UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL REPORT PURSUANT TO REGULATION A OF THE SECURITIES ACT OF 1933

For the fiscal year ended: December 31, 2025

| Red Oak Capital Fund III, LLC |

| (Exact name of issuer as specified in its charter) |

| Delaware | 84-2079441 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

5925 Carnegie Blvd, Suite 110

Charlotte, NC 28209

(Full mailing address of principal executive offices)

(616) 343-0697

(Issuer’s telephone number, including area code)

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION AND FIGURES

This Annual Report on Form 1-K, or the Annual Report, of Red Oak Capital Fund III, LLC and its subsidiaries (collectively, the “Company”), a Delaware limited liability company, contains certain forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are generally identified by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “outlook,” “seek,” “anticipate,” “estimate,” “approximately,” “believe,” “could,” “project,” “predict,” or other similar words or expressions. Forward-looking statements are based on certain assumptions, discuss future plans and strategies, contain projections or state other forward-looking information. Our ability to predict the results or the actual effect of future events, actions, plans or strategies is inherently uncertain. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth or anticipated in our forward-looking statements. Factors that could have a material adverse effect on our forward-looking statements and upon our business, results of operations, financial condition, funds derived from operations, cash available for distribution, cash flows, liquidity and prospects include, but are not limited to, the factors referenced in certain of our offering circulars, filed pursuant to Rule 253(c)2, under the caption “RISK FACTORS” and which are available at www.sec.gov.

In particular, this Annual Report contains forward-looking statements regarding the Company’s plan to liquidate its assets in an orderly manner pursuant to a Forbearance Agreement with UMB Bank, N.A., as Indenture Trustee, including statements about expected asset values, estimated costs and receipts during the liquidation period, the anticipated timeline for property dispositions, and the Company’s ability to satisfy its obligations to bondholders and other creditors. These forward-looking statements are subject to significant risks and uncertainties, including the Company’s ability to comply with the milestones set forth in the Forbearance Agreement, the actual proceeds realized from the sale of assets, the timing and cost of renovations, market conditions affecting property values and sale timelines, and the outcome of legal proceedings. Actual results may differ materially from those projected.

When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this report. Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our views as of the date of this report. The matters summarized below and elsewhere in this report could cause our actual results and performance to differ materially from those set forth or anticipated in forward-looking statements. Accordingly, we cannot guarantee future results or performance. Furthermore, except as required by law, we are under no duty to, and we do not intend to, update any of our forward-looking statements after the date of this report, whether as a result of new information, future events or otherwise.

All figures provided herein are approximate.

| 2 |

Item 1. Business

Red Oak Capital Fund III, LLC, a Delaware limited liability company, was formed on June 12, 2019, to acquire and manage commercial real estate loans and securities and other real estate-related debt instruments. Since July 2023, our assets have comprised exclusively of various real estate assets and available cash. We actively manage our assets through our manager, Red Oak Capital GP, LLC, or our Manager, who has also engaged third party asset and property managers, as well as project managers and general contractors to assist in the management and repositioning of our real property assets.

We filed an offering statement on Form 1-A, or the Offering Statement, with the United States Securities and Exchange Commission, or the SEC, on June 25, 2019, which was qualified by the SEC on September 18, 2019. Pursuant to the Offering Statement, we offered a minimum of $2.0 million in the aggregate and a maximum of $50.0 million in the aggregate of the Company’s 6.5% Series A and 8.5% Series B senior secured bonds, or the Bonds, respectively (the “Offering”). The purchase price per Bond was $1,000, with a minimum purchase amount of $10,000. Proceeds from the sale of the Bonds were used to invest primarily in unsecuritized senior commercial mortgage notes, or property loans, and to pay or reimburse selling commissions and other fees and expenses associated with the Offering. As of December 23, 2019, the Offering reached the maximum aggregate raise of $50.0 million through issuing $4.4 million and $45.6 million of Series A and Series B Bonds, respectively. Upon issuance of the maximum amount, the debt issuance costs incurred were approximately $4.5 million, resulting in net proceeds of approximately $45.5 million.

As described below under “Adoption of Liquidation Basis of Accounting,” on November 21, 2025, the Company entered into a Forbearance Agreement with UMB Bank, N.A., as Indenture Trustee, and adopted a plan to liquidate its remaining assets in an orderly manner. Effective December 1, 2025, the Company adopted the liquidation basis of accounting in accordance with Accounting Standards Codification (“ASC”) Topic 205-30, Presentation of Financial Statements—Liquidation Basis of Accounting. As of December 31, 2025, the Company held three properties acquired through foreclosure or deed-in-lieu of foreclosure and was in the process of repositioning and liquidating these assets pursuant to the Forbearance Agreement.

We are managed by our Manager, which is wholly owned by Red Oak Capital Holdings, LLC, or our Sponsor, a Charlotte, North Carolina based commercial real estate finance company specializing in the acquisition, processing, underwriting, operational management and servicing of commercial real estate debt instruments. Our Sponsor is wholly controlled by Red Oak Holdings Management, LLC, a Delaware limited liability company.

We do not have any employees. We rely on the employees of our Sponsor, as the sole member of our Manager, and its affiliates for the day-to-day operation of our business.

| 3 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

General

We commenced loan operations upon the first closing of our Offering on September 27, 2019. To date we have received approximately $45,500,000 in net proceeds from our Offering. Since the Offering reached the maximum allowable raise on December 23, 2019, the Company does not anticipate any further issuance of bonds.

As a result of macro events, most recently including inflation and geopolitical developments, but predominantly the COVID-19 pandemic, the Company’s loan portfolio experienced significant distress, and the Company acquired all of its remaining properties through foreclosure or deed-in-lieu of foreclosure. On February 3, 2025, the Company announced that it would no longer make regular quarterly payments of interest associated with its outstanding Bonds and would begin the process of liquidating its assets in an effort to provide the liquidity to pay off the principal and accrued interest associated with the Bonds. On March 10, 2025, UMB Bank, N.A., as the Indenture Trustee, issued a Notice of Events of Default and Reservation of Rights. On November 21, 2025, the Company entered into a Forbearance Agreement with the Indenture Trustee (the “Forbearance Agreement”), which provides for an orderly liquidation of the Company’s remaining real estate assets over an approximately two-year period.

As a result, effective December 1, 2025, the Company adopted the liquidation basis of accounting in accordance with ASC 205-30. The accompanying consolidated financial statements for the period from December 1, 2025 through December 31, 2025 are presented on the liquidation basis of accounting. The consolidated financial statements for the eleven months ended November 30, 2025 and the year ended December 31, 2024 continue to be presented on the going concern basis of accounting. Results for the liquidation period are not comparable to results for the going concern periods.

Adoption of Liquidation Basis of Accounting

On November 21, 2025, the Company executed a Forbearance Agreement with UMB Bank, N.A., as Indenture Trustee for the holders of the Company’s Series B Bonds, pursuant to which the Indenture Trustee agreed to forbear from exercising its remedies under the Trust Indenture for a defined period while the Company executes an orderly liquidation of its remaining real estate assets. The Forbearance Agreement was the culmination of a process that began with the Company’s February 3, 2025 announcement that it would cease regular quarterly interest payments and pursue an asset liquidation strategy, followed by the Indenture Trustee’s Notice of Events of Default on March 10, 2025, and the Company’s presentation of a Plan of Liquidation to bondholders on June 30, 2025.

