UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone:

Email:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

An aggregate of

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange

Act.

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared

or issued its audit report.

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

| * | If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐ |

If this is an annual report, indicate by check

mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

TABLE OF CONTENTS

i

INTRODUCTION

In this annual report on Form 20-F, unless the context otherwise requires, references to:

| ● | “ALEO” are to Aleo, a layer 1 blockchain platform that utilizes zero-knowledge cryptography; |

| ● | “ALPH” are to Alephium, a cryptocurrency operating on a sharded layer 1 blockchain; |

| ● | “amended and restated memorandum and articles” are to the amended and restated memorandum and articles of association of Bgin currently in effect; |

| ● | “ASIC(s)” are to application-specific integrated circuit(s), microchip(s) designed for a special application; |

| ● | “BGA” are to Bugna, a digital currency using proof-of-work consensus mechanism; |

| ● | “Bgin CA” are to Bgin CA Limited, a limited liability company formed under the laws of the British Virgin Islands and a former indirect wholly-owned subsidiary of Bgin, which was dissolved on March 13, 2025; |

| ● | “Bgin Chip” are to Bgin Chip Limited, a limited liability company formed in Hong Kong and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Construction” are to BGIN CONSTRUCTION INC., a corporation incorporated in the State of Delaware and a wholly-owned subsidiary of Bgin EU; |

| ● | “Bgin EU” are to BGIN EU LIMITED, a private company limited by shares formed under the laws of Ireland (as defined below) and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Field” are to Bgin Field Limited, a limited liability company formed under the laws of the British Virgin Islands and a wholly-owned subsidiary of Bgin; |

| ● | “Bgin HK” are to Bgin Tech Limited, a Hong Kong company incorporated on March 18, 2019 and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Infrastructure US” are to Bgin Infrastructure, LLC, a limited liability company formed in the State of Delaware and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Management” are to BGIN MANAGEMENT, LLC, a limited liability company formed in the State of Delaware and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Mining” are to Bgin Mining Inc., a corporation formed in the State of Nebraska and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Rig” are to Bgin Rig Limited, a limited liability company formed under the laws of the British Virgin Islands and a wholly-owned subsidiary of Bgin; |

| ● | “Bgin SG” are to Bgin Technologies Pte Ltd, a limited liability company formed in Singapore and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Singapore” are to Bgin Tech Pte. Ltd., a limited liability company formed in Singapore and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Trade HK” are to Bgin Trade HK Limited, a limited liability company formed in Hong Kong and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin Trading” are to Bgin Trading Limited, a limited liability company formed in Hong Kong and an indirect wholly-owned subsidiary of Bgin; |

| ● | “Bgin US” are to Bgin US Limited, a limited liability company formed under the laws of the British Virgin Islands and an indirect wholly-owned subsidiary of Bgin; |

| ● | “BVI” are to the British Virgin Islands; |

ii

| ● | “CAGR” are to compound annual growth rate; |

| ● | “China” or the “PRC” are to the People’s Republic of China, including the special administrative regions of Hong Kong and Macau for the purposes of this annual report only; |

| ● | “Class A ordinary shares” are to the Class A Ordinary Shares, par value US$0.0000695652173913043 per share, of Bgin; |

| ● | “Class B ordinary shares” are to Class B Ordinary Shares, par value US$0.0000695652173913043 per share, of Bgin; |

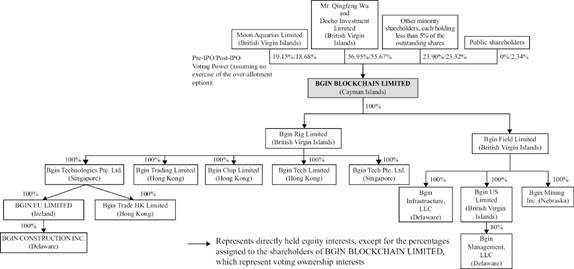

| ● | “Company,” “Bgin,” “we”, “us”, or “our,” are to BGIN BLOCKCHAIN LIMITED, a Cayman Islands exempted company; |

| ● | “cryptocurrency” are to any form of currency that only exists digitally, that usually has no central issuing or regulating authority but instead uses a decentralized system to record transactions and manage the issuance of new units, and that relies on cryptography to prevent counterfeiting and fraudulent transactions; |

| ● | “Decho Investment” are to Decho Investment Limited, a limited liability company formed under the laws of the British Virgin Islands and controlled by Mr. Qingfeng Wu; |

| ● | “digital assets” are to any digital representation of value that may function as a medium of exchange, a unit of account, and/or a store of value. Digital assets may include, but not limited to, cryptocurrencies; |

| ● | “FPGA(s)” are to field-programmable gate array(s), the integrated circuit(s) designed to be configured by customers after manufacturing; |

| ● | “GH” are to GigaHashes and “GH/s” are to GigaHashes per second, representing 1,000,000,000 hashes per second; |

| ● | “GPU(s)” are to graphics processing unit(s); |

| ● | “hash” are to the computation run by mining machines in support of the blockchain; |

| ● | “hash rate” are to the speed at which a computer can solve computations in support of the blockchain; |

| ● | “Hong Kong” or “HK” are to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| ● | “HK$” and “HK dollars” are to the legal currency of Hong Kong; |

| ● | “Investment Company Act” or “1940 Act” are to the Investment Company Act of 1940; |

| ● | “Ireland” are to the Republic of Ireland; |

| ● | “KAS” are to “Kaspa”, a cryptocurrency relying on proof-of-work system; |

| ● | “MH” are to MegaHashes and “MH/s” are to MegaHashes per second, representing 1,000,000 hashes per second; |

| ● | “Moon Aquarius” are to Moon Aquarius Limited, a limited liability company formed under the laws of the British Virgin Islands and controlled by Mr. Qiuhua Li; |

| ● | “Mainland China” are to the People’s Republic of China, excluding Taiwan, the Hong Kong Special Administrative Region and the Macao Special Administrative Region; |

| ● | “ordinary shares” are to our Class A ordinary shares and Class B ordinary shares; |

| ● | “PCB” are to printed circuit board, a base for mounting microelectronic components in electronics; |

| ● | “PH” are to PetaHash and “PH/s” are to PetaHashes per second, representing 1,000,000,000,000,000 hashes per second; |

iii

| ● | “RMB” and “Renminbi” are to the legal currency of China; |

| ● | “RXD” are to Radiant, a peer-to-peer programmable digital asset system; |

| ● | “SDR” are to Special Drawing Rights, an international reserve asset created by the International Monetary Fund to supplement the official reserves of its member countries; |

| ● | “Shenzhen Bgin” are to Shenzhen Bgin Technology Co., Ltd., a company formed in the PRC, where Mr. Qiuhua Li, our director and the executive chairman of our board of directors, serves as the supervisor, and Mr. Qi Shao, our chief technology officer, serves as the general manager; |

| ● | “Singapore dollars” and “S$” are to the legal currency of Singapore; |

| ● | “Tether” or “USDT” are to an asset-backed cryptocurrency “stablecoin” with an exchange rate pegged to fiat currency and designed to be valued at US$1.0; |

| ● | “TH” are to TeraHashes and “TH/s” are to TeraHashes per second, representing 1,000,000,000,000 hashes per second; |

| ● | “U.S.”, “US” or “United States” are to United States of America, its territories, its possessions and all areas subject to its jurisdiction; |

| ● | “U.S. GAAP” are to generally accepted accounting principles in the United States; and |

| ● | “$,” “dollars,” “US$” or “U.S. dollars” are to the legal currency of the United States. |

This annual report on Form 20-F includes our audited consolidated financial statements for the years ended December 31, 2025, 2024, and 2023.

