Western New England Bancorp, Inc. 8-K

Exhibit 99.2

Local banking is better than ever. INVESTOR PRESENTATION 1ST QUARTER 2026

FORWARD - LOOKING STATEMENTS 2 We may, from time to time, make written or oral “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 , including statements contained in our filings with the Securities and Exchange Commission (the “SEC”), our reports to shareholders and in other communications by us . This Investor Presentation contains “forward - looking statements” with respect to the Company’s financial condition, liquidity, results of operations, future performance, and business . Forward - looking statements may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” and “potential . ” Examples of forward - looking statements include, but are not limited to, estimates with respect to our financial condition, results of operations and business that are subject to various factors which could cause actual results to differ materially from these estimates . These factors include, but are not limited to : unpredictable changes in general economic or political conditions, financial markets, fiscal, monetary and regulatory policies, including actual or potential stress in the banking industry ; the possibility that future credit losses, loan defaults and charge - off rates are higher than expected due to changes in economic assumptions or adverse economic developments ; general business and economic conditions on a national basis and in the local markets in which we operate, including those impacting credit quality ; unstable political and economic conditions, including changes in tariff policies, which could materially impact credit quality trends and the ability to generate loans and gather deposits ; inflation and governmental responses to inflation, including potential future increases in interest rates that reduce net interest margins ; the effect on our operations of governmental legislation and regulation, including changes in accounting regulation or standards, the nature and timing of the adoption and effectiveness of new requirements under the Dodd - Frank Wall Street Reform and Consumer Protection Act of 2010 , Basel guidelines, capital requirements and other applicable laws and regulations ; changes in regulation, regulatory policy, legislation, accounting standards and practices, and fiscal monetary policy, particularly in light of the shift in presidential administrations and the potential for related shifts in agency policy and leadership ; operational risks or risk management failures by us or critical third parties, including without limitation with respect to data processing, information systems, cybersecurity incidents, technological integration, including AI, vendor issues, business interruption, and fraud risks ; significant changes in accounting, tax or regulatory practices or requirements ; new legal obligations or liabilities or unfavorable resolutions or litigation ; disruptive technologies in payment systems and other services traditionally provided by financial institutions ;

FORWARD - LOOKING STATEMENTS 3 severe weather, natural disasters, acts of war or terrorism and other external events which could significantly impact our business ; declines in real estate values in the Company’s market area, which may adversely affect our loan production ; decreases in the value of securities and other assets, or changes in the securities markets which affect investment management revenue ; decreases in deposit levels necessitating increased borrowing to fund loans, investments and other needs ; competitive pressures from other financial institutions ; the soundness of other financial services institutions which may adversely affect our credit risk ; failure or circumvention of our internal controls or procedures ; the risk that goodwill and intangibles recorded in our financial statements will become impaired ; the risk that we may not be successful in the implementation of our business strategy ; increases in Federal Deposit Insurance Corporation deposit insurance premiums and assessments ; introduction of new lines of business or new products and services, which may subject us to additional risks ; changes in key management personnel which may adversely impact our operations ; and other risks and uncertainties detailed in Part 1 A “Risk Factors” of the Company’s 2025 Annual Report on Form 10 - K . Although we believe that the expectations reflected in such forward - looking statements are reasonable, actual results may differ materially from the results discussed in these forward - looking statements. You are cautioned not to place undue reliance on the se forward - looking statements, which speak only as of the date hereof. We do not undertake any obligation to republish revised for ward - looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except to the extent required by law.

WHO WE ARE Every day, we focus on showing Westfield Bank customers “ what better banking is all about . ” For us, the idea of better banking starts with putting customers first, while adhering to our core values . Our Core Values : • Integrity • Enhance Shareholder Value • Customer Focus • Community Focus Our Core Mission : Our core mission is to help customers succeed in our community, while creating and increasing shareholder value . The Company’s mission drives the outcome we envision for Western New England Bancorp . 4 70 Center Street, Chicopee, MA.

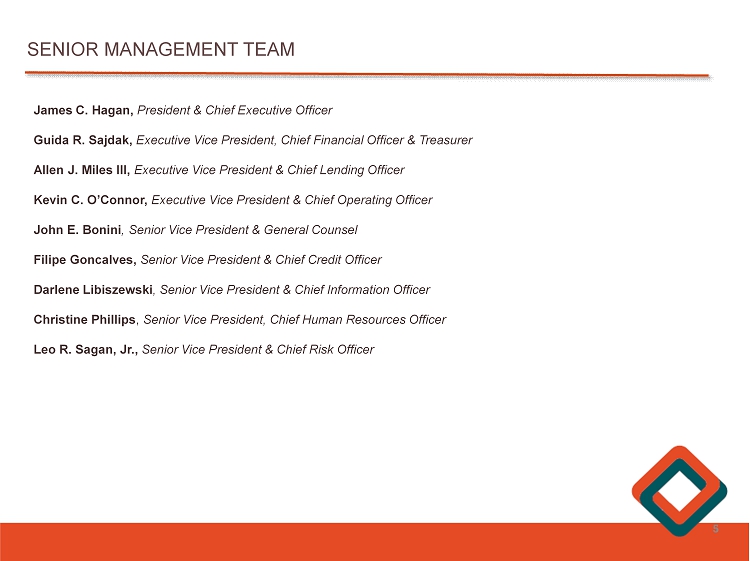

SENIOR MANAGEMENT TEAM James C . Hagan, President & Chief Executive Officer Guida R . Sajdak, Executive Vice President, Chief Financial Officer & Treasurer Allen J . Miles III, Executive Vice President & Chief Lending Officer Kevin C . O’Connor, Executive Vice President & Chief Operating Officer John E . Bonini , Senior Vice President & General Counsel Filipe Goncalves, Senior Vice President & Chief Credit Officer Darlene Libiszewski , Senior Vice President & Chief Information Officer Christine Phillips , Senior Vice President, Chief Human Resources Officer Leo R . Sagan, Jr . , Senior Vice President & Chief Risk Officer 5

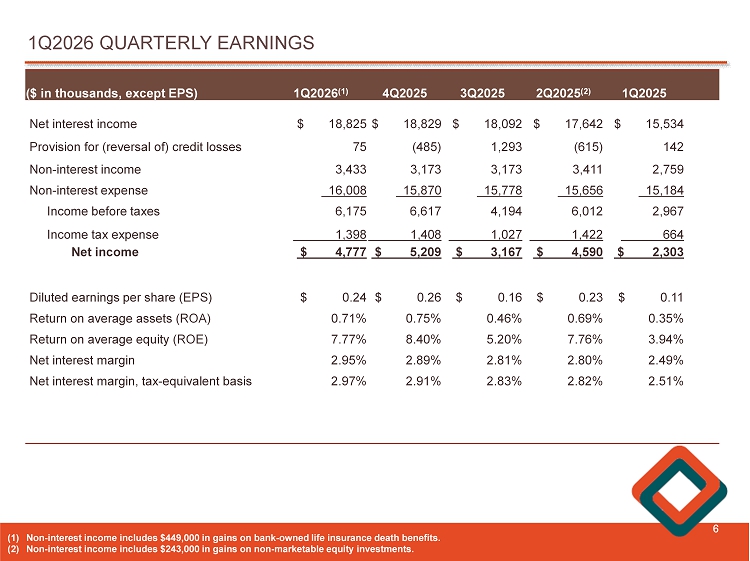

1Q2026 QUARTERLY EARNINGS 6 1Q2025 2Q2025 (2) 3Q2025 4Q2025 1Q2026 (1) ($ in thousands, except EPS) $ 15,534 $ 17,642 $ 18,092 $ 18,829 $ 18,825 Net interest income 142 (615) 1,293 (485) 75 Provision for (reversal of) credit losses 2,759 3,411 3,173 3,173 3,433 Non - interest income 15,184 15,656 15,778 15,870 16,008 Non - interest expense 2,967 6,012 4,194 6,617 6,175 Income before taxes 664 1,422 1,027 1,408 1,398 Income tax expense $ 2,303 $ 4,590 $ 3,167 $ 5,209 $ 4,777 Net income $ 0.11 $ 0.23 $ 0.16 $ 0.26 $ 0.24 Diluted earnings per share (EPS) 0.35% 0.69% 0.46% 0.75% 0.71% Return on average assets (ROA) 3.94% 7.76% 5.20% 8.40% 7.77% Return on average equity (ROE) 2.49% 2.80% 2.81% 2.89% 2.95% Net interest margin 2.51% 2.82% 2.83% 2.91% 2.97% Net interest margin, tax - equivalent basis (1) Non - interest income includes $449,000 in gains on bank - owned life insurance death benefits. (2) Non - interest income includes $243,000 in gains on non - marketable equity investments.

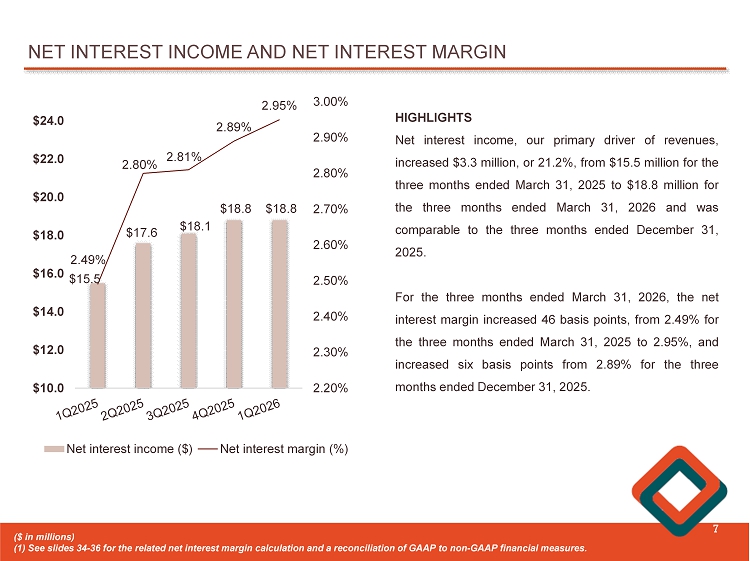

NET INTEREST INCOME AND NET INTEREST MARGIN 7 $15.5 $17.6 $18.1 $18.8 $18.8 2.49% 2.80% 2.81% 2.89% 2.95% 2.20% 2.30% 2.40% 2.50% 2.60% 2.70% 2.80% 2.90% 3.00% $10.0 $12.0 $14.0 $16.0 $18.0 $20.0 $22.0 $24.0 Net interest income ($) Net interest margin (%) ($ in millions) (1) See slides 34 - 36 for the related net interest margin calculation and a reconciliation of GAAP to non - GAAP financial measures . HIGHLIGHTS Net interest income, our primary driver of revenues, increased $ 3 . 3 million, or 21 . 2 % , from $ 15 . 5 million for the three months ended March 31 , 2025 to $ 18 . 8 million for the three months ended March 31 , 2026 and was comparable to the three months ended December 31 , 2025 . For the three months ended March 31 , 2026 , the net interest margin increased 46 basis points, from 2 . 49 % for the three months ended March 31 , 2025 to 2 . 95 % , and increased six basis points from 2 . 89 % for the three months ended December 31 , 2025 .

