UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

EXCHANGE ACT OF 1934

OR

OF 1934

For

the fiscal year ended

OR

ACT OF 1934

OR

EXCHANGE ACT OF

1934

Date of event requiring this shell company report……………….

Commission

File Number:

(Exact name of Registrant as specified in its charter)

| Not applicable | ||

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) |

People’s

Republic of

(Address of Principal Executive Offices)

People’s

Republic of

Tel:

+

Email:

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| The

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital ,or common stock as of the close of the period covered by the annual report: ordinary shares, comprised of 8,838,194 Class A ordinary shares, par value $0.001 per share, and 3,730,320 Class B ordinary shares, par value $0.001per share, as of December 31, 2025.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If

this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section

13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Emerging

growth company |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

If

this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes ☐ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate

by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities

Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No

TABLE OF CONTENTS

| i |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F (including information incorporated by reference herein, the “Report”) is being filed by LOBO TECHNOLOGIES LTD., a British Virgin Islands business company. Unless otherwise indicated, “we,” “us,” “our,” “LOBO,” the “Group” and similar terminology refer to LOBO TECHNOLOGIES LTD. and its subsidiaries.

Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward- looking. Forward-looking statements in this Report may include, for example, statements about:

| ● | assumptions about our future financial and operating results, including revenue, income, expenditures, cash balances, and other financial items; | |

| ● | our ability to execute our growth, and expansion, including our ability to meet our goals; | |

| ● | current and future economic and political conditions; | |

| ● | our capital requirements and our ability to raise any additional financing which we may require; | |

| ● | our ability to attract customers and dealers and further enhance our brand recognition; | |

| ● | our ability to hire and retain qualified management personnel and key employees in order to enable us to develop our business; | |

| ● | trends and competition in the e-bikes, e-tricycles, and electric four-wheeled carts; and | |

| ● | other assumptions described in this annual report underlying or relating to any forward-looking statements. |

These forward-looking statements are based on information available as of the date of this Report, and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

You should not place undue reliance on these forward-looking statements. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements.

This Report also contains statistical data and estimates that we obtained from industry publications and reports generated by third-party providers of market intelligence. These industry publications and reports generally indicate that the information contained therein was obtained from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information.

| ii |

INTRODUCTION

We are a holding company primarily operating in China through our subsidiaries. Unless otherwise stated or unless the context otherwise requires, the terms “Company,” “the registrant,” “our company,” “the company,” “we,” “us,” “our,” “ours” and “LOBO” refer to LOBO TECHNOLOGIES LTD., a British Virgin Islands business company, and its subsidiaries.

Our consolidated financial statements are presented in U.S. dollars. All references in this annual report to “$,” “U.S. $,” “U.S. dollars” and “dollars” mean U.S. dollars, unless otherwise noted.

Unless otherwise indicated or the context requires otherwise, the terms “we,” “us,” “our Company,” “our,” “the Company” and “LOBO” refer to LOBO TECHNOLOGIES LTD., a British Virgin Islands company. In addition, in this annual report:

| ● | “Beijing LOBO” refers to Beijing LOBO Intelligent Machine Co., Ltd., previously a wholly-owned subsidiary of Jiangsu LOBO and disposed of by Jiangsu LOBO in April 2025;; |

| ● | “BVI” refers to British Virgin Islands; |

| ● | “BVI Act” refers to the BVI Business Companies Act, (Revised),, as amended; |

| ● | “China” or the “PRC” refers to the People’s Republic of China, excluding Taiwan for the purposes of this annual report only; |

| ● | “Class A Ordinary Shares” refers to the Company’s Class A Ordinary Shares, par value US$0.001 per share, with 90,000,000 Class A Ordinary Shares authorized and 8,838,194 Class A Ordinary Shares outstanding as of the date of this annual report; |

| ● | “Class B Ordinary Shares” refers to the Company’s Class B Ordinary Shares, par value US$0.001 per share, with 10,000,000 Class B Ordinary Shares authorized and 3,730,320 Class B Ordinary Shares outstanding as of the date of this annual report; |

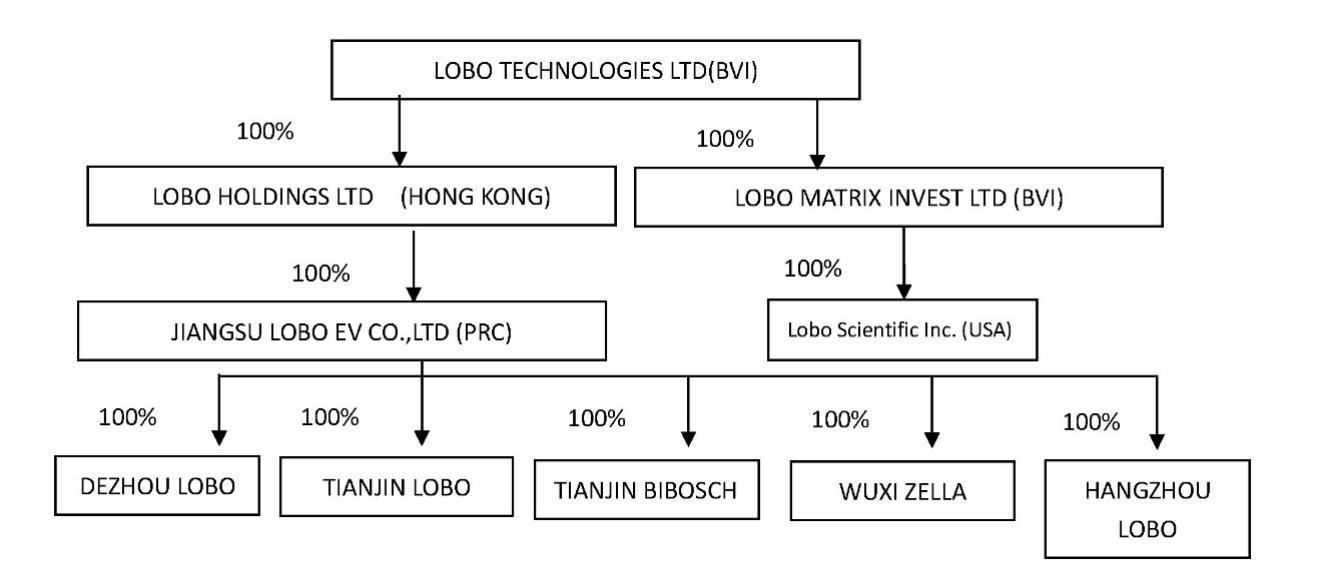

| ● | “Dezhou LOBO” refers to Dezhou LOBO Intelligent Manufacturing Co., Ltd., a wholly-owned subsidiary of Jiangsu LOBO; |

| ● | “EV” or “EVs” refers to two-wheeled electric vehicles, three-wheeled electric vehicles and off-highway four-wheeled electric shuttles or e-carts; |

