UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

________________________________________________

FORM 10-Q

________________________________________________

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2026

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ______ to ______

Commission File Number: 001-38636

________________________________________________

(Exact Name of Registrant as Specified in its Charter)

________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| and | |||||

| (Address of principal executive offices) (Zip Code) | |||||

+ | ||

| and | ||

+ | ||

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

As of April 24, 2026, the registrant had 187,188,503 shares of Common Stock, $0.001 par value per share, outstanding.

Table of Contents

| Page | ||||||||

1

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements

GARRETT MOTION INC.

CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS

(Unaudited)

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions, except per share amounts) | |||||||||||

Net sales (Note 3) | $ | $ | |||||||||

| Cost of goods sold | |||||||||||

| Gross profit | |||||||||||

| Selling, general and administrative expenses | |||||||||||

| Other expense, net | |||||||||||

| Interest expense | |||||||||||

| Non-operating income, net | ( | ( | |||||||||

| Income before taxes | |||||||||||

Tax expense (Note 5) | |||||||||||

| Net income | $ | $ | |||||||||

Earnings per common share (Note 19) | |||||||||||

| Basic | $ | $ | |||||||||

| Diluted | |||||||||||

| Weighted average common shares outstanding | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

The Notes to the Consolidated Interim Financial Statements are an integral part of this statement.

2

GARRETT MOTION INC.

CONSOLIDATED INTERIM STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Net income | $ | $ | |||||||||

| Foreign exchange translation adjustment | ( | ( | |||||||||

Changes in fair value of effective cash flow hedges, net of tax (Note 17) | |||||||||||

Changes in fair value of net investment hedges, net of tax (Note 17) | ( | ||||||||||

| Total other comprehensive income (loss), net of tax | ( | ||||||||||

| Comprehensive income | $ | $ | |||||||||

The Notes to the Consolidated Interim Financial Statements are an integral part of this statement.

3

GARRETT MOTION INC.

CONSOLIDATED INTERIM BALANCE SHEETS

(Unaudited)

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

Accounts, notes and other receivables – net (Note 6) | |||||||||||

Inventories – net (Note 8) | |||||||||||

Other current assets (Note 9) | |||||||||||

| Total current assets | |||||||||||

| Investments and long-term receivables | |||||||||||

| Property, plant and equipment – net | |||||||||||

| Goodwill | |||||||||||

| Deferred income taxes | |||||||||||

Other assets (Note 10) | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

Current maturities of long-term debt (Note 15) | |||||||||||

Accrued liabilities (Note 12) | |||||||||||

| Total current liabilities | |||||||||||

Long-term debt (Note 15) | |||||||||||

| Deferred income taxes | |||||||||||

Other liabilities (Note 13) | |||||||||||

| Total liabilities | $ | $ | |||||||||

COMMITMENTS AND CONTINGENCIES (Note 20) | |||||||||||

| EQUITY (DEFICIT) | |||||||||||

Common Stock, par value $ | |||||||||||

| Additional paid–in capital | |||||||||||

Retained deficit | ( | ( | |||||||||

Accumulated other comprehensive loss (Note 18) | ( | ( | |||||||||

Treasury Stock, at cost; | ( | ( | |||||||||

| Total deficit | ( | ( | |||||||||

| Total liabilities and deficit | $ | $ | |||||||||

The Notes to the Consolidated Interim Financial Statements are an integral part of this statement.

4

GARRETT MOTION INC.

CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

(Unaudited)

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Cash flows from operating activities: | |||||||||||

Net income | $ | $ | |||||||||

Adjustments to reconcile net income to net cash provided by operating activities | |||||||||||

| Deferred income taxes | |||||||||||

| Depreciation | |||||||||||

| Amortization of deferred issuance costs | |||||||||||

| Foreign exchange loss (gain) | ( | ||||||||||

| Stock compensation expense | |||||||||||

| Unrealized (gain) loss on derivatives | ( | ||||||||||

| Other | |||||||||||

| Changes in assets and liabilities: | |||||||||||

| Accounts, notes and other receivables | ( | ( | |||||||||

| Inventories | |||||||||||

| Other assets | ( | ( | |||||||||

| Accounts payable | ( | ||||||||||

| Accrued liabilities | ( | ||||||||||

| Other liabilities | ( | ||||||||||

Net cash provided by operating activities | $ | $ | |||||||||

| Cash flows from investing activities: | |||||||||||

| Expenditures for property, plant and equipment | ( | ( | |||||||||

Proceeds from cross-currency swap contracts | |||||||||||

Net cash used for investing activities | $ | ( | $ | ( | |||||||

| Cash flows from financing activities: | |||||||||||

| Proceeds from issuance of long-term debt, net of debt financing costs | |||||||||||

| Bank overdrafts | |||||||||||

| Payments of long-term debt | ( | ( | |||||||||

| Repurchases of Common Stock | ( | ( | |||||||||

| Dividend payments | ( | ( | |||||||||

| Payments for debt and revolving facility financing costs | ( | ||||||||||

| Other | ( | ||||||||||

Net cash used for financing activities | $ | ( | $ | ( | |||||||

| Effect of foreign exchange rate changes on cash, cash equivalents and restricted cash | ( | ||||||||||

Net (decrease) increase in cash, cash equivalents and restricted cash | ( | ||||||||||

| Cash, cash equivalents and restricted cash at beginning of the period | |||||||||||

| Cash, cash equivalents and restricted cash at end of the period | $ | $ | |||||||||

| Supplemental cash flow disclosure: | |||||||||||

| Income taxes paid (net of refunds) | $ | $ | |||||||||

| Interest paid | |||||||||||

| Supplemental disclosure of non-cash investing activities: | |||||||||||

| Expenditures for property, plant and equipment in accounts payable | |||||||||||

The Notes to the Consolidated Interim Financial Statements are an integral part of this statement

5

GARRETT MOTION INC.

CONSOLIDATED INTERIM STATEMENTS OF EQUITY (DEFICIT)

(Unaudited)

| Common Stock | Treasury Stock | Additional Paid-in Capital | Retained Deficit | Accumulated Other Comprehensive (Loss) / Income | Total Deficit | ||||||||||||||||||||||||||||||||||||||||||

Shares (1) | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||||||||||||||||||||||||||

Balance at December 31, 2025 | $ | $ | ( | $ | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Share repurchases | — | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||

| Excise tax on share repurchases | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||

| Shares issued under stock plan, net of shares withheld for employee taxes | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Dividends | — | — | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

Balance at March 31, 2026 | $ | $ | ( | $ | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||||||||

| Common Stock | Treasury Stock | Additional Paid-in Capital | Retained Deficit | Accumulated Other Comprehensive Income / (Loss) | Total Deficit | ||||||||||||||||||||||||||||||||||||||||||

Shares (1) | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||||||||||||||||||||||||||

Balance at December 31, 2024 | $ | $ | ( | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

| Share repurchases | — | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||

| Excise tax on share repurchases | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||

| Shares issued under stock plan, net of shares withheld for employee taxes | — | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||

Balance at March 31, 2025 | $ | $ | ( | $ | $ | ( | $ | $ | ( | ||||||||||||||||||||||||||||||||||||||

1) Common shares issued less treasury shares equals common shares outstanding

The Notes to the Consolidated Interim Financial Statements are an integral part of this statement.

6

GARRETT MOTION INC.

