UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For

the year ended

OR

OR

Date of event requiring this shell company report:

For the transition period from _________ to _____________.

Commission

file number:

(Exact name of Registrant as Specified in its Charter)

(Translation of Registrant’s name into English)

(Jurisdiction of Incorporation or Organization)

(Address of Principal Executive Offices)

Tel:

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s

classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes

☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Emerging growth company |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 13(a) of the Exchange Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the

registered public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of

the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | ☐ International Financial Reporting Standards as issued | ☐ Other |

| by the International Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐

If

this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes ☐ No

ONE AND ONE GREEN TECHNOLOGIES. INC

ANNUAL REPORT ON FORM 20-F

TABLE OF CONTENTS

i

CERTAIN TERMS AND CONVENSIONS

Unless otherwise indicated, in this annual report, the following terms shall have the meaning set out below:

| ● | “Amended and Restated Memorandum and Articles of Association” refers to the amended and restated memorandum of association and the articles of association of One and one Cayman (as defined below) adopted by special resolution passed on December 27, 2024; |

| ● | “BVI” refers to the British Virgin Islands; |

| ● | “CAGR” refers to compounded annual growth rate, the year-on-year growth rate over a specific period of time; |

| ● | “Companies Act” refers to the Companies Act (as revised) of the Cayman Islands, as amended, supplemented or otherwise modified from time to time; |

| ● | “Contractual Arrangements” means those agreements entered into by and among One and one HK, Yoda Metal, DL Metal, and certain shareholders of Yoda Metal and DL Metal, including the Exclusive Business Cooperation Agreement, Exclusive Option Agreement, and Shared Pledge Agreement, each dated June 10, 2024, which grants One and one HK contractual rights to (i) direct the activities of the VIEs that most significantly impact the VIEs’ economic performance, (ii) receive all of the economic benefits of the VIEs and their respective subsidiaries (if any); and (iii) have an exclusive option to purchase all or part of the equity interests in and assets of the VIEs and their respective subsidiaries (if any) when and to the extent permitted by Philippine law. |

| ● | “DL Metal” refers to DL Metal Corporation, the operating entity incorporated on March 3, 2022, under the law of the Republic of the Philippines; |

| ● | “FY2025” “FY2024” and “FY2023” refer to fiscal year ended December 31, 2025, 2024, and 2023, respectively; |

| ● | “Hong Kong” or “HK SAR” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| ● | “Mainland China” refers to the mainland of the People’s Republic of China; excluding Taiwan, Hong Kong and the Macau Special Administrative Regions of the People’s Republic of China for the purposes of this annual report only; |

| ● | “One and one Cayman”, “One and one” and “Company” refers to One and one Green Technologies. INC, the Cayman Islands holding company, incorporated on April 17, 2024; |

| ● | “One and one HK” refers to One and one International HK Limited, the intermediate holding company, incorporated on May 29, 2024; |

| ● | “Operating entities” refers to DL Metal and Yoda Metal, the variable interest entities of One and one Cayman, through One and one HK, unless otherwise specified; |

| ● | “PHP” refers to the legal currency of Philippine peso; |

| ● | “PRC” refers to the People’s Republic of China, including Hong Kong and the Macau Special Administrative Regions of the People’s Republic of China; |

| ● | “PRC government” or “Chinse government” refers to the government and governmental authorities of Mainland China for the purposes of this annual report only; |

| ● | “SEC” refers to the United States Securities and Exchange Commission; |

| ● | “US$”, “$”, or “U.S. dollar(s)” refer to the legal currency of the United States; |

| ● | “U.S.”, or “United States” refers to the United States of America; |

| ● | “U.S. GAAP” refers to generally accepted accounting principles in the United States; |

| ● | “VIEs” refers to DL Metal and Yoda Metal, collectively, and each of them is referred to as a “VIE”; |

| ● | “We”, “Group”, “us”, or “our” refer to One and one Cayman, its subsidiary and VIEs. |

| ● | “Yoda Metal” refers to Yoda Metal and Craft Trading and Services Corp., the operating entity incorporated on March 20, 2014 under the law of the Republic of the Philippines; |

ii

Our operations are principally conducted through the VIEs located in the Philippines where PHP is the functional currency. This annual report contains translations of certain PHP amounts into US dollar amounts at specified rates solely for the convenience of the reader. All reference to “US dollars”, “USD”, “US$” or “$” are to United States dollars. All reference to “HK dollars”, “HKD”, or “HK$” are to Hong Kong dollars. Assets and liabilities are translated using the exchange rate at each balance sheet date’s period end rate. Revenue and expenses are translated using average rates prevailing during each reporting period, and shareholders’ equity is translated at historical exchange rates. Adjustments resulting from the translation are recorded as a separate component of accumulated other comprehensive income (loss) in shareholders’ equity. Unless otherwise noted, all translations from PHP to U.S. dollars and from U.S. dollars to PHP in this annual report were made at the following rates:

| US$ to PHP | Period End | Average Rate | ||||||

| December 31, 2025 | 58.87250 | 57.48284 | ||||||

| December 31, 2024 | 58.08400 | 57.28670 | ||||||

Our year end is December 31. References to a particular “fiscal year” are to our year ended December 31 of that calendar year. Our audited consolidated financial statements (“CFS”) were prepared in accordance with the generally accepted accounting principles in the United States (the “U.S. GAAP”).

We obtained the industry, market and competitive position data in this annual report from our own internal estimates, surveys, and research as well as from publicly available information, industry and general publications and research, surveys and studies conducted by third parties. None of the independent industry publications used in this annual report were prepared on our behalf. Industry publications, research, surveys, studies and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this annual report, and to risks due to a variety of factors, including those described under “Item 3. Key Information – D. Risk Factors.” These and other factors could cause results to differ materially from those expressed in these forecasts and other forward-looking information.

We have proprietary rights to trademarks used in this annual report that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, the trademarks, service marks and trade names referred to in this annual report are without the ®, ™ and other similar symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

This annual report contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in this annual report are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other person.

When used herein, the references to laws and regulations of “China” or the “PRC” are only to such laws and regulations of mainland China, excluding, for the purpose of this annual report only, Taiwan, Hong Kong and Macau.

iii

FORWARD-LOOKING STATEMENTS

This annual report contains “forward-looking statements” for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 that represent our beliefs, projections and predictions about future events. You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to,” “potential,” “continue” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events that we believe may affect our financial condition, results of operations, business strategy and financial needs.

These forward-looking statements are subject to various and significant risks and uncertainties, including those which are beyond our control. Although we believe that our expectations expressed in these forward-looking statements are reasonable, our expectations may later be found to be incorrect. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should thoroughly read this annual report and the documents that we refer to herein with the understanding that our actual future results may be materially different from and worse than what we expect. We qualify all of our forward-looking statements by these cautionary statements. We disclaim any obligation to update our forward-looking statements, except as required by law.