| ● | “e” refers to electric. All of our products are driven by electric power whether labeled “e” or not; |

| ● | “E-bicycle” refers to the new national standard electric two-wheeled vehicle which conforms to the Safety Technical Specification for Electric Bicycle (GB 17761-2018); |

| ● | “E-moped” refers to the electric two-wheeled vehicle which conforms to the General specifications for electric motorcycles and electric mopeds (GB/T 24158-2018); |

| ● | “E-motorcycle” refers to the electric two-wheeled vehicle which conforms to the General specifications for electric motorcycles and electric mopeds (GB/T 24158-2018); |

| ● | “GAAP” refers to accounting principles generally accepted in the U.S.; |

| iii |

| ● | “Guangzhou LOBO” refers to Guangzhou LOBO Intelligent Technologies Co. Ltd., previously a wholly-owned subsidiary of Jiangsu LOBO and disposed of by Jiangsu LOBO on December 10, 2024; |

| ● | “Hangzhou LOBO” refers to LOBO (Hangzhou) Digital Service Co., Ltd., a wholly-owned subsidiary of Jiangsu LOBO; |

| ● | “Hong Kong” refers to Hong Kong Special Administrative Region of the PRC; |

| ● | “Jiangsu WFOE” or “Jiangsu LOBO” refers to Jiangsu LOBO Electric Vehicle Co. Ltd., a wholly-owned subsidiary of LOBO HK; |

| ● | “LOBO HK” refers to LOBO Holdings Ltd., a wholly-owned subsidiary of LOBO TECHNOLOGIES LTD.; |

| ● | “LOBO Matrix” refers to LOBO Matrix Invest Ltd., a wholly-owned subsidiary of LOBO TECHNOLOGIES LTD.; |

| ● | “LOBO Scientific” refers to LOBO Scientific Inc., a wholly-owned subsidiary of LOBO Matrix Invest Ltd. |

| ● | “Memorandum and Articles of Association” refers to the fourth amended and restated memorandum and articles of association of the Company, as adopted by a resolution of directors of the Company passed on December 8, 2025 and filed with the BVI registrar of corporate affairs on December 15, 2025; |

| ● | “R&D” refers to research and development |

| ● | “RMB” or “Chinese Yuan” refers to the legal currency of China; |

| ● | “SEC” or “Securities and Exchange Commission” refers to the U.S. Securities and Exchange Commission; |

| ● | “shares”, “Shares” or “Ordinary Shares” refer to the Ordinary Shares of LOBO TECHNOLOGIES LTD., consisting of Class A Ordinary Shares and Class B Ordinary Shares; |

| ● | “Tianjin LOBO” refers to Tianjin LOBO Intelligent Robot Co., Ltd., a wholly-owned subsidiary of Jiangsu LOBO; |

| ● | “Tianjin Bibosch” refers to Tianjin Bibosch Intelligent Technologies Co., Ltd., a wholly-owned subsidiary of Jiangsu LOBO; |

| ● | “U.S.” or “United States” refers to United States of America, its territories, its possessions and all areas subject to its jurisdiction; |

| ● | “U.S. dollars,” “dollars,” “USD” or “$” refers to the legal currency of the United States; |

| ● | “Wuxi Jinbang” refers to Wuxi Jinbang Electric Vehicle Manufacture Co., Ltd, previously an 85%-owned subsidiary of Beijing LOBO and disposed of by Beijing LOBO on December 30, 2024; and |

| ● | “Wuxi Zella” refers to Wuxi Zella Technology Trade Co., Ltd., a wholly-owned subsidiary of Jiangsu LOBO. |

| iv |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risks Related to Our Business and Industry

We may incur losses in the future.

We had net loss of $5,476,695 and $845,841 for the fiscal years ended December 31, 2025 and 2024, respectively. After we listed on Nasdaq, our operating expenses, together with the increased general administrative expenses of a growing public company, has increased as we seek to maintain and continue to grow our business, attract potential customers and further enhance our product offering. These efforts may prove more expensive than we currently anticipate, and we may not succeed in increasing our revenue sufficiently to offset these higher expenses. As a result of the foregoing and other factors, we may incur net losses in the future and may be unable to achieve or maintain profitability on a quarterly or annual basis for the foreseeable future.

Our success is dependent on our continued innovation and successful launches of new products and services, and we may not be able to anticipate or make timely responses to changes in the preferences of consumers.

The success of our operations depends on our ability to introduce new or enhanced e-bicycles, e-mopeds, e-tricycles, e-carts, and other new products and services. Consumer preferences differ across and within each of the regions in which we operate or plan to operate and may shift over time in response to changes in demographic and social trends, economic circumstances and the marketing efforts of our competitors. There can be no assurance that our existing products will continue to be favored by consumers or that we will be able to anticipate or respond to changes in consumer preferences in a timely manner. Our failure to anticipate, identify or react to these particular preferences could adversely affect our sales performance and our profitability. In addition, demand for many of our products, including accessories, are closely linked to customers’ purchasing power and disposable income levels, which may be adversely affected by unfavorable economic developments in the regions in which we operate.

We devote significant resources to product development and extensions. However, we may not be successful in developing innovative new products and services, and our new products may not be commercially successful. To the extent that we are not able to effectively gauge the direction of our key markets and successfully identify, develop and manufacture new or improved e-bicycles, e-mopeds, e-tricycles, e-carts in these changing markets, our financial results and our competitive position may suffer. Moreover, there are inherent market risks associated with new product introductions, including uncertainties about marketing and consumer preference, and there can be no assurance that we will be successful in introducing new products. We may expend substantial resources developing and marketing new products that may not achieve expected sales levels.

| 1 |

We have identified material weaknesses in our internal control over financial reporting. If we fail to develop and maintain an effective system of internal control over financial reporting, we may be unable to accurately report our financial results or prevent fraud.

In the course of auditing our consolidated financial statements as of and for the years ended December 31, 2025 and 2024, we and our independent registered public accounting firm identified two material weaknesses in our internal control over financial reporting as well as other control deficiencies. As defined in standards established by the PCAOB, a “material weakness” is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis. The material weaknesses identified relate to (1) we did not maintain proper accounting records and supporting document related to property, plant and equipment, and ordinary shares transactions; and (2) we had insufficient financial reporting and accounting personnel with appropriate knowledge of U.S. GAAP and SEC reporting requirements to properly address complex U.S. GAAP accounting issues and to prepare and review our consolidated financial statements and related disclosures to fulfil U.S. GAAP and SEC financial reporting requirements. We do not expect that our internal control over financial reporting and disclosure controls will prevent all error and all fraud. We will continue to take measures to remediate the material weakness in the future. However, we cannot be certain that these measures will successfully remediate the material weakness or that other material weaknesses will not be discovered in the future. If our efforts are not successful or other material weaknesses or control deficiencies occur in the future, we may be unable to report our financial results accurately on a timely basis or help prevent fraud, which could cause our reported financial results to be materially misstated and result in the loss of investor confidence or delisting and cause the market price of our Ordinary Shares to decline. In addition, it could in turn limit our access to capital markets, harm our results of operations, and lead to a decline in the trading price of our securities. Additionally, ineffective internal control over financial reporting could expose us to increased risk of fraud or misuse of corporate assets and subject us to potential delisting from the stock exchange on which we list, regulatory investigations and civil or criminal sanctions. We may also be required to restate our financial statements from prior periods. Because of our status as an emerging growth company, you will not be able to depend on any attestation from our independent registered public accountants as to our internal control over financial reporting for the foreseeable future.

