This summary highlights selected information from this proxy statement/prospectus and does not contain all of the information that may be important to you. To better understand the proposals to be submitted for a vote at the EGM, including the Business Combination Proposal and Domestication Proposal, you should read this entire document carefully, including the Business Combination Agreement attached as Annex A to this proxy statement/prospectus. The Business Combination Agreement is the legal document that governs the Business Combination and is also described in detail in this proxy statement/prospectus in the section entitled “The Business Combination.”

Parties to the Business Combination

Cartesian Growth Corporation III

CGC is a blank check company incorporated to effect a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. CGC was incorporated on October 29, 2024 as a Cayman Islands exempted company.

CGC Units, CGC Class A Shares and CGC Public Warrants are currently listed on Nasdaq under the symbols “CGCTU,” “CGCT” and “CGCTW,” respectively.

The mailing address of CGC’s principal executive offices is 505 Fifth Avenue, 15th Floor, New York, NY 10017, and its phone number is (212) 461-6363.

Fenway MS, Inc.

Merger Sub is a Delaware corporation and wholly-owned subsidiary of CGC. Merger Sub was formed solely for the purpose of effecting the Business Combination and has not carried on any activities other than those in connection with the Business Combination. The address and telephone number for Merger Sub’s principal executive offices are the same as those for CGC.

Factorial Inc.

Factorial, a U.S.-based leader in solid-state battery technology, develops next-generation battery technology with high energy density for planned use in drones, on-road vehicles, mobile robots, energy storage, and other applications that demand high energy density.

Background and Material Terms of the Business Combination

CGC was incorporated for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or other similar business combination with one or more businesses. Following the completion of its IPO, at the direction of the CGC Board, CGC’s management and directors commenced a search for potential business combination targets, leveraging CGC’s and Sponsor’s network of company founders and executives, investment bankers, private equity firms and hedge funds and numerous other business relationships, as well as the prior experience and network of CGC’s management and directors. CGC conducted preliminary due diligence on, and, in some cases, entered into confidentiality agreements with, more than one dozen companies from May 2025 through December 2025, including Factorial. CGC management ultimately decided to focus its efforts on Factorial because, following its preliminary review of other potential targets, CGC concluded that Factorial represented the most attractive opportunity based on its alignment with CGC’s investment criteria and strategic objectives established at the time of its IPO.

The terms of the Business Combination Agreement are the result of extensive negotiations between the representatives of CGC and Factorial, each in consultation with its advisors, which occurred between August 5, 2025 and December 17, 2025.

CGC and Factorial pursued the PIPE Investment in order to provide additional capital to fund Factorial’s operations, research and development, and administration after the Business Combination is completed.

Concurrently with the execution of the Business Combination Agreement, on December 17, 2025, CGC entered into a Stock Purchase Agreement with an affiliate of the Sponsor and a Stock Purchase Agreement with a certain institutional investor. Pursuant to the Investor Stock Purchase Agreements, the Institutional Investor subscribed for 7,500,000 shares of PubCo Series A Common Stock at a subscription price of $10.00 per share, and the Sponsor Investor subscribed for 2,427,184 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) at a subscription price equal to the Redemption Price. Pursuant to the Investor Stock Purchase Agreements, the Sponsor will transfer at the Closing (which transfer may be indirectly through forfeiture and reissuance) an aggregate of 750,000 shares of PubCo Series A Common Stock to the Institutional Investor and 250,000 shares of PubCo Series A Common Stock to the Sponsor Investor. The effective subscription prices are $9.09 per share and $9.34 per share for the Institutional Investor and the Sponsor Investor, respectively, assuming a Redemption Price of $10.30 per share and taking into account taking into account the transfer of an aggregate of 1,000,000 Founder Shares from the Sponsor. No existing Factorial Stockholders (other than investors who were existing CGC Shareholders) subscribed to the PIPE Investments, existing CGC Shareholders (other than investors who were existing Factorial Stockholders) or their affiliates subscribed for $25 million of the PIPE Investments, no investors who were both existing shareholders of CGC and Factorial subscribed for PIPE Investments, and investors who were neither existing Factorial Stockholders nor existing CGC Shareholders subscribed for $75 million of the PIPE Investments. Either PIPE Investor may satisfy the purchase obligations under its respective Investor Stock Purchase Agreement through the purchase of CGC Class A Shares on the open market, provided such PIPE Investor complies with the requirements of their Investor Stock Purchase Agreement or a separate Non-Redemption Agreement, as applicable, with respect to the treatment of such shares.

As contemplated by the Business Combination Agreement, the structure and timing of the Business Combination and PIPE Investment are consistent with common practice in initial business combination transactions consummated by special purpose acquisition companies. In addition, the timing for the consummation of the Business Combination provided for in the Business Combination Agreement and Investor Stock Purchase Agreements, which was effectively as soon as reasonably practicable following the execution of the Business Combination Agreement, was determined and agreed by the parties in light of general business considerations weighing in favor of consummating the transaction promptly and the deadline for CGC to complete an initial business combination pursuant to the CGC Articles.

For more information, see “Proposal No. 1 — The Business Combination Proposal — Background of the Business Combination.”

The Business Combination Agreement

Pursuant to the Business Combination Agreement, and subject to the satisfaction or waiver of certain conditions set forth therein, the following will occur: (1) the Domestication of CGC as a Delaware corporation is intended to occur one business day prior to the Closing Date, in which CGC will de-register from the Register of Companies in the Cayman Islands and transfer by way of continuation out of the Cayman Islands and into the State of Delaware so as to migrate to and domesticate as a Delaware corporation in accordance with the CGC Articles, Section 388 of the DGCL and Part XII of the Cayman Islands Companies Act (As Revised); (2) on the Closing Date, the Merger of Merger Sub with and into Factorial, with Factorial surviving the Merger as a wholly-owned subsidiary of CGC, in accordance with the Business Combination Agreement and DGCL; and (3) the other transactions contemplated by the Business Combination Agreement and documents related thereto, all as described in more detail elsewhere in this proxy statement/prospectus. In connection with the Closing, CGC will be renamed Factorial Holdings, Inc. To the extent any CGC Units remain outstanding and unseparated immediately prior to the Merger Effective Time, the Public Shares and CGC Public Warrants comprising each such issued and outstanding CGC Unit immediately prior to the Merger Effective Time will be automatically separated without any action required by the holder, and the holder of each CGC Unit will be deemed to hold one Public Share and one - half (1/2) of one CGC Public Warrant. The Public Shares and CGC Public Warrants held following the unit separation will be converted as described below in accordance with the Business Combination Agreement. Following the Merger Effective Time, the CGC Units will cease trading on Nasdaq, no CGC Units will be in existence, and the CGC Units will not be listed on Nasdaq following the Closing. Holders of CGC Units who wish to exercise their redemption rights with respect to the underlying Public Shares must separately elect to cause the separation of their CGC Units prior to exercising such redemption rights and prior to the applicable deadline for submitting redemption requests. See “The Extraordinary General Meeting—Redemption Rights.”

| (A) | Immediately prior to the Domestication, (1) CGC will effect the redemption of the Public Shares that are validly submitted for redemption and not withdrawn, and (2) the Class B Share Conversion will occur, whereby each holder of issued and outstanding CGC Class B Share will irrevocably and unconditionally elect to convert, on a one-for-one basis, each CGC Class B Share held by it into one CGC Class A Share. |

| (B) | The Domestication is intended to occur one business day prior to the Closing, whereby CGC will de- register in the Cayman Islands and transfer by way of continuation out of the Cayman Islands and into the State of Delaware so as to migrate to and domesticate as a Delaware corporation. In connection with the Domestication, CGC will change its name to “Factorial Holdings, Inc.” |

| (C) | At the Domestication Effective Time, each outstanding CGC Class A Share (excluding Public Shares validly submitted for redemption, but including CGC Class A Shares issued upon the Class B Share Conversion) will be reclassified as one share of PubCo Series A Common Stock. |

| (D) | On the day of the Closing, the Merger will occur. At the Merger Effective Time, each share of Factorial’s capital stock that is issued and outstanding as of immediately prior to the Merger Effective Time (excluding treasury shares, dissenting shares and shares held by the Factorial Founders) will be automatically canceled and converted into the right to receive a corresponding number of shares of PubCo Series A Common Stock equal to the Consideration Ratio and each share of Factorial’s capital stock that is issued and outstanding as of immediately prior to the Merger Effective Time held by the Factorial Founders will automatically be canceled and converted into the right to receive a corresponding number of shares of Pubco Series B Common Stock equal to the Consideration Ratio (see “Consideration” below). All of the shares of PubCo Series B Common Stock will be held by the Factorial Founders, both of whom will serve as executive officers and directors of PubCo. The rights of the holders of PubCo Series A Common Stock and PubCo Series B Common Stock will be identical, except with respect to voting and conversion rights. Each share of PubCo Series B Common Stock will be entitled to ten votes and will be convertible at any time into one share of PubCo Series A Common Stock. |