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

(Dollars in millions, except per share amounts)

Note 1. Background and Basis of Presentation

Background

Garrett Motion Inc. (the “Company” or “Garrett”) is a cutting-edge technology leader delivering differentiated solutions for emission reduction and energy efficiency. We design, manufacture, and sell highly engineered turbocharging, air and fluid compression, and high-speed electric motor technologies to original equipment manufacturers (“OEMs”) and independent aftermarket distributors in the mobility and industrial fields. We have significant expertise in delivering highly engineered products at scale for internal combustion engines using gasoline, diesel, natural gas, and hydrogen, as well as for zero-emission vehicles. Our products are key enablers for fuel economy, energy efficiency, thermal management, and compliance with greenhouse gas and other emission-reduction targets.

Basis of Presentation

The accompanying unaudited Consolidated Interim Financial Statements have been prepared in accordance with the rules and regulations of the Securities and Exchange Commission ("SEC") applicable to interim financial statements. While these statements reflect all normal recurring adjustments that are, in the opinion of management, necessary for fair presentation of the results of the interim period, they do not include all of the information and footnotes required by United States generally accepted accounting principles (“GAAP”) for complete financial statements. The unaudited Consolidated Interim Financial Statements should therefore be read in conjunction with the Consolidated Financial Statements and accompanying notes for the year ended December 31, 2025 included in our Annual Report on Form 10-K, as filed with the SEC on February 19, 2026 (our “2025 Form 10-K”). The results of operations and cash flows for the three months ended March 31, 2026 should not necessarily be taken as indicative of the entire year. All amounts presented are in millions, except per share amounts.

We evaluate segment reporting in accordance with ASC 280, Segment Reporting. We concluded that Garrett operates in a single operating segment and a single reportable segment based on the operating results available and evaluated regularly by the chief operating decision maker (“CODM”), which is our Chief Executive Officer, to make decisions about resource allocation and performance assessment. The CODM makes operational performance assessments and resource allocation decisions on a consolidated basis, inclusive of all of the Company’s products across channels and geographies.

The preparation of the financial statements in conformity with GAAP requires management to make estimates that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Management bases these estimates on assumptions that it believes to be reasonable under the circumstances. Actual results could differ from the original estimates, requiring adjustments to these balances in future periods.

Note 2. Summary of Significant Accounting Policies

The accounting policies of the Company are set forth in Note 2 to the Consolidated Financial Statements for the year ended December 31, 2025 included in our 2025 Form 10-K.

Accounting Standards Issued But Not Yet Adopted

In November 2024, the FASB issued ASU 2024-03, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses. The amendments in this update require disclosure of specified information about certain costs and expenses. In January 2025, the FASB issued ASU 2025-01, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40): Clarifying the Effective Date. The guidance, as clarified by ASU 2025-01, is effective for fiscal years beginning after December 15, 2026 on a prospective basis, with early adoption permitted. The Company is currently evaluating the guidance to determine the impact on its disclosures.

In September 2025, FASB issued ASU 2025-06, Intangibles—Goodwill and Other—Internal Use Software (Subtopic 350-40): Targeted Improvements to the Accounting for Internal-Use Software. The amendments revise the capitalization

7

criteria for internal-use software costs and eliminate stage-based development guidance. The update is effective for fiscal years beginning after December 15, 2027, with early adoption permitted. The Company is currently evaluating the guidance to determine the impact on its accounting policies and disclosures.

In December 2025, the FASB issued ASU 2025-10, Government Grants (Topic 832): Accounting for Government Grants Received by Business Entities. The amendments in this update establish the accounting for a government grant received by a business entity. The guidance is effective for fiscal years beginning after December 15, 2029, with early adoption permitted. The Company is currently evaluating the guidance to determine the impact on its accounting policies and disclosures.

There are no other recently issued, but not yet adopted, accounting pronouncements that are expected to have a material impact on the Company's Consolidated Interim Financial Statements and related disclosures.

Note 3. Revenue Recognition and Contracts with Customers

Disaggregated Revenue

Net sales by region (determined based on country of shipment) and channel is included in Note 22, Segments and Concentrations.

Contract Balances

The following table summarizes our contract assets and liabilities balances:

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Contract assets—January 1 | $ | $ | |||||||||

Contract assets—March 31 | |||||||||||

| Change in contract assets—Increase/(Decrease) | $ | $ | |||||||||

| Contract liabilities—January 1 | $ | ( | $ | ( | |||||||

Contract liabilities—March 31 | ( | ( | |||||||||

| Change in contract liabilities—Decrease/(Increase) | $ | ( | $ | ( | |||||||

Note 4. Research, Development and Engineering

Garrett conducts research, development, and engineering (“RD&E”) activities, which consist primarily of the development of new products and product applications. RD&E costs are included in Cost of goods sold. Customer reimbursements are netted against gross RD&E expenditures as they are considered a recovery of cost. RD&E costs are charged to expense as incurred unless the Company has a contractual guarantee of reimbursement from the customer, in which case the related costs are capitalized. Total RD&E expenses, net of customer reimbursements, amounted to the following:

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Research, development and engineering costs | $ | $ | |||||||||

8

Note 5. Income Taxes

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Tax expense | $ | $ | |||||||||

| Effective tax rate | % | % | |||||||||

The effective tax rates for the three months ended March 31, 2026 and 2025 were 19.5 % and 27.1 %, respectively. The change in the effective tax rate for the three months ended March 31, 2026 compared to the prior period is primarily related to a decrease in U.S. taxes on international operations, the global mix of earnings, and deductions related to employee share-based payments.

The effective tax rate for the three months ended March 31, 2026 was lower than the U.S. federal statutory rate of 21% primarily because of the global mix of earnings, benefits related to research and development expenses, and deductions related to employee share-based compensation.

Note 6. Accounts, Notes and Other Receivables—Net

| March 31, 2026 | December 31, 2025 | ||||||||||

(Dollars in millions) | |||||||||||

Trade receivables | $ | $ | |||||||||

Notes receivable | |||||||||||

Other receivables | |||||||||||

Less—Allowance for expected credit losses | ( | ( | |||||||||

| $ | $ | ||||||||||

Trade receivables include $72 million and $48 million of unbilled customer contract asset balances as of March 31, 2026 and December 31, 2025, respectively. These amounts are billed in accordance with the terms of customer contracts to which they relate. See Note 3, Revenue Recognition and Contracts with Customers.

Notes receivable is related to guaranteed bank notes without recourse that the Company receives in settlement of accounts receivables, primarily in the Asia Pacific region. See Note 7, Factoring and Notes Receivable.

Note 7. Factoring and Notes Receivable

The Company enters into arrangements with financial institutions to sell eligible trade receivables. The receivables are sold without recourse and the Company accounts for these arrangements as true sales. The Company also receives guaranteed bank notes without recourse, in settlement of accounts receivables, primarily in the Asia Pacific region. The Company can hold the bank notes until maturity, exchange them with suppliers to settle liabilities, or sell them to third-party financial institutions in exchange for cash. Bank notes sold to third-party financial institutions without recourse are likewise accounted for as true sales.

9

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Eligible receivables sold without recourse | $ | $ | |||||||||

| Guaranteed bank notes sold without recourse | |||||||||||

The expenses related to the sale of trade receivables and guaranteed bank notes are recognized within Other expense, net in the Consolidated Interim Statements of Operations, and were $1 million and $1 million for the three months ended March 31, 2026 and 2025, respectively.