We do not have a long history of running as an integrated group. Our limited operating history running as an integrated group in the industry may not provide an adequate basis to predict our future prospects and results of operations for this segment, and may increase the risk of your investment.

Our Company was incorporated in October 2021, and we acquired Jiangsu LOBO, including its subsidiaries, on April 8, 2022. We do not have a long history of running as an integrated group with standardized policies and procedures and on which our past performance may be predicted. Potential customers may not be familiar with our market and may have difficulty distinguishing our products and services from those of our competitors. Convincing potential target customers of the value of our products and services is critical to increasing the volume of sales and the success of our business. If we fail to promote or advertise the value of our products and services to our potential target customers, if the market for our services does not develop as we expect, or if we fail to address the needs of our target market in China or elsewhere, our business and results of operations will be harmed.

You should consider our business and future prospects in light of the risks and challenges we face as a new entrant into our industry, including, among other things, with respect to our ability to:

| ● | produce safe, reliable and quality e-bicycles, e-mopeds, e-tricycles, and e-carts, and AI products and services; |

| ● | build a well-recognized brand; |

| ● | establish and expand our customer base, including foreign customers; |

| 2 |

| ● | improve and maintain our operational efficiency; |

| ● | maintain a reliable, secure, high-performance and scalable technology infrastructure; |

| ● | attract, retain and motivate talented employees; |

| ● | anticipate and adapt to changing market conditions, including technological developments and changes in competitive landscape; |

| ● | navigate an evolving and complex regulatory environment; and |

| ● | identify suitable facilities to expand manufacturing capacity. |

If we fail to address any or all of these risks and challenges, our business may be materially and adversely affected.

We have limited experience to date in high volume manufacturing of our products. We cannot assure you that we will be able to develop or ensure efficient, automated, low-cost manufacturing capability and processes, and reliable sources of component supply that will enable us to meet the quality, price, engineering, design and production standards, as well as the production volumes required to successfully mass-market our currently available and future products. We may not be able to achieve similar results or grow at the same rate as we had in the past. As our business grows, we may adjust our product and service offerings. These adjustments may not achieve expected results and may have a material and adverse impact on our financial conditions and results of operations.

In addition, our growth and expansion have placed, and continue to place, a significant strain on our management and resources. This level of significant growth may not be sustainable or achievable at all in the future. We believe that our continued growth will depend on many factors, including continued launch of new products, effective marketing, successful entry into other overseas market and operating efficiency. We cannot assure you that we will achieve any of the above, and our failure to do so may materially and adversely affect our business and results of operations.

We face intense market competition. If we fail to develop and introduce new models of products, and AI-related products and services in anticipation of market demand in a timely and cost-effective manner, our competitive position and ability to generate revenues may be materially and adversely affected.

As a new player in the e-bicycles, e-tricycles, e-carts, and AI-related products and services, we face intense competition from current industry leaders. The introduction of new products is subject to risks and uncertainties. Unexpected technical, operational, logistical, regulatory or other problems could delay or prevent the introduction of our new products. Moreover, we cannot assure you that any of these new products will match the quality or popularity of those developed by our competitors, and achieve widespread market acceptance or generate the desired level of income for our customers.

Meanwhile, offering new products requires us to make investments in research and development, recruit and train additional qualified workers, and increase marketing efforts. In addition, some manufactures, including the large companies in this industry, like AIMA Technology Group Co., LTD and Yadea Group Holdings Ltd., have developed low-end and low-cost models which are sold at approximately RMB1,000 per two-wheel electric vehicle (without battery). Since most of the low-speed two-wheel EV users are low-income workers in China, we may encounter difficulties with the creation of the new products and in offering new products, we may face new risks and challenges that we are not familiar with. Furthermore, we may experience difficulties in recruiting or otherwise identifying qualified workers to develop the electric vehicles and AI-related products and services to address the new demand of potential customers. If we are unable to offer new products in a timely and cost-effective manner, our business, results of operations and financial condition could be adversely affected.

If we fail to adopt new technologies or adapt our e-bicycles, e-mopeds, e-tricycles, and off-highway four-wheeled electric shuttles and AI-related products and services to changing customer requirements or the industry standards, our business may be materially and adversely affected.

| 3 |

To remain competitive, we must continue to enhance and improve the functionality and features of our products. The production cycle of e-bicycles, e-mopeds, e-tricycles, and off-highway four-wheeled electric shuttles, from research and development stage to implementation stage takes one to two months. The changes in customer requirements and preferences, frequent introductions of new products and services embodying new technologies and the emergence of new industry standards and practices, any of which could render our existing technologies and products obsolete. Our success will depend, in part, on our ability to identify, develop, acquire or license leading technologies useful in our business, and respond to technological advances and new industry standards and practices in a cost-effective and timely way. The development of our products, and AI-related products and services entails significant technical and business risks. We may not be able to use new technologies effectively or adapt our proprietary technologies to meet customer requirements or new industry standards. If we are unable to adapt in a cost-effective and timely manner a response to changing market conditions or customer requirements, whether for technical, legal, financial or other reasons, our business, prospects, financial condition and results of operations may be materially and adversely affected.

If we fail to adopt new technologies or adapt our e-bicycles, e-mopeds, e-tricycles, e-carts, and AI products and services to changing customer requirements or the industry standards, our business may be materially and adversely affected.

To remain competitive, we must continue to enhance and improve the functionality and features of our products. The production cycle of e-bicycles, e-mopeds, e-tricycles, and e-carts, from research and development stage to implementation stage takes one to two months. The changes in customer requirements and preferences, frequent introductions of new products and services embodying new technologies and the emergence of new industry standards and practices, any of which could render our existing technologies and products obsolete. Our success will depend, in part, on our ability to identify, develop, acquire or license leading technologies useful in our business, and respond to technological advances and new industry standards and practices in a cost-effective and timely way. The development of our products, and AI-related products and services entails significant technical and business risks. We may not be able to use new technologies effectively or adapt our proprietary technologies to meet customer requirements or new industry standards. If we are unable to adapt in a cost-effective and timely manner a response to changing market conditions or customer requirements, whether for technical, legal, financial or other reasons, our business, prospects, financial condition and results of operations may be materially and adversely affected.