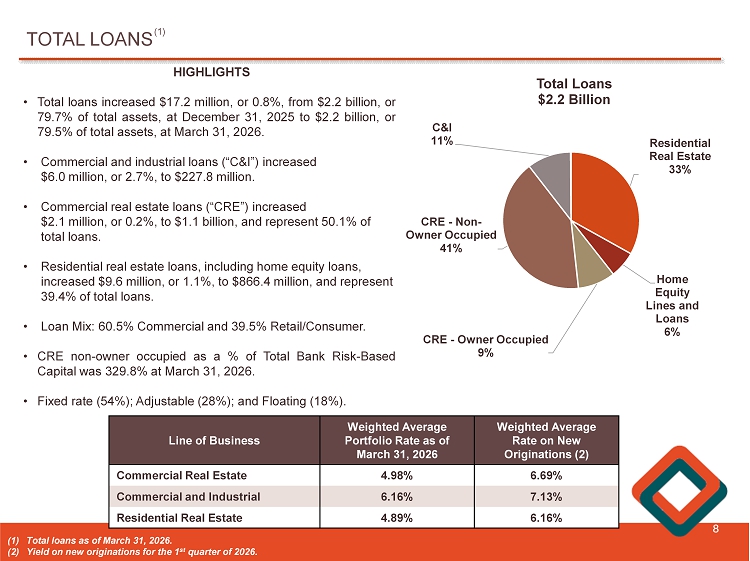

TOTAL LOANS 8 Residential Real Estate 33% Home Equity Lines and Loans 6% CRE - Owner Occupied 9% CRE - Non - Owner Occupied 41% C&I 11% Total Loans $2.2 Billion HIGHLIGHTS • Total loans increased $ 17 . 2 million, or 0 . 8 % , from $ 2 . 2 billion, or 79 . 7 % of total assets, at December 31 , 2025 to $ 2 . 2 billion, or 79 . 5 % of total assets, at March 31 , 2026 . • Commercial and industrial loans (“C&I”) increased $ 6 . 0 million, or 2 . 7 % , to $ 227 . 8 million . • Commercial real estate loans (“CRE”) increased $ 2 . 1 million, or 0 . 2 % , to $ 1 . 1 billion, and represent 50 . 1 % of total loans . • Residential real estate loans, including home equity loans, increased $ 9 . 6 million, or 1 . 1 % , to $ 866 . 4 million, and represent 39 . 4 % of total loans . • Loan Mix : 60 . 5 % Commercial and 39 . 5 % Retail/Consumer . • CRE non - owner occupied as a % of Total Bank Risk - Based Capital was 329 . 8 % at March 31 , 2026 . • Fixed rate ( 54 % ) ; Adjustable ( 28 % ) ; and Floating ( 18 % ) . Weighted Average Rate on New Originations (2) Weighted Average Portfolio Rate as of March 31, 2026 Line of Business 6.69% 4.98% Commercial Real Estate 7.13% 6.16% Commercial and Industrial 6.16% 4.89% Residential Real Estate (1) Total loans as of March 31, 2026. (2) Yield on new originations for the 1 st quarter of 2026. (1)

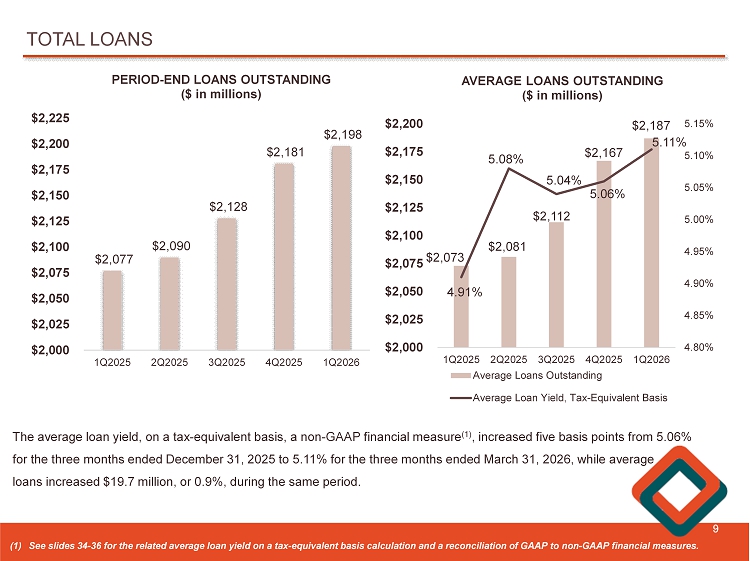

TOTAL LOANS 9 $2,073 $2,081 $2,112 $2,167 $2,187 4.91% 5.08% 5.04% 5.06% 5.11% 4.80% 4.85% 4.90% 4.95% 5.00% 5.05% 5.10% 5.15% 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $2,000 $2,025 $2,050 $2,075 $2,100 $2,125 $2,150 $2,175 $2,200 AVERAGE LOANS OUTSTANDING ($ in millions) Average Loans Outstanding Average Loan Yield, Tax-Equivalent Basis (1) See slides 34 - 36 for the related average loan yield on a tax - equivalent basis calculation and a reconciliation of GAAP to non - GA AP financial measures. $2,077 $2,090 $2,128 $2,181 $2,198 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $2,000 $2,025 $2,050 $2,075 $2,100 $2,125 $2,150 $2,175 $2,200 $2,225 PERIOD - END LOANS OUTSTANDING ($ in millions) The average loan yield, on a tax - equivalent basis, a non - GAAP financial measure (1) , increased five basis points from 5.06% for the three months ended December 31, 2025 to 5.11% for the three months ended March 31, 2026, while average loans increased $19.7 million, or 0.9%, during the same period.

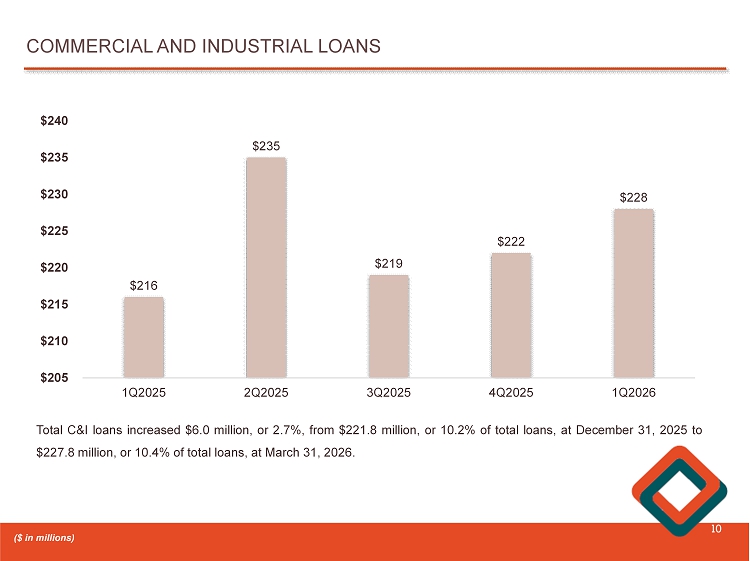

COMMERCIAL AND INDUSTRIAL LOANS 10 $216 $235 $219 $222 $228 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $205 $210 $215 $220 $225 $230 $235 $240 Total C&I loans increased $ 6 . 0 million, or 2 . 7 % , from $ 221 . 8 million, or 10 . 2 % of total loans, at December 31 , 2025 to $ 227 . 8 million, or 10 . 4 % of total loans, at March 31 , 2026 . ($ in millions)

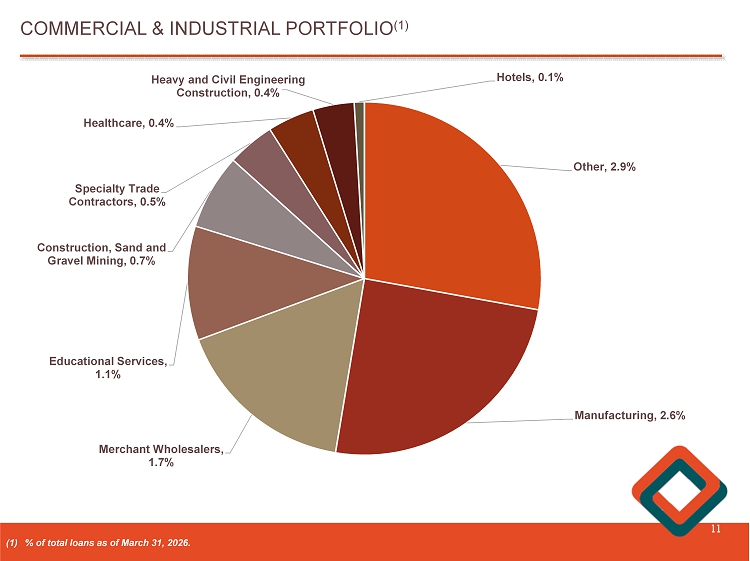

COMMERCIAL & INDUSTRIAL PORTFOLIO (1) 11 (1) % of total loans as of March 31, 2026. Other , 2.9% Manufacturing , 2.6% Merchant Wholesalers , 1.7% Educational Services , 1.1% Construction, Sand and Gravel Mining , 0.7% Specialty Trade Contractors , 0.5% Healthcare , 0.4% Heavy and Civil Engineering Construction , 0.4% Hotels , 0.1%

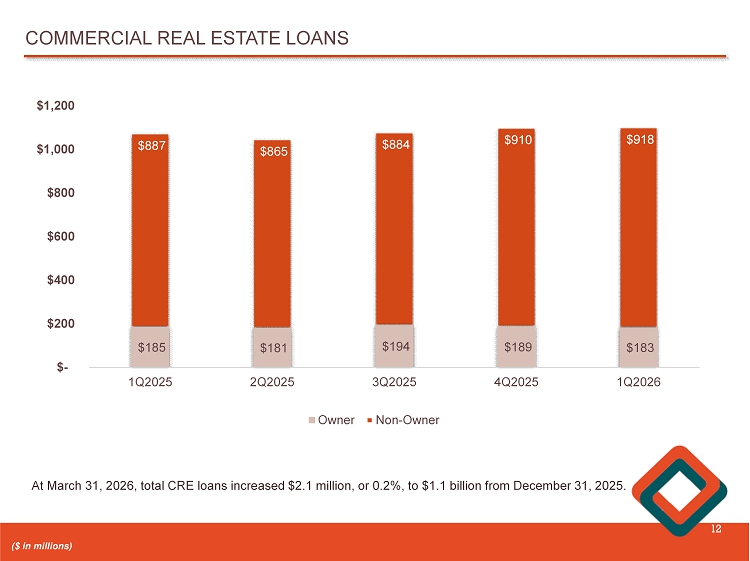

COMMERCIAL REAL ESTATE LOANS 12 $185 $181 $194 $189 $183 $887 $865 $884 $910 $918 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $- $200 $400 $600 $800 $1,000 $1,200 Owner Non-Owner At March 31 , 2026 , total CRE loans increased $ 2 . 1 million, or 0 . 2 % , to $ 1 . 1 billion from December 31 , 2025 . ($ in millions)

