AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION

ON APRIL 29, 2026

REGISTRATION NOS. 033-79858

811-08544

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM N-1A

| |

REGISTRATION STATEMENT UNDER THE SECURITIES

ACT OF 1933 |

☐ |

| |

PRE-EFFECTIVE AMENDMENT

NO. |

☐ |

| |

POST-EFFECTIVE AMENDMENT NO.

148 |

☒ |

| |

AND/OR |

|

| |

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY

ACT OF 1940 |

☐ |

| |

AMENDMENT NO. 149 |

☒ |

INVESTMENT MANAGERS SERIES TRUST III

(Exact Name of Registrant as Specified in Charter)

235 West Galena Street

Milwaukee, Wisconsin 53212

(Address of Principal Executive Offices, including

Zip Code)

Registrant’s Telephone Number, Including Area

Code: (626) 385-5777

Diane J. Drake

Mutual Fund Administration, LLC

2220 E. Route 66, Suite 226

Glendora, California 91740

(Name and Address of Agent for Service)

COPIES TO:

Laurie Anne Dee

Morgan, Lewis & Bockius LLP

600 Anton Boulevard, Suite 1800

Costa Mesa, California 92626

It is proposed that this filing will become effective (check appropriate

box):

| |

☐ |

immediately upon filing pursuant to paragraph

(b) of Rule 485; or |

| |

☒ |

on April 30, 2026 pursuant to paragraph (b) of Rule 485; or |

| |

☐ |

60 days after filing pursuant to paragraph (a)(1) of

Rule 485; |

| |

☐ |

on _______________ pursuant to paragraph (a)(1) of

Rule 485; or |

| |

☐ |

75 days after filing pursuant to paragraph (a)(2) of

Rule 485; or |

| |

☐ |

on _______________ pursuant to paragraph (a)(2) of

Rule 485; or |

| |

☐ |

on _______________ pursuant to paragraph (a)(3) of

Rule 485. |

If appropriate, check the following box:

☐ This post-effective amendment designates a new effective date

for a previously filed post-effective amendment.

FPA Crescent Fund

PROSPECTUS

Institutional Class Shares - (FPACX)

Investor Class Share - (FPFRX)

FPA Crescent Fund (the "Fund") seeks to generate equity-like returns over the long-term, take less risk than the market and avoid permanent impairment of capital. The Fund's portfolio managers employ a strategy of selectively investing across a company's capital structure in a combination of equity and debt securities that they believe have the potential to increase in market value, seeking to achieve rates of return with less risk than the broad U.S. equity indices.

THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

April 30, 2026

Distributor:

DISTRIBUTION SERVICES, LLC

190 Middle Street, Suite 301

Portland, ME 04101

FPA CRESCENT FUND

235 West Galena Street

Milwaukee, Wisconsin 53212

Table of Contents

|

|

|

Page |

|

|

Fund Summary |

|

|

2 |

|

|

|

Additional Information About the Fund |

|

|

15 |

|

|

|

Additional Information About the Principal Investment Strategies |

|

|

17 |

|

|

|

Additional Information About the Principal Risks |

|

|

19 |

|

|

|

Management of the Fund |

|

|

31 |

|

|

|

Investing with the Fund |

|

|

33 |

|

|

|

How to Buy Fund Shares |

|

|

36 |

|

|

|

How to Redeem Your Shares |

|

|

37 |

|

|

|

How to Exchange Your Shares |

|

|

39 |

|

|

|

Other Shareholder Services |

|

|

41 |

|

|

|

Distributions and Taxes |

|

|

43 |

|

|

|

Financial Highlights |

|

|

46 |

|

|

1

FUND SUMMARY

INVESTMENT OBJECTIVE

The Fund seeks to generate equity-like returns over the long-term, take less risk than the market and avoid permanent impairment of capital.

FEES AND EXPENSES OF THE FUND'S INSTITUTIONAL AND INVESTOR CLASSES

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund's Institutional and Investor Classes. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example below.

Shareholder Fees

(fees paid directly from your investment) |

|

|

|

Institutional

Class |

|

|

|

Investor

Class |

|

Maximum Sales Charge (Load) Imposed on

Purchases (as a percentage of offering price) |

|

|

|

|

|

|

None |

|

|

|

|

|

|

|

None |

|

|

Maximum Deferred Sales Charge (Load) (as a

percentage of original sales price or redemption

proceeds, as applicable) |

|

|

|

|

|

|

None |

|

|

|

|

|

|

|

None |

|

|

|

Exchange Fee |

|

|

|

|

|

|

None |

|

|

|

|

|

|

|

None |

|

|

Annual Operating Expenses of the Fund's Institutional and Investor Class of Shares

(expenses that you pay each year as a percentage of the value of your investment in this class)

|

|

|

Management Fees1

|

|

|

|

|

|

|

1.00

|

%

|

|

|

|

|

|

|

1.00

|

%

|

|

|

Distribution (Rule 12b-1) fees

|

|

|

|

|

|

|

None

|

|

|

|

|

|

|

|

None

|

|

|

|

Other Expenses

|

|

|

|

|

|

|

0.09

|

%

|

|

|

|

|

|

|

0.28

|

%

|

|

|

Shareholder Service Fee

|

|

|

0.06

|

%

|

|

|

|

|

|

|

0.25

|

%

|

|

|

|

|

All Other Expenses

|

|

|

0.03

|

%

|

|

|

|

|

|

|

0.03

|

%

|

|

|

|

|

Total Annual Fund Operating Expenses

|

|

|

|

|

|

|

1.09

|

%

|

|

|

|

|

|

|

1.28

|

%

|

|

|

Expense Reimbursement2

|

|

|

|

|

|

|

(0.04

|

)%

|

|

|

|

|

|

|

(0.13

|

)%

|

|

Total Annual Operating Expenses after Expense

Reimbursement2

|

|

|

|

|

|

|

1.05

|

%

|

|

|

|

|

|

|

1.15

|

%

|

|

1

2

2

Example. This Example is intended to help you compare the cost of investing in the Institutional Class and Investor Class of the Fund with the cost of investing in other mutual funds. The Example assumes you invest $10,000 in the Institutional Class and Investor Class for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund's operating expenses remain the same. The one-year figure is based on total annual Fund operating expenses after expense reimbursement. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

|

|

|

One Year

|

|

Three Years

|

|

Five Years

|

|

Ten Years

|

|

|

Institutional Class

|

|

$

|

107

|

|

|

$

|

338

|

|

|

$

|

593

|

|

|

$

|

1,321

|

|

|

|

Investor Class

|

|

$

|

117

|

|

|

$

|

380

|

|

|

$

|

677

|

|

|

$

|

1,522

|

|

|

Portfolio Turnover. The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 23% of the average value of its portfolio. The Fund's portfolio turnover rate may vary from year to year as well as within a year.

PRINCIPAL INVESTMENT STRATEGIES

To pursue the Fund's investment objective, the Fund's portfolio managers invest in both equity and debt securities of companies. The Fund's portfolio managers believe that this combination of securities broadens the universe of opportunities for the Fund, offers additional diversification and helps to lower volatility. The portfolio managers invest primarily in equity securities and the balance of the Fund's portfolio in debt securities, cash, and cash equivalents. The Fund has no limit on the amount of assets it may invest in non-U.S. securities. The decision to invest in a non-U.S. security will be based on the portfolio managers' fundamental security analysis. In addition, the Fund may sell securities short, and the portfolio managers may employ a short selling strategy for a portion of the Fund.

