As filed with the Securities and Exchange Commission on April 29, 2026

Registration No. 333-294440

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

to

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| N/A | ||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

The People’s Republic of

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

Henry Yin, Esq. Benjamin Yao, Esq. Loeb & Loeb LLP 2206-19 Jardine House 1 Connaught Place Central, Hong Kong SAR (852) 3923-1111 |

Joan S. Guilfoyle, Esq. Loeb & Loeb LLP 901 New York Avenue, NW Suite 300 West Washington, DC 20001 (202) 618-5000 |

Approximate date of commencement of proposed sale to the public: Promptly after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities

Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting any offer to buy these securities in any jurisdiction where such offer or sale is not permitted.

| SUBJECT TO COMPLETION | PRELIMINARY PROSPECTUS DATE APRIL 29, 2026 |

Up to 221,376,995 Class A Ordinary Shares

EPWK HOLDINGS LTD.

This prospectus relates to the resale by the selling shareholders identified in this prospectus (“Selling Shareholders”) of up to 221,376,995 Class A Ordinary Shares, par value $0.004 per share (“Class A Ordinary Shares”). The Class A Ordinary Shares were issued in private placements to certain Selling Shareholders, see the section titled “Recent Sales of Unregistered Securities” on page II-1 of this prospectus.

The Selling Shareholders are identified in the table commencing on page 41. No Class A Ordinary Shares are being registered hereunder for sale by us. We will not receive any proceeds from the sale of the Class A Ordinary Shares by the Selling Shareholders. All net proceeds from the sale of the Class A Ordinary Shares covered by this prospectus will go to the Selling Shareholders (see the section titled “Use of Proceeds”). The Selling Shareholders are offering their securities to further enhance liquidity in the public trading market for our equity securities in the United States. Unlike an initial public offering, any sale by the Selling Shareholders of the Class A Ordinary Shares is not being underwritten by any investment bank. The Selling Shareholders may sell the Class A Ordinary Shares being offered by this prospectus from time to time on terms to be determined at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under “Plan of Distribution.” The Selling Shareholders will sell the Class A Ordinary Shares at a fixed price of $0.033 per share until our Class A Ordinary Shares are quoted on the OTCQB or OTCQX marketplace, or listed on a national securities exchange. Thereafter, the prices at which the Selling Shareholders may sell the shares will be determined by the prevailing market price for the shares or in negotiated transactions. See “Plan of Distribution.”

Our Class A Ordinary Shares are quoted for trading on the OTCID under the symbol “EPWKF.” On April 28, 2026, the last reported sale price of our Class A Ordinary Shares on the OTCID was $0.033 per share.

Investing in our securities involves a high degree of risk. Before making an investment decision, please read the information under the heading “Risk Factors” beginning on page 24 of this prospectus and risk factors set forth in our most recent annual report on Form 20-F (the “2025 Annual Report”), in other reports incorporated herein by reference, and in an applicable prospectus supplement.

EPWK Holdings Ltd. is a Cayman Islands holding company with no material operations of its own. We are not a Chinese operating company and only conduct our operations through our subsidiaries and contractual arrangements with the variable interest entity, EPWK VIE, in China. This is an offering of the ordinary shares of the offshore holding company in Cayman Islands. Because EPWK VIE and its subsidiaries are based in China and are engaged in value-added telecom business (a commercial internet information service provider) and radio and TV program production and business operation, due to PRC legal restrictions on foreign ownership in the industries we and the VIE operate, we do not own any equity interest in the VIE. Instead, we receive the economic benefits of the VIE’s business operation through a series of contractual agreements (the “VIE Agreements”), which have not been tested in court. Neither we nor our subsidiaries own any equity interest in EPWK VIE. As a result, you are not investing in EPWK VIE and may never hold equity interests in the Chinese operating companies. Our corporate structure may involve unique risks to investors. Our corporate structure may not be enforceable in the PRC, if PRC government authorities or courts take a view that such corporate structure contravenes PRC laws and regulations or is otherwise not enforceable for public policy reasons. In addition, the Chinese governmental authorities may take a different view than us about our corporate structure because of the promulgation of new laws or regulations, or the new interpretation of existing laws and regulations. The VIE structure provides contractual exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies and investors directly holding equity interests in the Chinese operating entities, which involves unique risks to investors. Additionally, as of the date of this prospectus, the VIE agreements have not been tested in a court of law. We and our investors do not have an equity ownership in, direct foreign investment in, or control through such ownership/investment of the VIE. Therefore, the VIE agreements do not give us the same controlling power as if we had equity ownership in the VIE. On August 11, 2022, EPWK WFOE, which is our PRC subsidiary, EPWK VIE, and shareholders of EPWK VIE entered into a series of contractual agreements that established the VIE structure. We have evaluated the guidance in FASB ASC 810 and determined that EPWK WFOE is the primary beneficiary of EPWK VIE and its subsidiaries, for accounting purposes only, because, pursuant to the VIE Agreements, the VIE shall pay service fees equal to all of its net income to EPWK WFOE, while EPWK WFOE has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance and is obligated to absorb all of losses of the VIE. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of EPWK WFOE and, ultimately, EPWK Holdings Ltd, which has indirect ownership in 100% of the equity in EPWK WFOE. Accordingly, under U.S. GAAP and for accounting purpose only, we treat the VIE and its subsidiaries as consolidated affiliated entities and have consolidated their financial results in our financial statements. For a detailed description of the VIE Agreements, see “Our History and Corporate Structure” on page 29.

Because we do not hold equity interests in EPWK VIE, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard that could disallow the VIE structure, which would likely prevent us from offering or continue offering securities to investors and result in a material change in our operations, and the value of our Class A Ordinary Shares may depreciate significantly or become worthless.

However, EPWK Holdings Limited, one of our wholly-owned subsidiaries incorporated in Hong Kong, does not engage in any active operations and acts solely as a holding entity. Therefore, we do not believe that the Hong Kong holding company will be subject to similar legal or operational risks that may result in material changes in our operations and/or the value of the securities we are registering for sale or our ability to offer or continually offer securities to investors.

The VIE Agreements may not be effective in providing control over EPWK VIE. We may also be subject to sanctions imposed by PRC regulatory agencies including the Chinese Securities Regulatory Commission (“CSRC”), if we fail to comply with their rules and regulations. See “Item 3. Key Information—D. Risk Factors” in the 2025 Annual Report for more information.

We currently do not have any cash management policies that dictate the purpose, amount, and procedure of funds transfers among our Cayman Islands holding company, our subsidiaries, and the consolidated VIEs. Rather, the funds can be transferred in accordance with the applicable laws and regulations. We may require additional capital resources in the future, and we may seek to issue additional equity or debt securities or obtain new or expanded credit facilities, which could subject us to operating and financing covenants, including requirements to maintain a certain amount of cash reserves. See “Prospectus Summary – Dividend Distributions or Assets Transfer among the Holding Company, its Subsidiaries and the Consolidated VIE.”