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Receivables sold but not yet collected by the bank from the customer | $ | $ | |||||||||

| Guaranteed bank notes sold but not yet collected by the bank from the customer | |||||||||||

As of March 31, 2026 and December 31, 2025, the Company had no

Note 8. Inventories—Net

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Raw materials | $ | $ | |||||||||

| Work in process | |||||||||||

| Finished products | |||||||||||

| Less—Reserves | ( | ( | |||||||||

| $ | $ | ||||||||||

Note 9. Other Current Assets

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Prepaid expenses | $ | $ | |||||||||

| Taxes receivable | |||||||||||

| Advanced discounts to customers, current | |||||||||||

| Customer reimbursable engineering | |||||||||||

| Foreign exchange forward contracts | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

10

Note 10. Other Assets

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Advanced discounts to customers, non-current | $ | $ | |||||||||

(Note 14) | |||||||||||

| Income tax receivable | |||||||||||

| Pension and other employee related | |||||||||||

| Customer reimbursable engineering costs | |||||||||||

Designated and undesignated derivatives (Note 17) | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

Note 11. Supplier Financing

The Company has supplier financing arrangements with two third-party financial institutions under which certain suppliers may factor their receivables from Garrett. The Company also enters into arrangements with banking institutions to issue bankers acceptance drafts in settlement of accounts payables, primarily in the Asia Pacific region. The bankers acceptance drafts, or guaranteed bank notes, have a contractual maturity of six months or less, and may be held by suppliers until maturity, transferred to their suppliers, or discounted with financial institutions in exchange for cash. The supplier financing obligations and guaranteed bank notes outstanding are recorded within Accounts payable in our Consolidated Interim Balance Sheet.

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Supplier financing obligations outstanding with financial institutions | $ | $ | |||||||||

| Guaranteed bank notes outstanding | |||||||||||

Note 12. Accrued Liabilities

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Customer pricing reserve | $ | $ | |||||||||

| Compensation, benefit and other employee related | |||||||||||

| Repositioning | |||||||||||

Product warranties and performance guarantees - short-term (Note 20) | |||||||||||

| Income and other taxes | |||||||||||

Customer advances and deferred income (1) | |||||||||||

| Accrued interest | |||||||||||

(Note 14) | |||||||||||

| Accrued freight | |||||||||||

Designated and undesignated derivatives (Note 17) | |||||||||||

| Environmental reserve | |||||||||||

Other (primarily operating expenses) | |||||||||||

11

The Company accrues repositioning costs related to projects to optimize its product costs and right-size our organizational structure. Expenses related to the repositioning accruals are included in Cost of goods sold and Selling, general and administrative expenses in our Consolidated Interim Statements of Operations.

The following tables summarize the activity in our repositioning accrual:

| Severance Costs | Other Costs | Total | |||||||||||||||

| (Dollars in millions) | |||||||||||||||||

Balance at December 31, 2025 | $ | $ | $ | ||||||||||||||

| Charges | |||||||||||||||||

| Usage—cash | ( | ( | |||||||||||||||

Balance at March 31, 2026 | $ | $ | $ | ||||||||||||||

| Severance Costs | Other Costs | Total | |||||||||||||||

| (Dollars in millions) | |||||||||||||||||

Balance at December 31, 2024 | $ | $ | $ | ||||||||||||||

| Charges | |||||||||||||||||

| Usage—cash | ( | ( | |||||||||||||||

Balance at March 31, 2025 | $ | $ | $ | ||||||||||||||

Note 13. Other Liabilities

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Income taxes | $ | $ | |||||||||

Derivatives designated as net investment hedges (Note 17) | |||||||||||

Designated and undesignated derivatives (Note 17) | |||||||||||

| Pension and other employee related | |||||||||||

(Note 14) | |||||||||||

Product warranties and performance guarantees – long-term (Note 20) | |||||||||||

| Environmental remediation – long term | |||||||||||

| Long-term accounts payable | |||||||||||

| Asset retirement obligation | |||||||||||

Other (1) | |||||||||||

Note 14. Leases

We have operating leases that primarily consist of real estate, machinery, and equipment. As of March 31, 2026, the Company does not have any material finance leases. Our leases have remaining lease terms of up to 12 years, some of which include options to extend the leases for up to two years , and some of which include options to terminate the leases within the year.

12

The components of lease expense are as follows:

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Operating lease cost | $ | $ | |||||||||

| Short-term lease cost | |||||||||||

| Total lease cost | $ | $ | |||||||||

Supplemental cash flow information related to operating leases is as follows:

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

Cash paid for amounts included in the measurement of lease liabilities: | |||||||||||

Operating cash outflows from operating leases | $ | $ | |||||||||

Right-of-use assets obtained in exchange for lease obligations: | |||||||||||

| Operating leases | |||||||||||

Supplemental balance sheet information related to operating leases is as follows:

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| $ | $ | ||||||||||

| March 31, 2026 | December 31, 2025 | ||||||||||

| Weighted-average remaining lease term (in years) | |||||||||||

| Weighted-average discount rate | % | % | |||||||||

Maturities of operating lease liabilities as of March 31, 2026 were as follows:

| (Dollars in millions) | |||||

| 2026 | $ | ||||

| 2027 | |||||

| 2028 | |||||

| 2029 | |||||

| 2030 | |||||

| Thereafter | |||||

| Total lease payments | |||||

| Less imputed interest | ( | ||||

| $ | |||||

Note 15. Long-Term Debt and Credit Agreements

Senior Notes

On May 21, 2024, Garrett Motion Holdings Inc. and Garrett LX I S.à.r.l. (the "Issuers"), wholly owned subsidiaries of the Company, completed an offering of $800 million in aggregate principal amount of 7.75 % Senior Unsecured Notes due

13

2032 (the "2032 Senior Notes"). The 2032 Senior Notes mature on May 31, 2032. The Company incurred $12 million of debt issuance costs, which have been capitalized and are being amortized on a straight-line basis.

The 2032 Senior Notes are guaranteed by the Company and each of the Company's wholly owned subsidiaries that guarantee obligations under the Credit Agreement (as defined below), subject to certain exceptions. The proceeds from the sale of the 2032 Senior Notes, together with cash on hand, were used to repay approximately $800 million of term loan indebtedness and to pay related fees and expenses. The 2032 Senior Notes bear interest at a rate of 7.75 % per annum. Interest on the 2032 Senior Notes is payable semi-annually in arrears on May 31 and November 30 of each year, commencing on November 30, 2024.

The 2032 Senior Notes indenture contains certain covenants that limit the ability of the Company and its restricted subsidiaries to incur certain additional debt, incur certain liens securing debt, pay certain dividends or make other restricted payments, make certain investments, make certain asset sales, and enter into certain transactions with affiliates. These covenants are subject to a number of exceptions, limitations, and qualifications as set forth in the 2032 Senior Notes indenture. Additionally, the indenture contains certain change of control provisions that, under certain conditions, would require the Company to make an offer to repurchase all of the outstanding 2032 Senior Notes at a price equal to 101 % of the aggregate principal amount, plus accrued and unpaid interest. The indenture also contains customary events of default.

Credit Facilities

On January 30, 2025, the Company entered into a Restatement Agreement (the "Restatement Agreement"), which amends and restates the Credit Agreement, dated as of April 30, 2021 (as amended from time to time, the "Existing Credit Agreement" and as amended and restated by the Restatement Agreement, the "Credit Agreement"), by and among the Company, Garrett Motion Holdings Inc., Garrett Motion Sàrl and Garrett LX I S.à.r.l., as borrowers (the "Borrowers"), the lenders and issuing banks part thereto from time to time, and JPMorgan Chase Bank, N.A., as administrative agent. Under the Restatement Agreement, the Company refinanced in full its $692 million U.S. Dollar term loan facility (the "2021 Dollar Term Facility") under the Existing Credit Agreement with a new $692 million term loan (the "2025 Dollar Term Facility") in an aggregate principal amount of $692 million. The 2025 Dollar Term Facility will mature on January 30, 2032, and bear interest at a rate equal to, at the Company's option, the Adjusted Term SOFR Rate (as defined in the Restatement Agreement) plus 2.00 % per annum in the case of Term Benchmark Loans (as defined in the Restatement Agreement) and the Alternate Base Rate (as defined in the Restatement Agreement) plus 1.00 % per annum in the case of ABR Loans (as defined in the Restatement Agreement).

