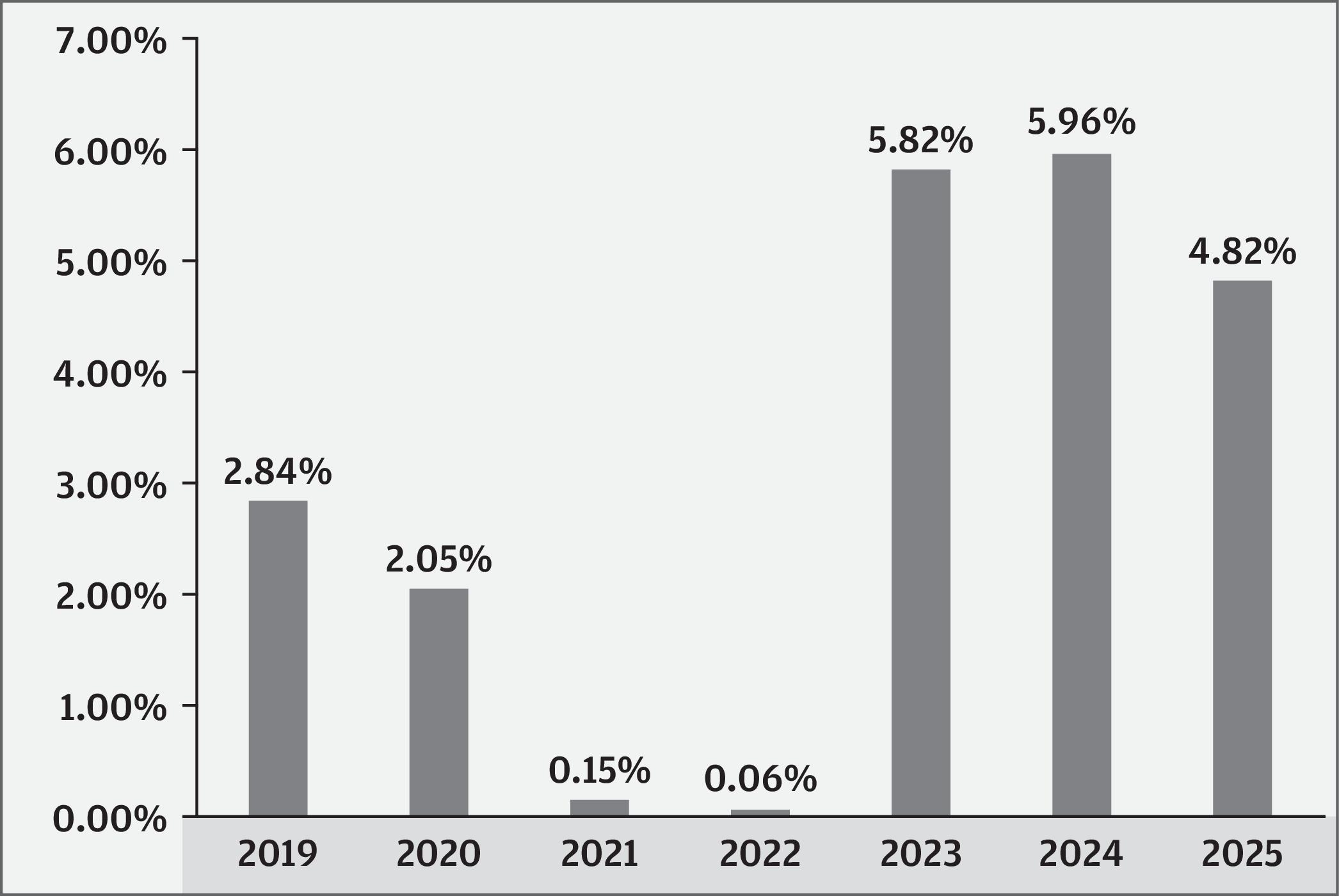

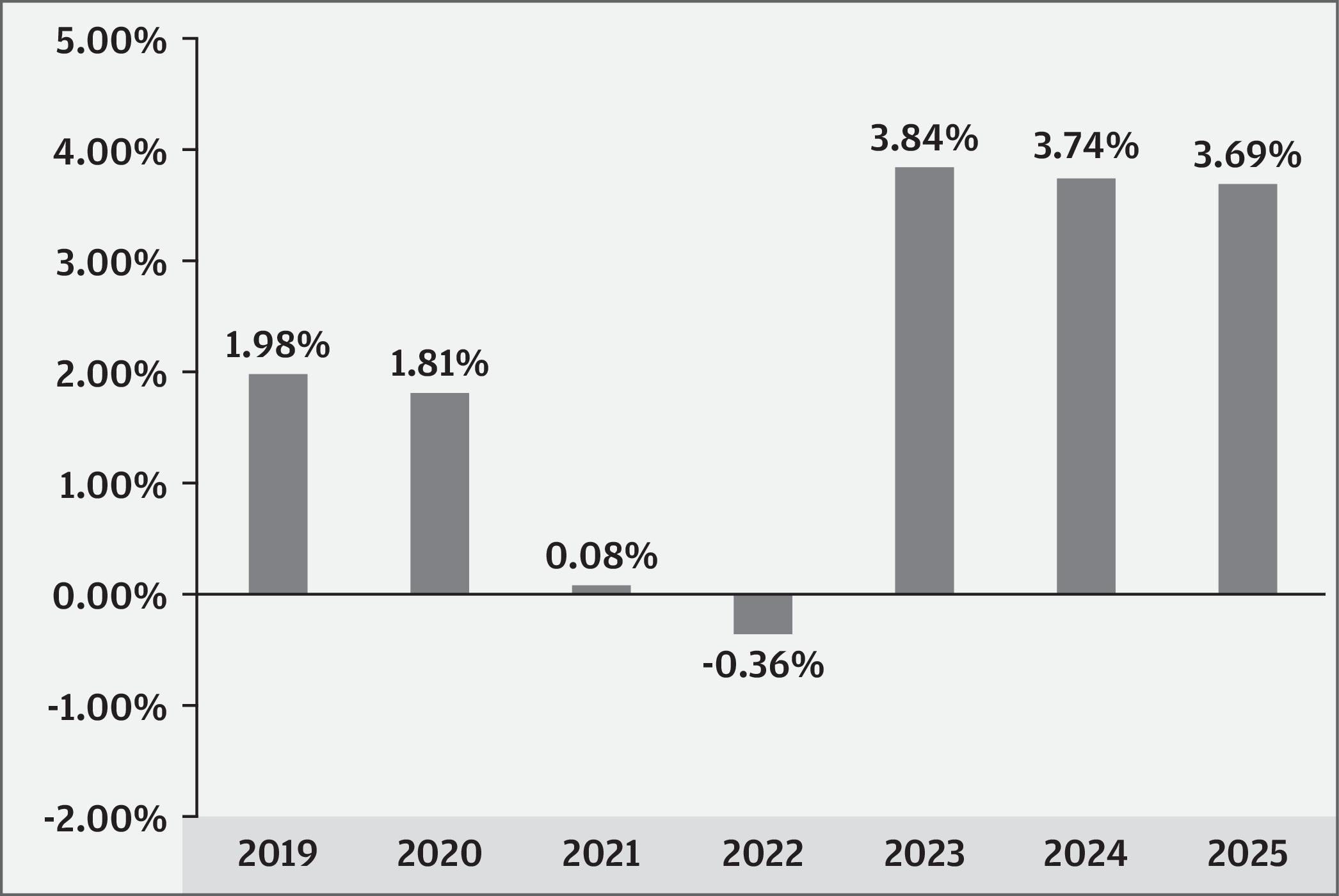

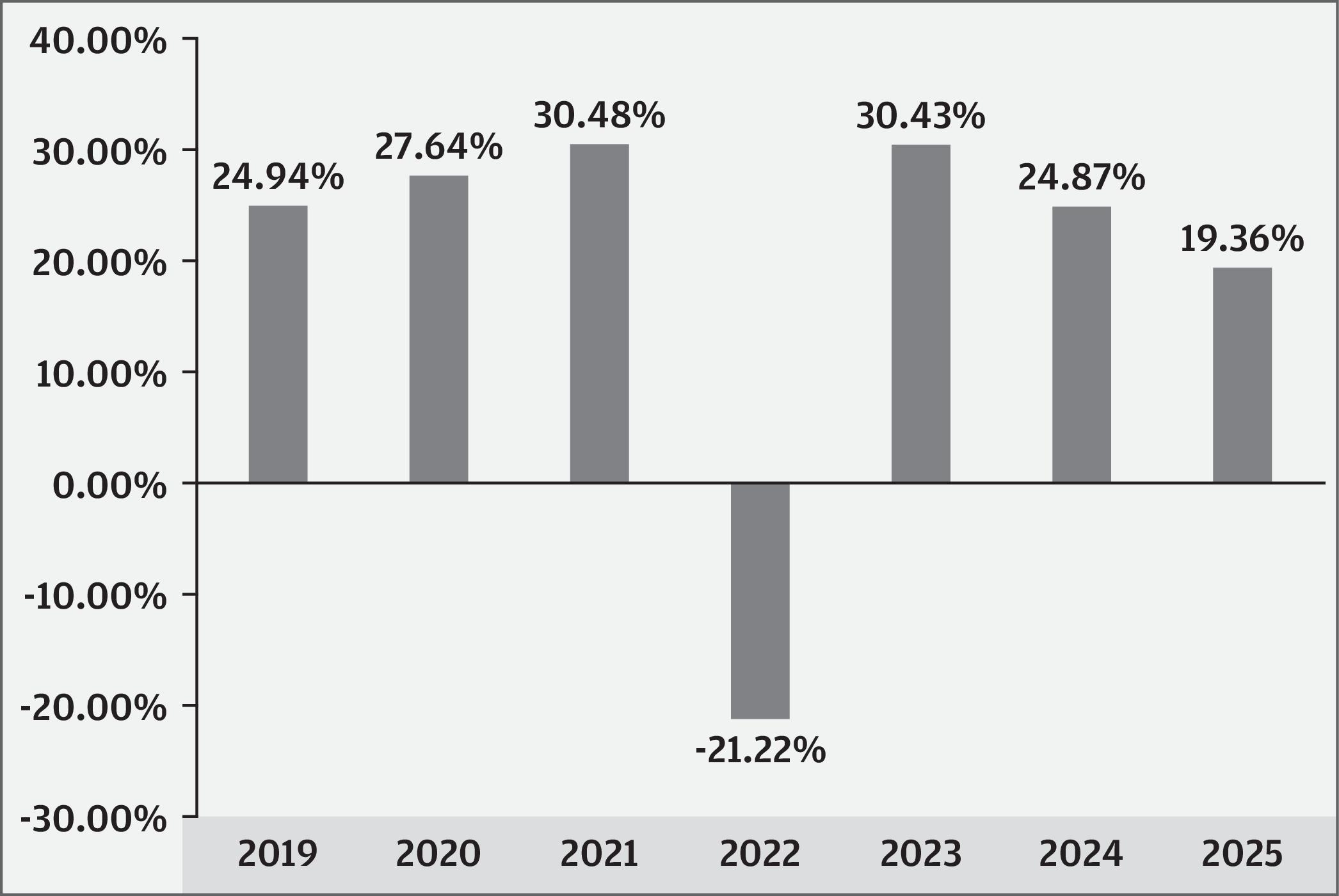

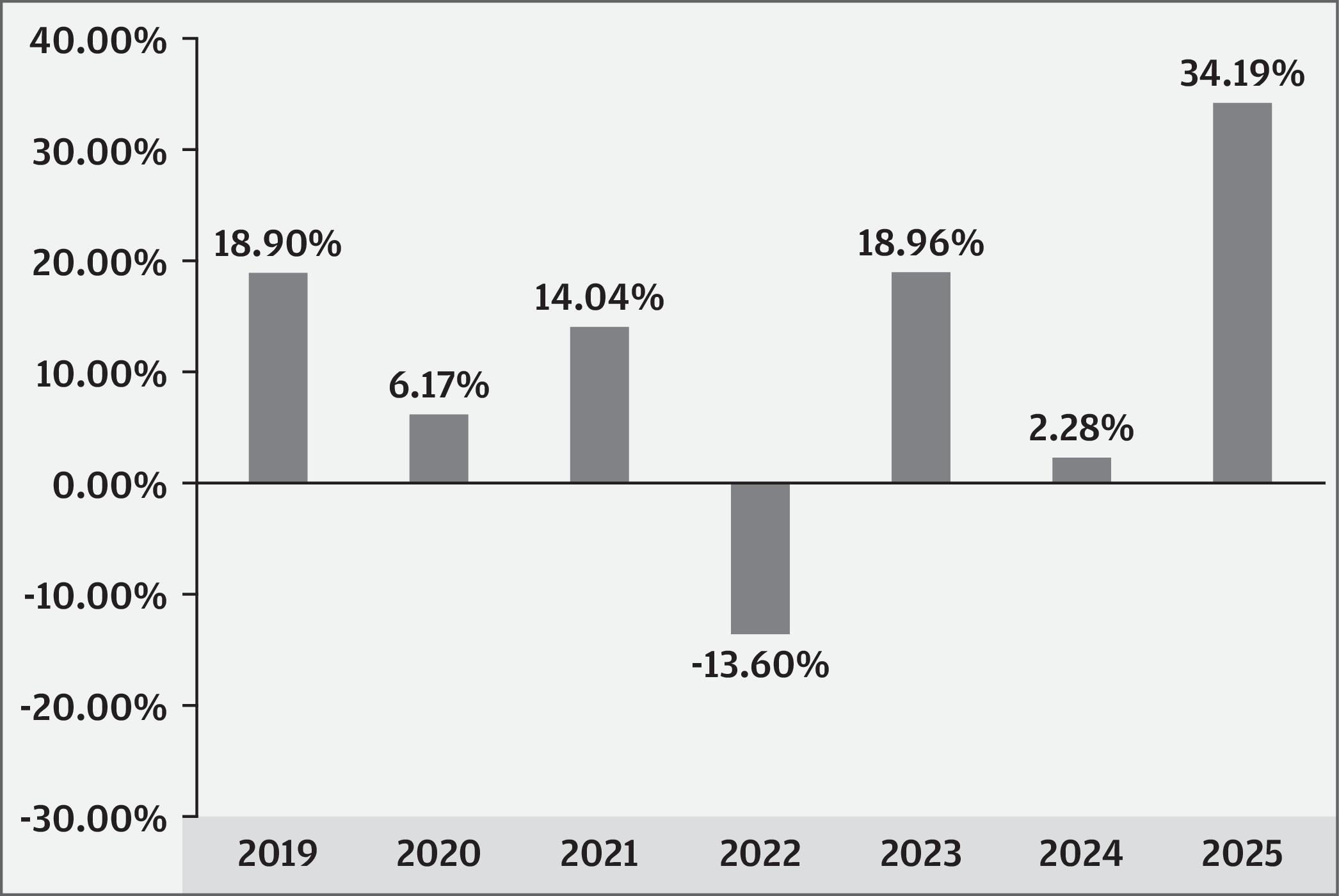

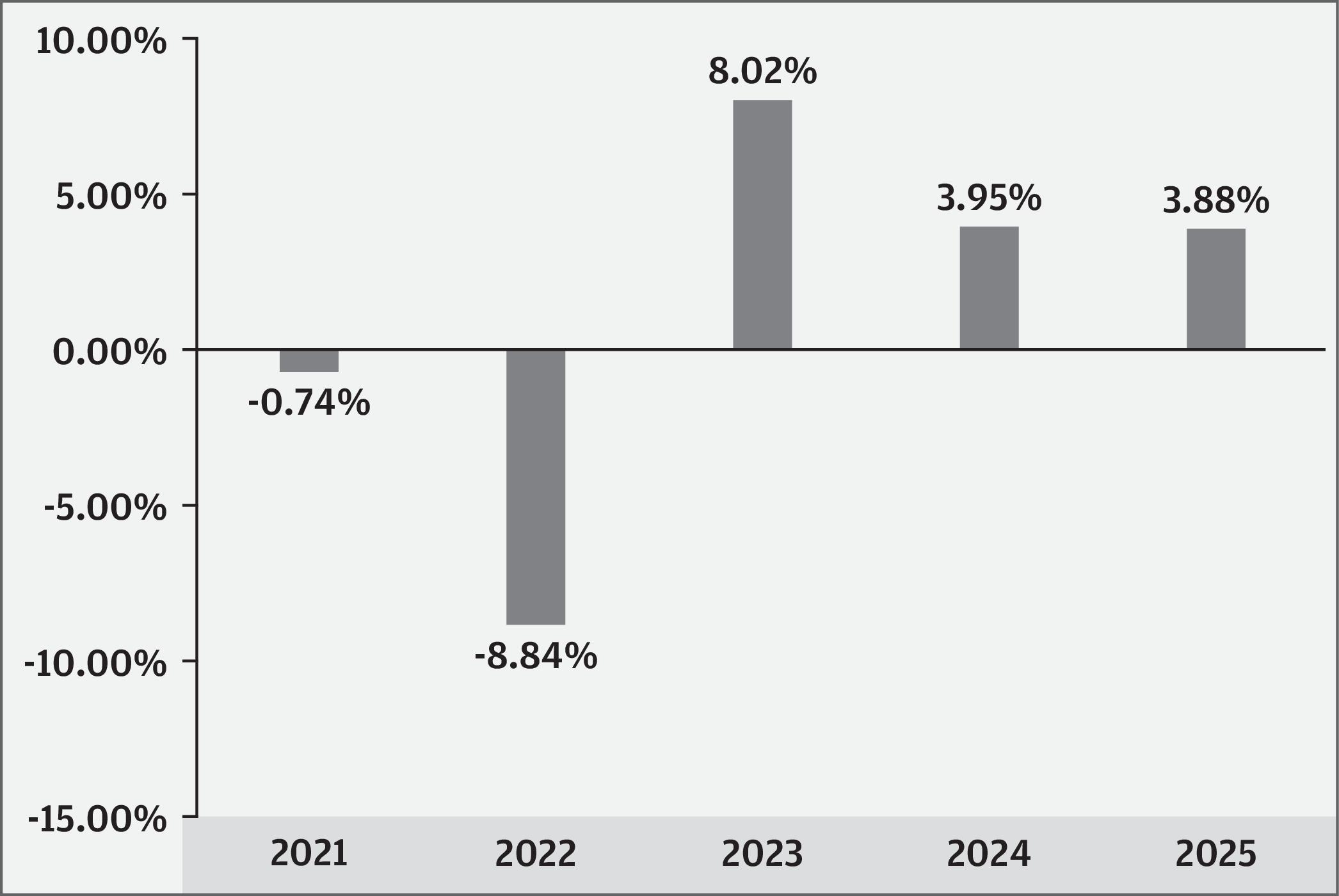

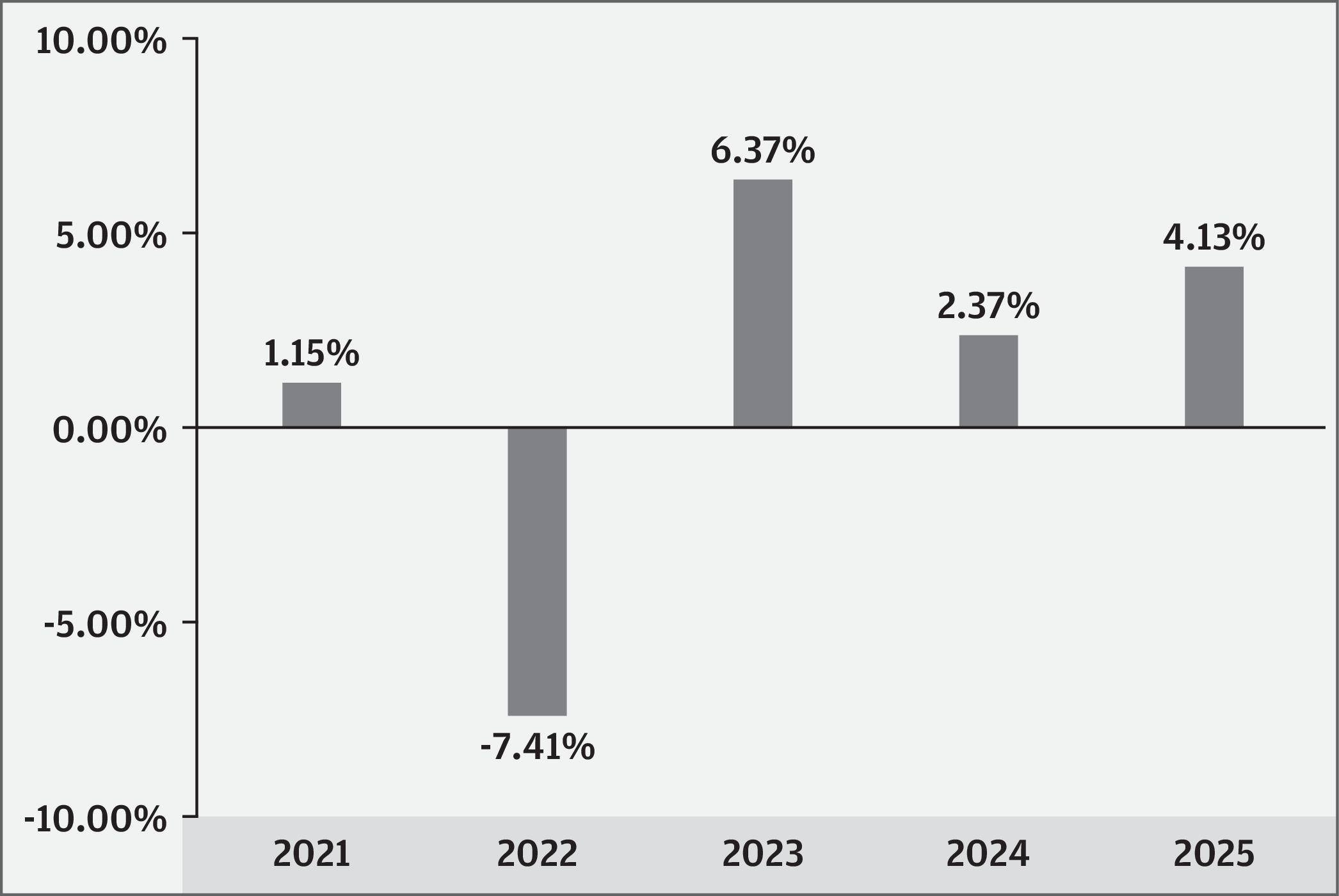

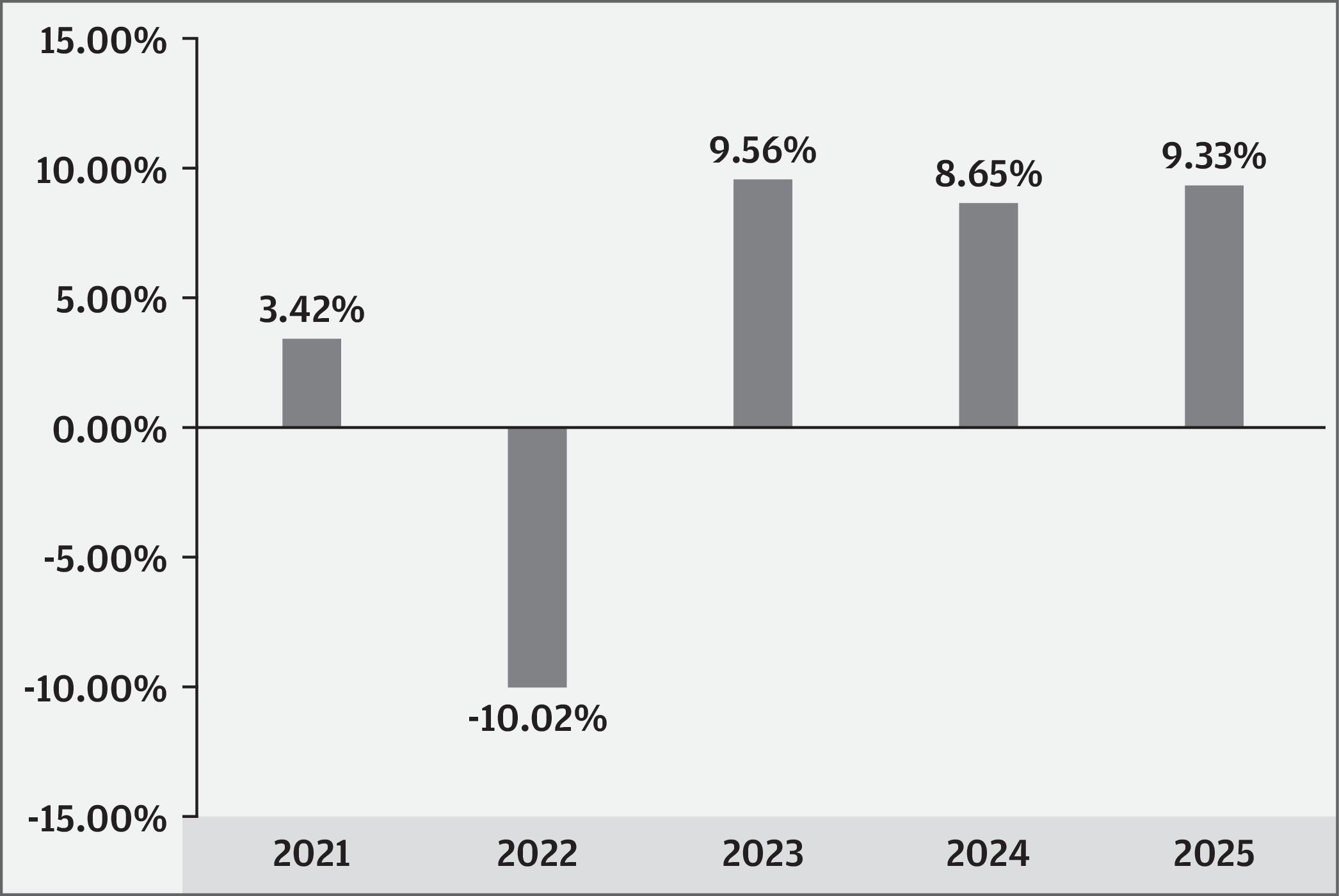

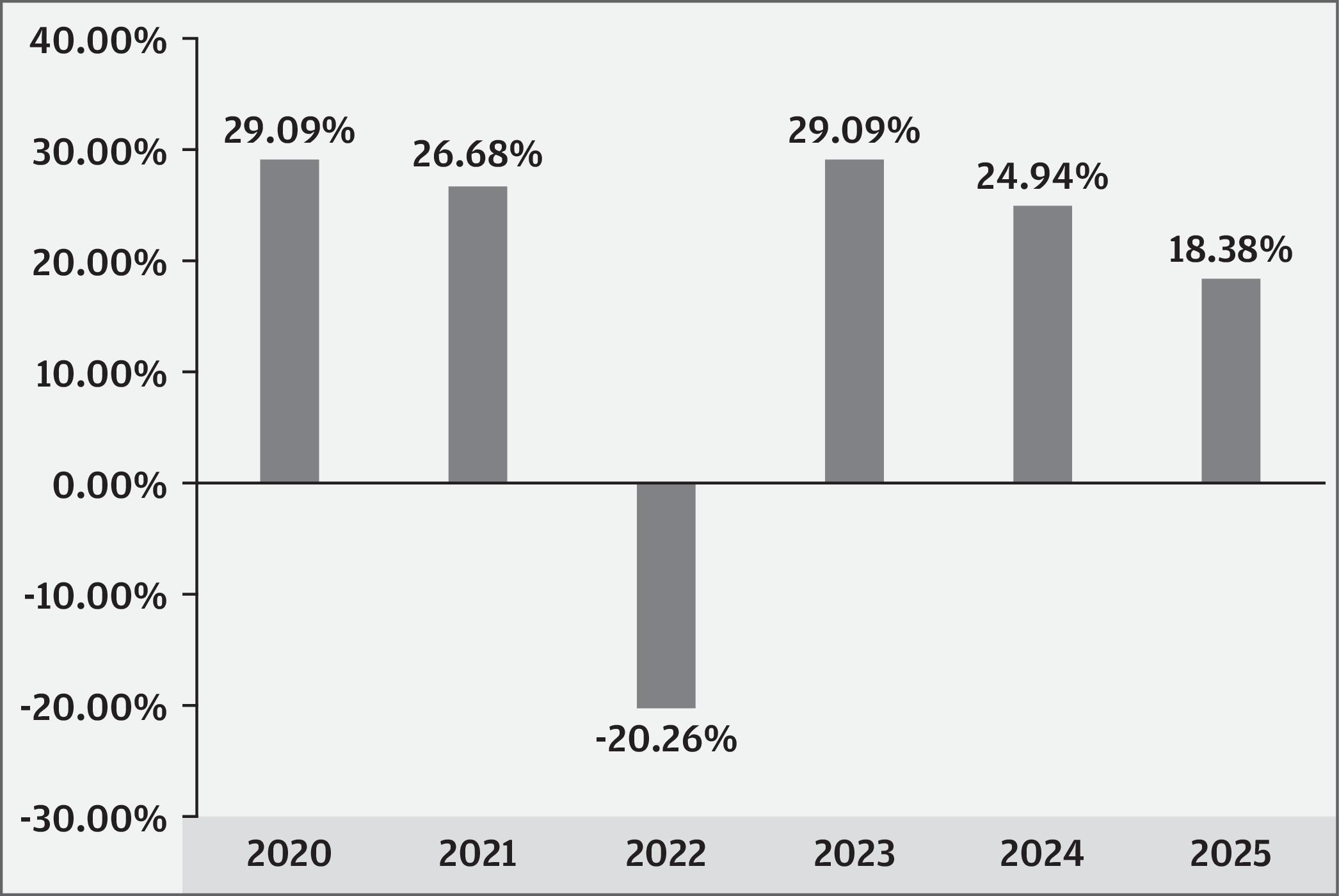

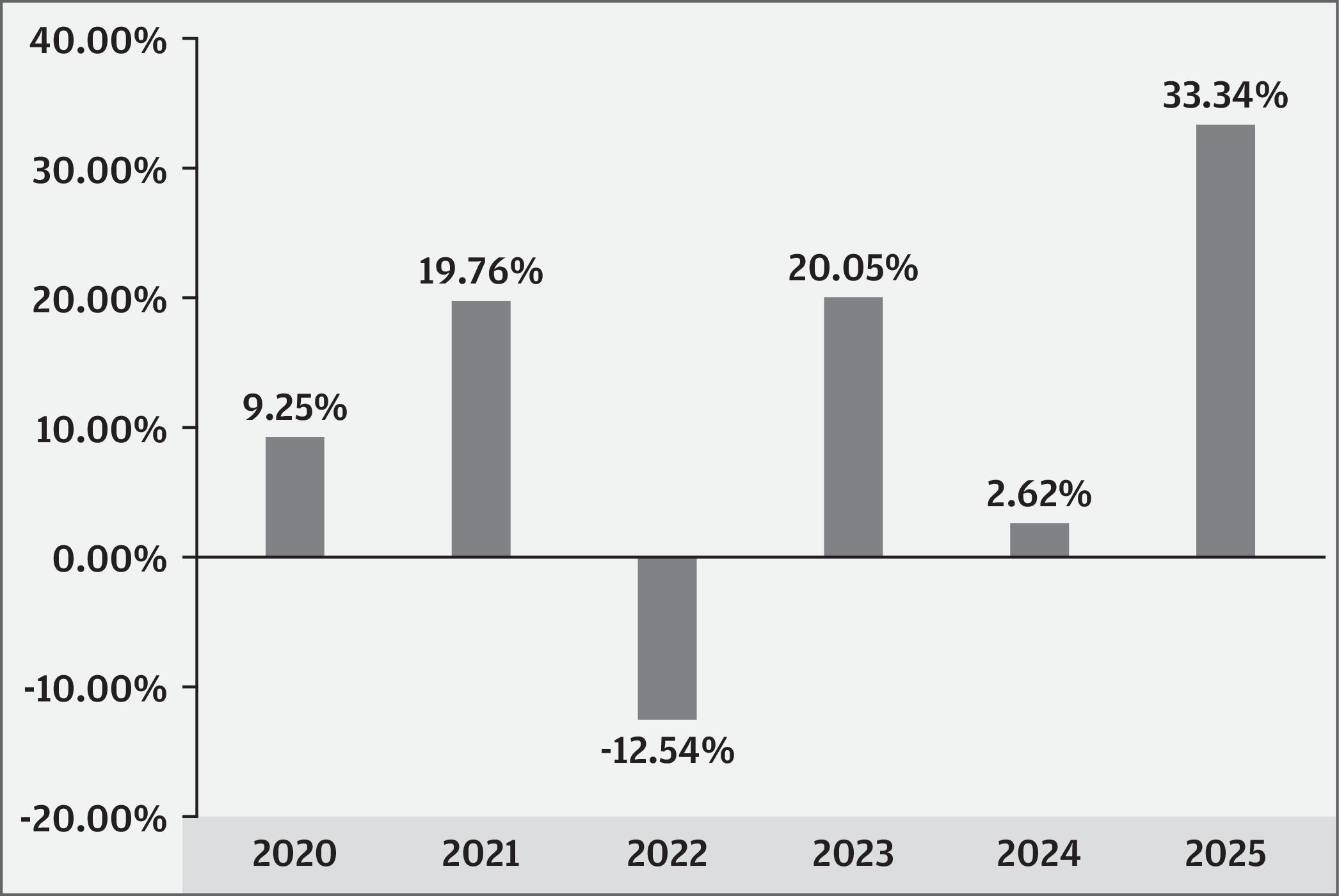

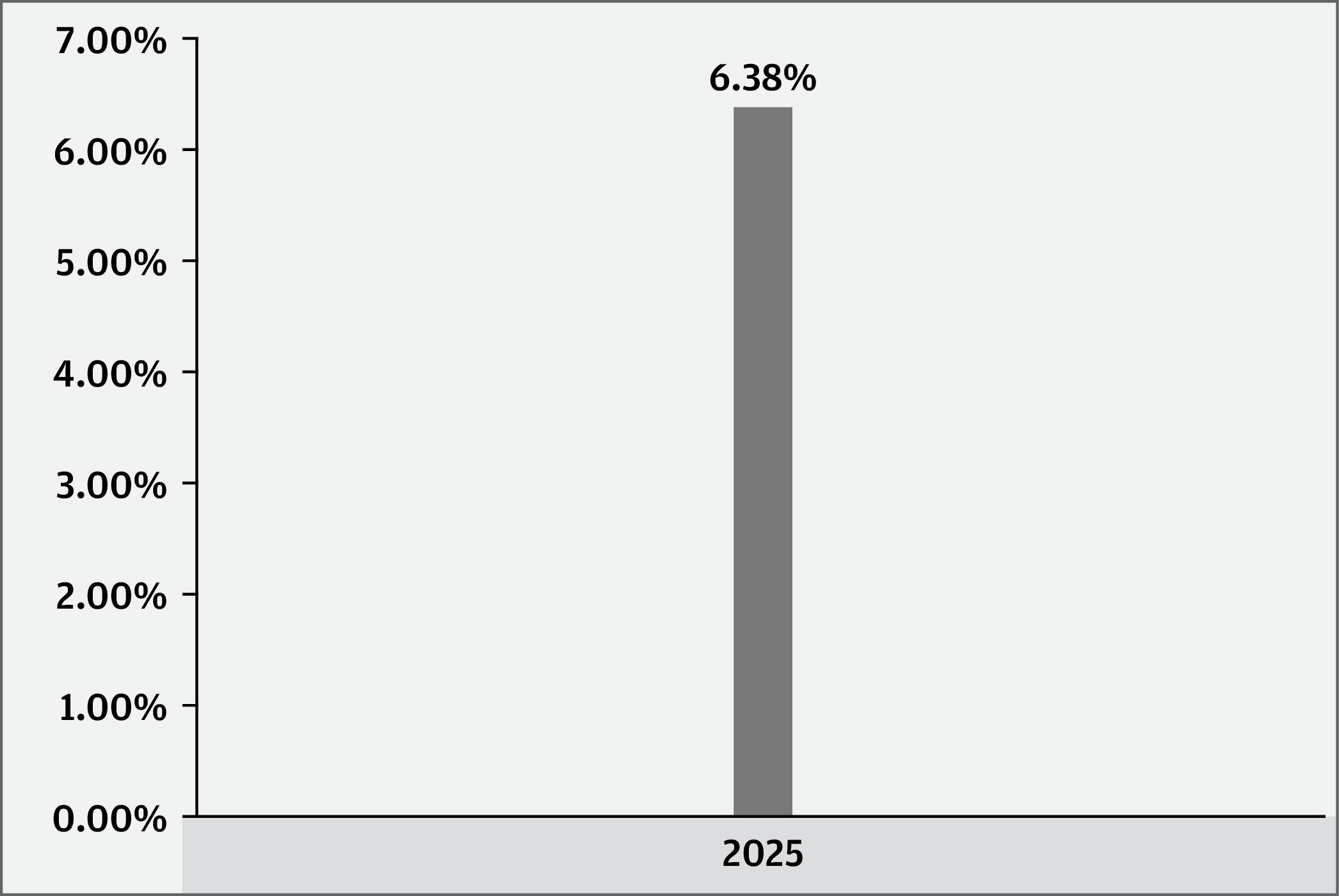

2025-12-31 0001724826 false 485BPOS 0.1890 0.0617 0.1404 0.1360 0.1896 0.0228 0.3419 0.0198 0.0181 0.0008 0.0036 0.0384 0.0374 0.0369 0.0115 0.0741 0.0637 0.0237 0.0413 0.0638 0.2909 0.2668 0.2026 0.2909 0.2494 0.1838 0.0342 0.1002 0.0956 0.0865 0.0933 0.0925 0.1976 0.1254 0.2005 0.0262 0.3334 0.2494 0.2764 0.3048 0.2122 0.3043 0.2487 0.1936 0.0074 0.0884 0.0802 0.0395 0.0388 0.0284 0.0205 0.0015 0.0006 0.0582 0.0596 0.0482 0001724826 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:AssetBackedMortgageRelatedandMortgageBackedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:SovereignObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:RegulationSSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:RestrictedandPrivatelyPlacedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:StructuredNotesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ToBeAnnouncedTransactionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:MunicipalObligationsandSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:CollateralizedLoanObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:NonMoneyMarketFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:ConvertibleSecuritiesandContingentConvertibleSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:BankLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000061650Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000199642Member 2025-12-31 2025-12-31 0001724826 jpm:C000199642Member 2025-01-01 2025-12-31 0001724826 jpm:C000199642Member 2021-01-01 2025-12-31 0001724826 jpm:C000199642Member 2018-07-09 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsMember 2018-07-09 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000199642Member oef:AfterTaxesOnDistributionsAndSalesMember 2018-07-09 2025-12-31 0001724826 jpm:BLOOMBERGUSAGGREGATETOTALRETURNVALUEUNHEDGEDUSDINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERGUSAGGREGATETOTALRETURNVALUEUNHEDGEDUSDINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERGUSAGGREGATETOTALRETURNVALUEUNHEDGEDUSDINDEXMember 2018-07-09 2025-12-31 0001724826 jpm:BLOOMBERG13MONTHUSTREASURYBILLINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERG13MONTHUSTREASURYBILLINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERG13MONTHUSTREASURYBILLINDEXMember 2018-07-09 2025-12-31 0001724826 jpm:S000061648Member 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:MunicipalObligationsandSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:SovereignObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:RestrictedandPrivatelyPlacedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:AssetBackedMortgageRelatedandMortgageBackedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:MunicipalProjectHousingRelatedRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:LoanParticipationsandAssignmentsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member us-gaap:PrepaymentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:InflationLinkedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:StructuredMunicipalProductRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:BankLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ImpairmentofCollateralRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:AuctionRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:TaxAwareInvestingRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:TaxabilityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:AlternativeMinimumTaxRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:MunicipalSecuritiesConcentrationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ToBeAnnouncedTransactionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000061648Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000199640Member 2025-12-31 2025-12-31 0001724826 jpm:C000199640Member 2025-01-01 2025-12-31 0001724826 jpm:C000199640Member 2021-01-01 2025-12-31 0001724826 jpm:C000199640Member 2018-07-09 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsMember 2018-07-09 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000199640Member oef:AfterTaxesOnDistributionsAndSalesMember 2018-07-09 2025-12-31 0001724826 jpm:BLOOMBERGMUNICIPALBONDINDEXTOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERGMUNICIPALBONDINDEXTOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERGMUNICIPALBONDINDEXTOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2018-07-09 2025-12-31 0001724826 jpm:BLOOMBERG115YEARMUNICIPALBONDINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERG115YEARMUNICIPALBONDINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERG115YEARMUNICIPALBONDINDEXMember 2018-07-09 2025-12-31 0001724826 jpm:S000061649Member 