There have been no transfers of cash or other assets, dividends, or distribution made to EPWK and among its subsidiaries and the VIE and its subsidiaries, and they have no plans to make any transfers of cash or other assets, distribution, or dividend payment to EPWK and among themselves in the near future. Neither EPWK nor any of its subsidiaries nor the VIE and its subsidiaries have made any transfer of cash or other assets, dividends. or distributions to investors as of the date of this prospectus. We, our subsidiaries, and the VIE have no present plans to distribute earnings or settle amounts owed under the VIE agreements and plan to retain EPWK’s retained earnings to continue to grow EPWK’s business. For more information, please refer to “Selected Condensed Consolidating Financial Statements of Parent, Subsidiaries, VIE and its Subsidiaries” and the consolidated financial statements starting from page 21. Our board of directors has complete discretion on whether to distribute dividends, subject to applicable laws. We do not have any current plan to declare or pay any cash dividends on our Class A Ordinary Shares in the foreseeable future after this offering. We are permitted under the laws of Cayman Islands to provide funding to our subsidiaries in Hong Kong and PRC through loans or capital contributions without restrictions on the amount of the funds, provided that in no circumstances may a dividend be paid if this would result in the company being unable to pay its debts due in the ordinary course of business. Our subsidiary in Hong Kong is also permitted under the laws of Hong Kong SAR to provide funds to us through dividend distribution out of profits available for distribution or other distributable reserves. However, we, our subsidiaries and the VIE’s abilities to use cash held in PRC or in a PRC entity through transfers, distributions, or dividends to fund operations or for other purposes outside of the PRC are subject to restrictions and limitations imposed by the PRC government. Current PRC regulations only permit EPWK WFOE, Yipinweike (Guangzhou) Network Technology Co., Ltd. to pay dividends to the Company out of its accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. The majority of our and the consolidated VIE’s revenues are collected in Renminbi; thus, foreign exchange shortages and foreign exchange control may limit our ability to pay dividends or other payments or otherwise meet our obligations denominated in foreign currencies. Furthermore, we may lose our ability to fund operations or for other uses outside of Hong Kong using cash in Hong Kong or a Hong Kong entity if, in the future, the PRC government expands its restrictions and limitations to include Hong Kong or Hong Kong entities. Therefore, our ability to transfer cash between EPWK VIE and us, our subsidiaries outside of China, and investors may be restricted. See “Prospectus Summary – Dividend Distributions or Assets Transfer among the Holding Company, its Subsidiaries and the Consolidated VIE,” “Summary of Risk Factors – We may not be able to use funds held in the PRC or Hong Kong or a PRC or Hong Kong entity to fund operations or for other purposes outside of the PRC due to the interventions or imposition of restrictions and limitations on the ability of us, our subsidiaries, or the consolidated VIE by the PRC government to transfer cash.” and “Item 3. Key Information—D. Risk Factors —Risk Relating to Doing Business in the PRC – Our ability to transfer cash between subsidiaries, the consolidated VIE, and investors outside PRC or Hong Kong may be significantly restricted by the Chinese government” in the 2025 Annual Report.

We are subject to certain legal and operational risks associated with our PRC subsidiaries and the VIE’s operations in China. PRC laws and regulations governing our current business operations are sometimes vague and uncertain, and therefore, these risks may result in a material change in the VIE’s operations, significant depreciation of the value of our Class A Ordinary Shares, or a complete hindrance of our ability to offer or continue to offer our securities to investors. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. In the opinion of our PRC counsel, Beijing Dacheng Law Offices, LLP (Fuzhou) (“Dacheng”), as of the date of this prospectus, we are not directly subject to these regulatory actions or statements, as we have not implemented any monopolistic behavior.

On February 17, 2023, the China Securities Regulatory Commission, or the CSRC, announced the Circular on the Administrative Arrangements for Filing of Securities Offering and Listing By Domestic Companies, or the Circular, and released a set of new regulations which consists of the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, and five supporting guidelines which came into effect on March 31, 2023. The Trial Measures refine the regulatory system by subjecting both direct and indirect overseas offering and listing activities to the CSRC filing-based administration. Requirements for filing entities, time points and procedures are specified. The Trial Measures apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the PRC and valued on the basis of interests in PRC domestic companies, or indirect offerings. Where a PRC domestic company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, file with the CSRC. The Trial Measures also lay out requirements for the reporting of material events. Breaches of the Trial Measures, such as offering and listing securities overseas without fulfilling the filing procedures, shall bear legal liabilities, including a fine between RMB1.0 million (approximately $150,000) and RMB10.0 million (approximately $1.5 million), and the Trial Measures heighten the cost for offenders by enforcing accountability with administrative penalties and incorporating the compliance status of relevant market participants into the Securities Market Integrity Archives. Pursuant to the provisions of the Trial Measures, overseas securities offering and listing refers to the offering and listing activities on overseas stock exchanges, and the listing of domestic companies on overseas over-the-counter, or OTC, markets is not within the scope of the filing-based administration. Accordingly, we are not required to complete the filing procedures pursuant to the Trial Measures in respect of this offering.

On February 24, 2023, the CSRC, Ministry of Finance of the PRC, National Administration of State Secrets Protection and National Archives Administration of China jointly revised the Provisions on Strengthening Confidentiality and Archives Administration in Overseas Issuance and Listing of Securities (the “Confidentiality and Archives Administration Provisions”), which came into effect on March 31, 2023. The Confidentiality and Archives Administration Provisions require that, overseas listed PRC domestic enterprises, as well as those to be listed, shall establish the confidentiality and archives system, and shall complete approval and filing procedures with competent authorities, if such PRC domestic enterprises or their overseas listing entities provide or publicly disclose documents or materials involving state secrets and work secrets of PRC government agencies to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals.

Our PRC counsel has opined that, as of the date of this prospectus, no effective laws or regulations in the PRC explicitly require us to seek approval from the CSRC or any other PRC governmental authorities for our overseas listing plan, nor has our Company or any of our subsidiaries received any inquiry, notice, warning or sanctions regarding our planned overseas listing from the CSRC or any other PRC governmental authorities. However, since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on an U.S. national stock exchange. Any change in the PRC laws and regulations could result in a material change in our and the VIE’s operations or the value of our Class A Ordinary Shares or significantly limit or completely hinder our ability to offer or continue to offer our Class A Ordinary Shares to investors and cause the value of our Class A Ordinary Shares to significantly decline or become worthless. Although our PRC subsidiaries and the VIE’s operations in the PRC are subject to certain legal and operational risks, EPWK HK is not currently engaging in any active business activities and merely acting as a holding company. As a result, we do not believe any securities, data security, or anti-monopoly laws or regulations in Hong Kong may impact our operations or the offering of our securities to foreign investors, nor do we foresee any material legal and operational risks associated with EPWK HK except those already disclosed in this prospectus.

