NVIT Real Estate

Fund

Summary Prospectus April 30, 2026

Class I / Class II

Before you invest, you may want to review the Fund’s Prospectus, which contains information about the Fund and its risks. This Summary Prospectus is intended for use in connection with variable insurance contracts, and is not intended for use by other investors. The Fund’s Prospectus and Statement of Additional Information, each dated April 30, 2026 (as may be supplemented or revised), are incorporated by reference into this Summary Prospectus. For free paper or electronic copies of the Fund’s Prospectus and other information about the Fund, go to nationwide.com/mutualfundsnvit, email a request to web_help@nationwide.com or call 800-848-0920, or ask any variable insurance contract provider who offers shares of the Fund as an underlying investment option in its products.

Objective

The NVIT Real Estate Fund seeks current income and long-term capital appreciation.

Fees and Expenses

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund.

Sales charges and other expenses that may be imposed by variable insurance

contracts are not included. If these charges were reflected, the expenses listed below would be higher. See the variable insurance contract prospectus, which may impose sales charges and other additional contract-level

expenses.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| |

Class I

Shares |

Class II

Shares |

| Management Fees |

0.70% |

0.70% |

| Distribution and/or Service (12b-1) Fees |

None |

0.25% |

| Other Expenses |

0.23% |

0.23% |

| Total Annual Fund Operating Expenses |

0.93% |

1.18% |

| Fee Waiver/Expense Reimbursement(1) |

(0.01)% |

(0.01)% |

| Total Annual Fund Operating Expenses After Fee Waiver/Expense

Reimbursement |

0.92% |

1.17% |

(1)

Nationwide Variable Insurance Trust (the “Trust”) and Nationwide Fund Advisors (the “Adviser”) have entered into a written contract waiving 0.013% of the

management fee to which the

Adviser would otherwise be entitled until April 30, 2027. The written contract may be changed or eliminated only with the consent of the Board of Trustees of the

Trust.

Example

This Example is intended to help you to compare the cost of investing in the Fund with the cost of investing in other mutual

funds. The Example, however, does not include charges that are imposed by variable insurance contracts. If these charges were reflected, the expenses listed below would be higher.

This Example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell all of your shares at the end of those time periods. It assumes a 5% return each year and no change in expenses, and any expense limitation or fee waivers that may apply for the periods indicated above under “Fees and Expenses.” Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| |

1 Year |

3 Years |

5 Years |

10 Years |

| Class I Shares |

$94 |

$295 |

$514 |

$1,142 |

| Class II Shares |

119 |

374 |

648 |

1,431 |

NSP-RE (4/26)

Summary Prospectus

April 30, 2026

1

NVIT Real Estate Fund

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or

“turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in Annual Fund Operating

Expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 111.04% of the average value of its

portfolio.

Principal Investment Strategies

Under normal circumstances, the Fund invests at least 80% of its net assets in equity securities of real estate companies. For these purposes, a real estate company is a company that (i) derives at least 50% of its revenues from the ownership, operation,

development, construction, financing, management or sale of commercial, industrial or residential real estate and similar activities, or (ii) invests at least 50% of its net revenues in such real estate. Equity securities in which the Fund invests are primarily common stocks of companies of any size, including smaller companies, and include the securities of real estate investment trusts (“REITs”). Issuers of the equity securities in which the Fund invests are located primarily in the United States. The Fund does not invest in real estate directly. The Fund is nondiversified for purposes of the Investment Company Act of 1940, which means that the Fund may hold larger positions in fewer securities than other funds.

The Fund’s subadviser actively manages the Fund using a combination of bottom-up analysis of factors affecting individual securities and top-down analysis of the real estate market. Using multiple valuation metrics, the subadviser seeks to identify

issuers evidencing short-term dislocations between stock prices and fundamentals, and ultimately invest at below-market valuations in real estate companies that the subadviser believes will be strong long-term performers. In seeking a diversified

exposure to all major real estate sectors, the subadviser’s top-down analysis studies macroeconomic, private real estate, industry and regional trends to influence the Fund’s sector and geographic weightings. The subadviser may sell a security when it believes it has become overvalued or no longer offers an attractive risk/reward profile, relative fundamentals have deteriorated, or to take advantage of other opportunities the subadviser believes to be more attractive. The Fund may engage in active and frequent

trading of portfolio securities.

Principal Risks

The Fund cannot guarantee that it will achieve its investment objective.

As with any fund, the value of the Fund’s investments—and therefore, the value of Fund shares—may fluctuate. These changes may occur because of:

Equity securities risk – stock markets are volatile. The price of an equity

security fluctuates based on changes in a company’s financial condition and overall market and economic conditions.

Market risk – the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the

markets will go down sharply and unpredictably. This occurs due to numerous factors, including interest rates, the outlook for corporate profits, the health of the national and world economies, and the fluctuation of other securities markets around the

world. These risks may be magnified if certain social, political, economic and other conditions and events (such as natural disasters, epidemics and pandemics, terrorism, conflicts, trade disputes and social unrest or rapid technological developments

such as artificial intelligence) adversely interrupt the global economy.

Selection risk – the risk that the securities

selected by the Fund’s subadviser will underperform the markets, the relevant indexes or the securities selected by other funds with similar investment objectives and

investment strategies.

Real estate

market risk – your investment in the Fund will be closely linked to the performance of the real estate markets. Property values may fall due to increasing vacancies or declining rents resulting from unanticipated economic, legal, cultural or technological developments, including the impact of changes in environmental laws. Real estate companies may have lower

trading volumes and prices also may drop because of the failure of borrowers to pay their loans and poor management, including any potential defects in mortgage documentation or in the foreclosure process. In addition, real estate companies are subject to the risk of increased competition, property taxes, capital expenditures, and operating expenses. These developments affecting

the real estate industry could adversely affect the real estate companies in which the Fund invests.