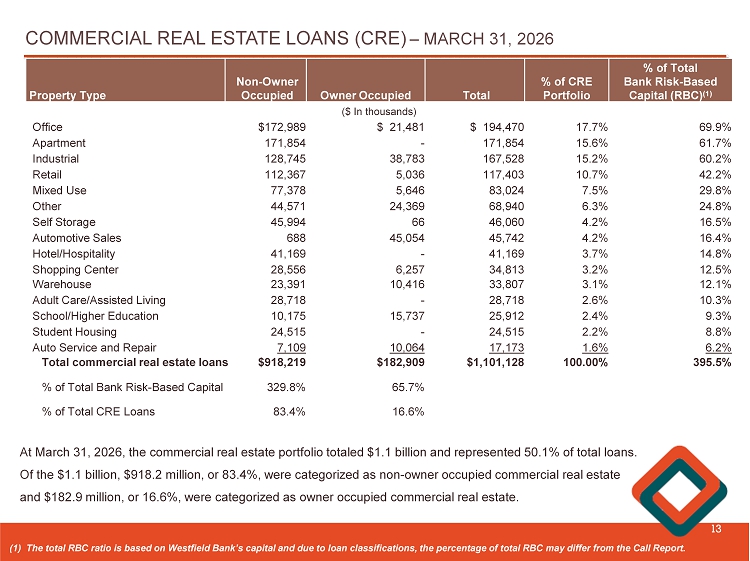

COMMERCIAL REAL ESTATE LOANS (CRE) – MARCH 31, 2026 13 (1) The total RBC ratio is based on Westfield Bank’s capital and due to loan classifications, the percentage of total RBC ma y d iffer from the Call Report. At March 31 , 2026 , the commercial real estate portfolio totaled $ 1 . 1 billion and represented 50 . 1 % of total loans . Of the $ 1 . 1 billion, $ 918 . 2 million, or 83 . 4 % , were categorized as non - owner occupied commercial real estate and $ 182 . 9 million, or 16 . 6 % , were categorized as owner occupied commercial real estate . % of Total Bank Risk - Based Capital (RBC) (1) % of CRE Portfolio Total Owner Occupied Non - Owner Occupied Property Type ($ In thousands) 69.9% 17.7% $ 194,470 $ 21,481 $172,989 Office 61.7% 15.6% 171,854 - 171,854 Apartment 60.2% 15.2% 167,528 38,783 128,745 Industrial 42.2% 10.7% 117,403 5,036 112,367 Retail 29.8% 7.5% 83,024 5,646 77,378 Mixed Use 24.8% 6.3% 68,940 24,369 44,571 Other 16.5% 4.2% 46,060 66 45,994 Self Storage 16.4% 4.2% 45,742 45,054 688 Automotive Sales 14.8% 3.7% 41,169 - 41,169 Hotel/Hospitality 12.5% 3.2% 34,813 6,257 28,556 Shopping Center 12.1% 3.1% 33,807 10,416 23,391 Warehouse 10.3% 2.6% 28,718 - 28,718 Adult Care/Assisted Living 9.3% 2.4% 25,912 15,737 10,175 School/Higher Education 8.8% 2.2% 24,515 - 24,515 Student Housing 6.2% 1.6% 17,173 10,064 7,109 Auto Service and Repair 395.5% 100.00% $1,101,128 $182,909 $918,219 Total commercial real estate loans 65.7% 329.8% % of Total Bank Risk - Based Capital 16.6% 83.4% % of Total CRE Loans

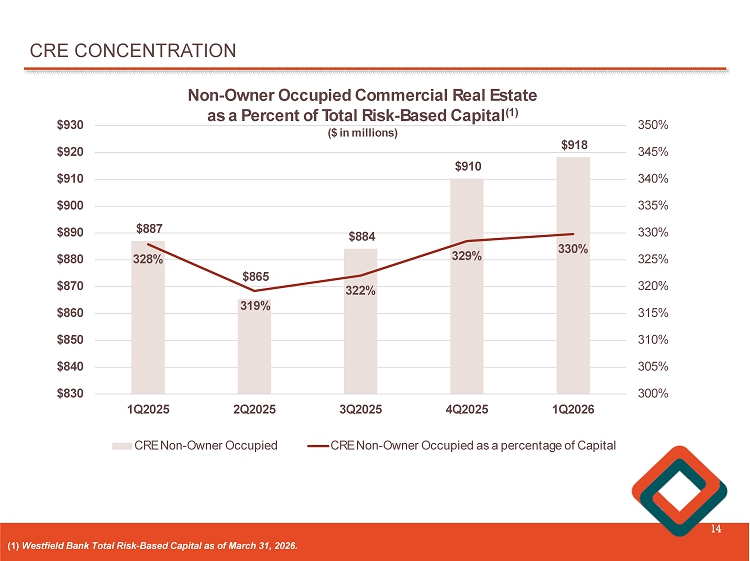

CRE CONCENTRATION 14 (1) Westfield Bank Total Risk - Based Capital as of March 31, 2026. $887 $865 $884 $910 $918 328% 319% 322% 329% 330% 300% 305% 310% 315% 320% 325% 330% 335% 340% 345% 350% $830 $840 $850 $860 $870 $880 $890 $900 $910 $920 $930 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 Non - Owner Occupied Commercial Real Estate as a Percent of Total Risk - Based Capital (1) ($ in millions) CRE Non-Owner Occupied CRE Non-Owner Occupied as a percentage of Capital

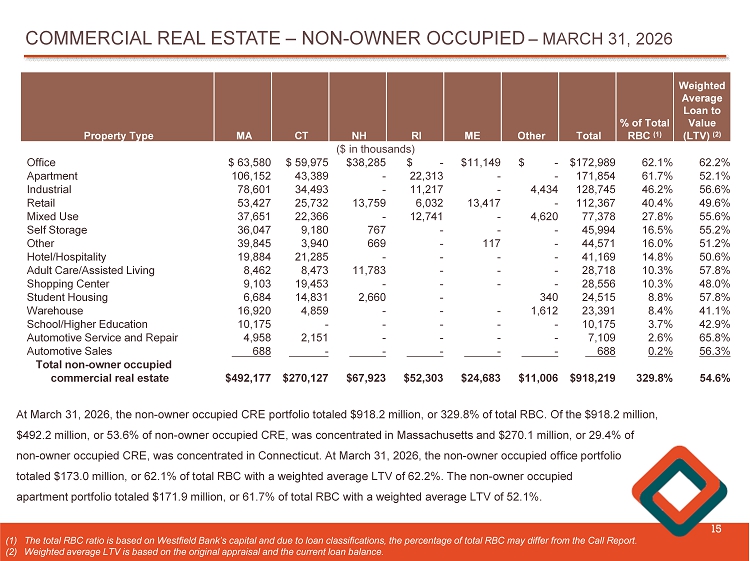

COMMERCIAL REAL ESTATE – NON - OWNER OCCUPIED – MARCH 31, 2026 15 At March 31 , 2026 , the non - owner occupied CRE portfolio totaled $ 918 . 2 million, or 329 . 8 % of total RBC . Of the $ 918 . 2 million, $ 492 . 2 million, or 53 . 6 % of non - owner occupied CRE, was concentrated in Massachusetts and $ 270 . 1 million, or 29 . 4 % of non - owner occupied CRE, was concentrated in Connecticut . At March 31 , 2026 , the non - owner occupied office portfolio totaled $ 173 . 0 million, or 62 . 1 % of total RBC with a weighted average LTV of 62 . 2 % . The non - owner occupied apartment portfolio totaled $ 171 . 9 million, or 61 . 7 % of total RBC with a weighted average LTV of 52 . 1 % . (1) The total RBC ratio is based on Westfield Bank’s capital and due to loan classifications, the percentage of total RBC may dif fer from the Call Report. (2) Weighted average LTV is based on the original appraisal and the current loan balance. Weighted Average Loan to Value % of Total Total Other ME RI NH CT MA Property Type (LTV) (2) RBC (1) ($ in thousands) 62.2% 62.1% $172,989 $ - $11,149 $ - $38,285 $ 59,975 $ 63,580 Office 52.1% 61.7% 171,854 - - 22,313 - 43,389 106,152 Apartment 56.6% 46.2% 128,745 4,434 - 11,217 - 34,493 78,601 Industrial 49.6% 40.4% 112,367 - 13,417 6,032 13,759 25,732 53,427 Retail 55.6% 27.8% 77,378 4,620 - 12,741 - 22,366 37,651 Mixed Use 55.2% 16.5% 45,994 - - - 767 9,180 36,047 Self Storage 51.2% 16.0% 44,571 - 117 - 669 3,940 39,845 Other 50.6% 14.8% 41,169 - - - - 21,285 19,884 Hotel/Hospitality 57.8% 10.3% 28,718 - - - 11,783 8,473 8,462 Adult Care/Assisted Living 48.0% 10.3% 28,556 - - - - 19,453 9,103 Shopping Center 57.8% 8.8% 24,515 340 - 2,660 14,831 6,684 Student Housing 41.1% 8.4% 23,391 1,612 - - - 4,859 16,920 Warehouse 42.9% 3.7% 10,175 - - - - - 10,175 School/Higher Education 65.8% 2.6% 7,109 - - - - 2,151 4,958 Automotive Service and Repair 56.3% 0.2% 688 - - - - - 688 Automotive Sales 54.6% 329.8% $918,219 $11,006 $24,683 $52,303 $67,923 $270,127 $492,177 Total non - owner occupied commercial real estate

