NORTHWESTERN MUTUAL SERIES FUND, INC.

PROSPECTUS

| EQUITY PORTFOLIOS |

INTERNATIONAL PORTFOLIOS |

| GROWTH STOCK PORTFOLIO |

INTERNATIONAL GROWTH PORTFOLIO |

| FOCUSED APPRECIATION PORTFOLIO |

RESEARCH INTERNATIONAL CORE PORTFOLIO |

| LARGE CAP CORE STOCK PORTFOLIO |

INTERNATIONAL EQUITY PORTFOLIO |

| LARGE CAP BLEND PORTFOLIO |

EMERGING MARKETS EQUITY PORTFOLIO |

| INDEX 500 STOCK PORTFOLIO |

|

| LARGE COMPANY VALUE PORTFOLIO |

FIXED INCOME PORTFOLIOS |

| DOMESTIC EQUITY PORTFOLIO |

GOVERNMENT MONEY MARKET PORTFOLIO |

| EQUITY INCOME PORTFOLIO |

SHORT-TERM BOND PORTFOLIO |

| |

SELECT BOND PORTFOLIO |

| MID CAP GROWTH STOCK PORTFOLIO |

LONG-TERM U.S. GOVERNMENT BOND PORTFOLIO |

| INDEX 400 STOCK PORTFOLIO MID CAP VALUE PORTFOLIO |

INFLATION MANAGED PORTFOLIO (formerly Inflation Protection Portfolio) |

| |

HIGH YIELD BOND PORTFOLIO |

| SMALL CAP GROWTH STOCK PORTFOLIO |

MULTI-SECTOR BOND PORTFOLIO |

| INDEX 600 STOCK PORTFOLIO |

|

| SMALL CAP VALUE PORTFOLIO |

ACTIVE/PASSIVE ALLOCATION PORTFOLIOS |

| |

ACTIVE/PASSIVE VERY AGGRESSIVE PORTFOLIO (formerly Active/Passive All Equity Portfolio) |

