1940 Act File No. 811-05002

SECURITIES AND EXCHANGE COMMISSION

FORM

Vice President and Secretary

100 Summer Street

Boston, MA 02110-2146

|

Copy to:

John S. Marten

Vedder Price P.C.

222 North LaSalle Street

Chicago, IL 60601-1104 |

|

|

|

|

|

|

|

| |

|

1 | |

|

1 | |

|

1 | |

|

3 | |

|

9 | |

|

10 | |

|

10 | |

|

10 | |

|

10 | |

|

| |

|

11 | |

|

11 | |

|

11 | |

|

12 | |

|

18 | |

|

18 | |

|

18 | |

|

18 | |

|

18 | |

|

| |

|

19 | |

|

19 | |

|

19 | |

|

20 | |

|

23 | |

|

24 | |

|

24 | |

|

24 | |

|

24 |

|

| |

|

25 | |

|

25 | |

|

25 | |

|

26 | |

|

29 | |

|

29 | |

|

29 | |

|

29 | |

|

29 | |

|

| |

|

30 | |

|

30 | |

|

30 | |

|

31 | |

|

34 | |

|

35 | |

|

35 | |

|

35 | |

|

35 | |

|

| |

|

36 | |

|

36 | |

|

36 | |

|

37 | |

|

40 | |

|

40 | |

|

40 | |

|

40 | |

|

40 |

|

| |

|

42 | |

|

42 | |

|

42 | |

|

43 | |

|

45 | |

|

46 | |

|

46 | |

|

46 | |

|

46 | |

|

| |

|

47 | |

|

47 | |

|

47 | |

|

48 | |

|

51 | |

|

51 | |

|

51 | |

|

51 | |

|

52 | |

|

| |

|

53 | |

|

53 | |

|

65 | |

|

74 | |

|

79 | |

|

84 | |

|

90 | |

|

94 | |

|

98 | |

|

103 | |

|

105 | |

|

108 |

|

| |

|

110 | |

|

110 | |

|

111 | |

|

113 | |

|

115 | |

|

115 | |

|

116 | |

|

125 | |

|

125 | |

|

129 |

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Acquired funds fees and expenses |

|

|

Total annual fund operating expenses |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 1 | DWS Alternative Asset Allocation VIP |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

MSCI ACWI All Cap

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

|

Bloomberg Global

Aggregate Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

- |

|

|

Blended Index (reflects

no deduction for fees,

expenses or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Total annual fund operating expenses |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 11 | DWS Global Income Builder VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

MSCI ACWI Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Bloomberg

U.S. Universal Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Blended Index (reflects

no deduction for fees,

expenses, or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses |

|

|

Total annual fund operating expenses |

|

|

Fee waiver/expense reimbursement |

|

|

Total annual fund operating expenses after fee waiver/

expense reimbursement |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 19 | DWS Small Mid Cap Value VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

Russell 3000® Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Russell 2500™ Value

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Total annual fund operating expenses |

|

|

Fee waiver/expense reimbursement |

|

|

Total annual fund operating expenses after fee waiver/

expense reimbursement |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 25 | DWS International Opportunities VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

MSCI ACWI ex USA

Index (reflects no deduc-

tions for fees, expenses,

or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Total annual fund operating expenses |

|

|

Fee waiver/expense reimbursement |

|

|

Total annual fund operating expenses after fee waiver/

expense reimbursement |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 30 | DWS High Income VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

Bloomberg U.S. Aggre-

gate Bond Index

(reflects no deductions

for fees, expenses, or

taxes) |

|

|

- |

|

|

ICE BofA US High Yield

Index (reflects no deduc-

tions for fees, expenses,

or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Total annual fund operating expenses |

|

|

Fee waiver/expense reimbursement |

|

|

Total annual fund operating expenses after fee waiver/

expense reimbursement |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 36 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

Russell 1000® Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Russell 1000® Value

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Total annual fund operating expenses |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 42 | DWS Government Money Market VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses |

|

|

Total annual fund operating expenses |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 47 | DWS Small Mid Cap Growth VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class A before tax |

|

|

|

|

|

Russell 3000® Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Russell 2500™ Growth

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

| Prospectus May 1, 2026 | 53 | Fund Details |

|

Real Asset |

48

% |

|

DWS Enhanced Commodity Strategy Fund |

17

% |

|

DWS RREEF Global Infrastructure Fund |

17

% |

|

DWS RREEF Real Estate Securities Fund |

9

% |

|

Xtrackers RREEF Global Natural Resources ETF |

5

% |

|

Alternative Equity |

22

% |

|

State Street SPDR Bloomberg Convertible Securities ETF |

17

% |

|

iShares Preferred & Income Securities ETF |

5

% |

|

Alternative Fixed Income |

21

% |

|

DWS Floating Rate Fund |

9

% |

|

iShares JP Morgan USD Emerging Markets Bond ETF |

9

% |

|

DWS Emerging Markets Fixed Income Fund |

3

% |

|

Absolute Return |

8

% |

|

DWS Global Macro Fund |

8

% |

|

Cash Equivalents |

1

% |

|

DWS Central Cash Management Government Fund |

1

% |

|

Other Assets and Liabilities, Net |

0

% |

|

Total |

100

% |

|

Fund Name |

Fee Paid |

|

DWS Alternative Asset Alloca-

tion VIP |

0.100

%* |

|

DWS Global Income Builder

VIP |

0.370

% |

|

DWS Small Mid Cap Value VIP |

0.603

%** |

|

DWS International Opportuni-

ties VIP |

0.173

%** |

|

DWS High Income VIP |

0.296

%** |

|

DWS CROCI® U.S. VIP |

0.512

%** |

|

DWS Government Money

Market VIP |

0.235

% |

|

DWS Small Mid Cap Growth

VIP |

0.550

% |

For DWS Alternative Asset Allocation VIP, the Advisor has contractually agreed to waive its fees and/or reimburse fund expenses through September 30, 2026 to the extent necessary to maintain the fund’s total annual operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage and interest expenses) at 1.06% for Class A shares. The agreement may only be terminated with the consent of the fund’s Board. Because acquired fund fees and expenses are presented as of the fund’s most recent fiscal year end, individual shareholders may experience total operating expenses higher or lower than this expense cap depending upon when shares are redeemed and the fund’s actual allocations to acquired funds.

| Prospectus May 1, 2026 | 110 | Investing in the Funds |

|

( |

Total

Assets |

− |

Total

Liabilities |

) |

÷ |

Total Number of

Shares Outstanding |

= |

NAV |

| Prospectus May 1, 2026 | 116 | Financial Highlights |

|

DWS Alternative Asset Allocation VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$12.95 |

