Multi-Sector Bond Portfolio

SUMMARY PROSPECTUS

MAY 1, 2026

Before you invest, you may want to review the Portfolio’s prospectus, which contains more information about the Portfolio and its risks. You can find the Portfolio’s prospectus, reports to shareholders, and other information about the Portfolio online at www.nmseriesfund.com. You can also get this information at no cost by calling (866) 910-1232 or by sending an e-mail request to sfprospectus@northwesternmutual.com. The current prospectus and statement of additional information, each dated May 1, 2026, along with the Portfolio’s most recent annual report dated December 31, 2025, are incorporated by reference into this Summary Prospectus. The Portfolio’s statement of additional information and annual report may be obtained, free of charge, in the same manner as the prospectus.

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

INVESTMENT OBJECTIVE

The investment objective of the Portfolio is to seek maximum total return, consistent with prudent investment management.

FEES AND EXPENSES OF THE PORTFOLIO

The table below describes the fees and expenses that you may pay when you buy, hold, and

sell interests in a separate account that invests in shares of the Portfolio as a result of your purchase of a variable annuity contract or variable

life insurance policy. The fees and expenses shown in the table and Example do not reflect fees and expenses separately charged by variable annuity

contracts or variable life insurance policies. If the fees and expenses separately charged by variable annuity contracts and variable life insurance

policies were included, the fees and expenses shown in the table and the Example would be higher.

| Shareholder Fees

(fees paid directly from your investment) |

N/A |

| Annual Portfolio Operating

Expenses (expenses that you pay each year as a percentage

of the value of your investment) |

|

| Management Fee |

0.77% |

| Distribution and Service (12b-1) Fees |

None |

| Other Expenses(1) |

0.08% |

| Interest Expense |

0.03% |

| Other Operating Expense |

0.05% |

| Total Annual Portfolio Operating Expenses |

0.85% |

| Fee Waiver(2) |

(0.10)% |

| Total Annual Portfolio Operating Expenses After

Fee Waiver(1),(2)

|

0.75% |

(1)

“Other Expenses” include interest expense of 0.03%. Interest expense is borne by the Portfolio separately from the management fees paid to the

Portfolio’s investment adviser, Mason Street Advisors, LLC, and the Portfolio’s sub-adviser, Pacific Investment Management Company LLC. Excluding interest expense, Total Annual Portfolio

Operating Expenses are 0.82% and Total Annual Portfolio Operating Expenses After

Expense Reimbursement are 0.72%.

(2)

The Portfolio's investment adviser has contractually agreed to waive a portion of its management fee. This contractual agreement will continue through at

least April 30, 2027 and may not be terminated prior to that date without action by the Board of Directors.

Example

This Example is intended to help you compare the cost of investing

in the Portfolio with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Portfolio for the time periods indicated and then redeem or hold

all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Portfolio’s operating expenses remain the same.

The Example reflects adjustments made to the Portfolio's

operating expenses due to the fee waiver agreement with the investment adviser for the first year only. Although your actual

costs may be higher or lower, based on these assumptions your costs

would be:

| 1 Year |

3 Years |

5 Years |

10 Years |

| $77 |

$261 |

$462 |

$1,040 |

Portfolio Turnover

The Portfolio pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in Annual Portfolio Operating Expenses or in the Example, affect the Portfolio’s performance. During the most recent fiscal year, the Portfolio’s portfolio turnover rate was 36% of

the average value of its portfolio.

PRINCIPAL

INVESTMENT STRATEGIES

Normally, the Portfolio invests at least 80%

of net assets (plus any borrowings for investment purposes) in debt securities. The debt securities may be represented by forwards or derivatives such

as options, futures contracts or swap agreements that have economic

NMSF-SP1Northwestern Mutual Series Fund, Inc.

Multi-Sector Bond Portfolio – Summary

characteristics that are similar to the debt securities included in the 80% policy. The

average portfolio duration of the Portfolio normally varies from three to eight years, based on the adviser’s forecast for interest rates.

Duration is a measure of the sensitivity of the price of the Portfolio’s fixed income securities to changes in interest rates; the longer the

duration, the more sensitive the price will be to changes in interest rates.

