Exhibit 99.1

NICOLA MINING INC.

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED

December 31, 2025

April 27, 2026

TABLE OF CONTENTS

ADVISORIES | 1 |

GLOSSARY OF TERMS | 5 |

CORPORATE STRUCTURE | 9 |

GENERAL DEVELOPMENT OF THE BUSINESS OF THE COMPANY | 9 |

DESCRIPTION OF THE BUSINESS OF THE COMPANY | 12 |

MINERAL PROJECTS | 15 |

RISK FACTORS | 19 |

DESCRIPTION OF CAPITAL STRUCTURE | 28 |

Market for Securities | 29 |

ESCROWED SECURITIES | 30 |

DIVIDENDS AND DISTRIBUTIONS | 30 |

DIRECTORS AND OFFICERS | 30 |

AUDIT COMMITTEE | 33 |

Legal Proceedings AND Regulatory actions | 35 |

INTERESTS OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 35 |

corporate governance | 35 |

AUDITOR, TRANSFER AGENT AND REGISTRAR | 39 |

MATERIAL CONTRACTS | 39 |

INTERESTS OF EXPERTS | 39 |

ADDITIONAL INFORMATION | 39 |

| |

SCHEDULe | |

| |

SCHEDULE A – Audit Committee Charter | |

| |

Schedule B – Compensation Committee Charter | |

| |

Schedule C – Corporate Governance Charter | |

ADVISORIES

In this Annual Information Form (“AIF”), unless otherwise specified or if the context otherwise requires, references to “we”, “us”, “our”, “its”, the “Company” or Nicola” mean Nicola Mining Inc. and its subsidiary, Huldra Properties Inc. The information in this AIF is stated as at December 31, 2025 unless otherwise indicated. For additional information and details, readers are referred to the audited consolidated financial statements for the year ended December 31, 2025 and notes that follow, as well as the accompanying annual MD&A (as defined herein), which are available on the Canadian Securities Administrator’s SEDAR+ System at www.sedarplus.ca.

Cautionary Statement Regarding Forward-Looking Information and Statements

This AIF contains forward-looking information and statements (collectively, “forward-looking statements”). These forward-looking statements relate to Nicola’s current expectations, estimates and projections as to future events or Nicola’s future performance and are provided to allow readers a better understanding of Nicola’s business and prospects and may not be suitable for other purposes. All statements, other than statements of historical fact, may be considered forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek”, “anticipate”, “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “targeting”, “intend”, “could”, “might”, “should”, “believe” and similar expressions. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in, or suggested by, such forward-looking statements. Nicola believes the expectations reflected in the forward-looking statements included in this AIF are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward-looking statements should not be unduly relied upon. These statements speak only as of the date of this AIF and are expressly qualified, in their entirety, by this cautionary statement. Nicola assumes no obligation to revise or update these statements except as required pursuant to applicable securities laws

In particular, this AIF contains forward-looking statements pertaining to the following:

· | expectations regarding the Company’s future operations and strategic direction; |

· | the Company’s reliance on key management personnel and the potential impact of changes to senior leadership; |

· | the Company’s current and proposed development initiatives, operational plans and timelines; |

· | anticipated costs, schedules and availability of services necessary to support the Company’s projects and operations; |

· | environmental considerations, compliance obligations and potential liabilities arising from exploration, development, extraction and related activities; |

· | risks related to property title, as well as the acquisition, maintenance and renewal of significant licenses, concessions, and permits; |

· | the Company’s capital structure, liquidity position and funding needs for both ongoing and future initiatives; |

· | the Company’s ability to secure additional financing or access capital markets on terms that are commercially reasonable and in line with business objectives; and |

· | other statements under the heading “Management’s Discussion and Analysis”. |

With respect to forward-looking statements contained in this AIF, the Company has made assumptions regarding, among other things:

· | the Company’s continued access to adequate services and supplies, as supported by disclosures elsewhere in this document; |

· | the persistence of favourable economic conditions, stable commodity prices, and suitable foreign exchange and interest rates, as well as ongoing access to capital and debt markets; |

· | the ongoing availability of a qualified workforce to support the Company’s operations; |

Nicola Mining Inc. | Annual Information Form Page 1

· | that exploration schedules and associated capital costs remain accurately estimated and are not materially impacted by unforeseen events or adverse weather conditions, consistent with the considerations outlined in this document; |

· | that any environmental or other legal proceedings or disputes, if initiated against the Company, are satisfactorily resolved, and that the Company maintains stable relationships with its business partners and relevant governmental authorities; |

· | the Company’s capacity to secure and maintain financing on terms that are acceptable and in line with its operational objectives; |

· | the influence of prevailing and emerging competition within the industry; |

· | potential changes to applicable laws, regulations and rules impacting the Company’s activities, as may be further detailed in this document; |

· | the Company’s ability to attract and retain key personnel critical to its success; and |

· | the absence of material adverse developments in the industry or within the broader Canadian and global economy, including those attributable to or arising from evolving global tariff policies, increased trade barriers and their resulting impact on international trade flows and broader economic stability. |

These forward-looking statements are based upon certain material factors, assumptions and analyses that were applied in drawing a conclusion or making a forecast or projection, including management’s experience and perceptions of historical trends, current market conditions and expected future developments, the timing and amount of capital and other expenditures, and other factors believed to be reasonable in the circumstances.

By their nature, forward-looking statements are subject to inherent risks and uncertainties which give rise to the possibility that expectations, forecasts, predictions, projections or conclusions will not prove to be accurate, that assumptions may not be correct, and that objectives, strategic goals and priorities will not be achieved. A variety of material factors, many of which are beyond the control of the Company, could cause actual results to differ materially from current expectations of estimated or anticipated events or results. The risks, uncertainties and other factors that could influence actual results include, but are not limited to:

· | the Company’s potential challenges in managing its operations effectively; |

· | broad economic and business conditions, including those arising from shifting global tariff policies, increased trade barriers and their resulting effects on both international trade flows and overall economic stability; |

· | the presence of negative operating cash flow within the Company; |

· | the Company’s capacity to secure additional financing necessary to carry out the activities outlined in the AIF; |

· | possible increases in both capital and operating expenditures; |

· | fluctuations in commodity prices and in the market price of the Company’s Common Shares; |

· | inherent risks associated with the mineral exploration industry as a whole; |

· | the Company’s ability to adhere to relevant governmental regulations and standards; |

· | risks stemming from regulatory changes or governmental actions; |

· | competition within the mineral exploration sector; and |

· | the other risk factors set out in the Company’s short form base shelf prospectus dated January 29, 2026, a copy of which has been filed on SEDAR+ at www.sedarplus.ca. |

Readers are cautioned that the foregoing list of factors is not exhaustive and that other factors may emerge from time to time. It is not possible for management to predict all such factors and to assess in advance the impact of each such factor on the business of the Company, or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statement. Readers are also cautioned to consider these and other factors, uncertainties and potential events carefully and not to put undue reliance on forward-looking statements. Although the forward-looking statements contained in this AIF are based upon what management of the Company currently believe to be reasonable assumptions, actual results, performance or achievements could differ materially from those expressed in, or implied by, the forward-looking

Nicola Mining Inc. | Annual Information Form Page 2

statements and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking statements will transpire or occur. The forward-looking statements contained herein are made as of the date of this AIF and, other than as specifically required by law, the Company does not assume any obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which such statement is made, or to reflect the occurrence of unanticipated events, whether as a result of new information, future events or results, or otherwise.

The Company has included the above summary of assumptions and risks related to forward-looking statements contained in this AIF in order to provide investors with a more complete perspective on the Company’s current and future operations and such information may not be appropriate for other purposes.

