2 Safe Harbor Statement New slide This presentation contains statements which, to the

extent they are not statements of historical or present fact, constitute “forward-looking statements” under the securities laws. These forward-looking statements are intended to provide management’s current expectations or plans for our

future operating and financial performance, business prospects, outcomes of regulatory proceedings, market conditions, and other matters, based on what we believe to be reasonable assumptions and on information currently available to us.

Forward-looking statements can be identified by the use of words such as “believe,” “expect,” “expectations,” “plans,” “strategy,” “prospects,” “estimate,” “project,” “target,” “anticipate,” “will,” “should,” “see,” “guidance,” “outlook,”

“confident,” “may,” and other words of similar meaning. The absence of such words, expressions or statements, however, does not mean that the statements are not forward-looking. In particular, express or implied statements relating to future

earnings, cash flow, results of operations, uses of cash, tax rates and other measures of financial performance, future actions, conditions or events, potential future plans, strategies or transactions of DT Midstream, and other statements

that are not historical facts, are forward-looking statements. Forward-looking statements are not guarantees of future results and conditions, but rather are subject to numerous assumptions, risks, and uncertainties that may cause actual

future results to be materially different from those contemplated, projected, estimated, or budgeted. Many factors may impact forward-looking statements of DT Midstream including, but not limited to, the following: changes in general economic

conditions, including increases in interest rates and associated Federal Reserve policies, a potential economic recession, and the impact of inflation on our business; industry changes, including the impact of consolidations, alternative

energy sources, technological advances, infrastructure constraints and changes in competition; changes in global trade policies and tariffs; global and domestic supply chain disruptions; actions taken by third-party operators, producers,

processors, transporters and gatherers; changes in expected production from Expand Energy and other third parties in our areas of operation; demand for natural gas gathering, transmission, storage, transportation, sand mining, and water

services; the availability and price of natural gas to the consumer compared to the price of alternative and competing fuels; our ability to successfully and timely implement our business plan; our ability to complete organic growth projects

on time and on budget; our ability to finance, complete, or successfully integrate acquisitions; our ability to realize the anticipated benefits from acquisitions and our ability to manage the risks associated with acquisition activity; the

price and availability of debt and equity financing; restrictions in our existing and any future credit facilities and indentures; the effectiveness of our information technology and operational technology systems and practices to detect and

defend against evolving cyber attacks on United States critical infrastructure; changing laws regarding cybersecurity and data privacy, and any cybersecurity threat or event; operating hazards, environmental risks, and other risks incidental

to gathering, storing and transporting natural gas; geologic and reservoir risks and considerations; natural disasters, adverse weather conditions, casualty losses and other matters beyond our control; the impact of outbreaks of illnesses,

epidemics and pandemics, and any related economic effects; the impacts of geopolitical events, including the conflicts in Ukraine and the Middle East; labor relations and markets, including the ability to attract, hire and retain key employee

and contract personnel; large customer defaults; changes in tax status, as well as changes in tax rates and regulations; the effects and associated cost of compliance with existing and future laws and governmental regulations, such as the

Inflation Reduction Act and the One Big Beautiful Bill Act; changes in environmental laws, regulations or enforcement policies, including laws and regulations relating to pipeline safety, climate change and greenhouse gas emissions; changes

in laws and regulations or enforcement policies, including those relating to construction and operation of new interstate gas pipelines, ratemaking to which our pipelines may be subject, or other non-environmental laws and regulations; our

ability to qualify for federal income tax credits; ability to develop low carbon business opportunities and deploy greenhouse gas reducing technologies; changes in insurance markets impacting costs and the level and types of coverage

available; the timing and extent of changes in commodity prices; the success of our risk management strategies; the suspension, reduction or termination of our customers’ obligations under our commercial agreements; disruptions due to

equipment interruption or failure at our facilities, or third-party facilities on which our business is dependent; the effects of future litigation; and the risks described in our Annual Report on Form 10-K for the year ended December 31,

2025 and our reports and registration statements filed from time to time with the SEC. The above list of factors is not exhaustive. New factors emerge from time to time. We cannot predict what factors may arise or how such factors may cause

actual results to vary materially from those stated in forward-looking statements, see the discussion under the section entitled “Risk Factors” in our Annual Report for the year ended December 31, 2025, filed with the SEC on Form 10-K and any

other reports filed with the SEC. Given the uncertainties and risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement, you should not put undue reliance on any

forward-looking statements. Any forward-looking statements speak only as of the date on which such statements are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements,

whether as a result of new information, subsequent events or otherwise.

Definition and reconciliation of Adjusted EBITDA (non-GAAP) to net income included in

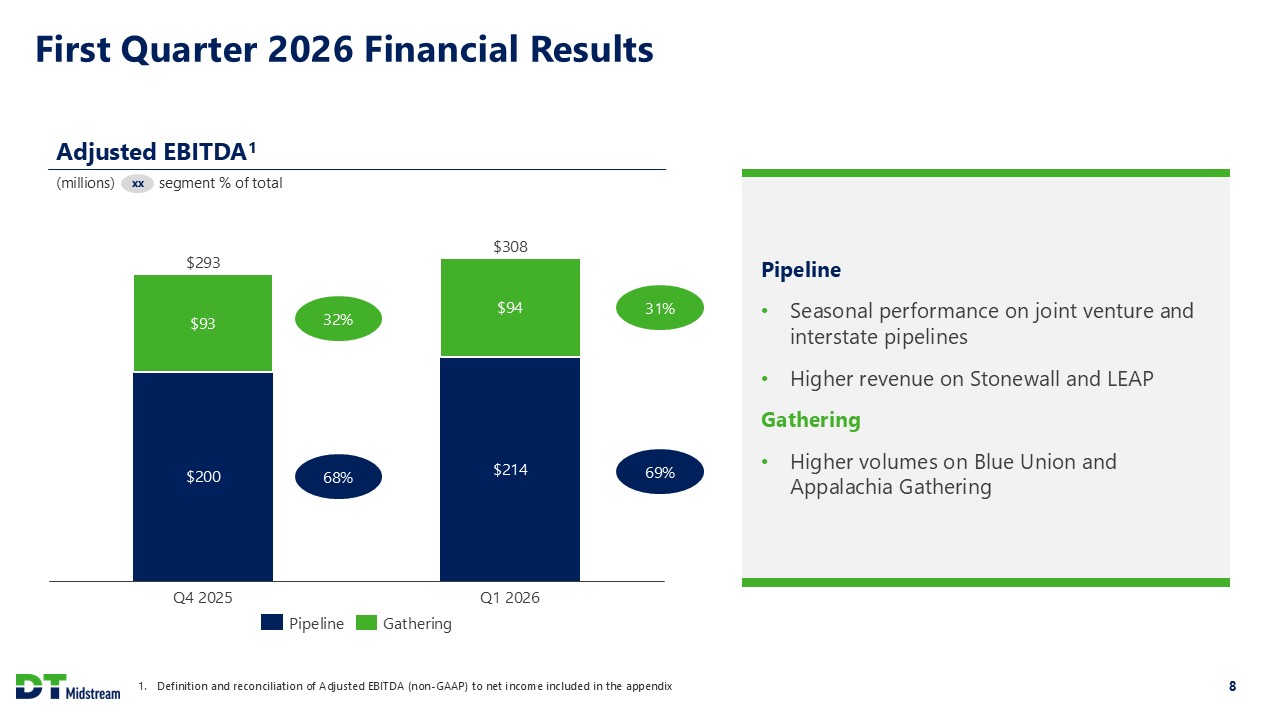

the appendix 3 First Quarter 2026 Accomplishments Strong financial performance First quarter 2026 net income of $130 million and Adjusted EBITDA1 of $308 million Reaffirming 2026 and 2027 Adjusted EBITDA guidance range and early outlook

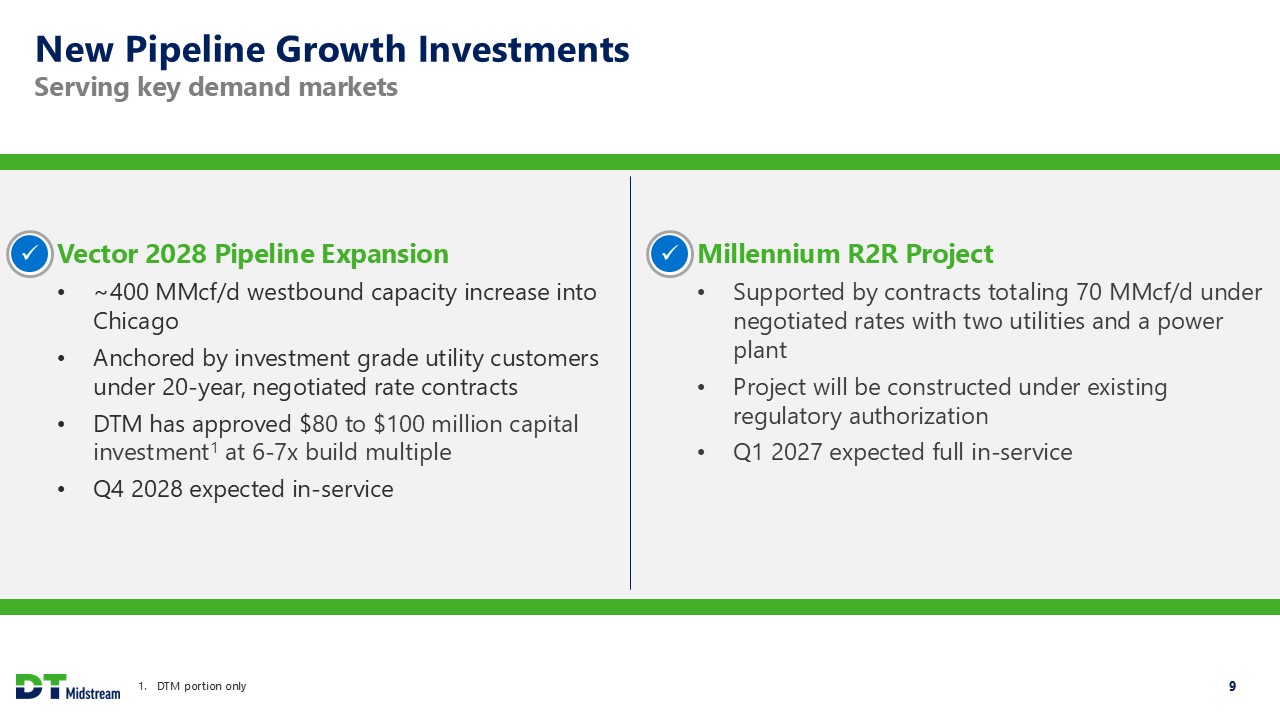

of $1,155 - $1,225 million and $1,225 - $1,295 million, respectively Executing on organic growth opportunities and construction projects DTM has approved investment in the Vector 2028 Pipeline expansion and Millennium R2R project

Midwestern Gas Transmission power plant lateral placed in-service on-time and under budget Progressing commercial opportunities Executed new agreement to serve new utility scale power development off of Midwestern Pipeline Recontracted

