| Class S | Class F | |||||||

| SHAREHOLDER TRANSACTION FEES | ||||||||

| Maximum sales load imposed on purchases(1) | None | None | ||||||

| Early Withdrawal Charge on Shares Repurchased Within 365 Days of Purchase (as a percentage of proceeds) | None | None | ||||||

| Maximum contingent deferred sales charge | None | None | ||||||

| (1) | While Class S Shares and Class F Shares are not subject to a front-end sales charge, if an investor purchases Class S Shares or Class F Shares through certain financial firms, such firms may directly charge the investor transaction or other fees in such amount as they may determine. An investor should consult its financial firm for additional information. See “Plan of Distribution.” |

| ANNUAL FUND EXPENSES(2) | ||||||||

| (as a percentage of average Net Assets attributable to Shares) | ||||||||

| Management Fee | 0.95 | % | 0.95 | % | ||||

| Incentive Fee(3) | 1.47 | % | 1.47 | % | ||||

| Interest Payments on Borrowed Funds(4) | 0.12 | % | 0.12 | % | ||||

| Other expenses(5) | ||||||||

| Distribution fee(6) | None | 0.50 | % | |||||

| All other expenses | 0.74 | % | 0.74 | % | ||||

| Total annual fund expenses | 3.28 | % | 3.78 | % | ||||

| Fee waiver and expense reimbursement(7) (8) | (0.94 | )% | (0.94 | )% | ||||

| Total annual fund expenses after fee waiver and expense reimbursement(7) (8) | 2.34 | % | 2.84 | % |

| (2) | Assumes the Fund raises $213 million in proceeds in the current fiscal year resulting in estimated average Net Assets of approximately $251 million. |

| (3) | The Fund anticipates that it may have interest income that could result in the payment of an Incentive Fee to the Adviser during certain periods. However, the Incentive Fee is based on the Fund’s performance and will not be paid unless the Fund achieves certain performance targets. The Fund expects the Incentive Fee the Fund pays to increase to the extent the Fund earns greater interest income through its investments. The Incentive Fee is calculated and payable quarterly in arrears based upon the Fund’s “pre-incentive fee net investment income” for the immediately preceding quarter, and is subject to a hurdle rate, expressed as a rate of return on the Fund’s Net Assets, equal to 1.50% per quarter, or an annualized hurdle rate of 6.00%, subject to a “catch-up” feature. See “Management and Incentive Fees” for a full explanation of how the Incentive Fee is calculated. |

| (4) | These expenses represent estimated interest payments the Fund expects to incur in connection with its credit facility during the current fiscal year. See “Summary of Terms — Leverage.” The amount shown in the table above is based on the assumption that the Fund borrows money for investment purposes at an average rate of 1.50% of Net Assets. |

| (5) | Other expenses include reasonably estimated costs the Fund can expect to incur related to accounting, custody, transfer agency, legal, valuation agent, pricing vendor and auditing fees of the Fund, organizational and offering costs applicable to each class, as well as the reimbursement of the compensation of administrative personnel and fees payable to the Independent Trustees. The amount presented in the table estimates the amounts the Fund expects to pay in the current fiscal year, assuming the Fund raises $213 million of proceeds during that time. |

| (6) | The Fund may charge a distribution and/or shareholder servicing fee totaling up to 0.50% per year on Class F Shares. With respect to Class F Shares, the entire fee is characterized as a “distribution fee.” The Fund may use these fees, in respect of the relevant class, to compensate Financial Intermediaries or financial institutions for distribution-related expenses, if applicable, and providing ongoing services in respect of clients with whom they have distributed Class S Shares or Class F Shares of the Fund. Such services may also include electronic processing of client orders, electronic fund transfers between clients and the Fund, account reconciliations with the Fund’s transfer agent, facilitation of electronic delivery to clients of Fund documentation, monitoring client accounts for back-up withholding and any other special tax reporting obligations, maintenance of books and records with respect to the foregoing, and such other information and liaison services as the Fund or the Adviser may reasonably request. |

| (7) | The Adviser and the Fund have entered into the Expense Limitation Agreement in respect of each of Class S Shares and Class F Shares under which the Adviser has agreed contractually until May 1, 2027 to waive its Management Fee and/or reimburse the Fund’s initial organizational and offering costs, as well as the Fund’s operating expenses on a monthly basis to the extent that the Fund’s monthly total annualized fund operating expenses in respect of each class (excluding (i) expenses directly related to the costs of making investments, including interest and structuring costs for borrowings and line(s) of credit, taxes, brokerage costs, the Fund’s proportionate share of expenses related to co-investments, litigation and extraordinary expenses, (ii) Incentive Fees and (iii) any distribution and/or shareholder servicing fees) exceed 1.50% of the average NAV of such class (the “Expense Cap”). In consideration of the Adviser’s agreement to waive its Management Fee and/or reimburse the Fund’s operating expenses, the Fund has agreed to repay the Adviser in the amount of any waived Management Fees and Fund expenses reimbursed in respect of each of Class S Shares and Class F Shares subject to the limitation that a reimbursement (an “Adviser Recoupment”) will be made only if and to the extent that: (i) it is payable not more than three years from the date on which the applicable waiver or expense payment was made by the Adviser; and (ii) the Adviser Recoupment does not cause the Fund’s total annual operating expenses (on an annualized basis and net of any reimbursements received by the Fund during such fiscal year) during the applicable quarter to exceed the Expense Cap of such class. The Adviser Recoupment for a class of Shares will not cause Fund expenses in respect of that class to exceed the Expense Cap either (i) at the time of the waiver or (ii) at the time of recoupment. See “Fund Expenses—Expense Limitation Agreement” for additional information. The Expense Limitation Agreement will remain in effect until May 1, 2027, unless and until the Board approves its modification or termination. |

| (8) | The Adviser has contractually agreed, through the first year after the date on which the Fund’s Net Assets equal $250 million, but in no instance sooner than May 1, 2027, to waive (i) the Management Fee it is entitled to receive from the Fund pursuant to the Investment Advisory Agreement to the extent necessary to limit its Management Fee to 0.70% of the average daily value of the Fund’s Net Assets and (ii) the catch-up feature related to the Incentive Fee, with the effect that the Incentive Fee will equal 15% of the portion of the Fund’s pre-incentive fee net investment income that exceeds the hurdle rate. The Adviser may not seek reimbursement from the Fund with respect to the Management Fee and Incentive Fee waived pursuant to the Management Fee Waiver Agreement. The Management Fee Waiver Agreement will continue through the date set forth above, at which time it will terminate unless otherwise agreed to in writing by the parties. In addition, the Management Fee Waiver Agreement will terminate upon termination of the Investment Advisory Agreement. |

Example:

The following example demonstrates the projected dollar amount of total expenses that would be incurred over various periods with respect to a hypothetical investment in Shares. In calculating the following expense amounts, the Fund has assumed its direct and indirect annual operating expenses would remain at the percentage levels set forth in the table above.

An investor would pay the following expenses on a $1,000 investment, assuming a 5.0% annual return:

Class S

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| $ | 24 | $ | 63 | $ | 104 | $ | 220 | |||||||||

Class F

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| $ | 29 | $ | 78 | $ | 130 | $ | 272 | |||||||||

The example and the expenses in the tables above should not be considered a representation of the Fund’s future expenses, and actual expenses may be greater or less than those shown. While the example assumes a 5.0% annual return, as required by the SEC, the Fund’s performance will vary and may result in a return greater or less than 5.0%. For a more complete description of the various fees and expenses borne directly and indirectly by the Fund, see “Fund Expenses” and “Management and Incentive Fees.”