Equity securities represent an ownership interest, or the right to acquire an ownership interest, in an issuer. Different types of equity securities provide different voting and dividend rights and priority in case of the bankruptcy of the issuer. The Fund may invest in a variety of equity securities, including common stocks, preferred stocks, convertible securities, rights, and warrants.

The portfolio managers look for large and small companies that they believe to have excellent future prospects that are undervalued by the securities markets. The portfolio managers believe that these opportunities often arise when companies are out-of-favor or undiscovered by most of Wall Street. The portfolio managers also search for companies that offer earnings growth, opportunity for price/earnings multiple expansion and the best combination of such quality criteria as strong market share, good management, high barriers to entry and high return on capital.

3

Using fundamental security analysis, the portfolio managers may look for investments that trade at a substantial discount to the portfolio managers' determination of the company's value (absolute value) rather than those that might appear inexpensive based on a discount to their peer groups or the market average (relative value). The portfolio managers attempt to determine a company's absolute value using fundamental security analysis, which they believe generally provides them with a thorough view of a company's financial and business characteristics. As a part of their process, the portfolio managers may:

• Review stock prices or industry group under-performance, insider purchases, management changes and corporate spin-offs.

• Communicate directly with company management, suppliers, and customers.

• Use their judgment to define the company's future potential, financial strength, and competitive position.

The portfolio managers generally seek to sell an equity investment when they believe that the company's value has been fully reflected in a higher valuation by the market or when a negative fundamental development occurs in the company or its industry that the portfolio managers believe could significantly impact future earnings growth.

A debt security is an interest-bearing security that companies or governments use to borrow money from investors. The issuer of a debt security promises to pay interest at a stated rate, which may be variable or fixed, and to repay the amount borrowed at maturity (the date when the debt security is due and payable). The Fund may invest in debt securities issued by companies, the U.S. government, and its agencies; mortgage-backed and asset-backed securities (i.e. securities that are backed by pools of loans or mortgages assembled for sale to investors); municipal notes and bonds; and commercial paper and certificates of deposit.

The portfolio managers invest in debt securities seeking to provide the Fund with a reliable and recurring stream of income, while seeking to preserve its capital. The Fund may also invest in debt securities rated below investment grade ("high yield bonds" or "junk bonds"). The Fund has the ability to invest up to 65% of its total assets in debt securities, although it will generally invest a greater percentage of its portfolio in equity securities than debt securities.

The portfolio managers select debt securities by using an approach that is similar to the approach they use to select equity securities and by trying to forecast current interest rate trends. The portfolio managers generally employ a defensive interest rate strategy, which means they seek to keep the average maturity of the debt-securities portion of the Fund to 10 years or less, by investing at different points along the yield curve. The portfolio managers also continually consider yield spreads and other underlying factors such as credit quality, investor perception and liquidity to determine which sectors offer the best investment value at any given time.

The portfolio managers may engage in a strategy known as selling short. Selling a security short is when the Fund sells a security it does not own. To sell a security short, the Fund must borrow the security from someone else to deliver to the buyer. The Fund then replaces the security it borrowed

4

by purchasing it at the market price at or before the time of replacement. Until it replaces the security, the Fund repays the person that lent it the security for any interest or dividends that may have accrued during the period of the loan. The Fund typically sells securities short to take advantage of an anticipated decline in prices or to protect a profit in a security it already owns.

PRINCIPAL RISKS

Risk is inherent in all investing and you could lose money by investing in the Fund. A summary description of certain principal risks of investing in the Fund is set forth below. Before you decide whether to invest in the Fund, carefully consider these risk factors associated with investing in the Fund, which may cause investors to lose money. There can be no assurance that the Fund will achieve its investment objective.

Market Risk. The market price of a security or instrument may decline, sometimes rapidly or unpredictably, due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic, political, or geopolitical conditions throughout the world, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. The market value of a security or instrument also may decline because of factors that affect a particular industry or industries, such as tariffs, labor shortages or increased production costs and competitive conditions within an industry. In addition, local, regional or global events such as war, acts of terrorism, international conflicts, trade disputes, supply chain disruptions, cybersecurity events, the spread of infectious illness or other public health issues, natural disasters or climate events, or other events could have a significant impact on a security or instrument. The increasing interconnectivity between global economies and financial markets increases the likelihood that events or conditions in one region or financial market may adversely impact issuers in a different country, region or financial market.

Risks Associated with Investing in Equities. Equity securities, generally common stocks and/or depositary receipts, held by the Fund may experience sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect the securities markets generally, such as adverse changes in economic or political conditions, the general outlook for corporate earnings, interest rates or investor sentiment. Sustained periods of market volatility, either globally or in any jurisdiction in which the Fund invests, may increase the risks associated with an investment in the Fund. Equity securities may also lose value because of factors affecting an entire industry or sector, such as increases in production costs, or factors directly related to a specific company, such as decisions made by its management. Equity securities generally have greater price volatility than debt securities. The Fund's shares are not bank deposits and are not guaranteed, endorsed, or insured by any financial institution, government authority or the FDIC.

Interest Rate Risk. Generally, fixed income securities decrease in value if interest rates rise and increase in value if interest rates fall, with longer-term securities being more sensitive than shorter-term securities. For example, the price of a security with a three-year duration would be expected to drop by approximately 3% in response to a 1% increase in interest rates. Generally, the longer the maturity and duration of a bond or fixed rate loan, the more sensitive it is to this risk. Falling interest rates also create the potential for a decline in the Fund's income. Changes in

5

governmental policy, rising inflation rates, and general economic developments, among other factors, could cause interest rates to increase and could have a substantial and immediate effect on the values of the Fund's investments. In addition, a potential rise in interest rates may result in periods of volatility and increased redemptions that might require the Fund to liquidate portfolio securities at disadvantageous prices and times.

Adjustable Rate Mortgage ("ARM") Risk. During periods of extreme fluctuations in interest rates, the resulting fluctuations of ARM rates could affect the ARMs' market value. Most ARMs have annual reset limits or "caps." Fluctuations in interest rates above these levels, thus, could cause the mortgage-backed securities to "cap out" and to behave more like long-term, fixed-rate debt securities. During periods of declining interest rates, of course, the coupon rates may readjust downward and result in lower yields.

Credit Risk. Credit risk refers to the likelihood that an issuer will default on the payment of principal and/or interest on a security. Various factors could affect the issuer's actual or perceived willingness or ability to make timely interest or principal payments, including changes in the issuer's financial condition or in general economic conditions. High yield bonds, commonly referred to as "junk" bonds, are highly speculative securities that are usually issued by smaller, less credit-worthy and/or highly leveraged (indebted) companies. Compared with investment-grade bonds, high yield bonds carry a greater degree of risk and are less likely to make payments of interest and principal. Market developments and the financial and business conditions of the corporation issuing these securities influence their price and liquidity more than changes in interest rates, when compared to investment-grade debt securities. Insufficient liquidity in the high yield bond market may make it more difficult to dispose of high yield bonds and may cause the Fund to experience sudden and substantial price declines. A lack of reliable, objective data or market quotations may make it more difficult to value high yield bonds accurately. There is no limit on the ratings of high yield securities that may be purchased or held by the Fund, and the Fund may invest in securities that are in default.