~30% of Midwestern Pipeline’s capacity with term extensions ranging from 5 – 25 years Commercialized new interconnect on NEXUS to serve data center generation project Received customer interest in excess of offered capacity for recently

closed open seasons on both Midwestern and Vector Pipelines

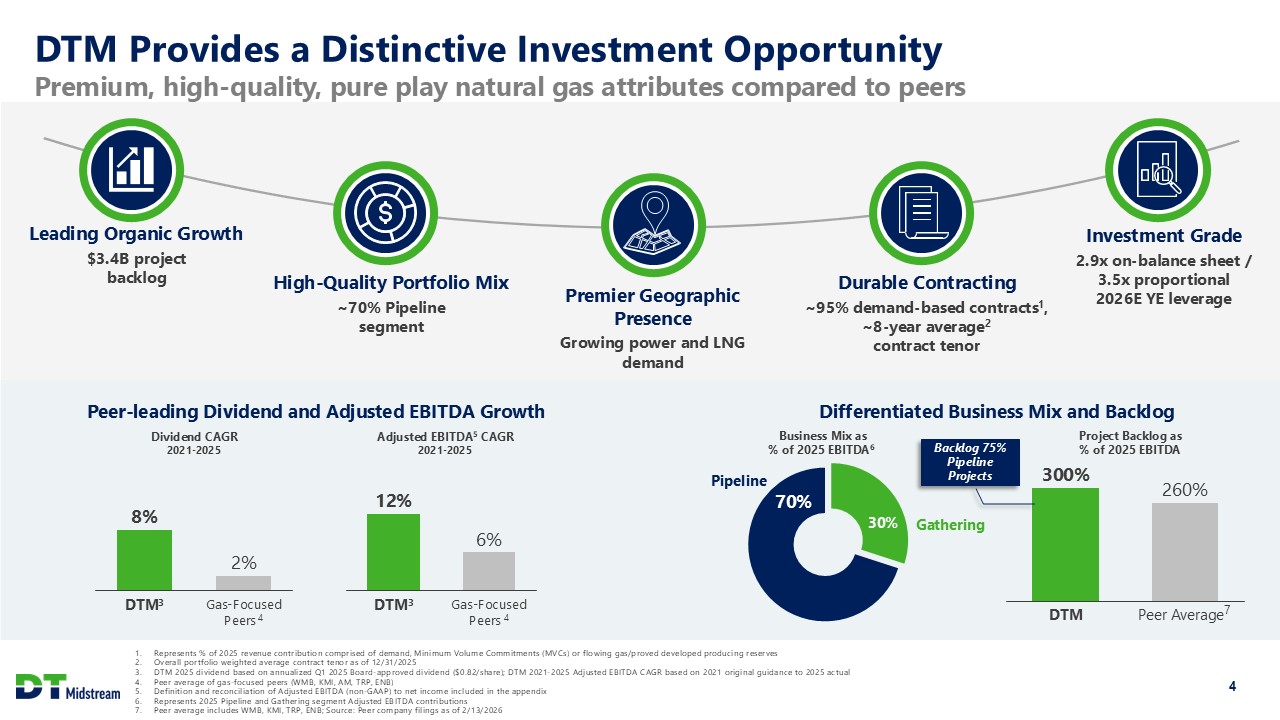

Leading Organic Growth $3.4B project backlog DTM Provides a Distinctive Investment

Opportunity Premium, high-quality, pure play natural gas attributes compared to peers High-Quality Portfolio Mix ~70% Pipeline segment Premier Geographic Presence Growing power and LNG demand Durable Contracting ~95% demand-based

contracts1, ~8-year average2 contract tenor Represents % of 2025 revenue contribution comprised of demand, Minimum Volume Commitments (MVCs) or flowing gas/proved developed producing reserves Overall portfolio weighted average contract

tenor as of 12/31/2025 DTM 2025 dividend based on annualized Q1 2025 Board-approved dividend ($0.82/share); DTM 2021-2025 Adjusted EBITDA CAGR based on 2021 original guidance to 2025 actual Peer average of gas-focused peers (WMB, KMI, AM,

TRP, ENB) Definition and reconciliation of Adjusted EBITDA (non-GAAP) to net income included in the appendix Represents 2025 Pipeline and Gathering segment Adjusted EBITDA contributions Peer average includes WMB, KMI, TRP, ENB; Source:

Peer company filings as of 2/13/2026 Investment Grade 2.9x on-balance sheet / 3.5x proportional 2026E YE leverage DTM3 Gas-Focused Peers 4 8% 2% Adjusted EBITDA5 CAGR 2021-2025 Dividend CAGR 2021-2025 Differentiated Business Mix

and Backlog Business Mix as % of 2025 EBITDA6 Pipeline Gathering 70% 4 30% Peer-leading Dividend and Adjusted EBITDA Growth DTM Peer Average7 300% 260% Project Backlog as % of 2025 EBITDA DTM3 Gas-Focused Peers

4 12% 6% Backlog 75% Pipeline Projects

Represents 2026-2030 probability-weighted capex Pre-FID Louisiana CCS

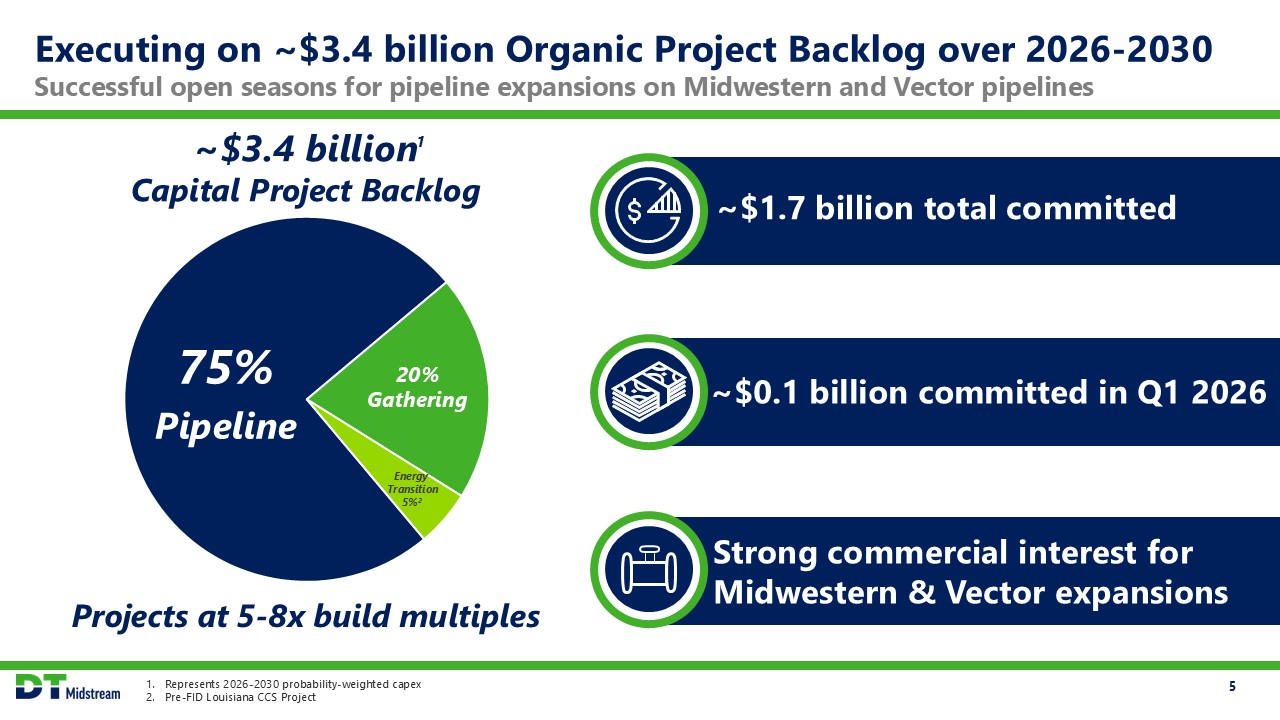

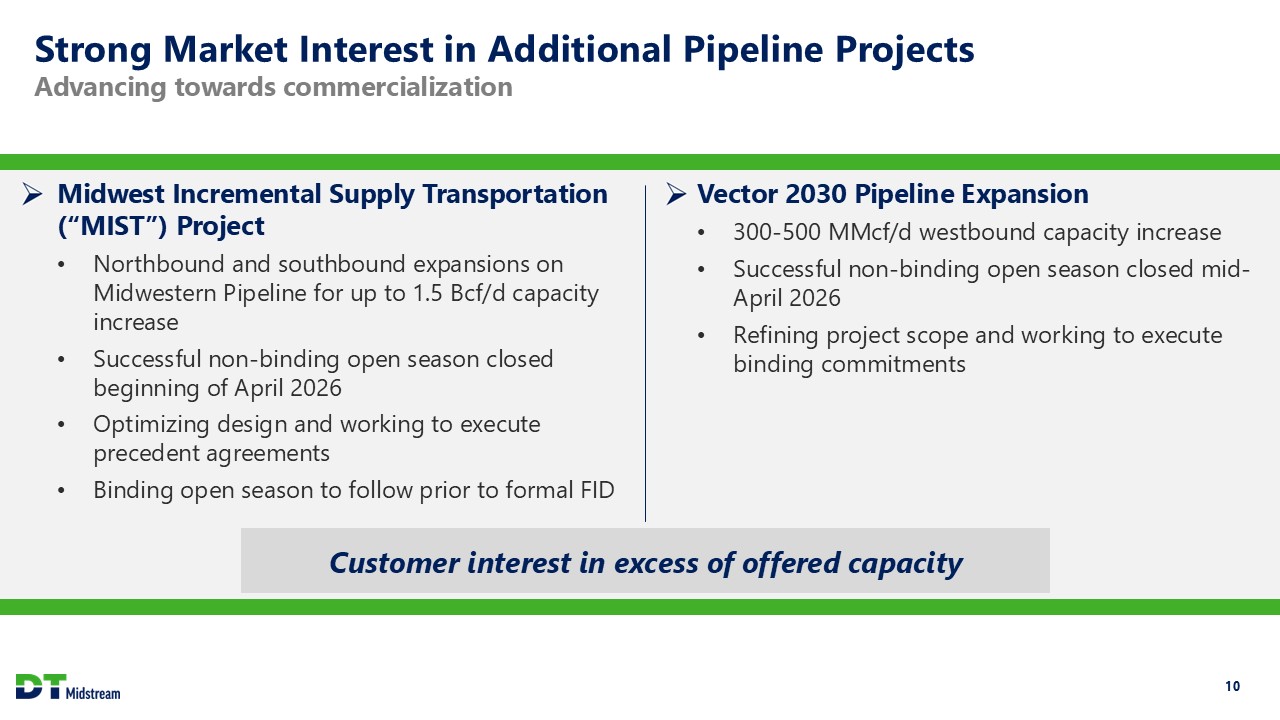

Project 5 Executing on ~$3.4 billion Organic Project Backlog over 2026-2030 Successful open seasons for pipeline expansions on Midwestern and Vector pipelines ~50% Reached FID 50% Pre-FID ~$3.4 billion Capital Project Backlog

~$1.7 billion total committed ~$0.1 billion committed in Q1 2026 Strong commercial interest for Midwestern & Vector expansions 1 75% Pipeline 20% Gathering Projects at 5-8x build multiples

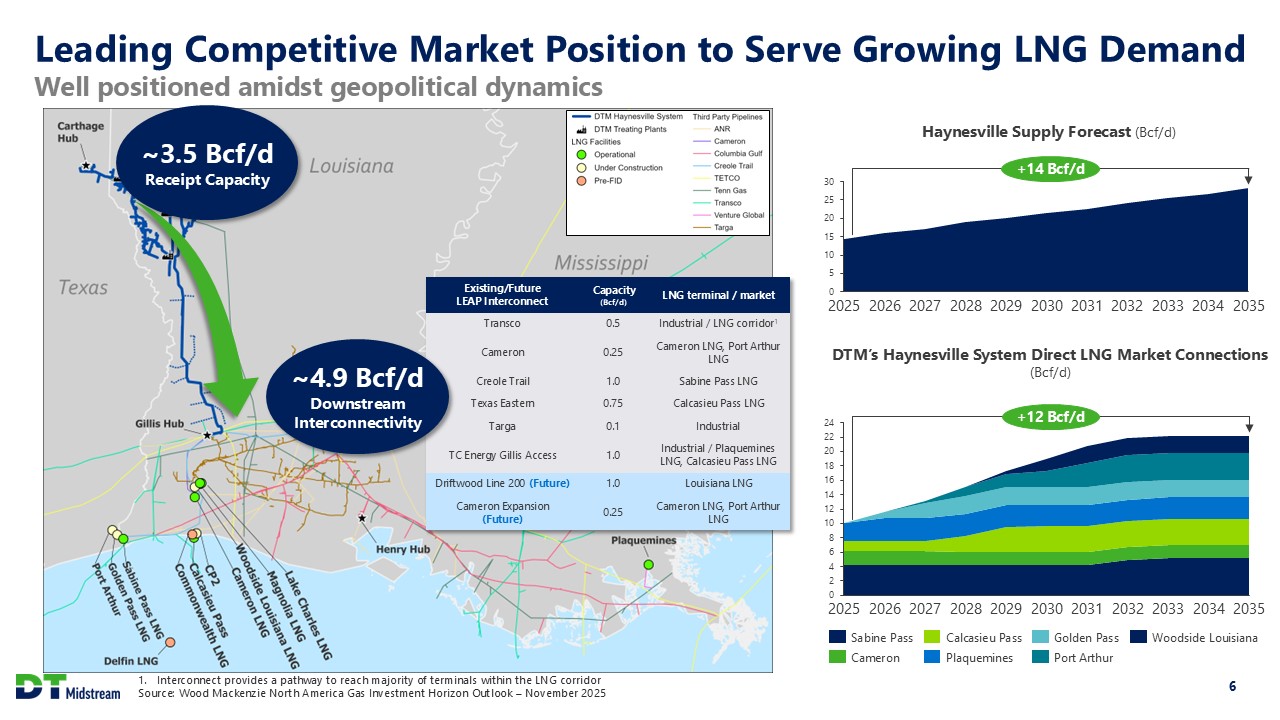

Interconnect provides a pathway to reach majority of terminals within the LNG

corridor Source: Wood Mackenzie North America Gas Investment Horizon Outlook – November 2025 6 Leading Competitive Market Position to Serve Growing LNG Demand Well positioned amidst geopolitical

dynamics 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 +14 Bcf/d Haynesville Supply Forecast (Bcf/d) 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 +12 Bcf/d DTM’s Haynesville System Direct LNG

