The information in this preliminary pricing supplement

is not complete and may be changed. This preliminary pricing supplement and the accompanying product supplement, underlying supplement,

prospectus supplement and prospectus are not an offer to sell these Notes and we are not soliciting an offer to buy these Notes in any

jurisdiction where the offer or sale is not permitted.

|

Subject to Completion, dated April 23, 2026

Pricing Supplement dated April , 2026

(To Product Supplement No. ELN-1 dated March 25, 2025,

Underlying Supplement No. ELN-1 dated March 25, 2025,

Prospectus Supplement dated March 25, 2025

and Prospectus dated March 25, 2025) |

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-285508

|

Bank of Montreal Trigger Autocallable Contingent Yield Notes

Linked to the Least Performing of the Nasdaq-100 Index®,

the Russell 2000® Index and the S&P 500® Index due on or about April 25, 2029

The Trigger Autocallable Contingent

Yield Notes (the “Notes”) are senior unsecured debt securities issued by Bank of Montreal (the “Issuer”)

linked to the least performing of the Nasdaq-100 Index®, the Russell 2000® Index and the S&P 500®

Index (each an “Underlier” and together the “Underliers”). On a quarterly basis, unless the Notes

have been previously called, the Issuer will pay you a coupon (the “Contingent Coupon”) if the Closing Value of each

Underlier on the applicable Coupon Observation Date is greater than or equal to its Coupon Barrier. However, if the Closing Value of any

Underlier on a Coupon Observation Date is less than its Coupon Barrier, you will not receive any Contingent Coupon for the relevant quarter.

If the Closing Value of each Underlier on any Call Observation Date is greater than or equal to its Closing Value on the Trade Date (the

“Initial Underlier Value”), the Notes will be automatically called, and the Issuer will pay you the Principal Amount

of the Notes plus a final Contingent Coupon, and no further payments will be made on the Notes. If the Notes are not automatically called

and the Closing Value of each Underlier on the Final Valuation Date (the “Final Underlier Value”) is greater than or

equal to its Downside Threshold, the Issuer will repay the Principal Amount at maturity plus any final Contingent Coupon otherwise due.

However, if the Final Underlier Value of any Underlier is less than its Downside Threshold, the Issuer will pay you a cash payment at

maturity that is less than the Principal Amount, if anything, resulting in a percentage loss on the Principal Amount of the Notes equal

to the negative Underlier Return of the Underlier with the lowest Underlier Return (the “Least Performing Underlier”).

In this case, you will have full downside exposure to the Least Performing Underlier from its Initial Underlier Value to its Final Underlier

Value, and will lose a significant portion, and possibly all, of your initial investment. Investing in the Notes involves significant

risks. You may lose a significant portion or all of your initial investment. You may receive few or no Contingent Coupons during the term

of the Notes. You will be exposed to the market risk of each Underlier and any decline in the value of one Underlier may negatively affect

your return and will not be offset or mitigated by a lesser decline or any potential increase in the value of any other Underlier. You

will not participate in any appreciation of any Underlier and will not receive any dividends on the securities included in any Underlier.

The Final Underlier Value of each Underlier is observed relative to its Downside Threshold only on the Final Valuation Date, and the contingent

repayment of principal feature applies only if you hold the Notes to maturity. Generally, the higher the Contingent Coupon Rate on a Note,

the greater the risk of loss on that Note. Any payment on the Notes, including any payment of the Principal Amount at maturity, is subject

to the credit of Bank of Montreal. If Bank of Montreal were to default on its payment obligations, you might not receive any amounts owed

to you under the Notes and you could lose your entire investment.

| q | Contingent Coupon: On each Contingent Coupon Payment Date, the Issuer will pay you a

Contingent Coupon if the Closing Value of each Underlier on the related Coupon Observation Date is greater than or equal to its Coupon

Barrier. However, if the Closing Value of any Underlier on any Coupon Observation Date is less than its Coupon Barrier, you will not receive

any Contingent Coupon on the related Contingent Coupon Payment Date. |

| q | Automatic Call: If the Closing Value of each Underlier on any Call Observation Date

is greater than or equal to its Initial Underlier Value, the Notes will be automatically called, and the Issuer will pay you the Principal

Amount of the Notes plus a final Contingent Coupon, and no further payments will be made on the Notes. |

| q | Downside Exposure with Contingent Repayment

of Principal at Maturity: If the Notes are not automatically called and the Final Underlier

Value of each Underlier is greater than or equal to its Downside Threshold, the Issuer will repay the Principal Amount at maturity plus

any final Contingent Coupon otherwise due. However, if the Final Underlier Value of any Underlier is less than its Downside Threshold,

the Issuer will repay less than the Principal Amount at maturity, if anything, resulting in a percentage loss on your investment equal

to the negative Underlier Return of the Least Performing Underlier. You may lose a significant portion or all of your initial investment.

Any payment on the Notes, including any payment of the Principal Amount at maturity, is subject to the credit of Bank of Montreal. |

| Trade Date: |

|

April 23, 2026 |

| Settlement Date: |

|

April 27, 2026 |

| Coupon Observation Dates2: |

|

Quarterly (see page PS-6) |

| Call Observation Dates2: |

|

Quarterly, beginning after six months (see page PS-6) |

| Final Valuation Date2: |

|

April 23, 2029 |

| Maturity Date2: |

|

April 25, 2029 |

| 1 | In the event that we make any changes to the expected Trade Date or Settlement Date, the other relevant

dates may be changed so that the stated term of the Notes remains the same. |

| 2 | Subject to postponement. See “Terms of the Notes” on page PS-5 of this pricing supplement. |

Notice to investors: The Notes are significantly

riskier than conventional debt instruments. The Issuer is not necessarily obligated to repay the full Principal Amount of the Notes at

maturity, and the Notes may have the full downside market risk of the Least Performing Underlier. This market risk is in addition to the

credit risk inherent in purchasing a debt obligation of the Issuer. You should not purchase the Notes if you do not understand or are

not comfortable with the significant risks involved in investing in the Notes.

You should carefully consider the risks described

under “Selected Risk Considerations” beginning on page PS-8 herein and “Risk Factors” beginning on page PS-5 of

the accompanying product supplement, page S-2 of the prospectus supplement and page 9 of the prospectus before purchasing any Notes. Events

relating to any of those risks, or other risks and uncertainties, could adversely affect the market value of, and the return on, your

Notes. You may lose a significant portion or all of your initial investment. The Notes will not be listed on any securities exchange.

We are offering Trigger Autocallable Contingent

Yield Notes linked to the least performing of the Nasdaq-100 Index®, the Russell 2000® Index and the

S&P 500® Index. The Contingent Coupon Rate and the Initial Underlier Value and corresponding Coupon Barrier and

Downside Threshold for each Underlier will be set on the Trade Date. The Initial Underlier Value of each Underlier will be its Closing

Value (as defined below) on the Trade Date. The Notes are offered at a minimum investment of $1,000 (100 Notes).

| Underlier |

Contingent

Coupon Rate |

Initial Underlier

Value |

Coupon Barrier* |

Downside Threshold* |

CUSIP/ ISIN |

| Nasdaq-100 Index® (NDX) |

At least 12.00% per annum |

|

75% of its Initial Underlier Value |

60% of its Initial Underlier Value |

063929640 / US0639296401 |

| Russell 2000® Index (RTY) |

|

75% of its Initial Underlier Value |

60% of its Initial Underlier Value |

| S&P 500® Index (SPX) |

|

75% of its Initial Underlier Value |

60% of its Initial Underlier Value |

|

*Rounded to two decimal places with respect to

the Nasdaq-100 Index® and S&P 500® Index and rounded to three decimal places with respect

to the Russell 2000® Index.

On the date of this preliminary pricing supplement,

the estimated initial value of the Notes is $9.97 per Note. The estimated initial value of the Notes at pricing may differ from this value

but will not be less than $9.67 per Note. However, as discussed in more detail in this pricing supplement, the actual value of the Notes

at any time will reflect many factors and cannot be predicted with accuracy. See “Estimated Value of the Notes” in this pricing

supplement.

The Notes are the unsecured obligations of

Bank of Montreal, and, accordingly, all payments on the Notes are subject to the credit risk of Bank of Montreal. If Bank of Montreal

defaults on its obligations, you could lose some or all of your investment. The Notes are not insured by the Federal Deposit Insurance

Corporation, the Deposit Insurance Fund, the Canada Deposit Insurance Corporation or any other governmental agency.

The Notes are not bail-inable notes and are

not subject to conversion into our common shares or the common shares of any of our affiliates under subsection 39.2(2.3) of the Canada

Deposit Insurance Corporation Act.

Neither the Securities and Exchange Commission

nor any state securities commission or other regulatory body has approved or disapproved of these Notes or passed upon the accuracy or

adequacy of this pricing supplement or the accompanying product supplement, underlying supplement, prospectus supplement and prospectus.