| |

ACTIVE/PASSIVE AGGRESSIVE PORTFOLIO |

| |

ACTIVE/PASSIVE MODERATE PORTFOLIO (formerly Asset Allocation Portfolio) |

| |

ACTIVE/PASSIVE BALANCED PORTFOLIO (formerly Balanced Portfolio) |

| |

ACTIVE/PASSIVE CONSERVATIVE PORTFOLIO |

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

| |

Page |

| 1 | |

| 1 | |

| 4 | |

| 8 | |

| 11 | |

| 15 | |

| 19 | |

| 23 | |

| 26 | |

| 29 | |

| 32 | |

| 35 | |

| 39 | |

| 43 | |

| 46 | |

| 50 | |

| 54 | |

| 58 | |

| 62 | |

| 66 | |

| 69 | |

| 73 | |

| 77 | |

| 82 | |

| 86 | |

| 89 | |

| 94 | |

| 99 | |

| 105 | |

| 111 | |

| 117 | |

| 123 | |

| 123 | |

| 124 | |

| 124 | |

| 128 | |

| 149 | |

| 150 | |

| 151 | |

| 151 | |

| 151 | |

| 153 | |

| 157 | |

| 160 | |

| 160 |

i Northwestern Mutual Series Fund, Inc. Prospectus

| |

Page |

| 161 | |

| 161 | |

| 161 | |

| 161 | |

| 162 | |

| 162 | |

| 162 | |

| 163 | |

| 164 | |

| 164 | |

| 166 | |

| 171 |

Northwestern Mutual Series Fund, Inc. Prospectus ii

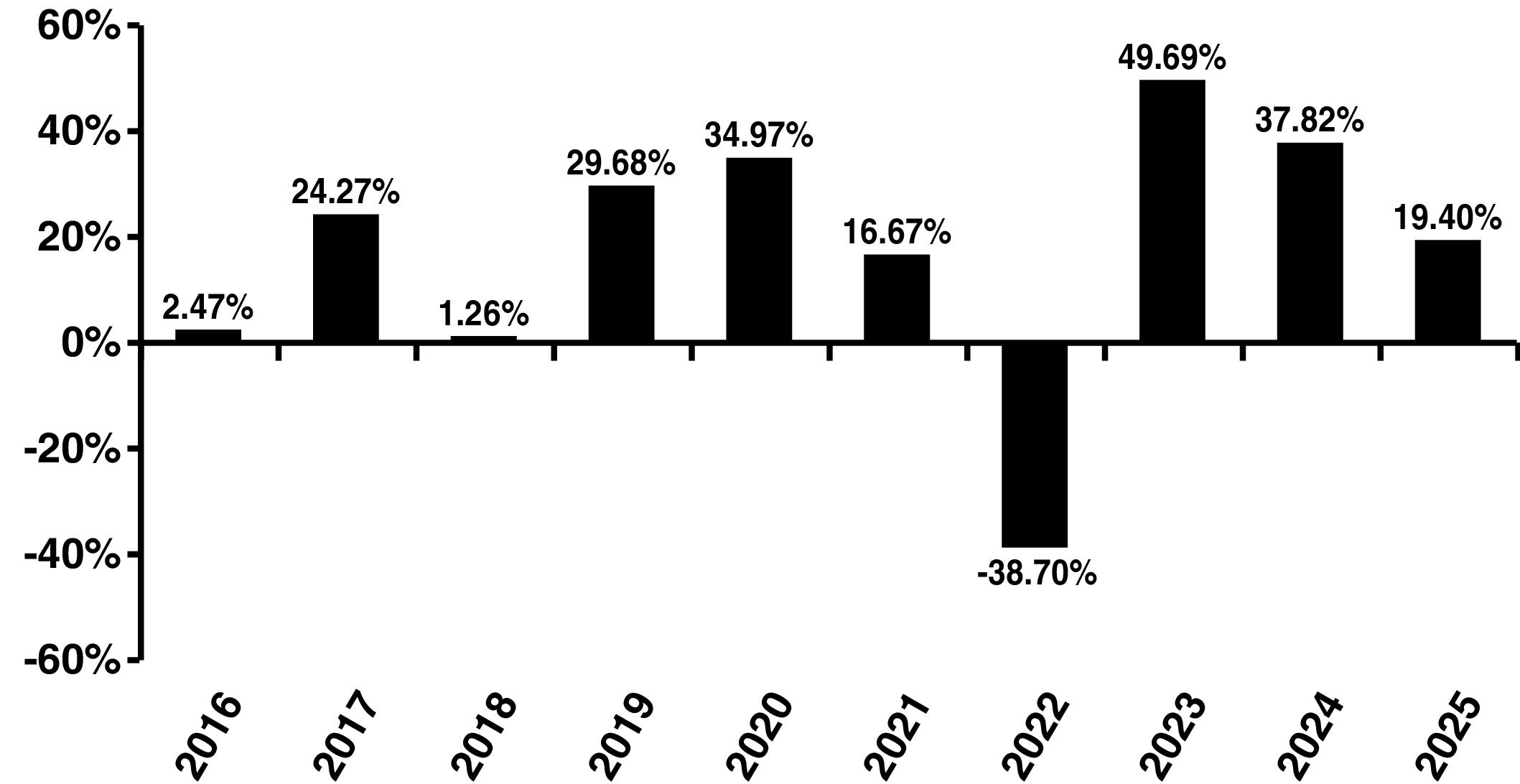

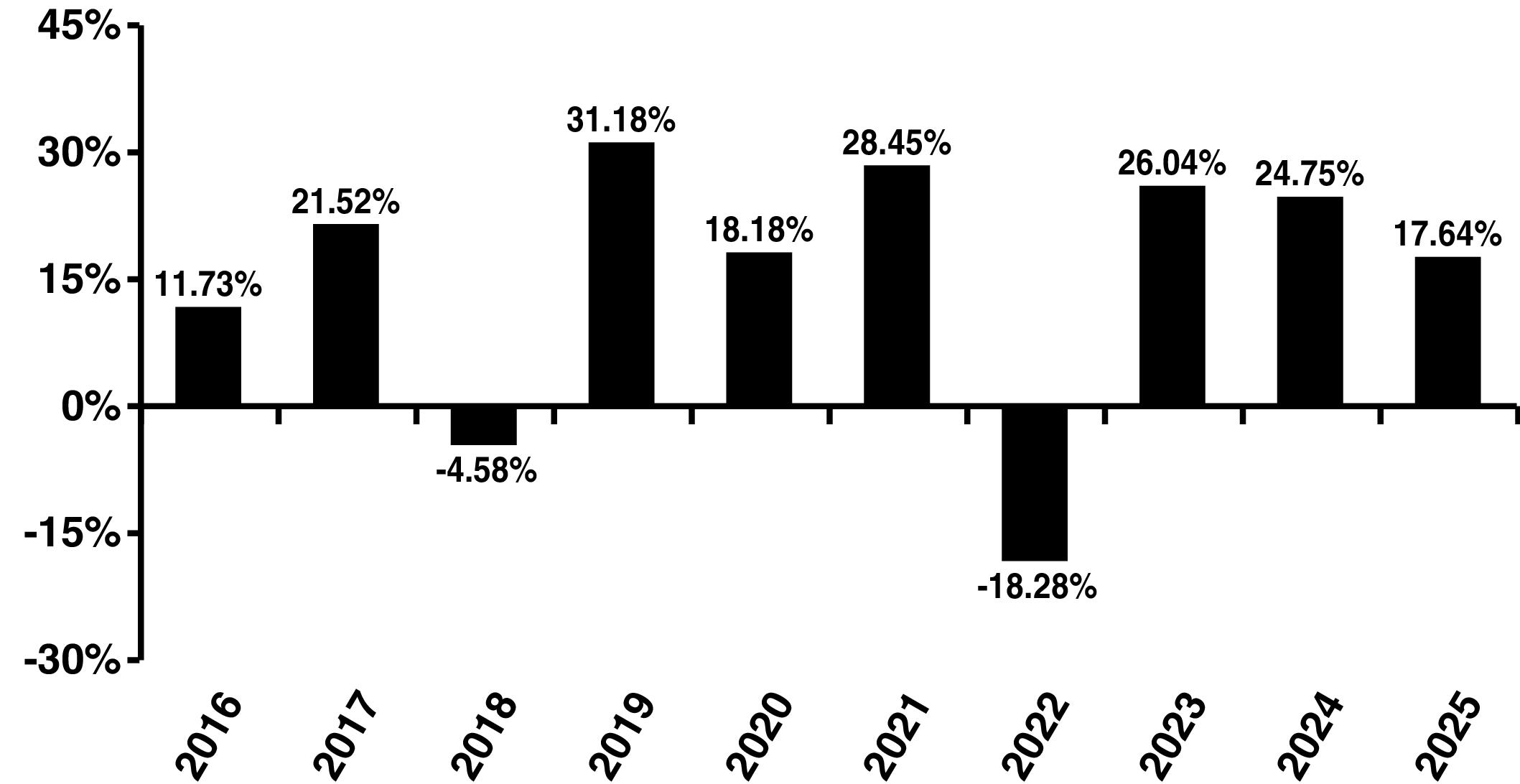