Market Connections (Bcf/d) Sabine Pass Cameron Calcasieu Pass Plaquemines Golden Pass Port Arthur Woodside Louisiana Existing/Future LEAP Interconnect Capacity (Bcf/d) LNG terminal / market Transco 0.5 Industrial / LNG

corridor1 Cameron 0.25 Cameron LNG, Port Arthur LNG Creole Trail 1.0 Sabine Pass LNG Texas Eastern 0.75 Calcasieu Pass LNG Targa 0.1 Industrial TC Energy Gillis Access 1.0 Industrial / Plaquemines LNG, Calcasieu Pass

LNG Driftwood Line 200 (Future) 1.0 Louisiana LNG Cameron Expansion (Future) 0.25 Cameron LNG, Port Arthur LNG ~4.9 Bcf/d Downstream Interconnectivity ~3.5 Bcf/d Receipt Capacity

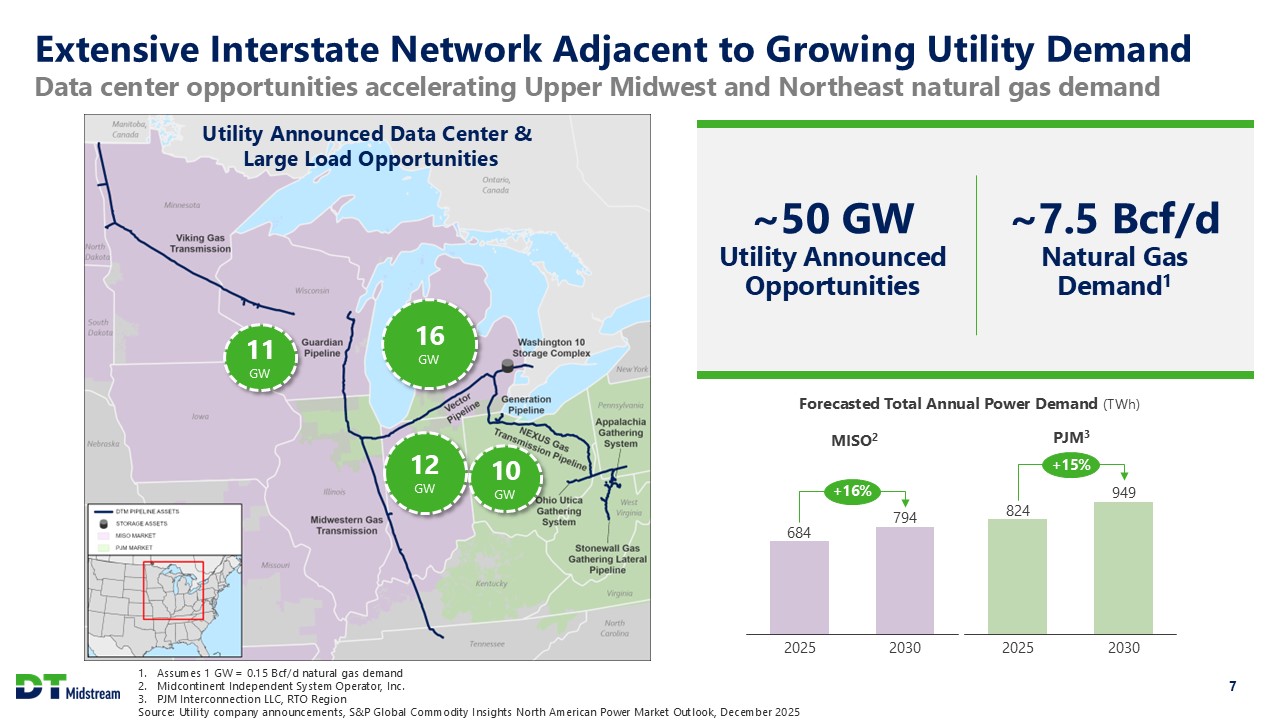

Assumes 1 GW = 0.15 Bcf/d natural gas demand Midcontinent Independent System Operator,

Inc. PJM Interconnection LLC, RTO Region Source: Utility company announcements, S&P Global Commodity Insights North American Power Market Outlook, December 2025 7 Extensive Interstate Network Adjacent to Growing Utility Demand Data

center opportunities accelerating Upper Midwest and Northeast natural gas demand 16 GW 11 GW 12 GW Utility Announced Data Center & Large Load Opportunities 10 GW ~50 GW Utility Announced Opportunities ~7.5 Bcf/d

Natural Gas Demand1 Forecasted Total Annual Power Demand (TWh) 2025 2030 +16% 2025 2030 +15% MISO2 PJM3

Definition and reconciliation of Adjusted EBITDA (non-GAAP) to net income included in

the appendix 8 First Quarter 2026 Financial Results Q4 2025 Q1 2026 $293 $308 Pipeline Gathering Pipeline Seasonal performance on joint venture and interstate pipelines Higher revenue on Stonewall and LEAP Gathering Higher

volumes on Blue Union and Appalachia Gathering 69% 31% xx Adjusted EBITDA1 (millions) segment % of total 68% 32%

Vector 2028 Pipeline Expansion ~400 MMcf/d westbound capacity increase into

Chicago Anchored by investment grade utility customers under 20-year, negotiated rate contracts DTM has approved $80 to $100 million capital investment1 at 6-7x build multiple Q4 2028 expected in-service Millennium R2R Project Supported

by contracts totaling 70 MMcf/d under negotiated rates with two utilities and a power plant Project will be constructed under existing regulatory authorization Q1 2027 expected full in-service DTM portion only 9 New Pipeline Growth

Investments Serving key demand markets

Midwest Incremental Supply Transportation (“MIST”) Project Northbound and southbound

expansions on Midwestern Pipeline for up to 1.5 Bcf/d capacity increase Successful non-binding open season closed beginning of April 2026 Optimizing design and working to execute precedent agreements Binding open season to follow prior to

formal FID Vector 2030 Pipeline Expansion 300-500 MMcf/d westbound capacity increase Successful non-binding open season closed mid-April 2026 Refining project scope and working to execute binding commitments 10 Strong Market Interest

in Additional Pipeline Projects Advancing towards commercialization Customer interest in excess of offered capacity

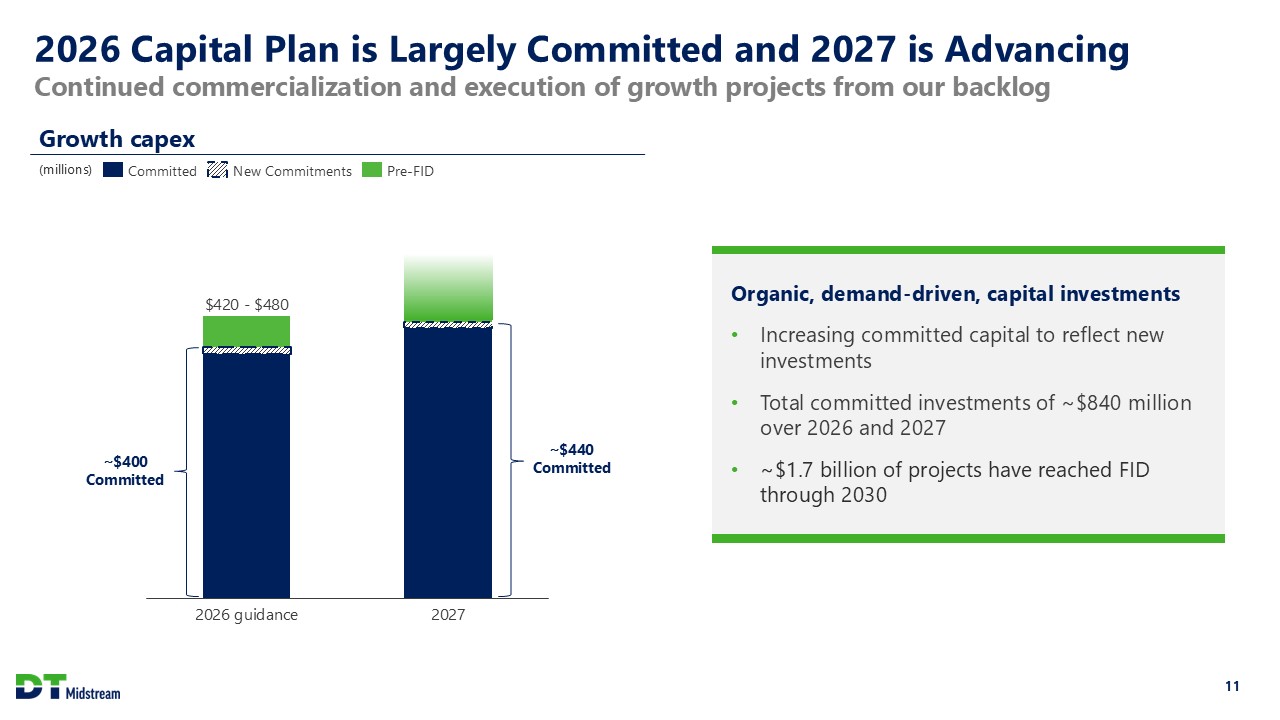

2026 guidance 2027 $420 - $480 11 2026 Capital Plan is Largely Committed and 2027 is

Advancing Continued commercialization and execution of growth projects from our backlog Growth capex (millions) Organic, demand-driven, capital investments Increasing committed capital to reflect new investments Total committed

investments of ~$840 million over 2026 and 2027 ~$1.7 billion of projects have reached FID through 2030 Committed New Commitments Pre-FID ~$400 Committed ~$440 Committed

