Registration Nos. 2-98326

811-04323

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | ☐ | |

| Pre-Effective Amendment No. | ☐ | |

| Post-Effective Amendment No. 166 | ☒ |

and/or

REGISTRATION STATEMENT

UNDER

| THE INVESTMENT COMPANY ACT OF 1940 | ☐ | |

| Amendment No. 167 | ☒ |

(Check appropriate box or boxes.)

(Exact Name of Registrant as Specified in Charter)

888 Boylston Street, Boston, Massachusetts 02199-8197

(Address of principal executive offices) (Zip Code)

Registrant’s Telephone Number, including Area Code (617) 449-2139

Susan McWhan Tobin, Esq.

Natixis Distribution, LLC

888 Boylston Street

Boston, Massachusetts 02199-8197

(Name and Address of Agent for Service)

Copy to:

Michael G. Doherty, Esq.

Jessica Reece, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, NY 10036-8704

Approximate Date of Proposed Public Offering

It is proposed that this filing will become effective (check appropriate box):

| ☐ | immediately upon filing pursuant to paragraph (b) | |

| ☒ | on May 1, 2026 pursuant to paragraph (b) | |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) | |

| ☐ | on (date) pursuant to paragraph (a)(1) | |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) | |

| ☐ | on (date) pursuant to paragraph (a)(2) of Rule 485. |

If appropriate, check the following box:

| ☐ | This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

|

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Gateway Equity Call Premium Fund

|

GCPAX

|

GCPCX

|

GCPNX

|

GCPYX

|

|

Gateway Fund

|

GATEX

|

GTECX

|

GTENX

|

GTEYX

|

|

Mirova Global Megatrends Fund

|

ESGMX

|

ESGCX

|

ESGNX

|

ESGYX

|

|

Vaughan Nelson Mid Cap Fund

|

VNVAX

|

VNVCX

|

VNVNX

|

VNVYX

|

|

Vaughan Nelson Small Cap Fund

|

NEFJX

|

NEJCX

|

VSCNX

|

NEJYX

|

|

(fees paid directly from your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price)

|

5.75%

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, as applicable)

|

None1

|

1.00%

|

None

|

None

|

|

Redemption fees

|

None

|

None

|

None

|

None

|

| 1 | A 1.00% contingent deferred sales charge (“CDSC”) may apply to certain purchases of Class A shares of $1,000,000 or more that are redeemed within eighteen months of the date of purchase. |

Annual Fund Operating Expenses

|

(expenses that you pay each year as a percentage of the value of your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Management fees

|

0.58%

|

0.58%

|

0.58%

|

0.58%

|

|

Distribution and/or service (12b-1) fees

|

0.25%

|

1.00%

|

0.00%

|

0.00%

|

|

Other expenses

|

0.22%

|

0.22%

|

0.49%

|

0.22%

|

|

Total annual fund operating expenses

|

1.05%

|

1.80%

|

1.07%

|

0.80%

|

|

Fee waiver and/or expense reimbursement1,2

|

0.12%

|

0.12%

|

0.44%

|

0.12%

|

|

Total annual fund operating expenses after fee waiver and/or expense reimbursement

|

0.93%

|

1.68%

|

0.63%

|

0.68%

|

| 1 | Gateway Investment Advisers, LLC (“Gateway” or the “Adviser”) has given a binding contractual undertaking to the Fund to limit the amount of the Fund’s total annual fund operating expenses to 0.93%, 1.68%, 0.63%, and 0.68% of the Fund’s average daily net assets for Class A, Class C, Class N, and Class Y shares, respectively, exclusive of brokerage expenses, interest expense, taxes, acquired fund fees and expenses, organizational and extraordinary expenses, such as litigation and indemnification expenses. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. The Adviser will be permitted to recover, on a class-by-class basis, management fees waived and/or expenses reimbursed to the extent that expenses in later periods fall below both (1) the class’ applicable expense limitation at the time such amounts were waived/reimbursed and (2) the class’ current applicable expense limitation. The Fund will not be obligated to repay any such waived/reimbursed fees and expenses more than one year after the end of the fiscal year in which the fees or expenses were waived/reimbursed. |

| 2 | Natixis Advisors, LLC (“Natixis Advisors”) has given a binding contractual undertaking to the Fund to reimburse any and all transfer agency expenses for Class N shares. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. |

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class A

|

$

|

664

|

$

|

879

|

$

|

1,110

|

$

|

1,774

|

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

271

|

$

|

555

|

$

|

964

|

$

|

1,909

|

|

Class N

|

$

|

64

|

$

|

297

|

$

|

547

|

$

|

1,266

|

|

Class Y

|

$

|

69

|

$

|

243

|

$

|

432

|

$

|

979

|

|

If shares are not redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

171

|

$

|

555

|

$

|

964

|

$

|

1,909

|

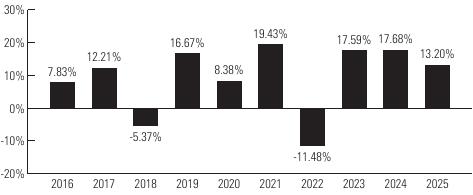

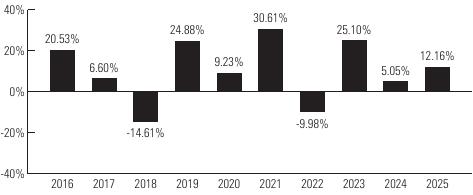

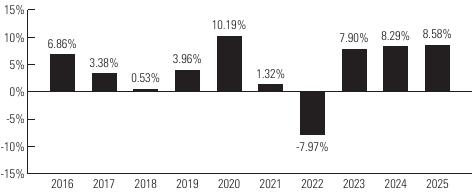

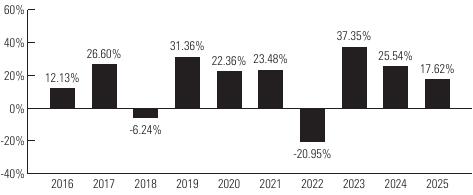

Risk/Return Bar Chart and Table

|

Highest Quarterly Return:

Second Quarter 2020, 11.74% Lowest Quarterly Return: First Quarter 2020, -15.92% |

|

Average Annual Total Returns

|

|

|

|

|

|

(for the periods ended December 31, 2025)

|

Past 1 Year

|

Past 5 Years

|

Past 10 Years

|

Life of Class N

(5/1/17) |

|

Class Y - Return Before Taxes

|

13.20%

|

10.61%

|

9.14%

|

-

|

|

Return After Taxes on Distributions

|

13.03%

|

10.41%

|

8.90%

|

-

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

7.92%

|

8.40%

|

7.44%

|

-

|

|

Class A - Return Before Taxes

|

6.42%

|

9.04%

|

8.22%

|

-

|

|

Class C - Return Before Taxes

|

11.09%

|

9.52%

|

8.22%

|

-

|

|

Class N - Return Before Taxes

|

13.27%

|

10.66%

|

-

|

9.15%

|

|

S&P 500® Index

|

17.88%

|

14.42%

|

14.82%

|

14.77%

|

|

CBOE S&P 500 BuyWrite Index (BXMSM)

|

8.91%

|

9.33%

|

7.31%

|

7.02%

|

|

Type of Account

|

Minimum Initial Purchase

|

|

Any account other than those listed below

|

$2,500

|

|

For shareholders participating in Natixis Funds’ Automatic Investment Plan

|

$1,000

|

|

For Traditional IRA, Roth IRA, Rollover IRA, SEP-IRA and Keogh plans

|

$1,000

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, Natixis Distribution, LLC (the “Distributor”) may waive any share class eligibility requirement.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Funds of funds that are distributed by the Distributor.

|

|

•

|

Sub-accounts held within an omnibus account, where the omnibus account has at least $1,000,000. (Effective June 1, 2026, this waiver no longer applies.)

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Certain Individual Retirement Accounts if the amounts invested represent rollover distributions from investments by any of the retirement plans invested in the Fund.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Fund Trustees, former Fund trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned) and Natixis affiliate employee benefit plans.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

The Fund’s shares are available for purchase and are redeemable on any business day through your investment dealer, directly from the Fund by writing to the Fund at Natixis Funds, P.O. Box 219579, Kansas City, MO 64121-9579, by exchange, by wire, by internet at im.natixis.com (certain restrictions may apply), through the Automated Clearing House system, or, in the case of redemptions, by telephone at 800-225-5478 or by the Systematic Withdrawal Plan.

|

(fees paid directly from your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price)

|

5.75%

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, as applicable)

|

None1

|

1.00%

|

None

|

None

|

|

Redemption fees

|

None

|

None

|

None

|

None

|

| 1 | A 1.00% contingent deferred sales charge (“CDSC”) may apply to certain purchases of Class A shares of $1,000,000 or more that are redeemed within eighteen months of the date of purchase. |

Annual Fund Operating Expenses

|

(expenses that you pay each year as a percentage of the value of your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Management fees

|

0.59%

|

0.59%

|

0.59%

|

0.59%

|

|

Distribution and/or service (12b-1) fees

|

0.25%

|

1.00%

|

0.00%

|

0.00%

|

|

Other expenses

|

0.13%

|

0.14%

|

0.06%

|

0.14%

|

|

Total annual fund operating expenses

|

0.97%

|

1.73%

|

0.65%

|

0.73%

|

|

Fee waiver and/or expense reimbursement1

|

0.03%

|

0.03%

|

0.00%

|

0.03%

|

|

Total annual fund operating expenses after fee waiver and/or expense reimbursement

|

0.94%

|

1.70%

|

0.65%

|

0.70%

|

| 1 | Gateway Investment Advisers, LLC (“Gateway” or the “Adviser”) has given a binding contractual undertaking to the Fund to limit the amount of the Fund’s total annual fund operating expenses to 0.94%, 1.70%, 0.65%, and 0.70% of the Fund’s average daily net assets for Class A, Class C, Class N, and Class Y shares, respectively, exclusive of brokerage expenses, interest expense, taxes, acquired fund fees and expenses, organizational and extraordinary expenses, such as litigation and indemnification expenses. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. The Adviser will be permitted to recover, on a class-by-class basis, management fees waived and/or expenses reimbursed to the extent that expenses in later periods fall below both (1) the class’ applicable expense limitation at the time such amounts were waived/reimbursed and (2) the class’ current applicable expense limitation. The Fund will not be obligated to repay any such waived/reimbursed fees and expenses more than one year after the end of the fiscal year in which the fees or expenses were waived/reimbursed. |

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class A

|

$

|

665

|

$

|

863

|

$

|

1,078

|

$

|

1,694

|

|

Class C

|

$

|

273

|

$

|

542

|

$

|

936

|

$

|

1,837

|

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class N

|

$

|

66

|

$

|

208

|

$

|

362

|

$

|

810

|

|

Class Y

|

$

|

72

|

$

|

230

|

$

|

403

|

$

|

904

|

|

If shares are not redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

173

|

$

|

542

|

$

|

936

|

$

|

1,837

|

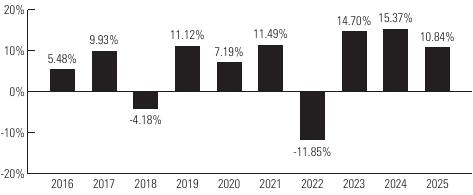

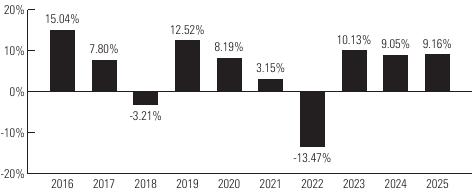

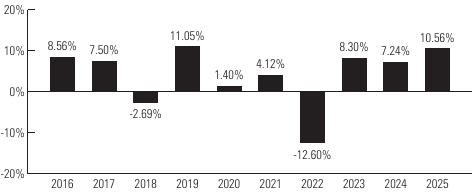

Risk/Return Bar Chart and Table

|

Highest Quarterly Return:

Second Quarter 2020, 8.36% Lowest Quarterly Return: First Quarter 2020, -10.01% |

|

Average Annual Total Returns

|

|

|

|

|

|

(for the periods ended December 31, 2025)

|

Past 1 Year

|

Past 5 Years

|

Past 10 Years

|

Life of Class N

(5/1/17) |

|

Class Y - Return Before Taxes

|

10.84%

|

7.59%

|

6.67%

|

-

|

|

Return After Taxes on Distributions

|

10.70%

|

7.40%

|

6.37%

|

-

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

6.51%

|

5.94%

|

5.29%

|

-

|

|

Class A - Return Before Taxes

|

4.22%

|

6.07%

|

5.79%

|

-

|

|

Class C - Return Before Taxes

|

8.72%

|

6.51%

|

5.77%

|

-

|

|

Class N - Return Before Taxes

|

10.89%

|

7.64%

|

-

|

6.67%

|

|

S&P 500® Index

|

17.88%

|

14.42%

|

14.82%

|

14.77%

|

|

Bloomberg U.S. Aggregate Bond Index

|

7.30%

|

-0.36%

|

2.01%

|

1.84%

|

|

Type of Account

|

Minimum Initial Purchase

|

|

Any account other than those listed below

|

$2,500

|

|

For shareholders participating in Natixis Funds’ Automatic Investment Plan

|

$1,000

|

|

For Traditional IRA, Roth IRA, Rollover IRA, SEP-IRA and Keogh plans

|

$1,000

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, Natixis Distribution, LLC (the “Distributor”) may waive any share class eligibility requirement.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Funds of funds that are distributed by the Distributor.

|

|

•

|

Sub-accounts held within an omnibus account, where the omnibus account has at least $1,000,000. (Effective June 1, 2026, this waiver no longer applies.)

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Certain Individual Retirement Accounts if the amounts invested represent rollover distributions from investments by any of the retirement plans invested in the Fund.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Fund Trustees, former Fund trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned) and Natixis affiliate employee benefit plans.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

The Fund’s shares are available for purchase and are redeemable on any business day through your investment dealer, directly from the Fund by writing to the Fund at Natixis Funds, P.O. Box 219579, Kansas City, MO 64121-9579, by exchange, by wire, by internet at im.natixis.com (certain restrictions may apply), through the Automated Clearing House system, or, in the case of redemptions, by telephone at 800-225-5478 or by the Systematic Withdrawal Plan.

|

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price)

|

|

|

|

|

|

Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, as applicable)

|

|

|

|

|

|

Redemption fees

|

|

|

|

|

| 1 |

|

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Management fees

|

|

|

|

|

|

Distribution and/or service (12b-1) fees

|

|

|

|

|

|

Other expenses

|

|

|

|

|

|

Total annual fund operating expenses

|

|

|

|

|

|

Fee waiver and/or expense reimbursement1,2

|

|

|

|

|

|

Total annual fund operating expenses after fee waiver and/or expense reimbursement

|

|

|

|

|

| 1 | Mirova US LLC (“Mirova US” or the “Adviser”) has given a binding contractual undertaking to the Fund to limit the amount of the Fund’s total annual fund operating expenses to 1.20%, 1.95%, 0.90%, and 0.95% of the Fund’s average daily net assets for Class A, C, N, and Y shares, respectively, exclusive of brokerage expenses, interest expense, taxes, acquired fund fees and expenses, organizational and extraordinary expenses, such as litigation and indemnification expenses. This undertaking is in effect through |

| 2 | Natixis Advisors, LLC (“Natixis Advisors”) has given a binding contractual undertaking to the Fund to reimburse any and all transfer agency expenses for Class N shares. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. |

|

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class A

|

$

|

|

$

|

|

$

|

|

$

|

|

|

Class C

|

$

|

|

$

|

|

$

|

|

$

|

|

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class N

|

$

|

|

$

|

|

$

|

|

$

|

|

|

Class Y

|

$

|

|

$

|

|

$

|

|

$

|

|

|

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

|

$

|

|

$

|

|

$

|

|

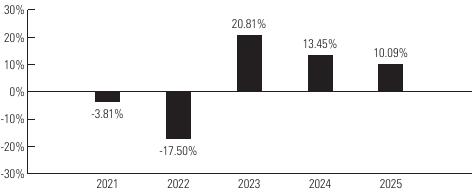

Risk/Return Bar Chart and Table

|

|

|

|

|

|

|

|

|

|

Past 1 Year

|

Past 5 Years

|

Life of Fund

(3/31/16) |

Life of Class N

(5/1/17) |

|

Class Y - Return Before Taxes

|

|

|

|

-

|

|

Return After Taxes on Distributions

|

|

|

|

-

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

|

|

|

-

|

|

Class A - Return Before Taxes

|

|

|

|

-

|

|

Class C - Return Before Taxes

|

|

|

|

-

|

|

Class N - Return Before Taxes

|

|

|

-

|

|

|

MSCI World Index (Net)

|

|

|

|

|

|

Type of Account

|

Minimum Initial Purchase

|

|

Any account other than those listed below

|

$2,500

|

|

For shareholders participating in Natixis Funds’ Automatic Investment Plan

|

$1,000

|

|

For Traditional IRA, Roth IRA, Rollover IRA, SEP-IRA and Keogh plans

|

$1,000

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, Natixis Distribution, LLC (the “Distributor”) may waive any share class eligibility requirement.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Funds of funds that are distributed by the Distributor.

|

|

•

|

Sub-accounts held within an omnibus account, where the omnibus account has at least $1,000,000. (Effective June 1, 2026, this waiver no longer applies.)

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Certain Individual Retirement Accounts if the amounts invested represent rollover distributions from investments by any of the retirement plans invested in the Fund.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Fund Trustees, former Fund trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned) and Natixis affiliate employee benefit plans.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