Any representation to the contrary is a criminal offense.

| |

Original Issue Price |

Underwriting Discount(1) |

Proceeds to Bank of Montreal |

| Per Note |

$10.00 |

$0.00 |

$10.00 |

| Total |

$ |

$ |

$ |

| (1) | BMO Capital Markets Corp. (“BMOCM”), our subsidiary, and UBS Financial Services Inc.

(“UBS”) are the agents for the distribution of the Notes. UBS has advised us that all sales of the Securities will

be made to certain fee-based advisory accounts for which UBS is an investment advisor at the Original Issue Price and UBS will not receive

a sales commission. See “Supplemental Plan of Distribution” in this pricing supplement for further information. |

| UBS Financial Services Inc. |

BMO Capital Markets |

| Estimated Value of the Notes |

Our estimated initial value of the Notes equals the sum of the values

of the following hypothetical components:

| · | a fixed-income debt component with the same tenor as the Notes, valued using

our internal funding rate for structured notes; and |

| · | one or more derivative transactions relating to the economic terms of the

Notes. |

The internal funding rate used in the determination of the initial estimated

value generally represents a discount from the credit spreads for our conventional fixed-rate debt. The value of these derivative transactions

is derived from our internal pricing models. These models are based on factors such as the traded market prices of comparable derivative

instruments and on other inputs, which include volatility, dividend rates, interest rates and other factors. As a result, the estimated

initial value of the Notes is based on market conditions at the time it is calculated.

For more information about the estimated initial value of the Notes,

see “Selected Risk Considerations” below.

| Additional Information About the Issuer and the Notes |

You should read this pricing supplement together

with product supplement no. ELN-1 dated March 25, 2025, underlying supplement no. ELN-1 dated March 25, 2025, the prospectus supplement

dated March 25, 2025 and the prospectus dated March 25, 2025 for additional information about the Notes. To the extent that disclosure

in this pricing supplement is inconsistent with the disclosure in the product supplement, underlying supplement, prospectus supplement

or prospectus, the disclosure in this pricing supplement will control. Certain defined terms used but not defined herein have the meanings

set forth in the product supplement, prospectus supplement or prospectus.

Our Central Index Key, or CIK, on the SEC website

is 927971. When we refer to “we,” “us” or “our” in this pricing supplement, we refer only to Bank

of Montreal.

You may access the product supplement, underlying

supplement, prospectus supplement and prospectus on the SEC website www.sec.gov as follows (or if such address has changed, by reviewing

our filings for the relevant date on the SEC website):

| · | Product Supplement No. ELN-1 dated March 25,

2025: |

https://www.sec.gov/Archives/edgar/data/927971/000121465925004723/o321252424b2.htm

| · | Underlying Supplement No. ELN-1 dated March 25,

2025: |

https://www.sec.gov/Archives/edgar/data/927971/000121465925004728/r321250424b2.htm

| · | Prospectus Supplement and Prospectus dated March

25, 2025: |

https://www.sec.gov/Archives/edgar/data/927971/000119312525062081/d840917d424b5.htm

The Notes may be appropriate for you if:

| ¨ | You fully understand the risks inherent in an

investment in the Notes, including the risk of loss of your entire investment. |

| ¨ | You can tolerate a loss of a significant portion

or all of your initial investment, and you are willing to make an investment that may have the full downside market risk of the Least

Performing Underlier. |

| ¨ | You are willing and able to accept the individual

market risk of each Underlier and understand that any decline in the value of one Underlier will not be offset or mitigated by a lesser

decline or any potential increase in the value of any other Underlier. |

| ¨ | You believe each Underlier is likely to close

at or above its Coupon Barrier on the specified Coupon Observation Dates, and, if any Underlier does not, you can tolerate receiving few

or no Contingent Coupons over the term of the Notes. |

| ¨ | You believe the Final Underlier Value of each

Underlier is not likely to be less than its Downside Threshold and, if the Final Underlier Value of any Underlier is less than its Downside

Threshold, you can tolerate a loss of a significant portion or all of your initial investment. |

| ¨ | You understand and accept that you will not participate

in any appreciation in the values of any Underlier and your potential return is limited to any Contingent Coupons paid on the Notes. |

| ¨ | You would be willing to invest in the Notes if

the Contingent Coupon Rate were set equal to the lowest possible Contingent Coupon Rate specified on the cover of this pricing supplement

(the actual Contingent Coupon Rate will be set on the Trade Date). |

| ¨ | You can tolerate fluctuations in the price of

the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the values of the Underliers. |

| ¨ | You do not seek guaranteed current income from

this investment, you are willing to accept the risk of contingent yield and you are willing to forgo any dividends paid on the securities

included in the Underliers. |

| ¨ | You are willing to invest in Notes that may be

automatically called early and you are otherwise willing to hold the Notes to maturity and accept that there may be little or no secondary

market for the Notes. |

| ¨ | You understand and are willing to accept the

risks associated with each Underlier. |

| ¨ | You

are willing and able to assume the credit risk of Bank of Montreal, as Issuer of the Notes, for all payments under the Notes and you

understand that, if Bank of Montreal defaults on its obligations, you might not receive any amounts due to you, including any payment

of the Principal Amount at maturity. |

The Notes may not be appropriate

for you if:

| ¨ | You do not fully understand the risks inherent

in an investment in the Notes, including the risk of loss of your entire investment. |

| ¨ | You cannot tolerate the loss of a significant

portion or all of your initial investment, or you are not willing to make an investment that may have the full downside market risk of

the Least Performing Underlier. |

| ¨ | You are unwilling or unable to accept the individual

market risk of each Underlier or do not understand that any decline in the value of one Underlier will not be offset or mitigated by a

lesser decline or any potential increase in the value of any other Underlier. |

| ¨ | You do not believe each Underlier is likely to

close at or above its Coupon Barrier on the specified Coupon Observation Dates, or you cannot tolerate receiving few or no Contingent

Coupons over the term of the Notes. |

| ¨ | You believe at least one Underlier will depreciate

over the term of the Notes and its Final Underlier Value is likely to be less than its Downside Threshold. |

| ¨ | You seek an investment that participates in the

full appreciation of the Underliers and whose return is not limited to any Contingent Coupons paid on the Notes. |

| ¨ | You would be unwilling to invest in the Notes

if the Contingent Coupon Rate were set equal to the lowest possible Contingent Coupon Rate specified on the cover of this pricing supplement

(the actual Contingent Coupon Rate will be set on the Trade Date). |

| ¨ | You cannot tolerate fluctuations in the price

of the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the values of the Underliers. |

| ¨ | You seek guaranteed current income from your

investment, you are unwilling to accept the risk of contingent yield or you would prefer to receive any dividends paid on the securities

included in the Underliers. |

| ¨ | You are unable or unwilling to hold Notes that

may be automatically called early, or you are otherwise unable or unwilling to hold the Notes to maturity, or you seek an investment for

which there will be an active secondary market. |

| ¨ | You do not understand or are not willing to accept

the risks associated with each Underlier. |

| ¨ | You prefer the lower risk, and therefore accept

the potentially lower returns, of fixed income investments with comparable maturities and credit ratings that bear interest at a prevailing

market rate. |

| ¨ | You are unwilling or unable to assume the credit

risk of Bank of Montreal, as Issuer of the Notes, for all payments under the Notes, including any payment of the Principal Amount at maturity. |

The considerations identified

above are not exhaustive. Whether or not the Notes are an appropriate investment for you will depend on your individual circumstances,

and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully

considered the appropriateness of an investment in the Notes in light of your particular circumstances. You should also review carefully

the sections titled “Selected Risk Considerations” herein and “Risk Factors” in the accompanying product supplement

for risks related to an investment in the Notes. For more information about the Underliers, please see the sections titled “The

Nasdaq-100 Index®,” “The Russell 2000® Index” and “The S&P 500® Index”

below.

| Issuer: |

Bank of Montreal |

| Original Issue Price: |

100% of the Principal Amount of Notes |

| Principal Amount: |

$10 per Note |

| Underliers: |

The Nasdaq-100 Index® (Bloomberg ticker symbol: NDX), the Russell 2000® Index (Bloomberg ticker symbol: RTY) and the S&P 500® Index (Bloomberg ticker symbol: SPX) |

| Term: |

Approximately 3 years, unless automatically called earlier |

| Automatic Call Feature: |

If the Closing Value of each Underlier on any Call Observation Date is greater than or equal to its Initial Underlier Value, the Notes will be automatically called, and the Issuer will pay you the Principal Amount of the Notes plus the Contingent Coupon due on the Contingent Coupon Payment Date that is also the Call Settlement Date, and no further payments will be made on the Notes. |

| Contingent Coupon: |

If the Closing Value of each Underlier is greater

than or equal to its Coupon Barrier on any Coupon Observation Date, the Issuer will pay you a Contingent Coupon on the related Contingent

Coupon Payment Date.