We do not have any operations of our own. We are a holding company with operations conducted (i) in Hong Kong through our Hong Kong operating subsidiaries Bgin HK, Bgin Trading, Bgin Trade HK and Bgin Chip, using U.S. dollars as their functional currency, (ii) in Singapore through our Singapore subsidiaries, Bgin Singapore and Bgin SG, using U.S. dollars as their functional currency, and (iii) in the U.S. through our U.S. subsidiaries, Bgin Infrastructure US, Bgin Management and Bgin Mining, using U.S. dollars as their functional currency. This annual report contains translations of certain foreign currency amounts into U.S. dollars for the convenience of its readers. Assets and liabilities are translated into U.S. dollars at the closing rate of exchange as of the balance sheet dates, the statement of income is translated using average rate of exchange in effect during the reporting periods, and the equity accounts are translated at historical exchange rates. Translation adjustments resulting from this process are included in accumulated other comprehensive income. Transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred. The shareholders’ equity accounts were stated at their historical rate. Cash flows are also translated at average translation rates for the periods, therefore, amounts reported on the statements of cash flows will not necessarily agree with changes in the corresponding balances on the consolidated balance sheets. No representation is made that the Renminbi amounts could have been, or could be, converted, realized or settled into US$ at such rate, or at any other rate.

Translations from HK dollars to U.S. dollars and from U.S. dollars to HK dollars in this annual report are made at a pegged exchange rate of US$1=HK$7.8. Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report are made as follows:

| December 31, 2023 | December 31, 2024 | December 31, 2025 | ||||||||||

| Period-end spot rate | Average rate | Period-end spot rate | Average rate | Period-end spot rate | Average rate | |||||||

| US$ against Renminbi | US$1=RMB 7.0999 | US$1=RMB 7.0809 | US$1=RMB 7.2993 | US$1=RMB 7.1957 | US$1=RMB 6.9931 | US$1=RMB 7.1875 | ||||||

iv

Part I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

This annual report refers to (i) BGIN BLOCKCHAIN LIMITED, a Cayman Islands holding company, as the “Company,” “Bgin”, “we”, “our” and “us”, and (ii) the Company’s subsidiaries as “our subsidiaries” or the “subsidiaries.” The Cayman Islands holding company does not conduct any business operations and the Company’s subsidiaries are entities that conduct business operations in Singapore, the Hong Kong Special Administrative Region of the People’s Republic of China (“Hong Kong”), and the U.S. Investors in our Class A ordinary shares and other equity securities we issue are not purchasing equity interests in our subsidiaries but instead are purchasing equity interests in the Company, the ultimate Cayman Islands holding company.

Bgin is not an operating company, but an exempted company with limited liability incorporated in the Cayman Islands. As an exempted company with no material operations, our operations are conducted by our subsidiaries, including (i) our subsidiaries in Singapore, Bgin Tech Pte. Ltd. (“Bgin Singapore”) and Bgin Technologies Pte Ltd (“Bgin SG”), (ii) our subsidiaries in Hong Kong, Bgin Tech Limited (“Bgin HK”), Bgin Trading Limited (“Bgin Trading”), Bgin Trade HK Limited (“Bgin Trade HK”), and Bgin Chip Limited (“Bgin Chip”), (iii) our subsidiaries in the U.S., Bgin Infrastructure, LLC (“Bgin Infrastructure US”), BGIN MANAGEMENT, LLC (“Bgin Management”) and Bgin Mining Inc. (“Bgin Mining”). This structure involves unique risks to the investors as you may never directly hold any equity interest in our operating subsidiaries, and our ability to receive dividends and other contribution from our subsidiaries in Hong Kong is significantly affected by regulations promulgated by Hong Kong or PRC authorities. Any change in the interpretation of existing rules and regulations or the promulgation of new rules and regulations would likely result in a material change in the operations of our operating entities and/or a material change in the value of the securities we are registering for sale, including that such event could cause the value of such securities to significantly decline or become worthless. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — Uncertainties arising from the legal system in Mainland China, including uncertainties regarding the interpretation and enforcement of laws in Mainland China and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause the Class A ordinary shares to significantly decline in value or become worthless.”

In addition to our operations in the U.S. and Singapore, a portion of our operations are conducted in Hong Kong by Bgin HK, Bgin Trading, Bgin Trade HK and Bgin Chip, our subsidiaries in Hong Kong. As such, we are subject to certain legal and operational risks associated with such operating subsidiaries being based in Hong Kong and having all of their operations to date in Hong Kong. Pursuant to the Basic Law of the Hong Kong Special Administrative Region (the “Basic Law”), which is a national law of the PRC and the constitutional document for Hong Kong, national laws of the PRC shall not be applied in Hong Kong except for those listed in Annex III of the Basic Law and applied locally by promulgation or local legislation. The Basic Law expressly provides that the national laws of the PRC which may be listed in Annex III of the Basic Law shall be confined to those relating to defense and foreign affairs as well as other matters outside the autonomy of Hong Kong. The basic policies of the PRC regarding Hong Kong as a special administrative region of the PRC are reflected in the Basic Law, providing Hong Kong with executive, legislative and independent judicial powers, including that of final adjudication under the principle of “one country, two systems”. Nevertheless, the Chinese government may intervene or influence our current or future operations in Hong Kong at any time. For details relating to risks of doing business in Hong Kong, see “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong.”

