Annual Meeting of Shareholders April 23, 2026

CAUTIONARY STATEMENT REGARDING FORWARD - LOOKING INFORMATION This presentation contains forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 , as amended, regarding our outlook or expectations relating to our future business, operations, financial condition, financial performance, asset quality and ca pit al levels, among other matters. Forward - looking statements are necessarily subject to numerous assumptions, risks and uncertainties, which change over time. Actual r esu lts or future events could differ from those indicated. The forward - looking statements in this presentation are qualified by the following factors: P ossible changes in economic and business conditions that may affect the prevailing interest rates, the prevailing rates of i nfl ation, or the amount of growth, stagnation, or recession in the global, U.S., and Northcentral Pennsylvania economies, the value of investments, collectabili ty of loans and the profitability of business entities; P ossible changes in monetary and fiscal policies, laws and regulations, and other activities of governments, agencies and simi lar organizations; T he effects of easing of restrictions on participants in the financial services industry, such as banks, securities brokers an d d ealers, investment companies and finance companies, and attendant changes in matters and effects of competition in the financial services industry; The cost and other effects of legal proceedings, claims, settlements and judgments; and O ur ability to achieve the expected operating results related to our operations which depends on a variety of factors, includi ng the continued growth of the markets in which we operate consistent with recent historical experience, and our ability to expand into new markets and to maintain pro fit margins in the face of pricing pressures. The possibility that the anticipated benefits of any transaction will not be realized when expected or at all because expecte d synergies and operating efficiencies may not be achievable within expected time frames or at all, and the potential impact of general economic, political and market f act ors, among other matters. The words “believe,” “expect,” “anticipate,” “project” and similar expressions signify forward - looking statements. Listene rs are cautioned not to place undue reliance on any forward - looking statement made by or on behalf of us. Any such statement speaks only as of April 23, 2026. We un dertake no obligation to update or revise any forward - looking statement that is made at our Annual Meeting. 2

Bank Counsel Dean H. Dusinberre , Esquire Stevens & Lee 3

Independent Registered Public Accountants Gregory J. Faulk, CPA, MBA Assurance Principal S.R. Snodgrass, P.C. Brendan Whalen, CPA Assurance Principal S.R. Snodgrass, P.C. 4

2025 Financial Review 5

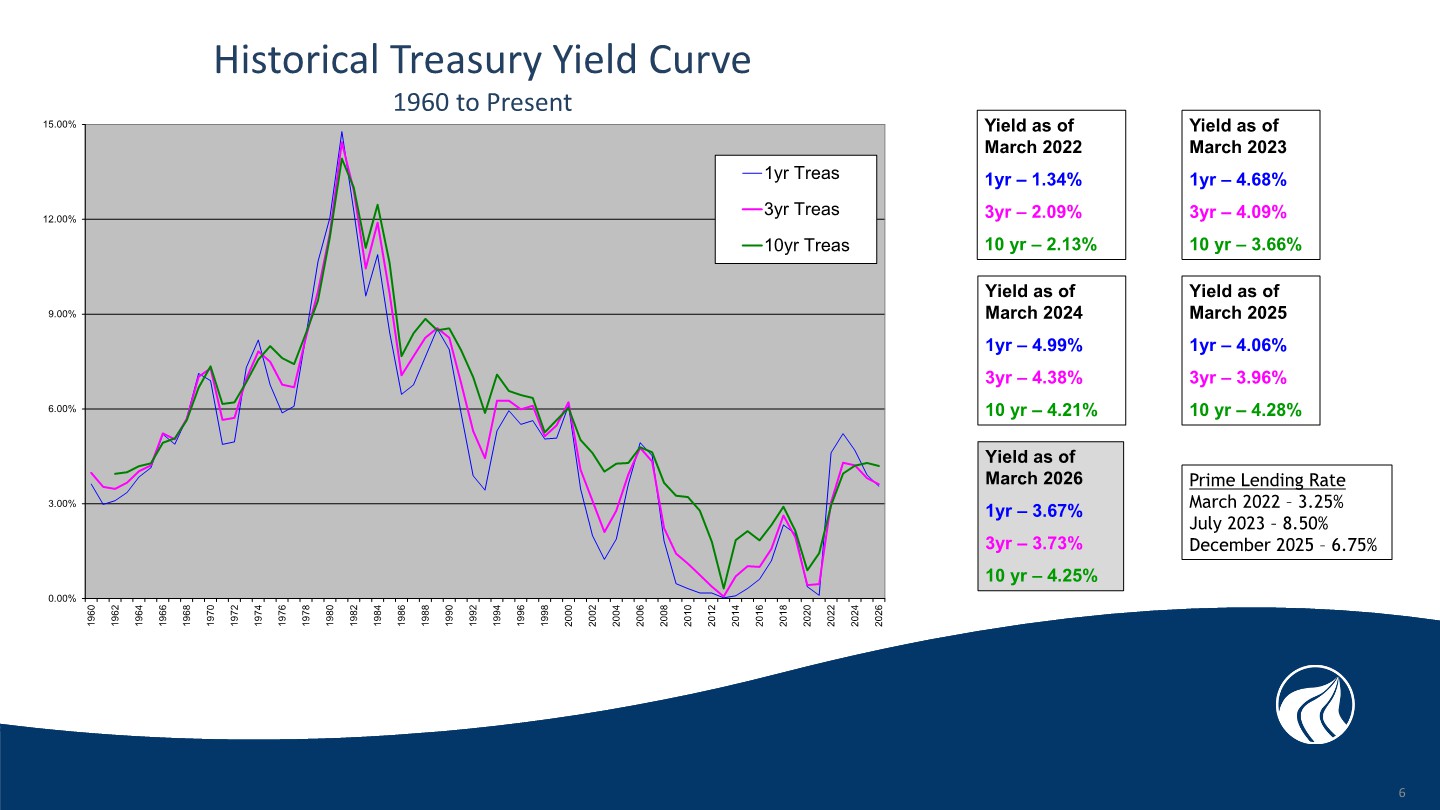

Historical Treasury Yield Curve 1960 to Present Yield as of March 2025 1yr – 4.06% 3yr – 3.96% 10 yr – 4.28% Yield as of March 2024 1yr – 4.99% 3yr – 4.38% 10 yr – 4.21% Yield as of March 2023 1yr – 4.68% 3yr – 4.09% 10 yr – 3.66% Yield as of March 2022 1yr – 1.34% 3yr – 2.09% 10 yr – 2.13% Prime Lending Rate March 2022 – 3.25% July 2023 – 8.50% December 2025 – 6.75% 0.00% 3.00% 6.00% 9.00% 12.00% 15.00% 1960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 1yr Treas 3yr Treas 10yr Treas Yield as of March 2026 1yr – 3.67% 3yr – 3.73% 10 yr – 4.25% 6

