exempted; the sale of the same would require a pre-clearance. |

| u |

Transfers of financial instruments between different accounts held by the same person. |

|

| |

| The exemption is tied to the instrument type, not the underlying |

|

| For example, an ETF on Bitcoin would be exempted, but not an option on an EU ETF. |

Minimum holding period

The Regulatory team will generally disapprove trades made within 180 days of a previous, opposite-direction trade on the same issuer or underlying, regardless of

instrument. For the avoidance of doubt, the minimum holding period applies to all transactions that are not Exempted Trades. For example, the following trades would be prohibited if made within 180 days of one another: buying a company’s bonds

and shorting the stock; buying a coal future and shorting a different maturity; generally trying to hedge a position. The Regulatory team can make exceptions for trades that are made at the same time as part of an overall long-term strategy, e.g. a

covered call, and declared as such, for as long as the strategy is maintained.

| 3 |

The SEC only exempts ETFs that are structured as open-end

funds. However, not all ETFs are open-end funds; some of the oldest and largest are structured as Unit Investment Trusts (UIT). We have been advised that there are 4 ETFs structured as UITs that are still

listed today: SPY, MDY, DIA and QQQ. We have concluded that their size and diversification are such that, considering CFM’s activities, investment style and execution, the risk of market abuse, financial crime or conflict of interest through

personal trading is insignificant. Therefore we will continue to exclude all ETFs from pre-clearance and reporting requirements, including UITs. |

8

Prohibited transactions

The following transactions are prohibited:

| u |

Any transaction that would be considered as market abuse under applicable regulation (please refer to CFM’s Market

Abuse Policy for more guidance); |

| u |

Any transaction relying on material non-public information or confidential

information; |

| u |

Any transaction in an instrument appearing on CFM’s Personal Trading Restricted List available on the intranet (LINK); |

| u |

Any IPO for employees who are a Registered Representative of a US broker-dealer or a Portfolio Manager or a deputy

Portfolio Manager. |

c. Transaction reporting

All Access Persons must file initial and annual holdings reports and quarterly trading reports (see above: “Acknowledgements”) with respect to all Trade

Reporting Accounts. Exempted Trades are excluded from this obligation.

Initial holdings reports must be filed no later than 10 days after becoming an

Access Person, and annual holdings reports must be filed within 30 days of year-end. Each such report must be current as of a date no more than 45 days before the report is submitted. The

confirmation of such initial and holding reports shall include a declaration that such reports also include transactions of any other related Access Persons.

| u |

For French employees, this report takes place on the intranet (LINK). Employees must

confirm each position in a non- Exempted Instrument as of the reporting date including associated account, instrument identifier, quantity and price. The Regulatory team may, on a sample basis, request

statements to confirm an employee’s report. |

| u |

US/UK/Canada employees that have private placements and/or accounts that do not provide feeds to MCO are required to

provide statements of all such private placements and accounts. |

Any statement must include, at a minimum, the employee’s name, account

identifier, bank/broker/financial institution and date. For the sake of clarity, initial and annual holdings reports must be filed for all Trade Reporting Accounts.

Quarterly trading reports must be filed within 30 days after the end of each quarter. Employees must confirm each

non-Exempted Trade made over the quarter including associated account, instrument identifier, quantity and price. Even if no transactions are required to be reported, each employee must submit such a report

certifying that all transactions have been reported. The confirmation of such initial and holding reports shall include a declaration that such reports also include transactions of any other related Access Persons.

Please note that the above deadlines are statutory. Non-compliance will expose CFM to regulatory sanctions.

All reports will be reviewed by the Regulatory team promptly after the end of each reporting period. They will reconcile quarterly reports against pre-clearances filed over the quarter and investigate any discrepancies, assess whether employees followed internal procedure, whether any restrictions were in effect at the time of trade, whether the employee is

receiving terms more favourable as those received by any CFM Client trading in the same instruments, and periodically analyse the employee’s trading for patterns that may indicate abuse.

d. Confidentiality

The Compliance

team will maintain records in a manner to safeguard their confidentiality. Each employee’s records will be accessible only to the employee, the Compliance team, senior officers and appropriate IT and human resources personnel. Employees should

understand that these records may also be made available to regulatory and other governmental authorities and may have to be produced in connection with legal proceedings.