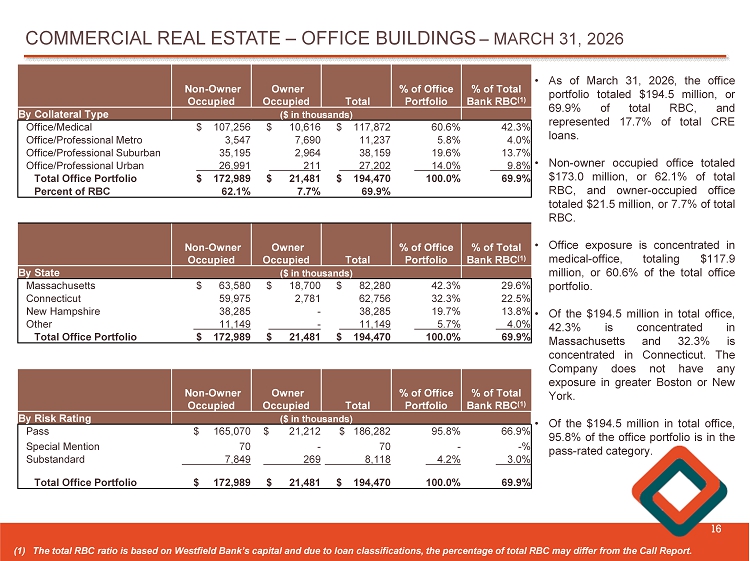

COMMERCIAL REAL ESTATE – OFFICE BUILDINGS – MARCH 31, 2026 16 (1) The total RBC ratio is based on Westfield Bank’s capital and due to loan classifications, the percentage of total RBC may dif fer from the Call Report. % of Total Bank RBC (1) % of Office Portfolio Total Owner Occupied Non - Owner Occupied ($ in thousands) By Collateral Type 42.3% 60.6% $ 117,872 $ 10,616 $ 107,256 Office/Medical 4.0% 5.8% 11,237 7,690 3,547 Office/Professional Metro 13.7% 19.6% 38,159 2,964 35,195 Office/Professional Suburban 9.8% 14.0% 27,202 211 26,991 Office/Professional Urban 69.9% 100.0% $ 194,470 $ 21,481 $ 172,989 Total Office Portfolio 69.9% 7.7% 62.1% Percent of RBC % of Total Bank RBC (1) % of Office Portfolio Total Owner Occupied Non - Owner Occupied ($ in thousands) By State 29.6% 42.3% $ 82,280 $ 18,700 $ 63,580 Massachusetts 22.5% 32.3% 62,756 2,781 59,975 Connecticut 13.8% 19.7% 38,285 - 38,285 New Hampshire 4.0% 5.7% 11,149 - 11,149 Other 69.9% 100.0% $ 194,470 $ 21,481 $ 172,989 Total Office Portfolio % of Total Bank RBC (1) % of Office Portfolio Total Owner Occupied Non - Owner Occupied ($ in thousands) By Risk Rating 66.9% 95.8% $ 186,282 $ 21,212 $ 165,070 Pass - % - 70 - 70 Special Mention 3.0% 4.2% 8,118 269 7,849 Substandard 69.9% 100.0% $ 194,470 $ 21,481 $ 172,989 Total Office Portfolio • As of March 31 , 2026 , the office portfolio totaled $ 194 . 5 million, or 69 . 9 % of total RBC, and represented 17 . 7 % of total CRE loans . • Non - owner occupied office totaled $ 173 . 0 million, or 62 . 1 % of total RBC, and owner - occupied office totaled $ 21 . 5 million, or 7 . 7 % of total RBC . • Office exposure is concentrated in medical - office, totaling $ 117 . 9 million, or 60 . 6 % of the total office portfolio . • Of the $ 194 . 5 million in total office, 42 . 3 % is concentrated in Massachusetts and 32 . 3 % is concentrated in Connecticut . The Company does not have any exposure in greater Boston or New York . • Of the $ 194 . 5 million in total office, 95 . 8 % of the office portfolio is in the pass - rated category .

RESIDENTIAL REAL ESTATE LOANS 17 $784 $805 $828 $857 $866 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $740 $760 $780 $800 $820 $840 $860 $880 At March 31 , 2026 , residential real estate loans, including home equity loans, increased $ 9 . 6 million, or 1 . 1 % , from $ 856 . 9 million, or 39 . 3 % of total loans, at December 31 , 2025 to $ 866 . 4 million, or 39 . 4 % of total loans . At March 31 , 2026 , the Company serviced $ 75 . 3 million in loans sold to the secondary market, with servicing retained, which are not included on the Company’s balance sheet under residential real estate loans . ($ in millions) Residential Real Estate 84% Home Equity 16% Residential Real Estate Loans As of March 31, 2026

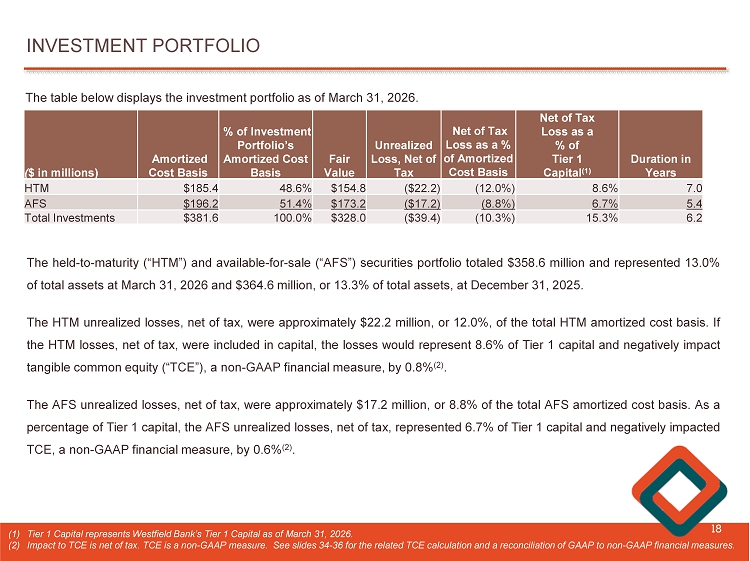

INVESTMENT PORTFOLIO 18 The held - to - maturity (“HTM”) and available - for - sale (“AFS”) securities portfolio totaled $ 358 . 6 million and represented 13 . 0 % of total assets at March 31 , 2026 and $ 364 . 6 million, or 13 . 3 % of total assets, at December 31 , 2025 . The HTM unrealized losses, net of tax, were approximately $ 22 . 2 million, or 12 . 0 % , of the total HTM amortized cost basis . If the HTM losses, net of tax, were included in capital, the losses would represent 8 . 6 % of Tier 1 capital and negatively impact tangible common equity (“TCE”), a non - GAAP financial measure, by 0 . 8 % ( 2 ) . The AFS unrealized losses, net of tax, were approximately $ 17 . 2 million, or 8 . 8 % of the total AFS amortized cost basis . As a percentage of Tier 1 capital, the AFS unrealized losses, net of tax, represented 6 . 7 % of Tier 1 capital and negatively impacted TCE, a non - GAAP financial measure, by 0 . 6 % ( 2 ) . (1) Tier 1 Capital represents Westfield Bank’s Tier 1 Capital as of March 31, 2026. (2) Impact to TCE is net of tax. TCE is a non - GAAP measure. See slides 34 - 36 for the related TCE calculation and a reconciliation o f GAAP to non - GAAP financial measures. The table below displays the investment portfolio as of March 31 , 2026 . Duration in Years Net of Tax Loss as a % of Tier 1 Capital (1) Net of Tax Loss as a % of Amortized Cost Basis Unrealized Loss, Net of Tax Fair Value % of Investment Portfolio’s Amortized Cost Basis Amortized Cost Basis ( $ in millions) 7.0 8.6% (12.0%) ($22.2) $154.8 48.6% $185.4 HTM 5.4 6.7% (8.8%) ($17.2) $173.2 51.4% $196.2 AFS 6.2 15.3% (10.3%) ($39.4) $328.0 100.0% $381.6 Total Investments

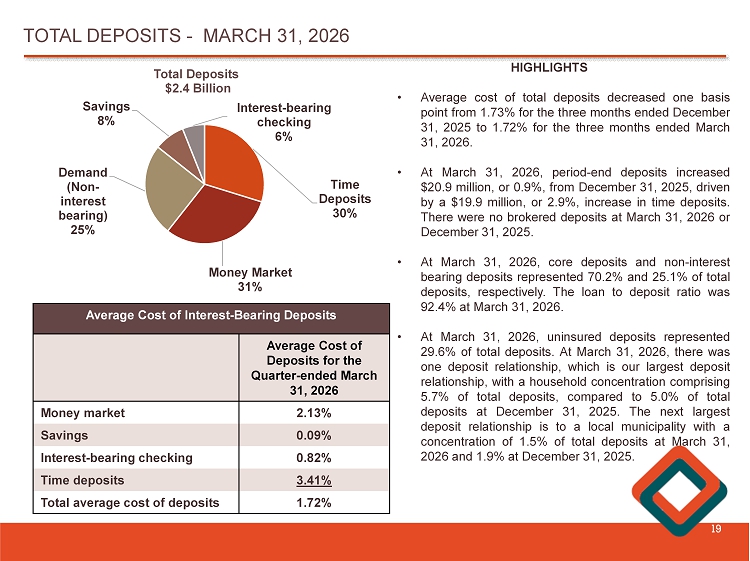

TOTAL DEPOSITS - MARCH 31, 2026 19 Time Deposits 30% Money Market 31% Demand (Non - interest bearing) 25% Savings 8% Interest - bearing checking 6% Total Deposits $2.4 Billion HIGHLIGHTS • Average cost of total deposits decreased one basis point from 1 . 73 % for the three months ended December 31 , 2025 to 1 . 72 % for the three months ended March 31 , 2026 . • At March 31 , 2026 , period - end deposits increased $ 20 . 9 million, or 0 . 9 % , from December 31 , 2025 , driven by a $ 19 . 9 million, or 2 . 9 % , increase in time deposits . There were no brokered deposits at March 31 , 2026 or December 31 , 2025 . • At March 31 , 2026 , core deposits and non - interest bearing deposits represented 70 . 2 % and 25 . 1 % of total deposits, respectively . The loan to deposit ratio was 92 . 4 % at March 31 , 2026 . • At March 31 , 2026 , uninsured deposits represented 29 . 6 % of total deposits . At March 31 , 2026 , there was one deposit relationship, which is our largest deposit relationship, with a household concentration comprising 5 . 7 % of total deposits, compared to 5 . 0 % of total deposits at December 31 , 2025 . The next largest deposit relationship is to a local municipality with a concentration of 1 . 5 % of total deposits at March 31 , 2026 and 1 . 9 % at December 31 , 2025 . Average Cost of Interest - Bearing Deposits Average Cost of Deposits for the Quarter - ended March 31, 2026 2.13% Money market 0.09% Savings 0.82% Interest - bearing checking 3.41% Time deposits 1.72% Total average cost of deposits

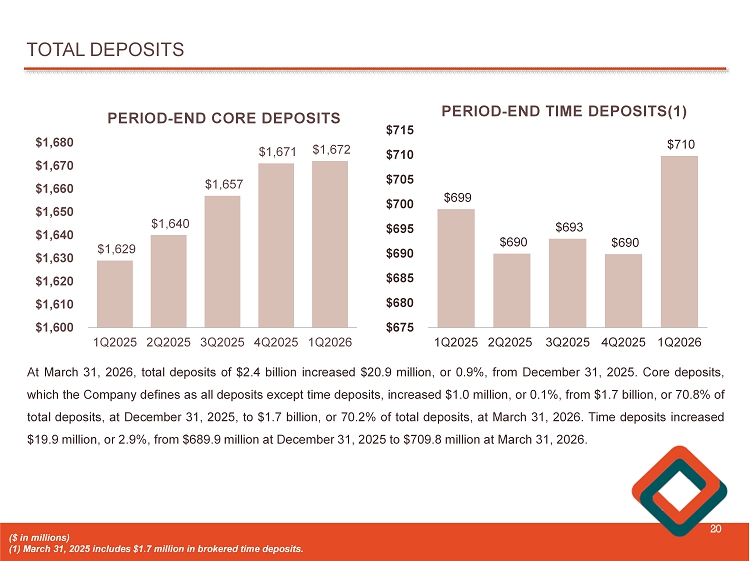

TOTAL DEPOSITS 20 $1,629 $1,640 $1,657 $1,671 $1,672 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $1,600 $1,610 $1,620 $1,630 $1,640 $1,650 $1,660 $1,670 $1,680 PERIOD - END CORE DEPOSITS At March 31 , 2026 , total deposits of $ 2 . 4 billion increased $ 20 . 9 million, or 0 . 9 % , from December 31 , 2025 . Core deposits, which the Company defines as all deposits except time deposits, increased $ 1 . 0 million, or 0 . 1 % , from $ 1 . 7 billion, or 70 . 8 % of total deposits, at December 31 , 2025 , to $ 1 . 7 billion, or 70 . 2 % of total deposits, at March 31 , 2026 . Time deposits increased $ 19 . 9 million, or 2 . 9 % , from $ 689 . 9 million at December 31 , 2025 to $ 709 . 8 million at March 31 , 2026 . $699 $690 $693 $690 $710 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $675 $680 $685 $690 $695 $700 $705 $710 $715 PERIOD - END TIME DEPOSITS(1) ($ in millions) (1) March 31, 2025 includes $1.7 million in brokered time deposits.