Additional information on these and other factors is available in the reports filed by the Company with Canadian securities regulators and available under the Company’s profile on SEDAR+ at www.sedarplus.ca. The forward-looking statements and information contained in this AIF are made as of the date hereof.

Readers are cautioned that the preparation of financial statements in accordance with international financial reporting standards in Canada requires management to make certain judgments and estimates that affect the reported amounts of assets, liabilities, revenues and expenses. These estimates may change, having either a negative or positive effect on net earnings as further information becomes available and as the economic environment changes. The information contained in this AIF, including the documents incorporated by reference herein, identifies additional factors that could affect the operating results and performance of the Company. Readers are encouraged to carefully consider such factors.

Readers are also cautioned against placing undue reliance on forward-looking statements, which are given as of the date expressed in this AIF, or the MD&A disclosure incorporated by reference herein, and not to use future-oriented information or financial outlooks for anything other than their intended purpose. The forward-looking statements contained herein are expressly qualified in their entirety by this cautionary statement. The Company undertakes no obligation to publicly update or revise any forward-looking statements in this AIF or the MD&A or other disclosure incorporated by reference herein, whether as a result of new information, future events or otherwise, except as required by law.

Technical Information

Unless otherwise noted, the disclosure contained in this AIF of a scientific or technical nature for the New Craigmont Project is based on the technical report prepared by Kevin Wells, P.Geo., and James N. Gray, P.Geo. dated May 21, 2020 and entitled “NI 43-101 Technical Report on the Preliminary Copper Resource for the Southern Dump and 3060 Portal Dumps” prepared in accordance with the requirements of NI 43-101.

Any mineral reserve or resource figures, and scientific, technical, or projected economic information or estimates referred to in this AIF are estimates, and no assurances can be given that the information will materialize. Such information is based on expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. While the Company believes that the information included in this AIF is well established, the information by its nature is imprecise and depends, to a certain extent, upon statistical inferences which may ultimately prove unreliable. If such estimates of such information are inaccurate or are reduced in the future, this could have a material adverse impact on the Company.

Reference should be made to the full text of the Technical Report which has been filed with Canadian securities regulatory authorities pursuant to NI 43-101 and is available for review under the Company’s profile on SEDAR+ at www.sedarplus.ca.

William Whitty, P. Geo., the VP of Exploration of the Company and a “Qualified Person” under NI 43-101, reviewed and approved the written scientific and technical disclosure contained in this AIF.

Nicola Mining Inc. | Annual Information Form Page 3

Monetary References

Except as otherwise indicated, all dollar amounts in this AIF are expressed in Canadian dollars and references to $ are to Canadian dollars. References to US$ are to United States dollars.

Securities Reference

Except as otherwise indicated, all information contained in this AIF relating to the securities of the Company is presented on a post-Consolidation (as defined herein) basis.

GLOSSARY OF TERMS

In this AIF, unless otherwise indicated or the context otherwise requires, the following terms shall have the indicated meanings. Words importing the singular include the plural and vice versa and words importing any gender include all genders. A reference to an agreement means the agreement as it may be amended, supplemented or restated from time to time.

“ADSs” | means American Depository Shares. |

“ADS Warrant” | means an ADS purchase warrant of the Company. |

“Affiliate” | means a company that is affiliated with another company as described below. A company is an Affiliate of another company if (a) one of them is the subsidiary of the other or (b) each of them is controlled by the same person. A company is “controlled” by a person if (a) voting securities of the company are held, other than by way of security only, by or for the benefit of that person and (b) the voting securities, if voted, entitle the person to elect a majority of the directors of the company. A person beneficially owns securities that are beneficially owned by (a) a company controlled by that person or (b) an Affiliate of that person or an Affiliate of any company controlled by that person. |

“AIF” | means this Annual Information Form dated April 27, 2026. |

“Applicants” | has the meaning ascribed to it under the heading Directors and Officers – Corporate Cease Trade orders, Bankruptcies, Penalties or Sanctions. |

“ARO” | means asset retirement obligations. |

“Audit Committee” | means the audit committee of the Company. |

“Audit Committee Charter” | means the audit committee charter. |

“Author” | means Kevin Wells, P. Geo. and James N. Gray, P. Geo., the authors of the Technical Report. |

“BCBCA” | means the Business Corporations Act (British Columbia), and the regulations thereunder, as amended from time to time. |

“BCSC” | British Columbia Securities Commission. |

“Blue Lagoon” | means Blue Lagoon Resources Inc. |

“Board” | means the board of directors of the Company. |

“CEO” | means chief executive officer. |

“CFO” | means chief financial officer. |

Nicola Mining Inc. | Annual Information Form Page 4

“Common Share” | means a common share in the capital of the Company. |

Nicola Mining Inc. | Annual Information Form Page 5

“company” | unless specifically indicated otherwise, means a corporation, incorporated association or organization, body corporate, partnership, trust, association or other entity other than an individual. |

“Company” or “Nicola” | means Nicola Mining Inc., a company incorporated under the laws of the Province of British Columbia. |

“Compensation Committee” | means the compensation committee of the Company. |

“Compensation Committee Charter” | means the compensation committee charter adopted by the Board on July 7, 2023. |

“Consolidation” | means the consolidation of the Common Shares which occurred on November 17, 2023, whereby the Company consolidated its then issued and outstanding Common Shares on the basis of one (1) Common Share for every two (2) Common Shares. |

“Corporate Governance Committee” | means the ccorporate governance committee of the Company. |

“Corporate Governance Committee Charter” | means the corporate governance committee charter adopted by the Board. |

“Court” | means the Supreme Court of British Columbia. |

“CSE” | means the Canadian Securities Exchange, operated by CNSX Markets Inc. |

“Dominion Creek Gold Property” | refers to a property consisting of eight mineral claims situated near Prince George, British Columbia, in which the Company holds a 50% ownership interest acquired from High Range Exploration Ltd. |

“DSUs” | means deferred share units of the Company. |

“Equity Incentive Plan” | means the equity incentive plan adopted by the Board on May 12, 2022, and as ratified by shareholders of the Company on July 11, 2025. |

“High Range” | Means High Range Exploration Ltd. |

“Huldra Properties” | means Huldra Properties Inc., the Company’s wholly-owned subsidiary, incorporated pursuant to the BCBCA. |

“IFRS” | means IFRS Accounting Standards as issued by the International Accounting Standards Board, applied on a consistent basis with prior periods. |

“IP” | means induced polarization. |

“LiDar” | means light detection and ranging laser system. |

“MD&A” | means Form 51-102F1 – Management’s Discussion & Analysis. |

“Merritt Mill” | refers to the Company’s milling operations in Merritt, British Columbia. |

Nicola Mining Inc. | Annual Information Form Page 6

“Mines Act” | means the Mines Act (British Columbia), and the regulations thereunder, as amended from time to time. |

“Nasdaq” | means the Nasdaq Capital Market. |

“New Craigmont Project” | refers to a property consisting of 22 mineral claims and 10 mineral leases situated near Lower Nicola, British Columbia. |

“NGOs” | means certain non-governmental organizations. |

“NI 43-101” | means National Instrument 43-101 – Standards of Disclosure for Mineral Projects. |

“NI 51-102” | means National Instrument 51-102 – Continuous Disclosure Obligations. |

“NI 52-110” | means National Instrument 52-110 – Audit Committees. |

“NI 58-101” | means National Instrument 58‐101 – Disclosure of Corporate Governance Practices. |

“Ocean Partners UK” | Ocean Partners UK Limited, a United Kingdom-based metals trading firm. |