$12.74 |

$12.99 |

$15.13 |

$13.70 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.51 |

.52 |

.47 |

.88 |

1.04 |

|

Net realized and unrealized gain (loss) |

.81 |

.18 |

.29 |

(1.93

) |

.69 |

|

Total from investment operations |

1.32 |

.70 |

.76 |

(1.05

) |

1.73 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.56

) |

(.48

) |

(.89

) |

(1.08

) |

(.30

) |

|

Net realized gains |

— |

(.01

) |

(.12

) |

(.01

) |

— |

|

Total distributions |

(.56

) |

(.49

) |

(1.01

) |

(1.09

) |

(.30

) |

|

Net asset value, end of period |

$13.71 |

$12.95 |

$12.74 |

$12.99 |

$15.13 |

|

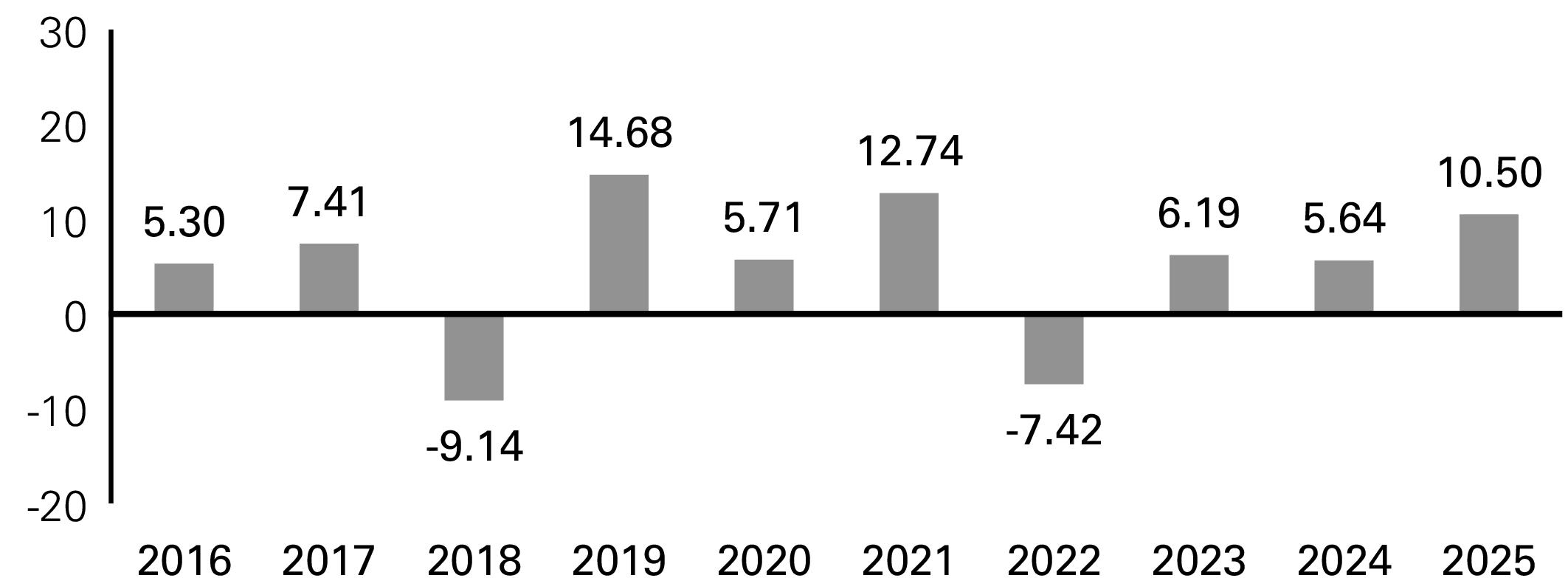

Total Return (%)b |

10.50 |

5.64 |

6.19 |

(7.42

) |

12.74 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

61 |

56 |

51 |

46 |

47 |

|

Ratio of expenses (%)c,d |

.24 |

.23 |

.23 |

.23 |

.23 |

|

Ratio of net investment income (%) |

3.86 |

4.02 |

3.76 |

6.44 |

7.13 |

|

Portfolio turnover rate (%) |

18 |

25 |

0 |

12 |

19 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower if the Advisor had not reduced some Underlying DWS Funds’ expenses. |

|

c |

The Fund invests in other Funds and indirectly bears its proportionate share of fees and expenses incurred by the Underlying Funds in which the

Fund is invested. This ratio does not include these indirect fees and expenses. |

|

d |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 117 | Financial Highlights |

|

DWS Global Income Builder VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$23.65 |

$22.49 |

$20.22 |

$26.78 |

$25.07 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.78 |

.98 |

.73 |

.61 |

.62 |

|

Net realized and unrealized gain (loss) |

2.23 |

1.00 |

2.21 |

(4.47

) |

2.08 |

|

Total from investment operations |

3.01 |

1.98 |

2.94 |

(3.86

) |

2.70 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(1.12

) |

(.82

) |

(.67

) |

(.69

) |

(.62

) |

|

Net realized gains |

(3.19

) |

— |

— |

(2.01

) |

(.37

) |

|

Total distributions |

(4.31

) |

(.82

) |

(.67

) |

(2.70

) |

(.99

) |

|

Net asset value, end of period |

$22.35 |

$23.65 |

$22.49 |

$20.22 |

$26.78 |

|

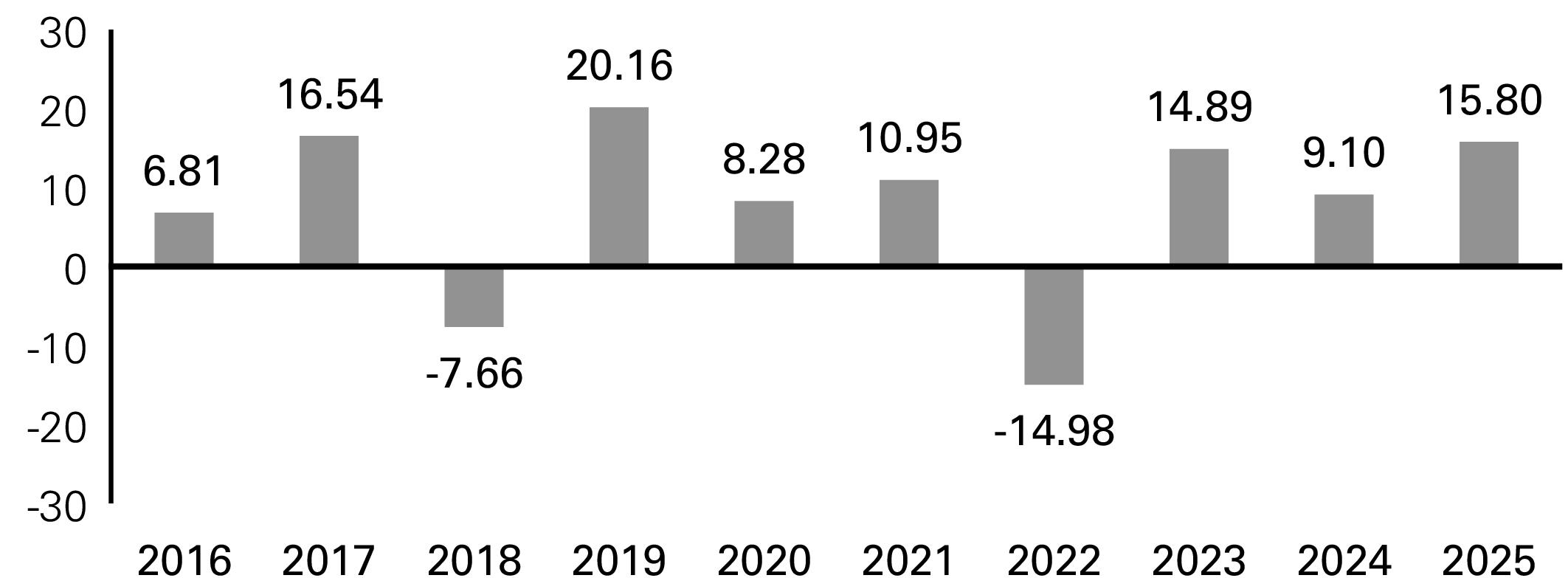

Total Return (%) |

15.80 |

9.10 |

14.89 |

(14.98

) |

10.95 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

116 |

110 |

110 |

103 |

131 |

|

Ratio of expenses (%)b |

.62 |

.63 |

.65 |

.65 |

.61 |

|

Ratio of net investment income (%) |

3.56 |

4.20 |

3.47 |

2.80 |

2.36 |

|

Portfolio turnover rate (%) |

165 |

294 |

180 |

95 |

104 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 118 | Financial Highlights |

|

DWS Small Mid Cap Value VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$13.81 |

$13.86 |

$12.73 |

$15.47 |

$12.00 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.08 |

.14 |

.15 |

.15 |

.11 |

|

Net realized and unrealized gain (loss) |

1.93 |

.68 |

1.64 |

(2.57

) |

3.54 |

|

Total from investment operations |

2.01 |

.82 |

1.79 |

(2.42

) |

3.65 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.14

) |

(.17

) |

(.15

) |

(.12

) |

(.18

) |

|

Net realized gains |

(1.59

) |

(.70

) |

(.51

) |

(.20

) |

— |

|

Total distributions |

(1.73

) |

(.87

) |

(.66

) |

(.32

) |

(.18

) |

|

Net asset value, end of period |

$14.09 |

$13.81 |

$13.86 |

$12.73 |

$15.47 |

|

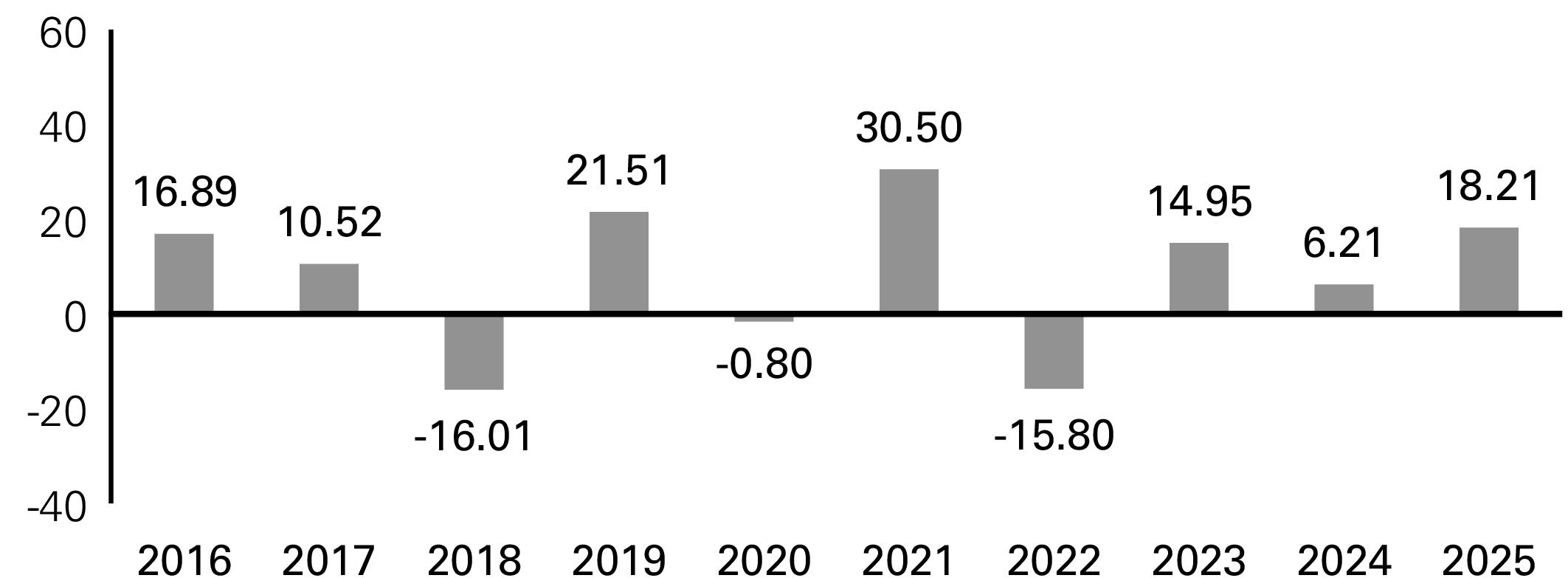

Total Return (%)b |

18.21 |

6.21 |

14.95 |

(15.80

) |

30.50 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

68 |

65 |

67 |

64 |

82 |

|

Ratio of expenses before expense reductions (%)c |

.87 |

.87 |

.87 |

.87 |

.85 |

|

Ratio of expenses after expense reductions (%)c |

.82 |

.82 |

.81 |

.83 |

.83 |

|

Ratio of net investment income (%) |

.61 |

.98 |

1.16 |

1.14 |

.76 |

|

Portfolio turnover rate (%) |

53 |

41 |

28 |

33 |

32 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 119 | Financial Highlights |

|

DWS International Opportunities VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$16.32 |