We are an “emerging growth company” as defined under the federal securities laws and will be subject to reduced public company reporting requirements. Please read the disclosures beginning on page 19 of this prospectus for more information.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated April 29, 2026

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or any prospectus supplement or amendment. Neither we, nor the placement agent, have authorized any other person to provide you with information that is different from, or adds to, that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we nor the placement agent take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. You should assume that the information contained in this prospectus or any free writing prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our securities. Our business, financial condition, results of operations and prospects may have changed since that date. We are not making an offer of any securities in any jurisdiction in which such offer is unlawful.

No action is being taken in any jurisdiction outside the United States to permit a public offering of our securities or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this public offering and the distribution of this prospectus applicable to that jurisdiction.

i

About this Prospectus

This prospectus describes the general manner in which the Selling Shareholders identified in this prospectus may offer from time to time up to 221,376,995 Class A Ordinary Shares. If necessary, the specific manner in which the Class A Ordinary Shares may be offered and sold will be described in a supplement to this prospectus, which supplement may also add, update or change any of the information contained in this prospectus. To the extent there is a conflict between the information contained in this prospectus and the prospectus supplement, you should rely on the information in the prospectus supplement, provided that if any statement in one of these documents is inconsistent with a statement in another document having a later date-for example, any prospectus supplement-the statement in the document having the later date modifies or supersedes the earlier statement.

Conventions that Apply to this Prospectus

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “We”, “us” or the “Company” in this prospectus are to EPWK Holdings Ltd., and its affiliated entities; |

| ● | “Affiliated entities” are to our subsidiaries and variable interest entity (“VIE”); |

| ● | “Buyer” is either a user who hires sellers from our platform or an offline customer who uses our other services; |

| ● | “China” or the “PRC” are to the People’s Republic of China, excluding Taiwan but including special administrative regions of Hong Kong and Macau for the purposes of this prospectus only; |

| ● | “Class A Ordinary Shares” are to the Class A ordinary shares of EPWK Holdings Ltd., par value $0.004 per share; |

| ● | “Daily Inquiries” are inquiries made by users each day regarding the services and products offered on our platform. |

| ● | “EPWK HK” are to the Company’s wholly owned subsidiary, EPWK Holdings Limited, a Hong Kong corporation; |

| ● | “EPWK VIE” are to Xiamen EPWK Network Technology Co., Ltd., a limited liability company organized under the laws of the PRC, that we control via a series of contractual arrangements between EPWK WFOE and EPWK VIE; |

| ● | “EPWK WFOE” or “WFOE” are to Yipinweike (Guangzhou) Network Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by us through EPWK HK; | |

| ● | “F&S” or “Frost & Sullivan” are to Frost & Sullivan Inc.; |

| ● | “Gross Merchandise Volume (GMV)” refers to the total volume of transactions we make over a specified period of time through our platform, which includes any fees or other deductions we may calculate separately; GMV is not our revenue and is not included in the statement of operations; unless indicated otherwise, the “GMV” in this prospectus refers to the total volume of transactions we make over one calendar year; | |

| ● | “Mini Programs” refer to various sub-applications incorporated into popular mobile applications in China like WeChat and Alipay that do not require separate installations and are ready to use at any time; | |

| ● | “our memorandum and articles of association” are to our third amended and restated memorandum and articles of association; | |

| ● | “Paid Members” are users who have subscribed to our self-operated services and tools, including design, software development, marketing, business writing, interior decoration, life service, intellectual properties registration and management services; | |

| ● | “Proprietary Data” is the data we created after analyzing the nature and type of the seller-posted services or products; | |

| ● | “Seller” is to a user who provides service to buyers on our platform; | |

| ● | “Trading Volume” includes all types of tasks and transactions posted on or completed through the platform; and | |

| ● | “Users” or “registered users” include buyers and sellers whose registered accounts have been verified by phone numbers, government identification documents, email accounts, or bank accounts, buyers and sellers who registered their accounts through third-party applications, including WeChat, Weibo or Tencent QQ, and buyers and sellers who registered their accounts without going through the verification process. Unverified users can only browse our platform and cannot use any of our services. |

Our business is conducted through EPWK WFOE and EPWK VIE in the PRC, using RMB, the currency of China. Our consolidated financial statements are presented in United States dollars. In this prospectus, we refer to assets, obligations, commitments and liabilities in our consolidated financial statements in United States dollars. These dollar references are based on the exchange rate of RMB to United States dollars, determined as of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of United States dollars which may result in an increase or decrease in the amount of our obligations (expressed in dollars) and the value of our assets.

ii

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our securities. Before you decide to invest in our securities, you should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements and related notes appearing at the end of this prospectus.

Business Overview

EPWK Holdings Ltd. was incorporated in the Cayman Islands as an exempted company in March 2022 as a holding company with no material operations of our own, we conduct our operations in China through EPWK VIE and its subsidiaries. Our platform, operated through EPWK VIE, is one of the only two comprehensive crowdsourcing platforms in China, with the other one operated by Zhubajie, and enables businesses (buyers) and service providers (sellers) to find each other. From January 2019 to June 30, 2025, our platform enabled approximately US$2.03 billion (RMB14.015 billion) of GMV across 564 million projects. As of June 30, 2025, our accumulated registered buyers were 9.04 million and accumulated registered sellers were 17.51 million covering all 34 provinces of China. Specifically, in 2024, we enabled approximately US$350 million of GMV across 0.994 million projects.

In 2023, we enabled approximately US$349 million of GMV across 0.986 million projects. Our accumulated registered buyers as of June 30, 2025, 2024 and 2023 were 9.04 million, 8.91 million and 8.59 million, respectively. Our accumulated registered sellers as of June 30, 2025, 2024 and 2023 were 17.51 million, 17.22 million and 16.68 million, respectively. In 2025, we enabled approximately $350 million of GMV across 994,100 projects and accumulated 8.91 million registered buyers and 17.51 million registered sellers.

For the years ended June 30, 2025, 2024 and 2023, our revenue was $27.84 million, $20.22 million and $19.8 million, respectively. For the same period, our net loss was $10.44 million, $1.20 million and $1.08 million, respectively.

Our marketplace platform was launched in 2011. We have achieved significant growth ever since our inception. Our platform users consist of buyers who seek talents for their jobs and sellers who offer different talents and skills. As of June 30, 2025, we had over 26.55 million registered users. We offer an expansive catalog to provide diversified services to businesses of all sizes. Our daily inquiries well exceed 10,000 from logo design to business name selection to software development.

