UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the Quarterly Period Ended

or

For the transition period from ______ to ______

Commission

File Number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification Number) |

(Address of principal executive offices, including zip code)

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding twelve months (or shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ☐ | Accelerated Filer ☐ | Smaller reporting company | ||||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE

PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

N/A

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at May 12, 2026 | |

| Common Stock, $0.0001 par value |

TABLE OF CONTENTS

-i-

PART I — FINANCIAL INFORMATION

ITEM 1. CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

ASIAFIN HOLDINGS CORP.

CONDENSED CONSOLIDATED BALANCE SHEETS

AS OF MARCH 31, 2026 (UNAUDITED) AND DECEMBER 31, 2025 (AUDITED)

(Currency expressed in United States Dollars (“US$”), except for number of shares or otherwise stated)

As of 2026 | As of 2025 | |||||||

| Unaudited | Audited | |||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | |||||||

| Account receivables, net | ||||||||

| Prepayment, deposits and other receivables | ||||||||

| Contract assets | ||||||||

Amount due from related parties (including $ | ||||||||

| Tax assets | ||||||||

| Total current assets | $ | |||||||

| Non-current Assets | ||||||||

| Right-of-use assets, net | $ | |||||||

| Property, plant and equipment, net | ||||||||

| Investment in associates | ||||||||

| Total non-current assets | $ | |||||||

| TOTAL ASSETS | $ | |||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

| Current liabilities | ||||||||

| Accrued liabilities and other payables | $ | |||||||

| Account payables (including $ | ||||||||

| Contract liabilities | ||||||||

| Income tax payable | ||||||||

| Amount due to director | ||||||||

| Finance lease liability – current portion | ||||||||

| Operating lease liability – current portion | ||||||||

| Total current liabilities | $ | |||||||

| Non-current liabilities | ||||||||

| Amount due to director – non-current portion | ||||||||

| Finance lease liability – non-current portion | ||||||||

| Operating lease liability – non-current portion | ||||||||

| Deferred tax liabilities | ||||||||

| Total non-current liabilities | $ | |||||||

| TOTAL LIABILITIES | $ | |||||||

| SHAREHOLDERS’ EQUITY | ||||||||

| Preferred shares, $ | $ | |||||||

| Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Non-controlling interest | ( | ) | ( | ) | ||||

| TOTAL SHAREHOLDERS’ EQUITY | $ | |||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | |||||||

See accompanying notes to unaudited condensed consolidated financial statements.

F-1

ASIAFIN HOLDINGS CORP.

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF OPERATIONS AND COMPREHENSIVE LOSS

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Currency expressed in United States Dollars (“US$”), except for number of shares or otherwise stated)

Three months March 31, | Three months ended March 31, 2025 | |||||||

| REVENUE | $ | $ | ||||||

| COST OF REVENUE (including $ | ( | ) | ( | ) | ||||

| GROSS PROFIT/(LOSS) | $ | $ | ( | ) | ||||

| SHARE OF LOSS FROM OPERATION OF ASSOCIATE | ( | ) | ( | ) | ||||

| OTHER INCOME (including $ | ||||||||

| SELLING, GENERAL AND ADMINISTRATIVE EXPENSES (including $ | ( | ) | $ | ( | ) | |||

| LOSS BEFORE INCOME TAX | ( | ) | $ | ( | ) | |||

| INCOME TAX EXPENSES | ||||||||

| NET LOSS | ( | ) | $ | ( | ) | |||

| Net loss attributable to non-controlling interest | ||||||||

| NET LOSS ATTRIBUTED TO COMMON SHAREHOLDERS OF ASIAFIN HOLDINGS CORP. | ( | ) | ( | ) | ||||

| Other comprehensive income: | ||||||||

| - Foreign currency translation loss | ||||||||

| TOTAL COMPREHENSIVE LOSS | ( | ) | $ | ( | ) | |||

| NET LOSS PER SHARE, BASIC AND DILUTED | ( | ) | ( | ) | ||||

| WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING, BASIC AND DILUTED | ||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

F-2

ASIAFIN HOLDINGS CORP.

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF SHAREHOLDERS’ EQUITY

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Currency expressed in United States Dollars (“US$”), except for number of shares or otherwise stated)

| COMMON STOCK | ADDITIONAL | SHARE SUBSCRIPTIONS | ACCUMULATED OTHER | NON- | TOTAL | |||||||||||||||||||||||||||

| NUMBER OF SHARES | AMOUNT | PAID-IN CAPITAL | RECEIVED

IN ADVANCE | ACCUMULATED DEFICIT | COMPREHENSIVE LOSS | CONTROLLING INTEREST | SHAREHOLDERS’ EQUITY | |||||||||||||||||||||||||

| Balance as of December 31, 2024 | | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | | |||||||||||||||||

| New issuance of shares on January 20, 2025 | ||||||||||||||||||||||||||||||||

| Share subscriptions received in advance | - | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation | - | |||||||||||||||||||||||||||||||

| Balance as of March 31, 2025 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||

| COMMON STOCK | ADDITIONAL | ACCUMULATED OTHER | NON- | TOTAL | ||||||||||||||||||||||||

| NUMBER OF SHARES | AMOUNT | PAID-IN CAPITAL | ACCUMULATED DEFICIT | COMPREHENSIVE LOSS | CONTROLLING INTEREST | SHAREHOLDERS’ EQUITY | ||||||||||||||||||||||

| Balance as of December 31, 2025 | | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | | ||||||||||||||

| Net loss for the period | - | ) | - | ) | ( | ) | ||||||||||||||||||||||

| Foreign currency translation | - | - | ||||||||||||||||||||||||||

| Balance as of March 31, 2026 | $ | $ | $ | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements

F-3

ASIAFIN HOLDINGS CORP.

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Currency expressed in United States Dollars (“US$”), except for number of shares or otherwise stated)

Three Months Ended March 31, 2026 | Three Months March 31, 2025 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net profit to net cash used in operating activities: | ||||||||

| Depreciation and amortization | ||||||||

| Share of loss from operation of associate | ||||||||

| Disposal of asset | ( | ) | ||||||

| Provision for credit loss allowance | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Account payables | ( | ) | ||||||

| Account receivables | ( | ) | ||||||

| Prepayment, deposits and other receivables | ||||||||

| Contract assets | ( | ) | ||||||

| Accrued liabilities and other payables | ( | ) | ( | ) | ||||

| Contract liabilities | ||||||||

| Tax assets | ( | ) | ( | ) | ||||

| Income tax payable | ( | ) | ( | ) | ||||

| Change in lease liability | ( | ) | ( | ) | ||||

| Net cash used in operating activities | $ | ( | ) | $ | ( | ) | ||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchase of property, plant and equipment | ( | ) | ( | ) | ||||

| Disposal of property, plant and equipment | ||||||||

| Net cash used in investing activities | $ | ( | ) | $ | ( | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from issuance of common shares | ||||||||

| Advance to director | ( | ) | ( | ) | ||||

| Repayment of finance lease liabilities | ( | ) | ||||||

| Advances to related companies | ( | ) | ( | ) | ||||

| Net cash used in financing activities | $ | ( | ) | $ | ( | ) | ||

| Effect of exchange rate changes on cash and cash equivalents | $ | $ | ||||||

| Net decrease in cash and cash equivalents | $ | ( | ) | $ | ( | ) | ||

| Cash and cash equivalents, beginning of period | ||||||||

| CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | $ | ||||||

| SUPPLEMENTAL CASH FLOWS INFORMATION | ||||||||

| Cash paid for income taxes | $ | $ | ||||||

| Cash paid for interest paid | $ | $ | ||||||

| SUPPLEMENTAL NON-CASH INVESTING AND FINANCING ACTIVITIES: | ||||||||

| Initial recognition of operating lease right-of-use assets and operating lease obligations upon adoption of ASC Topic 842 | $ | $ | ||||||

| Initial recognition of the balance payment of finance lease right-of-use asset by finance lease liabilities | $ | $ | ||||||

See accompanying notes to unaudited condensed consolidated financial statements.