$15.11 |

$13.12 |

$18.80 |

$17.65 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.18 |

.15 |

.18 |

.11 |

.08 |

|

Net realized and unrealized gain (loss) |

2.89 |

1.25 |

1.92 |

(5.45

) |

1.34 |

|

Total from investment operations |

3.07 |

1.40 |

2.10 |

(5.34

) |

1.42 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.17

) |

(.19

) |

(.11

) |

(.15

) |

(.06

) |

|

Net realized gains |

— |

— |

— |

(.19

) |

(.21

) |

|

Total distributions |

(.17

) |

(.19

) |

(.11

) |

(.34

) |

(.27

) |

|

Net asset value, end of period |

$19.22 |

$16.32 |

$15.11 |

$13.12 |

$18.80 |

|

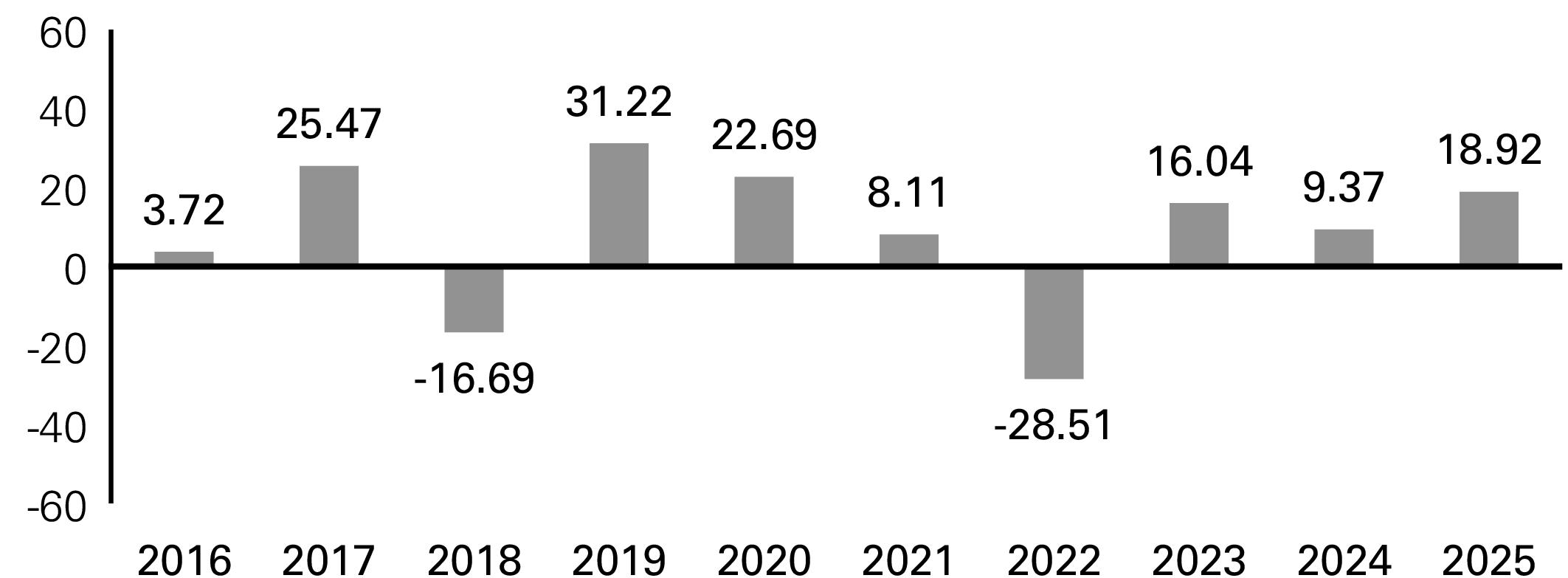

Total Return (%)b |

18.92 |

9.37 |

16.04 |

(28.51

) |

8.11 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

23 |

20 |

20 |

19 |

22 |

|

Ratio of expenses before expense reductions (%)c |

1.29 |

1.34 |

1.35 |

1.32 |

1.33 |

|

Ratio of expenses after expense reductions (%)c |

.84 |

.84 |

.89 |

.92 |

.90 |

|

Ratio of net investment income (%) |

.99 |

.94 |

1.27 |

.78 |

.41 |

|

Portfolio turnover rate (%) |

21 |

8 |

13 |

17 |

20 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 120 | Financial Highlights |

|

DWS High Income VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$5.67 |

$5.63 |

$5.34 |

$6.18 |

$6.23 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.35 |

.35 |

.33 |

.27 |

.27 |

|

Net realized and unrealized gain (loss) |

.13 |

.03 |

.25 |

(.81

) |

(.03

) |

|

Total from investment operations |

.48 |

.38 |

.58 |

(.54

) |

.24 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.41

) |

(.34

) |

(.29

) |

(.30

) |

(.29

) |

|

Net asset value, end of period |

$5.74 |

$5.67 |

$5.63 |

$5.34 |

$6.18 |

|

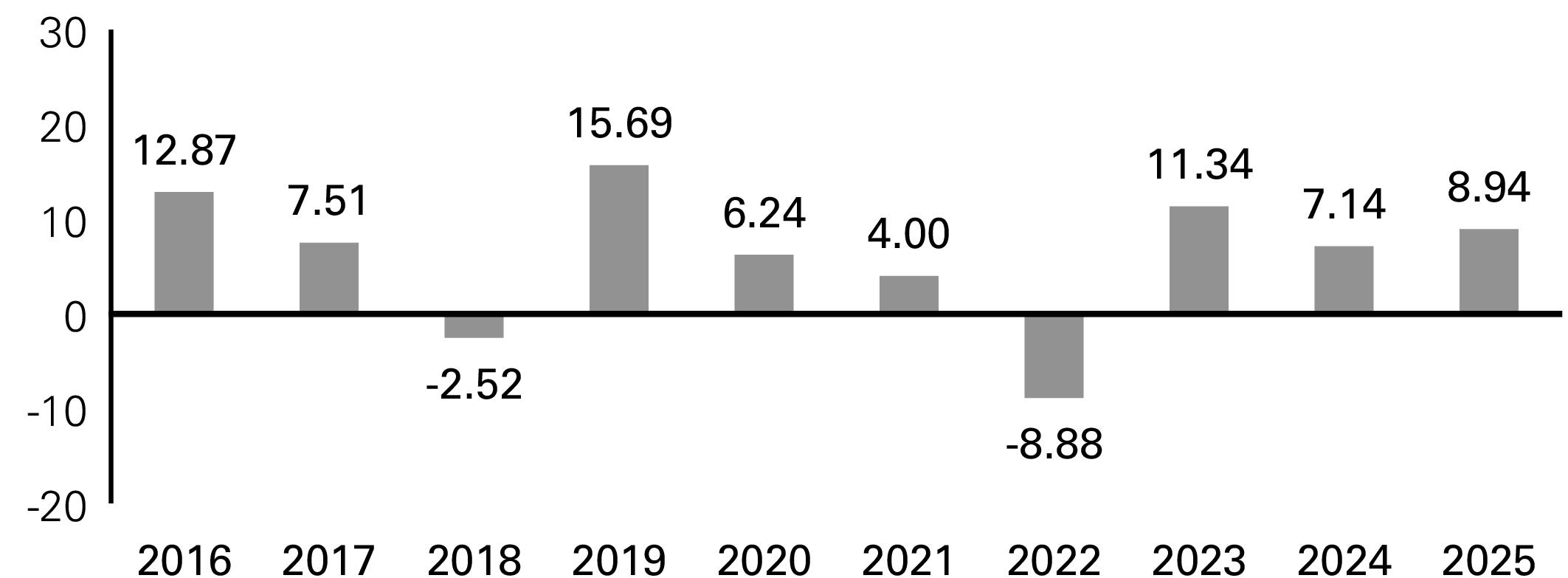

Total Return (%)b |

8.94 |

7.14 |

11.34 |

(8.88

) |

4.00 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

43 |

43 |

43 |

41 |

51 |

|

Ratio of expenses before expense reductions (%)c |

.94 |

.91 |

.90 |

.90 |

.84 |

|

Ratio of expenses after expense reductions (%)c |

.73 |

.70 |

.70 |

.71 |

.71 |

|

Ratio of net investment income (%) |

6.28 |

6.27 |

6.07 |

4.82 |

4.32 |

|

Portfolio turnover rate (%) |

154 |

143 |

62 |

45 |

56 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 121 | Financial Highlights |

