S-K 1604, De-SPAC Transaction

Apr. 28, 2026

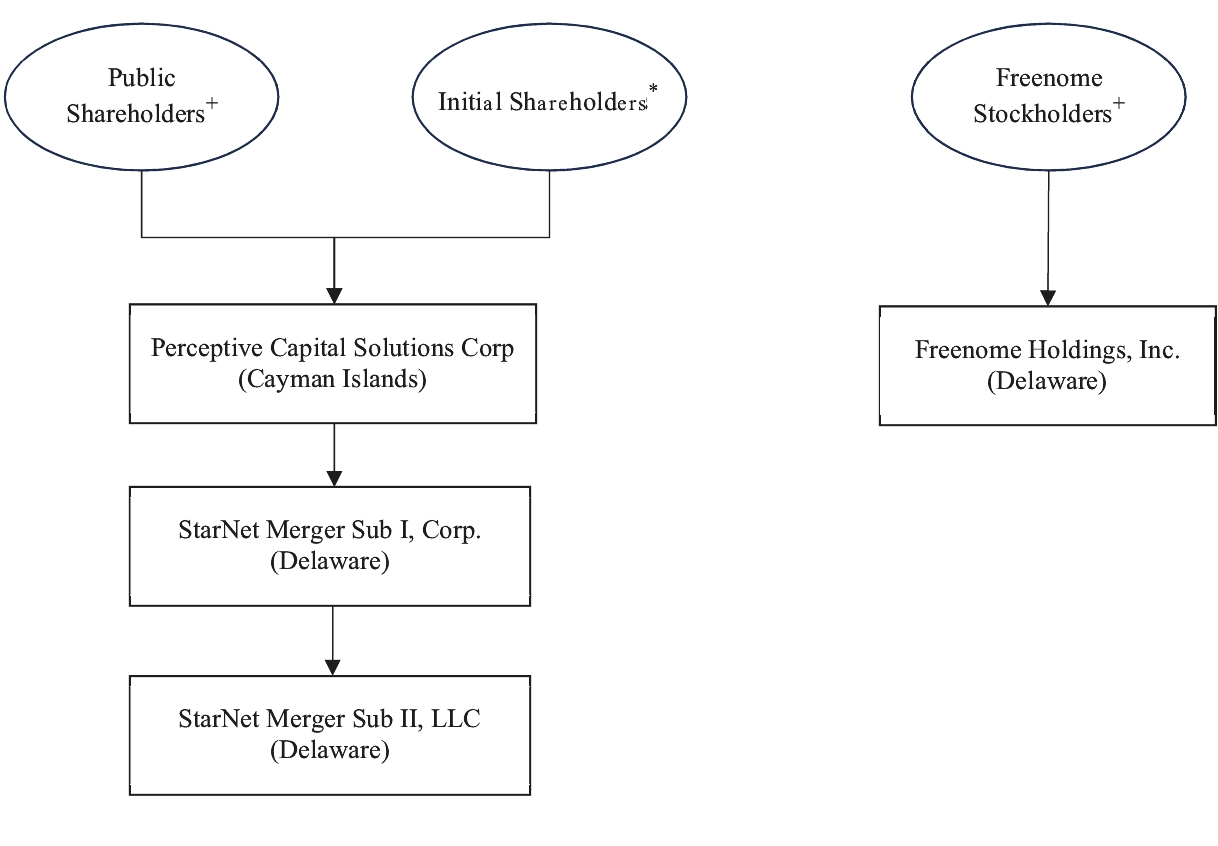

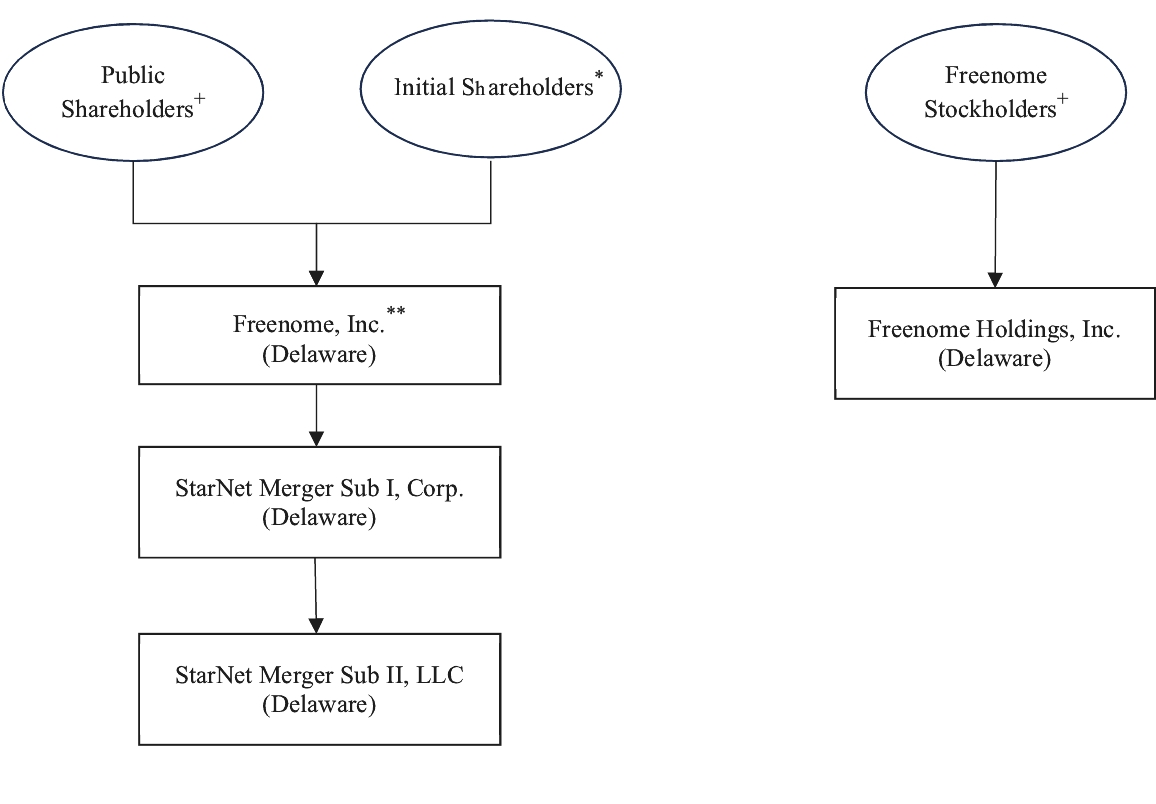

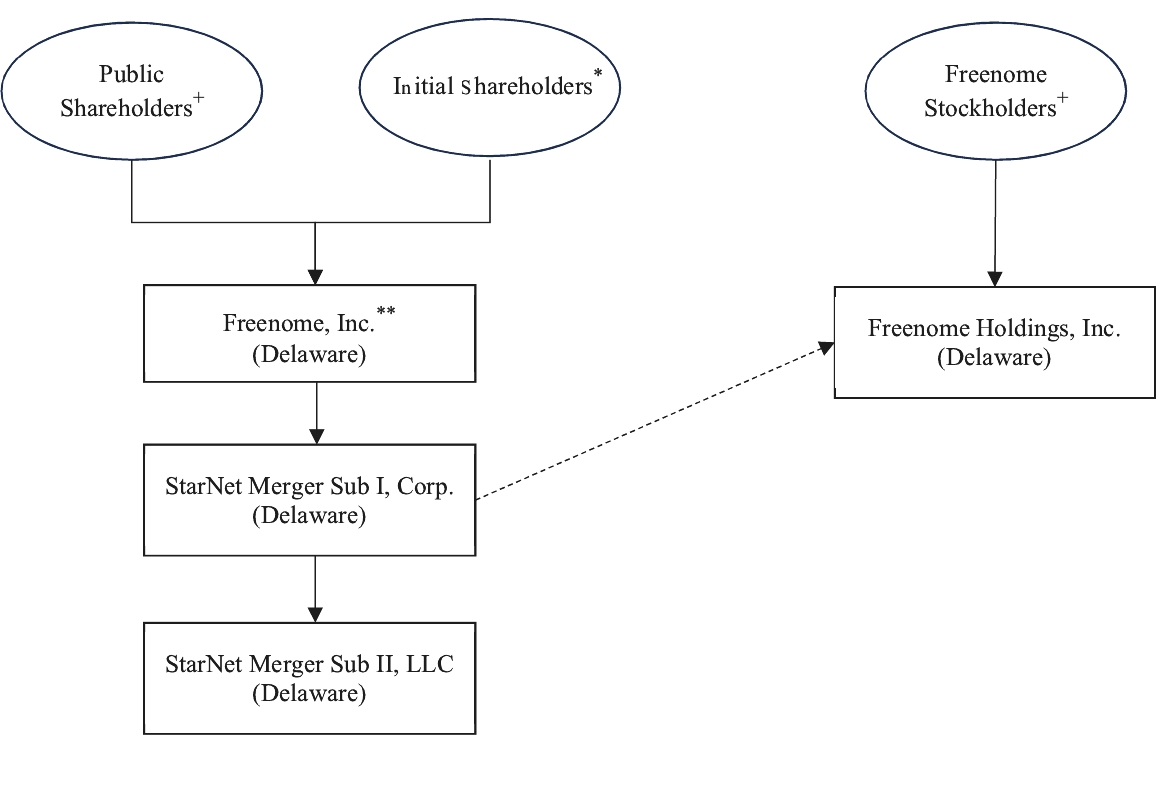

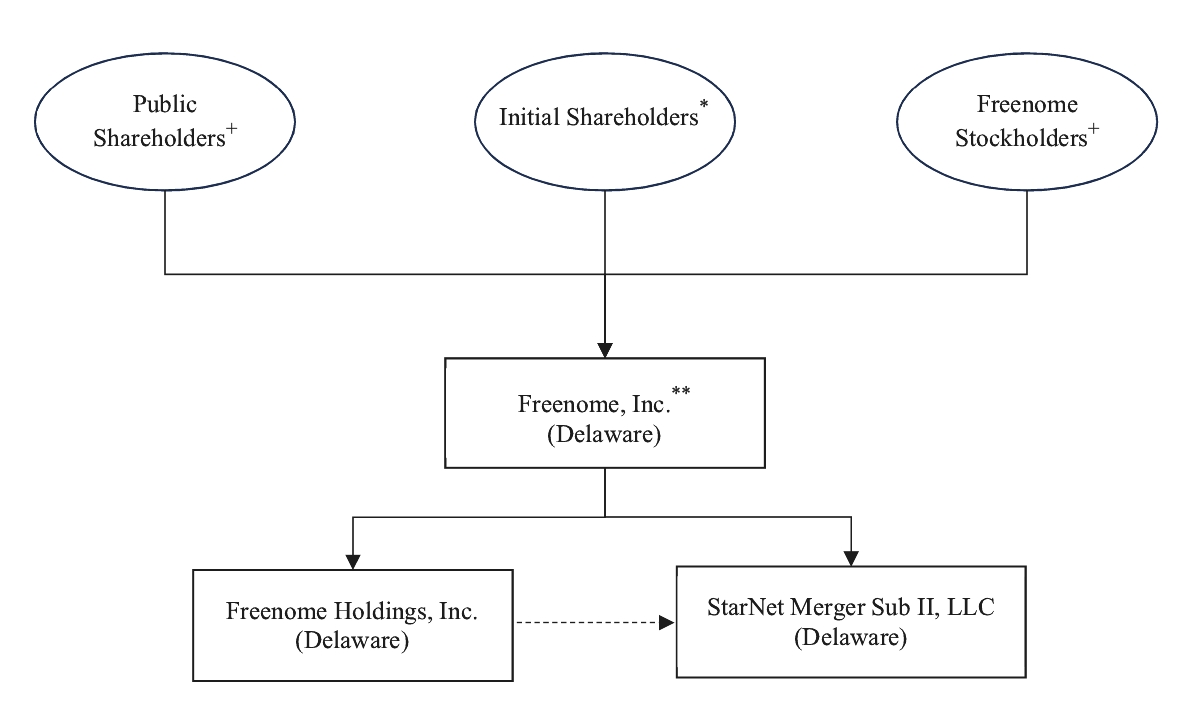

On December 4, 2025, the board of directors (the “PCSC Board”) of Perceptive Capital Solutions Corp, a Cayman Islands exempted company (“PCSC,” “we,” “us” or “our”), based on the unanimous recommendation of the special committee of the PCSC Board, unanimously approved the Business Combination Agreement, dated December 5, 2025 (as it may be amended, supplemented, or otherwise modified from time to time, the “Business Combination Agreement”), by and among PCSC, StarNet Merger Sub I, Corp., a Delaware corporation and wholly-owned subsidiary of PCSC (“Merger Sub I”), StarNet Merger Sub II, LLC, a Delaware limited liability company and wholly-owned subsidiary of PCSC (“Merger Sub II”) and Freenome Holdings, Inc., a Delaware corporation (“Freenome”), pursuant to which the following will occur: (a) at least one business day prior to the Closing Date (as defined below), PCSC will de-register from the Register of Companies in the Cayman Islands and transfer by way of continuation from the Cayman Islands to Delaware and domesticate as a Delaware corporation in accordance with Section 388 of the General Corporation Law of the State of Delaware and Part 12 of the Companies Act (Revised) of the Cayman Islands (the “Domestication”), upon which PCSC will change its name to “Freenome, Inc.” (“New Freenome”); (b) Merger Sub I will merge with and into Freenome, with Freenome as the surviving company in the merger (the “First Merger”) and, after giving effect to the First Merger (such time being the “Effective Time”), Freenome will be a wholly-owned subsidiary of PCSC, (c) as soon as practicable following the Effective Time, but no later than one business day following the Effective Time, Freenome, as the surviving corporation of the First Merger, will merge with and into Merger Sub II (the “Second Merger” and together with the First Merger, the “Mergers”), with Merger Sub II continuing as the surviving company in the Second Merger, and (d) the other transactions contemplated by the Business Combination Agreement and documents related thereto (such transactions, together with the Domestication and the Mergers, the “Business Combination”), all as described in more detail in the accompanying proxy statement/prospectus. The consummation of the Business Combination is referred to as the “Closing” and the date of the Closing, the “Closing Date.” References herein to New Freenome denote PCSC following the Business Combination. A copy of the Business Combination Agreement is attached to the accompanying proxy statement/prospectus as Annex A.

In connection with the execution of the Business Combination Agreement, on December 5, 2025, PCSC entered into subscription agreements (the “Subscription Agreements”) with certain qualified institutional buyers, institutional accredited investors, and other accredited investors, including, among others, Perceptive Life Sciences Master Fund, Ltd., a Cayman Islands exempted company (the “Perceptive PIPE Investor”) and an affiliate of Perceptive Capital Solutions Holding, a Cayman Islands exempted company (the “Sponsor”), as well as certain existing stockholders of Freenome (the “PIPE Investors”). Pursuant to the Subscription Agreements, the PIPE Investors agreed to subscribe for and purchase, and PCSC agreed to issue and sell to the PIPE Investors, on the Closing Date immediately following the Closing, an aggregate of 24,000,000 shares of New Freenome Common Stock (the “PIPE Shares”) for a purchase price of $10.00 per share, and aggregate gross proceeds of $240.0 million (the “PIPE Financing”). The obligations of each party to consummate the PIPE Financing are conditioned upon, among other things, (i) the New Freenome Common Stock (including the New Freenome Common Stock issuable to the PIPE Investors pursuant to the Subscription Agreements) having been approved for listing on Nasdaq; and (ii) satisfaction of all conditions precedent to the closing of the transactions set forth in the Business Combination Agreement. The obligations of the PIPE Investors to consummate the PIPE Financing are further subject to additional conditions, including, among other things: (i) the Business Combination Agreement shall not have been amended, modified, or supplemented, and no condition waived thereunder, in a manner that would reasonably be expected to materially and adversely affect the economic benefits that a PIPE Investor would reasonably expect to receive under the Subscription Agreement; (ii) the material truth and accuracy of the representations and warranties of PCSC in the Subscription Agreement, subject to customary bringdown standards; (iii) no subscription agreement, or other agreements or understandings (including side letters) entered into in connection with the sale of New Freenome Common Stock under the Subscription Agreements, with any other PIPE Investors shall have been amended, modified, or waived in any manner that benefits such other PIPE Investor unless all PIPE Investors have been offered substantially the same benefits; and (iv) there has not occurred any material adverse effect or parent material adverse effect since the date of the Subscription Agreement that is continuing. See “Business Combination Proposal—Related Agreements—PIPE Financing.”