Call Risk. Issuers of callable bonds are permitted to redeem these bonds before their final maturity. If an issuer calls a security in which the Fund is invested, the Fund could lose potential price appreciation and be forced to reinvest the proceeds in securities that bear a lower interest rate or more credit risk.

Risks Associated with Investing in Smaller-Cap and Mid-Cap Companies. The prices of securities of mid-cap and smaller-cap companies tend to fluctuate more widely than those of larger, more established companies. Mid-cap and smaller-cap companies may have limited product lines, markets or financial resources or may depend on the expertise of a few people and may be subject to more abrupt or erratic market movements than securities of larger, more established companies or market averages in general. In addition, these companies often have shorter operating histories and are more reliant on key products or personnel than larger companies. The securities of smaller- or medium- sized companies are often traded over-the-counter, and may not be traded in volumes typical of securities traded on a national securities exchange. Securities of such issuers may lack sufficient market liquidity to effect sales at an advantageous time or without a substantial drop in price.

6

Risks Associated with Investing in Non-U.S. Securities. Non-U.S. investments involve special risks not present in U.S. investments that can increase the chances that the Fund will lose money. The prices of non-U.S. securities may be more volatile than the prices of securities of U.S. issuers because of economic and social conditions abroad, political developments, and changes in the regulatory environments of foreign countries. Changes in exchange rates and interest rates, and the imposition of sanctions, confiscations, trade restrictions (including tariffs) and other government restrictions by the United States and/or other governments may adversely affect the values of the Fund's non-U.S. investments. Foreign companies are generally subject to different legal and accounting standards than U.S. companies, and foreign financial intermediaries may be subject to less supervision and regulation than U.S. financial firms. In addition, since January 20, 2025, the current U.S. administration has pursued an aggressive foreign policy agenda, including the imposition of tariffs, which may have unforeseen consequences on the United States' relations with foreign countries, the economy, and markets generally. Emerging markets tend to be more volatile than the markets of more mature economies and generally have less diverse and less mature economic structures and less stable political systems than those of developed countries.

Risks Associated with Investing in Emerging Markets. Investing in emerging markets may magnify the risks of investing in non-U.S. markets. Security prices in emerging markets can be significantly more volatile than those in more developed markets, reflecting the greater uncertainties of investing in less established markets and economies. In particular, countries with emerging markets may:

• Have relatively unstable governments;

• Present greater risks of nationalization of businesses, restrictions on foreign ownership and prohibitions on the repatriation of assets;

• Have government exchange controls, currencies with no recognizable market value relative to the established currencies of developed market economies, little or no experience in trading in securities, no financial reporting standards, or a lack of a banking and securities infrastructure to handle such trading;

• Offer less protection of property rights than more developed countries;

• Have economies that are based on only a few industries, may be highly vulnerable to changes in local or global trade conditions, and may suffer from extreme and volatile debt burdens or inflation rates; and

• Not have developed structures governing private or foreign investment or allowing for judicial redress for investment losses or injury to private property, which may limit legal rights and remedies available to the Fund and the ability of U.S. authorities (e.g., the SEC and the U.S. Department of Justice) to bring actions against bad actors may be limited.

Local securities markets may trade a small number of securities and may be unable to respond effectively to increases in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times.

7

Risks Associated with Short Selling. The Fund can lose money if the price of the security it sold short increases between the date of the short sale and the date on which the Fund replaces the borrowed security. These losses are theoretically unlimited. To borrow the security, the Fund also may be required to pay a premium, which would increase the cost of the security sold. The Fund will incur transaction costs in effecting short sales. The Fund's gains and losses will be decreased or increased, as the case may be, by the amount of the premium, dividends, interest, or expenses the Fund may be required to pay in connection with a short sale.

Risks Associated with Value Investing. Value securities, including those selected by the portfolio managers for the Fund, are subject to the risks that their intrinsic value may never be realized by the market and that their prices may go down. In addition, value style investing may fall out of favor and underperform growth or other styles of investing during given periods. The Fund's value discipline may result in a portfolio of securities that differs materially from its illustrative indices.

Securities selected by the portfolio managers using a value strategy may never reach their intrinsic value because the market fails to recognize what the portfolio managers consider to be the true business value or because the portfolio managers have misjudged those values. There may be periods during which the investment performance of the Fund suffers while using a value strategy.

Liquidity Risk. The Fund's investments in illiquid securities may reduce the returns of the Fund because it may not be able to sell the illiquid securities at an advantageous time or price.

Over-the-Counter ("OTC") Investments Risk. Securities and derivatives traded in OTC markets may trade in smaller volumes, and their prices may be more volatile, than securities principally traded on securities exchanges. Such securities may be less liquid than more widely traded securities. In addition, the prices of such securities may include an undisclosed dealer markup, which the Fund pays as part of the purchase price.

U.S. Government Securities Risk. Certain U.S. government securities are supported by the full faith and credit of the United States; others are supported by the right of the issuer to borrow from the U.S. Treasury; others are supported by the discretionary authority of the U.S. government to purchase the agency's obligations; and still others are supported only by the credit of the issuing agency, instrumentality, or enterprise. Although U.S. government-sponsored enterprises such as the Federal Home Loan Mortgage Corporation (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae) may be chartered or sponsored by Congress, they are not funded by Congressional appropriations, and their securities are not issued by the U.S. Treasury, are not supported by the full faith and credit of the U.S. government, and involve increased credit risks in comparison to U.S. Treasury securities or other securities supported by the full faith and credit of the U.S. government.

Mortgage-Related and Asset-Backed Securities Risk. Mortgage-related and other asset-backed securities represent interests in "pools" of mortgages or other assets such as consumer loans or receivables held in trust and often involve risks that are different from or possibly more acute than risks associated with other types of debt instruments. Mortgage-related securities, including commercial mortgage-backed securities ("CMBS") and residential mortgage-backed securities ("RMBS") are subject to prepayment risk (the risk that borrowers will repay a loan more quickly

8

in periods of falling interest rates) and "extension risk" (the risk that borrowers will repay a loan more slowly in periods of rising interest rates) and can be highly sensitive to changes in interest rates. Mortgage-backed securities, and in particular those not backed by a government guarantee, are subject to credit risk. The Fund's investments in other asset-backed securities are subject to risks similar to those associated with mortgage-related securities, as well as additional risks associated with the nature of the assets and the servicing of those assets.

Risks Associated with Investing in High Yield Securities. High yield bonds, which are sometimes called "junk" bonds, are highly speculative securities that are usually issued by smaller, less credit- worthy and/or highly leveraged (indebted) companies. High yield securities are generally subject to greater levels of credit, call and liquidity risks than higher-rated securities of similar maturity. In addition, such securities may, under certain circumstances, be less liquid than higher rated securities. These securities pay investors a premium (a high interest rate or yield) because of the potential illiquidity and increased risk of loss. These securities can also be subject to greater price volatility. In times of unusual or adverse market, economic or political conditions, these securities may experience higher than normal default rates.