| ● | each CGC Public Warrant that is issued and outstanding as of immediately prior to the Merger Effective Time will be automatically canceled and converted into the right to receive a PubCo Public Warrant and each CGC Private Warrant that is issued and outstanding as of immediately prior to the Merger Effective Time will be automatically canceled and converted into the right to receive a PubCo Private Warrant; |

| ● | each outstanding and unexercised option to purchase shares of Factorial common stock will become an option of PubCo containing the same terms, conditions, vesting and other provisions as are currently applicable to such Factorial Options, provided that each PubCo Option will be exercisable for the number of shares of PubCo Series A Common Stock equal to the Consideration Ratio multiplied by the number of shares of Factorial common stock subject to the Factorial Option as of immediately prior to the Merger Effective Time, rounded down to the nearest whole share, at an exercise price equal to the per share exercise price of the Factorial Option divided by the Consideration Ratio, rounded up to the nearest whole cent; |

| ● | each restricted stock unit award that is outstanding with respect to shares of Factorial Common Stock will be cancelled in exchange for a restricted stock unit award of PubCo under the PubCo Incentive Plan containing the same terms, conditions, vesting and other provisions as are currently applicable to such Factorial RSU, provided that each PubCo RSU will settle in a number of shares of PubCo Series A Common Stock equal to a number of shares of PubCo Series A Common Stock as set forth on an allocation schedule, rounded down to the nearest whole share; |

| ● | all convertible debt securities of Factorial will be converted into Factorial Common Stock pursuant to their respective terms; |

| ● | each issued and outstanding share of Factorial Preferred Stock will be converted into and become a number of shares of Factorial Common Stock in accordance with the terms of Section 5.1 of Factorial Certificate of Incorporation; and |

| ● | each issued and outstanding Factorial Warrant will be converted into and become a number of shares of Factorial Common Stock in accordance with the terms of the corresponding warrant agreement. |

For more information about the Business Combination, please see the section titled “Proposal No. 1 — The Business Combination Proposal — The Business Combination Agreement.” A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A.

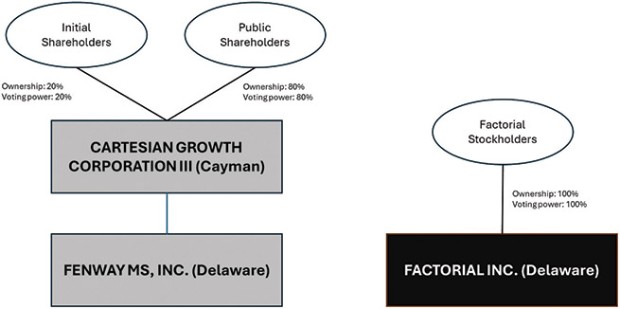

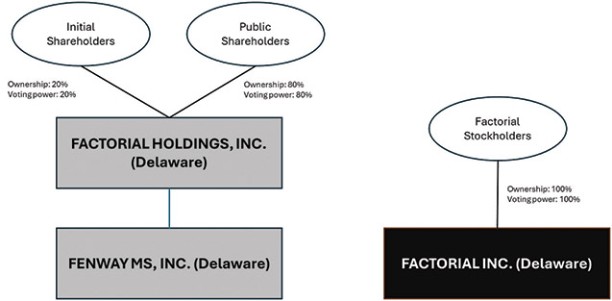

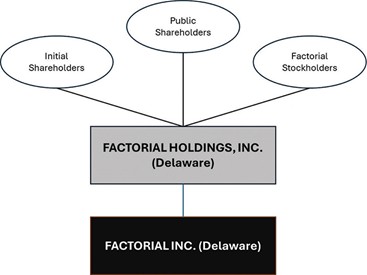

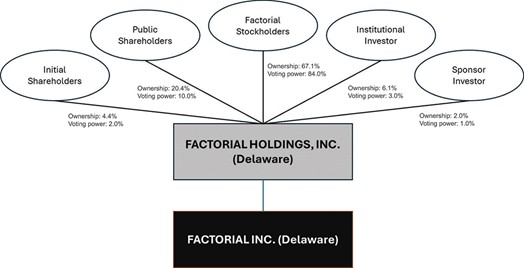

Structure Diagrams

The following diagrams illustrate in simplified terms the current structure of CGC and Factorial, the Business Combination, and the expected structure of Factorial immediately following the Closing.

Simplified Pre-Combination Structure

The Domestication

The Merger

Simplified Post-Combination Structure (with PIPE Financing)

* Percentages in the chart above assume no redemptions.

Investor Stock Purchase Agreements

Concurrently with the execution of the Business Combination Agreement, on December 17, 2025, CGC entered into a Stock Purchase Agreement with an affiliate of the Sponsor and a Stock Purchase Agreement with a certain institutional investor. Pursuant to the Investor Stock Purchase Agreements, the Institutional Investor subscribed for 7,500,000 shares of PubCo Series A Common Stock at a subscription price of $10.00 per share, and the Sponsor Investor subscribed for 2,427,184 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) at a subscription price equal to the Redemption Price. In connection with the Investor Stock Purchase Agreements, the Sponsor also agreed to transfer 1,000,000 Founder Shares to the PIPE Investors (750,000 Founder Shares to the Institutional Investor and 250,000 Founder Shares to the Sponsor Investor), which constructive transfer may be effectuated through a forfeiture of such Founder Shares by the Sponsor and reissuance thereof by PubCo. As a result of such Founder Share transfers, the effective subscription prices are $9.09 per share and $9.34 per share for the Institutional Investor and the Sponsor Investor, respectively, assuming a Redemption Price of $10.30 per share and taking into account the transfer of an aggregate of 1,000,000 Founder Shares from the Sponsor. The obligations of each party to consummate the PIPE Financing are conditioned upon,

among other things: (i) the PubCo Series A Common Stock (including the PubCo Series A Common Stock issuable to the PIPE Investors pursuant to the Investor Stock Purchase Agreements) having been approved for listing on Nasdaq or the New York Stock Exchange subject only to official notice of issuance; (ii) all conditions precedent to the Closing shall have been satisfied or waived and the closing of the Business Combination shall be scheduled to occur substantially concurrently with the closing of the PIPE Financing; and (iii) the absence of specified adverse judgments, orders, laws, rules or regulations enjoining or otherwise prohibiting the consummation of the transactions contemplated by the Investor Stock Purchase Agreements. The obligations of CGC to consummate the PIPE Financing are further subject to additional conditions, including, among other things: (i) material truth and accuracy of the representations and warranties of the PIPE Investors, subject to customary bringdown standards; and (ii) material compliance by the PIPE Investors with their covenants, agreements and conditions under the Investor Stock Purchase Agreements. The obligations of the PIPE Investors to consummate the PIPE Financing are further subject to additional conditions, including, among other things: (i) the material truth and accuracy of the representations and warranties of CGC in the Investor Stock Purchase Agreements, subject to customary bringdown standards; and (ii) material compliance by CGC with its covenants, agreements and conditions under the Investor Stock Purchase Agreements. For more information, see “Proposal No. 1 — The Business Combination Proposal — Ancillary Agreements — Investor Stock Purchase Agreements.” See also “— Sources and Uses of Proceeds.”