Corporate History and Structure

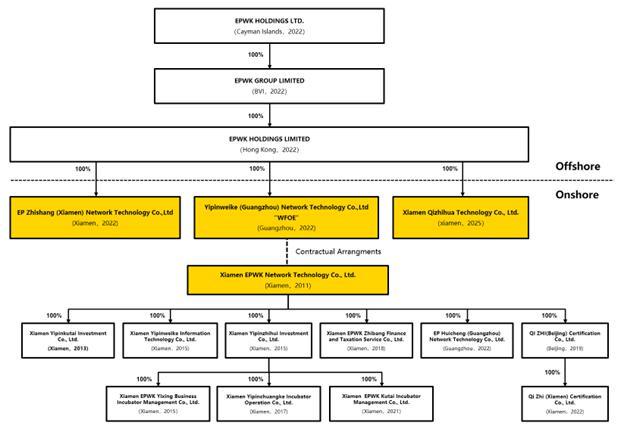

We were incorporated in the Cayman Islands on March 24, 2022. Our wholly-owned subsidiary, EPWK Group Limited (“EPWK BVI”), was incorporated in the British Virgin Islands on April 4, 2022. EPWK BVI wholly owns EPWK Holdings Limited (“EPWK HK”), a company incorporated in Hong Kong on April 28, 2022. Yipinweike (Guangzhou) Network Technology Co., Ltd. (“EPWK WFOE”), EPWK HK’s wholly owned subsidiary, was organized pursuant to PRC laws on July 26, 2022. Our variable interest entity, Xiamen EPWK Network Technology Co., Ltd., which we refer to as EPWK VIE, was established on March 25, 2011 in Xiamen, Fujian Province, PRC pursuant to PRC laws. EPWK VIE’s shareholders include certain PRC residents and corporate entities controlled by PRC residents. On August 11, 2022, the Company consummated a reorganization pursuant to which, EPWK WFOE, EPWK VIE and EPWK VIE’s shareholders entered into a series of contractual arrangements. Such agreements are described under “Business - Contractual Arrangements between EPWK WFOE and EPWK VIE. EPWK Holdings Ltd. is a holding company with no business operation other than holding the shares in EPWK HK and EPWK HK is a pass-through entity with no business operation. EPWK WFOE is exclusively engaged in the business of managing the operation of EPWK VIE.

On June 1, 2022, EPWK VIE established a wholly-owned subsidiary, Yipinhuicheng (Guangzhou) Network Technology Co., Ltd., a PRC company. Yipinhuicheng (Guangzhou) Network Technology Co., Ltd. is engaged in software development worldwide; network and information security software development; information technology consulting services.

1

On February 6, 2025, our Class A Ordinary Shares commenced trading on the Nasdaq Global Market under the ticker symbol “EPWK.”

On September 15, 2025, our shareholders approved (1) the increase of votes per Class B ordinary share of the Company from 15 to 100 with effect from the date of the special resolution be approved, (2) the increase of the Company’s authorised share capital, be increased from US$50,000 divided into: (i) 448,814,684 Class A Ordinary Shares of par value of US$0.0001 each, and (ii) 51,185,316 Class B Ordinary Shares of par value of US$0.0001 each, to US$1,000,000 divided into (i) 9,000,000,000 Class A Ordinary Shares of US$0.0001 par value each and (ii) 1,000,000,000 Class B Ordinary Shares of US$0.0001 par value each with immediate effect (the “Authorised Share Capital Increase”); conditional upon the approval of the board of directors of the Company (the “Board”) in its sole discretion, with effect as of the date within one (1) calendar year after the conclusion of the EGM as the Board may determine (the “Effective Date”): (i) the authorised, issued, and outstanding shares of the Company (collectively, the Shares) be consolidated by consolidating each 100 Shares of the Company, or such lesser whole share amount as the Board of Directors may determine in its sole discretion, such amount not to be less than 2, into 1 Share of the Company, with such consolidated Shares having the same rights and being subject to the same restrictions (save as to par value) as the existing Shares of such class as set out in the Company’s memorandum and articles of association (the “Share Consolidation”). The Company’s board of directors approved on October 20, 2025 that the authorised, issued, and outstanding shares of the Company be consolidated on a 40 for 1 ratio with the marketplace effective date of November 17, 2025. At the time the share consolidation is effective, the Company’s authorised share capital will be changed from US$1,000,000 divided into (i) 9,000,000,000 Class A Ordinary Shares of US$0.0001 par value each and (ii) 1,000,000,000 Class B Ordinary Shares of US$0.0001 par value each, to US$1,000,000 divided into 225,000,000 Class A Ordinary Shares with a par value of US$0.004 each and 25,000,000 Class B Ordinary Shares with a par value of US$0.004 each. The Company’s total issued and outstanding Class A ordinary shares will be changed from 144,506,412 Class A Ordinary Shares with a par value of US$0.0001 per share to approximately 3,612,660 Class A Ordinary Shares with a par value of US$0.004 per share. The Company’s total issued and outstanding Class B ordinary shares will be changed from 3,555,948 Class B Ordinary Shares with a par value of US$0.0001 per share to approximately 88,899 Class B Ordinary Shares with a par value of US$0.004 per share.

We received delisting notice from Nasdaq on October 24, 2025 and requested a hearing. On November 20, 2025, we received an additional delisting notice from Nasdaq. On December 19, 2025, Nasdaq notified us that the Nasdaq Hearings Panel has determined to deny our request to continue listing of our Class A ordinary shares. On December 23, 2025, we were delisted from Nasdaq when the staff of the Nasdaq Stock Market LLC filed a Form 25 Notification of Delisting. Our Class A ordinary shares have been quoted on the OTCID Basic Market under the symbol “EPWKF” since Nasdaq suspended the trading of our Class A ordinary shares on December 23, 2025.

Pursuant to PRC laws, each entity formed under PRC law shall have certain business scope approved by the Administration of Industry and Commerce or its local counterpart. As such, EPWK WFOE’s business scope is to primarily engage in business development, technology service, technology consulting, intellectual property service and business management consulting. Since the sole business of EPWK WFOE is to provide EPWK VIE with technical support, consulting services and other management services relating to its day-to-day business operations and management in exchange for a consulting fee solely at EPWK WFOE’s discretion and can be the net income of EPWK VIE, such business scope is necessary and appropriate under the PRC laws. EPWK VIE, on the other hand, has been granted a business scope different from EPWK WFOE to enable it to provide software development and IT services, animation and game development, advertising production, tax and financial advisory services, corporate management services, and certain value-added telecommunication services.

We control EPWK VIE through contractual agreements, which are described under “Business - Contractual Arrangements between EPWK WFOE and EPWK VIE. EPWK Holdings Ltd. is a holding company with no business operation other than holding the shares in EPWK HK and EPWK HK is a pass-through entity with no business operation. EPWK WFOE is exclusively engaged in the business of managing the operation of EPWK VIE.

The following diagram illustrates our corporate structure as of the date of this prospectus. All percentages in the following diagram reflect the voting ownership interests instead of the equity interests held by each of our shareholders given that each holder of Class B Ordinary Shares will be entitled to 100 votes per one Class B Ordinary Share and each holder of Class A Ordinary Shares will be entitled to one vote per one Class A Ordinary Share.