In addition, the new and rapidly changing nature of the display panel industry results in significant uncertainties for any projections or estimates relating to the growth prospects or future condition of our industry. Furthermore, if any one or more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based on these assumptions. You should not place undue reliance on these forward-looking statements.

iv

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

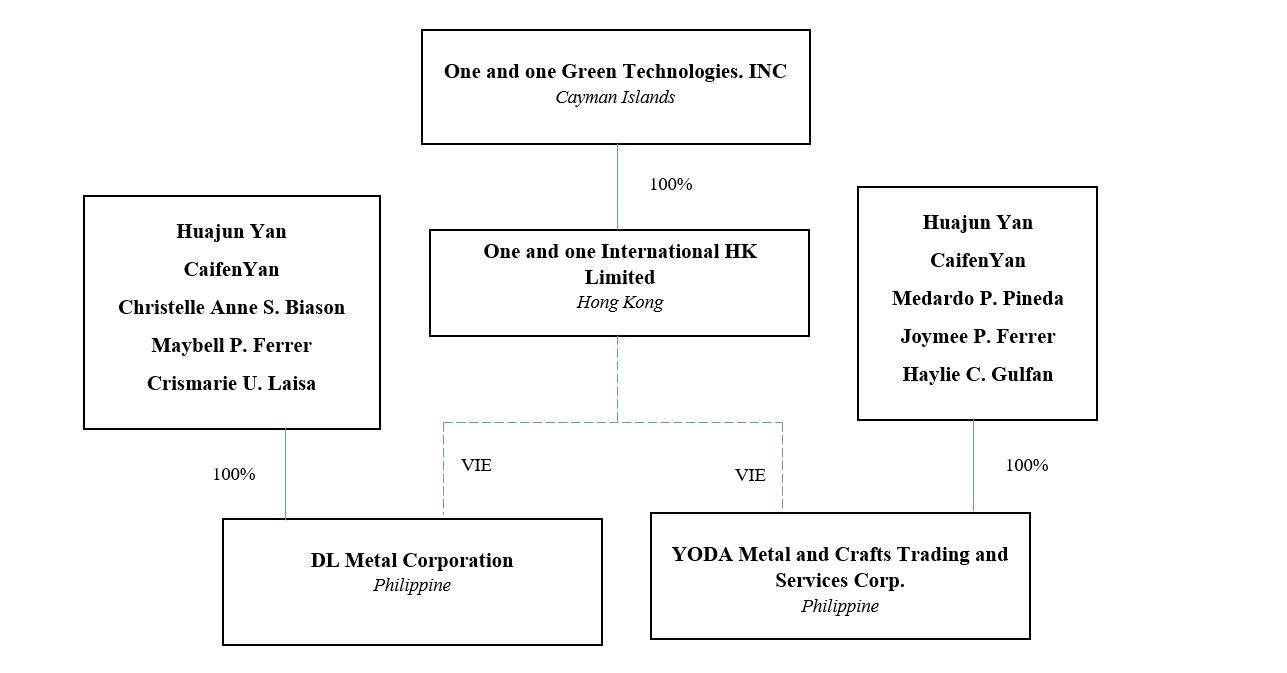

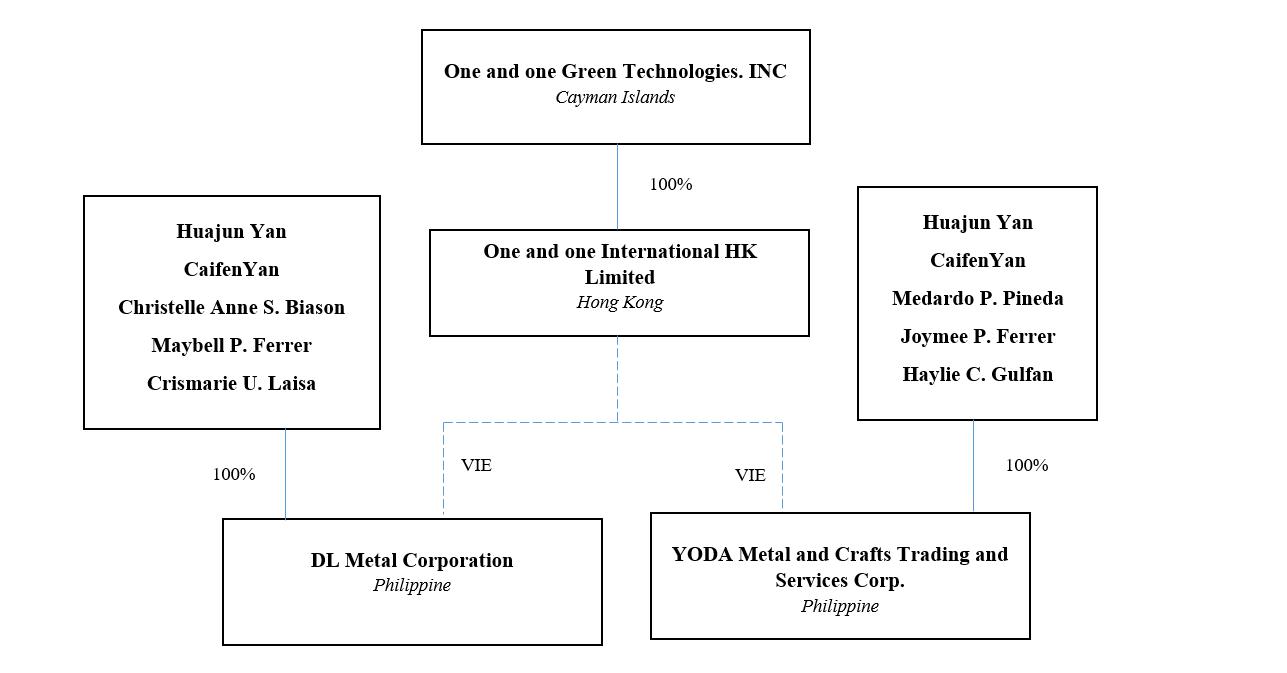

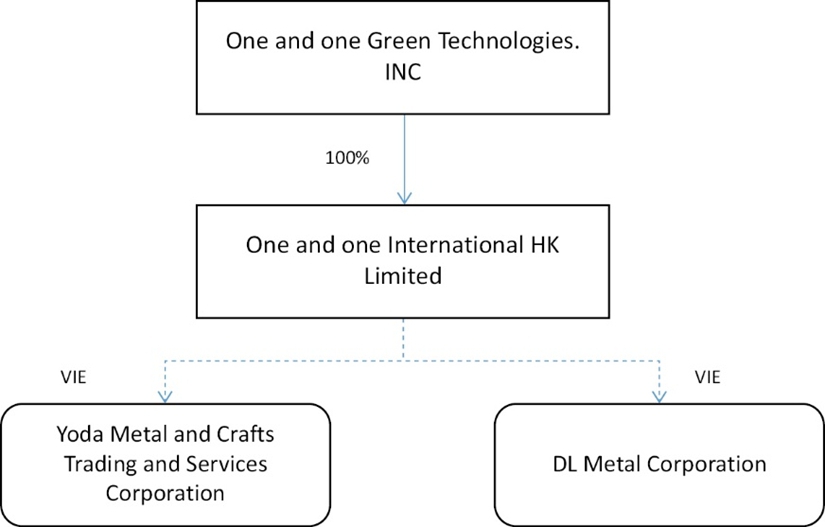

Company Structure

Below is a chart illustrating our current corporate structure:

1

Holding Company Structure

One and one Cayman was incorporated on April 17, 2024, under the laws of the Cayman Islands. As of the date of this annual report, the authorized share capital of the Company is US$50,000 divided into 500,000,000 ordinary shares, consisting of 489,796,040 Class A Ordinary Shares and 10,203,960 Class B Ordinary Shares, of which 44,096,040 Class A Ordinary Shares and 10,203,960 Class B Ordinary Shares are issued and outstanding. The Company is a holding company and is currently not actively engaging in any business. You may never hold equity interests in the operating entities in the Philippines. Further, One and one Cayman receives the economic benefits of the operations of two VIEs in the Philippines through an intermediate holding company (i.e., One and one HK) pursuant to the Contractual Arrangements.