1

In general, any risks related to doing business in Mainland China also apply to doing business in Hong Kong. Uncertainties arising from the legal system in the PRC, including Hong Kong, in which uncertainties regarding the interpretation and enforcement of laws and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our Class A ordinary shares to significantly decline in value or become worthless. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong.” In recent years, the PRC government initiated a series of regulatory actions and statements to regulate business operations in certain areas in China with little advance notice, including a cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using the variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement, which may in the future impact our ability to conduct out business, accept foreign investments or list on a U.S. or other foreign exchange if we were to become subject to such regulations. In light of the PRC government’s recent expansion of authority in Hong Kong, we may be subject to uncertainty about any future actions of the PRC government or authorities in Hong Kong. Moreover, all the legal and operational risks associated with having operations in the PRC also apply to operations in Hong Kong. There is no assurance that there will not be any changes in the economic, political and legal environment in Hong Kong. The PRC government has intervened and may continue to intervene or influence our current and future operations in Hong Kong at any time or may exert more oversight and control over offerings conducted overseas and/or foreign investment in issuers like ourselves. On February 17, 2023, the China Securities Regulatory Commission (“CSRC”) issued the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Overseas Listing Trial Measures, and five relevant supporting guidelines, which took effect on March 31, 2023. According to the Overseas Listing Trial Measures, PRC domestic companies that seek to offer and list securities in overseas markets, either by direct or indirect means, are required to fulfill the filing procedures with the CSRC and report relevant information. The Overseas Listing Trial Measures also provides that if the issuer both meets the following criteria, the overseas securities offering and listing conducted by such issuer will be deemed as indirect overseas offering by PRC domestic companies: (i) more than 50% of any of the issuer’s operating revenue, total profit, total assets or net assets as documented in its audited consolidated financial statements for the most recent fiscal year is accounted for by PRC domestic companies; and (ii) the main parts of the issuer’s business activities are conducted in mainland China, or its main place(s) of business are located in mainland China, or the majority of senior management staff in charge of its business operations and management are PRC citizens or have their usual place(s) of residence located in mainland China. Where a domestic company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, fulfil the filing procedure with the CSRC. As advised by our PRC legal counsel, we are not required to obtain the approval from or complete filings with the CSRC for our follow-on offerings based on the facts that: (1) we do not meet the above explicit conditions set out in the Overseas Listing Trial Measures to determine whether an overseas offering shall be deemed as an indirect overseas offering and listing by a domestic company; (2) we do not have any subsidiary in mainland China or use any VIE structure to control any entity in mainland China; and (3) the main parts of our business activities are not conducted in mainland China and our main place of business is located in Singapore, the U.S. and Hong Kong. However, as the Overseas Listing Trial Measures was newly published, there are substantial uncertainties as to the implementation and interpretation, and the CSRC may take a view that is contrary to our understanding of the Overseas Listing Trial Measures because the Overseas Listing Trial Measures adopts the principle of “substance over form” regarding the determination of “indirect overseas offering and listing by a domestic company”, over which the CSRC may have substantial discretions. If we are required by the CSRC to submit and complete the filing procedures for our follow-on offerings, we cannot assure you that we will be able to complete such filings in a timely manner, or even at all. Any failure by us to comply with such filing requirements under the Overseas Listing Trial Measures may result in an order to rectify, warnings and fines against us and could materially hinder our ability to offer or to continue to offer our securities. If certain PRC laws and regulations were to become applicable to a company such as us in the future, the application of such laws and regulations may have a material adverse impact on our business, financial condition and results of operations, and significantly limited or completely hinder our ability to continue our operations and/or our ability to offer or continue to offer securities to investors, any of which may cause the value of our securities, including the Class A ordinary shares, to significantly decline or become worthless. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — Uncertainties arising from the legal system in Mainland China, including uncertainties regarding the interpretation and enforcement of laws in Mainland China and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause the Class A ordinary shares to significantly decline in value or become worthless,” “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — The enactment of Law of the PRC on Safeguarding National Security in Hong Kong (the “Hong Kong National Security Law”) and the enactment of Safeguarding National Security Ordinance in Hong Kong (the “Hong Kong National Security Ordinance”) could impact our Hong Kong subsidiaries,” “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — Failure to comply with cybersecurity, data privacy, data protection, or any other laws and regulations related to data may materially and adversely affect our business, financial condition, and results of operations” and “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — If we were to be required to obtain any permission or approval from or complete filings with the CSRC, the CAC, or other PRC authorities in connection with our follow-on offerings under PRC law, our ability to offer or continue to offer our securities to investors could be significantly limited or hindered, which could cause the value of our Class A ordinary shares to significantly decline or become worthless, and we may be fined or subject to other sanctions, and our business, reputation financial condition, and results of operations may be materially and adversely affected.”

2

As of the date of this annual report, our subsidiaries’ mining operations (otherwise referred to as “self-mining”) are conducted in the United States, and a substantial amount of our assets are located in the United States. Since April 2023, our business of selling mining machines designed by us has also been conducted in the United States through Bgin Mining, in Hong Kong through Bgin Trading and in Singapore through Bgin SG. However, many of our directors and officers, including Mr. Zhao Xiang and Mr. Pengju Wang, are nationals and residents of mainland China, and a substantial portion of their assets are located in mainland China. Additionally, Mr. Qiuhua Li, Mr. Qingfeng Wu and Mr. Qi Shao, our directors and officers, while being nationals of Mainland China, are residents of Singapore, Hong Kong, and Hong Kong, respectively. Further, Mr. Boquan He and Mr. Chung Shing Paul Tsang, our independent directors, are residents of Hong Kong, and a substantial portion of their assets are located in Hong Kong. As a result, it may be difficult for a shareholder to effect service of process within the United States upon these persons, or to bring actions or enforce against us or our directors and officers judgments obtained in United States courts, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state in the United States.

Additionally, our current and former auditors, the independent registered public accounting firms that issue the audit report included elsewhere in this annual report, as auditors of companies that are traded publicly in the United States and firms registered with the Public Company Accounting Oversight Board (“PCAOB”), are subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. Our current and former auditors are subject to PCAOB inspections and PCAOB is able to inspect our current and former auditors, and they are not subject to the determinations announced by the PCAOB on December 16, 2021. However, an exchange may determine to delist our securities, and our Class A ordinary shares may be prohibited from being traded on a national exchange, or an exchange under the Holding Foreign Companies Accountable Act if the PCAOB is unable, or determines that it cannot, inspect or fully investigate our auditors for two consecutive years. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”), was signed into law. The Consolidated Appropriations Act contained, among other things, an identical provision to Accelerating Holding Foreign Companies Accountable Act, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the Holding Foreign Companies Accountable Act from three years to two, thus reducing the time period before our securities may be prohibited from trading or delisted. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”), governing inspections and investigations of audit firms based in China and Hong Kong. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control. The PCAOB is continuing to demand complete access in mainland China and Hong Kong moving forward and is already resuming regular inspections, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has indicated that it will act immediately to consider the need to issue new determinations with the Holding Foreign Companies Accountable Act if needed and does not have to wait another year to reassess its determinations. Our securities may be delisted or prohibited from trading if the PCAOB determines that it cannot inspect or investigate completely our auditor under the Holding Foreign Companies Accountable Act. The delisting of our Class A ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment in the future. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — Regulatory developments regarding auditor inspection requirements may affect our securities.”

We are permitted under the laws of the Cayman Islands to provide funding to our subsidiaries in Hong Kong through loans or capital contributions without restrictions on the amount of the funds. Bgin HK, Bgin Trading, Bgin Trade HK and Bgin Chip are permitted under the laws of Hong Kong to provide funding to Bgin, the holding company incorporated in the Cayman Islands, through dividend distribution or payments without restrictions on the amount of the funds.