If we are unable to manage our growth or execute our strategies effectively, our business and prospects may be materially and adversely affected.

To accommodate our growth, we anticipate that we will need to implement a variety of new and upgraded operational and financial systems, procedures and controls, including the improvement of our accounting and other internal management systems. We will also need to continue to expand, train, manage and motivate our workforce and manage our relationships with customers and suppliers. All of these endeavors involve risks, and will require substantial management effort and significant additional expenditures. We may not be able to manage our growth or execute our strategies effectively, and any failure to do so may have a material adverse effect on our business and prospects.

Our marketing strategy of appealing to and growing sales to a more diversified group of users may not be successful.

Our marketing is aimed at reinforcing customer perceptions of our brand as a premium brand. We aim to provide users with a good user experiences. We cannot assure you that our services or our efforts in products will be successful, which could impact our revenues as well as customer satisfaction and our marketing.

To grow the business over the long term, we must be successful in selling products and services and promoting our brand experiences to a broader scope of customers and more users. We must also execute our diversification strategy without adversely impacting the strength of our brand with core users. Failure to successfully drive demand for our e-bicycles, e-mopeds, e-tricycles, and e-carts may have a material adverse effect on our business and results of operations.

| 4 |

Our products and services may experience quality problems from time to time, which could result in decreased sales, adversely affect our results of operations and harm our reputation.

Our products and services may contain design and manufacturing defects. There can be no assurance that we will be able to detect and fix all defects in the products and services we offer. Failure to do so could result in lost revenues, significant warranty and other expenses and harm to our reputation.

Additionally, we source and purchase key components in our operations and production from third-party suppliers, such as tires, motors and controllers. The quality and functions of these key components supplied by suppliers may not be consistent with and maintained at our standard, even if we have adopted examination processes when we receive the components. Any defects or quality issues in these key components or any noncompliance incidents associated with these third-party suppliers could result in quality issues with our products, and hence compromise our brand image and results of operations.

We rely heavily on dealers for sales and distribution of our products and our success depends on our offline distribution network.

We have established a distinct whole-sales network to sell our products and services to our dealers. As of December 31, 2025, we had approximately 32 domestic dealers in China, and approximately 132 foreign dealers around the world. We sell products to dealers directly, which are our important business partners to market our products, provide services to end-users, and show our brand images. We rely on these dealers in China to directly interact with and serve our users, but the interest of our dealers may not be entirely aligned with ours or with that of other dealers. For the fiscal year ended December 31, 2025, there are three dealers accounted for greater than 10% of our net accounts receivable. There can be no assurance that we will be able to maintain our existing relationships with our dealers. Additionally, our existing dealers may not be able to maintain past levels of sales or expand their sales. In addition, as we seek to expand into new regions in China, we cannot assure you that we will be able to successfully establish and maintain relationships with new dealers in these regions on favorable terms or at all.

Furthermore, we cannot assure you that we will be successful in managing our dealers and detecting inconsistencies with our brand image or values or noncompliance with the provisions of our sales agreements by them. Any noncompliance by our dealers could, among other things, negatively affect our brand reputation, demands for our products and our relationships with other dealers. Any of these could have a material and adverse effect on our business, financial condition, results of operations and prospects.

Default in payment by clients that have large account receivable balances could adversely impact our cash flows, working capital, results of operations and financial condition.

Our net accounts receivable balance was $3,107,520 as of December 31, 2025.

We are subject to the risk that we may be unable to collect accounts receivable in a timely manner. As a result, our dealers may not be able to pay us in a timely fashion and our accounts receivable and allowance for doubtful accounts may accordingly increase. Our liquidity and cash flows from operations may be adversely affected if our accounts receivable cycles or collections periods lengthen or if we encounter a material increase in defaults of payment of our account receivable.

In order to mitigate such risks, we conduct rigorous due diligence checks on the dealers and regularly assess the creditworthiness of corporate account clients. However, these mitigating efforts cannot ensure that we will be able to collect accounts receivable. If the accounts receivable cannot be collected in time, or at all, a significant amount of bad debt expense will occur, and our business, financial condition and results of operation will likely be materially and adversely affected.

We may be subject to product liability claims if people or properties are harmed by our products and we may be compelled to undertake product recalls or take other actions, which could adversely affect our brand image and results of operations.

We are subject to product liability claims for our sold products. As a result, sales of such products could expose us to product liability claims relating to personal injury or property damage and may require product recalls or other actions. Third parties subject to such injury or damage may bring claims or legal proceedings against us as the manufacturer of the products. In the future, we may at various times, voluntarily or involuntarily, initiate a recall if any of our products, including any systems or parts sourced from our suppliers, prove to be defective or noncompliant with applicable laws and regulations. Such recalls, whether voluntary or involuntary or caused by systems or components engineered or manufactured by us or our suppliers, could involve significant expense and could adversely affect our brand image in our target markets, as well as our business, prospects, financial condition and results of operations.

| 5 |

The e-bicycles, e-moped, e-tricycles, and e-carts, and AI-related products and services industries experience significant product liability claims and we face inherent risk of exposure to claims in the event our products do not perform as expected or malfunction resulting in property damage, personal injury or death. A successful product liability claim against us could require us to pay a substantial monetary award. Moreover, a product liability claim could generate substantial negative publicity about our products and business and inhibit or prevent commercialization of our future products which would have material adverse effect on our brand, business, prospects and operating results. As of December 31, 2025, we did not maintain any insurance to cover product liability claims . Any insurance coverage might not be sufficient to cover all potential product liability claims. Any lawsuit seeking significant monetary damages may have a material adverse effect on our reputation, business and financial condition.

We generally provide various warranties on different components and parts of our products to the dealers. In China, we provide extended quality warranty to our users for terms varying from three months to one year, excluding the vulnerable parts subject to certain conditions, among others, including that warranty only applies to normal use and quality issues. The occurrence of any material defects in our products could make us liable for damages and warranty claims in excess of our current reserves. In addition, we could incur costs to correct any defects, warranty claims or other problems, including costs related to product recalls. Any negative publicity related to the perceived quality of our products could affect our brand image, retailers, dealers and customer demands, and adversely affect our operating results and financial condition. While our warranty is limited to repairs and returns, warranty claims may result in litigation, the occurrence of which could adversely affect our business and operating results.

Our products are subject to safety and other standards issued by the Chinese regulatory authorities and failure to satisfy such mandated standards would have a material adverse effect on our business and operating results.

Our products must comply with the safety standards of the market where they are sold. In China, electric vehicles must meet or exceed all mandated safety standards, including national level and local level standards. It is required under these standards to conduct rigorous testing and use approved materials and equipment.