e. Special provisions for certain teams

Due to the heightened risk for receiving non-public information in their activities, the following additional rules apply to staff

from the Semi-Systematic Research team (“SSR staff”) and Equity Capital Market team (“ECM staff”) :

| u |

Any UK and US-based SSR Staff and ECM staff may only keep personal trading

accounts with brokers that provide feeds to CFM through MCO (the list can be obtained from the Regulatory team). |

9

| u |

SSR Staff and ECM staff may not make any single-name personal trades (including stocks, bonds, derivatives). Funds,

ETFs, and cryptocurrencies can still be traded whilst respecting the other conditions laid out above. |

3. Gifts and entertainment

The giving or receiving of gifts or other items of value to or from persons doing business or seeking to do business with CFM could call into question the independence of

its judgment as a fiduciary of its Clients, or be seen as attempted bribery. If CFM and/or an employee were found to be acting in a position of undisclosed conflict of interest, it could be sanctioned under various applicable regulations.

In any instance, the giving or receipt of gifts must not be made with the intention of influencing a third party to obtain or retain business or a business advantage, or

in explicit or implicit exchange for favours or benefits. Gifts should not be offered to or accepted from, government officials or representatives or politicians or political parties, without the prior approval of CFM’s Board.

Prior to the start of their internship, interns declare in writing that they will refrain from offering or receiving gifts or entertainment to business contacts during

their stay at CFM.

a. Quick reference table

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Type of

non-cash compensation

(offered or received) |

|

CFM employee is a

Registered

Representative |

|

Must declare if

above |

|

Limit per occurrence

without pre-clearance |

|

Aggregate limit over

12 months |

|

|

|

|

|

| Gift |

|

Yes |

|

$0 |

|

$100 |

|

$100 |

|

|

|

|

|

| Gift |

|

No |

|

$0 |

|

$150 |

|

$150 |

|

|

|

|

|

| Gift – cash or equivalent |

|

Any |

|

Not allowed |

|

Not allowed |

|

Not allowed |

|

|

|

|

|

| Entertainment – any |

|

Yes |

|

$0 |

|

$275 |

|

- |

|

|

|

|

|

| Entertainment – reasonable meal or drinks when below conditions are met |

|

No |

|

$75 |

|

$275 |

|

- |

|

|

|

|

|

| Entertainment – sporting and cultural events |

|

Any |

|

$0 |

|

$0 |

|

- |

|

|

|

|

|

| Entertainment – all other |

|

No |

|

$0 |

|

$275 |

|

- |

Entertainment includes an occasional meal, a ticket to a sporting event or the theatre, or comparable entertainment that is neither so

frequent nor so extensive as to raise any question of propriety and is not preconditioned on achievement of a sales target or other incentives. If a representative from the offering party is not present, then it is a gift.

When giving or receiving gifts and entertainment, Registered Representatives must always declare the following details: the date and amount, the type of gift or

entertainment, information about the individuals involved, a description of the gift and its exact location.

If an employee is allowed to bring a plus one, the same

rules that apply to the employee will also apply to the guest. This gift or entertainment should be declared and pre-cleared, if needed.

10

b. Receiving gifts and entertainment

On occasion, because of an employee’s position with the Firm, the employee may be offered, or may receive, gifts or other forms of

non-cash compensation from Clients, brokers, vendors, or other persons that do business, or seek to do business with the Firm.

Extraordinary or extravagant gifts or entertainment (i.e., that have an aggregate value above the limit per occurrence or the aggregate limit over 12 months defined

above) are not permissible and must be declined or returned, absent prior approval by the Regulatory team. Cash gifts can never be accepted.

Other gifts and

entertainment at which both the employee and the giver are present and promotional items (e.g., pens, mugs) may be accepted, though entertainment other than reasonable food and drinks – such as sporting and cultural events of any value

– require the prior approval of the employee’s manager (to be provided by email to the Regulatory team). All sporting and cultural events must be pre-cleared before the event date and

declared, regardless of their value. Gifts should be received at one of CFM’s offices and may not be sent directly to an employee’s home.