F-4

ASIAFIN HOLDINGS CORP.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THREE MONTHS ENDED MARCH 31, 2026 AND 2025

(Currency expressed in United States Dollars (“US$”), except for number of shares or otherwise stated)

1. ORGANIZATION AND BUSINESS BACKGROUND

AsiaFIN

Holdings Corp. (“the Company”) was incorporated under the jurisdiction of Nevada on

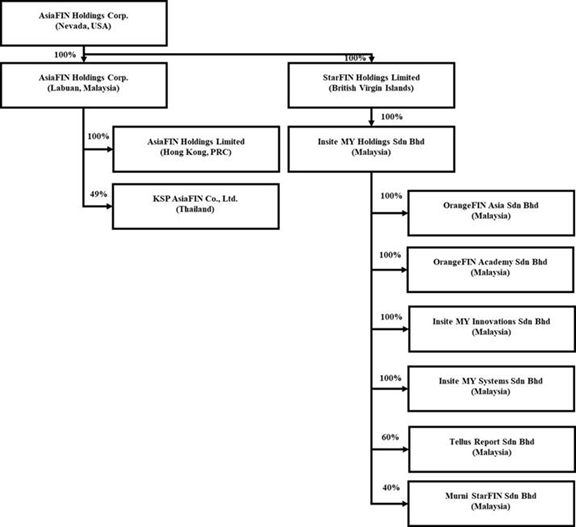

| No. | Subsidiary Company Name | Domicile and Date of Incorporation | Particulars of Issued Capital | Principal Activities | ||||

| 1 | AsiaFIN Holdings Corp. | |||||||

| 2 | AsiaFIN Holdings Limited | |||||||

| 3 | StarFIN Holdings Limited | |||||||

| 4 | Insite MY Holdings Sdn Bhd (FKA StarFIN Asia Sdn Bhd) | |||||||

| 5 | OrangeFIN Academy Sdn Bhd (FKA Insite MY.Com Sdn Bhd) | |||||||

| 6 | Insite MY Systems Sdn Bhd | |||||||

| 7 | Insite MY Innovations Sdn Bhd | |||||||

| 8 | OrangeFIN Asia Sdn Bhd | |||||||

| 9 | TellUS Report Sdn Bhd |

| No. | Associate Company Name | Domicile and Date of Incorporation | Particulars of Issued Capital | Principal Activities | ||||

| 1 | Murni StarFIN Sdn Bhd | |||||||

| 2 | KSP AsiaFIN Co., Ltd. (FKA KSP StarFIN Co., Ltd.) |

Mr. Kai Cheong Wong is the common director of all of aforementioned companies except KSP AsiaFIN Co., Ltd.

F-5

2.

Basis of Presentation

These accompanying financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

The accompanying financial statements include the accounts of the Company and its subsidiaries and associates. Intercompany transactions and balances were eliminated in consolidation. The Company has adopted December 31 as its fiscal year end.

The accompanying consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries and majority-owned subsidiaries which the Company controls and entities for which the Company is the primary beneficiary. For those consolidated subsidiaries where the Company’s ownership is less than 100%, the outside shareholders’ interests are shown as non-controlling interests in equity. Acquired businesses are included in the consolidated financial statements from the date on which control is transferred to the Company. Subsidiaries are deconsolidated from the date that control ceases. All inter-company accounts and transactions have been eliminated in consolidation.

Below is the organization chart of the Group.

Use of Estimates

In preparing these financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheets and revenues and expenses during the years reported. Actual results may differ from these estimates.

F-6

Cash and Cash Equivalents

The Company considers short-term, highly liquid investments with an original maturity of 90 days or less to be cash equivalents.

Our deposits in Malaysian banks are secured by

Perbadanan Insurans Deposit Malaysia, compensating up to a limit of Malaysia Ringgit per deposit per member bank, which is

equivalent to $

Property, Plant and Equipment

Property, plant and equipment are stated at cost, with depreciation and amortization provided using the straight-line method over the following periods:

| Asset Categories | Depreciation Periods | |

| Renovation | ||

| Computer Systems | ||

| Furniture and Fittings | ||

| Electrical Fittings | ||

| Handphone | ||

| Office Equipment | ||

| Motor Vehicle | ||

| Property |

Credit losses

The Company estimates and records a provision for its expected credit losses related to its financial instruments, including its trade receivables. Management considers historical collection rates, the current financial status of the Company’s customers, macroeconomic factors, and other industry-specific factors when evaluating current expected credit losses. Forward-looking information is also considered in the evaluation of current expected credit losses. However, because of the short time to the expected receipt of accounts receivable, management believes that the carrying value, net of expected losses, approximates fair value and therefore, relies more on historical and current analysis of such financial instruments, including its trade receivables.

Credit loss rate is determined by historical collection based on aging schedule, adjusted for current conditions using reasonable and supportable forecasts. Based on the aging categorization and the adjusted loss rate per category, an allowance for credit losses is calculated by multiplying the adjusted loss rate with the amortized cost in the respective age category.

In July 2025, the FASB issued ASU 2025-05, Financial Instruments—Credit Losses (Topic 326), which introduces a practical expedient for measuring expected credit losses on trade receivables and contract assets. Under ASU 2025-05, an entity is required to disclose whether it has elected to use the practical expedient. An entity that makes the accounting policy election is required to disclose the date through which subsequent cash collections are evaluated. ASU 2025-05 is effective for fiscal years beginning after December 15, 2025, and interim periods within fiscal years beginning after December 15, 2026. Early adoption is permitted. The Company already adopted this ASU on its consolidated financial statements and related disclosure. The Company has elected practical expedient under ASU 2025-05 for the quarter ended March 31, 2026 which permits assuming that current conditions as of the balance sheet date will remain unchanged for the remaining life of the asset when estimating expected credit losses. Accordingly, the Company’s estimate of the allowance for expected credit losses on current accounts receivable is determined by applying an adjusted loss rate to the amortized cost of receivables within each respective aging category, based on historical data over a 25-month period.

Investment in associate

The Company accounts for its investment in associate in accordance with ASC Topic 323, “Investments – Equity Method and Joint Ventures”, whereby equity investments of 20% or greater, but less than a controlling interest, are accounted for using the equity method. Under this method, the investment is initially recorded at cost and subsequently adjusted for the Company’s proportionate share of the investee’s net income or loss, which is recognized in the consolidated statements of operations and comprehensive income, with a corresponding adjustment to the carrying value of the investment. The Company evaluates its equity method investments for potential significant influence, if the Company became primary beneficiary, it could consolidate the investee and recognize a noncontrolling interest for the portion not owned.