Compensation to be Received by the Sponsor, the Perceptive PIPE Investor, and PCSC’s Officers and Directors in Connection with the Business Combination and PIPE Financing: Assuming the Aggregate Transaction Proceeds Condition Redemptions Scenario, the Sponsor will receive (i) 2,066,250 shares of New Freenome Common Stock upon the exchange of 2,066,250 PCSC Class B Shares, which were initially purchased in connection with PCSC’s initial public offering for approximately $0.01 per share and (ii) 286,250 shares of New Freenome Common Stock upon the exchange of 286,250 PCSC Class A Shares, which were initially purchased in a private placement that closed concurrently with PCSC’s initial public offering for $10.00 per share. The Perceptive PIPE Investor will receive (i) 5,500,000 shares of New Freenome Common Stock, which is equal to the Perceptive PIPE Investor’s $55.0 million PIPE Financing commitment divided by $10.00, the price per share of the PIPE Financing, and (ii) an estimated 5,615,003 shares of New Freenome Common Stock upon the exchange of Freenome capital stock, each of which is equal to $56.2 million divided by $10.00 per share, which is the assumed per share price used in the Business Combination pursuant to the Business Combination Agreement. PCSC’s independent directors (Messrs. McKenna, Song and Waksal) will each receive 30,000 shares of New Freenome Common Stock upon the exchange of 30,000 PCSC Class B Shares held by them. The securities to be issued to the Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors may result in a material dilution of the equity interests of non-redeeming public shareholders. See “Dilution,” and “Information About PCSC—Executive Compensation and Director Compensation.”

The Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors will also be reimbursed for loans, advances, and out-of-pocket expenses incurred by them related to identifying, negotiating, investigating and completing the Business Combination. No such loans, advances, or out-of-pocket expenses are outstanding as of the date of this proxy statement/prospectus. In addition, PCSC has agreed to pay the Sponsor $15,000 per month for office space, secretarial and administrative services and the Sponsor and PCSC’s officers and directors will be entitled to continued indemnification and the continuation of directors’ and officer’s liability insurance after the Business Combination.

PCSC’s independent directors are not members of the Sponsor and are not affiliates of the Perceptive PIPE Investor. None of the funds in the trust account will be used to compensate PCSC’s officers or directors. Except for administrative services fees and office rental fees paid or to be paid to the Sponsor, no compensation of any kind, including finder’s and consulting fees, have been paid or will be paid to the Sponsor, officers and directors, or any of their respective affiliates, for services rendered prior to or in connection with the completion of the Business Combination. However, these individuals will be reimbursed for any out-of-pocket expenses incurred in connection with activities performed on our behalf such as identifying potential target businesses and performing due diligence on suitable business combinations, as discussed above. The reimbursement of expenses and advances to the Sponsor, and PCSC’s officers and directors may result in a material dilution of the equity interests of non-redeeming public shareholders. See “Dilution,” and “Information About PCSC—Executive Compensation and Director Compensation.”

On December 4, 2025, the Special Committee received an opinion from Scalar as to the fairness, from a financial point of view, to PCSC and the PCSC Unaffiliated Shareholders of the shares of New Freenome Common Stock to be paid by PCSC in the First Merger pursuant to the Business Combination Agreement, a copy of which is attached hereto as Annex L. For more information, see “Business Combination Proposal—Background and Material Terms of the Business Combination,” “Business Combination Proposal—Interests of PCSC’s Sponsor, Directors and Officers in the Business Combination” and “Business Combination Proposal—Opinion of Scalar, LLC.”