Risks Associated with Investing in Sovereign and Government-Related Debt. Sovereign debt includes securities issued or guaranteed by a non-U.S. sovereign government or its agencies, authorities, or political subdivisions. Government-related debt includes securities issued by non-U.S. regional or local governmental entities or government-controlled entities. In the event an issuer of sovereign debt or government-related debt is unable or unwilling to make scheduled payments of interest or principal, holders may be asked to participate in a restructuring of the debt and to extend further credit to the issuer. In the event of a default by such an issuer, there may be few or no effective legal remedies for collecting on such debt.

Risks Associated with Investing in Convertible Securities. A convertible security is a bond, debenture, or note that may be exchanged for particular common stocks in the future at a predetermined price or formula within a specified period of time. A convertible security entitles the holder to receive interest paid or accrued on the debt security until the convertible security matures or is redeemed. Prior to redemption, convertible securities provide benefits similar to nonconvertible debt securities in that they generally provide income with higher yields than those of similar common stocks. Convertible securities may entail less risk than the corporation's common stocks. Convertible securities are generally not investment grade. The risks of nonpayment of the principal and interest increase when debt securities are rated lower than investment grade or are not rated.

Risks Associated with Investing in Repurchase Agreements. A repurchase agreement is a short-term investment. The Fund acquires a debt security that the seller agrees to repurchase at a future time and set price. If the seller declares bankruptcy or defaults, the Fund may incur delays and expenses liquidating the security. The security may also decline in value or fail to provide income.

Large Investor Risk. Ownership of shares of the Fund may be concentrated in one or a few large investors. Such investors may redeem shares in large quantities or on a frequent basis. Redemptions

9

by a large investor may affect the performance of the Fund, may increase realized capital gains, may accelerate the realization of taxable income to shareholders and may increase transaction costs. These transactions potentially limit the use of any capital loss carryforwards and certain other losses to offset future realized capital gains (if any). Such transactions may also increase the Fund's expenses. In addition, the Fund may be delayed in investing new cash after a large shareholder purchase, and under such circumstances may be required to maintain a larger cash position than it ordinarily would.

Management Risk. The Fund is subject to management risk as an actively managed investment portfolio. The portfolio managers will apply investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these will produce the desired results. The portfolio managers' opinions about the intrinsic worth or creditworthiness of a company or security may be incorrect, the portfolio managers may not make timely purchases or sales of securities for the Fund, the Fund's investment objective may not be achieved, or the market may continue to undervalue the Fund's securities. In addition, the Fund may not be able to quickly dispose of certain securities holdings. The frequency of trading within the Fund impacts portfolio turnover rates, which are shown in the financial highlights table. A higher rate of portfolio turnover could produce higher trading costs and taxable distributions, which would detract from the Fund's performance. Moreover, there can be no assurance that all of the Adviser's personnel will continue to be associated with the Adviser for any length of time. The loss of services of one or more key employees of the Adviser, including the portfolio managers, could have an adverse impact on the Fund's ability to achieve its investment objective. Certain securities or other instruments in which the Fund seeks to invest may not be available in the quantities desired. In such circumstances, the portfolio managers may determine to purchase other securities or instruments as substitutes. Such substitute securities or instruments may not perform as intended, which could result in losses to the Fund.

Recent Market Events. Periods of market volatility may occur in response to market events, public health emergencies, natural disasters or climate events, and other economic, political, and global macro factors. U.S. and international markets have recently experienced, and may continue to experience, periods of significant volatility due to various factors, including uncertainty regarding inflation and central banks' interest rate changes, the possibility of a national or global recession, trade tensions and tariffs, and political and geopolitical events. In addition, wars or threats of war and aggression, such as Russia's invasion of Ukraine and the conflicts among nations and militant groups in the Middle East, have led, and in the future may lead, to increased short-term market volatility and may have adverse long-term effects on the U.S. and world economies and markets generally, each of which may negatively impact the Fund's investments. Additionally, since the change in the U.S. presidential administration in 2025, the administration has pursued an aggressive foreign policy agenda, including through suggestions that the United States should control certain sovereign foreign territories, attempts to restructure federal government agencies with international influence, and the imposition of tariffs, and trade barriers on certain foreign countries, including China and long-time U.S. allies. These and other similar events could be prolonged and could adversely affect the value and liquidity of the Fund's investments, impair the Fund's ability to satisfy redemption requests, and negatively impact the Fund's performance.

10

Cybersecurity Risk. Cybersecurity incidents may allow an unauthorized party to gain access to Fund assets, customer data (including private shareholder information), or proprietary information, or cause the Fund, the Adviser, and/or other service providers (including custodians, sub-custodians, transfer agents and financial intermediaries) to suffer data breaches, data corruption or loss of operational functionality. In an extreme case, a shareholder's ability to exchange or redeem Fund shares may be affected. The use of artificial intelligence and machine learning could exacerbate these risks. Issuers of securities in which the Fund invests are also subject to cybersecurity risks, and the value of those securities could decline if the issuers experience cybersecurity incidents.

PERFORMANCE INFORMATION

The bar chart and Average Annual Total Returns table below provide an indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year for Institutional Class shares and by showing how the average annual total returns of Institutional Class and Investor Class shares of the Fund, for the 1, 5 and 10 calendar year periods, compare with those of the MSCI All Country World Index, a broad-based securities market index. The Fund also compares its performance to the Standard & Poor's 500 Stock Index ("S&P 500"), a customized index comprised of 60% S&P 500 and 40% Bloomberg U.S. Aggregate Bond Index, and the Consumer Price Index ("CPI"). The S&P 500 and 60%/40% S&P 500/Bloomberg U.S. Aggregate Bond indexes are included as broad-based comparisons to the capitalization characteristics of the Fund's portfolio. The CPI is included as a comparison of the Fund's results to inflation. Certain past performance information shown below is for Institutional Class shares of the Fund. Although Institutional Class shares would have similar annual returns to Investor Class shares because the classes are invested in the same portfolio of securities, the returns for Investor Class shares will vary from Institutional Class shares because of the higher expenses paid by Investor Class shares. The chart and table reflect the reinvestment of dividends and distributions. In addition, the Fund's past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future.

The MSCI All Country World Index is a float-adjusted market capitalization index that is designed to measure the combined equity market performance of developed and emerging market countries. The S&P 500 is a capitalization-weighted index which is considered a measure of large capitalization U.S. equity performance, covering approximately 80% of available market capitalization. The 60%/40% S&P 500 Index/Bloomberg U.S. Aggregate Bond Index is a composite blend of 60% of the S&P 500 Index and 40% of the Bloomberg U.S. Aggregate Bond Index. The Consumer Price Index ("CPI") is an unmanaged index representing the rate of inflation of U.S. consumer prices as determined by the U.S. Bureau of Labor Statistics.

To obtain updated monthly performance information, please visit the Fund's website at https://fpa.com/fund or call (800) 982-4372.