Non-Redemption Agreement

CGC may enter into non-redemption agreements with certain existing shareholders, or potential shareholders, including the PIPE Investors, pursuant to which, among other things, the Non-Redeeming Shareholders will irrevocably and unconditionally agree, for the benefit of CGC, that neither they nor their controlled affiliates will exercise any redemption rights under the CGC Articles with respect to certain CGC Class A Shares held by such Non-Redeeming Shareholders at any meeting of the CGC Shareholders. Each of the Non-Redeeming Shareholders will also agree (i) not to transfer directly or indirectly the NRA Shares held by it until the earlier of (x) the Closing Date, (y) the termination of the Business Combination Agreement in accordance with its terms and (z) the termination of the Non-Redemption Agreement in accordance with its terms; and (ii) to vote its NRA Shares in favor of the Business Combination Agreement, the Domestication and Merger and each other proposal brought by the CGC in connection with the Business Combination and in favor of any proposal brought by CGC to adjourn or postpone the EGM (provided, that, in the case of the Sponsor or any of its affiliates, such persons will tender an “abstain” vote with respect to such matters in compliance with the requirements of Rule 14e-5 under the Exchange Act). The Non-Redemption Agreements will not provide for any monetary consideration to be paid by CGC or Factorial to the Non-Redeeming Shareholders in connection with such agreements; however, a PIPE Investor’s acquisition of shares pursuant to a Non-Redemption Agreement will reduce, on a share for share basis, that PIPE Investor’s purchase obligation under its respective Investor Stock Purchase Agreement. Founder Shares deliverable to a PIPE Investor from Sponsor under an Investor Stock Purchase Agreement will continue to be delivered to such PIPE Investor in the same amounts regardless of whether a PIPE Investor enters into a Non-Redemption Agreement as contemplated by its Investor Stock Purchase Agreement. In the event the CGC Insiders or their affiliates were to purchase Public Shares from Public Shareholders in connection with such Non-Redemption Agreements, such purchases would be structured in compliance with the requirements of Rule 14e-5 under the Exchange Act including, in pertinent part, through adherence to the following:

| ● | if the CGC Insiders or their affiliates were to purchase Public Shares from Public Shareholders, they would do so at a price no higher than the Redemption Price; |

| ● | if the CGC Insiders or their affiliates were to purchase Public Shares from Public Shareholders, such shares would not be voted in favor of approving the Business Combination; |

| ● | the CGC Insiders and their affiliates would not possess any redemption rights with respect to our Public Shares or, if they do acquire and possess redemption rights, they would waive such rights; and |

| ● | we would disclose in a Form 8-K, before the EGM to approve the Business Combination, the following material items: |

| ● | the amount of our Public Shares purchased outside of the redemption offer by the CGC Insiders or their affiliates, along with the purchase price; |

| ● | the purpose of the purchases by the CGC Insiders or their affiliates; |

| ● | the impact, if any, of the purchases by the CGC Insiders or their affiliates on the likelihood that the Business Combination will be approved; |

| ● | the identities of our security holders who sold to the CGC Insiders or their affiliates (if not purchased on the open market) or the nature of our security holders (e.g., 5% security holders) who sold to the CGC Insiders or their affiliates; and |

| ● | the number of our Public Shares for which we have received redemption requests pursuant to our redemption offer. |

For more information, see “Proposal No. 1 — The Business Combination Proposal — Ancillary Agreements — Non-Redemption Agreement.”

Additionally, as discussed elsewhere in this proxy statement/prospectus, in connection with CGC’s IPO, the Sponsor, DirectorCo, and CGC Insiders entered into the Insider Letter with CGC, pursuant to which they agreed to waive their redemption rights with respect to their Founder Shares and Public Shares in connection with the completion of an initial business combination. Such redemption rights waiver was provided at the time of the IPO without any separate consideration paid. Additionally, pursuant to the Sponsor Support Agreement, the Sponsor, DirectorCo, and each of CGC’s independent directors and advisor who hold Founder Shares agreed not to redeem any CGC Ordinary Shares held by them in connection with the Business Combination. Such redemption rights waiver was provided without any separate consideration paid in connection with providing such waiver.

Transfer Restrictions

Pursuant to the proposed PubCo Bylaws, all Factorial Stockholders who are holders of Lock-up Shares will be subject to restrictions on transfer until, (i) with respect to 25% of the Lock-Up Shares, on the date 180 days after the Closing Date, (ii) with respect to 25% of the Lock-Up Shares, on the date 270 days after the Closing Date and (iii) with respect to 50% of the Lock-Up Shares, on the first anniversary of the Closing Date; provided, however, that, on the dates on which certain trading price conditions are satisfied, such transfer restrictions will terminate with respect to one-third of the Lock-Up Shares, with such Early Release Lock-Up Shares allocated first among the Lock-Up Shares with the earliest Lock-Up Termination Date that has not yet occurred and successively to each remaining tranche of Lock-Up Shares in chronological order. The foregoing transfer restrictions will not apply to a specified number of shares (such number to be agreed upon prior to Closing) held by each such holder and such specified shares are not Lock-up Shares. For more information, see “Proposal No. 1 — The Business Combination Proposal — Ancillary Agreements — Lock-Up Provisions of PubCo Bylaws.”

An aggregate of approximately 121,936,243 Lock-Up Shares are anticipated to be subject to such transfer restrictions (which includes 25,723,433 shares issuable upon exercise of PubCo Options and PubCo RSUs), representing approximately 92% of the total issued and outstanding shares of PubCo Series A Common Stock following the Business Combination (and shares issuable upon exercise of PubCo Options and PubCo RSUs), assuming the Maximum Redemptions Scenario, and that an aggregate of approximately $100 million of PIPE Investments are funded at the Closing (inclusive of the proceeds from the trust account resulting from NRA Shares acquired by PIPE Investors to satisfy their obligations under the applicable Investor Stock Purchase Agreement).

Set forth below is a tabular presentation of the post-closing lock-ups, including the number of shares to be issued to the Factorial Stockholders and the Sponsor that will not be subject to such transfer restrictions:

| | Lock-Up Shares | | Lock-Up Shares | | Lock-Up Shares | ||

Shares Not | subject to | subject to | subject to | |||||

Subject to | 180-day | 270-day | one-year | |||||

Category of Stockholder | Lock-Up | Lock-Up | Lock-Up | Lock-Up | ||||

Factorial Stockholders | 274,500 | 22,578,578 | 22,578,578 | 45,157,155 | ||||

Sponsor and DirectorCo | 1,500 | 1,474,625 | 1,474,625 | 2,949,250 | ||||

Total | 276,000 | 24,053,203 | 24,053,203 | 48,106,405 |

For more information, see Proposal No. 1 — The Business Combination Proposal — Ancillary Agreements — Lock-Up Provisions of PubCo Bylaws.”

Sources and Uses of Proceeds

The following tables summarize the anticipated sources and uses of funds in the Business Combination, in various redemption scenarios. Such tables are for illustrative purposes only. Where actual amounts are not known or knowable, the figures below represent good faith estimates of such amounts.

Sources and Uses of Proceeds (No Redemptions Scenario) (in millions)

Sources | | | Uses | | ||||

Implied Factorial Rollover Equity Value(1) | $ | 1,100.0 |

| Implied Factorial Rollover Equity Value | $ | 1,100.0 | ||

Implied Sponsor Equity |

| 60.8 |

| Implied Sponsor Equity |

| 60.8 | ||

Cash in Trust(2) |

| 284.3 |

| Cash to Balance Sheet |

| 388.6 | ||

Pro Forma Existing Cash Balances, as of December 31, 2025(3) |

| 33.8 |

| Estimated Unpaid Transaction Expenses, as of December 31, 2025 |

| 29.5 | ||

Cash Proceeds from the PIPE Financing |

| 100.0 |

| |

| | ||

Total Sources | $ | 1,578.9 |

| Total Uses | $ | 1,578.9 |

| (1) | Based upon an assumed Redemption Price of $10.30 per share. |

| (2) | Reflects the amount in the Trust Account at an assumed Redemption Price of $10.30 per share, with no cash payouts for Redemptions. |

| (3) | Reflects the pro forma combined cash and cash equivalents balance as of December 31, 2025 excluding the cash received from the Trust Account, the cash proceeds received from the PIPE financing, and the cash payouts of estimated transaction costs. |

Sources and Uses of Proceeds (25% Redemptions Scenario) (in millions)

Sources | | | Uses | |

| |||

Implied Factorial Rollover Equity Value(1) |

| $ | 1,100.0 |

| Implied Factorial Rollover Equity Value |

| $ | 1,100.0 |

Implied Sponsor Equity |

| 60.8 |

| Implied Sponsor Equity |

| 60.8 | ||

Cash in Trust(2) |

| 213.2 |

| Cash to Balance Sheet |

| 319.4 | ||

Pro Forma Existing Cash Balances, as of December 31, 2025(3) |

| 33.8 |

| Estimated Unpaid Transaction Expenses, as of December 31, 2025 |

| 27.6 | ||

Net Cash Proceeds from the PIPE Financing |

| 100.0 |

| |

| |||

Total Sources |

| $ | 1,507.8 |

| Total Uses |

| $ | 1,507.8 |

| (1) | Based upon an assumed Redemption Price of $10.30 per share. |

| (2) | Reflects the amount in the Trust Account at an assumed Redemption Price of $10.30 per share, with $71.1 million of cash payouts for Redemptions of 6,900,000 of CGC Class A Ordinary Shares. |

| (3) | Reflects the pro forma combined cash and cash equivalents balance as of December 31, 2025 excluding the cash received from the Trust Account, the cash proceeds received from the PIPE financing, and the cash payouts of estimated transaction costs. |