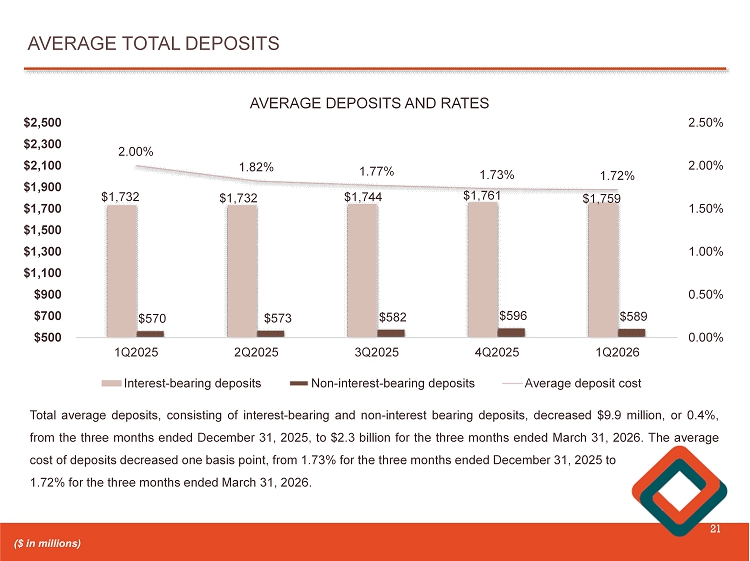

AVERAGE TOTAL DEPOSITS 21 $1,732 $1,732 $1,744 $1,761 $1,759 $570 $573 $582 $596 $589 2.00% 1.82% 1.77% 1.73% 1.72% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $500 $700 $900 $1,100 $1,300 $1,500 $1,700 $1,900 $2,100 $2,300 $2,500 AVERAGE DEPOSITS AND RATES Interest-bearing deposits Non-interest-bearing deposits Average deposit cost Total average deposits, consisting of interest - bearing and non - interest bearing deposits, decreased $ 9 . 9 million, or 0 . 4 % , from the three months ended December 31 , 2025 , to $ 2 . 3 billion for the three months ended March 31 , 2026 . The average cost of deposits decreased one basis point, from 1 . 73 % for the three months ended December 31 , 2025 to 1 . 72 % for the three months ended March 31 , 2026 . ($ in millions)

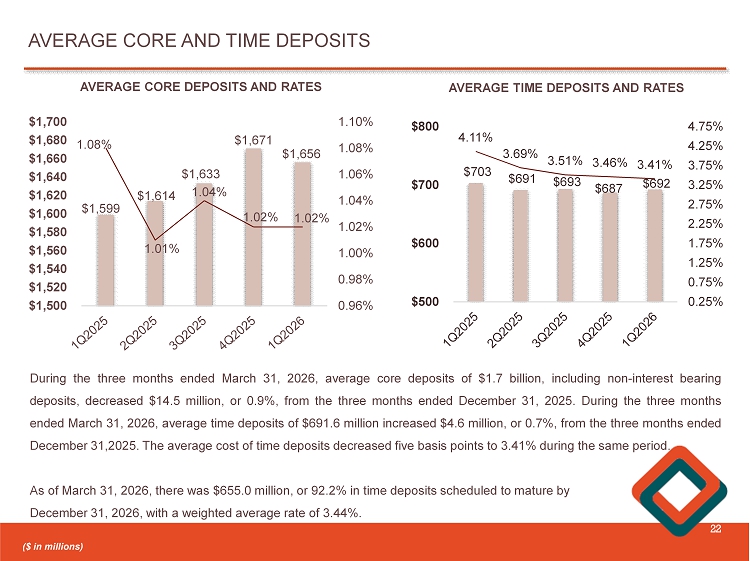

AVERAGE CORE AND TIME DEPOSITS 22 $1,599 $1,614 $1,633 $1,671 $1,656 1.08% 1.01% 1.04% 1.02% 1.02% 0.96% 0.98% 1.00% 1.02% 1.04% 1.06% 1.08% 1.10% $1,500 $1,520 $1,540 $1,560 $1,580 $1,600 $1,620 $1,640 $1,660 $1,680 $1,700 AVERAGE CORE DEPOSITS AND RATES During the three months ended March 31 , 2026 , average core deposits of $ 1 . 7 billion, including non - interest bearing deposits, decreased $ 14 . 5 million, or 0 . 9 % , from the three months ended December 31 , 2025 . During the three months ended March 31 , 2026 , average time deposits of $ 691 . 6 million increased $ 4 . 6 million, or 0 . 7 % , from the three months ended December 31 , 2025 . The average cost of time deposits decreased five basis points to 3 . 41 % during the same period . As of March 31 , 2026 , there was $ 655 . 0 million, or 92 . 2 % in time deposits scheduled to mature by December 31 , 2026 , with a weighted average rate of 3 . 44 % . ($ in millions) $703 $691 $693 $687 $692 4.11% 3.69% 3.51% 3.46% 3.41% 0.25% 0.75% 1.25% 1.75% 2.25% 2.75% 3.25% 3.75% 4.25% 4.75% $500 $600 $700 $800 AVERAGE TIME DEPOSITS AND RATES

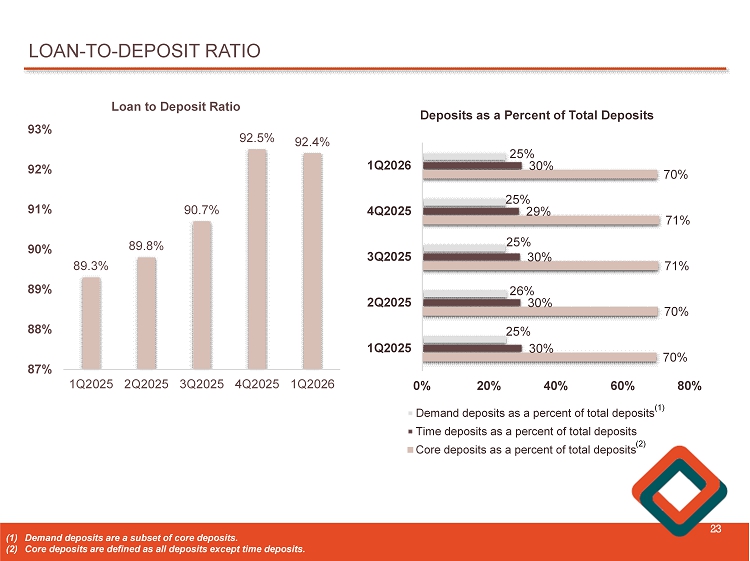

LOAN - TO - DEPOSIT RATIO 23 89.3% 89.8% 90.7% 92.5% 92.4% 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 87% 88% 89% 90% 91% 92% 93% Loan to Deposit Ratio 70% 70% 71% 71% 70% 30% 30% 30% 29% 30% 25% 26% 25% 25% 25% 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 0% 20% 40% 60% 80% Deposits as a Percent of Total Deposits Demand deposits as a percent of total deposits Time deposits as a percent of total deposits Core deposits as a percent of total deposits (1) Demand deposits are a subset of core deposits . (2) Core deposits are defined as all deposits except time deposits . (1) (2)

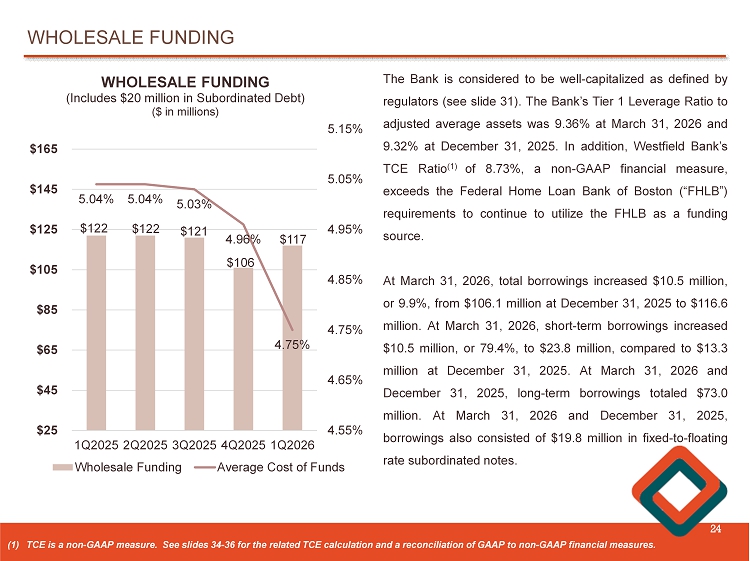

WHOLESALE FUNDING 24 $122 $122 $121 $106 $117 5.04% 5.04% 5.03% 4.96% 4.75% 4.55% 4.65% 4.75% 4.85% 4.95% 5.05% 5.15% 1Q2025 2Q2025 3Q2025 4Q2025 1Q2026 $25 $45 $65 $85 $105 $125 $145 $165 WHOLESALE FUNDING (Includes $20 million in Subordinated Debt) ($ in millions) Wholesale Funding Average Cost of Funds The Bank is considered to be well - capitalized as defined by regulators (see slide 31 ) . The Bank’s Tier 1 Leverage Ratio to adjusted average assets was 9 . 36 % at March 31 , 2026 and 9 . 32 % at December 31 , 2025 . In addition, Westfield Bank’s TCE Ratio ( 1 ) of 8 . 73 % , a non - GAAP financial measure, exceeds the Federal Home Loan Bank of Boston (“FHLB”) requirements to continue to utilize the FHLB as a funding source . At March 31 , 2026 , total borrowings increased $ 10 . 5 million, or 9 . 9 % , from $ 106 . 1 million at December 31 , 2025 to $ 116 . 6 million . At March 31 , 2026 , short - term borrowings increased $ 10 . 5 million, or 79 . 4 % , to $ 23 . 8 million, compared to $ 13 . 3 million at December 31 , 2025 . At March 31 , 2026 and December 31 , 2025 , long - term borrowings totaled $ 73 . 0 million . At March 31 , 2026 and December 31 , 2025 , borrowings also consisted of $ 19 . 8 million in fixed - to - floating rate subordinated notes . (1) TCE is a non - GAAP measure. See slides 34 - 36 for the related TCE calculation and a reconciliation of GAAP to non - GAAP financial measures.