11

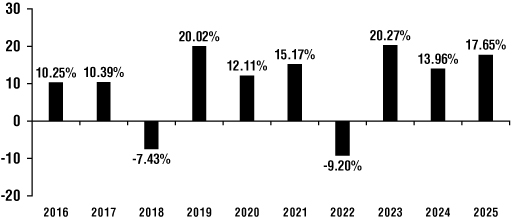

Calendar-Year Total Return (before taxes) for Institutional Class

For each calendar year at NAV

The Fund's highest/lowest quarterly results during this time period were:

Institutional Class

Highest 18.15% (Quarter ended 12/31/2020)

Lowest (20.51)% (Quarter ended 03/31/2020)

Average Annual Total Returns

(for the periods ended December 31, 2025)

|

|

One

Year

|

|

Five

Years

|

|

Ten

Years

|

|

|

Institutional Class Shares—Before Taxes

|

|

|

17.65

|

%

|

|

|

11.02

|

%

|

|

|

9.84

|

%

|

|

Institutional Class Shares—After Taxes on

Distributions1

|

|

|

15.15

|

%

|

|

|

9.20

|

%

|

|

|

8.25

|

%

|

|

Institutional Class Shares—After Taxes on

Distributions and Sale of Fund Shares1

|

|

|

12.19

|

%

|

|

|

8.43

|

%

|

|

|

7.64

|

%

|

|

|

Investor Class Shares—Before Taxes2

|

|

|

17.52

|

%

|

|

|

10.91

|

%

|

|

|

9.73

|

%

|

|

MSCI All Country World Index

(reflects no deductions for fees, expenses, or taxes)

|

|

|

22.34

|

%

|

|

|

11.19

|

%

|

|

|

11.72

|

%

|

|

S&P 500 Index (reflects no deductions for fees,

expenses, or taxes)

|

|

|

17.88

|

%

|

|

|

14.42

|

%

|

|

|

14.82

|

%

|

|

60%/40% S&P 500 Index/Bloomberg U.S. Aggregate

Bond Index (reflects no deductions for fees,

expenses, or taxes)

|

|

|

13.70

|

%

|

|

|

8.47

|

%

|

|

|

9.78

|

%

|

|

Consumer Price Index (reflects no deductions for fees,

expenses, or taxes)

|

|

|

2.63

|

%

|

|

|

4.47

|

%

|

|

|

3.21

|

%

|

|

1

2

12

INVESTMENT ADVISER

First Pacific Advisors, LP is the Fund's investment adviser.

PORTFOLIO MANAGERS

Steven Romick, a Managing Partner of the Adviser, has been a portfolio manager of the Fund since its inception on June 2, 1993. Mark Landecker and Brian Selmo, each a Partner of the Adviser, have been portfolio managers of the Fund since June 2, 2013. Messrs. Romick, Landecker and Selmo are primarily responsible for the day-to-day management of the Fund's portfolio.

PURCHASE AND SALE OF FUND SHARES

Investors may purchase or redeem shares on any business day by written request, check, wire, ACH (Automated Clearing House), telephone, or through dealers as further described in this prospectus. You may conduct transactions by mail (FPA Funds, c/o UMB Fund Services, Inc., P.O. Box 2175, Milwaukee, Wisconsin 53201-2175, or 235 West Galena Street, Milwaukee, Wisconsin 53212), by wire, or by telephone at (800) 638-3060. Purchases and redemptions by telephone are only permitted if you previously established this option in your account. Investors can use the Account Application for initial purchases.

Investors can purchase shares by contacting any investment dealer authorized to sell the Fund's shares. The minimum initial investment is $1,500 for both the Institutional Class and Investor Class Shares, and each subsequent investment, which can be made directly to UMB Fund Services, Inc., must be at least $100. However, as described herein, no minimum investment amount is imposed for investments in retirement plans. All purchases made by check should be in U.S. dollars and made payable to the FPA Funds. Third party, starter or counter checks will not be accepted. A charge may be imposed if a check does not clear. The Fund reserves the right to waive or lower purchase and investment minimums in certain circumstances. For example, the minimums listed above may be waived or lowered for investors who are Trustees or officers of the Fund, employees of the Adviser and/or customers of certain financial intermediaries that hold the Fund's shares in certain omnibus accounts, and investments in the Fund in connection with liquidity programs (described in additional detail below under "Management of the Fund"), at the discretion of the officers of the Fund. In addition, financial intermediaries may impose their own minimum investment and subsequent purchase amounts.

Subsequent investments and redemptions can be made directly to UMB Fund Services, Inc.

Notice to Non-U.S. Resident Individual Shareholders. The Fund and its shares are only registered in the United States and its territories ("United States"). Regulations outside of the United States may restrict the sale of shares to certain non-U.S. residents or subject certain shareholder accounts to additional regulatory requirements. As a result, individuals resident outside the United States are generally not eligible to invest in the Fund. The Fund reserves the right, however, to sell shares to certain other non-U.S. investors in compliance with applicable law. If a current shareholder of the Fund provides a non-U.S. address, this will be deemed a representation and warranty from such investor that he/she is not a U.S. resident and will continue to be a non-U.S. resident unless

13

and until the Fund is notified of a change in the investor's resident status. Any current shareholder that has a resident address outside of the United States may be restricted from purchasing additional shares.

TAX INFORMATION

The Fund's distributions are taxable and will be taxed as ordinary income and/or long-term capital gain, unless you are investing through a tax-deferred arrangement, such as an IRA or 401(k) plan.

INFORMATION REGARDING TRANSACTIONS THROUGH FINANCIAL INTERMEDIARIES

Shareholders may be required to pay a commission directly to their broker or other financial intermediary when buying or selling shares of the Fund. Shareholders and potential investors may wish to contact their broker or other financial intermediary for information regarding applicable commissions, transaction fees or other charges associated with transactions in shares of the Fund.

In addition, brokers, dealers, banks, trust companies and other financial representatives may receive compensation from the Fund or its service providers for providing a variety of services, which may include recordkeeping, transaction processing for shareholders' accounts and certain shareholder services not currently offered to shareholders that deal directly with the Fund. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's web site for more information.

14

ADDITIONAL INFORMATION ABOUT THE FUND

Investment Objective

The Fund seeks to generate equity-like returns over the long-term, take less risk than the market and avoid permanent impairment of capital.

The Fund's investment objective is not fundamental and may be changed by the Board without shareholder approval, upon at least 60 days' prior written notice to shareholders. The Fund's investment strategies and policies may be changed from time to time without shareholder approval or prior written notice, unless specifically stated otherwise in this Prospectus or the Statement of Additional Information ("SAI").

Principal Investment Strategies

To pursue the Fund's investment objective, the portfolio managers invest in both equity and debt securities of companies. The portfolio managers believe that this combination of securities broadens the universe of opportunities for the Fund, offers additional diversification and helps to lower volatility. The portfolio managers invest primarily in equity securities and the balance of the Fund's portfolio in debt securities, cash, and cash equivalents. The Fund has no limit on the amount of assets it may invest in non-U.S. securities. The decision to invest in a non-U.S. security will be based on the portfolio managers' fundamental security analysis. In addition, the Fund may sell securities short, and the portfolio managers may employ a short selling strategy for a portion of the Fund.

Equity securities represent an ownership interest, or the right to acquire an ownership interest, in an issuer. Different types of equity securities provide different voting and dividend rights and priority in case of the bankruptcy of the issuer. The Fund may invest in a variety of equity securities, including common stocks, preferred stocks, convertible securities, rights, and warrants.