2

The VIE Structure

The VIE entity, EPWK VIE, is Xiamen EPWK Network Technology Co., Ltd. This is an offering of the ordinary shares of the offshore holding company in Cayman Islands. Neither we nor our subsidiaries own any equity interest in EPWK VIE. As a result, you are not investing in EPWK VIE and may never hold equity interests in the Chinese operating companies. The VIE arrangements have not been tested in a court of law.

EPWK VIE generated revenues of $27.84 million, $20.22 million and $19.80 million for the years ended June 30, 2025 2024 and 2023, respectively.

Because EPWK VIE and its subsidiaries are based in China and are engaged in value-added telecom business and radio and TV program production and business operation, due to PRC legal restrictions on foreign ownership in the industries we and the VIE operate, we do not own any equity interest in the VIE. Instead, we receive the economic benefits of the VIE’s business operation through a series of contractual agreements (the “VIE Agreements”), which have not been tested in court. We have evaluated the guidance in FASB ASC 810 and determined that EPWK WFOE is the primary beneficiary of EPWK VIE and its subsidiaries, for accounting purposes only, because, pursuant to the VIE Agreements, the VIE shall pay service fees equal to all of its net income to EPWK WFOE, while EPWK WFOE has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance and is obligated to absorb all of losses of the VIE. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of EPWK WFOE and, ultimately, EPWK Holdings Ltd., which has indirect ownership in 100% of the equity in EPWK WFOE. Accordingly, under U.S. GAAP and for accounting purpose only, we treat the VIE and its subsidiaries as consolidated affiliated entities and have consolidated their financial results in our financial statements. Since we do not hold equity interests in EPWK VIE, we are subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to regulations on foreign ownership of internet technology companies, regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements. Our corporate structure may involve unique risks to investors. Our corporate structure may not be enforceable in the PRC, if PRC government authorities or courts take a view that such corporate structure contravenes PRC laws and regulations or is otherwise not enforceable for public policy reasons. We are also subject to the risks of uncertainty about any future actions of the PRC government in this regard that could disallow the VIE structure, which would likely prevent us from offering or continue offering securities to investors or result in a material change in our operations, and the value of our Class A Ordinary Shares may depreciate significantly or become worthless.

3

The VIE Agreements include:

| ● | Exclusive Business Cooperation Agreement, |

| ● | Call Option Agreements, |

| ● | Equity Pledge Agreements, |

| ● | Shareholders Powers of Attorney, and |

| ● | Irrevocable Commitment Letter. |

They are designed to provide our wholly-foreign owned entity, Yipinweike (Guangzhou) Network Technology Co., Ltd., with the power, rights, and obligations equivalent in all material respects to those it would possess as the principal equity holder of EPWK VIE. Under the VIE Agreements, EPWK WFOE is entitled to collect a service fee that is equal to 100% of the net income of the EPWK VIE, and EPWK WFOE has the power to direct the activities of the EPWK VIE that can significantly impact the EPWK VIE’s economic performance and is obligated to absorb losses of the EPWK VIE, which makes us, through our direct ownership of 100% of the equity in EPWK WFOE, the primary beneficiary to receive the economic benefits of the EPWK VIE’s business operation for accounting purposes only. Because our economic interest in the EPWK VIE is more than insignificant exposure to potential losses of or benefits from it, and we have power over the most significant economic activities of the EPWK VIE, we have consolidated the financial results of the EPWK VIE in our consolidated financial statements under generally accepted accounting principles in the U.S. (“U.S. GAAP”) for accounting purpose only. However, the economic interest in and the power over the EPWK VIE are based on contractual agreements and are not equivalent to equity ownership in the business of the EPWK VIE, and the structure involves unique risks to investors. See “Item 4. Information on the Company-A. History and Development of the Company” for a summary of these VIE Agreements in the 2025 Annual Report.

The VIE Agreements may not be effective in providing control over EPWK VIE as we are subject to certain legal and operational risks associated with EPWK VIE’s operations in China. PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on an U.S. exchange. We may also be subject to sanctions imposed by PRC regulatory agencies including the CSRC if we fail to comply with their rules and regulations.

4

We cannot assure you that the PRC courts or regulatory authorities may not determine that our corporate structure and the VIE Agreements violate PRC laws, rules or regulations. If the PRC courts or regulatory authorities determine that our contractual arrangements are in violation of applicable PRC laws, rules or regulations, the VIE Agreements will become invalid or unenforceable, and EPWK VIE will not be treated as a VIE, and we will not be entitled to treat EPWK VIE’s assets, liabilities and results of operations as our assets, liabilities and results of operations, which could effectively eliminate the assets, revenue and net income of EPWK VIE from our balance sheet, which would most likely require us to cease conducting our business and would result in the delisting of our Class A Ordinary Shares from Nasdaq Global Market and a significant impairment in the market value of our Class A Ordinary Shares. If the VIE structure is determined to be in violation of any existing or future PRC laws, rules or regulations, or if EPWK WFOE or the VIE fails to obtain or maintain any of the required governmental permits or approvals, the relevant PRC regulatory authorities would have broad discretion in dealing with such violations, including: imposing fines on the EPWK WFOE or the VIE, revoking the business and operating licenses of EPWK WFOE or the VIE, discontinuing or restricting the operations of EPWK WFOE or the VIE; imposing conditions or requirements with which we, EPWK WFOE, or the VIE may not be able to comply; requiring us, EPWK WFOE, or the VIE to restructure the relevant ownership structure or operations which may significantly impair the rights of the holders of our Class A Ordinary Shares in the equity of the VIE; and restricting or prohibiting our use of the proceeds from our public offering to finance our business and operations in China. See “Risk Factors - Risk Relating to Our Corporate Structure - PRC laws and regulations governing our current business operations are sometimes vague and uncertain and any changes in such laws and regulations may impair our ability to operate profitable”, and “Risk Factors - Risk Relating to Doing Business in the PRC - The Chinese government exerts substantial influence over the manner in which we must conduct our business and may intervene or influence our operations at any time, which actions could impact our operations materially and adversely, and significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our Class A Ordinary Shares to significantly decline or be worthless.” for more information. See “Risk Factors - Risks Relating to Our Corporate Structure”, “Risk Factors - Risks Relating to Doing Business in the PRC” for more information.

Contractual Arrangements between EPWK WFOE and EPWK VIE

Due to PRC legal restrictions on foreign ownership in industries we and the VIE operate, neither we nor our subsidiaries own any equity interest in EPWK VIE. This is an offering of the Class A Ordinary Shares of the offshore holding company in Cayman Islands. You are not investing in EPWK VIE.

