Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM F-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

Verdera Energy Corp.

(Exact name of Registrant as specified in its

charter)

Not Applicable

(Translation of Registrant’s Name into English)

| British

Columbia, Canada |

|

1094 |

|

Not

Applicable |

(State or other jurisdiction

of

incorporation or organization) |

|

(Primary Standard Industrial

Classification Code Number) |

|

(I.R.S. Employer

Identification No.) |

#250 – 750 West Pender St.

Vancouver, British Columbia, V6C 2T7, Canada

(505) 273-7724

(Address, including zip code, and telephone number,

including area code, of Registrant’s principal executive offices)

Cogency Global Inc.

122 E. 42nd Street, 18th Floor

New York, New York 10168

(800) 221-0102

(Names, address, including zip code, and telephone

number, including area code, of agent for service)

Copies to:

Jason K. Brenkert, Esq.

Dorsey & Whitney LLP

1400 Wewatta Street, Suite 400

Denver, Colorado 80202

303-352-1133 |

Approximate date of commencement of proposed sale to public: As

soon as practicable upon effectiveness of this Registration Statement.

If any of the securities being registered on

this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the

following box. ¨

If this Form is filed to register additional

securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities

Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment

filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment

filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement the same offering. ¨

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company x

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the

Securities Act. ¨

The Registrant hereby amends this Registration

Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which

specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the

Securities Act or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a),

may determine.

The

information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement

filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities

and it is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY

PROSPECTUS |

|

SUBJECT

TO COMPLETION |

|

DATED

APRIL 30, 2026 |

35,000,000 Common

Shares

Verdera Energy

Corp.

This prospectus

relates to the offer and sale of 35,000,000 common shares (the “Distribution Shares”) of Verdera Energy Corp. (the

“Company”, “we”, “us”, and “ours”) by way of a planned special

distribution (the “Special Distribution”) by the selling shareholder named herein, enCore Energy Corp., a corporation

incorporated pursuant to the laws of the Province of British Columbia (“enCore”), to the holders of common shares

of enCore (the “enCore Shareholders”) and is being delivered to enCore Shareholders in connection with the Special

Distribution. This prospectus relates to the Special Distribution of the Distribution Shares.

Pursuant to the

Special Distribution, each enCore Shareholder as of , 2026, the record date

for the Special Distribution as set by the board of directors of enCore (the “Distribution Record Date”), will be

entitled to receive their pro rata portion of the Distribution Shares per enCore common share held, [calculated by dividing the number

of Distribution Shares by the number of outstanding enCore common shares on the Distribution Record Date. EnCore shareholders who would

otherwise be entitled to a fractional Distribution Preferred Share will have the number of Distribution Shares rounded down to the nearest

whole Distribution Share.]

enCore holds 15,000,000 common shares and 35,000,000

Class A Preferred Shares of the Company, representing approximately 20.05% of the Company’s issued and outstanding voting securities.

Pursuant to their terms, the Class A Preferred Shares will convert in the Distribution Shares immediately prior to the Distribution

Record Date and be distributed to the enCore Shareholders pursuant to the Special Distribution. As a result, enCore is deemed an “affiliate”

of the Company and is deemed to be an underwriter within the meaning of Rule 145(c) under the Securities Act of 1933, as amended

(the “Securities Act”) in relation to the Special Distribution of the Distribution Shares.

We will not receive any proceeds from the Special

Distribution of the Distribution Shares or from the conversion of the Class A Preferred Shares into common shares prior to completion

of the Special Distribution.

Our common shares are currently listed for trading

on the TSX Venture Exchange (the “TSXV”) under the ticker symbol “V”. The closing price per share on the

TSXV on April 9, 2026 was C$0.55.

We are an “emerging

growth company,” as that term is used in the Jumpstart Our Business Startups Act of 2012, and as such, have elected to comply with

certain reduced public company reporting requirements for this prospectus and future filings. See “Prospectus Summary—Implications

of Being an Emerging Growth Company.”

Investing in

our common shares involves a high degree of risk. See “Risk Factors” beginning on page 16 of this prospectus for a

discussion of information that should be considered in connection with an investment in our common shares.

Neither the

U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined

if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this

prospectus is , 2026

TABLE OF CONTENTS

ABOUT THIS PROSPECUS

This prospectus is part of a registration statement

we filed with the U.S. Securities and Exchange Commission (the “SEC” or the “Commission”). If the

SEC declares the registration statement effective, the selling shareholder named herein, enCore, may sell up to 35,000,000 Distribution

Shares by way of the Special Distribution. We will update this prospectus from time to time to include new information about us, and we

will file supplements to the prospectus with the Securities and Exchange Commission. You should carefully read this prospectus, any prospectus

supplement, and the information we from time-to-time file with SEC as described under the caption “Where You Can Find Additional

Information.”

This prospectus

does not constitute an offer to sell, or a solicitation of an offer to buy, any securities in any jurisdiction in which, or from any

person with respect to whom, it is unlawful to make any such offer in such jurisdiction.

You should rely

only on the information contained in this prospectus. We have not authorized any other person to provide you with additional, different

or inconsistent information. If anyone provides you with additional, different or inconsistent information, you should not rely on it.

We may not sell these securities until the registration statement filed with, is effective. We are not making an offer to sell these

securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information appearing in this

prospectus is accurate as of any date other than the date on the front cover of this prospectus unless otherwise specified herein. Our

business, financial condition, results of operations and prospects may have changed since that date. Information contained on our website

does not constitute part of this prospectus.

The market data

and other statistical information used throughout this prospectus has been compiled from publicly available information and industry

publications. These sources generally state that the information they provide is believed to be reliable however, it is subject to subjective

assessments and changes and cannot always be verified with complete certainty due to limits on the availability and reliability of raw

data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any market research and

statistical survey. Therefore, the accuracy and completeness of the information are not guaranteed and estimates and beliefs based on

such data may not be reliable. In addition, such market data and statistical information may be different from other sources and may

not reflect all or even a comprehensive set of the actual events and transactions occurring in the market. Although we are responsible

for all of the disclosures contained in this prospectus and we believe that such market data and statistical information is reliable,

we have not independently verified its accuracy or completeness. In addition, some data is also based on our good faith estimates and

our management’s understanding of industry conditions. Such data involve risks and uncertainties and are subject to change based

on various factors, including those discussed under the headings “Forward-Looking Statements” and “Risk Factors”

in this prospectus.

GLOSSARY

For ease of reference,

the following factors for converting metric measurements into imperial equivalents are as follows:

| Metric Units | |

Multiply

By | | |

Imperial Units |

| Hectares | |

| 2.471 | | |

= acres |

| Meters | |

| 3.281 | | |

= feet |

| Kilometers | |

| 0.621 | | |

= miles (5,280 feet) |

| Grams | |

| 0.032 | | |

= ounces (troy) |

| Tonnes | |

| 1.102 | | |

= tons (short) (2,000 lbs) |

| grams/tonne | |

| 0.029 | | |

= ounces (troy)/ton |

Abbreviations

In this prospectus,

the abbreviations set forth below have the following meanings:

| $ |

U.S. Dollar |

|

km2 |

square kilometer |

| ° |

degrees |

|

kv |

kilovolt |

| % |

percent |

|

m |

meter |

| C$ |

Canadian Dollar |

|

m2 |

square meter |

| ft |

feet |

|

lb |

pound |

| g/t |

metric gram per metric

tonne |

|

U3O8 |

tri-Uranium octo-oxide |

| kg |

kilogram |

|

ppm |

parts per million |

| kg/t |

kilograms per tonne |

|

U |

Uranium |

| kl/t |

kiloliters per tonne

|

|

ac |

acres |

In this prospectus,

the following terms have the meanings set forth herein:

“BLM” means the U.S.