If the Closing Value of any Underlier is less

than its Coupon Barrier on any Coupon Observation Date, the Contingent Coupon applicable to that Coupon Observation Date will not

accrue or be payable and the Issuer will not make any payment to you on the related Contingent Coupon Payment Date.

The Contingent Coupon is a fixed amount based upon

equal quarterly installments at the Contingent Coupon Rate. |

Contingent Coupon

Rate: |

At least 12.00% per annum (to be set on the Trade Date). Accordingly, the Contingent Coupon with respect to each Coupon Observation Date will be equal to at least $0.30 per Note. Whether Contingent Coupons will be paid on the Notes will depend on the performance of the Underliers. |

Coupon Observation

Dates: |

Quarterly. See “Coupon Observation Dates/Call Observation Dates/Contingent Coupon Payment Dates/Call Settlement Dates” below. |

Contingent Coupon

Payment Dates: |

Quarterly. See “Coupon Observation Dates/Call Observation Dates/Contingent Coupon Payment Dates/Call Settlement Dates” below. |

| Call Observation Dates: |

Quarterly, beginning approximately six months after the Settlement Date, on the Coupon Observation Dates scheduled to occur from October 2026 to January 2029, inclusive. |

| Call Settlement Date: |

The Contingent Coupon Payment Date immediately following the applicable Call Observation Date, if applicable. See “Coupon Observation Dates/Call Observation Dates/Contingent Coupon Payment Dates/Call Settlement Dates” below. |

| Payment at Maturity: |

If the Notes are not automatically called, on the

Maturity Date, you will receive from the Issuer a cash payment per Note calculated as follows:

· If

the Final Underlier Value of each Underlier is greater than or equal to both its Downside Threshold and its Coupon Barrier, the Issuer

will repay the Principal Amount at maturity of $10 per Note plus the Contingent Coupon due on the Contingent Coupon Payment Date

that is also the Maturity Date.

· If

the Final Underlier Value of each Underlier is greater than or equal to its Downside Threshold but the Final Underlier Value of any Underlier

is less than its Coupon Barrier, the Issuer will repay the Principal Amount at maturity of $10 per Note, but no Contingent Coupon

will be paid.

· If

the Final Underlier Value of any Underlier is less than its Downside Threshold, the Issuer will repay less than the Principal Amount

at maturity, if anything, resulting in a percentage loss on your investment equal to the negative Underlier Return of the Least Performing

Underlier. Accordingly, the payment at maturity per Note would be calculated as follows:

$10 + ($10 × Underlier Return of the Least

Performing Underlier)

If the Notes are not automatically called

and the Final Underlier Value of any Underlier is less than its Downside Threshold, your investment is fully exposed to the decline in

the Least Performing Underlier, and you will lose a significant portion or all of your initial investment at maturity. |

| Underlier Return: |

With respect to each Underlier:

Final Underlier Value – Initial Underlier

Value

Initial Underlier Value |

Least Performing

Underlier: |

The Underlier with the lowest Underlier Return |

| Initial Underlier Value: |

With respect to each Underlier, its Closing Value on the Trade Date, as specified on the cover of this pricing supplement |

| Final Underlier Value: |

With respect to each Underlier, its Closing Value on the Final Valuation Date |

| Closing Value: |

With respect to each Underlier, Closing Value has the meaning assigned to “Closing Level” set forth under “General Terms of the Notes—Certain Terms for Notes Linked to an Index—Certain Definitions” in the accompanying product supplement. |

| Coupon Barrier: |

With respect to each Underlier, 75% of its Initial Underlier Value, as specified on the cover of this pricing supplement |

| Downside Threshold: |

With respect to each Underlier, 60% of its Initial Underlier Value, as specified on the cover of this pricing supplement |

| Calculation Agent: |

BMO Capital Markets Corp. (“BMOCM”) |

Market Disruption

Events and

Postponement

Provisions: |

Each Coupon Observation Date (including the Final

Valuation Date) and each call Observation Date is subject to postponement due to non-scheduled trading days and the occurrence of a market

disruption event. In addition, a Contingent Coupon Payment Date, a Call Settlement Date and/or the Maturity Date, as applicable, will

be postponed if the immediately preceding Coupon Observation Date or Call Observation Date, as applicable, is postponed and will be adjusted

for non-business days.

For more information regarding adjustments to the

Coupon Observation Dates, the Call Observation Dates, the Contingent Coupon Payment Dates, the Call Settlement Dates and the Maturity

Date, see “General Terms of the Notes—Consequences of a Market Disruption Event; Postponement of a Valuation Date—Notes

Linked to Multiple Underliers” and “—Payment Dates” in the accompanying product supplement. For purposes of the

accompanying product supplement, each Coupon Observation Date, the Final Valuation Date and each Call Observation Date is a “Valuation

Date” and each Contingent Coupon Payment Date, Call Settlement Date and the Maturity Date is a “Payment Date.” In addition,

for information regarding the circumstances that may result in a market disruption event, see “General Terms of the Notes—Certain

Terms for Notes Linked to an Index—Market Disruption Events” in the accompanying product supplement. |

|

Coupon Observation Dates/Call Observation Dates/Contingent Coupon Payment

Dates/Call Settlement Dates |

| Coupon Observation Dates/Call Observation Dates* |

Contingent Coupon Payment Dates/Call Settlement Dates* |

| July 23, 2026 |

July 27, 2026 |

| October 23, 2026 |

October 27, 2026 |

| January 25, 2027 |

January 27, 2027 |

| April 23, 2027 |

April 27, 2027 |

| July 23, 2027 |

July 27, 2027 |

| October 25, 2027 |

October 27, 2027 |

| January 24, 2028 |

January 26, 2028 |

| April 24, 2028 |

April 26, 2028 |

| July 24, 2028 |

July 26, 2028 |

| October 23, 2028 |

October 25, 2028 |

| January 23, 2029 |

January 25, 2029 |

| April 23, 2029 (the Final Valuation Date) |

April 25, 2029 (the Maturity Date) |

* Each Coupon Observation Date (other than the Final Valuation Date),

starting from the second Coupon Observation Date, which is October 23, 2026, is a Call Observation Date. Thus, the first possible Call

Settlement Date will be October 27, 2026.

| |

Trade Date: |

|

The Initial Underlier Value of each Underlier is observed, the Contingent Coupon Rate is set and the Coupon Barrier and Downside Threshold of each Underlier are determined. |

| |

|

|

|

| |

Coupon

Observation

Dates/Call

Observation

Dates (beginning

after six months): |

|

If the Closing Value of each Underlier is greater

than or equal to its Coupon Barrier on any Coupon Observation Date, the Issuer will pay you a Contingent Coupon on the related Contingent

Coupon Payment Date.

However, if the Closing Value of any Underlier

is less than its Coupon Barrier on any Coupon Observation Date, no Contingent Coupon payment will be made on the related Contingent Coupon

Payment Date.

In addition, if the Closing Value of each Underlier

on any Call Observation Date is greater than or equal to its Initial Underlier Value, the Notes will be automatically called, and the

Issuer will pay you the Principal Amount of the Notes plus a final Contingent Coupon, and no further payments will be made on the Notes.

|

| |

|

|

|

| |

Maturity Date: |

|

If the Notes are not automatically called, the

Final Underlier Value of each Underlier is observed and the Underlier Return of each Underlier is determined on the Final Valuation Date.

If the Final Underlier Value of each Underlier

is greater than or equal to both its Downside Threshold and its Coupon Barrier, the Issuer will repay the Principal Amount at maturity

of $10 per Note plus the Contingent Coupon due on the Contingent Coupon Payment Date that is also the Maturity Date.

If the Final Underlier Value of each Underlier

is greater than or equal to its Downside Threshold but the Final Underlier Value of any Underlier is less than its Coupon Barrier,

the Issuer will repay the Principal Amount at maturity of $10 per Note, but no Contingent Coupon will be paid.