Also on January 30, 2025, pursuant to the Restatement Agreement, the Company replaced its existing $600 million revolving commitments under the Existing Credit Agreement with new revolving commitments under the Credit Agreement in an aggregate principal amount of $630 million (the "New Revolving Facility" and, together with the New Term Loans, the "Credit Facilities"). The maturity date of the New Revolving Facility is January 30, 2030. The New Revolving Facility, when drawn, will bear interest at a rate equal to the applicable benchmark plus an applicable margin that varies based on the Company's leverage ratio. The applicable margin for revolving borrowings ranges from 2.25 % to 1.75 % per annum in the case of Term Benchmark Loans and 1.25 % to 0.75 % per annum in the case of ABR Loans. In addition to paying interest on outstanding borrowings under the New Revolving Facility, the Company must also pay a quarterly commitment fee based on the average daily unused portion of the New Revolving Facility during such quarter, which is determined by its leverage ratio and ranges from 0.25 % to 0.50 % per annum.

The Credit Agreement contains certain affirmative and negative covenants customary for financings of this type. The Credit Agreement also contains certain customary events of default. The New Revolving Facility is subject to a financial covenant requiring the maintenance of a consolidated total leverage ratio of not greater than 4.7 to 1.00 as of the end of each fiscal quarter if, on the last day of any such fiscal quarter, the aggregate amount of loans and letters of credit (excluding backstopped or cash collateralized letters of credit and other letters of credit with an aggregate face amount not exceeding $30 million) outstanding under the New Revolving Facility exceeds 35 % of the aggregate commitments in effect thereunder on such date. The Credit Facilities are secured on a first-priority basis by: (1) a perfected security interest in the equity interests of each direct material subsidiary of each guarantor under the Credit Facilities and (ii) perfected security interests in, and mortgages on, substantially all tangible and intangible personal property and material real property of each of the guarantors under the Credit Facilities, subject, in each case, to certain exceptions and limitations, including the agreed guaranty and security principles.

14

As of March 31, 2026, the Company was in compliance with all covenants under the 2032 Senior Notes indenture and Credit Agreement.

The principal outstanding and carrying amounts of our long-term debt as of March 31, 2026 and December 31, 2025 are as follows:

| Due | Interest Rate | March 31, 2026 | December 31, 2025 | ||||||||||||||||||||

| 2025 Dollar Term Facility | 1/30/2032 | SOFR plus | $ | $ | |||||||||||||||||||

| 2032 Senior Notes | 5/31/2032 | ||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Total principal outstanding | |||||||||||||||||||||||

| Less: unamortized deferred financing costs | ( | ( | |||||||||||||||||||||

| Less: current portion of long-term debt | ( | ( | |||||||||||||||||||||

| Total long-term debt | $ | $ | |||||||||||||||||||||

Separate from the New Revolving Facility, the Company has a bilateral letter of credit facility with outstanding letters of credit in the amount of $10 million and $10 million at March 31, 2026 and December 31, 2025, respectively. The letters of credit typically support customs arrangements and other obligations at our local affiliates.

Minimum scheduled principal repayments of long-term debt as of March 31, 2026 are as follow:

| March 31, 2026 | |||||

| (Dollars in millions) | |||||

| 2026 | $ | ||||

| 2027 | |||||

| 2028 | |||||

| 2029 | |||||

| 2030 | |||||

| Thereafter | |||||

| Total debt payments | $ | ||||

Note 16. Equity

Common Stock

Cash dividends paid to shareholders of our Common Stock for the three months ended March 31, 2026 and 2025 were as follows (in millions, except per share amounts):

| Quarterly Dividends | |||||||||||||||||||||||

| 2026 | 2025 | ||||||||||||||||||||||

| Per Share | Total | Per Share | Total | ||||||||||||||||||||

| First quarter | $ | $ | $ | $ | |||||||||||||||||||

Treasury Stock

Treasury stock represents shares of the Company's Common Stock that have been issued and subsequently repurchased by the Company or withheld to satisfy withholding tax obligations in connection with the vesting of equity awards, and that have not been retired or cancelled. The Company accounts for treasury stock under the cost method and includes treasury stock as a component of Equity (Deficit) on the Consolidated Interim Balance Sheet. The Company accounts for the reissuance of treasury stock using the average cost method. The Company did not reissue or retire any shares of treasury stock during the three months ended March 31, 2026.

15

Share Repurchase Program

Note 17. Financial Instruments and Fair Value Measures

Our credit, market, and foreign currency risk management policies are described in Note 17, Financial Instruments and Fair Value Measures, to the Consolidated Financial Statements for the year ended December 31, 2025 included in our 2025 Form 10-K. As of March 31, 2026 and December 31, 2025, we had contracts with aggregate gross notional amounts of $2,172 million and $1,374 million, respectively, to hedge foreign currencies, principally the U.S. Dollar, Swiss Franc, British Pound, Euro, Chinese Yuan, Japanese Yen, Mexican Peso, New Romanian Leu, Czech Koruna, Australian Dollar, and Korean Won.

Fair Value of Financial Instruments

The FASB’s accounting guidance defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (exit price). Financial and nonfinancial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The following table sets forth the Company’s financial assets and liabilities that were accounted for at fair value on a recurring basis as of March 31, 2026 and December 31, 2025:

| Fair Value | ||||||||||||||||||||||||||||||||||||||

| Notional Amounts | Assets | Liabilities | ||||||||||||||||||||||||||||||||||||

| March 31, 2026 | December 31, 2025 | March 31, 2026 | December 31, 2025 | March 31, 2026 | December 31, 2025 | |||||||||||||||||||||||||||||||||

| Designated instruments: | ||||||||||||||||||||||||||||||||||||||

| Designated forward currency exchange contracts | $ | $ | $ | $ | (a) | $ | $ | (c) | ||||||||||||||||||||||||||||||

| Designated cross-currency swaps | (b) | (d) | ||||||||||||||||||||||||||||||||||||

| Designated interest-rate swaps | (b) | (d) | ||||||||||||||||||||||||||||||||||||

| Total designated instruments | ||||||||||||||||||||||||||||||||||||||

| Undesignated instruments: | ||||||||||||||||||||||||||||||||||||||

| Undesignated forward currency exchange contracts | (a) | (c) | ||||||||||||||||||||||||||||||||||||

| Total undesignated instruments | ||||||||||||||||||||||||||||||||||||||

| Total designated and undesignated instruments | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

(a) Recorded within Other current assets and Other assets

(b) Recorded within Other assets

(c) Recorded within Accrued liabilities and Other liabilities

(d) Recorded within Other liabilities

Cash Flow Hedges

During 2025, the Company entered into float-to-fixed interest rate swap contracts with an aggregate notional amount of $625 million and maturities in January 2028, January 2029, January 2030 and January 2031, of which an interest rate swap contract with a notional amount of $50 million was early settled during 2025. Changes in the fair value of the interest

16

rate swap contracts are recorded in Accumulated Other Comprehensive Income ("AOCI") and will be reclassified to Interest expense in the Consolidated Interim Statement of Operations upon maturity. Amounts recognized related to the early settlement of the interest rate swap contract were immaterial.

The Company also has outstanding forward currency exchange contracts with maturities up to 18 months and an aggregate notional amount of $1,235 million and $637 million as of March 31, 2026 and December 31, 2025, respectively. These forward currency exchange contracts have been designated as cash flow hedges to mitigate foreign currency exposures primarily on our inventory purchases and manufacturing costs. The gains and losses on the forward currency exchange contracts are recorded in AOCI and reclassified to Cost of goods sold in the Consolidated Interim Statement of Operations when the underlying transactions are recognized in earnings.