The Portfolio may invest, without limitation, in high yield securities subject to a maximum of 10% of its total assets in

securities rated below B by Moody’s or equivalently rated by S&P or Fitch or, if unrated, determined by the Portfolio’s adviser to be of

comparable quality. High yield securities, commonly referred to as “junk” bonds, are non-investment grade securities. A security is considered to be non-investment grade when it is rated below investment grade by at least two of the three credit ratings agencies (BB+ or lower by S&P; Ba1 or lower by Moody’s; BB+ or lower by Fitch) or, if unrated, determined by the Portfolio’s adviser to be of comparable quality. The Portfolio may invest, without limitation, in securities denominated in foreign currencies and U.S. dollar denominated securities of foreign issuers. In addition, the Portfolio may invest, without limitation, in fixed income securities of issuers that are economically tied to emerging securities markets. The Portfolio may invest in illiquid securities. The Portfolio may also invest up to 10% of its net assets in preferred stocks.

The Portfolio may invest, without limitation, in derivative instruments, such as options, futures contracts or swap agreements

including the purchase or sale of credit defaults swaps, and interest rate swaps (to take a position on interest rates moving either up or down), in municipal bonds, contingent convertible securities, or in mortgage- or asset-backed securities, subject to the Portfolio’s objective and policies. The Portfolio may utilize currency forwards and currency options to manage or hedge currency exposure. The Portfolio may invest in mortgage- or asset-backed securities which are non-investment grade. Mortgage-backed securities may include residential and commercial mortgage-backed securities issued by a Federal agency and private label residential and commercial mortgage-backed securities. The adviser may invest in derivatives at any time it deems appropriate, generally when relative value and liquidity conditions make these investments more attractive relative to cash bonds.

The Portfolio may purchase or sell securities on a

when-issued, delayed delivery or forward commitment basis and may engage in short sales. A short sale involves the sale of a security that is borrowed

from a broker or other institution, and which must be purchased in the market at a later date and returned to the lender. The Portfolio may, without

limitation, seek to obtain market exposure to the securities in which it primarily invests by entering into a series of purchase and sale contracts or

by using other investment techniques (such as buy backs or dollar rolls). The Portfolio may invest in repurchase agreements; however, it may not invest more than 10% of its total assets in repurchase agreements which have maturities of more than seven days, nor invest in any repurchase agreements with maturities over 30 days. The Portfolio may invest up to 10% of its net assets in fixed- and floating-rate loans, including senior loans, and such investments may be in the form of loan participations and assignments. Senior loans are considered speculative instruments.

The “total return” sought by the Portfolio consists of income earned on the Portfolio’s investments, plus capital appreciation, if any, which generally arises from a decrease in interest rates or improving credit fundamentals for a particular sector or security. The Portfolio may engage in frequent and active trading of portfolio securities to achieve its investment objective, particularly during periods of volatile market movements.

In selecting securities for a Portfolio, the adviser develops an outlook for interest rates, foreign currency exchange rates and the economy, analyzes credit and call risks, which involves both macro and fundamental analysis. The proportion of a Portfolio’s assets committed to investment in securities with particular characteristics (such as quality, sector, interest rate or maturity) varies based on the adviser’s outlook for the U.S. and foreign economies, the financial markets and other factors.

The adviser attempts to identify areas of the bond market

that are undervalued relative to the rest of the market. The adviser identifies these areas by grouping bonds into the following sectors: money markets,

governments, corporates, mortgages, asset-backed and international. Sophisticated proprietary software then assists in evaluating sectors and pricing

specific securities. Once investment opportunities are identified, the adviser will shift assets among sectors depending upon changes in relative

valuations and credit spreads.

The Portfolio may sell a position when, in the adviser’s opinion, it no longer represents a good value, when a superior risk/return opportunity exists in a substitute position, or when it no longer fits within the Portfolio’s macroeconomic or structural strategy.

PRINCIPAL RISKS

Portfolio shares will rise and fall in value and there is a risk you could lose money by

investing in the Portfolio. There can be no assurance that the Portfolio will achieve its objective. The main risks of investing in this Portfolio are identified below.

•

Active Management Risk – The adviser’s investment strategies and techniques may not perform as expected and the adviser’s quality determinations with respect to securities that are unrated by the major credit rating agencies may be inaccurate, which could cause the Portfolio to underperform other mutual funds or lose money.