One and one HK was incorporated on May 29, 2024, under the laws and regulations in Hong Kong. One and one HK is a wholly owned subsidiary of the Company. One and one HK is a holding company and is currently not actively engaging in any business.

DL Metal was established on March 3, 2022, under the laws of the Philippines. Yoda Metal was established on March 20, 2014, under the laws of the Philippines. One and one HK controls 100% of Yoda Metal and DL Metal through the Contractual Arrangements.

Although we took every precaution available to effectively enforce the contractual and corporate relationship above, these Contractual Arrangements may still be less effective than direct ownership and that the Company may incur substantial costs to enforce the terms of these Contractual Arrangements. For example, the VIEs and their shareholders could breach the Contractual Arrangements with us by, among other things, failing to conduct their operations in an acceptable manner or taking other actions that are detrimental to our interests. If One and one Cayman had direct ownership of the VIEs, One and one Cayman would be able to exercise its rights as a shareholder to effect changes in the board of directors of the VIEs, which in turn could implement changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the current Contractual Arrangements, we rely on the performance by the VIEs and their shareholders of their obligations under the Contractual Arrangements to exercise our rights as the primary beneficiary of the VIEs. The shareholders of the VIEs may not act in the best interests of our company or may not perform their obligations under these contracts. As a legal matter, if the VIEs or their shareholders fail to perform their obligations under these Contractual Arrangements, One and one Cayman may have to incur substantial costs to enforce such Contractual Arrangements, and rely on legal remedies under Philippine laws, including contract remedies, which may be time-consuming, unpredictable and expensive. The Contractual Arrangements are governed by Philippine laws and provide for the resolution of disputes through arbitration in the Philippines. The legal environment in the Philippines is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the Philippine legal system could limit the ability of One and one Cayman to enforce these Contractual Arrangements. In the event One and one Cayman is unable to enforce these Contractual Arrangements, it may not be able to exert effective power as the primary beneficiary over the operating entities and it may be precluded from operating its business, which would have a material adverse effect on its financial condition and results of operations. In addition, there is uncertainty as to whether the courts of the Cayman Islands or the Philippines would recognize or enforce judgments of U.S. courts against us or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state. For a detailed description of the risks related to the Contractual Arrangements with the VIEs, see “Item 3. Key Information—D. Risk Relating to Our Business.”

Philippines Regulatory Licenses, Permissions and Approvals

Detailed below are all of the major permits and licenses necessary for the Company to operate its business in the Philippines, the failure to possess any of which could have a material adverse effect on its business and operations. However, the materiality of the adverse effect would depend on a case to case basis. The Company is required to have its permits to operate as a corporation, and its branches would have its own permits. A large branch losing its permits would have a more significant effect on the Company as opposed to a small branch.

The Company believes that it has all the applicable and material permits and licenses necessary to operate its business as currently conducted and such permits and licenses are valid, subsisting, or pending renewal.

Regulation on Business in the Philippines

As mandated by the Local Government Code of 1991, city and municipal mayors are mandated to issue, suspend and revoke business licenses and permits. Thus, corporations operating within the jurisdiction of the cities and municipalities are required to secure a business permit.

Regulation on Waste Disposal in the Philippines

Under Sec. 4 of PD 1568 which created the Environmental Impact assessment system, “no person, partnership, or corporation shall undertake to operate any such declared environmentally critical project or area without first securing an Environmental Compliance Certificate.” ECC is required for any activities that potentially has significant environmental impact. The company has acquired the Environmental Compliance Certificate.

2

Regulation on Taxation in the Philippines

The National Internal Revenue Code subjects sole proprietorship, partnership and corporation to internal revenue taxes in the Philippines. These entities are required to register their businesses with the appropriate Bureau of Internal Revenue in order for them to issue official receipts, file taxes, and claim for tax credits or deductions.

Regulation on Corporations in the Philippines

The Revised Corporation Code of the Philippines mandates the Securities and Exchange Commission to register corporations, collect fees from the registering corporations, and prescribe reportorial requirements.

Regulation on Exportation and Importation in the Philippines

The Bureau of Customs (“BOC”) is mandated to supervise and control the egress and ingress of goods in the Philippines. Persons or entities who intend to engage in the business of exportation and importation are required to be registered with the BOC.

Regulations on Environmental Protection

The Philippines is known for its rich biodiversity and stunning natural landscapes. Due to rapid industrialization, urbanization, and unsustainable exploitation of natural resources, the Philippines faces significant environmental challenges. In response to these threats, the country has enacted a comprehensive set of environmental laws aimed at conserving its natural resources, protecting its ecosystems, and promoting sustainable development including Presidential Decree No. 1151, Republic Act No. 9729, Republic Act No. 6969, Republic Act No. 8749, Republic Act No. 9003 and Republic Act No. 9275. Potential foreign investors shall also comply with these environmental laws.

Foreign Investment Laws and Restrictions

Retail Trade Liberalization Act as Amended by R.A. 11595

Republic Act No. 8762, or the Retail Trade Liberalization Act of 2000 (“R.A. 8762”), as amended by Republic Act No. 11595, liberalized the Philippine retail industry to encourage Filipino and foreign investors to forge an efficient and competitive retail trade sector in the interest of empowering the Filipino consumer through lower prices, high quality goods, better services, and wider choices. It allowed non-Filipino citizens to participate in retail on a limited basis.

“Retail Trade” is defined by R.A. 8762, as amended by R.A. 11595, to cover any act, occupation, or calling of habitually selling direct to the general public any merchandise, commodities, or goods for consumption. Under R.A. 8762, as amended by R.A. 11595, Foreign-owned partnerships, associations, and corporations may, upon registration with the Securities and Exchange Commission (SEC), or in case of foreign-owned single proprietorships, upon registration with the Department of Trade and Industry (DTI), engage or invest in the retail trade business, under the following conditions:

| (a) | A foreign retailer shall have a minimum paid-up capital of PhP 25 million; |

| (b) | The foreign retailer’s country of origin does not prohibit the entry of Filipino retailers; and |

| (c) | In the case of foreign retailers engaged in retail trade through more than one (1) physical store, the minimum investment per store must be at least PhP 10 million: Provided, That this requirement shall not apply to foreign investors and foreign retailers who are legitimately engaged in retail trade and were not required to comply with the minimum investment per store at the time of the effectivity of this Act: Provided, further, That proof of qualification to engage in retail trade under Republic Act No. 8762 and its implementing rules and regulations is submitted to the DTI. |

The foreign retailer shall be required to maintain in the Philippines at all times the paid-up capital PhP 25 million, unless the foreign retailer has notified the SEC or the DTI, whichever is appropriate, of its intention to repatriate its capital and cease operations in the Philippines. The actual use in Philippine operations of the minimum paid-up capital shall be monitored by the SEC, or by the DTI, whichever is appropriate.

Failure to maintain in the Philippines the paid-up capital required in the preceding paragraph, prior to notification of the SEC or the DTI, whichever is appropriate, shall subject the foreign retailer to penalties or restrictions on any future trading activities/business in the Philippines.

For purposes of registration with the SEC or DTI, the foreign retailer shall submit a certification from the Bangko Sentral ng Pilipinas (BSP) of the inward remittance of its capital investment, or in lieu thereof, such other proof certifying that is capital investment is deposited and maintained in a bank in the Philippines.

3

The implementing rules and regulations (“IRR”) of R.A. 8762, as amended by R.A. 11595, provides that foreign investors or foreign retailers may acquire shares in existing and operating retail stores, publicly listed or not. A foreign retailer is defined as a foreign national, partnership, association, or corporation of which more than forty percent (40%) of the capital stock outstanding and entitled to vote is owned and held by such foreign national, engaged in retail trade.