3

The PRC government’s significant authority to intervene in or influence operations of an offshore holding company at any time could limit our ability to transfer cash both into and outside of China, including Hong Kong. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong — The PRC government’s significant authority to intervene in or influence the China operations of an offshore holding company at any time could limit our ability to transfer or use our cash outside of China, and otherwise result in material adverse change in our operations and the value of our Class A ordinary shares.” From time to time, cash may be transferred between our Cayman Islands holding company and its subsidiaries, and among the Company’s subsidiaries as intercompany cash transfers. For the fiscal year ended December 31, 2023, (i) Bgin HK transferred cash in the amount of US$5,352,200 to Bgin Infrastructure US, US$8,800 to Bgin Chip, US$9,222,745 to Bgin Singapore, US$36,884,440 to Bgin Trading, and US$298,500 to Bgin Mining, (ii) Bgin Chip transferred cash in the amount of US$22,113 to Bgin HK and US$413,002 to Bgin Singapore, (iii) Bgin Singapore transferred cash in the amount of US$58,913 to Bgin HK, US$650,776 to Bgin Trading, US$446,186 to Bgin Chip, and US$59,467 to Bgin Infrastructure US, (iv) Bgin Trading transferred cash in the amount of US$45,181,002 to Bgin HK, US$27,668,359 to Bgin Singapore, US$1,203,102 to Bgin Mining, and US$8,000 to Bgin Chip, (v) Bgin Infrastructure US transferred cash in the amount of US$10,010 to Bgin Mining, and (vi) Bgin Mining transferred cash in the amount of US$680,000 to Bgin Infrastructure US. For the fiscal year ended December 31, 2024, (i) Bgin HK transferred cash in the amount of SG$400,000 (approximately US$298,418) to Bgin Singapore, US$220,651,271 to Bgin Trading, US$66,107,110 to Bgin Singapore, US$41,224 to Bgin Chip, and US$100 to Bgin Management, US$3,750,000 to Bgin Infrastructure; (ii) Bgin Trading transferred cash in the amount of US$15,665,000 to Bgin Infrastructure, US$134,485,959 to Bgin Singapore, and US$295,192,349 to Bgin HK, US$3,000,000 to Bgin Chip, US$1,000,000 to Bgin Mining, US$6,200,000 to Bgin SG, US$50,000 to Bgin Trade; (iii) Bgin Singapore transferred cash in the amount of US$1,964,400 to Bgin HK, US$3,290,000 to Bgin Infrastructure, US$1,390,000 to Bgin SG; (iv) Bgin Infrastructure transferred cash in the amount of US$793,400 to Bgin Mining, US$451,780 to Bgin HK, US$970,000 to Bgin Trading, US$1,000,000 to Bgin Singapore; (v) Bgin Management transferred cash in the amount of US$6,403,934 to Bgin HK, US$3,379,800 to Bgin Infrastructure, US$8,248 to Bgin Mining; (vi) Bgin Mining transferred cash in the amount of US$280,000 to Bgin Infrastructure, US$328,384 to Bgin HK, US$994,965 to Bgin Singapore; (vii) Bgin Chip transferred cash in the amount of US$102,716 to Bgin Singapore; (viii) Bgin SG transferred cash in the amount of US$10,550,992 to Bgin HK; and (ix) Bgin Trade transferred cash in the amount of US$701,009 to Bgin HK. For the fiscal year ended December 31, 2025, (i) Bgin HK transferred cash in the amount of US$1,370,000 to Bgin Mining, US$8,530,100 to Bgin Trading, US$3,006,132 to Bgin Management, US$57,530,099 to Bgin SG, US$31,000 to Bgin Singapore, US$993,888 to the Company, US$14,000 to Bgin Chip, US$418,746 to Bgin Trade, and US$3,190,000 to Bgin Infrastructure, (ii) Bgin Trading transferred cash in the amount of US$8,846,142 to Bgin HK, US$932,828 to Bgin Singapore, US$31,600,000 to Bgin Infrastructure, US$45,209,412 to Bgin SG, US$5,750,000 to the Company, US$50,000 to Bgin Chip, US$99,057 to Bgin Management, US$357,060 to Bgin Rig, and US$217,956 to Bgin Trade, (iii) Bgin Singapore transferred cash in the amount of US$970,000 to Bgin HK, US$24,624 to Bgin Mining, and US$308,064 to Bgin Chip, (iv) Bgin Infrastructure US transferred cash in the amount of US$2,886,200 to Bgin Management, US$73,000 to Bgin HK, US$634,339 to Bgin Singapore, and US$100 to Bgin Mining, (v) Bgin SG transferred cash in the amount of US$11,580,082 to Bgin HK, US$74,200,000 to Bgin Singapore, US$4,000,000 to Bgin Infrastructure, US$50,000 to Bgin EU, US$24,709,412 to Bgin Mining, and US$1,002,523 to the Company, (vi) Bgin Management transferred cash in the amount of US$2,321,384 to Bgin HK, US$500 to Bgin Singapore, and US$3,095,000 to Bgin Infrastructure, (vii) Bgin Mining transferred cash in the amount of US$605,806 to Bgin HK, US$300,000 to Bgin Management, and US$24,709,412 to Bgin SG, (viii) Bgin Trade transferred cash in the amount of US$1,049,996 to Bgin HK, US$20,016 to Bgin Singapore, US$6,230 to Bgin Infrastructure, and US$356,505 to Bgin Mining, (ix) the Company transferred cash in the amount of US$520,000 to Bgin Field, US$1,379,686 to Bgin Infrastructure, US$14,388,906 to Bgin SG, US$58,047 to Bgin Chip, US$4,070,489 to Bgin Singapore, US$2,900,181 to Bgin HK, and US$3,420,000 to Bgin Rig, (x) Bgin Chip transferred cash in the amount of US$39,937 to Bgin HK, US$314,013 to Bgin Trading, and US$800,100 to Bgin Infrastructure, (xi) Bgin Field transferred cash in the amount of US$500,000 to Bgin HK, and US$2,900,000 to Bgin SG, (xii) Bgin Rig transferred cash in the amount of US$500,000 to Bgin Infrastructure. From January 1, 2026 to the date of this annual report, (i) Bgin Trading transferred a cash dividend in the amount of US$127,400,000 to Bgin Rig, (ii) Bgin Rig transferred a cash dividend in the amount of US$118,000,000 to the Company, (iii) the Company injected capital in the amount of US$118,000,000 into Bgin Field, (iv) Bgin Field injected capital in the amount of US$100,000,000 into Bgin Mining and US$18,000,000 into Bgin Infrastructure US, (v) Bgin Trading transferred cash in the amount of US$164,985 to Bgin HK, US$2,000,000 to Bgin Singapore, US$600,000 to Bgin Mining, US$500,000 to Bgin SG, and US$400,000 to the Company, (vi) Bgin Chip transferred cash in the amount of US$1,000,000 to Bgin Trading, (vii) Bgin HK transferred cash in the amount of US$12,600 to Bgin Chip, US$21,500 to Bgin Management, US$900,000 to Bgin SG, US$24,618,002 to Bgin Trading, and US$40,000 to the Company, (viii) Bgin Singapore transferred cash in the amount of US$29,139,021 to Bgin Trading, (ix) Bgin SG transferred cash in the amount of US$6,608,002 to Bgin HK, US$481,235 to Bgin Singapore, and US$500,000 to the Company, (x) Bgin Management transferred cash in the amount of US$450,000 to Bgin SG, (xi) Bgin Mining transferred cash in the amount of US$25,579,832 to Bgin SG, (xii) Bgin Infrastructure US transferred cash in the amount of US$18,000,000 to Bgin HK, and US$51,618,096 to Bgin Trading.