Electric bicycles must meet the safety requirements set out in the Safety Technical Specification for Electric Bicycle (GB17761-2018), or the Electric Bicycle Standard, which was jointly issued by the State Administration for Market Regulation and the National Standardization Administration of China on May 15, 2018 and came into effect on April 15, 2019. Electric vehicles, as one type of the power-driven vehicles, must also meet the safety requirements set out in the Technical Specifications for Safety of Power-Driven Vehicles Operating on Roads (GB7258-2017), which was jointly issued by the AQSIQ and National Standardization Administration of China on September 29, 2017 and took effect in January 1, 2018. Furthermore, the Safety Specifications for Electric Motorcycles and Electric Mopeds (GB24155-2020), which issued by the State Administration for Market Regulation and the National Standardization Administration of China in May 2020 and became effective on January 1, 2021, also stipulates some specific safety requirements for electric motorcycles. There is no guarantee that our products will satisfy the relevant standard and requirements for electric bicycles or motorcycles, and we may be required to satisfy additional industry standards and face regulation changes relating to electric bicycle and motorcycle business in the future. If our models were found to be in non-compliance of relevant laws and regulations, the models in question would be prohibited from being sold in the Chinese market, which would in turn materially and adversely affect our sales and revenue, and cause damage to our brand and result in liabilities.

Furthermore, the electric bicycles and motorcycles must pass various tests, undergo a certification process and finally be affixed with China Compulsory Certification, or CCC, prior to being delivered from the factory, being sold, or being used in any commercial case in China, and such certification is also subject to periodic renewal. On March 14, 2019, the Opinions of the State Administration for Market Regulation, the MITT and the Ministry of Public Security on Intensifying Supervision of the Execution of National Standards for Electric Bicycles, or the Opinions, was promulgated. The Opinions provide that the market supervision department should strengthen the management of CCC certification for electric bicycles, strengthen inspections of certification agencies and manufacture enterprises, and should only allow vehicles that meet the Electric Bicycle Standards and obtained CCC certification flowing into the market. There is no guarantee, however, that all series of our products will always comply with the CCC standard and satisfy the requirements of CCC certification, or that we will be able to renew our current certification or certify timely our new products in the future. If our products were found to be in non-compliance with the CCC standard sold in China, we would be prohibited from selling electric vehicles in the Chinese market, which would in turn materially and adversely affect our sales and revenue, and cause damage to our brand and result in liabilities.

| 6 |

We may not be able to prevent others from unauthorized use of our intellectual property, which could harm our business and competitive position.

We consider our copyrights, trademarks, trade names, internet domain names, patents and other intellectual property rights invaluable to our ability to continue to develop and enhance our brand recognition. We have invested significant resources to develop our own intellectual property. Failure to maintain or protect these rights could harm our business. We rely on a combination of patents, patent applications, trade secrets, including know-how, copyright laws, trademarks, intellectual property licenses, contractual rights and any other agreements to establish and protect our proprietary rights in our technology. In addition, we enter into confidentiality and non-disclosure agreements with our employees and business partners. Statutory laws and regulations are subject to judicial interpretation and enforcement and may not be applied consistently due to the lack of clear guidance on statutory interpretation. Contractual rights may be breached by counterparties, and there may not be adequate remedies available to us for any such breach.

The measures we take to protect our intellectual property rights may not be sufficient or adequate to prevent infringement on or misuse of our intellectual property. Any unauthorized use of our intellectual property by third parties may adversely affect our current and future revenues and our reputation. Preventing unauthorized uses of intellectual property rights could be difficult, costly and time-consuming, particularly in China. Litigation may be necessary to enforce our intellectual property rights. Initiating infringement proceedings against third parties can be expensive and time-consuming, and divert management’s attention from other business concerns. We may not prevail in litigation to enforce our intellectual property rights against unauthorized use. Furthermore, the practice of intellectual property rights enforcement by the PRC regulatory authorities is subject to significant uncertainty. We may have to resort to litigation to protect our intellectual property rights. Failure to adequately protect our intellectual property could harm our brand name and materially affect our business and results of operations.

We may need to defend ourselves against patent, trademark or other proprietary rights infringement claims, which may be time-consuming and would cause us to incur substantial costs.

Companies, organizations or individuals, including our competitors, may hold or obtain patents, trademarks or other proprietary rights that would prevent, limit or interfere with our ability to make, use, develop, sell or market our products, and AI-related products and services, which could make it more difficult for us to operate our business. From time to time, we may receive communications from holders of patents or trademarks regarding their proprietary rights. Companies holding patents or other intellectual property rights may bring suits alleging infringement of such rights or otherwise assert their rights and urge us to take licenses. Our applications and uses of patents and trademarks relating to our design, software or artificial intelligence technologies could be found to infringe upon existing patents and trademark ownership and rights.

Additionally, we may fail to own or apply for key trademarks in a timely fashion, or at all, which may damage our reputation and brand. Additionally, we receive from time-to-time letters alleging infringement of patents, trademarks or other intellectual property rights by us. If the similar trademark were to pass the preliminary review by the PRC regulatory authorities, we plan to contest against the application decision in question during the announcement period.

As our patents may expire and may not be extended, our patent applications may not be granted and our patent rights may be contested, circumvented, invalidated or limited in scope, our patent rights may not protect us effectively.

As of December 31, 2025, we owned 136 trademarks such as “LOBOEV,” WEIQI,” in the 12th category, vehicle segment, 40 registered patents, 21 copyrights, and 12 patent applications in China. For our pending applications, we cannot assure you that we will be granted patents pursuant to our pending applications. Even if our patent applications succeed and we are issued patents in accordance with them, it is still uncertain whether these patents will be contested, circumvented or invalidated in the future.

| 7 |

In addition, the rights granted under any issued patents may not provide us with proprietary protection or competitive advantages. The claims under any patents that issue from our patent applications may not be broad enough to prevent others from developing technologies that are similar or that achieve results similar to ours. It is also possible that the intellectual property rights of others will bar us from licensing and from exploiting any patents that are issued from our pending applications. Numerous patents and pending patent applications owned by others exist in the fields in which we have developed and are developing our technology. These patents and patent applications might have priority over our patent applications and could subject our patent applications to invalidation. Finally, in addition to those who may claim priority, any of our existing or pending patents may also be challenged by others on the basis that they are otherwise invalid or unenforceable.

We may be materially and adversely affected by negative publicity.

We rely on our brand image in selling our products. Negative publicity relating to our products, shareholders, management, employees, operations, suppliers, dealers, industry or products similar to ours, could materially and adversely affect consumer perceptions of our brand and result in decreased demand for our products. As of the date of this annual report, we had not received any negative publicity. However, there can be no assurance that we will not experience negative publicity in the future or that such negative publicity will not have a material adverse effect on our business, results of operations, financial condition or prospects.

We may fail to comply with legal or regulatory requirements or to obtain or adhere to requirements under relevant licenses, permits, registrations or certificates.