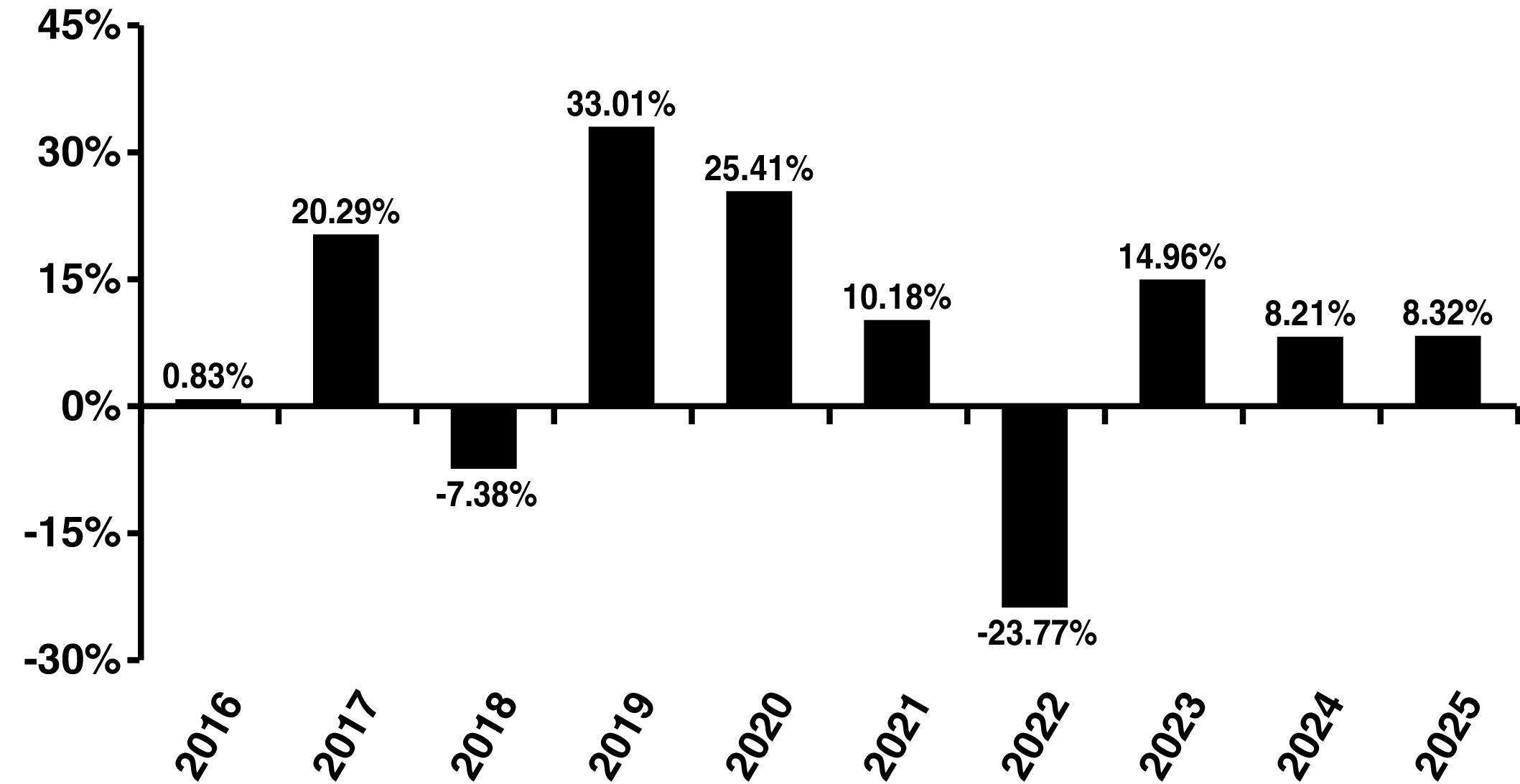

Growth Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

|

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

1 Northwestern Mutual Series Fund, Inc. Prospectus

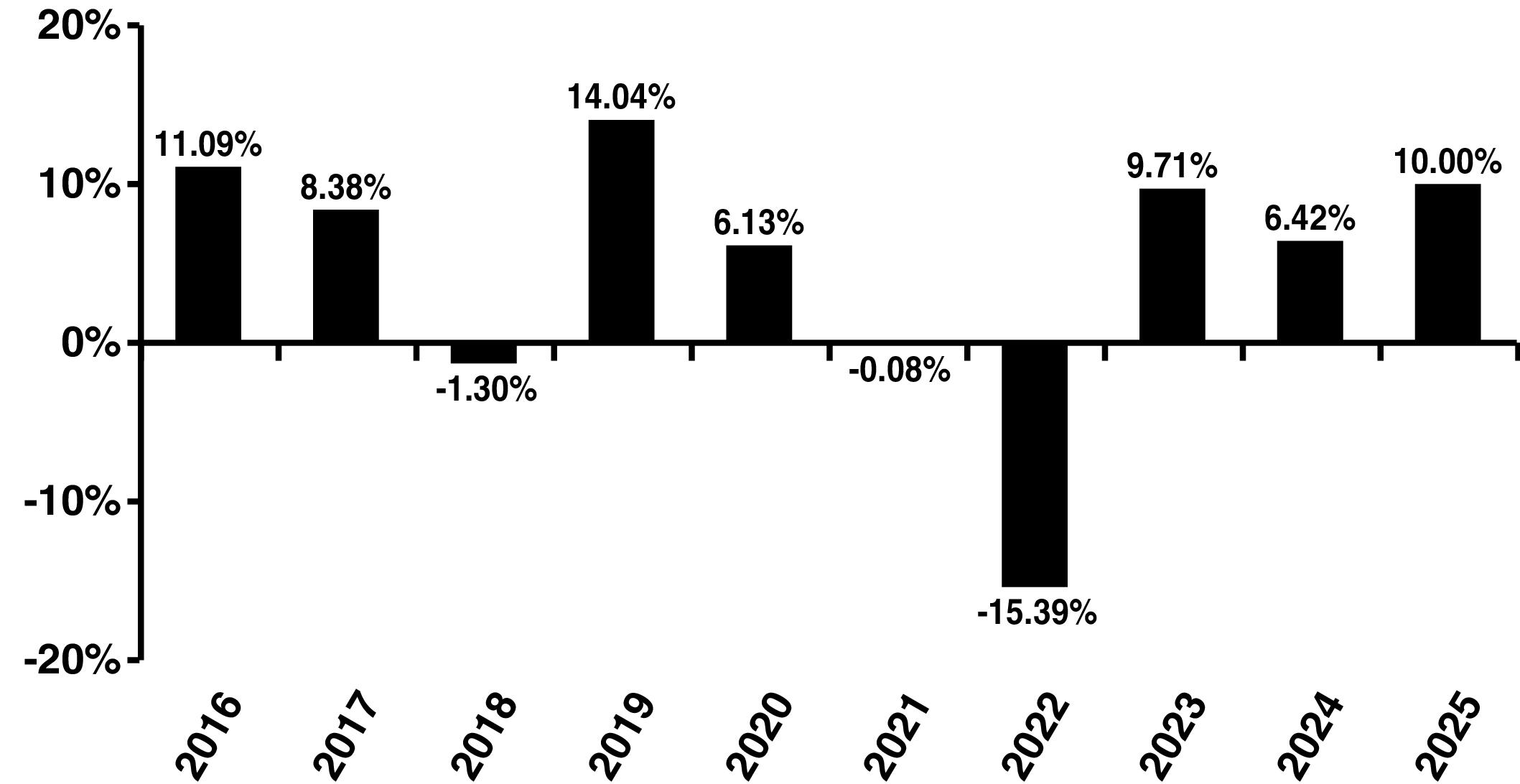

Growth Stock Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 2

Growth Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

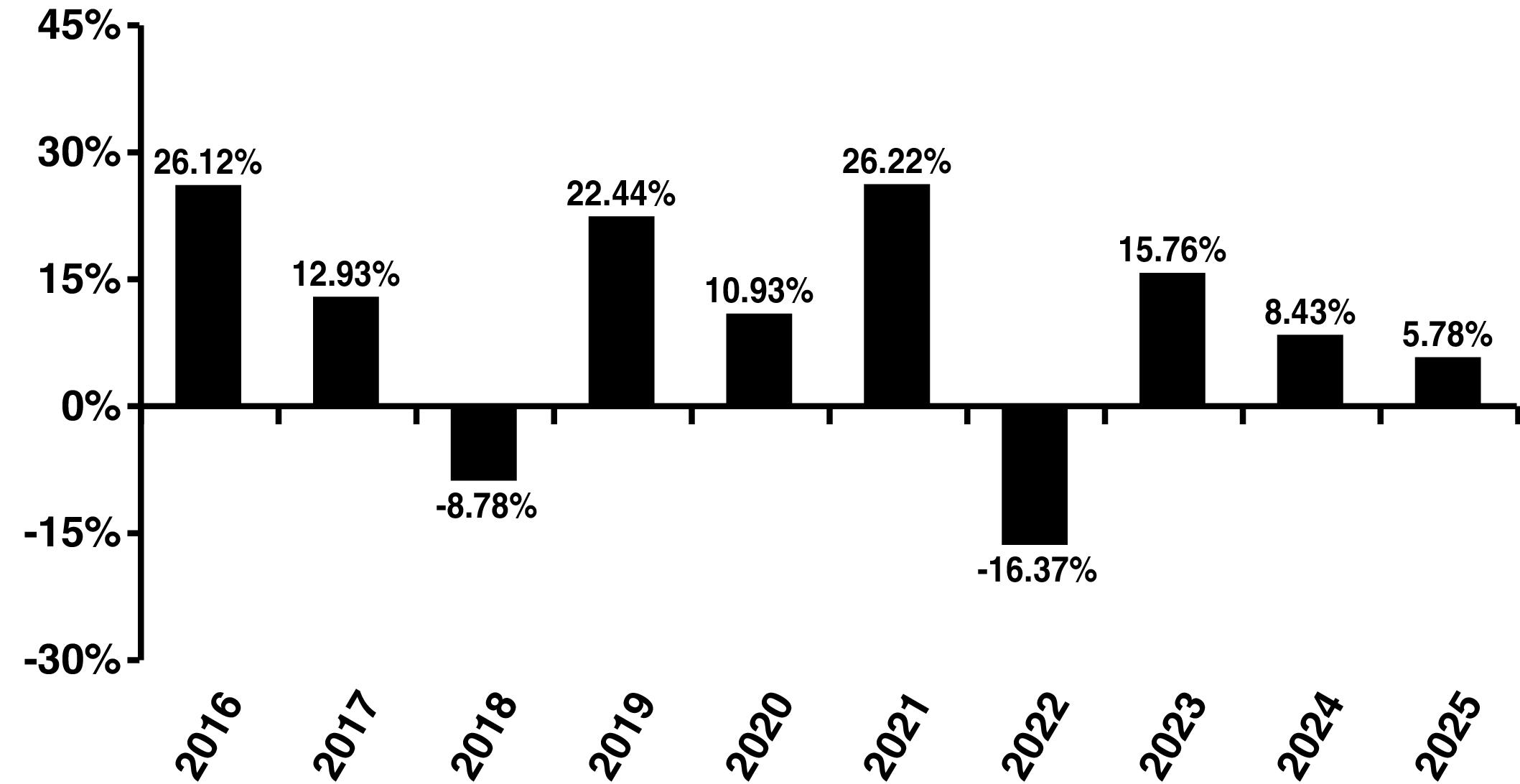

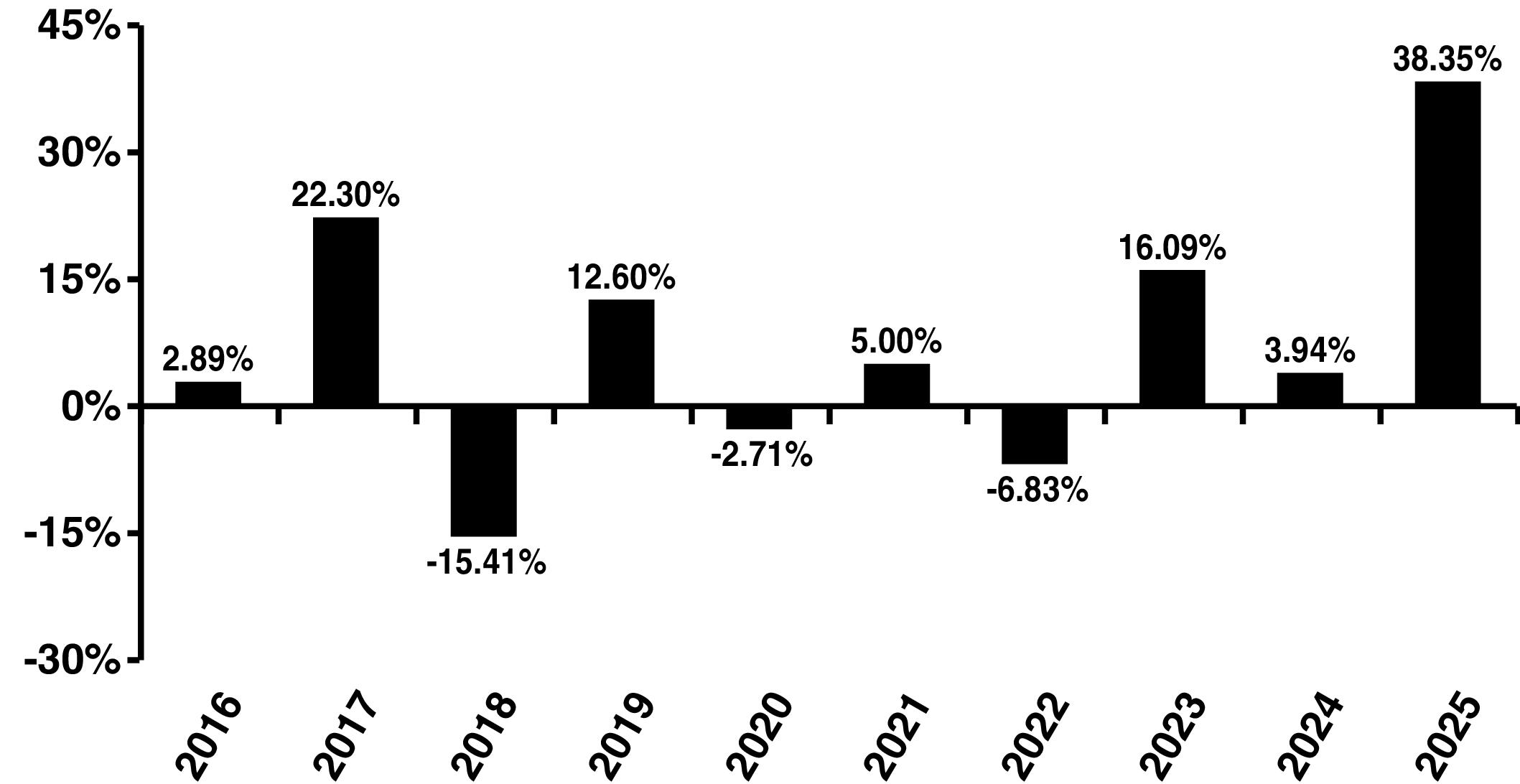

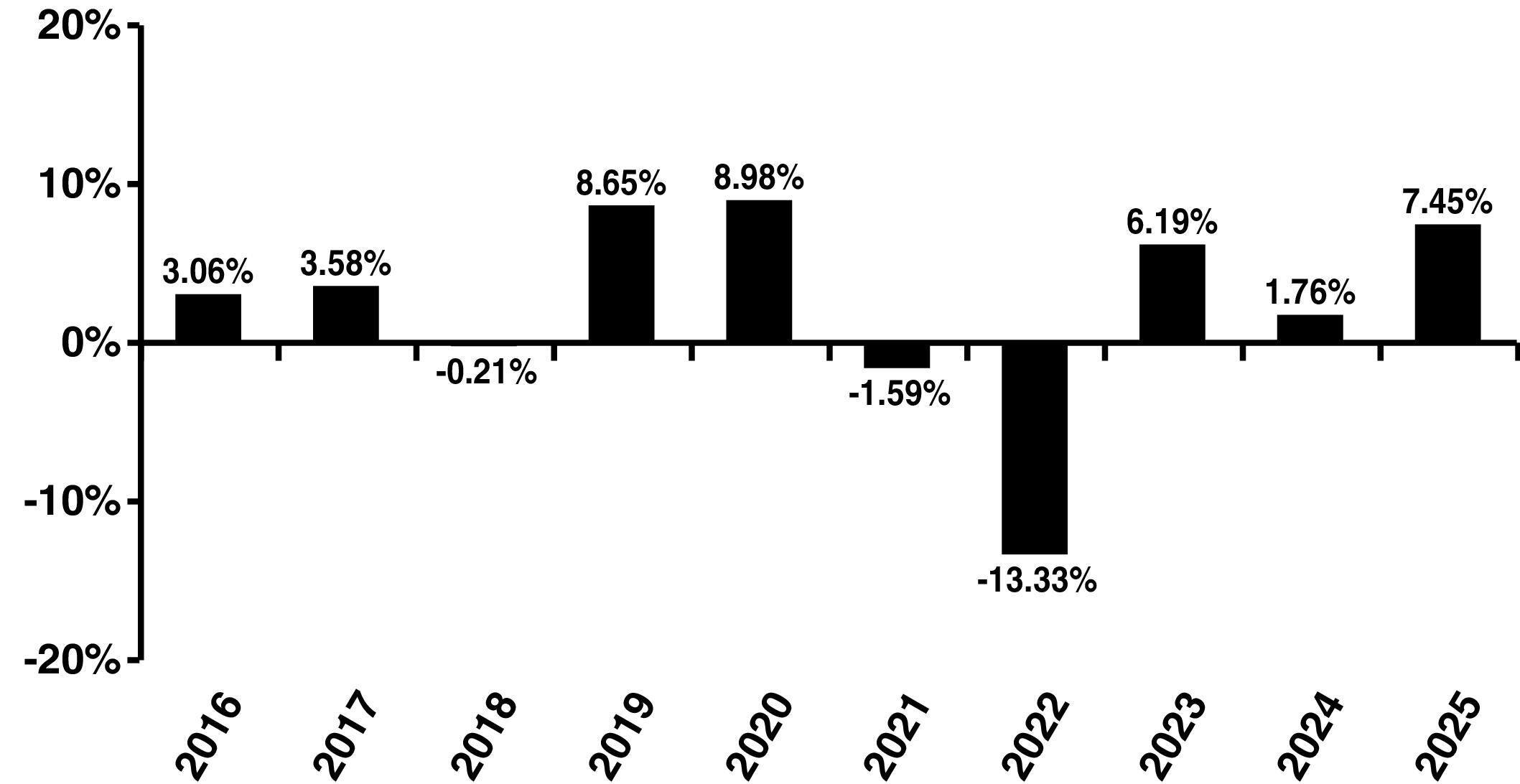

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Growth Stock Portfolio |

|

|

|

| Strategy Index: |

Russell 1000® Growth Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: Paul D. Greene II, Vice President and Associate Portfolio Manager of TRPA, joined T. Rowe Price in 2006 and has managed the Portfolio since 2020.

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: Paul D. Greene II, Vice President and Associate Portfolio Manager of TRPA, joined T. Rowe Price in 2006 and has managed the Portfolio since 2020.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