“Ocean Partners Holdings” | Ocean Partners Holdings Company. |

“Options” | means options to purchase Common Shares. |

“Oremex” | means Oremex Silver Inc. |

“Osisko” | means Osisko Development Corp. |

“Performance-Based Awards” | means RSUs, PSUs and DSUs collectively. |

“PSUs” | means performance share units of the Company. |

“Qualified Person” | has the meaning ascribed to such term in NI 43-101. |

“Reporting Issuer” | has the meaning ascribed to such term in the Securities Act (British Columbia), as amended. |

“RSUs” | means restricted share units of the Company. |

“SEDAR+” | means the System for Electronic Document Analysis and Retrieval. |

“Technical Report” | means the technical report of the Author dated May 21, 2020 entitled “NI 43-101 Technical Report on the Preliminary Copper Resource for the Southern Dump and 3060 Portal Dumps” prepared in accordance with the requirements of NI 43-101. |

“Treasure Mountain Project” | refers to a property consisting of 30 mineral claims and 1 mineral lease situated near Hope, British Columbia. |

“TSX” | means the Toronto Stock Exchange. |

Nicola Mining Inc. | Annual Information Form Page 7

“TSXV” | means the TSX Venture Exchange Inc. |

“Units” | means a security of the Company comprised of one or more of any combination of Common Shares, Warrants, or other securities of the Company, issued together as a single unit pursuant to the terms of the applicable offering. |

“United States”, “USA” or “US” | means, collectively, the United States of America, its territories and possessions. |

“Warrant” | means a Common Share purchase warrant of the Company. |

“Warrant Share” | means a Common Share issued or issuable by the Company upon the valid exercise of a Warrant in accordance with its terms. |

“ZTEM” | means Z-Axis tipper electromagnetic. |

Nicola Mining Inc. | Annual Information Form Page 8

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated by registration of its Memorandum and Articles pursuant to the provisions of the Company Act (British Columbia) on March 31, 1980 as “Huldra Silver Corporation”, with an authorized capital of 10,000,000 Common Shares without par value.

On April 21, 1980, the Company altered its Memorandum to change its name to “Huldra Silver Inc.” and to increase its authorized capital to 50,000,000 Common Shares without par value.

On April 9, 2005, the Company transitioned from the Company Act (British Columbia) to the BCBCA. At that time the Company filed its Notice of Articles, which effectively replaced its Memorandum, and adopted new Articles.

On June 23, 2010, the Company’s shareholders approved an amendment to the Company’s Notice of Articles to remove the pre-existing company provisions and to increase the authorized capital of the Company to an unlimited number of Common Shares without par value. On the same date, the Company’s shareholders approved an amendment to the Company’s Articles to bring the provisions of the Articles in line with the provisions of the BCBCA. On July 12, 2010, the Company filed a Notice of Alteration with respect to the amendment to the Notice of Articles.

On June 1, 2015, the Company changed its name from “Huldra Silver Inc.” to “Nicola Mining Inc.” and consolidated its issued and outstanding Common Shares on the basis of one (1) Common Share for every five (5) Common Shares.

On November 17, 2023, the Company completed the Consolidation whereby it consolidated its issued and outstanding Common Shares on the basis of one (1) Common Share for every two (2) Common Shares outstanding prior to the completion of the Consolidation.

The Company’s head office is located at Suite 1212 – 1030 West Georgia Street, Vancouver, British Columbia, V6E 2Y3, and its registered office is located at Suite 2501, 550 Burrard Street, Vancouver, British Columbia, V6C 2B5.

The Common Shares are listed and traded on the TSXV under the symbol “NIM” and the Frankfurt Securities Exchange under the symbol “HLI”. On April 14, 2026, the ADSs were listed and traded on Nasdaq under the symbol “NICM”. On November 3, 2021, the Company obtained Depository Trust Company eligibility in United States, and its Common Shares are quoted on OTCQB operated by the OTC Markets Group Inc. under the ticker “HUSIF”. The Company is a Reporting Issuer in British Columbia, Alberta and Ontario and files its continuous disclosure documents on SEDAR+ at www.sedarplus.ca. The Company’s filings through SEDAR+ are not incorporated by reference in this AIF.

Intercorporate Relationships

As of the date of this AIF, the Company has one wholly-owned subsidiary, Huldra Properties Inc. Huldra Properties was created pursuant to the BCBCA by an amalgamation between 0913103 B.C. Ltd. and Huldra Properties on January 1, 2016. Huldra Properties’ head office is located at 3329 Aberdeen Road, Lower Nicola, British Columbia, V0K 1Y0 and its registered office is located at Suite 2501, 550 Burrard Street, Vancouver, British Columbia, V6C 2B5.

GENERAL DEVELOPMENT OF THE BUSINESS OF THE COMPANY

Overview

Nicola is a junior exploration and custom milling company focused on the acquisition, exploration and development of mineral properties in British Columbia, Canada. The Company operates the Merritt Mill and holds interests in the New Craigmont Project, Treasure Mountain Project and Dominion Creek Gold Property.

Nicola Mining Inc. | Annual Information Form Page 9

Three Year History

A detailed description on the significant developments of the business of the Company for the past three years is set out below.

Recent Developments since the Fiscal Year Ended December 31, 2025

On January 29, 2026, the Company issued 5,512,001 Units for gross proceeds of $4,960,800 pursuant to a private placement offering. Each Unit consisted of one Common Share and one transferable Warrant, with each Warrant entitling the holder to purchase one Common Share at a price of $1.10 per Common Share for a period of three years following the date of issuance, provided that the expiry of the Warrants can be accelerated if the closing price of the Common Shares on the TSXV is $1.70 or greater for a minimum of ten consecutive trading days, and a notice of acceleration is provided in accordance with the terms of the Warrants.

On April 14, 2026, the Company completed its underwritten public offering in the United States which consisted of 930,233 ADSs and Warrants to purchase 930,233 ADSs at an offering price of US$6.45 per ADS and accompanying Warrant. Each ADS offered represents 12 Common Shares of the Company. The gross proceeds, before deducting underwriter discounts, and commissions and offering expenses, were US$6.0 million. The Warrants have an exercise price of CAD$12.2213 per ADS, are exercisable immediately upon issuance and will expire on the fifth anniversary of the original issuance date. On April 17, 2026, the Company issued an additional 139,534 ADSs at the public offering price of US$6.45 per ADS, for total gross proceeds of approximately US$900K pursuant to the partial exercise of the underwriters’ over-allotment option in connection with Company’s public offering of ADSs and Warrants.

Fiscal Year Ended December 31, 2025

On January 3, 2025, the Company converted the remaining outstanding principal and interest totaling $49,421 from a convertible debenture, scheduled to mature on January 9, 2025, into 246,995 Common Shares.

On March 12, 2025, the Company completed a non-brokered private placement issuing 4,038,955 Units at $0.28 per Unit, for an aggregate gross proceeds of $1,130,907. The Company paid $98,455 of finder’s fees, resulting in net proceeds of $1,032,452. Each Unit consisted of one Common Share and one-half of one Warrant, with each whole Warrant entitling the holder thereof to purchase one Warrant Share at a price of $0.40 per Warrant Share for a period of three years from the closing of the offering. The Warrants are subject to acceleration in the event that, during their exercise period and after the resale restrictions on the Common Shares have expired, the Common Shares trade at a closing price of $0.60 or greater per share on the TSXV (or any other exchange where they are listed) for ten consecutive trading days, in which case the Company may, by giving notice through a press release, accelerate the expiry date of the Warrants to the thirtieth (30th) day after such notice. On July 21, 2025, the Company gave notice of the acceleration of the Warrants issued on March 12, 2025. By the accelerated expiry date of August 20, 2025, all of the 2,019,477 Warrants then outstanding had been exercised, resulting in total proceeds of $807,791.