•

Contingent Convertible Securities Risk – Investing in convertible

contingent securities may subject the Portfolio to the risk of the occurrence of a triggering event which, depending on the underlying circumstances, may result in the

issuer converting the security to an equity interest or writing down the principal value of such securities (either partially or in full). In addition, coupons associated with contingent convertible securities are typically fully discretionary, and coupon payments can be deferred or cancelled by the issuer without causing an event of default.

•

Convertible Securities Risk – Convertible securities (which can be bonds, notes, debentures, preferred stock, or other securities

NMSF-SP2Northwestern Mutual Series

Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

which are convertible into or exercisable for common stock), are subject to both the credit and interest rate risks associated with fixed income securities and to the stock market risk associated with equity securities. The value of a convertible security may not increase or decrease as rapidly as the underlying common stock. The Portfolio may be forced to convert a security before it would otherwise choose, which may have an adverse effect on the Portfolio’s ability to achieve its investment objective.

•

Counterparty Risk – The Portfolio may sustain a loss in the event the other party(s) in an agreement or a participant to a transaction, such as a broker or swap counterparty, defaults on a contract or fails to perform by failing to pay amounts due, failing to fulfill delivery conditions, or failing to otherwise comply with the terms of the contract. Counterparty risk is inherent in many transactions, including derivatives transactions.

•

Credit Risk – The Portfolio could lose money if the issuer or guarantor of a fixed income security is unwilling or unable to meet its financial obligations. In addition, changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Portfolio’s investment in that issuer. Changes in credit spreads or improvements in an issuer’s credit quality may increase the risk that an issuer calls outstanding securities prior to their maturity.

•

Debt Obligations of Foreign Governments Risk – The issuer of the foreign debt or the governmental authorities that control the repayment of such

debt may be unable or unwilling to repay principal or interest when due, and the Portfolio may have limited recourse in the event of a default. The market prices of

debt obligations of governments and their agencies, and the Portfolio’s net asset value, may be more volatile than prices of U.S. debt obligations.

•

Derivatives Risk – The value of a derivative generally depends upon, or is derived from, an underlying asset, reference rate or index. The Portfolio’s use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in securities or other traditional investments. Investments in derivatives may not have the intended effects and may result in losses for the Portfolio that may not otherwise have occurred or missed opportunities for the Portfolio. Certain derivatives involve leverage, which could cause the Portfolio to lose more than the principal amount invested. The derivatives could involve management, credit, interest rate, liquidity and market risks, and the risks of misplacing or improper valuation. Changes in the value of the derivative may not correlate as intended with the underlying asset, rate or index. In addition, the Portfolio could sustain a loss in the event the counterparty to a derivatives transaction fails to make the required payments or otherwise comply with the terms of the contract. The Portfolio’s purchase of forwards and futures contracts may involve risks related to imperfect correlation between the prices of such instruments and the price of the underlying asset, as well as leverage, liquidity and volatility risks. In addition, the purchase of forwards also involves counterparty credit risk as well as heightened market risk. The Portfolio’s purchase of total return equity swap agreements may pose risk arising from losses if the underlying reference asset does not perform as anticipated; such agreements are also subject to counterparty credit, liquidity and leveraging risks. The Portfolio’s use of options involve risk related to the direction and timing of market movements in the price of the underlying asset, obligations related to exercise of the option, and potential loss in value of the initial investment.

•

Emerging Markets Risk – Investing in emerging market securities increases foreign investing risk, and may subject the

Portfolio to more rapid and extreme changes in the value of its holdings compared with investments made in U.S. securities or in foreign, developed countries. Investments in emerging markets may be subject to political, economic, legal, market, and currency risks. Emerging market securities trade in smaller markets which may experience significant price and market volatility, fluctuations in currency values, interest rates and commodity prices, higher transaction costs, and the increased likelihood of the occurrence of trading difficulties, such as delays in executing, clearing and settling Portfolio transactions or in receiving payment of dividends. Special risks associated with investments in emerging market issuers may include a lack of publicly available information, a lack of uniform disclosure, accounting, financial reporting, and recordkeeping standards, and more limited investor protection provisions when compared with developed economies. Emerging market risks also may include unpredictable and changing political, economic and tax policies, the imposition of capital controls and/or foreign investment limitations by a country, nationalization of businesses, and the imposition of sanctions or restrictions in certain investments by other countries, such as the United States.