Foreign-owned partnerships, associations and corporation, upon registration with the SEC; on in case of foreign-owned single proprietorships, upon registration with the Department of Trade and Industry (DTI), may engage or invest in retail trade, under the following conditions:

| ● | A foreign retailer shall have minimum paid-up capital of PhP25 million; |

| ● | The foreign retailer’s country of origin provides for reciprocity to Filipinos. |

Foreign Investments Act of 1991

Republic Act No. 7042, otherwise known as the Foreign Investments Act of 1991 (“Foreign Investments Act”), liberalized the entry of foreign investment into the Philippines. As a general rule, there are no restrictions on extent of foreign ownership of export enterprises. In domestic market enterprises, foreigners can invest as much as one hundred percent (100%) equity except in areas included in the Foreign Investment Negative List. The latest Foreign Investment Negative List (Twelfth) maintains the prohibition of foreign equity for retail trade enterprises with paid-up capital of less than PhP25 million under R.A. 11595, amending R.A. 8762.

For the purpose of complying with nationality laws, the term “Philippine National” is defined under the Foreign Investments Act as any of the following:

| ● | a citizen of the Philippines; |

| ● | a domestic partnership or association wholly owned by citizens of the Philippines; |

| ● | a corporation organized under the laws of the Philippines of which at least 60% of the capital stock outstanding and entitled to vote is owned and held by citizens of the Philippines; |

| ● | a corporation organized abroad and registered to do business in the Philippines under the Revised Corporation Code of the Philippines, of which 100% of the capital stock outstanding and entitled to vote is wholly owned by Filipinos; or |

| ● | a trustee of funds for pension or other employee retirement or separation benefits, where the trustee is a Philippine National and at least 60% of the fund will accrue to the benefit of Philippine Nationals. |

For as long as the percentage of Filipino ownership of the capital stock of the corporation is at least 60% of the total shares outstanding and voting, the corporation shall be considered as a 100% Filipino-owned corporation.

Registration of Foreign Investments and Exchange Controls

Under current BSP regulations, an investment in Philippine securities must be registered with the BSP if the foreign exchange needed to service the repatriation of capital and/or the remittance of dividends, profits, and earnings derived from such shares is to be sourced from the Philippine banking system. If the foreign exchange required to service capital repatriation or dividend remittance will be sourced outside the Philippine banking system, registration with the BSP is not required. BSP Circular No. 471 issued on January 24, 2005 subjects foreign exchange dealers and money changers to RA No. 9160 (the Anti-Money Laundering Act of 2001, as amended) and requires these non-bank sources of foreign exchange to require foreign exchange buyers to submit supporting documents in connection with their application to purchase foreign exchange for purposes of capital repatriation and remittance of dividends.

Cash and Asset Flows through Our Organization

One and one Cayman is a holding company with no operations of its own. Its business operations are conducted through Contractual Arrangements between the intermediary holding company, One and one HK, and the VIEs in the Philippines. One and one Cayman is permitted under Cayman Islands laws to provide funding to its subsidiary in Hong Kong through loans or capital contributions without restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval and filing requirements. According to the Companies Ordinance of Hong Kong, a Hong Kong company may only make a distribution out of profits available for distribution. If One and one HK incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to One and one Cayman.

We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant.

4

Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. The laws and regulations of the PRC do not currently have any material impact on transfer of cash from One and one Cayman to One and one HK or from One and one HK to One and one Cayman. There are no restrictions or limitations under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S. investors.

The Company’s business is conducted through the VIEs. Funds may be paid by the VIEs to One and one HK as service fees pursuant to the Contractual Arrangements. The Company may rely on dividends paid by the intermediary holding company (i.e., One and one HK) for its working capital and cash needs, including the funds necessary: (i) to pay dividends or cash distributions to its shareholders, (ii) to service any debt obligations and (iii) to pay operating expenses. Cash dividends, if any, on our Ordinary Shares will be paid in U.S. dollars.

In order for us to pay dividends to our shareholders, we may rely on payments made from the VIEs to One and one HK and from One and one HK to One and one Cayman. For the fiscal years ended December 31, 2025 and 2024 and as of the date of this annual report, the VIEs have not made any transfers, loans, or distributions, and no transfers, dividends, and distributions have been made between One and one HK and VIEs, or to investors. We do not anticipate any difficulties or limitations on our ability to transfer cash between us, our subsidiary and VIEs. Other than the above discussed pursuant to the Contractual Arrangements, we do not have any cash management policies that dictate the amount of such funding among the Group and the VIEs.

3.A. [Reserved]

3.B. Capitalization and Indebtedness

Not Applicable.

3.C. Reasons for the Offer and Use of Proceeds

Not Applicable.

3.D. Risk Factors

Investing in our Class A Ordinary Shares is highly speculative and involves a significant degree of risk. You should carefully consider the following risks as well as all other information contained in this annual report, including the matters discussed under the headings “Forward-Looking Statements” and “Item 5. Operating and Financial Review and Prospects” before you decide to make an investment in our Class A Ordinary Shares. The risks discussed below could materially and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the trading price of our Class A Ordinary Shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability to pay dividends, and you may lose all or part of your investment.

Such risks are not exhaustive. We may face additional risks that are presently unknown to us or that we believe to be immaterial as of the date of this annual report. Known and unknown risks and uncertainties may significantly impact and impair our business operations through our subsidiaries and VIEs in Hong Kong, and Philippines.

Risk Factors Summary

Our business is subject to numerous risks described in the section titled “Risk Factors” and elsewhere in this annual report. The main risks set forth below and others you should consider are discussed more fully in the section entitled “Risk Factors”, which you should read in its entirety.

Risks Related to Our Business

| ● | We do not have a long operating history as an integrated group. |

| ● | We have limited experience operating as a standalone public company. |

| ● | We may incur losses in the future. |

| ● | Our historical financial and operating results are not a guarantee of our future performance. |

5

| ● | We have a substantial supplier concentration with a limited number of suppliers accounting for a substantial portion of our total purchases. Changes or difficulties in our relationships with our suppliers and loss may harm our business and financial results. |

| ● | We are currently dependent on a small group of customers for most of our revenue and the loss of, or a significant reduction in purchases by, one or more of our principal customers could materially and adversely affect our business, financial condition, and results of operations. |

| ● | Our reliance on customers located in China and Hong Kong exposes us to significant geopolitical, regulatory, and economic risks that could adversely affect our business operations and financial performance. |

| ● | We may face operational, regulatory, and reputational risks related to environmental compliance, workplace safety, and the handling of waste materials |

| ● | We do not have any commercial insurance coverage. |

| ● | We may be subject to litigation and regulatory investigations and proceedings and may not always be successful in defending ourselves against such claims or proceedings. |

| ● | Our future strategic acquisitions, investments and partnerships could pose various risks, increase our leverage, dilute existing shareholders and significantly impact our ability to expand our overall profitability. |

| ● | Any failure by the VIEs or their shareholders to perform their obligations under our Contractual Arrangements with them would have a material and adverse effect on our business. |

| ● | Any lack of requisite approvals, licenses or permits applicable to our business, or any non-compliance with relevant laws and regulations, may have a material and adverse effect on our business, financial condition, results of operations and prospects. |

| ● | Any adverse material changes to the Philippines market (whether localized or resulting from global economic or other conditions) such as the occurrence of an economic recession, pandemic or widespread outbreak of an infectious disease, could have a material adverse effect on our business, results of operations and financial condition. |

| ● | We may be affected by disruptions to our production. |

| ● | We may regularly encounter potential conflicts of interest, and our failure to identify and address such conflicts of interest could adversely affect our business. |