F-7

Revenue recognition

The Company through subsidiaries generate multiple streams of revenues based on different business model adopted by each subsidiary through provisions of services and recognized upon customer obtained control of promised services and recognized in an amount that reflects the consideration that the Company expects to receive in exchange for those services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The Company applies the following five-step model in order to determine this amount:

| (i) | Identify contract with customer; |

| (ii) | Identify distinct performance obligations in contract, including promises if any; |

| (iii) | Measurement of the transaction price, including the constraint on variable consideration; |

| (iv) | Allocation of the transaction price to the performance obligations; and |

| (v) | Recognition of revenue when (or as) the Company satisfies each performance obligation. |

The Company adopted ASU 2014-09, Revenue from Contracts with Customers (Topic 606). Under Topic 606, the Company records revenue when persuasive evidence of an arrangement exists, delivery has occurred, the fee is fixed or determinable and collectability is probable. The Company records revenue from the delivery of the finalized information technology services such as business system integration and management services, computer programming activities and services to the customers (see Note 3).

Cost of revenue

Cost of revenue includes direct costs associated with provision of services such as development costs, purchases of third-party software, maintenance fees and consultation fees.

Income tax expense

Income taxes are determined in accordance with the provisions of ASC Topic 740, “Income Taxes” (“ASC Topic 740”). Under this method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. The Company also adopted ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures”, which requires disaggregated information about the reporting entity’s effective tax rate reconciliation as well as information on income taxes paid.

ASC 740 prescribes a comprehensive model for how companies should recognize, measure, present, and disclosed in their financial statements uncertain tax positions taken or expected to be taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement with the tax authority assuming full knowledge of the position and relevant facts.

The Company conducts major businesses in Malaysia and is subject to tax in their own jurisdictions. As a result of its business activities, the Company will file separate tax returns that are subject to examination by the foreign tax authorities.

F-8

Foreign currencies translation

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the statement of operations and comprehensive income (loss).

The functional currency of the Company is the United States Dollars (“US$” or “US dollars”) and the accompanying financial statements have been expressed in US dollars. In addition, the Company’s subsidiary maintains its books and record in Malaysia Ringgit (“MYR”), United States Dollars (“US$”), Hong Kong Dollars (“HK$”) and Thailand Baht (“THB”), which is the respective functional currency as being the primary currency of the economic environment in which the entity operates.

In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US dollars are translated into US dollars, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiary are recorded as a separate component of accumulated other comprehensive income.

Translation

of amounts from the local currency of the Company into US$

For

the three months ended | ||||||||

| 2026 | 2025 | |||||||

| Period-end MYR : US$1 exchange rate | | | ||||||

| Period-average MYR : US$1 exchange rate | ||||||||

| Period-end HK$ : US$1 exchange rate | ||||||||

| Period-average HK$ : US$1 exchange rate | ||||||||

| Period-end THB : US$1 exchange rate | ||||||||

| Period-average THB : US$1 exchange rate | ||||||||

Related parties

Parties, which can be a corporation or individual, are considered to be related if the Company has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Companies are also considered to be related if they are subject to common control or common significant influence.

F-9

Net Income/(Loss) per Share

The Company calculates net income/(loss) per share in accordance with ASC Topic 260, “Earnings per Share.” Basic income/(loss) per share is computed by dividing the net income/(loss) by the weighted-average number of common shares outstanding during the period. Diluted income per share is computed similar to basic income/(loss) per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common stock equivalents had been issued and if the additional common shares were dilutive.

Lease

The Company leases offices for fixed periods with pre-emptive extension options. The Company recognizes lease payments for its short-term lease on a straight-line basis over the lease term.

Lease liability is initially and subsequently measured at the present value of the unpaid lease payments at the lease commencement date. The right-of-use asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for lease payments made at or before the lease commencement date, plus any initial direct costs incurred less any lease incentives received. Costs associated with operating lease assets are recognized on a straight-line basis within operating expenses over the term of the lease.

In determining the present value of the unpaid lease payments, ASC 842 requires a lessee to discount its unpaid lease payments using the interest rate implicit in the lease or, if that rate cannot be readily determined, its incremental borrowing rate. As most of the Company leases do not provide an implicit rate, the Company uses its incremental borrowing rate as the discount rate for the lease. The Company’s incremental borrowing rate is estimated to approximate the interest rate on a collateralized basis with similar terms and payments.

Segment Reporting

The

Company follows the guidance of ASC 280, “Segment Reporting”, which establishes standards for reporting information about

operating segments on a basis consistent with the Company’s internal organization structure as well as information about services

categories, business segments and major customers in financial statements. For the

Recently Issued Accounting Standards

In November 2024, the FASB issued ASU 2024-03, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40), which requires enhanced disclosures of certain income statement expenses. In January 2025, the FASB issued ASU 2025-01 to clarify the effective date of ASU 2024-03. The standard is effective for fiscal years beginning after December 15, 2026, and interim periods within fiscal years beginning after December 15, 2027. Early adoption is permitted, either prospectively or retrospectively.

The Company reviews new accounting standards as issued. Management has not identified any other new standards that it believes will have a significant impact on the Company’s financial statements.

F-10

3. REVENUE FROM CONTRACTS WITH CUSTOMERS

The Company recognizes revenue in accordance with ASC 606, “Revenue from Contracts with Customers”, by applying the five-step model to all contracts with customers: (i) identification of the contract, (ii) identification of performance obligations, (iii) determination of the transaction price, (iv) allocation of the transaction price to the performance obligations, and (v) recognition of revenue when, or as, the Company satisfies a performance obligation.

The Company’s revenue is derived from the provision of system solutions in Payment Processing (Fintech), Regulatory Technology (RegTech) and Robotic Process Automation (RPA). Each contract specifies the services to be delivered, the total consideration, and the applicable payment terms.

Performance obligations generally consist of the delivery of software solutions, implementation services, customization, and, when applicable, post-implementation support and maintenance. The Company evaluates whether such services are distinct and accounts for them as separate performance obligations if appropriate.

The transaction price is determined based on the consideration specified in the contract, which may include fixed and variable amounts. Variable consideration, if any, is estimated using either the expected value or the most likely amount method, depending on which better predicts the amount of consideration to which the Company will be entitled. The Company includes variable consideration in the transaction price only to the extent that it is probable that a significant reversal of revenue will not occur.

Revenue is recognized when control of the promised goods or services is transferred to the customer. For implementation and customization services, revenue is generally recognized over time as the services are performed, as the customer simultaneously receives and consumes the benefits. For software solutions, revenue is recognized at a point in time or over time, depending on the nature of the arrangement and the transfer of control. Revenue from support and maintenance services is typically recognized over time on a straight-line basis over the service period.

The Company’s payment terms vary by contract but generally require payment within a specified period following invoicing. In certain arrangements, the Company may receive advance payments, which are recorded as contract liabilities and recognized as revenue when the related performance obligations are satisfied.

Cost of revenue

Cost of revenue includes direct costs associated with provision of services such as development costs, purchases of third-party software, maintenance fees and consultation fees.

Disaggregation of revenue

The table below shows the revenue disaggregation by type of services for the three months ended March 31, 2026 and 2025:

| Revenue disaggregation by type of services | For

the three | For

the three (Unaudited) | ||||||

| Payment Processing (Fintech) | $ | | $ | | ||||

| Regulatory Technology (RegTech) | ||||||||

| Robotic Process Automation (RPA) | ||||||||

| Total revenue | $ | $ | ||||||

F-11

Contract assets

Contract assets represent the Company’s right to consideration in exchange for services transferred to customers for which the Company has not yet billed the customer.

Contract liabilities

For a service contract where the performance obligation has not been completed, the contract liabilities are recorded for any payments received in advance from the customer before completion of the performance obligation.