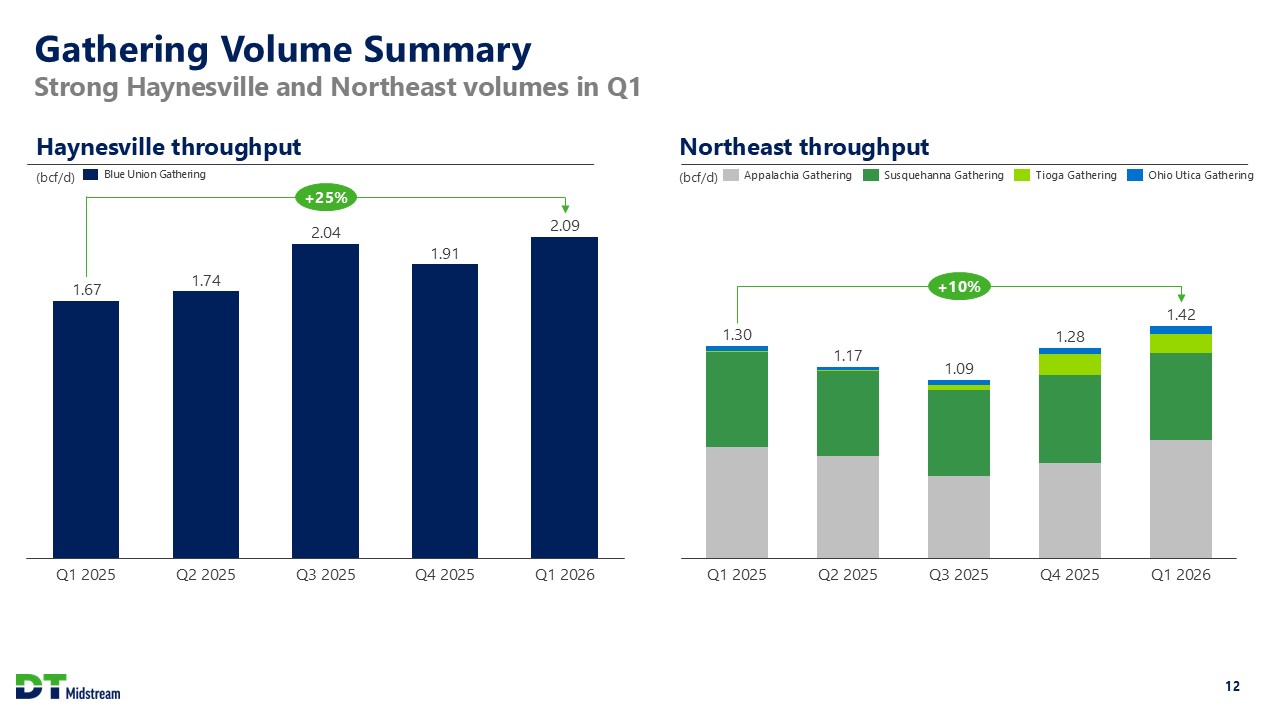

12 Gathering Volume Summary Strong Haynesville and Northeast volumes in Q1 Q1

2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 +25% Haynesville throughput (bcf/d) Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 1.30 1.17 1.09 1.28 1.42 +10% Northeast throughput (bcf/d) Appalachia Gathering Susquehanna

Gathering Tioga Gathering Ohio Utica Gathering Blue Union Gathering

Definition and reconciliation of Adjusted EBITDA (non-GAAP) to net income included in

the appendix Definition and reconciliation of Operating Earnings and Operating Earnings per Share (non-GAAP) to reported earnings included in the appendix; EPS calculation based on average share count of approximately 103 million shares

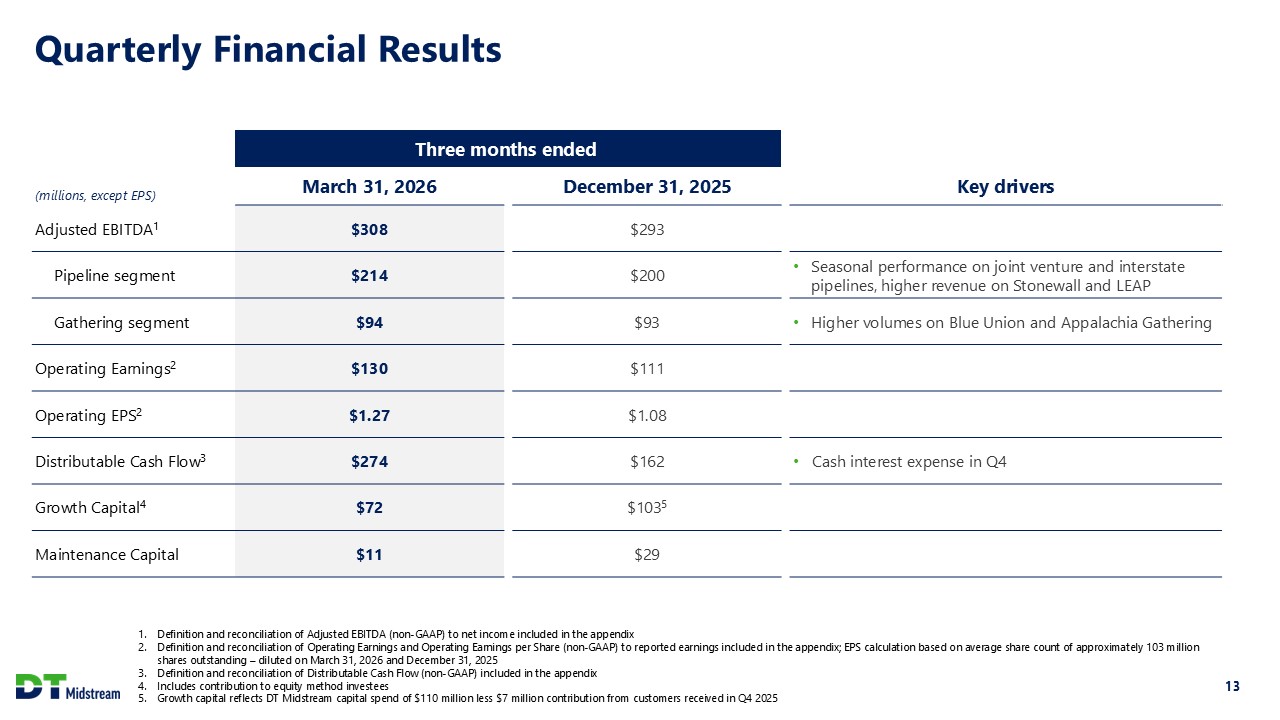

outstanding – diluted on March 31, 2026 and December 31, 2025 Definition and reconciliation of Distributable Cash Flow (non-GAAP) included in the appendix Includes contribution to equity method investees Growth capital reflects DT

Midstream capital spend of $110 million less $7 million contribution from customers received in Q4 2025 13 Quarterly Financial Results Three months ended (millions, except EPS) March 31, 2026 December 31, 2025 Key drivers Adjusted

EBITDA1 $308 $293 Pipeline segment $214 $200 Seasonal performance on joint venture and interstate pipelines, higher revenue on Stonewall and LEAP Gathering segment $94 $93 Higher volumes on Blue Union and Appalachia

Gathering Operating Earnings2 $130 $111 Operating EPS2 $1.27 $1.08 Distributable Cash Flow3 $274 $162 Cash interest expense in Q4 Growth Capital4 $72 $1035 Maintenance Capital $11 $29

14 Appendix

Definition and reconciliation of Adjusted EBITDA (non-GAAP) to net income included in

the appendix Definition and reconciliation of Operating Earnings and Operating Earnings per Share (non-GAAP) to reported earnings included in the appendix; EPS calculation based on average share count of approximately 103 million shares

outstanding - diluted Definition and reconciliation of Distributable Cash Flow (non-GAAP) to net income included in the appendix Includes contribution to equity method investees 15 2026/2027 Guidance Summary (millions, except

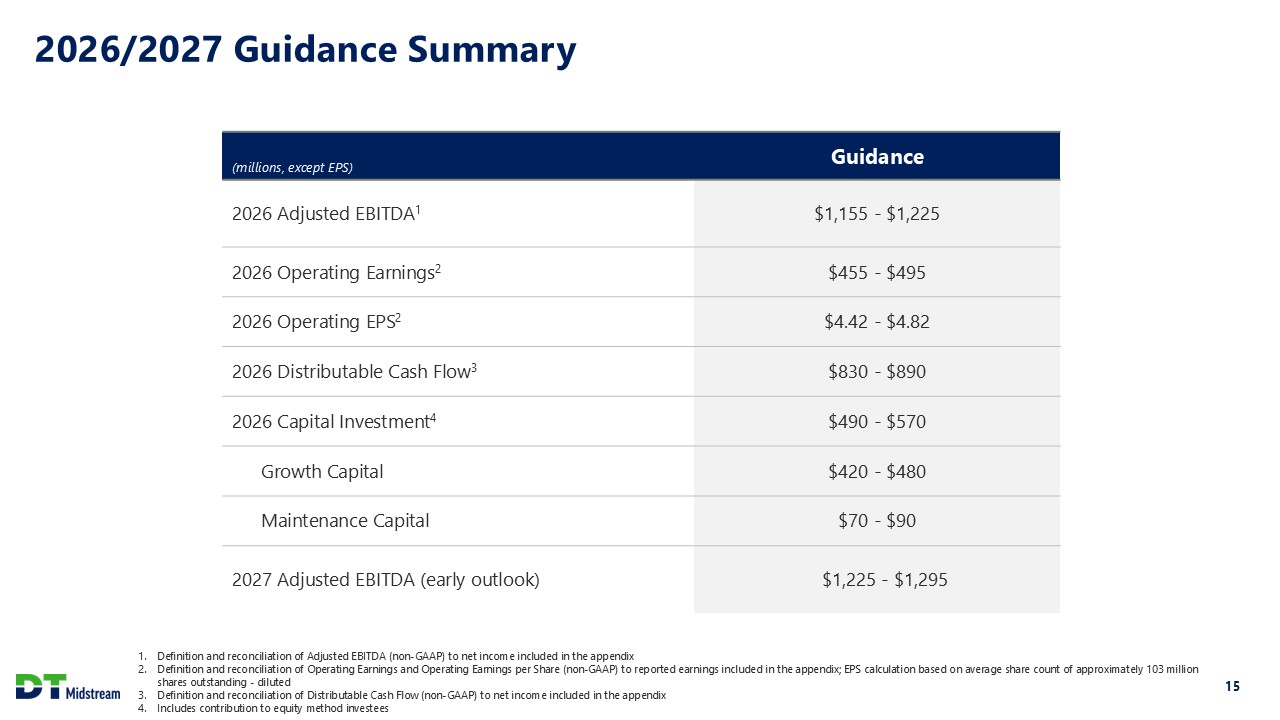

EPS) Guidance 2026 Adjusted EBITDA1 $1,155 - $1,225 2026 Operating Earnings2 $455 - $495 2026 Operating EPS2 $4.42 - $4.82 2026 Distributable Cash Flow3 $830 - $890 2026 Capital Investment4 $490 - $570 Growth Capital $420 -

$480 Maintenance Capital $70 - $90 2027 Adjusted EBITDA (early outlook) $1,225 - $1,295

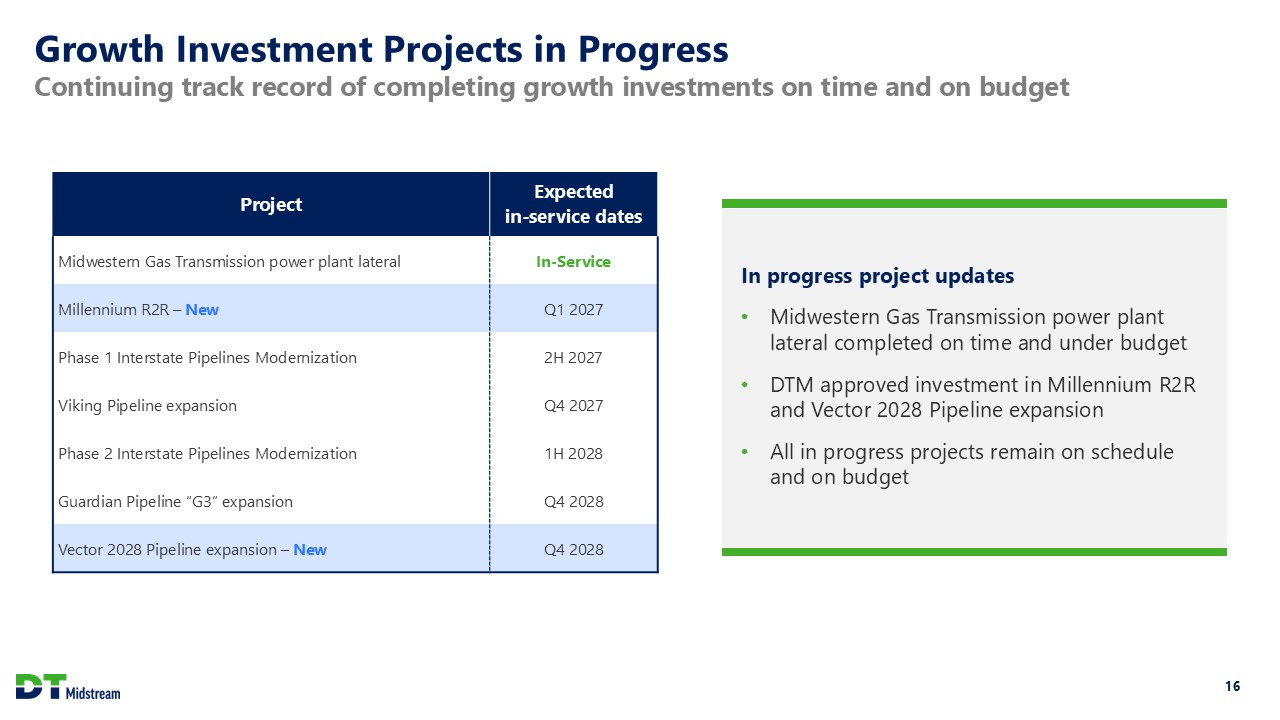

Growth Investment Projects in Progress Continuing track record of completing growth

investments on time and on budget In progress project updates Midwestern Gas Transmission power plant lateral completed on time and under budget DTM approved investment in Millennium R2R and Vector 2028 Pipeline expansion All in progress

projects remain on schedule and on budget Project Expected in-service dates Midwestern Gas Transmission power plant lateral In-Service Millennium R2R – New Q1 2027 Phase 1 Interstate Pipelines Modernization 2H 2027 Viking