If the Final Underlier Value of any Underlier

is less than its Downside Threshold, the Issuer will repay less than the Principal Amount at maturity, if anything, resulting in a

percentage loss on your investment equal to the negative Underlier Return of the Least Performing Underlier. Accordingly, the payment

at maturity per Note would be calculated as follows:

$10 + ($10 × Underlier Return of the Least

Performing Underlier)

If the Notes are not automatically called

and the Final Underlier Value of any Underlier is less than its Downside Threshold, your investment is fully exposed to the decline in

the Least Performing Underlier, and you will lose a significant portion or all of your initial investment at maturity.

|

Investing in the Notes

involves significant risks. You may receive few or no Contingent Coupons during the term of the Notes. You may lose a significant portion

or all of your investment. You will be exposed to the market risk of each Underlier and any decline in the value of one Underlier may

negatively affect your return and will not be offset or mitigated by a lesser decline or any potential increase in the value of any other

Underlier. The Final Underlier Value of each Underlier is observed relative to its Downside Threshold only on the Final Valuation Date,

and the contingent repayment of principal feature applies only if you hold the Notes to maturity. Generally, the higher the Contingent

Coupon Rate on a Note, the greater the risk of loss on that Note. Your return potential on the Notes is limited to any Contingent Coupons

paid on the Notes, and you will not participate in any appreciation of any Underlier. Any payment on the Notes, including any payment

of the Principal Amount at maturity, is subject to the creditworthiness of the Issuer. If Bank of Montreal were to default on its payment

obligations, you might not receive any amounts owed to you under the Notes and you could lose your entire investment.

|

Selected Risk Considerations |

The Notes involve risks not associated with an

investment in conventional debt securities. Some of the risks that apply to an investment in the Notes are summarized below, but we urge

you to read the more detailed explanation of the risks relating to the Notes generally in the “Risk Factors” section of the

accompanying product supplement and prospectus supplement. You should reach an investment decision only after you have carefully considered

with your advisors the appropriateness of an investment in the Notes in light of your particular circumstances.

Risks Relating To The Notes Generally

If The Notes Are Not Automatically Called Prior

To Maturity, You May Lose Some Or All Of The Principal Amount Of Your Notes At Maturity.

We will not repay you a fixed amount on the Notes

at maturity. If the Notes are not automatically called prior to maturity, you will receive a payment at maturity that will be equal to

or less than the Principal Amount, depending on the ending value of the Least Performing Underlier.

If the Final Underlier Value of the Least Performing

Underlier is less than its Downside Threshold, the payment at maturity will be less than the Principal Amount, you will have full downside

exposure to the decrease in the value of the Least Performing Underlier from its Initial Underlier Value, and you will lose 1% of the

Principal Amount for every 1% that the Final Underlier Value of the Least Performing Underlier is less than its Initial Underlier Value.

As a result, if the Final Underlier Value of the Least Performing Underlier is less than its Downside Threshold, you will lose a significant

portion, and possibly all, of the Principal Amount per Note at maturity. This is the case even if the value of the Least Performing Underlier

is greater than or equal to its Initial Underlier Value or its Downside Threshold at certain times during the term of the Notes.

Even if the Final Underlier Value of the Least

Performing Underlier is greater than its Downside Threshold, the payment at maturity will not exceed the Principal Amount (and any Contingent

Coupon otherwise due), and your yield on the Notes, taking into account any Contingent Coupons you may have received during the term of

the Notes, may be less than the yield you would earn if you bought a traditional interest-bearing debt security of Bank of Montreal or

another issuer with a similar credit rating with the same Maturity Date.

The Notes Do Not Provide For Fixed Payments

Of Interest And You May Receive No Contingent Coupons On One Or More Contingent Coupon Payment Dates, Or Even Throughout The Entire Term

Of The Notes.

On each Contingent Coupon Payment Date you will

receive a Contingent Coupon payment if, and only if, the Closing Value of each Underlier on the related Coupon Observation Date

is greater than or equal to its Coupon Barrier. If the Closing Value of any Underlier on any Coupon Observation Date is less than its

Coupon Barrier, you will not receive any Contingent Coupon payment on the related Contingent Coupon Payment Date. Furthermore, if the

Closing Value of any Underlier is less than its Coupon Barrier on each Coupon Observation Date over the term of the Notes, you will not

receive any Contingent Coupons over the entire term of the Notes.

The Notes Are Subject To The Full Risks Of Each

Underlier And Will Be Negatively Affected If Any Underlier Performs Poorly, Even If The Other Underliers Perform Favorably.

You are subject to the full risks of each Underlier.

If any Underlier performs poorly, you will be negatively affected, even if the other Underliers perform favorably. The Notes are not linked

to a basket composed of the Underliers, where the better performance of some Underliers could offset the poor performance of others. Instead,

you are subject to the full risks of each Underlier on each Coupon Observation Date. Furthermore, the risk that you will not receive one

or more, or any, Contingent Coupons during the term of the Notes and that you will lose a substantial portion, and possibly all, of the

Principal Amount at maturity is greater if you invest in the Notes as opposed to substantially similar securities that are linked to the

performance of a single Underlier. You should not invest in the Notes unless you understand and are willing to accept the full downside

risks of each Underlier.

You Will Not Benefit In Any Way From The Performance

Of The Better Performing Underliers.

Although it is necessary for each Underlier to

close at or above its respective Coupon Barrier on the relevant Coupon Observation Date in order for you to receive a Contingent Coupon

payment and at or above its respective Downside Threshold on the Final Valuation Date for you to receive the Principal Amount of your

Notes at maturity, you will not benefit in any way from the performance of the better performing Underliers. The Notes may underperform

an alternative investment linked to a basket composed of the Underliers, since in such case the performance of the Underliers would be

blended and the better performing Underliers could offset the poor performance of other Underliers.

You Will Be Subject To Risks Resulting From

The Relationship Among The Underliers.

It is preferable from your perspective for the

Underliers to be correlated with each other so that their values will tend to increase or decrease at similar times and by similar magnitudes.

By investing in the Notes, you assume the risk that the Underliers will not exhibit this relationship. The less correlated the Underliers,

the more likely it is that one of the Underliers will be performing poorly at any time over the term of the Notes. All that is necessary

for the Notes to perform poorly is for one of the Underliers to perform poorly; the performance of the better performing Underliers is

not relevant to your return on the Notes. It is impossible to predict what the relationship among the Underliers will be over the term

of the Notes. To the extent the Underliers represent a different equity market, such equity markets may not perform similarly over the

term of the Notes.

You May Be Fully Exposed To The Decline In The

Least Performing Underlier On The Final Valuation Date From Its Initial Underlier Value, But Will Not Participate In Any Positive Performance

Of Any Underlier.

Even though you will be fully exposed to a decline

in the value of the Least Performing Underlier if its Final Underlier Value is below its Downside Threshold, you will not participate

in any increase in the value of any Underlier over the term of the Notes. Your maximum possible return on the Notes will be limited to

the sum of the Contingent Coupons you receive, if any. Consequently, your return on the Notes may be significantly less than the return

you could achieve on an alternative investment that provides for participation in an increase in the value of any or each Underlier.

Contingent Repayment Of Your Initial Investment

Applies Only If You Hold The Notes To Maturity.

You should be willing to hold your Notes to maturity.

If you are able to sell your Notes prior to maturity in the secondary market, you may have to sell them at a substantial loss relative

to your initial investment, even if the value of any or each of the Underliers is greater than its Downside Threshold at the time of such

sale.

A Higher Contingent Coupon Rate And/Or A Lower

Coupon Barrier And/Or Downside Threshold Are Associated With Greater Risk.

The Notes offer Contingent Coupons at a higher

rate, if paid, than the fixed rate we would pay on conventional debt securities of the same maturity. These higher potential Contingent

Coupons are associated with greater levels of expected risk as of the Trade Date as compared to conventional debt securities, including

the risk that you may not receive a Contingent Coupon on one or more, or any, Contingent Coupon Payment Dates and the risk that you may

lose a substantial portion, and possibly all, of the Principal Amount at maturity. The volatility of the Underliers and the correlation

among the Underliers are important factors affecting this risk. Volatility is a measurement of the size and frequency of daily fluctuations

in the value of an Underlier, typically observed over a specified period of time. Volatility can be measured in a variety of ways, including

on a historical basis or on an expected basis as implied by option prices in the market. Correlation is a measurement of the extent to

which the values of the Underliers tend to fluctuate at the same time, in the same direction and in similar magnitudes. Greater expected

volatility of the Underliers or lower expected correlation among the Underliers as of the Trade Date may result in a higher Contingent

Coupon Rate and/or a lower Coupon Barrier and/or a lower Downside Threshold, but it also represents a greater expected likelihood as of

the Trade Date that the Closing Value of at least one Underlier will be less than its Coupon Barrier on one or more Coupon Observation

Dates, such that you will not receive one or more, or any, Contingent Coupons during the term of the Notes, and that the Closing Value

of at least one Underlier will be less than its Downside Threshold on the Final Valuation Date such that you will lose a substantial portion,

and possibly all, of the Principal Amount at maturity. In general, the higher the Contingent Coupon Rate is relative to the fixed rate

we would pay on conventional debt securities, the greater the expected risk that you will not receive one or more, or any, Contingent

Coupons during the term of the Notes and that you will lose a substantial portion, and possibly all, of the Principal Amount at maturity.

On the other hand, a lower Coupon Barrier or Downside Threshold does not necessarily indicate that the Notes have a greater likelihood

of paying Contingent Coupons or returning your principal at maturity.