Risks Related to Doing Business in the Philippines

| ● | We may face political and social instability. |

| ● | Inflation in the Philippines could negatively affect our profitability and growth. |

| ● | We may face customs restrictions for the importation and exportation of metals. |

| ● | Our ability to source our products efficiently and cost-effectively could be negatively impacted if new trade restrictions are imposed, existing trade restrictions become more burdensome or relationships with exporters are impaired or terminated. |

| ● | It may be difficult for you to enforce any judgment obtained in the United States against us, our Directors, Executive Officers or our affiliates. |

Risks Related to Our Corporate Structure

| ● | Our corporate actions are substantially controlled by Ms. Caifen Yan, the Chair of the Board and Director of the Company, through One and one International Limited, which has the ability to control or exert significant influence over important corporate matters that require approval of shareholders, which may deprive you of an opportunity to receive a premium for your ordinary shares and materially reduce the value of your investment. Additionally, we may be deemed to be a “controlled company” and may follow certain exemptions from certain corporate governance requirements that could adversely affect our public shareholders. |

| ● | We and our Hong Kong subsidiary rely on Contractual Arrangements with the VIEs and the VIEs’ shareholders to operate their business, which may not be as effective as direct ownership in providing operational control. |

| ● | We rely on dividends and other distributions on equity paid by the VIEs to fund any cash and financing requirements we may have. To the extent cash or assets in our business are held in Hong Kong or by One and one HK, such funds or assets may not be available to fund operations or for other use outside of Hong Kong. |

| ● | Our Chair of the Board and Director, Ms. Caifen Yan, has significant control over shareholder matters and the minority shareholder will have little or no control over our affairs. |

6

| ● | We are a foreign private issuer within the meaning of the rules under the Exchange Act, and, as such, we are exempt from certain provisions applicable to U.S. domestic public companies. |

| ● | As a foreign private issuer, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from Nasdaq corporate governance listing standards. These practices may afford less protection to shareholders than they would enjoy if we complied fully with Nasdaq corporate governance listing standards. |

| ● | We may lose our foreign private issuer status in the future, which could result in significant additional costs and expenses.

| |

| ● | We are a “foreign private issuer,” and our disclosure obligations differ from those of U.S. domestic reporting companies. As a result, we may not provide you the same information as U.S. domestic reporting companies or provide information at different times, making it more difficult for you to evaluate our performance and prospects. |

| ● | There can be no assurance that we will not be a PFIC for U.S. federal income tax purposes for any taxable year, which could result in adverse U.S. federal income tax consequences to U.S. holders of our Class A Ordinary Shares. |

Risks Related to Our Class A Ordinary Shares

| ● | Our share price may fluctuate significantly in the future and you may lose all or part of your investment, and litigation may be brought against us. |

| ● | The dual class structure of our Class A Ordinary Shares has the effect of concentrating voting control with our Chairman and CEO, and their interest may not be aligned with the interests of our other shareholders. |

| ● | Our Class A Ordinary Shares may trade under $5.00 per share and thus would be known as “penny stock”. Trading in penny stocks has certain restrictions and these restrictions could negatively affect the price and liquidity of our Class A Ordinary Shares. |

| ● | We may not be able to pay dividends in the future. |

| ● | If we fail to meet applicable listing requirements, Nasdaq may delist our Class A Ordinary Shares from trading, in which case the liquidity and market price of our Class A Ordinary Shares could decline. |

| ● | We have incurred significant expenses and devoted other significant resources and management time as a result of being a public company, which may negatively impact our financial performance and could cause our results of operations and financial condition to suffer. |

| ● | If we fail to maintain an effective system of disclosure controls and internal controls over financial reporting, our ability to timely produce accurate financial statements or comply with applicable regulations could be impaired. |

| ● | We are an emerging growth company within the meaning of the Securities Act and may take advantage of certain reduced reporting requirements. |

Risks Related to Our Business

We do not have a long operating history as an integrated group.

One and one Cayman was incorporated as a holding company on April 17, 2024. While the VIEs have been in operation since 2014, we do not have a long history of running an integrated group with standardized policies and procedures on which our past performance may be judged. Given our limited operating history as an integrated group and the rapidly evolving market in which we compete, we may encounter operational, financial and other difficulties as we establish and expand our operations, product and service developments, sales and marketing, technology and general and administrative capabilities.

We have limited experience operating as a standalone public company.

We have limited experience conducting our operations as a standalone public company. We may encounter operational, administrative, and strategic difficulties as we adjust to operating as a standalone public company. This may cause us to react more slowly than our competitors to industry changes and may divert our management’s attention from running our business or otherwise harm our operations.

In addition, since we are a public company, our management team will need to develop the expertise necessary to comply with the numerous regulatory and other requirements applicable to public companies, including requirements relating to corporate governance, listing standards and securities and investor relationships issues. As a standalone public company, our management will have to evaluate our internal controls system with new thresholds of materiality, and to implement necessary changes to our internal controls system. We cannot guarantee that we will be able to do so in a timely and effective manner.

7

We may incur losses in the future.

For the years ended December 31, 2025, and December 31, 2024, the Company recorded net income of $11,811,614 and $6,476,772, respectively. We anticipate that our operating expenses, together with the increased general administrative expenses of a public company, will increase in the foreseeable future as we seek to maintain and continue to grow our business, in particular retail store expansion, attract potential customers, and further enhance our service offering. Our expenses when expressed in US dollars also are exposed to increases due to depreciation of the Philippines Peso. These efforts may prove more expensive than we currently anticipate, and we may not succeed in increasing our revenue sufficiently to offset these higher expenses. As a result of the foregoing and other factors, we may incur net losses in the future and may be unable to achieve or maintain sufficient cash flows or profitability on a quarterly or annual basis for the foreseeable future.

Our historical financial and operating results are not a guarantee of our future performance.

Our annual and periodic financial results vary from year to year and from period to period, in response to a number of factors that we cannot predict, such as general business outlook and sentiment, economic market conditions, employment rates, inflation and interest rates and consumer confidence. As such, we believe that our annual and periodic financial results are not a guarantee of our future economic performance and undue reliance should not be placed on such results for future speculative purposes.

We have a substantial supplier concentration with a limited number of suppliers accounting for a substantial portion of our total purchases. Changes or difficulties in our relationships with our suppliers and loss may harm our business and financial results.

We rely on a limited number of waste exporters and commercial agents as our suppliers. For the fiscal years ended December 31, 2025, and December 31, 2024, we had four and four major suppliers respectively, who accounted for more than 10% of our total purchases. For the year ended December 31, 2025, four suppliers accounted for approximately 38.9%, 13.3%, 12.3%, and 10.6% of the total purchases. For the year ended December 31, 2024, four suppliers accounted for approximately 45.7%, 12.6%, 10.7% and 10.5% of the total purchases.

Inherent risks exist whenever procurement is concentrated with a limited number of suppliers. Our suppliers may fail to meet their procurement obligations, which may adversely affect our business. We enter into supply contracts with our suppliers, typically lasting for one year with automatic one year extension absent either party’s objection. Both parties have the right to terminate the agreement upon notifying the other party in advance. There is no assurance that we can continue to maintain stable and long-term business relationships with any supplier. Failure to maintain existing relationships with the suppliers or to establish new relationships in the future could negatively affect the Company’s ability to deliver products to customers in a price advantageous and timely manner. If the Company is unable to obtain ample supply of waste metal materials from existing suppliers or alternative sources of supply, the Company may be unable to satisfy the orders from its customers, which could materially and adversely affect our business, results of operations and financial condition.