Our manufacturing and other production facilities as well as the packaging, storage, distribution, advertising and labeling of our products, and AI-related products and services, are subject to extensive legal and regulatory requirements. For example, pursuant to the Opinions of the State Administration for Market Regulation, the MITT and the Ministry of Public Security on Intensifying Supervision of the Execution of National Standards for Electric Bicycles, we must maintain the CCC certification for our products. Loss of or failure to renew or obtain necessary permits, licenses, registrations or certificates could delay or prevent us from meeting product demand, introducing new products, building new facilities or acquiring new business and could materially and adversely affect our operating results. If we are found to be in violation of applicable laws and regulations, we could be subject to administrative punishment, including fines, injunctions, recalls or asset seizures, as well as potential criminal sanctions, any of which could have a material adverse effect on our business, financial condition, results of operations and prospects.

In addition, future material changes in industry standards, laws and regulations, such as increased restrictions on manufacturers, could result in increased operating costs or affect our ordinary operations, which could also have a material adverse effect on our operations and our financial results. We largely rely on our self-established standards concerning the production and quality control of such products. While we are committed to producing high-quality products, there can be no assurance that our current production or quality control standards will satisfy any applicable laws and regulations that may come into effect in the future.

We are subject to a variety of costs and risks due to our continued expansion that may not be successful and could adversely affect our profitability and operating results.

We may enter into new geographic markets where we have limited or no experiences in marketing, selling, and localizing and deploying our products. We also may increase the capacity of manufacture, sales, and operations. Business expansion may be subject to risks such as:

● costs associated with establishing new distribution networks;

● difficulty finding qualified dealers in the new markets;

● difficulty integrating new operations or new product manufacture;

● difficulties staffing and with management techniques; and

● burdens of complying with a wide variety of local laws and regulations.

| 8 |

The occurrence of any of these risks could negatively affect our business in the new markets and consequently our business and operating results. In addition, the concern over these risks may also prevent us from entering into or releasing certain of our smart e-scooters in certain markets.

We rely on third-party logistic service providers to deliver our orders.

We typically rely on third-party logistic service providers to deliver orders. Damage or disruption to our distribution logistics due to disputes, weather, natural disasters, fire, explosions, terrorism, pandemics or labor strikes could impair our ability to distribute or sell our products. Inadequate third-party logistics services could also potentially disrupt our distribution and sales and compromise our business reputation. Failure to take adequate steps to mitigate the likelihood or potential impact of such events, or to effectively manage such events if they occur, could adversely affect our business, financial condition and results of operations, as well as require additional resources to restore our supply chain.

Our operations may be interrupted by production difficulties due to mechanical failures, utility shortages or stoppages, fire, natural disaster or other calamities at or near our facilities.

We are reliant on equipment and technology in our facilities for the production and quality control of our products, and our operations are subject to production difficulties such as capacity constraints of our production facilities, mechanical and systems failures and the need for construction and equipment upgrades, any of which may cause the suspension of production or/and reduced output. There can be no assurance that we will not experience problems with our equipment or technology in the future or that we will be able to address any such problems in a timely manner. Problems with key equipment or technology in one or more of our production facilities may affect our ability to produce our products or cause us to incur significant expense to repair or replace such equipment or technology. Also, scheduled and unscheduled maintenance programs may affect our production output. Any of these could have a material adverse effect on our business, financial condition, results of operations and prospects.

Furthermore, we depend on a continuous supply of utilities, such as electricity and water, to operate our production facilities. Any disruption to the supply of electricity or other utilities to our production facilities may disrupt our production, or cause the deterioration or loss of our inventory. This could adversely affect our ability to fulfill our sales orders and consequently may have an adverse effect on our business and results of operations. In addition, our operations are subject to operational risks. Fire, natural disasters, pandemics or extreme weather, including earthquakes, droughts, floods, typhoons or other storms, or excessive cold or heat could cause power outages, fuel shortages, water shortages, damage to our production, processing or distribution facilities or disruption of transportation channels, any of which could impair or interfere with our operations. We cannot assure you that these events will not happen in the future or that we will be able to take adequate measures to mitigate the potential impact of such events, or to effectively respond to such events if they occur, which could materially and adversely affect our business, financial condition and results of operations.

If our suppliers or dealers fail to use ethical business practices and comply with applicable laws and regulations, our brand image could be harmed due to negative publicity.

Our core values, which include developing competitive products and AI-related products and services while operating with integrity, are an important component of our brand image, which makes our reputation sensitive to allegations of unethical business practices. We do not control the business practices of our independent suppliers or dealers. Accordingly, we cannot guarantee their compliance with ethical business practices, such as environmental responsibilities and fair wage practices. A lack of demonstrated compliance could lead us to seek alternative suppliers or dealers which could increase our costs and results in delayed delivery of our products or other disruptions of our operations.

| 9 |

Violation of labor or other laws by our suppliers or dealers or the divergence of their labor or other practices from those generally accepted as ethical in the markets in which we do business could also attract negative publicity for us and our brand. This could diminish the value of our brand image and reduce demand for our products if, as a result of such violation, we were to attract negative publicity. If we, or other players in our industry, encounter similar problems in the future, it could harm our brand image, business, prospects, results of operations and financial condition.

Our success depends on our ability to retain our core management team and other key personnel.

Our performance depends on the continued service and performance of our directors, officers and senior management as they are expected to play an important role in guiding the implementation of our business strategies and future plans. If any of our directors, officers or any members of our senior management were to terminate their service or employment, there can be no assurance that we would be able to find suitable replacements in a timely manner, at acceptable cost or at all. The loss of services of key personnel or the inability to identify, hire, train and retain other qualified and managerial personnel in the future may materially and adversely affect our business, financial condition, results of operations and prospects. Additionally, we rely on our research and development personnel for product development and technology innovation. If any of our key research and development personnel were to leave us, we cannot assure you that we can secure equally competent research and development personnel in a timely manner, or at all.

Higher employee costs and inflation may adversely affect our business and our ability to achieve or maintain profitability.

China’s overall economy and the average wage in China have increased in recent years and are expected to grow. The average wage level for our employees has also increased in recent years. We expect that our employee costs, including wages and employee benefits, will increase. Unless we are able to pass on these increased employee costs to those who pay for our products and services, our ability to achieve or maintain profitability and our results of operations may be materially and adversely affected.

Our costs and expenses may also be affected by China’s inflation level. Since our inception, inflation in China has not materially impacted our results of operations. Although we have not in the past been materially affected by inflation since our inception, we can provide no assurance that we will not be affected in the future by higher rates of inflation in China.

We rely substantially on external suppliers for certain components and raw materials used in our products.