The Company’s Plan of Liquidation contemplates the following key actions: (i) completing remaining renovations at the two Natchez, Mississippi hotel properties; (ii) operating the hotels only to the extent necessary to preserve asset value prior to sale; (iii) marketing and selling all remaining real estate assets in accordance with the disposition milestones set forth in the Forbearance Agreement; and (iv) applying sale proceeds in accordance with the legal priority established under the Trust Indenture, with Series B bondholders having priority claims on the net proceeds.

| 4 |

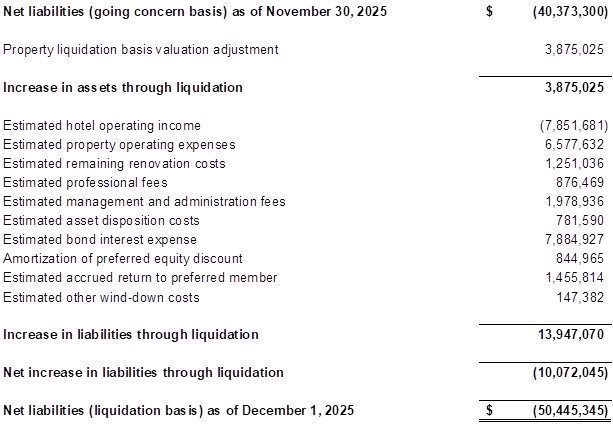

The Company determined that liquidation became imminent upon execution of the Forbearance Agreement on November 21, 2025, as this event satisfied the criteria set forth in ASC 205-30-25-2. The Company adopted a convenience date of December 1, 2025 for the transition to the liquidation basis of accounting. Management evaluated the impact of the nine-day period from November 21, 2025 through November 30, 2025 and determined the effect on the consolidated financial statements to be immaterial.

Under the liquidation basis of accounting, assets are measured at their estimated cash amounts expected to be collected, and liabilities are measured at their estimated settlement amounts through the end of the liquidation period. The Company presents its real estate assets at estimated values on a gross basis, with estimated costs to complete renovations, disposition costs, and other expected costs during the liquidation period accrued separately as liabilities. In accordance with ASC 205-30, estimated future cash flows are not discounted to present value. The Company currently estimates that the liquidation period will extend through December 31, 2027.

As of December 31, 2025, the Company’s net liabilities in liquidation were approximately $50.0 million, reflecting total estimated assets of approximately $21.4 million and total estimated liabilities of approximately $71.4 million. The Company does not expect to have sufficient assets to fully satisfy all of its outstanding obligations, including the full amount of principal and accrued interest due to Series B bondholders.

Results of Operations

For the Eleven Months Ended November 30, 2025 (Going Concern Basis)

The following discussion presents the Company’s results of operations for the eleven-month period ended November 30, 2025, which are presented on the going concern basis of accounting. Due to the adoption of the liquidation basis of accounting effective December 1, 2025 and the shortened reporting period, these results are not directly comparable to the full year ended December 31, 2024.

As of November 30, 2025, the Company did not hold any senior secured loans and held three properties acquired via foreclosure or deed-in-lieu of foreclosure with a carrying value of approximately $17.2 million, net of accumulated depreciation and accumulated impairment.

On April 25, 2025, ROCFIII Southfield, LLC, a wholly owned subsidiary of the Company, sold the medical office building located in Southfield, Michigan at auction. The Company received approximately $0.8 million in net proceeds from the sale on June 2, 2025, resulting in a realized loss of approximately $86,000. Following the sale, the Company’s real estate portfolio consisted of three properties: the Vue Hotel and the Bridges Hotel, both located in Natchez, Mississippi; and the Pembroke property.

During 2024, the Company authorized the special purpose entities associated with the two Natchez hotel properties to issue preferred membership interests to Red Oak Capital Properties, LLC (“ROCP,” whose rights and obligations were assumed by Red Oak Capital Holdings, LLC as successor-by-merger effective June 13, 2025), a related party. ROCFIII Vue Hotel, LLC issued preferred interests of up to $3.3 million at 8% per annum, maturing September 1, 2027. ROCFIII 10 Grand Soleil, LLC issued preferred interests of up to $2.1 million at 8% per annum, maturing September 1, 2027. Through November 30, 2025, ROCP had invested approximately $6.7 million in aggregate across both entities, including protective advances of approximately $1.3 million which accrue interest at 14% per annum.

| 5 |

On July 25, 2025, ROCFIII Pembroke, LLC, a wholly owned subsidiary of the Company, obtained a $1,650,000 senior secured note from Red Oak Income Opportunity Fund II, LLC (“ROIOF II”), a related party under common ownership. The note is secured by the Pembroke property and is subject to certain reserve requirements.

For the eleven months ended November 30, 2025, the Company’s total revenues, consisting of rental revenue of $390,912 and bank interest income of $17,617, amounted to $408,529. Operating costs for the same period, including bond interest expense of $4,040,928, interest on preferred membership liability of $991,276, property expenses of $1,651,100, management fees of $705,513, professional fees of $397,889, note interest expense of $70,696, and depreciation expense of $319,953, amounted to $8,177,355. The Company also recognized net other expense of $300,902, consisting of a realized loss on property of $85,694, unrealized loss on property of $707,981, and a change in fair value of derivative liability of $492,773. Net loss for the eleven months ended November 30, 2025 amounted to $8,069,728.

Rental revenue decreased modestly compared to the year ended December 31, 2024, primarily due to the Southfield property being sold in April 2025 and the Vue Hotel remaining offline for renovations during the period, partially offset by the reopening of the Bridges Hotel in the second quarter of 2025. Property expenses increased due to the resumption of hotel operations at the Bridges Hotel. Bond interest expense decreased on a pro rata basis as compared to the prior year, reflecting an eleven-month period versus a twelve-month period. Interest on the preferred membership liability increased as ROCP continued to fund preferred investments throughout 2025. Professional fees increased due to legal costs associated with the Forbearance Agreement negotiations and the Trust Instruction Proceeding.

For the One Month Ended December 31, 2025 (Liquidation Basis)

Effective December 1, 2025, the Company adopted the liquidation basis of accounting. Under the liquidation basis, the Company no longer reports results of operations in the traditional sense. Instead, the Company reports changes in net liabilities in liquidation, which reflect the estimated costs and receipts expected during the remaining liquidation period.

Upon adoption of the liquidation basis of accounting on December 1, 2025, the Company remeasured its assets to estimated values on a gross basis, representing the estimated cash amounts expected to be collected through the disposition of each property. Liabilities were adjusted to include accruals for estimated costs expected to be incurred during the liquidation period, including remaining renovation costs, property operating expenses, professional fees, disposition costs, interest on the Series B Bonds at the contractual rate of 8.5%, and amounts due to the preferred membership interest holder and other creditors.

As of December 1, 2025, net liabilities in liquidation were approximately $50.4 million. During the one month ended December 31, 2025, net liabilities in liquidation decreased by approximately $0.5 million, resulting in net liabilities in liquidation of approximately $50.0 million as of December 31, 2025. The decrease was primarily attributable to capital contributions from the Managing Member of $386,237, a net favorable remeasurement of assets in liquidation of $8,099, and a net favorable remeasurement of liabilities in liquidation of $91,220. See Note 4 to the consolidated financial statements for additional detail regarding the components of net liabilities in liquidation and the methods and significant assumptions underlying the Company’s estimates.

| 6 |

For the Year Ended December 31, 2024 (Going Concern Basis)

The following discussion presents the Company’s results of operations for the year ended December 31, 2024, which are presented on the going concern basis of accounting.

As of December 31, 2024, the Company did not hold any senior secured loans and held four properties acquired via foreclosure or deed-in-lieu of foreclosure with a carrying value of $16,374,629, net of $3,644,249 in accumulated depreciation and accumulated impairment. See the property footnote in the consolidated financial statements for additional information.