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:LargeCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:MidCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:SmallerCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:RealEstateInvestmentTrustsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:TechnologySectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000061649Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000199641Member 2025-12-31 2025-12-31 0001724826 jpm:C000199641Member 2025-01-01 2025-12-31 0001724826 jpm:C000199641Member 2021-01-01 2025-12-31 0001724826 jpm:C000199641Member 2018-07-09 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsMember 2018-07-09 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000199641Member oef:AfterTaxesOnDistributionsAndSalesMember 2018-07-09 2025-12-31 0001724826 jpm:MSCIUSAINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:MSCIUSAINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:MSCIUSAINDEXMember 2018-07-09 2025-12-31 0001724826 jpm:S000061647Member 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:EuropeanMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:AsiaPacificMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:GreaterChinaRegionRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:LargeCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:MidCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:SmallerCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:DepositaryReceiptsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:RealEstateInvestmentTrustsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:IndustrialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000061647Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000199639Member 2025-12-31 2025-12-31 0001724826 jpm:C000199639Member 2025-01-01 2025-12-31 0001724826 jpm:C000199639Member 2021-01-01 2025-12-31 0001724826 jpm:C000199639Member 2018-07-09 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsMember 2018-07-09 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000199639Member oef:AfterTaxesOnDistributionsAndSalesMember 2018-07-09 2025-12-31 0001724826 jpm:MSCIWORLDEXUSAINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:MSCIWORLDEXUSAINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:MSCIWORLDEXUSAINDEXMember 2018-07-09 2025-12-31 0001724826 jpm:S000068181Member 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:SovereignObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member us-gaap:PrepaymentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:AssetBackedMortgageRelatedandMortgageBackedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:RestrictedandPrivatelyPlacedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:StructuredNotesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ToBeAnnouncedTransactionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:EuropeanMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:AsiaPacificMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:GreaterChinaRegionRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:CollateralizedLoanObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:ConvertibleSecuritiesandContingentConvertibleSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:InflationLinkedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:BankLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000068181Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000218339Member 2025-12-31 2025-12-31 0001724826 jpm:C000218339Member 2025-01-01 2025-12-31 0001724826 jpm:C000218339Member 2021-01-01 2025-12-31 0001724826 jpm:C000218339Member 2020-05-19 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsMember 2020-05-19 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000218339Member oef:AfterTaxesOnDistributionsAndSalesMember 2020-05-19 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATETOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATETOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATETOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2020-05-19 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATEINDEXHEDGEDUSDMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATEINDEXHEDGEDUSDMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATEINDEXHEDGEDUSDMember 2020-05-19 2025-12-31 0001724826 jpm:S000068182Member 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:MunicipalObligationsandSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:InflationLinkedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:StructuredMunicipalProductRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member us-gaap:PrepaymentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:TaxAwareInvestingRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:AuctionRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:TaxabilityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:AlternativeMinimumTaxRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:MunicipalSecuritiesConcentrationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000068182Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000218340Member 