On July 1, 2025, the Company granted 400,000 Options to an employee of the Company, which Options are exercisable into one Common Share at a price of $0.495 per Common Share until July 1, 2030.

Nicola Mining Inc. | Annual Information Form Page 10

On July 17, 2025, the Company closed its non-brokered private placement in which it sold an aggregate of 4,350,000 Units at a price of $0.50 per Unit for gross proceeds of $2,175,000. Each Unit consists of one flow-through Common Share and one-half of one non-flow-through Warrant. Each Warrant is exercisable at a price of $0.65 and expires on July 17, 2027.

On December 3, 2025, the Company granted 2,850,000 Options to an directors, officers, consultants and employees of the Company, which Options are exercisable into one Common Share at a price of $1.00 per Common Share until December 3, 2030.

On December 3, 2025, the Company granted an aggregate of 1,015,000 RSUs to certain directors, officers and employees of the Company, which RSUs vest into Common Shares on January 1, 2027.

During the year ended December 31, 2025, debenture holders converted the principal and settled interest of $4,803,067 for the convertible debentures that matured on November 21, 2025, into 26,088,257 common shares.

During the year ended December 31, 2025, the Company issued 2,952,500 common shares from stock options exercised for total proceeds of $811,150.

During the year ended December 31, 2025, the Company issued 1,000,000 common shares to settle RSUs vested.

Fiscal Year Ended December 31, 2024

On December 3, 2024, the Company completed a flow-through private placement offering, pursuant to which it issued an aggregate of 1,641,790 Common Shares at a price of $0.335 per Common Share for aggregate gross proceeds of $550,000.

On December 18, 2024, the Company granted 500,000 Options to a consultant of the Company, which Options are exercisable into one Common Share at a price of $0.30 per Common Share until December 18, 2029.

On December 18, 2024, the Company granted an aggregate of 1,000,000 RSUs to certain directors, officers and employees of the Company, which RSUs vest into Common Shares on December 18, 2025.

On April 12, 2024, the Company completed a non-brokered private placement by the issuance of 5,499,994 Common Shares at a price of $0.23 per Common Share for aggregate gross proceeds of $1,264,999, which Common Shares were issued on a flow-through basis pursuant to the Income Tax Act (Canada).

On April 18, 2024, the Company granted an aggregate of 3,000,000 Options to certain directors, officers, consultants and employees, which Options are exercisable at a price of $0.265 until April 18, 2029.

On March 19, 2024, Warwick Bay resigned as the CFO and secretary and Sam Wong was appointed as the CFO and secretary of the Company.

Fiscal Year Ended December 31, 2023

On November 28, 2023, the Company issued 650,000 common shares at a value of $0.20 per share in connection with the exercise of 650,000 stock options for total proceeds of $130,000.

On November 21, 2023, a second tranche debenture holder elected to convert a total of $32,710 at a conversion price of $0.17 and was issued 213,529 common shares in accordance with terms of the debentures.

On November 17, 2023, the Company completed the Consolidation whereby it consolidated its issued and outstanding Common Shares on the basis of one (1) Common Share for every two (2) Common Shares.

On October 23, 2023, a second tranche debenture holder elected to convert a total of $234,776 at a conversion price of $0.17 and was issued 1,357,079 common shares in accordance with terms of the debentures.

Nicola Mining Inc. | Annual Information Form Page 11

On October 3, 2023, the Company granted 200,000 Options to one employee, which Options are exercisable into one Common Share at a price of $0.35 per Common Share until October 3, 2028.

On August 3, 2023, the Company granted 200,000 Options to one employee, which Options are exercisable into one Common Share at a price of $0.30 per Common Share until August 3, 2028.

On July 26, 2023, the Company granted 2,000,000 Options to certain directors, officers, consultants and employes, which Options are exercisable into one Common Share at a price of $0.36 per Common Share until July 26, 2028.

On May 18 and 19, 2023, the Company issued 113,834 common shares at a value of $0.20 per share in settlement of interest of $22,767 of May 20, 2020 debentures.

On May 19, 2023, a May 20, 2020 Debenture holder elected to convert a total of $45,000 at a conversion price of $0.20 and was issued 225,000 common shares in accordance with terms of the debentures.

On May 18, 2023, May 20, 2020 Debenture holders elected to convert a total of $185,000 at a conversion price of $0.20 and the Company issued 925,000 common shares in accordance with terms of the debentures.

On May 2, 2023, the Company granted 100,000 Options to one consultant, which Options are exercisable into one Common Share at a price of $0.30 per Common Share until May 2, 2028.

On April 19, 2023, the Company issued 500,000 common shares at a value of $0.16 per share in connection with the exercise of 500,000 stock options for gross proceeds of $80,000.

On March 15, 2023, the Company issued 121,321 common shares on conversion of $20,000 of convertible debentures issued November 21, 2022, exercised at $0.17.

On February 14, 2023, the Company issued 40,262 common shares on conversion of $8,000 of convertible debentures issued January 9, 2023, exercised at $0.20.

On January 13, 2023, the Company issued 8,000,000 common shares at a value of $0.25 per share for gross proceeds of $2,000,000.

Significant Acquisitions

During the most recently completed financial year ended December 31, 2025, Nicola did not complete any acquisition that would be considered a “significant acquisition” as defined under Part 8 of NI 51-102. Accordingly, the Company has not filed a Form 51-102F4 – Business Acquisition Report in respect of any acquisition during the year.

DESCRIPTION OF THE BUSINESS OF THE COMPANY

General

Nicola is a junior resource company engaged in two principal business segments:

1. | Mineral Exploration and Development |

2. | Custom Milling Operations |

These segments are considered reportable under IFRS as they represent distinct revenue-generating activities with separate operational and financial characteristics.

Mineral Exploration and Development

The mineral exploration and development segment encompasses Nicola’s efforts to identify, acquire and advance mineral properties in British Columbia. The Company’s principal exploration assets include the New Craigmont Project, the Treasure Mountain Project

Nicola Mining Inc. | Annual Information Form Page 12

and the Dominion Creek Gold Property. These projects are all in the exploration or pre-commercial development stage and have not yet reached commercial production and are further described below.

New Craigmont Project

The New Craigmont Project, a historic copper mine site near Merritt, British Columbia, is the Company’s flagship asset. It is permitted under Mine Permit M-68 and has been the focus of extensive geophysical surveys, soil sampling and diamond drilling. A mineral resource estimate was completed in 2020 for the Southern Mining Terraces and 3060 Portal Dump areas.

Treasure Mountain Project

The Treasure Mountain Project, located near Hope, British Columbia, is permitted for the removal of up to 60,000 tonnes of silver/lead/zinc mill feed annually but remains in care and maintenance. In June of 2025, the Company received a multi-year area-based exploration permit which allows for five years of exploration and plans to commence exploration at the MB Zone.

Dominion Creek Gold Property

The Dominion Creek Gold Property, in which Nicola holds a 50% interest and a 75% economic benefit through a profit-sharing agreement, received its bulk sample permit in March 2025. Nicola and its partner, High Range Exploration Ltd., are preparing for potential mining and milling activities in the current year.

The Company conducts its own exploration activities, including geological mapping, drilling, and geophysical surveys while subcontracting specialized services such as LiDAR and assay testing. The projects are not yet at the commercial production stage, and no sales have been made from these properties. The next steps toward commercialization include further drilling, resource definition and economic assessments. The Company has not disclosed specific cost estimates or timelines for achieving commercial production.