We purchase certain key components and raw material, such as batteries, motors, tires, battery chargers and controllers from external suppliers for use in our operations and production of products, and a continuous and stable supply of these components and raw materials that meet our standards is crucial to our operations and production. We normally enter into one-year procurement agreements with our main external suppliers. We expect to continue to rely on external suppliers for a substantial percentage of our production requirements in the future. We had no suppliers each accounting for greater than 10% of our total purchases in 2025 . We cannot assure you that we will be able to maintain our existing relationships with these suppliers and continue to be able to source electric motors, batteries or other key components and raw materials we use in our products on a stable basis and at a reasonable price or at all. For example, our suppliers may increase the prices for the components or materials we purchase and/or experience disruptions in their production of the components or materials.

The supply chain also exposes us to multiple potential sources of delivery failure or component shortages. While we obtain components from multiple sources whenever possible, some of the components used in our products are purchased by us from a single source. In the event that the supply of key components is interrupted for whatever reason or there are significant increases in the prices of these key components, our business, financial condition, results of operations and prospects may be materially and adversely affected. Additionally, changes in business conditions, force majeure, governmental changes and other factors beyond our control or that we do not presently anticipate could also affect our suppliers’ ability to deliver components to us on a timely basis.

| 10 |

We incur significant costs related to procuring components and raw materials required to manufacture and assemble our products. The prices for the components and raw materials fluctuate depending on factors beyond our control including market conditions and demand for these components and materials. Substantial increases in the prices for the components or raw materials we use in producing our products would increase our costs and reduce our margins. Any of the foregoing could materially and adversely affect our results of operations, financial condition and prospects. To date, we have not experienced cybersecurity attacks in our supply chain.

Any significant cybersecurity incident or disruption of our information technology systems or those of third-party partners could materially damage user relationships and subject us to significant reputational, financial, legal and operation consequences.

We depend on our enterprise resource planning (ERP) systems and claw agents, as well as those of third parties, to develop new products and services, store data, process transactions, respond to user inquiries, and manage inventory and our supply chain. Any material disruption or slowdown of our systems or those of third parties whom we depend upon could cause outages or delays in our business, which could harm our brand and adversely affect our operating results. We rely on cloud servers maintained by cloud service providers to store our data, and all of the data we collect are hosted at third-party cloud service providers.

Problems with our cloud service providers or the telecommunications network providers with whom they contract could adversely affect the user experience delivered by us. Our cloud service providers could decide to cease providing us services without adequate notice. Any change in service levels at our cloud servers or any errors, defects, disruptions or other performance problems with our information technology systems could harm our brand and may damage the data of our users. If changes in technology cause our information technology systems, or those of third parties whom we depend upon, to become obsolete, or if our or their information systems are inadequate to handle our growth, we could lose users, and our business and operating results could be adversely affected.

Changes in international trade policies, or the escalation of tensions in international relations, particularly with regard to China, may adversely impact our business and operating results.

There have been heightened tensions in international relations, particularly between the United States and China in recent years. The U.S. government has made statements and taken certain actions that have led to significant changes to U.S. and international trade policies towards China. In April 2025, the U.S. government imposed substantial tariff increases on Chinese imports, with rates reaching as high as 145% on certain goods. China has responded with retaliatory tariffs on U.S. products, escalating trade tensions between the two countries. It remains unclear what additional actions, if any, will be taken by the U.S. or other governments with respect to international trade agreements, the imposition of tariffs on goods imported into the U.S., tax policy related to international commerce, export controls, or other trade matters. Any unfavorable government policies on international trade, such as capital controls, tariffs, export restrictions, or limitations on the U.S. dollar payment and settlement system may affect the demand for our products, impact the competitive position of our products, prevent us from selling products in certain countries, or affect our participation in the U.S. dollar payment and settlement system, which would materially and adversely affect our international operations, results of operations and financial condition. If any new tariffs, legislation and/or regulations are implemented, or if existing trade agreements are renegotiated or, in particular, if the U.S. government takes further retaliatory trade actions due to the ongoing U.S.-China trade tensions, such changes could have an adverse effect on our business, financial condition and results of operations.

| 11 |

In addition to trade related tensions between China and the United States, the U.S. government has escalated tensions between the U.S. and China by revoking Hong Kong’s special trading status. Also, the Congress of the United States enacted the Uyghur Forced Labor Prevention Act (UFLPA) in December 2021. Effective from June 21, 2022, the UFLPA creates a rebuttable presumption that goods mined, produced, or manufactured (wholly or in part) in China’s Xinjiang Uyghur Autonomous Region are made with forced labor, where goods designated as such will be subject to an import ban into the United States. The President of the United States may also impose sanctions on companies that knowingly engage in, are responsible for, or facilitate forced labor in Xinjiang. Our factories are not in the Xinjiang Uyghur Autonomous Region of China (“XUAR”), and therefore, we do not experience labor shortages that impact our daily business. We have implemented policies and controls to mitigate risk of forced labor in our supply chain, and we do not believe that our suppliers source materials from the XUAR. However, these legal and policy developments could disrupt our supply chain or cause our suppliers to renegotiate existing arrangements with us or fail to perform on such obligations. To the extent we identify any potential non-compliance by any of our suppliers, we may have to find and establish relationships with alternative qualified suppliers under commercially acceptable terms. We cannot assure you that we will be able to do so in a timely manner. Under extreme situations, we may be subject to negative publicity or even be subject to regulatory actions, which may negatively affect our reputation and brand image, our business and results of operations, and may materially and adversely affect the price of our ordinary shares.

The ongoing war in Ukraine and sanctions on Russia continue to contribute to uncertainties in the relations between China and the United States, and tensions between these two countries remain elevated. These tensions have affected both diplomatic and economic ties between the two countries. Heightened tensions could reduce levels of trade, investments, technological exchanges, and other economic activities between the two major economies. The direct impacts of the war in Ukraine and sanctions on Russia to our business remain limited because we do not source our raw materials from the European Union, Russia, or Ukraine and can seek alternative suppliers to our current suppliers in China without undue cost or effort. However, the existing tensions and any further deterioration in international relations may have a negative impact on the general, economic, political, and social conditions in China and, given our reliance on the Chinese market, adversely impact our business, financial condition, and results of operations.

Our business plans require a significant amount of capital. In addition, our future capital needs may require us to issue additional equity or debt securities that may dilute the interests of our shareholders or introduce covenants that may restrict our operations or our ability to pay dividends.

We will need significant capital to, among other things, conduct research and development and expand our production capacity as well as roll out new products. We also expect to require significant capital and incur substantial costs in upgrading and expanding our manufacturing plant in China. As we ramp up our production capacity, operations, and research and development, we may also require significant capital to maintain our property, plant and equipment and such costs may be greater than anticipated.

Our ability to obtain the necessary financing to carry out our business plan is subject to a number of factors, including general market conditions and investor acceptance of our business plan. These factors may make the timing, amount, terms and conditions of such financing unattractive or unavailable to us. If we are unable to raise sufficient funds, we will have to significantly reduce our spending, delay or cancel our planned activities or substantially change our current corporate structure. We might not be able to obtain any funding, and we might not have sufficient resources to conduct our business as projected, both of which could mean that we would be forced to curtail or discontinue our operations.

