As filed with the Securities and Exchange Commission on April 24, 2026

Securities Act Registration No. 333-277580

Investment Company Act Reg. No. 811-23944

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | ☒ | |

| Pre-Effective Amendment No. __ | ☒ | |

| Post-Effective Amendment No. 7 | ☐ | |

| and/or | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | ☒ | |

| Amendment No. 9 | ☒ | |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

555 Theodore Fremd Avenue

Suite A-101

Rye, New York 10580

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: 212-922-2699

Cogency Global Inc.

850 New Burton Road

Suite 201

Dover, Delaware 19904

(Name and Address of Agent for Service)

With Copies To:

| Bo James Howell | Michael Semack |

| FinTech Law, LLC | New Age Alpha LLC |

| 6224 Turpin Hills Dr. | 555 Theodore Fremd Ave., Suite A-101 |

| Cincinnati, OH 45244 | Rye, NY 10580 |

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

It is proposed that this filing will become effective (check appropriate box)

| ☐ | immediately upon filing pursuant to paragraph (b) |

| ☒ | on April 30, 2026 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of Rule 485 |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

![]()

| NAA ALL CAP VALUE SERIES | Class S | |

| NAA LARGE CAP VALUE SERIES | Class S | |

| NAA LARGE CORE SERIES | Class S | Class L |

| NAA LARGE GROWTH SERIES | Class S | Class L |

| NAA MID GROWTH SERIES | Class S | |

| NAA SMALL CAP VALUE SERIES | Class S | |

| NAA SMALL GROWTH SERIES | Class S | |

| NAA SMID-CAP VALUE SERIES | Class S | |

| NAA WORLD EQUITY INCOME SERIES | Class S | Class L |

Managed by

New Age Alpha Advisors, LLC

(d/b/a New Age Alpha)

PROSPECTUS

For information or assistance in opening an account,

please call toll-free (833) 840-3937.

Shares of each of the Funds described in this Prospectus can be purchased by insurance company separate accounts. You can invest in Class S shares of the Funds through your purchase of a variable annuity or variable life insurance policy. You can invest in Class L shares of such Funds through your purchase of a variable life insurance policy. This Prospectus should be read along with the prospectus for the variable annuity contract or variable life insurance policy. This Prospectus has information about the Funds you should know before investing. You should read it carefully and keep it with your investment records.

The Securities and Exchange Commission has not approved or disapproved the Funds’ shares or passed on the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

TABLE OF CONTENTS

i

The NAA All Cap Value Series (the “Fund”) seeks long-term capital growth.

This table describes the fees and expenses you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and additional fees to financial intermediaries, which are not reflected in the table and example.

|

|

Class S |

| Management Fees | |

| Distribution and/or Service (12b-1) Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses | |

| Less Management Fee Reductions and/or Expense Reimbursements(1)(2) | ( |

| Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements(1)(2) |

| (1) |

|

| (2) |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the periods indicated and then redeem all your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the operating expenses remain the same, and the contractual agreement to limit expenses remains in effect through the expiration date described above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $ |

$ |

$ |

$ |

1

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or the Example, affect the Fund’s performance. During the fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was

Under normal circumstances, the Fund pursues its objective by investing at least 80% of its assets (net assets, plus the amount of any borrowings for investment purposes) in large-, mid-, and small capitalization securities that the Adviser considers having “value” characteristics. The Fund defines:

| ● | “value” as investments that appear to be undervalued relative to assets, earnings, growth potential or cash flows. |

| ● | “large-capitalization” as those companies with market capitalizations generally falling within the range of the S&P 500® Index. The capitalization range of the S&P 500® Index is between $5.3 billion and $4.2 trillion as of March 31, 2026. |

| ● | “mid-capitalization” as those companies with market capitalizations generally within the range of the S&P MidCap 400® Index. The capitalization range of the S&P MidCap 400® Index is between $1.7 billion and $28.0 billion as of March 31, 2026. |

| ● | “small-capitalization” as those companies with market capitalizations generally within the range of the S&P SmallCap 600® Index. The capitalization range of the S&P SmallCap 600® Index is between $354.8 million and $8.7 billion as of March 31, 2026. |

The Fund will primarily invest in equity securities, including common stocks, rights, real estate investment trusts (“REITs”), options, warrants, convertible debt securities of U.S. and U.S.-dollar denominated foreign issuers, and American Depositary Receipts (“ADRs”). Convertible securities are hybrid financial instruments that typically consist of bonds, debentures, or preferred shares that can be converted into a specified number of common shares of the issuing company, typically at the option of the security holder. The Fund may also invest in various investment vehicles for portfolio management purposes, such as mutual funds and exchange-traded funds (“ETFs”), including cash management and liquidity management, to obtain a higher return on collateral positions and achieve greater diversification and trading efficiency than would usually be experienced by investing directly and separately in individual securities. In selecting mutual funds and ETFs for investment, the Adviser will prioritize investments that align with and support the Fund’s overall strategy.

In selecting investments for the Fund, the Adviser uses qualitative and quantitative analysis, and other proprietary strategies to identify securities that, in combination, are expected to contribute to exceeding the total return of the S&P Composite 1500 Value Index by attempting to avoid the “losers” in the Index. The “avoid the losers” philosophy is fundamental to the underlying actuarial-like approach of the Adviser with respect to asset management. In its attempts to generate alpha, the Adviser does not aim to pick the winners; instead, it aims to avoid the losers. A loser is a company that, according to the Adviser’s investment methodology, cannot deliver revenue growth to support its stock price. The Adviser has developed a probability-based measure to identify and avoid these stocks, called the h-factor (“h-factor”), which is the foundation of the Adviser’s investment philosophy. The h-factor measures the probability a company cannot deliver the revenue growth indicated by its stock price. In buying and selling securities for the Fund, the Adviser will apply its proprietary h-factor methodology to its security selection process. H-factor uses an algorithm rooted in actuarial risk principles to construct a portfolio with exposure

2

to returns across sectors, styles, geographies, and asset classes. Using an actuarial-based approach, h-factor aims to identify underpriced and overpriced securities and assign them an h-factor score, which is the probability that the issuer will not deliver revenue growth to support the securities’ current price. Utilizing these scores, the Adviser seeks to avoid the overpriced securities and invest in the underpriced securities.

The Fund will sell investments when they no longer meet the Adviser’s investment criteria, market conditions change or to meet redemption requests.

PRINCIPAL RISKS

Market Risk. Market risk is the risk that the value of the securities in the Fund’s portfolio may decline due to daily fluctuations in the securities markets that are beyond the Adviser’s control, including fluctuations in interest rates, the quality of the Fund’s investments, economic conditions, and general equity market conditions. Certain market events could increase volatility and exacerbate market risks, such as changes in government’s economic policies, political turmoil, environmental events, trade disputes, epidemics, pandemics, or other public health issues. Turbulence in financial markets and reduced liquidity in equity, credit, and fixed-income markets may negatively affect many issuers domestically and worldwide. It can result in trading halts, any of which could hurt the Fund. During periods of market volatility, security prices (including securities held by the Fund) could fall drastically and rapidly and, therefore, adversely affect the Fund.

Large-Capitalization Company Risk. Large-capitalization companies are more mature and may be unable to respond as quickly as smaller companies to new competitive challenges, such as changes in technology and consumer tastes, and may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Mid-Capitalization Company Risk. Investments in mid-capitalization companies often involve higher risks than large-capitalization companies because these companies may lack the management experience, financial resources, product diversification, and competitive strengths of larger companies. Therefore, the securities of mid-capitalization companies may be more susceptible to market downturns and other events, and their prices may be subject to greater price fluctuations. Mid-capitalization companies are typically subject to greater earnings and changes in business prospects than larger, more established companies. Investors may not follow them widely, which can lower the demand for their stock.

Small-Capitalization Company Risk. The Fund is subject to the risk that securities of small capitalization companies may underperform other segments of the equity market or the equity market as a whole. Investing in the securities of small capitalization companies involves greater risk and the possibility of greater price volatility than investing in larger and more established companies. Because smaller companies may have inexperienced management and limited operating history, product lines, market diversification, and financial resources, the securities of these companies may be more speculative, volatile, and less liquid than the securities of larger companies. They can be particularly sensitive to expected changes in interest rates, borrowing costs and earnings, or other adverse developments.

