AS FILED WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION ON APRIL 30, 2026

File No. 033-50718

File No. 811-07102

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

REGISTRATION STATEMENT UNDER THE

SECURITIES ACT OF 1933

| POST-EFFECTIVE AMENDMENT NO. 324 | /X/ |

AND

REGISTRATION STATEMENT UNDER THE

INVESTMENT COMPANY ACT OF 1940

| AMENDMENT NO. 328 | /X/ |

(Exact Name of Registrant as Specified in Charter)

One Freedom Valley Drive

Oaks, Pennsylvania 19456

(Address of Principal Executive Offices, Zip Code)

1-800-932-7781

(Registrant’s Telephone Number)

Michael Beattie

c/o SEI Investments

One Freedom Valley Drive

Oaks, Pennsylvania 19456

(Name and Address of Agent for Service)

Copies to:

| David W. Freese |

| Morgan, Lewis & Bockius LLP |

| 2222 Market Street |

| Philadelphia, Pennsylvania 19103 |

| John J. O’Brien |

| Morgan, Lewis & Bockius LLP |

| 2222 Market Street |

| Philadelphia, Pennsylvania 19103 |

It is proposed that this filing become effective (check appropriate box)

| / X / Immediately upon filing pursuant to paragraph (b) |

| / / On [date] pursuant to paragraph (b) |

| / / 60 days after filing pursuant to paragraph (a)(1) |

| / / 75 days after filing pursuant to paragraph (a)(2) |

| / / On [date] pursuant to paragraph (a) of Rule 485 |

About This Prospectus

This prospectus has been arranged into different sections so that you can easily review this important information. For detailed information about the Funds, please see:

Page |

||

More Information about the Funds’ Investment Objectives and Strategies |

||

Advisor Shares of the Champlain Strategic Focus Fund are currently not available for purchase.

The Champlain Small Company Fund (the “Small Company Fund” or the “Fund”) seeks capital appreciation.

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may be required to pay commissions and/or other forms of compensation to a broker for transactions in Institutional Shares, which are not reflected in the table or the example below.

Advisor Shares |

Institutional Shares |

|

Management Fees |

||

Distribution (12b-1) Fees |

||

Other Expenses |

||

Total Annual Fund Operating Expenses1 |

|

1 |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 Year |

3 Years |

5 Years |

10 Years |

|

Advisor Shares |

$ |

$ |

$ |

$ |

Institutional Shares |

$ |

$ |

$ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in total annual fund operating expenses or in the example, affect the Fund’s performance. During its most recent fiscal year, the Fund’s portfolio turnover rate was

1 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Under normal circumstances, the Fund invests at least 80% of its net assets, plus any borrowings for investment purposes, in securities of small companies. For purposes of this policy, a small company is a company that, at the time of initial purchase, is included in either the S&P SmallCap 600 or the Russell 2000 Index, or that has a market capitalization that falls within the range of the Russell 2000 Index as measured as of the index’s most recent annual reconstitution. The Fund seeks capital appreciation by investing mainly in common stocks of small companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a diversified portfolio of small companies which trade at a discount to their estimated intrinsic, or fair values. The Adviser seeks to mitigate company specific risk by limiting position sizes to 5% of the Fund’s total assets at market value. The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or when new information or fresh perspective about a security invalidates the Adviser’s original thesis for making the investment. Additionally, the Adviser may also sell securities in order to maintain the 5% limit on position sizes or when exposure to a sector exceeds the Adviser’s sector weight rules, which require that each of the five major sectors (healthcare, consumer, technology, industrial and financial) represent (i) no more than the greater of 25% of the Fund’s total assets or 125% of the sector’s weighting in the S&P SmallCap 600 Index; and (ii) no less than 75% of the sector’s weighting in the S&P SmallCap 600 Index. The Fund is broadly diversified and seeks to create value primarily through favorable stock selection.

Principal Risks of Investing in the Fund

As with all mutual funds, there is no guarantee that the Fund will achieve its investment objective.

Market Risk – The prices of and the income generated by the Fund’s securities may decline in response to, among other things, investor sentiment, general economic and market conditions, regional or global instability, and currency and interest rate fluctuations. A variety of factors can lead to volatility in local, regional, or global markets, including regulatory events, inflation, interest rates, government defaults, government shutdowns, war, regional conflicts, acts of terrorism, social unrest, the imposition of tariffs, trade disputes, and substantial economic downturn. In addition, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on your investment in the Fund.

Small-Capitalization Company Risk – The Fund is also subject to the risk that small-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. The small-capitalization companies that the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these small-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, small-cap stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

Active Management Risk – The Fund is subject to the risk that the Adviser’s judgments about the attractiveness, value, or potential appreciation of the Fund’s investments may prove to be incorrect. If the investments selected and strategies employed by the Fund fail to produce the intended results, the Fund could underperform in comparison to other funds with similar objectives and investment strategies.

Equity Risk – Since it purchases equity securities, the Fund is subject to the risk that stock prices will fall over short or extended periods of time. Historically, the equity markets have moved in cycles, and the value of the Fund’s equity securities may fluctuate drastically from day to day. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments. The prices of securities issued by such companies may suffer a decline in response. These factors contribute to price volatility, which is a principal risk of investing in the Fund.

2 |

CHAMPLAIN INVESTMENT |

PARTNERS |

|

|

|

( |

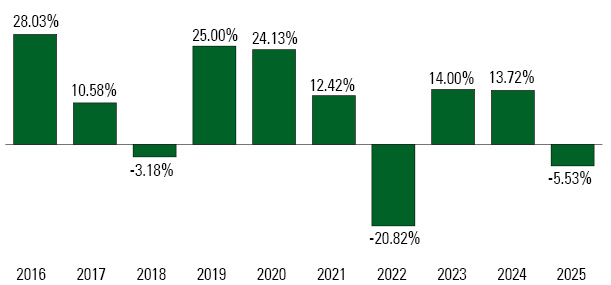

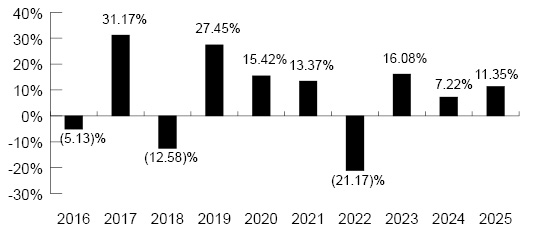

The performance information shown above is based on a calendar year.

This table compares the Fund’s average annual total returns for the periods ended December 31, 2025 to those of an appropriate broad-based index and a more narrowly based index with characteristics relevant to the Fund’s investment strategies.