2025-12-31 2025-12-31 0001724826 jpm:C000218340Member 2025-01-01 2025-12-31 0001724826 jpm:C000218340Member 2021-01-01 2025-12-31 0001724826 jpm:C000218340Member 2020-05-19 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsMember 2020-05-19 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000218340Member oef:AfterTaxesOnDistributionsAndSalesMember 2020-05-19 2025-12-31 0001724826 jpm:BLOOMBERGMUNICIPALBONDINDEXTOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2020-05-19 2025-12-31 0001724826 jpm:BLOOMBERG115YEARMUNICIPALBONDINDEXMember 2020-05-19 2025-12-31 0001724826 jpm:S000068977Member 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:LoanParticipationsandAssignmentsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:DistressedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:IssuerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:BankLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:CovenantLiteLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ImpairmentofCollateralRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:SovereignObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member us-gaap:PrepaymentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:AssetBackedMortgageRelatedandMortgageBackedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:RestrictedandPrivatelyPlacedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:SubsidiaryRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:RegulationSSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:InflationLinkedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:StructuredNotesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ToBeAnnouncedTransactionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:AsiaPacificMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:GreaterChinaRegionRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:EuropeanMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:CollateralizedLoanObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:ConvertibleSecuritiesandContingentConvertibleSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000068977Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000220641Member 2025-12-31 2025-12-31 0001724826 jpm:C000220641Member 2025-01-01 2025-12-31 0001724826 jpm:C000220641Member 2021-01-01 2025-12-31 0001724826 jpm:C000220641Member 2020-08-19 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsMember 2020-08-19 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000220641Member oef:AfterTaxesOnDistributionsAndSalesMember 2020-08-19 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATETOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2020-08-19 2025-12-31 0001724826 jpm:BLOOMBERGUSINTERMEDIATECORPORATEBONDINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:BLOOMBERGUSINTERMEDIATECORPORATEBONDINDEXMember 2021-01-01 2025-12-31 0001724826 jpm:BLOOMBERGUSINTERMEDIATECORPORATEBONDINDEXMember 2020-08-19 2025-12-31 0001724826 jpm:S000063724Member 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:LargeCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:MidCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:SmallerCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:RealEstateInvestmentTrustsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:TechnologySectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:ConsumerDiscretionarySectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:CommunicationServicesSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000063724Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000206545Member 2025-12-31 2025-12-31 0001724826 jpm:C000206545Member 2025-01-01 2025-12-31 0001724826 jpm:C000206545Member 2021-01-01 2025-12-31 0001724826 jpm:C000206545Member 2019-04-10 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsMember 2019-04-10 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000206545Member oef:AfterTaxesOnDistributionsAndSalesMember 2019-04-10 2025-12-31 0001724826 jpm:MSCIUSAINDEXMember 2019-04-10 2025-12-31 0001724826 jpm:S000063725Member 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:EuropeanMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:AsiaPacificMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:GreaterChinaRegionRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:LargeCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:MidCapCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:SmallerCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:DepositaryReceiptsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:RealEstateInvestmentTrustsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:IndustrialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:FinancialsSectorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:TrackingErrorRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000063725Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000206546Member 2025-12-31 2025-12-31 0001724826 jpm:C000206546Member 2025-01-01 2025-12-31 0001724826 jpm:C000206546Member 2021-01-01 2025-12-31 0001724826 jpm:C000206546Member 2019-04-10 