REIT risk – involves the risks that are associated with direct ownership of real estate and with the real estate industry in general. REITs are dependent upon management skills and may not be diversified. REITs are also subject to heavy cash flow dependency,

defaults by borrowers and self-liquidation. In addition, REITs could possibly fail to qualify for pass-through of income under the Internal Revenue Code of 1986, as amended, affecting their value. Other factors may also adversely affect a borrower’s or a

Summary Prospectus April 30, 2026

2

NVIT Real Estate

Fund

lessee’s ability to meet its obligations to

the REIT. In the event of a default by a borrower or lessee, the REIT may experience delays in enforcing its

rights as a mortgagee or lessor and may incur substantial costs associated with protecting its investments.

REITs may have lower trading volumes and may be subject to more abrupt or erratic price movements than the

overall securities markets.

Value style risk – value investing carries the risk that the market will not recognize a security’s intrinsic value for a long time or that a stock judged to be undervalued

actually is appropriately priced. In addition, value stocks as a group sometimes are out of favor and

underperform the overall equity market for long periods while the market concentrates on other types of stocks,

such as “growth” stocks.

Sector risk – emphasizing investments in real

estate businesses makes the Fund more susceptible to financial, market or economic events affecting the

particular issuers and real estate businesses in which it invests than funds that do not emphasize particular

sectors.

Smaller company risk – smaller companies are usually less stable in price and less liquid than larger, more established companies. Smaller companies are more vulnerable than larger companies to adverse business and economic developments and may have more limited resources. Therefore, they generally involve greater risk.

Nondiversified fund risk – because the Fund may hold larger positions in fewer securities and financial instruments than diversified funds, a single security’s or instrument's increase or decrease in value may have a greater impact on the

Fund’s value and total return.

Portfolio turnover risk – a higher portfolio turnover rate increases transaction costs and may adversely impact the Fund’s performance.

Loss of money is a risk of investing in the Fund. An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government

agency.

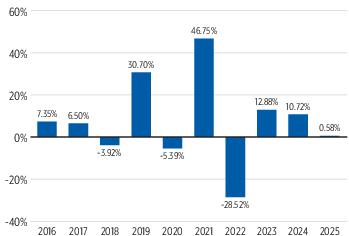

Performance

The following bar chart and table provide some indication of the risks of investing in the Fund. The bar chart shows the volatility or variability of the Fund’s annual total returns over time and shows that Fund performance can change from

year to year. The table shows the Fund’s average annual total returns for certain time periods compared

to the returns of a broad-based securities market index and an additional index. The additional index has

characteristics relevant to the Fund’s investment strategy. Remember, however, that past performance is not necessarily an indication of how the Fund will perform in the future. The returns shown in the bar chart and table do not include charges that will be imposed by

variable insurance contracts. If these amounts

were reflected, returns would be less than those shown.

The Fund compares its performance to the Russell 1000 Index to satisfy a Securities and Exchange Commission (SEC) disclosure requirement.

Annual Total Returns– Class I Shares

(Years Ended December 31,)

(Years Ended December 31,)

| Highest Quarter: |

17.25% |

– |

4Q 2021 |

| Lowest Quarter: |

-23.37% |

– |

1Q 2020 |

Average Annual Total Returns

(For the Periods Ended December 31, 2025)

(For the Periods Ended December 31, 2025)

| |

1 Year |

5 Years |

10 Years |

| Class I Shares |

0.58% |

5.69% |

6.00% |

| Class II Shares |

0.33% |

5.43% |

5.75% |

| Russell 1000® Index (reflects no deduction for

fees or expenses) |

17.37% |

13.59% |

14.59% |

| Dow Jones U.S. Select Real Estate Securities

Index (reflects no deduction for fees or

expenses) |

3.67% |

6.62% |

4.79% |

Portfolio Management

Investment Adviser

Nationwide Fund Advisors

Subadviser

Wellington Management Company LLP

Portfolio Manager

| Portfolio Manager |

Title |

Length of Service with Fund |

| Bradford D. Stoesser |

Senior Managing

Director, Partner and

Global Industry Analyst |

Since 2017 |

Summary Prospectus April 30, 2026

3

NVIT Real Estate

Fund

Tax Information

The dividends and distributions paid by the Fund to the insurance company separate accounts will consist of ordinary income, capital gains, or some combination of both. Because

shares of the Fund must be purchased through separate accounts used to fund variable insurance contracts, such

dividends and distributions will be exempt from current taxation by contract holders if left to accumulate

within a separate account. Consult the variable insurance contract prospectus for additional tax

information.

Payments to Broker-Dealers and Other

Financial Intermediaries

This Fund is only offered as an underlying investment option for variable insurance contracts. The Fund and its related

companies may make payments to the sponsoring insurance companies (or their affiliates) for distribution and/or

other services, and to broker-dealers and other financial intermediaries that distribute the variable insurance

contracts. These payments may create a conflict of interest by influencing the insurance companies to include

the Fund as an underlying investment option in the variable insurance contracts, and by influencing the

broker-dealers and other financial intermediaries to distribute variable insurance contracts that include the

Fund as an underlying investment option over other variable insurance contracts or to otherwise recommend the

selection of the Fund as an underlying investment option by contract owners instead of other funds that also

may be available investment options. The prospectus (or other offering document) for your variable insurance

contract may contain additional information about these payments.

Summary Prospectus April 30, 2026

4

NVIT Real Estate Fund