The Fund’s shares are available for purchase and are redeemable on any business day through your investment dealer, directly from the Fund by writing to the

|

(fees paid directly from your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price)

|

5.75%

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, as applicable)

|

None1

|

1.00%

|

None

|

None

|

|

Redemption fees

|

None

|

None

|

None

|

None

|

| 1 | A 1.00% contingent deferred sales charge (“CDSC”) may apply to certain purchases of Class A shares of $1,000,000 or more that are redeemed within eighteen months of the date of purchase. |

|

(expenses that you pay each year as a percentage of the value of your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Management fees

|

0.75%

|

0.75%

|

0.75%

|

0.75%

|

|

Distribution and/or service (12b-1) fees

|

0.25%

|

1.00%

|

0.00%

|

0.00%

|

|

Other expenses

|

0.27%

|

0.27%

|

0.17%

|

0.27%

|

|

Total annual fund operating expenses

|

1.27%

|

2.02%

|

0.92%

|

1.02%

|

|

Fee waiver and/or expense reimbursement1,2

|

0.12%

|

0.12%

|

0.07%

|

0.12%

|

|

Total annual fund operating expenses after fee waiver and/or expense reimbursement

|

1.15%

|

1.90%

|

0.85%

|

0.90%

|

| 1 | Natixis Advisors, LLC (“Natixis Advisors” or the “Adviser”) has given a binding contractual undertaking to the Fund to limit the amount of the Fund’s total annual fund operating expenses to 1.15%, 1.90%, 0.85%, and 0.90% of the Fund’s average daily net assets for Class A, Class C, Class N, and Class Y shares, respectively, exclusive of brokerage expenses, interest expense, taxes, acquired fund fees and expenses, organizational and extraordinary expenses, such as litigation and indemnification expenses. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. The Adviser will be permitted to recover, on a class-by-class basis, management fees waived and/or expenses reimbursed to the extent that expenses in later periods fall below both (1) the class’ applicable expense limitation at the time such amounts were waived/reimbursed and (2) the class’ current applicable expense limitation. The Fund will not be obligated to repay any such waived/reimbursed fees and expenses more than one year after the end of the fiscal year in which the fees or expenses were waived/reimbursed. |

| 2 | Natixis Advisors, LLC (“Natixis Advisors”) has given a binding contractual undertaking to the Fund to reimburse any and all transfer agency expenses for Class N shares. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. |

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class A

|

$

|

685

|

$

|

943

|

$

|

1,221

|

$

|

2,011

|

|

Class C

|

$

|

293

|

$

|

622

|

$

|

1,077

|

$

|

2,145

|

|

If shares are redeemed:

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class N

|

$

|

87

|

$

|

286

|

$

|

502

|

$

|

1,125

|

|

Class Y

|

$

|

92

|

$

|

313

|

$

|

552

|

$

|

1,237

|

|

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

193

|

$

|

622

|

$

|

1,077

|

$

|

2,145

|

|

•

|

Companies earning a positive return on capital with stable-to-improving returns.

|

|

•

|

Companies valued at a discount to their asset value.

|

|

•

|

Companies with an attractive and sustainable dividend level.

|

|

•

|

Vaughan Nelson employs a value-driven investment philosophy that selects stocks selling at a relatively low value based on business fundamentals, economic margin analysis and discounted cash flow models. Vaughan Nelson selects companies that it believes are out of favor or misunderstood.

|

|

•

|

Vaughan Nelson uses fundamental analysis to construct a portfolio that, in the opinion of Vaughan Nelson, is made up of quality companies with the potential to provide significant increases in share price over a three year period.

|

|

•

|

Vaughan Nelson will generally sell a security when it reaches Vaughan Nelson’s price target or when the issuer shows a change in financial condition, competitive pressures, poor management decisions or internal or external forces reducing future expected returns from those expected at the time of investment.

|

|

•

|

Invest in foreign securities, including emerging markets securities.

|

|

•

|

Invest in other investment companies, to the extent permitted by the Investment Company Act of 1940.

|

|

•

|

Invest in REITs.

|

|

•

|

Invest in securities offered in initial public offerings (“IPOs”), securities issued pursuant to Rule 144A under the Securities Act of 1933 (“Rule 144A securities”), and other privately placed investments such as private equity investments.

|

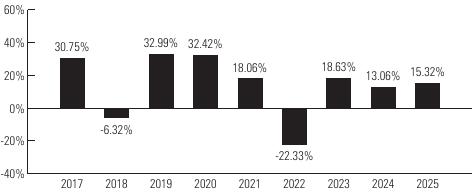

Cybersecurity and Technology Risk: The Fund, its service providers, and other market participants increasingly depend on complex information technology and communications systems, which are subject to a number of different threats and risks that could adversely affect the Fund and its shareholders. Cybersecurity and other operational and technology issues may result in financial losses to the Fund and its shareholders.

|

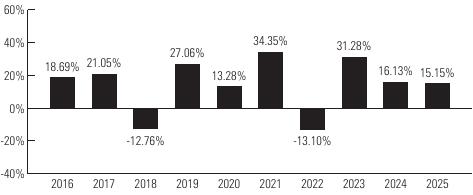

Highest Quarterly Return:

Fourth Quarter 2020, 22.51% Lowest Quarterly Return: First Quarter 2020, -28.21% |

|

Average Annual Total Returns

|

|

|

|

|

(for the periods ended December 31, 2025)

|

Past 1 Year

|

Past 5 Years

|

Past 10 Years

|

|

Class Y - Return Before Taxes

|

12.39%

|

11.08%

|

9.47%

|

|

Return After Taxes on Distributions

|

1.84%

|

7.33%

|

6.88%

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

11.43%

|

8.08%

|

7.10%

|

|

Class A - Return Before Taxes

|

5.67%

|

9.49%

|

8.55%

|

|

Class C - Return Before Taxes

|

10.59%

|

9.98%

|

8.53%

|

|

Class N - Return Before Taxes

|

12.44%

|

11.13%

|

9.54%

|

|

Russell 3000® Index

|

17.15%

|

13.15%

|

14.29%

|

|

Russell Midcap® Value Index

|

11.05%

|

9.83%

|

9.78%

|

|

Type of Account

|

Minimum Initial Purchase

|

|

Any account other than those listed below

|

$2,500

|

|

For shareholders participating in Natixis Funds’ Automatic Investment Plan

|

$1,000

|

|

For Traditional IRA, Roth IRA, Rollover IRA, SEP-IRA and Keogh plans

|

$1,000

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, Natixis Distribution, LLC (the “Distributor”) may waive any share class eligibility requirement.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Funds of funds that are distributed by the Distributor.

|

|

•

|

Sub-accounts held within an omnibus account, where the omnibus account has at least $1,000,000. (Effective June 1, 2026, this waiver no longer applies.)