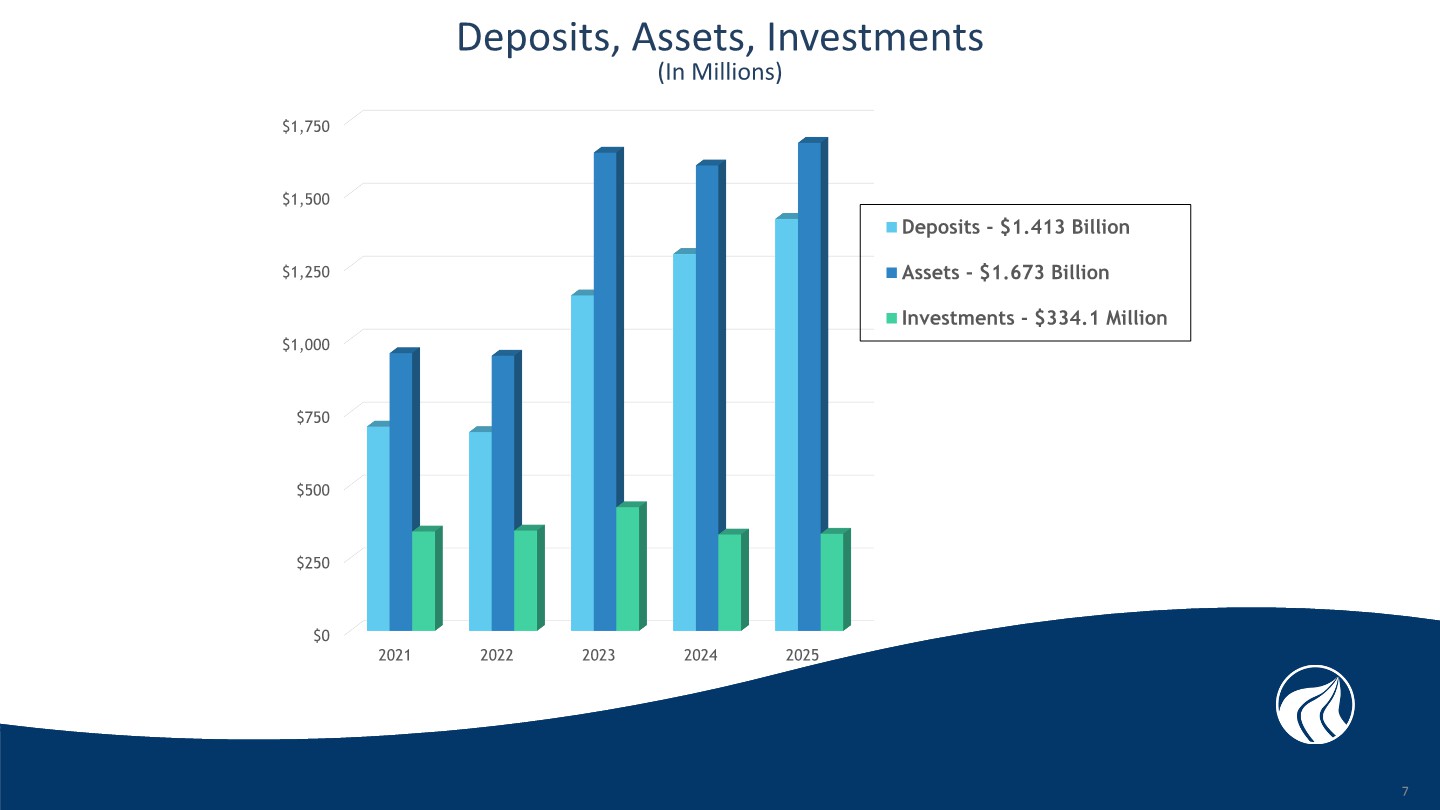

Deposits, Assets, Investments (In Millions) $0 $250 $500 $750 $1,000 $1,250 $1,500 $1,750 2021 2022 2023 2024 2025 Deposits - $1.413 Billion Assets - $1.673 Billion Investments - $334.1 Million 7

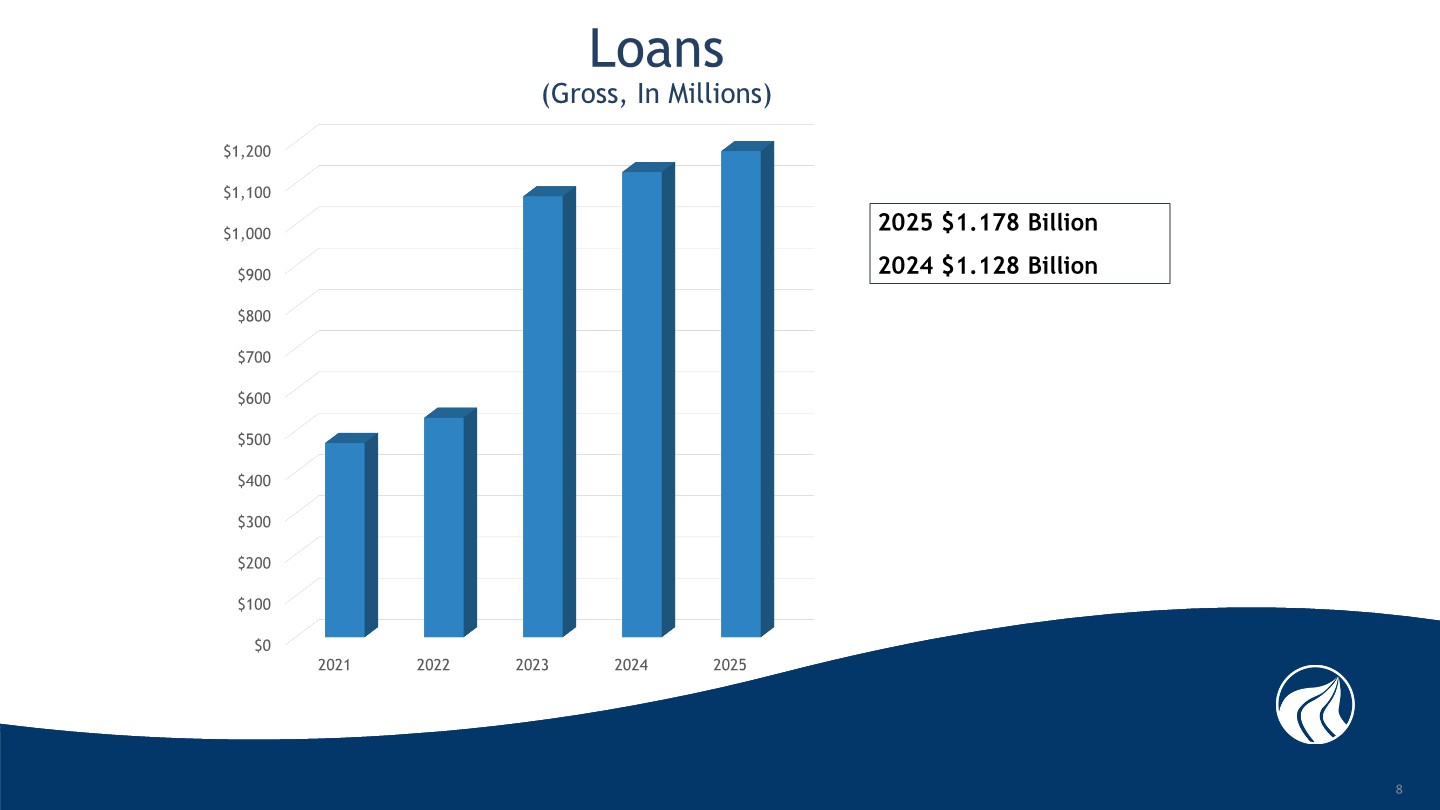

Loans (Gross, In Millions) $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 $1,100 $1,200 2021 2022 2023 2024 2025 2025 $1.178 Billion 2024 $1.128 Billion 8

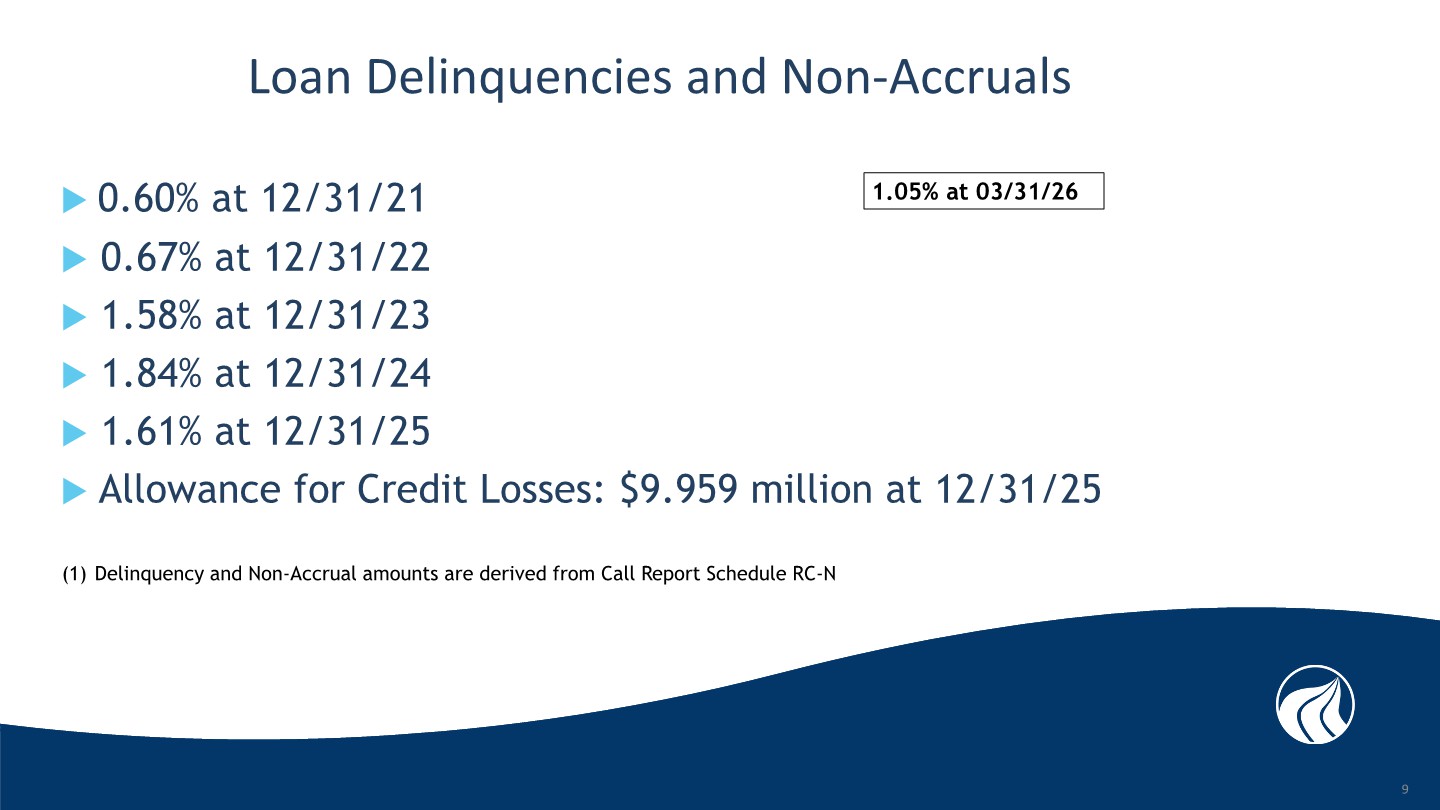

0.60% at 12/31/21 0.67% at 12/31/22 1.58% at 12/31/23 1.84% at 12/31/24 1.61% at 12/31/25 Allowance for Credit Losses: $9.959 million at 12/31/25 Loan Delinquencies and Non - Accruals 9 1.05% at 03/31/26 (1) Delinquency and Non - Accrual amounts are derived from Call Report Schedule RC - N