3

Value Investing Risk. Value investing includes the risk that stocks of undervalued companies may not rise as quickly as anticipated if the market doesn’t recognize their intrinsic value or value stocks are out of favor. Value investing may be out of favor with investors occasionally, and value stocks may underperform the securities of other companies or the stock market in general.

Management Style Risk. The Adviser’s method of security selection may not be successful, and the Fund may underperform relative to its benchmark index or to other mutual funds that employ similar investment strategies. In addition, the Adviser may select investments that fail to perform as anticipated. The ability of the Fund to meet its investment objective is directly related to the success of the Adviser’s investment process, and there is no guarantee that the Adviser’s judgments about the attractiveness, value, and potential appreciation of a particular investment for the Fund will be correct or produce the desired results.

Equity Securities Risk. Equity risk is the risk that securities held by the Fund will fall due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds. Although common stocks have historically generated higher average returns than fixed-income securities over the long term, common stocks also have experienced significantly more volatility in returns. Below are additional risks related to specific equity securities the Fund invests in.

Investment Company Risk. Investing in other investment vehicles, including ETFs, closed-end funds, and other mutual funds, subjects the Fund to those risks affecting the investment vehicle, including the possibility that the value of the underlying securities held by the investment vehicle could decrease or the portfolio becomes illiquid. Moreover, the Fund and its shareholders will incur its pro rata share of the underlying vehicles’ expenses, reducing the Fund’s performance. In addition, investments in an ETF or a listed closed-end fund are subject to, among other risks, the risk that the shares may trade at a discount or premium relative to the net asset value of the shares, and the listing exchange may halt trading of the shares.

Preferred Stock Risk. Preferred stock represents an equity or ownership interest in an issuer that pays dividends at a specified rate and has precedence over common stock in paying dividends. If an issuer is liquidated or declares bankruptcy, the claims of bond owners take precedence over those who own preferred and common stock.

Convertible Securities Risk. Convertible securities may be subordinate to other securities. The total return for a convertible security depends, in part, upon the performance of the underlying security into which it can be converted. The value of convertible securities tends to decline as interest rates increase. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality.

Warrants Risk. Warrants are instruments that entitle the holder to buy an equity security at a specific price for a particular period. Warrants may be more speculative than other types of investments. The cost of a warrant may be more volatile than the price of its underlying security, and a warrant may offer more significant potential for capital appreciation and loss. A warrant ceases to have value if it is not exercised before its expiration date.

Foreign Securities Risk. Since the Fund’s investments may include ADRs, representing interests in foreign securities, the Fund is subject to risks beyond those associated with investing in domestic securities. The value of foreign securities is subject to currency fluctuations. Foreign companies are generally not subject to the same regulatory requirements as U.S. companies, resulting in less publicly available information about these companies. In addition, foreign accounting, auditing, and financial reporting standards differ from those applicable to U.S. companies. In addition, periodic U.S. Government

4

restrictions on investments in issuers from certain foreign countries may require the Fund to sell such investments at inopportune times, which could result in losses to the Fund. Below are additional risks related to specific types of foreign securities the Fund invests in.

Depositary Receipt Risk. The Fund may hold the securities of non-U.S. companies in the form of depositary receipts. The underlying securities of the depositary receipts in the Fund’s portfolio are subject to fluctuations in foreign currency exchange rates that may affect the value of the Fund’s portfolio. In addition, the value of the securities underlying the depositary receipts may change materially when the U.S. markets are not open for trading. Investments in the underlying foreign securities also involve political and economic risks distinct from those associated with investing in the securities of U.S. issuers.

REITs Risk. REITs are companies that own or finance income-producing real estate. Investments in REITs are subject to the risks associated with investing in the real estate industry, such as adverse developments affecting the real estate industry and real property values, including losses from casualty or condemnation, and changes in local and general economic conditions, supply and demand, interest rates, zoning laws, regulatory limitations on rents, property taxes, and operating expenses. The Fund’s REIT investments also subject it to management and tax risks.

Options Risk. Options and options on futures contracts give the holder of the option the right, but not the obligation, to buy (or sell) a position in a security or contract to the writer of the option at a specific price. Options are subject to correlation risk because there may be an imperfect correlation between the options and the markets for underlying instruments that could cause a given transaction to fail to achieve its objectives. The successful use of options depends on the Adviser’s ability to predict correctly future price fluctuations and the degree of correlation between the markets for options and the underlying instruments. Exchanges can limit the number of positions held or controlled by the Fund or the Adviser, thus limiting the ability to implement the Fund’s strategies. Options are also particularly subject to leverage risk and can be subject to liquidity risk.

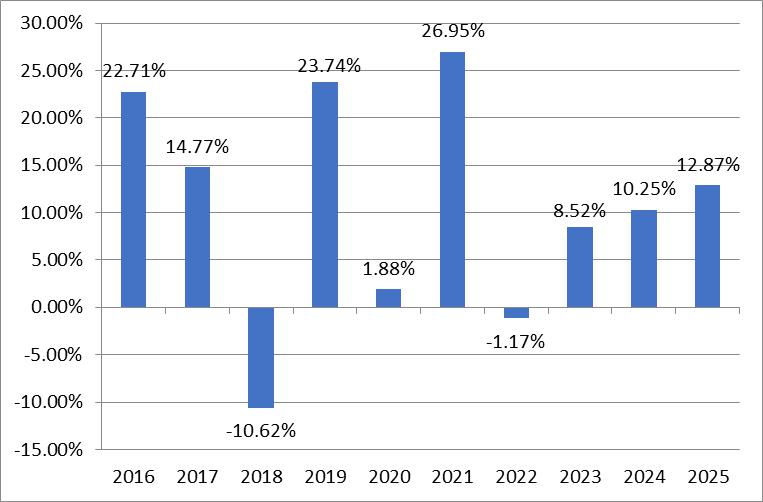

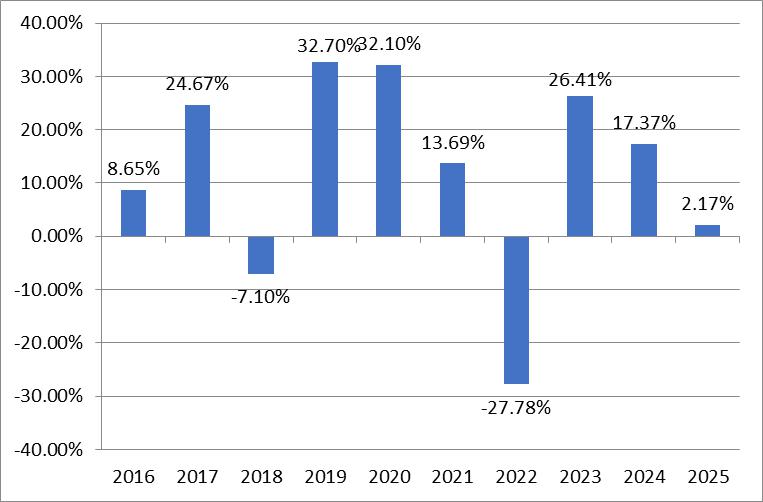

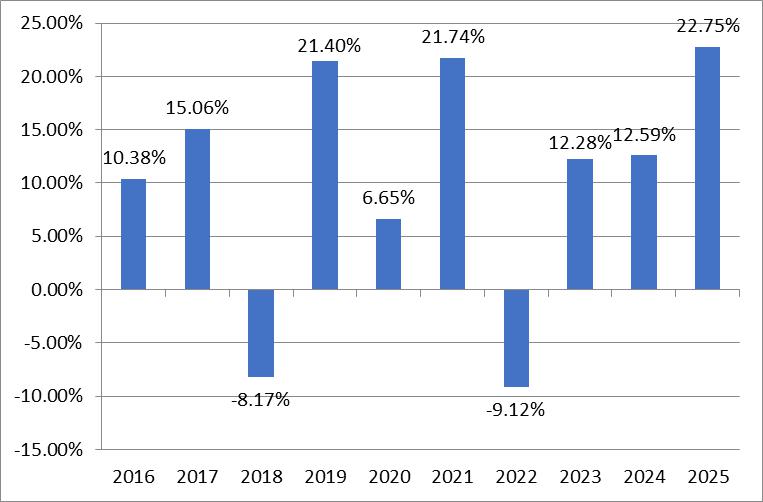

The Fund was reorganized as of the close of business on October 25, 2024, from Series O (All Cap Value Series), a series of Guggenheim Variable Funds Trust (the “Predecessor Fund”). As a result of the reorganization, the Fund is the accounting successor of the Predecessor Fund. Performance results shown in the bar chart and the performance table below for periods prior to October 25, 2024 reflect the performance of the Predecessor Fund prior to the commencement of the Fund’s operations.