You Will Be Subject To Reinvestment Risk.

If your Notes are automatically called, the term

of the Notes may be reduced. There is no guarantee that you would be able to reinvest the proceeds from an investment in the Notes at

a comparable return for a similar level of risk in the event the Notes are automatically called prior to maturity.

The Notes Are Subject To Credit Risk.

The Notes are our obligations and are not, either

directly or indirectly, an obligation of any third party. Any amounts payable under the Notes are subject to our creditworthiness and

you will have no ability to pursue any securities included in any Underlier for payment. As a result, our actual and perceived creditworthiness

may affect the value of the Notes and, in the event we were to default on our obligations under the Notes, you may not receive any amounts

owed to you under the terms of the Notes and you could lose your entire investment.

The U.S. Federal Income Tax Consequences Of

An Investment In The Notes Are Unclear.

There is no direct legal authority regarding the

proper U.S. federal income tax treatment of the Notes, and significant aspects of the tax treatment of the Notes are uncertain. Moreover,

non-U.S. investors should note that we intend to withhold on any coupon paid to a non-U.S. investor, generally at a rate of 30%. We will

not pay any additional amounts in respect of such withholding. You should review carefully the section entitled “United States Federal

Income Tax Considerations” herein, in combination with the section entitled “United States Federal Income Tax Considerations”

in the accompanying product supplement, and consult your tax advisor regarding the U.S. federal income tax consequences of an investment

in the Notes.

The Maturity Date Will Be Postponed If The Final

Valuation Date Is Postponed.

The Final Valuation Date will be postponed if the

originally scheduled Final Valuation Date is not a scheduled trading day or if the calculation agent determines that a market disruption

event has occurred or is continuing on the Final Valuation Date. If such a postponement occurs, the Maturity Date will be postponed. See

“General Terms of the Notes—Consequences of a Market Disruption Event; Postponement of a Valuation Date—Notes Linked

to Multiple Underliers” and “—Payment Dates” in the accompanying product supplement.

Risks

Relating To The Estimated Value Of The Notes And Any Secondary Market

The Estimated Value Of The Notes On The Trade

Date, Based On Our Proprietary Pricing Models, Will Be Less Than The Original Issue Price.

Our initial estimated value of the Notes is

only an estimate, and is based on a number of factors. The Original Issue Price of the Notes may exceed our initial estimated value, because

costs associated with offering, structuring and hedging the Notes are included in the Original Issue Price, but are not included in the

estimated value. These costs will include any underwriting discount and selling concessions and the cost of hedging our obligations under

the Notes through one or more hedge counterparties (which may be one or more of our affiliates). Such hedging cost includes our or our

hedge counterparty’s expected cost of providing such hedge, as well as the profit we or our hedge counterparty expect to realize

in consideration for assuming the risks inherent in providing such hedge.

The Terms Of The Notes Are Not Determined By

Reference To The Credit Spreads For Our Conventional Fixed-Rate Debt.

To determine the terms of the Notes, we use an

internal funding rate that represents a discount from the credit spreads for our conventional fixed-rate debt. As a result, the terms

of the Notes are less favorable to you than if we had used a higher funding rate.

The Estimated Value Of The Notes Is Not An Indication

Of The Price, If Any, At Which We, BMOCM Or Any Other Person May Be Willing To Buy The Notes From You In The Secondary Market.

Our initial estimated value of the Notes is

derived using our internal pricing models. This value is based on market conditions and other relevant factors, which include volatility

and correlation of the Underliers, dividend rates and interest rates. Different pricing models and assumptions, including those used by

other market participants, could provide values for the Notes that are greater than or less than our initial estimated value. In addition,

market conditions and other relevant factors after the Trade Date are expected to change, possibly rapidly, and our assumptions may prove

to be incorrect. After the Trade Date, the value of the Notes could change dramatically due to changes in market conditions, our creditworthiness,

and the other factors discussed in the next risk factor. These changes are likely to impact the price, if any, at which we, BMOCM or any

other party would be willing to purchase the Notes from you in any secondary market transactions. Our initial estimated value does not

represent a minimum price at which we, BMOCM or any other party would be willing to buy your Notes in any secondary market at any time.

For a period of approximately 1 month following

issuance of the Notes, the price, if any, at which we or our affiliates would be willing to buy the Notes from investors, and the value

that BMOCM may also publish for the Notes through one or more financial information vendors and which could be indicated for the Notes

on any brokerage account statements, will reflect a temporary upward adjustment from our estimated value of the Notes that would otherwise

be determined and applicable at that time. This temporary upward adjustment represents a portion of (a) the hedging profit that we or

our affiliates expect to realize over the term of the Notes and (b) any underwriting discount and selling concessions paid in connection

with this offering. The amount of this temporary upward adjustment will decline to zero on a straight-line basis over the 1-month period.

The Value Of The Notes Prior To Maturity Will

Be Affected By Numerous Factors, Some Of Which Are Related In Complex Ways.

The payout on the Notes could be replicated by

a hypothetical combination of financial instruments consisting of a fixed-income debt component and one or more derivative transactions.

As a result, the factors that influence the values of fixed-income bonds and derivative instruments will also influence the terms of the

Notes at issuance and the value of the Notes prior to maturity. The value of the Notes prior to maturity will be affected by the then-current

value of each Underlier, interest rates at that time and a number of other factors, some of which are interrelated in complex ways. The

effect of any one factor may be offset or magnified by the effect of another factor. The following factors, which are described in more

detail in the accompanying product supplement, are expected to affect the value of the Notes: performance of the Underliers; interest

rates; volatility of the Underliers; correlation among the Underliers; time remaining to maturity; and dividend yields on the securities

included in the Underliers. When we refer to the “value” of your Notes, we mean the value you could receive for your

Notes if you are able to sell them in the open market before the Maturity Date.

In addition to these factors, the value of the

Notes will be affected by actual or anticipated changes in our creditworthiness. You should understand that the impact of one of the factors

specified above, such as a change in interest rates, may offset some or all of any change in the value of the Notes attributable to another

factor, such as a change in the value of any or all of the Underliers. Because numerous factors are expected to affect the value of the

Notes, changes in the values of the Underliers may not result in a comparable change in the value of the Notes.

The Notes Will Not Be Listed On Any Securities

Exchange And We Do Not Expect A Trading Market For The Notes To Develop.

The Notes will not be listed or displayed on any

securities exchange. Although BMOCM and/or its affiliates intend to make a secondary market in relation to the Notes, they are not obligated

to do so. There can be no assurance that a secondary market will develop. Because we do not expect that any market makers will participate

in a secondary market for the Notes, the price at which you may be able to sell your Notes is likely to depend on the price, if any, at

which BMOCM is willing to buy your Notes. If a secondary market does exist, it may be limited. Accordingly, there may be a limited number

of buyers if you decide to sell your Notes prior to maturity. This may affect the price you receive upon such sale. Consequently, you

should be willing to hold the Notes to maturity.

Risks Relating To The Underliers

Any Payments On The Notes And Whether The Notes

Are Automatically Called Will Depend Upon The Performance Of The Underliers And Therefore The Notes Are Subject To The Following Risks,

Each As Discussed In More Detail In The Accompanying Product Supplement.

| · | Investing In The Notes Is Not The Same As

Investing In The Underliers. Investing in the Notes is not equivalent to investing in the Underliers. As an investor in the Notes,

your return will not reflect the return you would realize if you actually owned and held the securities included in each Underlier for

a period similar to the term of the Notes because you will not receive any dividend payments, distributions or any other payments paid

on those securities. As a holder of the Notes, you will not have any voting rights or any other rights that holders of the securities

included in the Underliers would have. |

| · | Historical Values Of The Underliers Should

Not Be Taken As An Indication Of The Future Performance Of The Underliers During The Term Of The Notes. |

| · | Changes That Affect The Underliers May Adversely

Affect The Value Of The Notes And Any Payments On The Notes. |

| · | We Cannot Control Actions By Any Of The Unaffiliated

Companies Whose Securities Are Included In The Underliers. |

| · | We And Our Affiliates Have No Affiliation

With Any Index Sponsor And Have Not Independently Verified Their Public Disclosure Of Information. |

The Notes Are Subject To Risks Relating To Non-U.S.

Securities With Respect To The Nasdaq-100 Index®.

Because some of the equity securities composing

the Nasdaq-100 Index® are issued by non-U.S. issuers, an investment in the Notes involves risks associated with the

home countries of those issuers. The prices of securities of non-U.S. companies may be affected by political, economic, financial and

social factors in those countries, or global regions, including changes in government, economic and fiscal policies and currency exchange

laws.

The Notes Are Subject To Small-Capitalization

Companies Risk With Respect To The Russell 2000® Index.