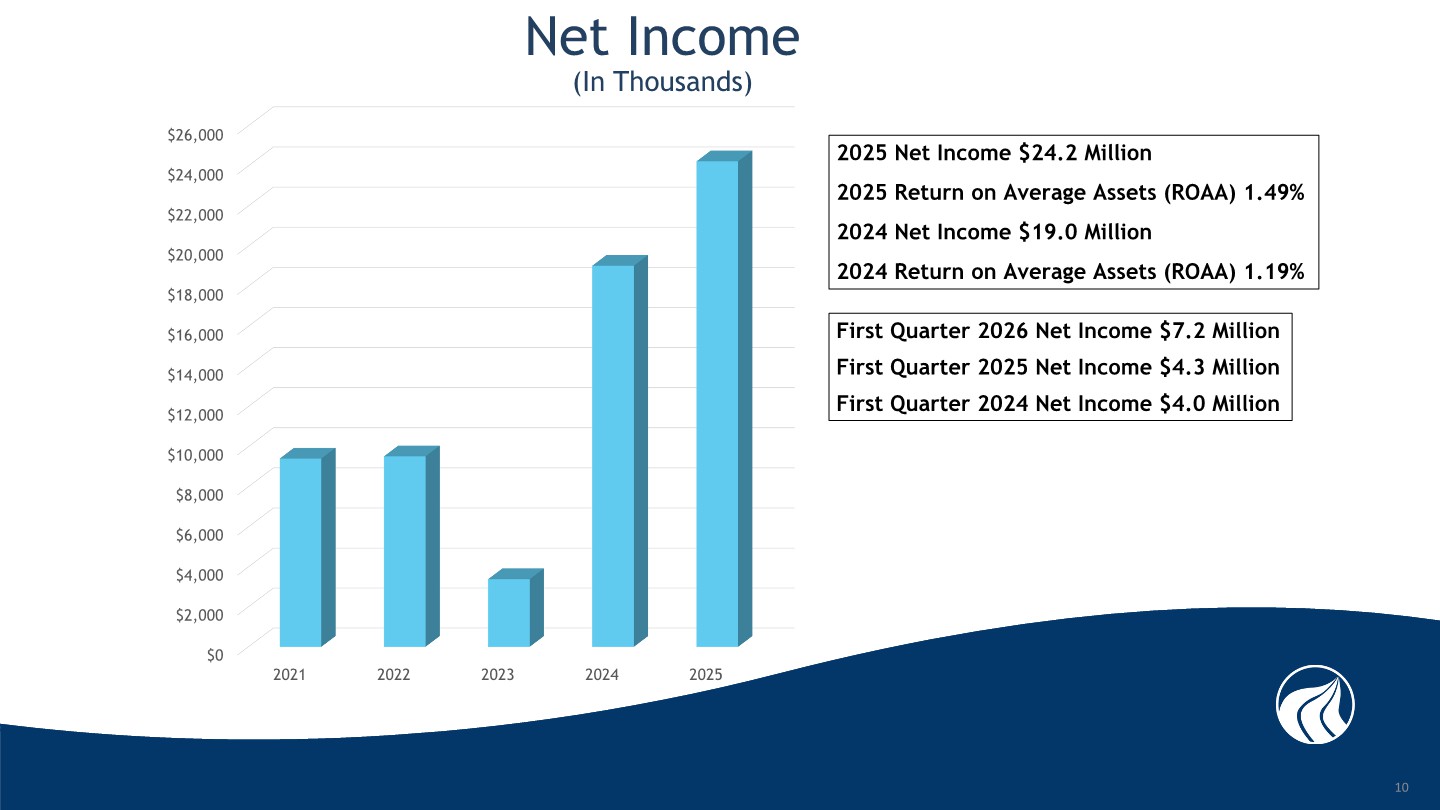

Net Income (In Thousands) $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000 $20,000 $22,000 $24,000 $26,000 2021 2022 2023 2024 2025 2025 Net Income $24.2 Million 2025 Return on Average Assets (ROAA) 1.49% 2024 Net Income $19.0 Million 2024 Return on Average Assets (ROAA) 1.19% First Quarter 2026 Net Income $7.2 Million First Quarter 2025 Net Income $4.3 Million First Quarter 2024 Net Income $4.0 Million 10

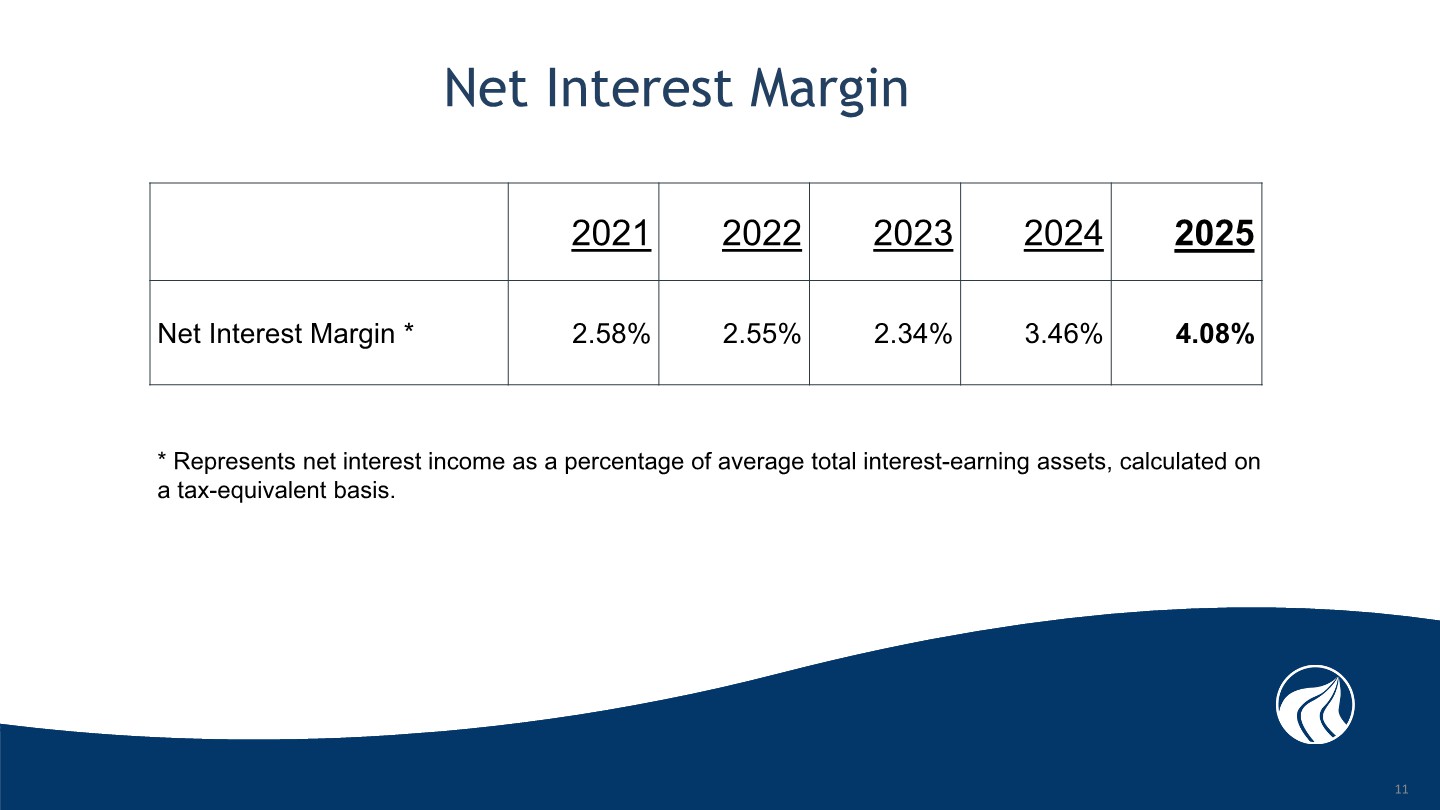

Net Interest Margin 2025 2024 2023 2022 2021 4.08% 3.46% 2.34% 2.55% 2.58% Net Interest Margin * * Represents net interest income as a percentage of average total interest - earning assets, calculated on a tax - equivalent basis. 11