Sources and Uses of Proceeds (50% Redemptions Scenario) (in millions)

Sources | | | Uses | |

| |||

Implied Factorial Rollover Equity Value(1) |

| $ | 1,100.0 |

| Implied Factorial Rollover Equity Value |

| $ | 1,100.0 |

Implied Sponsor Equity |

| 60.8 |

| Implied Sponsor Equity |

| 60.8 | ||

Cash in Trust(2) |

| 142.1 |

| Cash to Balance Sheet |

| 250.4 | ||

Pro Forma Existing Cash Balances, as of December 31, 2025(3) |

| 33.8 |

| Estimated Unpaid Transaction Expenses, as of December 31, 2025 |

| 25.5 | ||

Net Cash Proceeds from the PIPE Financing |

| 100.0 |

| |

| |||

Total Sources |

| $ | 1,436.7 |

| Total Uses |

| $ | 1,436.7 |

| (1) | Based upon an assumed Redemption Price of $10.30 per share. |

| (2) | Reflects the amount in the Trust Account at an assumed Redemption Price of $10.30 per share, with $142.1 million of cash payouts for Redemptions of 13,800,000 of CGC Class A Ordinary Shares. |

| (3) | Reflects the pro forma combined cash and cash equivalents balance as of December 31, 2025 excluding the cash received from the Trust Account, the cash proceeds received from the PIPE financing, and the cash payouts of estimated transaction costs. |

Sources and Uses of Proceeds (75% Redemptions Scenario) (in millions)

Sources | | | Uses | |

| |||

Implied Factorial Rollover Equity Value(1) |

| $ | 1,100.0 |

| Implied Factorial Rollover Equity Value |

| $ | 1,100.0 |

Implied Sponsor Equity |

| 60.8 |

| Implied Sponsor Equity |

| 60.8 | ||

Cash in Trust(2) |

| 71.1 |

| Cash to Balance Sheet |

| 181.6 | ||

Pro Forma Existing Cash Balances, as of December 31, 2025(3) |

| 33.8 |

| Estimated Unpaid Transaction Expenses, as of December 31, 2025 |

| 23.3 | ||

Net Cash Proceeds from the PIPE Financing |

| 100.0 |

| |

| |||

Total Sources |

| $ | 1,365.7 |

| Total Uses |

| $ | 1,365.7 |

| (1) | Based upon an assumed Redemption Price of $10.30 per share. |

| (2) | Reflects the amount in the Trust Account at an assumed Redemption Price of $10.30 per share, with $213.2 million of cash payouts for Redemptions of 20,700,000 of CGC Class A Ordinary Shares. |

| (3) | Reflects the pro forma combined cash and cash equivalents balance as of December 31, 2025 excluding the cash received from the Trust Account, the cash proceeds received from the PIPE financing, and the cash payouts of estimated transaction costs. |

Sources and Uses of Proceeds (Maximum Redemptions Scenario) (in millions)

Sources | | | Uses | |

| |||

Implied Factorial Rollover Equity Value(1) |

| $ | 1,100.0 |

| Implied Factorial Rollover Equity Value |

| $ | 1,100.0 |

Implied Sponsor Equity |

| 60.8 |

| Implied Sponsor Equity |

| 60.8 | ||

Cash in Trust(2) |

| — |

| Cash to Balance Sheet |

| 114.8 | ||

Pro Forma Existing Cash Balances, as of December 31, 2025(3) |

| 33.8 |

| Estimated Unpaid Transaction Expenses, as of December 31, 2025 |

| 19.0 | ||

Cash Proceeds from the PIPE Financing |

| 100.0 |

| |

|

| ||

Total Sources |

| $ | 1,294.6 |

| Total Uses |

| $ | 1,294.6 |

| (1) | Based upon an assumed Redemption Price of $10.30 per share. |

| (2) | Reflects the amount in the Trust Account at an assumed Redemption Price of $10.30 per share, with $284.3 million of cash payouts for Redemptions of all 27,600,000 of CGC Class A Ordinary Shares. |

| (3) | Reflects the pro forma combined cash and cash equivalents balance as of December 31, 2025 excluding the cash received from the Trust Account, the cash proceeds received from the PIPE financing, and the cash payouts of estimated transaction costs. |

Conditions to Closing

Under the Business Combination Agreement, the obligations of the parties to consummate the Business Combination are subject to the satisfaction or waiver of certain closing conditions of the respective parties, including, without limitation: (i) the PubCo Series A Common Stock to be issued in connection with the Business Combination Agreement, including the Aggregate Merger Consideration and the PIPE Shares, having been approved for listing on Nasdaq, subject to official notice of issuance; (ii) this registration statement having been declared effective by the SEC under the Securities Act, no stop order suspending the effectiveness of this registration statement being in effect, and no proceedings for purposes of suspending the effectiveness of this registration statement having been initiated or threatened in writing by the SEC; and (iii) CGC Shareholder Approval and Factorial Stockholder Approval. The obligation of Factorial to consummate the Business Combination is subject to the fulfillment of other customary closing conditions, including, but not limited to, each PIPE Investor having funded the purchase price for such PIPE Investor’s Purchased Shares pursuant to such PIPE Investor’s Investor Stock Purchase Agreement into an escrow account and such PIPE Investor having otherwise fully performed its obligations thereunder and CGC having issued to the escrow agent such escrow release instructions as are required by the Investor Stock Purchase Agreements and/or such PIPE Investor having purchased any shares subject to any non-redemption agreement (in accordance with the provisions of such Investor Stock Purchase Agreement) to which such PIPE Investor is a party and otherwise fully performed its obligations under such non-redemption agreement. For more information, see “Proposal No. 1 — The Business Combination Proposal — The Business Combination Agreement — Conditions to Closing.”

Termination

The Business Combination Agreement may be terminated under certain customary and limited circumstances prior to the Closing, including, but not limited to, (i) by mutual written consent of CGC and Factorial, (ii) by CGC if the representations and warranties of Factorial are not true and correct or if Factorial fails to perform any pre-closing covenant or agreement set forth in the Business Combination Agreement such that certain conditions to closing cannot be satisfied and the breach or breaches of such representations or warranties or the failure to perform such covenant or agreement, as applicable, are not cured or cannot be cured within certain specified time periods, (iii) termination by Factorial if the representations and warranties of CGC or Merger Sub are not true and correct or if CGC or Merger Sub fails to perform any covenant or agreement set forth in the Business Combination Agreement such that certain conditions to closing cannot be satisfied and the breach or breaches of such representations or warranties or the failure to perform such covenant or agreement, as applicable, are not cured or cannot be cured within certain specified time periods, (iv) subject to certain limited exceptions, by either CGC or Factorial if the Business Combination is not consummated by November 12, 2026, (v) by either CGC or Factorial if the requisite CGC shareholder approvals are not obtained after the conclusion of the meeting at which CGC’s shareholders voted on such matters, (vi) by either CGC or Factorial, if any governmental entity has issued a final and non-appealable order prohibiting the Business Combination, and (vii) by CGC if Factorial’s stockholders do not deliver to CGC a

written consent approving the Business Combination within two business days following the date on which the Registration Statement / Proxy Statement is declared effective.

If the Business Combination Agreement is terminated, the agreement will become void, and there will be no liability under the Business Combination Agreement on the part of any party thereto, except for any liability on the part of any party for fraud or willful breach of the Business Combination Agreement. For more information, see “Proposal No. 1 — The Business Combination Proposal — The Business Combination Agreement — Termination; Effectiveness.”

Ancillary Agreements

In connection with the Business Combination, CGC and Factorial have entered into, or intend to enter into or otherwise adopt on or prior to the Closing Date, several agreements, including the Sponsor Support Agreement, Factorial Support Agreement, Investor Stock Purchase Agreements, Non-Redemption Agreements, the PubCo Bylaws, and A&R Registration Rights Agreement. For additional information about each of these agreements, see “Proposal No. 1 — The Business Combination Proposal — Ancillary Agreements.”

Ownership of PubCo after the Closing

The following tables illustrate estimated ownership levels in PubCo, immediately following the consummation of the Business Combination, based on varying levels of redemptions by Public Shareholders.