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Certain Individual Retirement Accounts if the amounts invested represent rollover distributions from investments by any of the retirement plans invested in the Fund.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Fund Trustees, former Fund trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned) and Natixis affiliate employee benefit plans.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

The Fund’s shares are available for purchase and are redeemable on any business day through your investment dealer, directly from the Fund by writing to the Fund at Natixis Funds, P.O. Box 219579, Kansas City, MO 64121-9579, by exchange, by wire, by internet at im.natixis.com (certain restrictions may apply), through the Automated Clearing House system, or, in the case of redemptions, by telephone at 800-225-5478 or by the Systematic Withdrawal Plan.

|

(fees paid directly from your investment)

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price)

|

|

|

|

|

|

Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, as applicable)

|

|

|

|

|

|

Redemption fees

|

|

|

|

|

| 1 |

|

|

Class A

|

Class C

|

Class N

|

Class Y

|

|

Management fees

|

|

|

|

|

|

Distribution and/or service (12b-1) fees

|

|

|

|

|

|

Other expenses

|

|

|

|

|

|

Acquired fund fees and expenses1

|

|

|

|

|

|

Total annual fund operating expenses

|

|

|

|

|

|

Fee waiver and/or expense reimbursement2,3

|

|

|

|

|

|

Total annual fund operating expenses after fee waiver and/or expense reimbursement

|

|

|

|

|

| 1 | The expense information shown in the table above differs from the expense information disclosed in the Fund’s financial highlights table because the financial highlights table reflects the operating expenses of the Fund and does not include acquired fund fees and expenses. |

| 2 | The Fund’s investment adviser has given a binding contractual undertaking to the Fund to limit the amount of the Fund’s total annual fund operating expenses to 1.25%, 2.00%, 0.95%, and 1.00% of the Fund’s average daily net assets for Class A, Class C, Class N, and Class Y shares, respectively, exclusive of brokerage expenses, interest expense, taxes, acquired fund fees and expenses, organizational and extraordinary expenses, such as litigation and indemnification expenses. This undertaking is in effect through |

| 3 | Natixis Advisors, LLC (“Natixis Advisors”) has given a binding contractual undertaking to the Fund to reimburse any and all transfer agency expenses for Class N shares. This undertaking is in effect through April 30, 2027 and may be terminated before then only with the consent of the Fund’s Board of Trustees. |

|

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class A

|

$

|

|

$

|

|

$

|

|

$

|

|

|

Class C

|

$

|

|

$

|

|

$

|

|

$

|

|

|

Class N

|

$

|

|

$

|

|

$

|

|

$

|

|

|

Class Y

|

$

|

|

$

|

|

$

|

|

$

|

|

|

|

1 year

|

3 years

|

5 years

|

10 years

|

||||

|

Class C

|

$

|

|

$

|

|

$

|

|

$

|

|

|

•

|

Companies earning a positive return on capital with stable-to-improving returns.

|

|

•

|

Companies valued at a discount to their asset value.

|

|

•

|

Companies with an attractive and sustainable dividend level.

|

|

•

|

Value-driven investment philosophy that selects stocks selling at a relatively low value based on discounted cash flow models. Vaughan Nelson selects companies that it believes are out of favor or misunderstood.

|

|

•

|

Vaughan Nelson starts with an investment universe of 5,000 securities. Vaughan Nelson then uses value-driven screens to create a research universe of companies with market capitalizations of at least $100 million.

|

|

•

|

Vaughan Nelson uses fundamental analysis to construct a portfolio of 60 to 80 securities that, in the opinion of Vaughan Nelson, is made up of quality companies with the potential to provide significant increases in share price over a three year period.

|

|

•

|

Vaughan Nelson will generally sell a security when it reaches Vaughan Nelson’s price target or when the issuer shows a change in financial condition, competitive pressures, poor management decisions or internal or external forces reducing future expected returns from those expected at the time of investment.

|

|

•

|

Invest in convertible preferred stock and convertible debt securities.

|

|

•

|

Invest in foreign securities, including emerging market securities.

|

|

•

|

Invest in REITs.

|

|

•

|

Invest in securities offered in initial public offerings (“IPOs”).

|

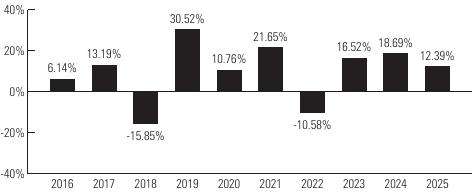

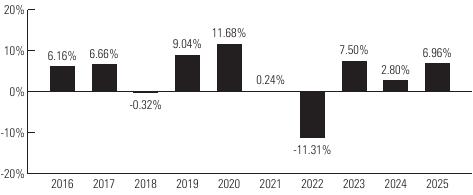

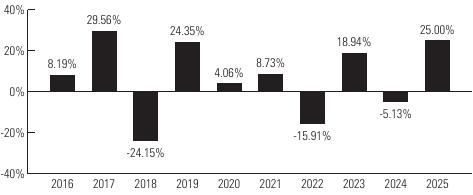

Risk/Return Bar Chart and Table

|

|

|

|

|

|

|

|

|

|

Past 1 Year

|

Past 5 Years

|

Past 10 Years

|

Life of Class N

(5/1/17) |

|

Class Y - Return Before Taxes

|

|

|

|

-

|

|

Return After Taxes on Distributions

|

|

|

|

-

|

|

Return After Taxes on Distributions and Sale of Fund Shares

|

|

|

|

-

|

|

Class A - Return Before Taxes

|

|

|

|

-

|

|

Class C - Return Before Taxes

|

|

|

|

-

|

|

Class N - Return Before Taxes

|

|

|

-

|

|

|

Russell 3000® Index

|

|

|

|

|

|

Russell 2000® Value Index

|

|

|

|

|

|

Type of Account

|

Minimum Initial Purchase

|

|

Any account other than those listed below

|

$2,500

|

|

For shareholders participating in Natixis Funds’ Automatic Investment Plan

|

$1,000

|

|

For Traditional IRA, Roth IRA, Rollover IRA, SEP-IRA and Keogh plans

|

$1,000

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, Natixis Distribution, LLC (the “Distributor”) may waive any share class eligibility requirement.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Funds of funds that are distributed by the Distributor.

|

|

•

|

Sub-accounts held within an omnibus account, where the omnibus account has at least $1,000,000. (Effective June 1, 2026, this waiver no longer applies.)