|

DWS CROCI® U.S. VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$18.08 |

$15.59 |

$13.14 |

$16.05 |

$12.92 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.29 |

.22 |

.24 |

.23 |

.24 |

|

Net realized and unrealized gain (loss) |

2.32 |

2.52 |

2.45 |

(2.68

) |

3.17 |

|

Total from investment operations |

2.61 |

2.74 |

2.69 |

(2.45

) |

3.41 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.25

) |

(.25

) |

(.24

) |

(.25

) |

(.28

) |

|

Net realized gains |

(1.62

) |

— |

— |

(.21

) |

— |

|

Total distributions |

(1.87

) |

(.25

) |

(.24

) |

(.46

) |

(.28

) |

|

Net asset value, end of period |

$18.82 |

$18.08 |

$15.59 |

$13.14 |

$16.05 |

|

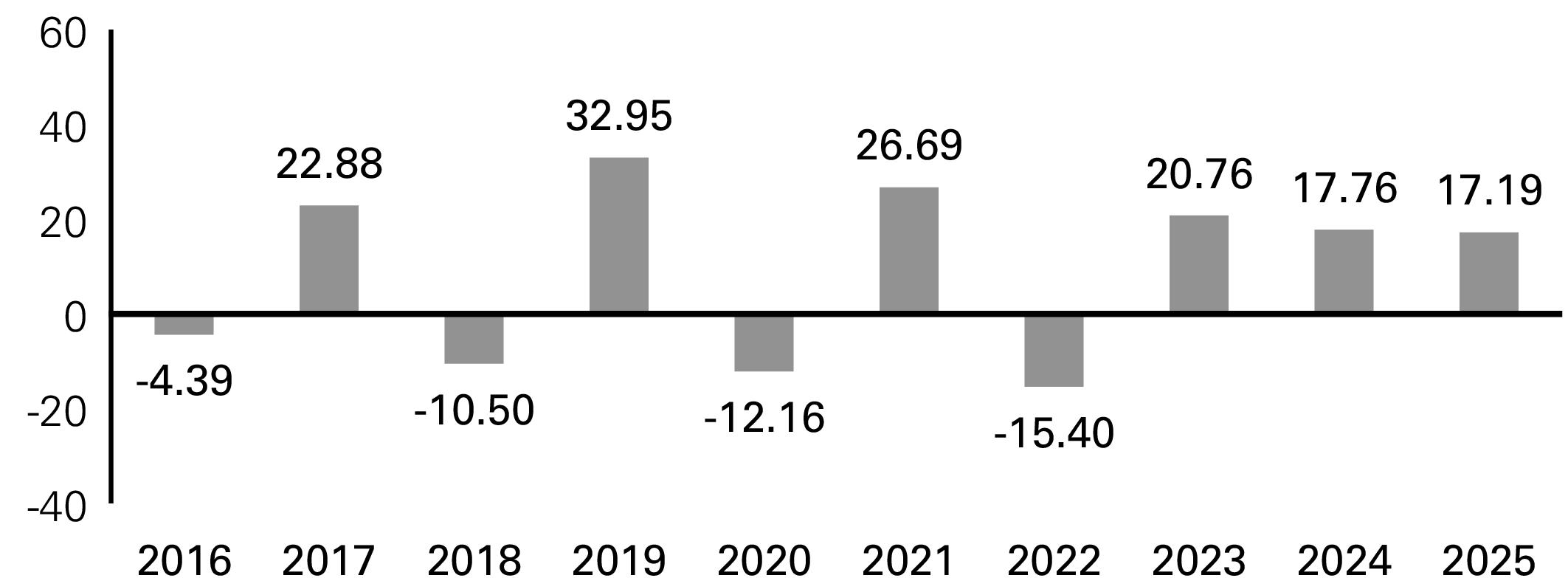

Total Return (%)b |

17.19 |

17.76 |

20.76 |

(15.40

) |

26.69 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

146 |

138 |

131 |

116 |

149 |

|

Ratio of expenses before expense reductions (%)c |

.80 |

.78 |

.79 |

.79 |

.78 |

|

Ratio of expenses after expense reductions (%)c |

.71 |

.68 |

.68 |

.65 |

.71 |

|

Ratio of net investment income (%) |

1.66 |

1.31 |

1.69 |

1.66 |

1.62 |

|

Portfolio turnover rate (%) |

76 |

60 |

60 |

60 |

99 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 122 | Financial Highlights |

|

DWS Government Money Market VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$1.00 |

$1.00 |

$1.00 |

$1.00 |

$1.00 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment income |

.039 |

.048 |

.047 |

.013 |

.000

* |

|

Net realized gain (loss) |

.000

* |

.000

* |

.000

* |

(.000

)* |

(.000

)* |

|

Total from investment operations |

.039 |

.048 |

.047 |

.013 |

.000

* |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.039

) |

(.048

) |

(.047

) |

(.013

) |

(.000

)* |

|

Net asset value, end of period |

$1.00 |

$1.00 |

$1.00 |

$1.00 |

$1.00 |

|

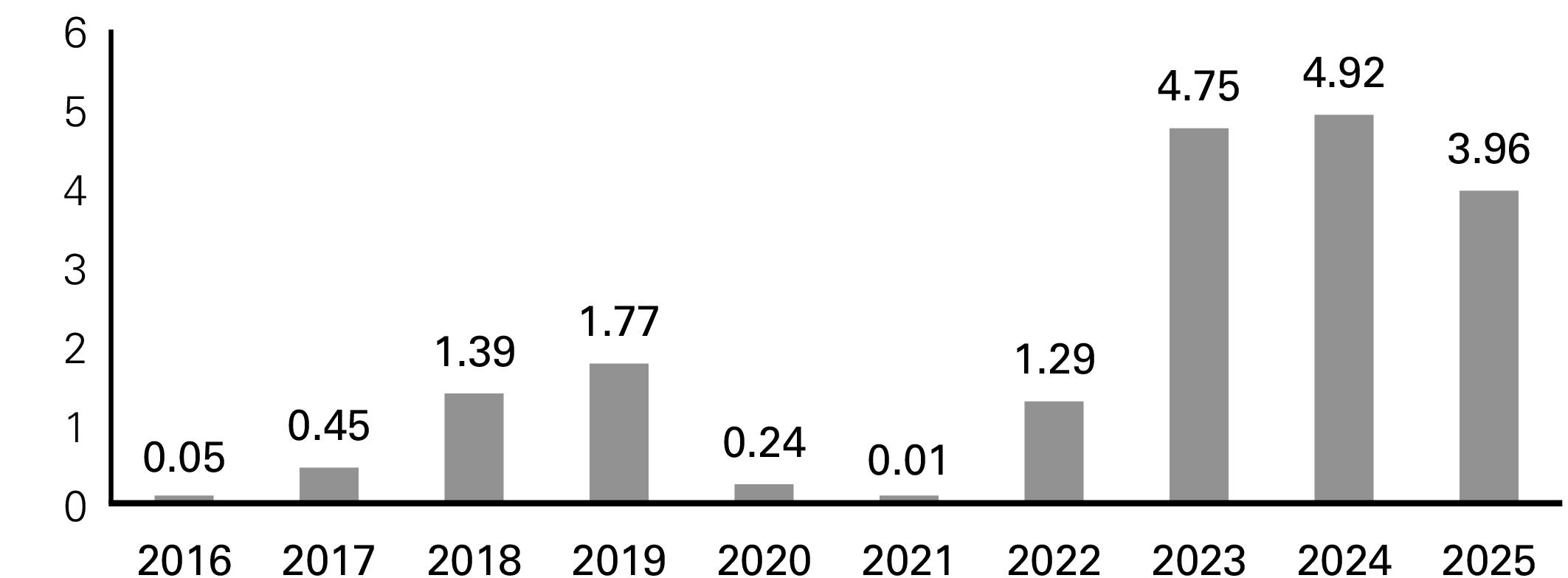

Total Return (%) |

3.96 |

4.92 |

4.75 |

1.29

a |

.01

a |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

208 |

215 |

286 |

187 |

197 |

|

Ratio of expenses before expense reductions (%)b |

.40 |

.40 |

.39 |

.40 |

.42 |

|

Ratio of expenses after expense reductions (%)b |

.40 |

.40 |

.39 |

.32 |

.06 |

|

Ratio of net investment income (%) |

3.89 |

4.80 |

4.70 |

1.25 |

.01 |

|

a |

Total return would have been lower had certain expenses not been reduced. |

|

b |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

|

* |

Amount is less than $.0005. |

| Prospectus May 1, 2026 | 123 | Financial Highlights |

|

DWS Small Mid Cap Growth VIP — Class A | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data | |||||

|

Net asset value, beginning of period |

$14.27 |

$13.70 |

$11.97 |

$18.87 |

$17.43 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment income (loss)a |