On September 1, 2024, ROCFIII Vue Hotel, LLC, which owns the hotel located in Natchez, Mississippi, formerly owned by RVH Investments, Inc., amended its operating agreement to accept Red Oak Capital Properties, LLC, a related party, as a Preferred Member. The preferred investment is up to $3.3 million, accrues interest at 8% per annum, and matures on September 1, 2027. Through December 31, 2024, Red Oak Capital Properties, LLC had invested $2,508,423.

On September 1, 2024, ROCFIII 10 Grand Soleil, LLC, which owns the hotel located in Natchez, Mississippi, formerly owned by ONRD, Inc., amended its operating agreement to accept Red Oak Capital Properties, LLC, a related party, as a Preferred Member. The preferred investment is up to $2.1 million, accrues interest at 8% per annum, and matures on September 1, 2027. Through December 31, 2024, Red Oak Capital Properties, LLC had invested $2,239,991. The $189,991 invested above the preferred investment amount is treated as a protective advance and accrues protective interest at 14% per annum.

Under the terms of each JV entity’s amended and restated limited liability company agreement, the Preferred Member may make Protective Advances to the entity when funds are needed to cure or prevent a loan default, fund a shortfall, or otherwise meet the entity’s obligations. Each Protective Advance accrues a return at 14% per annum (the “Protective Rate”), non-compounding, and is repaid on a priority basis from net cash flow and net capital proceeds ahead of distributions to the Common Member. The outstanding Protective Balance and accrued Protective Return must be returned by the earlier of the full repayment of the Preferred Payment Amount or the Preferred Investment Maturity Date (September 1, 2027). The Common Member may return any Protective Advance at any time by funding an amount equal to the Protective Balance plus accrued Protective Return.

The distribution of net cash flow from operations and net sale proceeds of the two JV entities follows a structured priority. For net cash flow, 100% is first allocated to the Preferred Member until they have received all accrued Preferred Current Returns, defined as 8% of the net Preferred Investment per annum, then to the Preferred Member for any outstanding Protective Balance and accrued Protective Return, with any remaining net cash flow distributed entirely to ROCFIII (the “Common Member”). Similarly, for net sale proceeds, the initial distribution is 100% to the Preferred Member until they receive all accrued Preferred Current Returns and any outstanding Protective Balance and Protective Return, then 100% to the Preferred Member until the entire Preferred Investment has been returned. Thereafter, any residual proceeds are distributed on a pro rata basis, with 10% to the Preferred Member (the “contingent return”) and the remaining to the Common Member. The Preferred Member retains certain rights to approve “Major Decisions” as defined in the limited liability agreements upon any event of Material Default. Upon a Material Default or the third anniversary of the Preferred Investment, the Common Member must cause the entity to immediately prepay the net Preferred Investment, any Protective Advances, and any accrued returns.

| 7 |

For the year ended December 31, 2024, the Company’s total revenues from operations, including rental income of $479,394 and bank interest income of $110,597, amounted to $589,991. Operating costs for the same period, including bond interest expense of $4,459,991, property expenses of $2,175,233, and management fees of $777,897, amounted to $8,089,669. Net loss for the period amounted to $7,724,398. Rental revenues and expenses decreased from 2023 as a result of pulling two hotels offline for part of 2024 for full renovations.

Liquidity and Capital Resources

As of December 31, 2025, the Company had sold $4,386,000 and $45,614,000 of Series A and Series B Bonds, respectively, pursuant to its offering of Bonds. On September 15, 2022, the Company elected to redeem all outstanding Series A Bonds. As of December 31, 2025, $43,980,000 of Series B Bonds remained outstanding. No Series B Bonds were redeemed during the year ended December 31, 2025.

On February 3, 2025, the Company announced that it would no longer make regular quarterly payments of interest associated with its outstanding Bonds. As of that date, the Company had made all payments of interest through December 31, 2024. The Company did not make payments of interest for any quarter during 2025. On March 10, 2025, UMB Bank, N.A., as the Indenture Trustee, issued a Notice of Events of Default and Reservation of Rights, asserting that the Company’s announcement constituted a default under the covenants of the Bonds.

On November 21, 2025, the Company entered into the Forbearance Agreement with the Indenture Trustee. Under the Forbearance Agreement, the Indenture Trustee agreed to forbear from exercising its remedies under the Trust Indenture while the Company executes its Plan of Liquidation, subject to the Company’s compliance with specified disposition milestones and reporting requirements. The Forbearance Agreement provides for an orderly liquidation of the Company’s remaining assets over an approximately two-year period.

As of December 31, 2025, cash on hand was $103,224. The Company’s primary anticipated sources of liquidity during the liquidation period are proceeds from the disposition of its remaining real estate assets and capital contributions from the Managing Member. The Company has not identified any additional external sources of financing and there is no assurance that such sources would be available.

The bond service reserve that was required pursuant to the Trust Indenture, equal to 3.75% of gross proceeds from the Offering ($1,875,000), was depleted on October 23, 2020. No bond service reserves were available as of December 31, 2025.

Under the liquidation basis of accounting, the Company has accrued estimated costs expected to be incurred and estimated receipts expected to be received during the remaining liquidation period. As of December 31, 2025, net liabilities for estimated costs in excess of estimated receipts through liquidation of approximately $2.2 million were accrued, reflecting estimated future property operating expenses, remaining renovation costs, professional fees, disposition costs, management and administration fees, and other wind-down costs, net of estimated hotel operating income during the pre-sale period. See Note 4 to the consolidated financial statements for additional detail. The Company’s ability to fund its operations and satisfy its obligations during the liquidation period is dependent on the successful execution of the Plan of Liquidation, including the timely disposition of assets at values consistent with or in excess of current estimates.

| 8 |

As of December 31, 2025, the Company’s net liabilities in liquidation were approximately $50.0 million. The Company does not expect to fully satisfy all of its outstanding obligations from the proceeds of its asset liquidation. Under the terms of the Trust Indenture and Forbearance Agreement, net proceeds from asset dispositions will be applied in accordance with the legal priority established thereunder, with amounts due to Series B bondholders having priority over the Managing Member’s equity interest in the Company.

Trend Information

The Company reached the maximum allowable raise and closed its Offering as of December 23, 2019. As such, the Company will no longer issue additional bonds. The Company is focused on executing its Plan of Liquidation through the orderly repositioning and disposition of its remaining real estate assets.

Subsequent to December 31, 2025, the following developments have occurred:

Pembroke Property. ROCFIII Pembroke, LLC entered into a binding purchase and sale agreement for the Pembroke property at a sale price of $2,650,000. The sale is expected to close in May 2026.

Vue Hotel Renovations. Renovations on the property owned by ROCFIII Vue Hotel, LLC are expected to be completed and the hotel is expected to reopen in May 2026. Upon completion of renovations and stabilization of operations, the Company expects property-level net operating income to increase, resulting in an increase to the property’s market value; however, the magnitude and timeframe are uncertain and subject to operating performance, market conditions, and other factors.