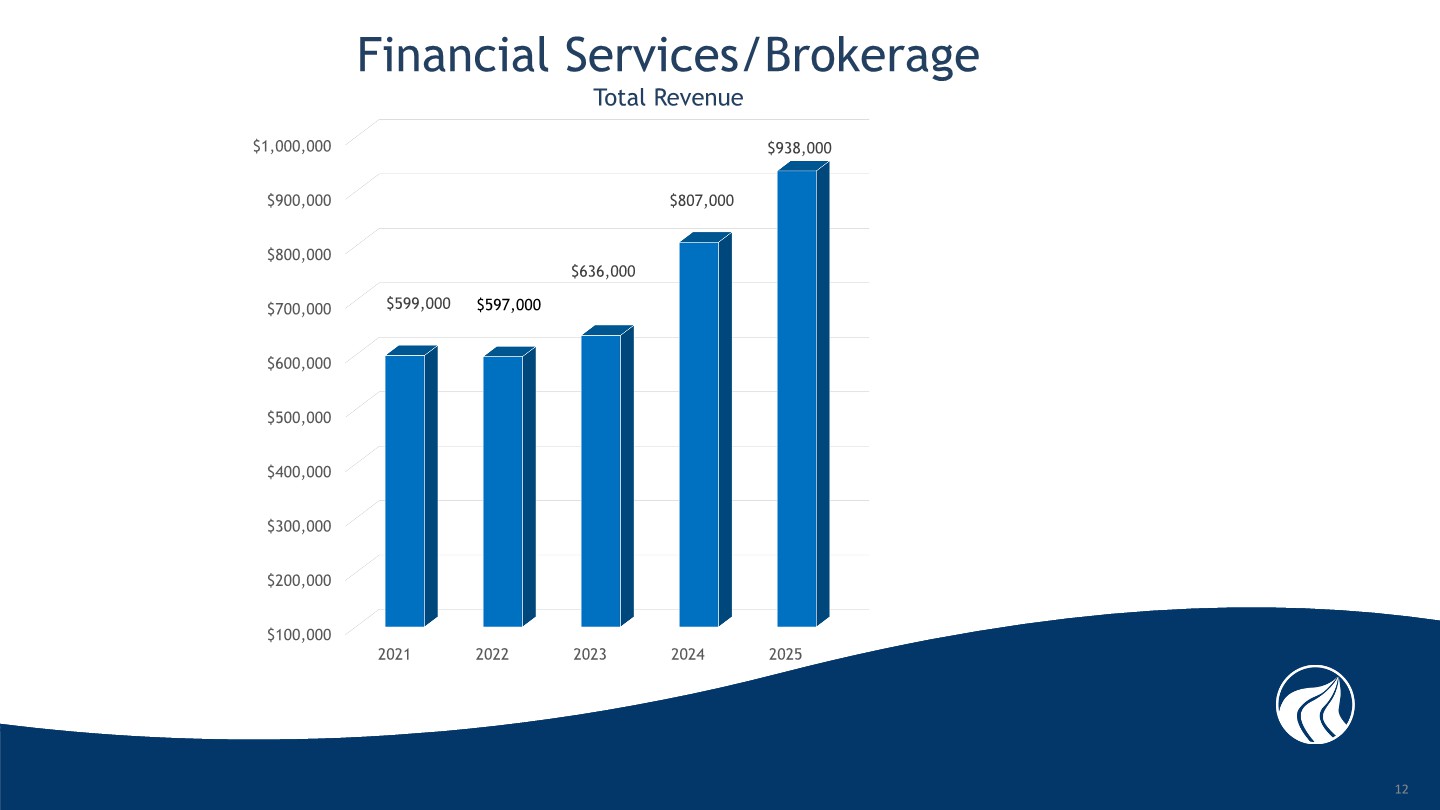

Financial Services/Brokerage Total Revenue $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 $900,000 $1,000,000 2021 2022 2023 2024 2025 $599,000 $597,000 $ 636,000 $ 807,000 $ 938,000 12

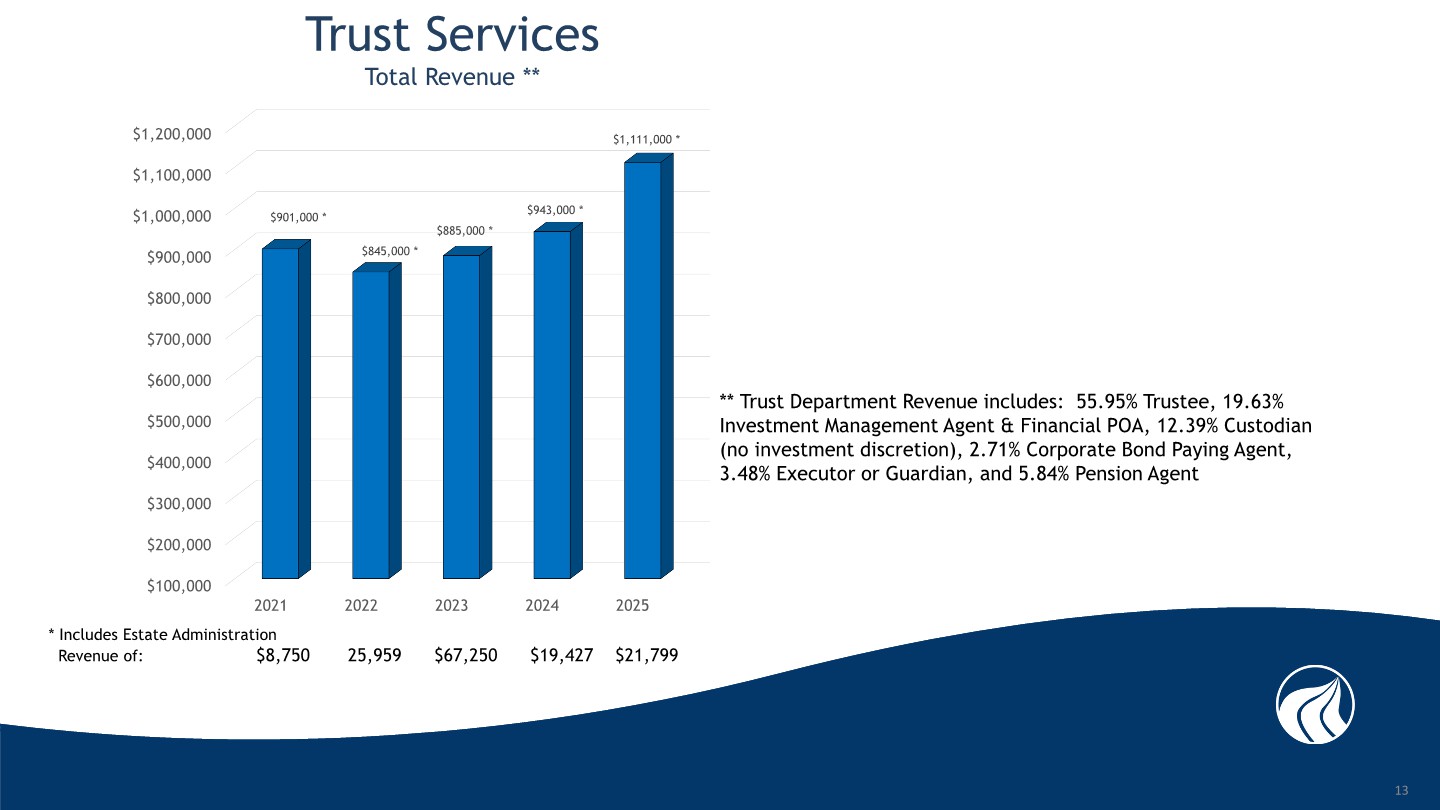

Trust Services Total Revenue ** $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 $900,000 $1,000,000 $1,100,000 $1,200,000 2021 2022 2023 2024 2025 $901,000 * $845,000 * $885,000 * $943,000 * $1,111,000 * * Includes Estate Administration Revenue of: $8,750 25,959 $67,250 $19,427 $21,799 ** Trust Department Revenue includes: 55.95% Trustee, 19.63% Investment Management Agent & Financial POA, 12.39% Custodian (no investment discretion), 2.71% Corporate Bond Paying Agent, 3.48% Executor or Guardian, and 5.84% Pension Agent 13

Stockholders’ Equity (In Millions) $0 $20 $40 $60 $80 $100 $120 $140 $160 $180 $200 2021 2022 2023 2024 2025 Equity $192.5 Million Total Equity before AOCI $196.6 Million 14