Custom Milling Operations

The custom milling operations segment is centered around the Merritt Mill, a fully permitted and operational facility located near Merritt, British Columbia. The mill is licensed to process up to 200 tonnes per day of silver, lead and gold ore. Nicola provides toll milling services to third-party mining companies, producing concentrate that is sold to offtake partners such as Ocean Partners UK. In 2025, the Company generated $1.54 million in milling revenue and $0.8 million from gravel, ash, soil and other income which compares to $818,000 in milling revenue and $1.97 million from gravel, ash, soil and other income in 2024 and $1.62 million and $8.15 million, respectively, in 2023. All revenue was derived from sales to external customers; there were no sales to joint ventures, equity-accounted entities or controlling shareholders. The method of providing milling services involves receiving ore shipments from clients, processing the ore through crushing, grinding and flotation circuits at the Merritt Mill, and producing gold and silver concentrate. The concentrate is then shipped to offtake partners for sale. The Company also provides ancillary services such as storage, logistics coordination, and compliance with environmental and safety regulations.

The Merritt Mill has processed ore from clients including Blue Lagoon, Talisker Resources Ltd. and Osisko under profit-sharing agreements. The facility underwent upgrades in 2023 and 2024 to support increased throughput and quality control. The Company continues to seek new custom milling contracts to support its cash flow and maintain operational flexibility.

Production and Services

The Company’s custom milling services are conducted at its wholly-owned Merritt Mill, located near Merritt, British Columbia. The Merritt Mill is a fully permitted facility authorized under the Mines Act to process up to 200 tonnes per day of silver, lead and gold ore. The mill was originally constructed in 2012 and has undergone extensive modifications since 2017, including upgrades completed in 2023 to enhance its processing capabilities. The Company provides toll milling services to third-party mining companies, whereby it processes ore into concentrate on behalf of clients. The concentrate is then sold to offtake partners, such as Ocean Partners UK, under purchase agreements. Nicola has entered into profit-sharing agreements with clients including Blue Lagoon and Osisko, under which it receives a share of the proceeds from the sale of processed concentrate.

The method of providing milling services involves receiving ore shipments from clients, processing the ore through crushing, grinding and flotation circuits at the Merritt Mill, and producing gold and silver concentrate. The concentrate is then shipped to offtake partners

Nicola Mining Inc. | Annual Information Form Page 13

for sale. The Company also provides ancillary services such as storage, logistics coordination and compliance with environmental and safety regulations.

In addition to milling, Nicola is actively engaged in mineral exploration and development at its New Craigmont, Treasure Mountain and Dominion Creek properties. These projects are in the exploration stage and are not yet producing. The Company’s exploration activities include geological mapping, soil and rock sampling, geophysical surveys (including ZTEM and IP), and diamond drilling. These activities are conducted by Nicola’s in-house geological team, with certain specialized services subcontracted to third-party providers. The Company has received multi-year area-based permits that allow for extensive exploration activities, including trenching and drilling, through to 2027.

Nicola Mining Inc. | Annual Information Form Page 14

The Company does not currently produce any mineral products for sale from its exploration properties.

Specialized Skill and Knowledge

Nicola’s operations require specialized geological, metallurgical and engineering expertise, particularly in mineral exploration, resource modelling and custom milling. The Company relies on experienced geologists for exploration planning and execution, including geophysical surveys, soil sampling, and diamond drilling. Metallurgical knowledge is essential for operating and optimizing the Merritt Mill, which processes complex ore types into concentrate. Nicola also depends on regulatory and permitting expertise to navigate environmental and mining legislation. These skills are sourced through a combination of in-house personnel and external consultants. The Company has been able to access the required expertise without material constraint.

Competitive Conditions

The Company operates in a highly competitive environment. In mineral exploration, it competes with junior and senior mining companies for land, capital, and talent—many with greater resources. In custom milling, Nicola’s Merritt Mill competes with other processors on capacity, turnaround and pricing. Its competitive edge lies in its fully permitted 200 tpd facility, flexible profit-sharing agreements and established client relationships. However, limited financial resources and reliance on third-party contracts constrain its position. Continued success depends on exploration outcomes, operational efficiency, and access to capital.

Cycles

The Company’s business segments, mineral exploration and custom milling, are subject to seasonal and cyclical influences. Exploration activities are typically concentrated in the spring through autumn months due to weather and ground conditions in British Columbia, which limit access and drilling during winter. Custom milling operations at the Merritt Mill are influenced by the availability and scheduling of third-party mill feed contracts, which can vary throughout the year. As such, both revenue and expenses may fluctuate significantly between quarters depending on project activity and contract timing.

Economic Dependence

Nicola is substantially dependent on a key offtake and financing agreement with Ocean Partners UK, a metals trading firm. This agreement governs the sale of gold and silver concentrate produced at the Company’s Merritt Mill and includes a revolving prepayment facility. Under the amended agreement signed on July 12, 2022, Ocean Partners UK agreed to purchase concentrate from Nicola and increased the revolving prepayment facility from US$500,000 to US$3,000,000. Nicola has drawn down US$750,000 under this facility, which was repaid December 29, 2022. The agreement provides critical working capital support and a guaranteed buyer for concentrate produced under custom milling contracts, including those with Blue Lagoon and Osisko. The Company’s reliance on this agreement is significant, as Ocean Partners UK accounted for 100% of Nicola’s milling revenue in both 2023 and 2024. The agreement also enables Nicola to process third-party ore at its Merritt Mill, which is a core component of its business model.

The Company also entered into a Mining and Milling Profit Share Agreement with High Range for the Dominion Creek Property. This agreement entitles Nicola to a 75% economic interest in the project and includes provisions for funding initial development and processing ore at the Merritt Mill.

These contracts are essential to Nicola’s operations and financial viability, providing both revenue generation and access to capital.

Changes to Contracts

Nicola Mining Inc. | Annual Information Form Page 15

The Company does not currently anticipate any material renegotiation or termination of contracts that would significantly affect its business. However, the Company’s operations rely heavily on custom milling agreements, particularly with Ocean Partners UK. Any changes to this offtake agreement could impact revenue and working capital. Similarly, profit-sharing agreements with High Range and Osisko are integral to the Merritt Mill’s utilization. While no changes are expected, any termination or renegotiation of these agreements could adversely affect operational continuity and financial performance.

Environmental Protection

Nicola is subject to environmental protection regulations under the Mines Act and related provincial legislation. These requirements have a material impact on the Company’s capital expenditures, primarily through its asset retirement obligations or “ARO”, which totaled $13.8 million as of December 31, 2025. The ARO reflects estimated future reclamation and closure costs for the Merritt Mill and Treasure Mountain Project, including tailings management and site remediation.

In 2025, the Company recognized a $0.9 million reduction in ARO due to changes in estimates, partially offset by $0.5 million in accretion expense. These environmental liabilities directly affect the Company’s net loss and working capital position. While no immediate capital outlays were required in 2025, the obligations are expected to result in significant future expenditures over the next 8 to 15 years.

Environmental compliance also influences the Company’s competitive position, as it must maintain sufficient financial assurance (e.g., $1.4 million in restricted cash) to satisfy regulatory bonding requirements. These requirements may limit flexibility in capital allocation and increase the cost of operations relative to peers with lower environmental liabilities.

Nicola remains committed to maintaining compliance and proactively managing its environmental responsibilities.

Employees

As of the date of this AIF, the Company has 25 employees.

MINERAL PROJECTS

The Company’s principal mineral project is the New Craigmont Project in Lower Nicola, British Columbia. For the purposes of mineral project disclosure required to be included in this AIF, the New Craigmont Project is the Company’s sole material mineral project.

In addition to the New Craigmont Project, the Company holds a 100% interest in 30 mineral claims and 1 mineral lease comprising the Treasure Mountain Project located near Hope, British Columbia, subject to a 2% net smelter royalty. The Company also holds a 50% interest in 8 mineral claims comprising the Dominion Creek Gold Property located near Prince George, British Columbia.