Bureau of Land Management.

“Central

Processing Plant” or “CPP” means the central operational facilities Uranium processing occurs following

Uranium extraction from the ore body using ISR.

“Crownpoint”

or “Crownpoint Project” means the Crownpoint and Hosta Butte Uranium Project located in McKinely

County, New Mexico, USA.

“Crownpoint

Technical Report” means the S-K 1300 technical report summary entitled “Crownpoint and Hosta Butte Uranium Project,

McKinely County, New Mexico, USA, Initial Assessment, S-K 1300” dated December 5, 2025 and effective as of February 25,

2025 prepared by BRS Inc.

“EPA”

means the U.S. Environmental Protection Agency.

“Exploration

Stage Issuer” is an issuer that has no material property with Mineral Reserves disclosed.

“Exploration

Stage Property” is a property that has no Mineral Reserves disclosed.

“GT” means grade-thickness,

a measure referring to the concentration of a mineral in Ore and the width of the Ore body.

“Inferred

Mineral Resource” is a component of Mineral Resource for which quantity and grade or quality are estimated on the basis

of limited geological evidence and sampling; where the term limited geological evidence means evidence that is only sufficient to establish

that geological and grade or quality continuity is more likely than not. The level of geological uncertainty associated with an Inferred

Mineral Resource is too high to apply relevant technical and economic factors likely to influence the prospects of economic extraction

in a manner useful for evaluation of economic viability. Because an Inferred Mineral Resource has the lowest level of geological confidence

of all Mineral Resources, which prevents the application of the modifying factors in a manner useful for evaluation of economic viability,

an Inferred Mineral Resource may not be considered when assessing the economic viability of a mining project and may not be converted

to a Mineral Reserve.

“Indicated

Mineral Resource” is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis

of adequate geological evidence and sampling. The level of geological certainty associated with an Indicated Mineral Resource is sufficient

to allow a qualified person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability

of the deposit. Because an Indicated Mineral Resource has a lower level of confidence than the level of confidence of a Measured Mineral

Resource, an Indicated Mineral Resource may only be converted to a Probable Mineral Reserve.

“Initial

Assessment” is a preliminary technical and economic study of the economic potential of all or parts of mineralization to support

the disclosure of Mineral Resources. The Initial Assessment must be prepared by a qualified person and must include appropriate assessments

of reasonably assumed technical and economic factors, together with any other relevant operational factors, that are necessary to demonstrate

at the time of reporting that there are reasonable prospects for economic extraction. An Initial Assessment is required for disclosure

of Mineral Resources but cannot be used as the basis for disclosure of Mineral Reserves.

“Ion-exchange” or

“IX” means a reversible chemical reaction that swaps ions between a solid and a solution. In the case of the Company’s

operation, the ion exchange occurs in a bed of strong base anionic polystyrene resin beads contained in a vessel or column.

“ISR”

means In Situ Recovery (literally, ‘in place’ recovery) describes rocks or formations that have not been moved from their

original position (also known as in situ leach or ISL).

“Measured

Mineral Resource” is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis

of conclusive geological evidence and sampling. The level of geological certainty associated with a Measured Mineral Resource is

sufficient to allow a qualified person to apply modifying factors, as defined in this section, in sufficient detail to support detailed

mine planning and final evaluation of the economic viability of the deposit. Because a Measured Mineral Resource has a higher level of

confidence than the level of confidence of either an Indicated Mineral Resource or an Inferred Mineral Resource, a Measured Mineral Resource

may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

“Mineral

Reserve” is an estimate of tonnage and grade or quality of Indicated and Measured Mineral Resources that, in the opinion of

the qualified person, can be the basis of an economically viable project. More specifically, it is the economically mineable part of

a Measured or Indicated Mineral Resource, which includes diluting materials and allowances for losses that may occur when the material

is mined or extracted.

“Mineral

Resource” is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such

form, grade or quality and quantity that there are reasonable prospects for economic extraction. A Mineral Resource is a reasonable estimate

of mineralization, taking into account relevant factors such as cut-off grade, likely mining dimensions, location or continuity, that,

with the assumed and justifiable technical and economic conditions, is likely to, in whole or in part, become economically extractable.

It is not merely an inventory of all mineralization drilled or sampled.

“Mineralization”

means, in exploration, a reference to a notable concentration of metals and their associated mineral compounds, or a specific mineral,

within a body of rock.

“Modifying

Factors” are the factors that a qualified person must apply to Indicated and Measured Mineral Resources and then evaluate in

order to establish the economic viability of Mineral Reserves. A qualified person must apply and evaluate modifying factors to convert

Measured and Indicated Mineral Resources to Proven and Probable Mineral Reserves. These factors include but are not restricted to: mining;

processing; metallurgical; infrastructure; economic; marketing; legal; environmental compliance; plans, negotiations, or agreements with

local individuals or groups; and governmental factors. The number, type and specific characteristics of the modifying factors applied

will necessarily be a function of and depend upon the mineral, mine, property, or project.

“NRC”

means US Nuclear Regulatory Commission.

“Ore”

means a natural aggregate of one or more minerals which may be mined and sold at a profit, or from which some part may be profitably

separated. A company may only refer to Mineral Reserves (as that term is defined in S-K 1300) as “ore.”

“Probable

Mineral Reserve” is the economically mineable part of an Indicated Mineral Resource, and in some circumstances, a Measured

Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven

Mineral Reserve.

“Proven

Mineral Reserve” is the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high

degree of confidence in the Modifying Factors.

“Qualified

Person” or “QP” means an individual who:

| a. | is

an engineer or geoscientist with a university degree, or equivalent accreditation, in an

area of geoscience, or engineering, relating to mineral exploration or mining; |

| b. | has

at least five years of experience in mineral exploration, mine development or operation or

mineral project assessment, or any combination of these, that is relevant to his or her professional

degree or area of practice; |

| c. | has

experience relevant to the subject matter of the mineral project and the technical report; |

| d. | is

in good standing with a professional association; |

| e. | in

the case of a professional association in a foreign jurisdiction, has a membership designation

that requires attainment of a position of responsibility in their profession that requires

the exercise of independent judgment; and requires: |

| i. | favorable

confidential peer evaluation of the individual’s character, professional judgement,

experience, and ethical fitness; or |

| ii. | a

recommendation for membership by at least two peers and demonstrated prominence or expertise

in the field of mineral exploration or mining. |

“Uranium”

means naturally radioactive, heavy, metallic element of atomic number 92. Uranium in its pure form is a heavy metal.

Its two principal isotopes are U-238 and U-235, of which U-235 is the necessary component for the nuclear fuel cycle. However, “uranium”

used in this annual report refers to triuranium octoxide, also called “U3O8,” and is produced from uranium deposits. It is

the most actively traded uranium-related commodity. Our operations extract and ship “yellowcake” which typically contains

70% to 90% U3O8 by weight.

“USGS”

means United States Geological Survey.

“U3O8” a

standard chemical formula commonly used to express the natural form of uranium mineralization. U represents uranium and O represents

oxygen. U3O8 is contained in “yellowcake” or “uranium concentrate” accounting for 70% to 90% by weight.

CURRENCY AND

EXCHANGE RATES

Unless otherwise

noted, the Company’s financial and related information included in this prospectus is presented in Canadian dollars (“C$”).

As of February 26, 2026 the average exchange rate, as reported by the Bank of Canada for the conversion of United States dollars

into Canadian dollars was US$0.7306 (US$1.00 = C$1.3688). Unless otherwise indicated in this prospectus, all other references herein

are to United States dollars.