(.01

) |

(.03

) |

.00

* |

(.00

)* |

(.06

) |

|

Net realized and unrealized gain (loss) |

.96 |

.73 |

2.17 |

(5.10

) |

2.43 |

|

Total from investment operations |

.95 |

.70 |

2.17 |

(5.10

) |

2.37 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

— |

— |

(.00

)* |

— |

(.01

) |

|

Net realized gains |

(1.03

) |

(.13

) |

(.44

) |

(1.80

) |

(.92

) |

|

Total distributions |

(1.03

) |

(.13

) |

(.44

) |

(1.80

) |

(.93

) |

|

Net asset value, end of period |

$14.19 |

$14.27 |

$13.70 |

$11.97 |

$18.87 |

|

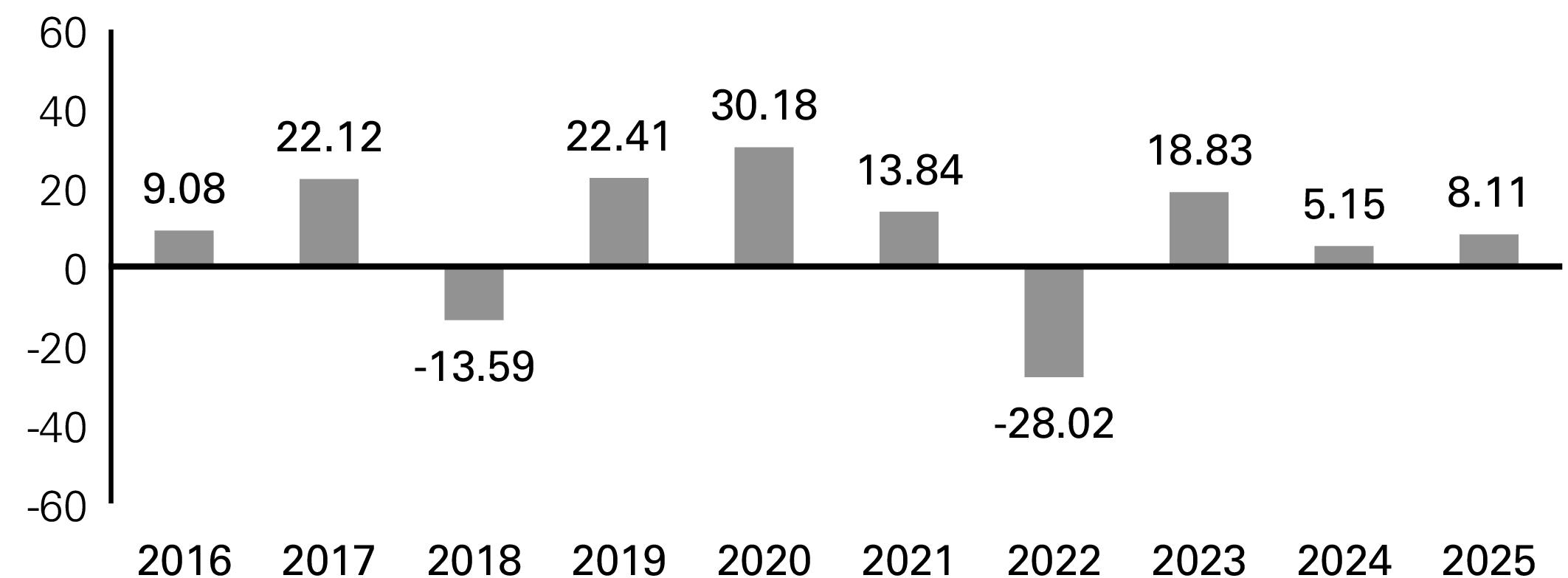

Total Return (%) |

8.11 |

5.15 |

18.83

b |

(28.02

)b |

13.84 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

48 |

49 |

53 |

50 |

75 |

|

Ratio of expenses before expense reductions (%)c |

.85 |

.83 |

.85 |

.83 |

.78 |

|

Ratio of expenses after expense reductions (%)c |

.85 |

.83 |

.84 |

.81 |

.78 |

|

Ratio of net investment income (loss) (%) |

(.08

) |

(.22

) |

.02 |

(.02

) |

(.33

) |

|

Portfolio turnover rate (%) |

11 |

4 |

4 |

11 |

16 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

|

* |

Amount is less than $.005. |

| Prospectus May 1, 2026 | 124 | Financial Highlights |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.93% |

4.07% |

$10,407.00 |

$94.89 |

|

2 |

10.25% |

0.93% |

8.31% |

$10,830.56 |

$98.75 |

|

3 |

15.76% |

0.93% |

12.71% |

$11,271.37 |

$102.77 |

|

4 |

21.55% |

0.93% |

17.30% |

$11,730.11 |

$106.96 |

|

5 |

27.63% |

0.93% |

22.08% |

$12,207.53 |

$111.31 |

|

6 |

34.01% |

0.93% |

27.04% |

$12,704.38 |

$115.84 |

|

7 |

40.71% |

0.93% |

32.21% |

$13,221.44 |

$120.56 |

|

8 |

47.75% |

0.93% |

37.60% |

$13,759.56 |

$125.46 |

|

9 |

55.13% |

0.93% |

43.20% |

$14,319.57 |

$130.57 |

|

10 |

62.89% |

0.93% |

49.02% |

$14,902.38 |

$135.88 |

|

Total |

$1,142.99 | ||||

| Prospectus May 1, 2026 | 125 | Appendix |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.61% |

4.39% |

$10,439.00 |

$62.34 |

|

2 |

10.25% |

0.61% |

8.97% |

$10,897.27 |

$65.08 |

|

3 |

15.76% |

0.61% |

13.76% |

$11,375.66 |

$67.93 |

|

4 |

21.55% |

0.61% |

18.75% |

$11,875.05 |

$70.91 |

|

5 |

27.63% |

0.61% |

23.96% |

$12,396.37 |

$74.03 |

|

6 |

34.01% |

0.61% |

29.41% |

$12,940.57 |

$77.28 |

|

7 |

40.71% |

0.61% |

35.09% |

$13,508.66 |

$80.67 |

|

8 |

47.75% |

0.61% |

41.02% |

$14,101.69 |

$84.21 |

|

9 |

55.13% |

0.61% |

47.21% |

$14,720.75 |

$87.91 |

|

10 |

62.89% |

0.61% |

53.67% |

$15,367.00 |

$91.77 |

|

Total |

$762.13 | ||||

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.80% |

4.20% |

$10,420.00 |

$81.68 |

|

2 |

10.25% |

0.87% |

8.50% |

$10,850.35 |

$92.53 |

|

3 |

15.76% |

0.87% |

12.98% |

$11,298.47 |

$96.35 |

|

4 |

21.55% |

0.87% |

17.65% |

$11,765.09 |

$100.33 |

|

5 |

27.63% |

0.87% |

22.51% |

$12,250.99 |

$104.47 |

|

6 |

34.01% |

0.87% |

27.57% |

$12,756.96 |

$108.78 |

|

7 |

40.71% |

0.87% |

32.84% |

$13,283.82 |

$113.28 |

|

8 |

47.75% |

0.87% |

38.32% |

$13,832.44 |

$117.96 |

|

9 |

55.13% |

0.87% |

44.04% |

$14,403.72 |

$122.83 |

|

10 |

62.89% |

0.87% |

49.99% |

$14,998.59 |

$127.90 |

|

Total |

$1,066.11 | ||||

| Prospectus May 1, 2026 | 126 | Appendix |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.86% |

4.14% |

$10,414.00 |

$87.78 |

|

2 |

10.25% |

1.30% |

7.99% |

$10,799.32 |

$137.89 |

|

3 |

15.76% |

1.30% |

11.99% |

$11,198.89 |

$142.99 |

|

4 |

21.55% |

1.30% |

16.13% |

$11,613.25 |

$148.28 |

|

5 |

27.63% |

1.30% |

20.43% |

$12,042.94 |

$153.77 |

|

6 |

34.01% |

1.30% |

24.89% |

$12,488.53 |

$159.45 |

|

7 |

40.71% |

1.30% |

29.51% |

$12,950.61 |

$165.35 |

|

8 |

47.75% |

1.30% |

34.30% |

$13,429.78 |

$171.47 |

|

9 |

55.13% |

1.30% |

39.27% |

$13,926.68 |

$177.82 |

|

10 |

62.89% |

1.30% |

44.42% |

$14,441.97 |

$184.40 |

|

Total |

$1,529.20 | ||||

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.71% |

4.29% |

$10,429.00 |

$72.52 |

|

2 |

10.25% |

0.90% |

8.57% |

$10,856.59 |

$95.79 |

|

3 |

15.76% |

0.90% |

13.02% |

$11,301.71 |

$99.71 |

|

4 |

21.55% |

0.90% |

17.65% |

$11,765.08 |

$103.80 |

|

5 |

27.63% |

0.90% |

22.47% |

$12,247.45 |

$108.06 |

|

6 |

34.01% |

0.90% |

27.50% |

$12,749.59 |

$112.49 |

|

7 |

40.71% |

0.90% |

32.72% |

$13,272.33 |

$117.10 |

|

8 |

47.75% |

0.90% |

38.16% |

$13,816.49 |

$121.90 |

|

9 |

55.13% |

0.90% |

43.83% |

$14,382.97 |

$126.90 |

|

10 |

62.89% |

0.90% |

49.73% |

$14,972.67 |

$132.10 |

|

Total |

$1,090.37 | ||||

| Prospectus May 1, 2026 | 127 | Appendix |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.71% |