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

|

•

|

Fee Based Programs (such as wrap accounts) where an advisory fee is paid to the broker-dealer or other financial intermediary. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees.

|

|

•

|

Certain Retirement Plans. Please consult your retirement plan administrator to determine if your retirement plan is subject to additional or different conditions or fees imposed by the plan administrator.

|

|

•

|

Certain Individual Retirement Accounts if the amounts invested represent rollover distributions from investments by any of the retirement plans invested in the Fund.

|

|

•

|

Clients of a Registered Investment Adviser where the Registered Investment Adviser receives an advisory, management or consulting fee.

|

|

•

|

Fund Trustees, former Fund trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned) and Natixis affiliate employee benefit plans.

|

|

•

|

Effective June 1, 2026, accounts invested through certain intermediaries held within an Intermediary Omnibus Account.

|

|

•

|

Effective June 1, 2026, in its sole discretion, the Distributor may waive any share class eligibility requirement.

|

The Fund’s shares are available for purchase and are redeemable on any business day through your investment dealer, directly from the Fund by writing to the Fund at Natixis Funds, P.O. Box 219579, Kansas City, MO 64121-9579, by exchange, by wire, by internet at im.natixis.com (certain restrictions may apply), through the Automated Clearing House system, or, in the case of redemptions, by telephone at 800-225-5478 or by the Systematic Withdrawal Plan.

|

•

|

Companies earning a positive return on capital with stable-to-improving returns.

|

|

•

|

Companies valued at a discount to their asset value.

|

|

•

|

Companies with an attractive and sustainable dividend level.

|

|

•

|

Vaughan Nelson employs a value-driven investment philosophy that selects stocks selling at a relatively low value based on business fundamentals, economic margin analysis and discounted cash flow models. Vaughan Nelson selects companies that it believes are out of favor or misunderstood.

|

|

•

|

Vaughan Nelson uses fundamental analysis to construct a portfolio that, in the opinion of Vaughan Nelson, is made up of quality companies with the potential to provide significant increases in share price over a three year period.

|

|

•

|

Vaughan Nelson will generally sell a security when it reaches Vaughan Nelson’s price target or when the issuer shows a change in financial condition, competitive pressures, poor management decisions or internal or external forces reducing future expected returns from those expected at the time of investment.

|

|

•

|

Invest in foreign securities, including emerging markets securities.

|

|

•

|

Invest in other investment companies, to the extent permitted by the Investment Company Act of 1940.

|

|

•

|

Invest in REITs.

|

|

•

|

Invest in securities offered in initial public offerings (“IPOs”), securities issued pursuant to Rule 144A under the Securities Act of 1933 (“Rule 144A securities”), and other privately placed investments such as private equity investments.

|

|

•

|

Companies earning a positive return on capital with stable-to-improving returns.

|

|

•

|

Companies valued at a discount to their asset value.

|

|

•

|

Companies with an attractive and sustainable dividend level.

|

|

•

|

Value-driven investment philosophy that selects stocks selling at a relatively low value based on discounted cash flow models. Vaughan Nelson selects companies that it believes are out of favor or misunderstood.

|

|

•

|

Vaughan Nelson starts with an investment universe of 5,000 securities. Vaughan Nelson then uses value-driven screens to create a research universe of companies with market capitalizations of at least $100 million.

|

|

•

|

Vaughan Nelson uses fundamental analysis to construct a portfolio of 60 to 80 securities that, in the opinion of Vaughan Nelson, is made up of quality companies with the potential to provide significant increases in share price over a three year period.

|

|

•

|

Vaughan Nelson will generally sell a security when it reaches Vaughan Nelson’s price target or when the issuer shows a change in financial condition, competitive pressures, poor management decisions or internal or external forces reducing future expected returns from those expected at the time of investment.

|

|

•

|

Invest in convertible preferred stock and convertible debt securities.

|

|

•

|

Invest in foreign securities, including emerging market securities.

|

|

•

|

Invest in REITs.

|

|

•

|

Invest in securities offered in initial public offerings (“IPOs”).

|

|

•

|

You pay a sales charge when you buy Class A shares. There are several ways to reduce this charge. See the section “How Sales Charges Are Calculated.”

|

|

•

|

You pay lower annual expenses than Class C shares, giving you the potential for higher returns per share. However, where front-end sales charges are applicable, returns are earned on a smaller amount of your investment.

|

|

•

|

You pay higher expenses than Class N and Class Y shares.

|

|

•

|

You do not pay a sales charge if your total investment reaches $1 million or more, but you may pay a charge on redemptions if you redeem these shares within 18 months of purchase.

|

|

•

|

The Gateway Fund acquired the assets and liabilities of the Gateway Predecessor Fund in a Reorganization on February 15, 2008. If you held shares of the Gateway Predecessor Fund in your existing account as of the date of the Reorganization, you are eligible to purchase additional Class A shares without a sales charge or a contingent deferred sales charge (“CDSC”) through your existing account, provided you have held fund shares in your existing account since that date.

Due to operational limitations at your financial intermediary, a sales charge or CDSC may be assessed unless you inform the financial intermediary at the time you make any additional purchase that you were a shareholder of the Gateway Predecessor Fund and are eligible to purchase Class A shares |

|

without a sales charge or CDSC. Notwithstanding the foregoing, former shareholders of the Gateway Predecessor Fund may not be eligible to purchase shares at NAV through a financial intermediary if the nature of your relationship with, and/or the services you receive from, the financial intermediary changes. Please consult your financial representative for further details.

|

|

•

|

You do not pay a sales charge when you buy Class C shares. All of your money goes to work for you right away.

|

|

•

|

You pay higher annual expenses than Class A, Class N and Class Y shares.

|

|

•

|

You may pay a sales charge on redemptions if you sell your Class C shares within one year of purchase.

|

|

•

|

Investors will not be permitted to purchase $1 million or more of Class C shares as a single investment per account. There may be certain exceptions to this restriction for omnibus and other nominee accounts. Investors may want to consider the lower operating expense of Class A shares in such instances. You may pay a charge on redemptions if you redeem Class A shares within 18 months of purchase.

|

|

•

|

Except as noted below, Class C shares will automatically convert to Class A shares after eight years. Please see the section “Exchanging or Converting Shares” for details regarding a conversion of shares. Generally, to be eligible to have your Class C shares automatically converted to Class A shares, the Fund or the financial intermediary through which you purchased your shares will need to have records verifying that your Class C shares have been held for eight years. Due to operational limitations at your financial intermediary, your ability to have your Class C shares automatically converted to Class A shares may be limited. Group retirement plans of certain financial intermediaries who hold Class C shares with a Fund in an omnibus account do not track participant level aging of shares and therefore these shares will not be eligible for an automatic conversion. Certain intermediaries may convert your Class C shares to Class A shares in accordance with a conversion schedule that may differ from the one described above. Please consult your financial representative for more information.