SUMMARY OF THE PROXY STATEMENT/PROSPECTUS

This summary highlights selected information from this proxy statement/prospectus and does not contain all of the information that is important to you. To better understand the proposals to be submitted for a vote at the extraordinary general meeting, including the Business Combination, you should read this proxy statement/prospectus, including the Annexes, such as the Business Combination Agreement attached as Annex A to this proxy statement/prospectus and other documents referred to herein, carefully and in their entirety. The Business Combination Agreement is the legal document that governs the Business Combination and the other transactions that will be undertaken in connection with the Business Combination. The Business Combination Agreement is also described in detail in this proxy statement/prospectus in the section entitled “Business Combination Proposal—The Business Combination Agreement.”

Parties to the Business Combination

Perceptive Capital Solutions Corp

PCSC is a blank check company incorporated on March 22, 2024 as a Cayman Islands exempted company formed for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses.

PCSC Class A Shares are currently listed on Nasdaq under the symbol “PCSC.”

PCSC’s principal executive offices are located at 51 Astor Place, 10th Floor, New York, New York 10003, and its phone number is (212) 284-2300.

StarNet Merger Sub I, Corp.

Merger Sub I is a Delaware corporation and wholly-owned subsidiary of PCSC. Merger Sub I was formed solely for the purpose of effecting the Business Combination and has not carried on any activities other than those in connection with the Business Combination. The address and telephone number for Merger Sub I’s principal executive offices are the same as those for PCSC.

StarNet Merger Sub II, LLC

Merger Sub II is a Delaware limited liability company and wholly-owned subsidiary of PCSC. Merger Sub II was formed solely for the purpose of effecting the Business Combination and has not carried on any activities other than those in connection with the Business Combination. The address and telephone number for Merger Sub II’s principal executive offices are the same as those for PCSC.

Freenome Holdings, Inc.

Freenome is a development stage, early cancer detection company developing blood-based screening tests leveraging a proprietary artificial intelligence/machine learning multiomics technology platform to transform multi-cancer and ultimately multi-disease detection.

Freenome is developing a range of blood-based cancer screening tests. Its lead product, SimpleScreen CRC (v1), has been submitted to the FDA for premarket approval, with a decision expected in 2026, and an improved version is also in development. A blood-based lung cancer test aimed at high-risk individuals is on track to launch in the second half of 2026 . Freenome also recently initiated a clinical study which will inform its plans and timing with respect to a regulatory submission to the FDA to support clinical validation of an in vitro device. Looking ahead, Freenome’s preliminary strategy is to eventually expand its platform to screen for more than ten types of cancer, with a broader general-population offering planned for the longer term, each subject to regulatory approval.

Freenome currently has no products approved for commercial sale in the United States and has not generated any material revenue to date, and it continues to incur significant R&D and other expenses related to ongoing operations. Freenome’s ability to generate product revenue sufficient to achieve profitability, if ever, will depend on premarket approval of the SimpleScreen CRC (v1) and future development of multi-cancer early detection tests.

Freenome has incurred operating losses in each year since its inception. Freenome’s net losses were $219.3 million and $274.4 million for the years ended December 31, 2025 and 2024, respectively. As of December 31, 2025, Freenome had an accumulated deficit of $1.3 billion.

Freenome’s principal executive offices are located at Genesis Marina, 3300 Marina Blvd, Brisbane, California 94005, and its phone number is (650) 446-6630.

Background and Material Terms of the Business Combination

PCSC is a blank check company formed for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. Following the completion of its initial public offering on June 13, 2024, at the direction of the PCSC Board, representatives of PCSC, including Messrs. Stone and Poukalov, and Dr. Hukkelhoven commenced an active, targeted search for potential business combination candidates, leveraging the Sponsor’s network of investment bankers, private equity firms and hedge funds (including Perceptive Advisors and its affiliates), consulting firms, legal and accounting firms, and numerous other business relationships, as well as the prior experience and network of PCSC’s officers and directors. During this targeted search, PCSC reviewed approximately 200 potential business combination targets and conducted varying levels of preliminary due diligence on each, and evaluated and analyzed each as a potential business combination target based on, among other things, publicly available information and other market research available to PCSC and its representatives and their existing knowledge of the potential targets as a result of their network and existing relationships. Between October 2024 and December 2024, PCSC submitted non-binding term sheets to two companies, neither of which progressed to a business combination. Thereafter, PCSC continued to assess other potential business combination targets. Through this process, and based on discussion with members of the PCSC Board, PCSC further refined its focus and determined to concentrate its near-term efforts on a smaller set of potential business combination targets, including Freenome, that PCSC believed were the most compelling opportunities relative to the others reviewed.

On February 19, 2025, Dr. Hukkelhoven, in her capacity as an executive officer of the Perceptive PIPE Investor, reached out to the other members of the Freenome Board, consisting of Deepika Pakianathan, Douglas VanOort, Randal Scott, Peter Kolchinsky, Moritz Hartmann, and Josh Lauer, to inquire whether Freenome would be interested in exploring a potential business combination with PCSC. The Perceptive PIPE Investor, was as of such time, and remains, an existing investor in Freenome, and Dr. Hukkelhoven, an executive officer of the Perceptive PIPE Investor, was as of such time, and remains, a member of the Freenome Board. As the Perceptive PIPE Investor has been an investor in Freenome since 2019, the Perceptive PIPE Investor has continuously monitored Freenome’s business progress and capital needs. Dr. Hukkelhoven has been a representative appointed by the Perceptive PIPE Investor on the Freenome Board since 2020. At the direction of the Freenome Board, Dr. Hukkelhoven informed the Perceptive PIPE Investor that Freenome was interested in exploring a capital raising transaction involving the Perceptive PIPE Investor and Dr. Hukkelhoven proposed the terms of the PIPE Financing to the Perceptive PIPE Investor. For more information, see “Business Combination Proposal — Interests of PCSC’s Sponsor, Directors and Officers in the Business Combination.”

The key terms of the Business Combination Agreement are the result of extensive negotiations between the representatives of PCSC and Freenome, each in consultation with its advisors, which occurred between mid-May 2025 through early August 2025. During such period, Freenome was also negotiating its exclusive licensing agreement with Exact Sciences Corporation (“Exact Sciences”) to advance the commercialization of Freenome’s colorectal (CRC) blood-based screening test, which was ultimately signed and announced on August 6, 2025 (the “Exact Sciences Transaction”). The terms of the Exact Sciences Transaction included an upfront payment by Exact Sciences to Freenome of $75 million, as well as potential milestone payments of up to $700 million in connection with specified regulatory developments, royalties on test sales, $20 million in funding for joint R&D expenses leveraging the technology for three years and a convertible note of $50 million at an interest rate of 5% per annum.

On August 6, 2025, PCSC and Freenome executed the Non-Binding Term Sheet, setting out the material terms of the Business Combination, including that Freenome would be valued at approximately $1.05 billion on a post-Business Combination equity value basis, taking into account, among other things, (i) an assumed $300 million in aggregate proceeds from (a) the PIPE Financing (which would include at least $25 million expected to be contributed by Perceptive Advisors or its affiliates and at least $50 million expected to be contributed by RA Capital or its affiliates) and (b) the Trust Account at the closing, and (ii) an agreed pre-Business Combination base equity value for Freenome of $725 million. The Non-Binding Term Sheet further contemplated, among other things, (a) certain adjustments for leakage to the Freenome base equity value, (b) that any proceeds from the Exact Sciences Transaction or any transaction entered into with Roche would not be counted as part of the base equity value of Freenome and that any shares or other equity interests of Freenome issued and outstanding in connection with such transactions would not be taken into account as part of the Freenome shares outstanding as of immediately prior to the closing of the Business Combination

for purposes of determining the applicable Exchange Ratio, (c) that in addition to other customary closing conditions, the obligation of Freenome to consummate the Business Combination would be subject to there being Aggregate Transaction Proceeds of at least $250,000,000, (d) a six-month lockup period after consummation of the Business Combination with respect to New Freenome shares to be issued to insider Freenome stockholders, including Perceptive Advisors and RA Capital, in the Business Combination, as well as certain demand and piggyback registration rights for certain stockholders, and (e) an Exclusivity Period binding on both PCSC and Freenome.

Between October 6, 2025 and December 4, 2025, PCSC and Freenome, with the assistance of their respective advisors, exchanged and negotiated drafts of the definitive Business Combination Agreement, the disclosure schedules to the Business Combination Agreement and the other ancillary documents, including the Investor Rights Agreement, the Transaction Support Agreement, the New Freenome certificate of incorporation and bylaws, the Lock-Up Agreement and the Sponsor Letter Agreement.

Concurrently with the execution of the Business Combination Agreement and the related ancillary documents, on December 5, 2025, the PIPE Investors executed and delivered the Subscription Agreements, which provided for binding subscriptions to purchase an aggregate of 24,000,000 shares of New Freenome Common Stock at $10.00 per share.

As contemplated by the Business Combination Agreement, the structure and timing of the Business Combination and the PIPE Financing are consistent with common practice in initial business combination transactions consummated by special purpose acquisition companies. In addition, the timing for the consummation of the Business Combination provided for in the Business Combination Agreement and the Subscription Agreements, which was effectively as soon as reasonably practicable following the execution of the Business Combination Agreement, was determined and agreed by the parties in light of general business considerations weighing in favor of consummating the transaction promptly and the deadline for PCSC to complete an initial business combination by June 13, 2026 (unless otherwise extended).

For more information, see “Business Combination Proposal—Background and Material Terms of the Business Combination.”

The Business Combination Agreement

Pursuant to the Business Combination Agreement: (a) at least one business day prior to the Closing Date, PCSC will de-register from the Register of Companies in the Cayman Islands and transfer by way of continuation from the Cayman Islands to Delaware and domesticate as a Delaware corporation in accordance with Section 388 of the General Corporation Law of the State of Delaware and Part 12 of the Companies Act (Revised) of the Cayman Islands, upon which PCSC will change its name to “Freenome, Inc.”; (b) Merger Sub I will merge with and into Freenome, with Freenome as the surviving company in the merger and, after giving effect to the First Merger, Freenome will be a wholly-owned subsidiary of PCSC, (c) as soon as practicable following the Effective Time, but no later than one business day following the Effective Time, Freenome, as the surviving corporation of the First Merger, will merge with and into Merger Sub II, with Merger Sub II continuing as the surviving company in the Second Merger, and (d) the other transactions contemplated by the Business Combination Agreement and documents related thereto, all as described in more detail in the accompanying proxy statement/prospectus. References herein to New Freenome denote PCSC following the Business Combination.