4.29% |

$10,429.00 |

$72.52 |

|

2 |

10.25% |

0.79% |

8.68% |

$10,868.06 |

$84.12 |

|

3 |

15.76% |

0.79% |

13.26% |

$11,325.61 |

$87.66 |

|

4 |

21.55% |

0.79% |

18.02% |

$11,802.41 |

$91.36 |

|

5 |

27.63% |

0.79% |

22.99% |

$12,299.30 |

$95.20 |

|

6 |

34.01% |

0.79% |

28.17% |

$12,817.10 |

$99.21 |

|

7 |

40.71% |

0.79% |

33.57% |

$13,356.70 |

$103.39 |

|

8 |

47.75% |

0.79% |

39.19% |

$13,919.01 |

$107.74 |

|

9 |

55.13% |

0.79% |

45.05% |

$14,505.00 |

$112.27 |

|

10 |

62.89% |

0.79% |

51.16% |

$15,115.66 |

$117.00 |

|

Total |

$970.47 | ||||

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.39% |

4.61% |

$10,461.00 |

$39.90 |

|

2 |

10.25% |

0.39% |

9.43% |

$10,943.25 |

$41.74 |

|

3 |

15.76% |

0.39% |

14.48% |

$11,447.74 |

$43.66 |

|

4 |

21.55% |

0.39% |

19.75% |

$11,975.48 |

$45.68 |

|

5 |

27.63% |

0.39% |

25.28% |

$12,527.55 |

$47.78 |

|

6 |

34.01% |

0.39% |

31.05% |

$13,105.07 |

$49.98 |

|

7 |

40.71% |

0.39% |

37.09% |

$13,709.21 |

$52.29 |

|

8 |

47.75% |

0.39% |

43.41% |

$14,341.20 |

$54.70 |

|

9 |

55.13% |

0.39% |

50.02% |

$15,002.33 |

$57.22 |

|

10 |

62.89% |

0.39% |

56.94% |

$15,693.94 |

$59.86 |

|

Total |

$492.81 | ||||

| Prospectus May 1, 2026 | 128 | Appendix |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

0.85% |

4.15% |

$10,415.00 |

$86.76 |

|

2 |

10.25% |

0.85% |

8.47% |

$10,847.22 |

$90.36 |

|

3 |

15.76% |

0.85% |

12.97% |

$11,297.38 |

$94.11 |

|

4 |

21.55% |

0.85% |

17.66% |

$11,766.22 |

$98.02 |

|

5 |

27.63% |

0.85% |

22.55% |

$12,254.52 |

$102.09 |

|

6 |

34.01% |

0.85% |

27.63% |

$12,763.08 |

$106.32 |

|

7 |

40.71% |

0.85% |

32.93% |

$13,292.75 |

$110.74 |

|

8 |

47.75% |

0.85% |

38.44% |

$13,844.40 |

$115.33 |

|

9 |

55.13% |

0.85% |

44.19% |

$14,418.94 |

$120.12 |

|

10 |

62.89% |

0.85% |

50.17% |

$15,017.33 |

$125.10 |

|

Total |

$1,048.95 | ||||

| Prospectus May 1, 2026 | 129 | Appendix |

| Prospectus May 1, 2026 | 130 | Appendix |

|

DWS |

222 South Riverside Plaza

Chicago, IL 60606-5808

dws.com |

|

|

(800) 728-3337 |

|

Distributor |

DWS Distributors, Inc.

222 South Riverside Plaza

Chicago, IL 60606-5808

(800) 621-1148 |

|

SEC File Number |

Deutsche DWS Variable Series II

811-05002 |

|

|

|

|

|

|

|

| |

|

1 | |

|

1 | |

|

1 | |

|

3 | |

|

9 | |

|

10 | |

|

10 | |

|

10 | |

|

10 | |

|

| |

|

11 | |

|

11 | |

|

11 | |

|

12 | |

|

15 | |

|

16 | |

|

16 | |

|

16 | |

|

16 | |

|

| |

|

17 | |

|

17 | |

|

29 | |

|

34 | |

|

35 | |

|

37 |

|

| |

|

38 | |

|

38 | |

|

39 | |

|

41 | |

|

42 | |

|

42 | |

|

43 | |

|

44 | |

|

46 | |

|

46 | |

|

47 |

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses1 |

|

|

Acquired funds fees and expenses |

|

|

Total annual fund operating expenses |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 1 | DWS Alternative Asset Allocation VIP |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class B before tax |

|

|

|

|

|

MSCI ACWI All Cap

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

|

Bloomberg Global

Aggregate Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

- |

|

|

Blended Index (reflects

no deduction for fees,

expenses or taxes) |

|

|

|

|

|

(paid directly from your investment) |

|

(expenses that you pay each year as a % of the value of your investment)

|

Management fee |

|

|

Distribution/service (12b-1) fees |

|

|

Other expenses |

|

|

Total annual fund operating expenses |

|

|

Fee waiver/expense reimbursement |

|

|

Total annual fund operating expenses after fee waiver/

expense reimbursement |

|

|

|

1 Year |

3 Years |

5 Years |

10 Years |

|

|

$ |

$ |

$ |

$ |

| Prospectus May 1, 2026 | 11 | DWS Small Mid Cap Value VIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(For periods ended 12/31/2025 expressed as a %)

|

|

Class

Inception |

1

Year |

5

Years |

10

Years |

|

Class B before tax |

|

|

|

|

|

Russell 3000® Index

(reflects no deduction for

fees, expenses or taxes) |

|

|

|

|

|

Russell 2500™ Value

Index (reflects no deduc-

tion for fees, expenses

or taxes) |

|

|

|

|

| Prospectus May 1, 2026 | 17 | Fund Details |

|

Real Asset |

48

% |

|

DWS Enhanced Commodity Strategy Fund |

17

% |

|

DWS RREEF Global Infrastructure Fund |

17

% |

|

DWS RREEF Real Estate Securities Fund |

9

% |

|

Xtrackers RREEF Global Natural Resources ETF |

5

% |

|

Alternative Equity |

22

% |

|

State Street SPDR Bloomberg Convertible Securities ETF |

17

% |

|

iShares Preferred & Income Securities ETF |

5

% |

|

Alternative Fixed Income |

21

% |

|

DWS Floating Rate Fund |

9

% |

|

iShares JP Morgan USD Emerging Markets Bond ETF |

9

% |

|

DWS Emerging Markets Fixed Income Fund |

3

% |

|

Absolute Return |

8

% |

|

DWS Global Macro Fund |

8

% |

|

Cash Equivalents |

1

% |

|

DWS Central Cash Management Government Fund |

1

% |

|

Other Assets and Liabilities, Net |

0

% |

|

Total |

100

% |

|

Fund Name |

Fee Paid |

|

DWS Alternative Asset Alloca-

tion VIP |

0.100

%* |

|

DWS Small Mid Cap Value VIP |

0.603

%** |

For DWS Alternative Asset Allocation VIP, the Advisor has contractually agreed to waive its fees and/or reimburse fund expenses through September 30, 2026 to the extent necessary to maintain the fund’s total annual operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage and interest expenses) at 1.44% for Class B shares. The agreement may only be terminated with the consent of the fund’s Board. Because acquired fund fees and expenses are presented as of the fund’s most recent fiscal year end, individual shareholders may experience total operating expenses higher or lower than this expense cap depending upon when shares are redeemed and the fund’s actual allocations to acquired funds.

| Prospectus May 1, 2026 | 38 | Investing in the Funds |

|

( |

Total

Assets |

− |

Total

Liabilities |

) |

÷ |

Total Number of

Shares Outstanding |

= |

NAV |

|

DWS Alternative Asset Allocation VIP — Class B | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data |