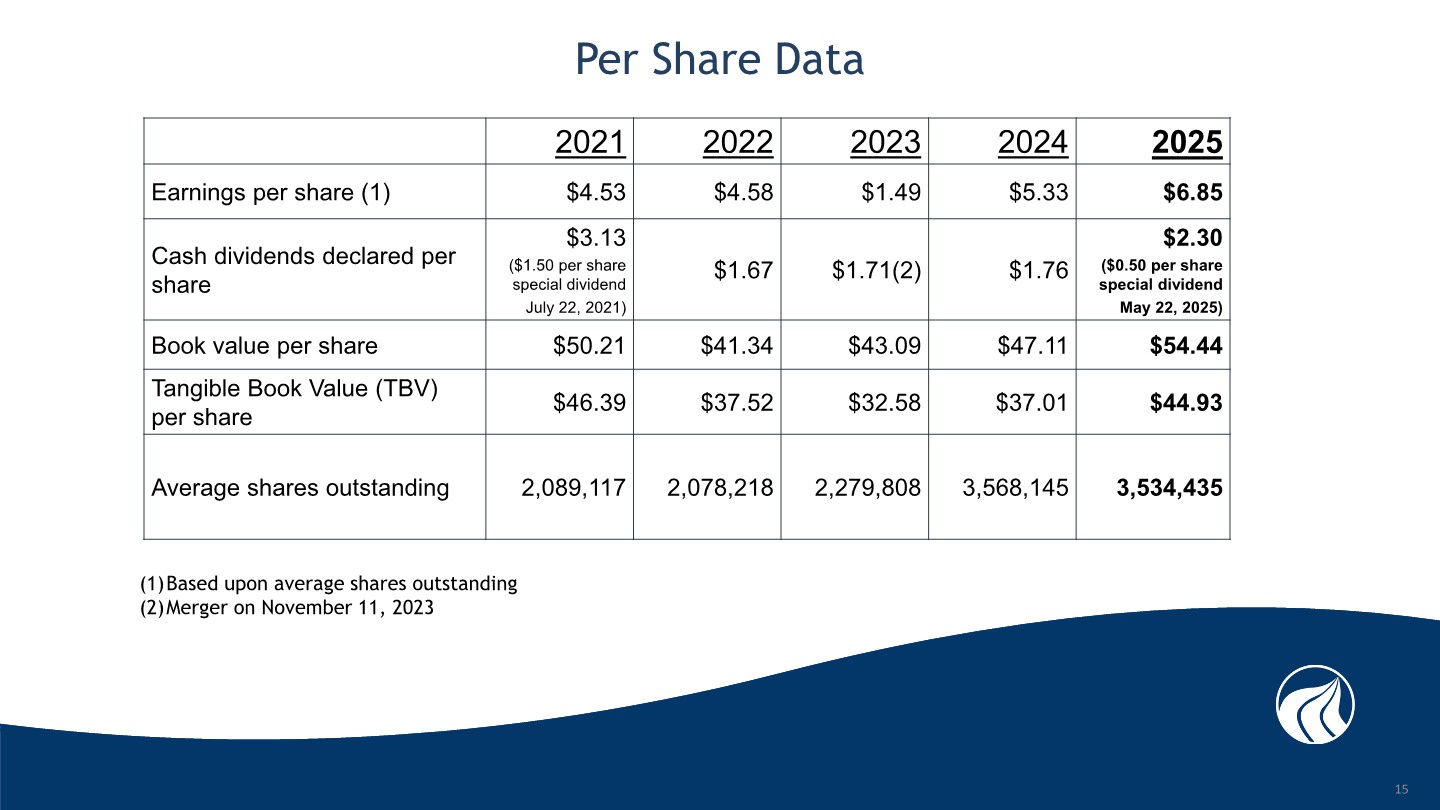

Per Share Data 2025 2024 2023 2022 2021 $6.85 $5.33 $1.49 $4.58 $4.53 Earnings per share (1) $2.30 ($0.50 per share special dividend May 22, 2025) $1.76 $1.71(2) $1.67 $3.13 ($1.50 per share special dividend July 22, 2021) Cash dividends declared per share $54.44 $47.11 $43.09 $41.34 $50.21 Book value per share $44.93 $37.01 $32.58 $37.52 $46.39 Tangible Book Value (TBV) per share 3,534,435 3,568,145 2,279,808 2,078,218 2,089,117 Average shares outstanding (1) Based upon average shares outstanding (2) Merger on November 11, 2023 15

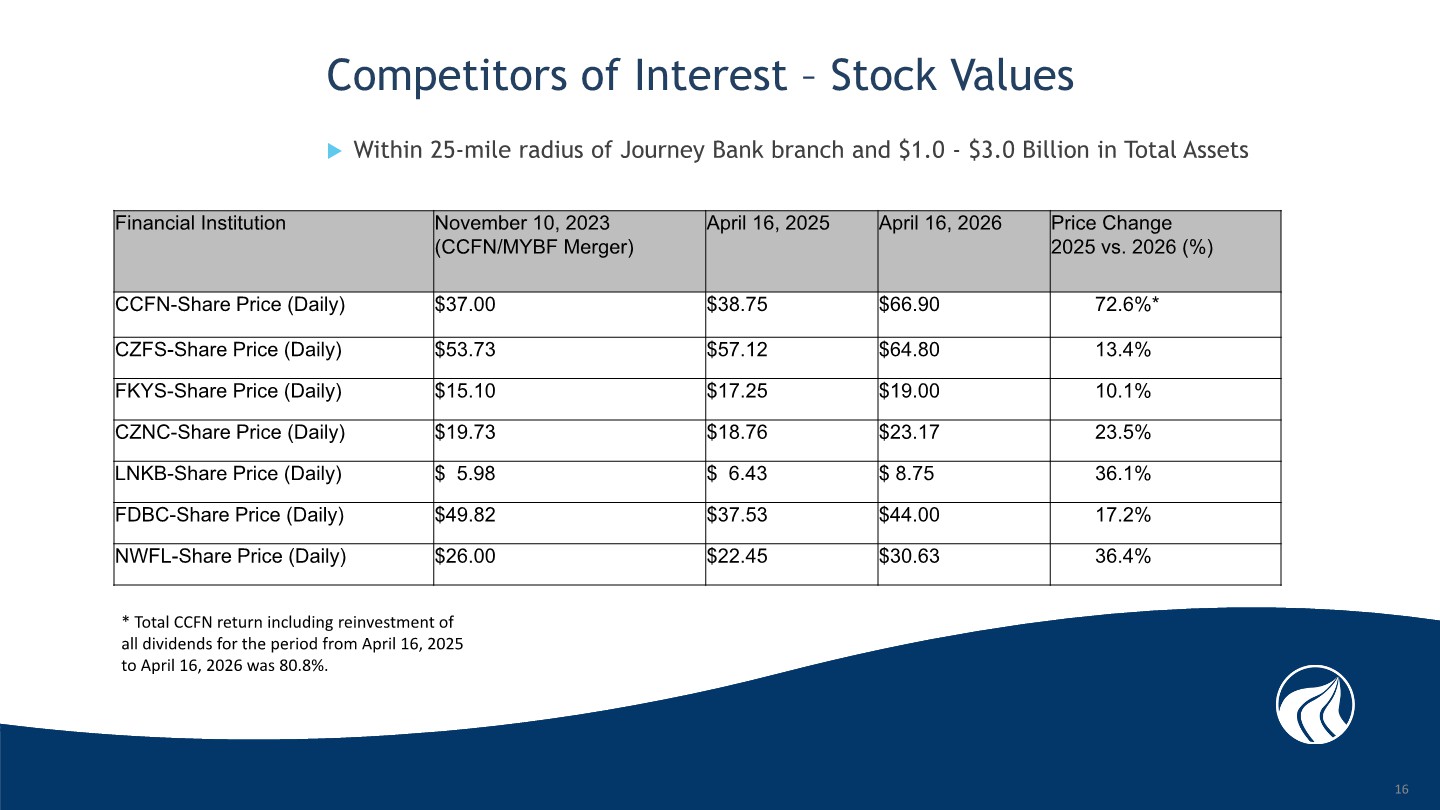

Competitors of Interest – Stock Values Within 25 - mile radius of Journey Bank branch and $1.0 - $3.0 Billion in Total Assets Price Change 2025 vs. 2026 (%) April 16, 2026 April 16, 2025 November 10, 2023 (CCFN/MYBF Merger) Financial Institution 72.6%* $66.90 $38.75 $37.00 CCFN - Share Price (Daily) 13.4% $64.80 $57.12 $53.73 CZFS - Share Price (Daily) 10.1% $19.00 $17.25 $15.10 FKYS - Share Price (Daily) 23.5% $23.17 $18.76 $19.73 CZNC - Share Price (Daily) 36.1% $ 8.75 $ 6.43 $ 5.98 LNKB - Share Price (Daily) 17.2% $44.00 $37.53 $49.82 FDBC - Share Price (Daily) 36.4% $30.63 $22.45 $26.00 NWFL - Share Price (Daily) 16 * Total CCFN return including reinvestment of all dividends for the period from April 16, 2025 to April 16, 2026 was 80.8%.