The Russell 2000® Index tracks

securities issued by companies with relatively small market capitalizations. These companies often have greater stock price volatility,

lower trading volume and less liquidity than large-capitalization companies. As a result, the value of the Russell 2000® Index

may be more volatile than that of a market measure that does not track solely small-capitalization stocks. Stock prices of small-capitalization

companies are also generally more vulnerable than those of large-capitalization companies to adverse business and economic developments,

and the stocks of small-capitalization companies may be thinly traded and may be less attractive to many investors if they do not pay

dividends. In addition, small-capitalization companies are often less well-established and less stable financially than large-capitalization

companies and may depend on a small number of key personnel, making them more vulnerable to loss of personnel. Small-capitalization companies

are often subject to less analyst coverage and may be in early, and less predictable, periods of their corporate existences. Small-capitalization

companies tend to have lower revenues, less diverse product lines, smaller shares of their target markets, fewer financial resources and

fewer competitive strengths than large-capitalization companies. These companies may also be more susceptible to adverse developments

related to their products or services.

Risks Relating To Conflicts Of Interest

Our Economic Interests And Those Of Any Dealer

Participating In The Offering Are Potentially Adverse To Your Interests.

You should be aware of the following ways in which

our economic interests and those of any dealer participating in the distribution of the Notes, which we refer to as a “participating

dealer,” are potentially adverse to your interests as an investor in the Notes. In engaging in certain of the activities described

below and as discussed in more detail in the accompanying product supplement, our affiliates or any participating dealer or its affiliates

may take actions that may adversely affect the value of and your return on the Notes, and in so doing they will have no obligation to

consider your interests as an investor in the Notes. Our affiliates or any participating dealer or its affiliates may realize a profit

from these activities even if investors do not receive a favorable investment return on the Notes.

| · | The calculation agent is our affiliate

and may be required to make discretionary judgments that affect the return you receive on the Notes. BMOCM, which is our affiliate,

will be the calculation agent for the Notes. As calculation agent, BMOCM will determine any values of the Underliers and make any other

determinations necessary to calculate any payments on the Notes. In making these determinations, BMOCM may be required to make discretionary

judgments that may adversely affect any payments on the Notes. See the sections entitled “General Terms of the Notes—Certain

Terms for Notes Linked to an Index—Market Disruption Events” and “—Discontinuation of, or Adjustments to, an Index”

in the accompanying product supplement. In making these discretionary judgments, the fact that BMOCM is our affiliate may cause it to

have economic interests that are adverse to your interests as an investor in the Notes, and BMOCM’s determinations as calculation

agent may adversely affect your return on the Notes. |

| · | The estimated value of the Notes was calculated

by us and is therefore not an independent third-party valuation. |

| · | Research reports by our affiliates or any

participating dealer or its affiliates may be inconsistent with an investment in the Notes and may adversely affect the values of the

Underliers. |

| · | Business activities of our affiliates or

any participating dealer or its affiliates with the companies whose securities are included in the Underliers may adversely affect the

values of the Underliers. |

| · | Hedging activities by our affiliates or

any participating dealer or its affiliates may adversely affect the values of the Underliers. |

| · | Trading activities by our affiliates or

any participating dealer or its affiliates may adversely affect the values of the Underliers. |

| · | A participating dealer or its affiliates

may realize hedging profits projected by its proprietary pricing models in addition to any selling concession and/or fee, creating a further

incentive for the participating dealer to sell the Notes to you. |

Hypothetical terms only. Actual terms may vary.

See the cover page for actual offering terms.

The examples below illustrate the payment upon

an automatic call or at maturity for a $10 Principal Amount Note on a hypothetical offering of Notes under various scenarios, with the

assumptions set forth in the table below. The terms used for purposes of these hypothetical examples do not represent the actual Contingent

Coupon Rate, Contingent Coupon, Initial Underlier Values, Coupon Barriers or Downside Thresholds. The hypothetical Initial Underlier Value

of 100.00 for each Underlier has been chosen for illustrative purposes only and does not represent the actual Initial Underlier Value

for any Underlier. The actual Contingent Coupon Rate, Contingent Coupon, Initial Underlier Values, Coupon Barriers and Downside Thresholds

will be determined on the Trade Date and will be set forth on the cover page and under “Terms of the Notes” above. For actual

historical data of the Underliers, see the historical information set forth herein. These examples are for purposes of illustration only

and the values used in the examples may have been rounded for ease of analysis. In these examples, we refer to the Nasdaq-100® Index,

the Russell 2000® Index and the S&P 500® Index as the “NDX Index,” the “RTY

Index” and the “SPX Index,” respectively.

| Term: |

Approximately 3 years (unless called earlier) |

| Hypothetical Contingent Coupon Rate: |

5.00% per annum (or 1.25% per quarter) |

| Hypothetical Contingent Coupon: |

$0.125 per quarter |

| Hypothetical Initial Underlier Value: |

For each Underlier, 100.00 |

| Hypothetical Coupon Barrier: |

For each Underlier, 90.00 (90% of its hypothetical Initial Underlier Value) |

| Hypothetical Downside Threshold: |

For each Underlier, 80.00 (80% of its hypothetical Initial Underlier Value) |

| Coupon Observation Dates: |

Quarterly |

| Call Observation Dates: |

Quarterly (callable after six months) |

The “total return” as used in this pricing supplement

is the number, expressed as a percentage, that results from comparing the total payments per Note over the term of the Notes to the purchase

price of $10 per Note.

Example 1 — Notes Are Automatically Called on the Second Coupon

Observation Date

Coupon Observation

Date |

|

Closing Value |

|

Payment (per Note) |

First Coupon

Observation Date |

|

NDX Index: 80.00

RTY Index: 65.00

SPX Index: 70.00

|

|

Not Callable.

Closing Value of at least one Underlier below its

Coupon Barrier; Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Second Coupon

Observation Date |

|

NDX Index: 110.00

RTY Index: 115.00

SPX Index: 105.00

|

|

Closing Value of each Underlier at or above its Initial Underlier Value; Notes are automatically called; Issuer pays Principal Amount plus Contingent Coupon of $0.125 on Call Settlement Date. |

| Total Payments (per Note): |

|

Payment on Call Settlement Date: |

$10.125 ($10.00 + $0.125) |

| |

|

Prior Contingent Coupons: |

$0.00 |

| |

|

Total: |

$10.125 |

| |

|

Total Return: |

1.25% |

Because the Closing Value of each Underlier is

greater than or equal to its Initial Underlier Value on the second Coupon Observation Date (which is the first Call Observation Date),

the Notes are automatically called on that Coupon Observation Date. The Issuer will pay you on the related Call Settlement Date $10.125

per Note, which is equal to the Principal Amount plus the Contingent Coupon due on the Contingent Coupon Payment Date that is also

the Call Settlement Date. No further amounts will be owed to you under the Notes.

However, because the Closing Value of at least

one Underlier was less than its Coupon Barrier on the first Coupon Observation Date, the Issuer will not pay any Contingent Coupon on

the Contingent Coupon Payment Date following that Coupon Observation Date. Accordingly, the Issuer will have paid a total of $10.125 per

Note for a total return of 1.25% on the Notes.

Example 2 — Notes Are NOT Automatically Called and the Final

Underlier Value of Each Underlier Is At or Above Its Downside Threshold and Coupon Barrier

Coupon Observation

Date |

|

Closing Value |

|

Payment (per Note) |

First Coupon Observation

Date |

|

NDX Index: 110.00

RTY Index: 125.00

SPX Index: 105.00

|

|

Not Callable.

Closing Value of each Underlier at or above its

Coupon Barrier; Issuer pays Contingent Coupon of $0.125 on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Second Coupon

Observation Date |

|

NDX Index: 95.00

RTY Index: 110.00

SPX Index: 105.00

|

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of each Underlier at or above its

Coupon Barrier; Issuer pays Contingent Coupon of $0.125 on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Third Coupon Observation

Date |

|

NDX Index: 90.00

RTY Index: 70.00

SPX Index: 95.00

|

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of RTY Index below its Coupon Barrier;

Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Fourth to Eleventh Coupon

Observation Dates |

|

Various (at least one Underlier below Coupon Barrier) |

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of at least one Underlier below its

Coupon Barrier; Issuer DOES NOT pay Contingent Coupon on any of the related Contingent Coupon Payment Dates.

|

| |

|

|

|

|

Twelfth Coupon

Observation Date (the

Final Valuation Date) |

|

NDX Index: 105.00

RTY Index: 95.00

SPX Index: 110.00

|

|

Not Callable.