Employees must

in no circumstances solicit gifts, entertainment or other gratuities.

c. Offering gifts and entertainment

General rules

Offering gifts and entertainment to

persons CFM does business with, or seeks to do business with, follows similar rules: extraordinary or extravagant gifts or entertainment (i.e., that have an aggregate value above the limit per occurrence or the aggregate limit over 12 months defined

above) may not be offered, absent prior approval by the Regulatory team. Cash gifts can never be offered either. Gifts of lower value and promotional items may be offered provided they are given in CFM’s name and given in person or sent to the

recipient’s office. As above, offers of entertainment other than reasonable food and drinks – such as sporting and cultural events of any value – require the prior approval of the employee’s manager (to be provided by email

to the Regulatory team).

High-risk recipients

Under various anti-bribery rules, CFM will face increased scrutiny when offering gifts to certain types of recipients. In particular, providing gifts and entertainment to

non-US officials may violate the U.S. Foreign Corrupt Practices Act (“FCPA”). CFM could face potentially serious civil and/or criminal penalties for offering, promising, paying, or authorising any

bribe, kickback or similar improper payment to any non-US official, political party or official or candidate for political office in order to assist CFM in obtaining, retaining, or directing business,

including investments in the funds managed by CFM. Under the FCPA, a non-US official includes any officer or employee of any government department, agency or instrumentality, including employees of

government-owned business entities and sovereign wealth funds. As such, the following persons – whether US or non-US – are considered to be high-risk recipients:

| u |

Elected officials and candidates to office, where such office could influence investments in CFM funds or mandates;

|

| u |

ERISA clients and their staff; and |

| u |

Civil servants and officials whose position and/or seniority place them in a position to influence investments in CFM

funds or mandates, including but not limited to employees and agents of pension funds, sovereign wealth funds, or large government-owned or government-controlled institutional investors. |

Employees should be particularly mindful when offering gifts to the above persons, and seek guidance if necessary from the Regulatory team.

Conferences and events

In certain circumstances an

employee may wish to set up an event where multiple investors, prospective investors or third parties would be invited. Such events may offer hospitalities to invitees such as food, beverages, promotional merchandise, etc. Such events should be

reported within Dynamo including:

11

| u |

Organiser (either a CFM individual or team); |

| u |

Location name and type (e.g. hotel, restaurant, conference hall, etc.); |

| u |

Invited organisations along with their expected number of attendees; and |

| u |

Budget per attendee as broken down in the “Budget” tab (gifts, entertainment including food & drinks,

cost of speakers, other organizational costs). |

Should the gift budget per attendee be over $100, or the entertainment budget per attendee over

$275, the Regulatory team should confirm its approval in writing before the event can take place.

d. Declaring gifts and

entertainment

All gifts and entertainment given or received must be declared using the declaration form on CFM’s intranet (LINK). By exception to this rule, reasonable meals or drinks (offered or received) do not need to be declared (and, for the avoidance of doubt,

will not count against the aggregate limit over 12 months) where the following conditions are met:

| u |

You are not a Registered Representative of a U.S. broker-dealer; |

| u |

They take place in the ordinary course of business; |

| u |

Both the offering party and the recipient are physically present; |

| u |

The recipient is not a High-Risk Recipient as described above; and |

| u |

The value per person is under US$75. |

Where the value of a gift or entertainment is not known precisely, a reasonable, good-faith estimate must be given.

If the aggregate value of gifts received from (or offered to) a single giver over 12 months exceeds US$150 (US$100 if you are a Registered Representative of a U.S.

broker-dealer), the Regulatory team will notify the employee that he should no longer accept (or offer) gifts from this giver, and indicate the date at which this suspension will be lifted. Only the CCO may approve an exception to this rule in

exceptional cases; such approval will be documented in writing.

By exception to the above paragraph, de minimis and promotional items of nominal value (i.e. under

$50) that display CFM’s logo do not count toward the US$150/100 per person above gift limit and are not subject to reporting. However, multiple nominal or promotional items to/from the same individual over the course of 12 months where the

combined value exceeds $50 must be reported and are considered a gift subject to the $150/100 limit.

e. Raising a concern

CFM has a zero-tolerance approach to bribery and corruption. Employees must raise a concern if they are offered a

bribe by a third party, asked to make one or have a suspicion of malpractice at the earliest possible stage to the CCO.