•

Equity Securities Risk – The value of equity securities, such as common and

preferred stocks, could decline if the financial condition of the companies the Portfolio is invested in declines or if overall market and economic conditions

deteriorate. Equity securities generally have greater price volatility than fixed income securities.

•

Foreign Currency Risk – The risk that foreign (non-U.S. dollar) currency denominated securities, or derivatives that provide exposure to foreign currencies, may be adversely affected by decreases in foreign currency values relative to the U.S. dollar, or, in the case of hedged positions, that the U.S. dollar will decline in value relative to the currency being hedged. Investments in securities subject to foreign currency risk may have more rapid and extreme changes in value or more losses than investments in U.S. dollar denominated securities.

•

Foreign Investing Risk – Investing in foreign securities may subject the Portfolio to more rapid and extreme changes in value or more losses than a fund that invests exclusively in U.S. securities. This risk is due to potentially smaller markets, differing reporting, accounting and auditing standards, and nationalization, expropriation or confiscatory taxation, currency blockage, political and economic conditions, or diplomatic developments. Foreign securities may be less liquid, more volatile, and harder to value than U.S. securities.

•

High Portfolio Turnover Risk – Active and frequent trading may cause higher

brokerage expenses and other transaction costs, which may adversely affect the Portfolio’s performance.

NMSF-SP3Northwestern Mutual Series Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

•

High Yield Debt Risk – High yield debt securities (so called “junk

bonds”) in which the Portfolio invests have greater interest rate and credit risk, may be more difficult to sell or sell at a reasonable price, have greater risk

of loss than higher rated securities, and are predominantly speculative with respect to an issuer’s ability to pay interest and repay principal. In addition,

high yield debt securities may be particularly sensitive to changes in the securities markets.

•

Inflation Risk – Your investment in the Portfolio may not provide enough income to keep pace with inflation.

•

Interest Rate Risk – Prices of fixed income instruments generally rise and fall in response to changes in market interest rates. In a rising interest rate environment, the value of the Portfolio’s fixed income investments is likely to decline. A significant rise in interest rates over a short period of time could cause significant losses in the market value of the Portfolio’s fixed income instruments. A portfolio with a longer average portfolio duration will be more sensitive to changes in interest rates than a portfolio with a shorter average portfolio duration. For example, the market value of a fixed income portfolio with an average duration of five years generally would be expected to fall approximately 5% if interest rates rose by one percentage point. Declining interest rates may increase the risk that an issuer calls outstanding securities prior to their maturity.

•

Issuer Risk – The risk that the value of a security may decline for a

reason directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services.

•

Leverage Risk – Certain transactions, such as when issued, delayed delivery

or forward commitments transactions, or the use of derivative transactions, may give rise to leverage, causing more volatility than if the Portfolio had not been

leveraged.

•

Loan Risk – The risks associated with investing in fixed- and floating-rate

loans, including senior loans, through loan participations and assignments or otherwise, can include credit risk, interest rate risk, liquidity risk, call risk,

settlement risk, and risks associated with being a lender. With respect to senior loans, there may also be heightened credit risk to the extent such loans are below investment grade and made to less creditworthy companies. Senior loans that are considered to be “covenant-lite” offer less protection to the loan holder and may have increased credit risk and call risk.

•

Liquidity Risk – Fixed income and derivative investments can be difficult to purchase or sell at an advantageous time or price, if at all, during periods of reduced marketability for the investment or due to the size of the transaction. These risks may be magnified during periods of economic turmoil or in an extended economic downturn or when investing in emerging markets.

•

Market Risk – The risk that the market price of securities owned by the

Portfolio may go up or down, sometimes rapidly or unpredictably. The value of a security may decline due to changes in general market conditions, economic trends or

events that are not specifically related to the issuer of the security, or factors that affect a particular issuer or issuers, exchange, country, group of countries, region, market, industry, group of industries, sector or asset class. Global economies and financial markets are increasingly interconnected, which magnifies the potential that conditions in one country or region might adversely impact issuers in, or foreign exchange rates with, a different country or region. Geopolitical and other events, including war, terrorism, economic uncertainty, trade disputes, tariffs, public health crises (such as epidemics and pandemics), and related events have led, and in the future may lead, to increased market volatility, which may disrupt U.S. and world economies and markets and may have significant adverse direct or indirect effects on the Portfolio and its investments.