New Craigmont Project

The following is an updated reproduction of the summary section from the Technical Report. Definitions contained in this section shall have the meanings ascribed to such definitions in the Technical Report and may not match definitions used elsewhere in this AIF. The Technical Report was prepared in accordance with NI 43-101 and has been filed with the securities regulatory authorities in Alberta, British Columbia and Ontario. Portions of the following information are based on assumptions, qualifications and procedures which are not fully described herein.

The Technical Report is incorporated by reference into this AIF. Readers are cautioned that the following summary should be read in the context of the qualifying statements, procedures and accompanying discussion within the complete Technical Report, and this summary is qualified in its entirety by the Technical Report.

Nicola Mining Inc. | Annual Information Form Page 16

Property Description and Location

The Craigmont Project is in southern British Columbia, 18 km northwest of the city of Merritt. The UTM coordinates for the Craigmont Project are 5563500 North and 648500 East (geographic projection: NAD 83, Zone 10N). Access to the property is provided by paved and gravel roads. Additional mineral claims totaling 828 hectares were staked in December 2019, as a result the Craigmont Project now consists of 22 mineral tenures and 10 mineral leases with a total area of 10,913 hectares.

Ownership

The Craigmont Property is currently 100% owned by Nicola On March 3, 2011, Nicola agreed to buy all the outstanding shares of Craigmont Holdings Ltd. in consideration for certain cash and share payments.

On November 19, 2015, Nicola acquired the remaining shares of Craigmont Holdings Ltd. for a 2.0% net smelter royalty.

History

The property covers a large area along the southern extents of the Guichon Batholith, which is host to many copper prospects that have been intermittently explored since the early 1930’s. The most important discovery to date has been the past producing Craigmont Copper-iron mine located in the central portion of the property.

The Craigmont Mine was operated by Craigmont Mines Ltd. from 1961 to 1967 as an open pit mine before moving to an underground sub-level cave operation from 1967 to 1982. The mine produced in excess of 36,750,000 tons at an average grade of 1.30% Cu, containing approximately 900 000 000 lbs. of copper. The mine was shut down in 1982 due to low copper prices.

Following the mine shutdown in 1982, Craigmont shipped up to 60,000 tonnes of clean metallurgical magnetite per year until 1992 from its stockpile to coal producers throughout North America for use in the coal flotation process. After 1992, Craigmont continued to produce a limited amount of magnetite product for the coal industry from re-worked iron fines in the tailings pond. This operation was shut down in 2014 due to economic grades of magnetite being exhausted.

Status of Exploration

Nicola has been actively exploring the property since the project ownership was consolidated in 2015. This work has consisted of over 18,000m of diamond drilling, property-wide geological mapping, widespread soil sampling, IP surveys, and property-wide aeromagnetic and ZTEM surveys. Additionally, 1869m of RC drilling at the historic mine dump and the higher grade 3060 portal.

Geology and Mineralization

The geology of the property is underlain by an east-northeast trending, steeply dipping volcanic pile of Upper Triassic Nicola Group rocks that are bound to the north by the multistage Early Jurassic-Late Triassic Guichon Creek Batholith and unconformably overlain by the Middle and Upper Cretaceous Spences Bridge Group. Most of the area is covered by thick gravel overburden.

Near the project area, the Border phase of the Guichon Creek Batholith varies in composition from quartz diorite to granodiorite and intrude the Nicola Group, a thick volcanic and sedimentary series of agglomerate, breccia, andesitic flows, limestone, argillite and greywacke. Nicola Group sediments immediately adjacent to the batholith are

Nicola Mining Inc. | Annual Information Form Page 17

hornfelsed quartzo-feldspathic greywackes. Spences Bridge Group agglomerates and flows dip approximately 15 degrees to the south and crop out in the areas south and west of the Craigmont mine area.

The property holds at least two types of mineralization described as copper-iron skarn and copper porphyry. Carbonate-rich, silicate-rich or intrusive rocks along the southern flank of the Guichon Batholith host the two types of mineralization. Within the property, mineralization is commonly associated with copper and iron skarn assemblages. Chalcopyrite, magnetite, specularite and minor bornite are principal minerals. Accessory assemblages at the Craigmont Mine include supergene minerals such as chalcocite and native copper have developed above the mineralized body. Gold, molybdenum and silver contents are generally low.

Several major faults cut through the property. Faults around the Craigmont mine include the northwest trending east and West Embayment Fault, the Mine East Fault and the East-West Fault.

Sample Database and Validation

A review of the sample collection and analysis practices used during the various drilling campaigns indicates that this work was conducted using generally accepted industry procedures.

Sampling programs conducted by Nicola were monitored using a QA/QC program that is typically accepted in the industry. It is the QPs’ opinion that the database is sufficiently accurate and precise to generate a mineral resource estimate.

Mineral Resource Estimate

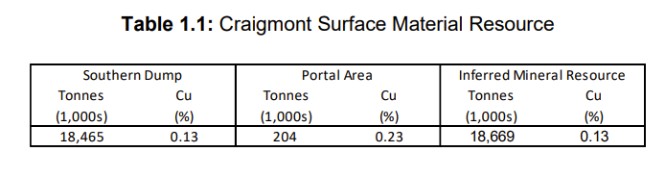

Two areas of Inferred Mineral Resource have been outlined, both consisting of historically subeconomic material remaining from past mining at the New Craigmont Project. A portion of the southern mine dumps, covering an area of 82.5 hectares, has been tested at a drill spacing of approximately 100 m. A smaller area (1.4 ha) of stockpiled material, adjacent to the 3060 portal, is of much smaller tonnage but of higher grade and is generally drilled at a 10-20 m spacing.

Resource tonnage is based on the volume between a LiDAR survey of current topography and a recent contractor generated pre-mine surface based on historic contour maps tied into current survey control. Density was assigned based on historic and current assumptions; no bulk density measurements are currently available. Future work must include density measurement work. The southern dump material was assigned a density of 1.8 t/m3; portal area material was assigned a density of 2.15 t/m3.

Inverse distance weighting was chosen as the most appropriate grade estimation approach due in part to the fact that the material being evaluated is not, in its present form, a naturally occurring mineral deposit. The southern dump material was estimated using 15x15x8 m blocks with 4 m composites from 60 RC holes. The 3060 portal area material was estimated using 5x5x4 m blocks and 4 m composites from 39 RC holes.

Material was classified as Inferred Mineral Resource where it was within the area of reasonably consistent drill spacing. In the southern dump area, blocks classified as Inferred are generally within 100 m of the closest sample and the drill spacing is approximately 100 m. In the portal area, drill spacing is typically less than 25 m and the resource extends a maximum of 40 m beyond drilling to the edge of the pile.

In order to establish reasonable prospects of eventual economic extraction a three-year trailing average copper price of US$2.8/lb and an anticipated annual production scenario was considered and a cut-off grade of 0.06% copper is deemed appropriate. The resource is included in Table 1.1.

Nicola Mining Inc. | Annual Information Form Page 18

Ongoing Exploration

Ongoing exploration at New Craigmont consists of drilling at several targets across the property, all of which show signs of porphyry-style alteration, mineral chemistry and mineralization. To date, over 8000 m of core has been drilled at porphyry targets throughout the property, and data analysis is ongoing. Geophysical and geochemical data from across the property is being compiled and analyzed to help generate exploration targets. Nicola collaborated with the Mineral Deposit Research Unit (MDRU) at UBC on a recently completed academic study which concluded that Craigmont is part of a porphyry-linked skarn system.