EPWK WFOE, EPWK VIE and its shareholders entered into a series of contractual arrangements, also known as VIE Agreements, on August 11, 2022. Under the VIE Agreements, EPWK WFOE is entitled to collect a service fee that is equal to 100% of the net income of the EPWK VIE, and EPWK WFOE has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance and is obligated to absorb losses of the VIE, which makes us, through our direct ownership of 100% of the equity in EPWK WFOE, the primary beneficiary to receive the economic benefits of the VIE’s business operation for accounting purposes. Because our economic interest in the VIE is more than insignificant exposure to potential losses of or benefits from it, and we have power over the most significant economic activities of the VIE, we have consolidated the financial results of the VIE in our consolidated financial statements under generally accepted accounting principles in the U.S. (“U.S. GAAP”). The VIE structure has its inherent risks that may affect your investment, including less effectiveness and certainties than direct ownership and potential substantial costs to enforce the terms of the VIE Agreements. We, as a Cayman Islands holding company, may incur significant difficulties and costs in enforcing any rights we may have under the VIE Agreements with the VIE, its founders and owners, in PRC because all of the VIE Agreements are governed by the PRC laws and provide for the resolution of disputes through arbitration in the PRC, where legal environment in the PRC is not as developed as in the United States. Furthermore, these VIE Agreements may not be enforceable in China if PRC government authorities or courts take a view that such VIE Agreements contravene PRC laws and regulations or are otherwise not enforceable for public policy reasons. In the event we are unable to enforce these VIE Agreements, we may not be able to exert effective control over EPWK VIE, and our ability to conduct our business may be materially and adversely affected.

Each of the VIE Agreements is described in detail below.

5

Exclusive Business Cooperation Agreement

Pursuant to the exclusive business cooperation agreement between EPWK WFOE and EPWK VIE, EPWK WFOE has the exclusive right to provide EPWK VIE with technical support services, consulting services and other services, including technical support, technical assistance, technical consulting, and professional training necessary for EPWK VIE’s operation, network support, database support, software services, business management consulting, grant use rights of intellectual property rights, lease hardware and device, provide system integration service, research and development of software and system maintenance, provide labor support and to develop the related technologies based on EPWK VIE’s needs. In exchange, EPWK WFOE is entitled to a service fee that equates to all of the consolidated net income after offsetting previous year’s loss (if any) of EPWK VIE. The service fees may be adjusted based on the actual scope of services rendered by EPWK WFOE and the operational needs of EPWK VIE.

Pursuant to the exclusive business cooperation agreement, EPWK WFOE has the unilateral right to adjust the service fee at any time, and EPWK VIE has no right to adjust the service fee. We believe that such conditions under which the service fee may be adjusted will be primarily based on the needs of EPWK VIE to operate and develop its business in the AR market. For example, if EPWK VIE needs to expand its business, increase research investment or consummate mergers or acquisitions in the future, EPWK WFOE has the right to decrease the amount of the service fee, which would allow EPWK VIE to have additional capital to operate and develop its business.

The exclusive business cooperation agreement remains in effect for 10 years until August 10, 2032 and shall be automatically renewed for one year at the expiration date of the validity term. However, EPWK WFOE shall have the right to terminate this agreement upon giving 30 days’ prior written notice to EPWK VIE at any time.

Call Option Agreements

Pursuant to the call option agreements, among EPWK WFOE, EPWK VIE and the shareholders who collectively owned all of EPWK VIE, such shareholders jointly and severally grant EPWK WFOE an option to purchase their equity interests in EPWK VIE. The purchase price shall be the lowest price then permitted under applicable PRC laws. EPWK WFOE or its designated person may exercise such option at any time to purchase all or part of the equity interests in EPWK VIE until it has acquired all equity interests of EPWK VIE, which is irrevocable during the term of the agreements.

The call option agreements remain in effect for 10 years until August 10, 2032 and shall be automatically renewed for one year at the expiration date of the validity term. However, EPWK WFOE shall have the right to terminate these agreements upon giving 30 days’ prior written notice to EPWK VIE at any time.

Equity Pledge Agreements

Pursuant to the equity pledge agreements, among the shareholders who collectively owned all of EPWK VIE, such shareholders pledge all of the equity interests in EPWK VIE to EPWK WFOE as collateral to secure the obligations of EPWK VIE under the exclusive business cooperation agreement and call option agreements. These shareholders are prohibited or may not transfer the pledged equity interests without prior consent of EPWK WFOE unless transferring the equity interests to EPWK WFOE or its designated person in accordance with the call option agreements.

The equity pledge agreement will take effect from the date of signing, that is, on August 11, 2022, and three days after the agreement is signed, the share pledge will be recorded under the EPWK VIE shareholder register.

The equity pledge agreements remain in effect for 10 years until August 10, 2032 and shall be automatically renewed for one year at the expiration date of the validity term. However, EPWK WFOE shall have the right to terminate these agreements upon giving 30 days’ prior written notice to EPWK VIE at any time.

Shareholders Powers of Attorney (“POAs”)

Pursuant to the shareholders powers of attorney, the shareholders of EPWK VIE give EPWK WFOE an irrevocable proxy to act on their behalf on all matters pertaining to EPWK VIE and to exercise all of their rights as shareholders of EPWK VIE, including the right to attend shareholders meetings, to exercise voting rights and all of the other rights, and to sign transfer documents and any other documents in relation to the fulfillment of the obligations under the call option agreements and the equity pledge agreements.

6

The shareholders powers of attorney remain in effect for 10 years until August 10, 2032 and shall be automatically renewed for one year at the expiration date of the validity term. However, shareholders of EPWK VIE shall have the right to terminate these agreements upon giving 30 days’ prior written notice to EPWK WFOE at any time.

Irrevocable Commitment Letter

Pursuant to the irrevocable commitment letter, the individual shareholders of EPWK VIE commit that their spouses or inheritors have no right to claim any rights or interest in relation to the shares that they hold in EPWK VIE and have no right to impose any impact on the daily managing duties of EPWK VIE, and commit that if any event which refrains them from exercising shareholders’ rights as a registered shareholder, such as death, incapacity, divorce or any other event, could happen to them, the shareholders of EPWK VIE will take corresponding measures to guarantee the rights of other registered shareholders and the performance of the Contractual Arrangements. The letter is irrevocable and shall not be withdrawn without the consent of EPWK WFOE. The spouses of EPWK VIE individual shareholders also undertake that they have no right to claim any rights or interest in relation to the shares that they hold in EPWK VIE and have no right to impose any impact on the daily managing duties of EPWK VIE.

Based on the foregoing contractual arrangements, which grant EPWK WFOE effective control of EPWK VIE and enable EPWK WFOE to receive all of their expected residual returns, we account for EPWK VIE as a VIE. Accordingly, we consolidate the accounts of EPWK VIE for the periods presented herein, in accordance with Regulation S-X-3A-02 promulgated by the Securities Exchange Commission (“SEC”), and Accounting Standards Codification (“ASC”) 810-10, Consolidation.