Exchange Rate Information

The following tables

set forth certain exchange rates based on the average exchange rate are reported by the Bank of Canada. Each of the tables set forth

the number of Canadian dollars required under that formula to buy one United States dollar.

The following table sets forth the exchange

rate for the past five fiscal years ended September 30:

| | |

Fiscal

Year Ended

September 30, 2025 | | |

Fiscal

Year Ended

September 30, 2024 | | |

Fiscal

Year Ended

September 30, 2023 | | |

Fiscal

Year Ended

September 30, 2022 | | |

Fiscal

Year Ended

September 30, 2021 | |

| Average | |

| 1.3978 | | |

| 1.3698 | | |

| 1.3497 | | |

| 1.3011 | | |

| 1.2535 | |

The following table sets forth the high

and low exchanges rates for each month under the most recently completed six months:

| |

|

Month |

|

| |

|

October 2025 |

|

|

November 2025 |

|

|

December 2025 |

|

|

January 2026 |

|

|

February 2026 |

|

|

March 2026 |

|

| High |

|

|

1.4048 |

|

|

|

1.4120 |

|

|

|

1.3986 |

|

|

|

1.3913 |

|

|

|

1.3708 |

|

|

|

1.3939 |

|

| Low |

|

|

1.3916 |

|

|

|

1.3979 |

|

|

|

1.3674 |

|

|

|

1.3515 |

|

|

|

1.3544 |

|

|

|

1.3567 |

|

PROSPECTUS SUMMARY

This section

summarizes material information that appears later in this prospectus and is qualified in its entirety by the more detailed information

and financial statements included elsewhere herein. This summary may not contain all of the information that may be important to you.

As an investor or prospective investor, you should carefully review the entire prospectus, including the risk factors and the more detailed

information that appears later in this prospectus before you consider making an investment in our securities.

Unless

otherwise indicated, references in this prospectus to “Verdera,” the “Company,” “we,”

“our,” and “us,” refer to Verdera Energy Corp. or any one or more of its subsidiaries, or to such entities

collectively.

Our Company

Overview

We were incorporated

under the Business Corporations Act (Ontario) on December 31, 2021, under the corporate name “POCML 7 Inc.”. On November 16,

2022, we completed our initial public offering of 1,641,413 of our common shares at a price of C$0.15 per share, for aggregate gross

proceeds of C$250,000.

On November 25,

2025, we and our wholly-owned subsidiary, 1564752 B.C. Ltd., a corporation incorporated pursuant to the laws of the Province of British

Columbia (“SubCo”), entered into an amalgamation agreement (the “Amalgamation Agreement”) with

former Verdera Energy Corp. (“Former Verdera”), a corporation incorporated pursuant to the laws of the Province of

British Columbia, Canada. Pursuant to the Amalgamation Agreement, we completed a transaction (the “Transaction”),

which included a number of steps including, but not limited to: the acquisition of Former Verdera (including the Amalgamation as described

below), a transaction financing, changing our name to “Verdera Energy Corp.”, our continuation into British Columbia under

the Business Corporations Act (British Columbia), the creation of the Class A Preferred Shares, the reconstitution of our board

of directors, the reconstitution of our management team, a consolidation of the Common Shares, and any other related actions contemplated

by the Amalgamation Agreement. As part of the Transaction, SubCo and Former Verdera amalgamated (the “Amalgamation”).

The Amalgamation was structured as a three-cornered amalgamation whereby Former Verdera and SubCo amalgamated to form an amalgamated

company, Verdera Energy Holdings Inc. (“Verdera Holdings”), which is now our wholly owned subsidiary.

The Transaction closed on February 20, 2026,

and in connection therewith we changed our name to “Verdera Energy Corp.”, and completed the Consolidation (as described below).

Subsequent to closing of the Transaction we continued into British Columbia, which continuation was effective March 16, 2026.

On closing of the

Transaction, we issued 15,000,000 common shares to enCore in exchange for 15,000,000 of the preferred shares of Former Verdera (the “Former

Verdera Preferred Shares”) and we also issued 35,000,000 Class A Preferred Shares to enCore in exchange for the remainder

of the Former Verdera Preferred Shares and immediately prior to the completion of the Special Distribution, we will issue the Distribution

Shares upon conversion of the Class A Preferred Shares.

We currently have three subsidiaries, Verdera

Energy Holdings Inc., NM Energy Holding Canada Corp. and NM Energy Holding Corp. The chart below sets out our intercorporate relationships:

Verdera

Energy Corp.

(formerly POCML

7 Inc.)

(British Columbia) |

| |

100% |

Verdera

Energy Holdings Inc.

(formerly Verdera

Energy Corp.)

(British Columbia) |

| |

100% |

NM

Energy Holding Canada Corp.

(British Columbia) |

| |

100% |

NM

Energy Holding Corp.

(Texas) |

Our head office

is located at #250 – 750 West Pender St., Vancouver, British Columbia, V6C 2T7, Canada and our registered office is located at

1200-750 West Pender Street, Vancouver, British Columbia, V6C 2T8. Our website is https://verderauranium.com. The information

on our website is not incorporated by reference into this prospectus.

Business

We are focused on the exploration and, if warranted,

development of uranium assets in New Mexico, considered to be the seventh largest uranium producing district in the world. We are working

to advance our significant known In-Situ Recovery (“ISR”) amendable uranium projects to meet the growing demand for

clean, reliable domestic uranium in the United States, backed by our strategic shareholder, enCore. Strategically positioned with mineral

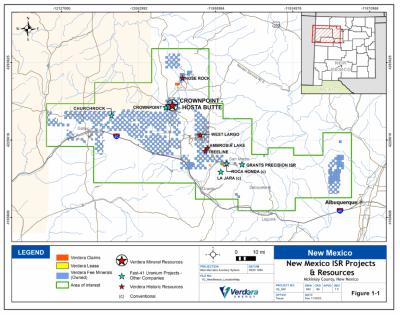

rights spanning approximately 400 square miles in the Grants Uranium District, our principal asset is our Crownpoint Project.

We are an Exploration

Stage Mining Company. The Crownpoint Project has no known Mineral Reserves under subpart 1300 of Regulation S-K of the SEC (“SK

1300”) and is an Exploration Stage Property.

Recent Developments

Acquisition

of NM Energy Holding Canada Corp

In April 2025,

we, through Former Verdera, completed the acquisition of NM Energy Holding Canada Corp. from enCore. NM Energy Holding Canada Corp was

a newly incorporated holding company with no transactions other than holding NM Energy Texas, which was incorporated in late 2024 for

the purpose of acquiring the New Mexico mining assets of enCore in an internal reorganization of those assets. The New Mexico mining

assets were previously held by Tigris Uranium Corp. and Uranco, Inc., both being subsidiaries of enCore. Both those subsidiaries

were acquired by NM Energy Holding Corp. (Texas) in a divisive merger transaction, whereby the only assets acquired by NM Energy Holding

Corp. (Texas) were the New Mexico mining assets. The divisive merger was effective on December 19, 2024.

Pursuant to a share

purchase agreement with enCore, Former Verdera acquired 100% of NM Energy Holding Canada Corp., which owned 100% of NM Energy Holding

Corp. (Texas), on April 9, 2025. NM Energy Holding Corp. (Texas) owns 100% of the Crownpoint Project except for a portion of one

section owned 40% by NuFuel Inc. (a subsidiary of Laramide Resources Ltd.), as well as several other uranium properties in New Mexico.

In consideration for the acquisition of NM Energy

Holding Canada Corp, Fromer Verdera issued enCore 50,000,000 Former Verdera Preferred Shares, made a cash payment of US$350,000 and granted

enCore a 2% net proceeds royalty on uranium, and a 2% net smelter royalty on net smelter returns received for other minerals, mined from

properties held by NM Energy Holding Canada Corp.