10 Grand Soleil Hotel. Renovations on the property owned by ROCFIII 10 Grand Soleil, LLC (the Bridges Hotel) were completed in the fourth quarter of 2024. The hotel is operating and generating revenue. The Company continues to seek to stabilize operations and maximize the property’s value prior to disposition.

| 9 |

Trust Instruction Proceeding. On February 17, 2026, UMB Bank, N.A., in its capacity as Indenture Trustee, filed a Trust Instruction Proceeding (“TIP”) petition in the Hennepin County District Court, State of Minnesota, Fourth Judicial District (Court File No. 27-TR-CV-26-8), captioned In the Matter of the Trusteeship Under the Indenture between Red Oak Capital Fund III, LLC and UMB Bank, N.A. as Trustee, seeking an order from the court, among other things, approving the Indenture Trustee’s execution of the Forbearance Agreement. On April 1, 2026, the court held a hearing on the petition, at which no objections were submitted. On April 7, 2026, the court entered Findings of Fact, Conclusions of Law and Order (the “TIP Order”), granting the relief requested. The TIP Order approves and confirms the Indenture Trustee’s execution of, and continued performance under, the Forbearance Agreement, finds that the Plan of Liquidation is in the best interest of the holders of the Series B Bonds, and authorizes and instructs the Indenture Trustee to take such actions as are consistent with and reasonably necessary to effectuate the transactions contemplated by the Forbearance Agreement.

Managing Member Capital Contributions. Through the date of this report, the Managing Member has contributed approximately $1.6 million in aggregate capital to the Company to fund Vue Hotel renovations and operating shortfalls. Of this amount, approximately $0.5 million was contributed through December 31, 2025 (including $0.1 million during the going concern period and $0.4 million during the liquidation period), and approximately $1.1 million was contributed subsequent to year-end. These contributions are subordinate to all bondholder claims under the Trust Indenture.

The Company’s ability to successfully execute its Plan of Liquidation is subject to significant risks and uncertainties, including market conditions, the timing and cost of completing renovations, the Company’s ability to comply with disposition milestones under the Forbearance Agreement, and the actual proceeds realized from the sale of assets. There can be no assurances that these actions will generate sufficient cash flows to repay all outstanding liabilities, including the interest and principal due to the Series B bondholders.

| 10 |

Item 3. Directors, Executive Officers and Significant Employees

The following table sets forth information on our board of managers and executive officers of our Sponsor as of the date of this submission. We are managed by our Manager, which is majorly owned and controlled by our Sponsor. Consequently, we do not have our own separate board of managers or executive officers.

| Name |

| Age |

| Position with our Company |

| Director/Officer Since |

| Gary Bechtel |

| 68 |

| Chief Executive Officer |

| August 2020 |

| Kevin P. Kennedy |

| 60 |

| Chief Sales and Distribution Officer* |

| November 2019 |

| Raymond T. Davis |

| 59 |

| President and Chief Strategy Officer* |

| March 2025 (President) November 2019 (Chief Strategy Officer) |

| Paul Cleary |

| 62 |

| Chief Operating Officer |

| March 2022 |

| Thomas McGovern |

| 47 |

| Chief Financial Officer |

| April 2022 |

| Robert Kaplan |

| 55 |

| Chief Legal Officer and EVP |

| March 2023 |

| Matthew Webster |

| 59 |

| Chief Credit Officer and EVP |

| March 2025 |

*Member of the board of managers of the Sponsor, which controls our Manager, which controls our Company.

Gary Bechtel is Chief Executive Officer of our Sponsor and a member of the board of managers of ROHM. Gary previously served as President of Money360 and was responsible for developing and executing Money360’s growth strategy. Gary also served as Money360’s Chief Credit Officer. Prior to joining Money360, he was Chief Lending Officer of CU Business Partners, LLC, the nation’s largest credit union service organization (CUSO). Previously, Gary held management or production positions with Garn & Ellis Company, Meridian Capital, Johnson Capital, and JMB Capital. Gary began his career with the Allison Company and over the past thirty-four years has been involved in all aspects of the commercial real estate finance industry, as a lender and as an intermediary.

Kevin P. Kennedy is a founding partner, Chief Sales and Distribution Officer of our Sponsor and a member of the board of managers of ROHM. He is responsible for capital acquisition, platform distribution and broker dealer relationships. Kevin has more than 25 years of experience in investment management. He previously served as Managing Director and National Sales Director at BlackRock Investment Management Corporation and, prior to BlackRock, served as a Director and Vice President for Merrill Lynch Investment Managers covering the Midwest region. Kevin holds Series 7, 24, 63 and 65 securities licenses. He received his Bachelor of Arts degree from the University of Pennsylvania.

| 11 |

Raymond T. Davis is President and Chief Strategy Officer of our Sponsor and a member of the board of managers of ROHM. He is responsible for the Company’s long-term business strategy, including supporting our lending product development, and leading capital strategy, which includes concurrently developing strategic offerings with investment partners amongst the independent broker dealer community, family offices and pension funds. Ray has more than 20 years of management experience. Since 2014, Ray has focused his operational and strategic skills on implementing policy, process and operational enhancements for various investment funds and vehicles distributed in the independent broker dealer community. Ray has served both private companies and registered alternative investment funds in various senior roles. Ray attended Wayne State University.

Paul Cleary is Chief Operating Officer of our Sponsor. Paul brings nearly 25 years of national commercial real estate lending experience involving small-balance originations, construction loans, as well as a federally chartered credit union’s national CRE loan portfolio. He most recently served as a Senior Loan Originator for Parkview Financial, a national private mid-market commercial construction lender. He previously served as Chief Operating Officer for Money360, a national private mid-market commercial real estate lender. Prior to joining Money360, Paul was a founding member and the EVP, National Production Manager for Cherrywood Commercial Lending. Paul has held management or production positions with Kinecta Federal Credit Union, Impac Commercial Capital, Hawthorne Savings, Fremont Investment and Loan, as well as FINOVA Realty Capital. He earned a Master’s degree in Business Administration from the University of California, Irvine, a Juris Doctor degree (JD) from the University of San Diego School of Law and a Bachelor’s degree with a Political Science concentration from the University of California, Santa Barbara.

Thomas McGovern is Chief Financial Officer of our Sponsor. Thomas is responsible for leading the financial accounting and reporting function, including supporting the capital raising and investor relations efforts. Thomas previously served as Interim Chief Financial Officer for Westchester Insurance. Thomas is an experienced M&A consultant covering both non-depository lenders and financial institution sponsors and previously served as an Executive Director at Barclays Securities International. He also served depository and non-depository lenders as a financial institution specialist at Morgan Stanley. Thomas has been a sell-side equity research analyst at Lehman Brothers covering banks and thrifts for the top ranked institutional investor mortgage & specialty finance research group. He earned an MBA from the Darden Graduate School of Business at the University of Virginia and a B.A. in Economics from Hamilton College, where he graduated summa cum laude. Thomas is a Certified Public Accountant (CPA), holds the Chartered Financial Analyst (CFA) designation, and the Series 79 securities license.

Robert R. Kaplan, Jr. serves as Chief Legal Officer and Executive Vice President for Corporate Development of our Sponsor. Throughout his nearly 30-year career, Robert has represented clients and worked in such diverse industries as financial services and products, real estate, technology, professional sports, manufacturing and retail/consumer products. He has completed more than $4 billion worth of securities transactions, including registered and exempt securities offerings, private equity and institutional investment, real estate funds and syndications and REITs, in addition to institutional financings of real estate acquisitions and M&As. Recognized in Best Lawyers in America within his fields each year since 2013, Robert was selected as “Lawyer of the Year” by Best Lawyers® for leveraged buyouts and private equity law. From 2012 to 2016, the Governor of the Commonwealth of Virginia called on Robert to serve on the Virginia Board of Housing and Community Development. Rob received his J.D. from the Marshall-Wythe School of Law at the College of William & Mary and his A.B. from the College of William & Mary.

| 12 |

Matthew Webster serves as Chief Credit Officer and Executive Vice President of our Sponsor. Matthew leads the Sponsor’s credit strategy, portfolio risk management, and underwriting operations. Matthew brings more than 30 years of experience in capital markets, structured finance, and risk management having worked across balance sheet and securitized lending, senior and mezzanine debt, equity investments, and non-performing loan acquisitions. He has structured and executed over $250 billion in transactions and worked with some of the world’s most sophisticated institutional investors, including sovereign wealth funds, global REITs, and alternative asset managers. Matthew previously served as Global Head of Real Estate Finance at HSBC, managing more than $100 billion in commercial real estate exposure. His expertise spans key roles at Morgan Stanley, Goldman Sachs, Hypo Real Estate, and Fitch Ratings, where he led major capital markets initiatives and advised regulatory bodies on financial stability and capital requirements. Matthew holds a Chartered Financial Analyst (CFA) certificate and earned dual bachelor’s degrees in Business Management and Economics from North Carolina State University.