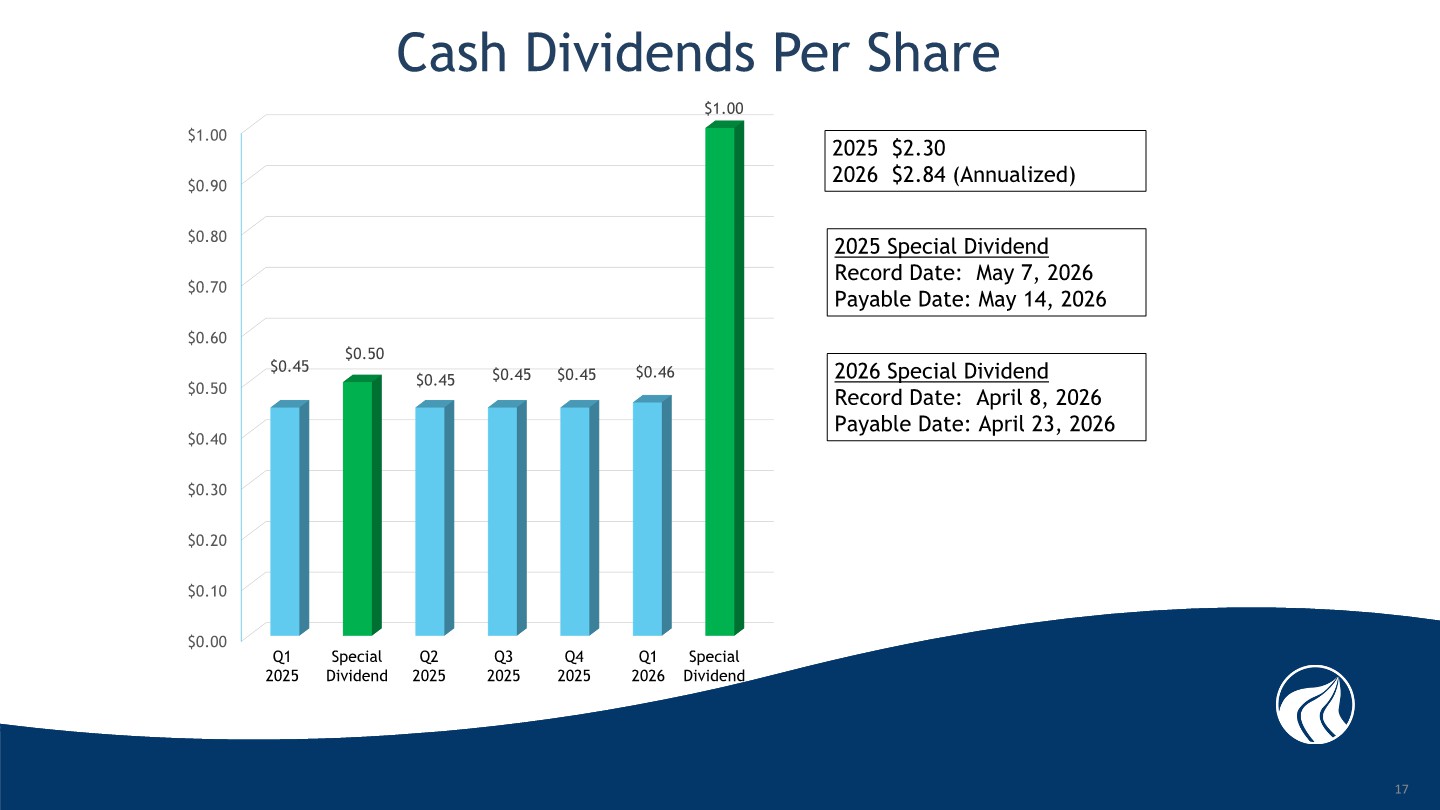

Cash Dividends Per Share $0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00 $0.45 $0.50 $0.45 $0.45 $0.45 $0.46 $1.00 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Special Dividend Special Dividend Q1 2025 2025 $2.30 2026 $2.84 (Annualized) 2025 Special Dividend Record Date: May 7, 2026 Payable Date: May 14, 2026 2026 Special Dividend Record Date: April 8, 2026 Payable Date: April 23, 2026 17

Three - For - One Stock Split This morning, the Board of Directors approved and declared a three - for - one stock split in the form of a 200% stock dividend on its outstanding shares of common stock. Each shareholder of record as of the close of business on May 7, 2026, will receive two additional shares of Company common stock for each share then held, to be distributed after the close of business on May 14, 2026. Based on the number of shares currently outstanding, the Company will have 10,612,227 shares of common stock issued and outstanding, net of treasury shares, on a split - adjusted basis. 18