The following table illustrates the aggregate fees and expenses that the Fund expects to incur and that Shareholders can expect to bear directly or indirectly. The expenses shown in the table below are based on the assumption that the Fund borrows money for investment purposes at an average rate of 1.50% of Net Assets.

| Class and Year Ended | Total Amount Outstanding Exclusive of Treasury Securities(1) |

Asset Coverage Per Unit(2) |

Involuntary Liquidating Preference Per Unit(3) |

Average Market Value Per Unit(4) |

||||||||||||

| Line of Credit | ||||||||||||||||

| December 31, 2025 | $ | 15,500,000 | $ | 11,080 | — | |||||||||||

| December 31, 2024 | $ | 10,820,000 | $ | 7,603 | ||||||||||||

SENIOR SECURITIES

Information about the Fund’s senior securities as of December 31, 2025 is shown in the following table and has been derived from the Fund’s audited consolidated financial statements, which have been audited by Cohen & Company, Ltd., an independent registered public accounting firm.

| Class and Year Ended | Total Amount Outstanding Exclusive of Treasury Securities(1) |

Asset Coverage Per Unit(2) |

Involuntary Liquidating Preference Per Unit(3) |

Average Market Value Per Unit(4) |

||||||||||||

| Line of Credit | ||||||||||||||||

| December 31, 2025 | $ | 15,500,000 | $ | 11,080 | — | |||||||||||

| December 31, 2024 | $ | 10,820,000 | $ | 7,603 | ||||||||||||

| (1) | Total amount of each class of senior securities outstanding at principal value at the end of the period presented. |

| (2) | The asset coverage ratio for a class of senior securities representing indebtedness is calculated as the Fund’s consolidated total assets, less all liabilities and indebtedness not represented by senior securities, divided by total senior securities representing indebtedness in accordance with Section 18(h) of the 1940 Act. The asset coverage ratio is multiplied by $1,000 to determine the “Asset Coverage Per Unit”. |

| (3) | The amount to which such class of senior security would be entitled upon our involuntary liquidation in preference to any security junior to it. The “—” in this column indicates that the SEC expressly does not require this information to be disclosed for certain types of senior securities. |

| (4) | Not applicable to senior securities outstanding as of period end. |

INVESTMENT OBJECTIVE, OPPORTUNITIES AND STRATEGIES

Investment Objective

The Fund’s investment objective is to generate attractive current income from a differentiated portfolio of credit investments, while maintaining capital stability and selectively seeking opportunities for capital appreciation.

Investment Opportunities and Strategies

Under normal circumstances, the Fund will invest at least 80% of its assets in private Loans sourced by the Adviser. These Loans would typically be made by the Fund either (a) directly to borrowers, (b) sourced from or financed in partnership with Non-Bank Finance Companies that the Adviser has a proprietary relationship with, or (c) in some cases, sourced from or financed in partnership with banks or traditional financial institutions that the Adviser has a proprietary relationship with. The Adviser analyzes a broad group of specialty credit and asset-based finance segments, spanning consumer Loans, commercial Loans and Loans with specialized collateral, and seeks to select what the Adviser believes are the best opportunities within the various segments of the asset-based finance market. The Adviser believes that the opportunity set in these specialty credit and asset-based finance segments is attractive, with the potential to generate compelling returns, and highly scalable as banks and traditional financial institutions continue to narrow their lending focus due to market, structural and secular forces. The Fund’s investment strategy is designed to produce a portfolio that is low to moderate duration, high yielding, well collateralized, with consistent cash flow characteristics, a strong risk/return edge and low correlation to liquid or traditional fixed income markets. Through these types of investments, the Adviser seeks to further reduce the overall risk and duration of the Fund’s portfolio and to give the Fund exposure to the continued growth of non-bank finance opportunities5 as banks and traditional financial institutions continue to narrow the focus of their direct lending activities. The form of the Loans that the Adviser will originate for the Fund could include senior credit, structured credit (on a senior or subordinated basis) or other forms of credit-related instruments such as leases, receivables, loan purchase relationships, forward flow programs, preferred instruments or equivalent, or other payment streams. In addition to its primary focus of investing in private Loans, the Adviser will also seek to hold a portion of the Fund’s investment portfolio in certain types of tradeable instruments, which will generally be structured products or ETFs, that are aligned to its broader specialty credit and asset-based finance investment strategy, in order to facilitate liquidity for the Fund and, at certain times, to opportunistically capitalize on market conditions. There is no limit on the maturity or duration of the loans that the Fund will originate. The Fund may invest in additional strategies in the future as opportunities in different strategies present.

The Adviser believes that some of the most compelling reasons for investing in the Fund are:

| ● | Potential for elevated current income resulting from the high interest income that the Fund expects to generate; |

| ● | Focus on private asset-based finance, generally negotiated directly with borrower or counterparty, where the Adviser believes it can earn additional return over the public markets for originating and structuring such deals; |

| ● | Ability of the Fund to be a term and price setter in the Loans due to the Adviser’s direct sourcing, negotiation and structuring of those Loans and/or the credit criteria and portfolio parameters for the lending programs in which they are originated; |

| ● | Collateralized and/or waterfall payment structures (in which subordinate lenders get paid after any senior lender gets paid in full) inherent in specialty credit and asset-based finance that greatly enhance the risk and return profiles of the overall loan portfolio; |

| ● | Portfolio granularity of the Fund’s specialty credit and asset-based finance strategy, with Loans being secured by, or otherwise having exposure to, underlying assets and collateral; |

5 The global assets under management of private credit markets have grown at a compounded annual growth rate of 8% over the last 2 years (Preqin June 2025).

| ● | Lower interest rate risk due to the short duration of its investments; |

| ● | The Adviser’s proprietary investment and portfolio management process, which is meant to reduce annual charge-offs resulting from borrowers defaulting on their loans; and |

| ● | Significant experience of the Adviser, its team members and the Global Credit Solutions investment group of its parent MA Financial Group, which believes it was an early mover in the specialty credit segment, creating a genuine strategic advantage for the Fund. |

The Adviser does not guarantee a specific return to the Shareholders. The Fund does not expect to generate meaningful capital gains or other tax efficient income.

Portfolio Composition

The Fund will invest in a tailored and actively managed portfolio of loans and credit investments in the private credit market, which involves providing financing where banks and traditional financial institutions are not the efficient provider of capital due to market, structural or secular forces, such as increased regulatory requirements on banks, including bank capital rules, market uncertainty impacting regional banks and recent market dislocation resulting in high credit spreads for new loans in the $10 to $50 million range.

The private credit investments fall into three primary sectors as follows:

| ● | Private Asset-Based Finance: Funding granular portfolios of loans, receivables or credits in the asset-based finance segment, typically originated by Non-Bank Finance Companies, or in some cases, banks and traditional financial institutions. The underlying loans or credits in this segment would typically fall within the commercial, consumer or specialty segments. | |

| Examples in the commercial segment, without limitation, include equipment finance, receivables finance, supply chain or inventory finance, bridging loans and business loans. | ||

| Examples in the consumer segment, without limitation, include auto finance, housing related loans, consumer asset finance, general consumer loans and point of sale finance. | ||

| Examples in the specialty segment, without limitation, include healthcare receivables, insurance-related receivables, royalty receivables and litigation finance; |

| ● | Private Direct Lending: Direct private loans, or investing in portfolios of directly negotiated private loans, to borrowers with differentiated characteristics that are originated by the Adviser through its proprietary relationships and channels; and |

| ● | Strategic Lending Partnerships: Primary and secondary liquidity solutions for banks and Non-Bank Finance Companies. |

In addition, to support the Fund in facilitating liquidity and to capitalize opportunistically on market dynamics, the Fund will have an allocation in its portfolio to:

| ● | Tradeable Credit: Investments in tradeable instruments, generally structured products such as CLOs and asset-backed securities, that are aligned to the broader specialty credit and asset-based finance strategy of the Fund, which can be bought and sold in more liquid markets than the Fund’s primary focus in the private loan market; and |

| ● | Cash: An allocation to cash and cash equivalents. |

The Investment Process

The Adviser has adopted a rigorous, five-phase investment process which applies across MA Financial Group’s Global Credit Solutions group (the “Investment Process”). The Investment Process is designed to ensure all investments are thoroughly vetted and evaluated to maximize returns while identifying and controlling for investment and portfolio risks in a disciplined manner. The Investment Process is governed by a dual-structured investment committee (“Investment Committee” or, in short form, “IC”).