Permission Required from the PRC Authorities to Operate the VIE or Offer Our Class A Ordinary Shares to Foreign Investors

In the opinion of our PRC counsel, Dacheng, we, our subsidiaries, and the VIE have obtained all the requisite licenses, permissions, and approvals from the PRC government to operate their business and engage in the business activities currently conducted by them in China, including through contractual arrangements, and we offer the securities being registered to foreign investors. As of the date of this prospectus, none of our, our subsidiaries’, or the VIE’s licenses, permissions, or approvals have ever been denied. Dacheng further advises us that we and the VIE are not currently required to obtain any licenses, permissions, or approvals from CSRC or CAC, to operate their business, including through contractual arrangements, or offer the securities being registered to foreign investors. We have disclosed the details of the licenses, permissions, and approvals issued by the PRC government to us, our subsidiaries, or the VIE as of the date of this prospectus. See “Item 4. Information on the Company-A. History and Development of the Company.”

The General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the Opinions, which was made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements and similar matters. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future. Given the current regulatory environment in the PRC, we are still subject to the uncertainty of different interpretation and enforcement of the rules and regulations in the PRC adverse to us, which may take place quickly with little advance notice. On December 28, 2021, the CAC, together with 12 other government departments of the PRC, jointly promulgated the Cybersecurity Review Measures, which became effective on February 15, 2022. We are not subject to cybersecurity review with the CAC in accordance with the Cybersecurity Review Measures, because (a) as of the date of this prospectus, our data processing activities (including the collection, storage, usage, transmission and publicity of data) do not damage national security; and (b) as of the date of this prospectus, we have not received any notice or determination from applicable PRC governmental authorities identifying it as a critical information infrastructure operator.

7

On February 17, 2023, the CSRC announced the Circular on the Administrative Arrangements for Filing of Securities Offering and Listing By Domestic Companies, and released a set of new regulations which consists of the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, and five supporting guidelines which came into effect on March 31, 2023. The Trial Measures refine the regulatory system by subjecting both direct and indirect overseas offering and listing activities to the CSRC filing-based administration. Requirements for filing entities, time points and procedures are specified. The Trial Measures apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the PRC and valued on the basis of interests in PRC domestic companies, or indirect offerings. Where a PRC domestic company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, file with the CSRC. The Trial Measures also lay out requirements for the reporting of material events. Breaches of the Trial Measures, such as offering and listing securities overseas without fulfilling the filing procedures, shall bear legal liabilities, including a fine between RMB1.0 million (approximately $150,000) and RMB10.0 million (approximately $1.5 million), and the Trial Measures heighten the cost for offenders by enforcing accountability with administrative penalties and incorporating the compliance status of relevant market participants into the Securities Market Integrity Archives. We are not required to complete the filing procedures pursuant to the Trial Measures in respect of this offering.

In the opinion of our PRC legal counsel, Beijing Dacheng Law Offices, LLP (Fuzhou) (“Dacheng”), there is no explicit provisions under currently effective PRC laws, regulations, or rules require companies like us who indirectly list their shares through contractual arrangements to obtain approvals from PRC authorities. However, due to the lack of further clarifications or detailed rules and regulations on overseas listing, Dacheng has further advised us that there are still uncertainties as to how such rules and regulations will be interpreted or implemented and whether the PRC regulatory agencies may adopt new laws, regulations, rules, or detailed implementation and interpretation, and there is no guarantee that PRC regulatory agencies, including the CSRC or CAC, would take the same view as they do. And we cannot assure you that we and the VIE can fully or timely comply with such new laws, regulations, rules or detailed implementation and interpretation. As the Circular and Trial Measures were newly published and there exists uncertainty with respect to the filing requirements and their implementation, we cannot be sure that we will be able to complete such filings in a timely manner, or at all. Any failure or perceived failure of us to fully comply with such new filing requirements under the Trial Measures may result in forced rectification, warnings and fines against us and could significantly hinder our ability to offer or continue to offer securities.

Additionally, because our Hong Kong subsidiary, EPWK Holdings Limited (“EPWK HK”), is not currently engaging in any active business activities and merely acting as a holding company, we do not believe we need to obtain additional permissions and approvals, including those under securities, data security, or anti-monopoly laws or regulations in Hong Kong, except those already disclosed in this prospectus.

Furthermore, our Class A ordinary shares had been delisted from Nasdaq when the staff of the Nasdaq Stock Market LLC filed a Form 25 Notification of Delisting. Our Class A ordinary shares have been quoted on the OTCID Basic Market under the symbol “EPWKF” since Nasdaq suspended the trading of our Class A ordinary shares on December 23, 2025, which does not constitute securities offering and listing, so we do not need to file with the CSRC for the OTC trading of our shares. However, we believe we will be required to file with the CSRC within three business days after the closing of any subsequent offerings of our securities. As the Overseas Listing Trial Measures was newly published, and there may be different interpretations or explanations, we cannot assure you that we would be able to complete the filing procedures, obtain the approvals or complete other compliance procedures in a timely manner, or at all, or that any completion of filing or approval or other compliance procedures would not be rescinded. Any such failure would subject us to sanctions by the CSRC or other PRC regulatory authorities. These regulatory authorities may impose restrictions and penalties on the operations in China, significantly limit or completely hinder our ability to launch any new offering of our securities, limit our ability to pay dividends outside of China, delay or restrict the repatriation of the proceeds from future capital raising activities into China, or take other actions that could materially and adversely affect our business, results of operations, financial condition and prospects, as well as the trading price of the Class A ordinary shares. Accordingly, the value of your investment may be materially and adversely affected or become worthless.

8

Dividend Distributions or Assets Transfer among the Holding Company, its Subsidiaries, the Consolidated VIE, and Investors

We currently do not have any cash management policies that dictate the purpose, amount and procedure for fund transfers among our Cayman Islands holding company, our subsidiaries, the consolidated VIEs, or investors. Rather, the funds can be transferred in accordance with the applicable laws and regulations. We may require additional capital resources in the future, and we may seek to issue additional equity or debt securities or obtain new or expanded credit facilities, which could subject us to operating and financing covenants, including requirements to maintain certain amount of cash reserves.

We intend to keep any future earnings to re-invest in and finance the expansion of our business, and we do not anticipate that any cash dividends will be paid or any assets will be transferred in the foreseeable future. As of the date of this prospectus, no transfers of cash, dividend payment or distribution has been made among the holding company, our subsidiaries, the consolidated VIE, or investors. Under Cayman Islands law, a Cayman Islands company may pay a dividend on its shares out of either profit or share premium amount, provided that in no circumstances may a dividend be paid if this would result in the company being unable to pay its debts due in the ordinary course of business. If we determine to pay dividends on any of our Class A Ordinary Shares in the future, as a holding company, we will be dependent on receipt of funds from our Hong Kong subsidiary, EPWK HK. EPWK HK is permitted under the laws of Hong Kong SAR to provide funds to us through dividend distribution out of profits available for distribution (that is, accumulated realized profits less accumulated realized losses) or other distributable reserves but not through share capital.

However, we, our subsidiaries and the VIE’s abilities to use cash held in the PRC or in a PRC entity through transfers, distributions, or dividends to fund operations or for other purposes outside of the PRC are subject to restrictions and limitations imposed by the PRC government. Current PRC regulations permit our indirect PRC subsidiaries to pay dividends to the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations through the current VIE Agreements, we may be unable to pay dividends on our Class A Ordinary Shares.