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsMember 2021-01-01 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsMember 2019-04-10 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsAndSalesMember 2021-01-01 2025-12-31 0001724826 jpm:C000206546Member oef:AfterTaxesOnDistributionsAndSalesMember 2019-04-10 2025-12-31 0001724826 jpm:MSCIWORLDEXUSAINDEXMember 2019-04-10 2025-12-31 0001724826 jpm:S000086732Member 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:C000252360Member 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:GeneralMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:DerivativesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:GeographicFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ContractsforDifferenceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:QuantitativeModelInvestingRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RisksAssociatedwiththeUseofArtificialIntelligenceToolsMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ForeignCurrencyForwardContractsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:FuturesContractsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:SwapAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CommodityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CFTCRegulationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:LeveragingRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:LiquidityRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:MultiManagerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:TaxRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:StructuredProductRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:FloatingandVariableRateSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:FloatingRateLoansRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:SeniorLoansRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:InflationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member us-gaap:CreditRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:HighYieldSecuritiesandLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member us-gaap:InterestRateRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:DebtSecuritiesandOtherCallableSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:DistressedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:IssuerRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:BankLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ShortSalesandOtherShortPositionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:LoanParticipationsandAssignmentsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CovenantLiteLoanRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ImpairmentofCollateralRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:GovernmentSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ForeignSecuritiesandEmergingMarketsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:SovereignObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:IncomeRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member us-gaap:PrepaymentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CounterpartyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:AssetBackedMortgageRelatedandMortgageBackedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:USTreasuryObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CurrencyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ZeroCouponBondRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:LIBORDiscontinuanceRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RestrictedandPrivatelyPlacedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:SubsidiaryRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RegulationSSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RepurchaseAgreementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:InflationLinkedSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RealEstateInvestmentTrustsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:HedgingRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:RelativeValueStrategiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:MacroStrategyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:EventLinkedInstrumentRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ExchangeTradedFundETFandInvestmentCompanyRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:StructuredNotesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ToBeAnnouncedTransactionsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:MortgageDollarRollRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:IndustryandSectorFocusRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:AllocationRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:HighPortfolioTurnoverRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ManagementRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:CollateralizedLoanObligationsRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:EquityMarketRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:EquitySecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:NonDiversifiedFundRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:ConvertibleSecuritiesandContingentConvertibleSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:PreferredSecuritiesRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member