Team structure

The Adviser has carefully structured its credit team structure to balance its professionals’ focus on what the Adviser believes are three equally important pillars of operating a successful private credit strategy in the specialty credit segment: (i) investments, (ii) portfolio management, and (iii) risk management.

The Adviser’s teams are split into two distinct groups, facilitating specialization of skill sets while mitigating ml hazard risks and encouraging rigorous debate, robust evaluation of Loans and prudent oversight of the overall portfolio for the Fund:

| ● | Investment Team: A team of investment professionals whose responsibility is to source, diligence and execute new investment opportunities for the Fund (the “Investment Team”). Our Investment Team members also own a Loan for the lifecycle of the deal, ensuring these professionals are accountable and incentivized to achieve the Investment Objective for each Loan from origination to maturity. |

| ● | Portfolio Management Team: The senior executives managing the portfolio for the Fund (“Portfolio Manager(s)” or, in short form, “PM(s)”), supported by a team of portfolio analysts. The Portfolio Management Team is responsible for the rigorous management of the overall Fund portfolio as fiduciaries of Shareholders’ capital. This team is focused on managing overall portfolio dynamics, realizing the investment objective for the Fund in its totality, balancing Portfolio Composition across the different segments within the principal investment strategies, and setting overall strategic investment focus in consultation with the Investment Team and with oversight of the Investment Committee. |

These two functions actively collaborate on a daily basis. They are also encouraged to debate, challenge and engage with each other on the substantive merits of prospective investments or Loans, the robustness of the Fund’s portfolio and the optimal approach to maximize the probability of achieving the Fund’s investment objective.

Both the Investment Team and Portfolio Management Team are responsible collectively to be proactive risk managers at the individual Loan and portfolio level for the Fund. The Adviser considers risk management to be an equal third pillar of success alongside (i) making investments, and (ii) rigorously managing the portfolio of Loans. The Adviser has established a number of formally enshrined and informal culturally-embedded processes to create a disciplined risk management philosophy within its firm and in supporting the Fund.

The Investment Team and Portfolio Management Team are overseen by a robust and empowered Investment Committee that includes highly experienced senior members of the Adviser and its parent MA Financial Group, with complementary and differentiated skill sets.

Phases of the Investment Process

The Investment Team and Portfolio Management Team each play pivotal roles in the Investment Process.

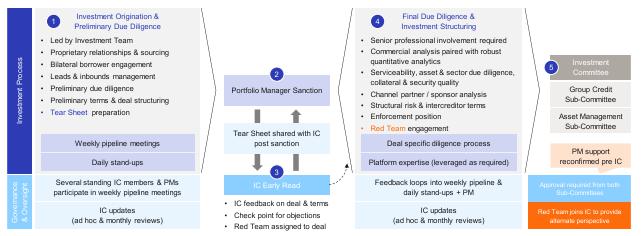

Phase 1 – Investment origination and preliminary due diligence

The Investment Team utilizes their proprietary relationships to source and evaluate potential investment opportunities based on the Adviser’s investment criteria and the Fund’s mandate. As potential opportunities are identified, the relevant Investment Team member(s) engage bilaterally with prospective borrowers and conducts preliminary due diligence to understand their objectives, understand borrower’s commercial and economic fundamentals, evaluate the borrower’s financial performance, creditworthiness and ascertain any potential investment risks.

Based on the results of this preliminary due diligence, the investment team prepares initial terms and structure for the Loan. Finally, the team prepares a tear sheet which summarizes the key information about the Loan and the lending opportunity (a “Tear Sheet”) for review by the Portfolio Manager(s).

Phase 2 – Portfolio Manager sanction

Once an investment opportunity has been identified and been through an adequate preliminary due diligence process by the investment team, the Tear Sheet will be put forward to one of more of the relevant Portfolio Manager to assess. The Portfolio Managers, in conjunction with the broader Portfolio Management Team, act as an additional check in the review process, evaluating the opportunity based on a range of further considerations including (but not limited to):

| ● | alignment with the Fund mandate and investment objective; |

| ● | consistency with the principal investment strategies for the Fund; |

| ● | impact on pro-forma portfolio construction and portfolio composition dynamics; |

| ● | any treasury and risk considerations; and |

| ● | any idiosyncratic issues related to the investment itself. |

Based on this evaluation, the Portfolio Managers will collaborate with the Investment Team to determine whether the opportunity will progress through the investment process.

Phase 3 – Investment Committee Early Read

Where a prospective investment opportunity is sanctioned by the Portfolio Managers, the opportunity progresses through to the Investment Committee for an initial review (known as an “Early Read”). This Early Read allows for a more holistic overview of the prospective Loan and proposed terms, as well as providing a check point for any objections to be raised.

Should there be no objections, the investment team continues evaluating the opportunity.

In addition, a ‘red team’ is assigned to provide an independent, contrarian perspective on any potential risks related to the investment (the “Red Team”). The Red Team is one or more investment professionals of the Adviser that was not directly involved in the origination of the prospective Loan and is not working as part of the main deal team for that potential investment. The Red Team is covered in further detail below.

This phase of the Investment Process is intended to ensure that any focus areas, concerns, structural enhancements to the Loan or other important considerations can be addressed in detail as part of final due diligence, to later be thoroughly considered as part of the Investment Committee process itself.

Phase 4 – Final due diligence and investment structuring

In the final phase of due diligence, overseen by at least one or several senior professionals of the Adviser, commercial and qualitative analysis is paired with robust quantitative analytics for a comprehensive review. The Adviser is generally evaluating the probability of default of the collateral and the loss given the default, and the Adviser then applies that to a specific security. This includes (but is not limited to):

| ● | Thorough asset level due diligence, including key performance drivers; |

| ● | Assessment of serviceability and asset / collateral / security quality; |

| ● | Counterparty / sponsor / originator / channel partner analysis; |

| ● | Critical analysis of management quality; |

| ● | Industry and competitive landscape dynamics; |

| ● | Assessment of structural risk, tail risks and intercreditor terms; |

| ● | Establishment of an enforcement position in the event of a default; and |

| ● | Extensive stress testing based on what the Adviser terms a ‘what you have to believe’ approach, which means understanding the practical dynamics (which could be asset level, business level, economic, market, competitive, commercial, stakeholder, regulatory, or facility structural drivers, among others) that are foundational to obtaining conviction in the prospective investment’s merits, contribution to achieving the investment objective and complementing the Fund’s overall portfolio (the “What You Have To Believe” approach). As part of the What You Have To Believe approach, extensive consideration of the scenarios that would result in the investment being unsuccessful are evaluated alongside what needs to be believed for the investment to be acceptable at a minimum and a success. |

The Fund’s Portfolio Managers must re-confirm support and sanction for the prospective investment before it can proceed to obtain Investment Committee approval.