•

Mortgage- and Asset-Backed Securities Risk – The risks of investing in mortgage-related and other asset-backed securities, including interest

rate risk, credit risk, liquidity risk, prepayment risk and extension risk. Privately-issued mortgage-backed securities carry a heightened risk of nonpayment because

there are no direct or indirect government or agency guarantees of payments. The use of mortgage dollar rolls involves potential risks of loss that are different from

those related to the mortgage securities underlying the transactions, including counterparty risk, market risk, and financial risk (including the risk that the value of the principal and interest payments associated with the mortgage instrument sold to a counterparty exceeds the compensation paid to the Portfolio by the counterparty). Asset-backed securities are subject to risks similar to those associated with mortgage-backed securities, as well as risks associated with the nature and servicing of the assets underlying the securities. Asset-backed securities may not have the benefit of a security interest in collateral comparable to that of mortgage assets, resulting in additional credit risk. Investments in mortgage-related and other asset-backed securities that are non-investment grade may have heightened liquidity risk.

•

Municipal Securities Risk – The value of municipal securities in which the Portfolio invests may be more sensitive to certain

adverse conditions than other fixed income securities and the yields of municipal securities may move differently and adversely compared to the yields of the overall debt securities markets. Certain municipal securities may be or become highly illiquid. Illiquidity may be exacerbated from time to time by market or economic events. Municipal securities may lose their tax-exempt status if certain legal requirements are not met, or if federal or state tax laws change. The Portfolio’s investments in certain municipal securities with principal and interest payments that are made from the revenues of a specific project or facility, and not general tax revenues, may have increased risks.

•

Preferred Stocks Risk – Preferred stocks often lack a fixed maturity or redemption date and are therefore more susceptible to price fluctuations when interest rates change. They also carry a greater risk of non-receipt of income because unlike interest on debt securities, dividends on preferred stocks must be declared by the issuer’s board of directors before becoming payable.

•

Prepayment and Extension Risk – Prepayment risk is the risk that principal

on a debt obligation will be paid earlier than scheduled or expected, which could reduce yield and market value of the security and shorten the Portfolio’s

average effective maturity. The rate of prepayments tends to increase as interest rates fall. Extension risk is the risk that, as interest rates rise,

NMSF-SP4Northwestern Mutual Series Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

repayments on a debt obligation may occur more slowly than anticipated by the market and the obligation may remain outstanding longer.

•

Repurchase Agreements Risk – If the other party to a repurchase agreement defaults on its obligation under the agreement, the

Portfolio may suffer delays and incur costs or lose money in exercising its rights under the agreement. These risks may be heightened if the other party is located outside of the U.S. If the seller fails to repurchase the security and the market value of the security declines, the Portfolio may lose money.

•

Short Sale Risk – The risk of entering into short sales, including the potential loss of more money than the actual cost of the investment, and the risk that the third party to the short sale may fail to honor its contract terms, causing a loss to the Portfolio.

•

Underlying Portfolio Risk – The Portfolio may serve as an investment

option, or “Underlying Portfolio,” for other portfolios of Northwestern Mutual Series Fund, Inc. that are managed as “fund of funds.” As a

result, from time to time, the Portfolio may experience relatively large investments or redemptions from those other portfolios and could be required to invest cash or

sell securities at a time when it is not advantageous to do so.

•

U.S. Government Securities Risk – Not all obligations of the U.S. government, its agencies and instrumentalities are backed by the

full faith and credit of the U.S. Treasury. Some obligations are backed only by the credit of the issuing agency or instrumentality, and in some cases there may be

some risk of default by the issuer. Any guarantee by the U.S. government or its agencies or instrumentalities of a security held by the Portfolio does not apply to the

market value of such security or to shares of the Portfolio itself.

•

When Issued, Delayed Delivery and Forward Commitment Risk

– When issued, delayed delivery purchases and forward commitment transactions

involve a risk of loss if the value of the securities declines prior to the settlement date. This risk is in addition to the risk that the Portfolio’s other

assets will decline in value. Therefore, these transactions may result in a form of leverage and increase the Portfolio’s overall investment

expense.