jpm:LargeShareholderRiskMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member oef:RiskNotInsuredDepositoryInstitutionMember 2025-12-31 2025-12-31 0001724826 jpm:S000086732Member oef:RiskLoseMoneyMember 2025-12-31 2025-12-31 0001724826 jpm:C000252360Member 2025-12-31 2025-12-31 0001724826 jpm:C000252360Member 2025-01-01 2025-12-31 0001724826 jpm:C000252360Member 2024-09-18 2025-12-31 0001724826 jpm:C000252360Member oef:AfterTaxesOnDistributionsMember 2025-01-01 2025-12-31 0001724826 jpm:C000252360Member oef:AfterTaxesOnDistributionsMember 2024-09-18 2025-12-31 0001724826 jpm:C000252360Member oef:AfterTaxesOnDistributionsAndSalesMember 2025-01-01 2025-12-31 0001724826 jpm:C000252360Member oef:AfterTaxesOnDistributionsAndSalesMember 2024-09-18 2025-12-31 0001724826 jpm:BLOOMBERGGLOBALAGGREGATETOTALRETURNINDEXVALUEUNHEDGEDUSDMember 2024-09-18 2025-12-31 0001724826 jpm:HFRXGLOBALHEDGEFUNDINDEXMember 2025-01-01 2025-12-31 0001724826 jpm:HFRXGLOBALHEDGEFUNDINDEXMember 2024-09-18 2025-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2019-01-01 2019-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2020-01-01 2020-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2021-01-01 2021-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2022-01-01 2022-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2023-01-01 2023-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2024-01-01 2024-12-31 0001724826 jpm:S000061647Member jpm:C000199639Member 2025-01-01 2025-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2019-01-01 2019-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2020-01-01 2020-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2021-01-01 2021-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2022-01-01 2022-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2023-01-01 2023-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2024-01-01 2024-12-31 0001724826 jpm:S000061648Member jpm:C000199640Member 2025-01-01 2025-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2021-01-01 2021-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2022-01-01 2022-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2023-01-01 2023-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2024-01-01 2024-12-31 0001724826 jpm:S000068182Member jpm:C000218340Member 2025-01-01 2025-12-31 0001724826 jpm:S000086732Member jpm:C000252360Member 2025-01-01 2025-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2020-01-01 2020-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2021-01-01 2021-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2022-01-01 2022-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2023-01-01 2023-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2024-01-01 2024-12-31 0001724826 jpm:S000063724Member jpm:C000206545Member 2025-01-01 2025-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2021-01-01 2021-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2022-01-01 2022-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2023-01-01 2023-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2024-01-01 2024-12-31 0001724826 jpm:S000068977Member jpm:C000220641Member 2025-01-01 2025-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2020-01-01 2020-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2021-01-01 2021-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2022-01-01 2022-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2023-01-01 2023-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2024-01-01 2024-12-31 0001724826 jpm:S000063725Member jpm:C000206546Member 2025-01-01 2025-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2019-01-01 2019-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2020-01-01 2020-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2021-01-01 2021-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2022-01-01 2022-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2023-01-01 2023-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2024-01-01 2024-12-31 0001724826 jpm:S000061649Member jpm:C000199641Member 2025-01-01 2025-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2021-01-01 2021-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2022-01-01 2022-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2023-01-01 2023-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2024-01-01 2024-12-31 0001724826 jpm:S000068181Member jpm:C000218339Member 2025-01-01 2025-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2019-01-01 2019-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2020-01-01 2020-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2021-01-01 2021-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2022-01-01 2022-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2023-01-01 2023-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2024-01-01 2024-12-31 0001724826 jpm:S000061650Member jpm:C000199642Member 2025-01-01 2025-12-31 xbrli:pure iso4217:USD