Phase 5 – Investment Committee

The Investment Committee is the last stage of the Investment Process, where a final decision is made. This forum utilizes the benefit of the multiple lenses of consideration undertaken through the preceding five phases of the Investment Process, to ensure final investment evaluation can be made on a fully informed basis.

In addition to considering the diligence and analysis undertaken throughout the Investment Process, the Investment Committee obtains the perspective of the Red Team. The Red Team is tasked with reviewing the underlying diligence materials related to an investment, and conducting its own research and assessment, to provide a critical independent assessment and/or contrarian opinion on the deal. This is designed to ensure many perspectives are addressed and the Investment Committee is able to make an informed decision.

The Investment Committee is structured with two sub-committees: the Group Credit Sub-Committee which includes senior executives from across MA Financial Group, including its Joint CEO, and an Asset Management Sub-Committee which includes senior executives in MA Financial Group’s Asset Management function, including the Adviser’s Head of Asset Management US. Both Sub-Committees meet together, but vote in separate cohorts. Both Sub-Committees must approve a prospective investment, each on a defined minimum quorum and majority basis.

The Investment Committee considers the investment objective, the principal investment strategies, portfolio composition, credit fundamentals and portfolio dynamics, as well as leveraging its members’ experience, insights and expertise, in making its decision regarding any specific investment.

Investment Process Diagram

The diagram below illustrates the five phases of the Investment Process:

Ongoing investment and portfolio management governance

In addition to the Investment Process outlined above, the Adviser also employs a robust framework for governing and managing investments across the Fund with embedded checks and balances. A number of these frameworks are outlined below.

| Investment Governance | Frequency | Adviser’s Approach |

| Market Analysis | Daily to Weekly | Continuous market analysis, insight gathering, cross-pollination of expertise and feedback loops are utilized by the Adviser, including by leveraging knowledge from across its parent organization MA Financial Group. This includes daily stand-ups and weekly pipeline meetings, among other processes. |

| Investment Committee Portfolio Reviews | Monthly | The Fund’s investment portfolio is thoroughly reviewed on a monthly basis, with oversight of the Investment Committee. Any potential risks or concerns are identified and added to a watch list for further monitoring. |

| Asset Management Reviews | Either Quarterly or Semi-Annually | Adviser and MA Financial Group undertake a comprehensive review of funds on a quarterly or semi-annual basis. During this review, the Fund’s portfolio, achievement of investment objective, efficacy of its principal investment strategies are reviewed, in addition to a range of other investor, treasury, compliance and financing dynamics. |

| Semi-Annual Stress Testing | Semi-Annually | Extensive stress testing and simulation analysis twice per year for substantially all private credit assets within the Fund’s portfolio and managed by the Adviser and MA Financial Group in its Global Credit Solutions group. This exercise estimates the impact on portfolios of three economic downturn scenarios: (i) moderate recession, (ii) severe recession, and (iii) a crisis or depression. In addition, idiosyncratic discrete investment level risks are also assessed on a selective basis, determined by the Investment Committee, Portfolio Management Team and Investment Team’s professional judgement. The stress testing exercise focuses on capital protection strategies in adverse scenarios, as well as considering specific strategies to rectify risks that could emerge. |

It is important to note that the Investment Process is overseen, governed and refined by the Adviser’s Investment Committee and is subject to change at the Investment Committee’s discretion. Variations to the Investment Process for any individual investment or portfolio segment may also be adopted, implemented or ratified (prospectively or retrospectively) by the Investment Committee in its discretion.

In addition, it should be noted that for investments of a smaller size (relative to Fund assets under management) and certain less material decisions regarding the Fund’s investments and portfolio transactions, the Investment Committee may delegate decision making authority up to a threshold (and subject to certain notification and review provisions) to its Portfolio Managers or other such executives of the Adviser.

TYPES OF INVESTMENTS AND RELATED RISKS

Investors should carefully consider the risk factors described below, before deciding on whether to make an investment in the Fund. The risks set out below are not the only risks the Fund faces. Additional risks and uncertainties not currently known to the Fund or that the Fund currently deems to be immaterial also may materially adversely affect the Fund’s business, financial condition and/or operating results. If any of the following events occur, the Fund’s business, financial condition and results of operations could be materially adversely affected. In such case, the NAV of the Fund’s Shares could decline, and investors may lose all or part of their investment.

Investors should be aware that in light of the current uncertainty, volatility and distress in economies, financial markets, and labor and health conditions over the world, the risks below are heightened significantly compared to normal conditions. The fact that a particular risk below is not specifically identified as being heightened under current conditions does not mean that the risk is not greater than under normal conditions.

Risks Relating to the Fund’s Investment Program.

Nature of the Fund’s Investments Risks. The Fund has a very broad mandate with respect to the type and nature of investments in which it participates. While some of the loans in which the Fund will invest may be secured, the Fund may also invest in debt and equity securities that are either unsecured and subordinated to substantial amounts of senior indebtedness, or a significant portion of which may be unsecured. In such instances, the ability of the Fund to influence an issuer’s affairs, especially during periods of financial distress or following an insolvency is likely to be substantially less than that of senior creditors. For example, under terms of subordination agreements, senior creditors are typically able to block the acceleration of the debt or other exercises by the Fund of its rights as a creditor. Accordingly, the Fund may not be able to take the steps necessary to protect its investments in a timely manner or at all. In addition, the debt securities in which the Fund will invest may not be protected by financial covenants or limitations upon additional indebtedness, may have limited liquidity and may not be rated by a credit rating agency.

The borrowers of loans constituting the Fund’s assets may seek the protections afforded by bankruptcy, insolvency and other debtor relief laws. Bankruptcy proceedings are unpredictable as described further below in “Bankruptcy of Borrower Risk.” Additionally, the numerous risks inherent in the insolvency process create a potential risk of loss by the Fund of its entire investment in any particular investment. Insolvency laws may, in certain jurisdictions, result in a restructuring of the debt without the Fund’s consent under the “cramdown” provisions of applicable insolvency laws and may also result in a discharge of all or part of the debt without payment to the Fund.

Debt securities are also subject to other risks, including (i) the possible invalidation of an investment transaction as a “fraudulent conveyance,” (ii) the recovery of liens perfected or payments made on account of a debt in the period before an insolvency filing as a “preference,” (iii) equitable subordination claims by other creditors, (iv) so called “lender liability” claims by the issuer of the obligations (see “Risks Related to Investments in Loans”) and (v) environmental liabilities that may arise with respect to collateral securing the obligations. Additionally, adverse credit events with respect to any issuer, such as missed or delayed payment of interest and/or principal, bankruptcy, receivership, or distressed exchange, can significantly diminish the value of the Fund’s investment in any such company. The Fund’s investments may be subject to early redemption features, refinancing options, pre-payment options or similar provisions which, in each case, could result in the issuer repaying the principal on an obligation held by the Fund earlier than expected. Accordingly, there can be no assurance that the Fund’s investment objective will be realized.

Credit Risk. One of the fundamental risks associated with the Fund’s investments is credit risk, which is the risk that an issuer will be unable to make principal and interest payments on its outstanding debt obligations when due. The Fund’s return to investors would be adversely impacted if an issuer of debt in which the Fund invests becomes unable to make such payments when due.