1 Year |

5 Years |

10 Years |

Since |

|

Fund Returns Before Taxes |

||||

Advisor Shares |

( |

|||

Institutional Shares |

( |

|||

Fund Returns After Taxes on Distributions |

||||

Advisor Shares |

( |

( |

3 |

CHAMPLAIN INVESTMENT |

PARTNERS |

1 Year |

5 Years |

10 Years |

Since |

|

Fund Returns After Taxes on Distributions and Sale of Fund Shares |

||||

Advisor Shares |

( |

|||

Russell 3000 Index (reflects no deduction for fees, expenses or taxes) |

||||

Russell 2000 Index (reflects no deduction for fees, expenses or taxes) |

Investment Adviser

Champlain Investment Partners, LLC

Portfolio Managers

Portfolio Manager |

Position with the Adviser |

Years of Experience with the Fund |

Scott T. Brayman |

Chief Investment Officer/Managing Partner |

Since Inception (2004) |

Joseph M. Caligiuri |

Deputy Chief Investment Officer/Partner |

Since 2010 |

Rachel C. Drakon |

Member of the Investment Team |

Since 2020 |

Ethan C. Ellison |

Member of the Investment Team/Principal |

Since 2020 |

Joseph J. Farley |

Member of the Investment Team/Partner |

Since 2014 |

Robert D. Hallisey |

Member of the Investment Team/Partner |

Since 2016 |

James A. Mallon |

Trader/Principal |

Since 2023 |

Finn R. McCoy |

Head Trader/Partner |

Since 2008 |

Henry C. Sinkula |

Member of the Investment Team/Partner |

Since 2022 |

Jacqueline W. Williams |

Member of the Investment Team/Partner |

Since 2019 |

Courtney A. Flyer |

Member of the Investment Team/Principal |

Since 2018 |

For important information about the purchase and sale of Fund shares, taxes and financial intermediary compensation, please turn to “Summary Information about Purchasing and Selling Fund Shares, Taxes and Financial Intermediary Compensation” on page 14 of the prospectus.

4 |

CHAMPLAIN INVESTMENT |

PARTNERS |

The Champlain Mid Cap Fund (the “Mid Cap Fund” or the “Fund”) seeks capital appreciation.

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may be required to pay commissions and/or other forms of compensation to a broker for transactions in Institutional Shares, which are not reflected in the table or the example below.

Advisor Shares |

Institutional Shares |

|

Management Fees |

||

Distribution (12b-1) Fees |

||

Other Expenses |

||

Total Annual Fund Operating Expenses1 |

|

1 |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 Year |

3 Years |

5 Years |

10 Years |

|

Advisor Shares |

$ |

$ |

$ |

$ |

Institutional Shares |

$ |

$ |

$ |

$ |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in total annual fund operating expenses or in the example, affect the Fund’s performance. During its most recent fiscal year, the Fund’s portfolio turnover rate was

5 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Under normal circumstances, the Fund invests at least 80% of its net assets, plus any borrowings for investment purposes, in securities of medium-sized companies. For purposes of this policy, a medium-sized company is a company that, at the time of initial purchase, is included in either the S&P MidCap 400 or the Russell Midcap Index, or that has a market capitalization that falls within the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution. The Fund seeks capital appreciation by investing mainly in common stocks of medium-sized companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a diversified portfolio of medium-sized companies that trade at a discount to their estimated intrinsic, or fair values. The Adviser seeks, under normal circumstances, to mitigate company-specific risk by limiting position sizes to 5% of the Fund’s total assets at market value. The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or when new information or fresh perspective about a security invalidates the Adviser’s original thesis for making the investment. The Adviser may also sell securities in order to maintain the 5% limit on position sizes or when exposure to a sector exceeds the Adviser’s sector weight rules, which require that each of the five major sectors (healthcare, consumer, technology, industrial and financial) represent no more than 25% of the Fund’s total assets. The Fund is broadly diversified and the Adviser seeks to create value primarily through favorable stock selection.

Principal Risks of Investing in the Fund

As with all mutual funds, there is no guarantee that the Fund will achieve its investment objective.

Market Risk – The prices of and the income generated by the Fund’s securities may decline in response to, among other things, investor sentiment, general economic and market conditions, regional or global instability, and currency and interest rate fluctuations. A variety of factors can lead to volatility in local, regional, or global markets, including regulatory events, inflation, interest rates, government defaults, government shutdowns, war, regional conflicts, acts of terrorism, social unrest, the imposition of tariffs, trade disputes, and substantial economic downturn. In addition, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on your investment in the Fund.

Mid-Capitalization Company Risk – The Fund is also subject to the risk that medium-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. The medium-sized companies the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these medium-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, mid-capitalization stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

Active Management Risk – The Fund is subject to the risk that the Adviser’s judgments about the attractiveness, value, or potential appreciation of the Fund’s investments may prove to be incorrect. If the investments selected and strategies employed by the Fund fail to produce the intended results, the Fund could underperform in comparison to other funds with similar objectives and investment strategies.

Equity Risk – Since it purchases equity securities, the Fund is subject to the risk that stock prices will fall over short or extended periods of time. Historically, the equity markets have moved in cycles, and the value of the Fund’s equity securities may fluctuate drastically from day to day. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments. The prices of securities issued by such companies may suffer a decline in response. These factors contribute to price volatility, which is a principal risk of investing in the Fund.

6 |

CHAMPLAIN INVESTMENT |

PARTNERS |

|

|

|

( |

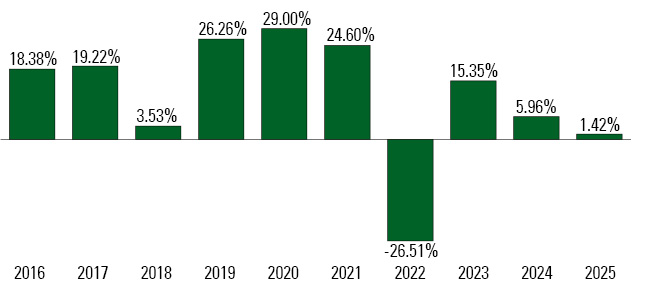

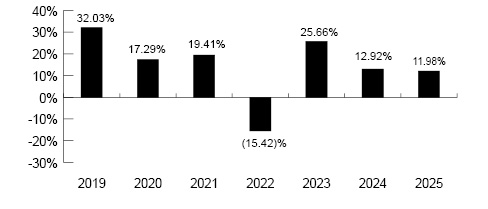

The performance information shown above is based on a calendar year.

This table compares the Fund’s average annual total returns for the periods ended December 31, 2025 to those of an appropriate broad-based index and a more narrowly based index with characteristics relevant to the Fund’s investment strategies.

1 Year |

5 Years |

10 Years |

Since |

|

Fund Returns Before Taxes |

||||

Advisor Shares1 |

||||

Institutional Shares2 |

||||

Fund Returns After Taxes on Distributions |

||||

Advisor Shares |

( |

|||

Fund Returns After Taxes on Distributions and Sale of Fund Shares |

||||

Advisor Shares |

||||

Russell 3000 Index (reflects no deduction for fees, expenses or taxes) |

||||

Russell Midcap Index (reflects no deduction for fees, expenses or taxes)3 |

|

1 |

|

|

2 |

|

3 |

7 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Investment Adviser

Champlain Investment Partners, LLC

Portfolio Managers

Portfolio Manager |

Position with the Adviser |

Years of Experience with the Fund |

Scott T. Brayman |

Chief Investment Officer/Managing Partner |

Since Inception (2008) |

Joseph M. Caligiuri |

Deputy Chief Investment Officer/Partner |

Since 2010 |

Rachel C. Drakon |

Member of the Investment Team |

Since 2020 |

Ethan C. Ellison |

Member of the Investment Team/Principal |

Since 2020 |

Joseph J. Farley |

Member of the Investment Team/Partner |

Since 2014 |

Robert D. Hallisey |

Member of the Investment Team/Partner |

Since 2016 |

James A. Mallon |

Trader/Principal |

Since 2023 |

Finn R. McCoy |

Head Trader/Partner |

Since Inception (2008) |

Henry C. Sinkula |

Member of the Investment Team/Partner |

Since 2022 |

Jacqueline W. Williams |

Member of the Investment Team/Partner |

Since 2019 |

Courtney A. Flyer |

Member of the Investment Team/Principal |

Since 2018 |

For important information about the purchase and sale of Fund shares, taxes and financial intermediary compensation, please turn to “Summary Information about Purchasing and Selling Fund Shares, Taxes and Financial Intermediary Compensation” on page 14 of the prospectus.