Recommendations

The following work is recommended for the New Craigmont Project:

· | Drill a large untested ZTEM anomaly (Jotun target) north of the historical pit, which could represent a porphyry system (planned for 2026). |

· | Create a 3D geological model of the property, particularly of the target areas. |

· | Continue to collect XRF and SWIR data from the core on site to incorporate into in the geochemical/geophysical dataset to help refine porphyry targeting. |

· | Mobile Metal Ion (MMI) soil sampling over areas of interest to refine drill targets. |

· | Airborne Audio-Frequency Magnetotellurics (MobileMT) survey as required to refine geophysical targeting across the property. |

· | Upgrading the historical waste dump resource by: |

o | Trench sampling or sonic drilling to determine the grade and volume of the fine material. |

o | Bulk density measurements. |

o | Additional testing on the cost benefit of Tomra sorting. |

o | Additional RC or sonic drilling at a spacing of 50 m on the Northern dump. |

Exploration, Development, and Production

Current exploration consists of compiling and validating current and historical data for New Craigmont into a unified database for targeting and geological modelling. Ongoing drilling during the summer with the possibility of geophysical surveys and soil sampling are being contemplated for New Craigmont. Exploration drilling is planned for 2026 on an untested tarted (MB Zone) at Treasure Mountain.

For more information, please see the Technical Report a copy of which is filed under Nicola’s profile on SEDAR+ at www.sedarplus.ca.

Nicola Mining Inc. | Annual Information Form Page 19

RISK FACTORS

The following specific factors could materially adversely affect the Company and should be considered when deciding whether to make an investment in the Company. You should carefully consider the risks described below, which are qualified in their entirety by reference to, and must be read in conjunction with, the detailed information appearing elsewhere in this AIF, and all other information contained in this AIF. The risks and uncertainties described in this AIF and the information incorporated by reference herein are those the Company currently believes to be material, but they are not the only ones the Company will face. If any of the following risks, or any other risks and uncertainties that the Company has not identified or that it currently considers not to be material, actually occur or become material risks, the Company’s business, prospects, financial condition, results of operations and cash flows, and consequently the price of the Common Shares could be materially and adversely affected. In all these cases, the trading price of the Company’s securities could decline, and prospective investors could lose all or part of their investment.

Investors should carefully consider the risk factors set out below and consider all other information contained herein and in the Company’s other public filings before making an investment decision.

Any reference to “the Company” or “Nicola” in the risk factors refers to the Company and its subsidiary together on a consolidated basis.

Insufficient Capital

The Company currently has minimal revenue producing operations and may report a working capital deficit from time to time. To maintain its activities, the Company will require additional funds which may be obtained either by the sale of equity capital, debt financing, government grants or by entering into an option or joint venture agreement with a third party providing such funding. There is no assurance that the Company will be successful in obtaining such additional financing; failure to do so could result in the loss or substantial dilution of the Company. The Company’s unallocated working capital may not suffice to fund its business goals and objects as stated elsewhere in the AIF.

The Company expects to continue to incur negative investing and operating cash flows until such time as it enters into commercial production of its properties. This will require the Company to deploy its working capital to fund such negative cash flow and to seek additional sources of financing. There is no assurance that any such financing sources will be available or sufficient to meet the Company’s requirements. There is no assurance that the Company will be able to continue to raise equity capital or that the Company will not continue to incur losses.

Lack of Operating Cash Flow

The Company currently has a minimal source of operating cash flow and is expected to continue to do so for the foreseeable future. The Company’s failure to achieve profitability and positive operating cash flows could have a material adverse effect on its financial condition and results of operations. If the Company sustains losses over an extended period of time, it may be unable to continue its business. Further exploration and development of its mineral properties will require the commitment of substantial financial resources. It may be several years before the Company may generate any substantial revenues from operations, if at all. There can be no assurance that the Company will realize revenue or achieve profitability.

Resale of Common Shares

The continued operation of the Company will be dependent upon its ability to generate operating revenues and to procure additional financing. There can be no assurance that any such revenues can be generated or sustained or that other financing can be obtained. If the Company is unable to generate such revenues or obtain such additional

Nicola Mining Inc. | Annual Information Form Page 20

financing, any investment in the Company may be lost. In such event, the probability of resale of the Common Shares purchased would be diminished.

Exploration of Mineral Property Interests

Although substantial benefits may be derived from the discovery of a major mineralized deposit, no assurance can be given that minerals will be discovered in sufficient quantities to justify commercial operations or that the funds required for development can be obtained on a timely basis. The discovery of mineral deposits is dependent upon a number of factors. The commercial viability of a mineral deposit once discovered is also dependent upon a number of factors, some of which relate to particular attributes of the deposit, such as size, grade and proximity to infrastructure, and some of which are more general such as commodity prices and government regulations, including environmental protection. Most of these factors are beyond the control of the Company. In addition, because of these risks, there is no certainty that the expenditures to be made by the Company on the exploration of its various mineral properties as described herein will result in the discovery of commercial quantities of ore. The Company has no history of operating earnings and the likelihood of success must be considered in light of problems, expenses, etc. which may be encountered in establishing a business.

Exploring and developing natural resource projects bears a high potential for all manner of risks. Additionally, few exploration projects successfully achieve development due to factors that cannot be predicted or foreseen. Moreover, even one such factor may result in the economic viability of a project being detrimentally impacted, such that it is neither feasible nor practical to proceed. Natural resource exploration involves many risks, which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Operations in which the Company has a direct or indirect interest will be subject to all the hazards and risks normally incidental to exploration, development and production of natural resources, any of which could result in work stoppages, damage to property, and possible environmental damage. If any of the Company’s exploration programs are successful, there is a degree of uncertainty attributable to the calculation of resources and corresponding grades and in the analysis of the economic viability of future development and mineral extraction. In addition, the quantity of reserves and resources may vary depending on commodity prices and various technical and economic assumptions. Any material change in quantity of reserves, grade or recovery ratio, may affect the economic viability of the Company’s properties.

Exploration, Development and Production Risks

The exploration for and development of minerals involves significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. Few properties that are explored are ultimately developed into producing mines. There can be no guarantee that the estimates of quantities and qualities of minerals disclosed will be economically recoverable. With all mining operations there is uncertainty and, therefore, risk associated with operating parameters and costs resulting from the scaling up of extraction methods tested in pilot conditions. Mineral exploration is speculative in nature and there can be no assurance that any minerals discovered will result in an increase in the Company’s resource base.

The Company’s operations will be subject to all of the hazards and risks normally encountered in the exploration, development and production of minerals. These include unusual and unexpected geological formations, rock falls, seismic activity, flooding and other conditions involved in the extraction of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to life or property, environmental damage and possible legal liability. In addition, operations are subject to hazards that may result in environmental pollution, and consequent liability that could have a material adverse impact on the business, operations and financial performance of the Company.

Substantial expenditures are required to establish Ore Reserves through drilling, to develop metallurgical processes to extract the metal from the ore and, in the case of new properties, to develop the mining and processing facilities and infrastructure at any site chosen for mining. Although substantial benefits may be derived from the discovery of a major mineralized deposit, no assurance can be given that minerals will be discovered in sufficient quantities to

Nicola Mining Inc. | Annual Information Form Page 21

justify commercial operations or that funds required for development can be obtained on a timely basis. The economics of developing gold and other mineral properties is affected by many factors including the cost of operations, variations in the grade of ore mined, fluctuations in metal markets, costs of processing equipment and such other factors as government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals and environmental protection. The remoteness and restrictions on access of properties in which the Company has an interest will have an adverse effect on profitability as a result of higher infrastructure costs. There are also physical risks to the exploration personnel working in the terrain in which the Company’s properties will be located, often in poor climate conditions.