Transaction

Financing

On February 12,

2026, we and Former Verdera completed a brokered financing of 17,330,000 Former Verdera subscription receipts (“Former Verdera

Subscription Receipts”) and 2,670,000 Subscription Receipts of the Company (“Company Subscription Receipts”,

together with the Former Verdera Subscription Receipts, the “Subscription Receipts”) at C$1.00 per Subscription Receipt,

for gross proceeds of C$20,000,000 (the “Brokered Financing”). On closing of the Transaction, each Verdera Subscription

Receipt converted, without payment of additional consideration, into one common share of Former Verdera, which were automatically exchanged

for one of our common shares pursuant to the Transaction. On closing of the Transaction, each Company Subscription Receipt converted,

without payment of additional consideration, into one of our common shares.

Concurrently

with closing of the Transaction, we also issued, on a non-brokered basis, an additional 400,000 of our common shares at $1.00 per

common share for gross proceeds of up to C$400,000 (the “Non-Brokered Financing”).

Advisory

Fee

PowerOne Capital Markets Limited acted as advisor

to Former Verdera in connection with the Transaction. Former Verdera paid PowerOne a cash fee equal to 1.5% of the gross proceeds of the

Brokered Financing and Non-Brokered Financing, and PowerOne received options of the Company equal to 1.5% of the number of Subscription

Receipts issued in the Brokered Financing and common shares issued in the Non-Brokered Financing. Each Advisory Option is exercisable

into one of our common shares at $1.00 for 18 months. David D’Onofrio, a former director and officer of the Company, also acted

as advisor to Former Verdera in connection with the Transaction. Former Verdera issued 250,000 common shares as an advisory fee to Mr.

D’Onofrio immediately prior to closing of the Transaction.

Share Consolidation

On February 20, 2026, we completed a consolidation

(the "Consolidation") of our common shares on the basis of 0.656565 of a "new" common share for every one (1) "old"

common share outstanding. The Consolidation was completed prior to our issuance of securities to the securityholders of Former Verdera

and under the Brokered Financing and Non-Brokered Financing.

Except otherwise indicated, all references to

our historical common shares, share data, per share data and related information contained in this prospectus prior to the date of the

Consolidation depict the effect of the Consolidation as if it had occurred at the beginning of the earliest period presented. Historical

common shares, share data and per share data of Former Verdera was not affected by the Consolidation nor were issuances of securities

in the Transaction which occurred after the Consolidation. The Consolidation correspondingly adjusted, among other things, the number

of common shares issuable upon exercise of outstanding options, restricted stock units and warrants and the exercise price of such options,

restricted stock units and warrants and shares issuable upon conversion of preferred stock and other convertible securities. No fractional

shares will be issued in connection with the Consolidation, and any fractional shares resulting from the Consolidation were rounded down

to the nearest whole share.

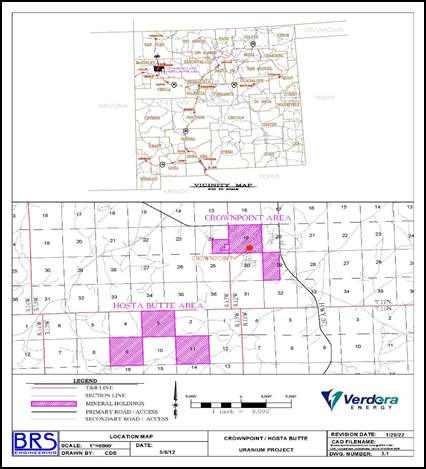

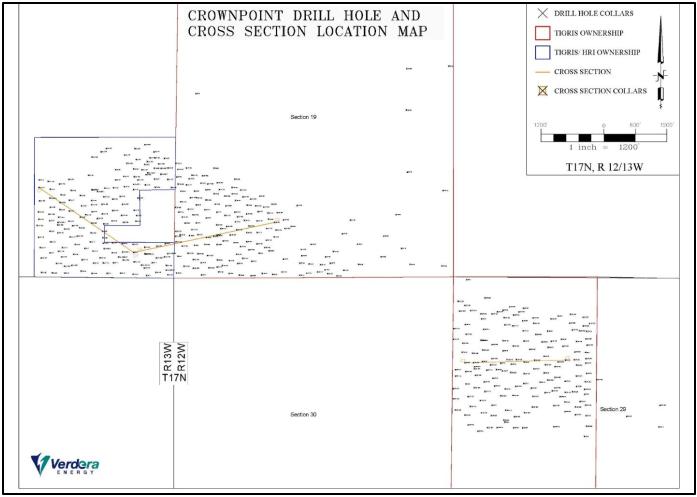

The Crownpoint Project

The Crownpoint Project is located in the Grants

Uranium Region and offers a long-term opportunity for the Company. Surface rights on the Crownpoint Project are held separately from the

mineral rights and have not been removed from development and are not under other restrictions. The Crownpoint Project consists of approximately

3,020 acres of mineral estate.

We, through our subsidiaries, hold a 100% interest

in the Crownpoint Project, except for a portion of one section which is 60% owned by us and 40% owned by NuFuel Inc. (subsidiary of Laramide

Resources Ltd.), subject to a 3% gross proceeds royalty on uranium held by NZ Uranium LLC, and a 2% net proceeds royalty on uranium and

2% net smelter royalty on other minerals, held by enCore.

The property is outside of the Navajo Reservation

and is situated on the western edge and to the southwest of the small town of Crownpoint, New Mexico. A portion of the Crownpoint Project

is included within the existing NRC source material license area that is held by a subsidiary of Laramide Resources, Ltd. The

Crownpoint area of the Crownpoint Project is wholly within NuFuels, Inc.’s (a wholly owned subsidiary of Laramide Resources

LTD) Source Materials License SUA-1580 for the in-situ recovery (“ISR”) of uranium which was issued by the US Nuclear

Regulatory Commission (NRC). Water rights have been approved by the New Mexico State Engineer for a portion of the Crownpoint Project

area. Other permits will be required to operate the Crownpoint Project at the Crownpoint area.

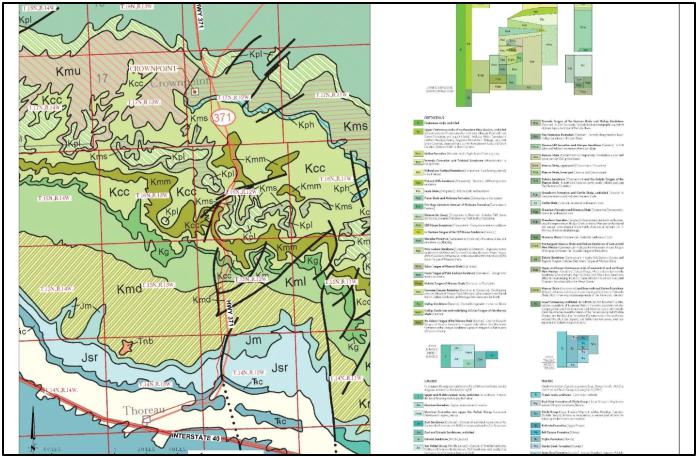

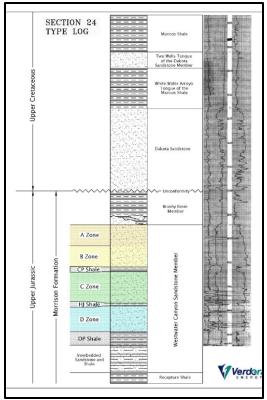

The technical and scientific description of the

Crownpoint Project contained in this prospectus is based in part on the S-K 1300 technical report summary entitled “Crownpoint

and Hosta Butte Uranium Project, McKinely County, New Mexico, USA, Initial Assessment, S-K 1300”, dated December 5,

2025 and effective as of February 25, 2025, and prepared by BRS Inc. The Crownpoint Technical Report was prepared in accordance with

SK 1300.