The portfolio managers look for large and small companies that they believe to have excellent future prospects that are undervalued by the securities markets. The portfolio managers believe that these opportunities often arise when companies are out-of-favor or undiscovered by most of Wall Street. The portfolio managers also search for companies that offer earnings growth, opportunity for price/earnings multiple expansion and the best combination of such quality criteria as strong market share, good management, high barriers to entry and high return on capital.

Using fundamental security analysis, the portfolio managers may look for investments that trade at a substantial discount to the portfolio managers' determination of the company's value (absolute value) rather than those that might appear inexpensive based on a discount to their peer groups or the market average (relative value). The portfolio managers attempt to determine a company's absolute value using fundamental security analysis, which they believe generally provides them with a thorough view of a company's financial and business characteristics. As a part of their process, the portfolio managers may:

• Review stock prices or industry group under-performance, insider purchases, management changes and corporate spin-offs.

15

• Communicate directly with company management, suppliers, and customers.

• Use their judgment to define the company's future potential, financial strength, and competitive position.

The portfolio managers generally seek to sell an equity investment when they believe that the company's value has been fully reflected in a higher valuation by the market or when a negative fundamental development occurs in the company or its industry that the portfolio managers believe could significantly impact future earnings growth.

A debt security is an interest-bearing security that companies or governments use to borrow money from investors. The issuer of a debt security promises to pay interest at a stated rate, which may be variable or fixed, and to repay the amount borrowed at maturity (the date when the debt security is due and payable). The Fund may invest in debt securities issued by companies, the U.S. government, and its agencies; mortgage-backed and asset-backed securities (i.e. securities that are backed by pools of loans or mortgages assembled for sale to investors); municipal notes and bonds; and commercial paper and certificates of deposit.

The portfolio managers invest in debt securities seeking to provide the Fund with a reliable and recurring stream of income, while seeking to preserve its capital. The Fund may also invest in debt securities rated below investment grade ("high yield bonds" or "junk bonds"). The Fund has the ability to invest up to 65% of its total assets in debt securities, although it will generally invest a greater percentage of its portfolio in equity securities than debt securities.

The portfolio managers select debt securities by using an approach that is similar to the approach they use to select equity securities and by trying to forecast current interest rate trends. The portfolio managers generally employ a defensive interest rate strategy, which means they seek to keep the average maturity of the debt-securities portion of the Fund to 10 years or less, by investing at different points along the yield curve. The portfolio managers also continually consider yield spreads and other underlying factors such as credit quality, investor perception and liquidity to determine which sectors offer the best investment value at any given time.

The portfolio managers may engage in a strategy known as selling short. Selling a security short is when the Fund sells a security it does not own. To sell a security short, the Fund must borrow the security from someone else to deliver to the buyer. The Fund then replaces the security it borrowed by purchasing it at the market price at or before the time of replacement. Until it replaces the security, the Fund repays the person that lent it the security for any interest or dividends that may have accrued during the period of the loan. The Fund typically sells securities short to take advantage of an anticipated decline in prices or to protect a profit in a security it already owns.

16

ADDITIONAL INFORMATION ABOUT THE PRINCIPAL INVESTMENT STRATEGIES

To pursue the Fund's investment objective, the portfolio managers generally invest the Fund's assets in common stocks and other securities of international and U.S. companies and debt securities, including but not limited to the following securities:

Equity Securities. Equity securities represent ownership shares in a company, and include securities that convey an interest in, may be converted into or give holders a right to purchase or otherwise acquire such ownership shares in a company.

Common Stock. Common stocks represent shares of ownership in a company. After other company obligations are satisfied, common stockholders participate in company profits on a pro-rata basis; profits may be paid out in dividends or reinvested in the company to help it grow. Increases and decreases in earnings are usually reflected in a company's stock price, so common stocks generally have the greatest appreciation and depreciation potential of all corporate securities. Ownership of common stock of a non-U.S. company may be represented by depositary receipts (which are certificates evidencing ownership of securities of a non-U.S. issuer).

Preferred Stock. Preferred stock is typically subordinated to an issuer's senior debt, but senior to the issuer's common stock. Typically, preferred stock is structured as a long-dated or perpetual bond that distributes income on a regular basis. Issuers are permitted to skip ("non-cumulative" preferred stock) or defer ("cumulative" preferred stock) distributions. Preferred stock may be convertible into common stock and may contain call or maturity extension features.

Warrants and Rights. Warrants are options to buy a stated number of shares of common stock at a specified price anytime during the life of the warrants (generally two or more years). They have no voting rights, pay no dividends, and have no rights with respect to the assets of the entity issuing them. Rights are similar to warrants but normally have a shorter duration and are typically distributed directly by the issuers to existing shareholders, while warrants are typically attached to new debt or preferred stock issuances. The market price of warrants may be substantially lower than the current market price of the underlying common stock, yet warrants are subject to similar price fluctuations. As a result, warrants may be more volatile investments than the underlying common stock. If a warrant is exercised, the Fund may hold common stock in its portfolio even if it does not ordinarily invest in common stock. Warrants and rights generally do not entitle the holder to dividends or voting rights with respect to the underlying common stock and do not represent any rights in the assets of the issuer. Warrants and rights will expire if not exercised on or prior to the expiration date.

Non-U.S. Securities. The Fund may invest in securities of U.S.-dollar denominated non-U.S. issuers traded in the United States and in non-U.S. currency-denominated securities of non-U.S. issuers. For purposes of this prospectus, non-U.S. issuers are generally non-U.S. governments or companies either domiciled outside the U.S. or traded on non-U.S. exchanges, but the portfolio managers may make a different designation in certain circumstances. The non-U.S. issuers that the Fund may invest in include issuers with significant exposure to countries with developing economies and/or markets.

17

Cash Equivalents. Cash equivalents are short-dated instruments that are readily convertible into cash. They may include bank obligations, commercial paper, and repurchase agreements. Bank obligations include certificates of deposit and bankers' acceptances. Commercial paper is a short-term promissory note issued by a corporation, which may have a floating or variable rate. Repurchase agreements are transactions under which the Fund purchases a security from a dealer counterparty and agrees to resell the security on a specified future date at the same price, plus a specified interest rate.

U.S. Government Securities. The U.S. government sector includes fixed-income securities issued by the U.S. government or its agencies and instrumentalities, such as U.S. Treasury and U.S. government agency securities, mortgage pass-through securities, including Government National Mortgage Association (Ginnie Mae), Federal Home Loan Mortgage Corporation (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae), and agency mortgage-backed securities.

Mortgage-Backed Securities. In addition to the U.S. government mortgage-pass through securities described above, the mortgage sector includes non-agency mortgage-backed securities, such as collateralized mortgage obligations ("CMOs"), CMBS, RMBS and single- and multi-class pass- through securities. Mortgage-backed securities represent direct or indirect participation in mortgage loans secured by real property.