In order to mitigate foreign currency risk on its 2032 Senior Notes, the Company entered into fixed-to-fixed cross-currency swap contracts with an aggregate notional amount of €507 million ($550 million) and notional exchanges occurring in May 2027, May 2028, May 2029, and May 2030. Changes in the fair value of the cross-currency swap contracts are recognized in AOCI and reclassified to Non-operating (income) expense in the Consolidated Interim Statement of Operations, based upon changes in the spot rate remeasurement of the underlying debt. The net interest settlements on the cross-currency swap contracts are recorded in Interest expense in the Consolidated Interim Statements of Operations.

All of the Company's cash flow hedges are assessed as highly effective.

Net Investment Hedges

The Company has designated cross-currency swaps with aggregate notional amounts of €1,157 million ($1,225 million) as net investment hedges of its Euro-denominated operations. Changes in the fair value of the net investment hedges are recorded in AOCI until the net investment is liquidated or sold. The fair values of the net investment hedges were net liabilities of $87 million and $124 million as of March 31, 2026 and December 31, 2025, respectively. No ineffectiveness has been recorded on the net investment hedges.

Non-Designated Derivatives

The Company has outstanding forward currency exchange contracts with maturities generally up to 3 months and an aggregate notional amount of $937 million and $737 million as of March 31, 2026 and December 31, 2025, respectively. Changes in the fair value of the forward currency exchange contracts are recorded in Non-operating (income) expense in the Consolidated Interim Statements of Operations.

The Company had float-to-fixed interest rate swap contracts that were early settled in 2025. Changes in the fair value of the undesignated interest rate swap contracts were recorded in Interest expense in the Consolidated Interim Statements of Operations.

Effect of Derivatives on the Statements of Operations and Statements of Comprehensive Income (Loss)

The following tables present the pretax impact that changes in the fair values of derivatives designated as cash flow hedges and net investment hedges had on OCI, AOCI and earnings:

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Cash flow hedges | |||||||||||

| Gain (loss) reclassified from AOCI to income: | |||||||||||

| Cost of goods sold | $ | ( | $ | ||||||||

| Interest expense | |||||||||||

| Non-operating (expense) income | ( | ||||||||||

| Gain (loss) recognized in other comprehensive income (loss) | |||||||||||

| Net investment hedges | |||||||||||

| Gain (loss) recognized in other comprehensive income (loss) | ( | ||||||||||

17

During the next twelve months, $14 million of pretax gain on cash flow hedges is expected to be reclassified from AOCI into income.

The following table summarizes the pretax gain (loss) that changes in the fair values of derivatives not designated as hedging instruments had on earnings:

| Three Months Ended March 31, | ||||||||||||||||||||

| 2026 | 2025 | |||||||||||||||||||

| Contract Type | Location | (Dollars in millions) | ||||||||||||||||||

| Interest rate swaps | Interest expense (1) | $ | $ | |||||||||||||||||

| Forward currency exchange contracts | Non-operating income | ( | ||||||||||||||||||

(1) Includes interest income of $6 million, partially offset by marked-to-market remeasurement losses of $6 million, for the three months ended March 31, 2025. There were no undesignated interest rate swaps outstanding during 2026.

Fair Value Measurement

The foreign currency exchange, interest rate swap and cross-currency swap contracts are valued using market observable inputs. As such, these derivative instruments are classified within Level 2. The assumptions used in measuring the fair value of the cross-currency swap are considered Level 2 inputs, which are based upon market-observable interest rate curves, cross-currency basis curves, credit default swap curves, and foreign exchange rates.

The carrying value of Cash, cash equivalents, and restricted cash, Account receivables and Notes and Other receivables contained in the Consolidated Interim Balance Sheet approximates fair value.

The following table sets forth the Company’s financial assets and liabilities that were not carried at fair value:

March 31, 2026 | December 31, 2025 | ||||||||||||||||||||||

| Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||

Term Loan Facilities | $ | $ | $ | $ | |||||||||||||||||||

| 2032 Senior Notes | |||||||||||||||||||||||

Note 18. Accumulated Other Comprehensive Income

The changes in AOCI by component are set forth below:

18

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Foreign Exchange Translation Adjustment | |||||||||||

| Balance at beginning of period | $ | ( | $ | ( | |||||||

| Other comprehensive (loss) income before reclassifications | ( | ( | |||||||||

| Income tax benefit (expense) associated with comprehensive income (loss) before reclassifications | |||||||||||

| Amounts reclassified from AOCI | |||||||||||

| Balance at end of period | ( | ( | |||||||||

| Pension Adjustments | |||||||||||

| Balance at beginning of period | ( | ( | |||||||||

| Other comprehensive income (loss) before reclassifications | |||||||||||

| Income tax benefit (expense) associated with comprehensive income (loss) before reclassifications | |||||||||||

| Balance at end of period | ( | ( | |||||||||

| Changes in Fair Value of Effective Cash Flow Hedges | |||||||||||

| Balance at beginning of period | ( | ( | |||||||||

| Other comprehensive (loss) income before reclassifications | |||||||||||

| Income tax benefit (expense) associated with comprehensive income (loss) before reclassifications | ( | ||||||||||

| Amounts reclassified from AOCI | ( | ||||||||||

| Income taxes associated with reclassifications from AOCI | ( | ||||||||||

| Balance at end of period | ( | ||||||||||

| Changes in Fair Value of Net Investment Hedges | |||||||||||

| Balance at beginning of period | ( | ||||||||||

| Other comprehensive (loss) income before reclassifications | ( | ||||||||||

| Income tax benefit (expense) associated with comprehensive income (loss) before reclassifications | ( | ||||||||||

| Balance at end of period | |||||||||||

| Accumulated other comprehensive (loss) income, end of period | $ | ( | $ | ||||||||

19

Reclassifications from AOCI to income were as follows:

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Changes in Fair Value of Effective Cash Flow Hedges | |||||||||||

| Reclassification forward currency exchange contracts to Cost of goods sold | $ | $ | |||||||||

| Reclassification cross-currency swaps to Interest expense | |||||||||||

| Reclassification cross-currency swaps to Non-operating (income) expense | ( | ||||||||||

| Tax effect on reclassification to income | ( | ||||||||||

| Amounts reclassified from AOCI, net | ( | ||||||||||

| Total reclassifications for the period | $ | $ | ( | ||||||||

Note 19. Earnings Per Share

Basic earnings per share ("EPS") is computed using the two-class method. The deferred stock units ("DSUs") related to our stock-based compensation plan contain non-forfeitable rights to dividends and are considered as participating securities. The two-class method requires an allocation of earnings to all securities that participate in dividends with common shares to the extent that each such security may share in the Company's earnings. Basic EPS is then calculated by dividing undistributed earnings allocated to common stock by the weighted average number of common shares outstanding for the period. Under the two-class method, the impact of these participating securities was immaterial for the three months ended March 31, 2026 and 2025.

Diluted earnings per share is calculated by applying the two-class method for participating securities and then incorporating the dilutive effect of other potential common shares, determined using methods such as the treasury stock method, to arrive at the most dilutive EPS.