3 Northwestern Mutual Series Fund, Inc. Prospectus

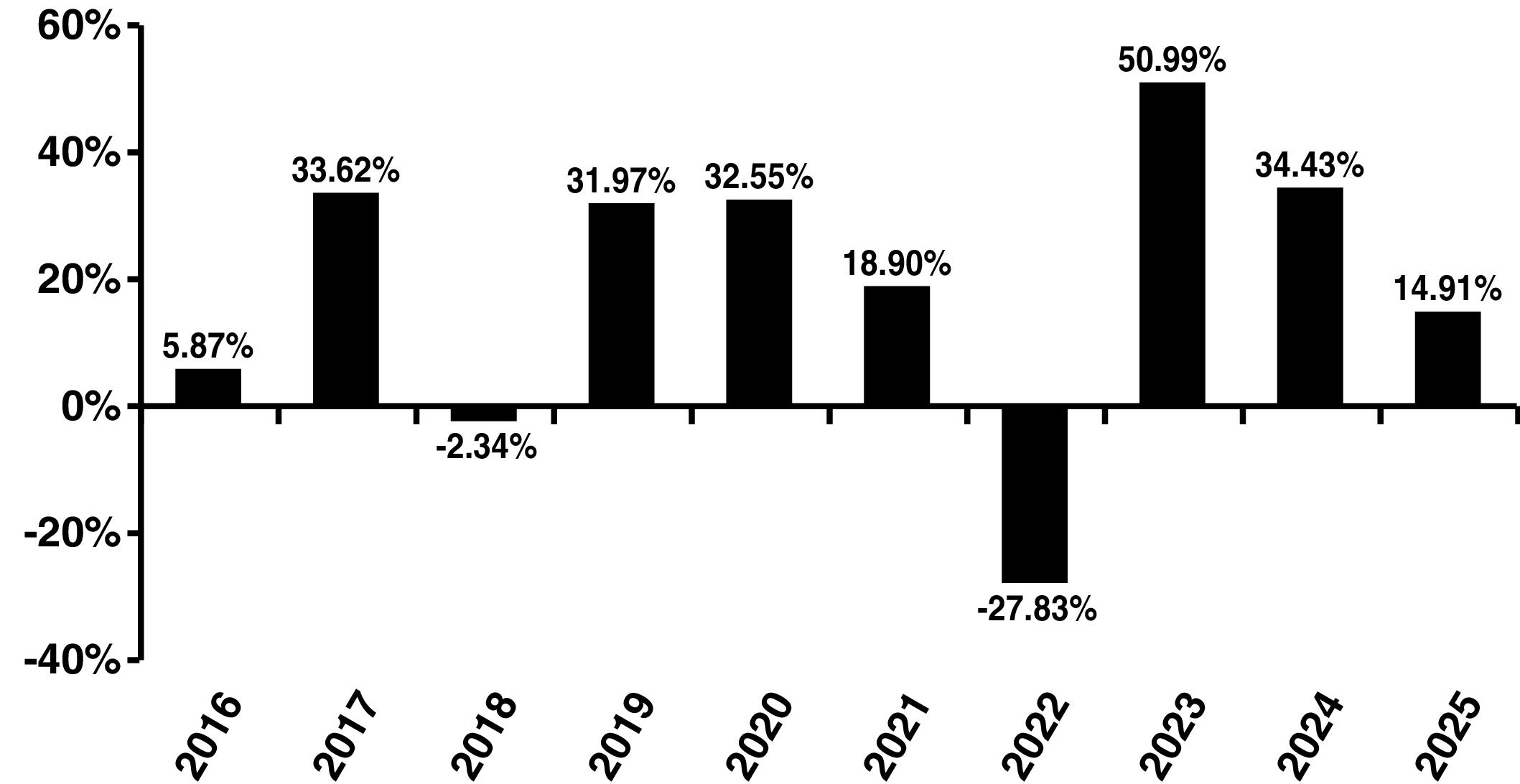

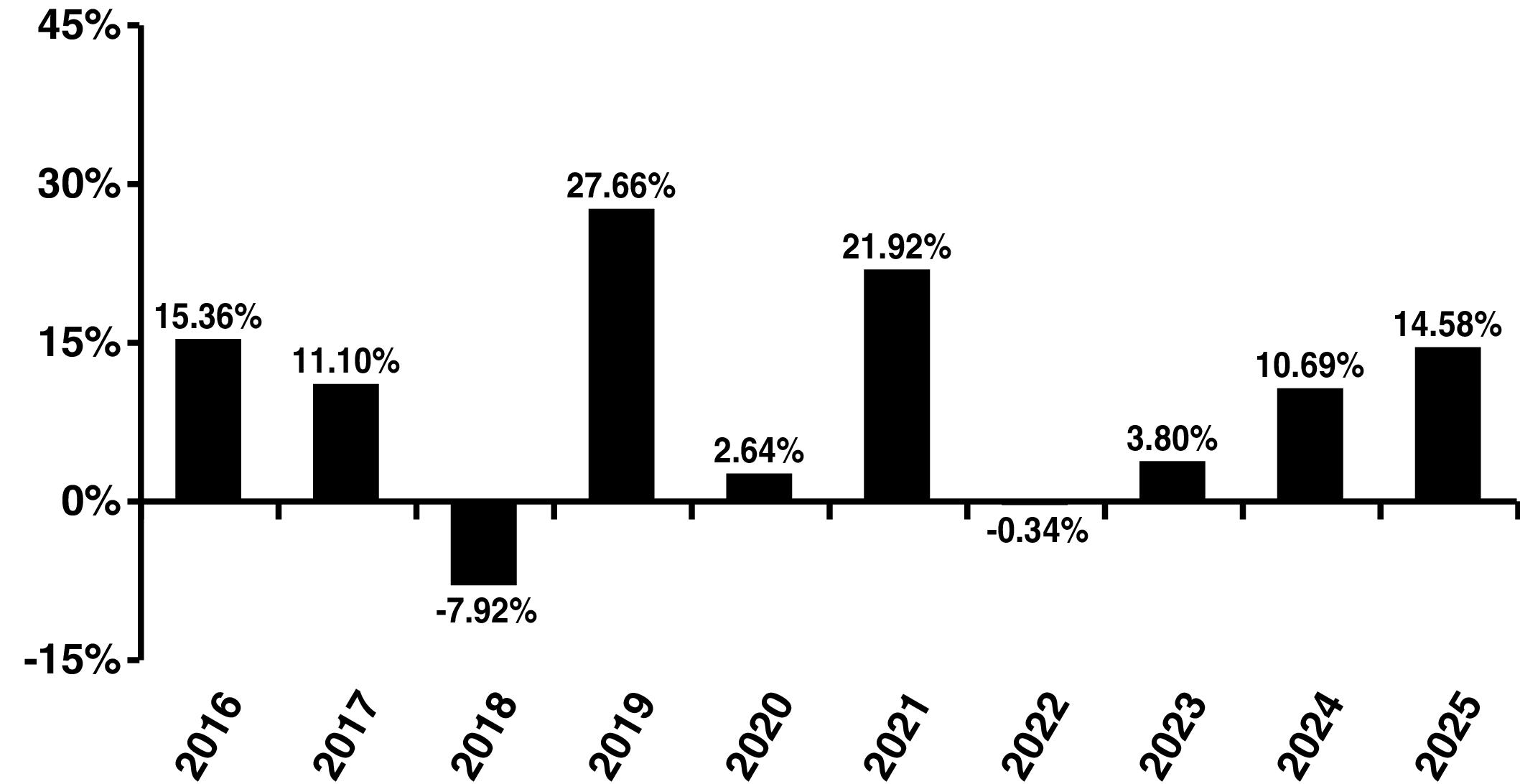

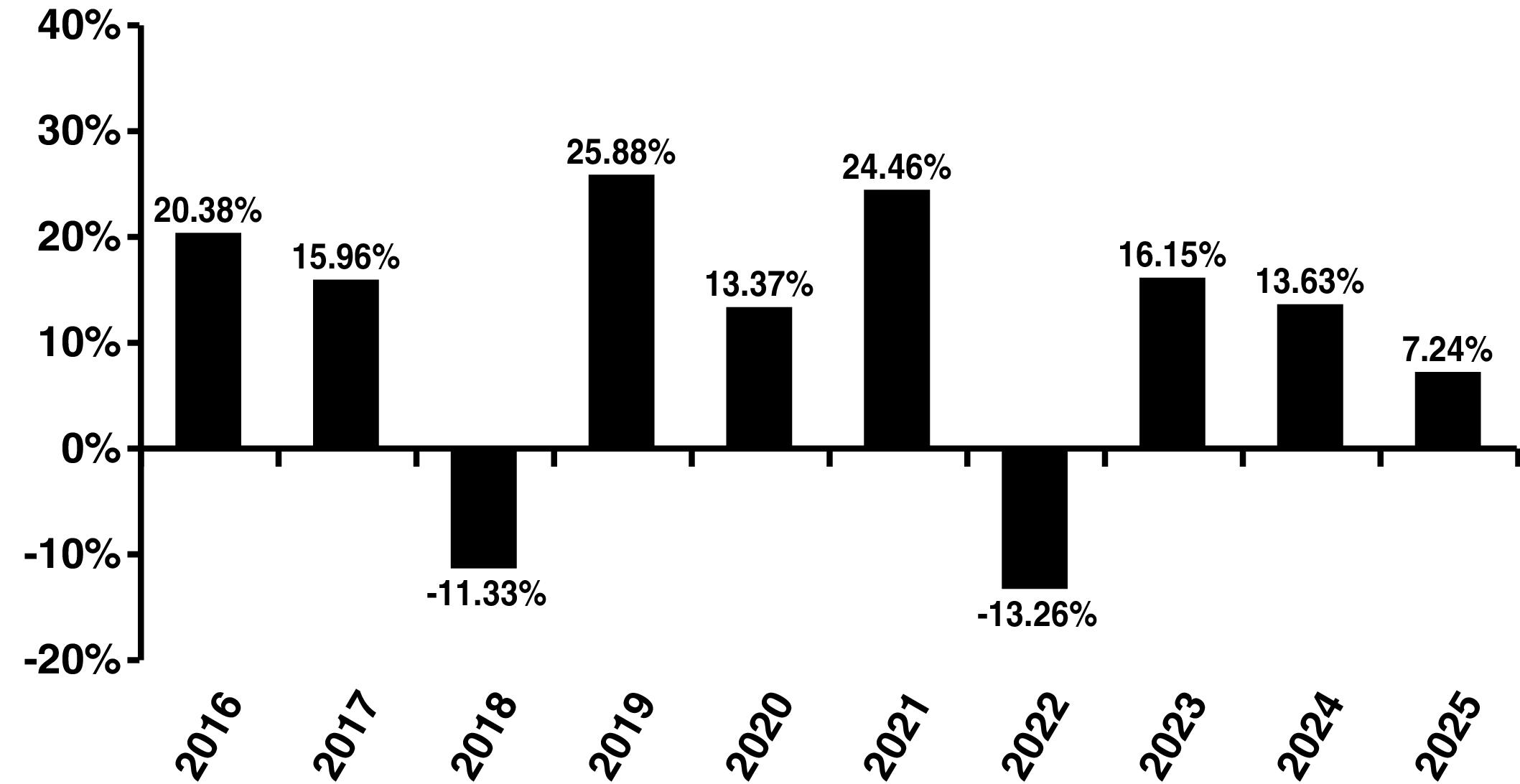

Focused Appreciation Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1),(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 4

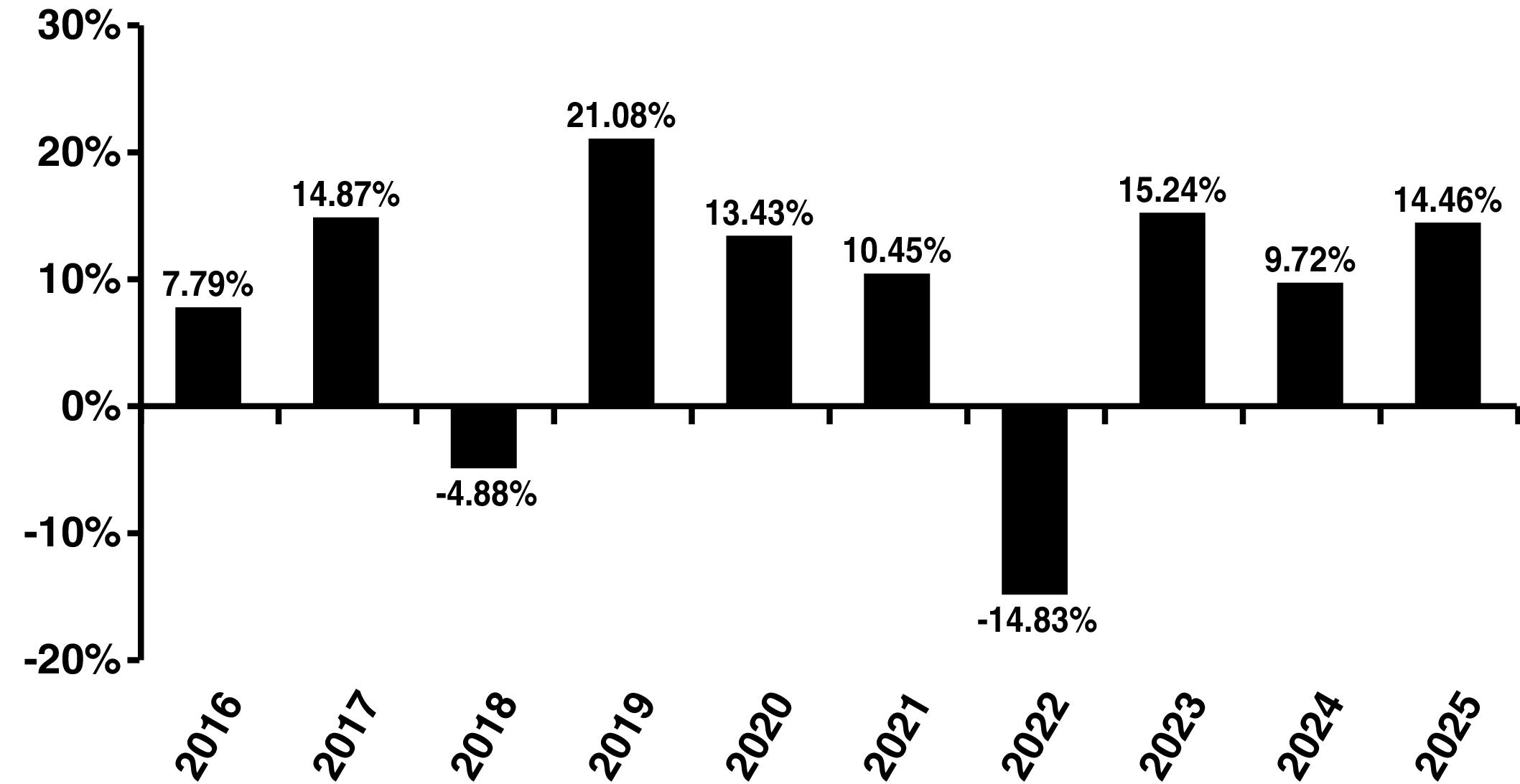

Focused Appreciation Portfolio – Summary

PRINCIPAL RISKS

5 Northwestern Mutual Series Fund, Inc. Prospectus

Focused Appreciation Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

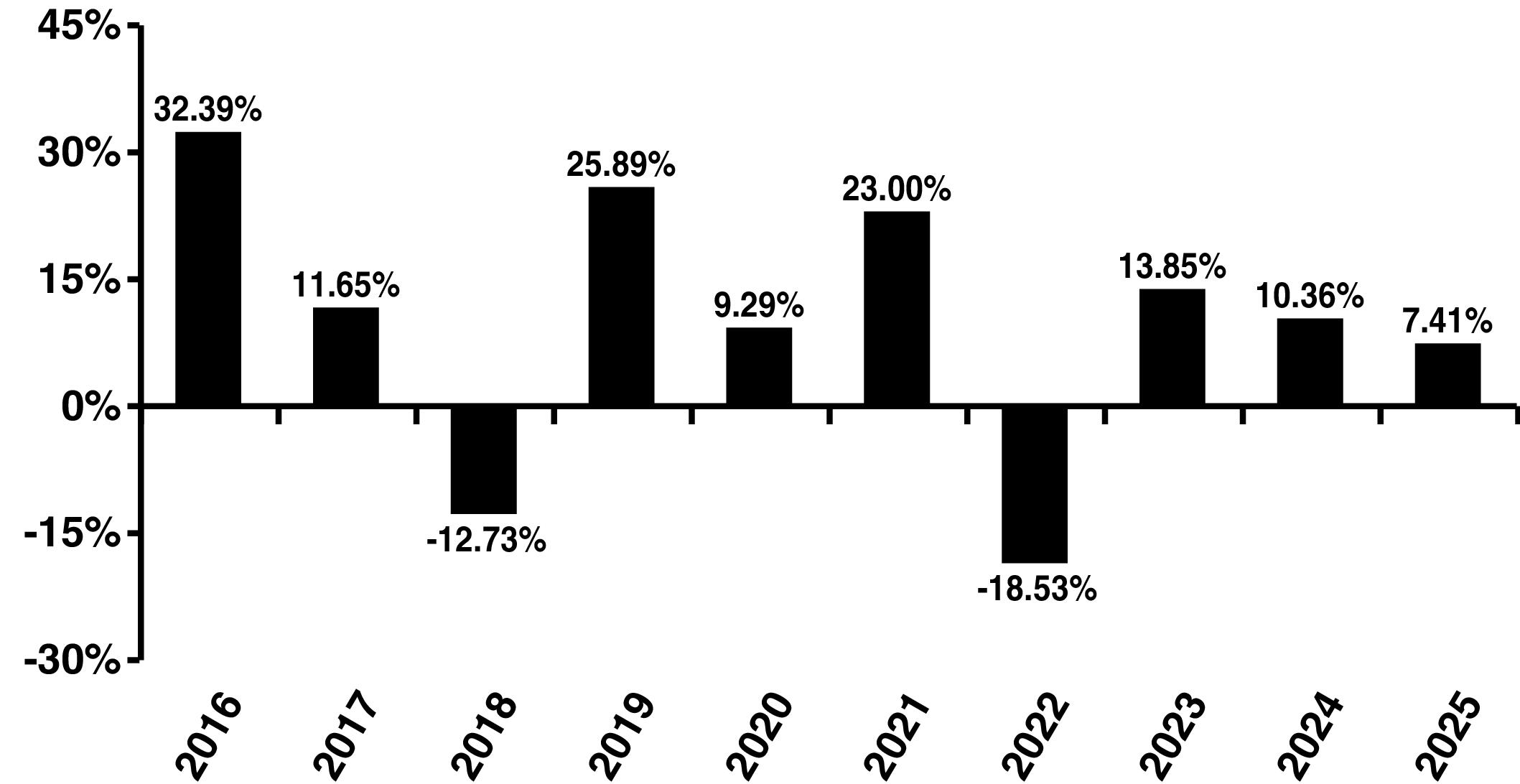

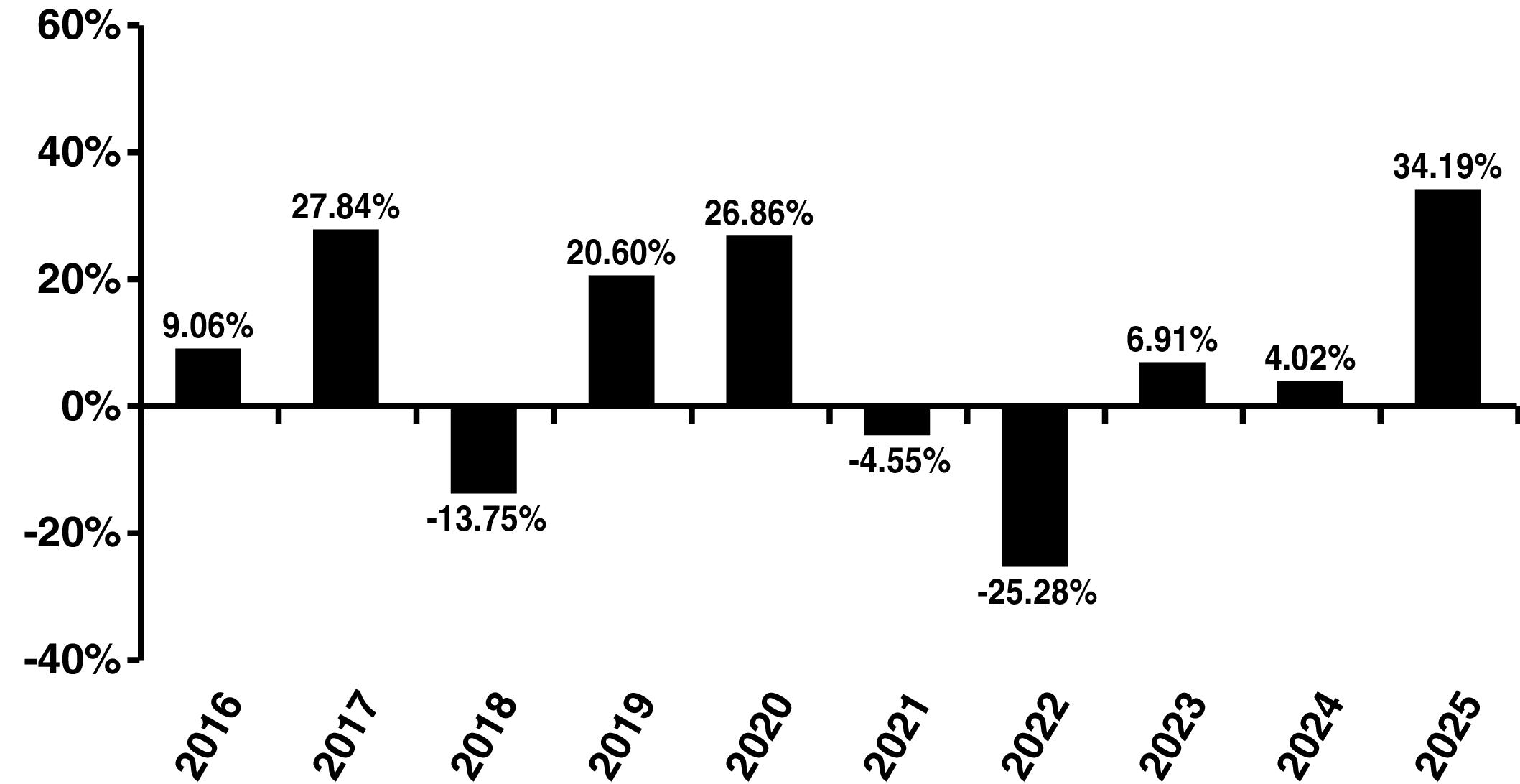

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Focused Appreciation Portfolio |

|

|

|

| Strategy Index: |

Russell 1000® Growth Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

Northwestern Mutual Series Fund, Inc. Prospectus 6

Focused Appreciation Portfolio – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Loomis, Sayles & Company, L.P. (Loomis Sayles)

Portfolio Manager: Aziz V. Hamzaogullari, CFA, Executive Vice President of Loomis Sayles, joined Loomis Sayles in 2010 and has managed the Portfolio since 2015.