Some red flags to look out for are:

| u |

the third party has a reputation of engaging in improper business practices; |

| u |

the third party insists on receiving a commission or fee payment before committing to sign a contract;

|

| u |

the third party requests payment in cash or refuses to sign up a formal commission or fee agreement;

|

| u |

the third party requests that payment is made to a country or geographic location different from where the third party

resides or conducts business; |

| u |

the third party requests an unexpected additional fee to facilitate a service; |

| u |

the third party offers an unusually generous gift or lavish hospitality. |

Any concerns raised will remain confidential. The CCO will analyse such report and decide whether it is appropriate to contact relevant authorities (e.g. UK Serious Fraud

Office, French Agence Française Anti-corruption).

12

4. Outside business activities

The Conflicts of interest and reputational business considerations may arise where employees have interests outside of

CFM’s business hours and/or that are unconnected to the individual’s role within CFM. Employees must seek prior approval from the Regulatory team before

engaging in any outside business activities, and in particular:

| u |

being engaged in any other material business; |

| u |

being an officer of or employed or compensated by any other person for business-related activities; |

| u |

serving as general partner, managing member or in a similar capacity with partnerships, limited liability companies or

private funds other than those managed by CFM or its affiliates; |

| u |

having a majority ownership in any non-CFM business enterprise;

|

| u |

engaging in personal investment transactions to an extent that diverts an employee’s attention from or impairs the

performance of his or her duties in relation to the business of CFM and its Clients; |

| u |

having any direct or indirect financial interest or investment in any dealer, broker or other current or prospective

supplier of goods or services to CFM (other than ownership of publicly traded securities) from which the employee might benefit or appear to benefit materially; |

| u |

serving on the board of directors or trustees (or in any similar capacity) of another company, including not-for-profit corporations and charities. Authorisation for board service will normally require that CFM not hold or purchase any securities of the company on whose board the

employee sits; or |

| u |

providing investment advice to entities/individuals that are not CFM Clients. |

a. Prior approval

Upon joining

and before undertaking any outside business activity, the employee must provide to the Regulatory team certain information regarding all aspects of the proposed activity. This is carried out using the

pre-clearance form available on CFM’s intranet (LINK). In deciding whether to approve an

outside business activity, the Regulatory team will consider the materiality of the potential conflicts and whether they can be effectively managed by CFM. The Regulatory team will also generally seek approval from the employee’s line manager.

When the Regulatory team approves an outside business activity, it will make the individual in question aware of any arrangements that are to be implemented in order to manage the conflicts identified. The Regulatory team will inform the Board of

CFM SA of any new approved outside business activity.

The termination of any outside business activity must be reported promptly on the same intranet screen.

b. Annual reporting

All

employees will also be required to update the Regulatory team within 30 days of every year-end of his or her outside business activities using the form available on CFM’s intranet (LINK).

c.

Restrictions on activities

With respect to any outside activities engaged in by an employee, the following restrictions shall be in effect:

| (i) |

the employee is generally prohibited from implying that he or she is acting on behalf of, or as a representative of, CFM;

|

| (ii) |

the employee is prohibited from using CFM’s offices, equipment or stationery for any purpose not directly related to

CFM’s business, unless such employee has obtained prior approval from the CCO; and |

| (iii) |

if the activity was required to be and has been approved by the Regulatory team, the employee must report any material

change with respect to such activity. |

d. Family and other personal relationships

Conflicts of interest may also arise through an employee’s immediate family (including parents, children, spouses, civil partners e.g. PACS). For instance, an

employee’s spouse could be employed by a competitor of CFM, or a decision-maker of a client, counterparty or vendor of CFM. In such instances, they must file a pre-clearance form as described above.

While of

13

course CFM is unable to disapprove the activity of a non-employee, this will

serve as notification to the Regulatory team, which will then be able to examine and escalate the potential conflict as necessary.