5

|

During the periods shown in the chart above: |

Quarter Ended | Return |

| - |

(for periods ended December 31, 2025)

| One Year | Five Years | 10 Years | |

| NAA All Cap Value Series | |||

| S&P Composite 1500 Value Index ( |

MANAGEMENT OF THE FUND

New Age Alpha Advisors, LLC (d/b/a New Age Alpha) is the Fund’s investment adviser.

|

Portfolio Managers |

Investment Experience with the Fund |

Primary Title with Adviser |

| Armen Arus | Portfolio Manager since inception | Chief Executive Officer |

| Julian Koski | Portfolio Manager since inception | Chief Investment Officer |

| Hugo Chang | Portfolio Manager since inception | Head of Research |

| Konstantin Tourevski | Portfolio Manager since inception | Managing Partner |

| Burak Hurmeydan | Portfolio Manager of the Fund since inception and of the Predecessor Fund since 2018 | Head of Quantitative Strategies |

| Gennadiy Khayutin | Portfolio Manager since April 2025 | Managing Partner |

6

PURCHASE AND SALE OF FUND SHARES

You may purchase shares of the Fund only through variable annuity contracts or variable life insurance policies offered by participating insurance companies. Fund shares are not offered directly to the public.

You should refer to the Prospectus for the variable annuity contract or variable life insurance policy for information on how to purchase a variable contract or policy and select the Fund as an investment option for your contract or policy.

You may redeem shares of the Fund only through participating insurance companies.

We redeem shares of the Fund on any business day when the New York Stock Exchange (“NYSE”) is open. The price at which the Fund will redeem a share will be its NAV next determined after the order is considered received. The Fund has authorized the participating insurance companies to accept redemption requests on its behalf.

TAX INFORMATION

The dividends and distributions paid by the Fund to the insurance company’s separate accounts will consist of ordinary income, capital gains, or some combination of both. Because shares of the Fund must be purchased through separate accounts used to fund variable insurance contracts, such dividends, and distributions will be exempt from current taxation by contract holders if left to accumulate within a separate account. Withdrawals from such contracts may be subject to ordinary income tax and, if made before age 59½, a 10% penalty tax. Investors should ask their tax advisors for more information on their tax situation, including possible state or local taxes. Refer to the Prospectus of your insurance company’s separate account for a discussion of the tax status of your variable contract.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

The Fund’s shares are generally available only through participating insurance companies offering variable annuity contracts and variable life insurance policies. A broker-dealer or other financial intermediary generally purchases life insurance policies and variable annuities. The Fund and/or its related companies may pay the participating insurance companies for services; some payments may go to broker-dealers and other intermediaries. These payments may create a conflict of interest for an intermediary or be a factor in the participating insurance companies’ decision to include the Fund as an underlying investment option in a variable contract. Ask your salesperson or visit your financial intermediary’s website for more information.

7

The NAA Large Cap Value Series (the “Fund”) seeks long-term capital growth.

This table describes the fees and expenses you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and additional fees to financial intermediaries, which are not reflected in the table and example.

|

|

Class S |

| Management Fees | |

| Distribution and/or Service (12b-1) Fees | |

| Other Expenses | |

| Total Annual Fund Operating Expenses | |

| Less Management Fee Reductions and/or Expense Reimbursements(1)(2) | ( |

| Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements(1)(2) |

| (1) |

|

| (2) |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the periods indicated and then redeem all your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the operating expenses remain the same, and the contractual agreement to limit expenses remains in effect through the expiration date described above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $ |

$ |

$ |

$ |

8

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or the Example, affect the Fund’s performance. During the fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was

Under normal circumstances, the Fund pursues its objective by investing at least 80% of its assets (net assets, plus the amount of any borrowings for investment purposes) in large-capitalization securities that the Adviser considers having “value” characteristics. The Fund defines:

| ● | “value” as investments that appear to be undervalued relative to assets, earnings, growth potential or cash flows. |

| ● | “large-capitalization” as those companies with market capitalizations generally falling within the range of the S&P 500® Index. The capitalization range of the S&P 500® Index is between $5.3 billion and $4.2 trillion as of March 31, 2026. |

The Fund will primarily invest in equity securities, including common stocks, rights, real estate investment trusts (“REITs”), options, warrants, convertible debt securities of U.S. and U.S. dollar-denominated foreign issuers, and American Depositary Receipts (“ADRs”). Convertible securities are hybrid financial instruments that typically consist of bonds, debentures, or preferred shares that can be converted into a specified number of common shares of the issuing company, typically at the option of the security holder.

The Fund may also invest in various investment vehicles for portfolio management purposes, such as mutual funds and exchange-traded funds (“ETFs”), including cash management and liquidity management, to obtain a higher return on collateral positions and achieve greater diversification and trading efficiency than would usually be experienced by investing directly and separately in individual securities. In selecting mutual funds and ETFs for investment, the Adviser will prioritize investments that align with and support the Fund’s overall strategy.

In selecting investments for the Fund, the Adviser uses qualitative and quantitative analysis, and other proprietary strategies to identify securities that, in combination, are expected to contribute to exceeding the total return of the S&P 500 Value Index by attempting to avoid the “losers” in the Index. The “avoid the losers” philosophy is fundamental to the underlying actuarial-like approach of the Adviser with respect to asset management. In its attempts to generate alpha, the Adviser does not aim to pick the winners; instead, it aims to avoid the losers. A loser is a company that, according to the Adviser’s investment methodology, cannot deliver revenue growth to support its stock price. The Adviser has developed a probability-based measure to identify and avoid these stocks, called the h-factor (“h-factor”), which is the foundation of the Adviser’s investment philosophy. The h-factor measures the probability a company cannot deliver the revenue growth indicated by its stock price. In buying and selling securities for the Fund, the Adviser will apply its proprietary h-factor methodology to its security selection process. H-factor uses an algorithm rooted in actuarial risk principles to construct a portfolio with exposure to returns across sectors, styles, geographies, and asset classes. Using an actuarial-based approach, h-factor aims to identify underpriced and overpriced securities and assign them an h-factor score, which is the probability that the issuer will not deliver revenue growth to support the securities’ current price. Utilizing these scores, the Adviser seeks to avoid the overpriced securities and invest in the underpriced securities.

The Fund will sell investments when they no longer meet the Adviser’s investment criteria, market conditions change, or to meet redemption requests.

9

PRINCIPAL RISKS

Market Risk. Market risk is the risk that the value of the securities in the Fund’s portfolio may decline due to daily fluctuations in the securities markets that are beyond the Adviser’s control, including fluctuations in interest rates, the quality of the Fund’s investments, economic conditions, and general equity market conditions. Certain market events could increase volatility and exacerbate market risks, such as changes in government’s economic policies, political turmoil, environmental events, trade disputes, epidemics, pandemics, or other public health issues. Turbulence in financial markets and reduced liquidity in equity, credit, and fixed-income markets may negatively affect many issuers domestically and worldwide. It can result in trading halts, any of which could hurt the Fund. During periods of market volatility, security prices (including securities held by the Fund) could fall drastically and rapidly and, therefore, adversely affect the Fund.

Large-Capitalization Company Risk. Large-capitalization companies are more mature and may be unable to respond as quickly as smaller companies to new competitive challenges, such as changes in technology and consumer tastes, and may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Value Investing Risk. Value investing includes the risk that stocks of undervalued companies may not rise as quickly as anticipated if the market doesn’t recognize their intrinsic value or value stocks are out of favor. Value investing may be out of favor with investors occasionally, and value stocks may underperform the securities of other companies or the stock market in general.

Management Style Risk. The Adviser’s method of security selection may not be successful, and the Fund may underperform relative to its benchmark index or to other mutual funds that employ similar investment strategies. In addition, the Adviser may select investments that fail to perform as anticipated. The ability of the Fund to meet its investment objective is directly related to the success of the Adviser’s investment process, and there is no guarantee that the Adviser’s judgments about the attractiveness, value, and potential appreciation of a particular investment for the Fund will be correct or produce the desired results.