Pipeline expansion Q4 2027 Phase 2 Interstate Pipelines Modernization 1H 2028 Guardian Pipeline “G3” expansion Q4 2028 Vector 2028 Pipeline expansion – New Q4 2028 16

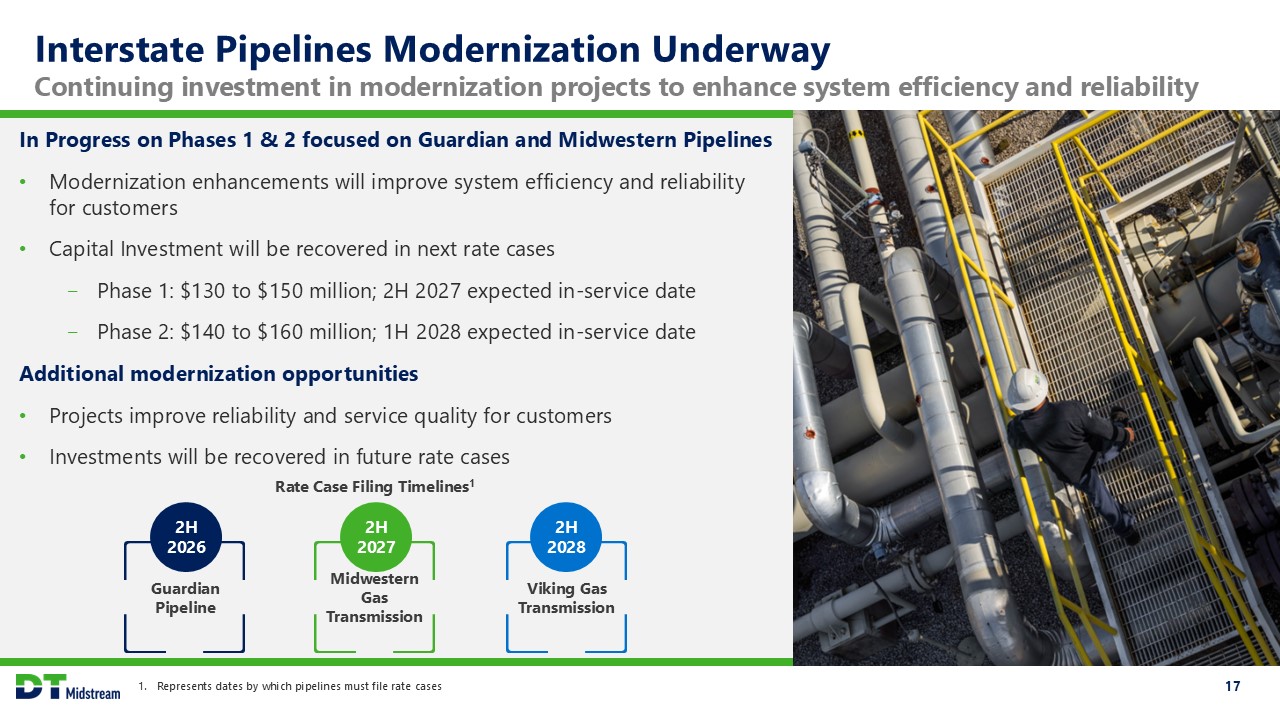

Represents dates by which pipelines must file rate cases 17 Interstate Pipelines

Modernization Underway Continuing investment in modernization projects to enhance system efficiency and reliability In Progress on Phases 1 & 2 focused on Guardian and Midwestern Pipelines Modernization enhancements will improve

system efficiency and reliability for customers Capital Investment will be recovered in next rate cases Phase 1: $130 to $150 million; 2H 2027 expected in-service date Phase 2: $140 to $160 million; 1H 2028 expected in-service

date Additional modernization opportunities Projects improve reliability and service quality for customers Investments will be recovered in future rate cases Rate Case Filing Timelines1 Guardian Pipeline Midwestern Gas

Transmission Viking Gas Transmission 2H 2026 2H 2027 2H 2028

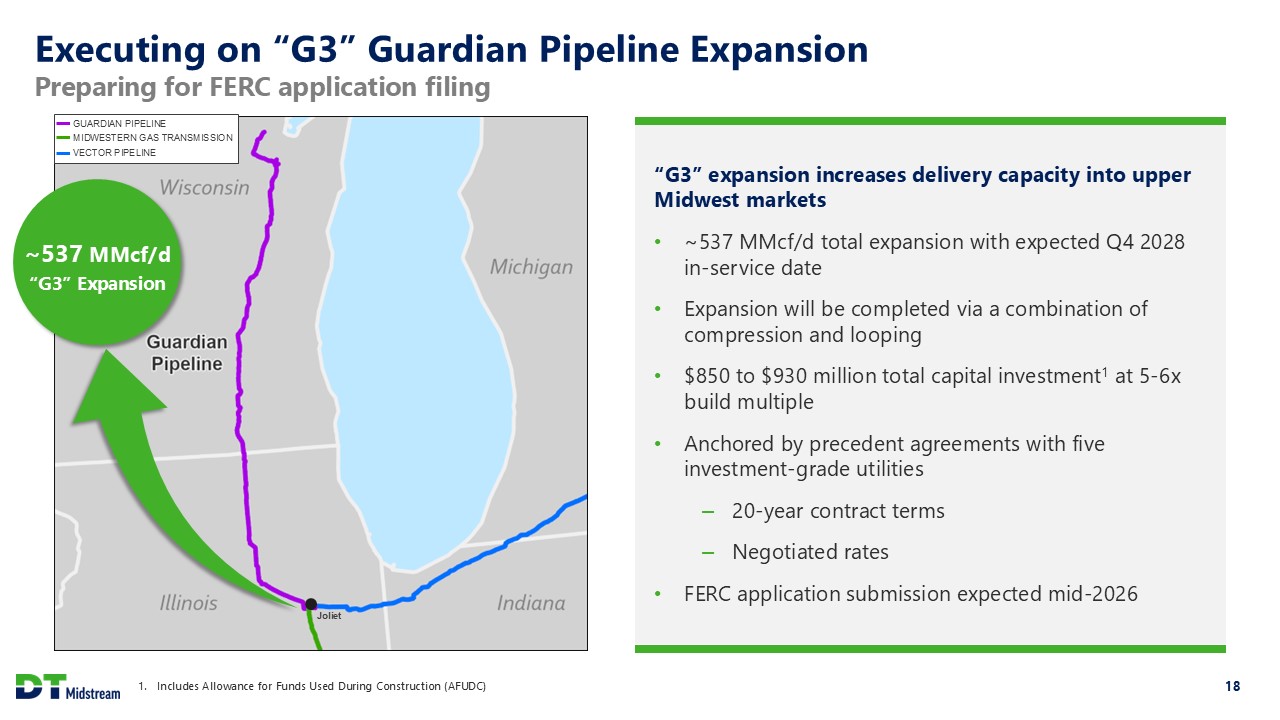

Includes Allowance for Funds Used During Construction (AFUDC) 18 Executing on “G3”

Guardian Pipeline Expansion Preparing for FERC application filing Map Update In Progress “G3” expansion increases delivery capacity into upper Midwest markets ~537 MMcf/d total expansion with expected Q4 2028 in-service date Expansion

will be completed via a combination of compression and looping $850 to $930 million total capital investment1 at 5-6x build multiple Anchored by precedent agreements with five investment-grade utilities 20-year contract terms Negotiated

rates FERC application submission expected mid-2026 GUARDIAN PIPELINE MIDWESTERN GAS TRANSMISSION VECTOR PIPELINE Joliet ~537 MMcf/d “G3” Expansion

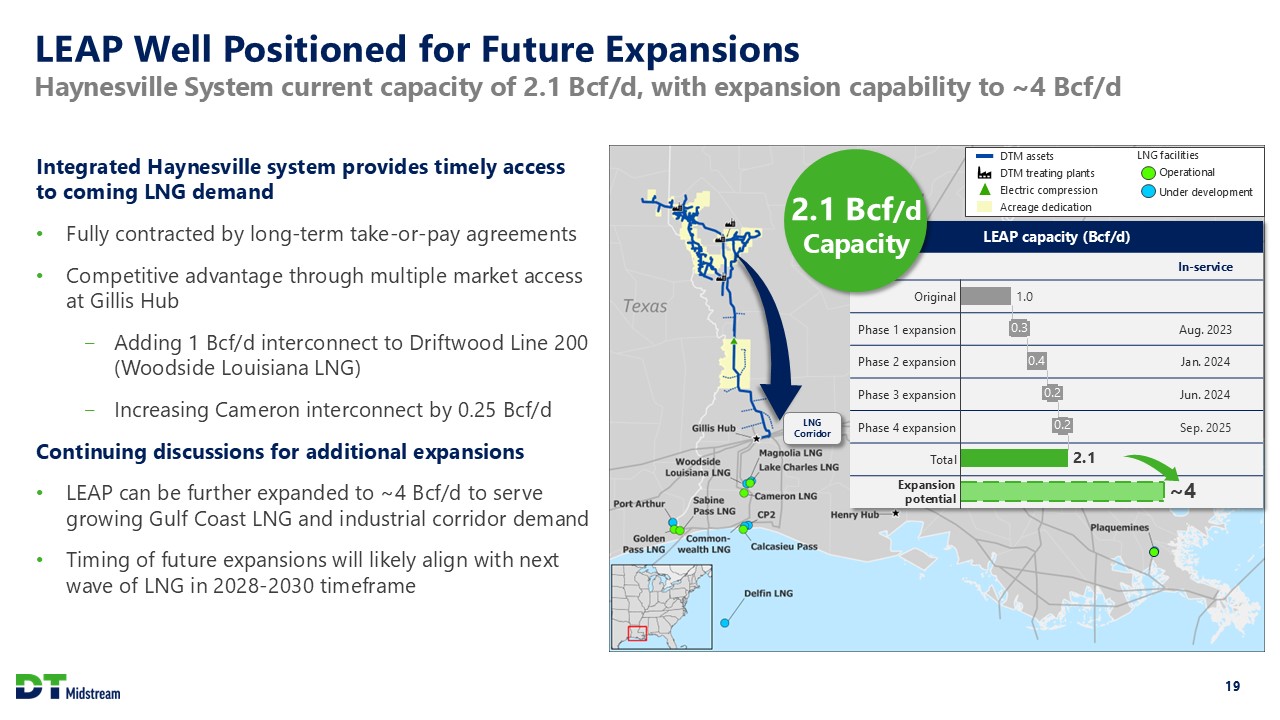

19 LEAP Well Positioned for Future Expansions Haynesville System current capacity of

2.1 Bcf/d, with expansion capability to ~4 Bcf/d LEAP capacity (Bcf/d) LEAP capacity (Bcf/d) In-service Original Phase 1 expansion Aug. 2023 Phase 2 expansion Jan. 2024 Phase 3 expansion Jun. 2024 Phase 4 expansion Sep.