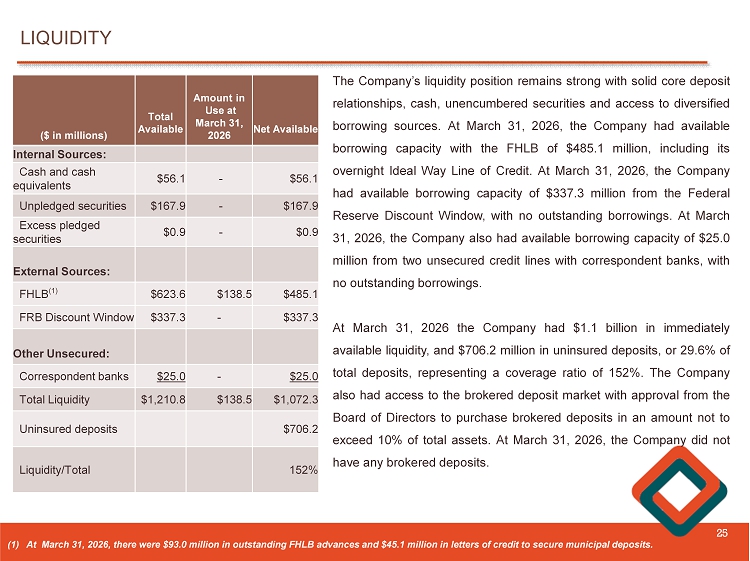

25 The Company’s liquidity position remains strong with solid core deposit relationships, cash, unencumbered securities and access to diversified borrowing sources . At March 31 , 2026 , the Company had available borrowing capacity with the FHLB of $ 485 . 1 million, including its overnight Ideal Way Line of Credit . At March 31 , 2026 , the Company had available borrowing capacity of $ 337 . 3 million from the Federal Reserve Discount Window, with no outstanding borrowings . At March 31 , 2026 , the Company also had available borrowing capacity of $ 25 . 0 million from two unsecured credit lines with correspondent banks, with no outstanding borrowings . At March 31 , 2026 the Company had $ 1 . 1 billion in immediately available liquidity, and $ 706 . 2 million in uninsured deposits, or 29 . 6 % of total deposits, representing a coverage ratio of 152 % . The Company also had access to the brokered deposit market with approval from the Board of Directors to purchase brokered deposits in an amount not to exceed 10 % of total assets . At March 31 , 2026 , the Company did not have any brokered deposits . LIQUIDITY Net Available Amount in Use at March 31, 2026 Total Available ($ in millions) Internal Sources: $56.1 - $56.1 Cash and cash equivalents $167.9 - $167.9 Unpledged securities $0.9 - $0.9 Excess pledged securities External Sources: $485.1 $138.5 $623.6 FHLB (1) $337.3 - $337.3 FRB Discount Window Other Unsecured: $25.0 - $25.0 Correspondent banks $1,072.3 $138.5 $1,210.8 Total Liquidity $706.2 Uninsured deposits 152% Liquidity/Total (1) At March 31 , 2026 , there were $ 93 . 0 million in outstanding FHLB advances and $ 45 . 1 million in letters of credit to secure municipal deposits .

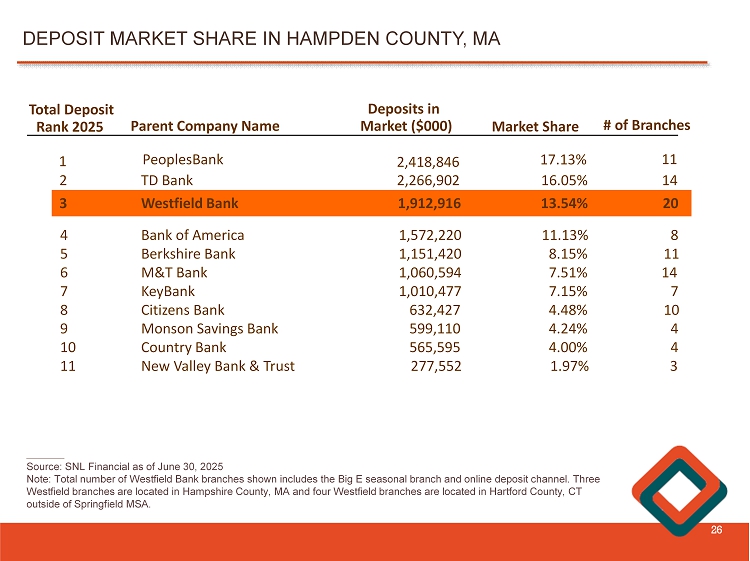

________ Source: SNL Financial as of June 30, 2025 Note: Total number of Westfield Bank branches shown includes the Big E seasonal branch and online deposit channel. Three Westfield branches are located in Hampshire County, MA and four Westfield branches are located in Hartford County, CT outside of Springfield MSA. DEPOSIT MARKET SHARE IN HAMPDEN COUNTY, MA 26 Total Deposit Rank 2025 Parent Company Name Deposits in Market ($000) Market Share # of Branches 1 PeoplesBank 2,418,846 17.13% 11 1,762,519 13.1% 20 3 Westfield Bank 1,912,916 13.54% 20 2 TD Bank 2,266,902 16.05% 14 4 Bank of America 1,572,220 11.13% 8 5 Berkshire Bank 1,151,420 8.15% 11 6 M&T Bank 1,060,594 7.51% 14 7 KeyBank 1,010,477 7.15% 7 8 Citizens Bank 632,427 4.48% 10 9 Monson Savings Bank 599,110 4.24% 4 10 Country Bank 565,595 4.00% 4 11 New Valley Bank & Trust 277,552 1.97% 3

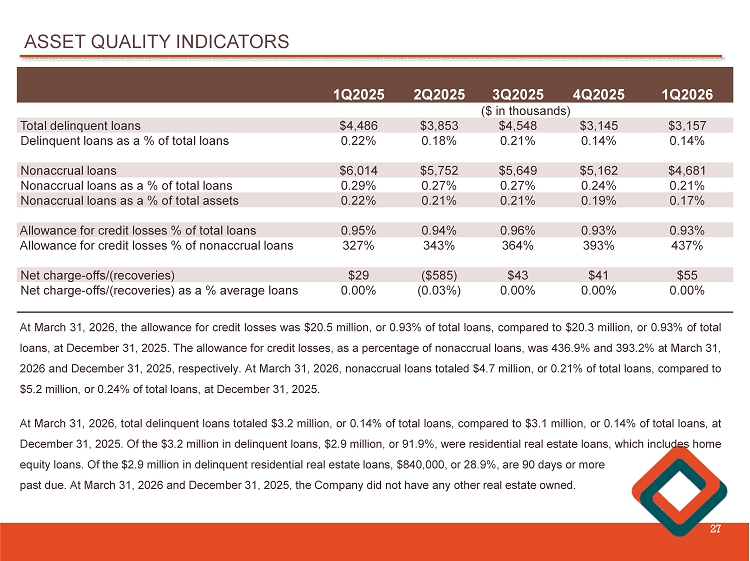

ASSET QUALITY INDICATORS 27 1Q2026 4Q2025 3Q2025 2Q2025 1Q2025 ($ in thousands) $3,157 $3,145 $4,548 $3,853 $4,486 Total delinquent loans 0.14% 0.14% 0.21% 0.18% 0.22% Delinquent loans as a % of total loans $4,681 $5,162 $5,649 $5,752 $6,014 Nonaccrual loans 0.21% 0.24% 0.27% 0.27% 0.29% Nonaccrual loans as a % of total loans 0.17% 0.19% 0.21% 0.21% 0.22% Nonaccrual loans as a % of total assets 0.93% 0.93% 0.96% 0.94% 0.95% Allowance for credit losses % of total loans 437% 393% 364% 343% 327% Allowance for credit losses % of nonaccrual loans $55 $41 $43 ($585) $29 Net charge - offs/(recoveries) 0.00% 0.00% 0.00% (0.03%) 0.00% Net charge - offs/(recoveries) as a % average loans At March 31 , 2026 , the allowance for credit losses was $ 20 . 5 million, or 0 . 93 % of total loans, compared to $ 20 . 3 million, or 0 . 93 % of total loans, at December 31 , 2025 . The allowance for credit losses, as a percentage of nonaccrual loans, was 436 . 9 % and 393 . 2 % at March 31 , 2026 and December 31 , 2025 , respectively . At March 31 , 2026 , nonaccrual loans totaled $ 4 . 7 million, or 0 . 21 % of total loans, compared to $ 5 . 2 million, or 0 . 24 % of total loans, at December 31 , 2025 . At March 31 , 2026 , total delinquent loans totaled $ 3 . 2 million, or 0 . 14 % of total loans, compared to $ 3 . 1 million, or 0 . 14 % of total loans, at December 31 , 2025 . Of the $ 3 . 2 million in delinquent loans, $ 2 . 9 million, or 91 . 9 % , were residential real estate loans, which includes home equity loans . Of the $ 2 . 9 million in delinquent residential real estate loans, $ 840 , 000 , or 28 . 9 % , are 90 days or more past due . At March 31 , 2026 and December 31 , 2025 , the Company did not have any other real estate owned .

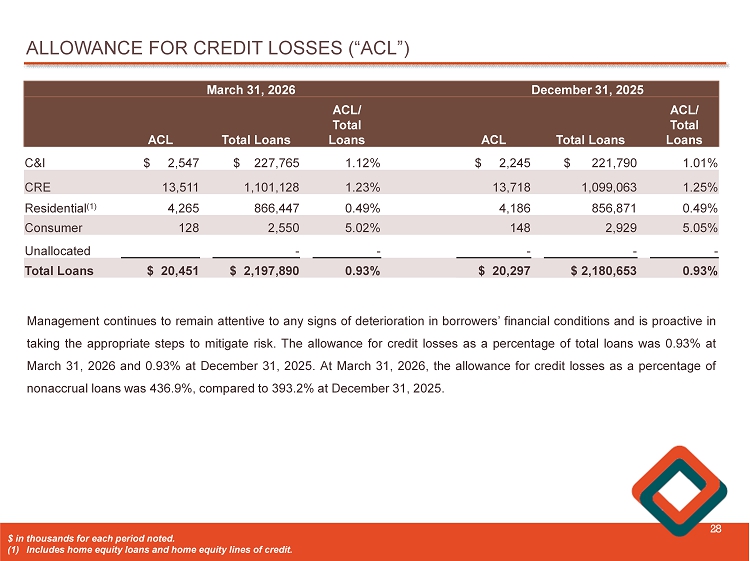

ALLOWANCE FOR CREDIT LOSSES (“ACL”) 28 Management continues to remain attentive to any signs of deterioration in borrowers’ financial conditions and is proactive in taking the appropriate steps to mitigate risk . The allowance for credit losses as a percentage of total loans was 0 . 93 % at March 31 , 2026 and 0 . 93 % at December 31 , 2025 . At March 31 , 2026 , the allowance for credit losses as a percentage of nonaccrual loans was 436 . 9 % , compared to 393 . 2 % at December 31 , 2025 . December 31, 2025 March 31, 2026 ACL/ Total Loans Total Loans ACL ACL/ Total Loans Total Loans ACL 1.01% $ 221,790 $ 2,245 1.12% $ 227,765 $ 2,547 C&I 1.25% 1,099,063 13,718 1.23% 1,101,128 13,511 CRE 0.49% 856,871 4,186 0.49% 866,447 4,265 Residential (1) 5.05% 2,929 148 5.02% 2,550 128 Consumer - - - - - Unallocated 0.93% $ 2,180,653 $ 20,297 0.93% $ 2,197,890 $ 20,451 Total Loans $ in thousands for each period noted . (1) Includes home equity loans and home equity lines of credit .