As of March 31, 2026 and December 31, 2025, the Company’s contract assets and contract liabilities are classified as current assets and current liabilities, respectively, as presented below:

As of March 31, 2026 (Unaudited) | As of December 31, (Audited) | |||||||

| Current assets | ||||||||

| Contract assets | $ | $ | ||||||

| Current liabilities | ||||||||

| Contract liabilities | $ | $ | ||||||

Changes in contract assets during the three months ended March 31, 2026 are as follows:

For

the three | ||||

| Contract assets, January 1, 2026 | $ | |||

| New contract assets | ||||

| Revenue recognized and billed | ( | ) | ||

| Exchange difference | ( | ) | ||

| Contract assets, March 31, 2026 | $ | |||

Changes in contract liabilities during the three months ended March 31, 2026 are as follows:

| For the three months ended March 31, 2026 (Unaudited) |

||||

| Contract liabilities, January 1, 2026 | $ | |||

| New contract liabilities | ||||

| Performance obligations satisfied | ( |

) | ||

| Exchange difference | ( |

) | ||

| Contract liabilities, March 31, 2026 | $ | |||

Remaining performance obligations

Remaining

performance obligations represent the transaction price of firm orders for which a good or service has not been delivered to our customer. As

of March 31, 2026, the aggregate amount of the transaction price allocated to remaining performance obligations was $

F-12

4. ACCOUNT RECEIVABLES, NET

As

of | As

of | |||||||

| Account receivables, gross | $ | $ | ||||||

| Allowance for expected credit loss | ( | ) | ( | ) | ||||

| Account receivables, net | $ | $ | ||||||

5. PREPAYMENT, DEPOSITS AND OTHER RECEIVABLES

As

of | As

of | |||||||

| Prepaid expenses | $ | $ | ||||||

| Other receivables | ||||||||

| Other deposits | ||||||||

| Total | $ | $ | ||||||

Prepaid expenses include website domain, third party software maintenance and subscription, OTC Markets fee, employee and motor vehicle insurance.

Other receivables include receivables from service tax and management of car park for director and employees.

Other deposits primarily include deposit of the tenancy agreement and deposit made for security deposit for renovation and car park deposit.

6. PROPERTY, PLANT AND EQUIPMENT, NET

As

of | As

of (Audited) | |||||||

| Computer systems | $ | $ | ||||||

| Furniture and fittings | ||||||||

| Electrical fittings | ||||||||

| Handphone | ||||||||

| Office equipment | ||||||||

| Renovation | ||||||||

| Motor vehicle | ||||||||

| Property | ||||||||

| Total property, plant and equipment | $ | $ | ||||||

| Less: Accumulated depreciation | ( | ) | ( | ) | ||||

| Total property, plant and equipment, net | $ | $ | ||||||

For

three | For

the three (Unaudited) | |||||||

| Investment in computer systems | $ | $ | ||||||

| Investment in furniture and fittings | ||||||||

| Investment in motor vehicle | ||||||||

| Investment in handphone | ||||||||

| Investment in office equipment | ||||||||

| Investment in renovation | ||||||||

| Total investment in property, plant and equipment | $ | $ | ||||||

| Depreciation for the period | $ | $ | ||||||

F-13

7. ACCRUED LIABILITIES AND OTHER PAYABLES

As of March 31, 2026 (Unaudited) | As of December 31, 2025 (Audited) | |||||||

| Accrued expenses | $ | $ | ||||||

| Other payable | ||||||||

| Total | $ | $ | ||||||

Accrued expenses consist of outstanding audit fee, employee claims and salary, service tax and miscellaneous expenses.

Other payable includes primarily payable to third parties.

8. AMOUNT DUE TO DIRECTOR

As of March 31, 2026 and December 31, 2025, the

Company had an outstanding amount due to director amounted $

Aforementioned amount is unsecured, interest bearing and payable on demand or with tenure of 60 months.

9. RELATED PARTY BALANCES AND TRANSACTIONS

In September 2025, the Company, through its subsidiary,

entered into a loan agreement with a related party for working capital purposes, with a loan amount of approximately $

1) Nature of relationships with related parties

The table below sets forth the major related parties and their relationships with the Company, with which the Company entered into transactions for the quarters ended March 31, 2026 and 2025 or recorded balances as of March 31, 2026 and December 31, 2025, respectively.

| Name of Related Party | Relationship to the Company | |

| Kai Cheong Wong | ||

| Murni StarFIN Sdn Bhd | ||

| KSP AsiaFIN Co., Ltd. | ||

| Tan Siew Meng | ||

| Insite MY International Inc. | ||

| AsiaFIN Talent Sdn Bhd |

2) Balances with related parties

| As of March 31, 2026 | As of December 31, 2025 | |||||||

| Trade | ||||||||

| Amount due to Insite MY International, Inc. | $ | $ | ||||||

| Non-trade | ||||||||

| Amount due to Murni StarFIN Sdn Bhd | $ | ( | ) | $ | ( | ) | ||

| Amount due from KSP AsiaFIN Co., Ltd. | ||||||||

| Amount due from Insite MY International Inc. | ||||||||

| Amount due from AsiaFIN Talent Sdn Bhd | ||||||||

| Amount due from related parties | $ | $ | ||||||

F-14

3) Transactions with related parties

| For the three months ended March 31, 2026 | For the three months ended March 31, 2025 | |||||||

| Purchases from Insite MY International, Inc. | $ | $ | ||||||

| Rental payment to Kai Cheong Wong | $ | $ | ||||||

| Rental payment to Tan Siew Meng | $ | $ | ||||||

| Expenses charged by Murni StarFIN Sdn Bhd | $ | $ | ||||||

| Interest income from KSP AsiaFIN Co., Ltd. | $ | ( | ) | $ | ) | |||

| Expenses charged by Insite MY International Inc. | $ | $ | ||||||

10. FINANCE LEASE LIABILITY

On

August 28, 2025, the Company, through its subsidiary, acquired a motor vehicle amounted $

For

the three months ended March 31, 2026, the Company repaid $

Maturities of the loan for the remaining years are as follows:

| Year ending December 31, | ||||

| 2026 | $ | |||

| 2027 | ||||

| 2028 | ||||

| Total | $ | |||

11. LEASE RIGHT-OF-USE ASSET AND OPERATING LEASE LIABILITIES

Leases are classified as operating leases or finance leases in accordance with ASC 842. The Company’s operating leases are mainly related to office facilities. For leases with terms greater than 12 months, the Company records the related asset and liability at the present value of lease payments over the term. The Company’s lease agreements do not contain any material guarantees or restrictive covenants. The Company does not have any material finance leases or any sublease activities. Short-term leases, defined as leases with initial term of 12 months or less, are not reflected on the consolidated balance sheet.

