2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

These accompanying financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

The accompanying financial statements include the accounts of the Company and its subsidiaries and associates. Intercompany transactions and balances were eliminated in consolidation. The Company has adopted December 31 as its fiscal year end.

The accompanying consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries and majority-owned subsidiaries which the Company controls and entities for which the Company is the primary beneficiary. For those consolidated subsidiaries where the Company’s ownership is less than 100%, the outside shareholders’ interests are shown as non-controlling interests in equity. Acquired businesses are included in the consolidated financial statements from the date on which control is transferred to the Company. Subsidiaries are deconsolidated from the date that control ceases. All inter-company accounts and transactions have been eliminated in consolidation.

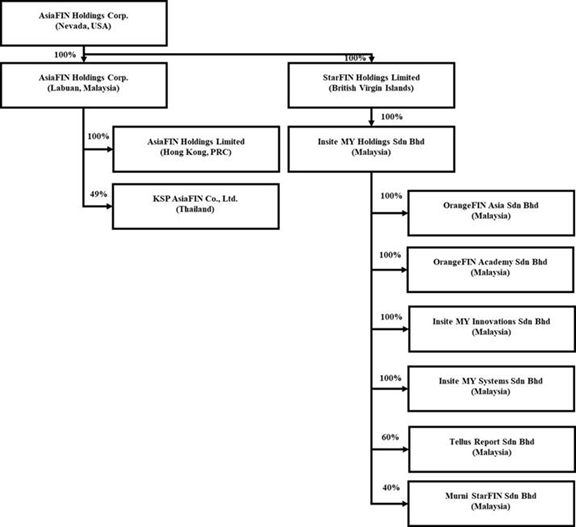

Below is the organization chart of the Group.

Use of Estimates

In preparing these financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheets and revenues and expenses during the years reported. Actual results may differ from these estimates.

Cash and Cash Equivalents

The Company considers short-term, highly liquid investments with an original maturity of 90 days or less to be cash equivalents.

Our deposits in Malaysian banks are secured by Perbadanan Insurans Deposit Malaysia, compensating up to a limit of Malaysia Ringgit per deposit per member bank, which is equivalent to $61,771, if any of our banks fail.

Property, Plant and Equipment

Property, plant and equipment are stated at cost, with depreciation and amortization provided using the straight-line method over the following periods:

| Asset Categories | Depreciation Periods | |

| Renovation | ||

| Computer Systems | 4 to 5 years | |

| Furniture and Fittings | 10 years | |

| Electrical Fittings | 10 years | |

| Handphone | 5 years | |

| Office Equipment | 10 years | |

| Motor Vehicle | 5 years | |

| Property | 50 years |

Credit losses

The Company estimates and records a provision for its expected credit losses related to its financial instruments, including its trade receivables. Management considers historical collection rates, the current financial status of the Company’s customers, macroeconomic factors, and other industry-specific factors when evaluating current expected credit losses. Forward-looking information is also considered in the evaluation of current expected credit losses. However, because of the short time to the expected receipt of accounts receivable, management believes that the carrying value, net of expected losses, approximates fair value and therefore, relies more on historical and current analysis of such financial instruments, including its trade receivables.

Credit loss rate is determined by historical collection based on aging schedule, adjusted for current conditions using reasonable and supportable forecasts. Based on the aging categorization and the adjusted loss rate per category, an allowance for credit losses is calculated by multiplying the adjusted loss rate with the amortized cost in the respective age category.

In July 2025, the FASB issued ASU 2025-05, Financial Instruments—Credit Losses (Topic 326), which introduces a practical expedient for measuring expected credit losses on trade receivables and contract assets. Under ASU 2025-05, an entity is required to disclose whether it has elected to use the practical expedient. An entity that makes the accounting policy election is required to disclose the date through which subsequent cash collections are evaluated. ASU 2025-05 is effective for fiscal years beginning after December 15, 2025, and interim periods within fiscal years beginning after December 15, 2026. Early adoption is permitted. The Company already adopted this ASU on its consolidated financial statements and related disclosure. The Company has elected practical expedient under ASU 2025-05 for the quarter ended March 31, 2026 which permits assuming that current conditions as of the balance sheet date will remain unchanged for the remaining life of the asset when estimating expected credit losses. Accordingly, the Company’s estimate of the allowance for expected credit losses on current accounts receivable is determined by applying an adjusted loss rate to the amortized cost of receivables within each respective aging category, based on historical data over a 25-month period.

Investment in associate

The Company accounts for its investment in associate in accordance with ASC Topic 323, “Investments – Equity Method and Joint Ventures”, whereby equity investments of 20% or greater, but less than a controlling interest, are accounted for using the equity method. Under this method, the investment is initially recorded at cost and subsequently adjusted for the Company’s proportionate share of the investee’s net income or loss, which is recognized in the consolidated statements of operations and comprehensive income, with a corresponding adjustment to the carrying value of the investment. The Company evaluates its equity method investments for potential significant influence, if the Company became primary beneficiary, it could consolidate the investee and recognize a noncontrolling interest for the portion not owned.