4

On January 13, 2024, the board of directors of Bgin Trading declared a dividend with an aggregate amount of US$17,005,000, payable in USDT coins to Bgin Rig, which has been paid to Bgin Rig in full. On January 14, 2024, the sole director of Bgin Rig declared a dividend with an aggregate amount of US$17,000,000, payable in USDT coins to the Company, which has been paid to the Company in full. On January 15, 2024, our board of directors declared a final dividend with an aggregate amount of US$5,000,000, payable in USDT coins to our shareholders of record as of December 31, 2023, to be paid on or before February 29, 2024. As of February 2024, all of the US$5,000,000 of declared dividend had been paid. On March 12, 2024, our board of directors passed resolutions reclassifying the dividend as an interim dividend rather than a final dividend. On March 15, 2024, our shareholders unanimously passed written resolutions ratifying, approving and confirming in all respects the reclassification by the board of directors of the dividend as an interim dividend rather than a final dividend.

On June 2, 2025, the board of directors of Bgin Trading declared a dividend with an aggregate amount of US$5,005,000, payable in USDT coins to Bgin Rig, which has been paid to Bgin Rig in full. On June 3, 2025, the sole director of Bgin Rig declared a dividend with an aggregate amount of US$5,000,000, payable in USDT coins to the Company, which has been paid to the Company in full. On June 6, 2025, our board of directors recommended a final dividend with an aggregate amount of US$5,000,000 be declared by ordinary resolution of the shareholders of the Company and that any such dividend declared by the shareholders of the Company be settled in cash. On June 21, 2025, our board of directors passed further resolutions updating the recommendation of June 6, 2025, to recommend that a final dividend with an aggregate amount of US$5,000,000 be declared by ordinary resolution of the shareholders of the Company and that any such dividend declared by the shareholders of the Company be settled in cash or by a distribution in specie of USDT coins, in each case at the sole discretion of the shareholder entitled to payment of the said final dividend. On June 21, 2025, our board of directors passed resolutions recommending that a final dividend with an aggregate amount of US$5,000,000 be declared by ordinary resolution of the shareholders of the Company, and that any such dividend declared by the shareholders of the Company be settled either in cash or by a distribution in specie of USDT coins, in each case at the sole discretion of the shareholders entitled to payment of the said final dividend, to our shareholders of record as of December 31, 2024. On June 23, 2025, our shareholders unanimously passed written resolutions declaring a final dividend with an aggregate amount of US$5,000,000 to be paid, at the election of each relevant shareholder, in either cash or by a distribution in specie of USDT coins. As of June 30, 2025, all US$5,000,000 of the declared final dividend had been paid to the shareholders, among which US$949,000 was paid in USDT coins.

On February 6, 2026, Bgin Rig declared and made a dividend of US$118,000,000 to the Company. On February 13, 2026, the Company resolved to transfer the sum of the aforementioned dividend to Bgin Field by way of capital contribution. The Company transferred monies by way of capital contribution to Bgin Field in three tranches separately on March 4, 2026, March 9, 2026, and March 14, 2026. Notwithstanding the Company’s prior resolution to transfer the sum by way of capital contribution, the Company was issued 59,000,000 ordinary shares of a single class with a par value of US$2.00 each in the capital of Bgin Field, in consideration of the receipt of the sum of US$118,000,000 from the Company. Bgin Field subsequently injected capital in the amount of US$100,000,000 into Bgin Mining and US$18,000,000 into Bgin Infrastructure US.

On April 17, 2026, Bgin Rig injected capital in the amount of S$25,000,000 (approximately US$19,590,941) into Bgin SG.

As of the date of this annual report, no other dividend declarations have been made by our board of directors or by a subsidiary to the Company. For a discussion of the risks in connection with distributing USDT coins to our shareholders as dividends, see “Item 3. Key Information—D. Risk Factors — Risks Related to Our Business and Industry — If USDT were to be deemed a “security” under the Securities Act, we might have liabilities arising out of a possible violation of Section 5 of the Securities Act in connection with our distributions of dividends to shareholders in the form of USDT coins and our compensation payments to certain service providers in USDT.” Our board of directors has complete discretion on whether to distribute dividends, subject to applicable laws. See “Item 3. Key Information—D. Risk Factors — Risks Related to Our Class A ordinary shares — We may or may not pay dividends in the foreseeable future, and any future determination related to our dividend policy will be made at the discretion of our board of directors. In the event that our board of directors does not declare any dividends, you must rely on price appreciation of our Class A ordinary shares for return on your investment” and our consolidated financial statements and notes for the fiscal years ended December 31, 2025, 2024 and 2023 included elsewhere in this annual report. Subject to certain contractual, legal and regulatory restrictions, cash and capital contributions may be transferred among our Cayman Islands holding company and its subsidiaries.

5

Under the current practice of the Inland Revenue Department of Hong Kong, generally no tax is payable in Hong Kong in respect of dividends paid by us on the Class A ordinary shares. As of the date of this annual report, there are no restrictions or limitation under the laws of Hong Kong imposed on the conversion of Hong Kong dollars into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S. investors.

Bgin and our subsidiaries may from time to time declare or pay dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Summary of Risk Factors

Investing in our securities involves significant risks. You should carefully consider all of the information in this annual report before investing in our securities. Below is a summary of the principal risks we face. These risks are discussed more fully under “Item 3. Key Information—D. Risk Factors.”

Risks Related to Doing Business in Hong Kong (for a more detailed discussion, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in Hong Kong”)

A portion of our operations are conducted in Hong Kong through Bgin HK, Bgin Trading, Bgin Trade HK and Bgin Chip, our Hong Kong subsidiaries, and therefore, we face risks arising from the legal system in Hong Kong and Mainland China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with little advance notice. In addition, the Chinese government has intervened and may continue to intervene or influence our operations at any time or may exert more oversight and control over offerings conducted overseas and/or foreign investment in Hong Kong based issuers, which could result in a material change in our operations and/or the value of our Class A ordinary shares. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in Hong Kong-based issuers could significantly limit or completely hinder our ability to offer or continue to offer our securities to investors and cause the value of such securities to significantly decline or be worthless. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong and Mainland China.”

If we do not receive or maintain the approvals, or we inadvertently conclude that such approvals are not required, or applicable laws, regulations, or interpretations change such that we are required to obtain approval in the future, we may be subject to an investigation by competent regulators, fines or penalties, ordered to suspend our relevant business and rectify, prohibited from engaging in relevant business, or subject to an order prohibiting us from conducting an offering, and these risks could result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors or cause such securities to significantly decline in value or become worthless. For details, see “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong.”