As filed with the Securities and Exchange Commission on April 30, 2026

Securities Act File No. 333-225588

Investment Company Act File No. 811-23325

SECURITIES AND EXCHANGE COMMISSION

FORM N-1A

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933 |

|

Pre-Effective Amendment No. |

|

Post-Effective Amendment No. 65 |

|

UNDER THE INVESTMENT COMPANY ACT OF 1940 |

|

| |

|

(Check appropriate box or boxes)

(Exact Name of Registrant Specified in Charter)

270 Park Avenue

New York, NY, 10017

(Address of Principal Executive Offices)

Registrant’s Telephone Number, Including Area Code: (212) 270-6000

The Corporation Trust Company

1209 Orange Street

Wilmington, Delaware 19801

(Name and Address of Agent for Service)

Abby L. Ingber, Esq. J.P. Morgan Private Investments Inc. 277 Park Avenue, 10th Floor New York, NY 10004 |

|

Gregory S. Rowland, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 |

It is proposed that this filing will become effective (check appropriate box):

| |

immediately upon filing pursuant to paragraph (b). |

| |

60 days after filing pursuant to paragraph (a)(1). |

| |

75 days after filing pursuant to paragraph (a)(2). |

| |

on May 1, 2026 pursuant to paragraph (b). |

| |

on (date) pursuant to paragraph (a)(1). |

| |

on (date) pursuant to paragraph (a)(2). |

If appropriate, check the following box:

| |

The post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

EXPLANATORY NOTE

This Post-Effective Amendment No. 65 to the Registration Statement of Six Circles Trust relates to the Six Circles Ultra Short Duration Fund, Six Circles Tax Aware Intermediate Duration Fund, Six Circles U.S. Unconstrained Equity Fund, Six Circles International Unconstrained Equity Fund, Six Circles Global Bond Fund, Six Circles Tax Aware Bond Fund, Six Circles Credit Opportunities Fund, Six Circles Managed Equity Portfolio U.S. Unconstrained Fund, Six Circles Managed Equity Portfolio International Unconstrained Fund and Six Circles Multi- Strategy Fund series of the Registrant.