Sub-Adviser: Loomis, Sayles & Company, L.P. (Loomis Sayles)

Portfolio Manager: Aziz V. Hamzaogullari, CFA, Executive Vice President of Loomis Sayles, joined Loomis Sayles in 2010 and has managed the Portfolio since 2015.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

7 Northwestern Mutual Series Fund, Inc. Prospectus

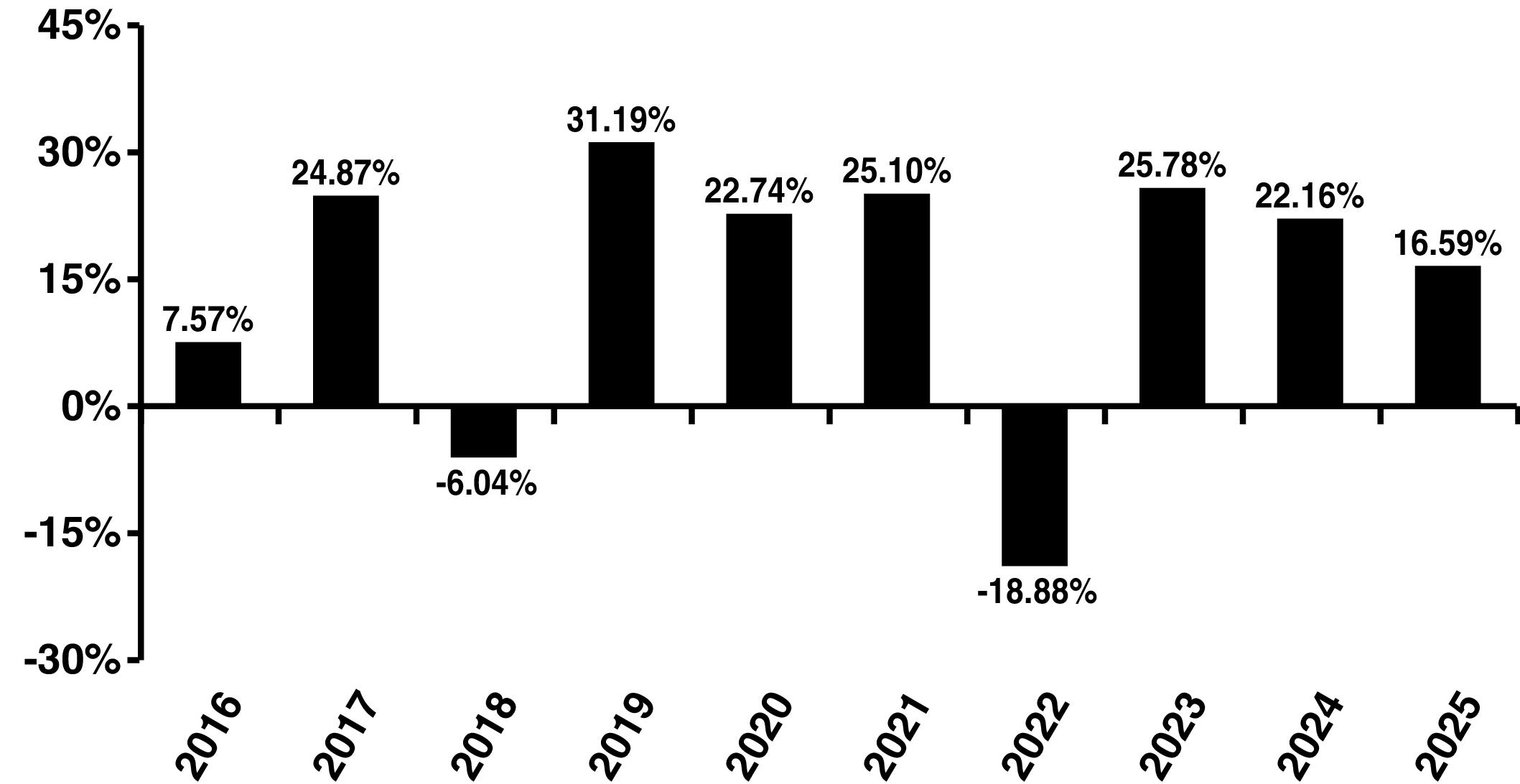

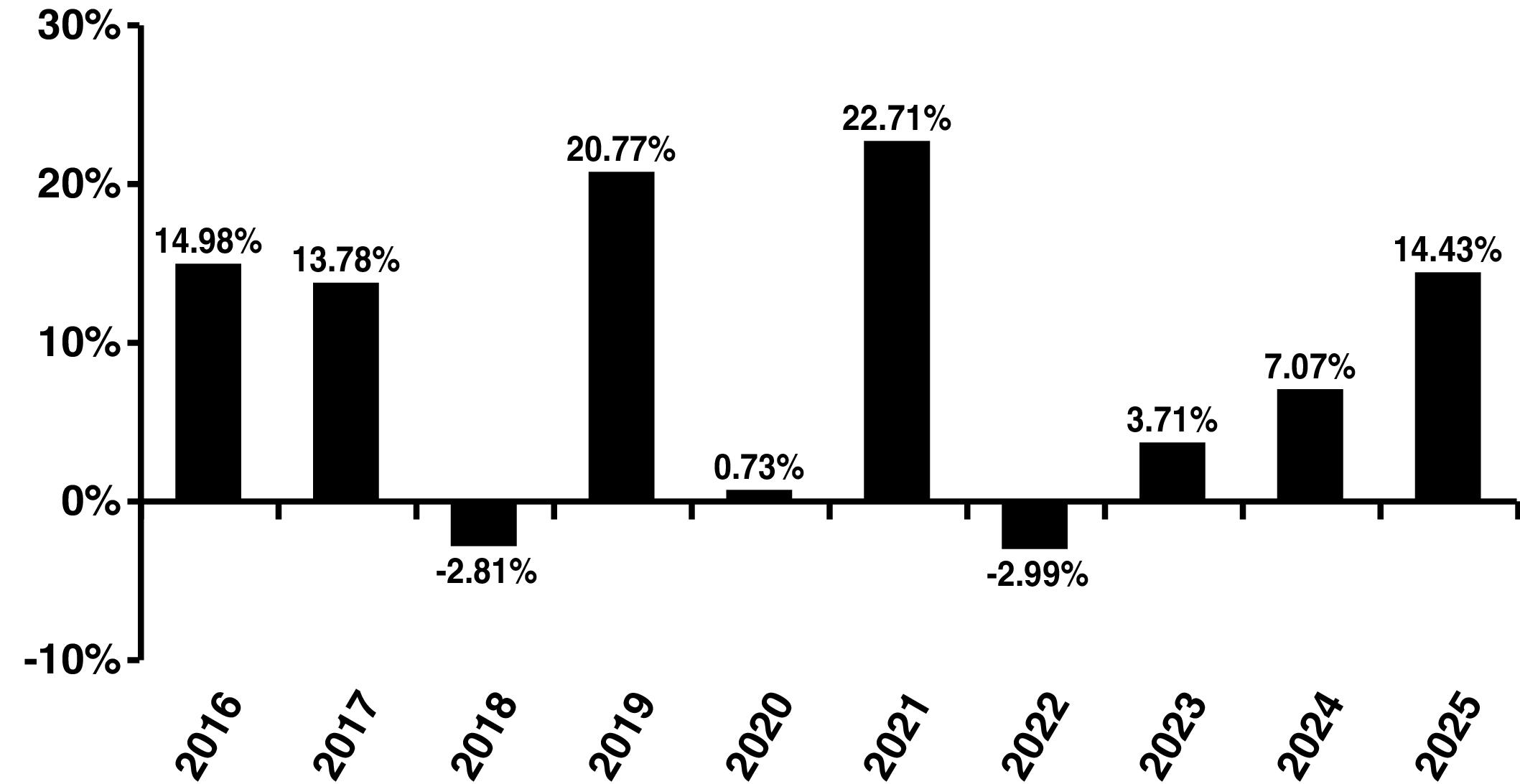

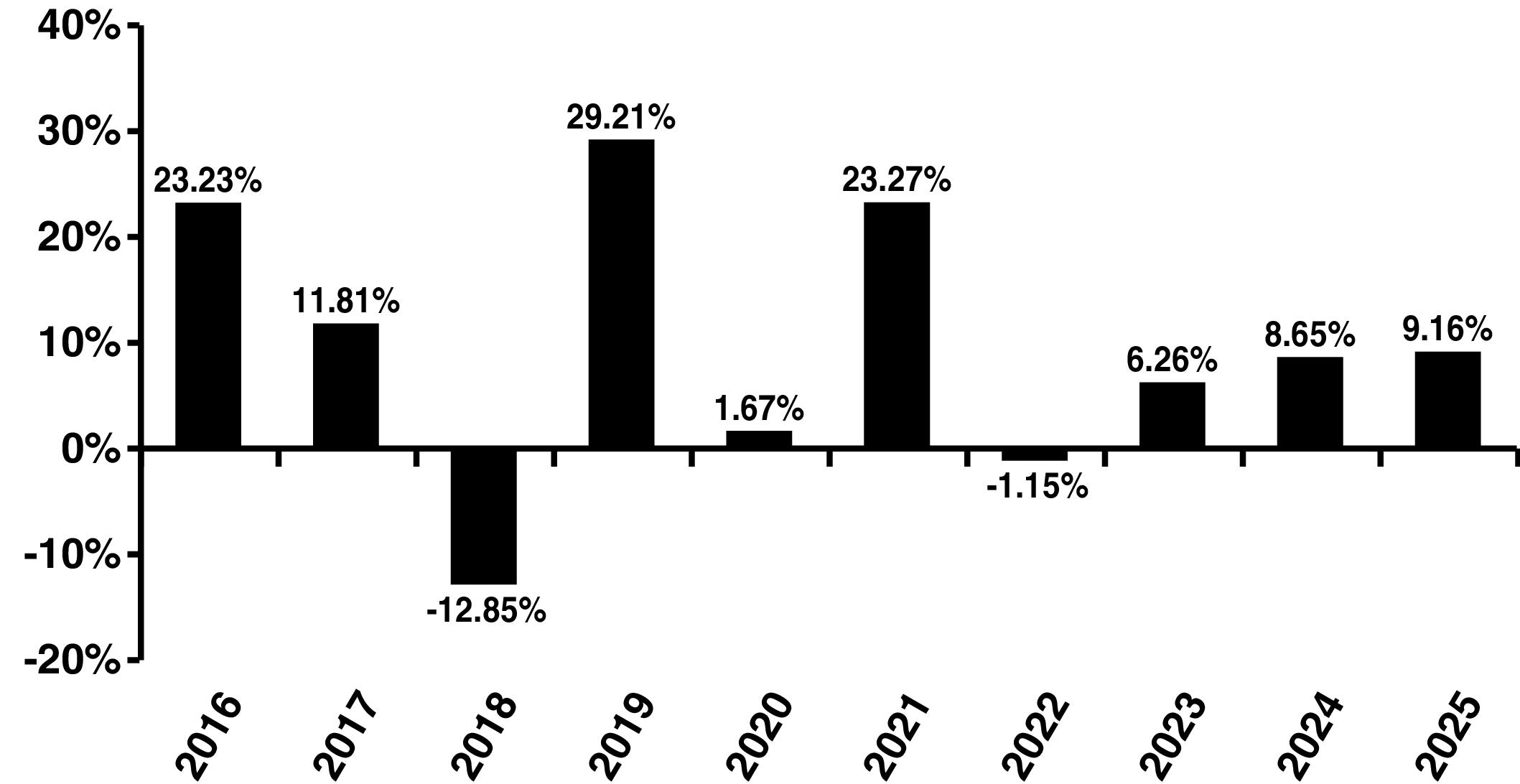

Large Cap Core Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses(1) |

|

| Total Annual Portfolio Operating Expenses(1) |

|

| Fee Waiver(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 8

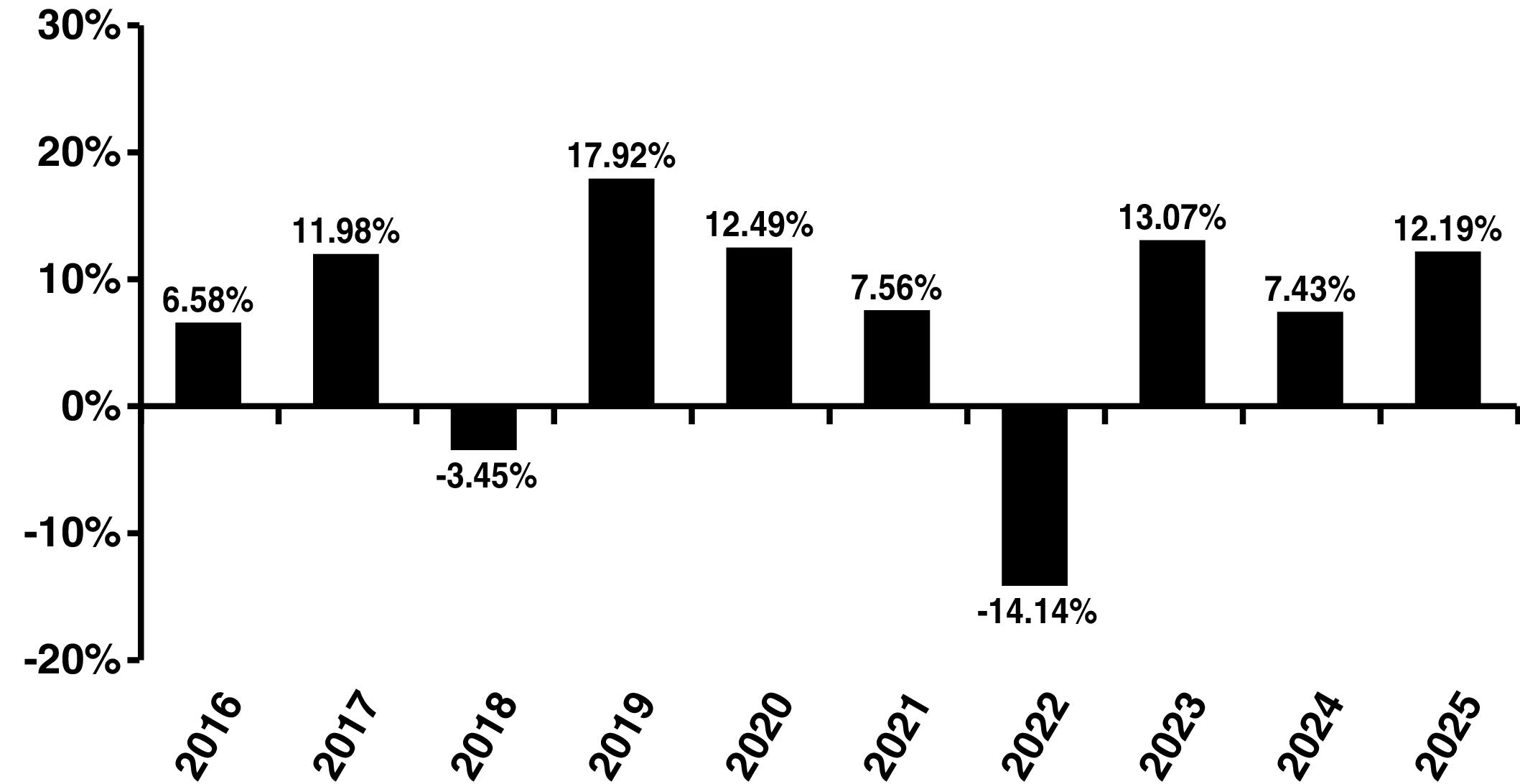

Large Cap Core Stock Portfolio – Summary

PRINCIPAL RISKS

9 Northwestern Mutual Series Fund, Inc. Prospectus

Large Cap Core Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

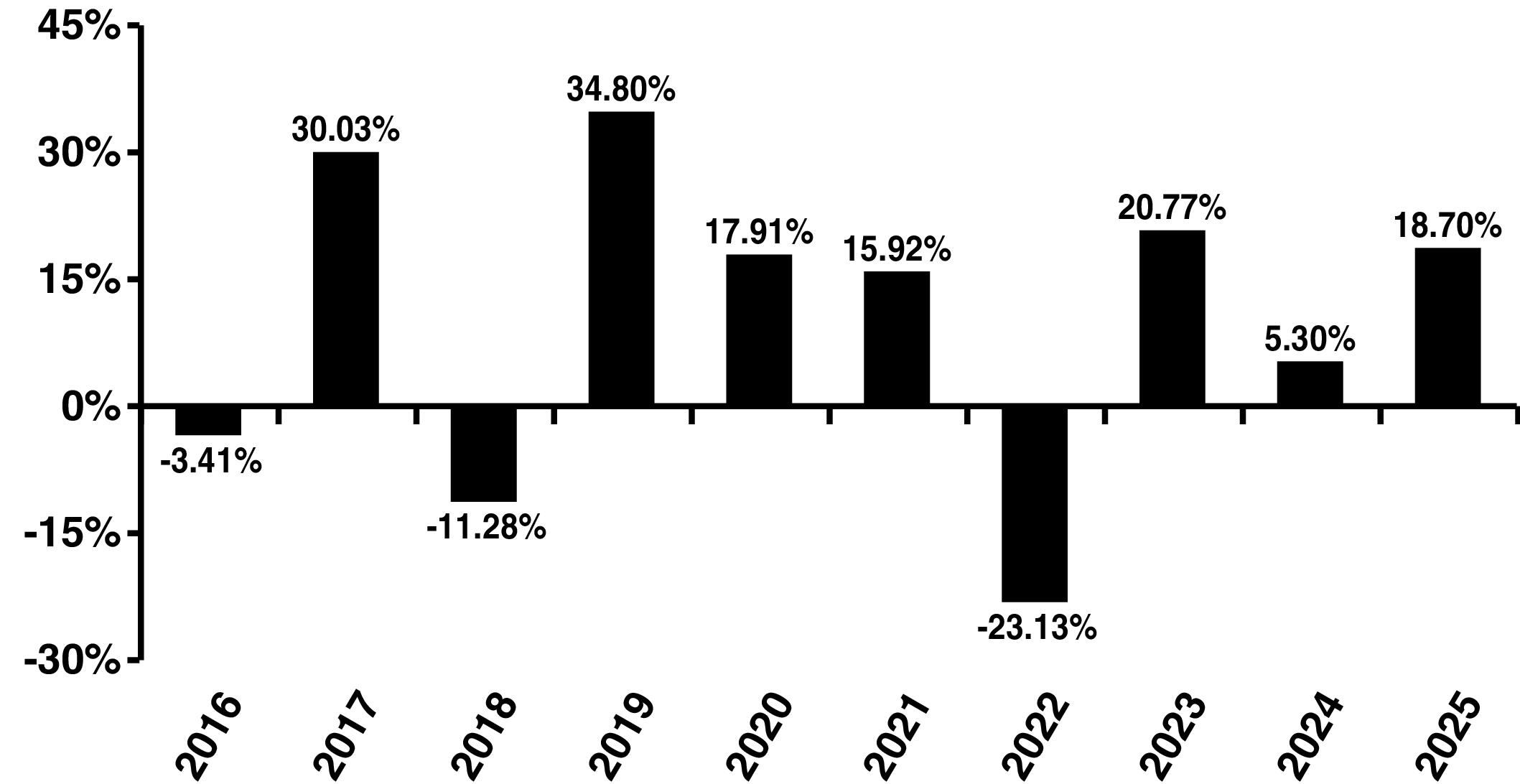

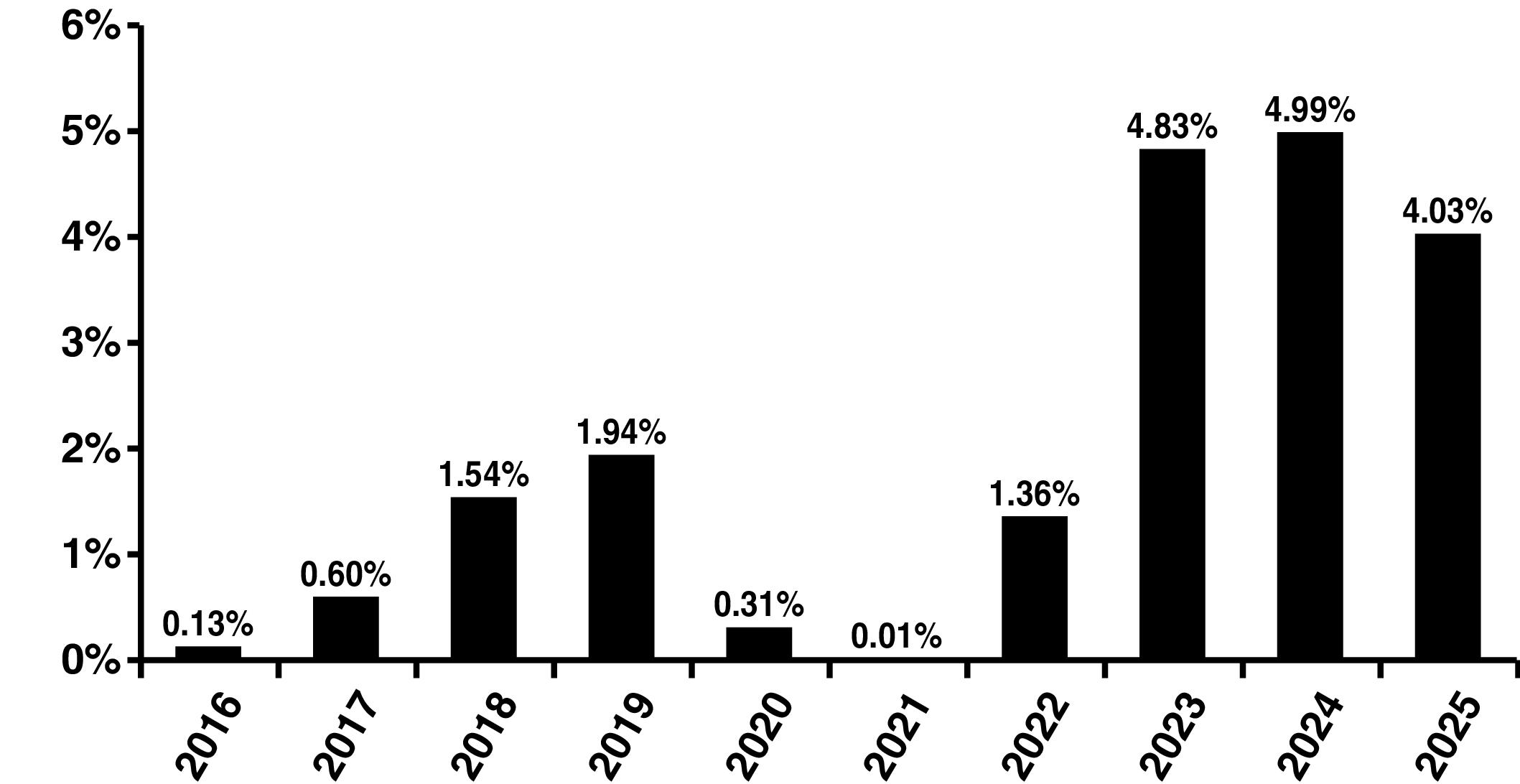

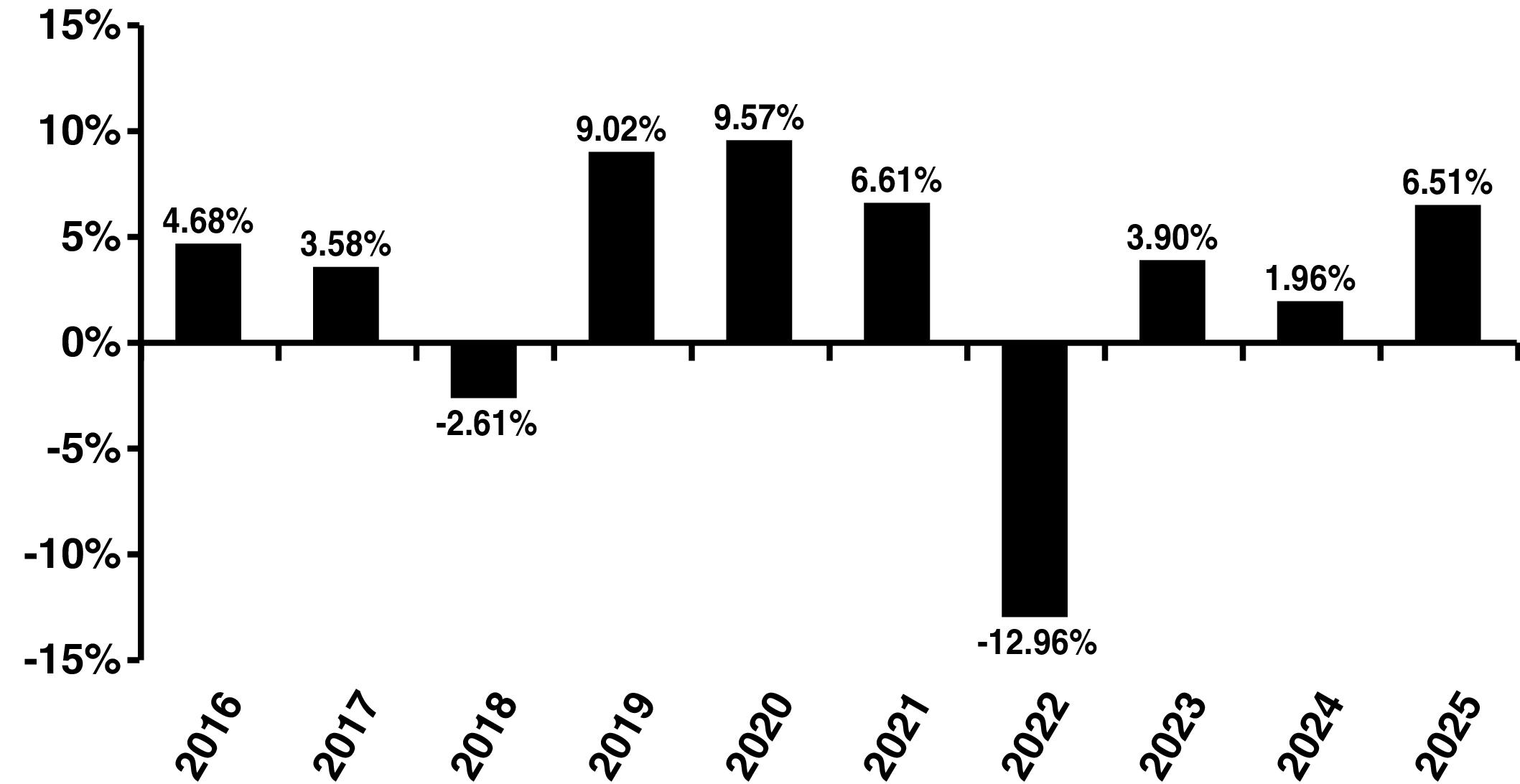

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Large Cap Core Stock Portfolio |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Wellington Management Company LLP (Wellington Management)

Portfolio Managers: Jonathan G. White, CFA and Director of Research Portfolios, joined Wellington Management in 1999 and has managed the Portfolio since 2017.

Mary L. Pryshlak, CFA and Head of Investment Research, joined Wellington Management in 2004 and has managed the Portfolio since 2018.

Sub-Adviser: Wellington Management Company LLP (Wellington Management)

Portfolio Managers: Jonathan G. White, CFA and Director of Research Portfolios, joined Wellington Management in 1999 and has managed the Portfolio since 2017.

Mary L. Pryshlak, CFA and Head of Investment Research, joined Wellington Management in 2004 and has managed the Portfolio since 2018.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 10