As further described in the accompanying proxy statement/prospectus,

• | the Domestication is intended to occur at least one business day prior to the Closing Date. In connection with the Domestication, (1)(a) immediately prior to the Domestication, the holders of each issued and outstanding PCSC Class B Share will elect to convert their PCSC Class B Shares into PCSC Class A Shares, (b) immediately prior to the Domestication, PCSC will effect the redemption of the public shares initially issued in PCSC’s initial public offering that are validly submitted for redemption and not withdrawn, (c) and after effecting the PCSC Shareholder Redemptions, upon the Domestication, each issued and outstanding PCSC Class A Share will convert automatically by operation of law, on a one-for-one basis, into one share of New Freenome Common Stock, and (2) upon the Domestication, the governing documents of PCSC will become the certificate of incorporation and the bylaws as described in this proxy statement/prospectus and attached as Annex H and Annex I, and PCSC’s name will change to “Freenome, Inc.”; and |

• | at the Effective Time, (i) the Freenome Common Shares issued and outstanding as of immediately prior to the Effective Time (including such shares issued upon the conversion of all shares of Freenome preferred stock into Freenome Common Shares prior to the Effective Time in accordance with the terms of the Business Combination Agreement, but excluding Freenome Common Shares held in treasury or by Freenome |

stockholders who have properly demanded appraisal of such Freenome Common Shares in accordance with Section 262 of the DGCL) will be automatically canceled and extinguished and converted into the right to receive a number of shares of New Freenome Common Stock equal to the Exchange Ratio, which is based on an implied Freenome base equity value of $725,000,000 and subject to certain adjustments as set forth in the Business Combination Agreement; (ii) each Freenome Option, whether vested or unvested, will cease to represent the right to purchase Freenome Common Shares and will be canceled in exchange for a Rollover Option under the New Freenome Equity Incentive Plan, in an amount equal to the product (rounded down to the nearest whole number) of (x) the number of Freenome Common Shares subject to such Freenome Option immediately prior to the Effective Time, multiplied by (y) the Exchange Ratio, at an exercise price per share (rounded up to the nearest whole cent) equal to the quotient of (i) the exercise price per share of such Freenome Option immediately prior to the Effective Time, divided by (ii) the Exchange Ratio, and generally subject to the same terms and conditions (including applicable vesting, expiration and forfeiture provisions) that applied to the corresponding Freenome Option immediately prior to the Effective Time; and (iii) each Freenome RSU Award, whether vested or unvested, will cease to have any rights in respect of the Freenome Common Shares and will be canceled in exchange for a Rollover RSU Award that settles in a number of shares of New Freenome Common Stock (rounded down to the nearest whole share) in an amount and subject to such terms and conditions, in each case, as to be set forth on an allocation schedule, that will generally be subject to the same terms and conditions (including applicable vesting, expiration and forfeiture provisions) that applied to the corresponding Freenome RSU Award immediately prior to the Effective Time.

For more information about the Business Combination, please see the section titled “Business Combination Proposal—The Business Combination Agreement.” A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A.

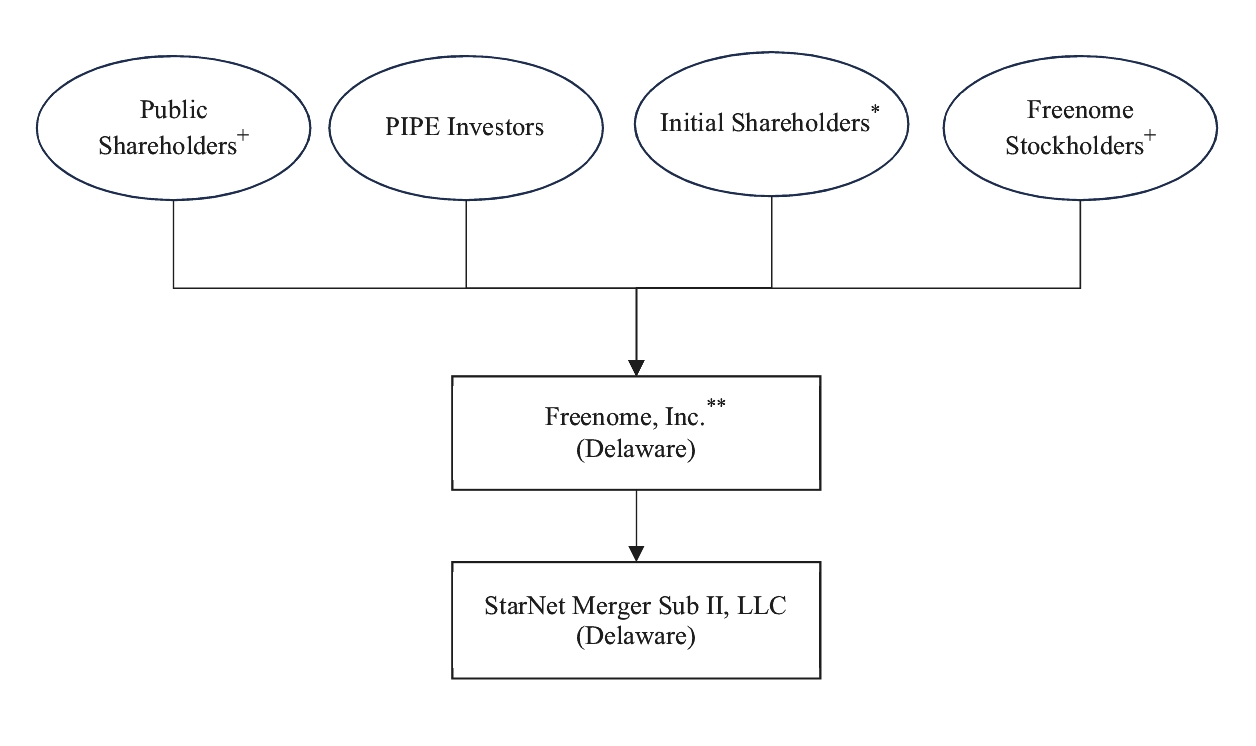

Structure Diagrams

The following diagrams illustrate in simplified terms the current structure of PCSC and Freenome, the Business Combination, and the expected structure of Freenome immediately following the Closing.

Simplified Pre-Combination Structure

The Domestication

The First Merger

The Second Merger

Simplified Post-Combination Structure

+ | Includes the Perceptive PIPE Investor. |

* | The Sponsor and PCSC’s independent directors (Messrs. McKenna, Song and Waksal). |

** | Previously Perceptive Capital Solutions Corp before the Domestication. |

PIPE Financing

In connection with entering into the Business Combination Agreement, on December 5, 2025, PCSC entered into Subscription Agreements with the PIPE Investors. Pursuant to the Subscription Agreements, the PIPE Investors agreed to subscribe for and purchase, and PCSC agreed to issue and sell to the PIPE Investors, on the Closing Date immediately following the Closing, an aggregate of 24,000,000 shares of New Freenome Common Stock for a purchase price of $10.00 per share, and aggregate gross proceeds of $240.0 million.

Existing Freenome stockholders (other than the Perceptive PIPE Investor and investors who were existing PCSC shareholders) subscribed for approximately $72.4 million of the PIPE Financing. Existing PCSC shareholders (other than the Perceptive PIPE Investor and investors who were existing Freenome stockholders) subscribed for approximately $15.0 million of the PIPE Financing. PIPE Investors who were both existing shareholders of PCSC and Freenome (other than the Perceptive PIPE Investor) subscribed for approximately $52.6 million of the PIPE Financing. The Perceptive PIPE Investor subscribed for an aggregate of $55 million of the PIPE Financing. Investors who were neither existing Freenome stockholders nor existing PCSC shareholders subscribed for approximately $45.0 million of the PIPE Financing.

The obligations of each party to consummate the PIPE Financing are conditioned upon, among other things, (i) the New Freenome Common Stock (including the New Freenome Common Stock issuable to the PIPE Investors pursuant to the Subscription Agreements) having been approved for listing on Nasdaq; and (ii) satisfaction of all conditions precedent to the closing of the transactions set forth in the Business Combination Agreement. The obligations of the PIPE Investors to consummate the PIPE Financing are further subject to additional conditions, including, among other things: (i) the Business Combination Agreement shall not have been amended, modified, or supplemented, and no condition waived thereunder, in a manner that would reasonably be expected to materially and adversely affect the economic benefits that a PIPE Investor would reasonably expect to receive under the Subscription Agreement; (ii) the material truth and accuracy of the representations and warranties of PCSC in the Subscription Agreement, subject to customary bringdown standards; (iii) no subscription agreement, or other agreements or understandings (including side letters) entered into in connection with the sale of New Freenome Common Stock under the Subscription Agreements, with any other PIPE Investors shall have been amended, modified, or waived in any manner that benefits such other PIPE Investor unless all PIPE Investors have been offered substantially the same benefits; and (iv) there has not occurred any material adverse effect or parent material adverse effect since the date of the Subscription Agreement that is continuing. See “Business Combination Proposal—Related Agreements—PIPE Financing.”

Lock-Up Agreement

In connection with the Closing, the Sponsor and certain former Freenome stockholders will enter into the Lock-Up Agreement with PCSC. Pursuant to the Lock-Up Agreement, the Sponsor and certain Freenome stockholders will agree not to transfer (except for certain permitted transfers) any shares of New Freenome Common Stock held by such holder after the Domestication until six (6) months after the Closing Date. See “Business Combination Proposal—Related Agreements—Lock-up Agreements.”

Sources and Uses of Proceeds

The following tables summarize the anticipated sources and uses of funds in the Business Combination, in various redemption scenarios. Such tables are for illustrative purposes only. Where actual amounts are not known or knowable, the figures below represent good faith estimates of such amounts.