8 |

CHAMPLAIN INVESTMENT |

PARTNERS |

The Champlain Strategic Focus Fund (the “Fund”) seeks capital appreciation.

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may be required to pay commissions and/or other forms of compensation to a broker for transactions in Institutional Shares, which are not reflected in the table or the example below.

Advisor Shares |

Institutional Shares |

|

Management Fees |

||

Distribution (12b-1) Fees |

||

Other Expenses |

||

Total Annual Fund Operating Expenses |

||

Less Fee Reductions and/or Expense Reimbursements1 |

( |

( |

Total Annual Fund Operating Expenses After Fee Reductions and/or Expense Reimbursements |

|

1 |

|

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses (including one year of capped expenses in each period) remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 Year |

3 Years |

5 Years |

10 Years |

|

Advisor Shares |

$ |

$ |

$ |

$ |

Institutional Shares |

$ |

$ |

$ |

$ |

9 |

CHAMPLAIN INVESTMENT |

PARTNERS |

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in total annual fund operating expenses or in the example, affect the Fund’s performance. For the fiscal year ended December 31, 2025, the Fund’s portfolio turnover rate was

The Fund invests primarily in securities of medium- to large-sized companies. For purposes of this strategy, a medium-sized company is a company that, at the time of initial purchase, is included in either the S&P MidCap 400 or the Russell Midcap Index, or that has a market capitalization that falls within the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution, while a large-sized company would be any whose market capitalization falls above the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution. The Fund may also invest in securities of small-sized companies, which the Adviser considers to be a company that, at the time of initial purchase, is included in either the S&P SmallCap 600 or the Russell 2000 Index, or that has a market capitalization that falls within the range of the Russell 2000 Index as measured as of the index’s most recent annual reconstitution.

The Fund seeks capital appreciation by investing mainly in common stocks of companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. The Adviser’s stock selection process seeks to manage business model and valuation risk and includes three analytical steps: sector factors (making qualitative judgments targeting attractive business models), company attributes (analyzing business model, competitive landscape and management) and valuation analysis (employing a multi-faceted approach including discounted cash flow analysis). The Adviser seeks, under normal circumstances, to mitigate company-specific risk by limiting position sizes. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a portfolio of fifteen (15) to thirty (30) mid- to large-sized companies that trade at a discount to their estimated intrinsic, or fair values. The Fund may pursue a “growth style” of investing, meaning that the Fund may invest in equity securities of companies that the Adviser believes will increase their earnings at a certain rate that is generally higher than the rate expected for non-growth companies.

The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or based on new information or analyses about a security. The Adviser may also sell securities in order to limit position sizes or to reduce sector exposure.

The Fund is classified as “non-diversified,” which means that it may invest a larger percentage of its assets in a smaller number of issuers than a diversified fund.

Principal Risks of Investing in the Fund

As with all mutual funds, there is no guarantee that the Fund will achieve its investment objective.

Market Risk – The prices of and the income generated by the Fund’s securities may decline in response to, among other things, investor sentiment, general economic and market conditions, regional or global instability, and currency and interest rate fluctuations. A variety of factors can lead to volatility in local, regional, or global markets, including regulatory events, inflation, interest rates, government defaults, government shutdowns, war, regional conflicts, acts of terrorism, social unrest, the imposition of tariffs, trade disputes, and substantial economic downturn. In addition, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on your investment in the Fund.

Mid-Capitalization Company Risk – The Fund is also subject to the risk that medium-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. The medium-sized companies the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these medium-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, mid-capitalization stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

10 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Large-Capitalization Company Risk – The large-capitalization companies in which the Fund invests may not respond as quickly as smaller companies to competitive challenges, the growth rates of investments in these large-sized companies may lag the growth rates of well-managed smaller companies during strong economic periods.

Active Management Risk – The Fund is subject to the risk that the Adviser’s judgments about the attractiveness, value, or potential appreciation of the Fund’s investments may prove to be incorrect. If the investments selected and strategies employed by the Fund fail to produce the intended results, the Fund could underperform in comparison to other funds with similar objectives and investment strategies.

Equity Risk – Since it purchases equity securities, the Fund is subject to the risk that stock prices will fall over short or extended periods of time. Historically, the equity markets have moved in cycles, and the value of the Fund’s equity securities may fluctuate drastically from day to day. Individual companies may report poor results or be negatively affected by industry and/or economic trends and developments. The prices of securities issued by such companies may suffer a decline in response. These factors contribute to price volatility, which is a principal risk of investing in the Fund.

Growth Investment Style Risk – An investment in growth stocks may be susceptible to rapid price swings, especially during periods of economic uncertainty. Growth stocks typically have little or no dividend income to cushion the effect of adverse market conditions. In addition, growth stocks may be particularly volatile in the event of earnings disappointments or other financial difficulties experienced by the issuer.

Small-Capitalization Company Risk – The Fund is also subject to the risk that small-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. The small capitalization companies that the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these small-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, small-cap stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

Advisor Shares had not commenced operations as of the date of this prospectus. Therefore, performance information for Advisor Shares is not presented. Advisor Shares would have substantially similar performance as Institutional Shares because the shares are invested in the same portfolio of securities and the returns would generally differ only to the extent that expenses of Advisor Shares are higher than the expenses of Institutional Shares, in which case the returns for Advisor Shares would be lower than those of Institutional Shares.

11 |

CHAMPLAIN INVESTMENT |

PARTNERS |

|

|

|

( |

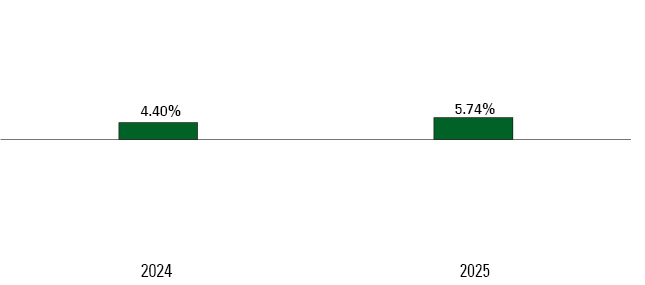

The performance information shown above is based on a calendar year.

This table compares the Fund’s average annual total returns for the periods ended December 31, 2025 to those of an appropriate broad-based index and a more narrowly based index with characteristics relevant to the Fund’s investment strategies.