Director and Executive Compensation

Our Company does not have executives. It is operated by our Manager. We will not reimburse our Manager for any portion of the salaries and benefits paid to its executive officers.

| 13 |

Item 4. Security Ownership of Management and Certain Security Holders

The table below sets forth, as of the issuance date of this report, certain information regarding the beneficial ownership of our outstanding membership units for (1) each person who is expected to be the beneficial owner of 5% or more of our outstanding membership units, and (2) each of our named executives and managers. Each person named in the table has sole voting and investment power with respect to all membership units shown as beneficially owned by such person. The SEC has defined “beneficial ownership” of a security to mean the possession, directly or indirectly, of voting power and/or of investment power over such security.

| Title of Class |

| Name and Address of Beneficial Owner* |

| Amount and Nature of Beneficial Ownership** |

| Percent of Class |

| Common Units |

| Red Oak Capital Holdings, LLC |

| 6,000 |

| 100% (1) |

| Common Units |

| Gary Bechtel |

| 6,000 |

| 100% (2) |

| Common Units |

| Kevin Kennedy |

| 6,000 |

| 100% (3) |

| Common Units |

| Raymond Davis |

| 6,000 |

| 100% (4) |

| Common Units |

| All Executives and Managers as a group |

| 6,000 |

| 100% |

* Unless otherwise noted above, the address of the persons and entities listed in the table is c/o 5925 Carnegie Boulevard, Suite 110, Charlotte, North Carolina 28209.

** Under SEC rules, a person is deemed to be a “beneficial owner” of a security if that person has or shares “voting power,” which includes the power to vote or direct the voting of such security, or “investment power,” which includes the power to dispose of or to direct the disposition of such security. A person also is deemed to be a beneficial owner of any securities which that person has a right to acquire within 60 days. Under these rules, more than one person may be deemed to be a beneficial owner of the same securities, and a person may be deemed to be a beneficial owner of securities regardless of whether he or she has any economic or pecuniary interest in such securities.

(1) Issued to our Sponsor, Red Oak Capital Holdings, LLC (“Sponsor”), in consideration for a capital commitment of $1,500,000, which may be called at times and in amounts in the discretion of the Manager. As such, each of Messrs. Bechtel, Kennedy and Davis have shared voting and dispositive power over such Common Units owned by our Sponsor. Messrs. Bechtel, Kennedy and Davis are officers of our Sponsor, which is the sole member of our Manager, and on the board of managers of Red Oak Holdings Management, LLC (“ROHM”), which is the manager of, and holder of 100% of the voting interests in, our Sponsor. Messrs. Bechtel, Kennedy and Davis collectively own a majority of the non-voting units of our Sponsor. Each disclaims beneficial ownership of the shares held by our Sponsor, except to the extent of their proportionate pecuniary interest therein.

(2) Reflects Common Units held by our Sponsor, of which ROHM is the manager and holder of 100% of the voting interests. Mr. Bechtel is an officer of our Sponsor, which is the sole member of our Manager, and a member of the board of managers of ROHM, and as such, is deemed to have shared voting and dispositive power over the shares held by our Sponsor. Mr. Bechtel disclaims beneficial ownership of shares held by our Sponsor, except to the extent of his proportionate pecuniary interest therein.

(3) Reflects Common Units held by our Sponsor, of which ROHM is the manager and holder of 100% of the voting interests. Mr. Kennedy is an officer of our Sponsor, which is the sole member of our Manager, and a member of the board of managers of ROHM, and as such, is deemed to have shared voting and dispositive power over the shares held by our Sponsor. Mr. Kennedy disclaims beneficial ownership of shares held by our Sponsor, except to the extent of his proportionate pecuniary interest therein.

(4) Reflects Common Units held by our Sponsor, of which ROHM is the manager and holder of 100% of the voting interests. Mr. Davis is an officer of our Sponsor, which is the sole member of our Manager, and a member of the board of managers of ROHM, and as such, is deemed to have shared voting and dispositive power over the shares held by our Sponsor. Mr. Davis disclaims beneficial ownership of shares held by our Sponsor, except to the extent of his proportionate pecuniary interest therein.

| 14 |

Item 5. Interest of Management and Others in Certain Transactions

For further details, please see Note 9, Related Party Transactions in Item 7, Consolidated Financial Statements.

Item 6. Other Information

None

| 15 |

Item 7. Financial Statements

RED OAK CAPITAL FUND III, LLC AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

AND

INDEPENDENT AUDITOR'S REPORT

DECEMBER 31, 2025 AND DECEMBER 31, 2024

| 16 |

| Red Oak Capital Fund III, LLC and Subsidiaries |

| ||

|

| |||

|

|

|

|

|

|

|

|

|

|

|

| 18-19 |

| |

|

|

|

|

|

| Financial Statements |

|

|

|

|

|

|

|

|

| Consolidated Statements of Net Liabilities in Liquidation (Liquidation Basis) |

| 20 |

|

|

|

|

|

|

|

| 21 |

| |

|

|

|

|

|

| Consolidated Statement of Changes in Net Liabilities in Liquidation (Liquidation Basis) |

| 22 |

|

|

|

|

|

|

|

| 23 |

| |

|

|

|

|

|

| Consolidated Statements of Changes in Member's Deficit (Going Concern Basis) |

| 24 |

|

|

|

|

|

|

|

| 25 |

| |

|

|

|

|

|

|

| 26-39 |

|

| 17 |

| Table of Contents |

To the Managing Member

Red Oak Capital Fund III, LLC and Subsidiaries

Opinion

We have audited the accompanying consolidated financial statements of Red Oak Capital Fund III, LLC (the “Company,” a Delaware limited liability corporation), which comprise the consolidated balance sheets as of November 30, 2025 and December 31, 2024, and the related consolidated statements of operations, changes in member’s deficit, and cash flows for the period from January 1, 2025 to November 30, 2025 and for the year ended December 31, 2024, the consolidated statement of net liabilities in liquidation as December 31, 2025, the related consolidated statement of changes in net liabilities in liquidation for the period from December 1, 2025 to December 31, 2025, and the related notes to the consolidated financial statements.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of November 30, 2025 and December 31, 2024, and the results of its operations, changes in member’s deficit, and cash flows for the period from January 1, 2025 to November 30, 2025 and for the year ended December 31, 2024, as well as the net liabilities in liquidation as of December 31, 2025, and the changes in net liabilities in liquidation for the period from December 1, 2025 to December 31, 2025, in accordance with accounting principles generally accepted in the United States of America.

Basis for Opinion

We conducted our audits in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of the Company and to meet our other ethical responsibilities in accordance with the relevant ethical requirements relating to our audits. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Basis of Accounting

As described in Note 2 to the consolidated financial statements, the Company executed a Forbearance Agreement with UMB Bank, N.A., requiring the Company to implement an orderly liquidation of its assets. As a result, the Company changed its basis of accounting for periods subsequent to November 30, 2025 from the going concern basis to a liquidation basis. Generally accepted accounting principles require financial statements to be prepared on the liquidation basis of accounting when an entity is in liquidation or when liquidation is imminent. Our opinion is not modified with respect to that matter.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

| 18 |

| Table of Contents |

To the Managing Member

Red Oak Capital Fund III, LLC and Subsidiaries

Page Two

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the financial statements.