Equity Securities Risk. Equity risk is the risk that securities held by the Fund will fall due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds. Although common stocks have historically generated higher average returns than fixed-income securities over the long term, common stocks also have experienced significantly more volatility in returns. Below are additional risks related to specific equity securities the Fund invests in.

Investment Company Risk. Investing in other investment vehicles, including ETFs, closed-end funds, and other mutual funds, subjects the Fund to those risks affecting the investment vehicle, including the possibility that the value of the underlying securities held by the investment vehicle could decrease or the portfolio becomes illiquid. Moreover, the Fund and its shareholders will incur its pro rata share of the underlying vehicles’ expenses, reducing the Fund’s performance. In addition, investments in an ETF or a listed closed-end fund are subject to, among other risks, the risk that the shares may trade at a discount or premium relative to the net asset value of the shares, and the listing exchange may halt trading of the shares.

10

Preferred Stock Risk. Preferred stock represents an equity or ownership interest in an issuer that pays dividends at a specified rate and has precedence over common stock in paying dividends. If an issuer is liquidated or declares bankruptcy, the claims of bond owners take precedence over those who own preferred and common stock.

Convertible Securities Risk. Convertible securities may be subordinate to other securities. The total return for a convertible security depends, in part, upon the performance of the underlying security into which it can be converted. The value of convertible securities tends to decline as interest rates increase. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality.

Warrants Risk. Warrants are instruments that entitle the holder to buy an equity security at a specific price for a particular period. Warrants may be more speculative than other types of investments. The cost of a warrant may be more volatile than the price of its underlying security, and a warrant may offer more significant potential for capital appreciation and loss. A warrant ceases to have value if it is not exercised before its expiration date.

Foreign Securities Risk. Since the Fund’s investments may include ADRs, representing interests in foreign securities, the Fund is subject to risks beyond those associated with investing in domestic securities. The value of foreign securities is subject to currency fluctuations. Foreign companies are generally not subject to the same regulatory requirements as U.S. companies, resulting in less publicly available information about these companies. In addition, foreign accounting, auditing, and financial reporting standards differ from those applicable to U.S. companies. In addition, periodic U.S. Government restrictions on investments in issuers from certain foreign countries may require the Fund to sell such investments at inopportune times, which could result in losses to the Fund. Below are additional risks related to specific types of foreign securities the Fund invests in

Depositary Receipt Risk. The Fund may hold the securities of non-U.S. companies in the form of depositary receipts. The underlying securities of the depositary receipts in the Fund’s portfolio are subject to fluctuations in foreign currency exchange rates that may affect the value of the Fund’s portfolio. In addition, the value of the securities underlying the depositary receipts may change materially when the U.S. markets are not open for trading. Investments in the underlying foreign securities also involve political and economic risks distinct from those associated with investing in the securities of U.S. issuers.

REITs Risk. REITs are companies that own or finance income-producing real estate. Investments in REITs are subject to the risks associated with investing in the real estate industry, such as adverse developments affecting the real estate industry and real property values, including losses from casualty or condemnation, and changes in local and general economic conditions, supply and demand, interest rates, zoning laws, regulatory limitations on rents, property taxes, and operating expenses. The Fund’s REIT investments also subject it to management and tax risks.

Options Risk. Options and options on futures contracts give the holder of the option the right, but not the obligation, to buy (or sell) a position in a security or contract to the writer of the option at a specific price. Options are subject to correlation risk because there may be an imperfect correlation between the options and the markets for underlying instruments that could cause a given transaction to fail to achieve its objectives. The successful use of options depends on the Adviser’s ability to predict correctly future price fluctuations and the degree of correlation between the markets for options and the underlying instruments. Exchanges can limit the number of positions held or controlled by the Fund or the Adviser, thus limiting the ability to implement the Fund’s strategies. Options are also particularly subject to leverage risk and can be subject to liquidity risk.

11

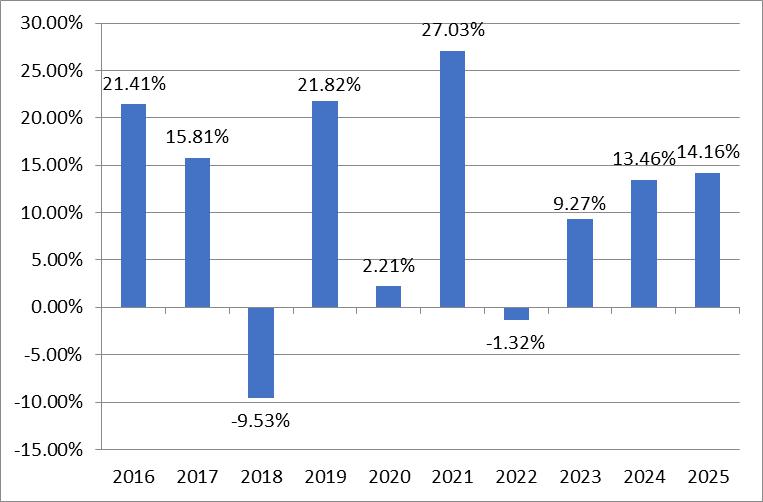

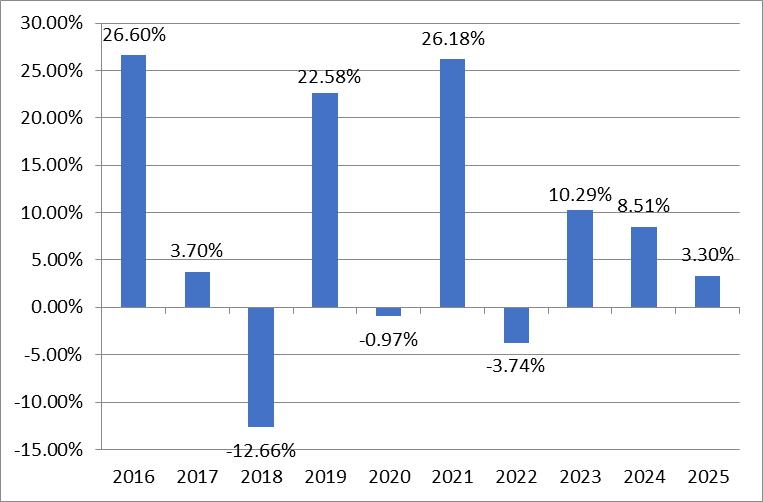

The Fund was reorganized as of the close of business on October 25, 2024, from Series B (Large Cap Value Series), a series of Guggenheim Variable Funds Trust (the “Predecessor Fund”). As a result of the reorganization, the Fund is the accounting successor of the Predecessor Fund. Performance results shown in the bar chart and the performance table below for periods prior to October 25, 2024 reflect the performance of the Predecessor Fund prior to the commencement of the Fund’s operations.

|

During the periods shown in the chart above: |

Quarter Ended | Return |

| - |

(for periods ended December 31, 2025)

| One Year | Five Years | 10 Years | |

| NAA Large Cap Value Series | |||

| S&P 500® Value Index ( |

12

MANAGEMENT OF THE FUND

New Age Alpha Advisors, LLC (d/b/a New Age Alpha) is the Fund’s investment adviser.

|

Portfolio Managers |

Investment Experience with the Fund |

Primary Title with Adviser |

| Armen Arus | Portfolio Manager since inception | Chief Executive Officer |

| Julian Koski | Portfolio Manager since inception | Chief Investment Officer |

| Hugo Chang | Portfolio Manager since inception | Head of Research |

| Konstantin Tourevski | Portfolio Manager since inception | Managing Partner |

| Burak Hurmeydan | Portfolio Manager of the Fund since inception and of the Predecessor Fund since 2018 | Head of Quantitative Strategies |

| Gennadiy Khayutin | Portfolio Manager since April 2025 | Managing Partner |

PURCHASE AND SALE OF FUND SHARES

You may purchase shares of the Fund only through variable annuity contracts or variable life insurance policies offered by participating insurance companies. Fund shares are not offered directly to the public.

You should refer to the Prospectus for the variable annuity contract or variable life insurance policy for information on how to purchase a variable contract or policy and select the Fund as an investment option for your contract or policy.

You may redeem shares of the Fund only through participating insurance companies.