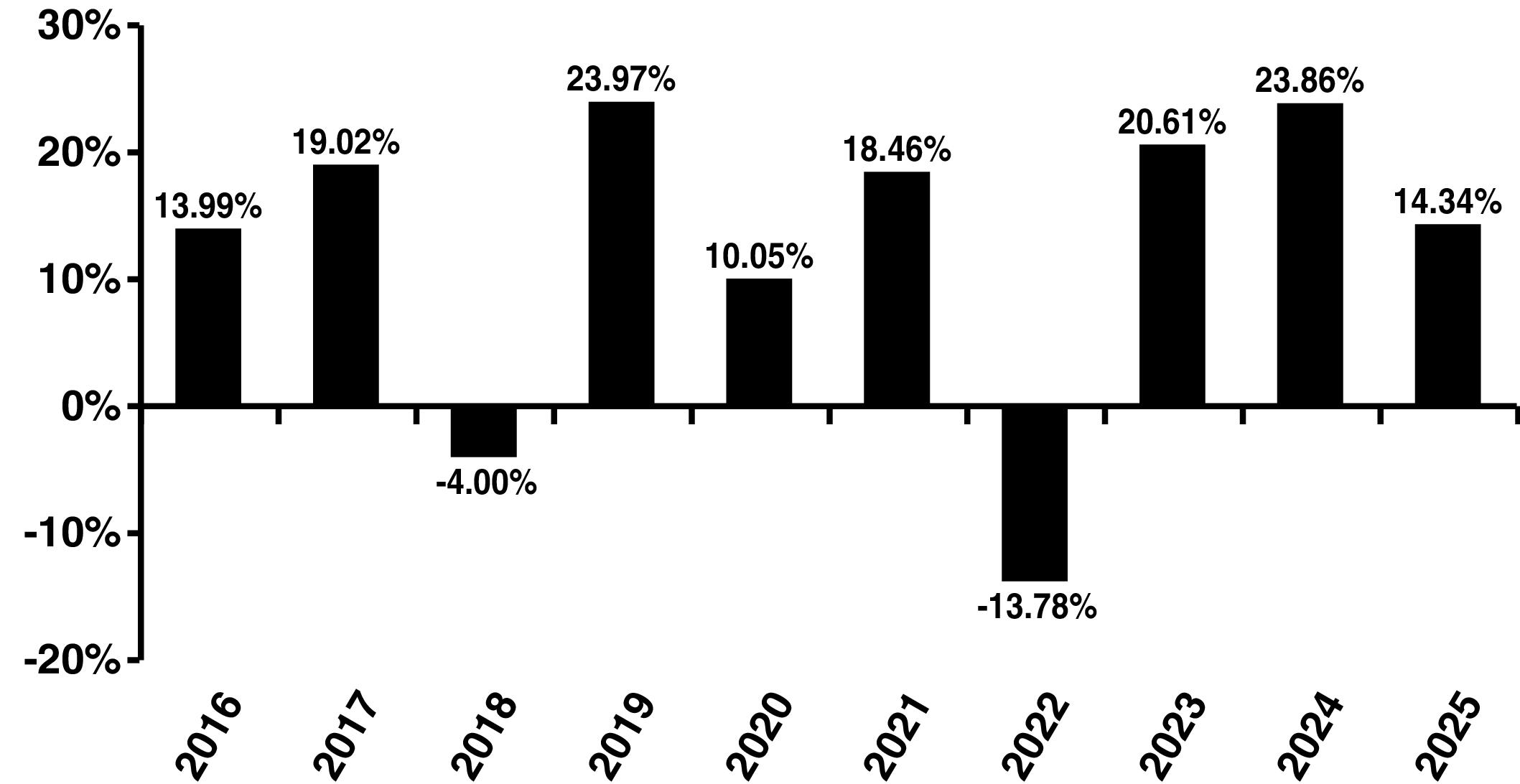

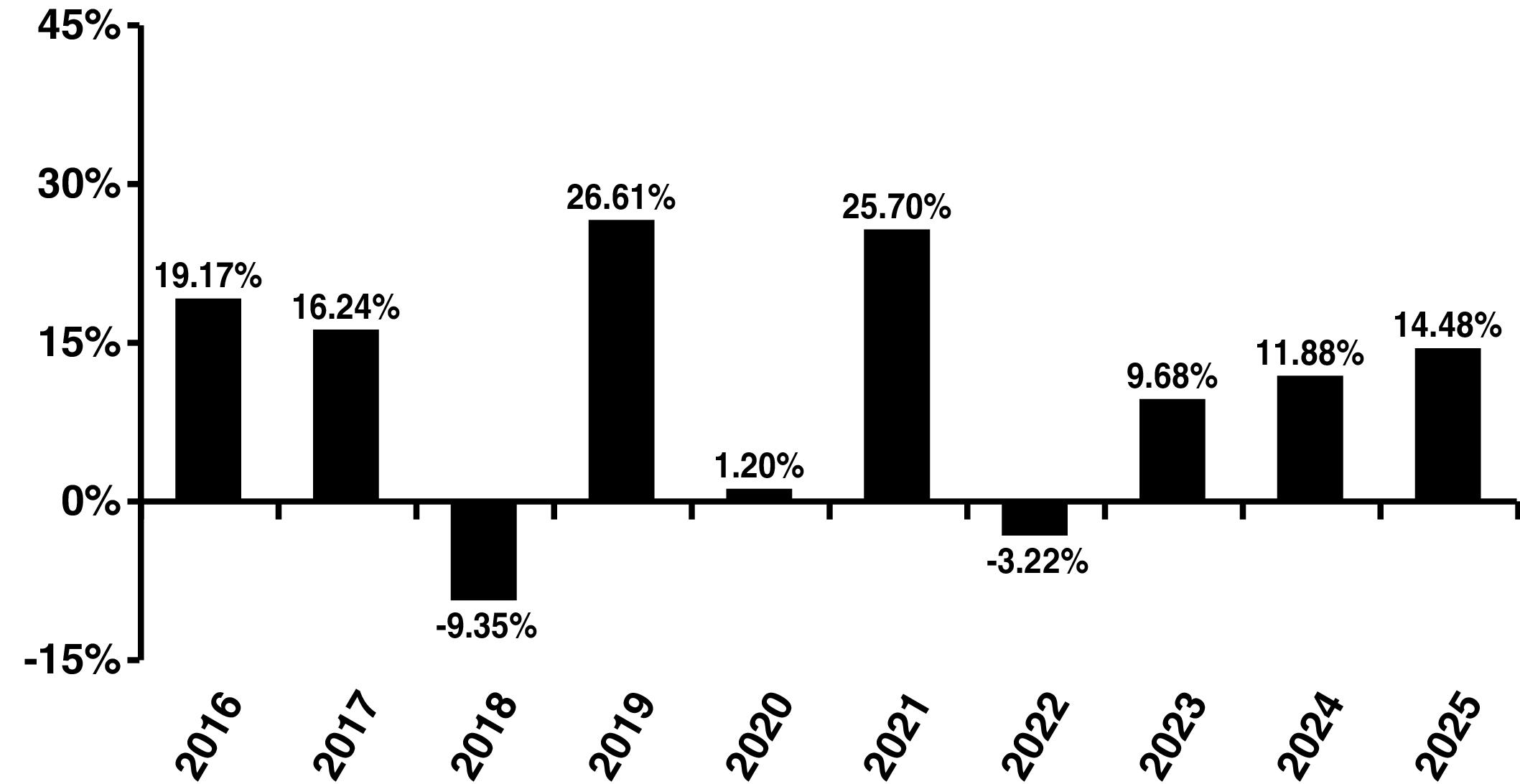

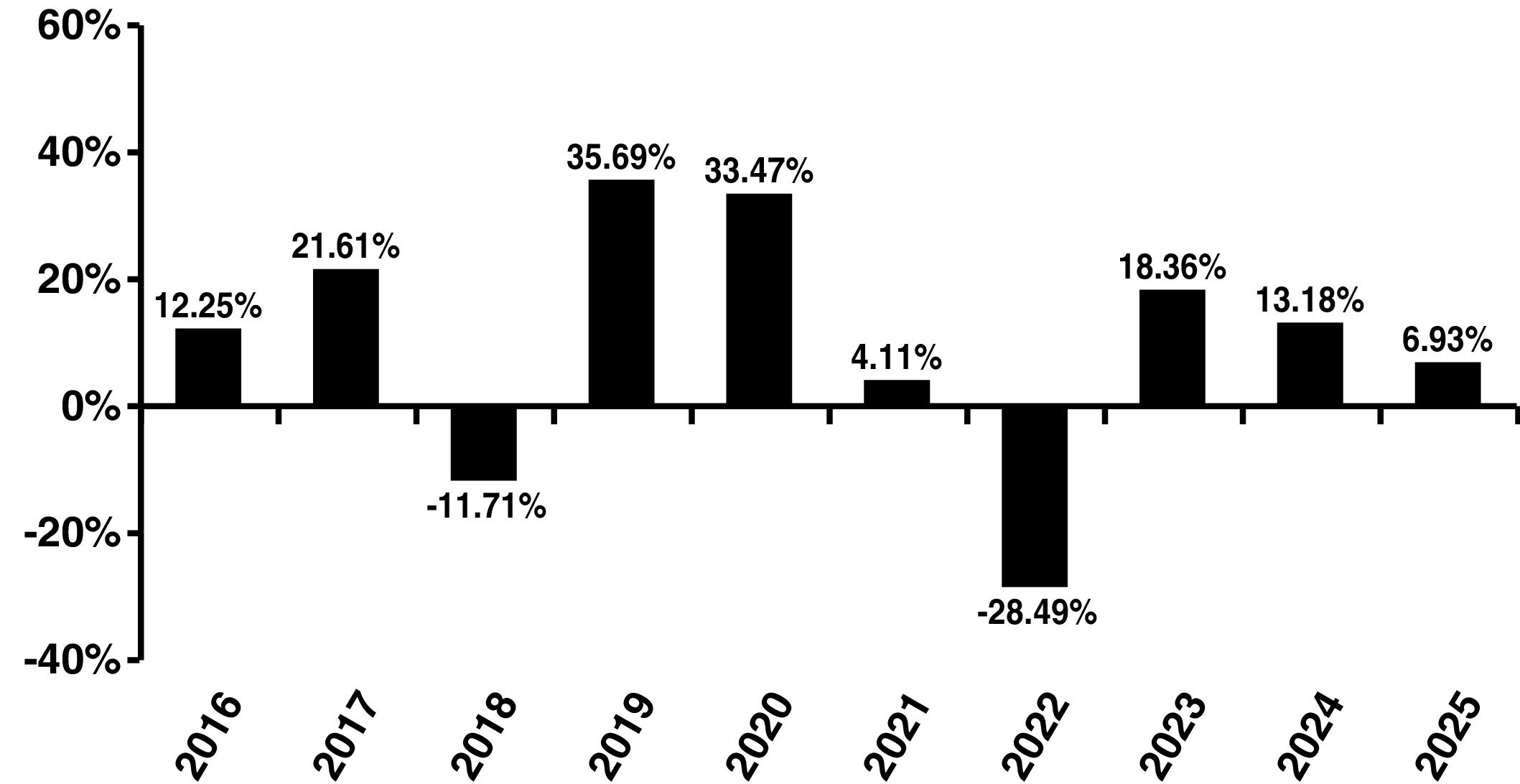

Large Cap Blend Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

11 Northwestern Mutual Series Fund, Inc. Prospectus

Large Cap Blend Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 12

Large Cap Blend Portfolio – Summary

13 Northwestern Mutual Series Fund, Inc. Prospectus

Large Cap Blend Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

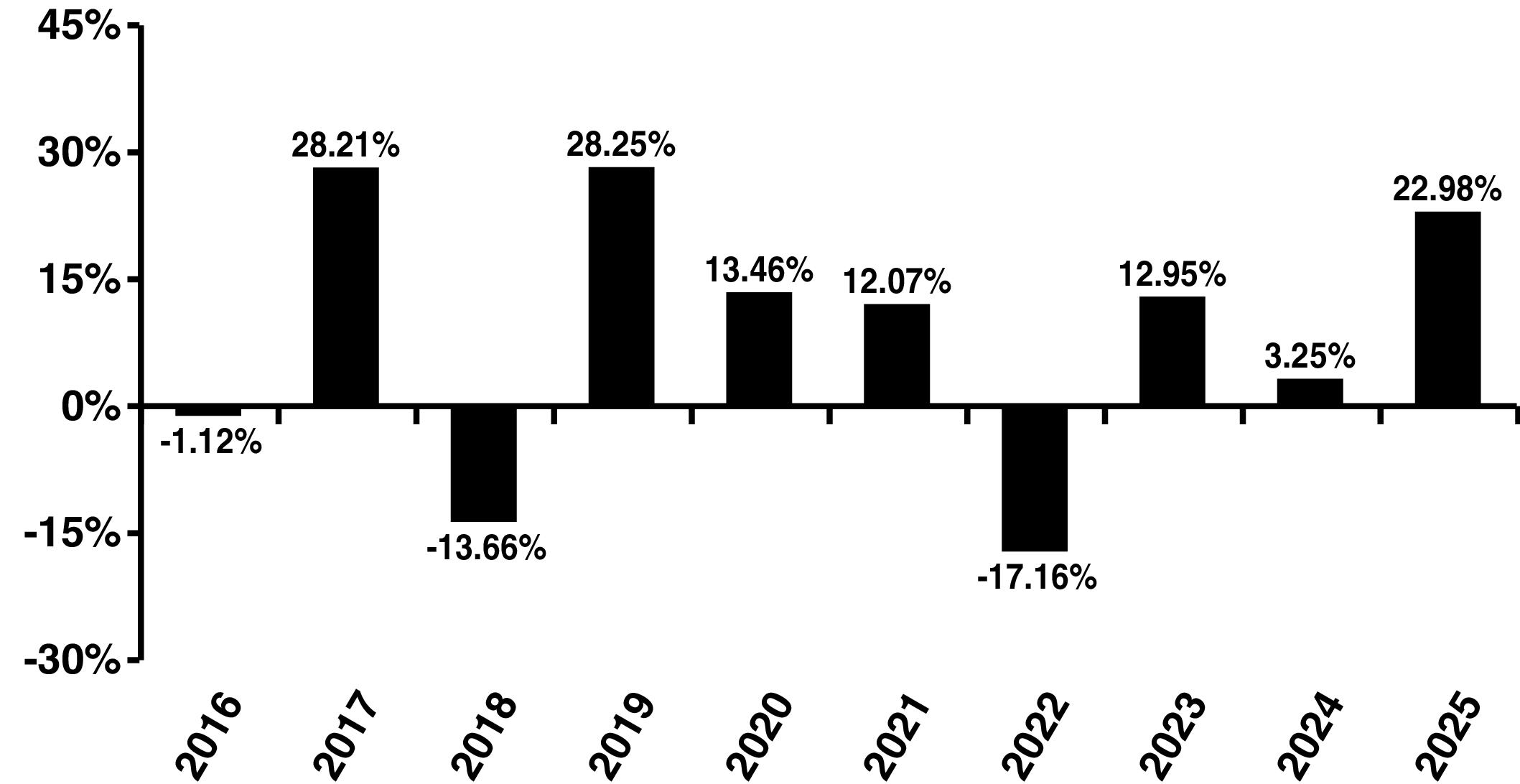

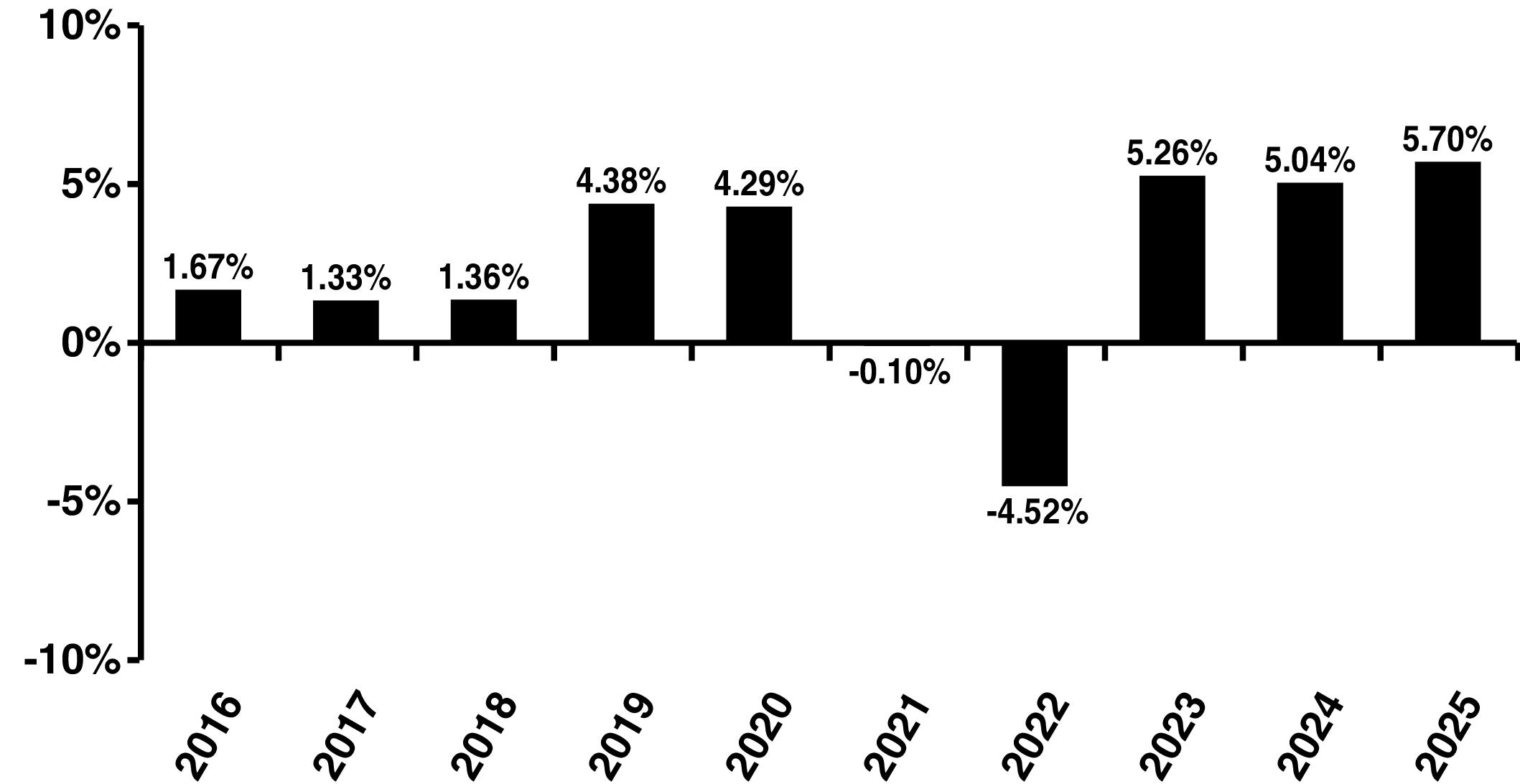

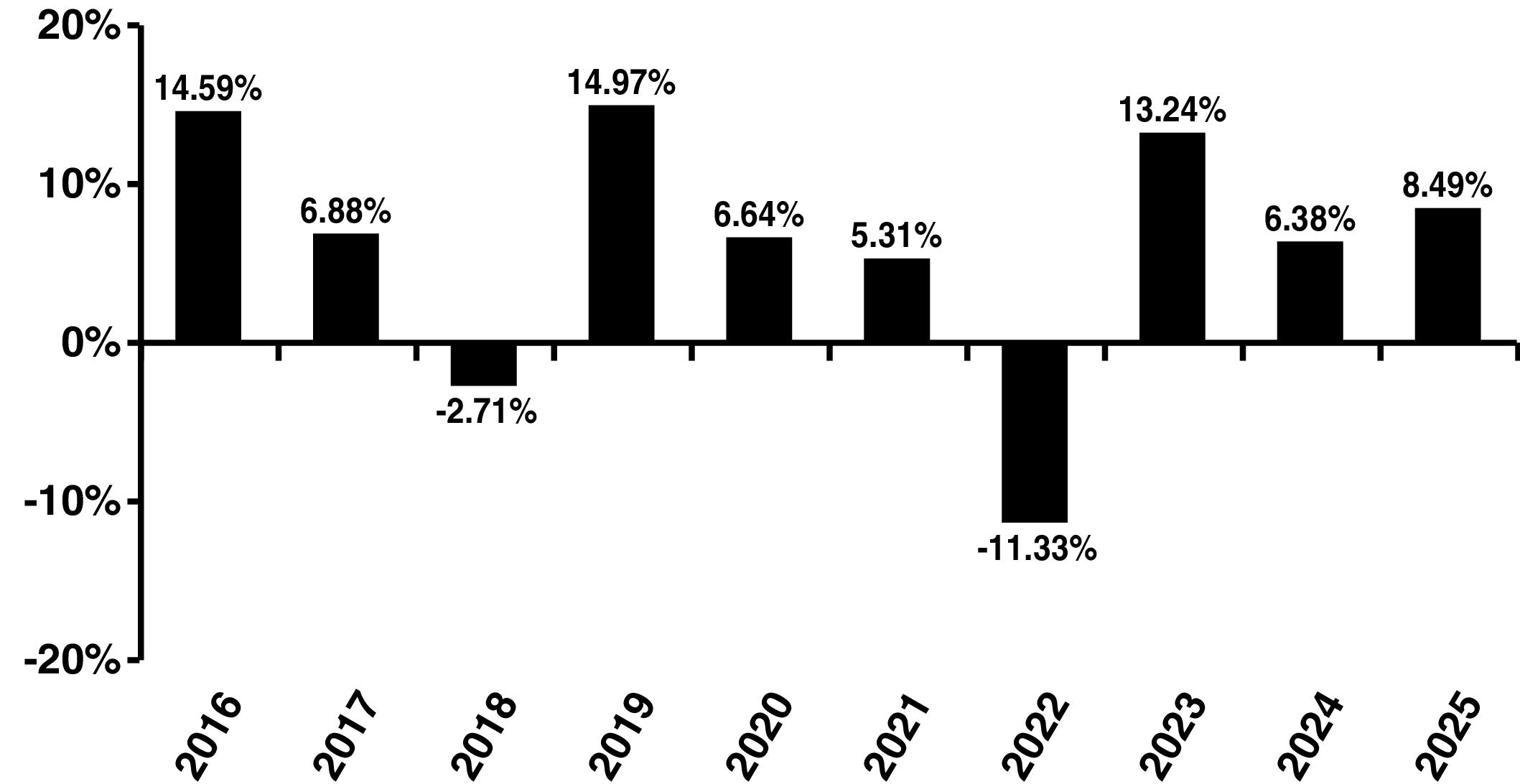

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Large Cap Blend Portfolio |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: J.P. Morgan Investment Management, Inc. (JP Morgan)

Portfolio Managers: Scott B. Davis, Managing Director, joined JP Morgan in 2006 and has managed the Portfolio since 2023.