In performing an audit in accordance with GAAS, we:

|

| · | Exercise professional judgment and maintain professional skepticism throughout the audit. |

|

|

|

|

|

| · | Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. |

|

|

|

|

|

| · | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed. |

|

|

|

|

|

| · | Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the financial statements. |

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audit.

Other Information Included in the Company’s Annual Report

Management is responsible for the other information included in the Company’s annual report. The other information comprises the Company’s annual report on Form 1-K, but it does not include the financial statements and our auditor’s report thereon. Our opinion on the financial statements does not cover the other information, and we do not express an opinion or any form of assurance on it.

In connection with our audit of the financial statements, our responsibility is to read the other information and consider whether a material inconsistency exists between the other information and the financial statements, or other information otherwise appears to be materially misstated. If, based on the work performed, we conclude that an uncorrected material misstatement of the other information exists, we are required to describe it in our report.

/s/ UHY LLP

Farmington Hills, Michigan

April 30, 2026

| 19 |

| Table of Contents |

|

|

|

| ||

| Consolidated Statements of Net Liabilities in Liquidation |

|

| ||

| (Liquidation Basis) |

|

| ||

|

|

|

|

| |

|

|

| December 31, 2025 |

| |

|

|

|

|

| |

| Assets |

|

|

| |

|

|

|

|

| |

| Property, net realization value |

| $ | 21,053,000 |

|

| Cash and cash equivalents |

|

| 103,224 |

|

| Other current assets |

|

| 73,154 |

|

| Mortgage loan interest reserves |

|

| 168,433 |

|

|

|

|

|

|

|

| Total assets |

| $ | 21,397,811 |

|

|

|

|

|

|

|

| Liabilities |

|

|

|

|

|

|

|

|

|

|

| Bond interest payable |

| $ | 11,214,900 |

|

| Note interest payable |

|

| 93,846 |

|

| Accrued return to preferred member |

|

| 2,051,387 |

|

| Due to managing member |

|

| 2,369,667 |

|

| Other current liabilities |

|

| 160,658 |

|

| Series B bonds payable |

|

| 43,980,000 |

|

| Net liabilities for estimated costs through liquidation |

|

| 2,154,966 |

|

| Preferred membership interest |

|

| 6,677,077 |

|

| Derivative liability |

|

| 1,005,099 |

|

| Mortgage loan payable |

|

| 1,650,000 |

|

|

|

|

|

|

|

| Total liabilities |

| $ | 71,357,600 |

|

|

|

|

|

|

|

| Net liabilities in liquidation |

| $ | (49,959,789) | |

| 20 |

| Table of Contents |

|

|

|

| ||||||

| Consolidated Balance Sheets |

|

|

|

| ||||

| (Going Concern Basis) |

|

|

|

| ||||

|

|

| November 30, 2025 |

|

| December 31, 2024 |

| ||

|

|

|

|

|

|

|

| ||

| Assets |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

| ||

| Current assets: |

|

|

|

|

|

| ||

| Cash and cash equivalents |

| $ | 253,312 |

|

| $ | 1,154,587 |

|

| Accounts receivable |

|

| - |

|

|

| 35,165 |

|

| Other current assets |

|

| 65,055 |

|

|

| 34,350 |

|

| Prepaid expenses |

|

| - |

|

|

| 4,125 |

|

| Mortgage loan interest reserves |

|

| 182,527 |

|

|

| - |

|

| Total current assets |

|

| 500,894 |

|

|

| 1,228,227 |

|

|

|

|

|

|

|

|

|

|

|

| Long-term assets: |

|

|

|

|

|

|

|

|

| Property, net |

|

| 17,177,975 |

|

|

| 16,374,629 |

|

| Total long-term assets |

|

| 17,177,975 |

|

|

| 16,374,629 |

|

|

|

|

|

|

|

|

|

|

|

| Total assets |

| $ | 17,678,869 |

|

| $ | 17,602,856 |

|

|

|

|

|

|

|

|

|

|

|

| Liabilities and Member's Deficit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Current liabilities: |

|

|

|

|

|

|

|

|

| Interest payable |

| $ | 3,437,912 |

|

| $ | 934,575 |

|

| Accrued return to preferred member |

|

| 595,573 |

|

|

| 96,509 |

|

| Due to managing member |

|

| 766,229 |

|

|

| 39,290 |

|

| Other current liabilities |

|

| 161,088 |

|

|

| 45,818 |

|

| Series B bonds payable, net |

|

| 43,922,998 |

|

|

| 43,308,845 |

|

| Accounts payable |

|

| 771,537 |

|

|

| 726,977 |

|

| Total current liabilities |

|

| 49,655,337 |

|

|

| 45,152,014 |

|

|

|

|

|

|

|

|

|

|

|

| Long-term liabilities: |

|

|

|

|

|

|

|

|

| Preferred membership liability, net |

|

| 5,832,112 |

|

|

| 3,411,237 |

|

| Derivative liability, at fair value |

|

| 952,735 |

|

|

| 1,445,508 |

|

| Mortgage loans payable, net |

|

| 1,611,985 |

|

|

| - |

|

| Total long-term liabilities |

|

| 8,396,832 |

|

|

| 4,856,745 |

|

|

|

|

|

|

|

|

|

|

|

| Member's deficit |

|

| (40,373,300) |

|

| (32,405,903) | ||

|

|

|

|

|

|

|

|

|

|

| Total liabilities and member's deficit |

| $ | 17,678,869 |

|

| $ | 17,602,856 |

|

| 21 |

| Table of Contents |

|

|

| |||||||||

| Consolidated Statement of Changes in Net Liabilities in Liquidation | ||||||||||