The Crownpoint

Project does not have any known Mineral Reserves under SK 1300. The Crownpoint Project is an Exploration Stage Property.

Map of Location

of the Crownpoint Project

See “Property

– Verdera – Crownpoint Project” for further information on the Crownpoint Project.

Additional Information

You should rely

only on the information contained in this prospectus. We have not authorized anyone to provide you with additional information or information

different from that contained in this prospectus filed with the SEC. We take no responsibility for, and can provide no assurance

as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, the common

shares and pre-funded warrants only in jurisdictions where offers and sales are permitted. The information contained in this prospectus

is accurate only as of the date of this document, regardless of the time of delivery of this prospectus or any sale of the common shares

and pre-funded warrants. Our business, financial condition, results of operations, and prospects may have changed since the date

hereof.

Risk Factors Summary

An investment in

our securities is subject to a number of risks, including risks relating to our industry, business and corporate structure. The following

summarizes some, but not all, of these risks, the occurrence of which could have a material adverse effect on our business, financial

condition and results of operations, which could cause the trading price of our common shares to decline and could result in a loss of

all or part of your investment. Please carefully consider all of the information discussed in the section entitled “Risk Factors”

in this prospectus for a more thorough description of these and other risks.

Risks Related to Our Business

| · | We

have a limited operating history and no history of revenue, which makes it difficult for

investors to evaluate our prospects. |

| · | We

have incurred losses and expects to continue to incur losses and negative cash flow, which

raises substantial doubt about our ability to continue operations without additional financing. |

| · | We

may be unable to obtain financing on acceptable terms or at all which may impact our exploration opportunities. |

| · | We

may seek funding through debt financing which could result in restrictive operating covenants

and the potential to lose assets if an event of default occurs, each of which could adversely

affect our business, financial condition and results of operations. |

| · | We

are highly dependent on the success of our single material property, the Crownpoint Project,

and any failure to advance this project could materially adversely affect our business. |

| · | We

are an early state mining company subject to significant risks regarding is ability to continue

our plan of operations, explore and, if warranted, develop the Crownpoint Project. |

| · | Our

properties do not contain Mineral Reserves under S-K 1300, and our properties, projects and

facilities may not be economic at any point in time or at all. |

| · | Mining

on properties having no known Mineral Resources or Mineral Reserves is inherently speculative

and may not prove to be economic at any point in time or at all. |

| · | We

may not realize any or all of the anticipated benefits from the Crownpoint Project. |

| · | We

may experience difficulty in exploiting successful discoveries, including at the Crownpoint

Project, which may adversely affect our business, financial condition and results of operations. |

| · | There

may be defects or disputes relating the property interests at the Crownpoint Project or our

other future property interests. |

| · | There

could be defects in the title to our properties, including at the Crownpoint Project, which

could result in us losing our interests in the property or impair our ability to conduct

activities at the project. |

Risks related

to the Mining Industry

| · | Mineral

exploration and development are speculative and inherently risky, and we may never discover

economically recoverable mineral resources. |

| · | We

have not commenced commercial production on any of our mineral properties and may never generate

revenues or achieve profitability. |

| · | We

will be subject to the risks and hazards normally encountered by companies in the mineral

exploration and extraction industry. |

| · | Economic

extraction of minerals from uranium deposits may not be commercially viable. |

| · | Estimates

of mineral resources are inherently uncertain and may not accurately reflect the economic

viability of our properties. |

| · | Shortages

of drilling contractors, drilling supplies or other key materials could adversely affect

our operations. |

| · | Projects

may not advance or achieve production if key permits are not obtained or retained. |

| · | Native

American tribes may be involved in the permitting process, which could cause delays or increased

expenses. |

Risks Related to Taxation

| · | If

we are characterized as a passive foreign investment company, U.S. Holders may be subject

to adverse U.S. federal income tax consequences. |

| · | We

will be subject to Canadian tax on its worldwide income. |

| · | Dividends,

if ever paid, on our common shares are subject to Canadian withholding tax. |

| · | Changes

in tax laws may affect us and our shareholders. |

Risk Factors

Relating to Our Common Shares

| · | There

may be no active trading market for our common shares, which could limit shareholders’

ability to sell their shares. |

| · | The

market price of our common shares may be volatile, which could result in substantial losses

for investors. |

| · | We

may issue additional equity securities, which could dilute existing shareholders and reduce

per-share value. |

| · | We

do not anticipate paying dividends on our common shares in the foreseeable future, which

may limit returns for certain investors. |

General Risk

Factors

| · | Global

financial conditions and risks could materially impact our ability to raise equity or obtain

debt and impact global supply chains, which could adversely impact our operations and financial

condition. |

| · | General

inflationary pressures may impact our costs and affect our results of operations. |

Implications of Being an Emerging

Growth Company

We qualify as an

“emerging growth company” under the Jumpstart Our Business Act of 2012, as amended, or the JOBS Act. As a result, we will

be permitted to, and intend to, rely on exemptions from certain disclosure requirements, including:

| · | an

exemption from the auditor attestation requirement in the assessment of our internal controls

over financial reporting required by Section 404 of the Sarbanes-Oxley Act of 2002,

or the Sarbanes-Oxley Act; and |

| · | an

exemption from compliance with any new requirements adopted by the Public Company Accounting

Oversight Board, or the PCAOB, requiring mandatory audit firm rotation or a supplement to

the auditor’s report in which the auditor would be required to provide additional information

about our audit and our financial statements. |

In other words,

an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private

companies. We have elected to take advantage of the benefits of this extended transition period. Our consolidated financial statements

may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

We will remain

an emerging growth company until the earliest of (i) the last day of the fiscal year during which we have total annual gross revenues

of at least US$1.235 billion; (ii) the last day of our fiscal year following the fifth anniversary of the completion of this offering;

(iii) the date on which we have, during the preceding three year period, issued more than US$1.0 billion in non- convertible debt;

or (iv) the date on which we are deemed to be a “large accelerated filer” under the Exchange Act, which could occur

if the market value of our common shares that are held by non-affiliates exceeds US$700 million as of the last business day of our most

recently completed second fiscal quarter. Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided

in the JOBS Act discussed above.

Implications of Being a Foreign Private

Issuer

Once the registration

statement of which this prospectus is a part is declared effective by the SEC, we will become subject to the reporting requirements of

the Securities Exchange Act of 1934, as amended (the “Exchange Act”) that are applicable to “foreign private

issuers,” and under those requirements we will file certain reports with the SEC. As a foreign private issuer, we will not be subject

to the same requirements that are imposed upon U.S. domestic issuers by the SEC. Under the Exchange Act, we will be subject to reporting

obligations that, in certain respects, are less detailed and less frequent than those of U.S. domestic reporting companies. For example,

although we report our financial results on a quarterly basis, we will not be required to issue quarterly reports, proxy statements that

comply with the requirements applicable to U.S. domestic reporting companies, or individual executive compensation information that is

as detailed as that required of U.S. domestic reporting companies. We also will have four months after the end of each fiscal year to

file our annual reports with the SEC and we will not be required to file current reports as frequently or promptly as U.S. domestic reporting

companies. We also present our consolidated financial statements pursuant to International Financial Reporting Standards, or IFRS, as

issued by the International Accounting Standards Board, instead of pursuant to U.S. generally accepted accounting principles. Furthermore,

our officers, directors and principal shareholders will be exempt from the short-swing profit liability provisions contained in Section 16

of the Exchange Act. As a foreign private issuer, we will also not be subject to the requirements of Regulation FD (Fair Disclosure)

promulgated under the Exchange Act. These exemptions and leniencies reduce the frequency and scope of information and protections available

to you in comparison to those applicable to shareholders of U.S. domestic reporting companies.