We are currently dependent on a small group of customers for most of our revenue and the loss of, or a significant reduction in purchases by, one or more of our principal customers could materially and adversely affect our business, financial condition, and results of operations.

We derive a significant portion of our revenue from a limited number of long-term, cooperative importer customers located primarily in Mainland China and Hong Kong. As of the date of this annual report, we have established cooperative relationships with nine principal importers. While we enter into master sales agreements or purchase orders with these customers that specify key terms such as product specifications, pricing, weight, delivery, and payment terms, such contracts may be written, oral, or implied through customary business practices, and are typically subject to six-month credit terms, which may be extended for large projects.

For the fiscal years ended December 31, 2025, and 2024, we had three and three major customers respectively, who accounted for more than 10% of our total revenue. For the year ended December 31, 2025, three customers accounted for approximately 26.8%, 48.8% and 24.4% of the total revenue, respectively. For the year ended December 31, 2024, three customers accounted for approximately 56.37%, 22.23%, and 17.43% of the total revenue.

Due to this customer concentration, a loss of, or material reduction in orders from, any one of these key customers — whether due to customer-specific factors, market conditions, shifts in demand, or deteriorating business relationships — could result in a substantial decline in our revenue. In addition, if any of our major customers were to delay payment or become unable to meet their financial obligations, it could adversely affect our liquidity and cash flow. Our dependence on a small group of customers exposes us to increased risks and limits our ability to mitigate downturns in specific customer segments or geographic regions.

If we are unable to maintain our existing customer relationships, or if we fail to attract new customers to diversify our client base, our business, financial condition, and results of operations may be materially and adversely affected.

8

Our reliance on customers located in China and Hong Kong exposes us to significant geopolitical, regulatory, and economic risks that could adversely affect our business operations and financial performance.

We currently depend on a limited number of long-term importers based in China and Hong Kong for the sale of our processed metal products. The evolving political and legal landscape in China and Hong Kong, has introduced heightened legal and regulatory uncertainties for businesses. Both China and Hong Kong maintain distinct import regulations, customs policies, and environmental standards. Sudden changes in import licensing rules, inspection procedures, or restrictions on the import of scrap metal products could delay shipments, increase costs, or reduce demand for our products. While we are based in the Philippines, broader geopolitical tensions involving China — such as its relations with neighboring countries in the Asia-Pacific region — could indirectly impact trade routes, port access, or cross-border logistics efficiency, thereby affecting our ability to deliver products in a timely manner. Economic slowdowns, policy shifts, or financial instability within China and Hong Kong can also lead to decreased demand for our products, payment delays, or defaults by our customers. Such economic fluctuations can have a direct adverse effect on our revenue and profitability.

We may face operational, regulatory, and reputational risks related to environmental compliance, workplace safety, and the handling of waste materials.

Our operations involve the processing of waste materials, including imported industrial residues that have undergone preliminary detoxification prior to transportation. While these materials are delivered to us in a secured manner, and we implement emission control systems during the incineration and processing phases, our activities may still pose certain environmental and safety risks.

We are subject to Philippine environmental, and safety regulations governing emissions, waste handling, and workplace safety. These regulations may become more stringent over time, potentially requiring us to upgrade our facilities, adopt new technologies, or incur higher compliance costs. Any failure to comply with these regulations, or any perception of inadequate handling of materials, could result in fines, operational delays, or reputational damage.

In addition, the sorting of scrap materials presents inherent occupational safety risks. Although we have adopted workplace safety protocols, any lapse or accident could disrupt operations, lead to regulatory scrutiny, or expose us to liability. Furthermore, inconsistent quality or composition of scrap materials, and any delays or disruptions in logistics, could impact our processing efficiency and operating margins.

We do not have any commercial insurance coverage.

Our company does not currently maintain any insurance coverage, which exposes us to significant operational and financial risks. As a metal scrap processing company operating in the Philippines, we are highly dependent on our large workforce. In the event of accidents, workplace injuries, or other unforeseen incidents, the absence of insurance could result in substantial financial liabilities and disruptions to our operations. Additionally, without insurance, we face increased risks related to property damage, equipment failures, and potential legal claims, all of which could severely impact our business. This lack of insurance coverage may also affect our ability to attract and retain employees, further jeopardizing our operational stability and growth prospects. Consequently, our financial condition, results of operations, and overall business prospects could be materially and adversely affected by our lack of insurance.

To mitigate against such risk, we have outsourced our property security to professional safety officers who conduct regular, daily patrols to prevent emergency situations. All employees are provided with fully paid social insurance, which includes coverage for medical care and accident insurance.

We may be subject to litigation and regulatory investigations and proceedings and may not always be successful in defending ourselves against such claims or proceedings.

Along with the growth and expansion of our business, we may be involved in litigation, regulatory proceedings, and other disputes arising outside the ordinary course of our business. Such litigation and disputes may result in claims for actual damages, freezing of our assets, diversion of our management’s attention and reputational damage to us and our management, as well as legal proceedings against our directors, officers, or employees, and the probability and amount of liability, if any, may remain unknown for long periods of time. In market downturns, the number of legal claims and the amount of damages sought in litigation and regulatory proceedings may increase. Our clients may also be involved in litigation, investigation or other legal proceedings, some of which may relate to deals that we have advised, whether or not there has been any fault on our part.

Our future strategic acquisitions, investments and partnerships could pose various risks, increase our leverage, dilute existing shareholders and significantly impact our ability to expand our overall profitability.

Acquisitions involve inherent risks, such those relating to increased leverage and debt service requirements and post-acquisition integration challenges, which could have a material and adverse effect on our results of operations and/or cash flow and could strain our human resources. We may be unable to successfully implement effective cost controls or achieve expected synergies as a result of a future acquisition. Acquisitions may result in our assumption of unexpected liabilities and the diversion of management’s attention from the operation of our business. Acquisitions may also result in our having greater exposure to the industry risks of the businesses underlying the acquisition. Strategic investments and partnerships with other companies expose us to the risk that we may not be able to control the actions of our investees or partners, which could decrease the amount of benefits we realize from a particular relationship. We are also exposed to the risk that our partners in strategic investments and infrastructure may encounter financial difficulties that could lead to a disruption of investee or partnership activities, or an impairment of assets acquired, which could adversely affect future reported results of operations and shareholders’ equity. Acquisitions may subject us to new or different regulations or tax consequences which could have an adverse effect on our operations.

9

In addition, we may be unable to obtain the financing necessary to complete acquisitions on attractive terms or at all. If we raise additional funds through future issuances of equity or convertible debt securities, our existing shareholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences and privileges superior to those of holders of our Class A Ordinary Shares. Future equity financings would also decrease our earnings per share and the benefits derived by us from such new ventures or acquisitions might not outweigh or exceed their dilutive effect. Any additional debt financing we secure could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital or to pursue business opportunities. Realization of any of the foregoing risks associated with future strategic acquisitions, investments and partnerships could materially and adversely affect our business, results of operations and financial condition.

As of the date of this annual report, we have not identified any specific acquisition, investment, or partnership target.

Any failure by the VIEs or their shareholders to perform their obligations under our Contractual Arrangements with them would have a material and adverse effect on our business.