Sources and Uses of Proceeds (No Redemptions Scenario) (in millions)

The following table summarizes the sources and uses of funds for the Business Combination assuming no redemptions by PCSC shareholders.

Sources | Uses | ||||||||

Cash in Trust Account(1) | $91.9 | Cash to Balance Sheet | $387.2 | ||||||

Marketable Securities of Freenome | 138.1 | Marketable securities to Balance Sheet | 138.1 | ||||||

Existing Cash Balances, as of December 31, 2025 | 79.4 | Estimated Unpaid Transaction Expenses, as of December 31, 2025 | 24.1 | ||||||

Cash Proceeds from the PIPE Financing | 240.0 | ||||||||

Total Sources | $549.4 | Total Uses | $549.4 | ||||||

Sources and Uses of Proceeds (25% Redemptions Scenario) (in millions)

The following table summarizes the sources and uses of funds for the Business Combination assuming 25% redemptions by PCSC shareholders.

Sources | Uses | ||||||||

Cash in Trust Account(1) | 91.9 | Cash to Balance Sheet | 364.2 | ||||||

Marketable Securities of Freenome | 138.1 | Marketable securities to Balance Sheet | 138.1 | ||||||

Existing Cash Balances, as of December 31, 2025 | 79.4 | Redemption of PCSC Class A Shares held by public shareholders(2) | 23.0 | ||||||

Cash Proceeds from the PIPE Financing | 240.0 | Estimated Unpaid Transaction Expenses, as of December 31, 2025 | 24.1 | ||||||

Total Sources | 549.4 | Total Uses | 549.4 | ||||||

Sources and Uses of Proceeds (50% Redemptions Scenario) (in millions)

The following table summarizes the sources and uses of funds for the Business Combination assuming 50% redemptions by PCSC shareholders.

Sources | Uses | ||||||||

Cash in Trust Account(1) | 91.9 | Cash to Balance Sheet | 341.3 | ||||||

Marketable Securities of Freenome | 138.1 | Marketable securities to Balance Sheet | 138.1 | ||||||

Existing Cash Balances, as of December 31, 2025 | 79.4 | Redemption of PCSC Class A Shares held by public shareholders(2) | 45.9 | ||||||

Cash Proceeds from the PIPE Financing | 240.0 | Estimated Unpaid Transaction Expenses, as of December 31, 2025 | 24.1 | ||||||

Total Sources | 549.4 | Total Uses | 549.4 | ||||||

Sources and Uses of Proceeds (Aggregate Transaction Proceeds Condition Redemptions Scenario)

(in millions)

The following table summarizes the sources and uses of funds for the Business Combination assuming the Aggregate Transaction Proceeds Condition Redemptions Scenario.

Sources | Uses | ||||||||

Cash in Trust Account(1) | 91.9 | Cash to Balance Sheet | 317.2 | ||||||

Marketable Securities of Freenome | 138.1 | Marketable securities to Balance Sheet | 138.1 | ||||||

Existing Cash Balances, as of December 31, 2025 | 79.4 | Redemption of PCSC Class A Shares held by public shareholders(2) | 70.0 | ||||||

Cash Proceeds from the PIPE Financing | 240.0 | Estimated Unpaid Transaction Expenses, as of December 31, 2025 | 24.1 | ||||||

Total Sources | 549.4 | Total Uses | 549.4 | ||||||

(1) | Reflects the amount in the trust account as of December 31, 2025. |

(2) | Assumes a redemption price of $10.65 per share, based on the amount in the trust account as of December 31, 2025. |

Conditions to Closing of the Business Combination

Under the Business Combination Agreement, the obligations of the parties to consummate the Business Combination are subject to the satisfaction or waiver of certain closing conditions of the respective parties, including, without limitation, the Aggregate Transaction Proceeds equaling no less than $250.0 million. As of the date of this proxy statement/prospectus, the Aggregate Transaction Proceeds Condition has not been satisfied. The parties intend to satisfy the Aggregate Transaction Proceeds Condition through the PIPE Financing and through amounts released to us from the trust account. In the event the Aggregate Transaction Proceeds Condition is not satisfied as a result of redemptions of public shares which reduce the amount available to be released to us from the trust account, Freenome may, in its sole discretion, waive the Aggregate Transaction Proceeds Condition. If Freenome waives the Aggregate Transaction

Proceeds Condition, PCSC intends to file a Current Report on Form 8-K within four business days of such event, however such condition may be waived at any time prior to the Closing, including after the deadline for submitting redemption requests or the extraordinary general meeting, and, given such timing, you may not be notified before the deadline for submitting redemption requests or the extraordinary general meeting. For more information, see “Business Combination Proposal—The Business Combination Agreement—Conditions to Closing of the Business Combination.”

Termination

The Business Combination Agreement may be terminated under certain customary and limited circumstances at any time prior to the Closing, including, among others, the following: (i) by either PCSC or Freenome if the transactions contemplated by the Business Combination Agreement are not consummated on or prior to September 5, 2026; (ii) by either PCSC or Freenome if the requisite approvals by the PCSC shareholders of the Condition Precedent Proposals are not obtained at the extraordinary general meeting (including any adjournment thereof); (iii) by PCSC, if Freenome has not delivered, or caused to be delivered to PCSC, the Freenome Stockholder Written Consent or the Transaction Support Agreements as and when required under the Business Combination Agreement; (iv) by PCSC or Freenome, if Freenome or PCSC, as applicable, has breached any of its respective representations, warranties, agreements or covenants under the Business Combination Agreement, and such breach or failure would render certain conditions precedent to the Closing incapable of being satisfied, and such breach or failure is not cured by the time allotted in the Business Combination Agreement; and (v) by the mutual written consent of PCSC and Freenome.

If the Business Combination Agreement is validly terminated, none of the parties to the Business Combination Agreement will have any liability or any further obligation under the Business Combination Agreement other than in the case of a willful breach of any covenant or agreement under the Business Combination Agreement or fraud. For more information, see “Business Combination Proposal—The Business Combination Agreement—Termination.”

Related Agreements

In connection with the Business Combination, certain other related agreements have been, or will be entered into on or prior to the closing of the Business Combination, including the Transaction Support Agreements, the Sponsor Letter Agreement, and the Investor Rights Agreement. See “—Related Agreements” for more information.

Ownership of New Freenome

The following tables illustrate estimated ownership levels in New Freenome, immediately following the consummation of the Business Combination, based on varying levels of redemptions by public shareholders. In the following tables, the No Redemptions Scenario, the 25% Redemptions Scenario, the 50% Redemptions Scenario and the Aggregate Transaction Proceeds Condition Redemptions Scenario each assume that the $250.0 million Aggregate Transaction Proceeds Condition is satisfied through a combination of the $240.0 million PIPE Financing and retained funds in the trust account. In the event the Aggregate Transaction Proceeds Condition is not satisfied as a result of redemptions of public shares which reduce the amount available to be released to us from the trust account, Freenome may, in its sole discretion, waive the Aggregate Transaction Proceeds Condition. If Freenome waives the Aggregate Transaction Proceeds Condition, PCSC intends to file a Current Report on Form 8-K within four business days of such event, however such condition may be waived at any time prior to the Closing, including after the deadline for submitting redemption requests or the extraordinary general meeting, and, given such timing, you may not be notified before the deadline for submitting redemption requests or the extraordinary general meeting.

The following table excludes the dilutive effect of Rollover Options, Rollover RSU Awards, the Exact Sciences Note (as defined in section “Description of New Freenome Securities—Outstanding Exact Sciences Convertible Note”), and shares of New Freenome Common Stock that will initially be available for issuance under the New Freenome Equity Incentive Plan and the New Freenome Employee Stock Purchase Plan.

Pro Forma Combined | ||||||||||||||||||||||||

No Redemptions Scenario | 25% Redemptions Scenario | 50% Redemptions Scenario | Aggregate Transaction Proceeds Condition Redemptions Scenario | |||||||||||||||||||||

Shares | % | Shares | % | Shares | % | Shares | % | |||||||||||||||||

PCSC public shareholders(1) | 8,625,000 | 7.66% | 6,468,750 | 5.85% | 4,312,500 | 3.98% | 2,056,878 | 1.94% | ||||||||||||||||

Sponsor and the Perceptive PIPE Investor(2) | 13,554,087 | 12.03% | 13,554,087 | 12.26% | 13,554,087 | 12.51% | 13,554,087 | 12.77% | ||||||||||||||||

PCSC independent directors(3) | 90,000 | 0.08% | 90,000 | 0.08% | 90,000 | 0.08% | 90,000 | 0.08% | ||||||||||||||||

Freenome stockholders (excluding the Perceptive PIPE Investor and Roche)(4) | 52,699,707 | 46.77% | 52,699,707 | 47.69% | 52,699,707 | 48.64% | 52,699,707 | 49.67% | ||||||||||||||||

PIPE Investors (excluding the Perceptive PIPE Investor)(5) | 18,500,000 | 16.42% | 18,500,000 | 16.74% | 18,500,000 | 17.07% | 18,500,000 | 17.44% | ||||||||||||||||

Roche(6) | 19,198,197 | 17.04% | 19,198,197 | 17.37% | 19,198,197 | 17.72% | 19,198,197 | 18.09% | ||||||||||||||||

Pro forma total shares of the New Freenome Common Stock outstanding at Closing | 112,666,991 | 100.00% | 110,510,741 | 100.00% | 108,354,491 | 100.00% | 106,098,869 | 100.00% | ||||||||||||||||

* | Less than 1%. |

(1) | Amount comprises the unredeemed public shares in a variety of redemptions scenarios. This amount reflects the assumed redemption of 0 shares under the No Redemptions Scenario, 2,156,250 shares redeemed under the 25% Redemptions Scenario, 4,312,500 shares redeemed under the 50% Redemptions Scenario, and 6,568,122 shares redeemed under the Aggregate Transaction Proceeds Condition Redemptions Scenario. |