|

|

|

|

|

|

Net asset value, beginning of period |

$12.94 |

$12.72 |

$12.98 |

$15.11 |

$13.68 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.46 |

.46 |

.42 |

.80 |

.93 |

|

Net realized and unrealized gain (loss) |

.80 |

.20 |

.28 |

(1.90

) |

.75 |

|

Total from investment operations |

1.26 |

.66 |

.70 |

(1.10

) |

1.68 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.50

) |

(.43

) |

(.84

) |

(1.02

) |

(.25

) |

|

Net realized gains |

— |

(.01

) |

(.12

) |

(.01

) |

— |

|

Total distributions |

(.50

) |

(.44

) |

(.96

) |

(1.03

) |

(.25

) |

|

Net asset value, end of period |

$13.70 |

$12.94 |

$12.72 |

$12.98 |

$15.11 |

|

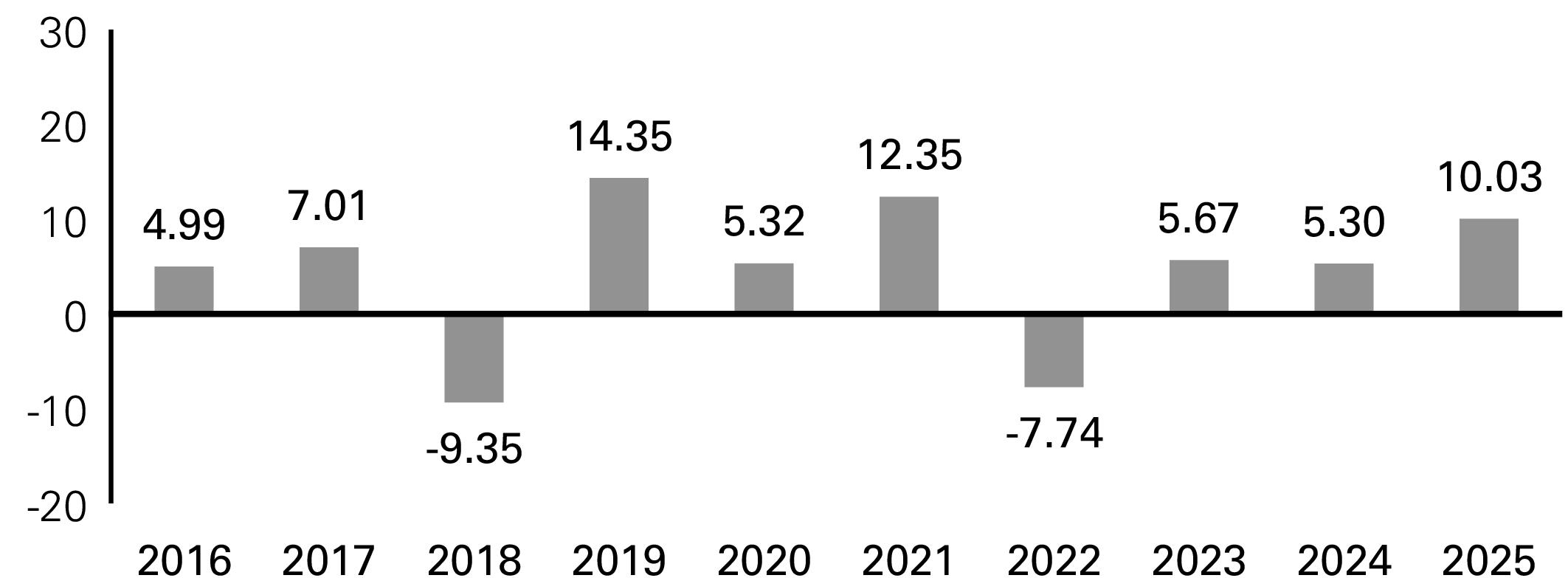

Total Return (%)b |

10.03 |

5.30 |

5.67 |

(7.74

) |

12.35

c |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

349 |

358 |

371 |

376 |

447 |

|

Ratio of expenses before expense reductions (%)d,e |

.62 |

.61 |

.61 |

.61 |

.61 |

|

Ratio of expenses after expense reductions (%)d,e |

.62 |

.61 |

.61 |

.61 |

.60 |

|

Ratio of net investment income (%) |

3.44 |

3.60 |

3.35 |

5.81 |

6.37 |

|

Portfolio turnover rate (%) |

18 |

25 |

0 |

12 |

19 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower if the Advisor had not reduced some Underlying DWS Funds’ expenses. |

|

c |

Total return would have been lower had certain expenses not been reduced. |

|

d |

The Fund invests in other Funds and indirectly bears its proportionate share of fees and expenses incurred by the Underlying Funds in which the

Fund is invested. This ratio does not include these indirect fees and expenses. |

|

e |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 44 | Financial Highlights |

|

DWS Small Mid Cap Value VIP — Class B | |||||

|

|

Years Ended December 31, | ||||

|

|

2025 |

2024 |

2023 |

2022 |

2021 |

|

Selected Per Share Data |

|

|

|

|

|

|

Net asset value, beginning of period |

$13.81 |

$13.86 |

$12.72 |

$15.46 |

$11.99 |

|

Income (loss) from investment operations: |

|

|

|

|

|

|

Net investment incomea |

.03 |

.08 |

.10 |

.10 |

.06 |

|

Net realized and unrealized gain (loss) |

1.95 |

.69 |

1.66 |

(2.58

) |

3.53 |

|

Total from investment operations |

1.98 |

.77 |

1.76 |

(2.48

) |

3.59 |

|

Less distributions from: |

|

|

|

|

|

|

Net investment income |

(.08

) |

(.12

) |

(.11

) |

(.06

) |

(.12

) |

|

Net realized gains |

(1.59

) |

(.70

) |

(.51

) |

(.20

) |

— |

|

Total distributions |

(1.67

) |

(.82

) |

(.62

) |

(.26

) |

(.12

) |

|

Net asset value, end of period |

$14.12 |

$13.81 |

$13.86 |

$12.72 |

$15.46 |

|

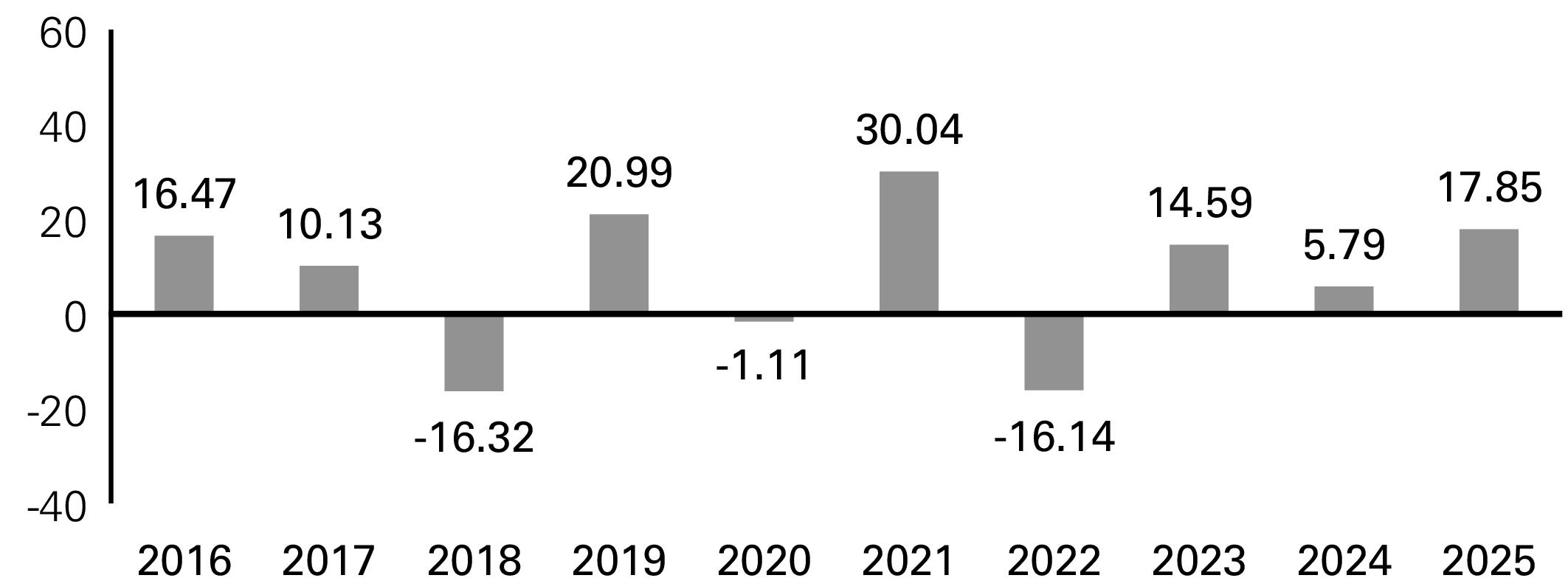

Total Return (%)b |

17.85 |

5.79 |

14.59 |

(16.14

) |

30.04 |

|

Ratios to Average Net Assets and Supplemental Data | |||||

|

Net assets, end of period ($ millions) |

15 |

15 |

17 |

16 |

21 |

|

Ratio of expenses before expense reductions (%)c |

1.24 |

1.24 |

1.24 |

1.24 |

1.22 |

|

Ratio of expenses after expense reductions (%)c |

1.19 |

1.18 |

1.18 |

1.20 |

1.20 |

|

Ratio of net investment income (%) |

.23 |

.61 |

.79 |

.77 |

.40 |

|

Portfolio turnover rate (%) |

53 |

41 |

28 |

33 |

32 |

|

a |

Based on average shares outstanding during the period. |

|

b |

Total return would have been lower had certain expenses not been reduced. |

|

c |

Expense ratio does not reflect charges and fees associated with the separate account that invests in the Fund or any variable life insurance policy or

variable annuity contract for which the Fund is an investment option. |

| Prospectus May 1, 2026 | 45 | Financial Highlights |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

1.31% |

3.69% |

$10,369.00 |

$133.42 |

|

2 |

10.25% |

1.31% |

7.52% |

$10,751.62 |

$138.34 |

|

3 |

15.76% |

1.31% |

11.48% |

$11,148.35 |

$143.44 |

|

4 |

21.55% |

1.31% |

15.60% |

$11,559.72 |

$148.74 |

|

5 |

27.63% |

1.31% |

19.86% |

$11,986.28 |

$154.23 |

|

6 |

34.01% |

1.31% |

24.29% |

$12,428.57 |

$159.92 |

|

7 |

40.71% |

1.31% |

28.87% |

$12,887.19 |

$165.82 |

|

8 |

47.75% |

1.31% |

33.63% |

$13,362.72 |

$171.94 |

|

9 |

55.13% |

1.31% |

38.56% |

$13,855.81 |

$178.28 |

|

10 |

62.89% |

1.31% |

43.67% |

$14,367.09 |

$184.86 |

|

Total |

$1,578.99 | ||||

| Prospectus May 1, 2026 | 46 | Appendix |

|

|

Maximum

Sales Charge:

0.00% |

Initial Hypothetical

Investment:

$10,000 |

Assumed Rate

of Return:

5% | ||

|

Year |

Cumulative

Return Before

Fees &

Expenses |

Annual

Fund

Expense

Ratios |

Cumulative

Return After

Fees &

Expenses |

Hypothetical

Year-End

Balance After

Fees &

Expenses |

Annual Fees

&

Expenses |

|

1 |

5.00% |

1.17% |

3.83% |

$10,383.00 |

$119.24 |

|

2 |

10.25% |

1.24% |

7.73% |

$10,773.40 |

$131.17 |

|

3 |

15.76% |

1.24% |

11.78% |

$11,178.48 |

$136.10 |

|

4 |

21.55% |

1.24% |

15.99% |

$11,598.79 |

$141.22 |

|

5 |

27.63% |

1.24% |

20.35% |

$12,034.91 |

$146.53 |

|

6 |

34.01% |

1.24% |

24.87% |

$12,487.42 |

$152.04 |

|

7 |

40.71% |

1.24% |

29.57% |

$12,956.95 |

$157.76 |

|

8 |

47.75% |

1.24% |

34.44% |

$13,444.13 |

$163.69 |

|

9 |

55.13% |

1.24% |

39.50% |

$13,949.63 |

$169.84 |

|

10 |

62.89% |

1.24% |

44.74% |

$14,474.13 |

$176.23 |

|

Total |

$1,493.82 | ||||

| Prospectus May 1, 2026 | 47 | Appendix |

|

DWS |

222 South Riverside Plaza

Chicago, IL 60606-5808

dws.com |

|

|

(800) 728-3337 |

|

Distributor |

DWS Distributors, Inc.