The following table excludes the dilutive effect of PubCo Options, PubCo RSUs and shares of PubCo Series A Common Stock that will initially be available for issuance under the PubCo Incentive Plan and ESPP, and assumes that no PIPE Investor elects to use Class A ordinary shares held by it (if any) to satisfy its obligations under its respective Investor Stock Purchase Agreement.

| Pro Forma Combined |

| |||||||||||||||||||

25% | | 50% | 75% | | Maximum |

| |||||||||||||||

No Redemptions | Redemptions | Redemptions | Redemptions | Redemptions |

| ||||||||||||||||

Scenario | Scenario | Scenario | Scenario | Scenario |

| ||||||||||||||||

| Shares | | % | Shares | | % |

| Shares | | % | Shares | | % |

| Shares | | % |

| |||

CGC Public Shareholders(1) |

| 27,600,000 |

| 21 | % | 20,700,000 | 16 | % | 13,800,000 |

| 11 | % | 6,900,000 | 6 | % | 0 |

| 0 | % | ||

Sponsor and DirectorCo(2) |

| 5,900,000 |

| 4 | % | 5,900,000 | 5 | % | 5,900,000 |

| 5 | % | 5,900,000 | 5 | % | 5,900,000 |

| 6 | % | ||

Factorial Stockholders(3) |

| 90,588,810 |

| 67 | % | 90,588,810 | 71 | % | 90,588,810 |

| 75 | % | 90,588,810 | 80 | % | 90,588,810 |

| 84 | % | ||

PIPE Institutional Investor(4) |

| 8,250,000 |

| 6 | % | 8,250,000 | 6 | % | 8,250,000 |

| 7 | % | 8,250,000 | 7 | % | 8,250,000 |

| 8 | % | ||

PIPE Sponsor Investor(5) | 2,677,184 | 2 | % | 2,677,184 | 2 | % | 2,677,184 | 2 | % | 2,677,184 | 2 | % | 2,677,184 | 2 | % | ||||||

Cantor Advisor Fee(6) | — | 0 | % | — | 0 | % | — | 0 | % | — | 0 | % | 121,359 | 0 | % | ||||||

Pro forma total shares of the PubCo Common Stock outstanding at Closing |

| 135,015,994 |

| 100 | % | 128,115,994 | 100 | % | 121,215,994 |

| 100 | % | 114,315,994 | 100 | % | 107,537,353 |

| 100 | % | ||

| (1) | Represents Public Shares held by CGC’s Public Shareholders under the no redemption, 25% redemption, 50% redemption, 75% redemption, and 100% redemption scenarios. |

| (2) | Amount includes 5,800,000 Founder Shares held by the Sponsor and 100,000 Founder Shares held by DirectorCo (in which, each of CGC’s independent directors hold an interest in 30,000 Founder Shares). |

| (3) | Includes (i) an aggregate of 3,289,809 shares of PubCo Series A Common Stock issued to holder of Factorial Common Stock from conversion of Factorial Common Stock based upon the Consideration Ratio; (ii) an aggregate of 15,776,088 shares of PubCo Series B Common Stock issued to the Factorial Founders from the exchange of shares of Factorial Common Stock based upon the Consideration Ratio; (iii) an aggregate of 68,457,804 shares of PubCo Series A Common Stock issued to holders of Factorial Preferred Stock from the exchange of shares of Factorial Preferred Stock; (iv) an aggregate of 2,692,202 shares of PubCo Series A Common Stock issued to holders of the Factorial Convertible Notes from conversion of the Factorial Convertible Notes along with accrued interest (assuming interest accrues from the date the proceeds were received under such notes, (August 2025, January 2026, or February 2026 through May 14, 2026)) into shares of Factorial Common Stock immediately before the Business Combination and the subsequent exchange into shares of PubCo Series A Common Stock; and (v) an aggregate of 372,907 shares of PubCo Series A Common Stock issued to holders of the Factorial Warrants from their cashless exercise of the warrants for shares of Factorial Preferred Stock and converted into shares of Factorial Common Stock immediately before the Business Combination and subsequent exchange for PubCo Series A Common Stock. |

| (4) | Amount includes (i) the Institutional Investors subscription for 7,500,000 shares of PubCo Series A Common Stock at a subscription price of $10.00 per share; plus (ii) the constructive transfer at the Closing of an aggregate of 750,000 shares of PubCo Series A Common Stock from the Sponsor to the Institutional Investor. The effective subscription price of the Institutional Investor is $9.09 per share, taking into account the foregoing transfer from the Sponsor. |

| (5) | Amount includes (i) the Sponsor Investors subscription for an estimated 2,427,184 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) at a subscription price equal to the Redemption Price; plus (ii) the constructive transfer at the Closing of an aggregate of 250,000 shares of PubCo Series A Common Stock from the Sponsor to the Sponsor Investor. The effective subscription price of the Sponsor Investor is $9.34 per share, assuming a Redemption Price of $10.30 per share and taking into account the foregoing transfer from the Sponsor. |

| (6) | Amount includes 121,359 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) issued to Cantor pursuant to the financial advisor engagement letter as outlined in the section entitled “Certain Engagements in Connection with the Business Combination” elsewhere in this prospectus. |

The shares of PubCo Common Stock issued to Factorial Stockholders set forth in the table above include shares of PubCo Series A Common Stock and PubCo Series B Common Stock. All of the shares of PubCo Series B Common Stock will be held by the Factorial Founders, both of whom will serve as executive officers and directors of PubCo. The rights of the holders of PubCo Series A Common Stock and PubCo Series B Common Stock will be identical, except with respect to voting and conversion rights. Each share of PubCo Series B Common Stock will be entitled to ten votes and will be convertible at any time into one share of PubCo Series A Common Stock. Each share of PubCo Series B Common Stock will be automatically converted into one fully paid and nonassessable share of PubCo Series A Common Stock upon the earliest of: (i) the date specified by affirmative vote of the holders of at least 662∕3% of the outstanding shares of PubCo Series B Common Stock, voting as a single series; (ii) the date that is nine months following the death or incapacity of both Factorial Founders; and (iii) the date that is the seven year anniversary of the Closing Date.

The following table shows possible sources of dilution and the extent of such dilution that non- redeeming Public Shareholders could experience in connection with the closing of the Business Combination. In an effort to illustrate the extent of such dilution, the table below assumes the exercise of all PubCo Warrants for cash, which will each be exercisable for one share of PubCo Series A Common Stock at a price of $11.50 per share, the exercise of all PubCo Options for cash, which will each be exercisable for one share of PubCo Series A Common Stock at a price of approximately $1.04 per share (based on the Estimated Consideration Ratio) and settlement of all PubCo RSUs. The table excludes shares of PubCo Series A Common Stock that will initially be available for issuance under the PubCo Incentive Plan and ESPP, as such shares will not be outstanding on the Closing Date. The table does not assume the consummation of any exchange of the PubCo Warrants for shares of PubCo Series A Common Stock, and assumes that no PIPE Investor elects to use Class A ordinary shares held by it (if any) to satisfy its obligations under its respective Investor Stock Purchase Agreement.

| Pro Forma Combined |

| |||||||||||||||||||

25% | | 50% | 75% | | Maximum |

| |||||||||||||||

No Redemptions | Redemptions | Redemptions | Redemptions | Redemptions |

| ||||||||||||||||

Scenario | Scenario | Scenario | Scenario | Scenario |

| ||||||||||||||||

| Shares | | % | Shares | | % |

| Shares | | % | Shares | | % |

| Shares | | % |

| |||

CGC Public Shareholders |

| 27,600,000 |

| 15 | % | 20,700,000 | 12 | % | 13,800,000 |

| 8 | % | 6,900,000 | 4 | % | — |

| 0 | % | ||

Sponsor and DirectorCo(1) |

| 5,900,000 |

| 3 | % | 5,900,000 | 3 | % | 5,900,000 |

| 4 | % | 5,900,000 | 4 | % | 5,900,000 |

| 4 | % | ||

Factorial Stockholders |

| 116,312,243 |

| 64 | % | 116,312,243 | 66 | % | 116,312,243 |

| 69 | % | 116,312,243 | 72 | % | 116,312,243 |

| 76 | % | ||

PIPE Institutional Investor(2) |

| 8,250,000 |

| 5 | % | 8,250,000 | 5 | % | 8,250,000 |

| 5 | % | 8,250,000 | 5 | % | 8,250,000 |

| 5 | % | ||

PIPE Sponsor Investor(3) |

| 2,677,184 |

| 1 | % | 2,677,184 | 2 | % | 2,677,184 |

| 2 | % | 2,677,184 | 2 | % | 2,677,184 |

| 2 | % | ||

Public Warrants | 13,800,000 | 8 | % | 13,800,000 | 8 | % | 13,800,000 | 8 | % | 13,800,000 | 9 | % | 13,800,000 | 9 | % | ||||||