During

the quarter ended March 31, 2026, the Company entered into two new lease agreements primarily related to office facilities. As a result,

the Company recognized operating lease right-of-use assets of $

During

the quarter ended March 31, 2026, the Company reassessed its lease term assumptions for certain leased office facilities and determined

that it is no longer reasonably certain to exercise certain renewal options. This reassessment was primarily driven by changes in the

terms of the underlying lease agreements. As a result, the Company remeasured the related lease liabilities, resulting in a decrease

of $

F-15

The following table presents a summary of changes in the Company’s operating lease liabilities for the quarter ended March 31, 2026:

| Right-Of-Use Assets | ||||

| Balance as of December 31, 2025 | $ | |||

| New right-of-use assets recognized | ||||

| Amortization for the three months ended March 31, 2026 | ( | ) | ||

| Adjustment for non-exercising option | ( | ) | ||

| Adjustment for foreign currency translation difference | ||||

| Balance as of March 31, 2026 | $ | |||

| Operating Lease Liability | ||||

| Balance as of December 31, 2025 | $ | |||

| New lease liability recognized | ||||

| Imputed interest for the three months ended March 31, 2026 | ||||

| Gross repayment for the three months ended March 31, 2026 | ( | ) | ||

| Adjustment for non-exercising option | ( | ) | ||

| Adjustment for foreign currency translation difference | $ | |||

| Balance as of March 31, 2026 | $ | |||

| Operating lease liability current portion | $ | |||

| Operating lease liability non-current portion | $ | |||

Other information:

| Three months ended March 31, 2026 | Three months ended March 31, 2025 | |||||||

| Cash paid for amounts included in the measurement of lease liabilities: | ||||||||

| Operating cash flow to operating lease | $ | $ | ||||||

| Right-of-use assets obtained in exchange for operating lease liabilities | ||||||||

| Remaining lease term for operating lease (years) | ||||||||

| Weighted average discount rate for operating lease | % | % | ||||||

12. CONCENTRATION OF RISK

| (a) | Major Customers |

For

the three months ended March 31, 2026, the Company generated total revenue of $

| For the three months ended March 31 | ||||||||||||||||||||||||

| 2026 | 2025 | 2026 | 2025 | 2026 | 2025 | |||||||||||||||||||

| Revenue | Percentage of Revenue | Accounts receivable, gross | ||||||||||||||||||||||

| Customer A | $ | $ | % | % | $ | $ | ||||||||||||||||||

| Customer B | % | % | ||||||||||||||||||||||

| Customer C | % | % | ||||||||||||||||||||||

| Customer D | % | % | ||||||||||||||||||||||

| Others | % | % | ||||||||||||||||||||||

| Total | $ | $ | % | % | $ | $ | ||||||||||||||||||

| (b) | Major Suppliers |

For

the three months ended March 31, 2026, the Company incurred cost of revenue of $

F-16

13. INCOME TAXES

The loss before income taxes of the Company for the three months ended March 31, 2026 and 2025 were comprised of the following:

| For the three months ended March 31, | ||||||||

| 2026 | 2025 | |||||||

| Tax jurisdictions from: | ||||||||

| - Local | $ | ( | ) | $ | ( | ) | ||

| - Foreign, representing: | ||||||||

| Hong Kong | ( | ) | ( | ) | ||||

| British Virgin Islands (non-taxable jurisdiction) | ( | ) | ||||||

| Labuan, Malaysia (non-taxable jurisdiction) | ( | ) | ||||||

| Malaysia | ( | ) | ( | ) | ||||

| Loss before income taxes | $ | ( | ) | $ | ( | ) | ||

Provision for income taxes consisted of the following:

| For the three months ended March 31 | ||||||||

| 2026 | 2025 | |||||||

| Current: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | $ | $ | ||||||

| Deferred tax assets: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | $ | $ | ||||||

| Deferred tax liabilities: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | $ | $ | ||||||

| Income tax payable: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | $ | $ | ||||||

| Tax assets: | ||||||||

| - Local | $ | $ | ||||||

| - Foreign | $ | $ | ||||||

Effective and Statutory Rate Reconciliation

The

The following table summarizes a reconciliation of the Company’s income taxes expenses:

| For the three months ended March 31, | ||||||||||||||||

| 2026 | 2025 | |||||||||||||||

| Amount | Percentage | Amount | Percentage | |||||||||||||

| Computed expected expenses and federal income tax rate | $ | ( | ) | ( | )% | $ | ( | ) | ( | )% | ||||||

| Effect of foreign tax rate difference | ( | ) | ( | )% | ( | ) | ( | )% | ||||||||

| Changes in valuation allowances | % | % | ||||||||||||||

| Others | ( | ) | ( | )% | % | |||||||||||

| Total income tax expense and effective tax rate | $ | % | $ | % | ||||||||||||

F-17

The following table sets forth the significant components of the aggregate deferred tax assets of the Company as of March 31, 2026 and 2025:

As of March 31, 2026 | As of March 31, 2025 | |||||||

| Deferred tax assets: | ||||||||

| Net operating losses carry forwards | ||||||||

| - United States of America | $ | $ | ||||||

| - Hong Kong | ||||||||

| - British Virgin Islands | ||||||||

| - Labuan, Malaysia | ||||||||

| - Malaysia | ||||||||

| Total deferred tax assets | $ | $ | ||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Deferred tax assets, net of valuation allowance | $ | $ | ||||||

The effective tax rate in the years presented is the result of the mix of income earned in various tax jurisdictions that apply a broad range of income tax rates. During the period presented, the Company has a number of subsidiaries that operates in various countries: the United States of America, Hong Kong, the British Virgin Islands and Malaysia that are subject to taxes in the jurisdictions in which they operate, as follows:

United States of America

The

Company is registered in the State of Nevada and is subject to United States of America tax law with a tax rate of

British Virgin Islands

The British Virgin Islands currently levies no taxes on individuals or corporations based upon profits, income, gains or appreciation and there is no taxation in the nature of inheritance tax or estate duty. There are no other taxes likely to be material to us levied by the government of the British Virgin Islands except for stamp duties which may be applicable on instruments executed in, or, after execution, brought within the jurisdiction of the British Virgin Islands. The British Virgin Islands is not party to any double tax treaties that are applicable to any payments made to or by our company. There are no exchange control regulations or currency restrictions in the British Virgin Islands. Payments of dividends and capital in respect of our ordinary shares will not be subject to taxation in the British Virgin Islands and no withholding will be required on the payment of a dividend or capital to any holder of our ordinary shares, nor will gains derived from the disposal of our ordinary shares be subject to British Virgin Islands income or corporation tax. No stamp duty is payable in respect of the issue of the shares or on an instrument of transfer in respect of a share.

Hong Kong

AsiaFIN

Holdings Corp. is subject to Hong Kong Profits Tax, which is charged at the statutory income tax rate of

F-18

Labuan, Malaysia

Labuan

was established an international offshore financial center in 1990 with its own specific laws and regulations to attract foreign investment

and promoting financial services. Under the current laws of Labuan, AsiaFIN Holdings Corp. is governed under the Labuan Business Activity

Tax Act 1990. Labuan offers a low fixed tax rate of 3% for a Labuan incorporated company carrying a Labuan trading activity while the

profit of a Labuan incorporated company carrying a Labuan non-trading activity for the tax assessment year shall not be charged to tax

under Labuan Business Activity Tax Act 1990, effectively subjecting to a 0% tax rate. Labuan trading activity includes banking, insurance,

trading, management, licensing, shipping operations or any other activity which is not a Labuan non-trading activity while Labuan non-trading

activity is defined as an activity relating to the holding of investments in securities, stock, shares, loans, deposits or any other

properties situated in Labuan by a Labuan incorporated company. For a Labuan incorporated company which fails to meet the substantial

activity requirements issued in a circular on April 29, 2020, the tax charge for such company is based on

Malaysia

Under

the Malaysian tax regulatory system, companies incorporated or operating in Malaysia that are wholly or partially owned by foreign entities

are generally subject to the standard corporate income tax rate of

As

of March 31, 2026, the Company’s operations in Malaysia incurred cumulative net operating losses of $

As

of March 31, 2026, the Company’s management believes that it is more likely than not that the deferred tax assets will not be fully

realizable in the future. As the Company incurred a net loss for the year, and in light of ongoing economic uncertainties, management

has determined that it is appropriate to maintain a full valuation allowance against its deferred tax assets. The Company will continue

to evaluate its valuation allowance policy and will consider adjustments only upon demonstrating sustained profitability over consecutive

reporting periods. Accordingly, the Company has recorded a full valuation allowance against its deferred tax assets of $

F-19

14. SHAREHOLDERS’ EQUITY

On

June 14, 2019, the Company issued

On

December 18, 2019, we, “the Company” acquired

On

December 20, 2019, the Company issued

On

December 20, 2019, the Company issued

On

December 20, 2019, the Company issued

On

December 20, 2019, the Company issued

Mr. Kang Kok Seng Michael and Mr. Ng Kai Thim are each an Officer and Director of, and also the controlling shareholders of AsiaFIN Talent Sdn. Bhd.