An economic downturn or economic uncertainty may adversely affect consumer discretionary spending and demand for our products and services.

Our products and services may be considered discretionary items for some consumers. Factors affecting the level of consumer spending for such discretionary items include general economic conditions, and other factors, such as consumer confidence in future economic conditions, fears of recession, the availability and cost of consumer credit, levels of unemployment and tax rates. As global economic uncertainty remains, trends in consumer discretionary spending also remain unpredictable and subject to reductions. Unfavorable economic conditions may lead consumers to delay or reduce purchases of our products and services and consumer demand for our products and services may not grow as we expect. Our sensitivity to economic cycles and any related fluctuation in consumer demand for our products and services may have an adverse effect on our operating results and financial condition.

| 12 |

As of December 31, 2025, we do not have insurance coverage, which could expose us to significant costs and business disruption.

We are exposed to various risks associated with our business and operations, and we do not have liability insurance coverage. A successful liability claim against us due to injuries or damages suffered by our users could materially and adversely affect our reputation, results of operations and financial conditions. Even if unsuccessful, such a claim could cause us adverse publicity, require substantial costs to defend, and divert the time and attention of our management. In addition, we do not have any business disruption insurance. Any business disruption event could result in substantial costs to us and a diversion of our resources.

Competition for highly skilled personnel is often intense and we may incur significant costs or be unsuccessful in attracting, integrating, or retaining qualified personnel to fulfill our current or future needs.

We have, from time to time, experienced, and we expect to continue to experience, difficulty in hiring and retaining highly skilled employees with appropriate qualifications. In addition, if any of our senior management or key personnel joins a competitor or engages in a competing business, we may lose business, knowhow, trade secrets, business partners and key personnel. Furthermore, prospective candidates and existing employees often consider the value of the equity awards they receive in connection with their employment. Thus, our ability to attract or retain highly skilled employees may be adversely affected by declines in the perceived value of our equity or equity awards. Furthermore, there are no assurances that the number of shares reserved for issuance under our share incentive plans will be sufficient to grant equity awards adequate to recruit new employees and to compensate existing employees.

We are or may be subject to risks associated with our joint research arrangement, strategic alliances or acquisitions.

We have entered into joint research and development agreements with Jiangsu Research Institute of Dalian University of Technology and Jinan University, respectively, to conduct research and development in several different prospects. We may in the future enter into joint research and development agreements with various third parties to further our business purpose from time to time. The collaborations could subject us to a number of risks, including risks associated with sharing proprietary information, non-performance by the third party and increased expenses in establishing new strategic alliances, any of which may materially and adversely affect our business. We may have limited ability to monitor or control the actions of these third parties and, to the extent any of these strategic third parties suffers negative publicity or harm to their reputation from events relating to their business, we may also suffer negative publicity or harm to our reputation by virtue of our association with any such third party.

If appropriate opportunities arise, we may acquire additional assets, products, technologies or business that are complementary to our existing business. In addition to possible shareholders’ approval, we may also have to obtain approvals and licenses from relevant government authorities for the acquisitions and to comply with any applicable PRC laws and regulations, which could result in increased delay and costs, and may derail our business strategy if we fail to do so. Furthermore, past and future acquisitions and the subsequent integration of new assets and business into our own require significant attention from our management and could result in a diversion of resources from our existing business, which in turn could have an adverse effect on our business operations. Acquired assets or business may not generate the financial results we expect. Acquisitions could result in the use of substantial amounts of cash, potentially dilutive issuances of equity securities, the occurrence of significant goodwill impairment charges, amortization expenses for other intangible assets and exposure to potential unknown liabilities of the acquired business. Moreover, the costs of identifying and consummating acquisitions may be significant.

Our business could be adversely affected by trade tariffs or other trade barriers.

Starting from early 2018, the U.S. announced the imposition of tariffs on Chinese goods entering the United States and both China and the U.S. each imposed additional tariffs. In April 2025, the U.S. government introduced a new series of tariff increases on Chinese imports. The United States may also in the future impose tariffs on the importation of consumer products that may affect our business, including, among others, electric vehicles. In addition, the European Union has imposed additional tariffs on imports of e-bikes, which are defined as cycle with pedal assistance and an auxiliary electric motor, originating in the PRC. We currently export e-bikes into the United States, the Republic of Korea, ASEAN countries, and Latin American countries through our dealers, and we may increase our export volume through our dealers. To date, the impact of export restrictions, sanctions, tariffs, trade barriers, or political or trade tensions from these countries to our products is limited. However, ASEAN countries, and Latin American countries may in the future also impose tariffs on electric vehicles or other products that we currently sell to them, which may cause us to incur significant additional costs to conduct business and operation in the these countries. It is not yet clear what impact these tariffs may have or what actions other governments, including the Chinese government, may take in retaliation. In addition, these developments could have a material adverse effect on global economic conditions and the stability of global financial markets. Any of these factors could have a material adverse effect on our business, financial condition and results of operations.

| 13 |

Risks Related to Doing Business in China

Changes in China’s economic, political or social conditions or government policies could have a material and adverse effect on our business and results of operations.

Substantially all of our revenues are expected to be derived in China in the near future and most of our operations, including all of our manufacturing, is conducted in China. Accordingly, our results of operations, financial condition and prospects are influenced by economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. The PRC government exercises significant control over China’s economic growth through strategically allocating resources, controlling the payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies different regions within the country. Any adverse changes in economic conditions in China, in the policies of the Chinese government or in the laws and regulations in China could have a material adverse effect on the overall economic growth of China. Such developments could adversely affect our business and operating results, leading to reduction in demand for our products and services and adversely affect our competitive position.

Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us.

The PRC legal system is a civil law system based on written statutes. Unlike the common law system, prior court decisions may be cited for reference but have limited precedential value. Our PRC subsidiaries are foreign-invested enterprises and are subject to laws and regulations applicable to foreign-invested enterprises as well as various Chinese laws and regulations generally applicable to companies incorporated in China. However, since these laws and regulations are relatively new and the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties.

From time to time, we may have to resort to administrative and court proceedings to enforce our legal rights. However, since the PRC administrative and court authorities have significant discretion in interpreting and implementing statutory and contractual terms, it may be more difficult to evaluate the outcome of administrative and court proceedings and the level of protection we enjoy than in more developed legal systems. Furthermore, the PRC legal system is based in part on government policies and internal rules, some of which are not published on a timely basis or at all, and which may have a retroactive effect. As a result, we may not be aware of our violation of any of these policies and rules until sometime after the violation. Such uncertainties, including uncertainty over the scope and effect of our contractual, property (including intellectual property) and procedural rights, and any failure to respond to changes in the regulatory environment in China could materially and adversely affect our business and impede our ability to continue our operations.