We redeem shares of the Fund on any business day when the New York Stock Exchange (“NYSE”) is open. The price at which the Fund will redeem a share will be its NAV next determined after the order is considered received. The Fund has authorized the participating insurance companies to accept redemption requests on its behalf.

TAX INFORMATION

The dividends and distributions paid by the Fund to the insurance company’s separate accounts will consist of ordinary income, capital gains, or some combination of both. Because shares of the Fund must be purchased through separate accounts used to fund variable insurance contracts, such dividends, and distributions will be exempt from current taxation by contract holders if left to accumulate within a separate account. Withdrawals from such contracts may be subject to ordinary income tax and, if made before age 59½, a 10% penalty tax. Investors should ask their tax advisors for more information on their tax situation, including possible state or local taxes. Refer to the Prospectus of your insurance company’s separate account for a discussion of the tax status of your variable contract.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

The Fund’s shares are generally available only through participating insurance companies offering variable annuity contracts and variable life insurance policies. A broker-dealer or other financial intermediary generally purchases life insurance policies and variable annuities. The Fund and/or its related companies may pay the participating insurance companies for services; some payments may go to broker-dealers and other intermediaries. These payments may create a conflict of interest for an intermediary or be a factor in the participating insurance companies’ decision to include the Fund as an underlying investment option in a variable contract. Ask your salesperson or visit your financial intermediary’s website for more information.

13

The NAA Large Core Series (the “Fund”) seeks long-term capital growth.

This table describes the fees and expenses you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and additional fees to financial intermediaries, which are not reflected in the table and example.

|

|

Class S | Class L |

| Management Fees | ||

| Distribution and/or Service (12b-1) Fees | ||

| Other Expenses(1) | ||

| Total Annual Fund Operating Expenses | ||

| Less Management Fee Reductions and/or Expense Reimbursements(2)(3) | ( |

( |

| Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements(2)(3) |

| (1) | |

| (2) |

|

| (3) |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the periods indicated and then redeem all your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the operating expenses remain the same, and the contractual agreement to limit expenses remains in effect through the expiration date described above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Class S | $ |

$ |

$ |

$ |

| Class L | $ |

$ |

$ |

$ |

14

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or the Example, affect the Fund’s performance. During the fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was

Under normal circumstances, the Fund pursues its objective by investing at least 80% of its assets (net assets, plus the amount of any borrowings for investment purposes) in large-capitalization securities that the Adviser considers having “core” characteristics. The Fund defines “core” as investments that typically represent a balance between value and growth investing. However, any particular security may have different degrees of growth or value characteristics. The Fund defines “large-capitalization” as those companies with market capitalizations generally falling within the range of the S&P 500® Index. The capitalization range of the S&P 500® Index is between $5.3 billion and $4.2 trillion as of March 31, 2026. The Fund defines:

| ● | “value” as investments that appear to be undervalued relative to assets, earnings, growth potential or cash flows. |

| ● | “growth” as investments having what the Adviser believes to be above-average growth rates (high growth rates for earnings, sales, book value, and cash flow) as compared to their industry or the overall market. |

The Fund will primarily invest in equity securities, including common stocks, rights, real estate investment trusts (“REITs”), options, warrants, convertible debt securities of U.S. and U.S. dollar-denominated foreign issuers, and American Depositary Receipts (“ADRs”). Convertible securities are hybrid financial instruments that typically consist of bonds, debentures, or preferred shares that can be converted into a specified number of common shares of the issuing company, typically at the option of the security holder. The Fund may also invest in various investment vehicles, such as mutual funds and exchange-traded funds (“ETFs”), for portfolio management purposes, including cash and liquidity management, to obtain a higher return on collateral positions and achieve greater diversification and trading efficiency than would usually be experienced by investing directly and separately in individual securities. In selecting mutual funds and ETFs for investment, the Adviser will prioritize investments that align with and support the Fund’s overall strategy.

In selecting investments for the Fund, the Adviser uses qualitative and quantitative analysis, and other proprietary strategies to identify securities that, in combination, are expected to exceed the total return of the S&P 500 Index by attempting to avoid the “losers” in the Index. The “avoid the losers” philosophy is fundamental to the underlying actuarial-like approach of the Adviser with respect to asset management. In its attempts to generate alpha, the Adviser does not aim to pick the winners; instead, it aims to avoid the losers. A loser is a company that, according to the Adviser’s investment methodology, cannot deliver revenue growth to support its stock price. The Adviser has developed a probability-based measure to identify and avoid these stocks, called the h-factor (“h-factor”), which is the foundation of the Adviser’s investment philosophy. The h-factor measures the probability a company cannot deliver the revenue growth indicated by its stock price. In buying and selling securities for the Fund, the Adviser will apply its proprietary h-factor methodology to its security selection process. H-factor uses an algorithm rooted in actuarial risk principles to construct a portfolio with exposure to returns across sectors, styles, geographies,

15

and asset classes. Using an actuarial-based approach, h-factor aims to identify underpriced and overpriced securities and assign them an h-factor score, which is the probability that the issuer will not deliver revenue growth to support the securities’ current price. Utilizing these scores, the Adviser seeks to avoid the overpriced securities and invest in the underpriced securities.

The Fund will sell investments when they no longer meet the Adviser’s investment criteria, market conditions change or to meet redemption requests.

PRINCIPAL RISKS

Growth Investing Risk. Growth investing includes the risk of investing in securities whose prices have historically been more volatile than other securities, especially over the short term. Growth stock prices reflect projections of future earnings or revenues, and if a company’s earnings or revenues fall short of expectations, its stock price may fall dramatically.

Value Investing Risk. Value investing includes the risk that stocks of undervalued companies may not rise as quickly as anticipated if the market doesn’t recognize their intrinsic value or value stocks are out of favor. Value investing may be out of favor with investors occasionally, and value stocks may underperform the securities of other companies or the stock market in general.

Market Risk. Market risk is the risk that the value of the securities in the Fund’s portfolio may decline due to daily fluctuations in the securities markets that are beyond the Adviser’s control, including fluctuations in interest rates, the quality of the Fund’s investments, economic conditions, and general equity market conditions. Certain market events could increase volatility and exacerbate market risks, such as changes in government’s economic policies, political turmoil, environmental events, trade disputes, epidemics, pandemics, or other public health issues. Turbulence in financial markets and reduced liquidity in equity, credit, and fixed-income markets may negatively affect many issuers domestically and worldwide. It can result in trading halts, any of which could hurt the Fund. During periods of market volatility, security prices (including securities held by the Fund) could fall drastically and rapidly and, therefore, adversely affect the Fund.

Large-Capitalization Company Risk. Large-capitalization companies are more mature and may be unable to respond as quickly as smaller companies to new competitive challenges, such as changes in technology and consumer tastes, and may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Management Style Risk. The Adviser’s method of security selection may not be successful, and the Fund may underperform relative to its benchmark index or to other mutual funds that employ similar investment strategies. In addition, the Adviser may select investments that fail to perform as anticipated. The ability of the Fund to meet its investment objective is directly related to the success of the Adviser’s investment process, and there is no guarantee that the Adviser’s judgments about the attractiveness, value, and potential appreciation of a particular investment for the Fund will be correct or produce the desired results.

16

Equity Securities Risk. Equity risk is the risk that securities held by the Fund will fall due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds. Although common stocks have historically generated higher average returns than fixed-income securities over the long term, common stocks also have experienced significantly more volatility in returns. Below are additional risks related to specific equity securities the Fund invests in.

Investment Company Risk. Investing in other investment vehicles, including ETFs, closed-end funds, and other mutual funds, subjects the Fund to those risks affecting the investment vehicle, including the possibility that the value of the underlying securities held by the investment vehicle could decrease or the portfolio becomes illiquid. Moreover, the Fund and its shareholders will incur its pro rata share of the underlying vehicles’ expenses, reducing the Fund’s performance. In addition, investments in an ETF or a listed closed-end fund are subject to, among other risks, the risk that the shares may trade at a discount or premium relative to the net asset value of the shares, and the listing exchange may halt trading of the shares.

Preferred Stock Risk. Preferred stock represents an equity or ownership interest in an issuer that pays dividends at a specified rate and has precedence over common stock in paying dividends. If an issuer is liquidated or declares bankruptcy, the claims of bond owners take precedence over those who own preferred and common stock.