On

December 23, 2019, AsiaFIN Holdings Corp., Malaysia Company acquired AsiaFIN Holdings Limited (herein referred to as the “Hong

Kong Company”), a private limited company incorporated in Hong Kong. In consideration of the equity interests of AsiaFIN Holdings

Limited, our Chief Executive Officer, Mr. Wong was compensated $

On

February 7, 2020, the Company issued

On

August 3, 2021, the Company issued

On

December 22, 2022, the Company entered into an acquisition agreement with the shareholders of StarFIN Holdings Limited, to acquire

On

January 20, 2025, the Company issued

As of March 31, 2026, the Company has an issued

and outstanding share of common stock of

15. DIVIDEND

dividend was declared for the three months ended March 31, 2026.

16. FOREIGN CURRENCY EXCHANGE RATE

The Company cannot guarantee that the current exchange rate will remain stable, therefore there is a possibility that the Company could post the same amount of income for two comparable periods and because of the fluctuating exchange rate post higher or lower income depending on exchange rate converted into US dollars at the end of the financial year. The exchange rate could fluctuate depending on changes in political and economic environments without notice.

F-20

17. SEGMENT REPORTING

ASC

280, “Segment Reporting” establishes standards for reporting information about operating segments on a basis consistent with

the Company’s internal organization structure as well as information about services categories, business segments and major customers

in financial statements. The Company has

The Company adopted the ASU 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures”, which expands annual and interim disclosure requirements for reportable segments, primarily through enhanced disclosures about significant segment expenses.

In

accordance with the “Segment Reporting” Topic of the ASC,

| For the Three Months Ended and As of March 31, 2026 | ||||||||||||||||

| By Business Unit | Fintech | Regtech | RPA | Total | ||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Cost of revenue | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Gross profit | $ | $ | $ | ( | ) | $ | ||||||||||

| Share of loss from operation of associate | ( | ) | ( | ) | ||||||||||||

| Selling, general and administrative expenses and other income | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Income/(loss) from operations | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||||

| Total assets | $ | $ | $ | $ | ||||||||||||

| Capital expenditure | $ | $ | $ | $ | ||||||||||||

| For the Three Months Ended and As of March 31, 2026 | ||||||||||||

| By Country | Malaysia | Non-Malaysia | Total | |||||||||

| Revenue | $ | $ | $ | |||||||||

| Cost of revenue | ( | ) | ( | ) | ||||||||

| Gross profit | $ | $ | $ | |||||||||

| Share of loss from operation of associate | ( | ) | ( | ) | ||||||||

| Selling, general and administrative expenses and other income | ( | ) | ( | ) | ( | ) | ||||||

| Loss from operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||

| Total assets | $ | $ | $ | |||||||||

| Capital expenditure | $ | $ | $ | |||||||||

F-21

| For the Three Months Ended and As of March 31, 2025 | ||||||||||||||||

| By Business Unit | Fintech | Regtech | RPA | Total | ||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Cost of revenue | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Gross loss | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||

| Share of loss from operation of associate | ( | ) | ( | ) | ||||||||||||

| Selling, general and administrative expenses and other income | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Loss from operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Total assets | $ | $ | $ | $ | ||||||||||||

| Capital expenditure | $ | $ | $ | $ | ||||||||||||

| For the Three Months Ended and As of March 31, 2025 | ||||||||||||

| By Country | Malaysia | Non-Malaysia | Total | |||||||||

| Revenue | $ | $ | $ | |||||||||

| Cost of revenue | ( | ) | ( | ) | ||||||||

| Gross loss | $ | ( | ) | $ | $ | ( | ) | |||||

| Share of loss from operation of associate | ( | ) | ( | ) | ||||||||

| Selling, general and administrative expenses and other income | ( | ) | ( | ) | ( | ) | ||||||

| Loss from operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||

| Total assets | $ | $ | $ | |||||||||

| Capital expenditure | $ | $ | $ | |||||||||

18. SUBSEQUENT EVENTS

In accordance with ASC Topic 855, “Subsequent Events”, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued, the Company has evaluated all events or transactions that occurred after March 31, 2026 up through the date the Company presented these unaudited financial statements.

F-22

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The information contained in this quarterly report on Form 10-Q is intended to update the information contained in our Form 10-K dated April 1, 2026, for the year ended December 31, 2025 and presumes that readers have access to, and will have read, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and other information contained in such Form 10-K. The following discussion and analysis also should be read together with our financial statements and the notes to the financial statements included elsewhere in this Form 10-Q.

The following discussion contains certain statements that may be deemed “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements appear in a number of places in this Report, including, without limitation, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. These statements are not guarantees of future performance and involve risks, uncertainties and requirements that are difficult to predict or are beyond our control. Forward-looking statements speak only as of the date of this quarterly report. You should not put undue reliance on any forward-looking statements. We strongly encourage investors to carefully read the factors described in our Form S-1/A registration statement, filed on November 28, 2025, in the section entitled “Risk Factors” for a description of certain risks that could, among other things, cause actual results to differ from these forward-looking statements. We assume no responsibility to update the forward-looking statements contained in this quarterly report on Form 10-Q. The following should also be read in conjunction with the unaudited Condensed Consolidated Financial Statements and notes thereto that appear elsewhere in this report.

Company Overview

AsiaFIN Holdings Corp., a company incorporated under the law of the State of Nevada, is a holding company operating through its wholly owned subsidiaries by offering a range of system solutions in payment processing (Fintech), Regulatory Technology (RegTech), and robotic process automation (RPA) to financial institutions, regulatory agencies, professional service providers and private enterprises from various industries, with existing clients in the Asia region and Saudi Arabia. Our subsidiary, SFHL, has over 90 bank customers for payment processing and RegTech, and our RPA solution system has more than 100 customers in Asia and Saudi Arabia. We maintain a corporate website at asiafingroup.com. The information on our website is not part of this report and shall not be deemed to be incorporated by reference into this report. Shares of our common stock are quoted on the OTCQB® Venture Market under the symbol “ASFH”.

Payment Processing (Fintech)

We have our own web-based payment processing system for check clearing used in central banks, financial institutions and payment system providers. This image-based check truncation system (CTS) is similar to the one used in the United States of America, under the CHECK21 standards. Our CTS systems are sold in Malaysia, Singapore, Indonesia, Philippines, Myanmar, Thailand, Pakistan, Bangladesh and in Saudi Arabia. INCHEQS (trademark pending) is our flagship Fintech product, through which we automate the clearing of checks, a payment instrument, for banks and central banks that either issue or collect checks, or both. INCHEQS is a check image-based solution where we deploy AI to identify the check amount, payee name, date, Magnetic Ink Character Recognition (MICR) code and signature to automate the approval and subsequent payment of checks to the customer. INCHEQS can be deployed at banks and clearing houses. The solution utilizes a web-based architecture and is sold either as a perpetual license with an annual maintenance contract or on an annual subscription basis.