THE SPECIAL DISTRIBUTION

| Issuer |

|

Verdera

Energy Corp. |

| |

|

|

| Selling

Shareholder |

|

enCore

Energy Corp. |

| |

|

|

| Special

Distribution |

|

A

planned special distribution by enCore to its holders of common shares.

Pursuant to

the Special Distribution, each enCore Shareholder as of the Distribution Record Date, will be entitled to receive their pro rata

portion of the Distribution Shares per enCore common share held, [calculated by dividing the number of Distribution Shares by the

number of outstanding enCore common shares on the Distribution Record Date. EnCore shareholders who would otherwise be entitled to

a fractional Distribution Share will have the number of Distribution Shares rounded down to the nearest whole Distribution Share]. |

| |

|

|

| Distribution

Shares |

|

35,000,000

common shares of the Company, which we refer to herein as the Distribution Shares. |

| |

|

|

| Conversion of Class A Preferred Shares |

|

Immediately

prior to the completion of the Special Distribution, the Class A Preferred Shares will convert into the Distribution Shares

to be distributed in the Special Distribution. |

| |

|

|

| Shares

Outstanding after the Special Distribution |

|

110,757,993 common shares of the Company (1) |

| Use

of proceeds |

|

We

will not receive any proceeds from the Special Distribution or from the conversion of the Class A Preferred Shares into the

Distribution Shares. |

| |

|

|

| Plan

of Distribution |

|

The

offering is made by the selling shareholder, enCore, to the enCore Shareholders by way of the Special Distribution. enCore’s

board of directors has set , 2026 as the Distribution Record Date for the enCore Shareholders

entitled to receive the Distribution Shares pursuant to the Special Distribution. enCore will publicly announce the Distribution

Record Date when the Distribution Record Date has been determined. See “Plan of Distribution”. |

| Listing |

|

Our common

shares are currently listed for trading on the TSXV under the ticker symbol “V”. |

| |

|

|

| Risk factors |

|

An

investment in our securities involves substantial risks. You should read this prospectus carefully, including the section entitled “Risk

Factors” and the financial statements and the related notes to those statements included elsewhere in this prospectus before investing

in our securities. |

| (1) |

Based

on 75,757,993 common shares issued and outstanding as of April 9, 2026. Assumes the conversion of the Class A Preferred Shares

into 35,000,000 Distribution Shares upon completion of the Special Distribution. Does not include as of April 9, 2026: 6,576,000

common shares underlying stock options to be issued by the Company to holders of options of Verdera and 800,000 compensation options

issued to brokers as part of the Financing. |

SUMMARY

CONSOLIDATED FINANCIAL DATA

The following

tables set forth a summary of the historical audited consolidated financial data of the Company as at and for the fiscal years ended

September 30, 2025 and 2024. The historical summary consolidated financial data set forth in the following tables has been derived

from the Company’s consolidated financial statements included elsewhere in this prospectus. You should read this data together with the

consolidated financial statements and the related notes appearing elsewhere in this prospectus and the information included under the

caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Our historical results

are not necessarily indicative of our future results.

Selected Statements of Loss and Comprehensive

Loss:

(expressed in Canadian

Dollars)

| | |

Three Months

ended

December 31,

2025 | | |

Three Months

ended

December 31,

2024 | | |

Year ended

September 30,

2025 | | |

Year ended

September 30,

2024 | |

| Total expenses | |

$ | 34,171 | | |

$ | 241 | | |

$ | 23,954 | | |

$ | 25,053 | |

| Interest Income | |

$ | (3,893 | ) | |

$ | (6,319 | ) | |

$ | (19,197 | ) | |

$ | (23,902 | ) |

| Net (income)/loss and comprehensive (income)/loss | |

$ | 30,278 | | |

$ | (6,078 | ) | |

$ | 4,757 | | |

$ | 1,151 | |

| Net loss per share | |

$ | 0 | | |

$ | 0 | | |

$ | 0 | | |

$ | 0 | |

| Weighted average number of common shares outstanding, basic and diluted | |

| 7,277,777 | | |

| 7,268,791 | | |

| 7,275,531 | | |

| 7,243,122 | |

Selected Statements of Financial Position

(expressed in Canadian

Dollars)

| | |

December 31,

2025 | | |

September 30,

2025 | | |

September 30,

2024 | |

| Cash and cash equivalents | |

$ | 605,403 | | |

$ | 606,725 | | |

$ | 598,838 | |

| Total assets | |

$ | 618,115 | | |

$ | 615,568 | | |

$ | 613,417 | |

| Current liabilities | |

$ | 73,707 | | |

| 40,882 | | |

| 36,804 | |

| Total liabilities | |

$ | 73,707 | | |

$ | 40,882 | | |

$ | 36,804 | |

| Total shareholder’s equity | |

$ | 544,408 | | |

$ | 574,686 | | |

$ | 576,613 | |

| Total liabilities and shareholder’s equity | |

$ | 618,115 | | |

$ | 615,568 | | |

$ | 613,417 | |

SUMMARY CONSOLIDATED

FINANCIAL DATA OF FORMER VERDERA

The following tables set forth a summary of

the historical audited consolidated financial data of Former Verdera as at and for the period from incorporation on September 27,

2024 to March 31, 2025 and for the month ended April 30, 2025 and the unaudited consolidated condensed financial data as at

and for the periods ended December 31, 2025 and 2024. The historical summary consolidated financial data set forth in the following

tables has been derived from Former Verdera’s consolidated financial statements included elsewhere in this prospectus. In our opinion,

the unaudited interim consolidated financial statements have been prepared on a basis consistent with our audited consolidated financial

statements and, in our opinion, contain all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation

of such interim financial statements. You should read this data together with the consolidated financial statements and the related

notes appearing elsewhere in this prospectus and the information included under the caption “Management’s Discussion and Analysis

of Financial Condition and Results of Operations.” Our historical results are not necessarily indicative of our future results.

Selected Consolidated Statements of Loss and

Comprehensive Loss:

(expressed in Canadian Dollars)

| | |

Nine Months

ended

December 31,

2025 | | |

From

incorporation

on September

27, 2024 to

December

31, 2024 | | |

Month ended

April 30, 2025 | | |

From

Incorporation

of September

27, 2024 to

March 31,

2025 | |

| Total expenses | |

$ | (1,326,660 | ) | |

$ | (129,327 | ) | |

$ | (81,891 | ) | |

$ | (387,502 | ) |

| Foreign Exchange | |

$ | (2,439 | ) | |

$ | (540 | ) | |

$ | 175 | | |

$ | (1,603 | ) |

| Loss and comprehensive loss | |

$ | (1,329,009 | ) | |

$ | (129,867 | ) | |

$ | (81,716 | ) | |

$ | (389,105 | ) |

| Basis and diluted loss per share | |

$ | (0.06 | ) | |

$ | (0.3 | ) | |

$ | (0.00 | ) | |

$ | (0.04 | ) |

| Weighted average number of common shares outstanding, basic and diluted | |

| 24,014,321 | | |

| 4,497,927 | | |

| 17,704,334 | | |

| 10,702,125 | |

Selected Consolidated

Statements of Financial Position

(expressed in Canadian

Dollars)