|

|

•

|

You have a minimum initial investment of $1,000,000. There are several ways to waive this minimum. See the section “Purchase and Sale of Fund Shares.”

|

|

•

|

You do not pay a sales charge when you buy Class N shares. All of your money goes to work for you right away.

|

|

•

|

You do not pay a sales charge on redemptions.

|

|

•

|

You may pay lower annual expenses than Class A, Class C and Class Y shares, giving you the potential for higher returns per share.

|

|

•

|

You have a minimum initial investment of $100,000. There are several ways to waive this minimum. See the section “Purchase and Sale of Fund Shares.”

|

|

•

|

You do not pay a sales charge when you buy Class Y shares. All of your money goes to work for you right away.

|

|

•

|

You do not pay a sales charge on redemptions.

|

|

•

|

You pay lower annual expenses than Class A and Class C shares, giving you the potential for higher returns per share.

|

|

•

|

You may pay higher annual expenses than Class N shares.

|

|

Class A Sales Charges*

|

||

|

|

All Funds

|

|

|

Your Investment

|

As a % of offering price

|

As a % of your investment

|

|

Less than $50,000

|

5.75%

|

6.10%

|

|

$50,000 – $99,999

|

4.50%

|

4.71%

|

|

$100,000 – $249,999

|

3.50%

|

3.63%

|

|

$250,000 – $499,999

|

2.50%

|

2.56%

|

|

$500,000 – $999,999

|

2.00%

|

2.04%

|

|

$1,000,000 or more**

|

0.00%

|

0.00%

|

|

•

|

Letter of Intent — By signing a Letter of Intent, you may purchase Class A shares of any Natixis Fund over a 13-month period but pay sales charges as if you had purchased all shares at once. This program can save you money if you plan to invest $50,000 or more within 13 months.

|

|

•

|

Cumulative Purchase Discount — You may be entitled to a reduced sales charge if your “total investment” reaches a breakpoint for a reduced sales charge. The total investment is determined by adding the amount of your current purchase in a Fund, including the applicable sales charge, to the current public offering price of all series and classes of shares of the Natixis Funds held by you in one or more accounts. If your total investment exceeds a sales charge breakpoint in the table above, the lower sales charge applies to the entire amount of your current purchase in a Fund.

|

|

•

|

Combining Accounts — This allows you to combine shares of multiple Natixis Funds and classes for purposes of calculating your sales charge

|

|

Individual Accounts: You may elect to combine your purchase(s) and your total investment, as defined above, with the purchases and total investment of your spouse, parents, children, siblings, grandparents, grandchildren, in-laws (of those previously mentioned), individual retirement accounts, sole proprietorships, single trust estates and any other individuals acceptable to the Distributor.

|

|

Certain Retirement Plan Accounts: The Distributor may, at its discretion, combine the purchase(s) and total investment of all qualified participants in the same retirement plan for purposes of determining the availability of a reduced sales charge. In most instances, individual accounts may not be linked with certain retirement plan accounts for the purposes of calculating sales charges. In most instances, individual accounts may not be linked with certain retirement plan accounts for the purposes of calculating sales charges. Savings Incentive Match Plan for Employees (“SIMPLE IRA”) contributions will automatically be linked with those of other participants in the same SIMPLE IRA Plan (Class A shares only) using the Natixis Funds prototype document. Effective May 8, 2026, all share classes will be linked for the purpose of calculating sales charges. SIMPLE IRA accounts may not be linked with any other Natixis Fund account for rights of accumulation. Please refer to the SAI for more detailed information on combining accounts.

|

|

•

|

Clients of a financial intermediary that has entered into an agreement with the Distributor and has been approved by the Distributor to offer Fund shares to self-directed investment brokerage accounts that may or may not charge a transaction fee;

|

|

•

|

Any government entity that is prohibited from paying a sales charge or commission to purchase mutual fund shares;

|

|

•

|

All employees of financial intermediaries under arrangements with the Distributor (this also applies to spouses and children under the age of 21 of those mentioned);

|

|

•

|

Fund trustees, former trustees, employees of affiliates of the Natixis Funds and other individuals who are affiliated with any Natixis Fund (this also applies to any spouse, parents, children, siblings, grandparents, grandchildren and in-laws of those mentioned);

|

|

•

|

Certain Retirement Plans. The availability of this pricing may depend upon the policies and procedures of your specific financial intermediary; consult your financial adviser;

|

|

•

|

Non-discretionary and non-retirement accounts of bank trust departments or trust companies, but only if they principally engage in banking or trust activities;

|

|

•

|

Investors who were Gateway Predecessor Fund shareholders as of the date of the Reorganization (see the section “Choosing a Share Class”);

|

|

•

|

Fee Based Programs of certain broker-dealers, the Advisers or the Distributor. Please consult your financial representative to determine if your fee based program is subject to additional or different conditions or fees; and

|

|

•

|

Registered Investment Advisers investing on behalf of clients in exchange for an advisory, management or consulting fee.

|

|

Year Since Purchase

|

CDSC on Shares Being Sold

|

|

1st

|

1.00%

|

|

Thereafter

|

0.00%

|

|

•

|

Is calculated based on the number of shares you are selling;

|

|

•

|

Calculation is based on either your original purchase price or the current NAV of the shares being sold, whichever is lower in order to minimize your CDSC;

|

|

•

|

Is deducted from the proceeds of the redemption unless you request, at the time of the redemption, that it be deducted from the amount remaining in your account; and

|

|

•

|

Applies to redemptions made within the time frame shown above for each class.

|

|

•

|

Increases in NAV above the purchase price;

|

|

•

|

Shares you acquired by reinvesting your dividends or capital gains distributions; or

|

|

•

|

Exchanges. However, the original purchase date of the shares from which the exchange is made determines if the newly acquired shares are subject to the CDSC when they are sold.