The details of the EPS calculations for the three months ended March 31, 2026 and 2025 are as follows:

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions except per share) | |||||||||||

Basic earnings per share: | |||||||||||

| Net income | $ | $ | |||||||||

| Weighted average common shares outstanding – Basic | |||||||||||

| EPS – Basic | $ | $ | |||||||||

Diluted earnings per share: | |||||||||||

| Weighted average common shares outstanding – Basic | |||||||||||

Dilutive effect of unvested RSUs and other contingently issuable shares | |||||||||||

| Weighted average common shares outstanding – Diluted | |||||||||||

| EPS – Diluted | $ | $ | |||||||||

Note 20. Commitments and Contingencies

We are involved in various lawsuits, claims, and proceedings incident to the operation of our businesses, including those pertaining to product liability, product safety, environmental, health and safety, intellectual property, employment, commercial and contractual matters and various other matters. We regularly assess the likelihood of adverse judgments or outcomes in these matters, as well as potential ranges of possible losses based on a careful analysis of each matter. We identify below the individual proceedings where we believe a material loss is reasonably possible or probable, and we accrue for matters when we believe that losses are probable and the amount of the potential loss is reasonably estimable. It is inherently difficult to determine whether a loss is probable or reasonably possible or to estimate the size or range of any

20

potential loss. Accordingly, while we believe that appropriate accruals have been established for losses that are probable and can be reasonably estimated, it is possible that adverse outcomes from such proceedings could exceed the amounts accrued by an amount that could be material to our financial position, results of operations or cash flows.

Brazilian Tax Matter

In September 2020, the Brazilian tax authorities issued an infraction notice against Garrett Motion Industria Automotiva Brasil Ltda, challenging the use of certain tax credits between January 2017 and February 2020. The estimated total amount of the loss contingency arising from this matter as of March 31, 2026 was $28 million, including penalties and interest. The Company believes, based on management’s assessment and the advice of external legal counsel, that it has meritorious arguments in connection with the infraction notice and any liability for the infraction notice is currently not probable. Accordingly, no accrual is required at this time.

Warranties and Guarantees

In the normal course of business, we issue product warranties and product performance guarantees. We accrue for the estimated cost of product warranties and performance guarantees based on contract terms and historical experience at the time of sale to the customer. Adjustments to initial obligations for warranties and guarantees are made as changes to the obligations become reasonably estimable. Product warranties and product performance guarantees are included in Accrued liabilities and Other liabilities. The following table summarizes information concerning our recorded obligations for product warranties and product performance guarantees.

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

(Dollars in millions) | |||||||||||

| Warranty and product performance guarantees at beginning of period | $ | $ | |||||||||

Accruals for warranties/guarantees issued during the period | |||||||||||

Settlement of warranty/guarantee claims | ( | ( | |||||||||

| Foreign currency translation | |||||||||||

Warranty and product performance guarantees at end of period | $ | $ | |||||||||

Other Commitments and Contingencies

We are subject to other lawsuits, investigations, and disputes arising out of the conduct of our business, including matters relating to commercial transactions, government contracts, product liability, prior acquisitions and divestitures, employment and employee benefit plans, intellectual property, and environmental, health and safety matters. We recognize a liability for any contingency that is probable of occurring and reasonably estimable. We regularly assess the likelihood of adverse judgments or outcomes in these matters, as well as potential ranges of possible losses (taking into consideration any insurance recoveries), based on a careful analysis of each matter with the assistance of outside legal counsel and, if applicable, other experts.

Note 21. Pension Benefits

We sponsor several funded U.S. and non-U.S. defined benefit pension plans. Significant plans outside the U.S. are in Switzerland and Ireland. Other pension plans outside the U.S. are not material to the Company, either individually or in the aggregate.

Our general funding policy for qualified defined benefit pension plans is to contribute amounts at least sufficient to satisfy regulatory funding standards. We are not required to make any contributions to our U.S. pension plan in 2026. We expect to make contributions of cash and/or marketable securities of approximately $5 million to our non-U.S. pension plans to satisfy regulatory funding standards in 2026. There have been no contributions as of March 31, 2026.

21

Net periodic benefit costs for our significant defined benefit plans include the following components:

| Three Months Ended March 31, | |||||||||||||||||||||||

| U.S. Plans | Non-U.S. Plan | ||||||||||||||||||||||

| 2026 | 2025 | 2026 | 2025 | ||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | |||||||||||||||||||

| Interest cost | |||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | |||||||||||||||||||

| Amortization of prior service (credit) | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

For both our U.S. and non-U.S. defined benefit pension plans, we estimate the service and interest cost components of net periodic benefit (income) cost by utilizing a full yield curve approach in the estimation of these cost components by applying the specific spot rates along the yield curve used in the determination of the pension benefit obligation to their underlying projected cash flows. This approach provides a more precise measurement of service and interest costs by improving the correlation between projected cash flows and their corresponding spot rates.

Note 22. Segments and Concentrations

The Company has identified our CODM as the Chief Executive Officer. The CODM reviews consolidated net income when assessing the Company's performance, allocating resources, and establishing management's compensation. In addition to consolidated net income, the CODM receives discrete information for net sales by product and by geographical location. Consolidated net income is used to monitor budget versus actual results.

The accounting policies of our operating segment are the same as those described in the Company's summary of significant accounting policies.

The Company derives revenues from customers through sales of turbocharging, air and fluid compression, and high-speed electric motor technologies for OEMs and independent aftermarket distributors in the mobility and industrial fields.

Sales concentration - Net sales by region (determined based on country of shipment) and product line are as follows:

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| United States | $ | $ | |||||||||

| Europe | |||||||||||

| Germany | |||||||||||

| Rest of Europe | |||||||||||

| Asia | |||||||||||

| China | |||||||||||

| Rest of Asia | |||||||||||

| Other International | |||||||||||

| $ | $ | ||||||||||

22

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Diesel | $ | $ | |||||||||

| Gas | |||||||||||

| Commercial Vehicles / Industrial | |||||||||||

| Aftermarket | |||||||||||

| Other | |||||||||||

| $ | $ | ||||||||||

The table below provides segment information about the Company:

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Net sales | $ | $ | |||||||||

| Less: | |||||||||||

| Material costs | |||||||||||

Variable manufacturing costs (1) | |||||||||||

Fixed manufacturing costs (2) | |||||||||||

| RD&E costs | |||||||||||

| Selling, general and administrative costs | |||||||||||

| Interest expense | |||||||||||

| Income tax expense | |||||||||||

Other segment items (3) | ( | ||||||||||

| Consolidated net income | $ | $ | |||||||||

(1) Variable manufacturing costs include freight, duties and tariffs, direct and indirect labor costs, repairs and maintenance, and variable overhead costs.

(2) Fixed manufacturing costs include depreciation and amortization, rent, overhead labor costs, repositioning costs, utilities and other fixed costs.

(3) Other segment items consist of non-service components of net periodic pension expense, interest income, equity income and other non-operating income items (if any).

The measure of segment assets is reported on the balance sheet as total consolidated assets. The Company had capital expenditures of $29 million and $26 million for the three months ended March 31, 2026 and 2025, respectively.

Note 23. Subsequent Events

On April 30, 2026, the Board of Directors declared a cash dividend of $0.08 per share of Common Stock, payable on June 15, 2026, to shareholders of record as of June 1, 2026.

23

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations, which we refer to as our “MD&A,” should be read in conjunction with our Consolidated Interim Financial Statements and related notes appearing elsewhere in this Quarterly Report on Form 10-Q as well as the audited annual Consolidated Financial Statements for the year ended December 31, 2025, included in our 2025 Form 10-K. Some of the information contained in this MD&A or set forth elsewhere in this Quarterly Report on Form 10-Q, including information with respect to our plans and strategy for our business, includes forward-looking statements that involve various risks and uncertainties. Please refer to the "Special Note Regarding Forward-Looking Statements" below.

The following MD&A is intended to help you understand the results of operations and financial condition of Garrett Motion Inc. for the three months ended March 31, 2026.