Revenue recognition

The Company through subsidiaries generate multiple streams of revenues based on different business model adopted by each subsidiary through provisions of services and recognized upon customer obtained control of promised services and recognized in an amount that reflects the consideration that the Company expects to receive in exchange for those services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The Company applies the following five-step model in order to determine this amount:

| (i) | Identify contract with customer; |

| (ii) | Identify distinct performance obligations in contract, including promises if any; |

| (iii) | Measurement of the transaction price, including the constraint on variable consideration; |

| (iv) | Allocation of the transaction price to the performance obligations; and |

| (v) | Recognition of revenue when (or as) the Company satisfies each performance obligation. |

The Company adopted ASU 2014-09, Revenue from Contracts with Customers (Topic 606). Under Topic 606, the Company records revenue when persuasive evidence of an arrangement exists, delivery has occurred, the fee is fixed or determinable and collectability is probable. The Company records revenue from the delivery of the finalized information technology services such as business system integration and management services, computer programming activities and services to the customers (see Note 3).

Cost of revenue

Cost of revenue includes direct costs associated with provision of services such as development costs, purchases of third-party software, maintenance fees and consultation fees.

Income tax expense

Income taxes are determined in accordance with the provisions of ASC Topic 740, “Income Taxes” (“ASC Topic 740”). Under this method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. The Company also adopted ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures”, which requires disaggregated information about the reporting entity’s effective tax rate reconciliation as well as information on income taxes paid.

ASC 740 prescribes a comprehensive model for how companies should recognize, measure, present, and disclosed in their financial statements uncertain tax positions taken or expected to be taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement with the tax authority assuming full knowledge of the position and relevant facts.

The Company conducts major businesses in Malaysia and is subject to tax in their own jurisdictions. As a result of its business activities, the Company will file separate tax returns that are subject to examination by the foreign tax authorities.

Foreign currencies translation

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the statement of operations and comprehensive income (loss).

The functional currency of the Company is the United States Dollars (“US$” or “US dollars”) and the accompanying financial statements have been expressed in US dollars. In addition, the Company’s subsidiary maintains its books and record in Malaysia Ringgit (“MYR”), United States Dollars (“US$”), Hong Kong Dollars (“HK$”) and Thailand Baht (“THB”), which is the respective functional currency as being the primary currency of the economic environment in which the entity operates.

In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US dollars are translated into US dollars, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiary are recorded as a separate component of accumulated other comprehensive income.

Translation of amounts from the local currency of the Company into US$1 has been made at the following exchange rates for the respective periods:

For

the three months ended | ||||||||

| 2026 | 2025 | |||||||

| Period-end MYR : US$1 exchange rate | 4.05 | 4.44 | ||||||

| Period-average MYR : US$1 exchange rate | 3.96 | 4.45 | ||||||

| Period-end HK$ : US$1 exchange rate | 7.84 | 7.78 | ||||||

| Period-average HK$ : US$1 exchange rate | 7.81 | 7.78 | ||||||

| Period-end THB : US$1 exchange rate | 32.69 | 33.95 | ||||||

| Period-average THB : US$1 exchange rate | 31.59 | 33.93 | ||||||

Related parties

Parties, which can be a corporation or individual, are considered to be related if the Company has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Companies are also considered to be related if they are subject to common control or common significant influence.

Net Income/(Loss) per Share

The Company calculates net income/(loss) per share in accordance with ASC Topic 260, “Earnings per Share.” Basic income/(loss) per share is computed by dividing the net income/(loss) by the weighted-average number of common shares outstanding during the period. Diluted income per share is computed similar to basic income/(loss) per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common stock equivalents had been issued and if the additional common shares were dilutive.

Lease

The Company leases offices for fixed periods with pre-emptive extension options. The Company recognizes lease payments for its short-term lease on a straight-line basis over the lease term.

Lease liability is initially and subsequently measured at the present value of the unpaid lease payments at the lease commencement date. The right-of-use asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for lease payments made at or before the lease commencement date, plus any initial direct costs incurred less any lease incentives received. Costs associated with operating lease assets are recognized on a straight-line basis within operating expenses over the term of the lease.

In determining the present value of the unpaid lease payments, ASC 842 requires a lessee to discount its unpaid lease payments using the interest rate implicit in the lease or, if that rate cannot be readily determined, its incremental borrowing rate. As most of the Company leases do not provide an implicit rate, the Company uses its incremental borrowing rate as the discount rate for the lease. The Company’s incremental borrowing rate is estimated to approximate the interest rate on a collateralized basis with similar terms and payments.

Segment Reporting

The Company follows the guidance of ASC 280, “Segment Reporting”, which establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organization structure as well as information about services categories, business segments and major customers in financial statements. For the three months ended March 31, 2026, the Company has three reportable segments based on business unit, Payment Processing (Fintech), Regulatory Technology (RegTech) and Robotic Process Automation (RPA) businesses and two reportable segments based on country, Malaysia and Non-Malaysia. The Company also adopted ASU 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures”, which expands annual and interim disclosure requirements for reportable segments, primarily through enhanced disclosures about significant segment expenses.

Recently Issued Accounting Standards

In November 2024, the FASB issued ASU 2024-03, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40), which requires enhanced disclosures of certain income statement expenses. In January 2025, the FASB issued ASU 2025-01 to clarify the effective date of ASU 2024-03. The standard is effective for fiscal years beginning after December 15, 2026, and interim periods within fiscal years beginning after December 15, 2027. Early adoption is permitted, either prospectively or retrospectively.

The Company reviews new accounting standards as issued. Management has not identified any other new standards that it believes will have a significant impact on the Company’s financial statements.