Shilpee Raina, Executive Director, joined JP Morgan in 2005 and has managed the Portfolio since 2023.

Sub-Adviser: J.P. Morgan Investment Management, Inc. (JP Morgan)

Portfolio Managers: Scott B. Davis, Managing Director, joined JP Morgan in 2006 and has managed the Portfolio since 2023.

Shilpee Raina, Executive Director, joined JP Morgan in 2005 and has managed the Portfolio since 2023.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 14

Index 500 Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

15 Northwestern Mutual Series Fund, Inc. Prospectus

Index 500 Stock Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 16

Index 500 Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Index 500 Stock Portfolio |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: BlackRock Advisors, LLC (BlackRock)

Portfolio Managers: Peter Sietsema, CFA, Director, joined BlackRock in 2007 and has managed the Portfolio since 2022.

Jennifer Hsui, CFA, Managing Director and Co-head and Chief Investment Officer of Global Index Equity, joined BlackRock in

Sub-Adviser: BlackRock Advisors, LLC (BlackRock)

Portfolio Managers: Peter Sietsema, CFA, Director, joined BlackRock in 2007 and has managed the Portfolio since 2022.

Jennifer Hsui, CFA, Managing Director and Co-head and Chief Investment Officer of Global Index Equity, joined BlackRock in

17 Northwestern Mutual Series Fund, Inc. Prospectus

Index 500 Stock Portfolio – Summary

2006 and has managed the Portfolio since 2021.

Steven White, Director and Head of the Active Risk Index ETF team in the Americas, and co-CIO for Index Equity Investments within BlackRock Global Markets & Index Investments, joined BlackRock in 2011 and has managed the Portfolio since 2025.

Steven White, Director and Head of the Active Risk Index ETF team in the Americas, and co-CIO for Index Equity Investments within BlackRock Global Markets & Index Investments, joined BlackRock in 2011 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 18

Large Company Value Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

19 Northwestern Mutual Series Fund, Inc. Prospectus

Large Company Value Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 20

Large Company Value Portfolio – Summary

21 Northwestern Mutual Series Fund, Inc. Prospectus

Large Company Value Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Large Company Value Portfolio |

|

|

|

| Strategy Index: |

Russell 1000® Value Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: Brian Woglom, CFA, Vice President and Senior Portfolio Manager, joined American Century in 2005 and has managed the Portfolio since 2016.

Philip Sundell, CFA, Vice President and Portfolio Manager, joined American Century in 1997 and has managed the Portfolio since 2019.

Adam Krenn, CFA, Vice President and Senior Investment Analyst, joined American Century in 2011 and has managed the Portfolio since 2022.

Kevin Toney, CFA, Chief Investment Officer – Global Value Equity, Senior Vice President and Senior Portfolio Manager, joined American Century in 1999 and has managed the Portfolio since 2025.

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: Brian Woglom, CFA, Vice President and Senior Portfolio Manager, joined American Century in 2005 and has managed the Portfolio since 2016.

Philip Sundell, CFA, Vice President and Portfolio Manager, joined American Century in 1997 and has managed the Portfolio since 2019.

Adam Krenn, CFA, Vice President and Senior Investment Analyst, joined American Century in 2011 and has managed the Portfolio since 2022.

Kevin Toney, CFA, Chief Investment Officer – Global Value Equity, Senior Vice President and Senior Portfolio Manager, joined American Century in 1999 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 22

Domestic Equity Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

PRINCIPAL RISKS

23 Northwestern Mutual Series Fund, Inc. Prospectus

Domestic Equity Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 24

Domestic Equity Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Domestic Equity Portfolio |

|

|

|

| Strategy Index: |

Russell 1000® Value Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Putnam Investment Management, LLC (Putnam)

Portfolio Managers: Darren Jaroch, CFA, Portfolio Manager, has been with Putnam since 1999, and has managed the Portfolio since 2025.

Lauren DeMore, CFA, Portfolio Manager, has been with Putnam since 2006, and has managed the Portfolio since 2025.

Sub-Adviser: Putnam Investment Management, LLC (Putnam)

Portfolio Managers: Darren Jaroch, CFA, Portfolio Manager, has been with Putnam since 1999, and has managed the Portfolio since 2025.

Lauren DeMore, CFA, Portfolio Manager, has been with Putnam since 2006, and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

25 Northwestern Mutual Series Fund, Inc. Prospectus

Equity Income Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 26

Equity Income Portfolio – Summary

27 Northwestern Mutual Series Fund, Inc. Prospectus

Equity Income Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Equity Income Portfolio |

|

|

|

| Strategy Index: |

Russell 1000® Value Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: John D. Linehan, CFA, Vice President, has been with TRPA since 1998. He has managed the Portfolio since November 2015.

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: John D. Linehan, CFA, Vice President, has been with TRPA since 1998. He has managed the Portfolio since November 2015.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 28

Mid Cap Growth Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

|

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

29 Northwestern Mutual Series Fund, Inc. Prospectus

Mid Cap Growth Stock Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 30

Mid Cap Growth Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Mid Cap Growth Stock Portfolio |

|

|

|

| Strategy Index: |

Russell MidCap® Growth Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: J.P. Morgan Investment Management, Inc. (JPMIM)

Portfolio Managers: Felise L. Agranoff, CFA, Managing Director of JPMIM and Portfolio Manager, joined JPMIM in 2004 and has managed the Portfolio since 2024.

Michael Stein, CFA, Managing Director of JPMIM and Portfolio Manager, joined JPMIM in 2014 and has managed the Portfolio since 2025.

Sub-Adviser: J.P. Morgan Investment Management, Inc. (JPMIM)

Portfolio Managers: Felise L. Agranoff, CFA, Managing Director of JPMIM and Portfolio Manager, joined JPMIM in 2004 and has managed the Portfolio since 2024.

Michael Stein, CFA, Managing Director of JPMIM and Portfolio Manager, joined JPMIM in 2014 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

31 Northwestern Mutual Series Fund, Inc. Prospectus

Index 400 Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 32

Index 400 Stock Portfolio – Summary

PRINCIPAL RISKS

33 Northwestern Mutual Series Fund, Inc. Prospectus

Index 400 Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Index 400 Stock Portfolio |

|

|

|

| Strategy Index: |

S&P MidCap 400® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Northern Trust Investments, Inc. (Northern Trust)

Portfolio Managers: Lucy Johnston, Portfolio Manager, joined Northern Trust in 1997 and has managed the Portfolio since February 2021.

Keith Carroll, Portfolio Manager, joined Northern Trust in 2007 and has managed the Portfolio since September 2024.

Sub-Adviser: Northern Trust Investments, Inc. (Northern Trust)

Portfolio Managers: Lucy Johnston, Portfolio Manager, joined Northern Trust in 1997 and has managed the Portfolio since February 2021.

Keith Carroll, Portfolio Manager, joined Northern Trust in 2007 and has managed the Portfolio since September 2024.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 34

Mid Cap Value Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses(1) |

|

| Total Annual Portfolio Operating Expenses(1) |

|

| Fee Waiver(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

35 Northwestern Mutual Series Fund, Inc. Prospectus

Mid Cap Value Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 36

Mid Cap Value Portfolio – Summary

37 Northwestern Mutual Series Fund, Inc. Prospectus

Mid Cap Value Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Mid Cap Value Portfolio |

|

|

|

| Strategy Index: |

Russell MidCap® Value Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: Kevin Toney, CFA, Chief Investment Officer - Global Value Equity, Senior Vice President and Senior Portfolio Manager, has served American Century as a Portfolio Manager since 2006 and has managed the Portfolio since 2009.

Brian Woglom, CFA, Vice President and Senior Portfolio Manager, has served American Century as a Portfolio Manager since 2012 and has managed the Portfolio since 2012.

Nathan Rawlins, CFA, Portfolio Manager and Senior Investment Analyst, has served American Century as a Portfolio Manager since March 2022 and has managed the Portfolio since 2022.

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: Kevin Toney, CFA, Chief Investment Officer - Global Value Equity, Senior Vice President and Senior Portfolio Manager, has served American Century as a Portfolio Manager since 2006 and has managed the Portfolio since 2009.

Brian Woglom, CFA, Vice President and Senior Portfolio Manager, has served American Century as a Portfolio Manager since 2012 and has managed the Portfolio since 2012.

Nathan Rawlins, CFA, Portfolio Manager and Senior Investment Analyst, has served American Century as a Portfolio Manager since March 2022 and has managed the Portfolio since 2022.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 38

Small Cap Growth Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses(1) |

|

| Total Annual Portfolio Operating Expenses(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

39 Northwestern Mutual Series Fund, Inc. Prospectus

Small Cap Growth Stock Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 40

Small Cap Growth Stock Portfolio – Summary

41 Northwestern Mutual Series Fund, Inc. Prospectus

Small Cap Growth Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Small Cap Growth Stock Portfolio |

|

|

|

| Strategy Index: |

Russell 2000® Growth Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Wellington Management Company LLP (Wellington Management)

Portfolio Manager: David Siegle, CFA, Managing Director and Equity Portfolio Manager, joined Wellington Management in 2001 and has managed the Portfolio since 2023.

Sub-Adviser: Wellington Management Company LLP (Wellington Management)

Portfolio Manager: David Siegle, CFA, Managing Director and Equity Portfolio Manager, joined Wellington Management in 2001 and has managed the Portfolio since 2023.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 42

Index 600 Stock Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

43 Northwestern Mutual Series Fund, Inc. Prospectus

Index 600 Stock Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 44

Index 600 Stock Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Index 600 Stock Portfolio |

|

|

|

| Strategy Index: |

S&P SmallCap 600® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Northern Trust Investments, Inc. (Northern Trust)

Portfolio Managers: Keith Carroll, Portfolio Manager, joined Northern Trust in 2007 and has managed the Portfolio since 2021.

Lucy Johnston, Portfolio Manager, joined Northern Trust in 1997 and has managed the Portfolio since 2024.

Sub-Adviser: Northern Trust Investments, Inc. (Northern Trust)

Portfolio Managers: Keith Carroll, Portfolio Manager, joined Northern Trust in 2007 and has managed the Portfolio since 2021.

Lucy Johnston, Portfolio Manager, joined Northern Trust in 1997 and has managed the Portfolio since 2024.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

45 Northwestern Mutual Series Fund, Inc. Prospectus

Small Cap Value Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 46

Small Cap Value Portfolio – Summary

PRINCIPAL RISKS

47 Northwestern Mutual Series Fund, Inc. Prospectus

Small Cap Value Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Small Cap Value Portfolio |

|

|

|

| Strategy Index: |

Russell 2000® Value Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: T. Rowe Price Investment Management, Inc. (TRPIM)

Portfolio Manager: J. David Wagner, CFA, a Vice President of TRPIM, has managed the Portfolio in his capacity with TRPIM since 2022 and had managed the Portfolio in his capacity with T. Rowe Price Associates, Inc. since 2014. Mr. Wagner joined T. Rowe Price in 2000.

Sub-Adviser: T. Rowe Price Investment Management, Inc. (TRPIM)

Portfolio Manager: J. David Wagner, CFA, a Vice President of TRPIM, has managed the Portfolio in his capacity with TRPIM since 2022 and had managed the Portfolio in his capacity with T. Rowe Price Associates, Inc. since 2014. Mr. Wagner joined T. Rowe Price in 2000.

Northwestern Mutual Series Fund, Inc. Prospectus 48

Small Cap Value Portfolio – Summary

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

49 Northwestern Mutual Series Fund, Inc. Prospectus

International Growth Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 50

International Growth Portfolio – Summary

PRINCIPAL RISKS

51 Northwestern Mutual Series Fund, Inc. Prospectus

International Growth Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 52

International Growth Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

International Growth Portfolio |

|

|

|

| Strategy Index: |

MSCI EAFE® Growth Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

MSCI® All Country World (ex- US) Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: FIAM LLC (FIAM)

Portfolio Manager: Jed Weiss, Portfolio Manager, has managed the Portfolio since 2015.

Sub-Adviser: FIAM LLC (FIAM)

Portfolio Manager: Jed Weiss, Portfolio Manager, has managed the Portfolio since 2015.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

53 Northwestern Mutual Series Fund, Inc. Prospectus

Research International Core Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1),(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 54

Research International Core Portfolio – Summary

PRINCIPAL RISKS

55 Northwestern Mutual Series Fund, Inc. Prospectus

Research International Core Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Research International Core Portfolio |

|

|

|

| Strategy Index: |

MSCI EAFE® Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

MSCI® All Country World (ex- US) Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

Northwestern Mutual Series Fund, Inc. Prospectus 56

Research International Core Portfolio – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Massachusetts Financial Services Company (MFS®)

Portfolio Managers: John Mahoney, CFA, Investment Officer of MFS, joined MFS in 2005 and has managed the Portfolio since 2024.

Nicholas Paul, CFA, Investment Officer of MFS, joined MFS in 2010 and has managed the Portfolio since 2022.

Sub-Adviser: Massachusetts Financial Services Company (MFS®)

Portfolio Managers: John Mahoney, CFA, Investment Officer of MFS, joined MFS in 2005 and has managed the Portfolio since 2024.

Nicholas Paul, CFA, Investment Officer of MFS, joined MFS in 2010 and has managed the Portfolio since 2022.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

57 Northwestern Mutual Series Fund, Inc. Prospectus

International Equity Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

|

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 58

International Equity Portfolio – Summary

PRINCIPAL RISKS

59 Northwestern Mutual Series Fund, Inc. Prospectus

International Equity Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 60

International Equity Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

International Equity Portfolio |

|

|

|

| Strategy Index: |

MSCI® All Country World (ex- US) Value Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

MSCI® All Country World (ex- US) Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Dodge & Cox

Portfolio Managers: The Portfolio is managed by Dodge & Cox’s International Equity Investment Committee (“IEIC”), whose members are jointly and primarily responsible for the management of the Portfolio. The IEIC consists of the following members:

Roger G. Kuo, CFA, Chief Executive Officer, President, Director, and Research Analyst, joined Dodge & Cox in 1998 and has been an IEIC member since 2006 and has managed the Portfolio since 2021.

Englebert T. Bangayan, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2002 and has been an IEIC member since 2015 and has managed of the Portfolio since 2021.

Sophie Chen, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2012 and has been an IEIC member since 2024 and has managed the Portfolio since 2024.

David C. Hoeft CFA, Chair, Senior Vice President, Director, Chief Investment Officer, joined Dodge & Cox in 1993 and has been an IEIC member since 2025 and has managed the Portfolio since 2025.

Raymond J. Mertens, CFA, Senior Vice President and Director, and Research Analyst, joined Dodge & Cox in 2003 and has been an IEIC member since 2018 and has managed the Portfolio since 2021.

Paritosh Somani, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2007 and has been an IEIC member since 2021 and has managed the Portfolio since 2021.

Sub-Adviser: Dodge & Cox

Portfolio Managers: The Portfolio is managed by Dodge & Cox’s International Equity Investment Committee (“IEIC”), whose members are jointly and primarily responsible for the management of the Portfolio. The IEIC consists of the following members:

Roger G. Kuo, CFA, Chief Executive Officer, President, Director, and Research Analyst, joined Dodge & Cox in 1998 and has been an IEIC member since 2006 and has managed the Portfolio since 2021.