6

In general, we face risks and uncertainties relating to doing business in Hong Kong, including, but not limited to, the following:

| ● | As of the date of this annual report, through our Hong Kong subsidiaries, we maintain service or freelancer agreements with 52 PRC individuals, including our officer, Mr. Pengju Wang, who is based in Mainland China, and provides services to us. The service relationship between our Hong Kong subsidiaries and such PRC citizens does not constitute a labor relationship which refers to a relationship between domestic enterprises and employees under the PRC Labor Law. As a result of this relationship, we may be subject to arbitration or litigation filed by such service providers or required to adjust such form of services in the future. (see page 12 of this annual report); |

| ● | The compensation to the PRC service providers who entered into service or freelancer agreements with Bgin HK is paid through one or more of the following methods: (i) in Renminbi by Bgin HK through a third-party payment institution, which exchanges the U.S. dollars received from Bgin HK for Renminbi; (ii) in USDT transferred directly from Bgin HK’s cold wallet to the relevant individual; or (iii) in Hong Kong dollars by Bgin HK to such individuals’ bank accounts in Hong Kong. In addition, prior to July 2023, Shenzhen Bgin, an affiliated entity of ours, was responsible for engaging with third-party production partners on behalf of Bgin HK. The payment to third-party suppliers was first made by Shenzhen Bgin in Renminbi, and then Bgin HK reimbursed Shenzhen Bgin through a third-party payment institution, which exchanged the U.S. dollars received from Bgin HK for Renminbi. If the third-party payment institution providing service for us fails to hold the relevant licenses for cross-border payment business, we shall have to make arrangements with other qualified third-party payment institutions or otherwise make the cross-border payment through a bank. (see page 12 of this annual report); |

| ● | The PRC government’s significant authority to intervene in or influence the China operations of an offshore holding company at any time could limit our ability to transfer or use our cash outside of China and limit our ability to transfer cash both into and outside of China, including Hong Kong, and otherwise result in material adverse change in our operations and the value of our Class A ordinary shares. (see page 13 of this annual report); |

| ● | Uncertainties arising from the legal system in Mainland China, including uncertainties regarding the interpretation and enforcement of laws in Mainland China and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause the Class A ordinary shares to significantly decline in value or become worthless. (see page 13 of this annual report); |

| ● | The Holding Foreign Companies Accountable Act calls for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, and on December 29, 2022, the Consolidated Appropriations Act was signed into law. The Consolidated Appropriations Act contained, among other things, an identical provision to Accelerating Holding Foreign Companies Accountable Act, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the Holding Foreign Companies Accountable Act from three years to two, thus reducing the time period before our securities may be prohibited from trading or delisted. The delisting of our Class A ordinary shares, or the threat of their being delisted, may materially and adversely affect the value of your investment in the future. Our current and former auditors are subject to PCAOB inspections and PCAOB are able to inspect our current and former auditors, and they are not subject to the determinations announced by the PCAOB on December 16, 2021. On August 26, 2022, the CSRC, the MOF and the PCAOB signed the Protocol, governing inspections and investigations of audit firms based in China and Hong Kong. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control. The PCAOB is continuing to demand complete access in mainland China and Hong Kong moving forward and is already resuming regular inspections, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has indicated that it will act immediately to consider the need to issue new determinations with the Holding Foreign Companies Accountable Act if needed and does not have to wait another year to reassess its determinations. Our securities may be delisted or prohibited from trading if the PCAOB determines that it cannot inspect or investigate completely our auditor under the Holding Foreign Companies Accountable Act. (see page 14 of this annual report); |

7

| ● | Failure to comply with cybersecurity, data privacy, data protection, or any other laws and regulations related to data may materially and adversely affect our business, financial condition, and results of operations. (see page 14 of this annual report); |

| ● | If we were to be required to obtain any permission or approval from or complete filings with the CSRC, the CAC, or other PRC authorities in connection with our follow-on offerings under PRC law, we may be fined or subject to other sanctions, and our business, reputation financial condition, and results of operations may be materially and adversely affected. (see page 17 of this annual report); |

| ● | It may be difficult for overseas shareholders and/or regulators to conduct investigations or collect evidence within the territory of China, including Hong Kong. (see page 18 of this annual report); |

| ● | You may incur additional costs and procedural obstacles in effecting service of legal process, enforcing foreign judgments or bringing actions in Mainland China/Hong Kong against us or our management based on Mainland China/Hong Kong laws. (see page 19 of this annual report); |

| ● | The enactment of Law of the PRC on Safeguarding National Security in Hong Kong (the “Hong Kong National Security Law”) and the enactment of Safeguarding National Security Ordinance in Hong Kong (the “Hong Kong National Security Ordinance”) could impact our Hong Kong subsidiaries. (see page 19 of this annual report); |

| ● | The Hong Kong legal system embodies uncertainties which could limit the availability of legal protections. (see page 20 of this annual report); and |

| ● | There are some political risks associated with conducting business in Hong Kong. (see page 20 of this annual report). |

In general, any risks related to doing business in Mainland China also apply to doing business in Hong Kong. Uncertainties arising from the legal system in the PRC, including Hong Kong, in which uncertainties regarding the interpretation and enforcement of laws and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our Class A ordinary shares to significantly decline in value or become worthless. See “Item 3. Key Information—D. Risk Factors — Risks Related to Doing Business in Hong Kong.”

Risks Relating to Doing Business in Singapore (for a more detailed discussion, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in Singapore”)

We are subject to risks and uncertainties relating to doing business in Singapore, which include without limitation the following:

| ● | We are subject to the laws of Singapore, which differ in certain material respects from the laws of the United States. (see page 21 of this annual report); |

8

| ● | We are subject to risks associated with operating in rapidly evolving Southeast Asia region, and we might therefore be exposed to various risks inherent in operating and investing in the region. (see page 21 of this annual report); |

| ● | Adverse changes in government regulations in Singapore may materially and adversely affect our operations and financial condition. (see page 22 of this annual report); |

| ● | The ability of our subsidiaries in Singapore to distribute dividends to us may be subject to restrictions under applicable laws. (see page 22 of this annual report); and |

| ● | It is not certain if the Company will be classified as a Singapore tax resident. (see page 22 of this annual report). |

Risks Relating to Our Business and Industry (for a more detailed discussion, see “Item 3. Key Information—D. Risk Factors— Risks Relating to Our Business and Industry”)

We are subject to risks and uncertainties relating to our business and industry, which include without limitation the following:

| ● | We have a limited operating history and have grown significantly in a short period of time. If we fail to manage our growth effectively, our business could be materially adversely affected. (see page 23 of this annual report); |

| ● | Our business operations are heavily dependent upon the stability and popularity of KAS coins and ALEO coins. (see page 24 of this annual report); |

| ● | Our business operations are subject to special risks with respect to the KAS blockchain and the ALEO blockchain. (see page 24 of this annual report); |

| ● | Our mining machines exported from Asia to the United States may be subject to the additional tariffs recently imposed by the U.S. government on certain products imported from China, which could adversely affect our supply chain, cost structure, and results of operations. (see page 25 of this annual report); |

| ● | There is no assurance that cryptocurrencies will maintain their long-term value and volatility in the market price of cryptocurrencies may adversely affect our business and results of operations. (see page 26 of this annual report); |

| ● | Bankruptcies and financial distress among cryptocurrency market participants, including the bankruptcy of FTX, a large cryptocurrency exchange, have caused widespread disruption in these markets and have negatively impacted our business operations, results of operations and financial condition. (see page 26 of this annual report); |

| ● | We use payment platforms to receive cash exchanged from Tethers and to make payments to our suppliers and other business partners. Such practice could expose us to substantial risks. (see page 27 of this annual report); |

| ● | We may experience reputational harm if disruption in the cryptocurrency markets occurs. (see page 27 of this annual report); |

| ● | If our policies and procedures surrounding the safeguarding of cryptocurrencies, conflicts of interest, or comingling of assets fail, we may be subject to risks of loss of assets and damaged reputation, which could negatively affect our business, financial position, and results of operations. (see page 28 of this annual report); |