Although the Fund may make investments that the Adviser believes are secured by specific collateral, the value of which may initially exceed the principal amount of such investments or the Fund’s fair value of such investments, there can be no assurance that the liquidation of any such collateral would satisfy the borrower’s obligation in the event of non-payment of scheduled interest or principal payments with respect to such investment, or that such collateral could be readily liquidated. The Fund may also invest in leveraged loans, high yield securities, marketable and non-marketable common and preferred equity securities and other unsecured investments, each of which involves a higher degree of risk than secured loans. Furthermore, the Fund’s right to payment and its security interest, if any, may be subordinated to the payment rights and security interests of a senior lender, to the extent applicable. Certain of these investments may have an interest-only payment schedule, with the principal amount remaining outstanding and at risk until the maturity of the investment. In addition, loans may provide for payments-in-kind, which have a similar effect of deferring current cash payments. In such cases, an issuer’s ability to repay the principal of an investment may depend on a liquidity event or the long-term success of the company, the occurrence of which is uncertain.

With respect to the Fund’s investments in any number of credit products, if the borrower or issuer breaches any of the covenants or restrictions under the credit agreement that governs loans of such issuer or borrower, it could result in a default under the applicable indebtedness as well as the indebtedness held by the Fund. Such default may allow the creditors to accelerate the related debt and may result in the acceleration of any other debt to which a cross-acceleration or cross-default provision applies. This could result in an impairment or loss of the Fund’s investment or a pre-payment (in whole or in part) of the Fund’s investment.

Issuers in which the Fund invests could deteriorate as a result of, among other factors, an adverse development in their business, a change in the competitive environment or the continuation or worsening of the current (or any future) economic and financial market downturns and dislocations. As a result, companies that the Fund expected to be stable or improve may operate, or expect to operate, at a loss or have significant variations in operating results, may require substantial additional capital to support their operations or maintain their competitive position, or may otherwise have a weak financial condition or experience financial distress. In addition, exogenous factors such as fluctuations of the equity markets also could result in warrants and other equity securities or instruments owned by the Fund becoming worthless.

Credit Spread Risk. Credit spread risk is the risk that credit spreads (i.e., the difference in yield between securities that is due to differences in their credit quality) may increase when the market expects debt securities to default more frequently. Widening credit spreads may quickly reduce the market values of debt securities. In recent years, the U.S. capital markets experienced extreme volatility and disruption following the spread of COVID-19, the impact of heightened geopolitical tensions (including those between the United States and China, Taiwan and mainland China, Israel and Iran and the Axis of Resistance, and between Ukraine and Russia) and other economic disruptions, which increased the spread between yields realized on risk-free and higher risk securities, resulting in illiquidity in parts of the capital markets. Central banks and governments played a key role in reintroducing liquidity to parts of the capital markets. Future exits of these financial institutions from the market may reintroduce temporary illiquidity. These and future market disruptions, including the imposition of tariffs and the prospect of escalating trade wars, and/or illiquidity would be expected to have an adverse effect on the Fund’s business, financial condition, results of operations and cash flows.

Interest Rate Risk. General interest rate fluctuations and changes in credit spreads on floating rate loans may have a substantial negative impact on the Fund’s investments and investment opportunities and, accordingly, may have a material adverse effect on the Fund’s rate of return on invested capital, the Fund’s net investment income and the Fund’s NAV. Certain of the Fund’s debt investments will have variable interest rates that reset periodically based on benchmarks such as SOFR and the prime rate, so an increase in interest rates may make it more difficult for issuers to service their obligations under the debt investments that the Fund will hold. In addition, to the extent the Fund borrows money to make investments, its returns will depend, in part, upon the difference between the rate at which it borrows funds and the rate at which it invests those funds. As a result, there can be no assurance that a significant change in market interest rates will not have a material adverse effect on the Fund’s net investment income to the extent it uses debt to finance its investments. In periods of rising interest rates, the Fund’s cost of funds would increase, which could reduce its net investment income. In general, rising interest rates will negatively impact the price of a fixed rate debt instrument and falling interest rates will have a positive effect on price. Adjustable rate instruments also react to interest rate changes in a similar manner, although generally to a lesser degree (depending, however, on the characteristics of the reset terms, including the index chosen, frequency of reset and reset caps or floors, among other factors). From time to time, the Fund may be exposed to medium- to long-term spread duration securities. Longer spread duration securities have a greater adverse price impact to increases in interest rates. Interest rate sensitivity is generally more pronounced and less predictable in instruments with uncertain payment or prepayment schedules.

If general interest rates rise, there is a risk that the issuers in which the Fund holds floating rate securities will be unable to pay escalating interest amounts, which could result in a default under their loan documents. The potential, however, for the value of a floating rate loan or security to increase in response to interest rate declines is limited. Rising interest rates could also cause issuers to shift cash from other productive uses to the payment of interest, which may have a material adverse effect on their business and operations and could, over time, lead to increased defaults. In addition, rising interest rates may increase pressure on the Fund to provide fixed rate loans, which could adversely affect the Fund’s net investment income, as increases in the cost of borrowed funds would not be accompanied by increased interest income from such fixed-rate investments.

Inflation Risk. Inflation risk is the risk that the value of certain assets or income from the Fund’s investments will be worth less in the future as inflation decreases the value of money. As inflation increases, the real value of investments and distributions can decline. Therefore, the income generated by debt investments may not keep pace with inflation. In addition, during any periods of rising inflation, the dividend rates or borrowing costs associated with the Fund’s use of leverage would likely increase, which would tend to further reduce returns to shareholders. Furthermore, actions by governments and central banking authorities can result in changes in interest rates. Periods of higher inflation could cause such authorities to raise interest rates, and vice versa, which may adversely impact the Fund and its investments.

Prepayment Risk. Prepayment risk relates to the early repayment of principal on a loan or debt security. Loans may be callable at any time, and certain loans may be callable at any time at no premium to par. The Adviser is generally unable to predict the rate and frequency of such repayments. Whether a loan is called will depend both on the continued positive performance of the issuer and the existence of favorable financing market conditions that allow such issuer the ability to replace existing financing with less expensive capital. As market conditions change frequently, the Adviser will often be unable to predict when, and if, this may be possible for each of the Fund’s issuers. Having the loan or other debt instrument called early may have the effect of reducing the Fund’s actual investment income below its expected investment income if the capital returned cannot be invested in transactions with equal or greater yields.

Change of Law Risk. Government counterparties or agencies may have the discretion to change or increase regulation of a issuer’s operations or implement laws or regulations affecting the issuer’s operations, separate from any contractual rights it may have. A portfolio investment also could be materially and adversely affected as a result of statutory or regulatory changes or judicial or administrative interpretations of existing laws and regulations that impose more comprehensive or stringent requirements on such investment. Governments have considerable discretion in implementing regulations and tax reform, including, for example, the possible imposition or increase of taxes on income earned by an issuer or gains recognized by the Fund on its investment in such issuer, that could impact an issuer’s business as well as the Fund’s return on investment with respect to such issuer.

Force Majeure Risk. Issuers may be affected by force majeure events (i.e., events beyond the control of the party claiming that the event has occurred, including, without limitation, acts of God, fire, flood, earthquakes, outbreaks of an infectious disease, pandemic or any other serious public health concern, war, terrorism, trade wars and labor strikes). Some force majeure events may adversely affect the ability of a party (including an issuer or a counterparty to the Fund or an issuer) to perform its obligations until it is able to remedy the force majeure event. In addition, the cost to an issuer or the Fund of repairing or replacing damaged assets resulting from such force majeure event could be considerable. Certain force majeure events (such as war or an outbreak of an infectious disease) could have a broader negative impact on the world economy and international business activity generally, or in any of the countries in which the Fund may invest specifically. Additionally, a major governmental intervention into industry, including the nationalization of an industry or the assertion of control over one or more issuers or its assets, could result in a loss to the Fund, including if its investment in such issuer is canceled, unwound or acquired (which could be without what the Fund considers to be adequate compensation). Any of the foregoing may therefore adversely affect the performance of the Fund and its investments.