If the VIEs or their shareholders fail to perform their respective obligations under the Contractual Arrangements, we may have to incur substantial costs and expend additional resources to enforce such arrangements. We may also have to rely on legal remedies under Philippine law, including seeking specific performance or injunctive relief, and contractual remedies, which we cannot assure you will be sufficient or effective under Philippine law. For example, if the shareholders of the VIEs were to refuse to transfer their equity interests in the VIEs to us or our designee if we exercise the purchase option pursuant to these Contractual Arrangements, or if they were otherwise to act in bad faith toward us, then we may have to take legal actions to compel them to perform their contractual obligations. In addition, if any third parties claim any interest in such shareholders’ equity interests in the VIEs, our ability to exercise shareholders’ rights or foreclose the share pledge according to the Contractual Arrangements may be impaired. If these or other disputes between the shareholders of the VIEs and third parties were to impair our control over the VIEs, our ability to consolidate the financial results of the VIEs would be affected, which would in turn result in a material adverse effect on our business, operations and financial condition.

These Contractual Arrangements are governed by and interpreted in accordance with the laws of the Philippines. The legal system in the Philippine is still developing. As a result, uncertainties in the Philippine legal system could limit our ability to enforce these Contractual Arrangements. Further, there are very few precedents and little formal guidance as to how Contractual Arrangements in the context of a consolidated VIE should be interpreted or enforced under Philippine law. There remain significant uncertainties regarding the ultimate outcome of such arbitration should legal action become necessary. In addition, under Philippine law, rulings by arbitrators are final and parties cannot appeal the arbitration results in courts, and if the losing parties fail to carry out the arbitration awards within a prescribed time limit, the prevailing parties may only enforce the arbitration awards in Philippine courts through arbitration award recognition proceedings, which would require additional expenses and delay. In the event we are unable to enforce the Contractual Arrangements, or we experience significant delays or other obstacles in the process of enforcing these Contractual Arrangements, we may not be able to exert effective control over the VIEs and may lose control over the assets owned by them. As a result, we may be unable to consolidate the consolidated financial statements of the Philippine operating entities and our ability to conduct business may be negatively affected.

Any lack of requisite approvals, licenses or permits applicable to our business, or any non-compliance with relevant laws and regulations, may have a material and adverse effect on our business, financial condition, results of operations and prospects.

Our business is subject to governmental supervision and regulation by various governmental authorities including, but not limited to, Bureau of Internal Revenue Philippines, Securities and Exchange Commission, Department of Trade and Industry Philippines, and various local government units. Such government authorities promulgate and enforce laws and regulations that cover a variety of business activities that our operations concern. These regulations in general regulate the entry into, the permitted scope of, as well as approvals, licenses and permits for, the relevant business activities.

In addition to obtaining necessary approvals, licenses and permits for conducting our business, we must comply with relevant laws and regulations. Our businesses, waste materials and scrap metal resource recovery, are subject to various and complex laws and regulations, extensive government regulations and supervision. We may not be fully informed of all and new requirements under relevant laws and regulations in a timely manner, and even if we become aware of new requirements, due to uncertainties in their interpretations and implementation, it will be difficult for us to determine what actions or omissions would be deemed as violations of applicable laws and regulations. We may also not be able to respond to evolving laws and regulations and take appropriate action in time to adjust our business model. As a result, we may be in violation or non-compliance with such laws and regulations.

Due to the uncertainties in the regulatory environment of the industries in which we operate, there can be no assurance that we have obtained or applied for all the approvals, permits and licenses required for conducting our business and all activities in the Philippines, or that we would be able to maintain our existing approvals, permits and licenses or obtain any new approvals, permits and licenses if required by any future laws or regulations. If we fail to obtain and maintain approvals, licenses or permits required for our business, or to comply with relevant laws and regulations, we could be subject to liabilities, fines, penalties and operational disruptions, or we could be required to modify our business model, which could materially and adversely affect our business, financial condition and results of operations.

10

Any adverse material changes to the Philippines market (whether localized or resulting from global economic or other conditions) such as the occurrence of an economic recession, pandemic or widespread outbreak of an infectious disease, could have a material adverse effect on our business, results of operations and financial condition.

Since 2014, all of our revenue was derived from our operations in Philippines. Any adverse circumstances affecting the Philippines market, such as an economic recession, epidemic outbreak or natural disaster or other adverse incident, may adversely affect our business, financial condition, results of operations and prospects. Any downturn in the industry which we operate in resulting in the postponement, delay or cancellation of contracts and delay in recovery of receivables is likely to have an adverse impact on our business and profitability.

Uncertain global economic conditions have had and may continue to have an adverse impact on our business in the form of lower net sales due to weakened demand, unfavorable changes in product price/mix, or lower profit margins. For example, global economic downturns have adversely impacted some of our dealers who are particularly sensitive to business and consumer spending.

An epidemic or outbreak of communicable diseases may also adversely affect our business, financial condition, results of operations and prospects. The COVID-19 epidemic resulted in a global health crisis, causing disruptions to social and economic activities, business operations and supply chains worldwide, including in Philippines. Measures taken by the Philippines government to tackle the spread of COVID-19 have included, among others, border closures, quarantine measures and lockdown measures.

In the event of a resurgence of COVID-19, if a substantial number of our employees are infected with and/or are suspected of having COVID-19, and our employees are required to be quarantined and/or hospitalized, this may disrupt our ability to manage our business which may have a material adverse effect on our business operations and reputation of our Group.

We may be affected by disruptions to our production.

Our production site in the Philippines is subject to adverse weather conditions, including rainfall, flood and typhoons, which could disrupt our operations. These weather conditions may cause damage to infrastructure, including walls, roads, and other facilities at our plant, necessitating costly repairs and maintenance. The occurrence of any of the above events may cause us to stop or suspend our production process, which would have an adverse impact on our business, financial position and profitability. While we have implemented measures to mitigate these risks, such as reinforcing infrastructure and roads, we cannot assure that these measures will be sufficient to prevent significant operational disruptions or financial losses. If we are unable to effectively manage these risks, our business, financial condition, and results of operations could be materially and adversely affected.

We may regularly encounter potential conflicts of interest, and our failure to identify and address such conflicts of interest could adversely affect our business.

We face the possibility of actual, potential, or perceived conflicts of interest in the ordinary course of our business operations. Conflicts of interest may exist between (i) us and our clients; (ii) our clients; (iii) us and our employees; (iv) our clients and our employees or (v) us and our major shareholders. As we expand the scope of our business and our client base, it is critical for us to be able to address timely potential conflicts of interest, including situations where two or more interests within our businesses naturally exist but are in competition or conflict. We have put in place internal control and risk management procedures that are designed to identify and address conflicts of interest, including a procedure for presenting potential conflicts of interest to the audit committee of our Board of Directors. However, appropriately identifying and managing actual, potential, or perceived conflicts of interest is complex and difficult, and our reputation and our clients’ confidence in us could be damaged if we fail, or appear to fail, to deal appropriately with one or more actual, potential, or perceived conflicts of interest. It is possible that actual, potential, or perceived conflicts of interest could also give rise to client dissatisfaction, litigation, or regulatory enforcement actions. Regulatory scrutiny of, or litigation in connection with, conflicts of interest could have a material adverse effect on our reputation, which could materially and adversely affect our business in a number of ways, including a reluctance of some potential clients and counterparties to do business with us. Any of the foregoing could materially and adversely affect our reputation, business, financial condition, and results of operations.