Convertible Securities Risk. Convertible securities may be subordinate to other securities. The total return for a convertible security depends, in part, upon the performance of the underlying security into which it can be converted. The value of convertible securities tends to decline as interest rates increase. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality.

Warrants Risk. Warrants are instruments that entitle the holder to buy an equity security at a specific price for a particular period. Warrants may be more speculative than other types of investments. The cost of a warrant may be more volatile than the price of its underlying security, and a warrant may offer more significant potential for capital appreciation and loss. A warrant ceases to have value if it is not exercised before its expiration date.

Sector Concentration Risk. Because the Fund may invest a significant portion of its assets in a particular sector of the market it may be especially sensitive to factors and economic risks that specifically affect that sector. As a result, the Fund’s share price may fluctuate more widely than the share price of a fund that is more broadly invested across numerous sectors.

Foreign Securities Risk. Since the Fund’s investments may include ADRs, representing interests in foreign securities, the Fund is subject to risks beyond those associated with investing in domestic securities. The value of foreign securities is subject to currency fluctuations. Foreign companies are generally not subject to the same regulatory requirements as U.S. companies, resulting in less publicly available information about these companies. In addition, foreign accounting, auditing, and financial reporting standards differ from those applicable to U.S. companies. In addition, periodic U.S. Government restrictions on investments in issuers from certain foreign countries may require the Fund to sell such investments at inopportune times, which could result in losses to the Fund. Below are additional risks related to specific types of foreign securities the Fund invests in.

Depositary Receipt Risk. The Fund may hold the securities of non-U.S. companies in the form of depositary receipts. The underlying securities of the depositary receipts in the Fund’s portfolio are subject to fluctuations in foreign currency exchange rates that may affect the value of the Fund’s portfolio. In addition, the value of the securities underlying the depositary receipts may change materially when the U.S. markets are not open for trading. Investments in the underlying foreign securities also involve political and economic risks distinct from those associated with investing in the securities of U.S. issuers.

17

REITs Risk. REITs are companies that own or finance income-producing real estate. Investments in REITs are subject to the risks associated with investing in the real estate industry, such as adverse developments affecting the real estate industry and real property values, including losses from casualty or condemnation, and changes in local and general economic conditions, supply and demand, interest rates, zoning laws, regulatory limitations on rents, property taxes, and operating expenses. The Fund’s REIT investments also subject it to management and tax risks.

Options Risk. Options and options on futures contracts give the holder of the option the right, but not the obligation, to buy (or sell) a position in a security or contract to the writer of the option at a specific price. Options are subject to correlation risk because there may be an imperfect correlation between the options and the markets for underlying instruments that could cause a given transaction to fail to achieve its objectives. The successful use of options depends on the Adviser’s ability to predict correctly future price fluctuations and the degree of correlation between the markets for options and the underlying instruments. Exchanges can limit the number of positions held or controlled by the Fund or the Adviser, thus limiting the ability to implement the Fund’s strategies. Options are also particularly subject to leverage risk and can be subject to liquidity risk.

Class L shares of the Fund have not commenced operations as of the date of this Prospectus, and do not have a full calendar year of performance history.

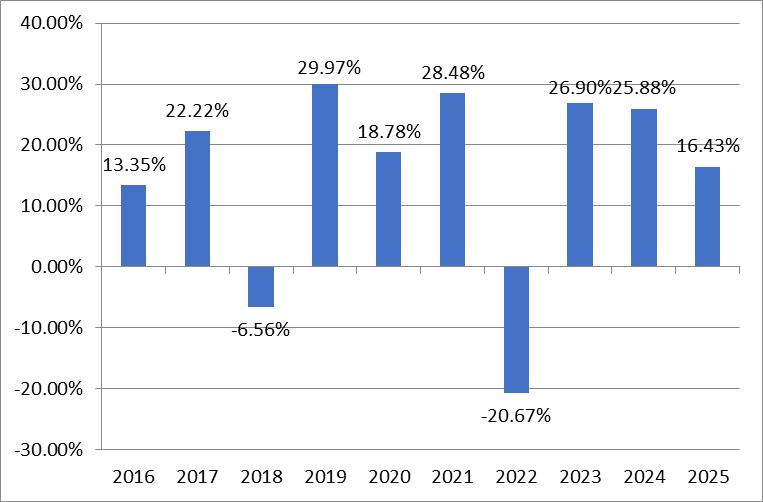

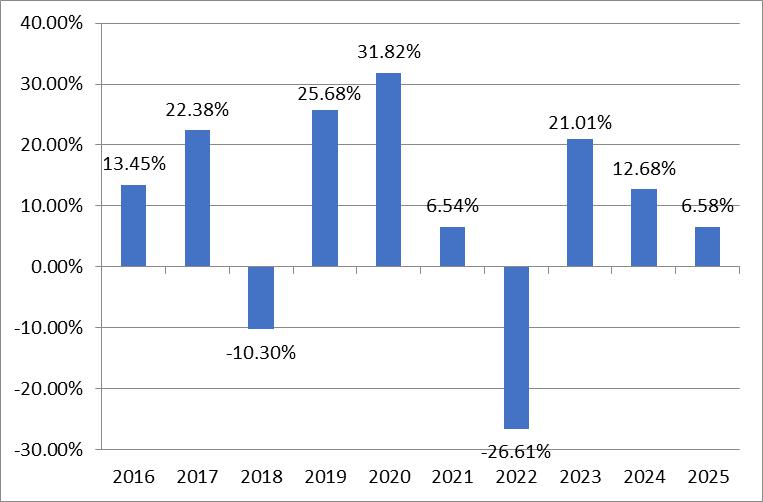

The Fund was reorganized as of the close of business on October 25, 2024, from Series A (StylePlus-Large Core Series), a series of Guggenheim Variable Funds Trust (the “Predecessor Fund”). As a result of the reorganization, the Fund is the accounting successor of the Predecessor Fund. Performance results shown in the bar chart and the performance table below for periods prior to October 25, 2024 reflect the performance of the Predecessor Fund prior to the commencement of the Fund’s operations.

18

|

During the periods shown in the chart above: |

Quarter Ended | Return |

| - |

(for periods ended December 31, 2025)

| One Year | Five Years | 10 Years | |

| NAA Large Core Series – Class S* | |||

| S&P 500® Index ( |

| * |

MANAGEMENT OF THE FUND

New Age Alpha Advisors, LLC (d/b/a New Age Alpha) is the Fund’s investment adviser.

|

Portfolio Managers |

Investment Experience with the Fund |

Primary Title with Adviser |

| Armen Arus | Portfolio Manager since inception | Chief Executive Officer |

| Julian Koski | Portfolio Manager since inception | Chief Investment Officer |

| Hugo Chang | Portfolio Manager since inception | Head of Research |

| Konstantin Tourevski | Portfolio Manager since inception | Managing Partner |

| Burak Hurmeydan | Portfolio Manager since inception | Head of Quantitative Strategies |

| Gennadiy Khayutin | Portfolio Manager since April 2025 | Managing Partner |

19

PURCHASE AND SALE OF FUND SHARES

You may purchase Class S shares of the Fund only through variable annuity contracts or variable life insurance policies, and Class L shares of the Fund only through variable life insurance policies, offered by participating insurance companies. Fund shares are not offered directly to the public.

You should refer to the Prospectus for the variable annuity contract or variable life insurance policy for information on how to purchase a variable contract or policy and select the Fund as an investment option for your contract or policy.

You may redeem shares of the Fund only through participating insurance companies.

We redeem shares of the Fund on any business day when the New York Stock Exchange (“NYSE”) is open. The price at which the Fund will redeem a share will be its NAV next determined after the order is considered received. The Fund has authorized the participating insurance companies to accept redemption requests on its behalf.

TAX INFORMATION

The dividends and distributions paid by the Fund to the insurance company’s separate accounts will consist of ordinary income, capital gains, or some combination of both. Because shares of the Fund must be purchased through separate accounts used to fund variable insurance contracts, such dividends, and distributions will be exempt from current taxation by contract holders if left to accumulate within a separate account. Withdrawals from such contracts may be subject to ordinary income tax and, if made before age 59½, a 10% penalty tax. Investors should ask their tax advisors for more information on their tax situation, including possible state or local taxes. Refer to the Prospectus of your insurance company’s separate account for a discussion of the tax status of your variable contract.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

The Funds’ Class S shares are generally available only through participating insurance companies offering variable annuity contracts and life insurance policies, and the Fund’s Class L shares are generally available only through participating insurance companies offering variable life insurance policies. A broker-dealer or other financial intermediary generally purchases life insurance policies and variable annuities. The Fund and/or its related companies may pay the participating insurance companies for services; some payments may go to broker-dealers and other intermediaries. These payments may create a conflict of interest for an intermediary or be a factor in the participating insurance companies’ decision to include the Fund as an underlying investment option in a variable contract. Ask your salesperson or visit your financial intermediary’s website for more information.