Private Warrants(4) | 6,800,000 | 4 | % | 6,800,000 | 4 | % | 6,800,000 | 4 | % | 6,800,000 | 4 | % | 6,800,000 | 4 | % | ||||||

Cantor Advisory Fee(5) | — | 0 | % | — | 0 | % | — | 0 | % | — | 0 | % | 121,359 | 0 | % | ||||||

Pro forma total shares of the PubCo Common Stock outstanding at Closing | 181,339,427 | 100 | % | 174,439,427 | 100 | % | 167,539,427 | 100 | % | 160,639,427 | 100 | % | 153,860,786 | 100 | % | ||||||

| (1) | Amount includes 5,800,000 Founder Shares held by the Sponsor and 100,000 Founder Shares held by DirectorCo (in which, each of CGC’s independent directors and advisor hold an interest in 30,000 Founder Shares). |

| (2) | Amount includes (i) the Institutional Investor’s subscription for 7,500,000 shares of PubCo Series A Common Stock at a subscription price of $10.00 per share; plus (ii) the constructive transfer at the Closing of an aggregate of 750,000 shares of PubCo Series A Common Stock from the Sponsor to the Institutional Investor. The effective subscription price of the Institutional Investor is $9.09 per share, taking into account the foregoing transfer from the Sponsor. |

| (3) | Amount includes (i) the Sponsor Investor’s subscription for an estimated 2,427,184 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) at a subscription price equal to the Redemption Price; plus (ii) the constructive transfer at the Closing of an aggregate of 250,000 shares of PubCo Series A Common Stock from the Sponsor to the Sponsor Investor. The effective subscription price of the Sponsor Investor is $9.34 per share, assuming a Redemption Price of $10.30 per share and taking into account the transfer of an aggregate of 1,000,000 Founder Shares from the Sponsor. |

| (4) | Represents 4,400,000 CGC Private Warrants held by Sponsor and 2,400,000 CGC Private Warrants held by Cantor. |

| (5) | Amount includes 121,359 shares of PubCo Series A Common Stock (assuming a Redemption Price of $10.30 per share) issued to Cantor pursuant to the financial advisor engagement letter as outlined in the section entitled “Certain Engagements in Connection with the Business Combination” elsewhere in this prospectus. |

Share ownership presented in the two tables above is only presented for illustrative purposes and does not necessarily reflect what PubCo’s share ownership will be after the Closing. CGC and Factorial cannot predict how many of the Public Shareholders will exercise their right to have their Public Shares redeemed for cash. As a result, the redemption amount and the number of Public Shares redeemed in connection with the Business Combination may differ from the amounts presented above, and therefore the ownership percentages of Public Shareholders may also differ if the actual redemptions are different from these assumptions. The Public Shareholders that do not elect to redeem their Public Shares will experience immediate dilution as a result of the Business Combination. The Public Shareholders currently represent approximately 80% of the total issued and outstanding CGC Ordinary Shares. As noted in the above table, even if no Public Shareholders redeem their Public Shares in the Business Combination, the Public Shareholders’ ownership is expected to decrease from approximately 80% of the total issued and outstanding CGC Ordinary

Shares prior to the Business Combination to approximately 15% of the total issued and outstanding PubCo Common Stock at the Closing. As redemptions increase, the overall percentage ownership held by the Sponsor and other CGC Insiders, Factorial Stockholders and the PIPE Investors will increase as compared to the overall percentage ownership held by Public Shareholders, thereby increasing dilution to Public Shareholders. For more information about the consideration to be received in the Business Combination, these scenarios, and the underlying assumptions, see “Unaudited Pro Forma Combined Financial Information.” See also “Risk Factors — Risks Related to CGC and the Business Combination — The CGC Shareholders will experience immediate dilution as a consequence of the issuance of PubCo Series A Common Stock as consideration in the Business Combination. Having a minority share position may reduce the influence that CGC’s current shareholders have on the management of PubCo.”

Interests of the Sponsor, and CGC’s Directors and Officers in the Business Combination

In considering the recommendation of the CGC Board to vote in favor of approval of the Business Combination Proposal, the Domestication Proposal, the BCA Stock Issuance Proposal, the PIPE Stock Issuance Proposal, the Organizational Documents Proposal, the Incentive Plan Proposal, the ESPP Proposal, Director Election Proposal and Adjournment Proposal, shareholders should keep in mind that CGC’s Sponsor, CGC’s directors and executive officers, and entities affiliated with them, have interests in such proposals that are different from, or in addition to, the interests of unaffiliated CGC Shareholders. See “Proposal No. 1 — The Business Combination Proposal — Interests of the Sponsor, and CGC’s Directors and Officers in the Business Combination.”

The existence of financial and personal interests of one or more of CGC’s directors may result in a conflict of interest on the part of such director(s) between what he or they may believe is in the best interests of CGC and its shareholders and what he or they may believe is best for himself or themselves. In addition, the Sponsor and CGC’s officers have interests in the Business Combination that may conflict with your interests as a shareholder.

The financial interests of the Sponsor, as well as CGC’s directors and officers may have influenced their motivation in identifying and selecting Factorial as a business combination target, completing an initial business combination with Factorial and influencing the operation of the business following the Closing. In considering the recommendation of the CGC Board to vote for the proposals, CGC’s shareholders should consider these interests.

Further, unaffiliated CGC Shareholders should keep in mind that Factorial officers, directors and entities affiliated with them, have interests in such proposals that are different from, or in addition to, those of unaffiliated CGC Shareholders. See “Proposal No. 1 — The Business Combination Proposal — Interests of the Sponsor, and CGC’s Directors and Officers in the Business Combination” and “Certain Relationships and Related Persons Transactions” for more information related to certain transactions and arrangements between Factorial and the Factorial Directors and Officers.

Compensation to be Received by the Sponsor and CGC’s Officers and Directors in Connection with the Business Combination and PIPE Investment

Set forth below is a summary of the amount of compensation and securities received or to be received by the Sponsor and CGC’s officers and directors in connection with the Business Combination and PIPE Investment.

| Securities to be Received | | Other Compensation | |

|---|---|---|---|---|

The Sponsor and DirectorCo | (i) 5,900,000 shares of PubCo Series A Common Stock upon the exchange of 6,900,000 Founder Shares, which were initially purchased prior to the IPO for approximately $0.004 per share, and transfer to the PIPE Investors of an aggregate amount of 1,000,000 shares of PubCo pursuant to the Investor Stock Purchase Agreements, (ii) 4,400,000 PubCo Private Warrants issued upon the exchange of 4,400,000 CGC Private Warrants, which were initially purchased in a private placement that closed concurrently with the IPO for $1.00 per warrant, and (iii) under the Sponsor Stock Purchase Agreement, an affiliate of the Sponsor will be issued an estimated 2,677,184 shares of PubCo Series A Common Stock, assuming a Redemption Price of $10.30 for the Public Shares estimated using an assumed Closing Date of May 14, 2026. | Reimbursement for loans and advances to CGC; no such amounts are outstanding as of the date of this proxy statement/ prospectus. $10,000 per month through the Closing to an affiliate of the Sponsor for office space, utilities, secretarial and administrative support services provided to members of the CGC management team. As of December 31, 2025, CGC incurred $80,000 in fees for these services, of which $50,000 have been paid as of December 31, 2025. Continued indemnification and the continuation of directors’ and officer’s liability insurance after the Business Combination. | ||

Peter Yu | See “Sponsor and DirectorCo” above. Mr. Yu may be deemed to control the Sponsor and DirectorCo. | See “Sponsor and DirectorCo” above. Mr. Yu may be deemed to control the Sponsor and DirectorCo. Reimbursement for out-of-pocket expenses incurred related to identifying, negotiating, investigating and completing the Business Combination; no such amounts are outstanding as of the date of this proxy statement/prospectus. | ||

CGC Independent Directors (through DirectorCo) | Each of our independent directors, Ali Bouzarif, Kevin Gold and Sanford Litvack, has received for their services as directors an indirect interest in 30,000 founder shares through membership interests in DirectorCo. | Reimbursement for loans and advances to CGC; no such amounts are outstanding as of the date of this proxy statement/ prospectus. Reimbursement for out-of-pocket expenses incurred related to identifying, negotiating, investigating and completing the Business Combination; no such amounts are outstanding as of the date of this proxy statement/prospectus. Continued indemnification and the continuation of directors’ and officer’s liability insurance after the Business Combination. |

The securities to be issued to the Sponsor and CGC’s officers and directors may result in a material dilution of the equity interests of non-redeeming Public Shareholders. CGC’s independent directors are not members of the Sponsor. None of the funds in the Trust Account will be used to compensate our officers or directors. Except for administrative services fees paid or to be paid to the Sponsor, and our independent directors’ indirect interest in 90,000 CGC Class B Shares held by DirectorCo on their behalf, no compensation of any kind, including finder’s and consulting fees, have been paid or will be paid to the Sponsor, officers and directors, or any of their respective affiliates, by CGC for services rendered prior to or in connection with the completion of the Business Combination.