Market Risk. The success of the Fund’s activities will be affected by general economic and market conditions, such as interest rates, availability of credit, credit defaults, inflation rates, economic uncertainty, changes in laws (including laws relating to taxation of the Fund’s investments), trade barriers, the imposition, or threatened imposition, of economic sanctions, including tariffs, currency exchange controls, disease outbreaks, pandemics, and national and international political, environmental and socioeconomic circumstances (including wars, terrorist acts or security operations). In addition, the current U.S. political environment and the resulting uncertainties regarding actual and potential shifts in U.S. foreign investment, trade, taxation, economic, environmental and other policies under the current Administration, as well as the impact of heightened geopolitical tensions (including those between the United States and China, Taiwan and mainland China, Israel and Iran and the Axis of Resistance, and between Ukraine and Russia) or other systemic issues or industry-specific economic disruptions, could lead to disruption, instability and volatility in the global markets. The U.S. government may renegotiate some of its global trade relationships with foreign governments and may impose or threaten to impose significant tariffs. The imposition or threatened imposition of tariffs, trade restrictions, currency restrictions and other federal government initiatives as well as foreign policy tensions with foreign nations, including embargoes, sanctions and trade wars, or similar actions (or retaliatory measures taken in response to such actions) could lead to price volatility and overall declines in the U.S. and global investment markets. Unfavorable economic conditions also would be expected to increase our funding costs, limit our access to the capital markets or result in a decision by lenders not to extend credit to us.

Economic sanctions may be, and have been, imposed against certain countries, organizations, companies, entities and/or individuals. Economic sanctions and other similar governmental actions or developments could, among other things, effectively restrict or eliminate the Fund’s ability to purchase or sell certain foreign securities or groups of foreign securities, and thus may make the Fund’s investments in such securities less liquid or more difficult to value. Such sanctions may also cause a decline in the value of securities issued by the sanctioned country or companies located in or economically tied to the sanctioned country and may result in economic disruptions in the sanctioned country and in countries with economic ties to the sanctioned country. When the United States is a significant trading partner of a foreign country in which the Fund may invest or to which the Fund may be exposed, such foreign country may be particularly sensitive to changes in U.S. foreign trading policies, including the threat or actual imposition of tariffs, sanctions or other similar measures. The imposition of tariffs (or threats thereof), trade restrictions, currency restrictions, deficit levels and any reduction plans and other federal government initiatives as well as foreign policy tensions with foreign nations, including embargoes, sanctions and trade wars, or similar actions (or retaliatory measures taken in response to such actions) could lead to price volatility and overall declines in the U.S. and global investment markets. In addition, as a result of economic sanctions and other similar governmental actions or developments, the Fund may be forced to sell or otherwise dispose of foreign investments at inopportune times or prices. Sanctions and other similar measures could significantly delay or prevent the settlement of securities transactions or their valuation, and significantly impact the Fund’s liquidity and performance. Sanctions and other similar measures may in be place for substantial periods of time and enacted with limited advance notice. The type and severity of sanctions and other measures, including counter sanctions and other retaliatory actions, that may be imposed could vary broadly in scope, and their impact is impossible to predict.

Current and historic market turmoil has illustrated that market environments may, at any time, be characterized by uncertainty, volatility and instability. Serious economic disruptions may result in governmental authorities and regulators enacting significant fiscal and monetary policy changes, including by providing direct capital infusions into companies, introducing new monetary programs and considerably increasing or lowering interest rates, which, in some cases resulted in negative interest rates.

As global systems, economies and financial markets are increasingly interconnected, events that once had only local impact are now more likely to have regional or even global effects. Events that occur in one country, region or financial market will, more frequently, adversely impact issuers in other countries, regions or markets. These impacts can be exacerbated by failures of governments and societies to adequately respond to an emerging event or threat. These types of events quickly and significantly impact markets in the U.S. and across the globe leading to extreme market volatility and disruption. The extent and nature of the impact on supply chains or economies and markets from these events is unknown, particularly if a health emergency or other similar event, such as the COVID-19 pandemic, persists for an extended period of time. Similarly, geopolitical and other events, such as actual or threatened war or military conflicts, acts of terrorism, social or political unrest, natural disasters, extreme weather, other geological events, man-made disasters, bank failures, trade wars, inflation, deflation, recessions or other events, and governments’ reactions (as well as responses to government reactions or interventions) to such events, may lead to increased market volatility and instability in world economies and markets generally. Furthermore, technological developments (including those related to artificial intelligence (“AI”)) or failures (such as widespread system outages, disruptions or faulty updates to software applications) and other similar events, each of which may be temporary or may last for extended periods, may impact the value of the Fund’s investments. Adverse changes in one sector or industry or with respect to a particular company could negatively impact companies in other sectors or industries or increase market volatility as a result of the interconnected nature of economies and markets and thus negatively affect the Fund’s performance, even if the Fund does not directly invest in issuers that participate in the sectors or industries experiencing these changes. These types of adverse developments could result from under-regulated markets, novel and maturing markets (for example, the markets for AI, cryptocurrencies and digital or blockchain assets and technologies), systemic risk, natural market forces, bad actors or other scenarios and could negatively affect the Fund’s performance or operations. The value of the Fund’s investment may decrease as a result of such events, particularly if these events adversely impact the operations and effectiveness of the Adviser or key service providers or if these events disrupt systems and processes necessary or beneficial to the investment advisory or other activities on behalf the Fund.

Many of the issuers in which the Fund will make investments may be susceptible to economic slowdowns or recessions and may be unable to repay the loans made to them during these periods. Therefore, non-performing assets may increase and the value of the Fund’s portfolio may decrease during these periods as the Fund is required to record the investments at their current fair value. Adverse economic conditions also may decrease the value of collateral securing some of the Fund’s loans and the value of its investments. Economic slowdowns or recessions could lead to financial losses in the Fund’s portfolio and a decrease in revenues, net income and assets. Unfavorable economic conditions also could increase the Fund’s and the issuers’ funding costs, limit the Fund’s and the issuers’ access to the capital markets or result in a decision by lenders not to extend credit to the Fund or the issuers. These events could prevent the Fund from increasing investments and harm its operating results.

An issuer’s failure to satisfy financial or operating covenants imposed by the Fund or other lenders could lead to defaults and, potentially, acceleration of the time when the loans are due and foreclosure on its secured assets, which could trigger cross-defaults under other agreements and jeopardize the issuer’s ability to meet its obligations under the debt that the Fund holds. The Fund may incur additional expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting issuer. In addition, if one of the issuers were to go bankrupt, depending on the facts and circumstances, including the extent to which the Fund will actually provide significant managerial assistance to that issuer, a bankruptcy court might subordinate all or a portion of the Fund’s claim to that of other creditors.

The prices of financial instruments in which the Fund may invest can be highly volatile. General fluctuations in the market prices of securities may affect the value of the investments held by the Fund. Instability in the securities markets may also increase the risks inherent in the Fund’s investments.