20

The NAA Large Growth Series (the “Fund”) seeks long-term capital growth.

This table describes the fees and expenses you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and additional fees to financial intermediaries, which are not reflected in the table and example.

|

Annual Fund Operating Expenses |

Class S | Class L |

| Management Fees | ||

| Distribution and/or Service (12b-1) Fees | ||

| Other Expenses(1) | ||

| Total Annual Fund Operating Expenses(1) | ||

| Less Management Fee Reductions and/or Expense Reimbursements(2) | ( |

( |

| Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements(2) |

| (1) |

| (2) |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the periods indicated and then redeem all your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, the operating expenses remain the same, and the contractual agreement to limit expenses remains in effect through the expiration date described above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Class S | $ |

$ |

$ |

$ |

| Class L | $ |

$ |

$ |

$ |

21

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or the Example, affect the Fund’s performance. During the fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was

Under normal circumstances, the Fund pursues its objective by investing at least 80% of its assets (net assets, plus the amount of any borrowings for investment purposes) in large-capitalization securities that the Adviser considers having “growth” characteristics. The Fund defines:

| ● | “growth” as investments having what the Adviser believes to be above-average growth rates (high growth rates for earnings, sales, book value, and cash flow) as compared to their industry or the overall market. |

| ● | “large-capitalization” as those companies with market capitalizations generally falling within the range of the S&P 500® Index. The capitalization range of the S&P 500® Index is between $5.3 billion and $4.2 trillion as of March 31, 2026. |

The Fund will primarily invest in equity securities, including common stocks, real estate investment trusts (“REITs”), options, warrants, convertible debt securities of U.S. and U.S.-dollar denominated foreign issuers, and American Depositary Receipts (“ADRs”). Convertible securities are hybrid financial instruments that typically consist of bonds, debentures, or preferred shares that can be converted into a specified number of common shares of the issuing company, typically at the option of the security holder. The Fund may also invest in various investment vehicles for portfolio management purposes, such as mutual funds and exchange-traded funds (“ETFs”), including cash management and liquidity management, to obtain a higher return on collateral positions and achieve greater diversification and trading efficiency than would usually be experienced by investing directly and separately in individual securities. In selecting mutual funds and ETFs for investment, the Adviser will prioritize investments that align with and support the Fund’s overall strategy.

In selecting investments for the Fund, the Adviser uses qualitative and quantitative analysis, and other proprietary strategies to identify securities that, in combination, are expected to exceed the total return of the S&P 500 Growth Index by attempting to avoid the “losers” in the Index. The “avoid the losers” philosophy is fundamental to the underlying actuarial-like approach of the Adviser with respect to asset management. In its attempts to generate alpha, the Adviser does not aim to pick the winners; instead, it aims to avoid the losers. A loser is a company that, according to the Adviser’s investment methodology, cannot deliver revenue growth to support its stock price. The Adviser has developed a probability-based measure to identify and avoid these stocks, called the h-factor (“h-factor”), which is the foundation of the Adviser’s investment philosophy. The h-factor measures the probability a company cannot deliver the revenue growth indicated by its stock price. In buying and selling securities for the Fund, the Adviser will apply its proprietary h-factor methodology to its security selection process. H-factor uses an algorithm rooted in actuarial risk principles to construct a portfolio with exposure to returns across sectors, styles, geographies, and asset classes. Using an actuarial-based approach, h-factor aims to identify underpriced and overpriced securities and assign them an h-factor score, which is the probability that the issuer will not deliver revenue growth to support the securities’ current price. Utilizing these scores, the Adviser seeks to avoid the overpriced securities and invest in the underpriced securities.

22

The Fund will sell investments when they no longer meet the Adviser’s investment criteria, market conditions change or to meet redemption requests.

PRINCIPAL RISKS

Market Risk. Market risk is the risk that the value of the securities in the Fund’s portfolio may decline due to daily fluctuations in the securities markets that are beyond the Adviser’s control, including fluctuations in interest rates, the quality of the Fund’s investments, economic conditions, and general equity market conditions. Certain market events could increase volatility and exacerbate market risks, such as changes in government’s economic policies, political turmoil, environmental events, trade disputes, epidemics, pandemics, or other public health issues. Turbulence in financial markets and reduced liquidity in equity, credit, and fixed-income markets may negatively affect many issuers domestically and worldwide. It can result in trading halts, any of which could hurt the Fund. During periods of market volatility, security prices (including securities held by the Fund) could fall drastically and rapidly and, therefore, adversely affect the Fund.

Large-Capitalization Company Risk. Large-capitalization companies are more mature and may be unable to respond as quickly as smaller companies to new competitive challenges, such as changes in technology and consumer tastes, and may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Growth Investing Risk. Growth investing includes the risk of investing in securities whose prices have historically been more volatile than other securities, especially over the short term. Growth stock prices reflect projections of future earnings or revenues, and if a company’s earnings or revenues fall short of expectations, its stock price may fall dramatically.

Management Style Risk. The Adviser’s method of security selection may not be successful, and the Fund may underperform relative to its benchmark index or to other mutual funds that employ similar investment strategies. In addition, the Adviser may select investments that fail to perform as anticipated. The ability of the Fund to meet its investment objective is directly related to the success of the Adviser’s investment process, and there is no guarantee that the Adviser’s judgments about the attractiveness, value, and potential appreciation of a particular investment for the Fund will be correct or produce the desired results.

Equity Securities Risk. Equity risk is the risk that securities held by the Fund will fall due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds. Although common stocks have historically generated higher average returns than fixed-income securities over the long term, common stocks also have experienced significantly more volatility in returns. Below are additional risks related to specific equity securities the Fund invests in.

Investment Company Risk. Investing in other investment vehicles, including ETFs, closed-end funds, and other mutual funds, subjects the Fund to those risks affecting the investment vehicle, including the possibility that the value of the underlying securities held by the investment vehicle could decrease or the portfolio becomes illiquid. Moreover, the Fund and its shareholders will incur its

23

pro rata share of the underlying vehicles’ expenses, reducing the Fund’s performance. In addition, investments in an ETF or a listed closed-end fund are subject to, among other risks, the risk that the shares may trade at a discount or premium relative to the net asset value of the shares, and the listing exchange may halt trading of the shares.

Preferred Stock Risk. Preferred stock represents an equity or ownership interest in an issuer that pays dividends at a specified rate and has precedence over common stock in paying dividends. If an issuer is liquidated or declares bankruptcy, the claims of bond owners take precedence over those who own preferred and common stock.

Convertible Securities Risk. Convertible securities may be subordinate to other securities. The total return for a convertible security depends, in part, upon the performance of the underlying security into which it can be converted. The value of convertible securities tends to decline as interest rates increase. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality.

Warrants Risk. Warrants are instruments that entitle the holder to buy an equity security at a specific price for a particular period. Warrants may be more speculative than other types of investments. The cost of a warrant may be more volatile than the price of its underlying security, and a warrant may offer more significant potential for capital appreciation and loss. A warrant ceases to have value if it is not exercised before its expiration date.

Sector Concentration Risk. Because the Fund may invest a significant portion of its assets in a particular sector of the market it may be especially sensitive to factors and economic risks that specifically affect that sector. As a result, the Fund’s share price may fluctuate more widely than the share price of a fund that is more broadly invested across numerous sectors.

Foreign Securities Risk. Since the Fund’s investments may include ADRs, representing interests in foreign securities, the Fund is subject to risks beyond those associated with investing in domestic securities. The value of foreign securities is subject to currency fluctuations. Foreign companies are generally not subject to the same regulatory requirements as U.S. companies, resulting in less publicly available information about these companies. In addition, foreign accounting, auditing, and financial reporting standards differ from those applicable to U.S. companies. In addition, periodic U.S. Government restrictions on investments in issuers from certain foreign countries may require the Fund to sell such investments at inopportune times, which could result in losses to the Fund. Below are additional risks related to specific types of foreign securities the Fund invests in.