(2) | Amount includes 2,066,250 PCSC Class B Shares held by the Sponsor, 286,250 private placement shares, which are PCSC Class A Shares, held by Sponsor, 5,500,000 shares purchased by the Perceptive PIPE Investor as part of the PIPE Financing, and 5,611,587 shares of New Freenome Common Stock to be issued as merger consideration. |

(3) | Amount includes 30,000 PCSC Class B Shares held by each of PCSC’s independent directors (Messrs. McKenna, Song and Waksal). |

(4) | Amount includes 71,089,352 shares of New Freenome Common Stock issued to Freenome stockholders less 5,611,587 and 12,778,058 shares that will be held by the Perceptive PIPE Investor and Roche, respectively, which are presented in the rows labeled “Sponsor and the Perceptive PIPE Investor” and “Roche.” The amounts in the table do not include the potentially dilutive shares that could be issued, specifically 8,252,587 Rollover Options issued to holders of Freenome Options (whether vested or unvested immediately prior to the Effective Time), 4,291,830 Rollover RSU Awards issued to holders of Freenome RSU Awards (whether vested or unvested immediately prior to the Effective Time) and 3,441,094 shares which would be issued upon Exact Sciences’ optional election to convert the Exact Sciences Note (assuming accrued interest through May 31, 2026). |

(5) | Amount includes the 18,500,000 shares of New Freenome Common Stock to be issued to the PIPE Investors, less the 5,500,000 shares to be purchased by the Perceptive PIPE Investor as part of the PIPE Financing (which are presented in the row labeled “Sponsor and the Perceptive PIPE Investor”). |

(6) | Includes 12,778,058 shares of New Freenome Common Stock to be issued as merger consideration and 6,420,139 shares of Freenome Common Stock issued upon conversion of the Roche Convertible Note. The Roche Convertible Note (including the principal amount and accrued interest) will automatically convert into shares of New Freenome Common Stock at a conversion price of $12.00 in connection with the Closing. This amount assumes accrued interest through May 31, 2026. |

The following table shows possible sources of dilution and the extent of such dilution that non-redeeming public shareholders could experience in connection with the closing of the Business Combination. The table excludes shares of New Freenome Common Stock that will initially be available for issuance under the New Freenome Equity Incentive Plan and the New Freenome Employee Stock Purchase Plan, as such shares are not expected to be outstanding on the Closing Date.

Pro Forma Combined, Including Dilutive Instruments | ||||||||||||||||||||||||

No Redemptions Scenario | 25% Redemptions Scenario | 50% Redemptions Scenario | Aggregate Transaction Proceeds Condition Redemptions Scenario | |||||||||||||||||||||

Shares | % | Shares | % | Shares | % | Shares | % | |||||||||||||||||

PCSC public shareholders(1) | 8,625,000 | 6.71% | 6,468,750 | 5.12% | 4,312,500 | 3.47% | 2,056,878 | 1.69% | ||||||||||||||||

Sponsor and the Perceptive PIPE Investor(2) | 13,554,087 | 10.54% | 13,554,087 | 10.72% | 13,554,087 | 10.91% | 13,554,087 | 11.11% | ||||||||||||||||

PCSC independent directors(3) | 90,000 | 0.07% | 90,000 | 0.07% | 90,000 | 0.07% | 90,000 | 0.07% | ||||||||||||||||

Freenome Stockholders (excluding the Perceptive PIPE Investors and Roche)(4) | 52,699,707 | 41.00% | 52,699,707 | 41.70% | 52,699,707 | 42.42% | 52,699,707 | 43.20% | ||||||||||||||||

PIPE Investors (excluding the Perceptive PIPE Investor)(5) | 18,500,000 | 14.39% | 18,500,000 | 14.64% | 18,500,000 | 14.89% | 18,500,000 | 15.17% | ||||||||||||||||

Rollover Options(6) | 8,252,587 | 6.42% | 8,252,587 | 6.53% | 8,252,587 | 6.64% | 8,252,587 | 6.77% | ||||||||||||||||

Rollover RSU Awards(7) | 4,291,830 | 3.34% | 4,291,830 | 3.40% | 4,291,830 | 3.45% | 4,291,830 | 3.52% | ||||||||||||||||

Roche(8) | 19,198,197 | 14.94% | 19,198,197 | 15.19% | 19,198,197 | 15.45% | 19,198,197 | 15.74% | ||||||||||||||||

Exact Sciences(9) | 3,333,333 | 2.59% | 3,333,333 | 2.64% | 3,333,333 | 2.68% | 3,333,333 | 2.73% | ||||||||||||||||

Pro forma total shares of the New Freenome Common Stock outstanding at Closing | 128,544,741 | 100.00% | 126,388,491 | 100.00% | 124,232,241 | 100.00% | 121,976,619 | 100.00% | ||||||||||||||||

* | Less than 1%. |

(1) | Amount comprises the unredeemed public shares in a variety of redemptions scenarios. This amount reflects the assumed redemption of 0 shares under the No Redemptions Scenario, 2,156,250 shares redeemed under the 25% Redemptions Scenario, 4,312,500 shares redeemed under the 50% Redemptions Scenario, and 6,568,122 shares redeemed under the Aggregate Transaction Proceeds Condition Redemptions Scenario. |

(2) | Amount includes 2,066,250 PCSC Class B Shares held by the Sponsor, 286,250 PCSC Class A Shares held by Sponsor, 5,500,000 shares purchased by the Perceptive PIPE Investor as part of the PIPE Financing, and 5,611,587 shares of New Freenome Common Stock to be issued as merger consideration. |

(3) | Amount includes 30,000 PCSC Class B Shares held by each of PCSC’s independent directors (Messrs. McKenna, Song and Waksal). |

(4) | Amount includes 71,089,352 shares of New Freenome Common Stock issued to Freenome stockholders less 5,611,587 and 12,778,058 shares that will be held by the Perceptive PIPE Investor and Roche, respectively, which are presented in the rows labeled “Sponsor and the Perceptive PIPE Investor” And “Roche.” |

(5) | Amount includes the 18,500,000 shares of New Freenome Common Stock to be issued to the PIPE Investors, less the 5,500,000 shares to be purchased by the Perceptive PIPE Investor as part of the PIPE Financing (which are presented in the row labeled “Sponsor and the Perceptive PIPE Investor”). |

(6) | Amount comprises the potentially dilutive shares that could be issued pursuant to 8,252,587 Rollover Options issued to holders of Freenome Options (whether vested or unvested immediately prior to the Effective Time) in accordance with the terms of the Business Combination Agreement. Does not include shares the Initial Equity Awards and Anti-Dilution Equity Awards. |

(7) | Amount comprises the potentially dilutive shares that could be issued pursuant to 4,291,830 Rollover RSU Awards issued to holders of Freenome RSU Awards (whether vested or unvested immediately prior to the Effective Time) in accordance with the terms of the Business Combination Agreement. Does not include shares the Initial Equity Awards and Anti-Dilution Equity Awards. |

(8) | Includes 12,778,058 shares of New Freenome Common Stock to be issued as Mergers Consideration and 6,420,139 shares of Freenome Common Stock issued upon conversion of the Roche Convertible Note. The Roche Convertible Note (including the principal amount and accrued interest) will automatically convert into shares of New Freenome Common Stock at a conversion price of $12.00 in connection with the Closing. This amount assumes accrued interest through May 31, 2026. |

(9) | Includes 3,333,333 shares of New Freenome Common Stock which would be issued upon Exact Sciences’ optional election to convert the Exact Sciences Note. |

Share ownership presented in the two tables above is only presented for illustrative purposes and does not necessarily reflect what New Freenome’s share ownership will be after the Closing. PCSC and New Freenome cannot predict how many of the public shareholders will exercise their right to have their public shares redeemed for cash. As a result, the redemption amount and the number of public shares redeemed in connection with the Business Combination may differ from the amounts presented above, and therefore the ownership percentages of public shareholders may also differ if the actual redemptions are different from these assumptions. The public shareholders that do not elect to redeem their public shares will experience immediate dilution as a result of the Business Combination. The public shareholders currently own approximately 77.9% of the issued and outstanding PCSC Shares. As noted in the above table, even if no public shareholders redeem their public shares in the Business Combination, the public shareholders’ ownership will decrease from approximately 77.9% of the PCSC Shares prior to the Business Combination to owning approximately 7.66% of the total outstanding New Freenome Common Stock at the Closing. As redemptions increase, the overall percentage ownership held by the Sponsor, the Perceptive PIPE Investor, PCSC’s independent directors (Messrs. McKenna, Song and Waksal), Freenome Stockholders and the PIPE Investors will increase as compared to the overall percentage ownership and voting percentage held by public shareholders, thereby increasing dilution to public shareholders. For more information about the consideration to be received in the Business Combination, these scenarios, and the underlying assumptions, see “Unaudited Pro Forma Combined Financial Information.” See also “Risk Factors—The public shareholders will experience immediate dilution as a consequence of the issuance of New Freenome Common Stock as consideration in the Business Combination and due to future issuances of equity awards to Freenome employees, directors, or consultants. Having a minority share position may reduce the influence that our current shareholders have on the management of New Freenome.”

Interests of PCSC’s Directors and Executive Officers, Sponsor and Others in the Business Combination

In considering the recommendation of the PCSC Board in favor of approval of the Business Combination Proposal, the Domestication Proposal, the Governing Documents Proposal, each of the Advisory Governing Documents Proposals, the Nasdaq Proposal, the Equity Incentive Plan Proposal, the Employee Stock Purchase Plan Proposal and the Adjournment Proposal, PCSC shareholders should keep in mind that the Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors have interests in the Business Combination that are different from or in addition to (and which may conflict with) the interests of unaffiliated PCSC shareholders. Further, PCSC’s officers and directors have additional fiduciary or contractual obligations to other entities pursuant to which such officer or director is or will be required to present a business combination opportunity to such entity, which are set forth in more detail in the section titled “Information About PCSC—Conflicts of Interest.” We believe there were no such opportunities that were not presented as a result of the existing fiduciary or contractual obligations of our officers and directors to other entities. The PCSC Board was aware of and considered these interests, among other matters, in evaluating and negotiating the Business Combination and Business Combination Agreement and in recommending to our shareholders that they vote in favor of the proposals to be presented at the extraordinary general meeting, including the Business Combination Proposal. PCSC shareholders should take these interests into account in deciding whether to approve the proposals presented at the extraordinary general meeting, including the Business Combination Proposal. See “Business Combination Proposal—Interests of PCSC’s Directors and Executive Officers, Sponsor and Others in the Business Combination.”