The long-term commercial success of the Company depends on its ability to explore, develop and commercially produce minerals from its properties and to locate and acquire additional properties worthy of exploration and development for minerals. No assurance can be given that the Company will be able to locate satisfactory properties for acquisition or participation. Moreover, if such acquisitions or participations are identified, the Company may determine that current markets, terms of acquisition and participation or pricing conditions make such acquisitions or participation uneconomic.

Mineral Resources and Reserves

The figures for mineral resources for the Treasure Mountain Project disclosed in the Company’s Annual Information Form for the year ended December 31, 2012, and in its technical report filed on SEDAR on June 12, 2012, are only estimates. Mineral reserves at the Treasure Mountain Project have not been defined therefore the mineral resources currently cannot be considered ore.

The figures for Inferred Copper Resource for the Southern Dump and 3060 Portal Dumps at New Craigmont Project in the Technical Report and final ALS Metallurgy Laboratory report for upgrading and copper recovery test work filed on SEDAR on June 12, 2020, are only estimates. The inferred mineral resources are not mineral reserves as the Company has not yet demonstrated the economic viability. There is no certainty that any expenditures made in the exploration of the Company’s mineral properties will result in identification of commercially recoverable quantities of ore or that ore reserves will be mined or processed profitably. In addition, substantial expenditures will be required to develop the mining and processing facilities and infrastructure at any site chosen for mining.

Uncertainty of Economic Viability of Production from the Treasure Mountain Project

The Company has not undertaken any preliminary economic assessment or preliminary feasibility study with respect to the Treasure Mountain Project or any of its other projects and does not intend to undertake such a study or assessment. There are significant risks associated with making a production decision without a valid, current, economic analysis and the Company may subsequently determine that recommencing operations at the Treasure Mountain Project is not economically feasible.

Governmental Regulation and Policy

Mining operations and exploration activities are subject to extensive laws and regulations. Such regulations relate to production, development, exploration, exports, imports, taxes and royalties, labor standards, occupational health, waste disposal, protection and remediation of the environment, toxic and radioactive substances, transportation safety and emergency response, and other matters. Compliance with such laws and regulations increases the costs of exploring, developing, constructing, and operating projects. It is possible that, in the future, the costs, delays and other effects associated with such laws and regulations may impact decisions of the Company with respect to the exploration and development of properties, such as the properties in which the Company has an interest. The Company will be required to expend significant financial and managerial resources to comply with such laws and regulations. Since legal requirements change frequently, are subject to interpretation and may be enforced in varying degrees in practice, the Company is unable to predict the ultimate cost of compliance with these requirements or their effect on operations. Furthermore, future changes in governments, regulations and policies and practices, such as those affecting exploration and development of the Company’s properties could materially

Nicola Mining Inc. | Annual Information Form Page 22

and adversely affect the results of operations and financial condition of the Company in a particular year or in its long-term business prospects.

No Assurances

There is no assurance that economic mineral deposits will ever be discovered, or if discovered, subsequently put into production. Most exploration activities do not result in the discovery of commercially mineable deposits. Mining exploration is highly speculative in nature, involves many risks and frequently is not productive. Most exploration projects do not result in the discovery of commercially mineable ore deposits and no assurance can be given that any anticipated level of recovery of mineral reserves will be realized or that any identified mineral deposit will ever qualify as a commercially mineable (or viable) ore body which can be legally and economically exploited.

Indigenous Peoples’ title claims and rights to consultation and accommodation may affect our existing operations as well as development projects and future acquisitions.

Governments in many jurisdictions must consult Indigenous Peoples with respect to grants of mineral rights and the issuance or amendment of exploration and project authorizations. Consultation and other rights of Indigenous Peoples may require accommodations, including undertakings regarding financial compensation, employment and other matters in impact and benefit agreements. This may affect the Company’s ability to acquire, explore or develop, within a reasonable time frame, mineral titles in these jurisdictions and may affect the timetable and costs of development of mineral properties in these jurisdictions. The risk of unforeseen aboriginal title claims also could affect existing operations as well as exploration and development projects and future acquisitions. These legal requirements may increase the Company’s operating costs and affect the Company’s ability to expand its operations or to explore and develop new projects.

Community Relations and License to Operate

The Company’s relationship with the host communities where it operates is critical to ensure the future success of its existing operations and the construction and development of its projects. There is an increasing level of public concern relating to the perceived effect of mining activities on the environment and on communities impacted by such activities. Certain non-governmental organizations (“NGOs”), some of which oppose globalization and resource development, are often vocal critics of extractive industries and their practices. Adverse publicity generated by such NGOs or others related to extractive industries generally, or the Company’s exploration or development activities specifically, could have an adverse effect on the Company’s reputation. Reputation loss may result in decreased investor confidence, increased challenges in developing and maintaining community relations and an impediment to the Company’s overall ability to advance its projects, which could have a material adverse impact on the Company’s results of operations, financial condition and prospects. While the Company is committed to operating in a socially responsible manner, there is no guarantee that the Company’s efforts in this respect will mitigate this potential risk.

Title Risks

Although the Company has exercised the usual due diligence with respect to determining title to properties in which it has a material interest, there is no guarantee that title to such properties will not be challenged or impugned. The Company’s mineral property interests may be subject to prior unregistered agreements or transfers or native land claims and title may be affected by undetected defects. Surveys have not been carried out on any of the Company’s mineral properties, therefore, in accordance with the laws of the jurisdiction in which such properties are situated; their existence and area could be in doubt. Until competing interests in the mineral lands have been determined, the Company can give no assurance as to the validity of title of the Company to those lands or the size of such mineral lands.

Uninsurable Risks

Nicola Mining Inc. | Annual Information Form Page 23

In the course of exploration, development and production of mineral properties, certain risks, and in particular, unexpected or unusual geological operating conditions including rock bursts, cave-ins, fires, flooding and earthquakes may occur. It is not always possible to fully insure against such risks and the Company may decide not to take out insurance against such risks as a result of high premiums or other reasons. Should such liabilities arise, they could reduce or eliminate any future profitability and result in increasing costs and a decline in the value of the securities of the Company.

Future Share Issuances May Affect the Market Price of the Common Shares and Results in Significant Dilution

In order to finance future operations, the Company may raise funds through the issuance of additional Common Shares or the issuance of debt instruments or other securities convertible into Common Shares. The Company cannot predict the size of future issuances of Common Shares or the issuance of debt instruments or other securities convertible into Common Shares or the dilutive effect, if any, that future issuances and sales of the Company’s securities will have on the market price of the Common Shares.

Dilution

Common Shares, including rights, warrants, special warrants, subscription receipts and other securities to purchase, to convert into or to exchange into Common Shares, may be created, issued, sold and delivered on such terms and conditions and at such times as the Board may determine. In addition, the Company may issue additional Common Shares from time to time pursuant to Common Share purchase warrants and the options to purchase Common Shares issued from time to time by the Board. The issuance of these Common Shares could result in significant dilution to holders of Common Shares.

Operational Risks

The Company will be subject to a number of operational risks and may not be adequately insured for certain risks, including: environmental contamination, liabilities arising from historic operations, accidents or spills, industrial and transportation accidents, which may involve hazardous materials, labor disputes, catastrophic accidents, fires, blockades or other acts of social activism, changes in the regulatory environment, impact of non-compliance with laws and regulations, natural phenomena such as inclement weather conditions, floods, earthquakes, ground movements, cave-ins, and encountering unusual or unexpected geological conditions and technological failure of exploration methods.

There is no assurance that the foregoing risks and hazards will not result in damage to, or destruction of, the property of the Company, personal injury or death, environmental damage or, regarding the exploration or development activities of the Company, increased costs, monetary losses and potential legal liability and adverse governmental action. These factors could all have an adverse impact on the Company’s future cash flows, earnings, results of operations and financial condition.