by the performance of a

CDO’s collateral manager (the entity responsible for selecting and managing the pool of collateral securities held by the SPE), especially during a period of market

volatility. CDOs may be illiquid securities and subject to the Fund’s restrictions on investments in illiquid securities. The Fund’s investment in CDOs will not

receive the same investor protection as an investment in registered securities. Also, prices of CDO tranches can decline considerably.

•

Derivatives Risk. Derivatives or other similar instruments (referred to collectively as “derivatives”), such as futures, forwards, options, swaps, structured securities and other similar instruments, are financial contracts whose value depends on, or is derived from, the value of an underlying asset, reference rate or index. Derivatives may involve costs and risks that are different from, or possibly greater than, the costs and risks associated with investing directly in securities and other traditional investments. Derivatives prices can be volatile, may correlate imperfectly with price of the applicable underlying asset, reference rate or index and may move in unexpected ways, especially in unusual market conditions, such as markets with high volatility or large market declines. Some derivatives are particularly sensitive to changes in interest rates. Other risks include liquidity risk, which refers to the potential inability to terminate or sell derivative positions and for derivatives to create margin delivery or settlement payment obligations for the Fund. Further, losses could result if the counterparty to a transaction does not perform as promised. Derivatives that involve a small initial investment relative to the investment risk assumed can magnify or otherwise increase investment losses. This is referred to as financial “leverage” due to the potential for greater investment loss. Derivatives are also subject to operational and legal risks.

•

Foreign Investments Risk. Foreign investments have additional risks that are not present when investing in U.S. investments. Foreign

currency fluctuations or economic or financial instability could cause the value of foreign investments to fluctuate. The value of foreign investments may be reduced by

foreign taxes, such as foreign taxes on interest and dividends. Additionally, foreign investments include the risk of loss from foreign government or political actions

including, for example, the imposition of exchange controls, the imposition of tariffs, economic and trade sanctions or embargoes, confiscations, and other government restrictions, or from problems in registration, settlement or custody. Investing in foreign investments may involve risks resulting from the reduced availability of public information concerning issuers. Foreign investments may be less liquid and their prices more volatile than comparable investments in U.S. issuers. In addition, certain foreign countries may be subject to terrorism, governmental collapse, regional conflicts and war, which could negatively impact investments in those countries.

•

Liquidity Risk. Liquidity risk is the risk that the Fund cannot meet requests to redeem Fund-issued shares without significantly diluting the remaining investors’ interest in the Fund. This may result when portfolio holdings may be difficult to value and may be difficult to sell, both at the time or price desired. Liquidity risk also may result from increased shareholder redemptions in the Fund. Actions by governments and regulators may have the effect of reducing market liquidity, market resiliency and money supply. Liquidity risk also refers to the risk that the Fund may be required to hold additional cash or sell other investments in order to obtain cash to close out derivatives or meet the liquidity demands that derivatives can create to make payments of margin, collateral, or settlement payments to counterparties. The Fund may have to sell a security at a disadvantageous time or price to meet such obligations. The Fund’s liquidity risk management program requires that the Fund invest no more than 15% of its net assets in illiquid investments.

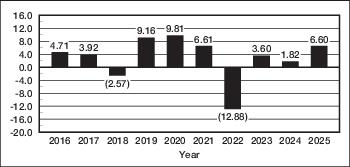

Fund Performance

The following bar chart and table provide some indication of the risks of choosing to invest in the Fund. The

information shows: (a) how the Fund's Standard Class II investment results have varied from year to year; and (b) how the average annual total returns of the Fund's Standard Class, Standard Class II and Service Class compare with those of a broad measure of market performance. Once the Standard Class of the Fund has had at least one full year of performance, average annual total

returns will be included in this prospectus. The bar chart shows performance of

the Fund's Standard Class II shares, but does not reflect the impact of variable contract expenses. If it did, returns would be lower than those shown. Performance in the average annual returns table does not reflect the impact of variable contract expenses.

The Fund's past performance is not necessarily an indication of how the Fund will perform in the

future.

Annual Total Returns (%)

LVIP American Century Inflation Protection Fund3