9

| ● | If USDT were to be deemed a “security” under the Securities Act, we might have liabilities arising out of a possible violation of Section 5 of the Securities Act in connection with our distributions of dividends to shareholders in the form of USDT coins and our compensation payments to certain service providers in USDT. (see page 29 of this annual report); |

| ● | We have identified deficiencies in our risk management processes and policies in light of current cryptocurrency market conditions and plan to adopt changes to address these deficiencies. Nevertheless, if our risk management process and policies are still inadequate to protect our assets, we may experience material loss and our business, financial condition and results of operations may be adversely affected. (see page 31 of this annual report); |

| ● | Disruptions in the cryptocurrency markets have caused and may continue to cause price declines and volatilities in cryptocurrencies. Additionally, prices of cryptocurrencies are volatile in nature, including those of the cryptocurrencies we mine. We adjust our mining strategy primarily based on the overall rate of return. The rate of return for mining a particular type of cryptocurrency typically depends upon a few crucial factors, including its trading price, mining difficulty, and the hash rate it takes to mine a unit of such cryptocurrency. An increase in a cryptocurrency’s trading price attracts more miners, and leads to an increase in mining difficulty of such cryptocurrency. As the cryptocurrency market is volatile in nature, we monitor the trading prices of alternative cryptocurrencies on a constant basis, and adjust the mining ratios of different types of cryptocurrencies on a daily basis to maximize the overall rate of return. However, in the event that the prices of cryptocurrencies our subsidiaries mine decrease, we may not be able to achieve the optimal rate of return or any return at all, and our financial position and results of operations may suffer as a result. (see page 32 of this annual report); |

| ● | We are subject to regulatory risks with regard to mining, holding, using, or transferring cryptocurrencies, which could negatively affect our business, results of operations and financial position. (see page 33 of this annual report); |

| ● | Erosion or loss of user confidence in cryptocurrencies could adversely impact our business, results of operations and financial condition. (see page 34 of this annual report); |

| ● | Producing new mining machines and obtaining machine components for such production has historically been capital intensive, and is likely to continue to be very capital intensive, which may have a material and adverse effect on our business and results of operations. (see page 34 of this annual report); |

| ● | Our subsidiaries source a substantial portion of the components for their mining machines from a major supplier and, historically, have depended on one manufacturer for their miners, making them vulnerable to supply disruption and price fluctuation. (see page 35 of this annual report); |

| ● | We rely on a steady and inexpensive power supply for operating mining farms and running mining machines. Failure to access large quantities of power at reasonable costs could significantly increase our expense related to certain businesses and adversely affect our business and results of operations. (see page 36 of this annual report); |

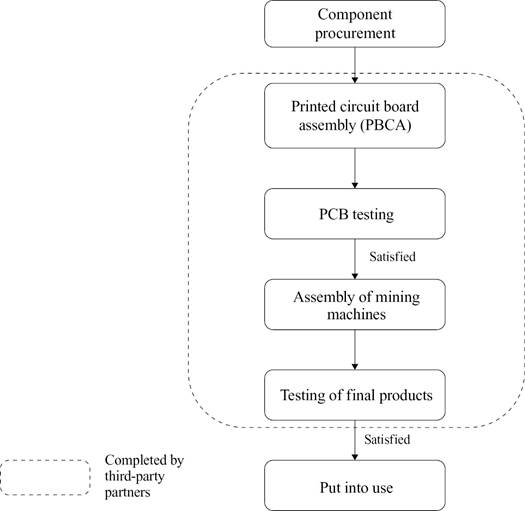

| ● | The quality of our subsidiaries’ mining machines relies on third-party production partners that we maintain business relationships with. Any failure by such third-party production partners to manufacture mining machines with high quality could materially and adversely affect our business, financial condition and results of operations. (see page 37 of this annual report); |

| ● | Our subsidiaries do not maintain long-term contracts with most of their suppliers. If our subsidiaries are unable to source from their current suppliers and unable to find acceptable substitutes at reasonable costs or at all, our production costs may increase and our business and results of operations may be materially and adversely affected. (see page 37 of this annual report); |

10

| ● | Changes in market conditions, including the competitive environment, may restrict our ability to price our mining machines and our services at our desired margins or sell our mining machines. (see page 44 of this annual report); |

| ● | If we fail to maintain an effective quality control system, our business could be materially and adversely affected. (see page 44 of this annual report); and |

| ● | Product defects resulting in a large-scale product recall or product liability claims against us could materially and adversely affect our business, results of operations and reputation. (see page 44 of this annual report). |

Risks Related to the Regulatory Framework

We are subject to risks and uncertainties relating to the regulatory framework, which include without limitation the following:

| ● | We invest a significant portion of our crypto assets in crypto short-term investments, if such crypto short-term investments or the cryptocurrencies we mine were deemed to be “investment securities”, we may inadvertently violate the Investment Company Act. We could incur significant losses in modifying our operations to avoid the need to register as an investment company or could incur significant expenses to register as an investment company or could terminate operations altogether. (see page 48 of this annual report); |

| ● | We may be required to register as an investment company under the 1940 Act, in which event, we may be deemed to be operating as an unregistered investment company in violation of the 1940 Act and required to either register as an investment company or to adjust our business strategies. (see page 49 of this annual report); |

| ● | If a regulator with jurisdiction on our activities concludes that we improperly characterized a cryptocurrency, we may be subject to regulatory scrutiny, inquiries, investigations, fines, and other penalties, which may adversely affect our business, operating results, and financial condition. (see page 49 of this annual report); |

| ● | Regulatory developments related to cryptocurrencies and cryptocurrency markets may impact our business, financial condition, and results of operations. (see page 52 of this annual report); and |

| ● | If U.S. and/or foreign regulators and other governmental authorities, including the Chinese government, assert jurisdiction over cryptocurrencies and cryptocurrency markets, we may become subject to additional regulations imposed by such regulators and governmental authorities and may be required to alter our business operations in order to achieve compliance therewith, which could result in increased compliance costs and could materially and adversely affect our business operations, financial position, and results of operations. (see page 53 of this annual report). |

Risks Related to Our Class A Ordinary Shares

We are subject to risks and uncertainties relating to our Class A ordinary shares, which include without limitation the following:

| ● | The trading price of our Class A ordinary shares is likely to be volatile, which could result in substantial losses to investors. (see page 53 of this annual report); |

| ● | If securities or industry analysts cease to publish research or reports about our business, or if they adversely change their recommendations regarding the Class A ordinary shares, the market price for the Class A ordinary shares and trading volume could decline. (see page 55 of this annual report); and |

11

| ● | We may or may not pay dividends in the foreseeable future, and any future determination related to our dividend policy will be made at the discretion of our board of directors. In the event that our board of directors does not declare any dividends, you must rely on price appreciation of our Class A ordinary shares for return on your investment. (see page 55 of this annual report). |

We also face other challenges, risks and uncertainties that may materially adversely affect our business, financial condition, results of operations and prospects. You should consider the risks discussed in “Item 3. Key Information—D. Risk Factors” and elsewhere in this annual report before investing in our Class A ordinary shares.