| (Liquidation Basis) |

|

|

| |||||||

|

|

|

|

| |||||||

|

|

| For the Period December 1, 2025 through December 31, 2025 |

| |||||||

|

|

|

|

| |||||||

| Net liabilities in liquidation, December 1, 2025 |

| $ | (50,445,345) | |||||||

| Changes in net liabilities in liquidation |

|

|

|

| ||||||

| Remeasurement of assets in liquidation |

|

| 8,099 |

| ||||||

| Remeasurement of liabilities in liquidation |

|

| 91,220 |

| ||||||

| Manager contributions |

|

| 386,237 |

| ||||||

| Changes in net liabilities in liquidation |

|

| 485,556 |

| ||||||

| Net liabilities in liquidation, December 31, 2025 |

| $ | (49,959,789) | |||||||

| 22 |

| Table of Contents |

|

|

|

| ||||||

| Consolidated Statements of Operations |

|

|

|

| ||||

| (Going Concern Basis) |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

| ||

|

|

| For the Period Ending November 30, 2025 |

|

| For the Year Ending December 31, 2024 |

| ||

|

|

|

|

|

|

|

| ||

| Revenue: |

|

|

|

|

|

| ||

| Bank interest income |

| $ | 17,617 |

|

| $ | 110,597 |

|

| Rental revenue |

|

| 390,912 |

|

|

| 479,394 |

|

| Total revenue |

|

| 408,529 |

|

|

| 589,991 |

|

|

|

|

|

|

|

|

|

|

|

| Expenses: |

|

|

|

|

|

|

|

|

| Bond interest expense |

|

| 4,040,928 |

|

|

| 4,459,991 |

|

| Note interest expense |

|

| 70,696 |

|

|

| - |

|

| Interest on preferred membership liability |

|

| 991,276 |

|

|

| 235,969 |

|

| Management fees |

|

| 705,513 |

|

|

| 777,897 |

|

| Professional fees |

|

| 397,889 |

|

|

| 190,363 |

|

| Property expenses |

|

| 1,651,100 |

|

|

| 2,175,233 |

|

| Depreciation expense |

|

| 319,953 |

|

|

| 250,216 |

|

| Total expenses |

|

| 8,177,355 |

|

|

| 8,089,669 |

|

|

|

|

|

|

|

|

|

|

|

| Other income (expense) |

|

|

|

|

|

|

|

|

| Realized gain on extinguished debt |

|

| - |

|

|

| 47,500 |

|

| Realized loss on property, net |

|

| (85,694) |

|

| - |

| |

| Change in fair value of derivative liability |

|

| 492,773 |

|

|

| 31,130 |

|

| Unrealized loss on property, net |

|

| (707,981) |

|

| (303,350) | ||

| Total other income (expense) |

|

| (300,902) |

|

| (224,720) | ||

|

|

|

|

|

|

|

|

|

|

| Net loss |

| $ | (8,069,728) |

| $ | (7,724,398) | ||

| 23 |

| Table of Contents |

|

|

|

| ||

| Consolidated Statements of Changes in Member's Deficit |

|

|

| |

| (Going Concern Basis) |

|

|

| |

|

|

| Managing Member |

| |

|

|

|

|

| |

| Member's deficit, January 1, 2024 |

| $ | (24,681,505) | |

|

|

|

|

|

|

| Net loss |

|

| (7,724,398) | |

|

|

|

|

|

|

| Member's deficit, January 1, 2025 |

| $ | (32,405,903) | |

|

|

|

|

|

|

| Capital contributions |

|

| 102,331 |

|

|

|

|

|

|

|

| Net loss |

|

| (8,069,728) | |

|

|

|

|

|

|

| Member's deficit, November 30, 2025 |

| $ | (40,373,300) | |

| 24 |

| Table of Contents |

|

|

|

|

| |||||

| Consolidated Statements of Cash Flows |

|

|

|

| ||||

| (Going Concern Basis) |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

| ||

|

|

| For the Period Ending November 30, 2025 |

|

| For the Year Ending December 31, 2024 |

| ||

|

|

|

|

|

|

|

| ||

| Cash flows from operating activities: |

|

|

|

|

|

| ||

| Net loss |

| $ | (8,069,728) |

| $ | (7,724,398) | ||

|

|

|

|

|

|

|

|

|

|

| Adjustments to reconcile net loss to net cash |

|

|

|

|

|

|

|

|

| used in operating activities: |

|

|

|

|

|

|

|

|

| Amortization of debt issuance costs |

|

| 1,117,851 |

|

|

| 834,022 |

|

| Depreciation expense |

|

| 319,953 |

|

|

| 250,216 |

|

| Realized loss on property, net |

|

| 85,694 |

|

|

| - |

|

| Unrealized loss on property, net |

|

| 707,981 |

|

|

| 303,350 |

|

| Change in fair value of derivative liability |

|

| (492,773) |

|

| (31,130) | ||

| Change in other operating assets and liabilities: |

|

|

|

|

|

|

|

|

| Net change in other current assets |

|

| (30,705) |

|

| 67,863 |

| |

| Net change in accounts receivable |

|

| 35,165 |

|

|

| (33,165) | |

| Net change in due from related parties |

|

| - |

|

|

| (348) | |

| Net change in prepaid expenses |

|

| 4,125 |

|

|

| (4,125) | |

| Net change in bond interest payable |

|

| 2,503,337 |

|

|

| (14,981) | |

| Net change in accrued return to preferred member |

|

| 499,064 |

|

|

| 96,509 |

|

| Net change in due to managing member |

|

| 726,939 |

|

|

| 39,290 |

|

| Net change in other current liabilities |

|

| 115,270 |

|

|

| (68,746) | |

| Net change in accounts payable |

|

| 44,560 |

|

|

| 472,403 |

|

|

|

|

|

|

|

|

|

|

|

| Net cash used in operating activities |

|

| (2,433,267) |

|

| (5,860,740) | ||

|

|

|

|

|

|

|

|

|

|

| Cash flows from investing activities: |

|

|

|

|

|

|

|

|

| Capitalized expenditures on property held |

|

| (2,757,956) |

|

| (4,419,915) | ||

| Proceeds from sale of property, net |

|

| 840,982 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| Net cash used in investing activities |

|

| (1,916,974) |

|

| (4,419,915) | ||

|

|

|

|

|

|

|

|

|

|

| Cash flows from financing activities: |

|

|

|

|

|

|

|

|

| Contributions |

|

| 102,331 |

|

|

| - |

|

| Proceeds from preferred membership liability |

|

| 1,928,662 |

|

|

| 4,748,414 |

|

| Proceeds from mortgage loans |

|

| 1,417,973 |

|

|

| - |

|

| Redemptions of Series B Bonds |

|

| - |

|

|

| (657,500) | |

|

|

|

|

|

|

|

|

|

|

| Net cash provided by financing activities |

|

| 3,448,966 |

|

|

| 4,090,914 |

|

|

|

|

|

|

|

|

|

|

|

| Net change in cash and cash equivalents |

|

| (901,275) |

|

| (6,189,741) | ||

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents, beginning of period |

|

| 1,154,587 |

|

|

| 7,344,328 |

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents, end of period |

| $ | 253,312 |

|

| $ | 1,154,587 |

|

|

|

|

|

|

|

|

|

|

|

| Supplemental non-cash disclosures of cash flow information: |

|

|

|

|

|

|

|

|

| Interest paid |

| $ | 934,575 |

|

| $ | 3,778,356 |

|

| 25 |

| Table of Contents |

| Red Oak Capital Fund III, LLC and Subsidiaries Notes to Financial Statements December 31, 2025 and December 31, 2024 |

1. Organization

Red Oak Capital Fund III, LLC, (the “Company”) formerly known as Red Oak Capital Fixed Income III, LLC, is a Delaware limited liability company formed to originate senior loans collateralized by commercial real estate in the United States of America. The Company’s plan is to originate, acquire, and manage commercial real estate loans and securities and other commercial real estate-related debt instruments. Red Oak Capital GP, LLC is the Managing Member and owns 100% of the member interests in the Company.

The Company was formed on June 12, 2019 and commenced operations on September 27, 2019. The Company raised a maximum of $50 million of Series A Bonds and Series B Bonds pursuant to an exemption from registration under Regulation A of the Securities Act of 1933, as amended. The minimum offering requirement of $2 million was achieved and an initial closing was held on September 27, 2019 whereby the initial offering proceeds were released from escrow. The Company’s term is indefinite.

The Company’s operations may be affected by macro events, including inflation, geopolitical developments, and tariffs on key imports and exports. Possible effects of these events may include, but are not limited to, delay of construction on properties, an increase in rehabilitation costs, higher rate of borrowings, and delayed asset sale closing periods. Any future disruption which may be caused by these developments is uncertain; however, it may result in a material adverse impact on the Company’s financial position, operations and cash flows.

The Company issued a notice to bondholders on February 3, 2025 that the Company did not have adequate cash flow or cash on hand to make further interest payments. UMB Bank, N.A. as the trustee of the Series B bond indenture, issued a Notice of Events of Default and Reservation of Rights, asserting that the Company’s February 3, 2025 announcement constituted a default under the covenants of the Bonds.