However, as detailed above, these individuals will be reimbursed for any out-of-pocket expenses incurred in connection with activities on our behalf such as identifying potential target businesses and performing due diligence on suitable business combinations, as discussed above. The reimbursement of expenses and advances to the Sponsor and CGC’s officers and directors may result in a material dilution of the equity interests of non-redeeming Public Shareholders.

Potential Purchases of Public Shares

Other than the Non-Redemption Agreements, if any (which will not provide any consideration from CGC or Factorial to the Non-Redeeming Shareholders in connection with their Non-Redemption Agreements), the Sponsor and CGC’s officers and directors do not have any plans at this time to purchase Public Shares from Public Shareholders or to take any other actions to incentivize non-redemption. However, at any time prior to the EGM, during a period when they are not then aware of any material nonpublic information regarding CGC or its securities, the Sponsor and CGC’s officers and directors or their affiliates may purchase Public Shares in privately negotiated transactions or in the open market, although they are under no obligation to do so. There is no limit on the number of Public Shares that such persons may purchase in such transactions, subject to compliance with applicable law and Nasdaq rules. However, other than as expressly stated herein (including in respect of the Investor Stock Purchase Agreements), they have no current commitments, plans or intentions to engage in such transactions and have not formulated any terms or conditions for any such transactions. None of the funds in the Trust Account will be used to purchase Public Shares in such transactions. Such purchases may include a contractual acknowledgment that such shareholder, although still the record holder of CGC’s shares, is no longer the beneficial owner thereof and therefore agrees not to exercise its redemption rights.

In the event that the Sponsor and CGC’s officers and directors or their affiliates purchase shares in privately negotiated transactions from Public Shareholders who have already elected to exercise their redemption rights, such selling shareholders would be required to revoke their prior elections to redeem their shares. The purpose of such transaction could be to increase the likelihood of obtaining shareholder approval of the Business Combination, subject to the limitations on voting contained in applicable SEC interpretations of Rule 14e-5 under the Exchange Act or to increase the proceeds from the Trust Account released to PubCo, where it appears that such requirement would otherwise not be met. CGC expects any such purchases will be reported pursuant to Section 13 and Section 16 of the Exchange Act to the extent such purchasers are subject to such reporting requirements.

In addition, if such purchases are made, the public “float” of CGC Class A Shares and the number of beneficial holders of CGC Class A Shares may be reduced, possibly making it difficult to obtain or maintain the quotation, listing or trading of CGC’s securities on Nasdaq.

In the event the Sponsor and CGC’s officers and directors or their affiliates were to purchase Public Shares from Public Shareholders, such purchases would be structured in compliance with the requirements of Rule 14e-5 under the Exchange Act. To the extent that the Sponsor and CGC’s officers and directors or their affiliates purchase Public Shares in compliance with the requirements of Rule 14e-5 under the Exchange Act, such shares would not be voted in favor of approving the Business Combination. See “Business Combination — Potential Purchases of Public Shares” for more information.

CGC Board’s Reasons for the Approval of the Business Combination

Before reaching their decisions that the Business Combination Agreement, each ancillary agreement, and the Business Combination are fair, advisable and in the best interests of CGC and its shareholders, the CGC Board each consulted with the CGC management team and their respective legal counsel. The CGC Board considered a variety of factors in connection with their evaluation of the Business Combination. In light of the complexity of those factors, the CGC Board, as a whole, did not consider it practicable to, nor did it attempt to, quantify or otherwise assign relative weights to the specific factors they took into account in reaching their decision. Different individual members of the CGC Board may have given different weight to different factors in their evaluation of the Business Combination.

The CGC Board determined that the Business Combination presents an attractive business opportunity in light of a variety of factors, including but not limited to Factorial’s compelling data and rigorous science, its market opportunity, intellectual property protections, experienced management team, and the existence and size of the PIPE Investment. The CGC Board also considered the potential detriments of the Business Combination to CGC, including Factorial’s limited operating history, regulatory risks, the uncertainty of the potential benefits of the Business Combination being achieved, macroeconomic risks, the absence of possible

structural protections for minority shareholders, and the risks and costs to CGC if the Business Combination is not achieved, including the risk that it may result in CGC being unable to complete a business combination and force CGC to liquidate.

For more information about the CGC Board’s reasons for the approval of the Business Combination, see “Proposal No. 1 — The Business Combination Proposal — The CGC Board’s Reasons for the Approval of the Business Combination.”

The Extraordinary General Meeting

The following is a summary of the process and procedures for registering for and attending the EGM, and voting and redeeming your CGC Ordinary Shares in connection with the EGM. For more information, see the section entitled “Extraordinary General Meeting.”

Date, Time and Place

The EGM will be held at [·] a.m., Eastern Time, on [·], 2026. The EGM will be a virtual meeting conducted via live webcast at [·]. For the purposes of Cayman Islands law and the CGC Articles, the physical location of the EGM will be the offices of Greenberg Traurig, LLP, CGC’s legal counsel, at One Vanderbilt Avenue, New York, NY 10017.

Proposals to be Submitted at the EGM

At the EGM, CGC is asking holders of Ordinary Shares to consider and vote upon:

| ● | the Business Combination Proposal; |

| ● | the Domestication Proposal; |

| ● | the BCA Stock Issuance Proposal; |

| ● | the PIPE Stock Issuance Proposal; |

| ● | the Organizational Documents Proposal; |

| ● | the Advisory Organizational Documents Proposals; |

| ● | the Incentive Plan Proposal; |

| ● | the ESPP Proposal; |

| ● | the Director Election Proposal; and |

| ● | the Adjournment Proposal (if presented). |

Registering for the EGM

Any shareholder wishing to attend the meeting should register for the meeting by [·], Eastern Time, on [·], 2026 by contacting Morrow Sodali.

Voting Power; Abstentions and Broker Non-Votes; Record Date

With respect to each proposal in this proxy statement/prospectus, you may vote “FOR,” “AGAINST” or “ABSTAIN.”

If a shareholder fails to return a proxy card and does not attend the EGM in person, then the shareholder’s shares will not be counted for purposes of determining whether a quorum is present at the EGM. If a valid quorum is established, any such failure to vote will have no effect on the outcome of any proposal in this proxy statement/prospectus.

Abstentions will be counted in connection with the determination of whether a valid quorum is established but will have no effect on any of the proposals.

CGC has fixed the close of business on May 1, 2026, as the “Record Date” for determining CGC Shareholders entitled to notice of and to attend and vote at the EGM. As of the close of business on the Record Date, there were 34,500,000 CGC Ordinary Shares outstanding and entitled to vote. Each share is entitled to one vote at the EGM, provided that only the CGC Class B Shares are entitled to vote on the Domestication Proposal.

As of the Record Date, the Sponsor and DirectorCo held of record and were entitled to vote an aggregate of 6,800,000 and 100,000 CGC Ordinary Shares, respectively. The CGC Ordinary Shares held by the Sponsor and DirectorCo currently constitute approximately 19.71% and 0.29%, respectively, of the outstanding CGC Ordinary Shares. Pursuant to the Sponsor Support Agreement, the Sponsor has agreed to vote any CGC Ordinary Shares held by it as of the Record Date in favor of the Business Combination, including voting in favor of each of the Condition Precedent Proposals. No consideration has been or will be paid by CGC or Factorial to the Sponsor in connection with such agreements. To the extent that Sponsor or its affiliates purchase Public Shares in compliance with the requirements of Rule 14e-5 under the Exchange Act, such shares would not be voted in favor of approving the Business Combination.