Risks Related to Doing Business in Hong Kong and Mainland China

Through our Hong Kong subsidiaries, we maintain service or freelancer agreements with PRC individuals, including our officer, Mr. Pengju Wang, who is based in Mainland China and provides services to us. Such service relationship does not constitute a labor relationship under the PRC laws and the service providers are unable to enjoy the protection under the PRC Labor Law and other related regulations, as a result of which we may be subject to arbitration or litigation filed by such service providers or required to adjust such form of services in the future.

As of the date of this annual report, through our Hong Kong subsidiaries, we maintained service or freelancer agreements with 52 PRC individuals, including our officer, Mr. Pengju Wang, who is based in Mainland China and provides services to us. The service relationship between our Hong Kong subsidiaries and such PRC citizens does not constitute a labor relationship which refers to a relationship between enterprises in mainland China and employees under the PRC Labor Law but rather a civil legal relationship of the provision and receipt of services under the PRC laws, as a result of which, we are not required to pay social insurance premiums and housing provident funds for such PRC individuals. Currently, there are no explicit regulations under the PRC laws that apply to or restrict the provision of services by PRC individual in mainland China to a Hong Kong company. However, if these PRC individuals believe that they have a substantial labor relationship under the PRC laws with Bgin HK, they may initiate labor arbitration or litigation against Bgin HK for compensation alleging their inability to enjoy the protection of the PRC Labor Law and such other related regulations of mainland China. In addition, we cannot assure you that this form of service provision will not be regulated by new legislation in the PRC in the future and then we may be required to make further adjustments to this kind of business service practice. Any such events may result in substantial and unexpected expenditures and could materially and adversely affect our business, financial condition, and results of operations.

The compensation to the PRC service providers and procurement and service fees to our affiliated entity are and were paid through one or more of the following methods: (i) in Renminbi by Bgin HK through a third-party payment institution; (ii) in USDT transferred directly from Bgin HK’s cold wallet to the relevant individual; or (iii) in Hong Kong dollars by Bgin HK to such individuals’ bank accounts in Hong Kong. If the third-party payment institution providing service for us fails to hold the relevant licenses for cross-border payment business, we shall have to make arrangements with other qualified third-party payment institutions or otherwise make the cross-border payments through a bank.

The compensation to the PRC service providers who entered into service or freelancer agreements with Bgin HK is paid through one or more of the following methods: (i) in Renminbi by Bgin HK through a third-party payment institution, which exchanges the U.S. dollars received from Bgin HK for Renminbi; (ii) in USDT transferred directly from Bgin HK’s cold wallet to the relevant individual; or (iii) in Hong Kong dollars by Bgin HK to such individuals’ bank accounts in Hong Kong. In addition, prior to July 2023, Shenzhen Bgin, an affiliated entity of ours, was responsible for engaging with third-party production partners on behalf of Bgin HK. The payment to third-party suppliers was first made by Shenzhen Bgin in Renminbi, and then Bgin HK reimbursed Shenzhen Bgin through a third-party payment institution, which exchanged the U.S. dollars received from Bgin HK for Renminbi.

According to the Regulation on Supervision and Administration of Non-bank Payment Institutions issued by the State Council on November 24, 2023 and effective on May 1, 2024, and the Implementation Rules for the Regulations on Supervision and Administration of Non-Bank Payment Institutions issued by the People’s Bank of China, or PBOC, on July 9, 2024 and effective on the same day, non-financial institutions are required to obtain the Payment Business License for their payment services. Furthermore, payment institutions may only conduct foreign exchange business after going through the formalities for the registration in the directory of trade foreign exchange receipt and payment enterprises (“Directory Registration”) pursuant to the Administrative Measures for the Foreign Exchange Business of Payment Institutions promulgated by the State Administration of Foreign Exchange (“SAFE”) on April 29, 2019 and effective on the same day. Therefore, third-party payment institutions shall not be permitted to provide cross-border payment services unless they obtain the Payment Business License and complete the Directory Registration. We cannot assure you that the third-party payment institution providing payment services for us could obtain or hold the relevant cross-border payment licenses and if it fails to obtain and hold the required licenses or cooperate with other institutions with such licenses, it may be subject to a fine of up to 30% of the amount involved in the illegal conversion of foreign exchange or ordered to terminate its payment business. If this were to occur, we would have to make arrangements with other qualified third-party payment institutions or make payments to the PRC service providers and our affiliated entities through a qualified bank.

12

The PRC government’s significant authority to intervene in or influence the China operations of an offshore holding company at any time could limit our ability to transfer or use our cash outside of China and limit our ability to transfer cash both into and outside of China, including Hong Kong, and otherwise result in material adverse change in our operations and the value of our Class A ordinary shares.

Our business, prospects, financial condition, and results of operations may be influenced to a significant degree by political, economic, and social conditions in China generally. In general, any risks related to doing business in Mainland China also apply to doing business in Hong Kong. Uncertainties arising from the legal system in the PRC, including Hong Kong, in which uncertainties regarding the interpretation and enforcement of laws and the possibility that regulations and rules can change quickly with little advance notice, could hinder our ability to offer or continue to offer our securities, result in a material adverse change to our business operations, and damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our Class A ordinary shares to significantly decline in value or become worthless. See “— Risks Related to Doing Business in Hong Kong” for other risk factors relating to doing business in Hong Kong.

The PRC government has significant authority to intervene in or influence the China operations of an offshore holding company at any time as the government deems appropriate to advance regulatory and social objectives and policy positions. We cannot assure you that policies and regulations implemented by the PRC government will not be extended in the future to cover businesses operating in Hong Kong including our subsidiaries. The PRC government may also prevent us from transferring the cash we maintain in Hong Kong outside of China, or restrict our ability to deploy our cash into the Company or the ability of our Hong Kong subsidiaries to pay dividends. The PRC government may also limit our ability to transfer cash both into and outside of China, including Hong Kong. Any such action could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our subsidiaries’ business, pay dividends, or otherwise fund and conduct our subsidiaries’ business, and could result in a material adverse change to our subsidiaries’ business operations, including our Hong Kong subsidiaries’ operations, our prospects, financial condition, and results of operations, require us to seek additional permission to continue our subsidiaries’ operations, and damage our reputation, which could cause the Class A ordinary shares to significantly decline in value or become worthless. See also “— Failure to comply with cybersecurity, data privacy, data protection, or any other laws and regulations related to data may materially and adversely affect our business, financial condition, and results of operations.”