| | |

December 31,

2025 | | |

April 30,

2025 | | |

March 31,

2025 | |

| Cash | |

$ | 7,040,098 | | |

$ | 2,403,259 | | |

$ | 2,421,377 | |

| Current assets | |

$ | 7,785,989 | | |

$ | 2,434,201 | | |

$ | 2,445,056 | |

| Deferred transaction cost | |

| -- | | |

| -- | | |

| 637,940 | |

| Exploration and evaluation assets | |

$ | 10,897,312 | | |

$ | 10,835,059 | | |

$ | -- | |

| Total assets | |

$ | 18,683,301 | | |

$ | 13,269,260 | | |

$ | 3,082,996 | |

| Current liabilities | |

$ | 250,000 | | |

$ | 420,741 | | |

$ | 339,511 | |

| Total liabilities | |

$ | 250,000 | | |

$ | 420,741 | | |

$ | 339,511 | |

| Share Capital | |

$ | 19,387,086 | | |

$ | 13,179,837 | | |

$ | 3,010,166 | |

| Deficit | |

$ | (1,718,204 | ) | |

$ | (470,821 | ) | |

$ | (389,105 | ) |

| Total shareholders’ equity | |

$ | 18,433,301 | | |

$ | 12,848,519 | | |

$ | 2,743,485 | |

| Total liabilities and shareholder’s equity | |

$ | 18,683,301 | | |

$ | 13,269,260 | | |

$ | 3,082,996 | |

SUMMARY PRO FORMA FINANCIAL

INFORMATION

The following

table sets out certain selected financial information for the Company and Verdera, as well as certain unaudited pro forma financial information

for the Company following the completion of the Transaction on a consolidated basis, after giving effect to the Transaction and the related

transaction financing. The following information is presented in Canadian dollars and should be read in conjunction with the financial

statements and pro forma financial statements set out in the Schedules hereto and incorporated by reference herein.

Selected Pro

Forma Financial Data

(expressed in Canadian

Dollars)

| | |

POCML7 as at

September 30,

2025 | | |

Verdera as at

September 30,

2025 | | |

Pro Forma

Adjustments | | |

Pro Forma

Consolidation | |

| Cash | |

$ | 606,725 | | |

$ | 7,250,531 | | |

$ | 19,000,000 | | |

$ | 26,857,256 | |

| Total Assets | |

$ | 615,568 | | |

$ | 18,269,425 | | |

$ | 19,000,000 | | |

$ | 37,884,993 | |

| Total Current Liabilities | |

$ | 40,882 | | |

$ | 107,234 | | |

| - | | |

$ | 148,116 | |

| Total Long Term Liabilities | |

| Nil | | |

| Nil | | |

| - | | |

| Nil | |

| Total Shareholders’ Equity | |

$ | 574,686 | | |

$ | 18,162,191 | | |

$ | 19,000,000 | | |

$ | 37,736,877 | |

RISK

FACTORS

You should carefully

consider the following risk factors that may affect our business, future operating results and financial condition, as well as the other

information set forth in this prospectus, before making a decision to invest in our securities. If any of the following risks actually

occurs, our business, operating results, cash flows, financial condition, and ability to pay dividends could be materially and adversely

affected. In such case, the trading price of our securities would likely decline, and you may lose all or part of your investment. The

risks below are not the only ones we face. Additional risks not currently known to us, or that we currently deem immaterial, may also

adversely affect us.

Risk Factors

Relating to Company

We have a limited operating history and

no history of revenue, which makes it difficult for investors to evaluate our prospects.

We are an Exploration Stage Mining Company with

a limited operating history and no history of revenues or profitability. As a result, investors may have difficulty evaluating our business,

prospects and likelihood of future success. Our ability to achieve profitability will depend on numerous factors, including the success

of our exploration activities, the development of economically viable mineral resources, if any, prevailing commodity prices and our ability

to raise additional capital, many of which are outside of our control. The likelihood of our success must be considered in light of the

problems, expenses, difficulties, complication and delays frequently encountered in connection with the establishment of any business,

particularly those in the junior mineral exploration sector. We will have limited financial resources and there can be no assurance that

additional funding will be available to fund further operations or to fulfill our obligations under applicable agreements. Further, there

can be no assurance that we will be able to generate revenues, operate profitably, or provide a return on investment, or that we will

successfully implement our plans.

We will have incurred losses and expects

to continue to incur losses and negative cash flow, which raises substantial doubt about our ability to continue operations without additional

financing.

We have incurred losses and negative cash flows

since inception and expects to continue to do so for the foreseeable future as we invest in exploration and, if warranted, development

and general corporate activities. We will require additional capital to fund our operations and advance our mineral properties. There

can be no assurance that we will be able to obtain additional financing on acceptable terms or at all. If we are unable to raise additional

capital when needed, we may be required to delay, reduce or eliminate certain exploration or development activities, which could adversely

affect our business, financial condition and results of operations.

We may be unable to obtain financing on

acceptable terms or at all which may impact our exploration opportunities.

Further exploration of the Crownpoint Project,

and any future exploration of other properties in which we hold an interest, will require additional capital, and the amount of capital

required may be significant. There can be no assurance that we will be successful in obtaining the required financing for such purposes

or for any other purposes, including for general working capital. Our ability to secure any required financing to sustain operations will

depend in part upon prevailing capital market conditions and business success. There can be no assurance that we will be successful in

our efforts to secure any additional financing on terms satisfactory to our management. If additional financing is raised through the

issuance of additional common shares or other securities of the Company, control of the Company may change and shareholders of the Company

may suffer dilution. If adequate funds are not available, or are not available on acceptable terms, we may be required to scale back our

current business plan or cease operating. Additionally, failure to obtain additional financing could impede our funding obligations, or

result in delay or postponement of further business activities, which could adversely affect our business, financial condition and results

of operations.

We

may seek funding through debt financing which could result in restrictive operating covenants and the potential to lose assets if an event

of default occurs, each of which could adversely affect our business, financial condition and results of operations.

From time to time, we may rely on debt financing

for a portion of our business activities, including capital and operating expenditures. There can be no assurance that we will be able

to comply at all times with any covenants imposed under our debt arrangements, if applicable. Similarly, there can be no assurance that

we will be able to secure new financing that may be necessary to finance our operations and capital growth program. Any failure by us

to secure financing or refinancing, obtain new financing, or comply with applicable covenants under our debt arrangements could adversely

affect our business, financial condition and results of operations. Further, any inability by us to obtain new financing may limit our

ability to support or sustain our future growth.

We are highly

dependent on the success of our single material property, the Crownpoint Project, and any failure to advance this project could materially

adversely affect our business.

Our future prospects are highly dependent on the

successful exploration and potential development of our only material mineral property, the Crownpoint Project. The continued exploration

operations and, if warranted, development of mining operations at the Crownpoint Project, will require the commitment of substantial additional

resources for capital expenditures and operating expenditures, which may increase in subsequent years as needed, and for consultants,

personnel and equipment associated with additional development and mining of the Crownpoint Project. The project is subject to numerous

risks, including geological uncertainty, permitting challenges, environmental considerations and changes in market conditions. Any failure

to advance the Crownpoint Project could adversely affect our business, financial condition and results of operations.

We are an

early state mining company subject to significant risks regarding our ability to continue our plan of operations, explore and, if warranted,

develop the Crownpoint Project.

We are in the business of exploration, with the

ultimate goal of achieving commercial production or extraction of Uranium. The Crownpoint Project will not have commenced commercial production

and we will have no history of earnings or cash flow from our operations. Due to the foregoing, there can be no assurance that we will

be able to develop the Crownpoint Project profitably, or that our activities will generate positive cash flow. We are unlikely to enjoy

earnings and are not expected to pay dividends in the immediate or foreseeable future. We will have limited cash and other assets. A prospective

investor in the Company must be prepared to rely solely upon the ability, expertise, judgment, discretion, integrity and good faith of

our management in all aspects of the development and implementation of our business activities.

Our properties

do not contain Mineral Reserves under S-K 1300, and our properties, projects and facilities may not be economic at any point in time

or at all.