On November 21, 2025, the Company executed a Forbearance Agreement with UMB Bank, N.A., the Trustee. Under the terms of the Forbearance Agreement, the Trustee agreed to temporarily forbear from exercising certain remedies under the Bond Documents while the Company executes its Plan of Liquidation. As discussed further in Note 2, the Company adopted the liquidation basis of accounting effect December 1, 2025 (see Note 3).

The Managing Member plans to address these matters by liquidating the portfolio of assets in an orderly manner in an effort to maximize value and distribute the proceeds to the bondholders. They plan to complete their renovations of two operating hotels and bring them to full occupancy, which they believe will generate the largest amount of proceeds from the subsequent liquidation.

There can be no assurances that these actions will generate sufficient cash flows to repay all outstanding liabilities, including the interest and principal due to the Series B bondholders.

2. Plan of liquidation

On November 21, 2025, the Company executed a Forbearance Agreement with UMB Bank, N.A. requiring the Company to implement an orderly liquidation of its assets. The Forbearance Agreement was preceded by the Company’s February 3, 2025 communication to bondholders stating that the Company did not have adequate cash flow or cash on hand to make further interest payments, and a Notice of Default issued by the Trustee on March 10, 2025. The Plan of Liquidation was formally presented to bondholders on June 30, 2025. The Plan of Liquidation includes:

| 26 |

| Table of Contents |

| Red Oak Capital Fund III, LLC and Subsidiaries Notes to Financial Statements December 31, 2025 and December 31, 2024 |

2. Plan of liquidation (continued)

|

| 1. | Completing the remaining renovations at the two Natchez hotel properties; |

|

| 2. | Operating the hotels only to the extent necessary to preserve asset value prior to sale; |

|

| 3. | Marketing and selling all real estate assets in accordance with the disposition milestones specified in the Forbearance Agreement: |

|

| 4. | Applying all liquidation proceeds in accordance with legal priority, including settlement of the Series B Bonds and preferred membership interests; and |

|

| 5. | Settling all other obligations expected to arise during the liquidation period. |

Management currently anticipates the liquidation period may extend through approximately December 2027, although timing is dependent on market conditions, renovation completion, and adherence to Forbearance Agreement milestones.

Under the terms of the Forbearance Agreement, the Trustee may terminate forbearance and exercise full remedies, including acceleration of the Series B Bonds, if the Company fails to meet specified milestones or otherwise defaults under the agreement. As of the date of these financial statements, the Company had not met certain disposition milestones under the Forbearance Agreement, including obtaining a binding purchase and sale agreement for the Pembroke property by the December 31, 2025 deadline. The Company is continuing discussions with the Trustee regarding these matters, and the Trustee has not, as of such date, terminated the forbearance. Subsequent to year-end, the Pembroke property was placed under contract.

On February 17, 2026, UMB Bank, N.A., as Trustee, filed a Trust Instruction Proceeding (“TIP”) petition in the Hennepin County District Court, State of Minnesota. The TIP seeks a court order approving the Trustee’s execution of the Forbearance Agreement and directs the Trustee to take such actions as are consistent with and reasonably necessary to effectuate the transactions contemplated by the Forbearance Agreement. On April 1, 2026, the court held a hearing on the petition, at which no objections were submitted. On April 7, 2026, the court entered Findings of Fact, Conclusions of Law and Order (the “TIP Order”), granting the relief requested. The TIP Order approves and confirms the Indenture Trustee’s execution of, and continued performance under, the Forbearance Agreement, finds that the Plan of Liquidation is in the best interest of the holders of the Series B Bonds, and authorizes and instructs the Indenture Trustee to take such actions as are consistent with and reasonably necessary to effectuate the transactions contemplated by the Forbearance Agreement.

3. Significant accounting policies

Going Concern Basis

Basis of presentation

The financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States ("GAAP") and all values are stated in United States dollars.

Principles of consolidation

The consolidated financial statements include the accounts of Red Oak Capital Fund III, LLC and its wholly owned operating subsidiaries, ROCFIII Vue Hotel, LLC, ROCFIII 10 Grand Soleil, LLC, and ROCFIII Pembroke, LLC (collectively, the "Company"). All significant inter-company transactions and account balances have been eliminated.

Use of estimates

The preparation of the financial statements requires the Managing Member to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. The Managing Member believes the estimates utilized in preparing the Company’s financial statements are reasonable and prudent; however, actual results could differ from these estimates and such differences could be material to the Company's financial statements.

| 27 |

| Table of Contents |

| Red Oak Capital Fund III, LLC and Subsidiaries Notes to Financial Statements December 31, 2025 and December 31, 2024 |

3. Significant accounting policies (continued)

Fair value – hierarchy of fair value

In accordance with FASB ASC 820-10, Fair Value Measurements and Disclosures, the Company discloses the fair value of its assets and liabilities in a hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to valuations based upon unadjusted quoted prices in active markets for identical assets and liabilities and the lowest priority to valuations based upon unobservable inputs that are significant to the valuation. FASB ASC 820-10-35-39 to 55 provides three levels of the fair value hierarchy as follows:

Level One - Inputs use quoted prices in active markets for identical assets or liabilities of which the Company has the ability to access.

Level Two - Inputs use other inputs that are observable, either directly or indirectly. These Level 2 inputs include quoted prices for similar assets and liabilities in active markets, and other inputs such as interest rates and yield curves that are observable at commonly quoted intervals.

Level Three - Inputs are unobservable inputs, including inputs that are available in situations where there is little, if any, market activity for the related asset.

In instances whereby inputs used to measure fair value fall into different levels of the fair value hierarchy, fair value measurements in their entirety are categorized based on the lowest level input that is significant to the valuation. The Company’s assessment of the significance of particular inputs to these fair value measurements requires judgement and considers factors specific to each asset or liability.

Cash and cash equivalents

Cash represents cash deposits held at financial institutions. Cash equivalents may include short-term highly liquid investments of sufficient credit quality that are readily convertible to known amounts of cash and have original maturities of three months or less. Cash equivalents are carried at cost, plus accrued interest, which approximates fair value. Cash equivalents are held to meet short-term liquidity requirements, rather than for investment purposes.

Cash and cash equivalents are held at major financial institutions and are subject to credit risk to the extent those balances exceed applicable Federal Deposit Insurance Corporation or Securities Investor Protection Corporation limitations.

Property, net

Property is initially recorded at lower of cost or fair value less estimated costs to sell establishing a new cost basis. Depreciation is recorded using the straight-line method over the estimated useful lives of the assets, currently 30 years. Physical possession of commercial real estate property collateralizing a commercial mortgage loan occurs when legal title is obtained upon completion of foreclosure or when the borrower conveys all interest in the property to satisfy the loan through completion of a deed in lieu of foreclosure or through a similar legal agreement. If fair value declines subsequent to foreclosure, an impairment charge will be recorded as an unrealized loss.

Mortgage loans receivable

As of December 31, 2025, the Company no longer holds any mortgage loans receivable and does not anticipate originating or acquiring new loans going forward.

| 28 |

| Table of Contents |

| Red Oak Capital Fund III, LLC and Subsidiaries Notes to Financial Statements December 31, 2025 and December 31, 2024 |

3. Significant accounting policies (continued)

Allowance for credit losses

As of December 31, 2025, the Company no longer holds any mortgage loans receivable and does not anticipate originating or acquiring new loans going forward in connection with its Plan of Liquidation. Accordingly, there are no financial assets subject to credit loss estimation, and an allowance for credit losses under ASC 326 (CECL) has not been recorded. Management has concluded that the allowance for loan losses/CECL methodology is no longer applicable to the Company’s financial statements.

Revenue recognition and accounts receivable