Compensation to be Received by the Sponsor, the Perceptive PIPE Investor, and PCSC’s Officers and Directors in Connection with the Business Combination and PIPE Financing

Set forth below is a summary of the amount of compensation and securities received or to be received by the Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors in connection with the Business Combination and PIPE Financing.

Securities to be Received | Other Compensation | |||||

The Sponsor | Assuming the Aggregate Transaction Proceeds Condition Redemptions Scenario: (i) 2,066,250 shares of New Freenome Common Stock upon the exchange of 2,066,250 PCSC Class B Shares in the Domestication, which were initially purchased prior to PCSC’s initial public | Reimbursement for Working Capital Loans to PCSC. To date, PCSC has no outstanding borrowings under Working Capital Loans. $15,000 per month through the Closing for office space, secretarial | ||||

Securities to be Received | Other Compensation | |||||

offering for approximately $0.01 per share and (ii) 286,250 shares of New Freenome Common Stock upon the exchange of 286,250 PCSC Class A Shares in the Domestication, which were initially purchased in a private placement that closed concurrently with PCSC’s initial public offering at a price of $10.00 per share. | and administrative services. As of December 31, 2025, PCSC incurred $180,000 in fees for these services, of which such amount is included in accrued expenses in PCSC’s balance sheet as of December 31, 2025. Continued indemnification and the continuation of directors’ and officer’s liability insurance after the Business Combination. | |||||

Perceptive PIPE Investor | Assuming the Aggregate Transaction Proceeds Condition Redemptions Scenario: (i) 5,500,000 shares of New Freenome Common Stock purchased by the Perceptive PIPE Investor for $10.00 per share in the PIPE Financing, for an aggregate amount of $55.0 million, and (iii) 5,615,003 shares of New Freenome Common Stock upon the exchange of Freenome capital stock in the First Merger, which is determined by reference to the Exchange Ratio. | Continued indemnification after the Business Combination. | ||||

PCSC’s independent directors (Messrs. McKenna, Song and Waksal) | Each will receive 30,000 shares of New Freenome Common Stock upon the exchange of 30,000 PCSC Class B Shares held by them in the Domestication, which shares were issued to them as consideration for services to PCSC. | Reimbursement for Working Capital Loans to PCSC. To date, PCSC has no outstanding borrowings under Working Capital Loans. Reimbursement for out-of-pocket expenses incurred related to identifying, negotiating, investigating and completing the Business Combination; no such amounts are outstanding as of the date of this proxy statement/prospectus. Continued indemnification and the continuation of directors’ and officer’s liability insurance after the Business Combination. | ||||

The securities to be issued to the Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors may result in a material dilution of the equity interests of non-redeeming public shareholders. PCSC’s independent directors are not members of the Sponsor and are not affiliates of the Perceptive PIPE Investor. None of the funds in the trust account will be used to compensate our officers or directors. Except for administrative services fees and office rental fees paid or to be paid to the Sponsor, no compensation of any kind, including finder’s and consulting fees, have been paid or will be paid to the Sponsor, the Perceptive PIPE Investor, officers and directors, or any of their respective affiliates, for services rendered prior to or in connection with the completion of the Business Combination. However, as detailed above, these individuals will be reimbursed for any out-of-pocket expenses incurred in connection with activities on our behalf such as identifying potential target businesses and performing due diligence on suitable business combinations, as discussed above. The reimbursement of expenses and advances to the Sponsor, the Perceptive PIPE Investor, and PCSC’s officers and directors may result in a material dilution of the equity interests of non-redeeming public shareholders.

The Special Committee’s and the PCSC Board’s Reasons for the Approval of the Business Combination

Before unanimously determining that the terms and conditions of the Business Combination Agreement, each ancillary agreement, and the Business Combination were fair, advisable, and in the best interests of PCSC and its shareholders as a whole, the Special Committee and the PCSC Board considered a wide variety of factors in connection with their evaluation of the Business Combination. In light of the complexity of the factors considered, the Special Committee and the PCSC Board, as a whole, did not consider it practicable to, and did not attempt to, quantify or otherwise assign relative weights to the specific factors they took into account in reaching their respective decisions. Rather, the Special Committee and the PCSC Board based their evaluation, negotiation and recommendation of the Business Combination on the totality of information available and the factors presented to and considered by them. In addition, individual members of the Special Committee and the PCSC Board may have given different weights to different factors.

The PCSC Board and the Special Committee reached its unanimous decision in light of a variety of factors, including but not limited to Freenome’s novel technology for early cancer detection, accompanied with positive data, Freenome’s critical and valuable commercial partnerships, Freenome’s market opportunity, Freenome’s experienced leadership team, and the size of the PIPE Financing committed. The Special Committee also reviewed the financial analysis and opinion of Scalar rendered to the Special Committee to the effect that, as of December 4, 2025 and subject to the procedures followed, assumptions made, matters considered, qualifications and limitations on the review undertaken, and other matters considered by Scalar in connection with the opinion, the consideration to be delivered to the Freenome Stockholders in the First Merger pursuant to the Business Combination was fair, from a financial point of view, to the PCSC Unaffiliated Shareholders. The Special Committee and the PCSC Board also considered a variety of factors and risks, potentially weighing negatively against pursuing the Business Combination, including, but not limited to macroeconomic risks that may cause Freenome’s future financial performance to not meet the Special Committee’s and the PCSC Board’s present expectations, the risk of regulatory changes that may adversely affect Freenome’s projected financial results and the other business benefits anticipated to result from the Business Combination, the redemption risk, the risk that PCSC shareholders may fail to provide the votes necessary to effect the Business Combination, the risks and costs to PCSC if the Business Combination is not completed, including the fact that PCSC may be forced to liquidate if PCSC being unable to effect a business combination by June 13, 2026 (unless otherwise extended), the risk that Closing may not occur due to failure to satisfy Closing conditions to the Business Combination, and the absence of possible structural protections for minority shareholders.

For more information about the Special Committee’s and PCSC Board’s reasons for the approval of the Business Combination, see “Business Combination Proposal — The Special Committee’s and the PCSC Board’s Reasons for the Approval of the Business Combination.”

Opinion of Scalar, LLC

On December 4, 2025, Scalar rendered its oral opinion to the Special Committee, subsequently confirmed in writing, as to the fairness, from a financial point of view, as of such date, to (1) the PCSC Class A Shareholders (other than (i) Freenome, (ii) Sponsor, (iii) the Key Supporting Company Stockholders, (iv) PCSC Class A Shareholders who elect to redeem their shares prior to or in connection with the Transaction, and (v) the PIPE Investors, (collectively, along with their respective affiliates, the “Excluded Parties”)) of the consideration to be delivered to the Freenome Stockholders in the Transaction, without giving effect to any impact of the Transaction on any particular PCSC Class A Shareholder other than in its capacity as a PCSC Class A Shareholder, and (2) PCSC. The full text of Scalar’s written opinion, dated December 4, 2025, which sets forth the procedures followed, assumptions made, matters considered, qualifications and limitations on the review undertaken, and other matters considered by Scalar in connection with the opinion are fully described in the subsection “Business Combination Proposal— Opinion of Scalar, LLC”. A copy of Scalar’s opinion is attached hereto as Annex L. The summary of Scalar’s opinion in this proxy statement/prospectus is qualified in its entirety by reference to the full text of Scalar’s written opinion. Scalar’s opinion was provided for the information and assistance of the Special Committee and does not constitute a recommendation as to how any shareholder of PCSC should vote or act (including with respect to any redemption rights) with respect to the Transaction or any other matter.

The Extraordinary General Meeting of PCSC

The following is a summary of the process and procedures for registering for and attending the extraordinary general meeting, and voting and redeeming your PCSC Shares in connection with the extraordinary general meeting. For more information, see the section entitled “Extraordinary General Meeting of PCSC.”

Date, Time and Place

The extraordinary general meeting will be held at [•] a.m., Eastern Time, on [•], 2026, at the offices of Cooley LLP located at 55 Hudson Yards, New York, New York 10001, and via a virtual meeting at [•].

Shareholders may attend the extraordinary general meeting in person. If you wish to attend the extraordinary general meeting in person at the offices of Cooley LLP located at 55 Hudson Yards, New York, New York 10001, you must reserve your attendance at least two business days in advance of the extraordinary general meeting by contacting PCSC’s secretary at [•] by 10:30 a.m., Eastern Time, on [•], 2026.

Proposals to be voted on at the Extraordinary General Meeting

At the extraordinary general meeting, PCSC’s shareholders are being asked to consider and vote upon:

• | the Business Combination Proposal; |

• | the Domestication Proposal; |

• | the Governing Documents Proposal; |

• | the Advisory Governing Documents Proposals; |

• | the Nasdaq Proposal; |

• | the Equity Incentive Plan Proposal; |

• | the Employee Stock Purchase Plan Proposal; and |

• | the Adjournment Proposal (if presented). |

Abstentions and Broker Non-Votes; Voting Your Shares; Record Date

With respect to each proposal in this proxy statement/prospectus, you may vote “FOR,” “AGAINST” or “ABSTAIN.”

Proxies that are marked “abstain” and proxies relating to “street name” shares that are returned to PCSC but marked by brokers as “not voted” will be treated as PCSC Shares present for purposes of determining the presence of a quorum on all matters. Abstentions and broker non-votes, while considered present for the purposes of establishing a quorum, will not count as votes cast at the extraordinary general meeting, and otherwise will have no effect on a particular proposal. If a shareholder does not give the broker voting instructions, under applicable self-regulatory organization rules, its broker may not vote its shares on “non-routine” proposals, such as the Business Combination Proposal or any of the other Condition Precedent Proposals.