Englebert T. Bangayan, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2002 and has been an IEIC member since 2015 and has managed of the Portfolio since 2021.

Sophie Chen, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2012 and has been an IEIC member since 2024 and has managed the Portfolio since 2024.

David C. Hoeft CFA, Chair, Senior Vice President, Director, Chief Investment Officer, joined Dodge & Cox in 1993 and has been an IEIC member since 2025 and has managed the Portfolio since 2025.

Raymond J. Mertens, CFA, Senior Vice President and Director, and Research Analyst, joined Dodge & Cox in 2003 and has been an IEIC member since 2018 and has managed the Portfolio since 2021.

Paritosh Somani, CFA, Vice President and Research Analyst, joined Dodge & Cox in 2007 and has been an IEIC member since 2021 and has managed the Portfolio since 2021.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

61 Northwestern Mutual Series Fund, Inc. Prospectus

Emerging Markets Equity Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1),(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 62

Emerging Markets Equity Portfolio – Summary

PRINCIPAL RISKS

63 Northwestern Mutual Series Fund, Inc. Prospectus

Emerging Markets Equity Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 64

Emerging Markets Equity Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Emerging Markets Equity Portfolio |

|

|

|

| Broad-Based Index: |

MSCI® Emerging Markets Index (Net) (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: abrdn Investments Limited (Aberdeen)

Portfolio Managers: The Portfolio is managed using a team-based approach, with the following team members being jointly and primarily responsible for the day-to-day management of the Portfolio:

Devan Kaloo, Global Head of Equities and Head of Global Emerging Markets Equities, has managed the Portfolio since 2017.

Nick Robinson, CFA, Senior Investment Director, has managed the Portfolio since February 2023.

Sub-Adviser: abrdn Investments Limited (Aberdeen)

Portfolio Managers: The Portfolio is managed using a team-based approach, with the following team members being jointly and primarily responsible for the day-to-day management of the Portfolio:

Devan Kaloo, Global Head of Equities and Head of Global Emerging Markets Equities, has managed the Portfolio since 2017.

Nick Robinson, CFA, Senior Investment Director, has managed the Portfolio since February 2023.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

65 Northwestern Mutual Series Fund, Inc. Prospectus

Government Money Market Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

PRINCIPAL RISKS

The main risks of investing in this Portfolio are identified below.

Northwestern Mutual Series Fund, Inc. Prospectus 66

Government Money Market Portfolio – Summary

67 Northwestern Mutual Series Fund, Inc. Prospectus

Government Money Market Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

1 Yr |

5 Yr |

10 Yr |

| Government Money Market Portfolio |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: BlackRock Advisors, LLC

Sub-Adviser: BlackRock Advisors, LLC

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 68

Short-Term Bond Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

69 Northwestern Mutual Series Fund, Inc. Prospectus

Short-Term Bond Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 70

Short-Term Bond Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Short-Term Bond Portfolio |

|

|

|

| Strategy Index: |

Bloomberg® 1-3 Year U.S. Government/Credit Bond Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

71 Northwestern Mutual Series Fund, Inc. Prospectus

Short-Term Bond Portfolio – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: Michael F. Reinartz, CFA, Portfolio Manager and Chairman of TRPA’s Short-Term Bond Investment Advisory Committee, joined TRPA in 1996, began managing the Portfolio in 2015 and has co-managed the Portfolio since 2023.

Steve Kohlenstein, CFA, Portfolio Manager and Chairman of TRPA’s Short-Term Bond Investment Advisory Committee, joined TRPA in 1996, and has co-managed the Portfolio since 2023.

Sub-Adviser: T. Rowe Price Associates, Inc. (TRPA)

Portfolio Manager: Michael F. Reinartz, CFA, Portfolio Manager and Chairman of TRPA’s Short-Term Bond Investment Advisory Committee, joined TRPA in 1996, began managing the Portfolio in 2015 and has co-managed the Portfolio since 2023.

Steve Kohlenstein, CFA, Portfolio Manager and Chairman of TRPA’s Short-Term Bond Investment Advisory Committee, joined TRPA in 1996, and has co-managed the Portfolio since 2023.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 72

Select Bond Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

73 Northwestern Mutual Series Fund, Inc. Prospectus

Select Bond Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 74

Select Bond Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Select Bond Portfolio |

|

- |

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Allspring Global Investments, LLC (Allspring)

Portfolio Managers: Maulik Bhansali, CFA, Senior Portfolio Manager and Co-Head of the Core Fixed Income team at Allspring, has managed the Portfolio in his capacity with Allspring since 2021 and had managed the Portfolio in his capacity with the previous sub-adviser since 2017.

Jarad Vasquez, Senior Portfolio Manager and Co-Head of the Core Fixed Income team at Allspring, has managed the Portfolio in his capacity with Allspring since 2021, and had managed the Portfolio in his capacity with the previous sub-adviser since 2017.

Sub-Adviser: Allspring Global Investments, LLC (Allspring)

Portfolio Managers: Maulik Bhansali, CFA, Senior Portfolio Manager and Co-Head of the Core Fixed Income team at Allspring, has managed the Portfolio in his capacity with Allspring since 2021 and had managed the Portfolio in his capacity with the previous sub-adviser since 2017.

Jarad Vasquez, Senior Portfolio Manager and Co-Head of the Core Fixed Income team at Allspring, has managed the Portfolio in his capacity with Allspring since 2021, and had managed the Portfolio in his capacity with the previous sub-adviser since 2017.

75 Northwestern Mutual Series Fund, Inc. Prospectus

Select Bond Portfolio – Summary

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 76

Long-Term U.S. Government Bond Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses(1) |

|

| Interest Expense |

|

| Other Operating Expense |

|

| Total Annual Portfolio Operating Expenses(1) |

|

| Expense Reimbursement(2) |

( |

| Total Annual Portfolio Operating Expenses After Expense Reimbursement(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

77 Northwestern Mutual Series Fund, Inc. Prospectus

Long-Term U.S. Government Bond Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 78

Long-Term U.S. Government Bond Portfolio – Summary

79 Northwestern Mutual Series Fund, Inc. Prospectus

Long-Term U.S. Government Bond Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Long-Term U.S. Government Bond Portfolio |

|

- |

- |

| Strategy Index: |

Bloomberg® Long-Term Treasury Index |

|

- |

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

Northwestern Mutual Series Fund, Inc. Prospectus 80

Long-Term U.S. Government Bond Portfolio – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Michael Cudzil joined PIMCO in 2012 and is a Managing Director in PIMCO’s Newport Beach office. He has managed the Portfolio since 2016.

Tim Crowley joined PIMCO in 2008 and is an Executive Vice President in PIMCO’s Newport Beach office. He has managed the Portfolio since 2025.

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Michael Cudzil joined PIMCO in 2012 and is a Managing Director in PIMCO’s Newport Beach office. He has managed the Portfolio since 2016.

Tim Crowley joined PIMCO in 2008 and is an Executive Vice President in PIMCO’s Newport Beach office. He has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

81 Northwestern Mutual Series Fund, Inc. Prospectus

Inflation Managed Portfolio (formerly Inflation Protection Portfolio) – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(1) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1) |

|

(1)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 82

Inflation Managed Portfolio (formerly Inflation Protection Portfolio) – Summary

PRINCIPAL RISKS

83 Northwestern Mutual Series Fund, Inc. Prospectus

Inflation Managed Portfolio (formerly Inflation Protection Portfolio) – Summary

sensitive to changes in interest rates than a portfolio with a shorter average portfolio duration. For example, the market value of a fixed income portfolio with an average duration of five years generally would be expected to fall approximately 5% if interest rates rose by one percentage point. Declining interest rates may increase the risk that an issuer calls outstanding securities prior to their maturity.

Northwestern Mutual Series Fund, Inc. Prospectus 84

Inflation Managed Portfolio (formerly Inflation Protection Portfolio) – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Inflation Managed Portfolio |

|

|

|

| Strategy Index: |

Bloomberg® U.S. Treasury Inflation Protected Securities (TIPS) Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: James E. Platz, CFA, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2003 and has managed the Portfolio since 2008.

Miguel Castillo, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2014 and has managed the Portfolio since 2015.

Stephen Bartolini, CFA, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2024 and has managed the Portfolio since 2024.

Sub-Adviser: American Century Investment Management, Inc. (American Century)

Portfolio Managers: James E. Platz, CFA, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2003 and has managed the Portfolio since 2008.

Miguel Castillo, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2014 and has managed the Portfolio since 2015.

Stephen Bartolini, CFA, Vice President and Portfolio Manager, has served American Century as a portfolio manager since 2024 and has managed the Portfolio since 2024.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

85 Northwestern Mutual Series Fund, Inc. Prospectus

High Yield Bond Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Total Annual Portfolio Operating Expenses |

|

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 86

High Yield Bond Portfolio – Summary

87 Northwestern Mutual Series Fund, Inc. Prospectus

High Yield Bond Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

High Yield Bond Portfolio |

|

|

|

| Strategy Index: |

Bloomberg® U.S. Corporate High Yield 2% Issuer Capped Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Federated Investment Management Company (Federated)

Portfolio Manager: Mark E. Durbiano, CFA, Senior Portfolio Manager and Senior Vice President of Federated, has been with Federated since 1982 and has managed the Portfolio since 2014.

Kathryn Glass, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 1999 and has managed the Portfolio since 2024.

Thomas Scherr, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 2006 and has managed the Portfolio since 2024.

Randal Stuckwish, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 2013 and has managed the Portfolio since 2024.

Sub-Adviser: Federated Investment Management Company (Federated)

Portfolio Manager: Mark E. Durbiano, CFA, Senior Portfolio Manager and Senior Vice President of Federated, has been with Federated since 1982 and has managed the Portfolio since 2014.

Kathryn Glass, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 1999 and has managed the Portfolio since 2024.

Thomas Scherr, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 2006 and has managed the Portfolio since 2024.

Randal Stuckwish, CFA, Portfolio Manager and Vice President of Federated, has been with Federated since 2013 and has managed the Portfolio since 2024.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 88

Multi-Sector Bond Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses(1) |

|

| Interest Expense |

|

| Other Operating Expense |

|

| Total Annual Portfolio Operating Expenses |

|

| Fee Waiver(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

89 Northwestern Mutual Series Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 90

Multi-Sector Bond Portfolio – Summary

91 Northwestern Mutual Series Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 92

Multi-Sector Bond Portfolio – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Multi-Sector Bond Portfolio |

|

|

|

| Strategy Index: |

1/3 each: Bloomberg® Global Aggregate — Credit Component ex Emerging Markets, Hedged USD; ICE BofA® Global High Yield BB-B Rated Constrained Developed Markets Index, Hedged USD; JP Morgan® EMBI Global (reflects no deduction for fees, expenses or taxes) |

|

|

|

| Broad-Based Index: |

Bloomberg® Global Aggregate Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Sonali Pier, Managing Director of PIMCO, joined PIMCO in 2013 and has managed the Portfolio since 2018.

Daniel J. Ivascyn, Group Chief Investment Officer and Managing Director of PIMCO, joined PIMCO in 1998 and has managed the Portfolio since 2016.

Alfred T. Murata, Managing Director of PIMCO, joined PIMCO in 2001 and has managed the Portfolio since 2016.

Charles Watford, Executive Vice President of PIMCO, joined PIMCO in 2007, and has managed the Portfolio since 2022.

Regina Borromeo, Executive Vice President of PIMCO, joined PIMCO in 2022, and has managed the Portfolio since 2022.

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Sonali Pier, Managing Director of PIMCO, joined PIMCO in 2013 and has managed the Portfolio since 2018.

Daniel J. Ivascyn, Group Chief Investment Officer and Managing Director of PIMCO, joined PIMCO in 1998 and has managed the Portfolio since 2016.

Alfred T. Murata, Managing Director of PIMCO, joined PIMCO in 2001 and has managed the Portfolio since 2016.

Charles Watford, Executive Vice President of PIMCO, joined PIMCO in 2007, and has managed the Portfolio since 2022.

Regina Borromeo, Executive Vice President of PIMCO, joined PIMCO in 2022, and has managed the Portfolio since 2022.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

93 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Very Aggressive Portfolio (formerly Active/Passive All Equity

Portfolio) – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Acquired Fund Fees and Expenses |

|

| Total Annual Portfolio Operating Expenses(1) |

|

| Fee Waiver and Expense Reimbursement(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver and Expense Reimbursement(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

Northwestern Mutual Series Fund, Inc. Prospectus 94

Active/Passive Very Aggressive Portfolio (formerly Active/Passive All Equity Portfolio) – Summary

| |

|

|

|

| |

|

|

|

PRINCIPAL RISKS

95 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Very Aggressive Portfolio (formerly Active/Passive All Equity

Portfolio) – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 96

Active/Passive Very Aggressive Portfolio (formerly Active/Passive All Equity Portfolio) – Summary

97 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Very Aggressive Portfolio (formerly Active/Passive All Equity

Portfolio) – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC (MSA)

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Brent G. Schutte, CFA, Chief Investment Officer of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Garrett D. Aird, CFA, Vice President of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Brent G. Schutte, CFA, Chief Investment Officer of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Garrett D. Aird, CFA, Vice President of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 98

Active/Passive Aggressive Portfolio – Summary

| |

|

| |

|

| Management Fee |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Acquired Fund Fees and Expenses |

|

| Total Annual Portfolio Operating Expenses(1) |

|

| Fee Waiver and Expense Reimbursement(2) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver and Expense Reimbursement(1),(2) |

|

(1)

(2)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

99 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Aggressive Portfolio – Summary

| |

|

|

|

| |

|

|

|

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 100

Active/Passive Aggressive Portfolio – Summary

101 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Aggressive Portfolio – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 102

Active/Passive Aggressive Portfolio – Summary

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC (MSA)

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

103 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Aggressive Portfolio – Summary

Brent G. Schutte, CFA, Chief Investment Officer of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Garrett D. Aird, CFA, Vice President of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 104

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

| |

|

| |

|

| Management Fee(1) |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Acquired Fund Fees and Expenses |

|

| Total Annual Portfolio Operating Expenses(2) |

|

| Fee Waiver(1),(3) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2),(3) |

|

(1)

(2)

(3)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

105 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

| |

|

|

|

| |

|

|

|

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 106

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

107 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

Northwestern Mutual Series Fund, Inc. Prospectus 108

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

109 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Moderate Portfolio (formerly Asset Allocation Portfolio) – Summary

| |

|

|

| |

|

|

| |

|

|

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Active/Passive Moderate Portfolio |

|

|

|

| Strategy Index: |

Active/Passive Moderate Portfolio Blended Composite Benchmark: S&P 500® Index (28%), S&P 400® MidCap Index (7%), S&P SmallCap 600® Index (3%), MSCI EAFE® Index (15%), MSCI® Emerging Markets Index (6%), Dow Jones U.S. Select REIT Index (4%), Bloomberg® Commodity IndexSM (5%), Bloomberg® Barclays U.S. Aggregate Bond Index (30%), and ICE of BofA® US 3-Month Treasury Bill Index (2%) |

|

|

|

| Broad-Based Index: |

Bloomberg® U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) |

|

- |

|

| Broad-Based Index: |

S&P 500® Index (reflects no deduction for fees, expenses or taxes) |

|

|

|

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC (MSA)

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Brent G. Schutte, CFA, Chief Investment Officer of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Garrett D. Aird, CFA, Vice President of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Portfolio Managers: James Fleming, CFA, Portfolio Manager of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Rodney Schmucker, CFA, Senior Research & Portfolio Analyst of MSA, joined MSA in 2008 and has managed the Portfolio since 2025.

Brent G. Schutte, CFA, Chief Investment Officer of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

Garrett D. Aird, CFA, Vice President of MSA, joined MSA in December 2021 and has managed the Portfolio since 2025.

TAXES AND INTERMEDIARY COMPENSATION

For important information about taxes, dividends and financial intermediary compensation, please see “SUMMARY OF IMPORTANT INFORMATION REGARDING THE PORTFOLIOS” on page 123 of the Northwestern Mutual Series Fund, Inc. Prospectus.

Northwestern Mutual Series Fund, Inc. Prospectus 110

Active/Passive Balanced Portfolio (formerly Balanced Portfolio) – Summary

| |

|

| |

|

| Management Fee(1) |

|

| Distribution and Service (12b-1) Fees |

|

| Other Expenses |

|

| Acquired Fund Fees and Expenses |

|

| Total Annual Portfolio Operating Expenses(2) |

|

| Fee Waiver(1),(3) |

( |

| Total Annual Portfolio Operating Expenses After Fee Waiver(1),(2),(3) |

|

(1)

(2)

(3)

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

111 Northwestern Mutual Series Fund, Inc. Prospectus

Active/Passive Balanced Portfolio (formerly Balanced Portfolio) – Summary

| |

|

|

|

| |

|

|

|

PRINCIPAL RISKS

Northwestern Mutual Series Fund, Inc. Prospectus 112

Active/Passive Balanced Portfolio (formerly Balanced Portfolio) – Summary

113 Northwestern Mutual Series Fund, Inc. Prospectus