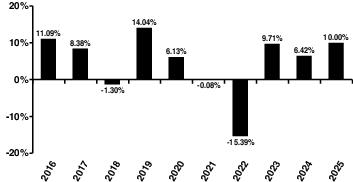

PERFORMANCE

The following bar chart illustrates the risks of investing in the Portfolio by showing how the performance of the Portfolio has varied from year to year. The table to the right of the bar chart shows the Portfolio’s average annual total return over certain time periods and compares the Portfolio’s returns with those of an index that has characteristics relevant to the Portfolio’s investment strategy (Strategy Index). The table also shows the Portfolio’s returns against an index that represents the overall securities market (Broad-Based Index), which the Portfolio has added to comply with new regulatory requirements. Returns are based on past results and are not an indication of future

performance. Neither the bar chart nor the table reflects the fees and expenses separately charged by the variable annuity contract or variable life insurance policy separate account that invests in the Portfolio and returns would be lower if those fees and expenses were reflected.

| |

Quarter/Year |

Return |

| Best Quarter |

2nd quarter, 2020 |

10.18% |

| Worst Quarter |

1st quarter, 2020 |

-10.35% |

Average Annual Total Return

(for periods ended December 31, 2025)

(for periods ended December 31, 2025)

| |

|

1 Yr |

5 Yr |

10 Yr |

| Portfolio: |

Multi-Sector Bond Portfolio |

10.00% |

1.66% |

4.56% |

| Strategy Index: |

1/3 each: Bloomberg® Global

Aggregate — Credit Component

ex Emerging Markets, Hedged

USD; ICE BofA® Global High

Yield BB-B Rated Constrained

Developed Markets Index,

Hedged USD; JP Morgan® EMBI

Global

(reflects no deduction for fees,

expenses or taxes) |

9.49% |

2.29% |

4.54% |

| Broad-Based Index: |

Bloomberg® Global Aggregate

Index

(reflects no deduction for fees,

expenses or taxes) |

8.17% |

-2.15% |

1.26% |

PORTFOLIO MANAGEMENT

Investment Adviser: Mason Street Advisors, LLC

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Sonali Pier, Managing Director of PIMCO, joined PIMCO in 2013 and has managed the Portfolio since 2018.

Daniel J. Ivascyn, Group Chief Investment Officer and Managing Director of PIMCO, joined PIMCO in 1998 and has managed the Portfolio since 2016.

Alfred T. Murata, Managing Director of PIMCO, joined PIMCO in 2001 and has managed the Portfolio since 2016.

Sub-Adviser: Pacific Investment Management Company LLC (PIMCO)

Portfolio Managers: Sonali Pier, Managing Director of PIMCO, joined PIMCO in 2013 and has managed the Portfolio since 2018.

Daniel J. Ivascyn, Group Chief Investment Officer and Managing Director of PIMCO, joined PIMCO in 1998 and has managed the Portfolio since 2016.

Alfred T. Murata, Managing Director of PIMCO, joined PIMCO in 2001 and has managed the Portfolio since 2016.

NMSF-SP5Northwestern Mutual Series Fund, Inc. Prospectus

Multi-Sector Bond Portfolio – Summary

Charles Watford, Executive Vice President of PIMCO, joined PIMCO in 2007, and has managed the Portfolio since 2022.

Regina Borromeo, Executive Vice President of PIMCO, joined PIMCO in 2022, and has managed the Portfolio since 2022.

TAX INFORMATION

Shares of the Portfolio are offered only for funding variable annuity contracts and variable life insurance policies offered by The Northwestern Mutual Life Insurance Company through separate accounts. Insurance company separate accounts generally do not pay tax on dividends or capital gain distributions. Investors in variable annuity contracts and variable life insurance policies should refer to the prospectuses for the variable products for a discussion of the tax considerations that affect the insurance company and its separate accounts and the tax consequences to investors of owning such products.

COMPENSATION TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

Neither the Portfolio nor any related companies pay compensation to broker-dealers or

other financial intermediaries for the sale of Portfolio shares or related services. Investors in variable annuity contracts and variable life insurance

policies should refer to the prospectuses for the variable products for important information about compensation paid to financial intermediaries for

sales of variable annuity contracts and variable life insurance policies.

NMSF-SP6Northwestern Mutual Series

Fund, Inc. Prospectus