1 Year |

Since |

|

Fund Returns Before Taxes |

||

Institutional Shares1 |

||

Fund Returns After Taxes on Distributions |

||

Institutional Shares |

||

Fund Returns After Taxes on Distributions and Sale of Fund Shares |

||

Institutional Shares |

||

Russell 3000 Index (reflects no deduction for fees, expenses or taxes) |

||

Russell Midcap Growth Index (reflects no deduction for fees, expenses or taxes) |

|

1 |

|

12 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Investment Adviser

Champlain Investment Partners, LLC

Portfolio Managers

Portfolio Manager |

Position with the Adviser |

Years of Experience with the Fund |

Scott T. Brayman |

Chief Investment Officer/Managing Partner |

Since Inception (2023) |

Joseph M. Caligiuri |

Deputy Chief Investment Officer/Partner |

Since Inception (2023) |

Rachel C. Drakon |

Member of the Investment Team |

Since Inception (2023) |

Ethan C. Ellison |

Member of the Investment Team/Principal |

Since Inception (2023) |

Joseph J. Farley |

Member of the Investment Team/Partner |

Since Inception (2023) |

Robert D. Hallisey |

Member of the Investment Team/Partner |

Since Inception (2023) |

James A. Mallon |

Trader/Principal |

Since Inception (2023) |

Finn R. McCoy |

Head Trader/Partner |

Since Inception (2023) |

Henry C. Sinkula |

Member of the Investment Team/Partner |

Since Inception (2023) |

Jacqueline W. Williams |

Member of the Investment Team/Partner |

Since Inception (2023) |

Courtney A. Flyer |

Member of the Investment Team/Principal |

Since Inception (2023) |

For important information about the purchase and sale of Fund shares, taxes and financial intermediary compensation, please turn to “Summary Information about Purchasing and Selling Fund Shares, Taxes and Financial Intermediary Compensation” on page 14 of the prospectus.

13 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Summary Information about Purchasing and Selling Fund Shares, Taxes and Financial Intermediary Compensation

Purchase and Sale of Fund Shares

To purchase Advisor Shares of the Funds for the first time, you must invest at least $10,000 ($3,000 for IRAs). To purchase Institutional Shares of the Funds for the first time, you must invest at least $1,000,000. There is no minimum for subsequent investments. The Funds may accept investments of smaller amounts in their sole discretion.

If you own your shares directly, you may redeem your shares on any day that the New York Stock Exchange (the “NYSE”) is open for business (a “Business Day”) by contacting the Funds directly by mail at: Champlain Funds, P.O. Box 219009, Kansas City, Missouri 64121-9009 (Express Mail Address: Champlain Funds, c/o SS&C Global Investor & Distribution Solutions, Inc., 801 Pennsylvania Avenue, Suite 219009, Kansas City, Missouri 64105-1307) or telephone at 1.866.773.3238.

If you own your shares through an account with a broker or other institution, contact that broker or other institution to redeem your shares. Your broker or financial intermediary may charge a fee for its services in addition to the fees charged by the Funds.

Advisor Shares of the Champlain Strategic Focus Fund are currently not available for purchase.

Tax Information

The Funds intend to make distributions that may be taxed as ordinary income, qualified dividend income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or IRA, in which case your distribution will be taxed when withdrawn from the tax-deferred account.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Funds through a broker-dealer or other financial intermediary (such as a bank), each Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend a Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

14 |

CHAMPLAIN INVESTMENT |

PARTNERS |

More Information about Risk

Investing in each Fund involves risk and there is no guarantee that a Fund will achieve its goal. The Adviser’s judgments about the markets, the economy, or companies may not anticipate actual market movements, economic conditions or company performance, and these judgments may affect the return on your investment. In fact, no matter how good of a job the Adviser does, you could lose money on your investment in a Fund, just as you could with similar investments.

The value of your investment in a Fund is based on the value of the securities the Fund holds. These prices change daily due to economic and other events that affect particular companies and other issuers. These price movements, sometimes called volatility, may be greater or lesser depending on the types of securities a Fund owns and the markets in which they trade. The effect on a Fund of a change in the value of a single security will depend on how widely the Fund diversifies its holdings.

Active Management Risk (All Funds) – Each Fund is subject to the risk that the Adviser’s judgments about the attractiveness, value, or potential appreciation of the Fund’s investments may prove to be incorrect. If the investments selected and strategies employed by a Fund fail to produce the intended results, the Fund could underperform in comparison to other funds with similar objectives and investment strategies.

Equity Risk (All Funds) – Equity securities in which the Funds invest include common stock, preferred stock, convertible debt, warrants and rights, shares of American Depositary Receipts (“ADRs”), and exchange traded funds (“ETFs”) that attempt to track the price movement of equity indices. Common stock represents an equity or ownership interest in an issuer. Preferred stock provides a fixed dividend that is paid before any dividends are paid to common stockholders, and which takes precedence over common stock in the event of a liquidation. Like common stock, preferred stocks represent partial ownership in a company, although preferred stock shareholders do not enjoy all of the voting rights of common stockholders. Also, unlike common stock, a preferred stock pays a fixed dividend that does not fluctuate, although the company does not have to pay this dividend if it lacks the financial ability to do so. Investments in equity securities in general are subject to market risks that may cause their prices to fluctuate over time. The value of securities convertible into equity securities, such as warrants or convertible debt, is also affected by prevailing interest rates, the credit quality of the issuer and any call provision. In addition, the impact of any epidemic, pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other instruments in which a Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on your investment in the Fund. Recent examples of events that have led to fluctuations in the equity market include pandemic risks related to COVID-19 and aggressive measures taken worldwide in response by governments and businesses, elevated inflation levels, problems in the banking sector and wars in Europe and in the Middle East. Fluctuations in the value of equity securities in which a mutual fund invests will cause a fund’s net asset value (“NAV”) to fluctuate. An investment in a portfolio of equity securities may be more suitable for long-term investors who can bear the risk of these share price fluctuations.

Growth Investment Style Risk (Strategic Focus Fund) – The Strategic Focus Fund invests in equity securities of companies that the Adviser believes will increase their earnings at a certain rate that is generally higher than the rate expected for non-growth companies. If a growth company does not meet these expectations, the price of its stock may decline significantly, even if it has increased earnings. Many growth companies do not pay dividends. Companies that pay dividends often have lower stock price declines during market downturns. Over time, a growth investing style may go in and out of favor, causing the Fund to sometimes underperform other equity funds that use differing investing styles.

Large-Capitalization Company Risk (Strategic Focus Fund) – The large-capitalization companies in which the Strategic Focus Fund may invest may lag the performance of smaller capitalization companies because investments in these large-sized companies may experience slower rates of growth than smaller capitalization companies and may not respond as quickly to market changes and opportunities.

Mid-Capitalization Company Risk (Mid Cap Fund and Strategic Focus Fund) – The mid-capitalization companies in which the Mid Cap Fund or Strategic Focus Fund may invest may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these mid-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, mid-cap stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

15 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Non-Diversification Risk (Strategic Focus Fund) – The Strategic Focus Fund is non-diversified, which means that it may invest in the securities of relatively few issuers. As a result, the Fund may be more susceptible to a single adverse economic or political occurrence affecting one or more of these issuers and may experience increased volatility due to its investments in those securities.

Small-Capitalization Company Risk (Small Company Fund and Strategic Focus Fund) – The Small Company Fund and Strategic Focus Fund are also subject to the risk that small-capitalization stocks may underperform other segments of the equity market or the equity market as a whole. The small-capitalization companies that a Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in these small-sized companies may pose additional risks, including liquidity risk, because these companies tend to have limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, small-cap stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed on an exchange.