5. U.S Political contributions; Pay-to Play

The SEC has stated that investment advisers who seek to influence the award of advisory contracts by public entities by making political contributions to U.S. public

officials may cause such officials to compromise their fiduciary duty to such entities. The SEC’s Pay-to-Play Rule addresses these practices. The Pay-to-Play Rule imposes a two-year “time out” on receiving compensation for providing advisory services to a government

entity, if (i) an adviser (or its “Covered Associates” as defined below) makes a contribution to an elected official (or candidate) of the government entity and (ii) the elected office held (or campaigned for) may directly or

indirectly influence the hiring of the adviser. A “government entity” for the purpose of the Pay-to-Play Rule only includes U.S. state or local governments,

their agencies and instrumentalities, public pension plans and other types of collective government funds.

a. Contributions

by CFM

CFM does not intend to make any contributions to U.S. political parties or organisations (including Political Action Committees). No donation must

be offered or made in CFM’s name without the prior approval of the Firm’s Board. Additionally, any donation must comply with the limits below.

b. Personal contributions

Covered Associates

For the purposes of the Pay-to-Play

rule, a Covered Associate includes:

| u |

any general partner, managing member, executive officer, or other individual with a similar status or function;

|

| u |

any employee who solicits a government entity for the adviser and any person who supervises, directly or indirectly, such

employee; and |

| u |

any PAC controlled by the adviser or by any of its covered associates. |

CFM considers CFM NA and CFMI Directors, Principals, and every employee of the Investor Relations team based in CFM’s NYC office to be Covered Associates.

Rules

Covered Associates are generally prohibited

from giving or offering gifts, entertainment, hospitality or any other thing of value (including paying for entertainment or travel-related expenses) to U.S. public or government officials, employees of government-controlled business, political

parties, public organisations or entities (including public pension plans and sovereign wealth funds, as well as their employees, representatives or any third party associated with their investment process or investment due diligence) or candidates

for political office.

A de minimis exemption may be granted where a Covered Associates wishes to make a personal contribution not exceeding US$150 per election cycle

per candidate to public office, per political party and per political action committee. This threshold may be raised to $350 if the Covered Associates in question is entitled to vote in said election.

Exceeding these thresholds could prevent CFM from providing advisory or management services to public organisations linked to the recipient of the contribution for two

years.

Declaring political contributions

Prior approval for all political contributions must be requested from the Regulatory team by using the following link: LINK.

Each new Covered Associates must report to the

CCO all contributions to any official or candidate for office in a national or local government unit (or a person that is running for national or local office) made in the two years prior to his or her hire date.

14

Monitoring

The CCO will monitor subscriptions and new managed accounts to identify any governmental units, including pensions and other benefit plans of such units, which become

clients of CFM or investors in its funds. CFM will compare such list to reports of contributions by Covered Associates to determine whether CFM will be permitted to provide services to such clients or investors, and if contributions have been made,

whether corrective action, including seeking a return of the contribution, should be taken.

6. Complaints

Any

statement alleging any specific, inappropriate conduct on the part of the Firm or one of its Employees that states or could support a claim of a violation of law, duty or contract constitutes a complaint. Clients and investors can file complaints

free of charge with CFM. Each complaint shall be properly recorded by the CCO, acknowledged within 10 business days, and responded to within two months. Complaints made by investors in EU-domiciled funds can

be made, and will be responded to, in one of the official languages of the Member State in which the fund is sold. Information on a management company’s policy on complaints handling shall be made available free of charge to investors upon

request.

Any employee receiving a complaint, whether oral or written, from any Client or from any investor in a private fund must promptly bring such complaint to

the attention of the CCO Employees should not attempt to respond to or resolve any complaint by themselves. All responses to such complaints must be handled by the CCO except that complaints related to the CCO should be brought to the attention of

the CEO of CFM SA. The CCO will maintain records of any complaints and accompanying responses for at least five years.

CFM does not generally admit retail investors

and does not expect to have any MiFID-eligible complaints.

a. Mediation

Where a Client or investor deems CFM’s response unsatisfactory, they can reach out free of charge to their relevant local complaints authority, including:

15

|

| France

Médiateur de l’Autorité des Marchés Financiers

17 place de la Bourse, 75082 Paris Cedex 2 https://www.amf-france.org/Le-mediateur-de-l-AMF/Presentation

UK

The Financial Ombudsman Service

Exchange Tower, London E14 9SR

complaint.info@financial-ombudsman.org.uk +800 023 4567 +44 20 7964 0500 (call from outside the UK

http://www.financial-ombudsman.org.uk/

Canada

Ombudsman for Banking Services and Investments (OBSI) 20 Queen Street West, Suite 2400 P.O. Box 8