Final Underlier Value of each Underlier at or above

Downside Threshold and Coupon Barrier; Issuer pays Principal Amount plus Contingent Coupon of $0.125 on Maturity Date.

|

| Total Payments (per Note): |

|

Payment at Maturity: |

$10.125 ($10.00 + $0.125) |

| |

|

Prior Contingent Coupons: |

$0.25 ($0.125 × 2) |

| |

|

Total: |

$10.375 |

| |

|

Total Return: |

3.75% |

Because the Closing Value of at least one Underlier

is less than its Initial Underlier Value on each Coupon Observation Date that is also a Call Observation Date, the Notes are not automatically

called. Because the Final Underlier Value of each Underlier is greater than or equal to its Downside Threshold and Coupon Barrier, the

Issuer will pay you on the Maturity Date $10.125 per Note, which is equal to the Principal Amount plus the Contingent Coupon due

on the Contingent Coupon Payment Date that is also the Maturity Date.

In addition, because the Closing Value of each

Underlier was greater than or equal to its Coupon Barrier on the first and second Coupon Observation Dates, the Issuer will pay the Contingent

Coupon of $0.125 on each of the related Contingent Coupon Payment Dates. However, because the Closing Value of at least one Underlier

was less than its Coupon Barrier on the third through eleventh Coupon Observation Dates, the Issuer will not pay any Contingent Coupon

on the Contingent Coupon Payment Dates following those Coupon Observation Dates. Accordingly, the Issuer will have paid a total of $10.375

per Note for a total return of 3.75% on the Notes.

Example 3 — Notes Are NOT Automatically Called and the Final

Underlier Value of Each Underlier Is At or Above Its Downside Threshold but the Final Underlier Value of At Least One Underlier Is Below

Its Coupon Barrier

Coupon Observation

Date |

|

Closing Value |

|

Payment (per Note) |

First Coupon

Observation Date |

|

NDX Index: 95.00

RTY Index: 125.00

SPX Index: 105.00

|

|

Not Callable.

Closing Value of each Underlier at or above its

Coupon Barrier; Issuer pays Contingent Coupon of $0.125 on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Second Coupon

Observation Date |

|

NDX Index: 95.00

RTY Index: 110.00

SPX Index: 105.00

|

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of each Underlier at or above its

Coupon Barrier; Issuer pays Contingent Coupon of $0.125 on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Third Coupon

Observation Date |

|

NDX Index: 120.00

RTY Index: 125.00

SPX Index: 65.00

|

|

Closing Value of SPX Index below its Initial Underlier

Value; Notes NOT automatically called.

Closing Value of SPX Index below its Coupon Barrier;

Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| |

|

|

|

|

Fourth to Eleventh

Coupon Observation

Dates |

|

Various (at least one Underlier below Coupon Barrier) |

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of at least one Underlier below its

Coupon Barrier; Issuer DOES NOT pay Contingent Coupon on any of the related Contingent Coupon Payment Dates.

|

| |

|

|

|

|

Twelfth Coupon

Observation Date (the

Final Valuation Date) |

|

NDX Index: 105.00

RTY Index: 95.00

SPX Index: 85.00

|

|

Not Callable.

Final Underlier Value of each Underlier at or above

its Downside Threshold but Final Underlier Value of SPX Index below its Coupon Barrier; Issuer pays Principal Amount but DOES NOT pay

Contingent Coupon on Maturity Date.

|

| Total Payments (per Note): |

|

Payment at Maturity: |

$10.00 |

| |

|

Prior Contingent Coupons: |

$0.25 ($0.125 × 2) |

| |

|

Total: |

$10.25 |

| |

|

Total Return: |

2.50% |

Because the Closing Value of at least one Underlier

is less than its Initial Underlier Value on each Coupon Observation Date that is also a Call Observation Date, the Notes are not automatically

called. Because the Final Underlier Value of each Underlier is greater than or equal to its Downside Threshold and the Final Underlier

Value of at least one Underlier is less than its Coupon Barrier, the Issuer will pay you on the Maturity Date $10.00 per Note, which is

equal to the Principal Amount, but no Contingent Coupon.

In addition, because the Closing Value of each

Underlier was greater than or equal to its Coupon Barrier on the first and second Coupon Observation Dates, the Issuer will pay the Contingent

Coupon of $0.125 on each of the related Contingent Coupon Payment Dates. However, because the Closing Value of at least one Underlier

was less than its Coupon Barrier on the third through eleventh Coupon Observation Dates, the Issuer will not pay any Contingent Coupon

on the Contingent Coupon Payment Dates following those Coupon Observation Dates. Accordingly, the Issuer will have paid a total of $10.25

per Note for a total return of 2.50% on the Notes.

Example 4 — Notes Are NOT Automatically

Called and the Final Underlier Value of At Least One Underlier Is Below its Downside Threshold

Coupon Observation

Date |

|

Closing Value |

|

Payment (per Note) |

| First Coupon Observation Date |

|

NDX Index: 70.00

RTY Index: 60.00

SPX Index: 80.00

|

|

Not Callable.

Closing Value of each Underlier below its Coupon

Barrier; Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| Second Coupon Observation Date |

|

NDX Index: 105.00

RTY Index: 85.00

SPX Index: 95.00

|

|

Closing Value of the SPX Index below its Initial

Underlier Value; Notes NOT automatically called.

Closing Value of RTY Index below its Coupon Barrier;

Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| Third Coupon Observation Date |

|

NDX Index: 40.00

RTY Index: 65.00

SPX Index: 90.00

|

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of at least one Underlier below its

Coupon Barrier; Issuer DOES NOT pay Contingent Coupon on the related Contingent Coupon Payment Date.

|

| Fourth to Eleventh Coupon Observation Dates |

|

Various (at least one Underlier below Coupon Barrier) |

|

Closing Value of at least one Underlier below its

Initial Underlier Value; Notes NOT automatically called.

Closing Value of at least one Underlier below its

Coupon Barrier; Issuer DOES NOT pay Contingent Coupon on any of the related Contingent Coupon Payment Dates.

|

| Twelfth Coupon Observation Date (the Final Valuation Date) |

|

NDX Index: 125.00

RTY Index: 110.00

SPX Index: 50.00

|

|

Not Callable.

Closing Value of SPX Index below its Coupon Barrier

and its Downside Threshold; Issuer DOES NOT pay Contingent Coupon on Maturity Date; Issuer repays less than the Principal Amount resulting

in a percentage loss on your investment equal to the negative Underlier Return.

|

| Total Payments (per Note): |

|

Payment at Maturity: |

$5.00 |

| |

|

Prior Contingent Coupons: |

$0.00 |

| |

|

Total: |

$5.00 |

| |

|

Total Return: |

-50.00% |

Because the Closing Value of at least one Underlier

is less than its Initial Underlier Value on each Coupon Observation Date that is also a Call Observation Date, the Notes are not automatically

called. Because the Final Underlier Value of at least one Underlier is less than its Downside Threshold on the Final Valuation Date, at

maturity, the Issuer will pay you a total of $5.00 per Note, for a total return of -50.00%

on the Notes, calculated as follows:

$10 + ($10 × Underlier Return of the Least

Performing Underlier)

Step 1: Calculate the Underlier Return of each Underlier:

Underlier Return of the NDX Index:

| Final Underlier Value – Initial Underlier Value |

= |

125.00 – 100.00 |

= 25.00% |

| Initial Underlier Value |

100.00 |

Underlier Return of the RTY Index:

| Final Underlier Value – Initial Underlier Value |

= |

110.00 – 100.00 |

= 10.00% |

| Initial Underlier Value |

100.00 |

Underlier Return of the SPX Index:

| Final Underlier Value – Initial Underlier Value |

= |

50.00 – 100.00 |

= -50.00% |

| Initial Underlier Value |

100.00 |

Step 2: Determine the Least Performing Underlier. The SPX Index

is the Underlier with the lowest Underlier Return and is, therefore, the Least Performing Underlier.

Step 3: Calculate the Payment at Maturity:

$10 + ($10 × Underlier Return of the Least

Performing Underlier)

$10 + ($10 × -50.00%) = $5.00

In addition, because the Closing Value of at least one Underlier is

less than its Coupon Barrier on each Coupon Observation Date, the Issuer will not pay any Contingent Coupons over the term of the Notes.

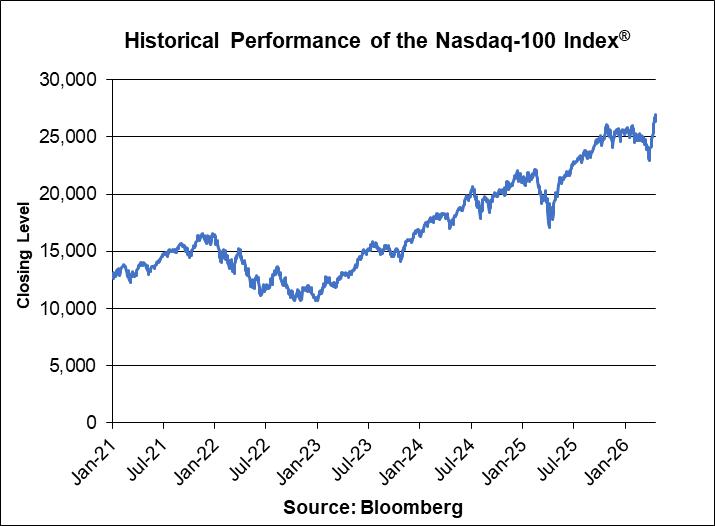

The Nasdaq-100 Index® is a

modified market capitalization-weighted index that is designed to measure the performance of 100 of the largest non-financial companies

listed on The Nasdaq Stock Market. For more information about the Nasdaq-100 Index®, see “Description of Indices—The

Nasdaq-100 Index®” in the accompanying underlying supplement.