|

Natixis Funds

P.O. Box 219579

Kansas City, MO 64121-9579

801 Pennsylvania Ave

Suite 219579

Kansas City, MO 64105-1307

Natixis Funds

P.O. Box 219579

Kansas City, MO 64121-9579

801 Pennsylvania Ave

Suite 219579

Kansas City, MO 64105-1307

|

•

|

If you are selling more than $100,000 per day from a single fund/account and you are requesting the proceeds by check (this does not apply to IRA transfer of assets to new custodian).

|

|

•

|

If you are requesting that the proceeds check (of any amount) be made out to someone other than the registered owner(s) or sent to an address other than the address of record.

|

|

•

|

If the account registration or bank account information has changed within the past 30 days.

|

|

•

|

If you are instructing us to send the proceeds by check, wire or ACH to a bank not already active on the fund account.

|

|

Restriction

|

Situation

|

|

Each Fund may suspend the right of redemption:

|

|

|

Each Fund reserves the right to suspend account services or refuse transaction requests:

|

|

|

Each Fund may pay the redemption price in whole or in part by a distribution in-kind of readily marketable securities in lieu of cash or may take up to 7 days to pay a redemption request in order to raise capital:

|

|

|

Each Fund may withhold redemption proceeds for 10 days from the purchase date:

|

|

|

•

|

A share’s NAV is determined at the close of regular trading on the NYSE on the days the NYSE is open for trading. This is normally 4:00 p.m., Eastern time. A Fund’s shares will not be priced on the days on which the NYSE is closed for trading. In addition, a Fund’s shares will not be priced on the holidays listed in the SAI. See the section “Net Asset Value” in the SAI for more details.

|

|

•

|

The price you pay for purchasing, redeeming or exchanging a share will be based upon the NAV next calculated (plus or minus applicable sales charges as described earlier in the Fund Summary) after your order is received by the transfer agent, SS&C Global Investor & Distribution Solutions, Inc., (rather than when the order arrives at the P.O. box) “in good order” (meaning that the order is complete and contains all necessary information).1

|

|

•

|

Requests received by the Funds after the NYSE closes will be processed based upon the NAV determined at the close of regular trading on the next day that the NYSE is open. If the transfer agent receives the order in good order prior to the NYSE market close (normally 4:00 p.m., Eastern time), the shareholder will receive that day’s NAV. Under limited circumstances, the Distributor may enter into contractual agreements pursuant to which orders received by your investment dealer before a Fund determines its NAV and transmitted to the transfer agent prior to market open on the next business day are processed at the NAV determined on the day the order was received by your investment dealer. Please contact your investment dealer to determine whether it has entered into such a contractual agreement. If your investment dealer has not entered into such a contractual agreement, your order will be processed at the NAV next determined after your investment dealer submits the order to a Fund.

|

|

•

|

If a Fund invests in foreign securities, it may have NAV changes on days when you cannot buy or sell its shares.

|

| 1 | Please see the section “How to Purchase Shares,” which provides additional information regarding who can receive a purchase order. |

|

•

|

Equity securities (including shares of closed-end investment companies and ETFs), exchange traded notes, rights, and warrants — listed equity securities are valued at the last sale price quoted on the exchange where they are traded most extensively or, if there is no reported sale during the day, the closing bid quotation as reported by a third-party pricing service. Securities traded on the NASDAQ Global Select Market, NASDAQ Global Market and NASDAQ Capital Market are valued at the NASDAQ Official Closing Price (“NOCP”), or if lacking an NOCP, at the most recent bid quotations on the

|

|

applicable NASDAQ Market. Unlisted equity securities (except unlisted preferred equity securities discussed below) are valued at the last sale price quoted in the market where they are traded most extensively or, if there is no reported sale during the day, the closing bid quotation as reported by a third-party pricing service. If there is no sale price or closing bid quotation available, unlisted equity securities will be valued using evaluated bids furnished by a third-party pricing service, if available. In some foreign markets, an official close price and a last sale price may be available from the foreign exchange or market. In those cases, the official close price is used. Valuations based on information from foreign markets may be subject to the Funds’ fair value policies described below. If a right is not traded on any exchange, its value is based on the market value of the underlying security, less the cost to subscribe to the underlying security (e.g., to exercise the right), adjusted for the subscription ratio. If a warrant is not traded on any exchange, a price is obtained from a broker-dealer.

|

|

•

|

Debt securities and unlisted preferred equity securities — evaluated bids furnished to a Fund by a third-party pricing service using market information, transactions for comparable securities and various relationships between securities, if available, or bid prices obtained from broker-dealers.

|

|

•

|

Senior Loans — bid prices supplied by a third-party pricing service, if available, or bid prices obtained from broker-dealers.

|

|

•

|

Bilateral Swaps — bilateral credit default swaps are valued based on mid prices (between the bid price and the ask price) supplied by a third-party pricing service. Bilateral interest rate swaps and bilateral standardized commodity and equity index total return swaps are valued based on prices supplied by a third-party pricing service. If prices from a third-party pricing service are not available, prices from a broker-dealer may be used.

|

|

•

|

Centrally Cleared Swaps — settlement prices of the clearing house on which the contracts were traded or prices obtained from broker-dealers.

|

|

•

|

Options — domestic exchange-traded index and single name equity options contracts (including options on ETFs) are valued at the mean of the National Best Bid and Offer quotations as determined by the Options Price Reporting Authority. Foreign exchange-traded single name equity options contracts are valued at the most recent settlement price. Options contracts on foreign indices are priced at the most recent settlement price. Options on futures contracts are valued using the current settlement price on the exchange on which, over time, they are traded most extensively. Other exchange-traded options are valued at the average of the closing bid and ask quotations on the exchange on which, over time, they are traded most extensively. OTC currency options and swaptions are valued at mid prices (between the bid price and the ask price) supplied by a third-party pricing service, if available. Other OTC options contracts (including currency options and swaptions not priced through a third-party pricing service) are valued based on prices obtained from broker-dealers. Valuations based on information from foreign markets may be subject to the Funds’ fair value policies as described below.

|

|

•

|

Futures —most recent settlement price on the exchange on which the valuation designee believes that, over time, they are traded most extensively. Valuations based on information from foreign markets may be subject to the Funds’ fair value policies as described below.

|

|

•

|

Forward Foreign Currency Contracts — interpolated rates determined based on information provided by a third-party pricing service.

|

|

•

|

Mutual Funds - net asset value.

|

|