Asset-Backed Securities. Asset-backed securities are bonds issued through special purpose vehicles and backed by pools of loans, other receivables, or other assets. Asset-backed securities are created from many types of assets, such as home equity loans, auto loans, student loans and credit card receivables. The credit quality of an asset-backed security depends on the quality and performance of the underlying assets and/or the level of any credit support provided by the securitization structure. The proportions of the Fund's portfolio invested in various types of asset-backed securities will depend on many factors, including the portfolio managers' appraisal of the economy, yield, credit quality, macroeconomic factors, and capital appreciation potential, among others. To the extent the Fund focuses its investments in a particular type of asset-backed security, it may be more susceptible to economic conditions and risks affecting the type of asset-backed security.

Corporate Debt Securities. The Fund may invest in corporate bonds, bank debt, notes and commercial paper of varying maturities and may invest in domestic bonds, bank debt and notes and those issued by non-U.S. corporations and governments. Issuers of these securities have a contractual obligation to pay interest at a specified rate on specified date and to repay principal on a specified maturity date, and may have provisions that allow the issuer to redeem or "call" the security before its maturity.

Temporary Investments and Other Measures. As a temporary measure for defensive purposes, the Fund may invest up to 100% of its total assets in short-term investments, including cash or cash equivalents, corporate debt, or direct or indirect U.S. and non-U.S. government and agency obligations, money market instruments, bank obligations, commercial paper, corporate notes and repurchase agreements. The Fund may make these investments or increase its investment in these securities when the managers are unable to find enough attractive long-term investments, to reduce exposure to the Fund's primary investments when the managers believe it is advisable to do so,

18

during periods of significant shareholder redemptions or when adverse or unusual market, economic, political, or other conditions exist. The Fund may take such portfolio positions for as long a period as deemed necessary. In doing so, the Fund may succeed in avoiding losses but may otherwise fail to achieve its investment objective. However, there can be no guarantee that a defensive strategy will be successful. Investing defensively may adversely affect Fund performance. During these times, the portfolio managers may make frequent portfolio holding changes, which could result in increased trading expenses and taxes, and decreased Fund performance.

As part of its normal operations, the Fund may hold cash or invest a portion of its portfolio in short-term interest bearing U.S. dollar denominated securities, pending investments or to provide for possible redemptions. Investments in such short-term debt securities can generally be sold easily and have limited risk of loss, but earn only limited returns. The Fund may increase its cash holdings and/or such short-term investments in anticipation of a greater than normal number of shareholder redemptions.

The Fund's emphasis on a value-oriented investment approach could result in a portfolio that does not reflect the national economy, differs significantly from broad market indices, and consists of securities considered by the average investor to be unpopular or unfamiliar.

Percentage Investment Limitations. Unless otherwise stated, all percentage limitations on Fund investments listed in this prospectus will apply at the time of purchase. The Fund would not violate these limitations unless an excess or deficiency occurs or exists immediately after and as a result of an investment.

Other Investments and Techniques. The Fund may invest in other types of securities and use a variety of investment techniques and strategies which are not principal investment strategies and are not described in this prospectus. These securities and techniques may subject the Fund to additional risks. Please see the Statement of Additional Information (the "SAI") for additional information about the securities and investment techniques described in this prospectus and about additional securities and techniques that may be used by the Fund.

ADDITIONAL INFORMATION ABOUT THE PRINCIPAL RISKS

The Fund's principal risks are set forth below. Before you decide whether to invest in the Fund, carefully consider these risk factors and special considerations associated with investing in the Fund, which may cause you to lose money.

Market Risk. The market price of a security or instrument may decline, sometimes rapidly or unpredictably, due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic, political, or geopolitical conditions throughout the world, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. The market value of a security or instrument also may decline because of factors that affect a particular industry or industries, such as tariffs, labor shortages or increased production costs and competitive conditions within an industry. In addition, local, regional or global events such as war, acts of terrorism, international conflicts, trade disputes, supply chain disruptions, cybersecurity events, the spread of infectious illness or other public health issues, natural disasters or climate events, or other events could have a significant

19

impact on a security or instrument. Such events could make identifying investment risks and opportunities especially difficult for the Adviser. In response to certain crises, the United States and other governments have taken steps to support financial markets. The withdrawal of this support or failure of efforts in response to a crisis could negatively affect financial markets generally as well as the value and liquidity of certain securities. In addition, policy and legislative changes in the United States and in other countries are changing many aspects of financial regulation. The impact of these changes on the markets, and the practical implications for market participants, may not be fully known for some time. The increasing interconnectivity between global economies and financial markets increases the likelihood that events or conditions in one region or financial market may adversely impact issuers in a different country, region or financial market.

Risks Associated with Investing in Equities. Equity securities, generally common stocks, preferred stocks and/or depositary receipts held by the Fund may experience sudden, unpredictable drops in value or long periods of decline in value. This may occur because of factors that affect the securities markets generally, such as adverse changes in economic or political conditions, the general outlook for corporate earnings, interest rates or investor sentiment. Sustained periods of market volatility, either globally or in any jurisdiction in which the Fund invests, may increase the risks associated with an investment in the Fund. Equity securities may also lose value because of factors affecting an entire industry or sector, such as increases in production costs or factors directly related to a specific company, such as decisions made by its management.

Common stock of an issuer in the Fund's portfolio may decline in price if the issuer fails to make anticipated dividend payments because, among other reasons, the issuer of the security experiences a decline in its financial condition. Common stock is subordinated to preferred stocks, bonds, and other debt instruments in a company's capital structure, in terms of priority with respect to corporate income, and therefore will be subject to greater dividend risk than preferred stocks or debt instruments of such issuers. In addition, while broad market measures of common stocks have historically generated higher average returns than fixed income securities, common stocks have also experienced significantly more volatility in those returns. Because preferred stock is generally junior to debt securities and other obligations of the issuer, deterioration in the credit quality of the issuer will cause greater changes in the value of a preferred stock than in a more senior debt security with similar stated yield characteristics.

Interest Rate Risk. As with most funds that invest in debt securities, changes in interest rates, including rates that fall below zero, are one of the most important factors that could affect the value of an investment in the Fund. Interest rate risk is the risk that debt securities will decline in value because of increases in interest rates. Any such change in interest rates may be sudden and significant, with unpredictable effects on the financial markets and the Fund's investments. Generally, bonds with longer maturities have a greater duration and thus are subject to greater price volatility from changes in interest rates. Adjustable rate instruments also react to interest rate changes in a similar manner although generally to a lesser degree (depending, however, on the characteristics of the reset terms, including the index chosen, frequency of reset and reset caps or floors, among other things). Low interest rates may pose heightened risks with respect to investments in fixed income securities. When interest rates rise from a low level, fixed income securities markets may experience lower prices, increased volatility, and lower liquidity. The negative impact on fixed income securities from rate increases, regardless of the cause, could be swift and significant, which could result in significant losses by the Fund, even if such rate increases

20

are anticipated by the portfolio managers. The Fund may be subject to heightened interest rate risk because the Federal Reserve has raised, and may continue to raise, interest rates. During periods of increasing interest rates the Fund may experience high redemptions and, as a result, increased portfolio turnover, which could increase the costs that the Fund incurs and may negatively impact the Fund's performance.