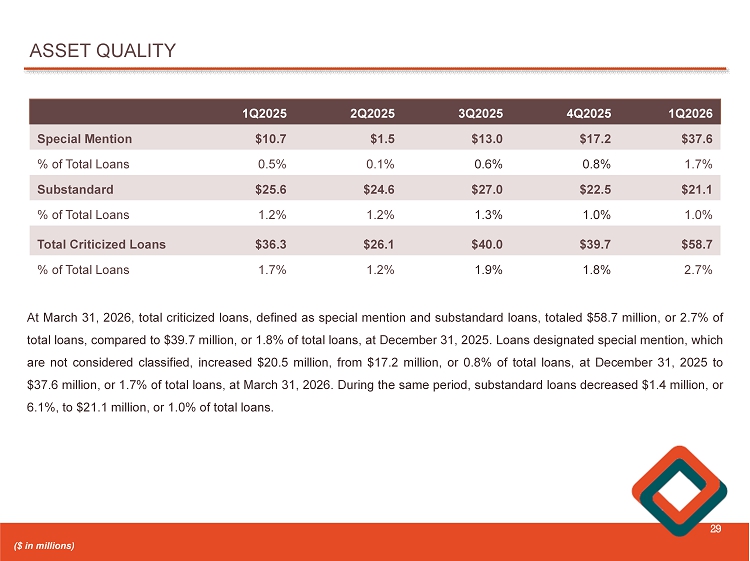

ASSET QUALITY 29 1Q2026 4Q2025 3Q2025 2Q2025 1Q2025 $37.6 $17.2 $13.0 $1.5 $10.7 Special Mention 1.7% 0.8% 0.6% 0.1% 0.5% % of Total Loans $21.1 $22.5 $27.0 $24.6 $25.6 Substandard 1.0% 1.0% 1.3% 1.2% 1.2% % of Total Loans $58.7 $39.7 $40.0 $26.1 $36.3 Total Criticized Loans 2.7% 1.8% 1.9% 1.2% 1.7% % of Total Loans At March 31 , 2026 , total criticized loans, defined as special mention and substandard loans, totaled $ 58 . 7 million, or 2 . 7 % of total loans, compared to $ 39 . 7 million, or 1 . 8 % of total loans, at December 31 , 2025 . Loans designated special mention, which are not considered classified, increased $ 20 . 5 million, from $ 17 . 2 million, or 0 . 8 % of total loans, at December 31 , 2025 to $ 37 . 6 million, or 1 . 7 % of total loans, at March 31 , 2026 . During the same period, substandard loans decreased $ 1 . 4 million, or 6 . 1 % , to $ 21 . 1 million, or 1 . 0 % of total loans . ($ in millions)

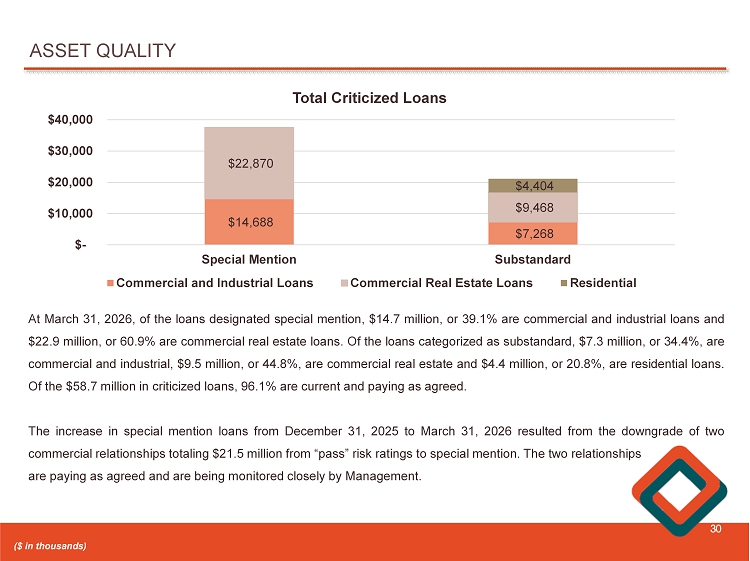

ASSET QUALITY 30 ($ in thousands) At March 31 , 2026 , of the loans designated special mention, $ 14 . 7 million, or 39 . 1 % are commercial and industrial loans and $ 22 . 9 million, or 60 . 9 % are commercial real estate loans . Of the loans categorized as substandard, $ 7 . 3 million, or 34 . 4 % , are commercial and industrial, $ 9 . 5 million, or 44 . 8 % , are commercial real estate and $ 4 . 4 million, or 20 . 8 % , are residential loans . Of the $ 58 . 7 million in criticized loans, 96 . 1 % are current and paying as agreed . The increase in special mention loans from December 31 , 2025 to March 31 , 2026 resulted from the downgrade of two commercial relationships totaling $ 21 . 5 million from “pass” risk ratings to special mention . The two relationships are paying as agreed and are being monitored closely by Management . $14,688 $7,268 $22,870 $9,468 $4,404 $- $10,000 $20,000 $30,000 $40,000 Special Mention Substandard Total Criticized Loans Commercial and Industrial Loans Commercial Real Estate Loans Residential

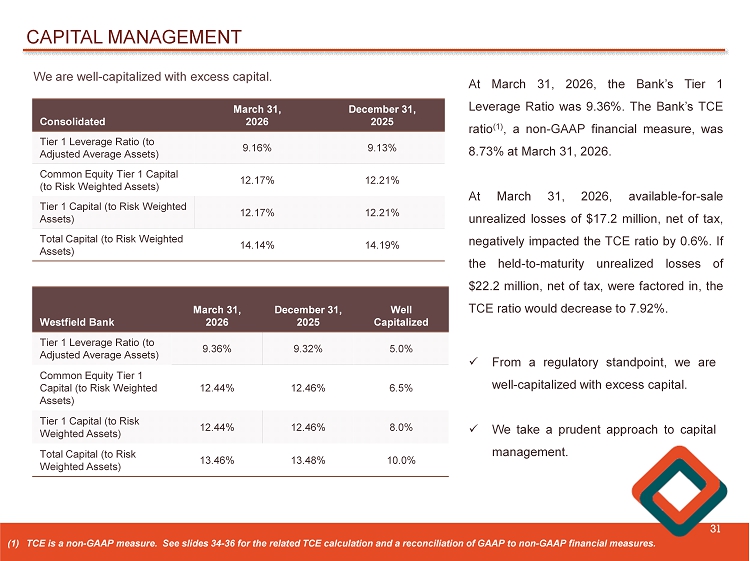

CAPITAL MANAGEMENT 31 We are well - capitalized with excess capital. December 31, 2025 March 31, 2026 Consolidated 9.13% 9.16% Tier 1 Leverage Ratio (to Adjusted Average Assets) 12.21% 12.17% Common Equity Tier 1 Capital (to Risk Weighted Assets) 12.21% 12.17% Tier 1 Capital (to Risk Weighted Assets) 14.19% 14.14% Total Capital (to Risk Weighted Assets) At March 31 , 2026 , the Bank’s Tier 1 Leverage Ratio was 9 . 36 % . The Bank’s TCE ratio ( 1 ) , a non - GAAP financial measure, was 8 . 73 % at March 31 , 2026 . At March 31 , 2026 , available - for - sale unrealized losses of $ 17 . 2 million, net of tax, negatively impacted the TCE ratio by 0 . 6 % . If the held - to - maturity unrealized losses of $ 22 . 2 million, net of tax, were factored in, the TCE ratio would decrease to 7 . 92 % . Well Capitalized December 31, 2025 March 31, 2026 Westfield Bank 5.0% 9.32% 9.36% Tier 1 Leverage Ratio (to Adjusted Average Assets) 6.5% 12.46% 12.44% Common Equity Tier 1 Capital (to Risk Weighted Assets) 8.0% 12.46% 12.44% Tier 1 Capital (to Risk Weighted Assets) 10.0% 13.48% 13.46% Total Capital (to Risk Weighted Assets) (1) TCE is a non - GAAP measure. See slides 34 - 36 for the related TCE calculation and a reconciliation of GAAP to non - GAAP financial measures. x From a regulatory standpoint, we are well - capitalized with excess capital . x We take a prudent approach to capital management .

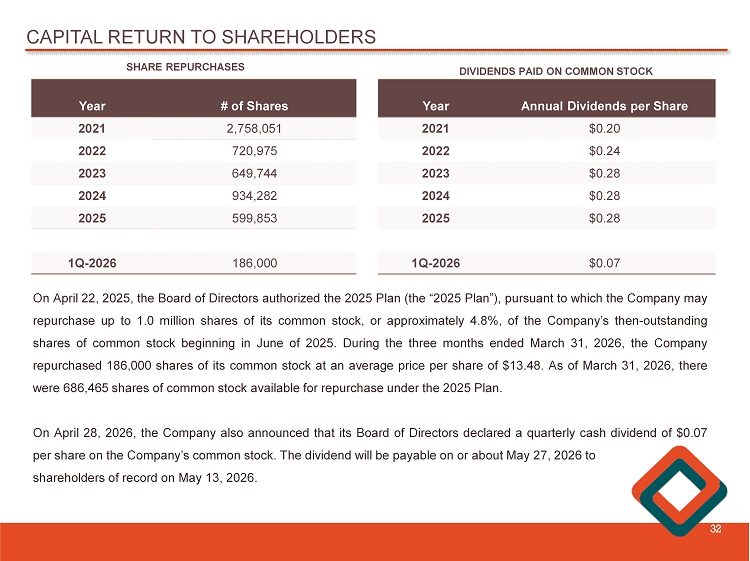

CAPITAL RETURN TO SHAREHOLDERS 32 # of Shares Year 2,758,051 2021 720,975 2022 649,744 2023 934,282 2024 599,853 2025 186,000 1Q - 2026 Annual Dividends per Share Year $0.20 2021 $0.24 2022 $0.28 2023 $0.28 2024 $0.28 2025 $0.07 1Q - 2026 SHARE REPURCHASES DIVIDENDS PAID ON COMMON STOCK On April 22 , 2025 , the Board of Directors authorized the 2025 Plan (the “ 2025 Plan”), pursuant to which the Company may repurchase up to 1 . 0 million shares of its common stock, or approximately 4 . 8 % , of the Company’s then - outstanding shares of common stock beginning in June of 2025 . During the three months ended March 31 , 2026 , the Company repurchased 186 , 000 shares of its common stock at an average price per share of $ 13 . 48 . As of March 31 , 2026 , there were 686 , 465 shares of common stock available for repurchase under the 2025 Plan . On April 28 , 2026 , the Company also announced that its Board of Directors declared a quarterly cash dividend of $ 0 . 07 per share on the Company’s common stock . The dividend will be payable on or about May 27 , 2026 to shareholders of record on May 13 , 2026 .