Depositary Receipt Risk. The Fund may hold the securities of non-U.S. companies in the form of depositary receipts. The underlying securities of the depositary receipts in the Fund’s portfolio are subject to fluctuations in foreign currency exchange rates that may affect the value of the Fund’s portfolio. In addition, the value of the securities underlying the depositary receipts may change materially when the U.S. markets are not open for trading. Investments in the underlying foreign securities also involve political and economic risks distinct from those associated with investing in the securities of U.S. issuers.

REITs Risk. REITs are companies that own or finance income-producing real estate. Investments in REITs are subject to the risks associated with investing in the real estate industry, such as adverse developments affecting the real estate industry and real property values, including losses from casualty or condemnation, and changes in local and general economic conditions, supply and demand, interest rates, zoning laws, regulatory limitations on rents, property taxes, and operating expenses. The Fund’s REIT investments also subject it to management and tax risks.

24

Options Risk. Options and options on futures contracts give the holder of the option the right, but not the obligation, to buy (or sell) a position in a security or contract to the writer of the option at a specific price. Options are subject to correlation risk because there may be an imperfect correlation between the options and the markets for underlying instruments that could cause a given transaction to fail to achieve its objectives. The successful use of options depends on the Adviser’s ability to predict correctly future price fluctuations and the degree of correlation between the markets for options and the underlying instruments. Exchanges can limit the number of positions held or controlled by the Fund or the Adviser, thus limiting the ability to implement the Fund’s strategies. Options are also particularly subject to leverage risk and can be subject to liquidity risk.

Class L shares of the Fund have not commenced operations as of the date of this Prospectus, and do not have a full calendar year of performance history.

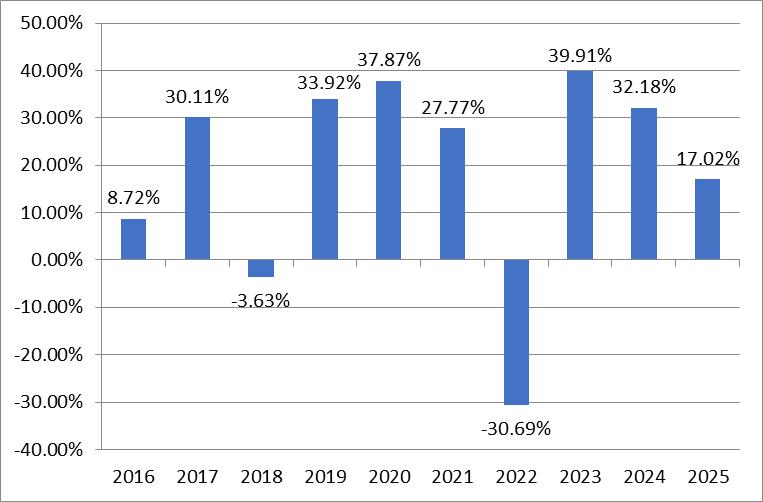

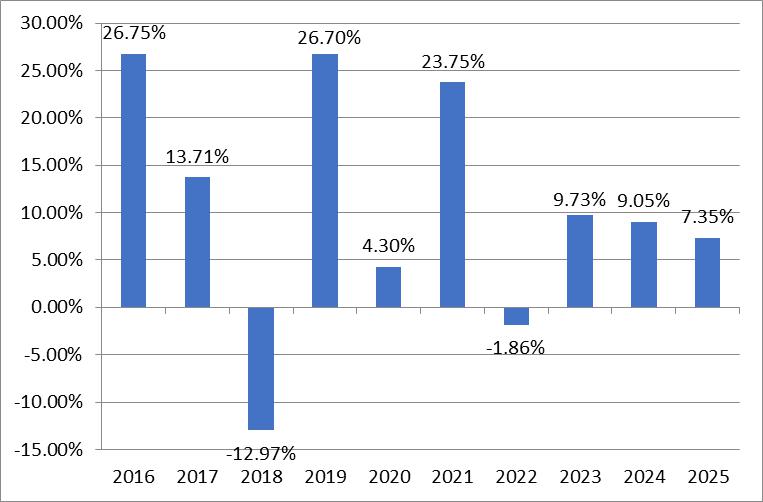

The Fund was reorganized as of the close of business on October 25, 2024, from Series Y (StylePlus-Large Growth Series), a series of Guggenheim Variable Funds Trust (the “Predecessor Fund”). As a result of the reorganization, the Fund is the accounting successor of the Predecessor Fund. Performance results shown in the bar chart and the performance table below for periods prior to October 25, 2024 reflect the performance of the Predecessor Fund prior to the commencement of the Fund’s operations.

25

Quarterly Returns During This Period

|

During the periods shown in the chart above: |

Quarter Ended | Return |

| - |

(for periods ended December 31, 2025)

| One Year | Five Years | 10 Years | |

| NAA Large Growth Series – Class S* | |||

| S&P 500® Growth Index ( |

| * |

MANAGEMENT OF THE FUND

New Age Alpha Advisors, LLC (d/b/a New Age Alpha) is the Fund’s investment adviser.

|

Portfolio Managers |

Investment Experience with the Fund |

Primary Title with Adviser |

| Armen Arus | Portfolio Manager since inception | Chief Executive Officer |

| Julian Koski | Portfolio Manager since inception | Chief Investment Officer |

| Hugo Chang | Portfolio Manager since inception | Head of Research |

| Konstantin Tourevski | Portfolio Manager since inception | Managing Partner |

| Burak Hurmeydan | Portfolio Manager since inception | Head of Quantitative Strategies |

| Gennadiy Khayutin | Portfolio Manager since April 2025 | Managing Partner |

26

PURCHASE AND SALE OF FUND SHARES

You may purchase Class S shares of the Fund only through variable annuity contracts or variable life insurance policies, and Class L shares of the Fund only through variable life insurance policies, offered by participating insurance companies. Fund shares are not offered directly to the public.

You should refer to the Prospectus for the variable annuity contract or variable life insurance policy for information on how to purchase a variable contract or policy and select the Fund as an investment option for your contract or policy.

You may redeem shares of the Fund only through participating insurance companies.

We redeem shares of the Fund on any business day when the New York Stock Exchange (“NYSE”) is open. The price at which the Fund will redeem a share will be its NAV next determined after the order is considered received. The Fund has authorized the participating insurance companies to accept redemption requests on its behalf.

TAX INFORMATION

The dividends and distributions paid by the Fund to the insurance company’s separate accounts will consist of ordinary income, capital gains, or some combination of both. Because shares of the Fund must be purchased through separate accounts used to fund variable insurance contracts, such dividends, and distributions will be exempt from current taxation by contract holders if left to accumulate within a separate account. Withdrawals from such contracts may be subject to ordinary income tax and, if made before age 59½, a 10% penalty tax. Investors should ask their tax advisors for more information on their tax situation, including possible state or local taxes. Refer to the Prospectus of your insurance company’s separate account for a discussion of the tax status of your variable contract.

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

The Fund’s Class S shares are generally available only through participating insurance companies offering variable annuity contracts and variable life insurance policies, and the Fund’s Class L shares are generally available only through participating insurance companies offering variable life insurance policies. A broker-dealer or other financial intermediary generally purchases life insurance policies and variable annuities. The Fund and/or its related companies may pay the participating insurance companies for services; some payments may go to broker-dealers and other intermediaries. These payments may create a conflict of interest for an intermediary or be a factor in the participating insurance companies’ decision to include the Fund as an underlying investment option in a variable contract. Ask your salesperson or visit your financial intermediary’s website for more information.

27

The NAA Mid Growth Series (the “Fund”) seeks long-term capital growth.

This table describes the fees and expenses you may pay if you buy, hold, and sell shares of the Fund. You may pay other fees, such as brokerage commissions and additional fees to financial intermediaries, which are not reflected in the table and example.

|

Annual Fund Operating Expenses |

Class S |

| Management Fees | |

| Distribution and/or Service (12b-1) Fees | |

| Other Expenses(1) | |

| Total Annual Fund Operating Expenses | |

| Less Management Fee Reductions and/or Expense Reimbursements(1)(2) | ( |

| Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements(1)(2) |

| (1) |

|

| (2) |

|