More Information about the Funds’ Investment Objectives and Strategies

Investment Objectives

The investment objective of each Fund is to seek capital appreciation. The investment objective of each Fund is a fundamental policy and may not be changed by the Board without shareholder approval.

Investment Strategies

Champlain Small Company Fund

Under normal circumstances, the Small Company Fund invests at least 80% of its net assets, plus any borrowings for investment purposes, in securities of small companies. For purposes of this policy, a small company is a company that, at the time of initial purchase, is included in either the S&P SmallCap 600 or the Russell 2000 Index, or that has a market capitalization that falls within the range of the Russell 2000 Index as measured as of the index’s most recent annual reconstitution. The Small Company Fund seeks capital appreciation by investing mainly in common stocks of small companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a diversified portfolio of small companies which trade at a discount to their estimated intrinsic, or fair values.

The Adviser seeks to mitigate company specific risk by limiting position sizes to 5% of the Small Company Fund’s total assets at market value. The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or when new information or fresh perspective about a security invalidates the Adviser’s original thesis for making the investment. Additionally, the Adviser may also sell securities in order to maintain the 5% limit on position sizes or when exposure to a sector exceeds the Adviser’s sector weight rules, which require that each of the five major sectors (healthcare, consumer, technology, industrial and financial) represent (i) no more than the greater of 25% of the Fund’s total assets or 125% of the sector’s weighting in the S&P SmallCap 600 Index; and (ii) no less than 75% of the sector’s weighting in the S&P SmallCap 600 Index. The Small Company Fund is broadly diversified and seeks to create value primarily through favorable stock selection.

Champlain Mid Cap Fund

Under normal circumstances, the Mid Cap Fund invests at least 80% of its net assets, plus any borrowings for investment purposes, in securities of medium-sized companies. For purposes of this policy, a medium-sized company is a company that, at the time of initial purchase, is included in either the S&P MidCap 400 or the Russell Midcap Index, or that has a market capitalization that falls within the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution. The Mid Cap Fund seeks capital appreciation by investing mainly in common stocks of medium-sized companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a diversified portfolio of medium-sized companies that trade at a discount to their estimated intrinsic, or fair values.

The Adviser seeks, under normal circumstances, to mitigate company-specific risk by limiting position sizes to 5% of the Mid Cap Fund’s total assets at market value. The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or when new information or fresh perspective about a security invalidates the Adviser’s original thesis for making the investment. The Adviser may also sell securities in order to maintain the 5% limit on position sizes or when exposure to a sector exceeds the Adviser’s sector weight

16 |

CHAMPLAIN INVESTMENT |

PARTNERS |

rules, which require that each of the five major sectors (healthcare, consumer, technology, industrial and financial) represent no more than 25% of the Mid Cap Fund’s total assets. The Mid Cap Fund is broadly diversified and the Adviser seeks to create value primarily through favorable stock selection.

Champlain Strategic Focus Fund

The Strategic Focus Fund invests primarily in securities of medium- to large-sized companies. For purposes of this strategy, a medium-sized company is a company that, at the time of initial purchase, is included in either the S&P MidCap 400 or the Russell Midcap Index, or that has a market capitalization that falls within the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution, while a large-sized company would be any whose market capitalization falls above the range of the Russell Midcap Index as measured as of the index’s most recent annual reconstitution. The Strategic Focus Fund may also invest in securities of small-sized companies, which the Adviser considers to be a company that, at the time of initial purchase, is included in either the S&P SmallCap 600 or the Russell 2000 Index, or that has a market capitalization that falls within the range of the Russell 2000 Index as measured as of the index’s most recent annual reconstitution.

The Strategic Focus Fund seeks capital appreciation by investing mainly in common stocks of companies that the Adviser believes have strong long-term fundamentals, superior capital appreciation potential and attractive valuations. The Adviser seeks to manage business model and valuation risk by utilizing a three-step stock selection process. The first step is sector factors, a set of qualitative judgments that target the most attractive business models. There are specific factors for each of the five major sectors: consumer, financials, health care, industrials, and technology. For example, in the consumer sector, the Adviser focuses on brands and avoids fashion risk. The next step of the process targets specific company attributes, including high or excess returns on capital, strong balance sheets, capable and sincere management, high-quality earnings (e.g., strong operating cash flow), superior growth relative to other companies in the sector and a predictable business model. The third and final step of the process is valuation analysis to determine the Adviser’s estimate of fair value, namely the estimate of the present value of future cash flows. The Adviser’s sector analysts employ a proprietary discounted cash flow model that expresses the analyst’s assessment of a company’s fundamentals. The model is designed to incorporate any material considerations in a company’s business landscape and is then used to calibrate the company’s risk profile against a risk-free rate-of-return that typically remains relatively static.

The Adviser seeks, under normal circumstances, to mitigate company-specific risk by limiting position sizes. Through the consistent execution of a fundamental bottom-up investment process, which focuses on an analysis of individual companies, the Adviser expects to identify a portfolio of fifteen (15) to thirty (30) mid- to large-sized companies that trade at a discount to their estimated intrinsic, or fair values. The Strategic Focus Fund may pursue a “growth style” of investing, meaning that the Strategic Focus Fund may invest in equity securities of companies that the Adviser believes will increase their earnings at a certain rate that is generally higher than the rate expected for non-growth companies.

The Adviser may sell a security when it reaches the Adviser’s estimate of its fair value or based on new information or analyses about a security. The Adviser may also sell securities in order to limit position sizes or to reduce sector exposure. The Adviser conducts diligence and monitoring of the Strategic Focus Fund and portfolio investments on an initial and ongoing basis, including the Strategic Focus Fund’s compliance with applicable legal and regulatory requirements. In this regard, the Adviser leverages its trade order management system for both pre- and post-trade monitoring of portfolio investment guidelines and restrictions, as well as for compliance with other applicable legal and regulatory requirements. Compliance personnel also perform periodic reviews and communicate with Fund portfolio managers as appropriate.

The Strategic Focus Fund is classified as “non-diversified,” which means that it may invest a larger percentage of its assets in a smaller number of issuers than a diversified fund.

All Funds

The investments and strategies described in this prospectus are those that the Funds use under normal conditions. For temporary defensive or liquidity purposes, each Fund may invest up to 100% of its assets in money market instruments or other cash equivalents that would not ordinarily be consistent with its investment objective. If a Fund invests in this manner, it may not achieve its investment objective. A Fund will do so only if the Adviser believes that the risk of loss outweighs the opportunity to pursue its investment objective.

This prospectus describes the Funds’ principal investment strategies, and the Funds will normally invest in the types of securities described in this prospectus. In addition to the securities and other investments and strategies described in this prospectus, each Fund also may invest, to a lesser extent, in other securities, use other strategies and engage in other investment practices that are not part

17 |

CHAMPLAIN INVESTMENT |

PARTNERS |

of its principal investment strategies. These investments and strategies are described in detail in the Funds’ Statement of Additional Information (“SAI”) (for information on how to obtain a copy of the SAI see the back cover of this prospectus). Of course, there is no guarantee that a Fund will achieve its investment goal.