Toronto, ON M5H 3R3

ombudsman@obsi.ca +1 888 451-4519 https://www.obsi.ca/en/

USA

Securities and Exchange Commission

Office of Investor Education and Advocacy 100 F Street, N.E. Washington, DC 20549-0213

+1 202-551-6500

Fax: +1 202 772-9295

https://www.sec.gov/oiea/Complaint.htm |

7. Whistleblowing

CFM is committed to providing a workplace conducive to open discussion of the CFM’s business practices and is committed to complying with the laws and regulations

to which it and its employees, contractors and interns are subject. All employees, contractors and interns have a responsibility to promptly report internally any suspected misconduct, breach of regulatory rules, illegal activities or fraud,

including any questionable accounting, internal accounting controls and auditing matters, or other violations of laws or of internal procedures (together, a “Reportable Concern”).

It is CFM’s policy to comply with all applicable laws that protect its employees, contractors and interns against unlawful discrimination or retaliation as a result

of their lawfully reporting information regarding Reportable Concerns.

a. Internal disclosure

Employees, contractors and interns must report any Reportable Concern promptly to the CCO. If the CCO is involved in the Reportable Concern or is unreachable, employees

may report them to the CEO of CFM SA. In lieu of speaking directly to the CCO or CEO of CFM SA, an employee may provide – anonymously or not – a detailed complaint to the CCO or the CEO of CFM SA in writing or orally. Any such reports

will be treated confidentially to the extent practicable or permitted by law. The CCO (or the CEO of CFM SA) will investigate any Reportable Concern, report to management on the factual findings and recommend sanctions, where appropriate. The CCO

(or the CEO of CFM SA) will acknowledge the receipt of the report to the reporting person within 7 days of the disclosure, diligently follow up and provide feedback in a reasonable

16

timeframe not exceeding 3 months from the acknowledgement of receipt. Employees, contractors and interns are required to

cooperate in any investigation. The CCO will maintain records of Reportable Concerns, tracking their receipt, investigation and resolution.

Concerns relating to

either suspected money laundering or bribery should be referred directly to the relevant Money Laundering Reporting Officer (as named in CFM’s group Anti-Money Laundering and Terrorist Financing Policy).

b. External disclosure

Reporting

through internal reporting channels before reporting to external channels is encouraged. However, where circumstances warrant, a disclosure may be made directly to the relevant authorities.

If a situation presents a clear and imminent danger to the general interest, or if even an external disclosure to a below channel creates a risk of retaliation against

the whistle-blower, of if a previous Reportable Concern was not dealt with within 3 months of the disclosure, then a whistle-blower may make a public disclosure.

|

| France

Médiateur de l’Autorité des

Marchés Financiers 17 place de la Bourse, 75082 Paris Cedex 2

https://www.amf-france.org/Le-mediateur-de-l-AMF/Presentation

UK

Intelligence Department (Ref PIDA)

The Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN

whistle@fca.org.uk

+44 20 7066 9200

Canada

The Financial Consumer Agency of Canada (FCAC)

https://fcpc-prdint01-whistleblower-wap.fcac-acfc.gc.ca/?GoCTemplateCulture=en-CA

USA

Securities and Exchange Commission

Office of the Whistleblower

100 F Street, N.E.

Washington, DC 20549

Fax: +1 202 813-9322

https://www.sec.gov/whistleblower/submit-a-tip

|

c. Protection of employees; prohibition against retaliation

CFM will not enter into agreements (including offer letters, confidentiality agreements, severance agreements and employment contracts) with its employees, former

employees and interns or with service providers that contain provisions that are intended to discourage an individual from lawfully reporting Reportable Concerns.

Retaliation against an individual who reports a Reportable Concern – as well as any third party providing him or her support and assistance, close associates,

family and colleagues – is prohibited and will be dealt with as a separate violation of policy. Individuals who believe they have been subject to retaliation should contact the CCO (or the CEO of CFM SA). Information that may lead to the

identification of the whistle-blower can only be divulged with his or her consent, except to the relevant authorities (in which case the whistle-blower will be informed).

17

8. Mandatory holidays

It is CFM’s internal policy that all employees must, in every full calendar year, take at least 10 consecutive business days of vacation.