Each PCSC Share that you own in your name entitles you to one vote. Your proxy card shows the number of PCSC Shares that you own. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

PCSC shareholders will be entitled to vote or direct votes to be cast at the extraordinary general meeting if they owned PCSC Shares at the close of business on [•], 2026, which is the record date for the extraordinary general meeting. As of the close of business on the record date, there were 11,067,500 PCSC Shares issued and outstanding, of which 8,911,250 were PCSC Class A Shares and 2,156,250 were PCSC Class B Shares.

Pursuant to the Sponsor Letter Agreement, the Sponsor and each of PCSC’s independent directors (Messrs. McKenna, Song and Waksal) have agreed to, among other things, vote all of their PCSC Shares in favor of the proposals being presented at the extraordinary general meeting. No consideration has been or will be paid by PCSC or Freenome to the Sponsor and each of PCSC’s independent directors in connection with the entry into the Sponsor Letter Agreement. As of the date of the accompanying proxy statement/prospectus, the initial shareholders collectively own 2,442,500 PCSC Shares, or approximately 22.1% of the issued and outstanding ordinary shares as follows: (i) the Sponsor owns 2,066,250 PCSC Class B Shares and 286,250 private placement shares, which are PCSC Class A Shares; and (ii) the PCSC independent directors each own 30,000 PCSC Class B Shares, for an aggregate of 90,000 PCSC Class B Shares.

Quorum and Required Vote for Proposals for the Extraordinary General Meeting

A quorum of PCSC shareholders is necessary to hold a valid meeting. A quorum will be present at the extraordinary general meeting if one or more shareholders who together hold not less than one-third of the issued and outstanding PCSC Shares entitled to vote at the extraordinary general meeting are represented in person or by proxy (or if a corporation or other non-natural person by duly authorized representative or proxy) at the extraordinary general meeting. As of the record date, 3,689,167 PCSC Shares would be required to achieve a quorum. As of the record date, the initial shareholders owned of record an aggregate of 2,442,500 PCSC Shares, representing approximately 22.1% of the issued and outstanding PCSC Shares. Therefore, an additional 1,246,667 public shares are required to establish a quorum.

The following votes are required to approve each Proposal:

• | Business Combination Proposal: The approval of the Business Combination Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

• | Domestication Proposal: The approval of the Domestication Proposal requires a special resolution of the holders of PCSC Class B Shares, being the affirmative vote of at least a two-thirds (2/3) majority of the votes cast by the holders of issued and outstanding PCSC Class B Shares who, being present in person or represented by proxy and entitled to vote at the extraordinary general meeting, vote at the extraordinary general meeting. The holders of the PCSC Class A Shares will have no right to vote on the Domestication Proposal, in accordance with Article 34.2 of the Existing Governing Documents. |

• | Governing Documents Proposal: The approval of the Governing Documents Proposal requires a special resolution of the holders of PCSC Class B Shares, being the affirmative vote of at least a two-thirds (2/3) majority of the votes cast by the holders of the issued and outstanding PCSC Class B Shares who, being present in person or represented by proxy and entitled to vote at the extraordinary general meeting, at the extraordinary general meeting. The holders of the PCSC Class A Shares will have no right to vote on the Governing Documents Proposal, in accordance with Article 34.2 of the Existing Governing Documents. |

• | Advisory Governing Documents Proposals: The approval of each Advisory Governing Documents Proposals requires an ordinary resolution, on a non-binding and advisory basis only, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

• | Nasdaq Proposal: The approval of the Nasdaq Proposal requires an ordinary resolution, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

• | Equity Incentive Plan Proposal: The approval of the Equity Incentive Plan Proposal requires an ordinary resolution, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

• | Employee Stock Purchase Plan Proposal: The approval of the Employee Stock Purchase Plan Proposal requires an ordinary resolution, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

• | Adjournment Proposal: The approval of the Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of at least a majority of the votes cast by the holders of the issued and outstanding PCSC Shares present in person or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. |

Each of the Business Combination Proposal, the Domestication Proposal, the Governing Documents Proposal, the Nasdaq Proposal, the Equity Incentive Plan Proposal and the Employee Stock Purchase Plan Proposal is conditioned on the approval and adoption of each of the other Condition Precedent Proposals. Consummation of the Business Combination is not conditioned upon the approval of the Advisory Governing Documents Proposals or the Adjournment Proposal. Neither the Advisory Governing Documents Proposals nor the Adjournment Proposal is conditioned upon the approval of any other proposal.

Redemption Rights

Pursuant to the Existing Governing Documents, a public shareholder may request that PCSC redeem its public shares for cash contemporaneously with the vote to approve the Business Combination and prior to the Domestication. If the Business Combination is approved, PCSC will pay to the holders any public shares that have been validly tendered or delivered for redemption a pro rata portion of the aggregate amount then on deposit in the trust account, calculated as of two business days prior to the consummation of the Business Combination and including interest earned on the funds held in the Trust Account not previously released to PCSC for permitted withdrawals. Pursuant to the Business Combination Agreement, the Domestication shall occur at least one business day prior to the Closing Date. As a holder of public shares, you will be entitled to receive cash for any public shares to be redeemed only if you:

(i) | hold public shares; and |

(ii) | prior to 5:00 p.m., Eastern Time, on [•], 2026 (two business days prior to the initially scheduled vote at the extraordinary general meeting), (a) submit a written request to the PCSC transfer agent in which you (i) request that PCSC redeem all or a portion of your public shares for cash, and (ii) identify yourself as the beneficial holder of the public shares and provide your legal name, phone number and address; and (b) deliver your public shares to the PCSC transfer agent physically or electronically through DTC. |

For illustrative purposes, based on funds in the trust account of approximately $91,918,776.09 on January 6, 2026, the estimated per share redemption price is expected to be approximately $10.66. A public shareholder who has properly tendered or delivered his, her or its public shares for redemption will be entitled to receive his, her or its pro rata portion of the aggregate amount then on deposit in the trust account in cash for such shares only if the Business Combination is completed. If the Business Combination is not completed, the redemptions will be canceled and the tendered shares will be returned to the relevant public shareholders as appropriate. If a public shareholder exercises its redemption rights in full, then it will be electing to exchange its public shares for cash and will no longer own any shares.

Public shareholders who seek to redeem their public shares must demand redemption no later than 5:00 p.m., Eastern Time, on [•], 2026 (two business days prior to the initially scheduled vote at the extraordinary general meeting) by (a) submitting a written request to the PCSC transfer agent that PCSC redeem such holder’s public shares for cash, (b) affirmatively certifying in such request to the PCSC transfer agent for redemption if such holder is acting in concert or as a “group” (as defined in Section 13d-3 of the Exchange Act) with any other shareholder with respect to PCSC Shares and (c) tendering or delivering their PCSC Shares, either physically or electronically through the DWAC system, at the holder’s option, to the PCSC transfer agent prior to the extraordinary general meeting. If you hold the shares in street name, you will have to coordinate with your broker to have your shares certificated or delivered electronically.

Notwithstanding the foregoing, a public shareholder, together with any affiliate of his, her, its or any other person with whom he, she or it is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Exchange Act) will be restricted from seeking redemption rights with respect to more than 15% of the public shares. Accordingly, any shares held by a public shareholder or “group” in excess of such 15% cap will not be redeemed by PCSC.

See the section entitled “Extraordinary General Meeting of PCSC—Redemption Rights” for a detailed description of the procedures to be followed if you wish to redeem your public shares for cash. See also “Questions and Answers about the Business Combination—Do I have redemption rights and is there a limit on the number of shares I may redeem?—How do I exercise my redemption rights?” for additional information on the exercise of redemption rights.

As set forth in more detail elsewhere in this proxy statement/prospectus, the public shareholders currently own approximately 77.9% of the issued and outstanding PCSC Shares prior to the Business Combination. Accordingly, public shareholders, as a group, will experience immediate dilution as a consequence of the Business Combination. As redemptions increase, the overall percentage ownership held by the Sponsor, the Perceptive PIPE Investor, Messrs. McKenna, Song and Waksal, Freenome Stockholders and the PIPE Investors will increase as compared to the overall percentage ownership and voting percentage held by public shareholders, thereby increasing dilution to public shareholders. For more information on the percentage of the issued and outstanding shares of New Freenome Common Stock immediately following the Closing that are expected to be held by securityholders, in various redemptions scenarios, see “Dilution.”

Appraisal Rights and Dissenters’ Rights

PCSC’s shareholders do not have appraisal rights in connection with the Business Combination or the Domestication under the DGCL. PCSC’s shareholders do not have dissenters’ rights in connection with the Business Combination or the Domestication under Cayman Islands law.

Proxy Solicitation Costs; Revoking Your Proxy; Changing Your Vote

PCSC is soliciting proxies on behalf of the PCSC Board. This solicitation is being made by mail but also may be made by telephone or in person. PCSC and its directors, officers and employees may also solicit proxies in person, by telephone or by other electronic means. PCSC will bear the cost of the solicitation.

PCSC has engaged Morrow as proxy solicitor to assist in the solicitation of proxies. PCSC has agreed to pay Morrow a fee of $25,000, plus disbursements, and will reimburse Morrow for its reasonable out-of-pocket expenses and indemnify Morrow and its affiliates against certain claims, liabilities, losses, damages and expenses.

If a shareholder grants a proxy, it may still vote its shares if it revokes its proxy before the extraordinary general meeting. A shareholder also may change its vote by submitting a later-dated proxy as described in the section entitled “Extraordinary General Meeting of PCSC—Revoking Your Proxy; Changing Your Vote.”

Regulatory Matters

Under the HSR Act and the rules that have been promulgated thereunder by the Federal Trade Commission (“FTC”), certain transactions may not be consummated unless information has been furnished to the Antitrust Division and the FTC and certain waiting period requirements have been satisfied. The Business Combination is subject to these requirements and may not be completed until the expiration of a 30-day waiting period following the filing of the required Notification and Report Forms with the Antitrust Division and the FTC or until early termination is granted. If the FTC or the Antitrust Division issues a second request within the initial 30-day waiting period, the waiting period with respect to the Business Combination will be extended for an additional period of 30 calendar days, which will begin on the date on which the filing parties each certify compliance with the second request. Complying with a second request can take a significant period of time.