222 South Riverside Plaza

Chicago, IL 60606-5808

(800) 621-1148 |

|

SEC File Number |

Deutsche DWS Variable Series II

811-05002 |

|

CLASS

A AND CLASS B SHARES |

|

|

875

Third Avenue, New York, New York 10022 |

|

|

DWS Alternative

Asset Allocation VIP (Class A and

Class B)

|

|

DWS International

Opportunities VIP (Class A only) |

|

DWS Global Income

Builder VIP (Class A only) |

|

DWS Government

Money Market VIP (Class A only) |

|

DWS High Income

VIP (Class A only) |

|

DWS CROCI®

U.S. VIP (Class A only) |

|

DWS Small Mid

Cap Growth VIP (Class A only) |

|

DWS Small

Mid Cap Value VIP (Class A and Class

B)

|

|

|

Page |

|

I-1

| |

|

I-1

| |

|

I-1

| |

|

I-2

| |

|

I-3

| |

|

I-3

| |

|

I-3

| |

|

I-3

| |

|

I-6

| |

|

I-6

| |

|

I-6

| |

|

I-7

| |

|

I-14

| |

|

I-17

| |

|

I-19

| |

|

I-26

| |

|

I-31

| |

|

I-32

| |

|

I-36

| |

|

I-41

| |

|

I-43

| |

|

Part

II |

II-1

|

|

Detailed

Part II table of contents precedes page II-1 |

|

|

Board

Member |

DWS

Alternative Asset

Allocation

VIP |

DWS

CROCI®

U.S. VIP |

DWS

Global Income

Builder

VIP |

|

Independent

Board Member: | |||

|

Jennifer

S. Conrad |

None

|

None

|

None

|

|

Mary

Schmid Daugherty |

None

|

None

|

None

|

|

Keith

R. Fox |

None

|

None

|

None

|

|

Chad

D. Perry |

None

|

None

|

None

|

|

Rebecca

W. Rimel |

None

|

None

|

None

|

|

Catherine

Schrand |

None

|

None

|

None

|

|

Board

Member |

DWS

Government

Money

Market VIP |

DWS

High Income VIP |

DWS

International

Opportunities

VIP |

|

Independent

Board Member: | |||

|

Jennifer

S. Conrad |

None

|

None

|

None

|

|

Mary

Schmid Daugherty |

None

|

None

|

None

|

|

Keith

R. Fox |

None

|

None

|

None

|

|

Chad

D. Perry |

None

|

None

|

None

|

|

Rebecca

W. Rimel |

None

|

None

|

None

|

|

Catherine

Schrand |

None

|

None

|

None

|

|

Board

Member |

DWS

Small Mid Cap Growth VIP |

DWS

Small Mid Cap Value VIP |

|

Independent

Board Member: | ||

|

Jennifer

S. Conrad |

None

|

None

|

|

Mary

Schmid Daugherty |

None

|

None

|

|

Keith

R. Fox |

None

|

None

|

|

Chad

D. Perry |

None

|

None

|

|

Rebecca

W. Rimel |

None

|

None

|

|

Catherine

Schrand |

None

|

None

|

|

Board

Member |

Funds

Overseen by

Board

Member in the

DWS

Funds |

|

Independent

Board Member: | |

|

Jennifer

S. Conrad |

Over

$100,000 |

|

Mary

Schmid Daugherty |

Over

$100,000 |

|

Keith

R. Fox |

Over

$100,000 |

|

Chad

D. Perry |

Over

$100,000 |

|

Rebecca

W. Rimel |

Over

$100,000 |

|

Catherine

Schrand |

Over

$100,000 |

|

Independent

Board

Member |

Owner

and

Relationship

to

Board

Member |

Company

|

Title

of

Class

|

Value

of

Securities

on an

Aggregate

Basis |

Percent

of

Class

on an

Aggregate

Basis |

|

Jennifer

S. Conrad |

|

None

|

|

|

|

|

Mary

Schmid Daugherty |

|

None

|

|

|

|

|

Keith

R. Fox |

|

None

|

|

|

|

|

Chad

D. Perry |

|

None

|

|

|

|

|

Rebecca

W. Rimel |

|

None

|

|

|

|

|

Catherine

Schrand |

|

None

|

|

|

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

NYLIAC

ATTN

ASHESH UPADHYAY

30

HUDSON ST

JERSEY

CITY NJ 07302-4804 |

19,876,000.50

|

69.94%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

TRANSAMERICA

LIFE INSURANCE CO

4333

EDGEWOOD RD XX XX XXXX

CEDAR

RAPIDS IA 52499-0001 |

310,245.89

|

27.52%

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

691,261.54

|

61.31%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

ZURICH

AMERICAN LIFE INS CO

ATTN

PRODUCT VALUATION

SECURITY

BENEFIT

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

2,342,618.79

|

46.24%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

ZURICH

AMERICAN LIFE INS CO

ATTN

PRODUCT VALUATION

SECURITY

BENEFIT

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

2,610,614.99

|

36.22%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

FARMERS

VUL

3003

77TH AVE SE

MERCER

ISLAND WA 98040-2837 |

2,494,208.98

|

33.15%%

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

3,364,161.75

|

44.71%%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

1,799,413.00

|

54.36%

|

|

ZURICH

AMERICAN LIFE INSURANCE CO

ATTN

PRODUCT VALUATION

SECURITY

BENEFIT

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

1,239,818.55

|

37.46%

|

|

Name

and Address of Investor |

Shares

|

Percentage

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

1,960,664.84

|

34.54%

|

|

Name

and Address of Investor |

Shares

|

Class

|

Percentage

|

|

LINCOLN

NATIONAL LIFE INSURANCE

VARIABLE

LIFE ACCOUNT M

1300

S CLINTON ST

FORT

WAYNE IN 46802-3506 |

3,249,020.39

|

A

|

72.40%

|

|

NYLIAC

ATTN

ASHESH UPADHYAY

30

HUDSON ST

JERSEY

CITY NJ 07302-4804 |

815,652.76

|

A

|

18.18%

|

|

RIVERSOURCE

LIFE INSURANCE CO

10468

AMERIPRISE FINANCIAL CENTER

MINNEAPOLIS

MN 55474-0001 |

286,569.38

|

A

|

6.39%

|

|

NYLIAC

ATTN

ASHESH UPADHYAY

30

HUDSON ST

JERSEY

CITY NJ 07302-4804 |

19,060,347.75

|

B

|

79.67%

|

|

LINCOLN

NATIONAL LIFE INSURANCE

VARIABLE

LIFE ACCOUNT M

1300

S CLINTON ST

FORT

WAYNE IN 46802-3506 |

2,547,361.95

|

B

|

10.65%

|

|

RIVERSOURCE

LIFE INSURANCE CO

10468

AMERIPRISE FINANCIAL CENTER

MINNEAPOLIS

MN 55474-0001 |

1,828,838.21

|

B

|

7.64%

|

|

Name

and Address of Investor |

Shares

|

Class

|

Percentage

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

691,261.54

|

A

|

61.31%

|

|

TRANSAMERICA

LIFE INSURANCE CO

4333

EDGEWOOD RD XX XX XXXX

CEDAR

RAPIDS IA 52499-0001 |

310,245.89

|

A

|

27.52%

|

|

Name

and Address of Investor |

Shares

|

Class

|

Percentage

|

|

ZURICH

AMERICAN LIFE INS CO

ATTN

PRODUCT VALUATION

SECURITY

BENEFIT

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

2,342,618.79

|

A

|

46.24%

|

|

Name

and Address of Investor |

Shares

|

Class

|

Percentage

|

|

NATIONWIDE

LIFE INSURANCE CO

C/O

IPO PORTFOLIO ACCOUNTING

PO

BOX 182029

COLUMBUS

OH 43218-2029 |

684,618.43

|

A

|

13.51%

|

|

ZALICO

DESTINATIONS FARMERS SVSII

ATTN

INVESTMENT ACCOUNTING XX-XX

150

GREENWICH ST 4WTC 54TH FL

NEW

YORK NY 10007-2798 |

483,908.06

|

A

|

9.55%

|

|

SYMETRA