9. Bad actor rule

CFM frequently relies on Rule 506 of Regulation D for the offering of its products in the USA. The SEC’s Bad Actor Rule prevents CFM from doing so where a Covered

Person (as defined below) is subject to a disqualifying event – a “bad act” (also defined below).

a.

Covered persons

Covered Persons include the following:

| u |

Investment managers of private fund issuers; |

| u |

The directors, executive officers, other officers participating in the offering, and general partners and managing members

of such investment managers; |

| u |

The directors and executive officers of such general partners and managing members and their other officers participating

in the offering; |

| u |

The issuer and any predecessor of the issuer or affiliated issuer; |

| u |

The directors, executive officers, other officers participating in the offering, and general partners or managing members

of the issuer; |

| u |

Any 20% beneficial owner of an issuer’s outstanding voting equity securities, calculated on the basis of voting

power; |

| u |

Persons compensated for soliciting investors as well as the general partners, directors, executive officers, other

officers participating in the offering and managing members of any compensated solicitor. |

CFM has determined that its Covered Persons are:

| u |

CFM SA, CFM LLP and CFM NA; |

| u |

Members of the Board of Directors of the above, as well as of any private fund managed by CFM; |

| u |

US-based members of the IR team; |

Since private funds managed or advised by CFM only issue non-voting shares to their investors, CFM does not anticipate that any

investor will become a Covered Person.

b. Bad Acts

Under the final rule, disqualifying events include:

| u |

Certain criminal convictions |

| u |

Certain court injunctions and restraining orders |

| u |

Final orders of certain state and federal regulators |

| u |

Certain SEC disciplinary orders |

| u |

Certain SEC cease-and-desist orders

|

| u |

SEC stop orders and orders suspending the Regulation A exemption |

| u |

Suspension or expulsion from membership in a self-regulatory organisation (SRO), such as FINRA, or from association with

an SRO member |

| u |

U.S. Postal Service false representation orders |

Many disqualifying events include a look-back period (for example, a court injunction that was issued within the last five years or a regulatory order that was issued

within the last ten years). Events that occurred before 23 September 2013 (entry in force of the rule) are not disqualifying but must be disclosed in writing to investors prior to any Regulation D offering. In

18

certain cases the SEC may grant a waiver of disqualification where it deems that it is not necessary, under the

circumstances, that the registration exemption be denied.

c. Background checks

CFM performs background checks prior to hiring any person in its US office. These background checks may be renewed periodically. In addition, every employee is required

to complete the SEC questionnaire upon joining and annually (as detailed in the Acknowledgements section above), which covers the above disqualifying events.

The

fund administrator identifies investors owning over 20% of the interests in a CFM private fund. CFM employees who are also identified as holding over 20% of the interests are subject to sanctions checks. Sanctions checks are performed using

WorldCheck One as detailed in CFM’s separate Anti-Money Laundering and Terrorist Financing Policy.

10. Other Policies

Certain

other policies also relate to employee obligations and should be read in conjunction with this Code of Ethics.

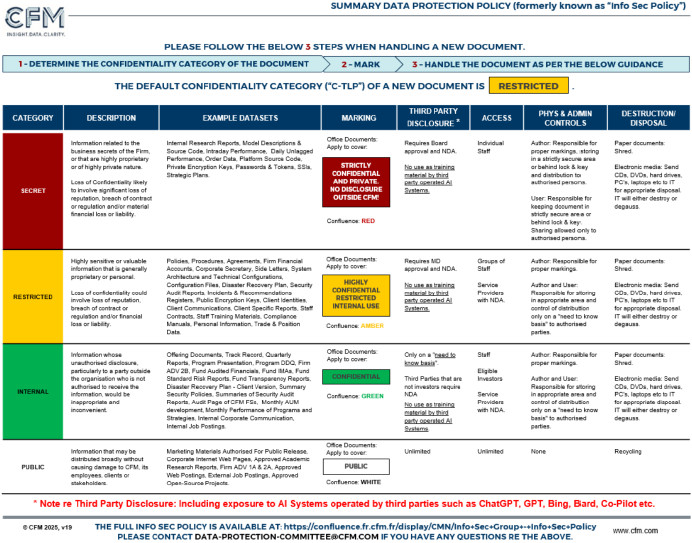

a. Data

protection

Due to the nature of its business as well as applicable laws & regulations, it is important to note that CFM and consequently you as

an employee are required to hold certain information confidential.