2025 Total Expansion potential 0.3 0.2 0.2 2.1 Integrated Haynesville system provides timely access to coming LNG demand Fully contracted by long-term take-or-pay agreements Competitive advantage through multiple market access at

Gillis Hub Adding 1 Bcf/d interconnect to Driftwood Line 200 (Woodside Louisiana LNG) Increasing Cameron interconnect by 0.25 Bcf/d Continuing discussions for additional expansions LEAP can be further expanded to ~4 Bcf/d to serve growing

Gulf Coast LNG and industrial corridor demand Timing of future expansions will likely align with next wave of LNG in 2028-2030 timeframe ~4 DTM assets DTM treating plants LNG facilities Electric compression Operational Under

development Acreage dedication 2.1 Bcf/d Capacity LNG Corridor

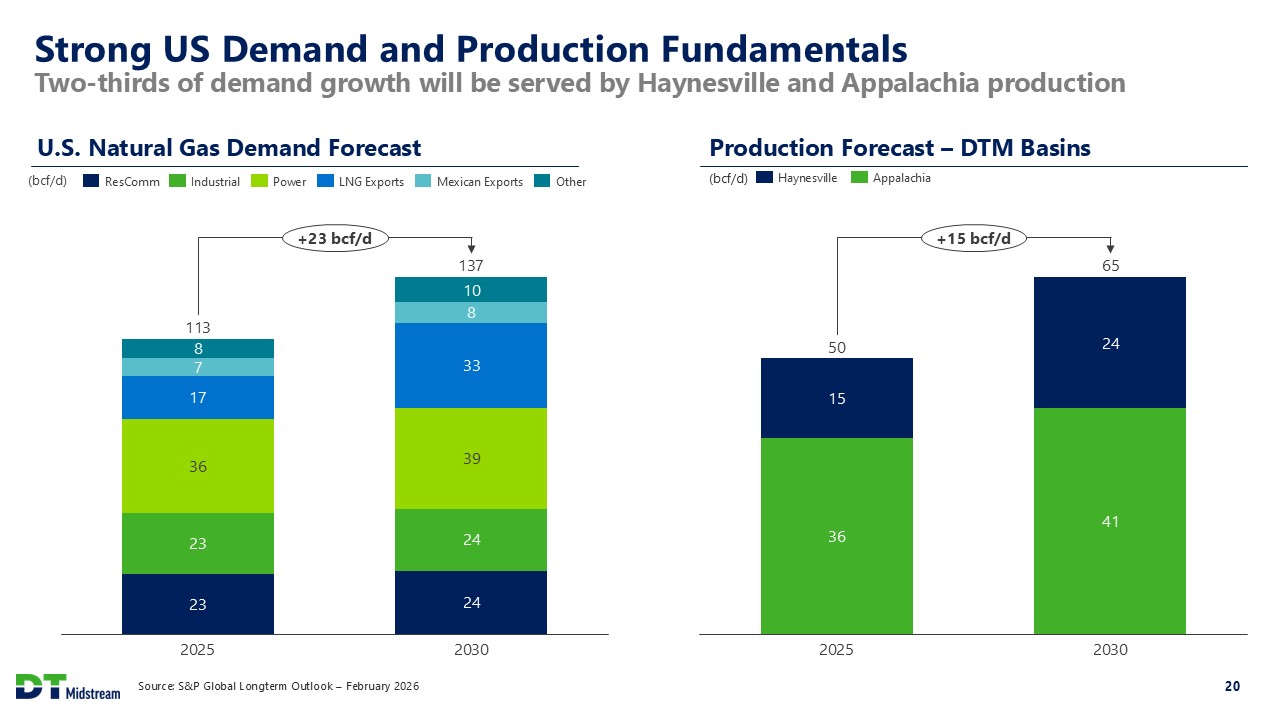

Source: S&P Global Longterm Outlook – February 2026 20 Strong US Demand and

Production Fundamentals Two-thirds of demand growth will be served by Haynesville and Appalachia production U.S. Natural Gas Demand Forecast 2025 2030 50 65 +15 bcf/d Production Forecast – DTM

Basins (bcf/d) Haynesville Appalachia (bcf/d) 2025 2030 113 137 +23 bcf/d Other Mexican Exports LNG Exports Power Industrial ResComm

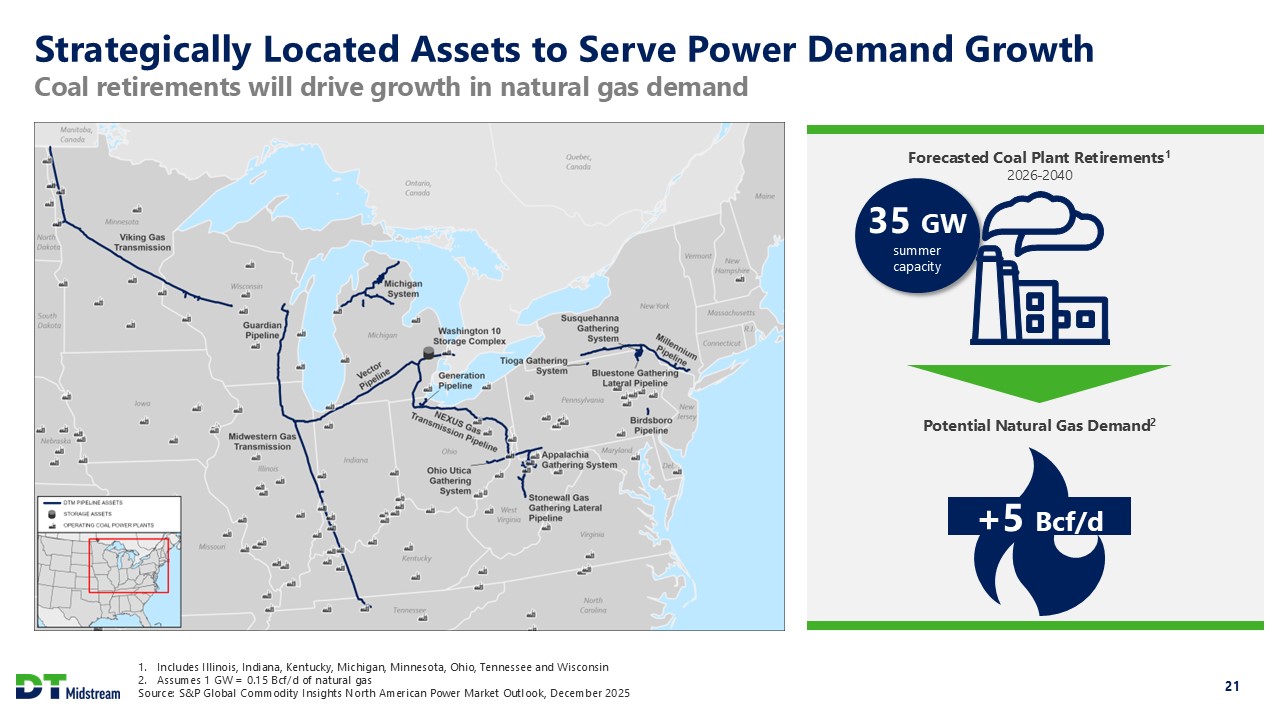

Includes Illinois, Indiana, Kentucky, Michigan, Minnesota, Ohio, Tennessee and

Wisconsin Assumes 1 GW = 0.15 Bcf/d of natural gas Source: S&P Global Commodity Insights North American Power Market Outlook, December 2025 21 Strategically Located Assets to Serve Power Demand Growth Coal retirements will drive

growth in natural gas demand 35 GW summer capacity Forecasted Coal Plant Retirements1 2026-2040 +5 Bcf/d Potential Natural Gas Demand2

22 Non-GAAP Definitions Adjusted EBITDA and Distributable Cash Flow (DCF) are non-GAAP

measures New slide Adjusted EBITDA is defined as GAAP net income attributable to DT Midstream before expenses for interest, taxes, depreciation and amortization, and loss from financing activities, further adjusted to include our

proportional share of net income from our equity method investees (excluding interest, taxes, depreciation and amortization), and to exclude certain items we consider non-routine. We believe Adjusted EBITDA is useful to us and external users

of our financial statements in understanding our operating results and the ongoing performance of our underlying business because it allows our management and investors to have a better understanding of our actual operating performance

unaffected by the impact of interest, taxes, depreciation, amortization and non-routine charges noted in the table below. We believe the presentation of Adjusted EBITDA is meaningful to investors because it is frequently used by analysts,

investors and other interested parties in our industry to evaluate a company’s operating performance without regard to items excluded from the calculation of such measure, which can vary substantially from company to company depending on

accounting methods, book value of assets, capital structure and the method by which assets were acquired, among other factors. We use Adjusted EBITDA to assess our performance by reportable segment and as a basis for strategic planning and

forecasting. Distributable Cash Flow (DCF) is calculated by deducting earnings from equity method investees, depreciation and amortization attributable to noncontrolling interests, cash interest expense, maintenance capital investment (as

defined below), and cash taxes from, and adding interest expense, income tax expense, depreciation and amortization, certain items we consider non-routine and dividends and distributions from equity method investees to, Net Income

Attributable to DT Midstream. Maintenance capital investment is defined as the total capital expenditures used to maintain or preserve assets or fulfill contractual obligations that do not generate incremental earnings. We believe DCF is a

meaningful performance measurement because it is useful to us and external users of our financial statements in estimating the ability of our assets to generate cash earnings after servicing our debt, paying cash taxes and making maintenance

capital investments, which could be used for discretionary purposes such as common stock dividends, retirement of debt or expansion capital expenditures. Adjusted EBITDA and DCF are not measures calculated in accordance with GAAP and

should be viewed as a supplement to and not a substitute for the results of operations presented in accordance with GAAP. There are significant limitations to using Adjusted EBITDA and DCF as a measure of performance, including the inability

to analyze the effect of certain recurring and non-recurring items that materially affect our net income or loss. Additionally, because Adjusted EBITDA and DCF exclude some, but not all, items that affect net income and are defined

differently by different companies in our industry, Adjusted EBITDA and DCF do not intend to represent net income attributable to DT Midstream, the most comparable GAAP measure, as an indicator of operating performance and are not necessarily

comparable to similarly titled measures reported by other companies. Reconciliation of net income attributable to DT Midstream to Adjusted EBITDA or DCF as projected for full-year 2026 or 2027 is not provided. We do not forecast net income

as we cannot, without unreasonable efforts, estimate or predict with certainty the components of net income. These components, net of tax, may include, but are not limited to, impairments of assets and other charges, divestiture costs,

acquisition costs, or changes in accounting principles. All of these components could significantly impact such financial measures. At this time, management is not able to estimate the aggregate impact, if any, of these items on future period

reported earnings. Accordingly, we are not able to provide a corresponding GAAP equivalent for Adjusted EBITDA or DCF.

23 Non-GAAP Definitions Operating Earnings and Operating Earnings per share are

non-GAAP measures New slide Use of Operating Earnings Information – Operating Earnings exclude non-recurring items, certain mark-to-market adjustments and discontinued operations. DT Midstream management believes that Operating Earnings

provide a more meaningful representation of the company’s earnings from ongoing operations and uses Operating Earnings as the primary performance measurement for external communications with analysts and investors. Internally, DT Midstream

uses Operating Earnings to measure performance against budget and to report to the Board of Directors. In this presentation, DT Midstream provides guidance for future period Operating Earnings. It is likely that certain items that impact

the company’s future period reported results will be excluded from operating results. A reconciliation to the comparable future period reported earnings is not provided because it is not possible to provide a reliable forecast of specific

line items (i.e., future non-recurring items, certain mark-to-market adjustments and discontinued operations). These items may fluctuate significantly from period to period and may have a significant impact on reported earnings.