Six Circles® Funds

Six Circles Ultra Short Duration Fund

Six Circles Tax Aware Intermediate Duration Fund (formerly Six Circles Tax Aware Ultra Short Duration Fund)

Six Circles U.S. Unconstrained Equity Fund

Six Circles International Unconstrained Equity Fund

Six Circles Global Bond Fund

Six Circles Tax Aware Bond Fund

Six Circles Credit Opportunities Fund

This Prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

The Securities and Exchange Commission has not approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Six Circles® Ultra Short Duration Fund

Ticker: CUSDX

What is the goal of the Fund?

The Fund seeks to generate current income consistent with capital preservation.

Fees and Expenses of the Fund

The following table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

ANNUAL FUND OPERATING EXPENSES (Expenses that you pay each year as a percentage of the value of your investment) |

| |

|

Distribution (Rule 12b-1) Fees |

|

| |

|

Total Annual Fund Operating Expenses |

|

Fee Waiver and Expense Reimbursement1,2 |

|

Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement1,2 |

|

1

The Fund’s adviser, J.P. Morgan Private Investments Inc. (“JPMPI”) and/or its affiliates have contractually agreed through at least April 30, 2027 to waive any management fees that exceed the aggregate management fees the adviser is contractually required to pay the Fund’s sub-advisers. Thereafter, this waiver will continue for subsequent one year terms unless terminated in accordance with its terms. JPMPI may terminate the waiver, under its terms, effective upon the end of the then-current term, by providing at least ninety (90) days prior written notice to the Six Circles Trust. The waiver may not otherwise be terminated by JPMPI without the consent of the Board of Trustees of the Six Circles Trust, which consent will not be unreasonably withheld. Such waivers are not subject to reimbursement by the Fund.

2

Additionally, the Fund’s adviser has contractually agreed through at least April 30, 2027 to reimburse expenses to the extent Total Annual Fund Operating Expenses (excluding acquired fund fees and expenses, if any, dividend and interest expenses related to short sales, brokerage fees, interest on borrowings, taxes, expenses related to litigation and potential litigation, and extraordinary expenses) exceed 0.40% of the average daily net assets of the Fund (the “Expense Cap”). An expense reimbursement by the Fund’s adviser is subject to repayment by the Fund only to the extent it can be made within thirty-six months following the date of such reimbursement by the adviser. Repayment must be limited to amounts that would not cause the Fund’s operating expenses (taking into account any reimbursements by the adviser and repayments by the Fund) to exceed the Expense Cap in effect at the time of the reimbursement by the adviser or at the time of repayment by the Fund. This expense reimbursement is in effect through April 30, 2027, at which time the adviser and/or its affiliates will determine whether to renew or revise it.

3

“Other Expenses” are based on actual expenses incurred in the most recent fiscal year.

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses are equal to the total annual fund

operating expenses after fee waivers and expense reimbursements shown in the fee table through April 30, 2027 and total annual fund operating expenses thereafter. Your actual costs may be higher or lower.

WHETHER OR NOT YOU SELL YOUR SHARES, YOUR COSTS WOULD BE: |

| |

|

|

|

|

| |

|

|

|

|

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. During the Fund’s most recent fiscal year, the Fund’s portfolio turnover rate was 59.33% of the average value of its portfolio.

What are the Fund’s main investment strategies?

The Fund mainly invests in U.S. dollar and non-U.S. dollar denominated investment grade short-term fixed and floating rate debt securities. While the Fund may invest in securities with various maturities, under normal market conditions, the Fund will seek to maintain an average effective portfolio duration of one year or less. Average effective portfolio duration could at times be higher, though it will not under normal market conditions exceed two years.

| |

Duration is a measure of the price sensitivity of a debt security or a portfolio of debt securities to relative changes in interest rates. Generally, the higher a debt security’s duration, the greater its price sensitivity to a change in interest rates. For instance, a duration of three years means that a security’s or portfolio’s price would be expected to decrease by approximately 3% with a 1% increase in interest rates (assuming a parallel shift in yield curve). In contrast to duration, maturity measures only the time until final payment is due. Investors should be aware that effective duration is not an exact measurement and may not predict a particular security’s sensitivity to changes in interest rates. |

As part of its principal investment strategy, the Fund may invest in debt securities of corporate issuers, obligations of governments, government agencies or instrumentalities, including U.S. Treasury securities (including Separate Trading of Registered Interest and Principal of Securities (“STRIPS”)), securities issued or guaranteed by the U.S. government or its agencies and instrumentalities, municipal securities, securities issued or guaranteed by supranational organizations and

Six Circles® Ultra Short Duration Fund (continued)

securities issued or guaranteed by foreign governments. The Fund may also invest in money market instruments such as certain instruments described above, as well as commercial paper, certificates of deposit, time deposits, deposit notes and bank notes. The instruments in which the Fund invests may pay fixed, variable, or floating interest rates and may include asset-backed securities, mortgage-backed securities (residential and commercial) (and which may include “to be announced” (“TBA”) transactions), zero-coupon securities, convertible securities, inflation-indexed bonds, repurchase agreements, privately-issued (Rule 144A) securities, Regulation S securities, structured notes, collateralized loan obligations, loan participations, loan assignments and other securities and instruments bearing fixed or variable interest rates. The Fund may also invest in foreign securities, including emerging market securities, that are U.S. dollar denominated or non-U.S. dollar denominated, and the Fund may seek to hedge such securities’ currency exposure to the U.S. dollar. The Fund may also invest in other investment companies, such as open-end, closed-end and exchange-traded funds.

Most of the Fund’s investments will be investment grade at the time of investment, although up to 10% of the Fund’s total assets may be invested in below investment grade securities (determined at the time of investment) as described below. The Fund’s investment grade investments will at the time of investment: (i) carry a short-term rating of P-2, A-2 or F2 or higher by any of Moody’s Investors Service Inc. (“Moody’s”), Standard & Poor’s Corporation (“S&P”) and Fitch Ratings (“Fitch”), respectively, or the equivalent by another nationally recognized statistical rating organization (“NRSRO”); (ii) carry a long-term rating of Baa3, BBB– or BBB– or higher by any of Moody’s, S&P and Fitch, respectively, or the equivalent by another NRSRO; or (iii) if such investments are unrated, be deemed by a Sub-Adviser (as defined below) to be of comparable quality at the time of investment. The Fund may invest up to 10% of its total assets in securities that are rated below investment grade (commonly known as “high yield securities” or “junk bonds”), or are unrated securities that a Sub-Adviser determines are of comparable quality. These securities generally offer a higher yield than investment grade securities, but involve a high degree of risk. A security’s quality is determined at the time of purchase and securities that are rated investment grade or the unrated equivalent may be downgraded or decline in credit quality such that subsequently they would be deemed to be below investment grade.

Due to the nature of the investments in which the Fund is seeking to invest, a significant portion of the issuers of the investments in the Fund’s portfolio may be in the financials sector.

The Fund is not a money market fund and is not subject to the special regulatory requirements (including maturity and credit quality constraints) designed to enable money market funds to maintain a stable share price and to limit investment risk. In

addition, shareholders are not eligible for certain simplified methods for calculating gains and losses afforded to money market mutual fund shareholders.

The Fund has flexibility to invest in derivatives and may use such instruments as substitutes for securities and other instruments in which the Fund can invest. Derivatives are instruments which have a value based on another instrument, exchange rate or index. The Fund may use futures, options, swaps, and forward contracts, as well as repurchase agreements and reverse repurchase agreements, in connection with its principal strategies in certain market conditions in order to hedge various investments, for risk management purposes and/or to increase income or gain to the Fund.

The Fund will likely engage in active and frequent trading. The frequency with which the Fund buys and sells securities will vary from year to year, depending on market conditions.

J.P. Morgan Private Investments Inc., the Fund’s investment adviser (“JPMPI” or the “Adviser”), constructs the Fund’s portfolio by allocating the Fund’s assets among investment strategies managed by one or more sub-advisers retained by the Adviser (each, a “Sub-Adviser”). The Adviser will periodically review and determine the allocations among investment strategies and may make changes to these allocations when it believes it is beneficial to the Fund. As such, the Adviser may, in its discretion, add to, delete from or modify the categories of investment strategies employed by the Fund at any time. In making allocations among investment strategies and/or in changing the categories of investment strategies employed by the Fund, the Adviser expects to take into account the investment goals of the broader investment programs administered by the Adviser or its affiliates, for whose use the Fund is exclusively designed. As such, the Fund may perform differently from a similar fund that is managed without regard to such broader investment programs.

Each Sub-Adviser may use both its own proprietary and external research and securities selection process to manage its allocated portion of the Fund’s assets. The Adviser is responsible for determining the amount of Fund assets allocated to each Sub-Adviser. The Adviser is not required to allocate a minimum amount of Fund assets to any specific Sub-Adviser and may allocate, or re-allocate, zero Fund assets to a specific Sub-Adviser at any time. The Adviser engages the following Sub-Advisers: BlackRock Investment Management, LLC (“BlackRock”) and Pacific Investment Management Company LLC (“PIMCO”). The Adviser may adjust allocations to the Sub-Advisers at any time or make recommendations to the Board of Trustees of the Six Circles Trust (the “Board”) with respect to the hiring, termination or replacement of a Sub-Adviser. As such, the identity of the Fund’s Sub-Advisers, the investment strategies they pursue and the portion of the Fund allocated to them, may change over time. For example, due to market conditions, the Adviser may choose not to allocate Fund assets to a Sub-Adviser or may reduce the portion of the Fund allocated to a Sub-Adviser to zero. Each Sub-Adviser is

responsible for deciding which securities to purchase and sell for its respective portion of the Fund and for placing orders for the Fund’s transactions. However, the Adviser reserves the right to instruct Sub-Advisers as needed on certain Fund transactions and manage a portion of the Fund’s portfolio directly, including without limitation, for portfolio hedging, to temporarily adjust the Fund’s overall market exposure or to temporarily manage assets as a result of a Sub-Adviser’s resignation or removal. Below is a summary of each current Sub-Adviser’s investment approach.