Executive Summary

During the first quarter of 2026, we outperformed the light vehicle industry across all verticals. This was driven by growth in diesel and gasoline volumes from new program launches, increased commercial vehicle demand in all key regions, as well as continued industrial strength. Aftermarket growth further contributed to a favorable product mix. We continued to deliver productivity year-over-year across both variable and fixed costs; however, these benefits were offset by the timing of foreign exchange pass-through. Our financial results were also impacted by the timing of customer recoveries. As a result, Net income for the quarter was $95 million, and Adjusted EBIT was $151 million. As the broader macroeconomic and geopolitical conditions evolve, we continue to actively monitor developments and their potential impacts on the industry and our operations.

We continue to have success across our differentiated technologies by winning business in both turbo and zero emission offerings. We secured light vehicle turbo, commercial vehicle and industrial awards across multiple regions, including turbo technology for data centers. We have also received favorable feedback from mobility and industrial customers related to expected efficiency gains from our E-Cooling oil-free compressor over existing recognized technologies.

For the three months ended March 31, 2026, we repurchased $87 million of Common Stock under our share repurchase program. These repurchases include a total of 2,500,000 shares from funds affiliated with Oaktree Capital Management, L.P., a related party, for $50 million. As of March 31, 2026, we had $163 million of the authorized amount remaining under our share repurchase program. The repurchased shares are held as treasury stock.

On February 19, 2026, the Board of Directors declared a cash dividend of $0.08 per share of Common Stock, payable on March 16, 2026, to shareholders of record as of March 2, 2026. The total amount of dividends paid on March 16, 2026 amounted to $16 million.

Disaggregated Revenue

The following tables show our revenues by geographic region and product line for the three months ended March 31, 2026 and 2025, respectively.

By Region

Three Months Ended March 31, | |||||||||||||||||||||||

| 2026 | 2025 | ||||||||||||||||||||||

(Dollars in millions) | |||||||||||||||||||||||

United States | $ | 179 | 18% | $ | 176 | 20% | |||||||||||||||||

Europe | 503 | 51% | 425 | 49% | |||||||||||||||||||

Asia | 277 | 28% | 257 | 29% | |||||||||||||||||||

Other | 26 | 3% | 20 | 2% | |||||||||||||||||||

Total | $ | 985 | $ | 878 | |||||||||||||||||||

24

By Product Line

Three Months Ended March 31, | |||||||||||||||||||||||

| 2026 | 2025 | ||||||||||||||||||||||

(Dollars in millions) | |||||||||||||||||||||||

| Diesel | $ | 232 | 24% | $ | 208 | 24% | |||||||||||||||||

| Gas | 443 | 45% | 403 | 46% | |||||||||||||||||||

| Commercial Vehicles / Industrial | 181 | 18% | 155 | 18% | |||||||||||||||||||

| Aftermarket | 114 | 12% | 98 | 11% | |||||||||||||||||||

| Other | 15 | 1% | 14 | 1% | |||||||||||||||||||

| Total | $ | 985 | $ | 878 | |||||||||||||||||||

Results of Operations for the Three Months Ended March 31, 2026

Net Sales

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Net sales | $ | 985 | $ | 878 | |||||||

| % change compared with prior period | 12.2 | % | |||||||||

Net Sales for the Three Months Ended March 31, 2026

For the three months ended March 31, 2026, net sales compared to the prior period increased by $107 million or 12% (including a favorable impact of $58 million or 6% due to foreign currency translation primarily driven by higher Euro-to-U.S. dollar exchange rates). The increase was primarily related to higher demand across all verticals, favorable foreign currency impacts and favorable product mix partially offset by price net of inflation pass-through. Net sales also increased by $5 million driven by recoveries on import tariffs.

Gasoline product sales increased by $40 million or 10% (including a favorable impact of $27 million or 7% due to foreign currency translation), primarily driven by new application launches and program ramp-ups in Europe.

Diesel product sales increased by $24 million or 12% (including a favorable impact of $18 million or 9% due to foreign currency translation), primarily driven by strong demand for light commercial vehicles and pickup trucks in North America, Brazil, Southeast Asia and application launches in India.

Commercial vehicles/industrial sales increased by $26 million or 17% (including a favorable impact of $6 million or 4% due to foreign currency translation), primarily driven by growth in all key regions as well as continued industrial growth.

Aftermarket sales increased by $16 million or 16% (including a favorable impact of $6 million or 6% due to foreign currency translation), primarily driven by stronger demand for commercial vehicle parts in all key regions.

Cost of Goods Sold and Gross Profit

25

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Cost of goods sold | $ | 789 | $ | 699 | |||||||

| % change compared with prior period | 12.9 | % | |||||||||

| Gross profit percentage | 19.9 | % | 20.4 | % | |||||||

Cost of Goods Sold and Gross Profit for the Three Months Ended March 31, 2026

| Cost of Goods Sold | Gross Profit | ||||||||||

| (Dollars in millions) | |||||||||||

Cost of Goods Sold / Gross Profit for the three months ended March 31, 2025 | $ | 699 | $ | 179 | |||||||

| Increase/(decrease) due to: | |||||||||||

| Volume | 42 | 19 | |||||||||

| Product mix | 4 | 4 | |||||||||

| Price, net of inflation pass-through | — | (11) | |||||||||

| Commodity, transportation & energy deflation | (2) | 2 | |||||||||

| Productivity, net | 7 | (21) | |||||||||

| Import tariffs | 6 | (1) | |||||||||

| Research, development & engineering | (7) | 7 | |||||||||

| Foreign exchange rate impacts | 40 | 18 | |||||||||

Cost of Goods Sold / Gross Profit for the three months ended March 31, 2026 | $ | 789 | $ | 196 | |||||||

For the three months ended March 31, 2026, cost of goods sold increased by $90 million, primarily driven by $42 million from higher sales volumes, $40 million from foreign currency impacts, $7 million of lower productivity net of labor inflation and repositioning costs, $6 million from import tariffs and $4 million of unfavorable product mix. These increases were partially offset by $7 million of lower RD&E costs and $2 million of commodity, transportation and energy deflation.

For the three months ended March 31, 2026, gross profit increased by $17 million, primarily driven by $19 million from higher sales volumes, $18 million from foreign currency impacts, $7 million of lower RD&E costs, $4 million of favorable product mix and $2 million from commodity, transportation and energy deflation. These increases were partially offset by $21 million of lower productivity net of labor deflation and repositioning costs, $11 million of pricing, net of inflation pass-through and $1 million from import tariffs.

Selling, General and Administrative Expenses

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Selling, general and administrative expense | $ | 58 | $ | 59 | |||||||

| % of sales | 5.9 | % | 6.7 | % | |||||||

Selling, general and administrative (“SG&A”) expenses for the three months ended March 31, 2026, decreased by $1 million compared with the prior period, primarily driven by $3 million of lower professional services, $2 million of bad debt recovery and $1 million of lower personnel costs, partially offset by $5 million of unfavorable foreign currency impacts.

Other Expense, Net

26

| Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Other expense, net | $ | 1 | $ | 7 | |||||||

Other expense, net for the three months ended March 31, 2026 decreased by $6 million compared to the prior period, primarily driven by $6 million in professional fees incurred in the prior year related to our Restatement Agreement.

Interest Expense

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Interest expense | $ | 27 | $ | 29 | |||||||

For the three months ended March 31, 2026, interest expense decreased by $2 million compared to the prior period. This decrease was primarily due to $3 million in lower interest expense due to a different notional amount of debt outstanding during the period.

Non-Operating Income, Net

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Non-operating income, net | $ | (8) | $ | (1) | |||||||

For the three months ended March 31, 2026, we had non-operating income of $8 million versus $1 million in the prior period. The increase in non-operating income was primarily driven by the resolution of certain environmental liabilities and foreign exchange transactional gains.