Information about Portfolio Holdings

A description of the Funds’ policy and procedures with respect to the circumstances under which the Funds disclose their portfolio securities is available in the SAI. Certain portfolio holdings information for the Funds is available on the Funds’ website – www.cipvt.com – by clicking the “Investments” link on the homepage followed by the “Mutual Fund” link under the appropriate strategy, followed by the “Fund Fact Sheet” link on the right side of the screen. By clicking these links, you can obtain a list of each Fund’s top 10 portfolio holdings as of the end of the most recent month-end. The portfolio holdings information available on the Funds’ website includes a top 10 list of the securities owned by each Fund and the percentage of each Fund’s overall portfolio represented by each listed security. In addition, the website includes a list of the sectors represented in each Fund’s portfolio. The portfolio holdings information on the Funds’ website is generally made available 10 to 12 business days following the close of the most recently completed month-end and will remain available until such information is included in a filing with the SEC. The Adviser may exclude any portion of the Funds’ portfolio holdings from such publication when deemed in the best interest of the Funds.

Investment Adviser

Champlain Investment Partners, LLC makes investment decisions for the Funds and continuously reviews, supervises and administers each Fund’s investment program. The Board oversees the Adviser and establishes policies that the Adviser must follow in its management activities. The Adviser is a Delaware limited liability company formed in 2004 that is independent and employee-owned and offers investment management services for institutions and retail clients. The Adviser’s principal place of business is located at 180 Battery Street, Suite 400, Burlington, Vermont 05401. As of March 31, 2026, the Adviser had approximately $8.23 billion in assets under management.

For its services, the Adviser is entitled to a fee, which is calculated daily and paid monthly, at the following annual rates based on the average daily net assets of each Fund:

Fund |

Advisory Fee |

Champlain Small Company Fund |

0.90% on the first $250 million in assets; 0.80% on assets over $250 million |

Champlain Mid Cap Fund |

0.80% on the first $250 million in assets; 0.70% on assets over $250 million |

Champlain Strategic Focus Fund |

0.80% on the first $250 million in assets; 0.70% on assets over $250 million |

The Adviser has contractually agreed to waive fees and reimburse expenses to the extent necessary in order to keep total annual Fund operating expenses (excluding interest, taxes, brokerage commissions, acquired fund fees and expenses, other expenditures which are capitalized in accordance with generally accepted accounting principles, and non-routine expenses (collectively, “excluded expenses”)) from exceeding the amounts listed in the table below, as a percentage of average daily net assets of the separate share classes of each Fund, until April 30, 2027.

Champlain Small Company Fund |

|

Advisor Shares |

1.30% |

Institutional Shares |

1.05% |

Champlain Mid Cap Fund |

|

Advisor Shares |

1.20% |

Institutional Shares |

0.95% |

Champlain Strategic Focus Fund |

|

Advisor Shares |

1.10% |

Institutional Shares |

0.85% |

18 |

CHAMPLAIN INVESTMENT |

PARTNERS |

In addition, the Adviser may receive from the Fund the difference between the total annual Fund operating expenses (not including excluded expenses) and the expense cap to recoup all or a portion of its prior fee waivers or expense reimbursements made during the three-year period preceding the recoupment if at any point total annual Fund operating expenses (not including excluded expenses) are below a Fund’s expense cap (i) at the time of the fee waiver and/or expense reimbursement and (ii) at the time of the recoupment. This agreement may be terminated: (i) by the Board, for any reason at any time; or (ii) by the Adviser, upon ninety (90) days’ prior written notice to the Trust, effective as of the close of business on April 30, 2027.

For the fiscal year ended December 31, 2025, the Adviser received advisory fees, stated as a percentage of average daily net assets of each Fund, as follows:

Fund |

Advisory Fees paid |

Champlain Small Company Fund |

0.81% |

Champlain Mid Cap Fund |

0.70% |

Champlain Strategic Focus Fund |

0.00% |

A discussion regarding the basis for the Board’s approval of the investment advisory agreement for the Funds is available in the Funds’ reports filed on Form-CSR for the fiscal year ended December 31, 2025.

Portfolio Managers

The Funds are managed by the following team of investment professionals headed by Scott T. Brayman, Chartered Financial Analyst (“CFA”). The portfolio managers are jointly and primarily responsible for the day-to-day management of each Fund’s portfolio.

Portfolio Manager |

Position with the Adviser |

Years of Industry Experience |

Scott T. Brayman |

Chief Investment Officer /Managing Partner |

42 |

Joseph M. Caligiuri |

Deputy Chief Investment Officer /Partner |

17 |

Rachel C. Drakon |

Member of the Investment Team |

5 |

Ethan C. Ellison |

Member of the Investment Team/Principal |

9 |

Joseph J. Farley |

Member of the Investment Team/Partner |

33 |

Robert D. Hallisey |

Member of the Investment Team/Partner |

32 |

James A. Mallon |

Trader/Principal |

10 |

Finn R. McCoy |

Head Trader/Partner |

19 |

Henry C. Sinkula |

Member of the Investment Team/Partner |

10 |

Jacqueline W. Williams |

Member of the Investment Team/Partner |

29 |

Courtney A. Flyer |

Member of the Investment Team/Principal |

15 |

Mr. Scott T. Brayman, CFA, has served as Chief Investment Officer and Managing Partner of the Adviser since September 2004. In addition, Mr. Brayman has led the Adviser’s investment team since the firm’s inception in September 2004. Prior to joining the Adviser, Mr. Brayman was a Senior Vice President at NL Capital Management, Inc. (“NL Capital”) and served as a portfolio manager at Sentinel Advisors Company (“Sentinel”) where he was responsible for managing small-cap and core mid-cap strategies. He also spent time as a portfolio manager and Director of Marketing at Argyle Capital Management in Allentown, Pennsylvania before joining NL Capital Management. Mr. Brayman began his career as a credit analyst with the First National Bank of Maryland. Mr. Brayman graduated cum laude from the University of Delaware with a Bachelor’s Degree in Business Administration. He earned his CFA designation in 1995 and is a member of the CFA Institute and the Vermont CFA Society. He has more than 42 years of investment experience.

19 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Mr. Joseph M. Caligiuri, CFA, Deputy Chief Investment Officer and Partner of the Adviser, joined the Adviser in 2008 as an Operations Analyst and moved to the investment team in 2010. His experience includes internships at Sheaffer & Roland Consulting Engineers as a business operations analyst and Sopher Investment Management as an assistant research analyst. Mr. Caligiuri graduated from Saint Michael’s College with a Bachelor of Arts in Philosophy. He earned his CFA designation in 2015 and is a member of the CFA Institute and the Vermont CFA Society. He has more than 17 years of investment experience.

Ms. Rachel C. Drakon, CFA, has been a member of the investment team of the Adviser since 2020. Prior to joining full-time, Ms. Drakon worked as an intern for the Adviser, and as a Peer Finance Coach at Champlain College where she developed investment-focused financial literacy curriculum. Ms. Drakon graduated summa cum laude from Champlain College with a Bachelor of Science degree in Finance. She earned her CFA designation in 2022 and is a member of the CFA Institute and the CFA Society Vermont. She has more than 5 years of investment experience.

Mr. Ethan C. Ellison, CFA, has been a member of the investment team of the Adviser since July 2020. Prior to joining the Adviser, Mr. Ellison was a Vice President in the Equity Research Department at Morgan Stanley where he focused on power, utilities, and clean technology stocks. Before his time on Wall Street, Mr. Ellison served for six years in the United States Air Force, most notably as a Space Operations Analyst. Mr. Ellison graduated from the University of Vermont with a Bachelor of Science degree in Business Administration, earned his Master of Science in Financial Analysis from the University of San Francisco, and earned his Master of Business Administration, with distinction, from New York University’s Stern School of Business. He earned his CFA designation in 2020 and is a member of the CFA Institute and the CFA Society Vermont. He has more than 9 years of investment experience.