A conflict of interest occurs when an individual’s private interest (or the interest of a member of his or her family or close friend(s) or business associate(s)) interferes, or even appears to interfere, with the interests of our company as a whole. A conflict of interest can arise when an employee, officer or Director (or a member of his or her family or a close friend(s) or business associate(s)) takes actions or has interests that may make it difficult to perform his or her work for our Company objectively and effectively. Conflicts of interest also arise when an employee, officer or Director (or a member of his or her family or close friend(s) or business associate(s)) receives improper personal benefits as a result of his or her position in our Company.

Directors and executive officers must seek determinations and prior authorizations or approvals of potential conflicts of interest exclusively from our audit committee. All other employees are required to approach our Chief Executive Officer or our Chief Financial Officer if they have any questions about reporting a suspected conflict of interest.

11

Risks Related to Doing Business in Philippines

We may face political and social instability.

Potential foreign investors should take into consideration the political and social environment in the Philippines and its current international conflicts. This is because any change in the political and international relations of the Philippines could affect its business operations in the Philippines.

Recently, the Republic of the Philippines and the People’s Republic of China have been in a dispute in the West Philippine Sea (also known as the South China Sea). The dispute is a complex geopolitical issue with significant implications for regional stability, maritime security, and international law.

The most recent development concerning this matter involves a confrontation between the Philippine coast guard and their Chinese counterparts. According to a statement from a Philippine government task force, China Coast Guard and Chinese Maritime Militia vessels engaged in acts of harassment, obstruction, and dangerous maneuvers during a routine resupply and rotation mission. The statement reported that during the incident, two China Coast Guard ships fired water cannons at Unaizah May 4, a military chartered boat carrying replacement soldiers and supplies to Second Thomas Shoal, where Filipino troops are stationed on a grounded Philippine navy vessel, the BRP Sierra Madre. Second Thomas Shoal, also called the Ayungin Shoal, serves as the location for BRP Sierra Madre, a navy vessel deliberately grounded on the sandbank in 1999 to assert the Philippines’ claim in the West Philippine Sea.

Before this incident, there were numerous harassments made by the Chinese coast guard to the boats of Philippine fishermen and the Philippine coast guard. These incidents were aggravated by the Chinese government in insisting that former President Rodrigo Duterte entered a “secret deal” with China wherein he purportedly relinquished the disputed territory in the West Philippine Sea to China and agreed not to have any repairs done on BRP Sierra Madre.

Due to the rising tension in the West Philippine Sea the Philippines, together with the American, Australian and French forces, began the Balikatan 2024 in the West Philippine Sea. According to Lt. Den Jurney during the opening ceremony of the Balikatan exercise, “Balikatan is more than an exercise; it’s a tangible demonstration of our shared commitment to each other. It matters for regional peace, it matters for regional stability,” When we increase our mutual response and defense capabilities, we strengthen our ability to promote regional security and protect our shared interests.”

Moreover, the Philippines has experienced various terrorist attacks in the past years, with the Armed Forces of the Philippines engaged in conflicts with groups responsible for kidnapping and terrorism within the country. Additionally, bombings have occurred primarily in urban areas in the southern region of the Philippines.

The escalation of the tension in the West Philippine Sea and the frequency, severity, or geographic extent of these terrorist activities could unsettle the Philippines and have detrimental effects on the nation’s economy. We cannot guarantee the stability of the political landscape in the Philippines or the economic policies pursued by the current or future administrations, which may impact the regulatory framework for retail and trade industries.

Inflation in the Philippines could negatively affect our profitability and growth.

The economy of the Philippines experienced significant growth, leading to inflation and increased costs. For 2025, the country recorded an annual average inflation rate of 1.7%, lower than the annual average rate of 3.2% in 2024. For 2024, The country recorded an average inflation rate of 3.2%, lower than the annual average rate of 6% in 2023. High inflation and monetary tightening are likely to soon weigh more significantly on domestic activity, which can negatively impact purchasing power and lead to tough financial decisions for company. Inflation refers to a broad rise in the prices of raw material and products over time, eroding purchasing power for company but in another way increasing revenue. The fluctuation of price of raw material effects the stability of supply chain that may play negative impact to our operation.

Our operations in the Philippines are exposed to inflationary pressures, which have been exacerbated by global supply chain disruptions, rising energy costs, and local economic factors. Inflation could lead to higher costs for materials, labor, and services, affecting the Company’s operating expenses and margins if these increases cannot be passed on to customers.

We may face customs restrictions for the importation and exportation of metals.

Every business engaged in the importation and exportation of goods is subject to regulatory framework marked by complexity and possible operational intricacies. The importation process is contingent upon meticulous compliance with a spectrum of regulations, encompassing customs procedures, health and safety standards, and adherence to evolving governmental policies.

12

Yoda Metal is a retail and trading company. One of its primary purposes is to engage with the exportation and importation of all kinds of metal scrap, goods, wares, merchandise, or products whether natural or artificial. Therefore, it is subject to the rules and regulations of the Philippines with respect to its importation and exportation activities.

Yoda Metal’s importation and exportation of metals should comply with the relevant directives and regulations of the Bureau of Customs (BOC). Republic Act. No. 10863, also referred to as the Customs Modernization and Tariff Act (CMTA), revised the Tariff and Customs Code of the Philippines, and serves as the primary law governing the importation and exportation process in the Philippines.

Pursuant to Sec. 104 of the CMTA, all goods imported into the Philippines, shall be subject to duty upon importation, including goods previously exported from the Philippines, unless otherwise exempted by the CMTA or other special laws.

It must be noted that an imported product can be classified either as: (a) Free Importation and Exportation — goods that may be freely imported into and exported without the need for other permits, licenses, and clearances; (b) Regulated Importation and Exportation — goods which are subject to regulation and requires prior declaration, clearances, licenses; (c) Restricted Importation and Exportation — goods which are generally prohibited unless the law grants a special exemption; and (d) Prohibited Importation and Exportation — goods which are expressly prohibited. One of the prohibited importations, as stated in Sec. 118(d) of RA 10863, is any goods manufactured in whole or in part of gold, silver or other precious metals or alloys and the stamp, brand or mark does not indicate the actual fineness of quality of the metals or alloys.

In the metal and steel processing and trading sector, Yoda Metal must adhere to rigorous regulations encompassing environmental standards, import and export protocols, and trade guidelines. Securing the requisite permits and abiding by the regulations are fundamental aspects of its operations. It is crucial to acknowledge the dynamic nature of the legislative and regulatory framework within which we operate. Changes, whether in the form of new laws, amendments, or shifting interpretations, may lead to increased operational expenses or necessitate adjustments in its business methodologies.

Our ability to source our products efficiently and cost-effectively could be negatively impacted if new trade restrictions are imposed, existing trade restrictions become more burdensome or relationships with exporters are impaired or terminated.

The Philippine Constitution has a mandate that certain industries be wholly owned by Filipinos or majority of its ownership is held by Filipinos. Foreign Investments Act of 1991 was also enacted to limit the amount of investment permitted to foreign investors.

Failure to comply with the foreign ownership restrictions mandated by the Philippine Constitution and relevant laws can result in significant legal and financial repercussions for the Company. Non-compliance may lead to the imposition of severe penalties, including fines, suspension or revocation of business permits and licenses. Additionally, the company could be subject to legal actions initiated by regulatory bodies or affected third parties, which could result in costly litigation and damage to the company’s reputation. This non-compliance could also hinder the company’s ability to raise capital, expand operations, and attract future foreign investment, thereby adversely affecting its financial performance and growth prospects.

It may be difficult for you to enforce any judgment obtained in the United States against us, our Directors, Executive Officers or our affiliates.