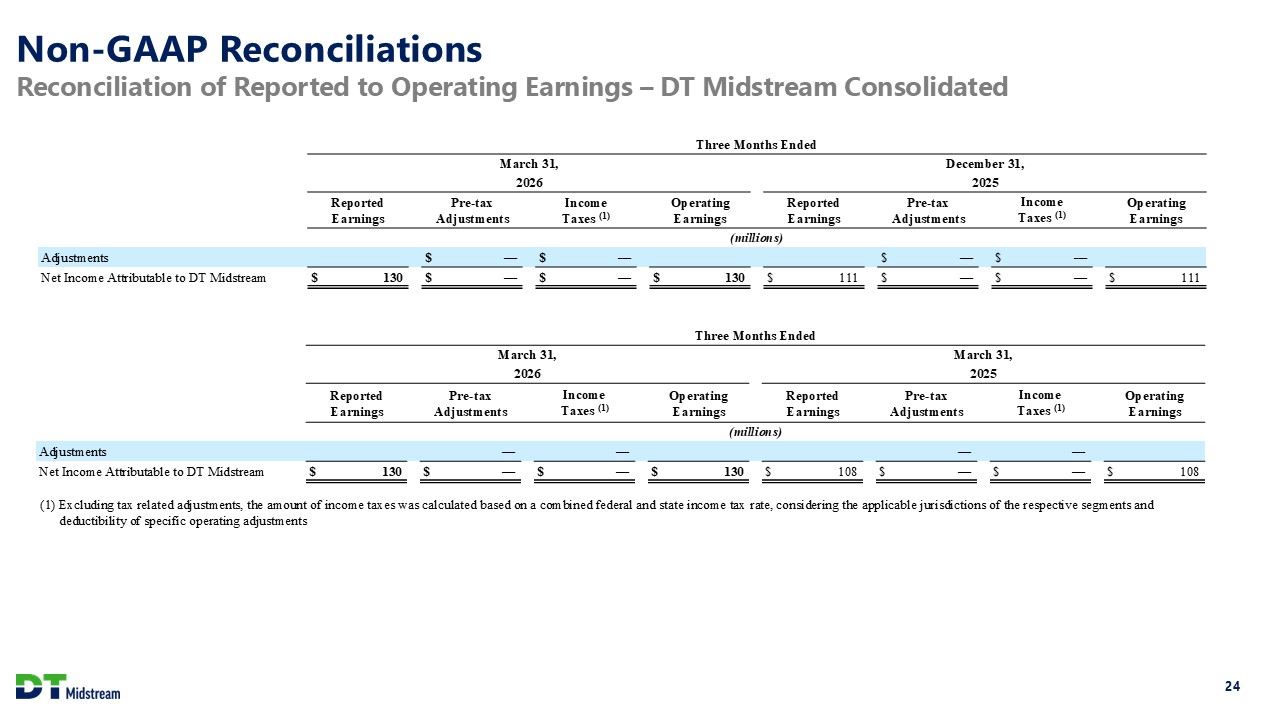

New slide 24 Non-GAAP Reconciliations Reconciliation of Reported to Operating

Earnings – DT Midstream Consolidated Three Months Ended March 31, December 31, 2026 2025 Reported Earnings Pre-tax Adjustments Income Taxes (1) Operating Earnings Reported Earnings Pre-tax Adjustments Income Taxes

(1) Operating Earnings (millions) Adjustments $ — $ — $ — $ — Net Income Attributable to DT Midstream $ 130 $ — $ — $ 130 $ 111 $ — $ — $ 111 Three Months Ended March 31, March

31, 2026 2025 Reported Earnings Pre-tax Adjustments Income Taxes (1) Operating Earnings Reported Earnings Pre-tax Adjustments Income Taxes (1) Operating Earnings (millions) Adjustments — — — — Net

Income Attributable to DT Midstream $ 130 $ — $ — $ 130 $ 108 $ — $ — $ 108 (1) Excluding tax related adjustments, the amount of income taxes was calculated based on a combined federal and state income tax

rate, considering the applicable jurisdictions of the respective segments and deductibility of specific operating adjustments

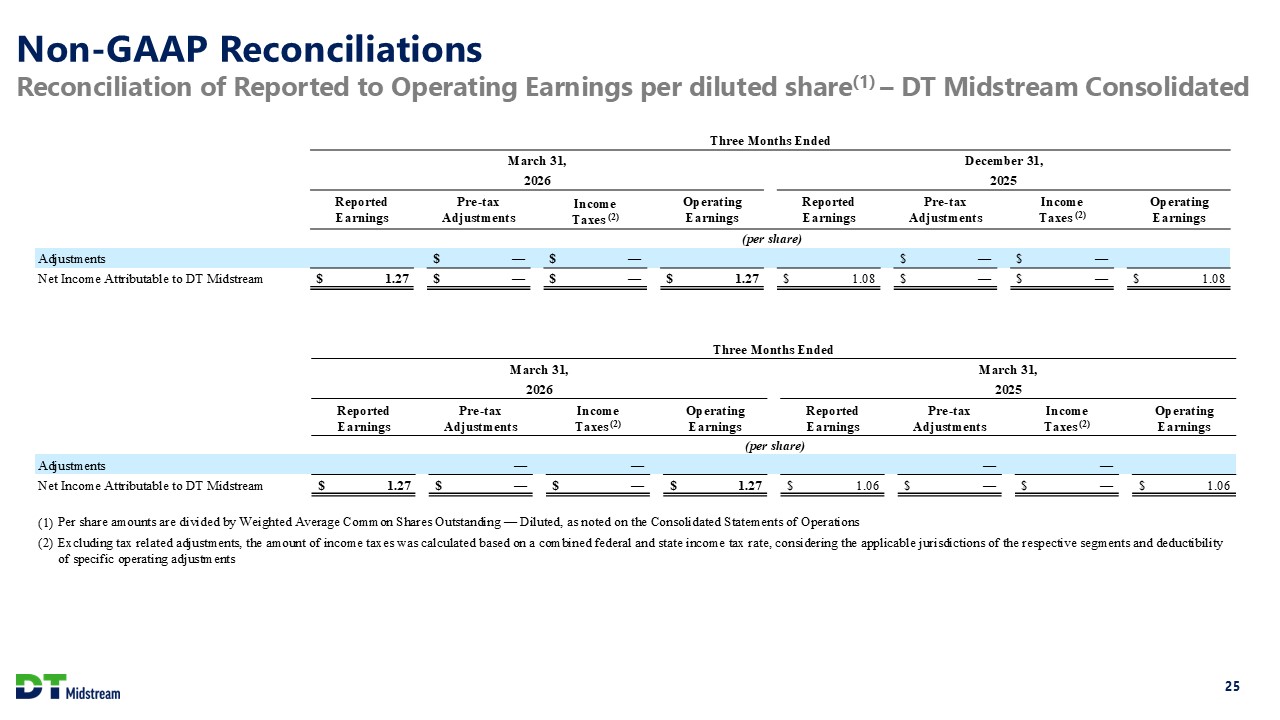

Non-GAAP Reconciliations New slide Reconciliation of Reported to Operating Earnings

per diluted share(1) – DT Midstream Consolidated 25 Three Months Ended March 31, December 31, 2026 2025 Reported Earnings Pre-tax Adjustments Income Taxes (2) Operating Earnings Reported Earnings Pre-tax

Adjustments Income Taxes (2) Operating Earnings (per share) Adjustments $ — $ — $ — $ — Net Income Attributable to DT Midstream $ 1.27 $ — $ — $ 1.27 $ 1.08 $ — $ — $ 1.08 Three

Months Ended March 31, March 31, 2026 2025 Reported Earnings Pre-tax Adjustments Income Taxes (2) Operating Earnings Reported Earnings Pre-tax Adjustments Income Taxes (2) Operating Earnings (per

share) Adjustments — — — — Net Income Attributable to DT Midstream $ 1.27 $ — $ — $ 1.27 $ 1.06 $ — $ — $ 1.06 (1) Per share amounts are divided by Weighted Average Common Shares

Outstanding — Diluted, as noted on the Consolidated Statements of Operations (2) Excluding tax related adjustments, the amount of income taxes was calculated based on a combined federal and state income tax rate, considering the applicable

jurisdictions of the respective segments and deductibility of specific operating adjustments

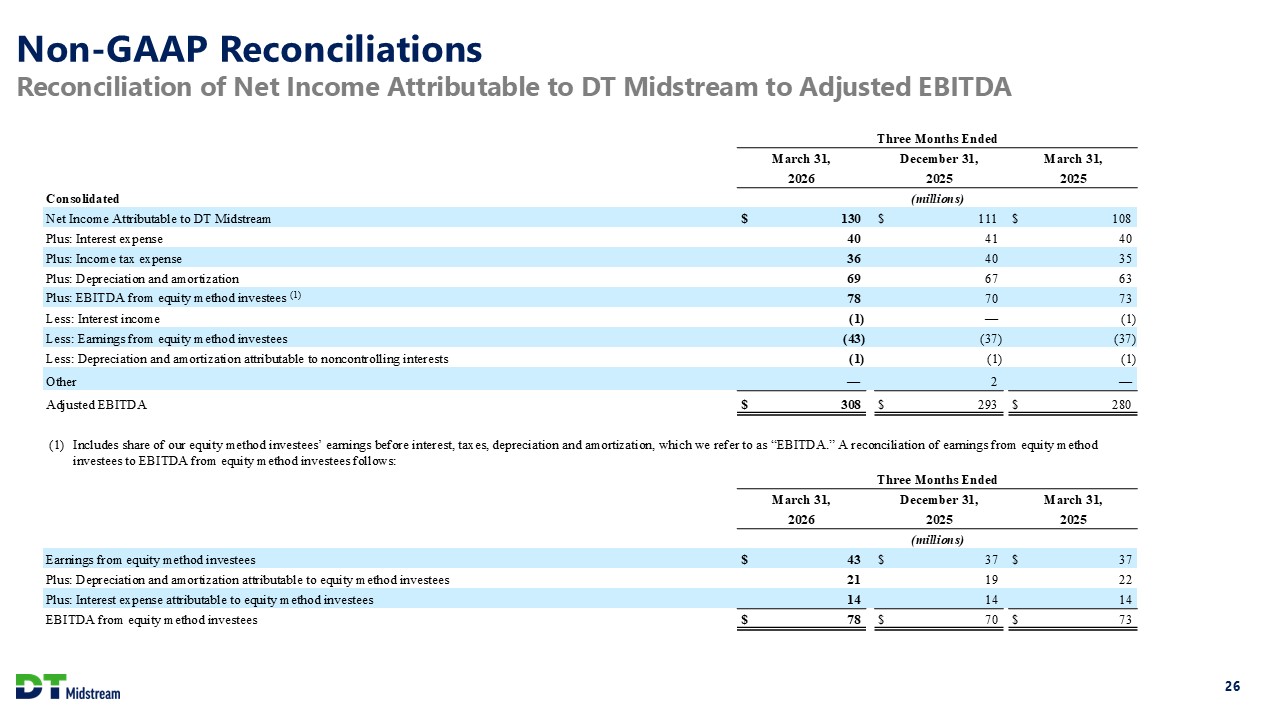

26 Reconciliation of Net Income Attributable to DT Midstream to Adjusted

EBITDA Non-GAAP Reconciliations Three Months Ended March 31, December 31, March 31, 2026 2025 2025 Consolidated (millions) Net Income Attributable to DT Midstream $ 130 $ 111 $ 108 Plus: Interest expense 40 41 40

Plus: Income tax expense 36 40 35 Plus: Depreciation and amortization 69 67 63 Plus: EBITDA from equity method investees (1) 78 70 73 Less: Interest income (1) — (1) Less: Earnings from equity method

investees (43) (37) (37) Less: Depreciation and amortization attributable to noncontrolling interests (1) (1) (1) Other — 2 — Adjusted EBITDA $ 308 $ 293 $ 280 (1) Includes share of our equity method investees’

earnings before interest, taxes, depreciation and amortization, which we refer to as “EBITDA.” A reconciliation of earnings from equity method investees to EBITDA from equity method investees follows: Three Months Ended March 31, December