The confidentiality requirement restricts how CFM employees may access information as well as

treat information that is accessible. The complete confidentiality guidelines are documented in the firm’s Information Security (“Info Sec”) Policy that can be accessed here: LINK..

The Info Sec Policy classifies information in

four categories (White (Public/Open), Green (Confidential/Internal), Amber (Restricted / Highly Confidential) and Red (Strictly Confidential / Secret)) depending on the sensitivity of the information. The Summary Info Sec Policy (below) includes the

key guidelines for confidentiality classification and handling many types of generally used documents.

19

Confidential information is to be held securely and shall only be disclosed to a third-party in line with the Info Sec Policy. If an

employee is in doubt in relation to the confidentiality of a certain piece of information and/or whether such information can be communicated to a third party, they should contact their manager or the Info Sec group at infosec@cfm.fr to discuss the

matter. More generally any information related to CFM shall only be communicated to third parties on a “need to know” basis.

Employees may produce

confidential information. Any information including files, documents, etc. should be marked systematically with the appropriate C-TLP badge as per the Info Sec Policy. If an employee needs to communicate

information on CFM to a third party, the Investor Relations department maintains a number of standard documents concerning CFM’s business, trading strategies, funds, performance etc. They may be in a position to assist on standard information

that may be shown to third parties.

As a part of its business, CFM may enter into confidentiality agreements, non-disclosure

agreements or like (collectively “NDAs”) with third parties. The firm may be comfortable to share certain confidential information with a third-party under an NDA. When CFM is the receiving party the applicable NDA may include additional

instructions on holding the information received from a third party on a confidential basis and may require CFM to destroy such confidential information in certain situations. Any such confidential information in relation to third parties that has

been received under an NDA should be held separately from that of other information should be marked again as confidential.

Any contact with the press should be

directed to the IR-Client Services team, who will deal with press queries separately. No employee should answer any questions from journalists directly.

20

Employees should show caution when participating in any conference, seminar, publication or like. Although they may be

tempted to impress peers, confidential information remains confidential. Any presentations or other hand-outs used in conferences or seminars must be validated by the Regulatory team prior to use. When publishing scientific or other articles, such

articles are to be pre-validated by the Regulatory team.

Employees should also be careful when discussing the business of CFM

in a public area. No confidential information may be divulged as the identity of the people in the vicinity may not be known for certain. Similarly, employees should be careful when using of laptops and/or mobile telephones in a public area.

Any known loss of confidential information including documents, source codes, applications or a PC, laptop or mobile telephone must be reported immediately to management.

b. Generative AI

CFM’s

Generative AI policy was drafted in accordance with the key ethical and fiduciary principles that CFM seeks to follow. It details which Generative AI systems are approved for use for CFM business and under which conditions. It also outlines certain

transparency and record-keeping requirements. The Generative AI policy can be found HERE.

c. Social Media

The Social Media

policy presents rules on the content that CFM staff can share over social media, and under which conditions. The Social Media policy can be found HERE.

d. Training

The Training Policy lists all the different mandatory compliance training provided to CFM staff. Trainings must generally be completed within 30 days. The Training Policy

can be found HERE.

11. Escalation and Breaches

a. Escalation

For periodic

acknowledgements and trainings, the Regulatory team will monitor the progress of concerned staff and apply the following escalation process:

| u |

One week before the deadline, they will send individual emails to each person with outstanding tasks, copying their

line manager; |

| u |

One day before the deadline, they will send individual emails to each person with outstanding tasks, copying their

line manager and Managing Director; |

| u |

One day after the deadline, they will send individual emails to each person with outstanding tasks, copying their

line manager, Managing Director and the CEO. They will also log a breach as detailed below. |

b. Breaches

In the event that the Regulatory team detects a potential breach of the above rules, it will investigate and seek to confirm whether a breach occurred and

why. If confirmed, they will log it in the CCOEB Jira project including date of breach, nature, concerned employee, and any other relevant information. CCOEB activity will be reported and discussed in the quarterly Compliance Committee.

If an employee’s contract is temporarily suspended (e.g. sick leave, maternity leave, garden leave, sabbatical), their obligations under this Code of Ethics are

delayed until their return.

21