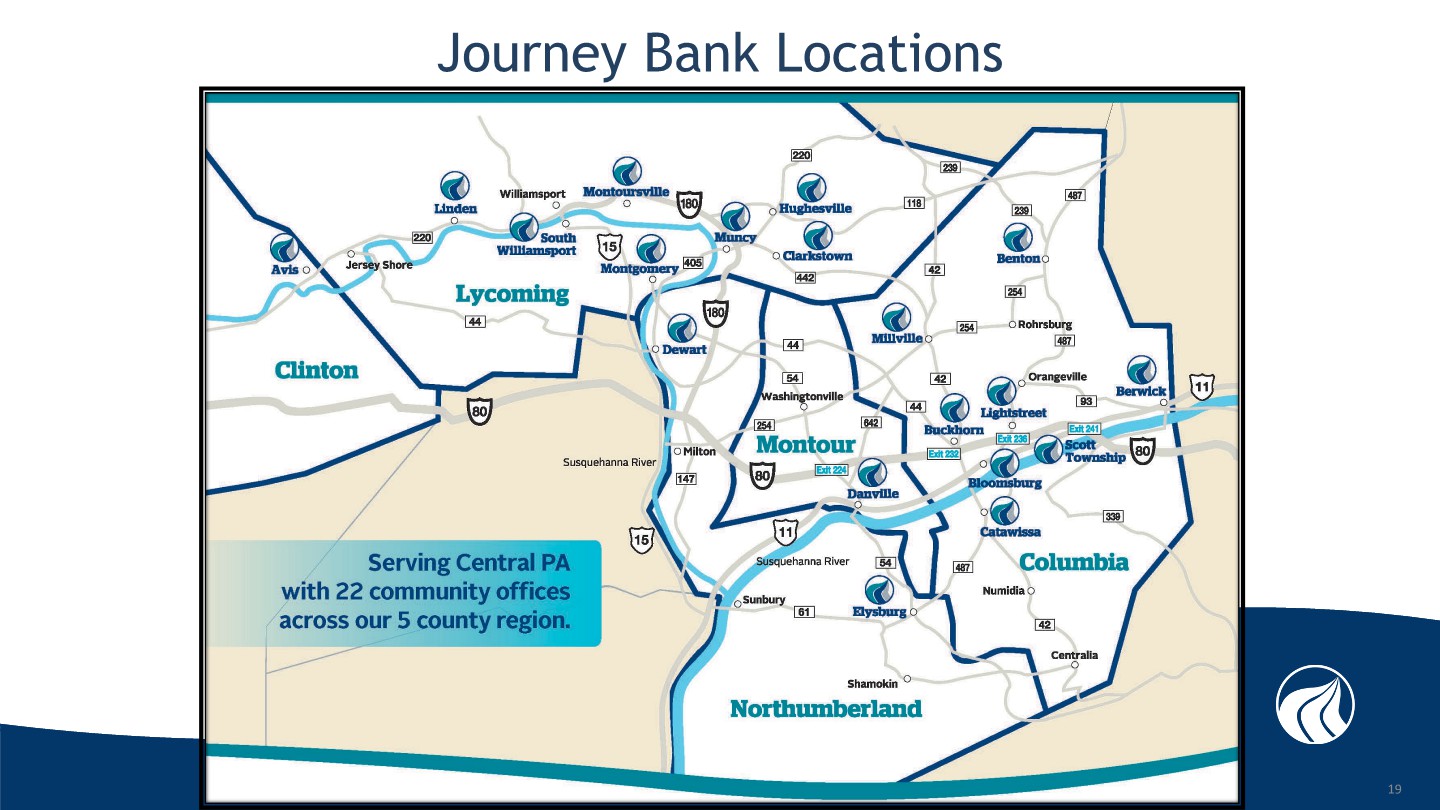

Journey Bank Locations 19

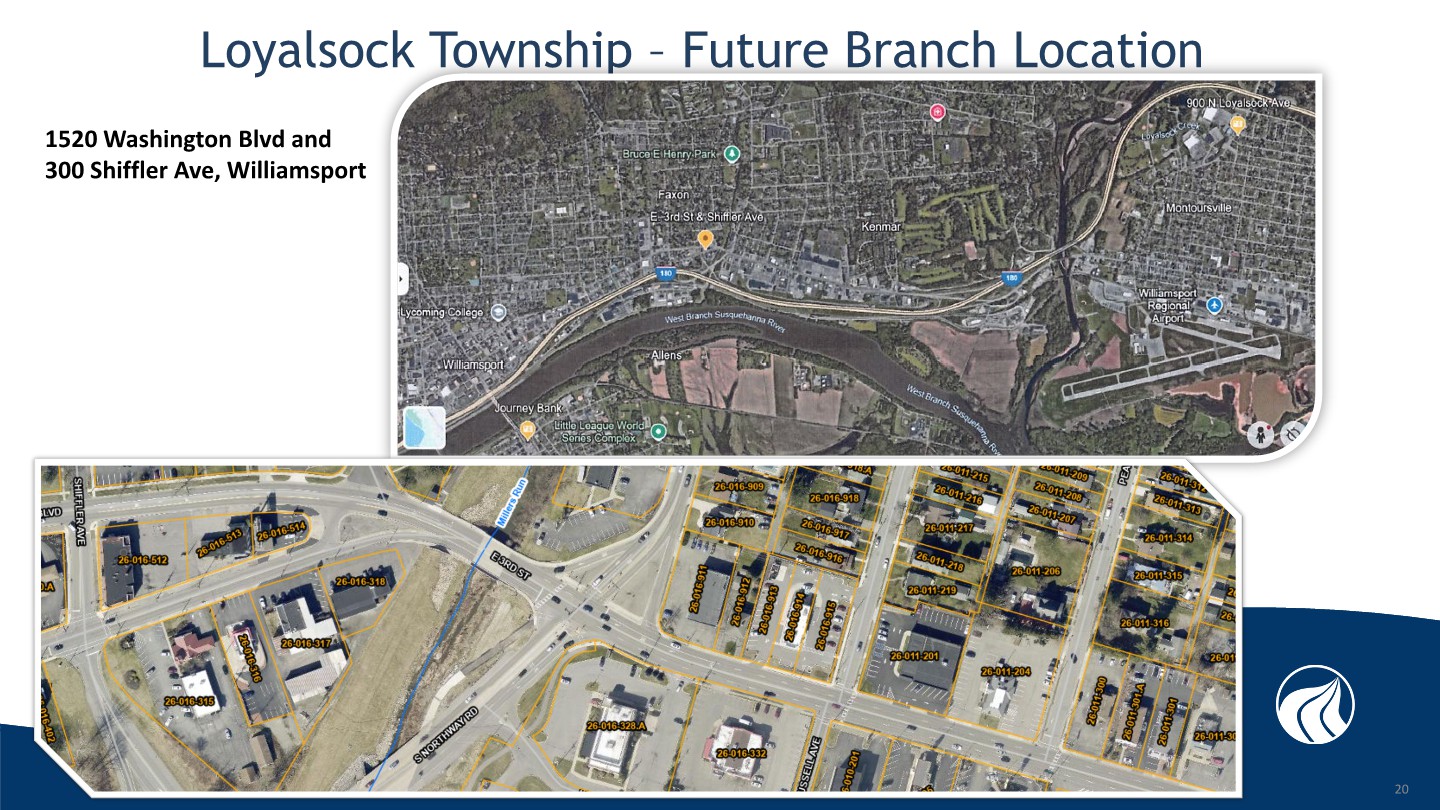

Loyalsock Township – Future Branch Location 20 1520 Washington Blvd and 300 Shiffler Ave, Williamsport

Signature Event – Journey Bank Teen Star Musical Competition 16 Continuous Years 221 Finalists $75,000 in Prize Money $56,000 to Local High School Music Departments Sunday, April 26 th at 2:00 PM Haas Auditorium Commonwealth University – Bloomsburg Tickets $5 in advance; $7 at door 21

Journey Bank Ballpark At Historic Bowman Field 22

Journey Bank Community Arts Center 23

Chris Herren Addiction / Resilience / Recovery 16 Schools (approximately 9,000 students ) Bloomsburg Fairgrounds Public Presentation on March 12, 2026 Future presentation at Journey Bank Community Arts Center on October 29 , 2026 24

Director Retirement Robert Rabb 04/22/2025 – 04/22/2026 Previously 09/12/1989 – 02/13/2024 35 years 25

Senior Management Retirement Tammy L. Gunsallus Senior Executive Vice President of Retail, Operations and Mortgage 2016 - 12/31/2025 43 year banking career 26

Executive Leadership Team 27

Jeffrey T. Arnold Senior EVP and Chief Operating and Risk Officer » Increasing Reliance on Third - Party Vendors • Limit speed to market on new products and digital abilities • Elevates oversight risk • Mitigation Efforts » Fraud • Increased risk in traditional banking products • AI improved Social Engineering abilities • 2025 Statistics • Mitigation Efforts 28

» Provide non - FDIC Insured Investments: • Mutual Funds, Stocks, Annuities, Life Insurance, and Financial Planning » Team of four advisors with two administrators, with advisor - ready customer service » Investment Center Progress • Grown from a commission - based revenue roller coaster to recurring revenue fiduciary model » Most popular products: • Fixed Annuities, MultiSector Bond Mutual Funds, Long Term Care Hybrid Policies » It’s YOUR money, not OUR money. We outline the benefits and drawbacks of each option for your decision. Matthew E. Beagle EVP and Chief Wealth Management Officer 29

Jason A. Fischer EVP and Chief Credit Officer » Responsible for the overall credit risk health of the bank • Oversee approval process & loan committee • Monitor health of the loan portfolio • Ensure compliance • Balance independence with lender partnerships • “Are we taking the right risks – and managing them well?” » Challenges • Maintain low Past Due & Non - Accruals levels • Commercial Real Estate Risk Exposure • Balancing credit growth while tightening underwriting standards » Opportunities in AI » Overall Credit Quality Remains Strong 30

» Responsibilities Accelerate growth across departments by aligning data analysis, marketing strategy, and customer engagement for the good of our bank and the communities we serve. » Market Realities Competition intensifying • Customer interactions evolving • Digital standards rising » Strategic Evolution Enhanced customer experience • Digital - first delivery adaptation • Data - driven decisions » Growth Priorities Deepen community relationships • Strengthen our trust & brand • Expand targeted products, services & markets • Leverage digital tools to improve reach and efficiency Loni N. Kline EVP and Chief Growth Officer 31

Jessica M. Lehman EVP and Trust Director » Responsibilities: • Administer Trusts/Estates • Manage Investment Accounts and Self - Directed IRAs • Orchestrate Scholarship Fund Distributions • Ensure proper administration of assets when Financial Power of Attorney » Challenges: • Educating the public on what Trust can do for them • Opening dialog on what Trusts are and how they are used • Antiquated Charlotte processing software » Opportunities: • Increase accessibility • Hold seminars/education • Ensure exceptional service for existing clients » Changes: • Trust Policy changes to encourage efficiency • Vetting new Trust Management Software • Streamline processes to allow Trust Officers to be more available for clients 32

Stephanie A. Oakes EVP and Chief Operations Officer » Information Technology (IT), Deposit Operations, E - Banking, Commercial Services, & Customer Support » Challenges » Evolving Threats » Artificial Intelligence, Social Engineering, Employee Awareness » Evolving Technology » Costs, Security, Balance, Speed, Competitive Advantage » Opportunities » Artificial Intelligence » Speed and efficiencies » Digital Growth » Multiple platform integrations, remote signature capabilities, financial education and wellness. Security and fraud prevention » Balance - Technology when you want it, people when you don’t 33

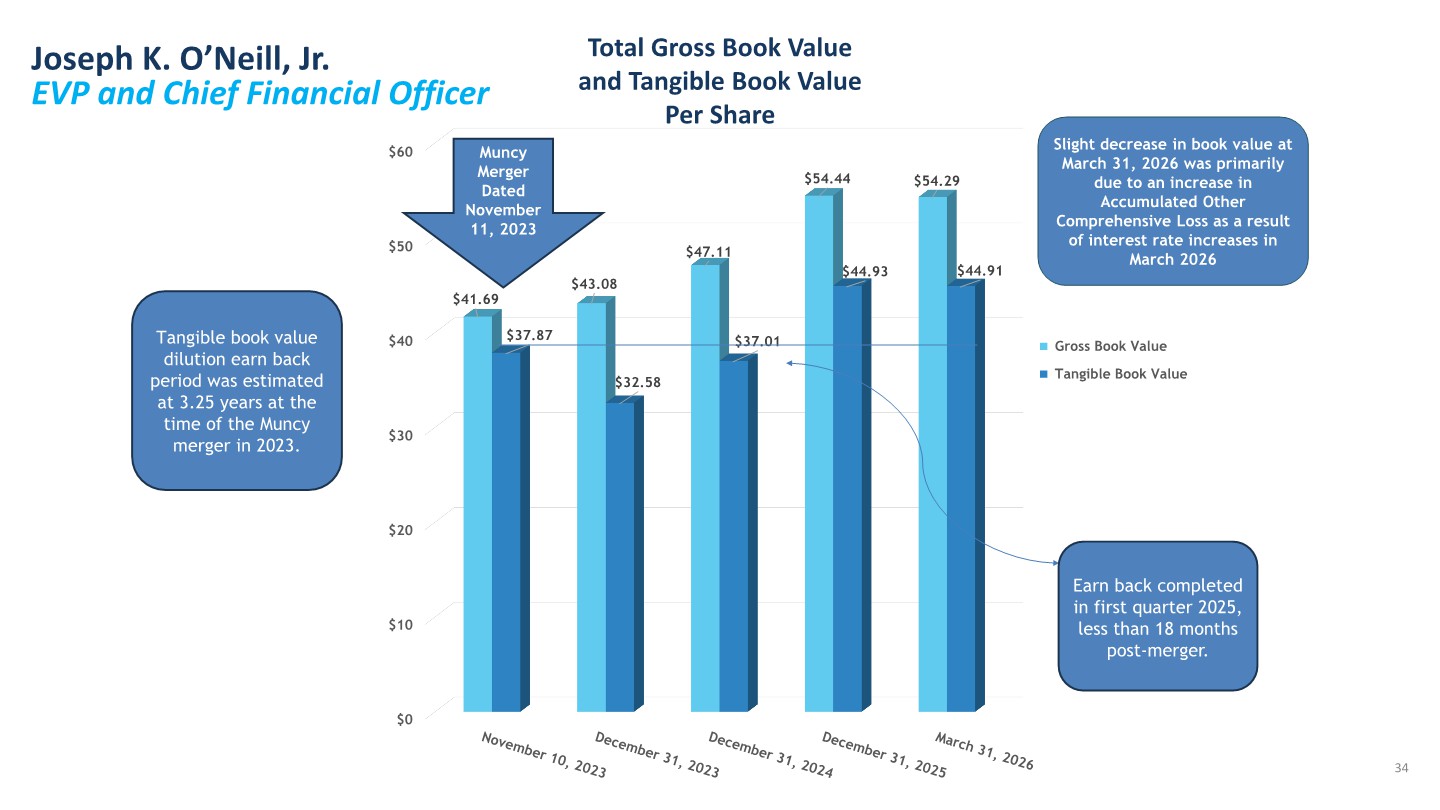

Joseph K. O’Neill, Jr. EVP and Chief Financial Officer $0 $10 $20 $30 $40 $50 $60 $41.69 $43.08 $47.11 $54.44 $54.29 $37.87 $32.58 $37.01 $44.93 $44.91 Gross Book Value Tangible Book Value Muncy Merger Dated November 11, 2023 Tangible book value dilution earn back period was estimated at 3.25 years at the time of the Muncy merger in 2023. Earn back completed in first quarter 2025, less than 18 months post - merger. Slight decrease in book value at March 31, 2026 was primarily due to an increase in Accumulated Other Comprehensive Loss as a result of interest rate increases in March 2026 Total Gross Book Value and Tangible Book Value Per Share 34