ARM Risk. During periods of extreme fluctuations in interest rates, the resulting fluctuations of ARM rates could affect the ARMs' market value. Most ARMs have annual reset limits or "caps." Fluctuations in interest rates above these levels, thus, could cause the mortgage-backed securities to "cap out" and to behave more like long-term, fixed-rate debt securities. During periods of declining interest rates, of course, the coupon rates may readjust downward and result in lower yields. Because of this feature, the value of ARMs will likely not rise during periods of declining interest rates to the same extent as fixed-rate instruments.

Credit Risk. Credit risk refers to the likelihood that an issuer will default on the payment of principal and/or interest on a security. Various factors could affect the issuer's actual or perceived willingness or ability to make timely interest or principal payments, including changes in the issuer's financial condition or in general economic conditions. In addition, lack of or inadequacy of collateral or credit enhancements for a fixed income security may affect its credit risk. Below investment grade securities have more risk with respect to the issuer's ability to pay interest and repay principal when due, and therefore involve a greater risk of default or nonpayment. Credit risk of a security may change over time. Ratings agencies periodically review certain securities and may downgrade a security that is held by the Fund. However, ratings are only opinions of the agencies issuing them and are not absolute guarantees as to quality.

Call Risk. Issuers of callable bonds are permitted to redeem these bonds before their final maturity. Issuers may call outstanding securities before maturity for a number of reasons, including decreases in prevailing interest rates or improvements to the issuer's credit profile. If an issuer calls a security in which the Fund is invested, the Fund could lose potential price appreciation and be forced to reinvest the proceeds in securities that bear a lower interest rate or more credit risk.

Risks Associated with Investing in Smaller-Cap and Mid-Cap Companies. The prices of securities of smaller-cap and mid-cap companies tend to fluctuate more widely than those of larger, more established companies. Smaller-cap and mid-cap companies may have limited product lines, markets or financial resources or may depend on the expertise of a few people and may be subject to more abrupt or erratic market movements than securities of larger, more established companies or market averages in general. In addition, these companies often have shorter operating histories and are more reliant on key products or personnel than larger companies. The securities of smaller- or medium-sized companies are often traded over-the-counter, and may not be traded in volumes typical of securities traded on a national securities exchange. Securities of such issuers may lack sufficient market liquidity to effect sales at an advantageous time or without a substantial drop in price.

Risks Associated with Investing in Non U.S. Securities. Non-U.S. investments involve special risks not present in U.S. investments that can increase the chances that the Fund will lose money.

21

Certain of the risks noted below may also apply to securities of U.S. issuers with significant non- U.S. operations. Investments in non-U.S. securities involve the following risks:

• The economies of some non-U.S. markets often do not compare favorably with that of the U.S. in areas such as growth of gross domestic product, reinvestment of capital, resources, and balance of payments. Some of these economies may rely heavily on particular industries or non-U.S. capital. They may be more vulnerable to adverse diplomatic developments, the imposition of economic sanctions against a country, changes in international trading patterns, trade barriers and other protectionist or retaliatory measures.

• Governmental actions—such as the imposition of capital controls, nationalization of companies or industries, expropriation of assets or the imposition of punitive taxes—may adversely affect investments in non-U.S. markets. Such governments may also participate to a significant degree, through ownership or regulation, in their respective economies.

• The governments of certain countries may prohibit or substantially restrict foreign investing in their capital markets or in certain industries. This could severely affect security prices. This could also impair the Fund's ability to purchase or sell non-U.S. securities or transfer its assets or income back to the U.S. or otherwise adversely affect the Fund's operations.

• Other non-U.S. market risks include foreign exchange controls, difficulties in pricing securities, defaults on non-U.S. government securities, difficulties in enforcing favorable legal judgments in non-U.S. courts, and political and social instability. Legal remedies available to investors in some non-U.S. countries are less extensive than those available to investors in the U.S. Many non-U.S. governments supervise and regulate stock exchanges, brokers, and the sale of securities to a lesser extent than the U.S. government does. Corporate governance may not be as robust as in more developed countries. As a result, protections for minority investors may not be strong, which could adversely affect the Fund's non-U.S. holdings or exposures.

• Accounting standards in other countries are not necessarily the same as in the U.S. If the accounting standards in another country do not require as much disclosure or detail as U.S. accounting standards, it may be harder for the portfolio managers to completely and accurately determine a company's financial condition or otherwise assess a company's creditworthiness.

• Because there may be fewer investors on non-U.S. exchanges and smaller numbers of shares traded each day, it may be difficult for the Fund to buy and sell securities on those exchanges. In addition, prices of non-U.S. securities may be more volatile than prices of securities traded in the U.S.

• Non-U.S. markets may have different clearance and settlement procedures. In certain markets, settlements may not keep pace with the volume of securities transactions. If this occurs, settlement may be delayed, and the Fund's assets may be uninvested and may not be earning returns. The Fund also may miss investment opportunities or not be able to sell an investment or reduce its exposure because of these delays.

22

• Changes in currency exchange rates will affect the value of the Fund's non-U.S. holdings or exposures.

• The costs of non-U.S. securities transactions tend to be higher than those of U.S. transactions, increasing the transaction costs paid directly or indirectly by the Fund.

• International trade barriers or economic sanctions against non-U.S. countries may adversely affect the Fund's non-U.S. holdings or exposures. Since January 20, 2025, the current U.S. administration has pursued an aggressive foreign policy agenda, including the imposition of tariffs, which may have unforeseen consequences on the United States' relations with foreign countries, the economy, and markets generally. In addition, the current administration has sought to reduce the size of the U.S. government by, for example, reducing the headcount of and freezing funding available to certain U.S. government agencies. Such efforts may continue throughout U.S. federal agencies, which could increase administrative burdens on remaining government employees, increase processing times of company filings, alter regulatory policymaking, and increase regulatory volatility. These, as well as other potential effects which are not currently known, may have a negative impact on the Fund or on markets generally.

• Global economies are increasingly interconnected, which increases the possibilities that conditions in one country region or financial market may adversely impact a different country, region, or financial market.

The severity or duration of these conditions may be affected if one or more countries leave the European Union or the euro currency or if other policy changes are made by governments or quasi- governmental organizations.

The Fund may invest in depositary receipts, including American Depositary Receipts ("ADRs"), European Depositary Receipts ("EDRs"), Global Depositary Receipts ("GDRs") and Global Depositary Notes ("GDNs"), which are certificates evidencing ownership of securities of a non-U.S. issuer. Depositary receipts may be sponsored by the non-U.S. issuer or unsponsored. Depositary receipts are subject to the risks of changes in currency or exchange rates and the risks of investing in non-U.S. securities that they evidence or into which they may be converted. The issuers of unsponsored depositary receipts are not obligated to disclose information that would be considered material in the U.S., or to pass through to shareholders any voting rights with respect to the deposited securities. Therefore, there may be less information available regarding these issuers, and there may not be a correlation between such information and the market value of the depositary receipts.

Risks Associated with Investing in Emerging Markets. In investing the Fund's assets, the portfolio managers focus on countries with established rules of law and political systems that allow for transparent and unbiased enforcement of those laws, although there can be no assurance that the Fund's assets will in all cases be invested in countries that offer such protections, and such investments may be subject to heightened risk. The Fund's investments in non-U.S. issuers in developing or emerging market countries may involve increased exposure to changes in economic, social, and political factors as compared to investments in more developed countries. The economies of most emerging market countries are in the early stage of capital market development and may

23