With respect to its allocated portion of the Fund, BlackRock primarily invests in fixed and floating-rate securities of varying maturities, such as corporate and government bonds, agency securities, instruments of U.S. and non-U.S. issuers, including emerging market securities, privately-issued securities, securitized products, including asset-backed and mortgage-backed securities (residential and commercial), structured securities, money market instruments, repurchase agreements and securities issued by investment companies. BlackRock may use derivatives such as options, futures or swap agreements to gain exposure to any or all of the foregoing types of investments. BlackRock will actively manage its portfolio and does not seek to replicate the performance of a specified index. The portfolio may have a higher portfolio turnover than portfolios that seek to replicate the performance of a specified index.

BlackRock’s portfolio management team invests across a range of assets while using a disciplined credit research process to analyze an underlying issuer’s creditworthiness and valuation. The strategy seeks to generate current income consistent with capital preservation by primarily investing in short-term, investment grade bonds.

With respect to its allocated portion of the Fund, PIMCO invests, under normal circumstances, mainly in a portfolio of bonds, debt securities, securitized products and other similar instruments issued by various U.S. and non-U.S. public- or private-sector entities with varying maturities, which may be represented by forwards or derivatives such as options, futures or swap agreements.

PIMCO’s strategy focuses on active management of high-quality, fixed income and cash equivalent securities to seek to preserve principal and maintain liquidity. Multiple sources of value are used to seek to generate consistent returns, which include both top-down and bottom-up strategies. Considerations of term, credit, volatility and liquidity are combined with multiple concurrent strategies to build the portfolio and potentially generate value.

The Fund’s Main Investment Risks

The Fund is subject to management risk and may not achieve its objective if the Adviser’s and/or Sub-Advisers’ expectations regarding particular instruments or markets are not met.

An investment in this Fund or any other fund is not designed to be a complete investment program. It is intended to be part of a broader investment program administered by the Adviser or its affiliates. The performance and objectives of the Fund should be evaluated only in the context of your complete investment program. The Fund is managed to take into account the investment goals of the broader investment program and therefore changes in value of the Fund may be particularly pronounced and the Fund may underperform a similar fund managed without consideration of the broader investment program. The Fund is NOT designed to be used as a stand-alone investment. The Fund is subject to the main risks noted below, any of which may adversely affect the Fund’s performance and ability to meet its investment objective.

General Market Risk. Economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. Securities in the Fund’s portfolio may underperform in comparison to securities in general financial markets, a particular financial market or other asset classes due to a number of factors, including inflation (or expectations for inflation), deflation (or expectations for deflation), interest rates, global demand for particular products or resources, market instability, financial system instability, debt crises and downgrades, embargoes, tariffs, sanctions and other trade barriers, supply chain disruptions, regulatory events, other governmental trade or market control programs and related geopolitical events. In addition, the value of the Fund’s investments may be negatively affected by the occurrence of global events such as war, terrorism, environmental disasters, natural disasters or events, country instability, and infectious disease epidemics or pandemics or the threat or potential of one or more such factors and occurrences.

Inflation Risk. Inflation risk is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the present value of the Fund’s assets and distributions may decline.

Interest Rate Risk. The Fund’s investments in bonds and other debt securities will change in value based on changes in interest rates. If rates increase, the value of these investments generally declines. Securities with greater interest rate sensitivity and longer maturities generally are subject to greater fluctuations in value. The Fund may invest in variable and floating rate securities. Although these instruments are generally less sensitive to interest rate changes than fixed rate instruments, the value of variable and floating rate securities may decline if their interest rates do not rise as quickly, or as much, as general interest rates. The Fund may face a heightened level of interest rate risk due to certain changes in monetary policy. It is difficult

Six Circles® Ultra Short Duration Fund (continued)

to predict the pace at which central banks or monetary authorities may change interest rates or the timing, frequency, or magnitude of such changes. Any such changes could be sudden and could expose debt markets to significant volatility and reduced liquidity for Fund investments.

Credit Risk. The Fund’s investments are subject to the risk that issuers and/or counterparties will fail to make payments when due or default completely. If an issuer’s or counterparty’s financial condition worsens, their credit quality may deteriorate. Prices of the Fund’s investments may be adversely affected if any of the issuers or counterparties it is invested in are subject to an actual or perceived deterioration in their credit quality. Credit spreads may increase, which may reduce the market values of the Fund’s securities. Credit spread risk is the risk that economic and market conditions or any actual or perceived credit deterioration may lead to an increase in the credit spreads (i.e., the difference in yield between two securities of similar maturity but different credit quality) and a decline in price of the issuer’s securities.

Income Risk. The Fund’s income may decline when interest rates fall because the Fund may hold a significant portion of short duration securities and/or securities that have floating or variable interest rates. The Fund’s income may decline because the Fund invests in lower yielding bonds, as bonds in its portfolio mature, are near maturity or are called, or when the Fund needs to purchase additional bonds.

Liquidity Risk. The Fund may make investments that are illiquid or that may become less liquid in response to market developments or adverse investor perceptions. Illiquid investments may be more difficult to value. The liquidity of portfolio securities can deteriorate rapidly due to credit events affecting issuers or guarantors, such as a credit rating downgrade, or due to general market conditions or a lack of willing buyers. An inability to sell one or more portfolio positions, or selling such positions at an unfavorable time and/or under unfavorable conditions, can increase the volatility of the Fund’s net asset value ("NAV") per share. Liquidity risk may also refer to the risk that the Fund will not be able to pay redemption proceeds within the allowable time period because of unusual market conditions, an unusually high volume of redemption requests, or other reasons. Liquidity risk may be the result of, among other things, the reduced number and capacity of traditional market participants to make a market in fixed income securities or the lack of an active market. The potential for liquidity risk may be magnified by a rising interest rate environment or other circumstances where investor redemptions from money market and other fixed income mutual funds may be higher than normal, potentially causing increased supply in the market due to selling activity.

Currency Risk. Changes in foreign currency exchange rates will affect the value of the Fund’s securities and may affect the price of the Fund’s shares. Generally, when the value of the U.S. dollar rises in value relative to a foreign currency, an investment impacted by that currency loses value because that currency is

worth less in U.S. dollars. Currency exchange rates may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates. Devaluation of a currency by a country’s government or banking authority also will have a significant impact on the value of any investments denominated in that currency. Currency markets generally are not as regulated as securities markets, may be riskier than other types of investments and may increase the volatility of the Fund. Although the Fund may attempt to hedge some or all of its currency exposure into the U.S. dollar, it may not be successful in reducing the effects of currency fluctuations. The Fund may also hedge from one foreign currency to another. In addition, the Fund’s use of currency hedging may not be successful, including due to delays in placing trades and other operational limitations, and the use of such strategies may lower the Fund’s potential returns.

Asset-Backed, Mortgage-Related and Mortgage-Backed Securities Risk. The Fund may invest in asset-backed, mortgage-related and mortgage-backed securities including so-called “sub-prime” mortgages, credit risk transfer securities and credit-linked notes issued by government-related organization that are subject to certain other risks including prepayment and call risks. When mortgages and other obligations are prepaid and when securities are called, the Fund may have to reinvest in securities with a lower yield or fail to recover additional amounts (i.e., premiums) paid for securities with higher interest rates, resulting in an unexpected capital loss and/or a decrease in the amount of dividends and yield. In periods of either rising or declining interest rates, the Fund may be subject to extension risk, and may receive principal later than expected. As a result, in periods of rising interest rates, the Fund may exhibit additional volatility. During periods of difficult or frozen credit markets, significant changes in interest rates or deteriorating economic conditions, such securities may decline in value, face valuation difficulties, become more volatile and/or become illiquid. Additionally, asset-backed, mortgage-related and mortgage-backed securities are subject to risks associated with their structure and the nature of the assets underlying the securities and the servicing of those assets. Certain asset-backed, mortgage-related and mortgage-backed securities may face valuation difficulties and may be less liquid than other types of asset-backed, mortgage-related and mortgage-backed securities, or debt securities.

Collateralized mortgage obligations and stripped mortgage-backed securities, including those structured as interest-only and principal-only, are more volatile and may be more sensitive to the rate of prepayments than other mortgage-related securities. The risk of default, as described under “Credit Risk,” for “sub-prime” mortgages is generally higher than other types of mortgage-backed securities. The structure of some of these securities may be complex and there may be less available information than other types of debt securities.

Credit risk transfer securities and credit-linked notes are general obligations issued by a government-related organization or special purpose vehicle, respectively, and are unguaranteed. Unlike mortgage-backed securities, investors in credit risk transfer securities and credit-linked notes issued by a government-related organization have no recourse to the underlying mortgage loans. In addition, some or all of the mortgage default risk associated with the underlying mortgage loans is transferred to the noteholder. There can be no assurance that losses will not occur on an investment. These investments are also subject to the risks described under “Prepayment Risk.”