Historical Information

We obtained the closing levels of the Nasdaq-100

Index® in the graph below from Bloomberg Finance L.P. (“Bloomberg”), without independent verification.

The following graph sets forth daily closing levels

of the Nasdaq-100 Index® for the period from January 4, 2021 to April 22, 2026. The closing level on April 22, 2026 was

26,937.28. The historical performance of the Nasdaq-100 Index® should not be taken as an indication of its future performance

during the term of the Notes.

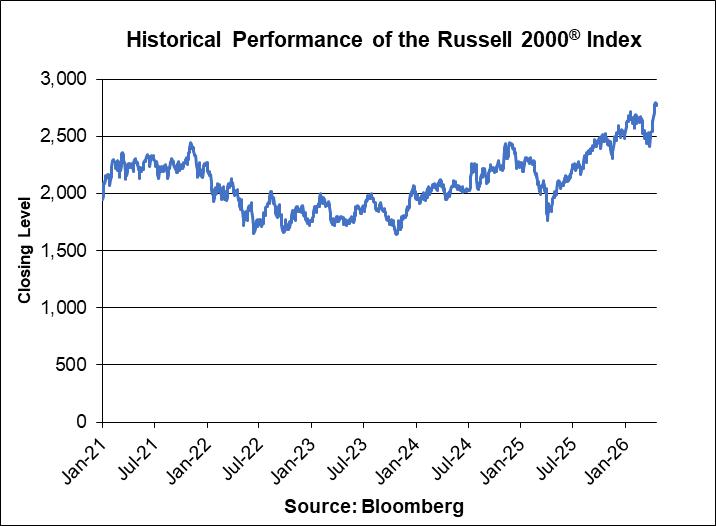

The Russell 2000® Index measures

the capitalization-weighted price performance of 2,000 U.S. small-capitalization stocks listed on eligible U.S. exchanges and is designed

to track the performance of the small-capitalization segment of the U.S. equity market. For more information about the Russell 2000® Index,

see “Description of Indices—The Russell Indices” in the accompanying underlying supplement.

Historical Information

We obtained the closing levels of the Russell 2000® Index

in the graph below from Bloomberg, without independent verification.

The following graph sets forth daily closing levels

of the Russell 2000® Index for the period from January 4, 2021 to April 22, 2026. The closing level on April 22, 2026

was 2,785.377. The historical performance of the Russell 2000® Index should not be taken as an indication of its future

performance during the term of the Notes.

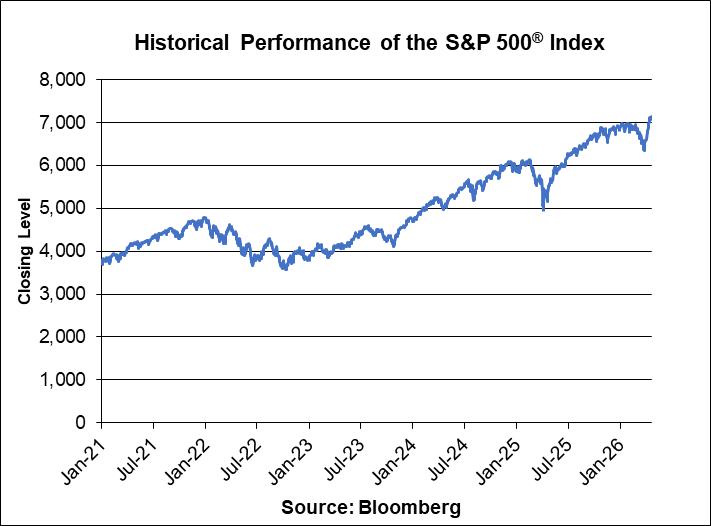

The S&P 500® Index consists

of stocks of 500 companies selected to provide a performance benchmark for the U.S. equity markets. For more information about the S&P

500® Index, see “Description of Indices—The S&P U.S. Indices” in the accompanying underlying supplement.

Historical Information

We obtained the closing levels of the S&P 500®

Index in the graph below from Bloomberg, without independent verification.

The following graph sets forth daily closing levels

of the S&P 500® Index for the period from January 4, 2021 to April 22, 2026. The closing level on April 22, 2026 was

7,137.90. The historical performance of the S&P 500® Index should not be taken as an indication of its future performance

during the term of the Notes.

|

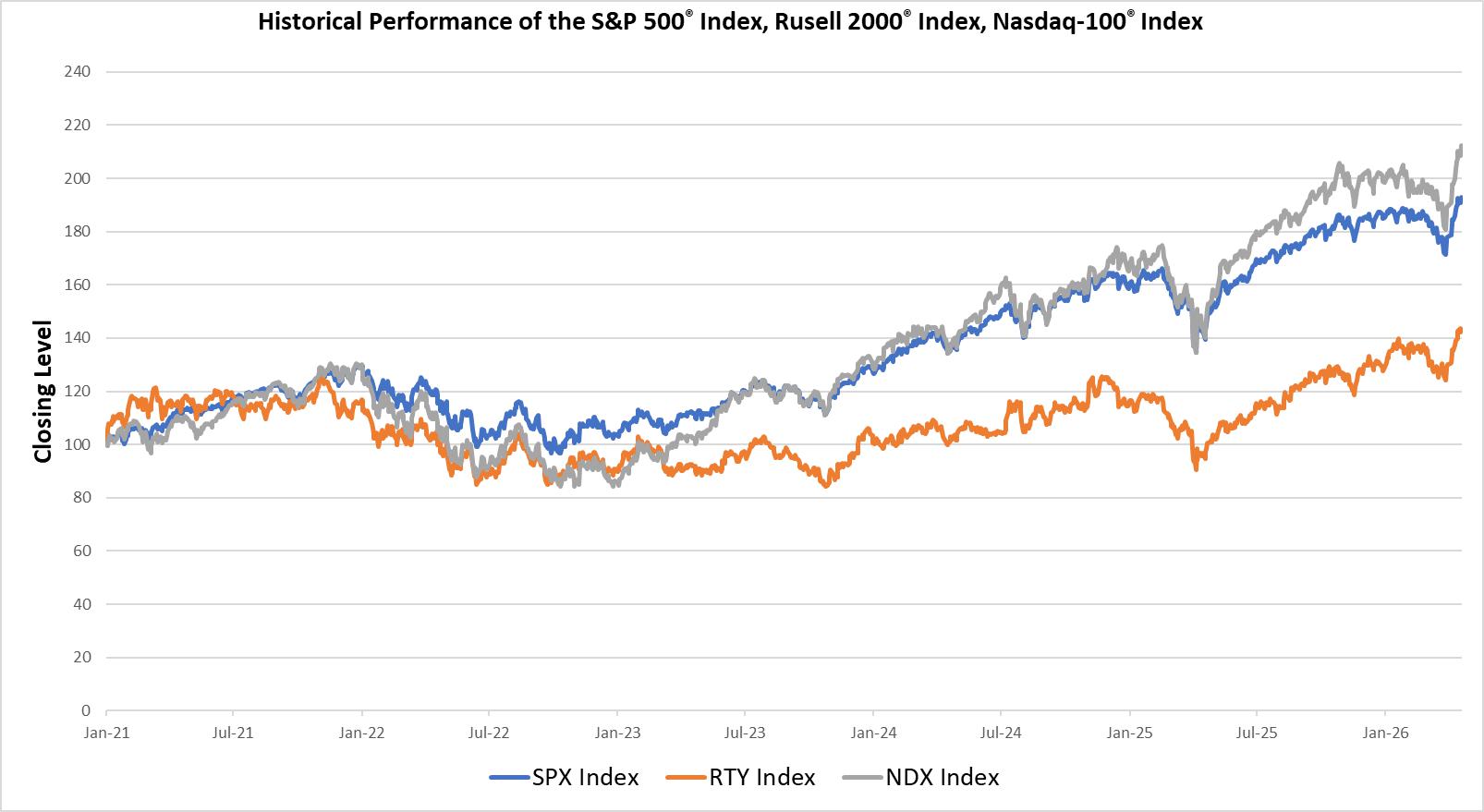

Correlation of the Underliers |

The following