Mr. Joseph J. Farley, Partner of the Adviser, has been a member of the investment team since August 2014. Prior to joining the Adviser, Mr. Farley was a founder and portfolio manager of Kelvingrove Partners, LLC, an investment management firm focused on technology, media, and telecommunications, where he was employed from 2008 to 2013. His investment management career began at Private Capital Management, where he was the managing director of investment research and a portfolio manager. Mr. Farley spent over 10 years as a securities analyst on Wall Street, and held senior investment research and management roles at Morgan Stanley, Donaldson Lufkin & Jenrette, and UBS. He began his career as a market analyst with AT&T. Mr. Farley earned both his Master and Bachelor of Arts degrees from the University at Albany, State University of New York. He has more than 33 years of investment experience.

Mr. Robert D. Hallisey, Partner of the Adviser, has been a member of the investment team of the Adviser since August 2016. Prior to joining the Adviser, Mr. Hallisey was a member of Fidelity’s fund manager due diligence team. Mr. Hallisey’s experience includes coverage of the small and mid cap health care sector at BlackRock, Sirios Capital, and John Hancock Funds. Mr. Hallisey graduated from Saint Michael’s College with a Bachelor of Science in Business Administration and earned his MBA from Babson College. He has more than 32 years of investment experience.

Mr. James A. Mallon joined the Adviser in 2015 as an Associate – Operations & Compliance, transitioned to focus solely on compliance in the fall of 2017, and moved to the trading desk in 2023. His prior experience includes a summer internship with LL Global. Mr. Mallon graduated from Colgate University with a Bachelor of Arts degree in Psychology and was awarded the Investment Foundations certificate by the CFA Institute in 2017. Mr. Mallon brings over 10 years of industry experience to his role with the Adviser.

Mr. Finn R. McCoy, Partner of the Adviser, joined Champlain as an Operations Analyst in 2006 and moved to the trading desk in 2008. Prior to joining the Adviser, Mr. McCoy held internships with the offices of United States Senators Patrick Leahy and James Jeffords and also spent a semester studying abroad in Buenos Aires, Argentina. Mr. McCoy graduated with honors with a Bachelor of Arts in Economics from the University of Vermont in May 2006. He has more than 19 years of investment experience.

Mr. Henry C. Sinkula, CFA, Partner of the Adviser, joined Champlain as a Quantitative Analyst in 2015 supporting the firm’s strategies with portfolio analytics, risk monitoring, and quantitative research before joining the emerging markets team in 2018, and then joining the Adviser’s small and mid cap investment team as a financials analyst in 2022. Prior to joining the Adviser, Mr. Sinkula was an intern with the Adviser and held a summer analyst position with NASDAQ’s New Listings and Capital Markets team in New York. Mr. Sinkula graduated from the University of Vermont with a Bachelor of Science degree in Finance and a minor in Economics. Mr. Sinkula earned his CFA designation in 2018 and is a member of the CFA Institute and the CFA Society Vermont. He has more than 10 years of investment management experience.

Ms. Jacqueline W. Williams, CFA, Partner of the Adviser, joined Champlain in July 2019. She is an analyst for the healthcare sector on the investment team. Prior to joining Champlain in July 2019, Ms. Williams held Vice President, Equity Analyst roles at GW&K Investment Management - where she focused on small and smid cap health care equities - and with AlphaOne Capital Partners, where she focused on small and micro cap health care and industrial equities. Ms. Williams graduated from Colgate University with a

20 |

CHAMPLAIN INVESTMENT |

PARTNERS |

Bachelor of Arts degree in Economics and German Literature and earned her Masters of Business Administration degree from NYU’s Leonard Stern School of Business. Ms. Williams earned her CFA designation in 2004 and is a member of the CFA Institute and the Boston CFA Society. She has more than 29 years of investment experience.

Ms. Courtney A. Flyer, CFA, has been a member of the investment team of the Adviser since May 2018. Prior to joining the Adviser, Ms. Willson held Equity Research Associate roles with Cowen & Company from 2014 to 2018, where she focused on retailing/specialty stores, luxury, broadlines, and department stores, and RBC Capital Markets from 2011 to 2014, where she focused on apparel retail. Ms. Willson earned her CFA designation in 2022 and is a member of the CFA Institute and CFA Society Vermont. Ms. Willson graduated with a Bachelor of Arts in Economics and Sociology from Boston College. She has more than 15 years of investment experience.

The SAI provides additional information about the portfolio managers’ compensation, other accounts managed and ownership of Fund shares.

Purchasing, Selling and Exchanging Fund Shares

This section tells you how to purchase, sell (sometimes called “redeem”) and exchange shares of the Funds.

Advisor and Institutional Shares of the Funds are for individual and institutional investors.

For information regarding the federal income tax consequences of transactions in shares of a Fund, including information about cost basis reporting, see “Taxes.”

How to Purchase Fund Shares

To purchase shares directly from the Funds through their transfer agent, complete and send in the application. If you need an application or have questions, please call 1.866.773.3238.

All investments must be made by check, Automated Clearing House (“ACH”), or wire. All checks must be made payable in U.S. dollars and drawn on U.S. financial institutions. The Funds do not accept purchases made by third-party checks, credit cards, credit card checks, cash, traveler’s checks, money orders or cashier’s checks.

The Funds reserve the right to reject any specific purchase order for any reason. The Funds are not intended for short-term trading by shareholders in response to short-term market fluctuations. For more information about the Funds’ policy on short-term trading, see “Excessive Trading Policies and Procedures.”

The Funds do not generally accept investments by non-U.S. persons. Non-U.S. persons may be permitted to invest in the Funds subject to the satisfaction of enhanced due diligence. Please contact the Funds for more information.

By Mail

You can open an account with the Funds by sending a check and your account application to the address below. You can add to an existing account by sending the Funds a check and, if possible, the “Invest by Mail” stub that accompanies your confirmation statement. Be sure your check identifies clearly your name, your account number, the Fund name and the share class.

Regular Mail Address |

Express Mail Address |

Champlain Funds P.O. Box 219009 Kansas City, MO 64121-9009 |

Champlain Funds

c/o SS&C Global Investor & Distribution Solutions, Inc.

801 Pennsylvania Avenue

Suite 219009

Kansas City, MO 64105-1307 |

The Funds do not consider the U.S. Postal Service or other independent delivery services to be their agents. Therefore, deposit in the mail or with such services of purchase orders does not constitute receipt by the Funds’ transfer agent. The share price used to fill the purchase order is the next price calculated by a Fund after the Funds’ transfer agent receives and accepts the order in good order at the P.O. Box provided for regular mail delivery or the office address provided for express mail delivery.

21 |

CHAMPLAIN INVESTMENT |

PARTNERS |

By Wire

To open an account by wire, first call 1.866.773.3238 for details. To add to an existing account by wire, wire your money using the wiring instructions set forth below (be sure to include the Fund name, the share class and your account number). The share price used to fill the purchase order is the next price calculated by a Fund after the Fund’s transfer agent receives and accepts the wire in good order.