Market Disruptions Risk. The U.S. capital markets have experienced extreme volatility and disruption in recent years following the spread of COVID-19 in the United States, the failure of certain regional banks, military conflicts (including the conflict between Russia and Ukraine and between Israel, Iran and the Axis of Resistance), changes in monetary policies in response to changes in interest rates and inflation and increasing tensions relating to trade relationships, such as between the United States and China. Disruptions in the capital markets have increased the spread between the yields realized on risk-free and higher risk securities, resulting in illiquidity in parts of the capital markets. These and future market disruptions and/or illiquidity would be expected to have an adverse effect on the Fund’s business, financial condition, results of operations and cash flows. Unfavorable economic conditions also would be expected to increase the Fund’s funding costs, limit the Fund’s access to the capital markets or result in a decision by lenders not to extend credit to the Fund. During periods of market disruption, portfolio companies may be more likely to seek to draw on unfunded commitments the Fund has made, and the risk of being unable to fund such commitments is heightened during such periods. These events have limited and could continue to limit the Fund’s investment originations, limit the Fund’s ability to grow and have a material negative impact on the Fund’s operating results and the fair values of the Fund’s debt and equity investments.

U.S. and global markets have also experienced increased volatility as a result of the failures of certain U.S. and non-U.S. banks, which could be harmful to the Fund and issuers in which it invests. For example, if a bank in which the Fund or issuer has an account fails, any cash or other assets in bank accounts may be temporarily inaccessible or permanently lost by the Fund or issuer. If a bank that provides a subscription line credit facility, asset-based facility, other credit facility and/or other services to the Fund or an issuer fails, the Fund or the issuer could be unable to draw funds under its credit facilities or obtain replacement credit facilities or other services from other lending institutions with similar terms. Even if banks used by the Fund and issuers in which the Fund invests remain solvent, volatility in the banking sector could cause or intensify an economic recession, increase the costs of banking services or result in the issuers being unable to obtain or refinance indebtedness at all or on as favorable terms as could otherwise have been obtained. Continued market volatility and uncertainty and/or a downturn in market and economic and financial conditions, as a result of developments in the banking industry or otherwise (including as a result of delayed access to cash or credit facilities), could have an adverse impact on the Fund and issuers in which it invests.

Bankruptcy of Borrower Risk. The issuers of loans constituting the Fund’s assets may seek the protections afforded by bankruptcy, insolvency and other debtor relief laws. When a borrower seeks relief under the U.S. Bankruptcy Code (or has a petition filed against it), an automatic stay prevents all entities, including creditors, from foreclosing or taking other actions to enforce claims, perfect liens or reach collateral securing such claims. Creditors who have claims against the borrower prior to the date of the bankruptcy filing must petition the court to permit them to take any action to protect or enforce their claims or their rights in any collateral. Such creditors may be prohibited from doing so if the court concludes that the value of the property in which the creditor has an interest will be “adequately protected” during the proceedings. If the Bankruptcy Court’s assessment of adequate protection is inaccurate, a creditor’s collateral may be wasted without the creditor being afforded the opportunity to preserve it. Bankruptcy proceedings are inherently litigious, time consuming, highly complex and driven extensively by facts and circumstances, which can result in challenges in predicting outcomes. The equitable power of bankruptcy judges also can result in uncertainty as to the ultimate resolution of claims.

Security interests held by creditors are closely scrutinized and frequently challenged in bankruptcy proceedings and may be invalidated for a variety of reasons. For example, security interests may be set aside because, as a technical matter, they have not been perfected properly under the Uniform Commercial Code or other applicable law. If a security interest is invalidated, the secured creditor loses the value of the collateral and because loss of the secured status causes the claim to be treated as an unsecured claim, the holder of such claim will almost certainly experience a significant loss of its investment.

Risks Relating to the Asset Classes in which the Fund Invests.

Risks Related to Investments in Loans. The Fund invests in loans, generally through a direct origination process. The value of the Fund’s loans may be detrimentally affected to the extent a borrower defaults on its obligations. There can be no assurance that the value assigned by the Adviser can be realized upon liquidation, nor can there be any assurance that any related collateral will retain its value. Furthermore, circumstances could arise (such as in the bankruptcy of a borrower) that could cause the Fund’s security interest in the loan’s collateral to be invalidated. Also, much of the collateral will be subject to restrictions on transfer intended to satisfy securities regulations, which will limit the number of potential purchases if the Fund intends to liquidate such collateral. The amount realizable with respect to a loan may be detrimentally affected if a guarantor, if any, fails to meet its obligations under a guarantee. Finally, there may be a monetary, as well as a time cost involved in collecting on defaulted loans and, if applicable, taking possession of various types of collateral.

The portfolio may include first lien senior secured, second and third lien loans and any other loans.

First Lien Senior Secured Loans. It is expected that when the Fund makes a senior secured term loan investment in an issuer, it will generally take a security interest in substantially all of the available assets of the issuer, including the equity interests of its domestic subsidiaries, which the Fund expects to help mitigate the risk that it will not be repaid. However, there is a risk that the collateral securing the Fund’s loans may decrease in value over time, may be difficult to sell in a timely manner, may be difficult to appraise and may fluctuate in value based upon the success of the business and market conditions, including as a result of the inability of the issuer to raise additional capital, and, in some circumstances, the Fund’s lien could be subordinated to claims of other creditors. In addition, deterioration in an issuer’s financial condition and prospects, including its inability to raise additional capital, may be accompanied by deterioration in the value of the collateral for the loan. Consequently, the fact that a loan is secured does not guarantee that the Fund will receive principal and interest payments according to the loan’s terms, or at all, or that it will be able to collect on the loan should it be forced to enforce its remedies.

Second Lien Senior Secured Loans and Junior Debt investments. Second and third lien loans are subject to the same investment risks generally applicable to senior loans described above. The Fund’s second lien senior secured loans will be subordinated to first lien loans and the Fund’s junior debt investments, such as mezzanine loans, generally will be subordinated to both first lien and second lien loans and have junior security interests or may be unsecured. As such, to the extent the Fund holds second lien senior secured loans and junior debt investments, holders of first lien loans may be repaid before the Fund in the event of a bankruptcy or other insolvency proceeding. Therefore, second and third lien loans are subject to additional risk that the cash flow of the related obligor and the property securing the second or third lien loan may be insufficient to repay the scheduled payments to the lender after giving effect to any senior secured obligations of the related obligor. This may result in an above average amount of risk and loss of principal. Second and third lien loans are also expected to be more illiquid than senior loans.

Unsecured Loans. Unsecured loans are subject to the same investment risks generally applicable to loans described above but are subject to additional risk that the assets and cash flow of the related obligor may be insufficient to repay the scheduled payments to the lender after giving effect to any secured obligations of the obligor. Unsecured loans will be subject to certain additional risks to the extent that such loans may not be protected and such loans are not secured by collateral, financial covenants or limitations upon additional indebtedness. Unsecured loans are also expected to be a more illiquid investment than senior loans for this reason.

Systemic Risks of Loan Portfolios. The Fund may acquire portfolios of loans. While the performance of individual loans within a portfolio generally would be tied to the specific characteristics of the borrower or the collateral securing those loans, such portfolios could be subject to systemic problems that affect a material portion of the loans in the portfolio, due to common characteristics among the underlying borrowers that make them susceptible to certain market or other developments, the underwriting practices of the originator of the loans or other factors.

Structured Finance Securities Risk. The Fund’s portfolios may include investments in structured finance securities, including asset-backed securities, collateralized loan obligations and other instruments. Structured finance securities are, generally, debt securities that entitle the holders thereof to receive payments of interest and principal that depend primarily on the cash flow from or sale proceeds of a specified pool of assets, either fixed or revolving, that by their terms convert into cash within a finite time period, together with rights or other assets designed to assure the servicing or timely distribution of proceeds to holders of such securities. If a particular asset or pool of assets held by the Fund becomes securitized with other assets, the value of such asset or pool of assets may be negatively impacted by the value of such other assets in such securitization transaction and may decrease as a result of the securitization.