Furthermore, we may lose our ability to fund operations or for other uses outside of Hong Kong using cash in Hong Kong or a Hong Kong entity if, in the future, the PRC government expands its restrictions and limitations to include Hong Kong or Hong Kong entities.

9

Cash dividends, if any, on our Class A Ordinary Shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

In order for us to pay dividends to our shareholders, we will rely on payments made from EPWK VIE to EPWK WFOE, pursuant to VIE Agreements between them, and the distribution of such payments to EPWK HK as dividends from EPWK WFOE. Certain payments from our EPWK VIE to EPWK WFOE are subject to PRC taxes, including business taxes and VAT.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC project. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong resident enterprise must be the beneficial owner of the relevant dividends; and (b) the Hong Kong resident enterprise must directly hold no less than 25% share ownership in the PRC project during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong resident enterprise must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by our PRC subsidiary to its immediate holding company, EPWK HK. As of the date of this prospectus, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. EPWK HK intends to apply for the tax resident certificate when EPWK WFOE plans to declare and pay dividends to EPWK HK. See “Item 3. Key Information-D. Risk Factors-There are significant uncertainties under the EIT Law relating to the withholding tax liabilities of our PRC subsidiary, and dividends payable by our PRC subsidiary to our offshore subsidiaries may not qualify to enjoy certain treaty benefits” in the 2025 Annual Report

Financial Significance of the VIE

Under PRC law, we may provide funding to EPWK WFOE only through capital contributions or loans, and to EPWK VIE only through loans, subject to satisfaction of applicable government registration and approval requirements. We rely on dividends and other distributions from EPWK WFOE to satisfy part of our liquidity requirement. EPWK WFOE enjoys the economic interest in the operations of EPWK VIE in the form of service fees under the contractual arrangements among EPWK WFOE, EPWK VIE, and shareholders of EPWK VIE. For risks relating to the fund flows of our China operations, see “Item 3. Key Information-D. Risk Factors-Risks Relating to Our Corporate Structure - PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from making loans to our PRC subsidiaries and VIE or making additional capital contributions to our wholly foreign-owned subsidiaries in China, which could materially and adversely affect our liquidity and our ability to fund and expand our business.” And “Item 3. Key Information-D. Risk Factors-Risks Relating to Our Corporate Structure - We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business” in the 2025 Annual Report.

The VIE and its subsidiaries contributed to 100% of our consolidated revenue for the year ended June 30, 2025 and accounted for 34.01% of consolidated total assets and 99.95% of consolidated total liabilities as of June 30, 2025. The VIE and its subsidiaries contributed to 100% of our consolidated revenue for the year ended June 30, 2024 and accounted for 99.98% of consolidated total assets and 99.97% of consolidated total liabilities as of June 30, 2024. The VIE and its subsidiaries contributed to 100% of our consolidated revenue for the year ended June 30, 2023. For the years ended June 30, 2025, 2024 and 2023, there was no reconciliation performed between the financial position, cash flows and results of operations of the VIE and us.

10

The following financial information of the VIE and its subsidiaries was included in the condensed consolidated financial statements (in U.S. dollars, except for share or otherwise noted):

| As of | ||||||||

| June 30, | June 30, | |||||||

| 2025 | 2024 | |||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash | $ | 388,565 | $ | 226,776 | ||||

| Escrow funds | 537,744 | 446,775 | ||||||

| Accounts receivable, net | 328,844 | 162,910 | ||||||

| Advance to suppliers | 41,531 | 245,723 | ||||||

| Prepaid expenses and other receivables, net | 108,958 | 40,156 | ||||||

| Deferred tax asset | - | 1,384 | ||||||

| Total current assets | 1,405,642 | 1,123,724 | ||||||

| Property and equipment, net | 542,385 | 671,038 | ||||||

| Right-of-use assets | 1,976,410 | 2,473,165 | ||||||

| Intangible assets, net | 85,302 | 135,993 | ||||||

| Other non-current assets | 100,998 | 107,466 | ||||||

| Total non-current assets | 2,705,095 | 3,387,662 | ||||||

| TOTAL ASSETS OF VIE | $ | 4,110,737 | $ | 4,511,386 | ||||

| Liabilities | ||||||||

| Current liabilities: | ||||||||

| Short term bank loans | $ | 3,343,291 | $ | 3,385,073 | ||||

| Accounts payable | 427,758 | 560,062 | ||||||

| Contract liabilities - current | 2,248,983 | 2,098,022 | ||||||

| Escrow liability | 537,744 | 446,775 | ||||||

| Related parties payable | 2,034,990 | 1,386,022 | ||||||

| Accrued expenses and other current liabilities | 1,088,010 | 778,020 | ||||||

| Lease payable-current portion | 613,447 | 584,591 | ||||||

| Total current liabilities | 10,294,223 | 9,238,565 | ||||||

| Contract liabilities - non-current | 135,209 | 127,439 | ||||||

| Lease payable-non-current | 1,719,509 | 2,299,697 | ||||||

| Other non-current liabilities | 35,004 | 43,723 | ||||||

| Total non-current liabilities | 1,889,722 | 2,470,859 | ||||||

| TOTAL LIABILITIES OF VIE | $ | 12,183,945 | $ | 11,709,424 | ||||

| For the years ended June 30, | ||||||||

| 2025 | 2024 | |||||||

| Revenue | $ | 27,841,607 | $ | 20,215,245 | ||||

| Net loss | $ | (765,653 | ) | $ | (1,200,039 | ) | ||

| Net cash used in operating activities | $ | (372,969 | ) | $ | (1,623,106 | ) | ||

| Net cash used in investing activities | $ | (4,040 | ) | $ | (1,280 | ) | ||

| Net cash provided by financing activities | $ | 534,404 | $ | 1,242,456 | ||||

Assets Transfer Between VIE and Other Consolidated Entities

We currently do not have any cash management policies that dictate the purpose, amount and procedure of fund transfers among our Cayman Islands holding company, our subsidiaries, the consolidated VIEs, or investors. Rather, the funds can be transferred in accordance with the applicable laws and regulations. We may require additional capital resources in the future, and we may seek to issue additional equity or debt securities or obtain new or expanded credit facilities, which could subject us to operating and financing covenants, including requirements to maintain certain amount of cash reserves.

As of the date of this prospectus, we have not distributed any earnings or settled any amounts owed under the Contractual Arrangements. We do not have any plan to distribute earnings or settle amounts owed under the VIE agreements in the foreseeable future. We do not have any cash flows or transfers of other assets between EPWK VIE and EPWK WFOE for the years ended June 30, 2025, 2024 and 2023, and there is no dividends or distributions that EPWK VIE or its subsidiaries have made to our Company. See “Selected Condensed Consolidating Financial Statements of Parent, Subsidiaries, VIE and its Subsidiaries.”

11

Dividends or Distributions Made to Us and U.S. Investors and Tax Consequences