Wiring Instructions |

UMB Bank, N.A. ABA #101000695 Champlain Funds DDA Account #9870523965 Ref: Fund name/account number/account name/share class |

By Automatic Investment Plan (Via ACH) (for Advisor Shares only)

You may not open an account via ACH. However, once you have established an account, you can set up an automatic investment plan by mailing a completed application to the Funds. These purchases can be made monthly, quarterly, semi-annually or annually in amounts of at least $25. To cancel or change a plan, write to the Funds at: Champlain Funds, P.O. Box 219009, Kansas City, MO 64121-9009 (Express Mail Address: Champlain Funds, c/o SS&C Global Investor & Distribution Solutions, Inc., 801 Pennsylvania Avenue, Kansas City, MO 64105-1307). Allow up to 15 days to create the plan and 3 days to cancel or change it.

Purchases In-Kind

Subject to the approval of the Funds, an investor may purchase shares of a Fund with liquid securities and other assets that are eligible for purchase by the Fund (consistent with the Fund’s investment policies and restrictions) and that have a value that is readily ascertainable in accordance with the valuation procedures used by the Funds. These transactions will be effected only if the Adviser deems the security to be an appropriate investment for the Fund. Assets purchased by the Fund in such a transaction will be valued in accordance with the valuation procedures used by the Funds. The Funds reserve the right to amend or terminate this practice at any time.

Minimum Purchases

To purchase Advisor Shares of the Funds for the first time, you must invest at least $10,000 ($3,000 for IRAs). To purchase Institutional Shares of the Funds for the first time, you must invest at least $1,000,000. There is no minimum for subsequent investments. A Fund may accept investments of smaller amounts in its sole discretion.

Advisor Shares of the Champlain Strategic Focus Fund are currently not available for purchase.

Fund Codes

Each Fund’s reference information, which is listed below, will be helpful to you when you contact the Fund to purchase Advisor or Institutional Shares, exchange shares, check a Fund’s daily NAV or obtain additional information.

Fund Name |

Share Class |

Trading Symbol |

CUSIP |

Fund Code |

Champlain Small Company Fund |

Advisor Shares |

CIPSX |

00764Q405 |

1352 |

Institutional Shares |

CIPNX |

00766Y190 |

1353 |

|

Champlain Mid Cap Fund |

Advisor Shares |

CIPMX |

00764Q744 |

1354 |

Institutional Shares |

CIPIX |

00766Y513 |

1355 |

|

Champlain Strategic Focus Fund |

Advisor Shares |

CIPRX |

00791R400 |

1350 |

Institutional Shares |

CIPTX |

00791R509 |

1351 |

22 |

CHAMPLAIN INVESTMENT |

PARTNERS |

General Information

You may purchase shares on any Business Day. Shares cannot be purchased by Federal Reserve wire on days when either the NYSE or the Federal Reserve is closed. The price per share will be the NAV next determined after a Fund or an authorized institution (as defined below) receives and accepts your purchase order in good order. “Good order” means that a Fund was provided a complete and signed account application, including the investor’s social security number or tax identification number, and other identification required by law or regulation, as well as sufficient purchase proceeds. Purchase orders that are not in good order cannot be accepted and processed even if money to purchase shares has been submitted by wire, check or ACH.

Each Fund calculates its NAV once each Business Day as of the close of normal trading on the NYSE (normally, 4:00 p.m., Eastern Time). To receive the current Business Day’s NAV, a Fund or an authorized institution must receive and accept your purchase order in good order before 4:00 p.m., Eastern Time. If your purchase order is not received and accepted in good order before the close of normal trading on the NYSE, you will receive the NAV calculated on the subsequent Business Day on which your order is received and accepted in good order. If the NYSE closes early, as in the case of scheduled half-day trading or unscheduled suspensions of trading, a Fund reserves the right to calculate NAV as of the earlier closing time. A Fund will not accept orders that request a particular day or price for the transaction or any other special conditions. Shares will only be priced on Business Days. Since securities that are traded on foreign exchanges may trade on days that are not Business Days, the value of a Fund’s assets may change on days when you are unable to purchase or redeem shares.

Buying or Selling Shares through a Financial Intermediary

In addition to being able to buy and sell Fund shares directly from the Funds through their transfer agent, you may also buy or sell shares of the Funds through accounts with financial intermediaries such as brokers and other institutions that are authorized to place trades in Fund shares for their customers. When you purchase or sell Fund shares through a financial intermediary (rather than directly from the Funds), you may have to transmit your purchase and sale requests to the financial intermediary at an earlier time for your transaction to become effective that day. This allows the financial intermediary time to process your requests and transmit them to the Funds prior to the time the Funds calculate their NAV that day. Your financial intermediary is responsible for transmitting all purchase and redemption requests, investment information, documentation and money to the Funds on time. If your financial intermediary fails to do so, it may be responsible for any resulting fees or losses. Unless your financial intermediary is an authorized institution, orders transmitted by the financial intermediary and received by the Funds after the time NAV is calculated for a particular day will receive the following day’s NAV.

Certain financial intermediaries, including certain broker-dealers and shareholder organizations, are authorized to act as agent on behalf of the Funds with respect to the receipt of purchase and redemption orders for Fund shares (“authorized institutions”). Authorized institutions are also authorized to designate other intermediaries to receive purchase and redemption orders on a Fund’s behalf. A Fund will be deemed to have received a purchase or redemption order when an authorized institution or, if applicable, an authorized institution’s designee, receives the order. Orders will be priced at a Fund’s next computed NAV after they are received by an authorized institution or an authorized institution’s designee. To determine whether your financial intermediary is an authorized institution or an authorized institution’s designee such that it may act as agent on behalf of a Fund with respect to purchase and redemption orders for Fund shares, you should contact your financial intermediary directly.

If you deal directly with a financial intermediary, you will have to follow its procedures for transacting with the Funds. Your financial intermediary may charge a fee for your purchase and/or redemption transactions. For more information about how to purchase or sell Fund shares through a financial intermediary, you should contact your financial intermediary directly.

How the Funds Calculate NAV

The NAV of a class of a Fund’s shares is determined by dividing the total value of the Fund’s portfolio investments and other assets attributable to the class, less any liabilities attributable to the class, by the total number of shares outstanding of the class. In calculating NAV, each Fund generally values its investment portfolio at market price. If market prices are not readily available or they are unreliable, such as in the case of a security value that has been materially affected by events occurring after the relevant market closes, securities are valued at fair value. The Board has designated the Adviser as the Funds’ valuation designee to make all fair value determinations with respect to the Funds’ portfolio investments, subject to the Board’s oversight. The Adviser has adopted and implemented policies and procedures to be followed when making fair value determinations, and it established a Valuation Committee through which the Adviser makes fair value determinations. The Adviser’s determination of a security’s fair value price often involves the consideration of a number of subjective factors, and is therefore subject to the unavoidable risk that the value that is assigned to a security may be higher or lower than the security’s value would be if a reliable market quotation for the security was readily available.

23 |

CHAMPLAIN INVESTMENT |

PARTNERS |

There may be limited circumstances in which the Adviser would price securities at fair value for stocks of U.S. companies that are traded on U.S. exchanges – for example, if the exchange on which a portfolio security is principally traded closed early or if trading in a particular security was halted during the day and did not resume prior to the time a Fund calculated its NAV.