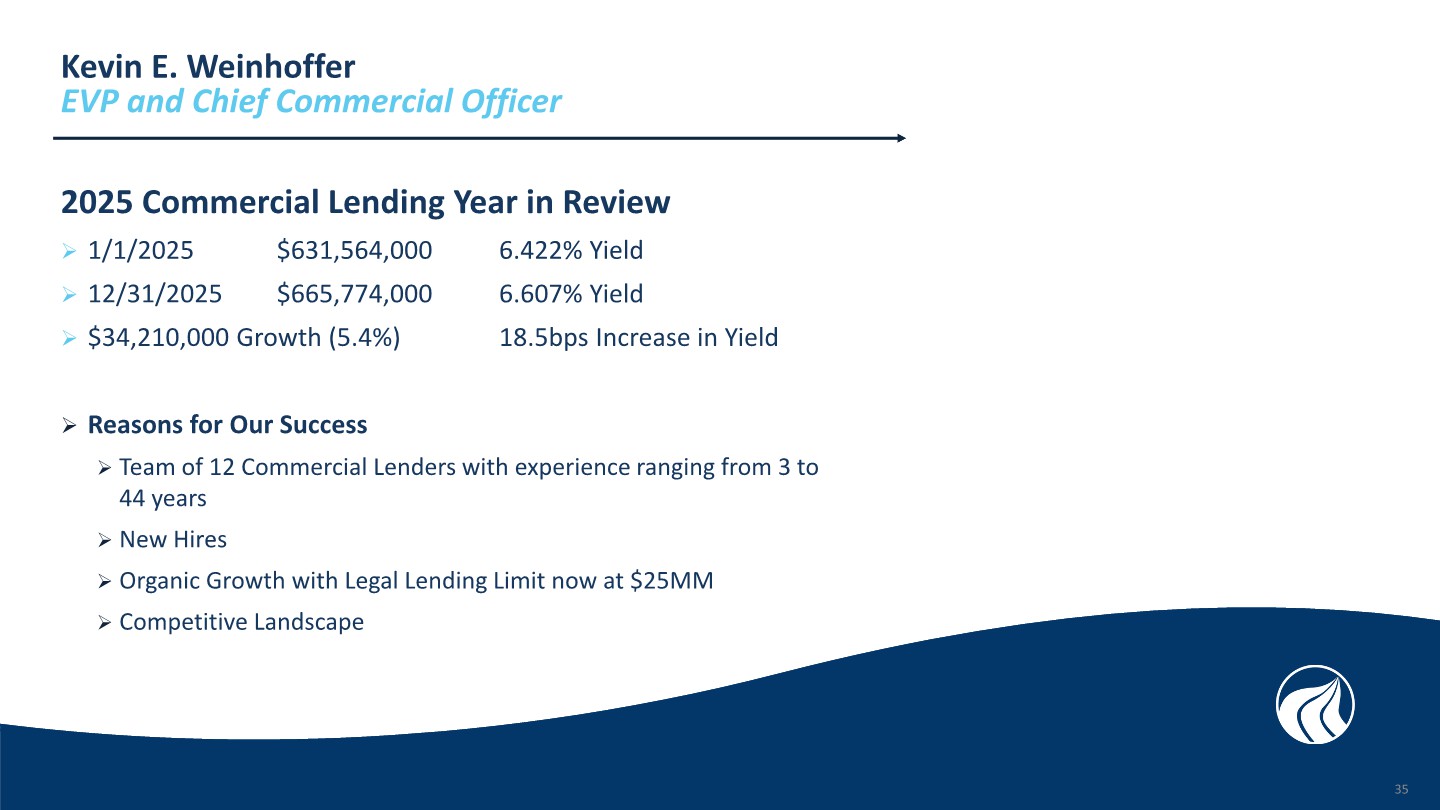

Kevin E. Weinhoffer EVP and Chief Commercial Officer 2025 Commercial Lending Year in Review » 1/1/2025 $631,564,000 6.422% Yield » 12/31/2025 $665,774,000 6.607% Yield » $34,210,000 Growth (5.4%) 18.5bps Increase in Yield » Reasons for Our Success » Team of 12 Commercial Lenders with experience ranging from 3 to 44 years » New Hires » Organic Growth with Legal Lending Limit now at $25MM » Competitive Landscape 35

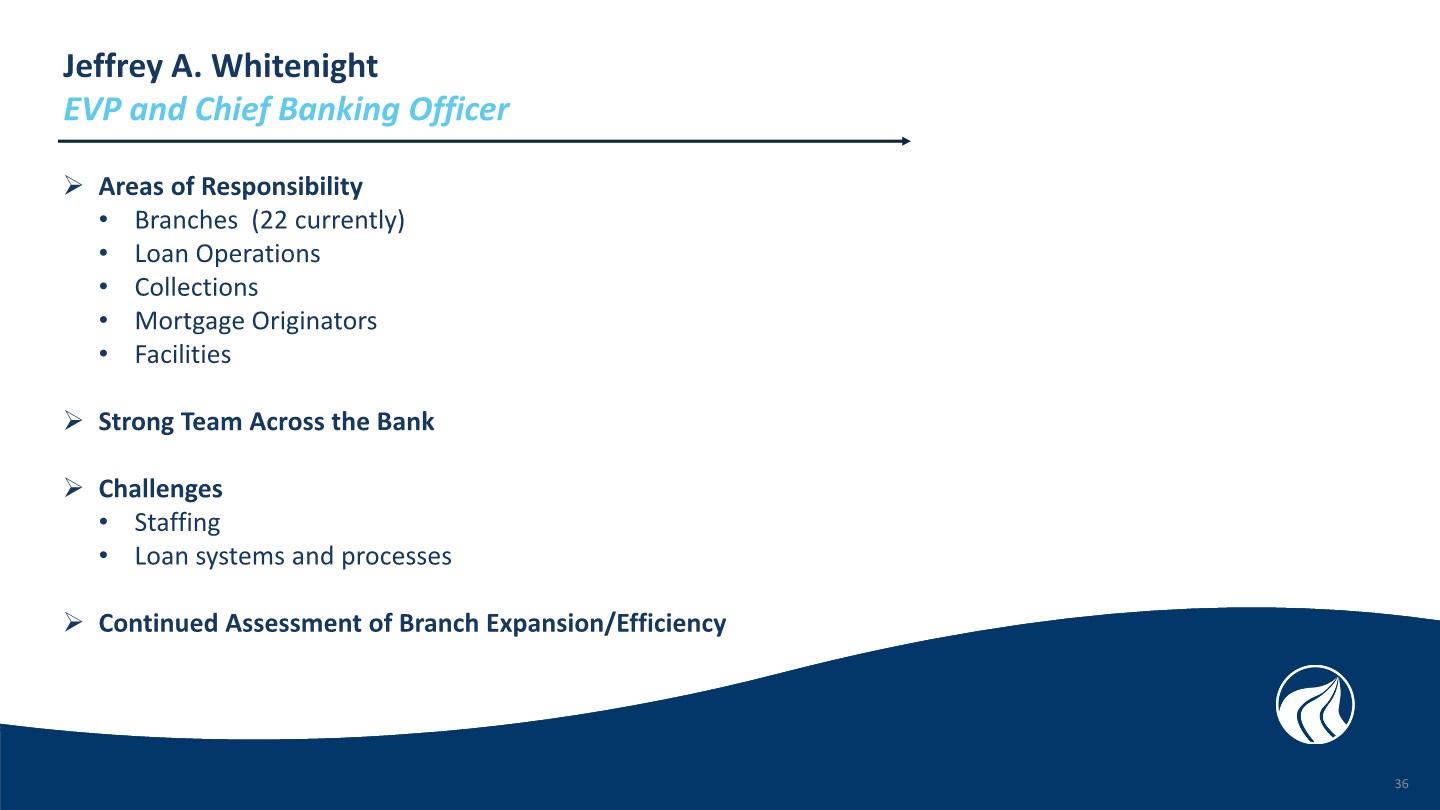

Jeffrey A. Whitenight EVP and Chief Banking Officer » Areas of Responsibility • Branches (22 currently) • Loan Operations • Collections • Mortgage Originators • Facilities » Strong Team Across the Bank » Challenges • Staffing • Loan systems and processes » Continued Assessment of Branch Expansion/Efficiency 36

Questions? 37

Thank you for attending the 2026 Annual Meeting of Shareholders 38