Quorum and Vote of CGC Shareholders

A quorum of CGC’s shareholders is necessary to hold a valid meeting. The presence, in person or by proxy, of one or more shareholders holding a majority of the issued and outstanding CGC Ordinary Shares entitled to vote at such meeting constitutes a quorum at the EGM. The following votes are required to approve each Proposal:

| ● | Business Combination Proposal: Approval of the Business Combination Proposal requires an ordinary resolution, being the affirmative vote of holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | Domestication Proposal: Approval of the Domestication Proposal requires a special resolution, being the affirmative vote of at least two-thirds of the holders of issued and outstanding CGC Class B Shares who, being present in person or represented by proxy and entitled to vote thereon at the EGM, vote at the EGM. The holders of the CGC Class A Shares will have no right to vote on the Domestication Proposal, in accordance with Article 47.2 of the CGC Articles. |

| ● | BCA Stock Issuance Proposal: Approval of the BCA Stock Issuance Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | PIPE Stock Issuance Proposal: Approval of the PIPE Stock Issuance Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | Organizational Documents Proposal: Approval of the Organizational Documents Proposal requires a special resolution, being the affirmative vote of the holders of a majority of at least two-thirds of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | Advisory Organizational Documents Proposals: Approval of each Advisory Organizational Documents Proposal requires an ordinary resolution on a non-binding and advisory only basis, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. The shareholder votes regarding these proposals are advisory in nature, and are not binding on CGC, the CGC Board, Factorial or PubCo Board. |

| ● | Incentive Plan Proposal: Approval of the Incentive Plan Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | ESPP Proposal: Approval of the ESPP Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | Director Election Proposal: Approval of the Director Election Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

| ● | Adjournment Proposal: Approval of the Adjournment Proposal requires an ordinary resolution, being the affirmative vote of the holders of a majority of the issued and outstanding CGC Ordinary Shares, who, being present in person or by proxy and entitled to vote thereon at the EGM, vote at the EGM. |

Redemption Rights

Pursuant to the CGC Articles, a Public Shareholder (other than the Sponsor and the CGC Insiders) may request that CGC redeem all or a portion of his, her or its Public Shares for cash if the Business Combination is consummated. Holders of Public Shares who wish to exercise their redemption rights must, prior to [·], Eastern Time, on [·], 2026 (which date is two business days before the scheduled vote at the EGM), (A) submit a written request to the Transfer Agent, which request includes the legal name, phone number and address of the beneficial owner of the Public Shares for which redemption is requested, that CGC redeem all or a portion of their Public Shares for cash and (B) deliver their Public Shares to the Transfer Agent physically or electronically using the DTC’s DWAC (Deposit and Withdrawal at Custodian) system. Any holder of Public Shares (other than the Sponsor and the CGC Insiders) will be entitled to demand that such holder’s Public Shares be redeemed for a full pro rata portion of the amount then in the Trust Account (including interest earned on the Trust Account not previously released to CGC to pay its taxes, net of taxes payable) (which, for illustrative purposes, was approximately $285,868,994, or $10.36 per Public Share, as of April 29, 2026).

Holders of CGC Units must elect to separate their CGC Units into the underlying Public Shares and Public Warrants prior to exercising their redemption rights with respect to the Public Shares. If holders of CGC Units hold their CGC Units in an account at a brokerage firm or bank, such holders must notify their broker or bank that they elect to separate their CGC Units into the underlying Public Shares and Public Warrants, or if a holder holds CGC Units registered in its own name, the holder must contact Continental Stock Transfer & Trust Company, CGC’s transfer agent, directly and instruct it to do so. The redemption rights include the requirement that a holder must identify itself to CGC in order to validly exercise its redemption rights.

Holders of CGC Units do not need to separate their CGC Units into the underlying Public Shares and Public Warrants prior to voting such underlying Public Shares at the EGM if they do not wish to exercise redemption rights.

Prior to exercising redemption rights, Public Shareholders should verify the market price of the CGC Class A Shares as they may receive higher proceeds from the sale of their Public Shares in the public market than from exercising their redemption rights if the market price per share is higher than the Redemption Price. CGC cannot assure shareholders that they will be able to sell their Public Shares in the open market, even if the market price per share is higher than the Redemption Price stated above, as there may not be sufficient liquidity in the CGC Class A Shares when Public Shareholders wish to sell their shares.

Any request for redemption, once made by a holder of Public Shares, may be withdrawn at any time up to the deadline to submitting redemption requests and thereafter, with CGC’s consent, until the Closing. If a holder delivers his, her or its Public Shares for redemption to the Transfer Agent and later decides to withdraw such request prior to the deadline for submitting redemption requests, the holder may request that the Transfer Agent return the shares (physically or electronically).

Any written demand of redemption rights must be received by the Transfer Agent prior to the redemption deadline. No demand for redemption will be honored unless the holder’s Public Shares have been delivered (either physically or electronically) to the Transfer Agent prior to the deadline for submitting redemption requests.

Notwithstanding the foregoing, a holder of Public Shares, together with any affiliate or any other person with whom he, she or it is acting in concert or as a partnership, syndicate or other group, will be restricted from seeking redemption with respect to more than 20% of the issued and outstanding Public Shares. Accordingly, all Public Shares in excess of 20% held by a shareholder, together with any affiliate of such holder or any other person with whom such holder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will not be redeemed.

See the section entitled “The Extraordinary General Meeting — Redemption Rights” for a detailed description of the procedures to be followed if you wish to redeem your Public Shares for cash. See also “Questions and Answers about the Business Combination — Do I have redemption rights?, — Will my ability to exercise redemption rights be impacted by how I vote on the Business Combination Proposal?, — How do I exercise my redemption rights?” for additional information on the exercise of redemption rights.

As set forth in more detail elsewhere in this proxy statement/prospectus, the Public Shareholders that do not elect to redeem their Public Shares will experience immediate dilution as a result of the Business Combination. The Public Shareholders currently own approximately 80% of the issued and outstanding CGC Ordinary Shares. Even if no Public Shareholders redeem their Public Shares in the Business Combination, and assuming no exercises of CGC Public Warrants, CGC Private Warrants or any options, the Public Shareholders’ ownership will decrease from approximately 80% of the CGC Ordinary Shares prior to the Business Combination to owning approximately 15% of the total outstanding PubCo Common Stock at the Closing. As redemptions increase, the overall percentage ownership held by the Sponsor and other CGC Insiders, Factorial Stockholders and the PIPE Investors will increase as compared to the overall percentage ownership and voting percentage held by Public Shareholders, thereby increasing dilution to Public Shareholders. See “Risk Factors — Risks Related to CGC and the Business Combination — The CGC Shareholders will experience immediate dilution as a consequence of the issuance of PubCo Series A Common Stock as consideration in the Business Combination. Having a minority share position may reduce the influence that CGC’s current shareholders have on the management of PubCo.”

Appraisal Rights and Dissenters’ Rights

CGC’s shareholders do not have appraisal rights in connection with the Business Combination or the Domestication under the DGCL. CGC’s shareholders do not have dissenters’ rights in connection with the Business Combination or the Domestication under Cayman Islands law.

Proxy Solicitation

Proxies may be solicited by mail, telephone, on the internet, or in person. CGC has engaged Morrow Sodali to assist in the solicitation of proxies. CGC has agreed to pay Morrow Sodali a fee of $20,000, plus disbursements.

If a shareholder grants a proxy, it may still vote its shares if it revokes its proxy before the EGM. A shareholder also may change its vote by submitting a later-dated proxy as described in the section entitled “The Extraordinary General Meeting — Proxy Solicitation.”

Regulatory Approvals

Each of CGC and Factorial has agreed to use their respective reasonable best efforts, and to cooperate fully with the other party, to take all actions necessary or desirable to complete the Business Combination, including its reasonable best efforts to (i) obtain all necessary actions, nonactions, waivers, consents, approvals and other authorizations from all applicable authorities or other third parties prior to the Merger Effective Time, (ii) avoid an action by any governmental authority and (iii) execute and deliver any additional instruments necessary to consummate the Business Combination. On January 16, 2026, the parties received early termination of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the “HSR Act”), and the rules and regulations promulgated thereunder. The regulatory approvals to which completion of the Business Combination are subject are described in more detail in the section of this proxy statement/prospectus entitled “The Business Combination — Regulatory Approvals.”

Stock Exchange Listing

Pursuant to the Business Combination Agreement, CGC agreed to use its reasonable best efforts to cause its initial listing application with Nasdaq in connection with the Business Combination to have been approved, all applicable initial and continuing listing requirements of Nasdaq to be satisfied, and the PubCo Series A Common Stock to be issued as Aggregate Merger Consideration or in connection with the PIPE Investment to be approved for listing on Nasdaq, subject to official notice of issuance, in each case, as promptly as reasonably practicable after the date of the Business Combination Agreement and in any event prior to the Merger Effective Time. Following the Merger Effective Time, the CGC Units will automatically separate and will cease trading on Nasdaq, and no CGC Units will be in existence and the CGC Units will not be listed on Nasdaq following the Closing. Holders of CGC Units who wish to exercise their redemption rights with respect to the underlying Public Shares must separately elect to cause the separation of their CGC Units prior to exercising such rights and prior to the applicable deadline for submitting redemption requests. See “The Extraordinary General Meeting—Redemption Rights.”