INGateway is a payment gateway solution that is designed to support and be compatible with the ISO20022 messaging standards for central banks and financial institutions. INGateway is capable of supporting the Straight Through Processing (STP) of all types of payment transactions (including SWIFT, Real-Time Gross Settlement (RTGS), GIRO (NACHA standards) and Fast and Secure Transfers (FAST) payment) and is extendable to interface with various types of payment gateways. Our STP payment gateway solutions are sold in Malaysia, Myanmar and Indonesia.

Regulatory Technology (RegTech)

INReport is a RegTech system which conforms to XBRL reporting standards and other compliance reporting required by regulatory agencies such as central banks, securities commissions, tax authorities and company registries. Our INReport reporting platform covers financial statistic reporting, credit risk exposure and analysis, risk management reports, Foreign Account Tax Compliance Act (FATCA) and EU Common Reporting Standard (CRS) reporting, external sector reporting, Goods and Services Tax (GST) reporting for reporting entities and lately e-Invoicing reporting for large corporations. We have more than 54 financial institutions and 61 large corporations using this RegTech platform.

Additionally, we have developed TellUS Report, a RegTech Software as a Service (SaaS) solution for public listed companies and financial institutions for Environmental, Social and Governance (ESG) compliant reporting and consultancy. ESG guidelines have already been issued by Bank Negara Malaysia, the central bank of Malaysia and Bursa Malaysia Stock Exchange for their members to reduce their carbon footprint. Our subsidiary, TellUS Report Sdn Bhd, was created to focus on this new line of business in both the consultancy and reporting. The current reporting standard that TellUS Report supports is the GRI Standards.

Robotic Process Automation (RPA)

OrangeFIN is AI-based RPA suite of products for financial institutions, large corporations and small medium enterprises. The OrangeWorkforce family of products, which consists of OrangeFIN Bots, OrangeFIN AI and OrangeFIN Vision, utilizes software robots for the automation of mundane, labor intensive, manual computer operations. Robots are utilized for the processes where they help to reduce operational costs and also costs arising from human error. Our system automates the capturing of customer information from identity cards, passports and other identification documents. Our solution will automatically extract data from customers’ identity card, passport, and other identity documents and will immediately complete the forms, eliminating the friction and errors caused by manual input, through Intelligent Character Recognition technology and other AI-based technologies. Information extracted from an official identification document will then be checked against existing financial institutions’ databases for regulatory screening in internal blacklist check, anti-money laundering, credit scoring check, FATCA, CRS and ESG reporting, etc. Our AI-based RPA has helped companies in Malaysia, Philippines, Indonesia and Pakistan. Also, we have a joint venture company KSP AsiaFIN Co., Ltd. that has fully translated our AI-based RPA to the Thai language.

-1-

Results of operations

Three months ended March 31, 2026 and 2025

| For the Three Months Ended March 31, | Increase (decrease) in | |||||||||||||||||||||||

| 2026 | 2025 | 2026 compared to 2025 | ||||||||||||||||||||||

| (In U.S. dollars, except for percentages) | ||||||||||||||||||||||||

| Revenue | $ | 1,275,522 | 100 | % | $ | 621,179 | 100.0 | % | $ | 654,343 | 105.3 | % | ||||||||||||

| Cost of revenue | (934,756 | ) | (73.3 | )% | (628,092 | ) | (101.1 | )% | 306,664 | 48.8 | % | |||||||||||||

| Gross profit/(loss) | $ | 340,766 | 26.7 | % | $ | (6,913 | ) | (1.1 | )% | $ | 347,679 | 5,029.4 | % | |||||||||||

| Share of loss from operation of associate | (74 | ) | (0.0 | )% | (1 | ) | (0.0 | )% | 73 | 7,300.0 | % | |||||||||||||

| Selling, general and administrative expenses | (509,622 | ) | (40.0 | )% | (485,831 | ) | (78.2 | )% | 23,791 | 4.9 | % | |||||||||||||

| Other income | 3,772 | 0.3 | % | 3,282 | 0.5 | % | 490 | 14.9 | % | |||||||||||||||

| Loss from operations | $ | (165,158 | ) | (12.9 | )% | $ | (489,463 | ) | (78.8 | )% | $ | (324,305 | ) | (66.3 | )% | |||||||||

| Income tax expense | - | - | % | - | - | % | - | - | % | |||||||||||||||

| Net loss | $ | (165,158 | ) | (12.9 | )% | $ | (489,463 | ) | (78.8 | )% | $ | (324,305 | ) | (66.3 | )% | |||||||||

| Net income attributable to non-controlling interest | 12,586 | 1.0 | % | 7,034 | 1.1 | % | 5,552 | 78.9 | % | |||||||||||||||

| Net loss attributed to common shareholders of AsiaFIN Holdings Corp. | $ | (152,572 | ) | (12.0 | )% | $ | (482,429 | ) | (77.7 | )% | $ | (329,857 | ) | (68.4 | )% | |||||||||

Revenues

For the three months ended March 31, 2026, the Company generated revenue in the amount of $1,275,522. The revenue was generated as a result of the Company having provided services related to information technology business to the customers.

For the three months ended March 31, 2025, the Company generated revenue in the amount of $621,179. The revenue was generated as a result of the Company having provided services related to information technology business to the customers.

Selling, General and Administrative Expenses

For the three months ended March 31, 2026, the Company had selling, general and administrative expenses in the amount of $509,622. These were primarily comprised of salary expenses, credit loss allowance, consultancy fee, legal services fee, lease expenses and other professional fee.

For the three months ended March 31, 2025, the Company had selling, general and administrative expenses in the amount of $485,831. These were primarily comprised of salary expenses, credit loss allowance, consultancy fee, advertisement fee, transportation charges and travelling expenses.

The increase in general and administrative expenses was primarily attributable to higher salary expenses, as the Company recruited additional employees to support its business expansion, and increased legal and other professional fees.

Net Loss

For the three months ended March 31, 2026, the Company has incurred a net loss of $152,572.

For the three months ended March 31, 2025, the Company has incurred a net loss of $482,429.

Liquidity and Capital Resources

Three months ended March 31, 2026 and 2025

Cash Provided by/ Used in Operating Activities

For the three months ended March 31, 2026, the Company has used $43,183 in operating activity, of which primarily consist of net loss, decrease in account payables, increase in account receivables, increase in contract assets, decrease in accrued liabilities and other payables, increase in tax assets, decrease in income tax payable and reduction in lease liability contra by share of loss from operation of associate, depreciation and amortization, provision for credit loss allowance, decrease in prepayment, deposits and other receivables and increase in contract liabilities.

For the three months ended March 31, 2025, the Company has used $45,148 in operating activity, of which primarily consist of net loss, disposal of asset, decrease in accrued liabilities and other payables, increase in tax assets, decrease in income tax payable and reduction in lease liability contra by share of loss from operation of associate, depreciation and amortization, provision for credit loss allowance, increase in account payables, decrease in account receivables, decrease in prepayment, deposits and other receivables and increase in contract liabilities.

-2-

Cash Used in Investing Activities

For the three months ended March 31, 2026, the Company has invested $114 in investing activities, for the acquisition of office equipment.

For the three months ended March 31, 2025, the Company has invested $5,010 in investing activities, for the acquisition of computer systems, furniture and fittings, and investment in associate.

Cash Used in Financing Activities

For the three months ended March 31, 2026, the Company has used $23,867 in financing activity, primarily consist of advances to director.

For the three months ended March 31, 2025, the Company has used $7,026 in financing activity, primarily consist of proceeds from share issuance and advances to director.

Off-balance Sheet Arrangements

We have no significant off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in our financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to our shareholders as of March 31, 2026.