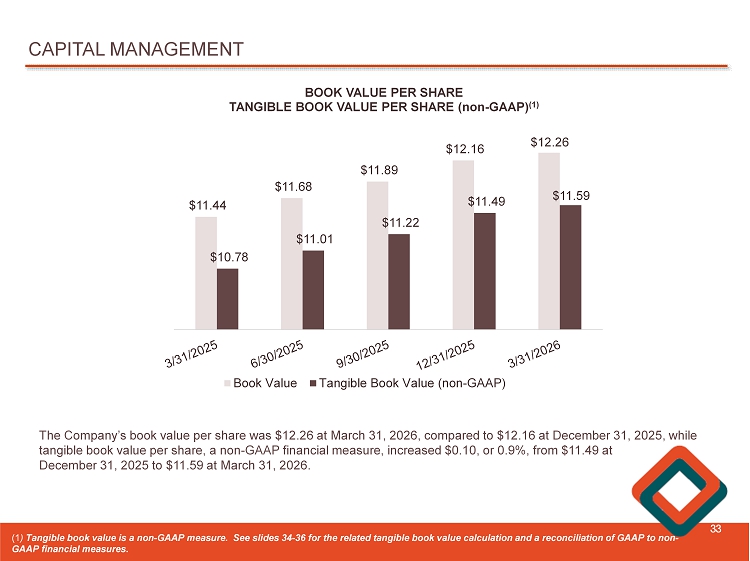

CAPITAL MANAGEMENT 33 $11.44 $11.68 $11.89 $12.16 $12.26 $10.78 $11.01 $11.22 $11.49 $11.59 BOOK VALUE PER SHARE TANGIBLE BOOK VALUE PER SHARE (non - GAAP) (1) Book Value Tangible Book Value (non-GAAP) The Company’s book value per share was $12.26 at March 31, 2026, compared to $12.16 at December 31, 2025, while tangible book value per share, a non - GAAP financial measure, increased $0.10, or 0.9%, from $11.49 at December 31, 2025 to $11.59 at March 31, 2026. (1 ) Tangible book value is a non - GAAP measure. See slides 34 - 36 for the related tangible book value calculation and a reconciliatio n of GAAP to non - GAAP financial measures .

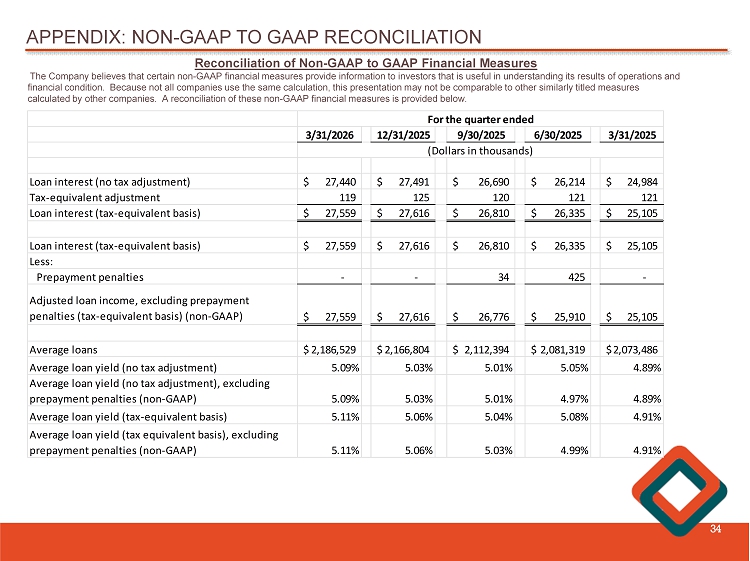

APPENDIX: NON - GAAP TO GAAP RECONCILIATION 34 Reconciliation of Non - GAAP to GAAP Financial Measures The Company believes that certain non - GAAP financial measures provide information to investors that is useful in understanding i ts results of operations and financial condition. Because not all companies use the same calculation, this presentation may not be comparable to other simil arly titled measures calculated by other companies. A reconciliation of these non - GAAP financial measures is provided below. 3/31/2026 12/31/2025 9/30/2025 6/30/2025 3/31/2025 Loan interest (no tax adjustment) 27,440$ 27,491$ 26,690$ 26,214$ 24,984$ Tax-equivalent adjustment 119 125 120 121 121 Loan interest (tax-equivalent basis) 27,559$ 27,616$ 26,810$ 26,335$ 25,105$ Loan interest (tax-equivalent basis) 27,559$ 27,616$ 26,810$ 26,335$ 25,105$ Less: Prepayment penalties - - 34 425 - Adjusted loan income, excluding prepayment penalties (tax-equivalent basis) (non-GAAP) 27,559$ 27,616$ 26,776$ 25,910$ 25,105$ Average loans 2,186,529$ 2,166,804$ 2,112,394$ 2,081,319$ 2,073,486$ Average loan yield (no tax adjustment) 5.09% 5.03% 5.01% 5.05% 4.89% Average loan yield (no tax adjustment), excluding prepayment penalties (non-GAAP) 5.09% 5.03% 5.01% 4.97% 4.89% Average loan yield (tax-equivalent basis) 5.11% 5.06% 5.04% 5.08% 4.91% Average loan yield (tax equivalent basis), excluding prepayment penalties (non-GAAP) 5.11% 5.06% 5.03% 4.99% 4.91% For the quarter ended (Dollars in thousands)

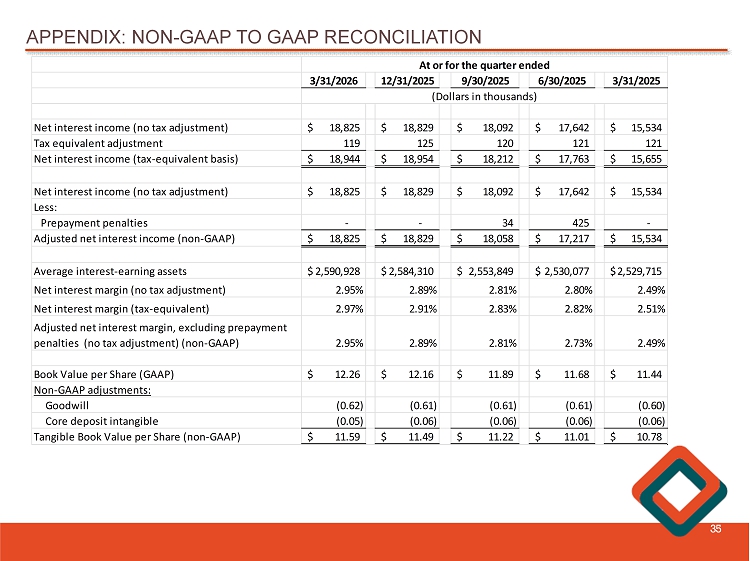

APPENDIX: NON - GAAP TO GAAP RECONCILIATION 35 3/31/2026 12/31/2025 9/30/2025 6/30/2025 3/31/2025 Net interest income (no tax adjustment) 18,825$ 18,829$ 18,092$ 17,642$ 15,534$ Tax equivalent adjustment 119 125 120 121 121 Net interest income (tax-equivalent basis) 18,944$ 18,954$ 18,212$ 17,763$ 15,655$ Net interest income (no tax adjustment) 18,825$ 18,829$ 18,092$ 17,642$ 15,534$ Less: Prepayment penalties - - 34 425 - Adjusted net interest income (non-GAAP) 18,825$ 18,829$ 18,058$ 17,217$ 15,534$ Average interest-earning assets 2,590,928$ 2,584,310$ 2,553,849$ 2,530,077$ 2,529,715$ Net interest margin (no tax adjustment) 2.95% 2.89% 2.81% 2.80% 2.49% Net interest margin (tax-equivalent) 2.97% 2.91% 2.83% 2.82% 2.51% Adjusted net interest margin, excluding prepayment penalties (no tax adjustment) (non-GAAP) 2.95% 2.89% 2.81% 2.73% 2.49% Book Value per Share (GAAP) 12.26$ 12.16$ 11.89$ 11.68$ 11.44$ Non-GAAP adjustments: Goodwill (0.62) (0.61) (0.61) (0.61) (0.60) Core deposit intangible (0.05) (0.06) (0.06) (0.06) (0.06) Tangible Book Value per Share (non-GAAP) 11.59$ 11.49$ 11.22$ 11.01$ 10.78$ At or for the quarter ended (Dollars in thousands)

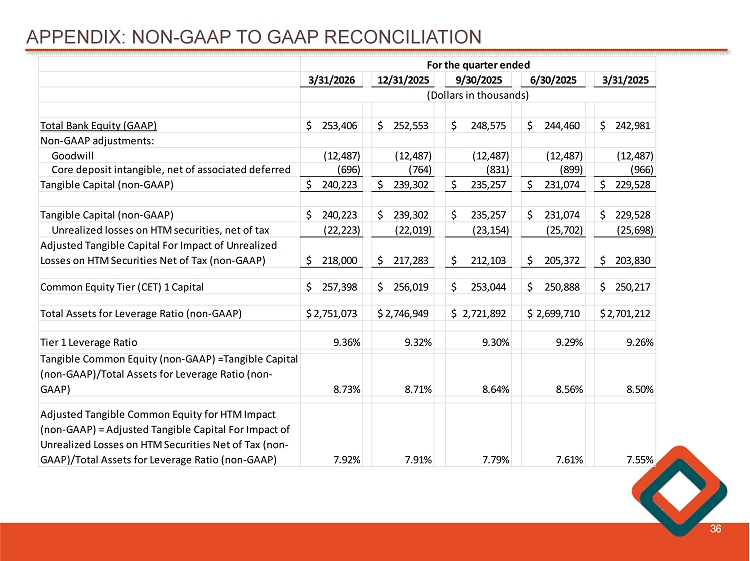

APPENDIX: NON - GAAP TO GAAP RECONCILIATION 36 3/31/2026 12/31/2025 9/30/2025 6/30/2025 3/31/2025 Total Bank Equity (GAAP) 253,406$ 252,553$ 248,575$ 244,460$ 242,981$ Non-GAAP adjustments: Goodwill (12,487) (12,487) (12,487) (12,487) (12,487) Core deposit intangible, net of associated deferred (696) (764) (831) (899) (966) Tangible Capital (non-GAAP) 240,223$ 239,302$ 235,257$ 231,074$ 229,528$ Tangible Capital (non-GAAP) 240,223$ 239,302$ 235,257$ 231,074$ 229,528$ Unrealized losses on HTM securities, net of tax (22,223) (22,019) (23,154) (25,702) (25,698) Adjusted Tangible Capital For Impact of Unrealized Losses on HTM Securities Net of Tax (non-GAAP) 218,000$ 217,283$ 212,103$ 205,372$ 203,830$ Common Equity Tier (CET) 1 Capital 257,398$ 256,019$ 253,044$ 250,888$ 250,217$ Total Assets for Leverage Ratio (non-GAAP) 2,751,073$ 2,746,949$ 2,721,892$ 2,699,710$ 2,701,212$ Tier 1 Leverage Ratio 9.36% 9.32% 9.30% 9.29% 9.26% Tangible Common Equity (non-GAAP) =Tangible Capital (non-GAAP)/Total Assets for Leverage Ratio (non- GAAP) 8.73% 8.71% 8.64% 8.56% 8.50% Adjusted Tangible Common Equity for HTM Impact (non-GAAP) = Adjusted Tangible Capital For Impact of Unrealized Losses on HTM Securities Net of Tax (non- GAAP)/Total Assets for Leverage Ratio (non-GAAP) 7.92% 7.91% 7.79% 7.61% 7.55% For the quarter ended (Dollars in thousands)

WESTFIELD BANK “WHAT BETTER BANKING’S ALL ABOUT” James C. Hagan , President and Chief Executive Officer Guida R. Sajdak , Executive Vice President and Chief Financial Officer Meghan Hibner , First Vice President and Investor Relations Officer 37 141 Elm Street, Westfield, MA