31, March 31, 2026 2025 2025 (millions) Earnings from equity method investees $ 43 $ 37 $ 37 Plus: Depreciation and amortization attributable to equity method investees 21 19 22 Plus: Interest expense attributable to

equity method investees 14 14 14 EBITDA from equity method investees $ 78 $ 70 $ 73

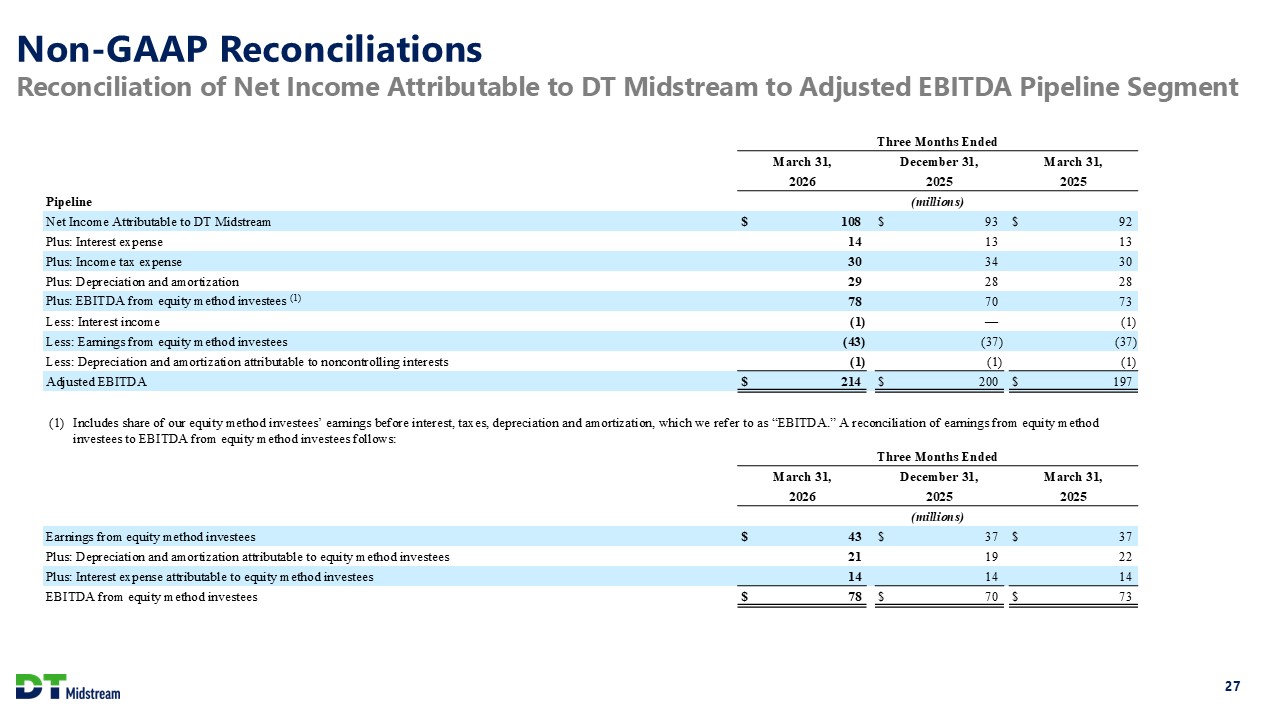

27 Reconciliation of Net Income Attributable to DT Midstream to Adjusted EBITDA

Pipeline Segment Non-GAAP Reconciliations Three Months Ended March 31, December 31, March 31, 2026 2025 2025 Pipeline (millions) Net Income Attributable to DT Midstream $ 108 $ 93 $ 92 Plus: Interest expense 14 13 13

Plus: Income tax expense 30 34 30 Plus: Depreciation and amortization 29 28 28 Plus: EBITDA from equity method investees (1) 78 70 73 Less: Interest income (1) — (1) Less: Earnings from equity method

investees (43) (37) (37) Less: Depreciation and amortization attributable to noncontrolling interests (1) (1) (1) Adjusted EBITDA $ 214 $ 200 $ 197 (1) Includes share of our equity method investees’ earnings before

interest, taxes, depreciation and amortization, which we refer to as “EBITDA.” A reconciliation of earnings from equity method investees to EBITDA from equity method investees follows: Three Months Ended March 31, December 31, March

31, 2026 2025 2025 (millions) Earnings from equity method investees $ 43 $ 37 $ 37 Plus: Depreciation and amortization attributable to equity method investees 21 19 22 Plus: Interest expense attributable to equity

method investees 14 14 14 EBITDA from equity method investees $ 78 $ 70 $ 73

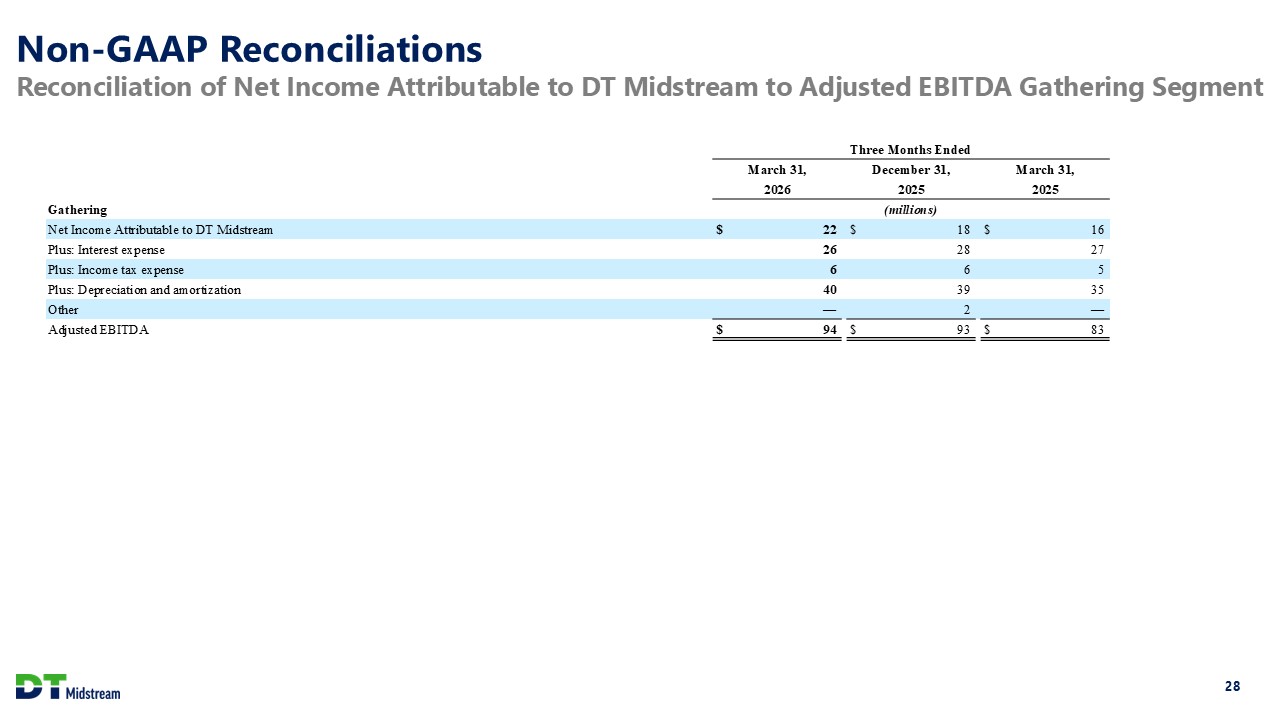

28 Reconciliation of Net Income Attributable to DT Midstream to Adjusted EBITDA

Gathering Segment Non-GAAP Reconciliations Three Months Ended March 31, December 31, March 31, 2026 2025 2025 Gathering (millions) Net Income Attributable to DT Midstream $ 22 $ 18 $ 16 Plus: Interest expense 26 28

27 Plus: Income tax expense 6 6 5 Plus: Depreciation and amortization 40 39 35 Other — 2 — Adjusted EBITDA $ 94 $ 93 $ 83

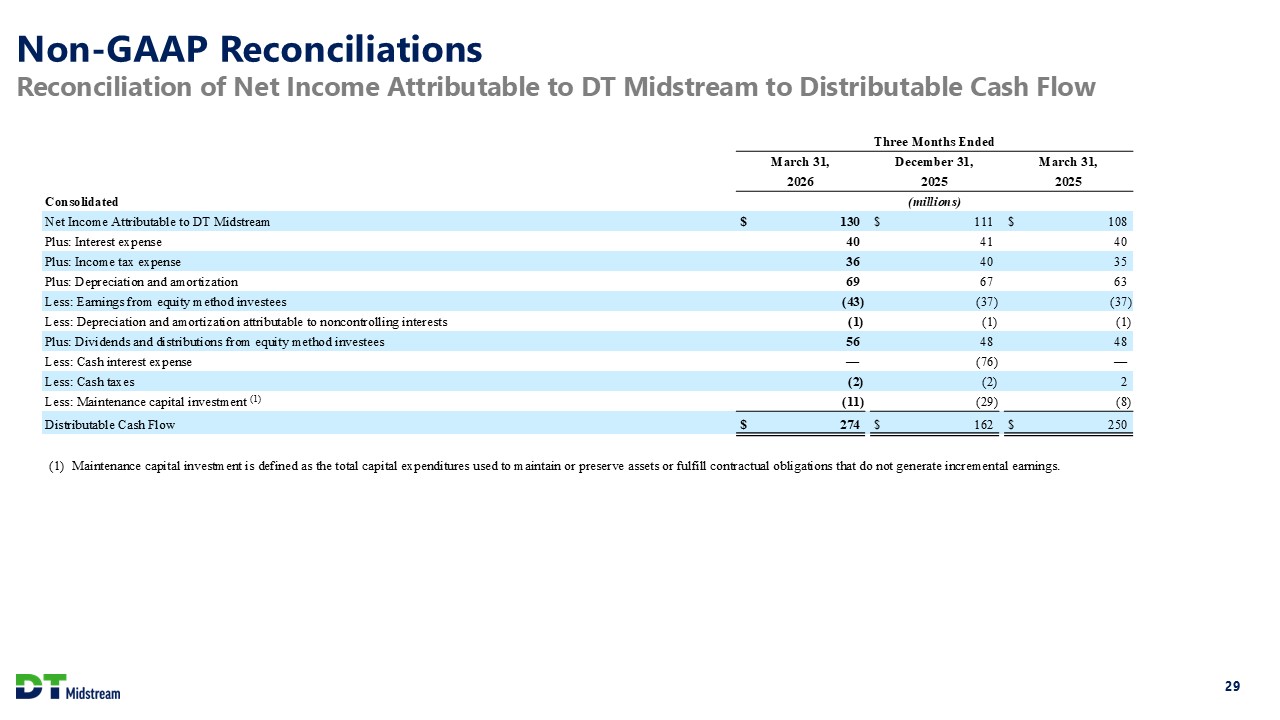

Non-GAAP Reconciliations 29 Reconciliation of Net Income Attributable to DT Midstream

to Distributable Cash Flow Three Months Ended March 31, December 31, March 31, 2026 2025 2025 Consolidated (millions) Net Income Attributable to DT Midstream $ 130 $ 111 $ 108 Plus: Interest expense 40 41 40 Plus:

Income tax expense 36 40 35 Plus: Depreciation and amortization 69 67 63 Less: Earnings from equity method investees (43) (37) (37) Less: Depreciation and amortization attributable to noncontrolling interests

(1) (1) (1) Plus: Dividends and distributions from equity method investees 56 48 48 Less: Cash interest expense — (76) — Less: Cash taxes (2) (2) 2 Less: Maintenance capital investment (1) (11) (29)

(8) Distributable Cash Flow $ 274 $ 162 $ 250 (1) Maintenance capital investment is defined as the total capital expenditures used to maintain or preserve assets or fulfill contractual obligations that do not generate incremental

earnings.