Investing in structured finance securities entails various risks: credit risks, liquidity risks, interest rate risks, market risks, operations risks, structural risks, geographical concentration risks, basis risks and legal risks. Structured finance securities are subject to the significant credit risks inherent in the underlying collateral and to the risk that the servicer fails to perform. Accordingly, such securities generally include one or more credit enhancements, which are designed to raise the overall credit quality of the security above that of the underlying collateral. However, insurance providers and other sources of credit enhancement may fail to perform their obligations. Structured finance securities are subject to risks associated with their structure and execution, including the process by which principal and interest payments are allocated and distributed to investors, how credit losses affect the issuing vehicle and the return to investors in such structured finance securities, whether the collateral represents a fixed set of specific assets or accounts, whether the underlying collateral assets are revolving or closed-end, under what terms (including maturity of the structured finance instrument) any remaining balance in the accounts may revert to the issuing entity and the extent to which the entity that is the actual source of the collateral assets is obligated to provide support to the issuing vehicle or to the investors in such structured finance securities. In addition, concentrations of structured finance securities of a particular type, as well as concentrations of structured finance securities issued or guaranteed by affiliated obligors, serviced by the same servicer or backed by underlying collateral located in a specific geographic region, may subject the structured finance securities to additional risk.

Certain structured finance securities that may be held by the Fund may be subordinate in right of payment and rank junior to other securities that are secured by or represent an ownership interest in the same pool of assets. In addition, many of the related transactions have structural features that divert payments of interest and/or principal to more senior classes when the delinquency or loss experience of the pool exceeds certain levels. As a result, such securities have a higher risk of loss due to delinquencies or losses on the underlying assets. In certain circumstances, payments of interest may be reduced or eliminated for one or more payment dates. Additionally, as a result of cash flow being diverted to payments of principal of more senior classes, the average life of such securities may lengthen. Subordinate structured finance securities generally do not have the right to call a default or vote on remedies following a default unless more senior securities have been paid in full. As a result, a shortfall in payments to subordinate investors in structured finance securities will generally result neither in a default being declared on the transaction nor in an acceleration or restructuring of the obligations thereunder. Furthermore, because subordinate structured finance securities may represent a relatively small percentage of the size of an asset pool being securitized, the impact of a relatively small loss on the overall asset pool may be substantial on the holders of such subordinate security.

Structured finance securities are also subject to the risks of the securitized assets. In particular, structured finance securities are subject to risks related to the quality of the control systems and procedures used by the parties originating and servicing the securitized assets. Deficiencies in these systems may result in higher-than-expected borrower delinquencies or other factors affecting the value of the underlying assets, such as the inability to effectively pursue remedies against borrowers due to defective documentation. The Fund may rely upon representations of the securitization vehicles in respect of control systems and the securitized assets and conduct little or no diligence in respect of them. Accordingly, there can be no assurance that the control systems and the securitized assets will not be defective in a manner that could adversely affect the Fund.

High Yield Debt. The Fund may invest in debt securities that may be classified as “higher-yielding” (and, therefore, higher-risk) debt securities (also known as “junk bonds”). In most cases, such debt will be rated below “investment grade” or will be unrated and will face both ongoing uncertainties and exposure to adverse business, financial or economic conditions and the issuer’s failure to make timely interest and principal payments. The market for high yield securities (junk bonds) has experienced periods of volatility and reduced liquidity. High yield securities (junk bonds) may or may not be subordinated to certain other outstanding securities and obligations of the issuer, which may be secured by all or substantially all of the issuer’s assets. High yield securities (junk bonds) may also not be protected by financial covenants or limitations on additional indebtedness. The market values of certain of these debt securities may reflect individual corporate developments. General economic recession or a major decline in the demand for products and services in the industry in which the borrower operates would likely have a materially adverse impact on the value of such securities or could adversely affect the ability of the issuers of such securities to repay principal and pay interest thereon and increase the incidence of default of such securities. In addition, adverse publicity and investor perceptions, whether or not based on fundamental analysis, may also decrease the value and liquidity of these high yield debt securities (junk bonds).

Equity Investments. When the Fund invests in loans, it may acquire equity securities as well. In addition, the Fund may invest directly in the equity securities of issuers. The Fund’s goal is ultimately to dispose of such equity interests and realize gains upon its disposition of such interests. However, the equity interests received may not appreciate in value and, in fact, may decline in value. Accordingly, the Fund may not be able to realize gains from its equity interests, and any gains that it does realize on the disposition of any equity interests may not be sufficient to offset any other losses experienced.

The value of the Fund’s portfolio may be affected by changes in the equity markets generally. Equity markets may experience significant short-term volatility and may fall sharply at times. Different markets may behave differently from each other and U.S. equity markets may move in the opposite direction from one or more foreign stock markets. Adverse events in any part of the equity or fixed-income markets may have unexpected negative effects on other market segments. The prices of individual equity securities generally do not all move in the same direction at the same time and a variety of factors can affect the price of a particular company’s securities. These factors may include, but are not limited to, poor earnings reports, a loss of customers, litigation against the company, general unfavorable performance of the company’s sector or industry, or changes in government regulations affecting the company or its industry.

Additionally, there are special risks associated with investing in preferred securities, including risks related to deferral, subordination, liquidity, limited voting rights and special redemption rights.

Exchange-Traded Funds. ETFs are investment companies whose shares are listed on a securities exchange and trade like a stock throughout the day. Certain ETFs use a “passive” investment strategy and will not attempt to take defensive positions in volatile or declining markets. Other ETFs are actively managed (i.e., they do not seek to replicate the performance of a particular index). Investments in ETFs are subject to a variety of risks, including risks of a direct investment in the underlying securities that the ETF holds. For example, the general level of stock prices may decline, thereby adversely affecting the value of the underlying common stock investments of the ETF and, consequently, the value of the ETF. Moreover, the market value of the ETF may differ from the value of its portfolio holdings because the market for ETF shares and the market for underlying securities are not always identical. Also, ETFs that track particular indices typically will be unable to match the performance of the index exactly due to the ETF’s operating expenses and transaction costs, among other things.

The Fund may invest in the securities of other investment companies to the extent that such investments are consistent with the Fund’s investment objective and permissible under the 1940 Act. Under one provision of the 1940 Act, the Fund may not acquire the securities of other investment companies if, as a result, (i) more than 10% of the Fund’s total assets would be invested in securities of other investment companies, (ii) such purchase would result in more than 3% of the total outstanding voting securities of any one investment company being held by the Fund or (iii) more than 5% of the Fund’s total assets would be invested in any one investment company. In some instances, the Fund may invest in an investment company in excess of these limits. For example, the Fund may invest in ETFs in excess of the statutory limits imposed by the 1940 Act in reliance on Rule 12d1-4 under the 1940 Act. These investments would be subject to the applicable conditions of Rule 12d1-4, which in part would affect or otherwise impose certain limits on the investments and operations of the underlying fund. Accordingly, if the Fund serves as an “underlying fund” to another investment company, the Fund’s ability to invest in other investment companies, private funds and other investment vehicles may be limited and, under these circumstances, the Fund’s investments in other investment companies, private funds and other investment vehicles will be consistent with applicable law and/or exemptive relief obtained from the SEC. The Fund, as a holder of the securities of other investment companies, will bear its pro rata portion of the other investment companies’ expenses, including advisory fees. These expenses will be in addition to the direct expenses incurred by the Fund.