Contractual Obligations

The contractual obligations presented in the table below represent our estimates of future cash payments under fixed contractual obligations.

The following table summarizes our contractual obligations as of March 31, 2026:

| Total | Due within 1 year | |||||||

| Operating lease obligations1 | $ | 574,106 | $ | 69,584 | ||||

| Loan obligation2 | 74,125 | 74,125 | ||||||

| Hire purchase obligation3 | 40,300 | 16,181 | ||||||

| Total contractual obligations | $ | 688,531 | $ | 159,890 | ||||

| 1 | Amount includes operating lease right-of-use obligations. We have one office space leasing agreement with our Chief Executive Officer and director, Mr. Kai Cheong Wong, and three office space leasing agreements with third party. |

| 2 | Represents the loan agreement with our Chief Executive Officer and director, Mr. Kai Cheong Wong, for the acquisition of property. |

| 3 | Represents the hire purchase agreement for the acquisition of motor vehicle. |

There were no outstanding obligations that were considered material as of March 31, 2026.

Critical Accounting Policies and Estimates

In preparing our Consolidated Financial Statements in accordance with generally accepted accounting principles in the United States (“GAAP”) and pursuant to the rules and regulations of the SEC, we make assumptions, judgments and estimates that affect the reported amounts of assets, liabilities, revenue and expenses, and related disclosures of contingent assets and liabilities. We base our assumptions, judgments and estimates on historical experience and various other factors that we believe to be reasonable under the circumstances. Actual results could differ materially from these estimates under different assumptions or conditions. We evaluate our assumptions, judgments and estimates on a regular basis. We also discuss our critical accounting policies and estimates with the Audit Committee of the Board of Directors.

-3-

We believe that the assumptions, judgments and estimates involved in the accounting for revenue recognition and credit losses have the greatest potential impact on our Consolidated Financial Statements. These areas are key components of our results of operations and are based on complex rules requiring us to make judgments and estimates, and consequently, we consider these to be our critical accounting policies. Historically, our assumptions, judgments and estimates relative to our critical accounting policies have not differed materially from actual results.

Credit losses

The Company estimates and records a provision for its expected credit losses related to its financial instruments, including its trade receivables. Management considers historical collection rates, the current financial status of the Company’s customers, macroeconomic factors, and other industry-specific factors when evaluating current expected credit losses. Forward-looking information is also considered in the evaluation of current expected credit losses. However, because of the short time to the expected receipt of accounts receivable, management believes that the carrying value, net of expected losses, approximates fair value and therefore, relies more on historical and current analysis of such financial instruments, including its trade receivables.

Credit loss rate is determined by historical collection based on aging schedule, adjusted for current conditions using reasonable and supportable forecasts. Based on the aging categorization and the adjusted loss rate per category, an allowance for credit losses is calculated by multiplying the adjusted loss rate with the amortized cost in the respective age category.

In July 2025, the FASB issued ASU 2025-05, Financial Instruments—Credit Losses (Topic 326), which introduces a practical expedient for measuring expected credit losses on trade receivables and contract assets. Under ASU 2025-05, an entity is required to disclose whether it has elected to use the practical expedient. An entity that makes the accounting policy election is required to disclose the date through which subsequent cash collections are evaluated. ASU 2025-05 is effective for fiscal years beginning after December 15, 2025, and interim periods within fiscal years beginning after December 15, 2026. Early adoption is permitted. The Company already adopted this ASU on its consolidated financial statements and related disclosure. The Company has elected practical expedient under ASU 2025-05 for the quarter ended March 31, 2026 which permits assuming that current conditions as of the balance sheet date will remain unchanged for the remaining life of the asset when estimating expected credit losses. Accordingly, the Company’s estimate of expected credit losses for current accounts receivables is based on the delinquency status of those uncollected balances as of March 31, 2026. The Company calculates the expected credit loss rate by applying the rate of change between the balances from the previous quarter and the uncollected balances in the current quarter on the historical loss rate.

Revenue recognition

The Company follows the guidance of ASC 606, “Revenue from Contracts” (“ASC 606”). ASC 606 creates a five-step model that requires entities to exercise judgment when considering the terms of contracts, which includes (1) identifying the contracts or agreements with a customer, (2) identifying our performance obligations in the contract or agreement, (3) determining the transaction price, (4) allocating the transaction price to the separate performance obligations, and (5) recognizing revenue as each performance obligation is satisfied. The Company only applies the five-step model to contracts when it is probable that the Company will collect the consideration it is entitled to in exchange for the services it transfers to its clients.

The Company’s revenue consists of revenue from providing information technology services such as business system integration and management services, computer programming activities and services to the customers.

-4-

Recent Adopted Accounting Pronouncements

In July 2025, the FASB issued ASU 2025-05, Financial Instruments—Credit Losses (Topic 326), which introduces a practical expedient for measuring expected credit losses on trade receivables and contract assets. Under ASU 2025-05, an entity is required to disclose whether it has elected to use the practical expedient. An entity that makes the accounting policy election is required to disclose the date through which subsequent cash collections are evaluated. ASU 2025-05 is effective for fiscal years beginning after December 15, 2025, and interim periods within fiscal years beginning after December 15, 2026. Early adoption is permitted. The Company already adopted this ASU on its consolidated financial statements and related disclosure during the third quarter of 2025.

Other than the pronouncements adopted as noted above, there are no recently issued accounting standards expected to have a material impact on the Company’s consolidated financial statements and related disclosures.

Item 3 Quantitative and Qualitative Disclosures About Market Risk.

As a “smaller reporting company” as defined by Item 10 of Regulation S-K, the Company is not required to provide information required by this Item.

Item 4 Controls and Procedures.

Disclosure Controls and Procedures

We maintain disclosure controls and procedures, as defined in Rule 13a-15(e) promulgated under the Securities Exchange Act of 1934 (the “Exchange Act”), that are designed to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission’s rules and forms and that such information is accumulated and communicated to our management, including our principal executive and principal financial officers, or persons performing similar functions, as appropriate, to allow timely decisions regarding required disclosure.

We carried out an evaluation, under the supervision and with the participation of our management, including our chief executive officer, of the effectiveness of our disclosure controls and procedures as of March 31, 2026. Based on the evaluation of these disclosure controls and procedures, and in light of the material weaknesses found in our internal controls over financial reporting, our chief executive officer concluded that our disclosure controls and procedures were not effective.

The matters involving internal controls and procedures that our management considered to be material weaknesses under the standards of the Public Company Accounting Oversight Board were: (i) inadequate written policies and procedures for accounting and financial reporting in accordance with the requirements and application of U.S. GAAP and SEC guidelines; (ii) inadequate segregation of duties and effective risk assessment; and (iii) lack of internal audit function due to the fact that the Company lacks qualified personnel to perform the internal audit functions effectively and that the scope and effectiveness of the internal audit function are yet to be developed. The aforementioned material weaknesses were identified by our chief executive officer in connection with the review of our financial statements as of March 31, 2026.

-5-

Management’s Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act. Our internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. The internal controls for the Company are provided by executive management’s review and approval of all transactions. Our internal control over financial reporting also includes those policies and procedures that:

| ● | Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the company; | |

| ● | Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with accounting principles generally accepted in the United States of America and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and | |

| ● | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the company’s assets that could have a material effect on the financial statements. |

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management assessed the effectiveness of the Company’s internal control over financial reporting as of March 31, 2026. In making this assessment, management used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control-Integrated Framework. Management’s assessment included an evaluation of the design of our internal control over financial reporting and testing of the operational effectiveness of these controls.