None of our

properties contain any known Mineral Reserves. Some or all of our properties, projects and facilities may not be economic for

uranium, extraction, recovery or processing at any point in time. Generally, we intend to continue to hold, and in certain cases

advance, properties, projects and facilities which may not be economic at any point in time in anticipation of possible future

increases in the prices of Uranium, as the case may be. However, in those circumstances, there can be no assurance at any time that

such prices will ever, or within a reasonable time period, increase to the levels required to advance those properties or, in the

case of projects or facilities on standby, to resume exploration, extraction, recovery or processing activities at those projects or

facilities. In the event of depressed commodity prices, we would continue to hold our standby properties, projects and facilities

because we believe that prices are likely to rise to such levels within a reasonable time period to justify future production.

However, as there is a cost associated with holding and, in some cases, maintaining such properties, projects and facilities on

standby during periods of depressed commodity prices, in those circumstances we continuously evaluate, on a case-by-case basis, such

costs against the prospects for price increases, and may from time to time sell, drop or reclaim any such properties, projects or

facilities.

Mining on

properties having no known Mineral Resources or Mineral Reserves is inherently speculative and may not prove to be economic at any point

in time or at all.

Mining is an

inherently speculative business. There is a possibility that we will not discover Uranium on any or all of our future acquired

properties which can be mined or extracted at a profit at any point in time or at all. Even if we do discover and mine such

minerals, the deposits may not be of the quality or size necessary for it or a potential purchaser of the property to make a profit

from mining it. Few properties that are explored are ultimately developed into producing mines, and mines that are developed may not

be profitable. Unusual or unexpected geological formations, geological formation pressures, fires, power outages, labor disruptions,

flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor, as well

as all necessary licenses and permits, are just some of the many risks involved in mineral exploration programs and their subsequent

development. However, we may elect, now or in the future, to proceed with the extraction of minerals on one or more of those

projects without having completed the technical work required to declare a Mineral Reserve. If we are then unable to extract uranium

in commercially viable quantities, the capital investment of mining such properties may be lost and could materially impact our

business.

We may not

realize any or all of the anticipated benefits from the Crownpoint Project.

The estimates of

the potential benefits and growth of the Crownpoint Project are based in part on a valuation of the project that may differ from the

actual performance of the Crownpoint Project on a going-forward basis. Achieving the benefits of the Crownpoint Project will depend,

in part, on our ability to effectively explore and, if warranted, develop the project. The challenges involved, which may be complex

and time-consuming, include the following:

| · | the

cost of exploration activities and the results of such exploration activities; |

| · | the

ability to locate, hire and retain experienced contractors to allow efficient exploration

activities at the project; |

| · | the

ability to locate, hire and retain experienced staff for development activities, if warranted,

including well drilling and installation; and |

| · | our

ongoing relations with the community and property owners in the project area. |

In addition, any benefits that we realize may

be offset, in whole or in part, by reductions in revenues, or through increases in other expenses, including costs to achieve the Crownpoint

Project’s estimated synergies and growth. Our plans for the Crownpoint Project are subject to numerous risks and uncertainties that

may change at any time. There is no assurance that our initiatives will be completed as anticipated or that the benefits we expect will

be achieved on a timely basis or at all. It may take longer than expected to achieve the anticipated benefits and growth and there is

no guarantee that the Crownpoint Project will reach near-term production. If the Crownpoint Project does not achieve the anticipated benefits

and growth or reach near-term production, this may adversely affect our future financial results.

We may experience difficulty in exploiting

successful discoveries, including at the Crownpoint Project, which may adversely affect our business, financial condition and results

of operations.

It may not always be possible for us to participate

in the exploitation of successful discoveries on our properties, including the Crownpoint Project. Such exploitation may involve the need

to obtain licenses or clearance from the relevant authorities, which may not be available on a timely basis, or may require conditions

to be satisfied and/or the exercise of discretion by such authorities. It may or may not be possible for such conditions to be satisfied,

and such conditions may prove uneconomic or impractical. Furthermore, the decision to proceed with further exploration may require the

participation of other persons and companies whose interest and objectives may not be consistent with those of the Company. Such further

exploitation may also require us to meet or commit to financial obligations that it may not have anticipated or may not be able to commit

to due to a lack of funds or an inability to raise funds. Failure to exploit successful discoveries could adversely affect our business,

financial condition and results of operations.

There may be defects or disputes relating

to the property interests at the Crownpoint Project or our other future property interests.

Defects in or disputes relating to the property

interests we hold, including those at the Crownpoint Project, or acquires may prevent us from realizing the anticipated benefits from

these interests. Material changes could also occur that may adversely affect the estimate of our management with respect to the carrying

value of our property interests, and could result in impairment charges. While we will seek to confirm the existence, validity, enforceability,

terms and geographic extent of the interests we acquire, there can be no assurance that disputes or other problems concerning these and

other matters or other problems will not arise. Confirming these matters is complex and is subject to the application of the laws of each

jurisdiction to the particular circumstances of each parcel of mineral property and to the documents reflecting the interest. The discovery

of any defects in, or any disputes in respect of, our property interests, including in respect of the Crownpoint Project, could adversely

affect our business, financial condition and results of operations.

There could

be defects in the title to our properties, including at the Crownpoint Project, which could result in us losing our interests in the

property or impair the ability of us to conduct activities at the project.

A defect in the chain of title to one of our property

interests or necessary for the anticipated development or operation of a particular project to which an interest relates may defeat or

impair our claim to a property, which could in turn result in a loss of our interest in respect of that property. In addition, claims

by third parties or Indigenous groups may impact our ability to conduct activities on a property in which we hold an interest, to the

detriment of our interest. To the extent that we, directly or indirectly, do not have title to a property, we may be required to cease

operations or transfer operational control to another party. Certain interests can be contractual in nature, rather than an interest in

land, with the risk that an assignment or bankruptcy or insolvency proceedings by an owner of a particular property may result in the

loss of any effective interest in such property. Further, even in those jurisdictions where there is a right to record or register interests

held by us in land registries or mining recorders offices, such registrations may not necessarily provide any protection to us. As a result,

known title defects, as well as unforeseen and unknown title defects, may impact operations at a project in respect of which we have an

interest and could adversely affect our business, financial condition and results of operations.

We could be subject to litigation in relation

to ownership of our property interests which could be costly and result in the loss of our interests in the property or payment of damages.

There is a potential that litigation may arise

with respect to a property in which we hold an interest (for example, litigation between joint venture partners or between us (or an operator)

and original property owners or neighboring property owners), including the Crownpoint Project. Any such litigation that results in the

cessation or reduction of production from a property in which we hold an interest (whether temporary or permanent) or the expropriation

or loss of rights to such property could adversely affect our business, financial condition and results of operations. As a holder of

such interests, we may, in certain circumstances, not have any influence on the litigation and may not have access to data.

We rely upon the reports of third parties

in relation to making decisions on the expenditure of funds to explore and, if warranted, develop our properties and on assessing the

potential economic viability of our projects. If such third-party reports are inaccurate or incomplete, we could be adversely affected.

We will rely upon third parties to provide analysis,

reviews, reports, advice and opinions regarding our properties, including the Crownpoint Project. There is a risk that such analyses,

reviews, reports, advice, and opinions in respect of such properties may be inaccurate, in particular with respect to resource estimation,

process development and recommendations for products to be produced, as well as with respect to economic assessments, including estimating

the capital and operation costs of our project and forecasting potential future revenue streams. Uncertainties are also inherent in such

estimations. Such inaccuracies and uncertainties could adversely affect our business, financial condition and results of operations.

We may fail to acquire additional property

interests for our future benefit which could adversely impact our operations.