Tax Expense

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Tax expense | $ | 23 | $ | 23 | |||||||

| Effective tax rate | 19.5 | % | 27.1 | % | |||||||

The effective tax rates for the three months ended March 31, 2026 and 2025 were 19.5% and 27.1%, respectively.

The change in the effective tax rate for the three months ended March 31, 2026, compared to the prior period is primarily related to a decrease in U.S. taxes on international operations, the global mix of earnings, and deductions related to employee share-based compensation.

The effective tax rate can vary from quarter to quarter due to changes in the Company’s global mix of earnings, the resolution of income tax audits, changes in tax laws (including updated guidance on U.S. tax reform), deductions related to employee share-based payments, internal restructurings, and pension mark-to-market adjustments.

27

Net Income

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Net income | $ | 95 | $ | 62 | |||||||

| Net income margin | 9.6 | % | 7.1 | % | |||||||

Net income for the three months ended March 31, 2026, increased by $33 million compared with the prior period, primarily due to $17 million of higher gross profit, $7 million of higher non-operating income, $6 million of lower other expense, net, $2 million of lower interest expense and $1 million of lower SG&A expense.

Non-GAAP Measures

It is management’s intent to provide non-GAAP financial information to supplement the understanding of our business operations and performance, and it should be considered by the reader in addition to, but not instead of, the financial statements prepared in accordance with GAAP. Each non-GAAP financial measure is presented along with the most directly comparable GAAP measure so as not to imply that more emphasis should be placed on the non-GAAP measure. The non-GAAP financial information presented may be determined or calculated differently by other companies and may not be comparable to other similarly titled measures used by other companies. Additionally, the non-GAAP financial measures have limitations as analytical tools and should not be considered in isolation from, or as a substitute for, an analysis of the Company’s operating results as reported under GAAP.

EBIT and Adjusted EBIT

We define “EBIT” as our net income calculated in accordance with U.S. GAAP, plus the sum of (i) interest expense net of interest income and (ii) tax expense. We define “Adjusted EBIT” as EBIT, plus the sum of (i) repositioning costs, (ii) foreign exchange (gain) loss on debt net of related hedging (gains) losses, (iii) discounting costs on factoring, (iv) gain on sale of equity investment, (v) acquisition and divestiture expenses, (vi) other non-operating income, and (vii) debt refinancing and redemption costs, if any.

We believe that EBIT and Adjusted EBIT are important indicators of operating performance and provide useful information for investors because EBIT and Adjusted EBIT exclude the effects of income taxes, as well as the effects of financing activities by eliminating the effects of interest. Certain adjustment items, while periodically affecting our results, may also vary significantly from period to period and have disproportionate effect in a given period, which affects the comparability of our results.

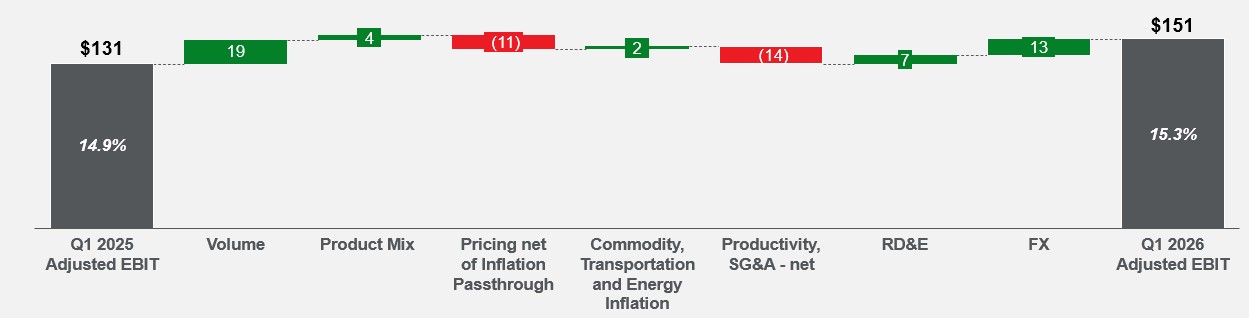

The following table reconciles Net income under GAAP to Adjusted EBIT:

Three Months Ended March 31, | |||||||||||

| 2026 | 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Net income | $ | 95 | $ | 62 | |||||||

Interest expense, net of interest income (1) | 26 | 29 | |||||||||

| Tax expense | 23 | 23 | |||||||||

| EBIT | 144 | 114 | |||||||||

Repositioning costs (2) | 12 | 7 | |||||||||

| Foreign exchange gain on debt, net of related hedging loss | — | 1 | |||||||||

Factoring and notes receivables discount fees | 1 | 1 | |||||||||

Other non-operating income (3) | (6) | (1) | |||||||||

Debt refinancing and redemption costs (4) | — | 6 | |||||||||

| Acquisition and divestiture expenses | — | 3 | |||||||||

| Adjusted EBIT | $ | 151 | $ | 131 | |||||||

28

(1)Reflects interest income of $1 million and $0 million for the three months ended March 31, 2026 and 2025, respectively.

(2)Repositioning costs includes severance costs related to restructuring projects to improve future productivity.

(3)Reflects the non-service component of net periodic pension income and, for the three months ended March 31, 2026, also includes $5 million related to the resolution of certain environmental liabilities not directly related to the Company's operations.

(4)Reflects third-party costs directly attributable to the refinancing of our credit facilities and any amendments.

Adjusted EBIT for the Three Months Ended March 31, 2026

For the three months ended March 31, 2026, net income increased by $33 million versus the prior period as discussed above within Results of Operations for Three Months Ended March 31, 2026.

Adjusted EBIT increased by $20 million compared to the prior period driven by $19 million of higher volumes, $13 million of benefit from foreign currency impacts, $7 million of lower RD&E costs, $4 million of favorable impacts from product mix and $2 million of commodity, transportation and energy deflation. This increase was partially offset by $14 million of lower productivity and $11 million of pricing net of inflation pass-through.

During the three months ended March 31, 2026, we saw volume growth across all verticals. Gasoline growth was driven by new application launches and program ramp-ups in Europe. Diesel growth was due to strong demand for light commercial vehicles and pickup trucks in North and South America, Southeast Asia and application launches in India. Commercial vehicles/industrial growth was driven by strong demand for commercial vehicles in all key regions, as well as continued industrial growth. Aftermarket volumes also increased across all regions for commercial vehicle parts, resulting in a favorable product mix.

The increased productivity from our ability to flex our variable cost structure while driving sustained fixed cost productivity was more than offset by year-over-year labor inflation, higher stock based compensation and the timing of our productivity actions. Our overall financial results for the three months ended March 31, 2026 were also impacted by the timing of customer recoveries.

Gains in foreign currency from translational, transactional, and hedging effects in the three months ended March 31, 2026, primarily driven by a higher Chinese Yuan-to-U.S. dollar versus the prior period, accounted for a $13 million increase in Adjusted EBIT.

29

Liquidity and Capital Resources

Overview

| March 31, 2026 | December 31, 2025 | ||||||||||

| (Dollars in millions) | |||||||||||

| Cash and cash equivalents | $ | 142 | $ | 177 | |||||||

| Restricted cash | 2 | 2 | |||||||||

| Revolving Facility - available borrowing capacity | 630 | 630 | |||||||||

| Revolving Facility - borrowings or letters of credit outstanding | — | — | |||||||||

| Term Loan Facilities - principal outstanding | 635 | 637 | |||||||||

| Senior Notes - principal outstanding | 800 | 800 | |||||||||

| Bilateral letter of credit facility - utilized capacity | 10 | 10 | |||||||||